立信出版社会计电算化参考文献

会计电算化-文献综述

会计电算化-文献综述尼古拉斯·科雷亚(Nicholas Correia)是美国著名的会计学家,他著作了《企业会计电算化研究》一部会计史学方面的名著。

这部著作以大量的论文和书籍中所包含的会计史知识为基础,通过对会计历史中所有重大发展阶段的重大问题进行讨论,以较详实的资料向读者介绍了有关会计电算化发展的基本观点。

在本书中,作者把研究重点放在20世纪会计电算化的发展上,以其特有的视角深入剖析各种观点的本质,并从中提炼吸收了有用的成分。

迈克尔·查特菲尔德(Chatfield Michael)在《会计思想史》中,提到了大量分散的会计史知识,通过对会计历史中所有重大发展阶段重大问题的讨论,以较翔实的资料向读者提供了有关会计思想发展的一般观点。

齐军在《企业会计电算化运行存在的问题及解决对策》一文中提出利用电子计算机进行会计核算和会计管理,实现会计电算化这一观点,已成为会计工作现代化的重要组成部分和会计改革的重要内容。

20世纪80年代中后期以来,特别是进入90年代,我国的会计电算化事业已有了一定的发展,对推动会计工作和更好地为经济管理服务发挥了不可低估的作用。

闻春晖《会计电算化的发展方向及培养措施探讨》中提到会计电算化的发展方向为会计电算化与管理会计系统相结合,促进企业管理信息系统的建立和完善。

获得普遍推广和应用,大范围的信息处理网络得以建立。

以机代账的单位将逐渐增加。

会计人员业务水平不断提高。

会计工作自身的发展和变革,也会推动会计电算化在新的基础上进一步完善和发展。

现代网络技术对会计电算化的发展方向起着至关重要的作用。

车俐在《对会计电算化系统审计工作的认识》文章中提到出了企业实施会计电算化的具体情况,从会计电算化的发展历史、现状入手与会计电算化的发展趋势与方向阐述了会计电算化条件下,对企业会计工作、审计工作的影响,力图解析会计电算化对企业的影响,目的就是为了给使用会计电算化的中小企业给予帮助,使它们能够正确的应用会计电算化这一工具,使它们能够认识到在使用会计电算化后会对企业产生什么样的影响,帮助它们在使用会计电算化过程中解决存在的问题。

关于会计电算化的文献综述

关于会计电算化的文献综述摘要随着信息技术的飞速发展和普及,会计电算化已经成为了当今社会中不可或缺的重要组成部分。

在这篇文献综述中,我们将会从多个角度来探讨会计电算化所引发的一系列问题,对相关文献进行综述和分析,以期能够更好地了解和掌握会计电算化的发展状况和现状。

一、会计电算化的概念会计电算化,简单来说就是将会计工作中的各种过程和数据信息处理化,借助计算机等现代信息技术手段来实现自动化、高效率、高度精确度的处理和管理。

这样,不仅能够大大提高会计工作的工作效率,还能够避免由于人为因素所引发的错误和问题。

二、会计电算化的优劣势与传统的手工会计工作相比,会计电算化具有众多的优劣势:优势1.精确度高:采用电子化会计处理手段后,会计数据的准确性和精度将得到有效保障。

2.提高效率:利用电子化会计处理手段,可以节省大量的人力和时间成本,避免由于手工计算带来的繁琐、重复的工作。

3.实时性好:采用电子化会计处理手段,会计数据的处理和统计可以实现实时性和及时性,便于各种业务决策和监管管理。

4.安全性高:采用电子化会计处理手段,会计数据的存储和传输安全性大大提高,数据可靠性能够得到有效保障。

劣势1.初期投资高:会计电算化需要配备一定的设备和软件,初期投资比较高。

2.技术门槛较高:会计电算化需要技术人员的配合才能够顺利实现,只有掌握一定的计算机技能才能够进行操作和维护。

3.安全威胁较高:会计电算化所涉及的数据信息非常重要和敏感,因此,其安全性和可靠性就成为非常重要的问题。

三、会计电算化对会计人员的影响会计电算化对会计人员的影响是非常显著的,主要体现在以下几个方面:1.技能要求越来越高:会计电算化需要相关人员具有较高的技能水平,需要了解计算机技术和数据处理能力等方面的知识。

2.工作内容更加复杂:会计电算化需要管理更加复杂的数据处理和计算,需要更多的专业领域和知识点的支持。

3.工作流程的变化:会计电算化可以实现自动化和高度的流程化,因此会计人员的工作流程也会受到很大的影响。

会计专业毕业论文参考文献

会计专业毕业论文参考文献会计专业毕业论文参考文献【1】牛明艳.财务指标体系应用研究——基于现金流量信息【D】.江苏大学硕士学位论文,2007.12.P1.2【2】萧维.企业资信评级【M】.北京:中国财政经济出版社,2005.5【3】袁敏.资信评级的功能检验与质量控制研究【M】.上海:立信会计出版社,2007.9【4】肖舟.中国工商银行信贷制度变迁研究【M】.北京:科学出版社,2008【5】朱顺泉.中国企业资信评级方法及应用研究【D】.中南大学博士学位论文,2001.10【6】潘永泉,杨志英,张敬秀.基于人工智能方法的企业资信评级【C】.中国控制与决策学术年会论文集,2004【7】黄爱华.企业资信等级的熵权评估模型研究阴.重庆文理学院学报(自然科学报),2007.10【8】邵海清,袁春振.对我国企业资信评级指标体系的探析[J].理论学刊,2005.10【9】梁雪春,谢岭南,陈森发,刘艳.企业资信等级的定性定量评估模型研究叨.东南大学学报(哲学社会科学版),2006.9【10】王一鸣,印为,石勇.基于次序逻辑斯蒂模型的企业贷款信用风险评级研究【R】.数学、力学、物学、高新技术研究进展,2008(12)卷【1l】陈志斌.基于价值创造的企业现金流管理研究【M】.大连:东北财经大学出版社,2007.5【12】陈建煌.现金流量的经验性评估—来自沪深股市的实证证据【D】.厦门大学博士学位论文,2000【13】晏静.现金流量信息功能研究:理论分析与实证【M】.广州:暨南大学出版社,2004.7【14】陆晓雯.中小企业板块会计盈余与现金流量信息含量的实证研究【D】.浙江大学硕士学位论文,2008.4【15】张友棠.财务预警系统管理研究[M].北京:中国人民大学出版社,2004.3【16】刘庆华.基于现金流量的企业财务预警系统研究【D】.西南财经大学博士学位论文,2006.4【17】刘格辉.基于现金流的财务风险预警研【D】.湖南大学MPAcc学位论文,2007.10【18】张传明,陈俊.报表收益与现金流量的决策有用性研究【J】.经济问题探索,2007.7【19】曹建新,王春丽.自由现金流量与盈利质量的关系研究【J】.粤港澳市场与价格,2008.6【20】李延喜.基于动态现金流量的企业价值评估模型研究【D】.大连理工大学博士学位论文,2002.12【21】史冬元.基于现金流量的企业业绩评价体系研究【J】.宁波职业技术学院学报,2008.6【22】朱荣恩编著.资信评级【M】.上海:上海财经大学出版社,2006.91.黄杰,“美国效绩审计的发展与思考”,《审计研究》,2011年4月。

会计电算化系统参考文献精选131条

数据处理技术与方法

数据采集与输入技术

01

介绍数据采集的来源、方法和输入设备,讨论如何保证数据的

准确性和完整性。

数据处理与存储技术

02

阐述计算机对数据的处理方式和存储介质,分析不同处理方式

和存储介质的特点和适用范围。

数据输出与传输技术

03

介绍数据输出的形式和传输方式,讨论如何保证数据的安全性

和保密性。

近期研究成果展示

研究成果1

《基于大数据的会计电算化系统优化研究》。该研究利用大数据技术对会计电算化系统进行了优化,提高了 系统的处理效率和准确性,为企业财务管理提供了更加便捷、高效的工具。

