穷爸爸富爸爸第一本现金流英文版

富爸爸穷爸爸系列 富爸爸巴比伦最富有的人

精彩摘录

第二个片段是关于“克服恐惧”。在投资和创业的过程中,很多人会因为害怕失败而犹豫不决。 然而,清崎在书中强调了克服恐惧的重要性。他认为,成功的人之所以成功,是因为他们敢于冒 险并克服了恐惧。对于普通人来说,克服恐惧是实现财务自由的关键之一。 第三个片段是关于“不断学习和教育”。清崎在书中提到了很多人通过不断学习和教育来提高自 己的投资和创业能力。他认为,成功是一种习惯,而习惯需要不断地培养。通过不断学习和教育, 我们可以更好地掌握投资和创业的技巧和方法,提高自己的财务状况。 这些摘录的内容都是清崎在书中的核心观点和思想。通过深入理解这些观点和思想,我们可以更 好地管理自己的财务状况,实现财务自由。这本书也提醒我们,成功的关键是克服恐惧、不断学 习和教育自己。无论是投资、创业还是其他方面的人生追求,这些思想都值得我们借鉴和学习。

阅读感受

阅读感受

《富爸爸穷爸爸系列:富爸爸巴比伦最富有的人》是一本引人入胜的财商教育读物,作者是知名 财务教育家罗伯特·清崎(Robert Kiyosaki)。本书以古代巴比伦为背景,通过讲述几个年轻 人的奋斗故事,揭示了关于财富、投资和成功的深刻洞见。阅读这本书,我对作者的独特观点和 深入浅出的表达方式产生了强烈的共鸣。

目录分析

通过深入浅出的方式,作者展示了富人和穷人之间的金钱观和理财技巧的差异。同时,书中还强 调了理财智慧和教育的重要性,以及改变思维方式对于实现财务自由的关键作用。这些思想和观 念对于帮助读者提高财务素养,实现个人财富的增长具有积极的指导意义。 通过对《富爸爸穷爸爸系列:富爸爸巴比伦最富有的人》这本书的目录进行深入分析,我们可以 清晰地看出全书的主旨、思想和内容结构。在深入理解全书的基础上,我们可以发现书中的重点 内容对于指导读者如何转变金钱观念、区分资产和负债、建立稳固的财务基础等方面具有极其重 要的价值。书中的主题思想也为读者提供了开启财富自由之门的钥匙。对于广大读者来说,这本 书不仅是一本理财投资的指南,更是一本改变思维方式、实现人生价值的重要读物。

“富爸爸”系列 富爸爸穷爸爸(实践篇)

和富爸爸一起采取行动在《富爸爸财务自由之路》一书中,我们介绍了神奇的现金流象限,把人们按照财务状况分成了4类。

自由职业者或者小企业主。

其典型特征是,雇员追求的是工作的稳定和保障;而自由职业者或者小企业主则最终自己做老板。

他们的事业越成功就越忙碌,也就在自己的工作中越陷越深、不能自拔。

传统的学校教育致力于把学生培养成左侧象限的人。

这类人的生活就像在“老鼠赛跑。

另一类是企业主和投资人。

企业主雇用别人为自己工作,并制定维持企业运转的各种制度。

因此,他们的企业可以独立运作。

而投资人则想方设法让金钱为自己工作。

总的来说,在现金流象限中,处于右侧的这两种人拥有财务自由右侧也通常被人们称为实现财务自由的“快车道。

本书收录了一些成功实践了“富爸爸”理论的人的故事,他们都有一个共同的目标:获得财务自由。

他们都竭尽全力进入右侧象限。

在我们与他们的交谈中,所有人都表示希望从左侧进入右侧。

没有一个人反其道而行之。

(金融市场分析师学会提供完整版阅读)因为他们都意识到,从左侧进入右侧,才是实现财务自由的正确途径。

富爸爸告诉我们,在现金流象限的右侧,你的金钱在为你工作。

许多“富爸爸”理论的成功实践者都告诉我们,他们一边受雇于人或者做小本买卖,一边又是某企业的企业主或者正在投资房地产,这样来努力从左侧进入右侧。

他们的目标是赚到足够的然后才能辞掉目前的工作或者放弃小本生意,成为完完全全的企业主或者投资人。

他们的经历向我们展示了两个象限的人之间的区别:一些人完全靠别人给发工资,另外一些人则把“钱途”完全掌握在自己手里。

他们不但会与大家分享自己面对种种困难时的恐惧,还将分享自己究竟如何克服那些困难。

正如富爸爸所说的,他们找到了最适合自己的成功之路。

为了获得财务自由,这些勇敢的实践者要么购买企业自己经营,要么进行房地产投资,还有人双管齐下。

(金融市场分析师学会提供完整版阅读)那些本来就是企业主的人,则借鉴富爸爸的经验与智慧,把自己的企业经营得更加红火、兴旺。

富爸爸穷爸爸系列 富爸爸如何经营自己的公司

目录分析

目录分析

在财务规划和投资领域中,罗伯特·清崎(Robert Kiyosaki)的《富爸爸穷爸爸系列:富爸爸 如何经营自己的公司》是一本具有深远影响力的著作。本书以富爸爸的视角,为读者展示了如何 有效经营自己的公司,从而实现财务自由。本书将对该书的目录进行深入分析,探讨其中的关键 点和亮点。 从整体上来看,《富爸爸如何经营自己的公司》的目录结构清晰且逻辑性强。全书共分为五个部 分,分别是: 每个部分都包含了若干章节,详细阐述了经营公司的各个阶段所需掌握的关键知识。以下是对于 每个部分的简要分析: 创业前的准备:这部分主要介绍了创业的初衷、目标和市场调研等,帮助读者在开始创业之前做 好充分的心理和物质准备。

阅读感受

阅读感受

《富爸爸穷爸爸系列:富爸爸如何经营自己的公司》是一本引人入胜的财商教育书籍,由知名财 商教育专家罗伯特·清崎(Robert Kiyosaki)精心撰写。在本书中,作者以自己和两位“爸 爸”——富爸爸、穷爸爸的经历为引子,阐述了经营公司的核心理念、策略和方法,旨在帮助读 者提高财商,实现财务自由。本书将分享我的阅读感受,带大家一起领略这本书的魅力。 在阅读这本书的过程中,我对作者罗伯特·清崎的观点和研究深感赞赏。他以简洁明了的行文风 格,将经营公司的核心理念、策略和方法呈现得淋漓尽致,使得读者能够轻松理解并掌握。书中 通过大量的真实案例和亲身经历,展示了成功经营公司的各个方面,使得这本书更具说服力和参 考价值。 学会从现金流的角度看待公司。富爸爸教导我们,现金流是企业的生命线,通过控制成本、提高 利润率,为企业创造稳定的现金流是至关重要的。

《穷爸爸,富爸爸》

eading读 书R《穷爸爸,富爸爸》"Poor Dad, Rich Dad"文/杨 子Reading读 书57房子到底属于资产还是负债,取决于人们如何使用它。

如果是上一辈子的人为这一辈子的人攒钱买房,这一辈子的人又为下一辈子的人攒钱买房,岂不是陷入了“子又生孙,孙又生子,子子孙孙无穷尽也”的恶性循环吗?再加上买房后随之而来的装修、水电、物业等各类费用,人们拼命赚下的钱流入了开发商和资本家的口袋中。

