HND会计考试outcome3

HND_商法outcome3

1.Actually Sole trade illustrates a person business in which the take full responsibilities in bothmanaging and having the possession of the business.AdvantagesBecause there are no legal formalities, naturally the business is easy to set upUsually, the sole trader could take all key decisions without concerning other unnecessary effectsIt is the simplest form of business organization recognized by Scots Law. The only one who takes responsibility for the owner is himself.It is convenient for owner to keep personal touches with customers.The owner could keep all the profits because he owns the company.Disadvantages:Unlimited liability: The owner has unlimited liability for all debts or obligations owed by the business if the business fails.His business is firmly associated with his personal possession which means he maintains a lot of pressures in raising finance.Intense competition will lead the company lacking of continuity and worry about the pressure from larger units.As the owner of the business.All major business decisions can be taken by XX has rights to lay down contracts and decisions about the management of the business.If the business is a success, X will share all profits. If not, he will be responsible for every penny owed. (可写可不写,X代表公司名字)Partnership is a business operated by 2 or more people, in which each partner contributes something to the business, whether it be a skill or merely capital investment.Advantage:Comparing to sole trader, partnership is much easier to raise finance and attract investment.Because two or people can have more ideas than one, partnership would take less risks in managing.It is an undeniable fact that it maximize the possibility to introduce limited liability.Disadvantage:For some situations, partners might have conflicts in managing decisions making.Partnership is normally sued for its debts first. All debts owed must be separated to all other partners equally.The liability of the partnership is normally unlimited.The capital is limited because of lack of finance.According to Partnership Act 1890, the right of partners in the running of the business and decision making is equal. Every partner’s act can bind the firm and their partners, and it is the partner’s implied authority. If this is not the case, the other partners have to their customers.pany is an organization that has been incorporated under Companies Act 2006 and mustfollow extensive legal requirements when setting up the business.Advantage:Limited liability: The members of a company are not responsible for the company’s debts without agreement. The way the members have made the risk lowest and cannot be asked to make contribution to further finance, especially when it’s in debts.The only responsibility for the debts is the investment in the company.Separate corporate personality: The Company becomes a separate legal person different from the members.The company can have assets, sue and be sued and takes responsible for company debts.The company has legal rights and becomes a part of contract which in participate in.The ownership can be exercised by company over property.Salomon V A Saloman& Co Ltd (1897)Mr. Aron Salomon made leather boots and shoes in a large Whitechapel High Street establishment. And he set up a company with his partners. But the business was not successful and ended up with liabilty of £7,733. The company’s liquidator claimed that the company’s business was still Salomom’s.The original judge agreed with the liquidator.The Court of Appeal agreed with the liquidator stating the principle of limited liability was privilege conferred by the Companies Acts only on genuinely independent shareholders and not on “one” substantial person and six mere dummies.It is easier to raise finance than other business and has less involvement.The ownership and control are separated to members.DisadvantageThere are extensive legal requirement when setting up the business.It must be registered and comply with Companies Act 2006.3.Sole traderThere are no formalities and agreements needed or documents to be registered. Just do the business when you want, in the common law.PartnershipA agreement about the details of the duties and obligations and authority of partners is needed.Partnership is leaded bu the Partnership Act 1890, if there is no agreement.The treats to all partners of the act are equal in the managenment of the type of business.Limited CompanyIt is the most difficult to set up because of the extensive legal requirement.The document and application must be sent to Companies House and be registered.Under previous Companies Acts, every registered company was required to have a memorandum of association.And now, it plays a minor role in company formation,providing the name of the company, the registered office address, items which must be kept at the registered office, statement of limited liability, capital clause, statement ofproposed officers, statement of compliance.It is mandatory for acompany to have articles of association., which are the regulations for the inrerna arrangements and the management of the company.Some fees are needed to pay for the process.。

(完整word版)HND人力outcome3.

1A.with reference to an appropriate theory explain the main roles and activities of a managerManagement roles refers to a specific type of management behavior. Mintzberg 10 kinds of management behavior can be further combination of three main aspects, namely the interpersonal roles, informational role and decisional role.Informational including Monitor, Disseminator,Spokesperson. Interpersonal including Figurehead,Leader and Liaison. Decision including Entrepreneur, Disturbance handler,Resource allocator and Negotiator.Monitor seek and get all kinds of internal and external information, in order to thoroughly understand the organization and the environment. Also known as supervisors.Disseminator will from external personnel and lower the information transmitted to other members of the organization.Spokesperson released to the outside world organization plan, policies, actions and results, etc. Figurehead must perform the routine many legal and social obligations. Also known as the representative.Leader responsible for motivating; Responsible for personnel, training and related responsibilities. Liaison maintenance developed by external relations and sources, get help and information. Entrepreneur opportunities for organizations and environments, establish "improvements" to initiate change.Disturbance handler when organizations face focus, accident chaos, responsible for corrective action.Resource allocator is responsible for the allocation of various resources organization - to develop and approve all relevant organizational decisions.Negotiators in the main negotiations as a representative of the organization.1B.explain how the roles identified in (a) are being carried out by managers in Shangri-la HotelsIn case Ailsa as Leader in Hotel.she took part in all events of Hotel and manage all staff in the Hotel.Such as when students chose become part-time staff in the Hotel,Ailsa would increase their salary.Craig as resource allocator in Hotel.Each day in the kitchen he personally prepared the menu for the restaurant, and allocated specific tasks to the waiters and kitchen staff. He kept close tabs on exactly what each one did, as he believed that every dish that left the kitchen had his signature on it and therefore had to meet his rigorous standards.Saskia as Disseminator in the hotel. Whenever Craig was away from the hotel, Saskia was delegated the job of issuing work to the kitchen and waiting staff.2A. Explain Likert's System theory on leadershipThis theory is he and his colleagues on the production as the center of the style of leadership and people-centered leadership after a comparative study of the results. The theory is that support relationship is a two-way street. Leaders want to consider the situation of subordinate staff, ideas, and hope, help staff to achieve its objectives, make the worker to realize their own value and importance. Leader this support can motivate subordinates to the worker the worker of leadership take the attitude of cooperation, trust, support the leader's job.He's led four system model is put forward in 1967, is the leadership style is divided into four types of systems. Exploitative authoritative, benevolent authoritative, consultative and participative.He thinks only a fourth way - "participative" to achieve truly effective leadership to correctly set goals for the organization and effectively reach your target. Given the leadership to take way to motivate people, so he thought, this is the most effective way of leading a group.Management style 1 is called "the exploitative authoritarian" or "authoritarian - authoritarian". In this way, the director of the personnel is very authoritarian, rarely trust subordinates, to make people fear and punishment, the method of combination rewards to motivate people, occasionally take a top-down communication, decision-making authority is limited to the top.Management way 2 is referred to as "benevolent authoritative" or "enlightened authoritarian", in this way, the director of the personnel have full of trust and confidence of the staff; Reward and punishment and incentive methods; Allow a certain amount of communication from bottom to top, solicited subordinates some ideas and Suggestions; Granted to certain decision-making power at a lower level, but firmly control policy.Management style 3 is called "consultation". Take this way, the director of the personnel of subordinates have quite big but not fully trust and confidence, he often try to adopt the subordinate ideas and opinions; The reward, occasionally with punishment and a certain degree of participation; Engaged in two-way communication information up and down; Top on major policy and overall decision-making at the same time, allow lower-level departments make specific decision problem, and in some cases.He believes that 4 is the most effective approach of management way, can be called“participatory" collective. Managers to take a fourth way of subordinates in all matters with full confidence and trust, always get ideas and opinions from subordinates, and actively adopt them; To determine the objectives and evaluation target the progress, organize groups to participate in, on the basis of the material rewards; More engaged in the communication between with colleagues between up anddown; I encourage organizations at all levels to make decisions, or as members of the group with their subordinates to work together.2B.Which system do you believe apply to Craig and Ailsa's approach to management . explain your answer.Craig often use the benevolent authoritative system in the hotel. At the end of each week, Craig always provided free drinks for the team to celebrate, and the team always enjoyed these get-togethers. Craig always made a point of telling the team they had done a good job at the weekly get-together.Ailsa often use the group participative system in the hotel. Ailsa knew that Antonio had many years’experience in the hotel trade and trusted him and the team to implement this strategy. The sales visits that Ailsa made meant she was often away from the hotel, but in her absence Antonio ran things with little problem or fuss.3A.Describe how the Tannenbaum and Schmidt Theory of leadership shows that different situations demand different leadership approachesR. Tannenbaum and Warren Schmidt in 1958 leading behavior continuum theory is proposed. , they argue, managers in deciding what behavior (style) is most suited to produce often difficult when dealing with a problem. They don't know whether should I make a decision, or authorized to make decisions.1, tells-the leaders make decisions and announced. In this mode, the leaders identify a problem, and is considering various alternatives, choose a, and then announced to subordinates, not to direct participation in decision-making.2,sells- leader to persuade subordinates executive decisions. In this mode, with the former mode, the leader of responsibility for the identified problems and make decisions. But he is not simply declared to implement the decision, but realized that subordinates may exist in opposition, and tries to illustrate the benefits of this decision may give subordinates to persuade subordinates to accept the decision, to eliminate the subordinate.3, leaders put forward plans and solicit opinions of the subordinates. In this mode, the leaders put forward a decision, and hopes to subordinates to accept the decision, he offered the subordinate a details about his plans, and allow the subordinate problems are put forward. In this way, the staff can better understand the leader's plan and intentions, leaders and subordinates to discuss the significance and role of decision making.4, leader can modify the plan is put forward. In this mode, the subordinates can affect decisions play a certain role, but the initiative in identifying and analysing problems are still in the hands of leaders. Leader first to think of a problem, which is a temporary plan is put forward. And give the tentative plan to relevant personnel to ask for some advice.5, leader to ask questions, ask for opinion make decisions. In the above several kinds of mode, the leaders before they ask for their opinions put forward their own solutions, and in this pattern, subordinates in the decision to make before put forward their own Suggestions. The leader's active role in problem determination, subordinate role is to put forward a variety of solutions, and finally, leaders from their own and subordinates of the solutions proposed a he thinks the best solution.6, leader scope issues, subordinates collective decision-making. In this model, the leader has decision-making authority to the subordinate group. The leader's job is to figure out what the problem to be solved, and put forward decision-making for subordinates the conditions and requirements of subordinates in accordance with the extent of leaders define the problem to make decisions.7, leader allows subordinates within the limits prescribed by the boss. This model represents the extreme freedom of groups. If the leader took part in the decision-making process, he should try to make myself and other members of the team is in equal status, and prior statement observe group made any decision.3B.Describe the Bass theory of leadership and explain how it can be used to enhance the motivation, moral and job performance of employeesBass will initially be transformational leadership is divided into six dimensions, and then summarized as three key factors, Avolio in its basic way of transformational leadership behavior will be summarized as four aspects,inspirational motivation, intellectual Stimulation,idealized Influence and individualized consideration.Inspirational motivation refers to the leader r of followers placed high expectations, through the incentive to make them involved in the business of achieving an organization's vision. In practice, the leader use beliefs and emotional appeal to condensed group members, in order to obtain greater achievement than individual interests, so the factors to enhance the team spirit.Intellectual Stimulation refers to leaders inspire their followers to creativity and innovation consciousness, on its own and the leader's beliefs and values, beliefs and values to the organization also questioned, leader support follower try the creation of new theory, new method to solve theproblems of the organization, to encourage the followers to think independently and solve problems.Idealized Influence refers to the leader to the follower by way of example, followers of the leader, and is willing to follow the leader, the leader usually have higher moral standards, values and moral behavior, the leaders provide followers goals and vision, a sense of mission to followers. charismaindividualized consideration refers to the leader to create a supportive atmosphere, followers to listen carefully to the individual needs, a leader in helping the individual self-fulfillment when playing with the coach and the role of advisor, help followers to achieve its own needs and development.3c. Explain how Craig could use the above approaches to improve his leadership styleCraig also believed it was important to study at college, but he spent a lot of time personally with the kitchen staff to ensure that they understood his personal methods and that meals had to be prepared to his exacting standards.At the end of each week, Craig always provided free drinks for the team to celebrate, and the team always enjoyed these get-togethers.4.Explain two ways in which managerial performance can be measured and in each case describe how the measure can be used to assess managerial performance.Measures of managerial effectiveness method is refers to the use of certain quantitative indicators and evaluation standard, to achieve its performance goals,and to achieve this the budget execution results taken by the comprehensive evaluation method. Measures of managerial effectiveness including Appraisal, Staff development, Management development and Development programmes. Staff development : Effective development requires a systematic approach, which begins when the human resources department formulates its plan, This plan outlines the job requirements for the future in order to achieve the organizational goals, along with performance criteria in order to achieve the goals.Management development is under the specific environment of group has the resources for effective planing, organizing, leading and controlling, in order to achieve the established process of organizational goals.In case , Ailsa and Craig always use staff development. Ailsa had close links with the local college who ran hospitality courses, and would often take on learners who were studying there as part-time staff. On completing their studies, many of these learners opted to take up full-time employment with the hotel, at which time Ailsa would increase their salary. Craig believed it was important to study at college, but he spent a lot of time personally with the kitchen staff to ensure that they understood his personal methods and that meals had to be prepared to his exacting standards.Craig always use management development. Craig depended greatly on Saskia, having worked together in London for many years. Whenever Craig was away from the hotel, Saskia was delegated the job of issuing work to the kitchen and waiting staff. Craig also insisted that only Saskia and he should have the authority to sign for the meat and vegetable deliveries.。