研究成果2

《会计电算化系统在智能财务中的应用》。该研究将会计电算化系统与智能财务相结合,实现了自动化、智 能化的财务管理,大大提高了企业的财务管理水平和效率。

03

实际应用案例分析

企业内部财务管理应用

自动化账务处理

通过会计电算化系统,实现企业内部财务数据的自动 化处理,提高账务处理效率。

实时监控与决策支持

系统提供实时监控功能,帮助企业管理者及时掌握财 务状况,为决策提供数据支持。

内部控制与风险管理

利用系统的内部控制功能,规范企业财务流程,降低 财务风险。

数据安全与隐私保护问题

数据泄露风险

随着会计电算化系统的广泛应用 ,数据泄露风险也随之增加,需 要采取有效措施加强数据安全保 护。

隐私保护法律法规

各国纷纷出台隐私保护法律法规 ,要求企业在处理会计信息时充 分保护个人隐私。

加密技术与访问控制

采用先进的加密技术和访问控制 机制,确保数据在传输和存储过 程中的安全性。

区块链技术采用分布式账本技术,实现会计信息的去中心 化管理和共享。

电算化论文参考文献

[2]吕文涛,张洪波,. 会计电算化专业人才培养模式改革与实践[J]. 会计之友(下旬刊),2010,(4).[3]贺军,. 高职会计电算化专业实践课程体系构建与实施[J]. 会计之友(下旬刊),2010,(3).[4]刘鹏,刘涛,. 浅谈会计电算化对会计工作的影响[J]. 财政监督,2010,(6).[5]侯丽平,. 河南经贸职业学院会计电算化专业特色综述[J]. 会计之友(中旬刊),2010,(2).[6]金美子,. 医院会计电算化软件应用问题及若干见解[J]. 中国卫生经济,2010,(2).[7]黄海娟,. 浅谈在会计电算化和企业信息化环境下的税务稽查[J]. 中国税务,2010,(2).[8]何群英,. 会计电算化专业工学结合教学模式研究[J]. 财政监督,2010,(2).[9]黄大双,. 浅谈会计电算化环境下的企业内部控制[J]. 财会通讯,2009,(35).[10]黄浩岚,. 构建基于工作过程的会计电算化课程教学模型[J]. 财会月刊,2009,(35).[11]刘建梅,. 论会计电算化系统的内部控制[J]. 财政监督,2009,(24).[12]郝素利,徐北辰,. 基于ISM的会计电算化教学内容设计[J]. 会计之友(上旬刊),2009,(12).[13]张鸿冰,. 会计电算化对内部会计控制的影响[J]. 山西财经大学学报,2009,(S2).[14]姜宏卫,. 会计电算化和网络化对会计的影响[J]. 山西财经大学学报,2009,(S2).[15]景青山,刘雨,. 基于VB的会计电算化无纸化考试系统[J]. 煤炭技术,2009,(11).[16]程萍,. 中小企业会计电算化成本核算技巧[J]. 会计之友(中旬刊),2009,(10).[17]张玉明,. 会计电算化条件下销售成本的自动结转[J]. 财会月刊,2009,(22).[18]张玉明,. 会计电算化条件下利润表的取数公式研究[J]. 财会月刊,2009,(22).[19]王珠强,汤义好,. 会计电算化考试系统的设计与实现[J]. 会计之友(中旬刊),2009,(7).[20]乔荣,. 会计电算化环境下的错账更正法[J]. 财会月刊,2009,(19).[21]胡晓翔,李宗快,. 会计电算化审计现状及其完善[J]. 商业时代,2009,(15).[22]刘红英,李茹,. 会计电算化中存在的缺陷及对策[J]. 山西财经大学学报,2009,(S1).[23]李乐红,. 会计电算化的舞弊行为及其防范[J]. 山西财经大学学报,2009,(S1).[24]李先文,. 企业会计电算化管理中的内部控制研究[J]. 财会研究,2009,(8).[25]党红娃,. 会计电算化对审计工作的影响及改进建议[J]. 商业会计,2009,(8).[26]熊小萍,. 会计电算化应用中存在的问题及完善措施[J]. 财政监督,2009,(8).[27]张县平,. 会计电算化条件下高校的内部会计控制[J]. 商业会计,2009,(7).[28]邢萃明,. 会计电算化对会计基础工作的影响及对策[J]. 商业会计,2009,(2).[29]魏民,. 试论会计电算化的反记账功能[J]. 特区经济,2008,(12).[30]田苗,. 试论会计电算化对会计信息质量的影响[J]. 会计之友(中旬刊),2008,(12). 李胜云:《浅谈实行会计电算化存在的风险及其对策》[J]中国集体经济.2009年19期.801 张芳;;会计电算化系统功能的完善方法[J];中国新技术新产品;2010年01期2 朱振宇;;会计电算化风险分析与防范[J];中国新技术新产品;2010年01期3 包根梅;;电算化会计信息系统环境下内部控制的分析[J];中国乡镇企业会计;2010年02期4 廖俊斌;;试谈会计电算化下会计数据资料的管理问题[J];职业;2010年05期5 尹彦蓉;;论会计电算化安全与防范[J];现代商贸工业;2010年03期6 郭婧洲;;我国中小企业会计电算化应用中存在的问题[J];知识经济;2010年03期7 李靖;;守好阵地适时抢滩——关于地市级报纸发展新兴媒体的思考[J];中国报业;2010年02期8 许哲;;谈网络环境下的会计信息质量保证[J];合作经济与科技;2010年08期9 刘许增;;浅议会计电算化系统的现状及对策[J];经济师;2010年03期10 李霞;;浅议医院会计电算化[J];科技信息;2010年01期- 施工企业会计电算化的现状问题及对策On current problems of account computerization of construction enterprises and their strategies 作者:张晋民, 期刊山西建筑SHANXI ARCHITECTURE 2010年第18期- 浅议会计电算化系统的现状及对策作者:刘许增, 期刊经济师CHINA ECONOMIST 2010年第03期- 浅谈新形势下我国会计电算化的现状、问题及对策作者:胡顺才, 期刊云南财贸学院学报(社会科学版)YUNNAN FINANCE & ECONOMICS UNIVERSITY JOURNAL OF ECONOMICS & MANAGEMENT 2004年第04期- 浅谈新形势下我国会计电算化的现状问题及对策作者:李兴凯, 期刊农业与技术AGRICULTURE & TECHNOLOGY 2010年第02期- 我国会计电算化现状及发展趋势作者:孙秀玲, 期刊-核心期刊管理与财富MANAGEMENT AND FORTUNE 2008年第11期- 浅谈新形势会计电算化存在的问题与对策作者:周金芝, 期刊科协论坛(下半月)SCIENCE & TECHNOLOGY ASSOCIATION FORUM 2007年第07期- 论会计电算化对会计工作的影响作者:刘华忠, 期刊现代农业科技XIANDAI NONGYE KEJI 2009年第14期- 我国会计电算化发展现状与趋势分析及对策探讨作者:赵凤香, 期刊山东气象JOURNAL OF SHANDONG METEOROLOGY 2005年第03期- 我国会计电算化的现状及发展对策作者:吴莉莉,张永亮, 期刊-核心期刊产业与科技论坛INDUSTRIAL & SCIENCE TRIBUNE 2009年第04期- 试论我国会计电算化现状及发展对策作者:章莉, 期刊中国商界BUSINESS CHINA 2009年第10期。

会计电算化的参考.doc

会计电算化的参考会计作为一个提供财务信息为主的信息系统,在企业经营管理中起着重要作用。

电算化会计不仅仅是使用计算机替代手工进行会计处理,还包括分析、预测、控制、决策等管理职能;它不仅减轻会计核算的劳动强度,而且对会计信息的产生与利用远不是传统会计所能做到的。

以下是会计电算化的参考,欢迎阅读。

摘要:文章简要介绍了会计电算化的发展历程及其在现代企业管理中的重要作用以及对企业内部控制方面的重要影响,分析了当前会计电算化与传统会计系统相比所存在的一系列问题,并相应提出了企业加强会计电算化内部控制的部分措施。

关键词:电算化;内部控制目前会计电算化被应用到很多领域,会计业务从传统的手工方式到被电子技术与信息技术所代替,以计算机为媒介的现代化数据处理工具,很好地实现了系统性的变革,提高了财会管理水平,使企业实现了核算管理一体化。