反之,如果情况是将购置的房子用来出租,把产生的收益用在其他途径,这样一来便可以把“现金流”盘活,扩大自身收益,产生更大的价值。

对于一件事物的两种不同观念会导致两种不同的结果,有的人一生都在为了房子奔波,与此同时却有人已经把手中的资源利用起来使其为自己工作了。

富人关心的焦点一直在长久的资产上,而穷人可能仅局限于短期的收入,做一个“长期主义者”有时会更有利于资产的积累。

莎士比亚说,最好的好人,都是犯过错误的过来人;一个人往往因为有一点小小的缺点,将来会变得更好。

同样,犯错误是一件好事,能够承认错误,在每一次的失败中吸取教训、总结经验并在错误中成长,那么即使是错误,也可以是无价之宝。

书中的富爸爸讲到:生活才是最好的老师,大多数时候,生活不会和你说什么,它只是推着你转,每一次推,它都像是在说:“喂,醒一醒,我要让你学点东西。

”生活正是有许多人缺乏犯错的勇气,导致了安分守己地选择了需要通过拼命工作才能维持自身生活、养家糊口的工作。

因为害怕和恐惧,人们只能选择“起床—上班—付账”的生活模式;因为害怕和恐惧人们错过了生活赐予的每一个机会;因为害怕和恐惧人们躲避着本可以克服无知的知识。

其实在生活中,每一次感觉到被生活“推着”向前时,都是一次机遇,一次挑战,抓住机遇,迎接挑战,若不克服软弱的心理,最终便只能自甘堕落地慢慢变老,在贫穷和胆怯中死去。

害怕和自我怀疑往往是毁掉人们才能和本领的因素,陈旧和消极的思想其实才是人们最大的“负债”,也许越早地试错,人们便可以越早地踏入正轨。

富爸爸系列图书简介及经典笔记

富爸爸系列图书《富爸爸,穷爸爸》《富爸爸,穷爸爸》罗伯特·T·清崎(Robert T.Kiyosaki) 莎伦·L·莱希特(Sharon L. Lechter)《富爸爸,穷爸爸》是一个真实的故事,作者罗伯特·T·清崎的亲生父亲和朋友的父亲对金钱的看法截然不同,这使他对认识金钱产生了兴趣,最终他接受了朋友的父亲的建议,也就是书中所说的“富爸爸”的观念,即:不要做金钱的奴隶,要让金钱为我们工作,并由此成为一名极富传奇色彩的成功的投资家。

富爸爸,财务自由之路《富爸爸,财务自由之路》罗伯特·T·清崎(Robert T.Kiyosaki) 莎伦·L·莱希特(Sharon L. Lechter)《富爸爸财务自由之路》是《富爸爸,穷爸爸》的续篇。

本书将所有的人分为四类:1 雇员;2 自由职业者;3 公司所有者;4 投资人。

本书分析了这四类人各自的价值,并为人们指明了通往财务自由的道路。

《富爸爸,投资指南》《富爸爸,投资指南》罗伯特·T·清崎(Robert T.Kiyosaki) 莎伦·L·莱希特(Sharon L. Lechter)《富爸爸投资指南》是《富爸爸,穷爸爸》系列丛书之一,由北京世界图书出版公司和北京读书人文化传播公司策划出版,读者可到各新华书店购买。

《富爸爸,富孩子,聪明孩子》《富爸爸,富孩子,聪明孩子》罗伯特·T·清崎(Robert T.Kiyosaki) 莎伦·L·莱希特(Sharon L. Lechter)为什么要在孩子的时候教给他们有关钱的知识答案非常的简单……因为小孩子对一切都有强烈的好奇心,包括金钱。

教育心理学家认为5-14岁的小孩对自己的人生和未来已经作出了许多重要决定,14岁以后,家长和老师将很难再让他们去接受新的观念。

罗伯特·清崎-富爸爸系列书目

罗伯特·清崎(Robert Toru Kiyosaki)系列01《Rich Dad, Poor Dad》(1997)(繁体中文)《富爸爸·穷爸爸》2001/01/01(简体中文)《富爸爸穷爸爸》2003-01-0102《Rich Dad's CASHFLOW Quadrant》(繁体中文)《富爸爸·有钱有理》2001/04/01(简体中文)《富爸爸财务自由之路神奇的现金流象限》2003-01-0103《Rich Dad's Guide to Investing》(繁体中文)《富爸爸·提早享受财富》1 2001/10/29(繁体中文)《富爸爸·提早享受财富》2 2001/12/01(简体中文)《富爸爸投资指南》2003-04-01 ISBN 7-121-01365-704《Rich Dad's Rich Kid Smart Kid》(繁体中文)《富爸爸·富小孩》上2002/05/29(繁体中文)《富爸爸·富小孩》下2002/07/08(简体中文)《富爸爸富孩子聪明孩子》2003-0505《Rich Dad's Prophecy》(繁体中文)《经济大预言》003/04/01(简体中文)《富爸爸大预言》2003-03-0106《Rich Dad's Retire Young, Retire Rich》(繁体中文)《财富执行力》2003/05/20(简体中文)《富爸爸年轻退休》2003-04-0107《Rich Dad's Success Stories》(繁体中文)未出版(简体中文)《富爸爸成功的故事》2005-01-01(简体中文)《富爸爸·穷爸爸实践篇》2009-01-0108《The Business School》(繁体中文)《富爸爸.商学院》2005/07/06(简体中文)《富爸爸商学院:直销致富的11大理由》2004-0709《Rich Dad's Before You Quit Your Job》(繁体中文)《富爸爸·辞职创业》2006/04/06(简体中文)《富爸爸辞职创业前的10堂课》2006-01-0110《Rich Dad's Increase Your Financial IQ》(繁体中文)《富爸爸财务IQ:愈精明愈有钱》2009/03/25(简体中文)《富爸爸·提高你的财商》2008-10-0111《Rich Dad's Conspiracy of the Rich: The 8 New Rules of Money》(繁体中文)《富爸爸之有钱人的大阴谋:八种全新的金钱法则》2010/09/0812《Unfair Advantage: The Power of Financial Education》(繁体中文)《富爸爸,赚钱时刻:挑战有钱人的不公平竞争优势》2011/12/1413《The Real Book of Real Estate: Real Experts. Real Stories. Real Life》(简体中文)《富爸爸房地产投资指南》2011-03-01其它相关书籍01《You Can Choose to Be Rich》有声:由各国出版商播音朗读(繁体中文)《富爸爸有声书:你可以选择富有》02《Sales Dogs》作者:布莱尔·辛格(Singer Blair)(繁体中文)《富爸爸销售狗》2005/05/12(简体中文)《富爸爸销售狗》2004-07-0103《Why We Want You To Be Rich》作者:罗伯特·清崎与唐纳德·川普(Donald Trump)合著(繁体中文)《川普清崎让你赚大钱》2007/07/05(简体中文)《富爸爸让你赚大钱》2008-01-0104《Rich Woman》作者:罗伯特·清崎的妻子金·清崎(繁体中文)《富爸爸富女人 - 女人就是要有钱》2009/09/30(简体中文)《富爸爸女人一定要有钱》2008-11-01。