HND项目专业大三财政预算答案报告参考Outcome3

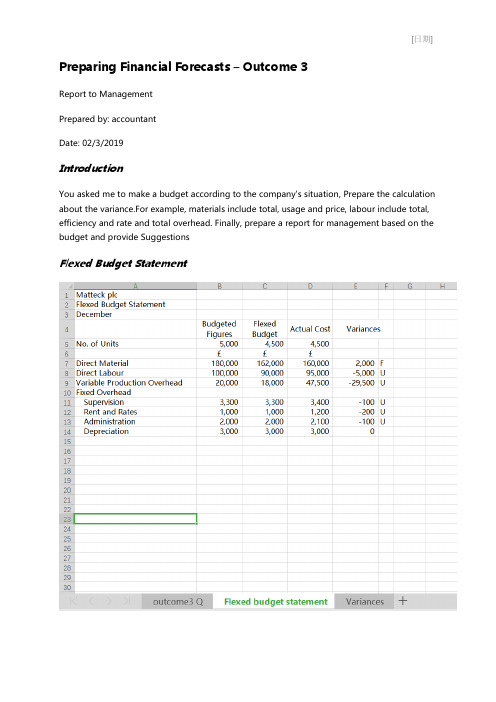

Preparing Financial Forecasts – Outcome 3Report to ManagementPrepared by: accountantDate: 02/3/2019IntroductionYou asked me to make a budget according to the company's situation, Prepare the calculation about the variance.For example, materials include total, usage and price, labour include total, efficiency and rate and total overhead. Finally, prepare a report for management based on the budget and provide SuggestionsFlexed Budget StatementPossible Reasons for VariancesDirect Material Total Variance: £2,000 F made up of:Direct Material Usage Variance:- £30,000 UDirect Material Price Variance:£ 32,000 FReasons for Direct Material Usage VarianceThe budgeted amount is 13,500 kilograms, while the actual amount is 16,000 kilograms.The possible reason for this change is that the company orders more, so the actual consumption increases.Reasons for Direct Material Price VarianceThe budget price is 12 / kg, but the actual price is 10 / kg. The possible reason for this change is that maybe the material used by the company is not good enough in quality, so the price is lowerDirect Labour Total Variance: -£5,000 U made up of:Direct Labour Efficiency Variance:£10,000 FDirect Labour Rate Variance: -£15,000 UReasons for Direct Labour Efficiency VarianceThe estimated working hours were 11,250 hours, while the actual working hours were 10,000 hours. The possible reason for this change was that the working hours were shortened due to the improvement of employees' working efficiency.The budget price is 8 pounds per hour, while the actual price is 9.5 pounds per hour. This change may be due to the increased demand of employees or the lack of sufficient labor forceReasons for Direct Labour Rate VarianceThe budget price is 8 pounds per hour, while the actual price is 9.5 pounds per hour. This change may be due to the increased demand of employees or the lack of sufficient labor forceTotal Overhead Variance:-£400 UThe direct material,direct labour,variable overhead,administration and insurance have changed.The possible reasons for this change are the improvement in working efficiency and the fact that employees can complete more work in a shorter time, or the company finds an alternative and cheaper product, which makes variable overhead reduced.RecommendationsAs can be seen from the fixed budget statement, labor costs have increased, and variable production costs have far exceeded the budget, possibly due to insufficient labor force. Therefore, I suggest that the company should attract more employees and purchase more raw materials。

