SE lecture 8(20120418)

visual basic 2012 大学教程(第8章)

8. FilesConsciousness ... does not appear to itself chopped up in bits. ... A “river”or a “stream” are the metaphors by which it is most naturally described.—William JamesI can only assume that a “Do Not File” document is filed in a “Do NotFile” file.—Senator Frank Church, Senate Intelligence Subcommittee Hearing, 1975ObjectivesIn this chapter you’ll learn:• To use file processing to implement a business app.• To create, write to and read from files.• To become familia r with sequential-access file processing.• To use classes StreamWriter and StreamReader to write text to and read textfrom files.• To organize GUI commands in menus.• To manage resources with Using statements and the Finally block of a Trystatement.Outline8.1 Introduction8.2 Data Hierarchy8.3 Files and Streams8.4 Test-Driving the Credit Inquiry App8.5 Writing Data Sequentially to a Text File8.5.1 Class CreateAccounts8.5.2 Opening the File8.5.3 Managing Resources with the Using Statement8.5.4 Adding an Account to the File8.5.5 Closing the File and Terminating the App8.6 Building Menus with the Windows Forms Designer8.7Credit Inquiry App: Reading Data Sequentially from a Text File8.7.1 Implementing the Credit Inquiry App8.7.2 Selecting the File to Process8.7.3 Specifying the Type of Records to Display8.7.4 Displaying the Records8.8 Wrap-UpSummary | Terminology | Self-Review Exercises | Answers to Self-Review Exercises | Exercises8.1. IntroductionVariables and arrays offer only temporary storage of data in memory—the data is lost, for example, when a local variable ―goes out of scope‖ or when the app terminates. By contrast, files (and databases, which we cover in Chapter 12) are used for long-term retention of large (and often vast) amounts of data, even after the app that created the data terminates, so data maintained in files is often called persistent data. Computers store files on secondary storage devices, such as magnetic disks, optical disks (like CDs, DVDs and Bluray Discs™), USB flash drives and magnet ic tapes. In this chapter, we explain how to create, write to and read from data files. We continue our treatment of GUIs, explaining how to organize commands in menus and showing how to use the Windows Forms Designer to rapidly create menus. We also discuss resource management—as apps execute, they often acquire resources, such as memory and files, that need to be returned to the system so they can be reused at a later point. We show how to ensure that resources are properly returned to the system when the y’re no longer needed.8.2. Data HierarchyUltimately, all data items that computers process are reduced to combinations of 0s and 1s. This occurs because it’s simple and economical to build electronic devices that can assume two stable states—one represents 0 and the other represents 1. It’s remarkable that the impressive functions performed by computers involve only the most fundamental manipulations of 0s and 1s!BitsThe smallest data item that computers support is called a bit, short for ―binary digit‖—a digit that can assume either the value 0 or the value 1. Computer circuitry performs various simple bit manipulations, such as examining the value of a bit, setting the value of a bit and reversing a bit (from 1 to 0 or from 0 to 1). For more information on the binary number system, see Appendix C, Number Systems.CharactersProgramming with data in the low-level form of bits is cumbersome. It’s preferable to program with data in forms such as decimal digits (that is, 0, 1, 2, 3, 4, 5, 6, 7, 8 and 9), letters (that is, the uppercase letters A–Z and the lowercase letters a–z) and special symbols (that is, $, @, %, &, *, (, ), -, +, ", :, ?, / and many others). Digits, letters and special symbols are referred to as characters. The set of all characters used to write programs and represent data items on a particular computer is called that computer’s character set. Because computers process only 0s and 1s, every character in a computer’s character set is represented as a pattern of 0s and 1s. Bytes are composed of eight bits. Visual Basic uses the Unicode character set, in which each character is typically composed of two bytes (and hence 16 bits). You create programs and data items with characters; computers manipulate and process these characters as patterns of bits. FieldsJust as characters are composed of bits, fields are composed of characters. A field is a group of characters that conveys meaning. For example, a field consisting of uppercase and lowercase letters can represent a person’s name.Data HierarchyData items processed by computers form a data hierarchy (Fig. 8.1), in which data items become larger and more complex in structure as we progress up the hierarchy from bits to characters to fields to larger data aggregates.Fig. 8.1. Data hierarchy (assuming that files are organized into records). RecordsTypically, a record is composed of several related fields. In a payroll system, for example, a record for a particular employee might include the following fields:1. Employee identification number2. Name3. Address4. Hourly pay rate5. Number of exemptions claimed6. Year-to-date earnings7. Amount of taxes withheldIn the preceding example, each field is associated with the same employee. A data file can be implemented as a group of related records.1A company’s payroll file normally contains one record for each employee. Companies typically have many files, some containing millions, billions or even trillions of characters of information.1. In some operating systems, a file is viewed as nothing more than a collection ofbytes, and any organization of the bytes in a file (such as organizing the data into records) is a view created by the programmer.To facilitate the retrieval of specific records from a file, at least one field in each record can be chosen as a record key, which identifies a record as belonging to a particular person or entity and distinguishes that record from all others. For example, in a payroll record, the employee identification number normally would be the record key. Sequential FilesThere are many ways to organize records in a file. A common organization is called a sequential file in which records typically are stored in order by a record-key field. In a payroll file, records usually are placed in order by employee identification number. DatabasesMost businesses use many different files to store data. For example, a company might have payroll files, accounts receivable files (listing money due from clients), accounts payable files (listing money due to suppliers), inventory files (listing facts about all the items handled by the business) and many other files. Related files often are stored in a database. A collection of programs designed to create and manage databases is called a database management system (DBMS). You’ll learn about databases in Chapter 12 and you’ll do additional work with databases in Chapter 13, Web App Development with , and online Chapters 24–25.8.3. Files and StreamsVisual Basic views a file simply as a sequential stream of bytes (Fig. 8.2). Depending on the operating system, each file ends either with an end-of-file marker or at a specific byte number that’s recorded in a system-maintained administrative data structure for the file. You open a file from a Visual Basic app by creating an object that enables communication between an app and a particular file, such as an object of class StreamWriter to write text to a file or an object of class StreamReader to read text from a file.Fig. 8.2. Visual Basic’s view of an n-byte file.8.4. Test-Driving the Credit Inquiry AppA credit manager would like you to implement a Credit Inquiry app that enables the credit manager to separately search for and display account information for customers with• debit balances—customers who owe the company money for previously received goods and services• credit balances—customers to whom the company owes money• zero balances—customers who do not owe the company moneyThe app reads records from a text file then displays the contents of each record that matches the type selected by the credit manager, whom we shall refer to from this point forward simply as ―the user.‖Opening the FileWhen the user initially executes the Credit Inquiry app, the Button s at the bottom of the window are disabled (Fig. 8.3(a))—the user cannot interact with them until a file has been selected. The company could have several files containing account data, so to begin processing a file of accounts, the user selects Open...from the app’s custom File menu (Fig. 8.3(b)), which you’ll create in Section 8.6. This displays an Open dialog (Fig.8.3(c)) that allows the user to specify the name and location of the file from which the records will be read. In our case, we stored the file in the folder C:\DataFiles and named the file Accounts.txt. The left side of the dialog allows the user to locate the file on disk. The user can then select the file in the right side of the dialog and click the Open Button to submit the file name to the app. The File menu also provides an Exit menu item that allows the user to terminate the app.a) Initial GUI with Buttons disabled until the user selects a file from which to readrecordsb) Selecting the Open... menu item from the File menu displays the Open dialog inpart (c)c) The Open dialog allows the user to specify the location and name of the fileFig. 