它代表的是一种与现代信息技术环境相适应的新的会计思想,是会计发展史上的一次革命。

随着全球经济一体化的发展,计算机和信息技术在会计行业中的广泛应用,未来会计电算化将向智能化、国际化和信息化的方向发展。

1 会计电算化的发展和重要性全球首次正式在会计领域使用会计电算化的是1954 年美国国际商用机器公司利用计算机进行工资核算。

我国的会计电算化工作起步较晚,从20 世纪70 年代末期开始,国内自1981年后才称为“会计电算化”,至今发展了3个阶段。

第一阶段是20世纪70 年代末至20 世纪80 年代末,该时期会计电算化处于以自我开发为主专用会计软件阶段。

最初计算机在会计工作中的应用,是由行业主管部门或大型企事业单位自己开发和使用的专用财务软件。

鉴于当时懂计算机技术和财务业务的双栖人才奇缺,造成这类软件开发普遍存在周期长、投资大和水平低的弊端。

第二阶段是20 世纪80 年代末至20 世纪90 年代末,该时期会计电算化主要应用在总账、报表和工资3个模块上。

第三阶段是20 世纪90 年代末至今,会计电算化软件向ERP 软件方向发展,主要应用于资金管理、预算管理和成本控制上。

会计电算化参考文献

会计电算化参考文献------------------------------------------作者xxxx------------------------------------------日期xxxx【精品文档】会计电算化参考文献序号文献标题来源年期来源数据库1 浅谈现代企业的会计电算化管理今日科苑 2008/02 中国期刊全文数据库2 企业会计电算化系统开发及实施浅谈财会通讯(理财版) 2008/01 中国期刊全文数据库3 浅析我国小企业会计电算化发展的问题和对策理论界 2008/01 中国期刊全文数据库4 浅谈煤炭企业会计电算化平台的构建煤炭经济研究 2008/02 中国期刊全文数据库5 谈如何加强企业会计电算化的内部控制山西财政税务专科学校学报 2008/01 中国期刊全文数据库6 对小企业会计电算化模式的探讨消费导刊 2008/07 中国期刊全文数据库7 我国企业会计电算化的发展现代商业 2008/12 中国期刊全文数据库8 企业会计电算化系统内部控制探讨财会通讯(理财版) 2008/04 中国期刊全文数据库9 企业会计电算化系统的网络化和安全性内蒙古统计 2008/02 中国期刊全文数据库10 试论企业会计电算化与内部控制党史博采(理论) 2008/05 中国期刊全文数据库序号文献标题来源年期来源数据库11 企业会计电算化的发展及核算项目的实际应用探索时代经贸(中旬刊) 2008/S6 中国期刊全文数据库12 企业会计电算化条件下的内部控制制度商情(财经研究) 2008/02 中国期刊全文数据库13 林业企业会计电算化发展过程中存在的问题及对策中国林业经济 2008/03 中国期刊全文数据库14 企业会计电算化若干问题的探讨会计之友(中) 2007/03 中国期刊全文数据库15 如何加强企业会计电算化后的内部控制商场现代化 2007/06 中国期刊全文数据库16 浅谈中小企业会计电算化的继续教育现代企业教育 2007/04 中国期刊全文数据库17 把脉企业会计电算化失败的症结财会信报 2005-01-1918 水利企业会计电算化实践拙见福建省会计学会理论研讨论文集 2006 中国重要会议论文全文数据库19 现代企业的会计电算化管理财税与会计 200201 中国引文数据库20 中国会计年鉴中国会计年鉴 1998 中国年鉴全文数据库序号文献标题来源年期来源数据库21 企业会计电算化的作用及应用哈尔滨商业大学学报(社会科学版) 1992/03 中国期刊全文数据库22 大陆与香港企业会计电算化的差异与协调暨南大学 2001 中国优秀硕士学位论文全文数据库23 企业会计电算化的现状与完善对策分析中国管理信息化(会计版) 2007/03 中国期刊全文数据库24 中小企业会计电算化信息平台如何构筑——关于中小企业实施会计电算化的设想中国管理信息化(会计版) 2007/04 中国期刊全文数据库25 浅谈企业会计电算化下的内部会计控制经济师 2007/06 中国期刊全文数据库26 浅谈企业会计电算化存在的问题及对策会计之友(中旬刊) 2007/06 中国期刊全文数据库27 中小企业会计电算化档案管理问题与对策山东档案 2007/02 中国期刊全文数据库28 企业会计电算化中的内部控制问题时代经贸(中旬刊) 2007/S3 中国期刊全文数据库29 浅谈企业会计电算化现状和发展电大理工 2007/01 中国期刊全文数据库30 企业会计电算化系统与内部控制科技广场 2007/04 中国期刊全文数据库【精品文档】。

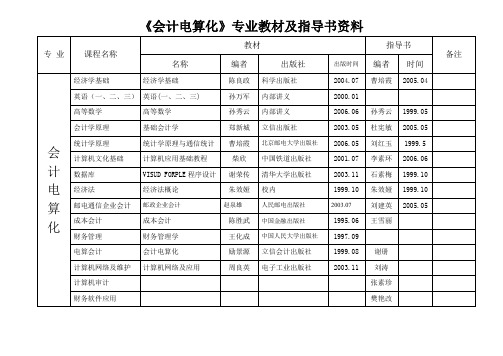

《会计电算化》专业教材及指导书资料(精)

郑新城

立信出版社

2003.05

杜宪敏

2005.05

统计学原理

统计学原理与通信统计

曹培霞

北京邮电大学出版社

2006.05

刘红玉

1999.5

计算机文化基础

计算机应用基础教程

柴欣

中国铁道出版社

2001.07

李素环

2006.06

数据库

VISUD FORPLE程序设计

谢荣传

清华大学出版社

2003.11

1999.08

谢册

计算机网络及维护

计算机网络及应用

周良英

电子工业出版社

2003.11

刘涛

计算机审计

张素珍

财务软件应用

樊艳改

《会计电算化》专业教材及指导书资料

专业

课程名称

教材

指导书

备注

名称

编者

出版社

出版时间

编者

时间

会

计

电

算

化

经济学基础

经济学基础

陈良政

科学出版社

2004.07

曹培霞

2005.04

英语(一、二、三)

英语(一、二、三)