HND商务会计高级outcome_3_4_5报告答案.docx

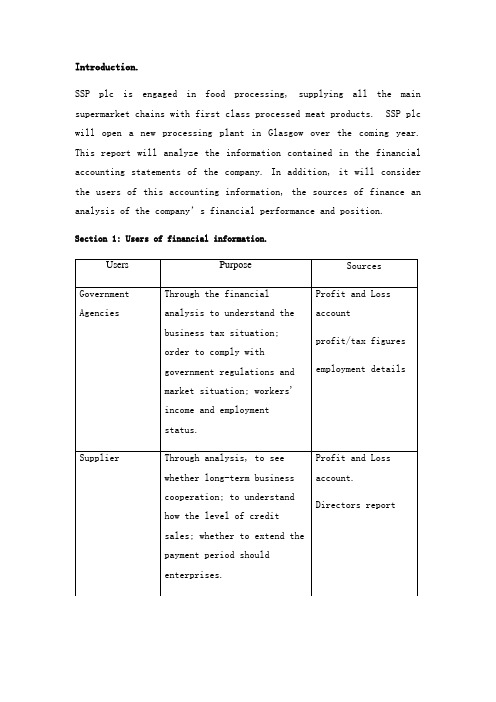

.word 可编辑 .Index pageIndex page⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯.. Introduction⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯.Background ⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯.. FindingsSection 1⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯Section 2⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯Section 3⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯Conclusion⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯Reference⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯⋯..word 可编辑 .IntroductionBackgroundSSP plc is a company operating in the food manufacturing industry. It is engaged in food processing, supplying all the main supermarket chains with first class process meat products. During the last few years the company has been difficult because of the BSE andFoot and Mouth disease made a declining demand for meat product. The bad outstanding achievement stopped in 2004 and a partial rebound in the market produced an increase in turnover by nearly 15%. It is expected that this rebound in the market will gather momentum over the coming year and the SSP plc is planning to take even greater strides forward by opening a new processing plant in Glasgow.As requested in the chief executive s memo’ of 30 December, here is my reportsummarising and analysising the financial position of the SSP plc for the year 2003 and2004.OutlineThe main body of the report will evaluate five parts:Part 1--- Analyze the users of financial information and the purpose of using.Part 2--- State of financial source and categorize with their characteristics.Part 3---Explain the cash flow statement of SSP plc.Analyze the recent financial performance and position of the SSP plc.(Including my recommendations about how to improvement of business performance).word 可编辑 .FindingsSection ers of financial accounts.Users of financial statements are a group of people or organizations who use the information to make evaluations and decisions. Users of financial information can bedivided into two categories: internal and external users.Now, I will use a table to show you the users’ purpose and sources of information to get the statements.Section 2.Source of financesTo run a business, organizations require finance for different proposes and for varyinglengths of time. In the finance, we divide sources of capital into two categories: equitycapital and loan capital. Equity capital is the finance provided by the owner and there is nointerest to pay. Loan capital refers to money that is borrowed from a source outside thebusiness. The interest of loan capital must be paid. Sources of finances could be clarifiedinto short, medium and long term. The short-term refers to finance that are borrowed fora period of no more than one year. The medium-term refers to funds that are borrowed fora period of between two and ten years. Long-term refers to funds that are borrowed for aperiod of more than ten years.In the case study, the source of finances of SSP plc is: trade creditors, tax, bank overdraft, debentures, ordinary share capital and the retained profits from last account period..word 可编辑 .Short-term sources:1.Trade creditors:Trade creditors are produced when the purchase of raw materials or stock is delaying topay, thus, there is more cash which would be used for other uses. There is also aninterest free way of raising finance. However, the credit could lead to poor relationswith suppliers and the customers may forfeit discounts.The credit is£544,000 in 2003 and it decreased to he percentage£405,000ofin 2004. T decrease is 25.56%. The decrease of credit infers that SSP plc has a good financialsituation that it has a strong ability to pay credits back to suppliers. This could improvethe relationship with suppliers.2.Bank overdraft:Bank account holders can prearrange with the bank to draw cheques to a greater valuethan the actual balance in the account. Interest should be paid by customers and bankcharges will apply where an overdraft limit has been exceeded. Bank overdraft is flexibleand cheap. It has a low cost. Some small bank overdraft even has a free of charge.SSP plc had no overdraft but the number increased to£86,000 in 2004. The shows that the company borrowed money from bank for its expansion in Glasgow.Long-term sources:1.Debentures:Debentures are loans make to companies that carry a fixed rate of interest.Thecompany ’fixeds assets normally secure debentures. Debentures have a fixed timeperiod or an open time period. The shareholders are not debenture holders.Adebenture interest is paid as an expense not an appropriation of profit.SSP plc has a fixed debenture (£1,560,000) in the year of 2003 and 2004. It tells us the company ’ s fixed assets are steady.2.Ordinary shares:Ordinary shareholders receiving pay-outs from company after preference shareholdersare paid. Ordinary share dividends are not fixed and subject to companyperformances and decisions of management in paying dividend.In SSP Company, the ordinary share capital is£1,950,000and in2004both.It2003infers that the company has a steady operation situation.3. Retained ProfitsThe retained profit is the finance brought from the last financial period. It is not fixedand may be a negative number. It presents operational situation of last period.The retained profits decreased from 505,000£ to420,000£. The percentage change ofdecrease is 16.83%. The lower ratio shows us the company had made fewer profits in2003 then it was in 2002.Section 3. Ratio Analysis1.Major inflows is Net cash flow op erating activates of£ 1,345,000.Major outflow is Payments to acquire fixed assets, which takes£ 984, 2.Ratio AnalysisProfitability Ratios:Gross Profit Percentage=Gross profit/Turnover x 100%2003: GPP=£ 7,000,000/£ 11,674,000 x59100.96%=2004: GPP=£ 8,037,000/£ 13,382,000 x60100.06%=Trend: IncreaseAnalysis: The increase of ratio is a good sign. The positive trend can be an indicationthat stock control of meat product has improved, demand for the meat product has increased after the diseases, or purchasing policies have improved. The managers should keep the good trend and go on develop it, such as improving marketing strategy, setting better pricing policy, or improving stock control.Net Profit Percentage=Net Profit before Taxation/ Turnover x 100%2003: NPP=£ 1,182,000/£ 11,674,000 x10100.13%=2004: NPP=£ 901,000/£ 13,382,000 x 6100.73%=Trend: DecreaseAnalysis: The decrease of the ratio is a bad sign that it indicates a low profit of the company. From the P&L Account of the SSP plc, we know that although the grossprofit increased, the operation cost is much higher in 2004; it leads to a decrease innet profit. So the managers should think about how to decrease our operation cost tohelp our company earn more profit.Liquidity Ratios:Current Ratio=Total Current Assets/Total Current Liabilities.word 可编辑 .2003: CR=£ 1,195,000/£ 767,000=1.562004: CR=£ 1,248,000/£ 701,000=.78Trend: IncreaseAnalysis: the increase of ratio is a good sign. Generally speaking a healthy current ratiois at least 2:1. The 1.56 and 1.78 indicate the company is a little bit over trading andhave difficulty in meeting its short-term debts. The main reason for the increase is the increase in the total current assets and decrease in the total current liabilities.I suggest that the company may keepmore profit for the short-term debts.The Acid Test Ratio=Liquid Assets/Current Liabilities2003: (£ 1,195,000-£608,000)/£ 767,000=.772004: (£ 1,248,000-£796,000)/£ 701,000=.64Trend: DecreaseAnalysis: The decrease is a bad sign. The ratio should be 1:1. But the ratio in both of2003 and 2004 is less that 1. And unfortunately, the ratio is still decreasing. SSP plcmeets a liquidity problem that the liquid assets decrease. The company managersshould pay attention to this ratio and organizatio n ’ s development.Efficiency Ratios:Fixed Asset Turnover=Turnover/Fixed Assets2003:£ 11,674,000/£ 4,017,000=2.91 times2004:£ 13,382,000/£ 4,318,000=.10times.word 可编辑 .Trend: IncreaseAnalysis: Where this ratio gas increase, this is a good sign. It indicates that the existingfixed assets are generating more sales and maybe investment in new fixed assets gascould be been paid off. Managers of SSP plc should develop and focus on it.Debtors Collection Period=Debtors/Turnover x 3652003:£ 306,000/£11,674,000 9x.57365=days2004:£ 452,000/£13,382,000 12x365=.33daysTrend: IncreaseAnalysis: It is a bad sign that there is an increase in DCP. It indicates that SSP’ s m have a poor credit control of poor invoicing system. The bad debts may also increase.The leaders of SSP should check their invoicing and reminder system to keep the ratioa proper range.Investment Ratios:Interest Cover=Profit Before Interest & Tax/Interest Charges2003:£ 1,416,000/£ 234,000=6.052004:£ 1,135,000/£ 234,000=.85Trend: DecreaseAnalysis: This ratio shows how capable the company is of covering its interest charges.The decrease is not good because the company is less able to meet its interest payments. But the ratio is still in a reasonable range. Leaders should try to increasecompany ’ s profit to keep this ratio a high level..word 可编辑 .Debt Ratio=Total Debts/Total Assets x 100%2003: (£ 767,000+£ 1,560,0(£4,017,000+0)/ £1,195,000) x 100%=44.65%2004: (£ 701,000+£ 1,560,000)/(£4,318,000+ £1,248,000) x 100%=40.62%Trend: DecreaseAnalysis: It is a good sign that the ratio increased. However, a healthy ratio shouldkeep around 50%. It indicates that SSP has fewer liabilities or keeps more assets. Thesign should be kept by managers.3.RecommendationAfter reading and analyzing three accounts from SSP Company, I found some problemswith it and now I will present my suggestions about the future management in thesetwo parts.Operational recommendationA ratio of Net Profit Percentage shows us that SSP plc has a high expenditure inoperation cost. It also indicates that the company has a low level of cost control.Therefore, I suggest that SSP should try to decrease the costs of sales and theoperation cost, such as adopting new management system and using contractors tofind distribution channels but to find them itself.Financial recommendationFor the source of finance, SSP has a bad performance of financial operating. In the CashFlow Statement, the Financing is£0, but the company is planning expansion in Glasgo The main inflow of the company is the sales. It is a dangerous phenomenon if the.word 可编辑 .company wants to use the turnover to expanse its business because it is impossible touse the current cash to support long-term investment. So I suggest that the companymay increase the number of share capital or make more debentures to get more long-term capital for expansion.ConclusionBy analyzing the P&L Account, Balance Sheet and Cash Flow Statement, we can infer thatSSP plc has a good operational performance. However, there are still many parts to improve and develop to help the company maximize profits.ReferenceRay H. Garrison, Managerial Accounting, Business Publications Inc., 1985, Printed inU.S.A.J.R.DYSON, Accounting for Non-accounting Students, Financial Times, 2004, Printed in Great Britain.Frank Wood & Alan Sangster, Business Accounting 2, Financial Times,Pitman Publishing, 1999, Printed in China.。