8.3. GUI for the Credit Inquiry app.Displaying Accounts with Debit, Credit and Zero BalancesAfter selecting a file name, the user can click one of the Button s at the bottom of the window to display the records that match the specified account type. Figure 8.4(a) shows the accounts with debit balances. Figure 8.4(b) shows the accounts with credit balances. Figure 8.4(c) shows the accounts with zero balances.a) Clicking the Debit Balances Button displays the accounts with positive balances(that is, the people who owe the company money)b) Clicking the Credit Balances Button displays the accounts with negative balances(that is, the people to whom the company owes money)c) Clicking the Zero Balances Button displays the accounts with zero balances (that is, the people who do not have a balance because they’ve already paid or have nothad any recent transactions)Fig.8.4. GUI for Credit Inquiry app.8.5. Writing Data Sequentially to a Text FileBefore we can implement the Credit Inquiry app, we must create the file from which that app will read records. Our first app builds the sequential file containing the account information for the company’s clients. For each client, the app obtains through its GUI the c lient’s account number, first name, last name and balance—the amount of money that the client owes to the company for previously purchased goods and services. The data obtained for each client constitutes a ―record‖ for that client. In this app, the accoun t number is used as the record key—files are often maintained in order by their record keys. For simplicity, this app assumes that the user enters records in account number order.GUI for the Create Accounts AppThe GUI for the Create Accounts app is shown in Fig. 8.5. This app introduces the Menu-Strip control which enables you to place a menu bar in your window. It alsointroduces ToolStripMenuItem controls which are used to create menus and menu items. We show how use the IDE to build the menu and menu items in Section 8.6. There you’ll see that the menu and menu item variable names are generated by the IDE and begin with capital letters. Like other controls, you can change the variable names in theProperties window by modifying the (Name) property.Fig. 8.5. GUI for the Create Accounts app.Interacting with the Create Accounts AppWhen the user initially executes this app, the Close menu item, the TextBox es and the Add Account Button are disabled (Fig. 8.6(a))—the user can interact with these controls only after specifying the file into which the records will be saved. To begin creating a fileof accounts, the user selects File > New... (Fig. 8.6(b)), which displays a Save As dialog (Fig. 8.6(c)) that allows the user to specify the name and location of the file into which the records will be placed. The File menu provides two other menu items—Close to close the file so the user can create another file and Exit to terminate the app. After the user specifies a file name, the app opens the file and enables the controls, so the user can begin entering account information. Figure 8.6(d)–(h) shows the sample data being entered for five accounts. The app does not depict how the records are stored in the file. This is a text file, so after you close the app, you can open the file in any text editor to see its contents. Figure 8.6(j)shows the file’s contents in Notepad.a) Initial GUI before user selects a fileb) Selecting New... to create a filec) Save As dialog displayed when user selects New... from the File menu. In this case,the user is naming the file Accounts.txt and placing the file in the C:\DataFilesfolder.d) Creating account 100e) Creating account 200f) Creating account 300g) Creating account 400h) Creating account 500i) Closing the filej) The Accounts.txt file open in Notepad to show how the records were written to the file. Note the comma separators between the data itemsFig. 8.6. User creating a text file of account information.8.5.1. Class CreateAccountsLet’s now study the declaration of class CreateAccounts, which begins in Fig. 8.7. Framework Class Library classes are grouped by functionality into namespaces, which make it easier for you to find the classes needed to perform particular tasks. Line 3 is an Imports statement, which indicates that we’re using classes from the System.IO namespace. This namespace contains stream classes such as StreamWriter (for text output) and Stream-Reader (for text input). Line 6 declares fileWriter as an instance variable of type Stream-Writer. We’ll use this variable to interact with the file that the user selects.Click here to view code image1' Fig. 8.7: CreateAccounts.vb2' App that creates a text file of account information.3Imports System.IO ' using classes from this namespace45Public Class CreateAccounts6Dim fileWriter As StreamWriter' writes data to text file7Fig. 8.7. App that creates a text file of account information.You must import System.IO before you can use the namespace’s classes. In fact, all namespaces except System must be imported into a program to use the classes in those namespaces. Namespace System is imported by default into every program. Classes like String, Convert and Math that we’ve used frequently in earlier examples are declared in the System namespace. So far, we have not used Imports statements in any of our programs, but we have used many classes from namespaces that must be imported. For example, all of the GUI controls you’ve used so far are classes in theSystem.Windows.Forms namespace.So why were we able to compile those programs? When you create a project, each Visual Basic project type automatically imports several namespaces that are commonlyused with that project type. You can see the namespaces (Fig. 8.8) that were automatically imported into your project by right clicking the project’s name in the Solution Explorer window, selecting Properties from the menu and clicking the References tab. The list appears under Imported namespaces:—each namespace with a checkmark is automatically imported into the project. This app is a Windows Forms app. The System.IO namespace is not imported by default. To import a namespace, you can either use an Imports statement (as in line 3 of Fig. 8.7) or you can scroll through the list in Fig. 8.8 and check the checkbox for the namespace you wish to import.Fig. 8.8. Viewing the namespaces that are pre-Imported into a Windows Forms app.8.5.2. Opening the FileWhen the user selects File > New..., method NewToolStripMenuItem_Click (Fig. 8.9) is called to handle the New... m enu item’s Click event. This method opens the file. First, line 12 calls method CloseFile (Fig. 8.11, lines 102–111) in case the user previously opened another file during the current execution of the app. CloseFile closes the file associated with this app’s StreamWriter.Click here to view code image8' create a new file in which accounts can be stored9Private Sub NewToolStripMenuItem_Click(sender As Object,10 e As EventArgs) Handles NewToolStripMenuItem.Click1112 CloseFile() ' ensure that any prior file is closed13Dim result As DialogResult' stores result of Save dialog14Dim fileName As String' name of file to save data1516' display dialog so user can choose the name of the file to save17Using fileChooser As New SaveFileDialog()18 result = fileChooser.ShowDialog()19 fileName = fileChooser.FileName ' get specified file name20End Using' automatic call to fileChooser.Dispose() occurs here2122' if user did not click Cancel23If result <> Windows.Forms.DialogResult.Cancel Then24Try25' open or create file for writing26 fileWriter = New StreamWriter(fileName, True)2728' enable controls29 CloseToolStripMenuItem.Enabled = True30 addAccountButton.Enabled = True31 accountNumberTextBox.Enabled = True32 firstNameTextBox.Enabled = True33 lastNameTextBox.Enabled = True34 balanceTextBox.Enabled = True35Catch ex As IOException36 MessageBox.Show("Error Opening File", "Error",37MessageBoxButtons.OK, MessageBoxIcon.Error)38End Try39End If40End Sub' NewToolStripMenuItem_Click41Fig. 8.9. Using the SaveFileDialog to allow the user to select the file into whichrecords will be written.Next, lines 17–20 of Fig. 8.9 display the Save As dialog and get the file name specified by the user. First, line 17 creates the SaveFileDialog object (namespace System.Windows.Forms) named fileChooser. Line 18 calls its ShowDialog