Chapter 17 Intercorporate Equity Investments

《公司理财》课后答案(英文版,第六版).doc

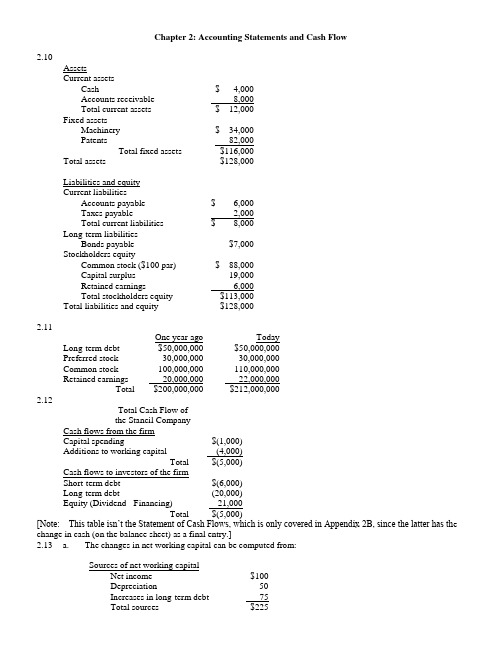

Chapter 2: Accounting Statements and Cash Flow2.10AssetsCurrent assetsCash $ 4,000Accounts receivable 8,000Total current assets $ 12,000Fixed assetsMachinery $ 34,000Patents 82,000Total fixed assets $116,000Total assets $128,000Liabilities and equityCurrent liabilitiesAccounts payable $ 6,000Taxes payable 2,000Total current liabilities $ 8,000Long-term liabilitiesBonds payable $7,000Stockholders equityCommon stock ($100 par) $ 88,000Capital surplus 19,000Retained earnings 6,000Total stockholders equity $113,000Total liabilities and equity $128,0002.11One year ago TodayLong-term debt $50,000,000 $50,000,000Preferred stock 30,000,000 30,000,000Common stock 100,000,000 110,000,000Retained earnings 20,000,000 22,000,000Total $200,000,000 $212,000,0002.12Total Cash Flow ofthe Stancil CompanyCash flows from the firmCapital spending $(1,000)Additions to working capital (4,000)Total $(5,000)Cash flows to investors of the firmShort-term debt $(6,000)Long-term debt (20,000)Equity (Dividend - Financing) 21,000Total $(5,000)[Note: This table isn’t the Statement of Cash Flows, which is only covered in Appendix 2B, since the latter has th e change in cash (on the balance sheet) as a final entry.]2.13 a. The changes in net working capital can be computed from:Sources of net working capitalNet income $100Depreciation 50Increases in long-term debt 75Total sources $225Uses of net working capitalDividends $50Increases in fixed assets* 150Total uses $200Additions to net working capital $25*Includes $50 of depreciation.b.Cash flow from the firmOperating cash flow $150Capital spending (150)Additions to net working capital (25)Total $(25)Cash flow to the investorsDebt $(75)Equity 50Total $(25)Chapter 3: Financial Markets and Net Present Value: First Principles of Finance (Advanced)3.14 $120,000 - ($150,000 - $100,000) (1.1) = $65,0003.15 $40,000 + ($50,000 - $20,000) (1.12) = $73,6003.16 a. ($7 million + $3 million) (1.10) = $11.0 millionb.i. They could spend $10 million by borrowing $5 million today.ii. They will have to spend $5.5 million [= $11 million - ($5 million x 1.1)] at t=1.Chapter 4: Net Present Valuea. $1,000 ⨯ 1.0510 = $1,628.89b. $1,000 ⨯ 1.0710 = $1,967.15c. $1,000 ⨯ 1.0520 = $2,653.30d. Interest compounds on the interest already earned. Therefore, the interest earned inSince this bond has no interim coupon payments, its present value is simply the present value of the $1,000 that will be received in 25 years. Note: As will be discussed in the next chapter, the present value of the payments associated with a bond is the price of that bond.PV = $1,000 /1.125 = $92.30PV = $1,500,000 / 1.0827 = $187,780.23a. At a discount rate of zero, the future value and present value are always the same. Remember, FV =PV (1 + r) t. If r = 0, then the formula reduces to FV = PV. Therefore, the values of the options are $10,000 and $20,000, respectively. You should choose the second option.b. Option one: $10,000 / 1.1 = $9,090.91Option two: $20,000 / 1.15 = $12,418.43Choose the second option.c. Option one: $10,000 / 1.2 = $8,333.33Option two: $20,000 / 1.25 = $8,037.55Choose the first option.d. You are indifferent at the rate that equates the PVs of the two alternatives. You know that rate mustfall between 10% and 20% because the option you would choose differs at these rates. Let r be thediscount rate that makes you indifferent between the options.$10,000 / (1 + r) = $20,000 / (1 + r)5(1 + r)4 = $20,000 / $10,000 = 21 + r = 1.18921r = 0.18921 = 18.921%The $1,000 that you place in the account at the end of the first year will earn interest for six years. The $1,000 that you place in the account at the end of the second year will earn interest for five years, etc. Thus, the account will have a balance of$1,000 (1.12)6 + $1,000 (1.12)5 + $1,000 (1.12)4 + $1,000 (1.12)3= $6,714.61PV = $5,000,000 / 1.1210 = $1,609,866.18a. $1.000 (1.08)3 = $1,259.71b. $1,000 [1 + (0.08 / 2)]2 ⨯ 3 = $1,000 (1.04)6 = $1,265.32c. $1,000 [1 + (0.08 / 12)]12 ⨯ 3 = $1,000 (1.00667)36 = $1,270.24d. $1,000 e0.08 ⨯ 3 = $1,271.25e. The future value increases because of the compounding. The account is earning interest on interest. Essentially, the interest is added to the account balance at the e nd of every compounding period. During the next period, the account earns interest on the new balance. When the compounding period shortens, the balance that earns interest is rising faster.The price of the consol bond is the present value of the coupon payments. Apply the perpetuity formula to find the present value. PV = $120 / 0.15 = $800a. $1,000 / 0.1 = $10,000b. $500 / 0.1 = $5,000 is the value one year from now of the perpetual stream. Thus, the value of theperpetuity is $5,000 / 1.1 = $4,545.45.c. $2,420 / 0.1 = $24,200 is the value two years from now of the perpetual stream. Thus, the value of the perpetuity is $24,200 / 1.12 = $20,000.pply the NPV technique. Since the inflows are an annuity you can use the present value of an annuity factor.ANPV = -$6,200 + $1,200 81.0= -$6,200 + $1,200 (5.3349)= $201.88Yes, you should buy the asset.Use an annuity factor to compute the value two years from today of the twenty payments. Remember, the annuity formula gives you the value of the stream one year before the first payment. Hence, the annuity factor will give you the value at the end of year two of the stream of payments.A= $2,000 (9.8181)Value at the end of year two = $2,000 20.008= $19,636.20The present value is simply that amount discounted back two years.PV = $19,636.20 / 1.082 = $16,834.88The easiest way to do this problem is to use the annuity factor. The annuity factor must be equal to $12,800 / $2,000 = 6.4; remember PV =C A T r. The annuity factors are in the appendix to the text. To use the factor table to solve this problem, scan across the row labeled 10 years until you find 6.4. It is close to the factor for 9%, 6.4177. Thus, the rate you will receive on this note is slightly more than 9%.You can find a more precise answer by interpolating between nine and ten percent.[ 10% ⎤[6.1446 ⎤a ⎡r ⎥bc ⎡6.4 ⎪ d⎣9%⎦⎣6.4177 ⎦By interpolating, you are presuming that the ratio of a to b is equal to the ratio of c to d.(9 - r ) / (9 - 10) = (6.4177 - 6.4 ) / (6.4177 - 6.1446)r = 9.0648%The exact value could be obtained by solving the annuity formula for the interest rate. Sophisticated calculators can compute the rate directly as 9.0626%.[Note: A standard financial calculator’s TVM keys can solve for this rate. With annuity flows, the IRR key on “advanced” financial c alculators is unnecessary.]a. The annuity amount can be computed by first calculating the PV of the $25,000 which youThat amount is $17,824.65 [= $25,000 / 1.075]. Next compute the annuity which has the same present value.A$17,824.65 = C 507.0$17,824.65 = C (4.1002)C = $4,347.26Thus, putting $4,347.26 into the 7% account each year will provide $25,000 five years from today.b. The lump sum payment must be the present value of the $25,000, i.e., $25,000 / 1.075 =$17,824.65The formula for future value of any annuity can be used to solve the problem (see footnote 11 of the text).Option one: This cash flow is an annuity due. To value it, you must use the after-tax amounts. Theafter-tax payment is $160,000 (1 - 0.28) = $115,200. Value all except the first payment using the standard annuity formula, then add back the first payment of $115,200 to obtain the value of this option.AValue = $115,200 + $115,200 30.010= $115,200 + $115,200 (9.4269)= $1,201,178.88Option two: This option is valued similarly. You are able to have $446,000 now; this is already on an after-tax basis. You will receive an annuity of $101,055 for each of the next thirty years. Those payments are taxable when you receive them, so your after-tax payment is $72,759.60 [= $101,055 (1 - 0.28)].AValue = $446,000 + $72,759.60 30.010= $446,000 + $72,759.60 (9.4269)= $1,131,897.47Since option one has a higher PV, you should choose it.et r be the rate of interest you must earn.$10,000(1 + r)12 = $80,000(1 + r)12= 8r = 0.18921 = 18.921%First compute the present value of all the payments you must make for your children’s educati on. The value as of one year before matriculation of one child’s education isA= $21,000 (2.8550) = $59,955.