HND SQA 财政预算outcome3 答案

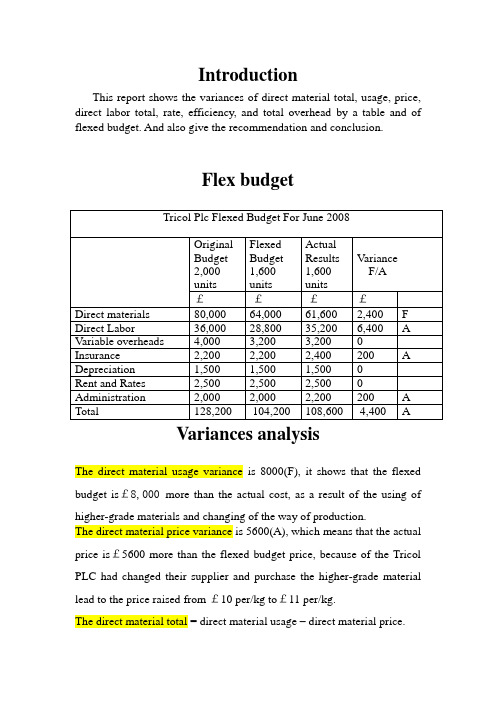

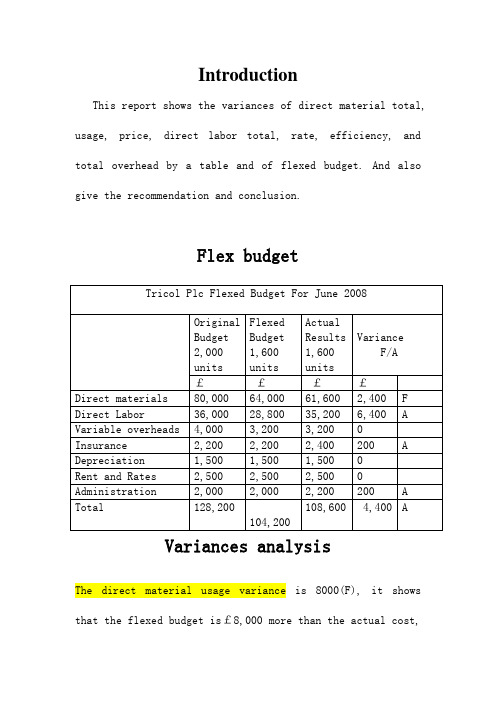

IntroductionThis report shows the variances of direct material total, usage, price, direct labor total, rate, efficiency, and total overhead by a table and of flexed budget. And also give the recommendation and conclusion.Flex budgetVariances analysisThe direct material usage variance is 8000(F), it shows that the flexed budget is£8,000 more than the actual cost, as a result of the using of higher-grade materials and changing of the way of production.The direct material price variance is 5600(A), which means that the actual price is£5600 more than the flexed budget price, because of the Tricol PLC had changed their supplier and purchase the higher-grade material lead to the price raised from £10 per/kg to£11 per/kg.The direct material total = direct material usage – direct material price.As calculated above, 8000-5600=2400, the direct material total variance is£2400.The direct labor rate variance is 3520(A), which means that the actual labor rate is£3520 more than the flexed budget, caused by the company supplied a higher-than-expected wage, the labor cost raised fro m£9 per hour to£10 per hour, and may because Some employees still apprentices, with poor efficiency.The direct labor efficiency variance is 2880(A), as to say, the actual labor efficiency is£2880 more than flexed budget efficiency.It may be because the machine on the production line equipment getting old and it influence the efficiency of employees at the time of production, or maybe the culture of the company is not so well at current time, which result in reduced efficiency.The direct labor total variance is 6400(A) caused by the labor rate variance and efficiency variance. It shows that the actual total labor is £6400 more than the flexed budget total labor.The total overhead variance is 400(A) that means the actual total overhead is £400 more than flexed budget, which caused by the changing of administration overhead and insurance cost both. These two things may change by the company change the salary of the management, and they may add extra insurances for the employees or the machinery.ConclusionThere is a policy of the company in which the company applies a rate of significance of 3% for any Variance analysis. According to the data above, we can clearly see that all the actual variances are higher than 3%, it may caused by the actual production for June was 80% of the target amount, and there are some respects had been changed in the factory.RecommendationI’d give some advices to Tricol Plc for improving their business.●To improve the efficiency not only by increase the salary but alsochange the way of production.●The company may discuss with the new supplier to lower rawmaterial prices.●Training a group of experienced staff.Appendix1. Direct material total variance(Standard units of actual production *standard price) - (actual quantity* actual price)10*4*1600- 61600=2,400(F) 2400/64000=3.75%2. Direct material usage varianceStandard price*(standard units of actual production –actual units)10*(4*1600-5600) =8,000(F) 8000/64000=12.5%3. Direct material price varianceActual quantity *(standard price –actual price)5600*(10-11) =5,600(A) 5600/64000=8.75%4. Direct labor total variance(Standard hours of actual production*standard rate ph) –(actual hours*actual rate ph)2*1600*9-35,200=6400(A) 6400/28800=22.22%5. Direct labor efficiency varianceStandard rate ph*(standard hours of actual production- actual hours)9*(1,600*2-3,520) =2880(A) 2880/28800=10%6. Direct labor rate varianceActual hours*(standard rate ph-actual rate ph)3520*(9-10) =3,520(A) 3520/28800= 12.22%7. Total overhead varianceTotal standard overhead for actual production- total actual overheads (1600*2-3,200) - (8,200-8,600) =400(A) 400/ (3200+8200) =3.51 %。

hnd经济学导论outcome3

Merit goodsThe merit goods are provided from government and basic on the human’s need. The merit goods not distributed through price system. But the private sector do not provide merit goods for people(SQA, 2013). Because the private sector just consider themself benefit, it do not consider ordinary people’s safeguard and maybe private sector do not assume to distribute for people . For example: The museum is merit goods from government to provide. It can free visit goods for people. But the private sector do not have many capital pay for the museum and they only collection of charges that people can visit goods. So the government can provide merit goods.Public goodsThe public goods that the social of the goods, the people can together share the goods. In other words, if you use this goods, but you do not prevent other people use goods that Non-rivalry in consumption or if you use this goods, but you do not reduce other people together use this public goods that Non-excludability. Such as: the government provide park for people that can do exercise or visit scenery in park and everyone do not pay ticket for park. But the private sector do not provide park, becausethe people can see the scenery outside the park and private sector do not prevent the people see the scenery. So the government provide public goods.The existence of imperfect marketThe existence of imperfect market is little or competition in companies. So they will appear monopoly and oligopoly. Monopoly goods provide from single supplier. Oligopoly that have less supplier play a leading role. The monopoly will goods have high price and the company does not update technology and bring many bad influence. For example: Communication enterprise are monopoly by Moving enterprise, Linking enterprise and Telecommuting enterprise. They are oligopoly. The most people use them enterprise to exchange. But have less people use network communicate. So, the government make anti monopoly policies, prevent cut-throat competition.ExternalitiesThe externalities that participate in an action, give people to bring benefit or harm. But these people does not fee charging or pay remuneration. It include external benefit and external cost. For example: A people smokein the public and another people smell of smoke, but people who smoke in public, he does not pay charge for another people. It is external cost. So, the government make a policy that doesn’t smoke in the public.For example: A people plant flowers in his garden. Then a bad mood person come with flowers. When he see flowers, his mood become better. But a people who plat flowers does not collect charge for another people. So this is external benefit.。

HND商法导论outcome3

又称“有限责任公司”。指由法律规定的一定人数的股

东所组成,股东以其出资额为限对公司债务承担责任, 公司以其全部资产对其债务承担责任的企业法人。

► 有限责任公司是企业法人,公司的股东以其出资额对公 司承担责任,公司以其全部资产对公司的债务承担责任。

► 有限责任公司的股东人数是有严格限制的。各国对有限 责任公司股东数的规定不尽相同。

➢ The shareholders of a public limited company are free to sell their shares at any time, this does not require the permission of the board of directors.18