method to display the SaveFileDialog (Fig. 8.6(c)). This dialog prevents the user from interacting with any other window in the app until the user closes it by clicking either Save or Cancel, so it’s a modal dialog. The user selects the location where the file should be stored and specifies the file name, then clicks Save. Method ShowDialog returns a DialogResult enumeration constant specifying which button (Save or Cancel) the user clicked to close the dialog. This is assigned to the DialogResult variable result (line 18). Line 19 uses SaveFileDialog property FileName to obtain the location and name of the file.8.5.3. Managing Resources with the Using StatementLines 17–20 introduce the Using statement, which simplifies writing code in which you obtain, use and release a resource. In this case, the resource is a SaveFileDialog. Windows and dialogs are limited system resources that occupy memory and should be returned to the system (to free up that memory) as soon as they’re no longer needed. Inall our previous apps, this happens when the app terminates. In a long-running app, if resources are not returned to the system when they’re no longer needed, a resource leak occurs and the resources are not available for use in this or other apps. Objects that represent such resources typically provide a Dispose method that must be called to return the resources to the system. The Using statement in lines 17–20 creates a SaveFileDialog object, uses it in lines 18–19, then automatically calls its Dispose method to release the object’s resources as soon as End Using is reached, thusguaranteeing that the resources are returned to the system and the memory they occupy is freed up (even if an exception occurs).Line 23 tests whether the user clicked Cancel by comparing result to the constant Windows.Forms.DialogResult.Cancel. If not, line 26 creates a StreamWriter object that we’ll use to write data to the file. The two arguments are a String representing the location and name of the file, and a Boolean indicating what to do if the file already exists. If the file doesn’t exist, this statement creates the file. If the file does exist, the second argument (True) indicates that new data written to the file should be appended at the end of the file’s current contents. If the second argument is False and the file already exists, the file’s contents will be discarded and new data will be written starting at the beginning of the file. Lines 29–34 enable the Close menu item and the TextBox es and Button that are used to enter records into the app. Lines 35–37 catch an IOException if there’s a problem opening the file. If so, the app displays an error message. If no exception occurs, the file is opened for writing. Most file-processing operations have the potential to throw exceptions, so such operations are typically placed in Try statements.8.5.4. Adding an Account to the FileAfter typing information in each TextBox, the user clicks the Add Account Button, which calls method addAccountButton_Click (Fig. 8.10) to save the data into the file. If the user entered a valid account number (that is, an integer greater than zero), lines 56–59 write the record to the file by invoking the StreamWriter’s WriteLine method, which writes a sequence of characters to the file and positions the output cursor to the beginning of the next line in the file. We separate each field in the record with a comma in this example (this is known as a comma-delimited text file), and we place each record on its own line in the file. If an IOException occurs when attempting to write the record to the file, lines 64–66 Catch the exception and display an appropriate message to the user. Similarly, if the user entered invalid data in the accountNumberTextBox or balanceTextBox lines 67–69 catch the FormatExceptions thrown by class Convert’s methods and display an appropriate error message. Lines 73–77 clear the TextBox es and return the focus to the accountNumberTextBox so the user can enter the next record. Click here to view code image42' add an account to the file43Private Sub addAccountButton_Click(sender As Object,44 e As EventArgs) Handles addAccountButton.Click4546' determine whether TextBox account field is empty47If accountNumberTextBox.Text <> String.Empty Then48' try to store record to file49Try50' get account number51Dim accountNumber As Integer =52 Convert.ToInt32(accountNumberTextBox.Text)5354If accountNumber > 0Then' valid account number?55' write record data to file separating fields by commas56 fileWriter.WriteLine(accountNumber & "," &57 firstNameTextBox.Text & "," &58 lastNameTextBox.Text & "," &59 Convert.ToDecimal(balanceTextBox.Text))60Else61 MessageBox.Show("Invalid Account Number", "Error",62MessageBoxButtons.OK, MessageBoxIcon.Error)63End If64Catch ex As IOException65 MessageBox.Show("Error Writing to File", "Error",66MessageBoxButtons.OK, MessageBoxIcon.Error)67Catch ex As FormatException68 MessageBox.Show("Invalid account number or balance",69"Format Error", MessageBoxButtons.OK,MessageBoxIcon.Error)70End Try71End If7273 accountNumberTextBox.Clear()74 firstNameTextBox.Clear()75 lastNameTextBox.Clear()76 balanceTextBox.Clear()77 accountNumberTextBox.Focus()78End Sub' addAccountButton_Click79Fig. 8.10. Writing an account record to the file.8.5.5. Closing the File and Terminating the AppWhen the user selects File > Close, method CloseToolStripMenuItem_Click (Fig. 8.11, lines 81–91) calls method CloseFile (lines 102–111) to close the file. Then lines 85–90 disable the controls that should not be available when a file is not open.Click here to view code image80' close the currently open file and disable controls81Private Sub CloseToolStripMenuItem_Click(sender As Object,82 e As EventArgs) Handles CloseToolStripMenuItem.Click8384 CloseFile() ' close currently open file85 CloseToolStripMenuItem.Enabled = False86 addAccountButton.Enabled = False87 accountNumberTextBox.Enabled = False88 firstNameTextBox.Enabled = False89 lastNameTextBox.Enabled = False90 balanceTextBox.Enabled = False91End Sub' CloseToolStripMenuItem_Click9293' exit the app94Private Sub ExitToolStripMenuItem_Click(sender As Object,95 e As EventArgs) Handles ExitToolStripMenuItem.Click9697 CloseFile() ' close the file before terminating app98 Application.Exit() ' terminate the app99End Sub' ExitToolStripMenuItem_Click100101' close the file102Sub CloseFile()103If fileWriter IsNot Nothing Then104Try105 fileWriter.Close() ' close StreamWriter106Catch ex As IOException107 MessageBox.Show("Error closing file", "Error",108MessageBoxButtons.OK, MessageBoxIcon.Error)109End Try110End If111End Sub' CloseFile112End Class' CreateAccountsFig. 8.11. Closing the file and terminating the app.When the user clicks the Exit menu item, method ExitToolStripMenuItem_Click (lines 94–99) respo nds to the menu item’s Click event by exiting the app. Line 97 closes the StreamWriter and the associated file, then line 98 terminates the app. The call to method Close (line 105) is located in a Try block. Method Close throws an IOExceptionif the file cannot be closed properly. In this case, it’s important to notify the user that the information in the file or stream might be corrupted.8.6. Building Menus with the Windows Forms DesignerIn the test-drive of the Credit Inquiry app (Section 8.4) and in the overview of the Create Accounts app (Section 8.5), we demonstrated how menus provide a convenient way to organize the commands that you use to interact with an app without ―cluttering‖ its user interface. Menus contain groups of related commands. When a command is selected, the app performs a specific action (for example, select a file to open, exit the app, etc.).Menus make it simple and straightforward to locate an app’s commands. They can also make it easier for users to use apps. For example, many apps provide a File menu that contains an Exit menu item to terminate the app. If this menu item is always placed in the File menu, then users become accustomed to going to the File menu to terminate an app. When they use a new app and it has a File menu, they’ll already be familiar with the location of the Exit command.The menu that contains a menu ite m is that menu item’s parent menu. In the Create Accounts app, File is the parent menu that contains three menu items—Ne w..., Close and Exit.Adding a MenuStrip to the FormBefore you can place a menu on your app, you must provide a MenuStrip to organize and manage the app’s menus. Double click the MenuStrip control in the Toolbox. This creates a menu bar (the MenuStrip) across the top of the Form (below the title bar; Fig.8.12) and places a MenuStrip icon in the component tray (the gray area) at the bottom of the designer. You can access the MenuStrip’s properties in the Properties window by clicking the MenuStrip icon in the component tray. We set the MenuStrip’s (Name) property to applicationMenuStrip.。