$21,000 415.0This is the value of the elder child’s education fourteen years from now. It is the value of the younger child’s education sixteen years from today. The present value of these isPV = $59,955 / 1.1514 + $59,955 / 1.1516= $14,880.44You want to make fifteen equal payments into an account that yields 15% so that the present value of the equal payments is $14,880.44.A= $14,880.44 / 5.8474 = $2,544.80Payment = $14,880.44 / 15.015This problem applies the growing annuity formula. The first payment is$50,000(1.04)2(0.02) = $1,081.60.PV = $1,081.60 [1 / (0.08 - 0.04) - {1 / (0.08 - 0.04)}{1.04 / 1.08}40]= $21,064.28This is the present value of the payments, so the value forty years from today is$21,064.28 (1.0840) = $457,611.46se the discount factors to discount the individual cash flows. Then compute the NPV of the project. NoticeYou can still use the factor tables to compute their PV. Essentially, they form cash flows that are a six year annuity less a two year annuity. Thus, the appropriate annuity factor to use with them is 2.6198 (= 4.3553 - 1.7355).Year Cash Flow Factor PV0.9091 $636.371$70020.8264 743.769003 1,000 ⎤4 1,000 ⎥ 2.6198 2,619.805 1,000 ⎥6 1,000 ⎦7 1,250 0.5132 641.508 1,375 0.4665 641.44Total $5,282.87NPV = -$5,000 + $5,282.87= $282.87Purchase the machine.Chapter 5: How to Value Bonds and StocksThe amount of the semi-annual interest payment is $40 (=$1,000 ⨯ 0.08 / 2). There are a total of 40 periods;i.e., two half years in each of the twenty years in the term to maturity. The annuity factor tables can be usedto price these bonds. The appropriate discount rate to use is the semi-annual rate. That rate is simply the annual rate divided by two. Thus, for part b the rate to be used is 5% and for part c is it 3%.A+F/(1+r)40PV=C Tra. $40 (19.7928) + $1,000 / 1.0440 = $1,000Notice that whenever the coupon rate and the market rate are the same, the bond is priced at par.b. $40 (17.1591) + $1,000 / 1.0540 = $828.41Notice that whenever the coupon rate is below the market rate, the bond is priced below par.c. $40 (23.1148) + $1,000 / 1.0340 = $1,231.15Notice that whenever the coupon rate is above the market rate, the bond is priced above par.a. The semi-annual interest rate is $60 / $1,000 = 0.06. Thus, the effective annual rate is 1.062 - 1 =0.1236 = 12.36%.A+ $1,000 / 1.0612b. Price = $30 12.006= $748.48A+ $1,000 / 1.0412c. Price = $30 1204.0= $906.15Note: In parts b and c we are implicitly assuming that the yield curve is flat. That is, the yield in year 5applies for year 6 as well.rice = $2 (0.72) / 1.15 + $4 (0.72) / 1.152 + $50 / 1.153= $36.31The number of shares you own = $100,000 / $36.31 = 2,754 sharesPrice = $1.15 (1.18) / 1.12 + $1.15 (1.182) / 1.122 + $1.152 (1.182) / 1.123+ {$1.152 (1.182)(1.06) / (0.12 - 0.06)} / 1.123= $26.95[Insert before last sentence of question: Assume that dividends are a fixed proportion of earnings.] Dividend one year from now = $5 (1 - 0.10) = $4.50Price = $5 + $4.50 / {0.14 - (-0.10)}= $23.75Since the current $5 dividend has not yet been paid, it is still included in the stock price.Chapter 6: Some Alternative Investment Rulesa. Payback period of Project A = 1 + ($7,500 - $4,000) / $3,500 = 2 yearsPayback period of Project B = 2 + ($5,000 - $2,500 -$1,200) / $3,000 = 2.43 yearsProject A should be chosen.b. NPV A = -$7,500 + $4,000 / 1.15 + $3,500 / 1.152 + $1,500 / 1.153 = -$388.96NPV B = -$5,000 + $2,500 / 1.15 + $1,200 / 1.152 + $3,000 / 1.153 = $53.83Project B should be chosen.a. Average Investment:($16,000 + $12,000 + $8,000 + $4,000 + 0) / 5 = $8,000Average accounting return:$4,500 / $8,000 = 0.5625 = 56.25%b. 1. AAR does not consider the timing of the cash flows, hence it does not consider the timevalue of money.2. AAR uses an arbitrary firm standard as the decision rule.3. AAR uses accounting data rather than net cash flows.aAverage Investment = (8000 + 4000 + 1500 + 0)/4 = 3375.00Average Net Income = 2000(1-0.75) = 1500=> AAR = 1500/3375=44.44%a. Solve x by trial and error:-$8,000 + $4,000 / (1 + x) + $3000 / (1 + x)2 + $2,000 / (1 + x)3 = 0x = 6.93%b. No, since the IRR (6.93%) is less than the discount rate of 8%.Alternatively, the NPV @ a discount rate of 0.08 = -$136.62.a. Solve r in the equation:$5,000 - $2,500 / (1 + r) - $2,000 / (1 + r)2 - $1,000 / (1 + r)3- $1,000 / (1 + r)4 = 0By trial and error,IRR = r = 13.99%b. Since this problem is the case of financing, accept the project if the IRR is less than the required rate of return.IRR = 13.99% > 10%Reject the offer.c. IRR = 13.99% < 20%Accept the offer.d. When r = 10%:NPV = $5,000 - $2,500 / 1.1 - $2,000 / 1.12 - $1,000 / 1.13 - $1,000 / 1.14When r = 20%:NPV = $5,000 - $2,500 / 1.2 - $2,000 / 1.22 - $1,000 / 1.23 - $1,000 / 1.24= $466.82Yes, they are consistent with the choices of the IRR rule since the signs of the cash flows change only once.A/ $160,000 = 1.04PI = $40,000 715.0Since the PI exceeds one accept the project.Chapter 7: Net Present Value and Capital BudgetingSince there is uncertainty surrounding the bonus payments, which McRae might receive, you must use the expected value of McRae’s bonuses in the computation of the PV of his contract. McRae’s salary plus the expected value of his bonuses in years one through three is$250,000 + 0.6 ⨯ $75,000 + 0.4 ⨯ $0 = $295,000.Thus the total PV of his three-year contract isPV = $400,000 + $295,000 [(1 - 1 / 1.12363) / 0.1236]+ {$125,000 / 1.12363} [(1 - 1 / 1.123610 / 0.1236]= $1,594,825.68EPS = $800,000 / 200,000 = $4NPVGO = (-$400,000 + $1,000,000) / 200,000 = $3Price = EPS / r + NPVGO= $4 / 0.12 + $3=$36.33Year 0 Year 1 Year 2 Year 3 Year 4 Year 51. Annual Salary$120,000 $120,000 $120,000 $120,000 $120,000 Savings2. Depreciation 100,000 160,000 96,000 57,600 57,6003. Taxable Income 20,000 -40,000 24,000 62,400 62,4004. Taxes 6,800 -13,600 8,160 21,216 21,2165. Operating Cash Flow113,200 133,600 111,840 98,784 98,784 (line 1-4)$100,000 -100,0006. ∆ Net workingcapital7. Investment $500,000 75,792*8. Total Cash Flow -$400,000 $113,200 $133,600 $111,840 $98,784 $74,576*75,792 = $100,000 - 0.34 ($100,000 - $28,800)NPV = -$400,000+ $113,200 / 1.12 + $133,600 / 1.122 + $111,840 / 1.123+ $98,784 / 1.124 + $74,576 / 1.125= -$7,722.52Real interest rate = (1.15 / 1.04) - 1 = 10.58%NPV A = -$40,000+ $20,000 / 1.1058 + $15,000 / 1.10582 + $15,000 / 1.10583= $1,446.76NPV B = -$50,000+ $10,000 / 1.15 + $20,000 / 1.152 + $40,000 / 1.153= $119.17Choose project A.PV = $120,000 / {0.11 - (-0.06)}t = 0 t = 1 t = 2 t = 3 t = 4 t = 5 t = 6 ...$12,000 $6,000 $6,000 $6,000$4,000$12,000 $6,000 $6,000 ...The present value of one cycle is:A+ $4,000 / 1.064PV = $12,000 + $6,000 306.0= $12,000 + $6,000 (2.6730) + $4,000 / 1.064= $31,206.37The cycle is four years long, so use a four year annuity factor to compute the equivalent annual cost (EAC).AEAC = $31,206.37 / 406.0= $31,206.37 / 3.4651= $9,006The present value of such a stream in perpetuity is$9,006 / 0.06 = $150,100o evaluate the word processors, compute their equivalent annual costs (EAC).BangAPV(costs) = (10 ⨯ $8,000) + (10 ⨯ $2,000) 414.0= $80,000 + $20,000 (2.9137)= $138,274EAC = $138,274 / 2.9137= $47,456IOUAPV(costs) = (11 ⨯ $5,000) + (11 ⨯ $2,500) 3.014- (11 ⨯ $500) / 1.143= $55,000 + $27,500 (2.3216) - $5,500 / 1.143= $115,132EAC = $115,132 / 2.3216= $49,592BYO should purchase the Bang word processors.Chapter 8: Strategy and Analysis in Using Net Present ValueThe accounting break-even= (120,000 + 20,000) / (1,500 - 1,100)= 350 units. The accounting break-even= 340,000 / (2.00 - 0.72)= 265,625 abalonesb. [($2.00 ⨯ 300,000) - (340,000 + 0.72 ⨯ 300,000)] (0.65)= $28,600This is the after tax profit.Chapter 9: Capital Market Theory: An Overviewa. Capital gains = $38 - $37 = $1 per shareb. Total dollar returns = Dividends + Capital Gains = $1,000 + ($1*500) = $1,500 On a per share basis, this calculation is $2 + $1 = $3 per sharec. On a per share basis, $3/$37 = 0.0811 = 8.11% On a total dollar basis, $1,500/(500*$37) = 0.0811 = 8.11%d. No, you do not need to sell the shares to include the capital gains in the computation of the returns. The capital gain is included whether or not you realize the gain. Since you could realize the gain if you choose, you should include it.The expected holding period return is:()[]%865.1515865.052$/52$75.54$50.5$==-+There appears to be a lack of clarity about the meaning of holding period returns. The method used in the answer to this question is the one used in Section 9.1. However, the correspondence is not exact, because in this question, unlike Section 9.1, there are cash flows within the holding period. The answer above ignores the dividend paid in the first year. Although the answer above technically conforms to the eqn at the bottom of Fig. 9.2, the presence of intermediate cash flows that aren’t accounted for renders th