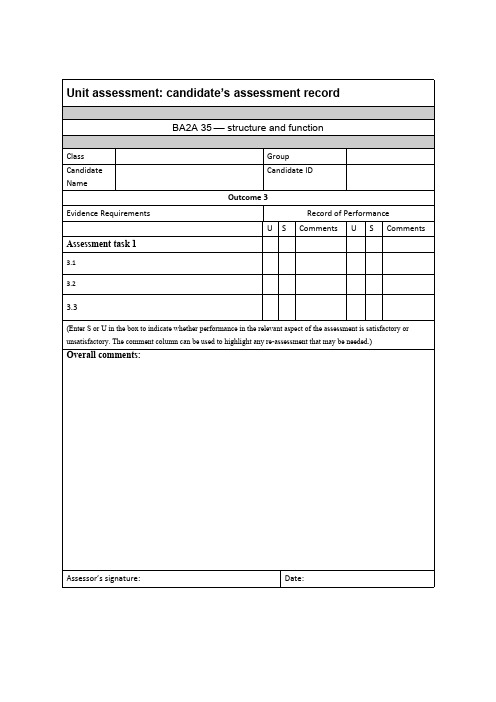

Outcome 3

1. Legal Differences between Sole Traders, Partnerships and Incorporated Bodies

1

Legal Differences between Sole Traders, Partnerships and

Incorporated Bodies

List and explain the key advantages and

disadvantages of Mary’s businesl authority Mary has in taking

【VIP专享】HND组织结构与功能outcome3

Assessment 3Outcome covered 3Assessment instructionsYou are required to read the information presented in the case study, which has been issued to you 2–3 weeks prior to the assessment event when the questions based on the case study will be given to you to respond to. During this period you may complete research and investigation into the case study and prepare notes for use at the assessment event.Following the case study of YTE from Outcome 1Increased demand had outpaced YTE’s ability to produce and deliver a product. Customers had to wait longer because productivity was diminishing and customer satisfaction was fading fast. The YTE plant is located near downtown Qingdao so it is impossible to expand its production size and acquire more facilities due to land development saturation. In addition, YTE outsourced its logistics and distribution to a local small-size third party logistics company. However, the logistics company put YTE aside when there was insufficient transportation and distribution capabilities during peak time period.YTE planned to set up a new plant in the western coast economic development zone of Qingdao due to the availability of greater government incentives and sufficient economic resources such as land and cheap skilled labour force. In addition, the senior management of YTE proposed to establish a Logistics Park including in-house warehousing and an international transportation business in the economic development zone area due to well-constructed infrastructure. The long-term plan of YTE is to diversify its business including manufacture and the related industry logistics business serving external customers within the industry. The Headquarters of YTE will still be located in the building in downtown Qingdao.At the end of 2012 a huge new manufacturing facility plant was started in the western economic development zone, as well as in-house warehouse of YTE. The start-up provided the opportunity to create a high performance work organisation within YTE in order to improve customer satisfaction levels and increase operational efficiency and effectiveness. The new plant is designed to have practically no management structure. Line managers will not exist, and all personnel will be empowered to make decisions. Staff from the Research Centre, Production Department and Sales Team will come together in teams each day to discuss and solve related product quality and production issues. The team will consult assembly workers about the process of the operation to make production adjustments based on suggestions from front-line staff and customer feedback. Meanwhile more training regarding knowledge and approaches will be provided for employees in the process of an empowered workplace. With Automated Storage and Retrieval System (AS/RS) application the logistics warehouse can speed up goods flow within YTE torespond to customers’ orders in a timely manner. In addition YTE will set up a close partnership directly with a local shipping company and port bureau so as to avoid any delays in delivery.Assessment 3Answer the following questions based on the second Yong Tong Electronics (YTE) case study. 、3.1 Describe the change process within YTE in detail, and explain four factors affecting change within the organisation from:global competitioncustomer focustechnologyshareholder pressureethical considerationssocial responsibilityenvironmental considerationsregulatory requirementscollaborative arrangementsspeed and flexibility changesquality and reliability issuesdiversificationrestructuringDue to the increase in demand over the YTE production and delivery capabilities, and logistics company is responsible for YTE logistics responsible, which lead to YET logistics unstable, resulting YTE cannot delivered on time in the logistics’ busy time. So they decided to establish Logistics Park in economic development zone in the western, logistics park staff from various departments who is allocated by YTE, in order to have higher efficiency, line managers would not exist, and all staff have the power to make decisions, and every day the talk together to discuss how to improve product quality, and share experience. At the same time, YTE provide the training to let the staff know how to use modern logistics system.Customer focus: Because customers buy YTE product have to takes a long time to wait, it leads to customer reduced their demand from YTE, which make YTE reduce product sales, at last, the company's cash flow shortage and making it decide to change its organization and do their own logistics.Environmental considerations: Because the logistics company put YTE aside when there was insufficient transportation and distribution capabilities during peak time period, which lead YTE customer have to wait a long time for their products. At the same time due to the availability of greater government incentives and sufficient economic resources such as land and cheap skilledlabor force, make YTE establish its own logistics park more easily.Speed and flexibility changes: Unlike YTE previous organizational structure, the logistics park of YTE did not have line manager, all the decided are belong to all the staff, it help the logistics with a rapid response capability, and its human resource are more flexibility, which will let its logistics more efficiency.Diversification; YTE is a manufacture enterprise of electronic products, because of its new business, which lead to YTE need to change its own human resources, transferred part of the staff from various departments, consist the logistics sector.3.2 Describe four tools and models for change management from the following:SWOT analysisforce field analysisstakeholder analysisBurke-Litwin’s Change ModelLewin’s Change Management ModelCongruence ModelThe Change CurveSWOT analysis:SWOT(Strengths Weakness Opportunity Threats)analysis, to ensure the company own strength, weakness, opportunity and threat. Combine the company’s strategy, internal resource and external environment.Strengths:1.There are many loyal customers in Europe.2.Have advance technology and provideperipheral products and service. Weakness:1.The enterprise is located in the city center,so that the enterprise cannot Large-scaleproduction.ck it own logistics system.Opportunity:Government incentives and adequate financial resources, such as cheap labor.Threats1.Customer loss the demand from thecompany because they have to wait long for their product.2.The competitor from the south of China.Force field analysis: Force Field Analysis is a diagnostic technique, which has been applied to ways of looking at the variables involved in determining whether organizational change will occur. It is base on the concept of “forces”, a term which refers to the perceptions of people in theorganization about a particular factor and its influence. From YTE’s force field analysis we can found the reason of the organization change which due to it driving is more than restraining.Stakeholder analysis:The stakeholder analysis tool gives visual representation of the expected behaviors of key stakeholders and identifies the level of effort that is likely to be required for each, in YTE, the most important stakeholders are government, staff, and senior manager, and customer.stakeholdersperformance StaffThey need salary , promotions and bonuses Senior managerCorporate decision-making power and glory CustomerCan get a quality assurance products GovernmentIncrease tax revenue and provide jobs for social.Levin’s Change Management Model:This model has three steps: Thaw - Change – thaw again, in the first stage, due to the logistics lead goods cannot deliver in the time, it let the customer decrease the demand from thecompany, which let the enterprise realize it must have it own logistics. In the second step, the enterprise has a clear development direction that establish a logistics park in the westerneconomic development zone, through change the manage structure and use new technology let its logistics has a high level, in the last step, they use its structure and technology to make the staff become skill labor, which improve the quality of staff.In addition, one model chosen from the above should be applied for change management within the YTE case study.3.3 Describe the stages and process of organisational development making reference to four of the following:chaosstabilityhigh performanceorganisational assessmentgoal settingemployee developmentrestructuringchange managementThe first step of the enterprise is realized the reason of change: because of its logistics can make the customers satisfied, it cause the customers decrease their demand from YTE, In order to ensure a stable logistics and maintain a well relationship with customers, YTE decided to establish its logistics park. Because the government support and have enough economic resource, they choose the western economic development zone for its Logistics Park, which contain manufactured and storage products, to ensure it has a high efficiency, unlike YTE original structure, the use the matrix organization structure which means it did not have line manager, all the decision was made by the staffs, which can lead the enterprise had a rapid react that can made the products flow more smoothly, all the staff had have a meeting every day, which means they can share the experience and talk about the issue in the work every day, meanwhile more training regarding knowledge and approaches will be provided for employees in the process of an empowered workplace. At last, because use Automated Storage and Retrieval System to ensure the transport speed and quality, finally, it assurance the relationships with customers and the customers desire of YTE products.。