lecture的意思用法大全

lecture的意思用法大全lecture的意思n. 演讲,训斥,教训vi. 作演讲vt. 给…作演讲,教训(通常是长篇大论的)变形:过去式: lectured; 现在分词:lecturing; 过去分词:lectured;lecture用法lecture可以用作名词lecture主要指教育性或学术性“演讲”,引申可指“冗长的训斥或谴责”。

lecture是可数名词,其后接介词on或about ,意为“关于…的演讲”“就…做演讲”“因…训斥或谴责某人”。

lecture作“讲演,讲课”解时,是不及物动词。

说“讲授某课程”时常与介词on连用,说“在某地讲演”时常与介词at〔in〕连用。

lecture用作名词的用法例句She ran over her notes before giving the lecture.她讲课前把讲稿匆匆看了一遍。

His lecture covered various aspects of language.他的讲课涉及到语言诸方面的问题。

They could not follow the lecture.他们听不懂这次演讲。

lecture可以用作动词lecture作“讲演,讲课”解时,是不及物动词。

说“讲授某课程”时常与介词on连用,说“在某地讲演”时常与介词at〔in〕连用。

lecture也可用作及物动词,意思是“向…讲演,给…讲课”,接名词或代词作宾语。

lecture还可作“责备”“教训”“训斥”解,用作及物动词,接名词或代词作宾语。

“因…而受到训斥”可说lecture sb for n./v -ing。

lecture用作动词的用法例句It was a shame for me to be lectured in front of the whole class.当着整个班级的面被训斥了一顿,真让我感到羞辱。

He lectured to his students on modern writers.他给学生们讲了关于现代作家的一课。

2012年英语专业八级真题解析

专八 2012 - 1 1

classified as "observation with intervention" or "observation without intervention". Observation with inter vention can be made in at least two ways, [ 11]participant observation and field experiment. In participant observation, observers, that is researchers, play a dual role: They observe people's behaviour and they par ticipate actively in the situation they are observing. If individuals who are being (!bserved lmow that the ob server is present to collect information about their behaviour, this is undisguised participant observation. But in disguised participant observation, those who are being observed do not lmow that they are being ob served.

托福听力tpo67全套对话讲座原文+题目+答案+译文

托福听力tpo67全套对话讲座原文+题目+答案+译文Section1 (1)Conversation1 (2)原文 (2)题目 (4)答案 (6)译文 (6)Lecture1 (8)原文 (8)题目 (10)答案 (12)译文 (13)Lecture2 (14)原文 (14)题目 (16)答案 (18)译文 (19)Section2 (20)Conversation2 (20)原文 (20)题目 (23)答案 (25)译文 (25)Lecture3 (27)原文 (27)题目 (29)答案 (31)译文 (32)Section1Conversation1原文Student:Hi.I know it's Friday afternoon and all,but this is kind of an emergency.Supervisor:Oh,what kind of emergency?Exactly?Student:Well,I mean,there's no danger or anything.It's like a personal emergency. It's about my apartment.Supervisor:Well,I really only deal with dormitories.The apartment facilities, supervisors,offices,next door room,208ask for Jim.Student:I just came from there.They sent me to you.It's a problem with my stove.Supervisor:And they sent you here.All right.Now,what's the problem?Student:My stove isn't working at all.It won't even turn on.Supervisor:It's electric?Student:Yes.Supervisor:Okay,our electrician is out today,his daughter is getting married tomorrow.So realistically he probably won't get to it until Monday afternoon. Perhaps Tuesday.Student:Really,we have to go without a stove for a whole weekend,possibly more?Supervisor:Yes,as you pointed out,this is not a dire emergency,so it's going to be handled under the normal maintenance schedule,which is Monday through Friday.And I know for a fact that Monday is already pretty tight,the electrician will have a lot to catch up on.So when I say possibly Tuesday,I'm just trying to be realistic.Student:But I really rely on that stove.I don't have any kind of on campus dining arrangement or contract.Supervisor:Well,I understand,but…Student:And it's not even the whole problem.I'm expecting a bunch of people to show up tomorrow night.I'm going to be hosting a meeting of the editorial staff of the school paper.And a dinner was scheduled.Supervisor:Now I see which you meant by a personal emergency,but all I can really do is put in a work request.I'm sorry.Student:I just got finished shopping for all the food for the meeting.Ah.I guess,I'll just have to call it off.Supervisor:Why would you cancel the meeting?Student:Well,I mean,I could do it next week.Supervisor:Couldn't you like use a neighbour or something?Student:I don't think so.I mean,the only neighbors I really know,well enough to ask the guys next door,if you saw the state of that kitchen,you'd understand.I'm not sure I could find the stove under all the mess.Supervisor:I see.Well,we could try to set you up in one of our conference rooms in the Johnson building.Student:Really?I thought that student groups couldn't book the rooms in Johnson.Supervisor:Well,normally they can't.However,given your situation,I can try to putin a word with some people and see if we can make an exception here.There is also a full kitchen in the Johnson building,so you'd be covered there.Student:Okay.Yes.That definitely would work.Um.Do you have any idea when you know if you can make this happen or not?Because I'll need to let people know.Supervisor:Yeah,I understand people need to know what's going on.Um.Let me get back to you in an hour or so on this.Can you leave me your phone number?Student:Sure.Thanks.题目1.Why does the woman go to see the facilities supervisor?A.To find out where there is a stove that she can useB.To complain about her treatment in another facilities officeC.To ask if a meeting can be moved to another locationD.To schedule repairs for a broken appliance2.Why does the woman believe that her problem is a serious one?[Click on2 answers.]A.She does not have an on-campus option for meals.B.She is concerned that the stove could be dangerous.C.She knows that other students have had similar problems.D.She was relying on using the stove for an upcoming event.3.What will the woman probably do next?A.Request an emergency repair for her stoveB.Prepare a meal that does not need to be cookedC.Move her event to a different locationD.Reschedule her event to the following week4.What does the woman imply about her next-door neighbors?A.Their kitchen is too dirty for her to use.B.Their stove is not functioning properly.C.They do not let other people use their stove.D.They will be using their kitchen this weekend.5.What can be inferred about the supervisor when he says this:Student:I just got finished shopping for all the food for the meeting.Ah.I guess,I'll just have to call it off.Supervisor:Why would you cancel the meeting?Student:Well,I mean,I could do it next week.A.He feels sorry for the woman.B.He believes that the woman's plan of action is not necessary.C.He wants to know the reason for the woman's decision.D.He wants the woman to confirm her plan.答案D AD C A B译文1.学生:嗨。