is measure questionable, at best. There is no similar example in the body of the text, and I have never seen holding period returns calculated in this way before.Although not discussed in this book, there are two generally accepted methods of computing holding period returns in the presence of intermediate cash flows. First, the time weighted return calculates averages (geometric or arithmetic) of returns between cash flows. Unfortunately, that method can’t be used here, because we are not given the va lue of the stock at the end of year one. Second, the dollar weighted measure calculates the internal rate of return over the entire holding period. Theoretically, that method can be applied here, as follows: 0 = -52 + 5.50/(1+r) + 60.25/(1+r)2 => r = 0.1306.This produces a two year holding period return of (1.1306)2 – 1 = 0.2782. Unfortunately, this book does not teach the dollar weighted method.In order to salvage this question in a financially meaningful way, you would need the value of the stock at the end of one year. Then an illustration of the correct use of the time-weighted return would be appropriate. A complicating factor is that, while Section 9.2 illustrates the holding period return using the geometric return for historical data, the arithmetic return is more appropriate for expected future returns.E(R) = T-Bill rate + Average Excess Return = 6.2% + (13.0% -3.8%) = 15.4%. Common Treasury Realized Stocks Bills Risk Premium -7 32.4% 11.2% 21.2%-6 -4.9 14.7 -19.6-5 21.4 10.5 10.9 -4 22.5 8.8 13.7 -3 6.3 9.9 -3.6 -2 32.2 7.7 24.5 Last 18.5 6.2 12.3 b. The average risk premium is 8.49%.49.873.125.246.37.139.106.192.21=++-++- c. Yes, it is possible for the observed risk premium to be negative. This can happen in any single year. The.b.Standard deviation = 03311.0001096.0=.b.Standard deviation = = 0.03137 = 3.137%.b.Chapter 10: Return and Risk: The Capital-Asset-Pricing Model (CAPM)a. = 0.1 (– 4.5%) + 0.2 (4.4%) + 0.5 (12.0%) + 0.2 (20.7%) = 10.57%b.σ2 = 0.1 (–0.045 – 0.1057)2 + 0.2 (0.044 – 0.1057)2 + 0.5 (0.12 – 0.1057)2+ 0.2 (0.207 – 0.1057)2 = 0.0052σ = (0.0052)1/2 = 0.072 = 7.20%Holdings of Atlas stock = 120 ⨯ $50 = $6,000 ⨯ $20 = $3,000Weight of Atlas stock = $6,000 / $9,000 = 2 / 3Weight of Babcock stock = $3,000 / $9,000 = 1 / 3a. = 0.3 (0.12) + 0.7 (0.18) = 0.162 = 16.2%σP 2= 0.32 (0.09)2 + 0.72 (0.25)2 + 2 (0.3) (0.7) (0.09) (0.25) (0.2)= 0.033244σP= (0.033244)1/2 = 0.1823 = 18.23%a.State Return on A Return on B Probability1 15% 35% 0.4 ⨯ 0.5 = 0.22 15% -5% 0.4 ⨯ 0.5 = 0.23 10% 35% 0.6 ⨯ 0.5 = 0.34 10% -5% 0.6 ⨯ 0.5 = 0.3b. = 0.2 [0.5 (0.15) + 0.5 (0.35)] + 0.2[0.5 (0.15) + 0.5 (-0.05)]+ 0.3 [0.5 (0.10) + 0.5 (0.35)] + 0.3 [0.5 (0.10) + 0.5 (-0.05)]= 0.135= 13.5%Note: The solution to this problem requires calculus.Specifically, the solution is found by minimizing a function subject to a constraint. Calculus ability is not necessary to understand the principles behind a minimum variance portfolio.Min { X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)}subject to X A + X B = 1Let X A = 1 - X B. Then,Min {(1 - X B)2σA2 + X B2σB2+ 2(1 - X B) X B Cov (R A, R B)}Take a derivative with respect to X B.d{∙} / dX B = (2 X B - 2) σA2+ 2 X B σB2 + 2 Cov(R A, R B) - 4 X B Cov(R A, R B)Set the derivative equal to zero, cancel the common 2 and solve for X B.X BσA2- σA2+ X B σB2 + Cov(R A, R B) - 2 X B Cov(R A, R B) = 0X B = {σA2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}andX A = {σB2 - Cov(R A, R B)} / {σA2+ σB2 - 2 Cov(R A, R B)}Using the data from the problem yields,X A = 0.8125 andX B = 0.1875.a. Using the weights calculated above, the expected return on the minimum variance portfolio isE(R P) = 0.8125 E(R A) + 0.1875 E(R B)= 0.8125 (5%) + 0.1875 (10%)= 5.9375%b. Using the formula derived above, the weights areX A = 2 / 3 andX B = 1 / 3c. The variance of this portfolio is zero.σP 2= X A2 σA2 + X B2σB2+ 2 X A X B Cov(R A , R B)= (4 / 9) (0.01) + (1 / 9) (0.04) + 2 (2 / 3) (1 / 3) (-0.02)= 0This demonstrates that assets can be combined to form a risk-free portfolio.14.2%= 3.7%+β(7.5%) ⇒β = 1.40.25 = R f + 1.4 [R M– R f] (I)0.14 = R f + 0.7 [R M– R f] (II)(I) – (II)=0.11 = 0.7 [R M– R f] (III)[R M– R f ]= 0.1571Put (III) into (I) 0.25 = R f + 1.4[0.1571]R f = 3%[R M– R f ]= 0.1571R M = 0.1571 + 0.03= 18.71%a. = 4.9% + βi (9.4%)βD= Cov(R D, R M) / σM 2 = 0.0635 / 0.04326 = 1.468= 4.9 + 1.468 (9.4) = 18.70%Weights:X A = 5 / 30 = 0.1667X B = 10 / 30 = 0.3333X C = 8 / 30 = 0.2667X D = 1 - X A - X B - X C = 0.2333Beta of portfolio= 0.1667 (0.75) + 0.3333 (1.10) + 0.2667 (1.36) + 0.2333 (1.88)= 1.293= 4 + 1.293 (15 - 4) = 18.22%a. (i) βA= ρA,MσA / σMρA,M= βA σM / σA= (0.9) (0.10) / 0.12= 0.75(ii) σB= βB σM / ρB,M= (1.10) (0.10) / 0.40= 0.275(iii) βC= ρC,MσC / σM= (0.75) (0.24) / 0.10= 1.80(iv) ρM,M= 1(v) βM= 1(vi) σf= 0(vii) ρf,M= 0(viii) βf= 0b. SML:E(R i) = R f + βi {E(R M) - R f}= 0.05 + (0.10) βiSecurity βi E(R i)A 0.13 0.90 0.14B 0.16 1.10 0.16C 0.25 1.80 0.23Security A performed worse than the market, while security C performed better than the market.Security B is fairly priced.c. According to the SML, security A is overpriced while security C is under-priced. Thus, you could invest in security C while sell security A (if you currently hold it).a. The typical risk-averse investor seeks high returns and low risks. To assess thetwo stocks, find theReturns:State of economy ProbabilityReturn on A*Recession 0.1 -0.20 Normal 0.8 0.10 Expansion0.10.20* Since security A pays no dividend, the return on A is simply (P 1 / P 0) - 1. = 0.1 (-0.20) + 0.8 (0.10) + 0.1 (0.20) = 0.08 = 0.09 This was given in the problem.Risk:R A - (R A -)2 P ⨯ (R A -)2 -0.28 0.0784 0.00784 0.02 0.0004 0.00032 0.12 0.0144 0.00144 Variance 0.00960Standard deviation (R A ) = 0.0980βA = {Corr(R A , R M ) σ(R A )} / σ(R M ) = 0.8 (0.0980) / 0.10= 0.784βB = {Corr(R B , R M ) σ(R B )} / σ(R M ) = 0.2 (0.12) / 0.10= 0.24The return on stock B is higher than the return on stock A. The risk of stock B, as measured by itsbeta, is lower than the risk of A. Thus, a typical risk-averse investor will prefer stock B.b. = (0.7) + (0.3) = (0.7) (0.8) + (0.3) (0.09) = 0.083σP 2= 0.72 σA 2 + 0.32 σB 2 + 2 (0.7) (0.3) Corr (R A , R B ) σA σB = (0.49) (0.0096) + (0.09) (0.0144) + (0.42) (0.6) (0.0980) (0.12) = 0.0089635 σP = = 0.0947 c. The beta of a portfolio is the weighted average of the betas of the components of the portfolio. βP = (0.7) βA + (0.3) βB = (0.7) (0.784) + (0.3) (0.240) = 0.621Chapter 11:An Alternative View of Risk and Return: The Arbitrage Pricing Theorya. Stock A:()()R R R R R A A A m m Am A=+-+=+-+βεε105%12142%...Stock B:()()R R R R R B B m m Bm B=+-+=+-+βεε130%098142%...Stock C:()R R R R R C C C m m Cm C=+-+=+-+βεε157%137142%)..(.b.()[]()[]()[]()()()()()()[]()()CB A m cB A m c m B m A m CB A P 25.045.030.0%2.14R 1435.1%925.1225.045.030.0%2.14R 37.125.098.045.02.130.0%7.1525.0%1345.0%5.1030.0%2.14R 37.1%7.1525.0%2.14R 98.0%0.1345.0%2.14R 2.1%5.1030.0R 25.0R 45.0R 30.0R ε+ε+ε+-+=ε+ε+ε+-+++++=ε+-++ε+-++ε+-+=++= c.i.()R R R A B C =+-==+-==+-=105%1215%142%)1113%09815%142%)137%157%13715%142%168%..(..46%.(......ii.R P =+-=12925%1143515%142%)138398%..(..To determine which investment investor would prefer, you must compute the variance of portfolios created bymany stocks from either market. Note, because you know that diversification is good, it is reasonable to assume that once an investor chose the market in which he or she will invest, he or she will buy many stocks in that market.Known:E EF ====001002 and and for all i.i σσεε..Assume: The weight of each stock is 1/N; that is, X N i =1/for all i.If a portfolio is composed of N stocks each forming 1/N proportion of the portfolio, the return on the portfolio is 1/N times the sum of the returns on the N stocks. Recall that the return on each stock is 0.1+βF+ε.()()()()()()[]()()()()()()()[]()[]()[]()()[]()()()()()j i 2j i 22j i i 2222222222P P P P iP ,0.04Corr 0.01,Cov s =isvariance the ,N as limit In the ,Cov 1/N 1s 1/N s )(1/N 1/N F 2F E 1/N F E 0.10.1/N F 0.1E R E R E R Var 0.101/N 00.1E 1/N F E 0.11/N F 0.1E R E 1/N F 0.1F 0.1(1/N)R 1/N R εε+β=εε+β∞⇒εε-+ε+β=ε∑+εβ+β=ε+β=-ε+β+=-==+β+=ε+β+=ε∑+β+=ε+β+=ε+β+==∑∑∑∑∑∑∑∑()()()()()()Thus,F R f E R E R Var R Corr Var R Corr ii ip P p i j PijR 1i =++=++===+=+010*********002250040002500412212111222.........,,εεεεεεa.()()()()Corr Corr Var R Var R i j i j p pεεεε112212000225000225,,..====Since Var ()()R p 1 Var R 2p 〉, a risk averse investor will prefer to invest in the second market.b. Corr ()()εεεε112090i j j ,.,== and Corr 2i()()Var R Var R pp120058500025==..。