孙万军

内部讲义

2000.01

高等数学

高等数学

孙秀云

99.05

会计学原理

石素梅

1999.10

经济法

经济法概论

朱效娅

校内

1999.10

朱效娅

1999.10

邮电通信企业会计

邮政企业会计

赵泉雄

人民邮电出版社

2003.07

刘建英

2005.05

成本会计

会计电算化文献综述适用于所有类型

添加标题

国内研究现状:会计 电算化在国内已经得 到了广泛应用,研究 主要集中在系统设计 与开发、内部控制与

风险管理等方面。

添加标题

国外研究现状:国外会 计电算化研究起步较早, 研究内容涵盖了从理论 框架到实际应用的各个 方面,尤其在人工智能 和大数据技术在会计电 算化中的应用方面研究

促进企业信息化 建设:会计电算 化是企业信息化 的重要组成部分, 有助于企业实现 全面信息化管理。

提高会计信息质 量:会计电算化 通过规范化的数 据处理流程,提 高了会计信息的 质量和可靠性。

增强企业竞争力: 会计电算化能够 帮助企业实现快 速决策和响应市 场变化,提高企 业的竞争力和市 场地位。

提高会计工作效率

数据安全问题:如何保证会计电算化中的数据安全是一个重要问题,需要采取有效的加密和备份措施。

内部控制问题:会计电算化可能导致内部控制失效,需要建立完善的审计和监管机制。

人员素质问题:会计电算化需要高素质的会计人员,但目前很多企业的会计人员素质不足,需要加强培训和人才 引进。

法规制度问题:会计电算化需要遵守相关法规制度,但目前相关法规制度还存在不完善之处,需要加强立法和监 管。

案例介绍:某企 业实施会计电算 化的过程和效果

经验分享:实施会 计电算化的关键要 素和注意事项

案例分析:会计 电算化对企业的 影响和优势

结论总结:会计 电算化的未来发 展趋势和前景

添加标题 添加标题 添加标题 添加标题

自动化和智能化:会计电算化提高了会计工作的自动化程度,减少了人 工干预,提高了工作效率。

会计电算化毕业论文参考文献汇总

案例中存在问题剖析与解决方案探讨

问题剖析

针对案例企业在会计电算化应用 过程中遇到的实际问题,进行深 入剖析,找出问题产生的原因和 影响因素。

解决方案探讨

结合理论知识和实践经验,提出 切实可行的解决方案和应对措施 ,帮助案例企业解决会计电算化 应用中的难题。

实践经验总结:成功因素、挑战和对策

01

02

政策法规对行业的影响

分析政策法规对会计电算化行业的规范、监管、发展等方面产生的 影响。

政策法规的执行与监管

探讨政策法规的执行情况、监管机制及其存在的问题和改进措施。

未来发展趋势预测及挑战应对策略

技术发展趋势

预测会计电算化行业未来的技术发展趋势,如人工智能、大数据、云计算等技术的应用。

市场格局、消费者需求等。

系统安全性保障措施

身份验证与权限控制

采用严格的身份验证和权限控制机制 ,确保用户访问和操作的安全性。

日志审计与监控

采取有效的网络安全措施,防范网络 攻击和病毒入侵对系统造成的破坏。

数据加密传输与存储

对敏感数据进行加密传输和存储,防 止数据泄露和非法访问。

防范网络攻击与病毒入侵

记录用户操作日志并进行审计和监控 ,及时发现和处理异常行为。

03

企业应用案例分析与实践经 验总结

典型企业应用案例选取原则及过程描述

典型性原则

优先选择行业代表性强、会计电 算化应用水平高的企业作为案例

研究对象。

数据可获取性

确保能够获取到案例企业详细、准 确的会计电算化应用数据和资料。

过程描述

通过实地调研、访谈、问卷调查等 方式,深入了解案例企业的会计电 算化应用背景、历程和现状。

的科学性和准确性。

推荐-会计电算化发展与问题文献综述 精品

《毕业设计与写作》课程题目“会计电算化发展与问题”文献综述学院专业___会计学____________年级___20XX级__________班级___会计2班__________学号姓名成绩_____________________年月日目录摘要:在经济全球化日益加深的21世纪,在信息化日趋普及的今天,会计电算化在各行各业的应用越来越广泛,但我国的会计电算化存在许多问题。

本文就目前我国会计电算化发展现状及存在的问题进行深入分析,并提出一些可供参考的建议。

关键词:会计电算化、发展、问题、对策正文内容:一、会计电算化的含义“会计电算化”是现代电子计算机在会计工作中应用的简称。

它将以计算机作账程序来替代手工作账。

使之做好“凭证—--总账---报表”三者完成任务。

“会计电算化”这个“化”字体现了一个循序渐进的演变过程,即从非电算化逐步过渡到电算化;从初级电算化过渡到高级电算化这样一个长期而艰巨的演变过程,而非一蹴而就,准确把握这个过程应从以下两方面进行理解:1、渐进性:会计电算化的内容应包括实现如下几个转变过程:(1)从单项应用向综合财务处理转变;(2)财务会计电算化向将财务会计和成本与管理会计有机结合后的电算化转变;(3)会计管理信息系统向会计决策支持系统转变。

与此同时,对会计数据的管理应从数据库管理向数据仓库管理方向发展。

2、动态性:在会计电算化的过程中,要将会计学和计算机科学相互结合和交叉并推动会计学科的发展。

会计电算化是一个变化的过程、发展的过程和创新的过程。

因此,不仅会计电算化的过程是变化的,而且对传统会计也不能看成是静止的,这里我们应该明确会计电算化是一个过程而不是目标。

二、研究背景1、知识经济要求发展会计电算化。

在知识经济下,要求信息高速的传递,信息科学技术将得到进一步的发展,各单位要提供更为标准、及时和相关的信息,以利于知识经济下投资者的决策,会计电算化的普及将是确定无疑的,也只有如此才能满足知识经济对于会计信息的需要。

关于会计电算化的文献综述

关于会计电算化的文献综述摘要:随着科技的高速发展,信息化、网络化已成为当今世界经济发展的主要趋势,信息技术渗透到社会经济发展的各个领域。

会计电算化更是如此,在经济大潮中发挥着越来越重要的作用。

纵观国际,国外会计电算化起步早,发展快;国内会计电算化也紧跟世界潮流。

做好国内外对比的研究,将有利于我国会计电算化更好地发展。

关键词:信息技术经济发展会计电算化一、国外会计电算化研究J. J. STAUNTON(2008)认为短语“公认会计原则”的基本财务报表是当今会计准则的先行者。

他通过研究早期的分析,在辩论的规则基础上将标准设置为两个维度,划分两个维度包含会计电计算化的全部内容,这对会计电算化的发展是有推动作用的。

Laura Davis DeLaune(2004)以路易斯安那州立大学会计部门为研究对象,得出会计电算化课程及活动和个人的发展能力有关的结论。

于是他对学校会计部门提出建议:用活动中的会计程序,培养学生领导技能和专业的技能。

这将会直接的将电计算化和人工相结合,真正做到人计合一,对电计算化的发展具有长远意义。

Martin S. Bressler(2006)指出,小型企业在美国的比重很大。

尽管大多数公司都是小型企业,但是美国的大多数研究主要是研究大型跨国公司。

在美国和其他州,从高科技到特许经营权,小型企业是重要的实体。

小企业可以选择各种不同的会计信息系统软件满足各行各业的需求,但企业家通常没有时间去研究所有选择。

美国的会计信息系统较为完善,管理者可以认识到会计信息系统的重要性。

二、国内会计电算化研究董金艳(2005)指出随着电子信息产业的不断发展,会计电算化在社会经济中的运用越来越广泛,如何发展我国会计电算化的问题越来越引起人们的关注。