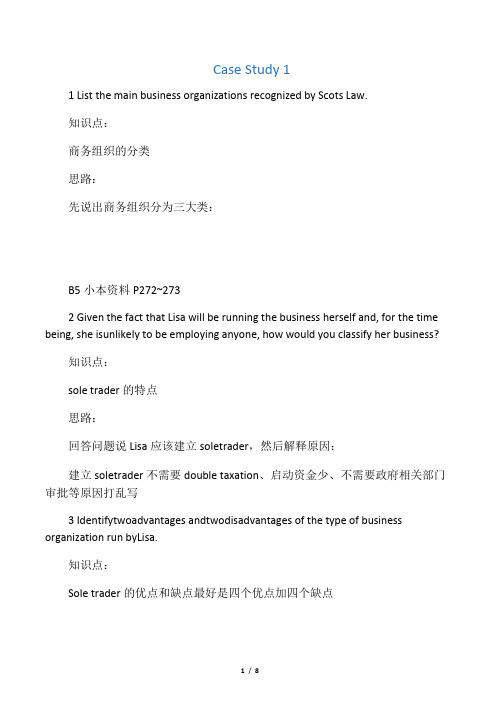

SQA HND 商法 Outcome 3 答题思路

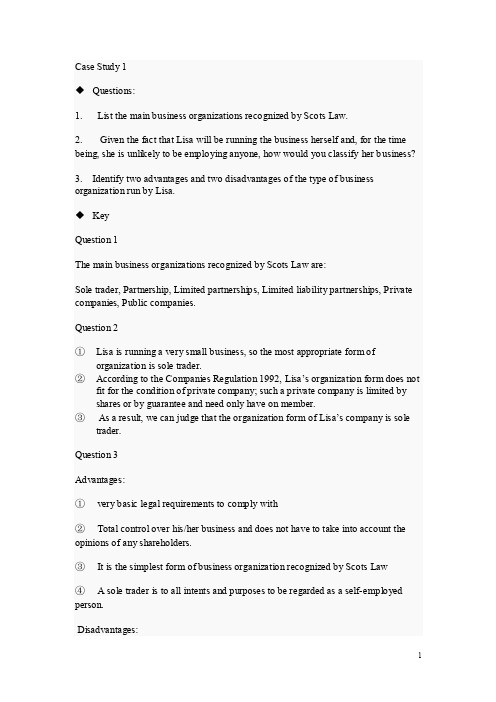

Case Study 11 List the main business organizations recognized by Scots Law.知识点:商务组织的分类思路:先说出商务组织分为三大类:B5小本资料P272~2732 Given the fact that Lisa will be running the business herself and, for the time being, she isunlikely to be employing anyone, how would you classify her business?知识点:sole trader的特点思路:回答问题说Lisa应该建立soletrader,然后解释原因:建立soletrader不需要double taxation、启动资金少、不需要政府相关部门审批等原因打乱写3 Identifytwoadvantages andtwodisadvantages of the type of business organization run byLisa.知识点:Sole trader的优点和缺点最好是四个优点加四个缺点B5小本资料P272或者A4材料1P1~P3推荐用这个材料答案更清晰一下每个优缺点下面有三句解释随机选择一个来写解释上面的小标题Case Study 21Whatarethemaindifferencesbetweenatraditionalpartnershipandalimitedliabilit ypartnership?知识点:无限合伙人(Unlimited partnership UP & limited liability partnership LLP)和有限责任合伙人之间的区别思路:1."法案不同UP:the Partnership Act 1890(在A4材料1 P287)LLP:The limitedliability partnership Act 20002.责任不同UP:Unlimited liability LLP:limited liability3.合伙人名称不同UP:Partners LLP:members4.设立条件不同:UP:there are no formal legal requirements for setting up a partnership LLP:5. UP:partnership agreement is no necessary to have. LLP:LLP agreement is necessary/must.6. UP:not necessary to reveal LLP:have to/must reveal financial information2版书P198~P201、"3版书P209~P213;再加上课堂笔记;B5小本资料P290以上6个不同点,随机选四个去答打乱顺序改变语序2Whatisthemainadvantageforanexistingpartnershipwhenitchangestoalimitedlia bility partnership?知识点:从无限责任更改成有限责任的最主要的好处是责任的改变思路:回答问题说明最主要的好处是责任的不同然后具体说明两个partnership的责任上有什么不同之处UP:责任是unlimited liability并且是无限连带责任(2版书P199第二段第四行到第六行;3版书P210倒数第三行到P211第一行)LLP:责任是limited liability是因投资额为限(2版书P200倒数第四段全部;3版书P212第三段全部)3 What is the nature of the legal relationship between partners in a firm and members of alimited liability partnership?知识点:法律关系是诚心关系fiduciary relationship思路:回答问题the nature of the legal relationship is fiduciary relationship,然后说partner代表的是公司和合伙人member代表的是只是公司先例:(A4资料1 P9中间部分)Law v Law [1905] 1 Ch 140A4资料1 P9Case Study 3知识点:公司备忘思路:objects clause的概念(A4资料2 P2总共有两个概念2选1或者写书上的2版P229倒数第三段3版P241倒数第四段)然后写ultra vires(和公司备忘的概念在同一处)A4资料2 P2、"2版书P229倒数第三段3版P241倒数第四段2 Does MacGregor have the right to withdraw from the project with Construct it?知识点:Ultra vires rule思路:回答问题:没有权利取消;在现代条款,在不违反法律的前提下,公司经营范围是无限制的;法案是theCompanyAct1989&2006;ultraviresrule没意义没有权限限制;Macgregor很难胜诉协议继续履行在历史上有一个old ultra vires rule越权无效原则;写出这个的概念(A4资料2 P3或2版P229 3版P241);如果法官参照这个原则那么这个project可以被withdraw;但是这是案例法成文法优先于案例法所以法官需要参照成文法MacGregor很难诉赢先例:A4资料2 P3——Ashbury Railway Carriage & Iron Co. V. Riche(1875)A4资料2 P3;2版P229、"3版P241知识点:公司章程思路:回答问题:股东不能要求公司进行分红;根据公司章程,股东没有绝对的权利分红;公司章程的性质是合同,是公司和股东之间&股东和股东之间的合同;股东没有绝对权利要求分红,公司可以不分红,并没有违约先例:Wood v Odessa Waterworks Co(1889)或者Hickman v Kent or Romney Marsh SheepBreeders Association [1915]二选一(2版P237、"3版P250)2版P237、"3版P250Case Study 4知识点:两种公司的区别思路:最好列出4个区别至少3个随机选择A4资料2 P1~P2;B5小本资料P309~P310公司设立的条件思路:回答问题:不能自己决定成立公司并且立刻交易;公司不能自己成立,公司成立需要进行注册;公司成立的5步骤;2版P226、"3版P238知识点:公司的法律地位思路:公司的法律地位是legal entity加上legal personality;公司是一个与其股东相分离的独立的法人;先例:Salomon v A Salomon & Co Ltd 1897 (2版P217~P218、"3版P229~P230)(判决部分从第二段的第六行“However”后面写到这段结束)2版P216~P218、"3版P228~P230公司谁responsible思路:Ltd是所有股东responsible;Plc是all employee responsible; employee其中分为managers和directors知识点:公司股东的责任思路:普遍的责任类型是有限责任;限于股东的出资额和股数;2版P200+P230、"3版P212+P242注:1." 2版书和3版书得区别在封皮右上角2. A4材料1指材料开头有四行加粗的标题3. A4材料2指材料开头为Private limited company vs. Public limited company 本文件为,仅供参考,如有雷同,概不负责- 3 -。

SQA HND 商法 Outcome 3 答题思路.doc

Case Study 11List the main business organizations recognized by Scots Law.知识点:商务组织的分类思路:先说出商务组织分为三大类:sole trader, partnership, company然后partnership具体说有三种:Ordinary/traditional/unlimited partnership 最后说company 具体分为private limited company 和public limited company来源:B5小本资料P272~2732Given the fact that Lisa will be running the business herself and, for the time being, she is unlikely to be employing anyone, how would you classify her business?知识点:sole trader的特点思路:回答问题说Lisa应该建立sole trader,然后解释原因:建立sole trader不需要double taxation、启动资金少、不需要政府相关部门审批等原因打乱写3Identify two advantages and two disadvantages of the type of business organization run by Lisa.知识点:Sole trader的优点和缺点最好是四个优点加四个缺点来源:B5小本资料P272或者A4材料1 P1〜P3推荐用这个材料答案更清晰一下每个优缺点下面有三句解释随机选择一个来写解释上面的小标题Case Study 21What are the main differences between a traditional partnership and a limited liability partnership?知识点:无限合伙人(Unlimited partnership UP & limited liability partnership LLP)和有限责任合伙人之间的区别思路:1,法案不同UP: the Partnership Act 1890 (在A4 材料 1 P287) LLP: The limited liability partnership Act 20002.责任不同UP: Unlimited liability LLP: limited liability3.合伙人名称不同UP: Partners LLP: members4.设立条件不同:UP: there are no formal legal requirements for setting up a partnership LLP: forming an LLP is more expensive and complicated than setting up a unlimited partnership (书上原话记得更改语序等)5.UP: partnership agreement is no necessary to have. LLP: LLP agreement is necessary/must.6.UP: not necessary to reveal LLP: have to/must reveal financial information来源:2版书P198〜P201、3版书P209〜P213;再加上课堂笔记;B5小本资料P290以上6个不同点,随机选四个去答打乱顺序改变语序2What is the main advantage for an existing partnership when it changes to a limited liability partnership?知识点:从无限责任更改成有限责任的最主要的好处是责任的改变思路:回答问题说明最主要的好处是责任的不同然后具体说明两个partnership的责任上有什么不同之处UP:责任是unlimited liability并且是无限连带责任(2版书P199第二段第四行到第六行;3版书P210倒数第三行到P211第一行)LLP:责任是limited liability是因投资额为限(2版书P200倒数第四段全部;3版书P212 第三段全部)3What is the nature of the legal relationship between partners in a firm and members of a limited liability partnership?知识点:法律关系是诚心关系fiduciary relationship思路:回答问题the nature of the legal relationship is fiduciary relationship,然后说partner 代表的是公司和合伙人member代表的是只是公司先例:(A4 资料1P9 中间部分)Law v Law [1905] 1 Ch 140来源:A4资料1P9Case Study 31What is a company9s objects clause?知识点:公司备忘思objects clause的概念(A4资料2 P2总共有两个概念2选1或者写书上的2版P229 倒数第三段3版P241倒数第四段)然后写ultra vires (和公司备忘的概念在同一处)来源:A4资料2 P2、2版书P229倒数第三段3版P241倒数第四段2Does MacGregor have the right to withdraw from the project with Construct it?知识点:Ultra vires rule思路:回答问题:没有权利取消;在现代条款,在不违反法律的前提下,公司经营范围是无限制的;法案是the Company Act 1989&2006; ultra vires rule没意义没有权限限制;Macgregor很难胜诉协议继续履行在历史上有一个old ultra vires rule越权无效原则;写出这个的概念(A4资料2 P3或2版P229 3版P241);如果法官参照这个原则那么这个project可以被withdraw;但是这是案例法成文法优先于案例法所以法官需要参照成文法MacGregor很难诉赢先例:A4 资料 2 P3-----------------------------------Ashbury Railway Carriage & Iron Co. V. Riche (1875)来源:A4资料2P3; 2版P229、3版P2413Will the legal action by MacGregor shareholders be successful so that the company will be forced to pay out the expected bonuses?知识点:公司章程思路:回答问题:股东不能要求公司进行分红;根据公司章程,股东没有绝对的权利分红; 公司章程的性质是合同,是公司和股东之间&股东和股东之间的合同;股东没有绝对权利要求分红,公司可以不分红,并没有违约先例:Wood v Odessa Waterworks Co (1889)或者Hickman v Kent or Romney Marsh Sheep Breeders Association [1915]二选一(2 版P237> 3 版P250)来源:2版P237、3版P250Case Study 41List three differences between a private company and a public company知识点:两种公司的区别思路:最好列出4个区别至少3个随机选择来源:A4资料2 P1~P2; B5小本资料P309-P3102Can people simply decide to set up any kind of company and begin to trade immediately?知识点:公司设立的条件思路:回答问题:不能自己决定成立公司并且立刻交易;公司不能自己成立,公司成立需要进行注册;公司成立的5步骤;来源:2版P226, 3版P2383What kind of legal status is a company said to have?知识点:公司的法律地位思路:公司的法律地位是legal entity加上legal personality;公司是一个与其股东相分离的独立的法人;先例:Salomon v A Salomon & Co Ltd 1897 (2 版P217~P218、3 版P229-P230)(判决部分从第二段的第六行“However,^后面写到这段结束)来源:2 版P216~P218、3 版P228-P2304What management body is responsible for the day-to-day running of a company?知识点:公司谁responsible思路:Ltd 是所有股东responsible; Pic 是all employee responsible; employee 其中分为managers 和directors5What is the most common type of liability for company members?知识点:公司股东的责任思路:普遍的责任类型是有限责任;限于股东的出资额和股数;来源:2 版P200+P230, 3 版P212+P242注:1. 2版书和3版书得区别在封皮右上角2.A4材料1指材料开头有四行加粗的标题3.A4 材料2 指材料开头为Private limited company vs. Public limited company。