F9-chapter 17

225Chapter 1717. Business ValuationChapter GuideG1. Nature and purpose of the valuation of business and financial assets a) Identify and discuss reasons for valuing businesses and financial assets. b) Identify information requirements for valuation and discuss the limitationsof different types of informationG2. Models for the valuation of shares a) Asset-based valuation models, including: i. Net book value (balance sheet basis) ii. Net realizable value basis iii. Net replacement cost basisb) Income-based valuation models, including: i. Price/ earnings ratio method ii. Earnings yield methodc) Cash flow-based valuation models, including:i. Dividend valuation model and the dividend growth model. ii. Discounted cash flow basis.G3. The valuation of debt and other financial assets Apply appropriate valuation methods to: i. Irredeemable Debt, ii. Redeemable Debt, iii. Convertible Debt iv. Preference Shares.226Chapter overview227There are number of different ways of putting a value on a business, or on shares in an unquoted company. It is important for the buyer to use several methods of valuation, ant to compare the values they produce.Here are some major valuation methods: ✓ Cash flow based valuation ✓ Income based valuation ✓ Asset based valuation ✓ Market capitallisationIf a business is difficult to sell, its owners may be prepared to accept a minimum bid that matched the value that they get from liquidation. There are 2 ways of assessing this:2.1 Different Valuesa) Balance sheet value - but the book value of assets will differ from theirmarket valueb) Realisable value - better, but more difficult to calculate.2.2 Advantages and Disadvantages of Asset based valuation1.Reasons for business valuations2.Asset valuation bases228Lecture example 1The summary statement of financial position of Tiger Plc is as follows.Non-current assts $ $ $ Land and buildings 160,000 Plant and machinery 80,000 Motor vehicle 20,000 260,000 Goodwill 20,000 Current assets Inventory 80,000 Receivables 60,000 Short-term investments 15,000Cash5,000 160,000 Current liabilities Payables 60,000 Taxation 20,000 Proposed ordinary dividend 20,000 (100,000) 60,000 340,000 12% bonds (60,000) Deferred taxation (10,000) 270,000 Ordinary share of $1 80,000 Reserves 140,000 220,000 4.9% preference shares if $1 50,000 270,000RequiredWhat is the value per ordinary share using the net assets basis of valuation?229As a measure of the ' security ' in a share value2.3 Circumstances of using Net asset based measuree.g. if the company went into liquidation, the investor could not expect to receive the full value of his shares when the underlying assets were realised.As a measure of comparison in a scheme of mergerA merger is essentially a business combination of two or more companies, of which none obtains control over any other.For example, if company A, which has a low asset backing, is planning a merger with company B, which has a high asset backing, the shareholders of B might consider that their shares value ought to reflect this. If might therefore be agreed that a something should be added to the value of the company B shares to allow for this difference in asset backing.As a ' floor value ' for a business that is up for sale-shareholders will bereluctant to sell for less than the NAV. However, if the sale is essential for cash flow purposes or to realign with corporate strategy, even the asset value may not be realised.For these reasons, it is always advisable to calculate the net assets per share.3.1 Price earning valuation (P/E)Market valuation / capitalisation = P/E ratio x Earnings per share or P/E ratio x total earningsP/E may need adjustments due to different business risks3.2 Advantages and Disadvantages of P/E valuation 3. Earning/ Income bases230(a) There are good reasons to believe that earnings growth will be achieved. 3.3 Use of forecast earningsWhen one company is thinking about taking over another, it should look at the target company’s forecast earnings, not just its historical results. Forecasts of earnings growth should only be used if:(b) Areasonable estimate of growth can be made.(c) Forecasts supplied by the target company’s directors are made in goodfaith and using reasonable assumptions and fair accounting policies.share per price Market EPS=yield Earnings 3.4Earnings yield valuationyield Earnings Earnings =ue Market valWe can incorporate earnings growth into this method in the same way as the growth model that we will discuss in later sections. Market value )()1(g EY g Earnings −+×=231Lecture Example 2A company has the following results.20×1 20×2 20×3 20×4$m $m $m $mProfit after tax6.0 6.2 6.3 6.3The company's earnings yield is 12%.RequiredCalculate the value of the company based on the present value of expected earnings.Cash flow based valuation models include Dividend valuation model,The dividend growth model and The discounted cash flow basis.KeDKe D Ke D Ke D =++++++....3)1(2)1(14.1 Dividend valuation modelThe dividend valuation model is based on the theory that an equilibrium price for any share (pr bond) on a stock market is the future expected stream of income from the security discounted at a suitable cost of capital. Equilibrium market price is thus a present value of a future expected income stream. The annual income stream for a share is the expected dividend every year in perpetuity.The basic dividend-based formula for the market value of shares is expressed in the dividend valuation model as follows: MV (ex div) =Where Do=Current year's dividendg=Growth rate in earnings and dividends Do (1+g)=Expected dividend in one year's time(D1) K e =Shareholder's required rate of return4. Cash flow based232gK g D P e −+=)1(004.2 Dividend growth valuation model Value per shareWhereD 0= dividend paid nowK e = cost of equity of the target g = growth rate in dividendsP o =Market value excluding any dividend currently payable.Disadvantages of dividend valuation model✓ It is difficult to estimating future dividend growth✓ It is inaccurate to assume that growth will be constant ✓ It creates zero values for zero dividend companies.✓ It creates negative values for high growth companies, if g >KeLecture example 3Target paid a dividend of $250,000 this year. The current return to shareholders of companies in the same industry as Target is 12%, although it is expected that an additional risk premium of 2% will be applicable to Target, being a smaller and unquote company.Compute the expected valuation of Target, if:a) The current level of dividend is expected to continue into the foreseeablefuture, orb) The dividend is expected to grow at a rate of 4% pa into the foreseeablefuturec) The dividend is expected to grow at a 3% rate for three years and 2%afterwards.233Lecture example 4Hawk Plc. wishes to make a bid for Pigeon Ltd. Pigeon makes after-tax profits of $40,000 a year. Hawk believes that if further money is spent on additional investments, the after-tax cash flows (ignoring the purchase consideration) could be as follows.Year Cash flow (net of tax) $ 0 (100,000) 1 (80,000) 2 60,000 3 100,000 4 150,000 5 150,000The after-tax cost of capital of Hawk plc is 15% and the company expects all its investments to pay back, in discounted terms, within five years. What is the maximum price that the company should be willing to pay for the shares of Tadpole?Discounted cash flow techniques can be used to value irredeemable debt, redeemable debt, convertible debt and preference shares, which covered in prior chapters (chapter 15)Valuation of other securities234Lecture example 5The directors of Carmen, a large conglomerate, are considering the acquisition of the entire share capital of Manon, which manufactures a range of engineering machinery. Neither company has any long-term debt capital. The directors of Carmen believe that if Manon is taken over, the business risk of Carmen will not be affected.The accounting reference date of Manon is 31 July. Its balance sheet as on 31 July 20x4 is expected to be as follows $ $ Non-current assets (net of depreciation) 651,600 Current assets: inventory and work in progress 515,900 receivables 745,000bank balances 158,1001,419,000 2,070,600 Current liabilities: payables 753,600 bank overdraft 862,900 1,616,500 Capital and reserves: issued ordinary shares of $1 each50,000 distributable reserves 404,100 2,070,600Manon’s summarized financial record for the five years to 31 July 20X4 is as follows.Year ended 31 July 20X0 20X1 20X2 20X320X4(estimated ) Profit before non recurring items 30,400 69,000 49,400 48,200 53,200Non recurringitems2,900 (2,200) (6,100) (9,800) (1,000)Profit after nonrecurring items 33,300 66,800 43,300 38,400 52,200Less dividends 20,500 22,600 25,000 25,000 25,000 Added toreserves 12,800 44,200 18,300 13,400 27,200235The following additional information is available:1) There have been no changes in the issued share capital of Manon duringthe past five years2) The estimated values of Manon’s non-current assets and inventory andwork in progress as on 31 July 20X4 are as follows. Replacement cost $ Realizable value$Non-current assets 725,000 450,000 Inventory and work in progress 550,000 570,0003) It is expected that 2% of Manon’s receivables at 31 July 20X4 will beuncollectable.4) The cost of capital of Carmen plc is 9%. The directors of Manon estimatethat the shareholders of Manon require a minimum return of 12% per annum from their investment in the company5) The current P/E ratio of Carmen is 12. Quoted companies with businessactivities and profitability similar to those of Manon have P/E ratios of approximately 10, although these companies tend to be much larger than Manon.Required(a) Estimate the value of the total equity (i.e. market capitalization) of Manonas on 31 July 20X4 using each of the following bases: (i) Balance sheet value(ii) Replacement cost of the assets (iii) Realizable value of the assets (iv) The dividend valuation model (v) The P/E ratio model(13 marks)(b) Explain the role and limitations of each of the above five valuation bases inthe process by which a price might be agreed for the purchase by Carmen of the total equity capital of Manon(6 marks)(c) State and justify briefly the approximate range within which the purchaseprice is likely to be agreed(6 marks)(Total = 25 marks)Ignore taxation236Chapter summary237Answer to lecture example 1Asset Value:= €62.8m – debt of 33.1 = €29.7mLack of the information about the industry, the nature of the assets or any intangible values.Solution to lecture example 2 Market value )()1(g EY g Earnings −+×=Earnings =$6.3m EY =12% g =%64.10164.010.63.63or =− Market value 0164.012.00164.13.6−×==$61.81mAnswer to lecture example 3Ke=12%+2%=14%(0.14) Do=$250,000 g(in (b))=4% or 0.04714,758,1$14.0000,250$===Ke Do Po000,600,2$04.014.0)04.1(000,250$)1(=−=−+=g Ke g Do PoTime1 2 3 4onwards Dividend ($000)258266274279 Annuity to infinity (g Ke −1) 8,333 Present value at Year 3 2,325 Discount factor @ 14% 0.877 0.769 0.675 0.6752262051851,569Total $2,185,000Answer to lecture examples238Lecture example 4The maximum price is one which would make the return from the total investment exactly 15% over five years, so that the NPV at 15% would be 0.Year Cash flow Discount factor Present value$ 15% $ 0 (100,000) 1.000 (100,000) 1 (80,000) 0.870 (69,600) 2 60,000 0.756 45,360 3 100,000 0.658 65,800 4 150,000 0.572 85,800 5 150,000 0.497 74,550Maximum purchase price 101,910Lecture example 5 (a)(i) Balance sheet value =$454,100.(ii) Replacement cost value =$454,100 + $(725,000 – 651,600) + $(550,000-515,900) = $561,600(iii) Realizable value = $454,100 + $(450,000 – 651,600) + (570,000 – 515,900)- $14,900 =$291,700Bad debts are 2% x $745,000 = $14,900. Bad debts are assumed not to be relevant to balance sheet and replacement cost values(iv) The dividend growth model value depends non-current an estimated ofgrowth, which is far from dear given the wide variations in earnings over the five years.1. The lowest possible value, assuming zero growth, is as follows.Value ex div =$25,0000.12= $208,333It is not likely that this will be the basis taken.2. Looking at dividend growth over the past five years we have:20X4 dividend = $25,000 20X0 dividend = $20,500If the annual growth rate in dividends is g(1+g)4 =(25,000)20,500=1.21952391+g =1.0508g = 0.0508, say 5.1%Then, MV ex div =Dividend in 1 year 0.12−g= 25,000 (1.051)0.069= $380,7973. Using the rb model, we have: Average proportion remained= 12,800+44,200+18,300+13,400+27,200+52,200=0.495 ≈0.5 Return on investment this year =53,200average investment=53,200(454,100+(454,100−27,200))/2= 0.1208 (say r =12%)Then g = 0.5 x 12%=6% So MV ex div =$25,000 (1.06)0.06 = $441,667(v) P/E ratio modelComparable quoted companies to Manon have P/E ratios of about 10. Manon is much smaller and being unquoted its P/E ratio would be less than 10, but how much less?If we take a P/E ratio of 5, we have MV = $53,200 x 5 =$266,000If we take a P/E ratio of 10 x 2/3, we have MV = $53,200 x 10 x2/3 =$354,667If we take a P/E ratio of 10, we have MV = $53,200 x 5 =$532,000 (b)(i) The balance sheet valueThe balance sheet value should not play a part in the negotiation process. Historical costs are not relevant to a decision on the future value of the company(ii) The replacement costThis gives the cost of setting up a similar business. Since this gives a higher figure then any other valuation in this case, it could show the240 maximum price for Carmon to offer. There is clearly no goodwill to value(iii) The realizable valueThis shows the cash which the shareholders in Manon could get by liquidating the business. It is therefore the minimum price which they would accept.All the method (i) to (ii) suffer from the limitation that they do not look at the going concern value of the business as a whole.Methods (iv) and (v) do consider this value. However, the realizable value is of use in assessing the risk attached to the business as a going concern, as it gives the base value if things go wrong and the business has to be abandoned.(iv) The dividend modelThe figures have been calculated using Manon’s K e(12%). If (2) or (3) were followed, the value would be the minimum that Manon’s shareholders would accept, as the value in use exceeds scrap value in (iii). The relevance of a dividend valuation to Carmen will depend on whether the current retention and reinvestment policies would be continued. Certainly the value to Carmen should be based on 9% rather than 12%. Both companies are ungeared and in the same risk class so the different required returns must be due to their relative sizes and the fact that Carmen’s shares are not more marketable.One of the main limitations on the dividend growth model is the problem of estimating the future value of g.(v) The P/E ratio modelThe P/E ratio model is an attempt to get at the value which the market would put on a company like Manon. It does provide an external yardstick, but is a very crude measure. As already stated, the P/E ratio which applies to larger quoted companies must be lowered to allow for the size of Manon and the non-marketability of its shares. Another limitation of P/E ratios is that the ratio is very dependent on the expected future growth of the firm. It is therefore not easy to find a P/E ratio of a ‘similar firm’. However, in practice the P/E model may well feature in the negotiations over price simply because it is an easily understood yardstick.(c) The range within which the purchase price is likely to be agreed will be theminimum price which the shareholders of Manon will accept and the maximum price which the directors of Carmen will pay.The minimum price which the shareholders of Manon will accept will be the241realizable value of the assets, £291,700. The maximum price Carmen will pay is the earnings basis using a P/E of 10 at £532,000.The dividend basis gives a value of about 5% gives a value of £380,797. This looks optimistic given the lack of dividend growth over the last couple of years.So the eventual purchase price will probably be in the range £291,700 and £375,000.。