适应社会主义市场经济改革与发展、加入世界贸易组织后中国会计改革与发展是我国会计电算化要面临的问题,为此她提出几点建议,深化我国会计电算化改革。

闫桂卿(2009) 针对会计电算化应用中存在的软件、人才缺乏等问题,提出了完善法规、培养高素质人才等具体措施,指出了我国会计电算化未来的发展趋势。

会计电算化外文文献

ASSESSING THE PERFORMANCE OF A COMPUTERIZED ACCOUNTING SYSTEM作者: Danciu, RaduAbstract: The study aims to present the criteria for assessing the performance of a computerized accounting system starting with completeness, ergonomics, information integration, flexibility, adaptability, accessibility, adaptability, accessibility, adaptability, safety and security in the operations. The study's conclusions formulate a set of minimum requirements for the creation, implementation and use of a computerized accounting system. Key words: computerized accounting system, ergonomics, information integration, flexibility, adaptability, accessibility, operational safety1. IntroductionThe deliverance of an independent opinion, by a group of specialists, referring to the informational system used for organizing and conducting the accounting is one of the modern business management goals. Among the objectives that must be considered in the process of assessing the financial and accounting system we can mention:* checking the operating system's correctness, completeness, flexibility, adaptability, cost of maintenance, ergonomics and operational safety* expressing an opinion on the computerized accounting system's usage facilities and efficiency (computing and software), as well as on the business's place in the informational economic environments, before and after its purchase/creation.* formulating some proposals regarding the achievement of the objectives, the informatics system's development and the elimination of the deficiencies consigned in the assessment reports.In order to be able to quantitatively and qualitatively asses the computerized accounting system one must answer at least the following questions:What is the system's degree of flexibility?Is the system ergonomic and accessible?Is the system adaptable?Is the system complete? Does it cover the information management needs of the enterprise?What kind of operational safety does the system offer?Do the programming language and the databases satisfy the requirements of an enterprise's dynamic modelling system?What are the mutations produced by such a system in the financial and accounting management?After the acquisition or creation of a computerized accounting system and its implementation, the system must undergo an audit to determine the weaknesses in the system's usage.The auditing of the information systems is a very complex operation and it involves the auditor expressing his opinion on real time data processing, database management, system integration, the work with computer networks, etc. The claims for an audit of the computerized accounting system are very high, which involves the implication of some specialists in accounting and in the field of applications design and implementation. Computerized systems audit should include the general examination of the computerized accounting systemand the analytical examination of each application individually.Among the objectives of the computerized accounting system's general examination we may include :* assessing the completeness of the information system, therefore the coverage degree of the accounting needs for organization and management* assessing the integration degree of the system's applications, of the way they communicate* assessing the flexibility and adaptability* assessing the accessibility, reliability and security* assessing the way the minimum conditions to be met by the computerized systems are being respected* assessing the delimitation procedure for the attributions and responsibilities of the people involved in the computerized systems management* assessing the way the computerized system complies with the accounting principles and methods* assessing the system's ergonomics.Among the objectives of the computerized accounting system's analytical examination we may include :* assessing each application's architecture* assessing the integrity and the integrality of the system's main functions and of their usage possibility* assessing the effects of using the application functions and of every function's usage degree* detecting function overlaps in the accounting's implementation* establishing and evaluating the application's additional functions* assessing the automation degree of accounting projects* assessing the degree of detail in the information description, namely the adequacy or inadequacy of the informational attributes necessary to identify the transactions, events and objects* assessing the menus of data collection and validation* assessing the fairness of the data processing and systematization procedures* assessing the manner of creating, consulting and printing the accounting reports as well as their informational content* assessing the manner of database presentation and consultation* assessing the level of maintenance and system administration functions accomplishmentTo facilitate the discovery of an answer for the questions formulated above and to detail the objectives of the computerized accounting system's general and analytical examination, the system's main characteristics will be described: flexibility, adaptability, ergonomics, accessibility, reliability, integration and operational safety.2. Qualitative characteristics of the computerized accounting system2.1. Flexibility and adaptabilityThe flexibility of the computerized applications refers both to the multitude of options available to create a function, as well as to the possibility of going behind some commands or application functions without altering the collected, processed and archived databases. All the application's functions must be characterized byflexibility, namely:User-defined sort keys should provide the opportunity to choose attributes ordering information by seeking data from a database or a table.* The data collecting function should provide at least the following facilities:* accessing auxiliary databases in order to choose data when collecting it through a control key / a command button. For example, when collecting an account, the user, by pressing a key / button control should be able to access the chart of accounts in order to select the desired account* allowing the user, when using the key / command button, to add new items to auxiliary databases or modify existing ones when the data he is searching for is not there* displaying the processed and stored data, useful in the collection process, such as: displaying the quantity available on stock and the stock's output unit price or showing the invoices to be paid to suppliers at the moment when the payment data is being collected, etc.* the data collection function should allow deletion or modification of not validated data* ensure the possibility of operating or de-operating data at a document's level* multi-criteria search and selection of data in order to choose the data by multiple informational attributes combined with mathematical operators: equal "=" lower "<", higher ">", lower and equal "<=", higher and equal ">=", including "$" different "#".* the multiple classification of data by one or more informational attributes, for example: in the case of stock entries sorting can be done by input document type, document number and date, etc. There are two types of ordering keys for flexible applications:- ordering keys defined by software- user defined ordering keys.The user defined ordering keys must provide him with the opportunity to choose the informational attributes based on which he wants the ordering of data from a database or a table to be made.* the generating, consulting and listing function for the financial and accounting statements must offer at least the following facilities:* obtaining accounting reports for any period of time by indicating the starting and closing dates for information to be included in the report* obtaining accounting reports both in foreign currencies and in lei when indicating a different currency than the domestic one* getting full reports or only for a list of indicated entities / objects , such as: accounts, distributors, partners, stock items, etc.* displaying in screen mode all the financial and accounting statements made before listing* listing of the reports with the following options type of printer (local or În network/printer name)- type of printing ( normal or reversed )- first page- final page- document's margins, etc.* the processing or auxiliary database consultation function must at least provide the following facilities:* prohibiting additions, changes and deletion from processed and archived* multi-criteria search and selection of data* enabling the listing of selected data* the application's parameterization and management function should provide at least the following facilities:* saving / restoring data and software from multiple drives. Thus, before performing these operations, the choice of the magnetic disk drive to / from which the backup / restore of data or software will be performed must be leftup to the user* facilitating the access to data belonging to any processing period by simply pointing it out* the possibility to update the readymade applications without intervention from the producer, based on the new software package provided, by using the software update option.The lack of options listed above leads to the creation of a system which is rigid and cumbersome in use. The existence of functions / options is not the only one important, but also the programmer's and analyst's tenacity in putting them into the right place , the control keys / control buttons having to be easy to remember, and to be the same for the same function / option in all applications.In fact, achieving a high flexibility of an integrated computerized system is the result of combining the accounting science with the computer science, which is easier to accomplish when the analyst and the programmer is the same person.The adaptability of the computerized accounting system to the specific conditions of accounting organization and management within an enterprise has two aspects, namely:a. adaptation and integration in the enterprise's computerized economic systemb. adjusting to the accounting's organization and management requirements.In order to express an opinion regarding the adaptation degree of a computerized system to the company's concrete conditions, we must analyze the types of computerized systems, namely:* the self created computerized system which has the following characteristics:* the enterprise's integration in the computerized system is easy to achieve as the computerized accounting system is compatible with other specific applications* the system's design will be made to match the information management requirements and the enterprise's management strategy* system implementation and user education is easier* the system creation in an economists-comp team leads to attachment and loyalty towards the created system, any improvement of the system being easily achievable* the system's production time is long, the system's analysis must be very careful, the making process involving high costs and a higher skilled workforce* the readymade computerized system with the following features:* the user can choose the applications package that meets the utmost of his requirements* the system's architecture and documentation is more comprehensive and complete, because it answers the requirements of many users, many times being updated according to their requirements* regular updating and software maintenance is done at much lower cost than independent upgrading and maintenance* the purchase price of the readymade software is smaller than that of the software developed by themselves, because of the competition on the accounting computerized applications market, and the fact that the development cost is distributed to more buyers* these computerized systems are usually closed systems in terms of analyst and programmer, being directly addressed to the accounting user* this type of software, frequently do not integrate in an enterprise's activity, so, very often the acquiring company's needs do not find themselves in the purchased applications, requiring a working style review, which may or may not have beneficial effect on the economic activity* the applications packages having a high degree of generalization do not have the same efficiency as their own software packages* the company providing readymade software can interrupt it's activity or stop doing business, which is a major impediment for updating and maintaining computer applications while the sources for software and system analysis are not owned by user* the pre-ordered computerized system which has the following characteristics:* the user, according to the delivered command can work under their individual data processing and information systematization requirements* costs may be lower than those for software developed with own forces* it integrates easily into the enterprise's computerized system* the user can take possession of sources and system analysis which helps making it easy to do future changes and updates, even if we are facing an interruption / termination of relationships with companies and program analysis that was used originally.To ensure continuity of he management and information integration principles of the financial and accounting computerized system, the best readymade computer system, completed and adapted where the enterprise information management require it.2.2. Ergonomics, accessibility and reliabilityFor the computerized accounting system to be ergonomic and accessible its component application must stand in line with the following requests:* using the same principles in developing and using the data collection models in all computer applications* using the same combinations of keys / command buttons to collect and access the data* using some information functions on the status and the content of the data in the system, namely:- showing the record statistics which displays the number of basic documents, the number of secondary documents and number of records for each database separately- displaying the selected records number that shows the number of basic documents, the number of secondary documents and the number of records for the database selection- displaying the document type and accounts names, allocators and other elements encoded in the recording where the cursor is positioned- generating at the user's request the list / report with full data / seected from the database- enabling access to explanations on the role and functioning of the application's functions /options. All the explanations given for each feature / option are enrolled in the system's user manual- the existence of a function to perform simple calculations on data, such as adding values in column / selected area- the option of displaying and distributing an account balance with the structure: Account, distribution, money. This function will provide data on:- Opening balance debtor / creditor- Aggregate debit and credit turnover- Monthly debit and credit turnover- Total debit and credit amounts- Final balance debtor / creditor- the option of calculating an expression for the user's need, in order to do some calculations outside offered the information management system- the option of duplicating the content of some information attributes previously collected designed to pick up data from the user common data for two consecutive records in a table.The system's availability refers to setting access levels for each worker individually, ensuring a certain degree of data confidentiality and to limit the rights of changing data collected by other operators or data from auxiliary databases.An accessible computerized system must provide the highlighting of the information by various technical means like:* colour differentiation* differentiation by font size* flashy markings* sound markings* grouping data in boxes* highlighting important data* displaying messages during work time* displaying short explanations for each system function / option.Moreover, a complex computerized system must alert the operator or the user of its abnormal operation, indicating where necessary the system's errors and defects.Particularly important in assessing ergonomics, accessibility and reliability of a computerized system is the tracking of its behaviour in use, at least in terms of the following aspects:* in terms of the system's operational tenacity which also considers the cases and reasons for computerized applications failure* in terms of user requirements, which means assessing the degree of weariness caused to the user after a longer work period and its causes* in terms of work speed, that is the extent to which the system responds to user commands and the reaction times* in terms of accuracy, that is the manner of fulfilling the system's displayed and executed functionsIn the making of an ergonomic and accessible computerized system there are also other important factors:* the creation of some menus with high intelligibility by using short names with intelligibility, logical grouping of data, etc* facilitate the consultation of multiple databases* achieving at least the following reporting features, data collection models, consulting data bases and their associate functions / options:- the high level of information synthesis- information's timeliness- information's completeness- data correctness- data accessibility.The computerized accounting system's reliability refers to the probability that this system will continue to function for a certain amount of time according to the designed and implemented standards. Regarding the reliability assessment of a computer programme, E. Yourdon in the paper "Decline &Fall of the American Programmer" (Oprea, 1999), addresses a number of indicators like:* average time between two failures* average time to remediate troubles* the area affected by failures* the error rate per hour, day, week or month* the error rate on the basic software components* the opportunity of the answer to the errors or the time granted to their remedy* the beneficiary's satisfaction about the quality of the intervention to remedy softdefectsThe system's reliability analysis by using these indicators leads the user to establishing of the software's place, both in the enterprise and comparatively with other software.2.3 Operational safetyThe system's safety includes its security and its capacity to function continuously with no malfunctions, and if malfunctions come up it need to have its own models of remediating them.The system's security is a complex problem, especially when using computer networks for data processing. The main objective of a computerized system's security is represented by insuring the data's confidentiality and integrity. The data confidentiality must be done by:* precisely determining the people who have access to the computer applications* precisely determining the applications and databases the operators and users have access to* precisely determining the access passwords for each person* regularly changing the access passwords and communicating them in maximum confidentialityTo achieve data confidentiality one must establish a Register regarding the use of computer applications inside the computerized accounting system. The structure of this register could present itself as follows:* Ist option considering the person as a benchmark, comprises:- the person - name and position- the computer application or parts of application he has access to- access password- the date of granting / modifying access- acknowledgement signature- observations* IInd option considering the computer application as a benchmark comprises:- the computer application- the people - name and position - having access to the application- access passwords- the date of granting / modifying access- acknowledgement signature- observationsThe data integrity aims to maintain and preserve the collected data, without altering them by data processing and the safe preservation of the processed data, any subsequent intervention being forbidden (change, deletion, mergers, etc.).The system's functioning security must also take into consideration the failure possibility, for them to be able to repair themselves. Some examples of interventions for the maintenance and repairing of the computerized system could be:*for the system's maintenance* database reorganization related to re-indexing them by the index keys defined when the application was created* setting the printing systems used for listing the accounting statements on paper* checking the integrity of the databases that ensure control over the existence of all databases and of their associated indexes* checking the databases structure which ensures the control over the database's structural updates occurring when new versions of the computer applications are created* the database and software saving / restoring, option which provides the saving/restoring of databases on/from floppy disks, local or central hard disks, CD-s, DVD-s, etc.*for the repairing of damaged data* recovery of destroyed database structures* recovery of the system's menus and functions* recovery of archived/saved data, previous to the incidentThe technical methods for carrying out the computerized system's security are:* the physical security which is designed to limit the physical access to the computer system by:- introduction of access codes and installation of alarm systems where the technical items are located- enclosing the microcomputers in protection cabinets or in a protective wrapper- installing a secured mechanism for connecting to the electrical network- storing the data saved on external magnetic devices in maximum security places: safes, safe deposit boxes, etc.* the softsecurity by password access to computers and computer applications, using encryption software for long distance transmitted data, by password access to created data archives, in order for them to only be accessible through the same applications that generated them, by using hidden files and secret file names, etc. If in the case of compute application functions, their completeness must be ensured as well as a wide variety of working options, in the case of features an optimum balance must be achieved, for the computerized system to be able to reach its objectives in the best conditions reported to the highest standards.3. ConclusionsThe introduction and use of a computerized financial and accounting system must ensure reconciliation between the individual vision and the collective network organization, along with the collection, processing, administration and delivery of information in terms of maximum speed and security conditions. For the creation of a computerized information system we may propose the compliance with the following requirements:* the computerized applications must be consistent with any type of computer and created in a performing operating system and programming language with perfecting perspectives* it should have the highest possible accessibility level, so that the level of computer knowledge the user needs to hold to be minimized* it should have a high flexibility degree, therefore to allow changes, deletions, searches, returning to current data, creation of extra reports defined by the user, returning to previous data collections, saving and restoring data collections, etc.* it should be ergonomic, therefore the organizing of the working menus should follow the same principles for all the applications and to be based on simplicity and intuition* to offer operational safety* to ensure data security and privacy by restricting the access to information* the user-computer relationship related to data collection should be as easy as possible and it should comprise explanations regarding every element of information* the mathematical and accounting relations used for validating and calculating the data collected in the system should comply with rules, regulations and laws* it should have a high working speed and data storage capacity* it should protect itself in case of major incidents ( fault of electric current, application failure, etc.) ensuring data preservation.Adapting the experience's effect theory (it comprises: learning effect, innovation effect and the mechanization, automation and robotization effects) to the computerized systems, theory which was elaborated by Boston Consulting Group (B.C.G.), one can say that as the number of financial and accounting computerized products has increased, the tendency of using them has become predominant, using them leads to the discovery of deficiencies and their removal generates the product improvement by eliminating redundant functions, cumbersome models, unnecessary work modules, etc. Perfecting the computer products is not sufficient, the consequences of their use must be insisted on and some accounting areas need to be improved, such as:* developing the accounting standards in line with information's processing and administration in the computerized environments; the financial and accounting computerizes systems must not be treated only as data processing systems, because they are financial and accounting data management systems as well* adapting the common and the special forms regarding the financial and accounting activity to the processing and administration need of the information in the computerized environment* completing the rules on creating and using financial and accounting software with a set of minimum informational attributes required in managing financial and accounting objects, transactions and events* developing a national standard on financial and accounting information processing and management in the computerized environment including:* architectural elements of the computerized system* main functions and characteristics of the computer applications* aspects related to the management of financial and accounting objects, transactions and events* The start of some national research programmes on the changes produced by the use of computerized informational systems and their effects on the accounting science.References1. Danciu, R.;(1994); Computerized accounting systems, Dacia, Cluj-Napoca2. Oprea, D.; (1999); Analysis and design of economic information, Polirom, Iasi3. Tugui, Al.;(2003); Products generalized accounting information, CECCAR, Bucharest4. ***, Manual of Use Systems ERP SAP FICO, MicrosoftDynamics Navision, Clarvision, WinMentor, Siveco Applications 2020, BAAN ERP。