罗伯特·清崎

罗伯特·清崎维基百科,自由的百科全书▼罗伯特·T·清崎(Robert Toru Kiyosaki,1947年4月8日-),日语名清崎彻(Kiyosaki Toru)美国夏威夷出身,第4代日裔美国人,富爸爸,穷爸爸系列书籍的主要作者。

以提倡理财智商(财商)的教育著名。

•••••[编辑]简历清崎彻父亲(穷爸爸)是夏威夷州教育部的教师,曾经成为该地教育部长。

他先在纽约攻读大学,毕业后曾加入美国海军陆战队,曾任舰载武装直升机机师,参加过越战。

退伍后曾入读航海学校,之后在富爸爸提议下,加入施乐公司(Xeros),学习销售技巧,然而推销工作成绩强差人意,令他几乎打算放弃,在富爸爸鼓励下,清崎在推销工作以外,亦为慈善机构,以致电陌生人(意外访问)方式募捐。

经过一番努力后,推销技巧突飞猛进,由几乎被革职的危局,变成登上思诺公司最佳营业额第一位。

1977年,清崎在业余时间创办生产“冲浪者”钱包的企业,日渐成长,令清崎毅然放弃在施乐的高薪厚职,全职投身企业,更曾一度借此致富,然而由于拍档在产品成功之后,变得松懈,令清崎决定离开,后又在拍档要求下,为拯救濒危公司而再次加入,最后由于中国、台湾等地不断有仿冒品出售,打击尼可龙生意,公司亦难逃倒闭命运。

虽然如此,清崎彻仍然坚持开设公司,经过九个月无工资收入,居住在汽车屋的艰难日子后,他的创业理想终于成真,包括在中国、委内瑞拉等地,收购或开设石油公司等。

其中房地产收入丰硕,更令他明白到现金流对致富极为关键,亦成为他在“富爸爸”系列中,一再强调的致富方法。

最后他在47岁时,与妻子金一同达成财务自由,两人更到斐济度假庆祝。

退休生活期间,清崎彻决定重操父亲故业——教师,希望透过游戏,将致富心得广为传授,便在深山隐居两年,专心钻研与理财有关的游戏。

1985年,“现金流游戏”(CASHFLOW GAME)终于面世。

为更易向大众介绍该游戏概念,他开始执笔撰写“富爸爸穷爸爸”,结果大受欢迎,连续六年成为纽约时报最畅销书籍。

Rich dad and poor dad富爸爸穷爸爸英语课件

Life of Mr. Robert

• “I have two dads, one is my own dad whom I called my ‘poor dad’, because he had been fighting with all kinds of debts (债务) all his life, even though he was well-educated and used to have a highpaying job. The other dad is actually dad of my best friend---Mike. He is my‘ rich dad’ in my way to becoming financial free. (财务自由)”

批注本地保存成功开通会员云端永久保存去开通

Rich dook about the way to become richI.n fact, it teaches us a

new way to think------that is, the way the rich sees the world and life!

• 4.You must give first and then receive ,that is why charity(慈善) is very important for the rich!

Four

quadrants (象限)

B E

rich dad poor dad 穷爸爸富爸爸

< previous

next >

Asset 资产

Liability 负债

KISS(keep it simple stupid),即傻瓜财务原则

通过这个原则我们可以轻松地判别出资产与负债,并去购买资产。

< previous

next >

Asset 资产

Liability 负债

‘The poor work for money,and the rich make money work for them.’

《Rich Dad,Poor Dad》

< previous

next >

Author

< previous

Robert T.Kiyosaki: Born and raised in Hawaii,Robert is fourth-generation Japanese american.He set up a company and began his own business in 1977,finally became a millionaire in 1985. Kiyosaki is the author of the Rich Dad series of books,an investor,entrepreneur and educator. His perspectives in Rich Dad,Poor Dad have changed the way people think about money and investing.

Kiyosaki followed his poor dad study hard in order to hunt a good job until 1977, the poor dad was laid off and bothered by the money all the time,meanwhile,the other one became the richest man in Hawaii. At last, Kiyosaki determined to follow the rich dad’s step and start his own business.

富爸爸穷爸爸PPT课件

金钱是一种思想, 如果你想要更多的钱,

只需改变你的思想

让金钱为你辛勤工作, 你的生活将会变得更轻松,更幸福

24

2020/1/8

25

对穷人----稳定的工作就是一切 对富人----不断学习才是一切

教育比金钱更有价值 工作是为了学习新东西

17

思考: 大部分人都能做出比麦当劳更好的汉堡包 那为什麽麦当劳比我们更能赚钱?

答案:……

1. 麦当劳拥有一套出色的商务体系, 许多才华横溢的 人之所以贫穷, 是因为他们只是专心于做好汉堡包, 而对 如何运作商务体系却知之甚少(主管与业务员)

基础 6英寸厚的水泥板----盖郊区小屋

----建造帝国大厦?!

9

规则1: 明白资产和负债的区别, 并且尽可能地购买资产.

富人得到资产而穷人和中产阶级得到负债. 资产----就是能把钱放进你口袋里的东西 负债----把钱从你口袋里取走的东西 不断买入资产----变富 不断买入负债----变穷 人们常常把负债当作资产买进----在财务问题中挣扎

害怕付不起帐单、没有足够的钱、挨饿等, 所以期望一份稳定的工作,拼命为钱工作,成 了钱的奴隶。如此度过一生。

4

避开人一生中最大的陷阱:

1. “老鼠赛跑”——恐惧(贪婪) 起床、上班、付帐、再起床、再上班、再付帐。。。 以更高的开支重复这种循环。成为高薪的奴隶。

2. “驴子拉车”——欲望 车夫在驴子鼻子前面放了个胡萝卜,车夫知道该把车

功之母, 避开失败, 也就避开了成功

15

做创造投资机会的投资者

1. 寻找到其他人都忽略的机会 2. 如何增加资金, 你知道的比你买到的更重要

投资不是买入, 而应该说是一个收集信息的过程 3. 怎样把精明的人们组织起来.