Private Equity in China. Challenges and Opportunities

BrochureMore information from /reports/2112831/Private Equity in China. Challenges and OpportunitiesDescription:Learn valuable lessons from the newly successful private equity players in China and explore the challenges and opportunities offered in Chinese marketsThe first book to deal with private equity finance in China, Private Equity in China: Challenges andOpportunities provides much-needed guidance on an investment concept that has so far provedelusive in Asia. Focusing on the opportunities that the Chinese finance market offers to privateequity firms, the book shows how these firms can strategically position themselves in order tomaximize success in this new marketplace.Private Equity in China includes in-depth case studies illustrating both successful and failedventures by private equity firms operating in China, outlining the challenges faced by private equityfirms in setting up new funds. It contains a collection of valuable experience and insights aboutacquiring companies and turning them around essential for any firm currently operating in, orconsidering entering, the Chinese market.- Discusses the challenges faced by private equity firms in China including setting up the initialfund, fund raising, deal sourcing, deal execution, and monitoring and exit strategies- Provides key insights drawn from keen observations and knowledge of the more mature privateequity market in Western countries, analyzing the way forward for the Chinese private equityindustry- Discusses the role of renminbi-denominated funds in the development of the private equityindustry in ChinaBreaking new ground in exploring and explaining the private equity market in China, the bookoffers incredible new insight into how equity companies can thrive in the Chinese marketplace.Contents:Preface xiiiAcknowledgments xviiCHAPTER 1 Private Equity: An Introduction 1Overview 1Stages of Development of a Company 2Differences between Private Equity and Venture Capital 5Differences between Private Equity Investments and Corporate Mergers and Acquisitions 6Inventis Private Equity Model 8Structure of a Private Equity Fund 11General Partners 11Limited Partners 12Investment Committee/Advisors 12Professionals 12Private Equity Investment Process 13Planning, Fund-Raising, and Deal Sourcing 14Due Diligence 16Deal Structuring 18Portfolio Management 21Exit Strategies 24CHAPTER 2 Overview of the Political, Macroeconomic, and Financial Landscape in China 33 Overview 33Regulatory Environment 35Chinese Government Agencies and Their Relevance to Private Equity 37China’s Macroeconomic Conditions and Trends 45Macroeconomic Condition 1: Inflation 48Macroeconomic Condition 2: Widening Income Disparity 49Macroeconomic Condition 3: Accelerated Aging Population Structure 50Macroeconomic Trend 1: Increasing Urbanization 51Macroeconomic Trend 2: Westward Shift in Industrialization and Development 53 Macroeconomic Trend 3: Strong Growth in Domestic Consumption 54Macroeconomic Trend 4: Shift Toward Value-Added Industries 56China’s Financial Markets 57Key Phases of Developments in China’s Capital Markets 58China’s Equity Markets 62Foreign Listings on Chinese Exchanges 65China’s Credit Market 67Trust Financing 72China’s Futures Markets: Commodity Exchanges and Derivatives Exchanges 73Summary 75CHAPTER 3 Private Equity in China 77Overview 77Key Market Trends and Developments 79Private Minority Placement Quadrant 81Private Majority Placement Quadrant 82PIPE Minority Deals Quadrant 83Private Equity Funds in China 97Foreign-Owned Private Equity Funds (FOPE) 97Chinese-Owned Private Equity Funds (COPE) 99State-Owned Industrial Private Equity Funds (SOPE) 100Hybrid Foreign/Chinese USD and RMB Private Equity Fund (HOPE) 101Private Equity Investment Structures in China 102Red Chip Structure or Round-Trip Investment 102Onshore Structures 108Leveraged Buyouts 112Valuation Adjustment Mechanism 114VAM in China’s Private Equity Industry 114Financial Measures 116Non-Financial Redemption Measures and Stock Offerings 117Stock Offering: Expiration of VAM Agreement 119Challenges of VAM 121Exit Strategies for Private Equity Investment in China 121Initial Public Offerings 122Initial Public Offerings in Domestic Markets 125Initial Public Offerings in Overseas Markets 129Trade Sales 130Secondary Sales 130Leveraged Recapitalization/Distribution of Dividend 131Benefits of Private Equity for China 132The Case for Demutualization of Chinese Stock Exchanges through Private Equity Investments 136 CHAPTER 4 Renminbi Private Equity Fund 137Overview 137Setting Up and Fund-Raising in China 138Investing in China 142Exit Options for the RMB Fund 143The Renminbi Private Equity Fund 144Types of RMB Funds 145Domestic Limited Partners 149Private Equity Regulations and Incentives 159RMB Funds’ Edge in Investing in China 160Challenges and Opportunities for FOPE-RMB Funds 161The Future of Domestic Limited Partners 162Qualifi ed Foreign Limited Partnership Pilot Program 163Management of Hybrid Funds 166Onshore Legal Structures of RMB Funds 171Restrictions for Foreign-Invested Partnerships (FIPs) 175Treatment of FOPE-RMB Funds: Domestic or Foreign? 176Exit Options for RMB Funds 177Domestic Listings on Chinese Stock Exchanges 178Private Equity Secondary Markets in China 179China’s Domestic Limited Partners 180Impacts of RMB Convertibility on RMB Private Equity Funds 181RMB Private Equity Outbound Investments 182CHAPTER 5 Investment Opportunities for Private Equity in China 187 Overview 187Foreign Acquisition and National Security Review 189China’s Five-Year Plan for National Economic and Social Development 191 China’s Seven Emerging Strategic Industries 195Energy Saving and Environmental Protection 199Renewable Energy 205Alternative Energy Vehicles 210Next Generation Information Technology 213High-End Equipment Manufacturing 215Biotechnology 217New Materials 221Investment Opportunities in China’s Energy Sector 224Key Energy Security Concerns 224Strategies to Tackle China’s Energy Challenges 227Trends in the Oil and Gas Sector in China 230Relationship between the Energy Firms and the Government 233CHAPTER 6 Challenges and the Future of Private Equity in China 235Overview 235Fund-Raising 236Deal Sourcing 238Good Deals Are Getting Scarce, Valuations Becoming Too High 239FOPE Funds Are Competing with COPE Funds in Deal Sourcing 239Moving West 240Consolidation Opportunities 240Seeking Uniqueness from Other Funding Sources 241Due Diligence 242Reliability of Financial Statements 243Intellectual Property Rights 245Deal Structuring 247Portfolio Management 250Change from Boss Culture to Management Culture 251Communication and Timely Information 251Resistance to Change 252Fighting for Control 253Exit 255Valuation Obstacles 256China’s Private Equity Secondary Sales Market Is in the Nascent Stage 257Foreign Exchange Controls and RMB Convertibility 258Avoiding the Restriction or Seeking Local Government’s Aid 258Gradual Loosening of Capital Inflows, Especially for Private Equity 259Capital Outflows Are Strict, But Less Stringent than Inflows 259The RMB Fund Advantage—Artificial and Temporary? 260Media Reports and Public Perception 262Guanxi Management 264One Party to Gain Positive Career Prospects, the Other to Gain Justice Support 265Private Equity Firms Do Not Invest in Green Fields, So No Need to Build Complicated Relationships 266The Company Shareholders and Management Team Already Have Guanxi for Running the Business266Private Equity Firms Can Engage an External Consulting or Public Relations Firm 266FOPE-RMB Funds 268COPE-USD Funds 269Leveraged Buyouts 270Private Equity Professionals in China 271Trend 1: From Foreign to Domestic Private Equity 273Trend 2: From Investment Banks to Private Equity 274Trend 3: From Traditional Industries to Private Equity 275Trend 4: From Entrepreneurs to GPs and LPs 275Conclusion 276APPENDIX A Government Structure of the People’s Republic of China 281APPENDIX B Key Points in a Private Placement Memorandum 287APPENDIX C Geography of China 289APPENDIX D Selected Private Equity Funds in Greater China 293About the Author 299IndexOrdering:Order Online - /reports/2112831/Order by Fax - using the form belowOrder by Post - print the order form below and send toResearch and Markets,Guinness Centre,Taylors Lane,Dublin 8,Ireland.Fax Order FormTo place an order via fax simply print this form, fill in the information below and fax the completed form to 646-607-1907 (from USA) or +353-1-481-1716 (from Rest of World). If you have any questions please visit/contact/Order Information Please verify that the product information is correct.Product Format Please select the product format and quantity you require:* Shipping/Handling is only charged once per order.Contact InformationPlease enter all the information below in BLOCK CAPITALSProduct Name:Private Equity in China. Challenges and Opportunities Web Address:/reports/2112831/Office Code:OC8DIROPONQPTX QuantityHard Copy :EURO€ 116.00 + Euro €25 Shipping/HandlingTitle:MrMrsDrMissMsProf First Name:Last Name:Email Address: *Job Title:Organisation:Address:City:Postal / Zip Code:Country:Phone Number:Fax Number:* Please refrain from using free email accounts when ordering (e.g. Yahoo, Hotmail, AOL)Payment InformationPlease indicate the payment method you would like to use by selecting the appropriate box.Please fax this form to:(646) 607-1907 or (646) 964-6609 - From USA+353-1-481-1716 or +353-1-653-1571 - From Rest of WorldPay by credit card:American ExpressDiners ClubMaster CardVisa Cardholder's Name Cardholder's Signature Expiry Date Card Number CVV Number Issue Date(for Diners Club only)Pay by check:Please post the check, accompanied by this form, to:Research and Markets,Guinness Center,Taylors Lane,Dublin 8,Ireland.Pay by wire transfer:Please transfer funds to:Account number833 130 83Sort code98-53-30Swift codeULSBIE2D IBAN numberIE78ULSB98533083313083Bank Address Ulster Bank,27-35 Main Street,Blackrock,Co. Dublin,Ireland.If you have a Marketing Code please enter it below:Marketing Code:Please note that by ordering from Research and Markets you are agreeing to our Terms and Conditions at /info/terms.asp。

Business Studies 02

Percentage

100 100 96 94 94 89 85 75 73 62 61 54

Chapter 2 - 12

Balancing Business and Stakeholders’ Rights

Business Investors

Maximize Profits

© Prentice Hall, 2005

Provide Jobs and Pay Taxes

Business In Action 3e

Balance Profits and Social Issues

Chapter 2 - 11

Percentage of Executives Who “Strongly Agree” or “Agree” That Companies Should:

Practicing Ethical Behavior and Social Responsibility

© Prentice Hall, 2005

Business In Action 3e

Chapter 2 - 1

Two Important Concepts

Social Responsibility

The Right to Safe Products The Right to Be Informed The Right to Choose The Right to Be Heard

© Prentice Hall, 2005 Business In Action 3e Chapter 2 - 18

•Be environmentally responsible •Be ethical in operations •Earn profits •Employ local residents •Pay taxes •Encourage and support employee volunteering •Contribute money and leadership to charities •Be involved in economic development •Be involved in public education •Involve community representatives in business decisions •Target a portion of purchasing toward local vendors •Help improve quality of life for low-income populations