托福听力tpo39 全套对话讲座原文+题目+答案+译文

托福听力tpo39全套对话讲座原文+题目+答案+译文Section1 (2)Conversation1 (2)原文 (2)题目 (4)答案 (5)译文 (5)Lecture1 (7)原文 (7)题目 (9)答案 (11)译文 (11)Lecture2 (13)原文 (13)题目 (16)答案 (17)译文 (18)Section2 (20)Conversation2 (20)原文 (20)题目 (22)答案 (23)译文 (23)Lecture3 (25)原文 (25)题目 (27)答案 (29)译文 (29)Lecture4 (30)原文 (30)题目 (33)答案 (34)译文 (35)Section1Conversation1原文NARRATOR:Listen to a conversation between a student and a theater professor.MALE STUDENT:Hi,Professor Jones.FEMALE PROFESSOR:Hey,didn't I see you at the performance of Crimes of the Heart last night?MALE STUDENT:Yeah…actually my roommate had a small part in it.FEMALE PROFESSOR:Really?I was impressed with the performance—there sure are some talented people here!What did you think?MALE STUDENT:You know,Beth Henley's an OK playwright;she's written some decent stuff,but it was a little too traditional,a little too ordinary…especially considering the research I’m doing.FEMALE PROFESSOR:Oh,what’s that?MALE STUDENT:On the Polish theater director Jerzy Grotowski.FEMALE PROFESSOR:Grotowski,yeah,that's a little out of the mainstream…pretty experimental.MALE STUDENT:That’s what I wanted to talk to you about.I had a question about our essay and presentation.FEMALE PROFESSOR:OK…MALE STUDENT:Yeah,some of these ideas,uh,Grotowski's ideas,are really hard to understand—they're very abstract,philosophical—and,well,I thought the class would get more out of it if I acted out some of it to demonstrate.FEMALE PROFESSOR:Interesting idea…and what happens to the essay?MALE STUDENT:Well,I'll do the best I can with that,but supplement it with the performance—you know,bring it to life.FEMALE PROFESSOR:All right,but what exactly are we talking about here?Grotowski, as I'm sure you know,had several phases in his career.MALE STUDENT:Right.Well,I’m mainly interested in his idea from the late1960s…Poor theater,you know,a reaction against a lot of props,lights,fancy costumes,and all that…so,it’d be good for the classroom.I wouldn’t need anything special.FEMALE PROFESSOR:Yes.I’m sure a lot of your classmates are unfamiliar with Grotowski—this would be good for them.MALE STUDENT:Right,and this leads…I think there's overlap between his Poor theater phase and another phase of his,when he was concerned with the relationship between performers and the audience.I also want to read more and write about that.FEMALE PROFESSOR:You know,I saw a performance several years ago…it really threw me for a loop.You know,you're used to just watching a play,sitting back…but this performance,borrowing Grotowski's principles,was really confrontational—a little uncomfortable.The actors looked right in our eyes,even moved us around, involved us in the action.MALE STUDENT:Yeah,I hope I can do the same when I perform for the class.I'm a bit worried,since the acting is so physical,that there's so much physical preparation involved.FEMALE PROFESSOR:Well,some actors spend their whole lives working on this…so don't expect to get very far in a few weeks…but I'm sure you can bring a couple of points across.And,if you need some extra class time,let me know.MALE STUDENT:No,I think I can fit it into the regular time for the presentation.FEMALE PROFESSOR:OK.I think this'll provide for some good discussion about these ideas,and other aspects of the audience and their relationship to theatricalproductions.题目1.What are the speakers mainly discussing?A.A play by Grotowski that was discussed in class.B.A proposal that the student has for an assignment.C.A play that is currently being performed at the university.D.The main phases in Grotowski's career as a director.2.What does the student imply when he talks about the play he recently attended?A.He attended the play because he is writing an essay on it.B.He wished the play were more experimental.C.He thought his roommate showed great talent.D.He was not familiar with the author of the play.3.What are two characteristics of Grotowski's theater that the speakers mention?[Click on2answers.]A.The minimal equipment on the stage in his productions.B.The single stories that his plays are based on.C.The elaborate costumes the actors wear in his plays.D.The actions of the performers in his plays.4.Why does the professor mention a play she attended several years ago?A.To compare it to the play she saw the previous evening.B.To suggest that Grotowski's principles do not necessarily lead to effective theater.C.To show how different it was from Poor theater.D.To provide an example of one of the ideas the student wants to research.5.What does the professor imply about the acting the student wants to do?A.Audiences are no longer surprised by that type of acting.B.The acting requires less physical preparation than he thinks.C.He will not be able to master that style of acting easily.D.He should spend less time acting for the class and more time on class discussion.答案B B AD D C译文旁白:请听一段学生和戏剧学教授之间的对话。

lecture 8

R R R

R

R

R

one phase inversion Möbius topology, 4 e, allowed

zero inversions Hückel topology, 4 e, forbidden

but not

In transition states, it is much easier to get to a Möbius topology. For example, dienes are known to close to cyclobutanes. We can draw arrows for this process:

R

However, the curly arrows don't give any guidance for whether the R groups end up syn or anti to each other. In fact, they end up syn. How did that happen?

R R

6. Finally, decide how many -electrons are involved. Here, there are four. As stated earlier: Aromatic (allowed) Hückel Topology Möbius Topology 4n+2 4n Anti-aromatic (not allowed) 4n 4n+2

Scope of Lecture Dewar-Zimmerman model endiandric acids the endo rule the frontier MO perspective pericyclic reactions I electrocyclizations

Contents COURSE STAFF......................................................................