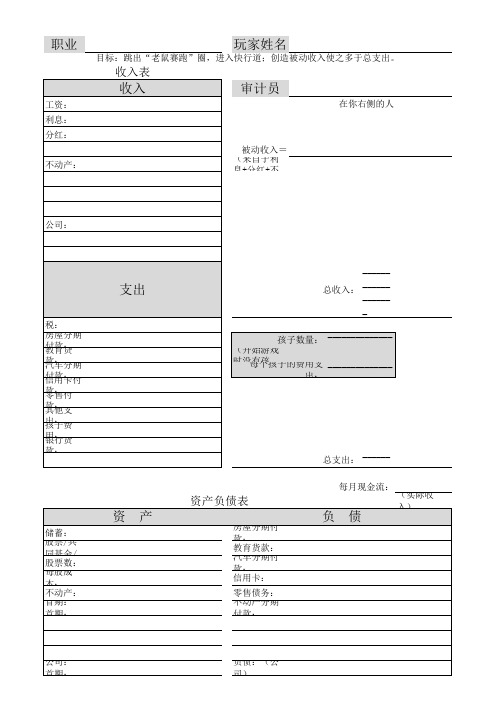

穷爸爸富爸爸-现金流游戏电子记录表(线下聚会版)

1、除银行贷款的其他负债您必须一次 性偿还,银行贷款可分次偿还

2

(利息+股利+房地产+企业现金流)

总收入: ¥ 25,002

小孩个数:

0

(游戏开始时小孩个数为0)

每个小孩支出: ¥

1,600

总支出: ¥ 19,500

每月现金流(即银行结算日发放工资)

5502元

借款人

其他

金额

后续将会增加卡片的扫描档,这样就可以在线下聚 会的时候直接将抽到的卡片投到屏幕上,而不需要 逐个逐个去看,会更加节省时间

穷爸爸富爸爸-现金流游戏电子记录表(线下聚会版)

玩家:

职业:

【目标:努力使您的非工资收入超过总支出,从“老鼠赛跑”进入“快车道”】

收入

支出

资产表

负债表

项目

现金流

项目

1

工资

¥

25,000 1

税金

¥

2

利息

2 住房抵押贷款 ¥

3

股利

3 教育贷款 ¥

4

房地产

现金流

4 购车贷款 ¥

4.1

5 信用卡支出 ¥

4.2

2

股票/基金/存单

股数 每股成本 2

教育贷款

¥ 12,000

2.1

3

购车贷款

20万元

2.2

4

信用卡

¥ 25,000

2.3

5

额外负债

பைடு நூலகம்

21万元

3

房地产

首期支付 总成本 6 房地产抵押贷款

金额

3.1

6.1

3.2

6.2

3.3

6.3

4

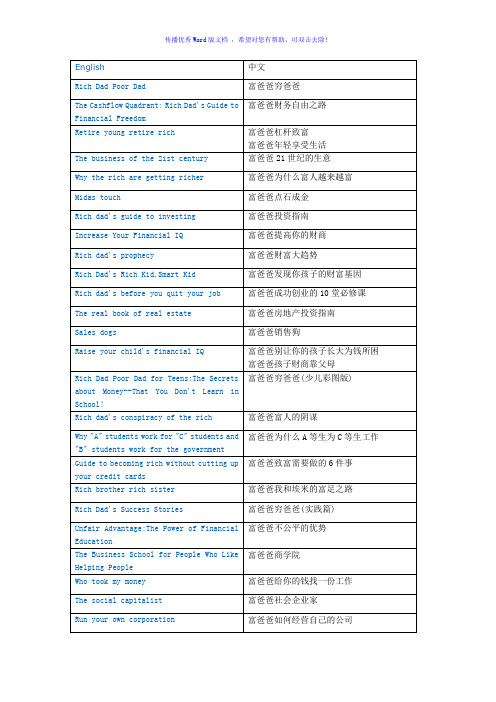

富爸爸穷爸爸系列书籍清单Word版

Who took my money

富爸爸给你的钱找一份工作

The social capitalist

富爸爸社会企业家

Run your own corporation

富爸爸如何经营自己的公司

Rich Woman:A Book on Investing for Women

富爸爸女人一定要有钱

富爸爸财富大趋势

Rich Dad's Rich Kid,Smart Kid

富爸爸发现你孩子的财富基因

Rich dad's before you quit your job

富爸爸成功创业的10堂必修课

The real book of real estate

富爸爸房地产投资指南

Sales dogs

富爸爸销售狗

Rich dad's conspiracy of the rich

富爸爸富人的阴谋

Why "A" students work for "C" students and "B" students work for the government

富爸爸为什么A等生为C等生工作

Guide to becoming rich without cutting up your credit cards

富爸爸21世纪的生意

Why the rich are getting richer

富爸爸为什么富人越来越富

Midas touch

富爸爸点石成金

Rich dad's guide to investing

富爸爸投资指南

Increase Your Financial IQ

穷爸爸富爸爸财务收入表

工资: 利息: 分红: 不动产:

玩家姓名

目标:跳出“老鼠赛跑”圈,进入快行道;创造被动收入使之多于总支出。

收入表

收入

审计员

在你右侧的人

被动收入= (来自于利

息+分红+不

公司:

税: 房屋分期 付教款育:贷 款汽:车分期 付信款用:卡付 款零:售付 款其:他支 出孩:子费 用银:行货 款:

支出

储蓄: 股票/共

同基金/ 股票数: 每股成

本: 不动产: 首期:

首期:

资产

______ 总收入: ______

______ _

孩子数量: ______________

(开始游戏

_

时没每有个孩孩子的费用支 ______________

出:

_

资产负债表

房屋分期付 款: 教育货款: 汽车分期付 款: 信用卡:

零售债务: 不动产分__

每月现金流: (实际收 入)

负债

公司: 首期:

负债:(公 司)

银行货款:

富爸爸,穷爸爸英文版

2012/10/2 P11

Without thinking, I responded, "Because if you don't get good grades, you won't get into college." "Regardless of whether I go to college," he replied, "I'm going to be rich."

2012/10/2 P19

He was right. He needed new answers, and so did I. My parents' advice may have worked for people born before 1945, but it may be disastrous for those of us born into a rapidly changing world. No longer can I simply say to my children, "Go to school, get good grades, and look for a safe, secure job."

2012/10/2 P17

“Mom,” he continued, “I don„t want to work as hard as you and dad do. You make a lot of money, and we live in a huge house with lots of toys. If I follow your advice, I‟ll wind up(上紧发条) like you, working harder and harder only to pay more taxes and wind up(结束) in debt.

富爸爸穷爸爸英文版第一章

Because I had two influential fathers, I learned from both of them. I had to think about each dad's advice, and in doing so, I gained valuable insight into the power and effect of one's thoughts on one's life. For example, one dad had a habit of saying, "I can't afford it." The other dad forbade those words to be used. He insisted I say, "How can I afford it?" One is a statement, and the other is a question. One lets you off the hook, and the other forces you to think. My soon-to-be-rich dad would explain that by automatically saying the words "I can't afford it," your brain stops working. By asking the question "How can I afford it?" your brain is put to work. He did not mean buy everything you wanted. He was fanatical about exercising your mind, the most powerful computer in the world. "My brain gets stronger every day because I exercise it. The stronger it gets, the more money I can make." He believed that automatically saying "I can't afford it" was a sign of mental laziness.