会计电算化外国文献

会计电算化外国文献China’s accounting work of the late start from the 1970s until the end of the year, try going through the stages of development and self-organized and planned way stage of steady development, the current management accounting software-development stage. In the 20 years of development, has made considerable progress, and commercialization of GM’s financial software is widely used. Many accounting software development has been toward specialization, commercialization and socialization of the track. However, due tothe financial characteristics of the work itself, as well as the rapid development of the network, the rapid rise of e-commerce and so on, a number of advanced, modern things keep cropping up on the accounting system, a higher demand, so that the establishment of modern Enterprise development needs of the new financial system has become imperative. Since the accounting is a systematic project, in the proceof development there is much work to do, there are many issues to be resolved in a timely manner or face serious obstacle to China’s accounting to a deeper level. This article on China’s accounting proceand must be resolved on a few issues.First, people’s thinking to solve problemsComputerization of China’s cause of a late start, people thought the idea has not yet fully aware of the significance and importance of computerization. Most units are used in computerized accounting in place of hand, is only alleviate the burden on the accounting staff and improve efficiency of the accounting aspects, it does not recognize the establishment of a complete accounting information systems for enterprises, so that the existing accounting information provided Timely and effective decision-ma-ki-ng and enterprise management services. At the same time, software updates andhardware investment in areas such as lack of support, not to mention the establishment of enterprise local area network as well as the registration of their Web site, did not make use of the advantages of information technology to improve the operational efficiency of enterprises. Accounting for this understanding is very detrimental to the development.Accounting is the accounting work in computer applications in the short to the computer is represented by modern data-processing tools and information theory, systems theory, cybernetics, databases and computer networks, such as new theories and technology used in accounting Accounting and financial management work to improve the management of accounting and economic benefits, and the realization of the modernization of accounting.We must recognize that accounting is not only changed the accounting method in the form of data storage, data-processing procedures and methods to expand the areas of accounting data to improve the quality of accounting information, but also changed the accounting and internal control audit methodology and technology, Thus promoted the theory of accounting and accounting for thefurther development of technology to improve and promote the accounting management system reform, is the study of accounting theory and accounting practice a fundamental change. On the face of it, accounting only applies to the computer accounting work to reduce the labor intensity of accountants, accounting to improve the speed and accuracy to the computer to replace manual accounting. In fact, accounting is not only accounting tools and methods to improve accounting, and would doubtlehave been a division of accounting and personnel changes, and promote the quality of personnel and accounting knowledge structure, accounting efficiency and quality of the all-round improvement Accountants to save time and energy, changing the functions of accounting, accounting theory and accounting to promote technological progress, raise the level of accounting work, a significant increase in economic efficiency of enterprises, accounting theory and practice so that all aspects will be unprecedented in-depth Change. For example, with a focus on data storage and management features of the “Computerized Accounting”, the use of advanced database and data warehouse technology, data classification has focused on storage, the total abolition of a variety of accounting and reconciliation operation, the various statements of the data Able to share data through timely and accurately made.Second, attention should be paid to accounting theory researchTheory is the precursor of action, accounting dependent on the development of computerized accounting theory of the development of computerized accounting theory behind the study, will be restricted accounting software maturity and development, computerized accounting The theory is to guide and promote the new accounting on the basis of constant improvement and development of practice guidelines.In a sense, the emergence and development of the computerized accounting process, but also break the traditional concept of accounting, the current method of accounting theory and new issues, new issues, as well as research and the establishment of new theories and methods. If the computerized accounting system in the design, work organization, information processing and accounting procedures to deal with ways and means to change itself to the current accounting theory and methods and improve the break. Although in the short term, the impact of these is the gradual, but in the。