财务管理 CHAPTER 模板

CHAPTER 8Stock Valuation II. CONCEPTSVALUATION OF ZERO GROWTH STOCKc 26. The James River Co. pays an annual dividend of $1.50 per share on its common stock.This dividend amount has been constant for the past 15 years and is expected to remainconstant. Given this, one share of James River Co. stock:a. is basically worthless as it offers no growth potential.b. has a market value equal to the present value of $1.50 paid one year from today.c. is valued as if the dividend paid is a perpetuity.d. is valued with an assumed growth rate of 3 percent.e. has a market value of $15.00.VALUATION OF ZERO GROWTH STOCKe 27. The common stock of the Kenwith Co. pays a constant annual dividend. Thus, themarket price of Kenwith stock will:a. also remain constant.b. increase over time.c. decrease over time.d. increase when the market rate of return increases.e. decrease when the market rate of return increases.DIVIDEND YIELD VS. CAPITAL GAINS YIELDc 28. The Koster Co. currently pays an annual dividend of $1.00 and plans on increasingthat amount by 5 percent each year. The Keyser Co. currently pays an annualdividend of $1.00 and plans on increasing their dividend by 3 percent annually.Given this, it can be stated with certainty that the _____ of the Koster Co. stock isgreater than the _____ of the Keyser Co. stock.a. market price; market priceb. dividend yield; dividend yieldc. rate of capital gain; rate of capital gaind. total return; total returne. capital gains; dividend yieldDIVIDEND GROWTH MODELd 29. The dividend growth model:I. assumes that dividends increase at a constant rate forever.II. can be used to compute a stock price at any point of time.III. states that the market price of a stock is only affected by the amount of the dividend.IV. considers capital gains but ignores the dividend yield.a. I onlyb. II onlyc. IIIand IV onlyd. I and II onlye. I, II, and III onlyDIVIDEND GROWTH MODELb 30. The underlying assumption of the dividend growth model is that a stock is worth:a. the same amount to every investor regardless of their desired rate of return.b. the present value of the future income which the stock generates.c. an amount computed as the next annual dividend divided by the market rate ofreturn.d. the same amount as any other stock that pays the same current dividend and has thesame required rate of return.e. an amount computed as the next annual dividend divided by the required rate ofreturn.DIVIDEND GROWTH MODELc 31. Assume that you are using the dividend growth model to value stocks. If you expectthe market rate of return to increase across the board on all equity securities, thenyou should also expect the:a. market values of all stocks to increase, all else constant.b. market values of all stocks to remain constant as the dividend growth will offset theincrease in the market rate.c. market values of all stocks to decrease, all else constant.d. stocks that do not pay dividends to decrease in price while the dividend-payingstocks maintain a constant price.e. dividend growth rates to increase to offset this change.NONCONSTANT GROWTHc 32. Latcher’s Inc. is a relatively new firm that is still in a period of rapid development. Thecompany plans on retaining all of its earnings for the next six years. Seven years fromnow, the company projects paying an annual dividend of $.25 a share and thenincreasing that amount by 3 percent annually thereafter. To value this stock as oftoday, you would most likely determine the value of the stock _____ years fromtoday before determining today’s value.a. 4b. 5c. 6d. 7e. 8NONCONSTANT GROWTHd 33. The Robert Phillips Co. currently pays no dividend. The company is anticipatingdividends of $0, $0, $0, $.10, $.20, and $.30 over the next 6 years, respectively. Afterthat, the company anticipates increasing the dividend by 4 percent annually. The firststep in computing the value of this stock today, is to compute the value of the stock inyear:a. 3.b. 4.c. 5.d. 6.e. 7.SUPERNORMAL GROWTHb 34. Supernormal growth refers to a firm that increases its dividend by:a. three or more percent per year.b. a rate which is most likely not sustainable over an extended period of time.c. a constant rate of 2 or more percent per year.d. $.10 or more per year.e. an amount in excess of $.10 a year.DIVIDEND YIELD AND CAPITAL GAINSe 35. The total rate of return earned on a stock is comprised of which two of thefollowingI. current yieldII. yield to maturityIII. dividend yieldIV. capital gains yielda. I and II onlyb. I and IV onlyc. II and III onlyd. II and IV onlye. IIIand IV onlyDIVIDEND YIELDc 36. The total rate of return on a stock can be positive even when the price of the stockdepreciates because of the:a. capital appreciation.b. interest yield.c. dividend yield.d. supernormal growth.e. real rate of return.DIVIDEND YIELD AND CAPITAL GAINSc 37. Fred Flintlock wants to earn a total of 10 percent on his investments. He recentlypurchased shares of ABC stock at a price of $20 a share. The stock pays a $1 a yeardividend. The price of ABC stock needs to _____ if Fred is to achieve his 10percent rate of return.a. remain constantb. decrease by 5 percentc. increase by 5 percentd. increase by 10 percente. increase by 15 percentDIVIDEND GROWTH MODELd 38. Which one of the following correctly defines the dividend growth modela. P0 = D0 (R-g)b. D = P0⨯ (R-g)c. R = (P0÷ D0) + gd. R = (D1÷ P0) + ge. P0 = (D1÷ R) + gSHAREHOLDER RIGHTSa 39. Shareholders generally have the right to:I. elect the corporate directors.II. select the senior management of the firm.III. elect the chief executive officer (CEO).IV. elect the chief operating officer (COO).a. I onlyb. I and III onlyc. II onlyd. I and II onlye. IIIand IV onlyCUMULATIVE VOTINGc 40. Jack owns 35 shares of stock in Beta, Inc. and wants to exercise as much control aspossible over the company. Beta, Inc. has a total of 100 shares of stock outstanding.Each share receives one vote. Presently, the company is voting to elect two newdirectors. Which one of the following statements must be true given thisinformationa. If straight voting applies, Jack is assured one seat on the board.b. If straight voting applies, Jack can control both open seats.c. If cumulative voting applies, Jack is assured one seat on the board.d. If cumulative voting applies, Jack can control both open seats.e. Regardless of the type of voting employed, Jack does not own enough shares tocontrol any of the seats.STRAIGHT VOTINGa 41. ABC Co. is owned by a group of shareholders who all vote independently and whoall want personal control over the firm. If straight voting is utilized, a shareholder:a. must either own enough shares to totally control the elections or else he/she has nocontrol whatsoever.b. will be able to elect at least one director as long as there are at least three openpositions and the shareholder owns at least 25 percent plus one of the outstandingshares.c. must own at least two-thirds of the shares, plus one, to exercise control over theelections.d. is only permitted to elect one director, regardless of the number of shares owned.e. who owns more shares than anyone else, regardless of the number of shares owned,will control the elections.PROXY VOTINGe 42. The Zilo Corp. has 1,000 shareholders and is preparing to elect three new boardmembers. You do not own enough shares to control the elections but aredetermined to oust the current leadership. The most likely result of this situation isa:a. negotiated settlement where you are granted control over one of the three openpositions.b. legal battle for control of the firm based on your discontent as an individualshareholder.c. arbitrated settlement whereby you are granted control over one of the three openpositions.d. total loss of power for you since you are a minority shareholder.e. proxy fight for control of the firm.SHAREHOLDER RIGHTSe 43. Common stock shareholders are generally granted rights which include the right to:I. share in company profits.II. vote for company directors.III. vote on proposed mergers.IV. residual assets in a liquidation.a. I and II onlyb. II and III onlyc. I and IV onlyd. I, II, and IV onlye. I, II, III, and IVDIVIDENDSe 44. The Scott Co. has a general dividend policy whereby they pay a constant annualdividend of $1 per share of common stock. The firm has 1,000 shares of stockoutstanding. The company:a. must always show a current liability of $1,000 for dividends payable.b. is obligated to continue paying $1 per share per year.c. will be declared in default and can face bankruptcy if they do not pay $1 per year toeach shareholder on a timely basis.d. has a liability which must be paid at a later date should the company miss paying anannual dividend payment.e. must still declare each dividend before it becomes an actual company liability.DIVIDENDSb 45. The dividends paid by a corporation:I. to an individual become taxable income of that individual.II. reduce the taxable income of the corporation.III. are declared by the chief financial officer of the corporation.IV. to another corporation may or may not represent taxable income to the recipient.a. I onlyb. I and IV onlyc. II and III onlyd. I, II, and IV onlye. I, III, and IV onlyPREFERRED STOCKa 46. The owner of preferred stock:a. is entitled to a distribution of income prior to the common shareholders.b. has the right to veto the outcome of an election held by the common shareholders.c. has the right to declare the company bankrupt whenever there are insufficient funds topay dividends to the common shareholders.d. receives tax-free dividends if they are an individual and own more than 20 percent ofthe outstanding preferred shares.e. has the right to collect payment on any unpaid dividends as long as the stock isnoncumulative preferred.PREFERRED STOCKb 47. A 6 percent preferred stock pays _____ a year in dividends per share.a. $3b. $6c. $12d. $30e. $60PREFERRED STOCKe 48. Which one of the following statements concerning preferred stock is correcta. Unpaid preferred dividends are a liability of the firm.b. Preferred dividends must be paid quarterly provided the firm has net income thatexceeds the amount of the quarterly dividend.c. Preferred dividends must be paid timely each quarter or the unpaid dividends startaccruing interest.d. All unpaid dividends on preferred stock, regardless of the type of preferred, must bepaid before any income can be distributed to common shareholders.e. Preferred shareholders may be granted voting rights and seats on the board ifpreferred dividend payments remain unpaid.PREFERRED STOCKe 49. In a liquidation, each share of 5 percent preferred stock is generally entitled to aliquidation payment of _____ as long as there are sufficient funds available.a. $1b. $5c. $10d. $50e. $100QUARTERLY INCOME PREFERRED SECURITIESb 50. Quarterly income preferred securities distribute payments to investors which are:I. taxed like interest income for tax purposes if the income recipient is an individual.II. excluded from the taxable income of any individual recipient.III. distributed from the after-tax income of the corporation.IV. tax deductible to the corporation.a. I and III onlyb. I and IV onlyc. II and III onlyd. II and IV onlye. II onlyPRIMARY MARKETd 51. Which one of the following transactions occurs in the primary marketa. the sale of ABC stock by Fred Jones to Mary Smithb. the tax-free gift of DEF stock to Heather by Jenniferc. the repurchase of GHI stock from Tim by GHId. the initial sale of JKL stock by JKL to Jamiee. the transfer of MNO stock from Tom to his son, JonDEALERS AND BROKERSd 52. Which one of the following statements concerning dealers and brokers is correcta. A dealer in market securities arranges sales between buyers and sellers for a fee.b. A dealer in market securities pays the asked price when purchasing securities.c. A broker in market securities earns income in the form of a bid-ask spread.d. A broker does not take ownership of the securities being traded.e. A broker deals solely in the primary market.NEW YORK STOCK EXHANGEa 53. Technically, the actual owners of the New York Stock Exchange are its:a. members.b. specialists.c. dealers.d. floor brokers.e. commission brokers.FLOOR BROKERSd 54. Which one of the following players on the floor of the New York Stock Exchange canbe likened to part-time help in that they are called to duty only when others are fullyemployeda. floor traderb. specialistc. dealerd. floor brokere. commission brokerSPECIALIST’S POSTb 55. The post is a stationary position on the floor of the New York Stock Exchangewhere a _____ is assigned to work.a. floor traderb. specialistc. dealerd. floor