穷爸爸富爸爸中英文对照版

穷爸爸富爸爸中英文对照版穷爸爸富爸爸中英文对照版:

Poor Dad, Rich Dad

穷爸爸(Poor Dad) --父亲的收入主要来自于工资收入,对于钱财和财务知识缺乏了解。

富爸爸(Rich Dad) --父亲不仅仅依靠工资收入,还通过投资等方式增加财富,并拥有财务智慧。

以下是两种观念和理念的对比:

1.观念

穷爸爸:做好本职工作,努力工作可以带来稳定收入。

富爸爸:让钱为你工作,通过投资等方式增加财富。

2.教育

穷爸爸:专注于学术知识和获得学位,认为学校教育是获取成功的必要途径。

富爸爸:注重财务教育,认为学习如何赚钱、理解投资和财务管

理等知识才能获得成功。

3.风险和机会

穷爸爸:避免风险,寻求稳定、安全的工作。

富爸爸:将风险视为机会,敢于冒险,相信投资和创业能够带来

财务自由。

4.负债和资产

穷爸爸:将房贷、车贷等债务视为负担。

富爸爸:通过投资房地产、股票等资产,使得资产带来更多收入。

5.工作和激励

穷爸爸:工作是为了工资,工资唯一的激励。

富爸爸:追求热爱并擅长的工作,享受工作所带来的成就感,并

通过投资等方式增加收入。

6.财务知识

穷爸爸:缺乏财务知识,往往容易成为被金钱支配的人。

富爸爸:注重财务知识的学习和理解,能够掌控金钱,并使金钱

为自己服务。

这些是两个父亲家庭背景和财务观念的对比,希望对你有所帮助。

富爸爸穷爸爸

VS

《富爸爸穷爸爸》是罗伯特·清崎于1999年4月出版的个人理财和投资指南。

书籍以作者与两位导师——富爸爸和穷爸爸——之间的对话形式展开,通过讲述两位导师不同的金钱观和投资观,向读者传达如何正确理解和实践财务自由的理念。

书籍概述

出版及影响力

该书籍启发了数百万人的理财观念,帮助他们开始追求财务自由的道路。

每个人都应该重视财务教育

财商是一个人对财务、投资、债务和资产的理解和掌握能力。通过接受财商教育,人们可以更好地评估投资机会、管理债务和增加资产。

培养财商

财务教育的重要性

资产是增加现金流的投资

资产包括股票、债券、房地产和自己的公司等,可以产生正的现金流,即带来收入。

负债是减少现金流的投资

负债包括汽车、房屋贷款、信用卡债务和其他贷款等,会导致现金流减少。

清崎的“富爸爸”系列书籍在全球范围内成为个人理财和投资的经典之作,对读者产生了深远的影响。

《富爸爸穷爸爸》自出版以来在全球范围内广受欢迎,成为畅销书,并被翻译成多种语言。

02

主要观点

无论一个人的目前财务状况如何,持续学习和教育都是至关重要的。通过了解财务,人们可以更好地为自己和家人的未来做出更明智的决策。

拓宽职业视野

《富爸爸穷爸爸》鼓励人们积极探索不同的职业机会,从而为自己的职业发展创造更多机会。

提升职业发展机会

04

对社会的影响

财务知识是个人和家庭生活的重要组成部分,缺乏财务知识会导致不健康的财务状况和不必要的压力。通过《富爸爸穷爸爸》的普及,越来越多的人开始意识到财务知识的重要性,并开始主动学习和应用这些知识。

对个人启示与收获

转变思维方式

02

本书帮助个人认识到穷人思维和富人思维之间的差异,并鼓励个人积极转变思维方式,以更有利于财务上的成功。

穷爸爸富爸爸之现金流

穷爸爸富爸爸之现金流首先我们来了解一下现金是怎样流动的?穷人有了闲钱后就把钱存入银行,银行是很赚钱的,因为银行把钱又贷了出去,贷给谁呢?会贷给穷人吗?当然不会。

银行把钱贷给有能力赚钱的富人。

富人拿到钱后会把钱存回银行吗?当然不会。

存钱是存不出富人的,只有投资才会赚到钱。

富人用这些钱投资建商店、超市等,建成后谁来消费呢?还是穷人。

因此,穷人的钱一方面通过银行给了富人,一方面通过消费给了富人。

现在你应该明白为什么穷人总是过的很辛苦,而且越老越辛苦,越没有保障了。

所以,我们宁愿辛苦一阵子,通过改变工作方式让自己成为一名富人,让现金源源不断的流向我们,我们再也不要辛苦一辈子做个穷人!那怎么做呢?工作有两种方式,一种是提桶,一种是建管道。

提桶永远是在用时间换金钱,有工作就有钱,没工作就没钱。

但终究有一天我们会老,会生病,会干不动,那我们就没有收入,所以聪明的人都会在提桶的同时给自己建一条管道,即使开始会多付出一点,一旦管道建成了,只要稍加维护,我们就会有源源不断的收入。

就好象赚钱有两种的方式一样:第一种是每天赚1000元,持续30天(1000元/天×30第二种是第一天赚1分,第二天赚2分,第三天赚4分,第四天赚8分,第每天以2的倍数递增,你知道么当到30天的时候,你就会有536万的收入(0.01元/天×2×2×2×2…..共计30次=5368079.12元)你愿意选择哪一种?当然要536万的赚钱方式了。

刚刚我们有谈过现金流的概念,我们不能改变现金的流向,只要改变我们的角色就可以了,那就是成为一个投资者,投资分两种:一种是大投资,一种是小投资,相信很多人都愿意以小搏大,现在有一种方式,我们根本不需要做额外的投资,只需改变消费的观念——让消费变成投资,也就是花钱同时赚钱!这是什么意思呢?世界上有三种人,一种是生产者,他们是赚钱的,他们生产很多产品来赚消费者的钱;另一种是消费者,他们是花钱的,他们花钱来购买生产者的产品,即使选择更低折扣的产品,其实还是在减少财富;最后一种是生产消费者,他们是花钱同时又赚钱。

《富爸爸穷爸爸》简介

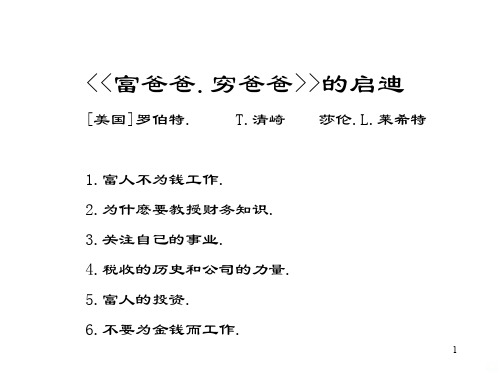

由于我开始金钱这门课的学习时只有9岁,因此富 爸爸只教我一些简单的东西。 当他把所有想教给 我的东西说完做完时, 总共也只有6门主要的课程, 但这些课程 在我的脑海中重复了30多年。 本书下 面的内容就是关于这6门课的介绍,其形式简 单得 就如同当年富爸爸教我时那样。这些课程不是最终 答案而是一个向导,一个在 这个不确定和飞速变 化的世界中帮助你和你的孩子积累财富的向导。 第一课富人不为钱工作第二课为什么要教授财务知 识第三课关注自己的事业第 四课税收的历史和公 司的力量第五课富人的投资第六课不要为金钱而工 作

1985年,他离开商界,与别人共同创建了一家国际教育公 司。这家公司在七个国家设有办事处,向成千上万的学生教授 商业和投资课程。他主持的长达一年的节目通过怀旧有线网在 全美播放,以传播他的教育理论。