Faculty of EngineeringSchool of Computer Science and EngineeringCOMP4511User Interface Design andConstructionSession 1, 2008ContentsCOURSE STAFF (2)COURSE DETAILS (2)TIMES (2)COURSE AIMS (2)LEARNING OUTCOMES (4)RATIONALE (4)TEACHING STRATEGIES (4)ASSESSMENT (5)ACADEMIC HONESTY AND PLAGIARISM (6)COURSE SCHEDULE (7)RESOURCES FOR STUDENTS (7)COURSE EVALUATION AND DEVELOPMENT (8)OTHER MATTERS (8)Course staff•Daniel Woo, Lecturer in Chargeo Room 307-K17o9385 6495o danielw@.au•Outside of consultation times e-mail Daniel directly or locate on-line course content via .au/~cs4511Course details• 6 units of credit (UoC)•Pre- and co-requisiteso COMP3511/9511 Human Computer Interaction (User centred design) (pre-requisite)o COMP4001 Object-Oriented Software Development (C++, UML) (co-requisite)•The course is currently run as a 4th year elective.•Postgraduate students are permitted to undertake this course under the undergraduate course code. Postgraduate students are assigned an additional assignment exercise to write a technical paper on a topic relevant to user interface software developmentTimes•Lectures: Monday 11:00am-1:00pm, Wed 10:00-11:00am•Studio: Thursday 3:00-6:00pmCourse aims•Extend paper-based user-centred design techniques introduced in COMP3511/9511 and object-oriented design concepts introduced in COMP4001•Provide practical object-oriented software development skills specifically for graphical user interfaces•Understand the design and programming constraints user interfaces•Provide experience in usability testing of software applicationsLearning outcomes•Write applications in the Objective-C programming language•Design and implement graphical user interface (GUI) software•Write two user interface software applications as part of assignment work to first gain confidence in developing GUI applications and then to develop your skills with more complex behaviour •Understand the role design patterns in user interface software, notably the model view controller and state design patterns•Understand concepts such as event handling and views•Develop graphical user interface software with features that support copy, paste, undo, menus and responding to mouse and keyboard actions•Conduct peer usability evaluations of software developed in this course•Describe aspects of your software using object oriented techniques such as Unified Markup Language (UML)•Become competent with version control systems to maintain source code and other project related documents•Work collaboratively in a multidisciplinary environmentRationale•COMP4511 is a highly practical course that introduces you to the programming aspects of user interface software. We do not assume that you have developed such an application before but require that you feel competent in object-oriented principles and programming techniques •Usability evaluation is a key component in the software design lifecycle, so the designs that you develop in this course will be evaluated by your peers. This provides feedback to help improve your design and gives you further experience to evaluate software systems.•We build on the user centred design principles introduced in COMP3511 expecting that you will conduct user interviews to better understand requirements, develop paper or electronic prototypes of your design and conduct usability walkthroughs of your designs preferably before you write code (but we understand that this is possibly the first time that you have engaged in this process). •One of your assignment tasks will be to develop an interactive application in the domain that is of interest to you. We believe that by helping you create something that you are passionate about then your desire to excel and learn far outweighs completing a project for which you have no interest.•The lecture and studio are conducted in the CHI Lab (G11-K17) so that you have the tools and technologies immediately in front of you during class. This allows us experiment with the material whilst we are learning, addressing practical issues as they arise.•Video streaming content will be used to provide on-line course material. The Moodle class web site will host an on-line forum. We are very interested to better understand user/student needs for on-line course delivery•Based on the feedback we have had from both former students and some of their employers, the students who successfully completed this course have a balanced view of the software development process: they care about user needs, they can carry out the user centred design process, they understand the rigour and technical demands of software engineering, and they have applied knowledge in the area of usability evaluation•We train software aware students to be more than just programmersTeaching strategies•The CHI lab will be available for access to Mac based computers for self study programming exercises, conducting usability tests and hold team design meetings•Thursday 3-6pm is reserved for “studio” where we conduct workshop exercises that are focussed on usability, in-class design or coding exercises. Tutors and the lecturer will be available to discuss and review your progress•Thursday 3-4pm will be also be used for small group or individual consultation to review progress and assigned checkpoints•Additional lecture material will be provided on-line using streaming multimedia to cover design topics and more in-depth programming topics•The Moodle site will be used to conduct on-line discussion.•The overall format of the lectures and studios provide opportunity for feedback and discussionAssessmentThe exact assignment topics are still subject to change given that we are investigating collaboration with the school of industrial design and possibly working with a commercial organisation as a possible “client” that will help focus the work around a theme. Typically we would allow you to choose your own topic. This will be discussed in classes in Week 1.•Assignment 1: Introductory User Interface Involving Timeo Code Due Week 5, Fridayo15 %o Assessment will be based on Software Design, Code Implementation, User Interface Design, Version Control, Paper Prototyping, User Interviewso There will be other deliverables in studio to demonstrate progress•Assignment 2: Part 1 Design and Prototyping of an Interactive Applicationo Code Due Week 8, Thursday 2pmo15 %o Assessment will be based on Project Planning, User Centred Design, Paper Prototyping, Software Design, Code Prototyping, Version Control and UsabilityEvaluationso There will be other deliverables in studio to demonstrate progress•Assignment 2: Part 2 Implementation and Evaluation of an Interactive Applicationo Code Due Week 11, Thursday 2pmo25 %o Assessment will be based on Iterative Improvements, Additional Features, Code Implementations, Version Control, Usability Evaluations and Final Poster Presentation o There will be other deliverables in studio to demonstrate progress•Participation (Undergraduate)o5%o Studio Participationo Design Diary useo Reflection on Progress in Journal•Paper (Postgraduate)o5%o Research Paper on a topic related to interaction design and user centred designo Participation will be recorded•Final Examinationo40%o Written examination•Assignment 1 is an introductory assignment that allows you to learn about the Objective C language and develop a basic graphical user interface application that can respond to simple events generated by timers•Assignment 2 is in two parts and is designed to be your major project for the course. You may choose to develop an application that is interactive and supports the concept of direct manipulation. This will involve responding to mouse and keyboard events and drawing to the screen using the graphics functionality available in Cocoa. Examples could be a drawing application, a furniture layout application or a file system / Finder replacement.•Assignment source code is not explicitly submitted but will utilise the version control system (subversion) used in the course. On the due date, your assignment repository will be copied and the tagged branch will be copied and used as the assessable work. Written design reports should also be kept in the repository with any other non-electronic submissions handed in to class on the due date.•Assignment code will be kept in the repository trunk. Submissions will use a tagged branch.Documentation relating to the assignments will be kept in the repository and/or the on-line trac/wiki system (which is different from Moodle).•All electronic work submitted will be retained by the University of New South Wales and can be used for teaching, research and review purposes. We will acknowledge your contribution if you wish, or withhold your name should you choose to remain anonymous.•You also have the right to use your electronic submissions for your own personal use. You must retain any copyright notices contained in other code used in your submissions so the origin of the source is retained (eg. From class examples).•Any data provided as part of assignments (eg. Test data sets) may not be used for commercial purposes and must not be provided in any form to any other party.Academic honesty and plagiarismWhat is Plagiarism?Plagiarism is the presentation of the thoughts or work of another as one’s own.* Examples include:•direct duplication of the thoughts or work of another, including by copying material, ideas or concepts from a book, article, report or other written document (whether published orunpublished), composition, artwork, design, drawing, circuitry, computer program or software, web site, Internet, other electronic resource, or another person’s assignment without appropriateacknowledgement;•paraphrasing another person’s work with very minor changes keeping the meaning, form and/or progression of ideas of the original;•piecing together sections of the work of others into a new whole;•presenting an assessment item as independent work when it has been produced in whole or part in collusion with other people, for example, another student or a tutor; and•claiming credit for a proportion a work contributed to a group assessment item that is greater than that actually contributed.†For the purposes of this policy, submitting an assessment item that has already been submitted for academic credit elsewhere may be considered plagiarism.Knowingly permitting your work to be copied by another student may also be considered to be plagiarism.Note that an assessment item produced in oral, not written, form, or involving live presentation, may similarly contain plagiarised material.The inclusion of the thoughts or work of another with attribution appropriate to the academic discipline does not amount to plagiarism.The Learning Centre website is main repository for resources for staff and students on plagiarism and academic honesty. These resources can be located via:.au/plagiarismThe Learning Centre also provides substantial educational written materials, workshops, and tutorials to aid students, for example, in:•correct referencing practices;•paraphrasing, summarising, essay writing, and time management;•appropriate use of, and attribution for, a range of materials including text, images, formulae and concepts.Individual assistance is available on request from The Learning Centre.Students are also reminded that careful time management is an important part of study and one of the identified causes of plagiarism is poor time management. Students should allow sufficient time for research, drafting, and the proper referencing of sources in preparing all assessment items.* Based on that proposed to the University of Newcastle by the St James Ethics Centre. Used with kind permission from the University of Newcastle† Adapted with kind permission from the University of Melbourne.Course scheduleSubject to changesLectures Studio Assignment Deliverables Week 0Week 1 Course IntroductionGoal Directed DesignIntroduction Obj-CMemoryFoundation Classes Object Oriented Design Interface Builder Actions and Outlets Assignment 1 DesignWeek 2 Contacts ExampleModel View ControllerTablesTimers Coding StyleDebuggingVersion ControlAssignment 1 DesignA1 Concept DocumentMid Semester BreakWeek 3 ControlsArchivingMenusToolbarsDialogs Unit Testing Usability TestingWeek 4 User Centred DesignProcess Assignment 1Usability EvaluationA1 OO Design BriefWeek 5 ViewsDrawingEventsA1 Presentation A1 Code DueWeek 6 Graphics ApplicationBehaviour and Form A1 ReviewA2 ConceptsA2 Project PlanWeek 7 Graphics ApplicationState Design PatternA2 Walkthroughs A2 Concept DocumentWeek 8 Graphics ApplicationCopy / Paste / UndoNIB and Window ControllersA2 Usability Evaluations A2 Code Part 1 DueWeek 9 Interaction Details A2 Usability EvaluationsWeek 10 Document ArchitectureUser PreferencesA2 Usability Evaluations A2 Usability ReportWeek 11 Interaction Design Topics A2 Usability Evaluations A2 Code Part 2 Due Week 12 Project/UCD Reflection A2 Presentations A2 Final ReportResources for studentsRequired Text Books•Cooper, Reimann and Cronin (2007), About Face 3: The Essentials of Interaction Design, John Wiley•Hillegrass (2004), Cocoa Programming for Mac OS X (2nd Ed), Addison WesleyReferences from COMP3511/9511 or COMP4001•Preece, Rogers, Sharp (2007), Interaction Design Beyond Human Computer Interaction, John Wiley & Sons Inc.•Nielsen (1993), Usability Engineering, Morgan Kaufmann.•Gamma, Helm, Johnson and Vlissides (1995), Design Patterns: Elements of Reusable Object-Oriented Software, Addison-Wesley.Other References•Apple Computer Inc. (2001), Learning Cocoa, O’Reilly and Associates Inc.•Garfunkel and Mahoney (2002), Building Cocoa Applications, O’Reilly and Associates Inc. •Kochran, SG (2004), Programming in Objective-C, Sams Publishing•Students seeking resources can also obtain assistance from the UNSW Library. One starting point for assistance is:.au/web/services/services.htmlOther Materials•Design Diary A4 or A3 bound sketchpad for design work. This will be assessed during Studio consultation.•Post-it Notes™, coloured pens and pencils will be used as part of the design work. Please use only Blu-Tack™ for placing posters on walls. Do not use sticky or masking tape.Course evaluation and development•We will use both paper-based and electronic survey tools throughout the session to gather feedback about the course. This is used to assess the quality of the course in order to make on going improvements. We do take this feedback seriously and approach the design of this course using the user centred design philosophies.Other matters•Students are expected to attend all classes•Please review the official school policies available at .au/~studentoffice/policies/yellowform.html. It contains important information regarding use of laboratories, originality of assignment submissions and special consideration. Note that in order to receive a CSE login account you must have agreed to the conditions stated in that document.•The Yellow Form also states the supplementary assessment policy and outlines what to do in case illness or misadventure that affects your assessment, and supplementary examinations procedures within the School of Computer Science and Engineering•Please read and understand the School Policy in relation to laboratory conduct.•Note that no food or drink is permitted in the laboratory. CSE fines will apply.•The laboratory is to be secured at all times. No equipment or furniture can be removed from the laboratory.•You are not permitted to provide unauthorised access to this laboratory.•UNSW Occupational Health and Safety policies and expectations.au/ohs/ohs.shtml•Computer Ergonomics for Students.au/ergonomics/ergoadjust.html•OHS Responsibility and Accountability for Students.au/ergonomics/ohs.html•Students who have a disability are encouraged to discuss their study needs with the course convener prior to, or at the commencement of the course, or with the Equity Officer (Disability) in the Equity and Diversity Unit (9385 4734). Information for students with disabilities is available at: .au/disabil.htmlIssues to be discussed may include access to materials, signers or note-takers, the provision of services and additional examination and assessment arrangements. Early notification is essential to enable any necessary adjustments to be made. Information on designing courses and course outlines that take into account the needs of students with disabilities can be found at:.au/acboardcom/minutes/coe/disabilityguidelines.pdf。