2017会计电算化参考文献

2017会计电算化参考文献参考文献的学术价值决定了一篇毕业论文的重要性。

下面是店铺为大家整理的会计电算化参考文献,欢迎参考~会计电算化参考文献[1]陈兴霞,曹军,费淋淇.浅析会计电算化实践教学仿真模拟题库建设[J].辽宁农业职业技术学院学报,2006,(04)[2]杜思晓.高校会计电算化专业建设研究[J].农村.农业.农民(A 版),2008,(10)[3]刘秋月.会计电算化专业实验教学模式的构思与实践[J].郑州牧业工程高等专科学校学报,1998,(Z1)[4]王健.加快林业企业会计电算化进程的建议[J].绿色财会,2006,(09)[5]芦杰.关于中专财会和会计电算化专业学科设置的构想[J].中国林业教育,2000,(02)[6]牛莉侠.高等职业教育会计电算化教学的思考[J].中国乡镇企业会计,2008,(01)[7]董丽晖.提高会计电算化实践能力的课堂因素分析[J].甘肃农业,2006,(09)[8]包准,程宝华.做好林业企业会计电算化工作的几点体会[J].绿色财会,2006,(09)[9]高俊杰,张东红.种子企业实行会计电算化之我见[J].种子科技,2008,(02)[10]丁丽娜.中小企业会计电算化问题研究[J].中国乡镇企业会计,2009,(03)会计电算化参考文献【1】牛明艳.财务指标体系应用研究——基于现金流量信息【D】.江苏大学硕士学位论文,2007.12.P1.2【2】萧维.企业资信评级【M】.北京:中国财政经济出版社,2005.5【3】袁敏.资信评级的功能检验与质量控制研究【M】.上海:立信会计出版社,2007.9【4】肖舟.中国工商银行信贷制度变迁研究【M】.北京:科学出版社,2008【5】朱顺泉.中国企业资信评级方法及应用研究【D】.中南大学博士学位论文,2001.10【6】潘永泉,杨志英,张敬秀.基于人工智能方法的企业资信评级【C】.中国控制与决策学术年会论文集,2004【7】黄爱华.企业资信等级的熵权评估模型研究阴.重庆文理学院学报(自然科学报),2007.10【8】邵海清,袁春振.对我国企业资信评级指标体系的探析[J].理论学刊,2005.10【9】梁雪春,谢岭南,陈森发,刘艳.企业资信等级的定性定量评估模型研究叨.东南大学学报(哲学社会科学版),2006.9【10】王一鸣,印为,石勇.基于次序逻辑斯蒂模型的企业贷款信用风险评级研究【R】.数学、力学、物学、高新技术研究进展,2008(12)卷【1l】陈志斌.基于价值创造的企业现金流管理研究【M】.大连:东北财经大学出版社,2007.5【12】陈建煌.现金流量的经验性评估—来自沪深股市的实证证据【D】.厦门大学博士学位论文,2000【13】晏静.现金流量信息功能研究:理论分析与实证【M】.广州:暨南大学出版社,2004.7【14】陆晓雯.中小企业板块会计盈余与现金流量信息含量的实证研究【D】.浙江大学硕士学位论文,2008.4【15】张友棠.财务预警系统管理研究[M].北京:中国人民大学出版社,2004.3【16】刘庆华.基于现金流量的企业财务预警系统研究【D】.西南财经大学博士学位论文,2006.4【17】刘格辉.基于现金流的财务风险预警研【D】.湖南大学MPAcc学位论文,2007.10【18】张传明,陈俊.报表收益与现金流量的决策有用性研究【J】.经济问题探索,2007.7【19】曹建新,王春丽.自由现金流量与盈利质量的关系研究【J】.粤港澳市场与价格,2008.6【20】李延喜.基于动态现金流量的企业价值评估模型研究【D】.大连理工大学博士学位论文,2002.122017会计电算化参考文献将本文的Word文档下载到电脑,方便收藏和打印推荐度:点击下载文档文档为doc格式。

会计电算化_--文献综述

把日期改了,里面你不需要的内容删了,适当借鉴啊!设计(论文)开题报告2009年1 月10 日选题浅谈会计电算化对会计实践的影响系财经系专业年级学生姓名学生学号本选题的意义及目前研究状况:2009年05月26日设计(论文)开题报告2009年1 月10 日选题浅谈会计电算化对会计实践的影响系财经系专业年级学生姓名学生学号本选题的意义及目前研究状况: 1. 研究目的和意义:随着计算机技术的迅猛发展,我国的会计电算化已跨入有组织、有计划的推广普及发展阶段。

会计信息系统的长足发展,对会计实践产生了巨大影响,同时也出现许多问题。

就会计电算化系统的应用对会计实践的影响和需要注意的几个问题进行探讨。

使会计电算化向更深层次发展有重要意义。

2. 目前该选题研究现状(文献综述)会计电算化软件正在趋向于网络化,未来的电算化会计将向着广域网的方向发展,信息传输范围大大增加,使会计数据的异地共享成为可能。

会计电算网络化将从原来企业内部的会计信息共享,上、下级单位之间的财务信息的传递转变到与外部相关机构的信息共享、与全世界进行信息交流。

网络会计环境是一个集供应商、生产商、经销商、用户和银行等机构为一体的网络体系。

电算化会计就是要充分利用计算机及网络技术,从不同的来源和渠道收集企业经营活动中的会计数据、会计资料,按照经济法规和会计制度的要求予以存储、加工,并生成会计信息,向企业内外部各方面传递,以帮助信息使用者改进经营管理,加强财务决策和有效控制经济活动。

在网络时代,电算化会计在实现其基本目标的基础上将顺应电子商务的发展。

会计电算化还将以在线报告的形势发展,在线报告的出现改变了传统的财务报告顺序结构,它的各个组成部分之间建立了超链接,人们可以借助相关链接主动而迅速地搜寻所需信息,企业还可根据不同用户的要求提供更加个性化的财务报告。

在线报告实现了会计信息的实时追踪,便于财务报告的需求者及时掌握相关企业的第一手资料,为本企业的理性决策提供了方便,实现了企业的在线管理,并利于会计信息系统的社会监督和政府监督。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

立信出版社会计电算化参考文献会计电算化也叫计算机会计,是指以电子计算机为主体的信息技术在会计工作的应用,具体而言,就是利用会计软件,指挥在各种计算机设备替代手工完成或在手工下很难完成的会计工作过程,会计电算化是以电子计算机为主的当代电子技术和信息技术应用到会计实务中的简称,是一个应用电子计算机实现的会计信息系统。