罗伯特在47岁时退休,做起他最喜欢的事情——投资。 深感“有产者”与“无产者”之间不断扩大的鸿沟,罗 伯特发明了一种教育玩具——“现金流”纸板游戏,并 用它教会人们去玩那些在以前只有富人们懂得的金钱游 戏。 他曾和沃格·曼了诺、Zig Zglar和安东尼·罗宾 斯等人一道同台演讲。罗伯特·T·清崎要传递的信息 是清楚的。“为你的财务负起责任或一生只听从别人的 命令,你要么是金钱的主人,要么是金钱的奴隶。”罗 伯特举办过长到一周短到一小时的辅导班,教给人们有 关富裕的秘密,他发出了一个强烈的信息,这个信息就 是:你的天赋正等待被开发出来,请唤醒你的理财天赋。

富爸爸则说: “金钱就是力量”。 尽管思想的力量从 不能被测量或评估,但当我还是一个小男孩时,我已经 开始 明确地关注我的思想以及我的自我表述了。我注意 到穷爸爸之所以穷不在于他挣到 的钱的多少(尽管这也 很重要),而在于他的想法和行动。我必须极其小心地 选择 他们两位向我传递的思想并为我所用。唉,我有两 个爸爸,我究竟应该听谁的话: 穷爸爸还是富爸爸? 两个爸爸都很重视教育和学习,但两人对于什么才是重 要的。应该学习些什么 的看法却不一致。一个爸爸希望 我努力学习,获得好成绩,找个挣钱多的好工作, 他希 望我能够成为一名教授。律师或会计师,或者去读MBA. 另一个爸爸则鼓励我学 习挣钱,去了解钱的运动规律并 让这种运动规律为我所用。“我不为钱工作”,这 是他 说了一遍又一遍的话,“钱要为我工作。”