lecture 08

9-6

1

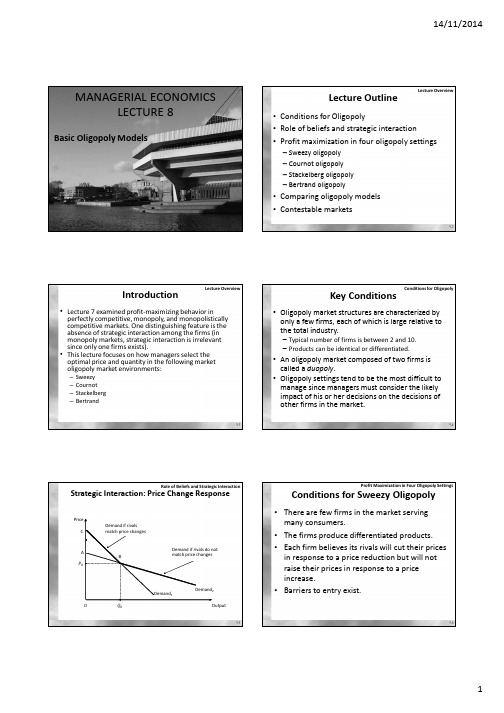

14/11/2014

Price A ܲ

0

Profit Maximization in Four Oligopoly Settings

Sweezy Oligopoly

Sweezy Demand B

C

E MR

ܳ

F MR2

MC0

MC1 Demand1 (rival holds price constant) MR1 Demand2 (rival matches price change)

and cost functions, ܥଵ ܳଵ ൌ ܿଵܳଵ and

ܥଶ ܳଶ ൌ ܿଶܳଶ the reactions functions are:

ܳଵ ൌ ݎଵ ܳଶ

=

ܽ

െ ܿଵ ʹܾ

−

1 2

ܳଶ

ܳଶ ൌ ݎଶ ܳଵ

=

ܽ

െ ܿଶ ʹܾ

−

1 2

ܳଵ

9-10

Profit Maximization in Four Oligopoly Settings

14/11/2014

MANAGERIAL ECONOMICS LECTURE 8

Basic Oligopoly Models

Lecture Outline

Lecture8

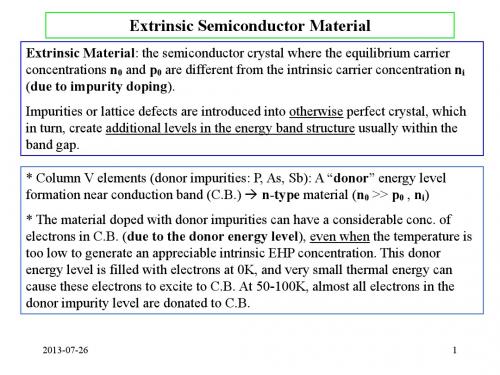

- Amphoteric impurities (Si, Ge) in III-V compound (in GaAs) :

- Si or Ge (column IV impurities) can serve as donors or acceptors, depending on whether they occupy the column III or column V sublattice of the crystal.

In III-V Compounds (in GaAs) :

- Column VI impurities (S, Se, Te) occupying column V sites (As) serve as donors, and column II impurities (Be, Zn, Cd) occupying column III serve as acceptors.

2013-07-26

4

Electrons and Holes in Quantum Wells

1. Single-valued (discrete) energy levels in the band gap arising from doping (donor/acceptor energy level)

•This acceptor level is empty of electrons at 0K, and very small thermal energy can excite the electrons from V.B. to acceptor level. At 50-100K, almost all empty sites in the acceptor impurity level are filled with the electrons, leaving behind holes in V.B.

、幅度调制(PDF)

DSB-SC 的波形特征:当()m t 为负时,()s t 的包络被翻了过来(图4.2.2)DSB-SC 的频谱特征:和AM 一样,都是双边带,带宽是基带的2倍,但没有载频线谱(假设()m t 不含直流)。

见图4.2.3。

标准调幅AM 和DSB-SC 都属于DSB 。

不过缺省情况下,我们说的DSB 指DSB-SC 。

四 SSBDSB 的两个边带是对称的,已知其中一个边带,等于已知两个边带。

因此,发送DSB 的时候,如果我们用滤波器切去一个边带,收端也应该有办法复原出DSB 或者()m t 。

这样的设计叫SSB 。

对于上单边带调制,()USB s t 的频谱是 ()DSB s t 频谱的上边带,其复包络()USB s t %就是()m t 的正频率部分,也即()USB s t %就是()m t 的解析信号,即()()()ˆUSB s t m t jm t =+%()()()ˆcos 2sin 2USB c c s t m t f t m t f t ππ=−显然,通过相干解调就可以解出 ()m t 。

对于下单边带,同理可得()()()ˆcos 2sin 2LSB c c s t m t f t m t f t ππ=+总之就是()()()ˆcos 2sin 2USB c c c s t A m t f t m t f t ππ= µ这个表达式说明,()SSB s t是由两个载波互相正交的DSB 构成的,后一个DSB 所起的作用就是为了抵消前一个DSB 中的一个边带。