hnd会计期末考

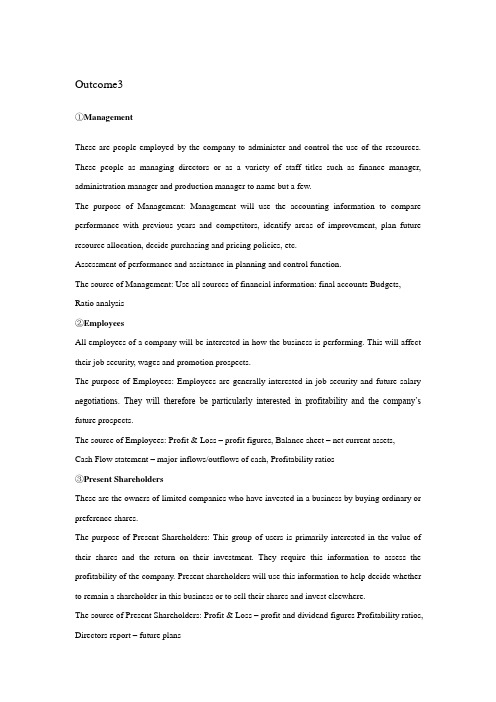

Outcome3①ManagementThese are people employed by the company to administer and control the use of the resources. These people as managing directors or as a variety of staff titles such as finance manager, administration manager and production manager to name but a few.The purpose of Management: Management will use the accounting information to compare performance with previous years and competitors, identify areas of improvement, plan future resource allocation, decide purchasing and pricing policies, etc.Assessment of performance and assistance in planning and control function.The source of Management: Use all sources of financial information: final accounts Budgets, Ratio analysis②EmployeesAll employees of a company will be interested in how the business is performing. This will affect their job security, wages and promotion prospects.The purpose of Employees: Employees are generally interested in job security and future salary n egotiations. They will therefore be particularly interested in profitability and the company’s future prospects.The source of Employees: Profit & Loss – profit figures, Balance sheet – net current assets,Cash Flow statement – major inflows/outflows of cash, Profitability ratios③Present ShareholdersThese are the owners of limited companies who have invested in a business by buying ordinary or preference shares.The purpose of Present Shareholders: This group of users is primarily interested in the value of their shares and the return on their investment. They require this information to assess the profitability of the company. Present shareholders will use this information to help decide whether to remain a shareholder in this business or to sell their shares and invest elsewhere.The source of Present Shareholders: Profit & Loss – profit and dividend figures Profitability ratios, Directors report – future plans④Potential ShareholdersThese are individuals or organizations that are considering investing in the company through buying ordinary or preference shares.The purpose of Potential Shareholders: Potential shareholders will be interested in the value of and return on their investment. More specifically, potential shareholders will compare the profitability and future prospects of the company with others to ascertain the best investment option. They use financial information to assess the risk attached to investment.The source of Potential Shareholders: Profit & Loss – profits retained/distributed, Balance sheet –capital structure, Ratio analysis⑤Short-term CreditorsThese are individuals or organizations that lend the company money or goods. This may be in the form of suppliers who sell goods on credit or a finance company giving short-term finance.The purpose of Short-term Creditors: They will be analyzing the liquidity and long-term future of the business to decide the level of finance to be given. Short-term investors use the financial information to evaluate the level of risk and the prospects of the money being repaid.The source of Short-term Creditors: Balance sheet – net current asset figures, Cash Flow statement – major inflows/outflows of cash, Liquidity ratio⑥Long-term CreditorsThese are individuals or organizations that lend the company money on a long-term basis. This may be a finance company lending capital to purchase new fixes assets or a bank giving a long-term loan or debenture.The purpose of Long-term Creditors: Long-term creditors will use the financial information to analyse the liquidity and long-term future of the company to evaluate the level of risk. They also use this information in order to determine if interest payment are likely to be made promptly and if the company can make the capital repayments.The source of Long-term Creditors: Profit & Loss – interest cover, Balance sheet – existing level of debt; Assets value, Cash Flow statement –major inflows/outflows of cash, Ratio analysis –liquidity ratios; Interest cover ratio⑦AuthoritiesThe tax authorities will be interested in the accounts of a company.The purpose of Authorities They will use the accounting information to ensure that the company adheres to all legal requirements. Inland Revenue uses the information to assess the corporation tax payable; Customs and excise uses them to assess V AT liability; CBI and NOS use them to show economic trends, foreign trade figures, employment statistics, etc.The source of Authorities: Profit & Loss –profit/tax figures, Directors report –future plans, employment details⑧CompetitorsCompetitors will be interested in the financial information in order to compare performance.The purpose of Competitors: Competitors will be interested in all areas of the business such as stability, pricing policy and performance. This inform ation may allow them to get a ‘lead’ in the market. Fundamentally competitors will use the information contained within the accounts in order to compare performance.The source of Competitors: Profit & Loss –turnover and expenses pattern, Directors report –future plans, Ratio analysis⑨AnalystsThey will then use this information to prepare reports, advice clients or they may sell their analysis to any interested party.The purpose of Analysts: To assess the performance of the company, identify trends and make comparisons with other companies. The actual purpose of the accounting information will depend on the brief received from the client or the focus of the report. Assessment of the company with a view to recommending investment or disinvestment, etc.The source of Analysts: All published informationOutcome41Source of finance type of finance term of financeBank Overdraft loan capital Short termAmounts falling due within one year loan capital short termAmounts falling due after one year loan capital long termTrade creditors loan capital Short termDebentures loan capital Long termShare capital equity capital Long termTax loan capital Short term Unappropriated profit equity capital Long term2 Bank OverdraftsSSP plc has a bank overdraft of £0 in 2003. The bank overdraft in 2004 is 86,000 which mean the company has more current liabilities than in 2003.A bank overdraft is an agreed sum by which a customer can overdraw their current account.Bank account holders can prearrange with the bank to draw cheques to a greater value than the actual balance in the account. Bank overdrafts are a fairly cheap from of finance with the added advantage of flexibility. In some cases a small overdraft facility may be offered free of charge.TaxThe corporation tax is one of the short-term liabilities of. SSP plc .The figure is not required to be paid until some months into the new financial year. The tax paid in 2003 was £223,000 while £210,000 was paid in 2004.which means that the profit that SSP plc made was decreased.As individuals pay tax on income, companies are requires to pay tax on profit. The current corporation tax rate varies between 10% and 30% depending on the size of business and the amount of profit made.DebenturesSSP plc has £1,560,000 of debentures both in 2003 and in 2004. A debenture is a form of borrowing by a firm. It may issue debentures of a fixed value at a certain rate of interest. Thesedebentures may be bought by individuals or by financial institutions. The debentures will have a fixed time period, after which they will be paid back. This may be 5 or 10 years or in some cases even longer.They are often attractive because they tend to be a secure investment, and because the interest will have to be paid, whatever the level of profit. This makes them less risky than ordinary shares. For, SSP plc they can be a good way of raising money because they are predictable. It can plan ahead the cash requirement for paying the interest, and knows exactly when they will have to be redeemed. This source of finance forms the long term funding of the company and won’t be easily changed in absolute terms from the previous year.Equity fiancéThe shareholders had paid a subscription of £1950, 000 to SSP plc. All profit, after expenses and tax have been paid, belongs to the shareholders of SSP plc. Some of this profit will be distributes to the shareholders by way of a dividend (which is payable at the discretion of directors) and the remainders is retouched in the company to help found continuing operations and expansion Ordinary Shares CapitalOrdinary Shares are the basic type of capital shares issued by the company. Ordinary Shares possess voting rights, participation in dividends, and a residual claim to assets in the event of liquidation.Outcome5IntroductionIn section 5 I will assess the performance of a company by analyzing and interpreting the final accounts. In addition to the final accounts, the trading, profit and loss account and the balance sheet, I will also consider the cash flow statement. This is a statement showing the main inflows and outflows of cash and how the business reached its current cash position.Profitability RatiosUsers of financial statements will be interested in the profit made by a company and then compare it with previous years or with competitors.The absolute profit figure is of little use when analyzing the performance of a company.Instead the relative profit, in proportion to the size of the company and how much capital is invested is more meaningful.Shareholders and potential investors will be most interested in this category of ratios in order to gauge the return on their investmentIncluding Gross profit percentage, net profit percentage and return on capital employed.⑪Gross profit percentage①This ratio is an indication of the level of profit the business has made from buying and selling its stock.