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

INTRODUCTIONThere is a NeedDoes school prepare children for the real world? "Study hard and get good grades and you will find a high-paying job with great benefits," my parents used to say. Their goal in life was to provide a college education for my older sister and me, so that we would have the greatest chance for success in life. When I finally earned my diploma in 1976-graduating with honors, and near the top of my class, in accounting from Florida State University-my parents had realized their goal. It was the crowning achievement of their lives. In accordance with the "Master Plan," I was hired by a "Big 8" accounting firm, and I looked forward to a long career and retirement at an early age.My husband, Michael, followed a similar path. We both came from hard-working families, of modest means but with strong work ethics. Michael also graduated with honors, but he did it twice: first as an engineer and then from law school. He was quickly recruited by a prestigious Washington, D.C., law firm that specialized in patent law, and his future seemed bright, career path well-defined and early retirement guaranteed.Although we have been successful in our careers, they have not turned out quite as we expected. We both have changed positions several times-for all the right reasons-but there are no pension plans vesting on our behalf. Our retirement funds are growing only through our individual contributions.Michael and I have a wonderful marriage with three great children. As I write this, two are in college and one is just beginning high school. We have spent a fortune making sure our children have received the best education available.One day in 1996, one of my children came home disillusioned with school. He was bored and tired of studying. "Why should I put time into studying subjects I will never use in real life?" he protested.Without thinking, I responded, "Because if you don't get good grades, you won't get into college.""Regardless of whether I go to college," he replied, "I'm going to be rich.""If you don't graduate from college, you won't get a good job," I responded with a tinge of panic and motherly concern. "And if you don't have a good job, how do you plan to get rich?"My son smirked and slowly shook his head with mild boredom. We have had this talk many times before. He lowered his head and rolled his eyes. My words of motherly wisdom were falling on deaf ears once again.Though smart and strong-willed, he has always been a polite and respectful young man."Mom," he began. It was my turn to be lectured. "Get with the times! Look around; the richest people didn't get rich because of their educations. Look at Michael Jordan and Madonna. Even Bill Gates, who dropped out of Harvard, founded Microsoft; he is now the richest man in America, and he's still in his 30s. There is a baseball pitcher who makes more than $4 million a year even though he has been labeled `mentally challenged.' "There was a long silence between us. It was dawning on me that I was giving my son the same advice my parents had given me. The world around us has changed, but the advice hasn't.Getting a good education and making good grades no longer ensures success, and nobody seems to have noticed, except our children."Mom," he continued, "I don't want to work as hard as you and dad do. You make a lot of money, and we live in a huge house with lots of toys. If I follow your advice, I'll wind up like you,working harder and harder only to pay more taxes and wind up in debt. There is no job security anymore; I know all about downsizing and rightsizing. I also know that college graduates today earn less than you did when you graduated. Look at doctors. They don't make nearly as much money as they used to. I know I can't rely on Social Security or company pensions for retirement.I need new answers."He was right. He needed new answers, and so did I. My parents' advice may have worked for people born before 1945, but it may be disastrous for those of us born into a rapidly changing world. No longer can I simply say to my children, "Go to school, get good grades, and look for a safe, secure job."I knew I had to look for new ways to guide my children's education.As a mother as well as an accountant, I have been concerned by the lack of financial education our children receive in school. Many of today's youth have credit cards before they leave high school, yet they have never had a course in money or how to invest it, let alone understand how compound interest works on credit cards. Simply put, without financial literacy and the knowledge of how money works, they are not prepared to face the world that awaits them, a world in which spending is emphasized over savings.When my oldest son became hopelessly in debt with his credit cards as a freshman in college, I not only helped him destroy the credit cards, but I also went in search of a program that would help me educate my children on financial matters.One day last year, my husband called me from his office. "I have someone I think you should meet," he said. "His name is Robert Kiyosaki. He's a businessman and investor, and he is here applying for a patent on an educational product. I think it's what you have been looking for."Just What I Was Looking ForMy husband, Mike, was so impressed with CASHFLOW, the new educational product that Robert Kiyosaki was developing, that he arranged for both of us to participate in a test of the prototype. Because it was an educational game, I also asked my 19-year-old daughter, who was a freshman at a local university, if she would like to take part, and she agreed.About fifteen people, broken into three groups, participated in the test.Mike was right. It was the educational product I had been looking for. But it had a twist: It looked like a colorful Monopoly board with a giant well-dressed rat in the middle. Unlike Monopoly, however, there were two tracks: one inside and one outside. The object of the game was to get out of the inside track-what Robert called the "Rat Race" and reach the outer track, or the "Fast Track." As Robert put it, the Fast Track simulates how rich people play in real life.Robert then defined the "Rat Race" for us."If you look at the life of the average-educated, hard-working person, there is a similar path. The child is born and goes to school. The proud parents are excited because the child excels, gets fair to good grades, and is accepted into a college. The child graduates, maybe goes on to graduateschool and then does exactly as programmed: looks for a safe, secure job or career. The child finds that job, maybe as a doctor or a lawyer, or joins the Army or works for the government. Generally, the child begins to make money, credit cards start to arrive in mass, and the shopping begins, if it already hasn't."Having money to burn, the child goes to places where other young people just like them hang out, and they meet people, they date, and sometimes they get married. Life is wonderful now, because today, both men and women work. Two incomes are bliss. They feel successful, their future is bright, and they decide to buy a house, a car, a television, take vacations and have children. The happy bundle arrives. The demand for cash is enormous. The happy couple decides that their careers are vitally important and begin to work harder, seeking promotions and raises. The raises come, and so does another child and the need for a bigger house. They work harder, become better employees, even more dedicated. They go back to school to get more specialized skills so they can earn more money. Maybe they take a second job. Their incomes go up, but so does the tax bracket they're in and the real estate taxes on their new large home, and their Social Security taxes, and all the other taxes. They get their large paycheck and wonder where all the money went. They buy some mutual funds and buy groceries with their credit card. The children reach 5 or 6 years of age, and the need to save for college increases as well as the need to save for their retirement. ."That happy couple, born 35 years ago, is now trapped in the Rat Race for the rest of their working days. They work for the owners of their company, for the government paying taxes, and for the bank paying off a mortgage and credit cards."Then, they advise their own children to `study hard, get good grades, and find a safe job or career.' They learn nothing about money, except from those who profit from their na飗et? and work hard all their lives. The process repeats into another hard-working generation. This is the `Rat Race'."The only way to get out of the "Rat Race" is to prove your proficiency at both accounting and investing, arguably two of the most difficult subjects to master. As a trained CPA who once worked for a Big 8 accounting firm, I was surprised that Robert had made the learning of these two subjects both fun and exciting. The process was so well disguised that while we were diligently working to get out of the "Rat Race," we quickly forgot we were learning.Soon a product test turned into a fun afternoon with my daughter, talking about things we had never discussed before. As an accountant, playing a game that required an Income Statement and Balance Sheet was easy. So I had the time to help my daughter and the other players at my table with concepts they did not understand. I was the first person-and the only person in the entire test group-to get out of the "Rat Race" that day. I was out within 50 minutes, although the game went on for nearly three hours.At my table was a banker, a business owner and a computer programmer. What greatly disturbed me was how little these people knew about either accounting or investing, subjects so important in their lives. I wondered how they managed their own financial affairs in real life. I could understand why my 19-year-old daughter would not understand, but these were grownadults, at least twice her age.After I was out of the "Rat Race," for the next two hours I watched my daughter and these educated, affluent adults roll the dice and move their markers. Although I was glad they were all learning so much, I was disturbed by how much the adults did not know about the basics of simple accounting and investing. They had difficulty grasping the relationship between their Income Statement and their Balance Sheet. As they bought and sold assets, they had trouble remembering that each transaction could impact their monthly cash flow. I thought, how many millions of people are out there in the real world struggling financially, only because they have never been taught these subjects?Thank goodness they're having fun and are distracted by the desire to win the game, I said to myself. After Robert ended the contest, he allowed us fifteen minutes to discuss and critique CASHFLOW among ourselves.The business owner at my table was not happy. He did not like the game. "I don't need to know this," he said out loud. "I hire accountants, bankers and attorneys to tell me about this stuff."To which Robert replied, "Have you ever noticed that there are a lot of accountants who aren't rich? And bankers, and attorneys, and stockbrokers and real estate brokers. They know a lot, and for the most part are smart people, but most of them are not rich. Since our schools do not teach people what the rich know, we take advice from these people. But one day, you're driving down the highway, stuck in traffic, struggling to get to work, and you look over to your right and you see your accountant stuck in the same traffic jam. You look to your left and you see your banker. That should tell you something."The computer programmer was also unimpressed by the game: "I can buy software to teach me this."The banker, however, was moved. "I studied this in school-the accounting part, that is-but I never knew how to apply it to real life. Now I know. I need to get myself out of the `Rat Race.' "But it was my daughter's comments that most touched me. "I had fun learning," she said. "I learned a lot about how money really works and how to invest."Then she added: "Now I know I can choose a profession for the work I want to perform and not because of job security, benefits or howmuch I get paid. If I learn what this game teaches, I'm free to do and study what my heart wants to study. . .rather than study something because businesses are looking for certain job skills. If I learn this, I won't have to worry about job security and Social Security the way most of my classmates already do."I was not able to stay and talk with Robert after we had played the game, but we agreed to meet later to further discuss his project. I knew he wanted to use the game to help others become more financially savvy, and I was eager to hear more about his plans.My husband and I set up a dinner meeting with Robert and his wife within the next week. Although it was our first social get-together, we felt as if we had known each other for years.We found out we had a lot in common. We covered the gamut, from sports and plays to restaurants and socio-economic issues. We talked about the changing world. We spent a lot of time discussing how most Americans have little or nothing saved for retirement, as well as the almost bankrupt state of Social Security and Medicare. Would my children be required to pay for the retirement of 75 million baby boomers? We wondered if people realize how risky it is to depend on apension plan.Robert's primary concern was the growing gap between the haves and have nots, in America and around the world. A self-taught, self-made entrepreneur who traveled the world putting investments