这个结构显示出SSB 也可以用两个DSB 调制来实现(图4.2.13),这种实现方式叫正交调制法,而图4.2.11的方法叫滤波法。

另外,SSB 也可以这样解调:插入大载波来包络检波()()ˆcos 2cos 2sin 2USB c c c c c s A f t A A m t f t A m t f t πππ+=+ µ。

MSE_SE-Guidelines-2012

GUIDELINES FOR M.S.E. DEGREE IN CIVIL ENGINEERING:CONCENTRATION IN STRUCTURAL ENGINEERING1GeneralAn applicant for the M.S.E. degree must present the equivalent of an undergraduate civil engineering program as preparation. If the applicant’s undergraduate degree is not in civil engineering, then some undergraduate prerequisite courses may be required. See the CEE Department Guidelines for additional information.CourseworkA student pursuing a M.S.E. degree in Structural Engineering must complete at least 30 credit hours of acceptable graduate work. (This usually corresponds to 10 courses.) A thesis is not required. In satisfying the credit hour requirement, the following requirements must be satisfied:∙At least 15 of the credit hours must be in Civil and Environmental Engineering (CEE) courses.∙At least 12 credit hours must correspond to courses within the Structures concentration area. Acceptable courses are listed below. However, no more than 21 credit hours from the courses listed below can be counted toward the MSE degree. Among the 12 credit hours required, at least 3 should be at the 600 level.CEE 510Finite Element Methods CEE 518Fiber-Reinforced Cement CompositesCEE 511Dynamics of Structures CEE 611Earthquake EngineeringCEE 512Theory of Structures CEE 613Metal Structural MembersCEE 513Plastic Analysis and Design of Frames CEE 614Advanced Prestressed ConcreteCEE 514Prestressed Concrete CEE 615Reinforced Concrete MembersCEE 515Advanced Design of R/C Structures CEE 617Random VibrationsCEE 516Bridge Structures CEE 619Adv. Struct. Dynamics and Smart Structures CEE 517Reliability of Structures CEE 910Structural Engineering ResearchCEE 519High-Perfor. Struct. Materials and Systems∙In addition to the minimum 12 credit hours of Structures courses, a student must complete 2 credit hours of the CEE 812 Structural Engineering Graduate Seminar. No more than 2 credit hours of CEE 812 will count towards the degree.∙ A student must satisfactorily complete at least two graduate level courses (cognate courses), with a minimum of 2 credit hours each, in a department other than Civil and Environmental Engineering. Cognate courses must be passed with a B- or better (see Rackham BULLETIN for more information). One of these cognate courses must be an advanced mathematics course. The list of courses on page 2 can be used as a guide to satisfy the cognate course requirement. Courses other than those listed should be approved by the student’s academic advisor in advance.Courses cross-listed with CEE courses do not qualify as cognates.∙No more than 6 credit hours of directed studies, seminars or research can be counted toward the 30-credit requirement. This covers credit hours received for CEE 910 and CEE 950.∙No more than 12 credit hours at the 400 level are acceptable. Of these 12 hours, a maximum of 9 hours can be in CEE courses. Structural engineering courses at the 400 level are not accepted for graduate credit unless approved in advance by the MSE graduate advisor in structural engineering.∙SGUS students are permitted to double count up to 9 credit hours, including CEE 413 and 415. However, students who double count 413 and 415 must take at least 3 structural engineering courses at the 500 level.∙ A maximum of 6 graduate level semester hours (with a grade of B or better) can be transferred from other institutions approved by Rackham.GradesThe grading system used for graduate studies is based on the following 9-point scale:A+ = 9; A = 8; A- = 7; B+ = 6; B = 5; B- = 4; C+ = 3; C = 2; C- = 1A minimum cumulative graduate grade point average (GPA) of 5 on this 9-point scale is required for all graduate courses taken for credit and applied toward the Master’s Degree.1 For additional information on M.S.E. degree requirements, see the Graduate Student Handbook (prepared by the Horace H. Rackham School of Graduate Studies) and the CEE Department Guidelines. The Graduate Student Handbook is available on the World Wide Web at /.To be considered for a master’s degree diploma, a student must submit a formal application to the Office of Graduate Academic Records of the Graduate School. The deadline for the Graduate School to receive the degree application form is four weeks after the first day of classes in a full term and one week after the first day of classes in a half term. These dates can usually be found on the Rackham Graduate School web site (/). Acceptable Cognate Courses for M.S.E. in Structural EngineeringShown below is a partial list of courses that can be used to satisfy the advanced math cognate course requirement for the CEE Department's M.S.E. degrees. In general, the math course should have a prerequisite of Math 215 or equivalent. Math 404 Intermediate Differential EquationsMath 412 Introduction to Modern Algebra BioStat 553 Applied BiostatisticsMath 416 Theory of AlgorithmsMath 417 Matrix Algebra IMath 419 Linear Spaces and Matrix TheoryIOE 510 Linear ProgrammingMath 433 Intro. to Differential GeometryMath 450 Adv. Math for Engineers IMath 451 Adv. Calculus IMath 454 Boundary Value Prob. for PDEMath 462 Mathematical ModelsMath 471 Intro. to Numerical MethodsMath 5XX Any 500 level math courseShown below is a partial list of courses that may be used to satisfy the second cognate course requirement for the CEE Department's M.S.E. degrees.ME 400 Mechanical Engineering Analysis Aero 416 Plates and ShellsME 401 Statistical Quality Control and Design Aero 513 Solid and Structural Mechanics IME 412 Advanced Strength of Materials Aero 514 Solid and Structural Mechanics IIME 515 Contact Mechanics Aero 516 Mechanics of CompositesME 501 Analytical Methods in Mechanics Aero 518 Theory of Elastic Stability IME 502 Methods of Diff. Eqns. In Mechanics Aero 565 Optimal Structural DesignME 511 Theory of Solid Continua Aero 611 Advanced Finite ElementsME 519 Theory of Plasticity IME 543 Analytical and Comp. Dynamics I MSE 514 Composite MaterialsME 555 Design OptimizationME 558 Discrete Design OptimizationME 563 Time Series ModelingME 564 Linear Systems TheoryME 605 Adv. Finite Element Methods in Mech.ME 619 Theory of Plasticity IIThere are many other courses in engineering, math, science, and architecture/urban planning that may satisfy the requirements for the non-math cognate course. (A cognate course must not be cross-listed with a CEE course, must be at the 400 level or higher, must be related to the field of specialization, and must be listed in the Rackham Bulletin. Cognate courses must be passed with a B- or better to count towards the degree.) Such courses must be approved for cognate credit in advance by the student’s academic advisor. Courses outside of engineering, math, science, and architecture/urban planning are generally not acceptable as cognate courses. Except as listed above, generally 400 level courses are not acceptable.Examples of courses accepted in the past: UP 538, UP 594, UP 565The checklist below can be used to monitor your progress toward your M.S.E. degree.Requirement Description CourseNumberCourse Description Credits Transfer1 Cognate–Math2 Cognate3 CEE(Concentration Area) 4 CEE(Concentration Area) 5 CEE(Concentration Area) 6 CEE(Concentration Area)600 level7 CEE8 OpenChoice9 OpenChoice10 NOT Structures andNOT Cognate11 CEE812(Graduate seminar) ExtraExtra。

NF EN 10028-1 - janv 2001 - Produits plats en acier pour appareils a pression - prescriptions genera