②The formula is Gross profit percentage =Gross Profit/ Turnover x 100③SSP plc he gross profit percentage in 2003 was 59.96% and in 2004 the percentage was60.06% which means an increase in the gross profit percentage is a good sign. The positive trend can be an indication that stock control has improved, purchasing policies have improved or demand for the product has increase⑫Net Profit Percentage①This ratio shows how profitable a business is after all expenses have been taken into account. It compares the net profit figure with sales revenue.②The formula is Net Profit Percentage =Net Profit before Tax / Turnover x100③SSP plc has the net profit percentage 10.13% in 2003 and6.73% in 2004 which means a decrease in the net profit percentage is a bad sign as it indicates SSP plc made less profitable, perhaps because sales have decrease, cost of sales has decreased or expenses have increased.⑬Return on Capital Employed①This ratio is used as an indication of the level of return on ordinary share capital. Ordinary shareholders do not receive a fixed level of return on their investment compared to preference shareholders and debenture holders②The formula is Net Profit Before Tax / Ordinary Shareholders Equity x 100③the figure has decrease. This is a bad sign as it indicates that SSP plc made less profitable and ordinary shareholders are likely to receive a lower return on their investment2Liquidity RatiosSometimes known as solvency ratios, liquidity ratios show the ability of the company to repay any loans. Creditors and lenders will use this category of ratios as an indication of acompany’s credit rating.Including Current Ratio (Working Capital Ratio), and the Acid Test Ratio.⑪Current Ratio (Working Capital Ratio)①This shows the ability of the business to pay its short term debts②The formula is Liquidity Ratios=Current Assets: Current Liabilities③Generally speaking a healthy current ratio is at least 2:1. In 2003 the current ratio of SSP plc c is 1.56:1; in 2004 the figure is 1.78:1. Both these two ratio are less than 2:1which indicate the company may be over trading and have difficulty in meeting its short-term debts. ⑫The Acid Test Ratio①This is a more precise (or immedia te) measure of a firm’s liquidity because it does not include closing stock. Stock takes time to convert into cash, therefore it cannot be considered to be liquid. This ratio is considered a better indication of the business’ ability to meet its current liabilities.②The formula is The Acid Test Ratio =liquid assets (current assets-closing stock): current liabilities③Generally speaking a healthy asset test ratio is at least 1:1. In 2003 SSP plc ‘s ratio is0.77:1 In 2004 SSP plc ‘s ratio i0.64:1 both the ratio are less than 1:1, it means that there are serious implications for SSP plc’ s ability to pay its suppliers (creditors).3EfficiencyA company’s performance and profit will be influences by how assets are utilized. Management can use efficiency ratio to identify inefficiencies that require investigation such as under utilization of fixed assets, over stocking or poor invoicing.Including fixed asset turnover, stock turnover debtors collection period and creditors payment period.⑪fixed asset turnover①This ratio ananlyses the relationship between turnover(or sales) and fixed assets, therefore indicating how efficient fixed assets are.②The formula is fixed turnover=turnover/fixed assets.③the ratio in 2003 was2.91 times, and increased to 3.10 times in 2004 of SSP plc. Where this ratio has increased, this is a good sign. If this ratio is moving upwards it indicates that eitherthe existing fixed assets are generating more sales or that investment in new fixed assets has paid off.⑫stock turnover①This shows the number of times in the period the business has replaced its stock. This ratio indicates how fast stock is turnover into sales hence earns a profit for the firm.②The formula is stock turnover=cost of goods sold/ closing stock③.Generally speaking a higher rate of stock turnover is a healthy sign . In 2003 the ratio is7.69 times and6.71 times in 2004, which indicate in 2004 stock is not being re-order as frequently as in 2003 .this may be a negative sign indicating that stock is not being as quickly. However, a higher rate of stock turnover can sometimes be a result of poor stock control. The company may be buying more stock as a result of stock being damaged, lost , stolen or wasted.⑬debetors collection period①the length of the credit period granted to customers is an important factor that determines liquidity. The length of time a debtor takes to pay should be as short as possible.②The formula is debtors collection period =debtors/turnove r×365③The figure in 2003 and 2004 for SSP plc: 9.57 days and 12.33 days. Between 2003 and2004, the number of days taken by debtors to settle has increase by almost 3 days. This isa bad sign as SSP plc’s liquidity benefits from slow payment from customers.⑭creditors payment period①The length of the credit period granted by suppliers also has an important influence on acompany’s liquidity.②The formula is creditors payment period= creditors /cost of goods sold ×365③The figure in 2003 and 2003 for SSP plc are 42.48 days and 27.66 days. The decrease inthe number of days allowed to pay creditors is a bad sign as it means that the money in SSP plc for a shorter time.4Investment RatiosInvestors, lenders and management can use this group of ratios to assess the way in which a company finances its activitiesIncluding Gearing Ratio, Interest Cover, and Debt Ratio.⑪Gearing Ratio①This ratio considers the proportion of ordinary capital compared with other capital②The formula is Gearing Ratio= Fixed Return Capital / Ordinary Share Capital x 100③the figure in 2003 and 2004 are the same 80% this figures too high which indicates that SSP plc has a poor control over how net profit is appropriated.⑫Interest Cover①This ratio shows how capable the company is of covering its interest charges.②The formula is Interest Cover =Profit Before Interest & Tax / Interest Charges③the figure in 2003 and 2004 for SSP plc: 6.05 times and 4.85 times. The decrease this ratio is an unhealthy sign indicating that SSP plc is not so secure in its ability to meet interest charges.⑬Debt Ratio①This is the ratio of a company’s total debts to its total assets.②The formula is Debt Ratio =Total Debts(Current Liabilities + Debentures) / TotalAssets(Fixed Assets + Current Assets) x 100③ A debt ratio in 2003 and 2004 for SSP plc: 44.65% and 40.62%. Both two figures are lessthan 50% and later one is smaller than the former one. This indicates that there were a decrease in debentures and current liabilities and an increase in assets.Section 2①Overall, the cash has decreased by £317,000. The company had cash and bank balances of £281,000 lying idle in 2003 while in 2004 there was no cash in the bank what is more this company overdraft £86,000 from bank.②The company made a profit of £901,000 that after adjustments translated to a cash inflow trading of £1345,000. This is a very healthy inflow of cash.③There was an inflow of £234,000 from interest paid. the net return on investment would have been even greater if there were received. This is an unavoidable payment but could be reduced in future by issuing ordinary shares instead of debentures. Alternatively, the company could seek to get a lower interest rate.④there was also an outflow of £234,000 for tax. This is a significant outflow as it is based on profit.⑤The next outflow on the cash flow statement was £984,000 paid for purchase of fixed assets. This was a significant outflow and is the main factor contributing to the overall decrease in cash. During this period, the company embarked on a major stadium expansion and renovation programme that is hoped to generate more cash in the future. Unfortunately, the new stadium was not fully utilized as demonstrated by the fixed asset turnover.⑥Ordinary share dividend paid was £260,000.This is equivalent to 19% of cash flow from operating activities and is therefore a reasonable amount.⑦there were not payments into and withdrawals from short-term investments⑧there were not financial activities to raise capital⑨The main factor causing the decrease in cash was the purchase of fixed assets and equity, dividend paid.⑩SSP plc should pay attention to the cash flow problem and control the cash outflows. The directors propose to restrict the dividends this year to retain profit for expansion.The expansion of the company needs a lot of capital SSP plc could ease the financial problem by giving credit reasonable. In addition, SSP pc should use short term financial resources reasonable to replace purchasing more fixed assets.ConclusionA range of ratios should be calculated during the section. Then those ratios calculations can be used to assess the performance of a company. What’s more, a company’s future development can be recommended through the cash flow statement. From these ratios analysis above, it can bee seen that however the stock control and purchasing policies have improved, SSP plc made less profit in 2004 which may due to the increased expenses and cost. What is more, SSP plc had difficult in meeting its short term debts, interest charges and current liabilities.Appendix2003 2004 ProfitabilityGross Profit Ratio 7,000/11,674×100=59.96% 8,037/13,382×100=60.06% Net Profit Percentage 1,182/11,674×100=10.13% 901/13,382×100=6.73% Return on CE 1,182/2,885×100=40.197% 901/3,305×100=27.26% LiquidityCurrent Ratio 1,195:767=1.56:1 1,248: 701=1.78:1The acid test ratio (1,195-608):767=1.56:1 (1248-796):701=0.64:1 EfficiencyFixed asset turnover 11,674/4017=2.91 times 117,382/4,318=3.10times Stock turnover 4,674/ 608=7.69 weeks 5345/796=6.71weeks Debtor CP 306/11674×365=9.57times 452/13382×365=12.33days Creditor PP 544/4674×365=42.48days 405/5345×365=27.66days Investment RatiosGearing Ratio 1560/1950×100=80% 1560/1950×100=80% Interest Cover 11146/234=6.05times 1135/234=4.85timesDebtor ratio (767+1560)/(4017+1195) ×100=44.65% (701+1560)/(4138+1248)=40.62%。

HND SQA 财政预算outcome3 答案