together, Robert was able to retire at the age of 47. He came out of retirement because he shares the same concern I have for my own children. He knows that the world has changed, but education has not changed with it. According to Robert, children spend years in an antiquated educational system, studying subjects they will never use, preparing for a world that no longer exists."Today, the most dangerous advice you can give a child is `Go to school, get good grades and look for a safe secure job,' " he likes to say. "That is old advice, and it's bad advice. If you could see what is happening in Asia, Europe, South America, you would be as concerned as I am."It's bad advice, he believes, "because if you want your child to have a financially secure future, they can't play by the old set of rules. It's just too risky."I asked him what he meant by "old rules?" ."People like me play by a different set of rules from what you play by," he said. "What happens when a corporation announces a downsizing?""People get laid off," I said. "Families are hurt. Unemployment goesup.""Yes, but what happens to the company, in particular a public company on the stock exchange?""The price of the stock usually goes up when the downsizing is announced," I said. "The market likes it when a company reduces its labor costs, either through automation or just consolidating the labor force in general.""That's right," he said. "And when stock prices go up, people like me, the shareholders, get richer. That is what I mean by a different set of rules. Employees lose; owners and investors win."Robert was describing not only the difference between an employee and employer, but also the difference between controlling your own destiny and giving up that control to someone else."But it's hard for most people to understand why that happens," I said. "They just think it's not fair.""That's why it is foolish to simply say to a child, `Get a good education,' " he said. "It is foolish to assume that the education the school system provides will prepare your children for the world they will face upon graduation. Each child needs more education. Different education. And they need to know the rules. The different sets of rules.""There are rules of money that the rich play by, and there are the rules that the other 95 percent of the population plays by," he said. "And the 95 percent learns those rules at home and in school. That is why it's risky today to simply say to a child, `Study hard and look for a job.' A child today needs a more sophisticated education, and the current system is not delivering the goods. I don't care how many computers they put in the classroom or how much money schools spend. How can the education system teach a subject that it does not know?"So how does a parent teach their children, what the school does not? How do you teach accounting to a child? Won't they get bored? And how do you teach investing when as a parent you yourself are risk averse? Instead of teaching my children to simply play it safe, I decided it was best to teach them to play it smart."So how would you teach a child about money and all the things we've talked about?" I asked Robert. "How can we make it easy for parents especially when they don't understand itthemselves?""I wrote a book on the subject, " he said."Where is it?""In my computer. It's been there for years in random pieces. I add to it occasionally but I've never gotten around to put it all together. I began writing it after my other book became a best seller, but I never finished the new one. It's in pieces."And in pieces it was. After reading the scattered sections, I decided the book had merit and needed to be shared, especially in these changing times. We agreed to co-author Robert's book.I asked him how much financial information he thought a child needed. He said it would depend on the child. He knew at a young age that he wanted to be rich and was fortunate enough to have a father figure who was rich and willing to guide him. Education is the foundation of success, Robert said. Just as scholastic skills are vitally important, so are financial skills and communication skills.What follows is the story of Robert's two dads, a rich one and a poorone, that expounds on the skills he's developed over a lifetime. The contrast between two dads provides an important perspective. The book is supported, edited and assembled by me. For any accountants who read this book, suspend your academic book knowledge and open your mind to the theories Robert presents. Although many of them challenge the very fundamentals of generally accepted accounting principles, they provide a valuable insight into the way true investors analyze their investment decisions.When we as parents advise our children to "go to school, study hard and get a good job," we often do that out of cultural habit. It has always been the right thing to do. When I met Robert, his ideas initially startled me. Having been raised by two fathers, he had been taught to strive for two different goals. His educated dad advised him to work for a corporation. His rich dad advised him to own the corporation. Both life paths required education, but the subjects of study were completely different. His educated dad encouraged Robert to be a smart person. His rich dad encouraged Robert to know how to hire smart people.Having two dads caused many problems. Robert's real dad was the superintendent of education for the state of Hawaii. By the time Robert was 16, the threat of "If you don't get good grades, you won't get a good job" had little effect. He already knew his career path was to own corporations, not to work for them. In fact, if it had not been for a wise and persistent high school guidance counselor, Robert might not have gone on to college. He admits that. He was eager to start building his assets, but finally agreed that the college education would also be a benefit to him.Truthfully, the ideas in this book are probably too far fetched and radical for most parents today. Some parents are having a hard enough time simply keeping their children in school. But in light of our changing times, as parents we need to be open to new and bold ideas. To encourage children to be employees is to advise your children to pay more than their fair share of taxes over a lifetime, with little or no promise of a pension. And it is true that taxes are a person's greatest expense. In fact, most families work from January to mid-May for the government just to cover their taxes. New ideas are needed and this book provides them.Robert claims that the rich teach their children differently. They teach their children at home, around the dinner table. These ideas may notbe the ideas you choose to discuss with your children, but thank you for looking at them. And I advise you to keep searching. In my opinion, as a momand a CPA, the concept of simply getting good grades and finding a good job is an old idea. We need to advise our children with a greater degree of sophistication. We need new ideas and different education. Maybe telling our children to strive to be good employees while also striving to own their own investment corporation is not such a bad idea.It is my hope as a mother that this book helps other parents. It is Robert's hope to inform people that anyone can achieve prosperity if they so choose. If today you are a gardener or a janitor or even unemployed, you have the ability to educate yourself and teach those you love to take care of themselves financially. Remember that financial intelligence is the mental process via which we solve our financial problems.Today we are facing global and technological changes as great or even greater than those ever faced before. No one has a crystal ball, but one thing is for certain: Changes lie ahead that are beyond our reality. Who knows what the future brings? But whatever happens, we have two fundamental choices: play it safe or play it smart by preparing, getting educated and awakening your own and your children's financial genius. - Sbaron LecbterFor a FREE AUDIO REPORT "What My Rich Dad Taught Me About Money" all you have to do is visit our special website at and the report is yours free.Thank youRich Dad, Poor DadCHAPTER ONERich Dad, Poor DadAs narrated by Robert KiyosakiI had two fathers, a rich one and a poor one. One was highly educated and intelligent; he hada Ph.D. and completed four years of undergraduate work in less than two years. He then went on to Stanford University, the University of Chicago, and Northwestern University to do his advanced studies, all on full financial scholarships. The other father never finished the eighth grade.Both men were successful in their careers, working hard all their lives. Both earned substantial incomes. Yet one struggled financially all his life. The other would become one of the richest men in Hawaii. One died leaving tens of millions of dollars to his family, charities and his church. The other left bills to be paid.Both men were strong, charismatic and influential. Both men offered me advice, but they did not advise the same things. Both men believed strongly in education but did not recommend the same course of study.If I had had only one dad, I would have had to accept or reject his advice. Having two dads advising me offered me the choice of contrasting points of view; one of a rich man and one of a poor man.Instead of simply accepting or rejecting one or the other, I found myself thinking more, comparing and then choosing for myself.The problem was, the rich man was not rich yet and the poor man not yet poor. Both were just starting out on their careers, and both were struggling with money and families. But they had very different points of view about the subject of money.For example, one dad would say, "The love of money is the root of all evil." The other, "The lack of money is the root of all evil."As a young boy, having two strong fathers both influencing me was difficult. I wanted to be a good son and listen, but the two fathers did not say the same things. The contrast in their points of view, particularly where money was concerned, was so extreme that I grew curious and intrigued.I began to start thinking for long periods of time about what each was saying.Much of my private time was spent reflecting, asking myself questions such as, "Why does he say that?" and then asking the same question of the other dad's statement. It would have been much easier to simply say, "Yeah, he's right. I agree with that." Or to simply reject the point of view by saying, "The old man doesn't know what he's talking about." Instead, having two dads whom I loved forced me to think and ultimately choose a way of thinking for myself. As a process, choosing for myself turned out to be much more valuable in the long run, rather than simply accepting or rejecting a single point of view.One of the reasons the rich get richer, the poor get poorer, and the middle class struggles in debt is because the subject of money is taught at home, not in school. Most of us learn about money from our parents. So what can a poor parent tell their child about money? They simply say "Stay in school and study hard." The child may graduate with excellent grades but with a poor person's financial programming and mind-set. It was learned while the child was young.Money is not taught in schools. Schools focus on scholastic and professional skills, but not on financial skills. This explains how smart bankers, doctors and accountants who earned excellent grades in school may still struggle financially all of their lives. Our staggering national debt is due in large part to highly educated politicians and government officials making financial decisions with little or no training on the subject of money.I often look ahead to the new millennium and wonder what will happen when we have millions of people who will need financial and medical assistance. They will be dependent on their families or the government for financial support. What will happen when Medicare and Social Security run out of money? How will a nation survive if teaching children about money continues to be left to parents-most of whom will be, or already are, poor?Because I had two influential fathers, I learned from both of them. I had to think about each dad's advice, and in doing so, I gained valuableinsight into the power and effect of one's thoughts on one's life. For example, one dad had a habit of saying, "I can't afford it." The other dad forbade those words to be used. He insisted I say, "How can I afford it?" One is a statement, and the other is a question. One lets you off the hook, and the other forces you to think. My soon-to-be-rich dad would explain that by automatically saying the words "I can't afford it," your brain stops working. By asking the question "How can I afford it?" your brain is put to work. He did not mean buy everything you wanted. He was fanatical about exercising your mind, the most powerful computer in the world. "My brain gets stronger every day because I exercise it. The stronger it gets, the more money I can make." He believed that automatically saying "I can't afford it" was a sign of mental laziness.Although both dads worked hard, I noticed that one dad had a habit of putting his brain to sleep when it came to money matters, and the other had a habit of exercising his brain. The long-term result was that one dad grew stronger financially and the other grew weaker. It is not much different from a person who goes to the gym to exercise on a regular basis versus someone who sits on the couch watching television. Proper physical exercise increases your chances for。