brokere. commission brokerSTOCK MARKET REPORTINGd 56. The closing price of a stock is quoted at 22.87, with a P/E of 26 and a net change of1.42. Based on this information, which one of the following statements is correcta. The closing price on the previous day was $1.42 higher than today’s closing price.b. A dealer will buy the stock at $22.87 and sell it at $26 a share.c. The stoc k increased in value between yesterday’s close and today’s close by$.0142.d. The earnings per share are equal to 1/26th of $22.87.e. The earnings per share have increased by $1.42 this year.STOCK QUOTEb 57. A stock listing contains the following information: P/E 17.5, closing price 33.10,dividend .80, YTD % chg 3.4, and a net chg of -.50. Which of the following statementsare correct given this informationI. The stock price has increased by 3.4 percent during the current year.II. The closing price on the previous trading day was $32.60.III. The earnings per share are approximately $1.89.IV. The current yield is 17.5 percent.a. I and II onlyb. I and III onlyc. II and III onlyd. IIIand IV onlye. I, III, and IV onlyIII. PROBLEMSSTOCK VALUEd 58. Michael’s, Inc. just paid $1.40 to their shareholders as the annual dividend.Simultaneously, the company announced that future dividends will be increasing by4.5 percent. If you require an 8 percent rate of return, how much are you willing topay to purchase one share of Michael’s stocka. $31.11b. $32.51c. $40.00d. $41.80e. $43.68STOCK VALUEe 59. Angelina’s made two announcements concerning their common stock today. First, thecompany announced that their next annual dividend has been set at $2.16 a share.Secondly, the company announced that all future dividends will increase by 4 percentannually. What is the maximum amount you should pay to purchase a share ofAngelina’s stock if your goal is to earn a 10 percent rate of returna. $21.60b. $22.46c. $27.44d. $34.62e. $36.00STOCK VALUEd 60. How much are you willing to pay for one share of stock if the company just paid an$.80 annual dividend, the dividends increase by 4 percent annually and you require an8 percent rate of returna. $19.23b. $20.00c. $20.40d. $20.80e. $21.63STOCK VALUEd 61. Lee Hong Imports paid a $1.00 per share annual dividend last week. Dividends areexpected to increase by 5 percent annually. What is one share of this stock worth toyou today if the appropriate discount rate is 14 percenta. $7.14b. $7.50c. $11.11d. $11.67e. $12.25STOCK VALUEc 62. Majestic Homes stock traditionally provides an 8 percent rate of return. The companyjust paid a $2 a year dividend which is expected to increase by 5 percent per year. Ifyou are planning on buying 1,000 shares of this stock next year, how much should youexpect to pay per share if the market rate of return for this type of security is 9 percentat the time of your purchasea. $48.60b. $52.50c. $55.13d. $57.89e. $70.00STOCK VALUEc 63. Leslie’s Unique Clothing Stores offers a common stock that pays an annual dividendof $2.00 a share. The company has promised to maintain a constant dividend. Howmuch are you willing to pay for one share of this stock if you want to earn 12 percentreturn on your equity investmentsa. $10.00b. $13.33c. $16.67d. $18.88e. $20.00STOCK VALUEb 64. Martin’s Yachts has paid annual dividends of $1.40, $1.75, and $2.00 a share over thepast three years, respectively. The company now predicts that it will maintain aconstant dividend since its business has leveled off and sales are expected to remainrelatively constant. Given the lack of future growth, you will only buy this stock if youcan earn at least a 15 percent rate of return. What is the maximum amount you arewilling to pay to buy one share of this stock todaya. $10.00b. $13.33c. $16.67d. $18.88e. $20.00REQUIRED RETURNc 65. The common stock of Eddie’s Engines, Inc. sells for $25.71 a share. The stock isexpected to pay $1.80 per share next month when the annual dividend is distributed.Eddie’s has established a pattern of increasing their div idends by 4 percent annuallyand expects to continue doing so. What is the market rate of return on this stocka. 7 percentb. 9 percentc. 11 percentd. 13 percente. 15 percentREQUIRED RETURNa 66. The current yield on Alpha’s common stock is 4.8 percent. The company just paid a$2.10 dividend. The rumor is that the dividend will be $2.205 next year. The dividendgrowth rate is expected to remain constant at the current level. What is the requiredrate of return on Alpha’s stocka. 10.04 percentb. 16.07 percentc. 21.88 percentd. 43.75 percente. 45.94 percentREQUIRED RETURNe 67. Martha’s Vineyardrecently paid a $3.60 annual dividend on their common stock. Thisdividend increases at an average rate of 3.5 percent per year. The stock is currentlyselling for $62.10 a share. What is the market rate of returna. 2.5 percentb. 3.5 percentc. 5.5 percentd. 6.0 percente. 9.5 percentREQUIRED RETURNd 68. Bet’R Bilt Bikes just announced that their annual dividend for this coming year will be$2.42 a share and that all future dividends are expected to increase by 2.5 percent annually. What is the market rate of return if this stock is currently selling for $22 asharea. 9.5 percentb. 11.0 percentc. 12.5 percentd. 13.5 percente. 15.0 percentDIVIDEND YIELD VS. CAPITAL GAINS YIELDb 69. Shares of common stock of the Samson Co. offer an expected total return of 12percent. The dividend is increasing at a constant 8 percent per year. The dividendyield must be:a. - 4 percent.b. 4 percent.c. 8 percent.d. 12 percent.e. 20 percent.CAPITAL GAINc 70. The common stock of Grady Co. returned an 11.25 percent rate of return last year.The dividend amount was $.70 a share which equated to a dividend yield of 1.5percent. What was the rate of price appreciation on the stocka. 1.50 percentb. 8.00 percentc. 9.75 percentd. 11.25 percente. 12.75 percentDIVIDEND AMOUNTb 71. Weisbro and Sons common stock sells for $21 a share and pays an annual dividendthat increases by 5 percent annually. The market rate of return on this stock is 9 percent. What is the amount of the last dividend paid by Weisbro and Sonsa. $.77b. $.80c. $.84d. $.87e. $.88DIVIDEND AMOUNTd 72. The common stock of Energizer’s pays an annual dividend that is expected to increaseby 10 percent annually. The stock commands a market rate of return of 12 percent andsells for $60.50 a share. What is the expected amount of the next dividend to be paidon Energizer’s common stocka. $.90b. $1.00c. $1.10d. $1.21e. $1.33d 73. The Reading Co. has adopted a policy of increasing the annual dividend on theircommon stock at a constant rate of 3 percent annually. The last dividend they paidwas $0.90 a share. What will their dividend be in six yearsa. $.90b. $.93c. $1.04d. $1.07e. $1.11e 74. A stock pays a constant annual dividend and sells for $31.11 a share. If the rate ofreturn on this stock is 9 percent, what is the dividend amounta. $1.40b. $1.80c. $2.20d. $2.40e. $2.80CONSTANT DIVIDENDb 75. You have decided that you would like to own some shares of GH Corp. but need anexpected 12 percent rate of return to compensate for the perceived risk of suchownership. What is the maximum you are willing to spend per share to buy GHstock if the company pays a constant $3.50 annual dividend per sharea. $26.04b. $29.17c. $32.67d. $34.29e. $36.59GROWTH DIVIDENDe 76. Turnips and Parsley common stock sells for $39.86 a share at a market rate of return of9.5 percent. The company just paid their annual dividend of $1.20. What is the rate ofgrowth of their dividenda. 5.2 percentb. 5.5 percentc. 5.9 percentd. 6.0 percente. 6.3 percentGROWTH DIVIDENDc 77. B&K Enterprises will pay an annual dividend of $2.08 a share on their common stocknext week. Last year, the company paid a dividend of $2.00 a share. The companyadheres to a constant rate of growth dividend policy. What will one share of B&Kcommon stock be worth ten years from now if the applicable discount rate is 8percenta. $71.16b. $74.01c. $76.97d. $80.05e. $83.25GROWTH DIVIDENDd 78. Wilbert’s Clothing Stores just paid a $1.20 annual dividend. The com pany has a policywhereby the dividend increases by 2.5 percent annually. You would like to purchase100 shares of stock in this firm but realize that you will not have the funds to do so foranother three years. If you desire a 10 percent rate of return, how much should youexpect to pay for 100 shares when you can afford to buy this stock Ignore tradingcosts.a. $1,640b. $1,681c. $1,723d. $1,766e. $1,810GROWTH DIVIDENDb 79. The Merriweather Co. just announced that they are increasing their annual dividend to$1.60 and establishing a policy whereby the dividend will increase by 3.5 percentannually thereafter. How much will one share of this stock be worth five years fromnow if the required rate of return is 12 percenta. $21.60b. $22.36c. $23.14d. $23.95e. $24.79GROWTH DIVIDENDb 80. Shares of the Katydid Co. common stock are currently selling for $27.73. The lastdividend paid was $1.60 per share. The market rate of return is 10 percent. At whatrate is the dividend growinga. 2.50 percentb. 4.00 percentc. 5.98 percentd. 13.05 percente. 14.91 percentSUPERNORMAL GROWTHc 81. The Bell Weather Co. is a new firm in a rapidly growing industry. The company isplanning on increasing its annual dividend by 20 percent a year for the next four yearsand then decreasing the growth rate to 5 percent per year. The company just paid itsannual dividend in the amount of $1.00 per share. What is the current value of oneshare of this stock if the required rate of return is 9.25 percenta. $35.63b. $38.19c. $41.05d. $43.19e. $45.81SUPERNORMAL GROWTHc 82. The Extreme Reaches Corp. last paid a $1.50 per share annual dividend. Thecompany is planning on paying $3.00, $5.00, $7.50, and $10.00 a share over the nextfour years, respectively. After that the dividend will be a constant $2.50 per share peryear. What is the market price of this stock if the market rate of return is 15 percenta. $17.04b. $22.39c. $26.57d. $29.08e. $33.71SUPERNORMAL GROWTHd 83. Can’t Hold Me Back, Inc. is preparing to pay their first dividends. They aregoing to pay $1.00, $2.50, and $5.00 a share over the next three years, respectively.After that, the company has stated that the annual dividend will be $1.25 per shareindefinitely. What is this stock worth to you per share if you demand a 7 percentrate of returna. $7.20b. $14.48c. $18.88d. $21.78e. $25.06NONCONSTANT DIVIDENDSc 84. NU YU announced today that they will begin paying annual dividends. The firstdividend will be paid next year in the amount of $.25 a share. The following dividendswill be $.40, $.60, and $.75 a share annually for the following three years, respectively.After that, dividends are projected to increase by 3.5 percent per year. How much areyou willing to pay to buy one share of this stock if your desired rate of return is 12 percenta. $1.45b. $5.80c. $7.25d. $9.06e. $10.58NONCONSTANT DIVIDENDSb 85. Now or Later, Inc. recently paid $1.10 as an annual dividend. Future dividends areprojected at $1.14, $1.18, $1.22, and $1.25 over the next four years, respectively.Beginning five years from now, the dividend is expected to increase by 2 percentannually. What is one share of this stock worth to you if you require an 8 percent rateof return on similar investmentsa. $15.62b. $19.57c. $21.21d. $23.33e. $25.98NONCONSTANT DIVIDENDSb 86. The Red Bud Co. pays a constant dividend of $1.20 a share. The company announcedtoday that they will continue to do this for another 3 years after which time they willdiscontinue paying dividends permanently. What is one share of this stock worth todayif the required rate of return is 7 percenta. $2.94b. $3.15c. $3.23d. $3.44e. $3.60NONCONSTANT DIVIDENDSb 87. Bill Bailey and Sons pays no dividend at the present time. The company plans to startpaying an annual dividend in the amount of $.30 a share for two years commencingtwo years from today. After that time, the company plans on paying a constant $1 ashare dividend indefinitely. How much are you willing to pay to buy a share of thisstock if your required return is 14 percenta. $4.82b. $5.25c. $5.39d. $5.46e. $5.58NONCONSTANT DIVIDENDSa 88. The Lighthouse Co. is in a downsizing mode. The company paid a $2.50 annualdividend last year. The company has announced plans to lower the dividend by $.50 ayear. Once the dividend amount becomes zero, the company will cease all dividendspermanently. You place a required rate of return of 16 percent on this particular stockgiven the company’s situation. What is one share of this stock worth to you todaya. $3.76b. $4.08c. $4.87d. $5.13e. $5.39NONCONSTANT DIVIDENDS。

公司理财第17章