以下是立信出版社会计电算化参考文献,欢迎大家阅读。

立信出版社会计电算化参考文献一:[1]马晓征。

我国会计电算化发展中的问题及解决措施[N]. 科学导报,2017-05-19(C04)。

[2]付文利。

对医院财务电算化及财务内控制度关系的研究[J]. 财经界(学术版),2017,(09):71-72.[3]戴锦炜。

会计电算化在应用中的问题分析及应对建议[J]. 财会学习,2017,(09):91+93.[4]张红燕。

企业会计电算化存在的问题及对策[J]. 内蒙古煤炭经济,2017,(08):67-68.[5]王建明。

会计电算化对企业审计工作的影响与对策[J]. 企业改革与管理,2017,(08):110.[6]张璋。

浅析新事业单位会计制度应注意的问题[J]. 财会学习,2017,(08):120.[7]吕萍。

会计电算化对会计工作方法的影响与策略初探[J]. 财会学习,2017,(08):128.[8]李黎。

试论新会计制度下的财务管理模式[J]. 时代金融,2017,(11):214+222.[9]颜荣荣。

中小企业会计电算化系统实施过程中存在的问题及研究[J]. 时代金融,2017,(11):193.[10]桂海清。

基于财会专业中会计电算化对审计的影响策略研究[J]. 劳动保障世界,2017,(12):60.[11]吴海宽。

浅析我国会计电算化存在的问题及对策[J]. 科技展望,2017,(11):267-268.[12]王文华,黄费连。

健全政府采购管理的内部控制制度[J]. 中国招标,2017,(15):28-29.[13]陈欣。

浅析事业单位会计信息化建设[J]. 中国集体经济,2017,(11):105-106.[14]马欣欣。

电子商务背景下企业动态财务管理模式探究[J]. 商场现代化,2017,(07):188-189.[15]熊诗丽。

探析中小企业实现会计电算化的有效策略[J]. 商场现代化,2017,(07):207-208.[16]刘彦。

会计电算化在企业运作中的问题及对策研究[J]. 市场周刊(理论研究),2017,(04):61-62.[17]贾东木。

会计电算化在我国的发展前景分析[J]. 中国乡镇企业会计,2017,(04):156-157.[18]刘晓苹。

浅析医院会计信息化与财务内控制度关系[J]. 财经界(学术版),2017,(07):83.[19]端萌。

会计电算化向会计信息化的发展研究[J]. 黑龙江科技信息,2017,(10):297.[20]陈云。

浅析市级机关单位财务管理系统的设计[J]. 电脑知识与技术,2017,(10):48-49.[21]黄雅莉。

中小企业会计电算化问题与对策[J]. 合作经济与科技,2017,(07):155-156.[22]赵娜。

电算化环境下的审计风险及应对策略研究[J]. 知识经济,2017,(07):38-39.[23]孙雯。

作会计电算化软件使用问题及解决方法探讨[J]. 科技展望,2017,(09):249-250.[24]边新苗。

信息化对会计核算模式的影响[J]. 企业改革与管理,2017,(06):130.[25]温芳。

新形势下陕西高校财务管理信息化的发展与改造[J]. 经济研究导刊,2017,(09):84-86.[26]田强。

现代工业会计管理趋势分析[J]. 时代金融,2017,(08):221+224.[27]赵蕾。

中小企业会计核算问题及其对策的分析[J]. 财经界(学术版),2017,(06):108-109.[28]伍春玲。

基层机关运用计算机审计存在的问题与对策[J]. 科技展望,2017,(08):289.[29]朱优恪。

事业单位会计电算化下的内部控制[J]. 全国流通经济,2017,(08):102-103.[30]钟培。

会计电算化的现状及发展趋势分析[J]. 商场现代化,2017,(05):181-182.[31]王伟利。

企业会计的网络安全素养与安全策略[J]. 中国管理信息化,2017,(06):35-36.[32]朱小桃。

基于风险管理的商业银行内部控制研究--以浦发银行为例[J]. 中国乡镇企业会计,2017,(03):144-145.[33]宋鹏玺。

网络工程的发展对会计电算化的影响[J]. 中国乡镇企业会计,2017,(03):162-163.[34]王丽娜。

中小企业会计电算化系统的设计与实现[J]. 山西农经,2017,(05):90.[35]许桂香。

探究分析林业会计核算的发展趋势[J]. 经营管理者,2017,(08):45.[36]余慧敏。

新形势下高校财务管理水平提升路径探讨[J]. 经营管理者,2017,(08):235.立信出版社会计电算化参考文献二:[37]代晓岚。

计算机网络环境下会计电算化的内部控制研究[J]. 教育教学论坛,2017,(10):197-198.[38]林泉。

浅析中小企业会计核算存在的问题和对策[J]. 中国集[39]张琳。

会计电算化在财务工作中的运用与发展[J]. 现代经济信息,2017,(05):284.[40]梁戈。

现代信息技术对高职会计电算化教育的影响[J]. 中国管理信息化,2017,(05):56-57.[41]张宁。

基于会计电算化的企业内部控制管理探析[J]. 知识经济,2017,(05):114+116.[42]樊艳。

论会计信息化对传统财务会计职能的影响[J]. 科技创新与应用,2017,(06):273-274.[43]张丹。

浅析会计电算化对企业内部控制的影响[J]. 时代金融,2017,(06):171+176.[44]李莉。

构建一键式财务核算新理念[J]. 商场现代化,2017,(04):213-214.[45]汪黎嘉。

浅谈会计如何适应新形势下经济发展[J]. 山西农经,2017,(04):98.[46]吴琼,罗美娜。

信息技术对传统会计流程的影响[J]. 市场研究,2017,(02):71-72.[47]魏奇慧。

会计电算化教学中的问题及思考[J]. 内蒙古煤炭经济,2017,(Z1):68-69.[48]郑惠尹,文贻霖。

中小企业会计电算化系统实施问题及途径的研究[J]. 财经界(学术版),2017,(04):62-63.[49]闫安。

探析会计电算化下的企业内部控制审计策略[J]. 中国[50]范增期。

浅谈会计电算化条件下企业内部控制管理[J]. 劳动保障世界,2017,(05):55.[51]郑姣。

电算化财务档案管理存在问题与建议[J]. 四川水利,2017,(01):90-91+103.[52]陈逵。

基于层次分析法的会计电算化技能分析[J]. 科技经济市场,2017,(02):59-61.[53]刘芳。

企业电算化下的内部控制实施[J]. 北方经贸,2017,(02):114-115.[54]胡晓燕。

高校会计电算化信息系统内部控制研究[J]. 经营管理者,2017,(05):250.[55]高金霞。

当前我国乡村财务管理新模式建设路径探析[J]. 中国乡镇企业会计,2017,(02):82-83.[56]胡锋娟。

事业单位会计信息化建设的有效途径[J]. 中国乡镇企业会计,2017,(02):161-162.[57]韩淑珍。

事业单位会计电算化推进过程中出现的问题及建议[J]. 中国乡镇企业会计,2017,(02):169-170.[58]葛绮。

论会计电算化在中小企业中的应用[J]. 佳木斯职业学院学报,2017,(02):483.[59]林显强,崔延巍,曲文静。

会计电算化在医院会计基础工作中的运用[J]. 经济师,2017,(02):137-138.[60]张丽洁。

会计电算化与企业内控管理[J]. 中国外资,2017,(03):94-95.[61]刘晓晖。

当前管理会计在我国的应用及存在问题分析[J]. 现代经济信息,2017,(03):223.[62]马姜宇。

企业会计电算化管理中的内部控制探讨[J]. 现代经济信息,2017,(03):288.[63]刘燕。

试论高校财务信息化的发展及趋势[J]. 中国管理信息化,2017,(03):43-45.[64]姚春华。

会计电算化系统舞弊的防范与控制[J]. 知识经济,2017,(03):93-94.[65]杨秋晨。

会计电算化对传统会计的影响研究[J]. 知识经济,2017,(03):116+118.[66]唐蕾蕾。

会计电算化对会计理论与会计实务的冲击[J]. 产业与科技论坛,2017,(03):108-109.[67]王华美。

浅析网络环境下的会计管理模式创新[J]. 时代金融,2017,(03):143+147.[68]苏霞。

浅谈会计诚信问题[J]. 时代金融,2017,(03):145.[69]张芯菱。

浅析会计专业大学生应具备的素质和能力[J]. 山西农经,2017,(02):112.[70]何雪。

我国会计电算化应用的现状及其发展趋势研究[J]. 商场现代化,2017,(02):171-173.[71]姜莹。

会计电算化系统在中小企业中的实施应用[J]. 商场现代化,2017,(02):205-206.[72]曲晓瑜,田智浩。

会计电算化对会计工作方法影响探析[J]. 农村经济与科技,2017,(02):92-93.附件下载:12下一页。