中级会计双语Chap007

中级财务会计(双语)第7章

Your site here

LOGO

Bond--HTM

Case study 2

● Purchased Masterwear Industries’ 12%, 3-

year (from July 1, 2011 to June 30, 2014) bonds for $666,633. The face amount was $700,000. Interest is payable semiannually on June 30 and December 31. The market rate is 14%. (Suppose it’s a HTM)

当公司取得一项投资而这项投资既不是以投机为目的进行经常性的买卖也不将持有至到期时公司把这项投资归为可供出售的证券

LOGO

Chapter 7 Investments

Investment classification

The investor lacks significant influence over the investee: 投资方对被投资方缺乏重大影响

C. Recognizing “unrealized gains and losses” No entry.

Your site here

LOGO

Bond--HTM

Case study 2

D. Selling the investment On June 30, 2014: (On the maturity date) Dr. Cash 42,000 Discount on bond investment 6,544 Cr. Investment revenue 48,544 Dr. Cash 700,000 Cr. Investment in bond 700,000

中级会计(英文)chap003

$ 221,392 $ 6,537 699,906 755,747 1,255,298 1,120,855 1,072,920 1,007,887 3,249,516 2,891,026 1,900,119 1,776,253 455,591 344,613 1,834,366 1,729,976 7,439,592 6,741,868

Liabilities are probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities as a result of past transactions or events.

Slide 3-7

FedEx Corporation Balance Sheet 31-May 2001 Liabilities: Current liabilities: Current portion of long-term debt Accrued salaries & employee benefits Accounts payable Accrued expenses Total current liabilities Long-term debt, less current portion Deferred income taxes Other liabilities Total liabilities 2000

Slide 3-6

Assets

Noncurrent Assets

Investments and Funds Property, Plant, & Equipment Intangibles Other

中级会计职称财务管理各章节考点.docx

中级会计职称财务管理各章节考点1 .财务管理目标:-各个观点的优缺点需要掌握,如股东财富最大化、利益相关者价值最大化等。

2 .财务管理体制:•集权和分权的区分,如集中式和分散式财务管理体制的特点。

3 .财务管理环境:-重点关注金融环境,如利率、汇率、通货膨胀等对财务管理的影响。

1 .时间价值系数之间的关系:-普通年金现值系数与资本回收系数、普通年金终值系数与偿债基金系数、预付年金现值系数与普通年金现值系数等之间的关系。

2 .风险管理:-两种证券组合的预期收益率、组合风险、相关系数与组合风险之间的关系。

3 .资本资产定价模型:•必要收益率的计算、证券市场线的含义、证券市场线中斜率的含义。

4 .成本性态分析:-约束性固定成本与酌量性固定成本的区分、技术变动成本和酌量性固定成本的区分、半变动成本、半固定成本等的区分。

1 .预算编制方法:-各种预算编制方法的优缺点,如增量预算法、零基预算法等。

2 .主要预算的编制:-各种预算编制的表述,如销售预算、生产预算、采购预算等。

3 .预算的分类与预算体系:-按内容不同的分类和按预算指标覆盖的时间长短的分类、预算体系中各种预算的逻辑关系。

4 .现金预算的编制:-可供使用的现金、现金支出和现金余缺。

5 .财务报表预算编制的依据。

1 .权益筹资方式的种类及特点:-三种股权筹资方式(如发行普通股、优先股等)各自的优缺点。

2 .无形资产出资方式:-《公司法》对无形资产出资方式另有限制,股东或者发起人不得以哪些无形资产出资。

3 .债务筹资方式的种类与特点:-三种长期负债资金筹集方式(如发行公司债券等)的特点,以及与股权筹资相比的优缺点。

1 .资金需要量预测:•因素分析法、销售百分比法等预测方法。

2 .资本成本:-资本资产定价模型的应用、公司价值分析法以及不同行业适用的资本结构。

3 .杠杆效应:-经营杠杆系数和财务杠杆系数的计算、企业不同发展时期的资本结构情况。

4 .衍生工具筹资:-可转换债券和认股权各自的筹资特点。

中级会计学英文课件 (7)

5. Dividends and interest receivable.

Chapter 7-10

LO 3 Define receivables and identify the different types of receivables.

Recognition of Accounts Receivables

Presentation and analysis

What is Cash?

Cash

Most liquid asset Standard medium of exchange

Basis for measuring and accounting for all items

Current asset Examples: coin, currency, available funds on deposit at the bank, money orders, certified checks, cashier’s checks, personal checks, bank drafts and savings accounts.

Trade Discounts

Reductions from the list price Not recognized in the accounting records Customers are billed net of discounts

10 % Discount for new Retail Store Customers

Cash and Receivables

Cash

What is cash?

Management and control of cash Reporting cash Summary of cashrelated items

中级会计双语Chap007解读

• • •

7-5

All disbursements, except petty cash, made by check.

Separate responsibilities for cash disbursement documents, check authorization, check signing, and record keeping.

To avoid misstating the financial statements, sales revenue and accounts receivable should be reduced by the amount of returns in the period of sale if the amount of returns is anticipated to be material.

• Bank overdrafts may be offset against other cash accounts.

7-7

Accounts Receivable

Result from the credit sales of goods or services to customers.

Are classified as current assets.

Enhances the reliability and accuracy of accounting data

7-4

Internal Control Procedures

Cash Receipts • Separate responsibilities for receiving cash, recording cash transactions, and reconciling cash balances. • Match the amount of cash received with the amount of cash deposited. • Close supervision of cash-handling and cash-recording activities. Cash Disbursements

双语中级会计第七章

LOGO

Repurchase the stocks

One 备抵账户: Treasury stock

+

-

LOGO

Retire the stocks 注销股票

If repurchase price>par value 当回购价>面值 时 , debit the ―common stock‖ and ―additional contributed capital‖, credit the ―treasury stock‖, then record the remaining amount as ―retained earnings‖. If repurchase price<par value 当回购价<面值 时 , debit the ―common stock‖, credit the ―treasury stock‖, then record the remaining amount as ―additional contributed capital‖.

LOGO

Repurchase the stocks 回购股票

When the company buys back stocks, both cash and shareholders’ equity are decreased, then the company becomes smaller 当公司回 购股票时,现金和股东权益均减少,公司规模即缩小. Exp. Alta Vena Company buys back 2,000 shares of its own common stocks for $9,000. (which it had originally sold for $8,000) Dr. Treasury stock 9,000 Cr. Cash 9,000 Shares repurchased and not retired are referred to as treasury stock 被回购而未被注销 的股票被称为“库存股”.

Chap007会计学基础

Provides information for reconciling journal entries.

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2005

GENERAL JOURNAL

Da te

Account Titles and Explanation

May 5 Cash

Cash Over and Short

De bit 10

Cre dit 10

Cash Over and Short is debited for shortages and credited for overages.

Prepare a cash budget. Prepare a control listing of cash receipts. Require daily deposits. Make all payments by check. Verify every expenditure before payment. Promptly reconcile bank statements.

stockholders.

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2005

7-13

Internal Control Over Cash

Segregate authorization, custody and recording of cash.

McGraw-Hill/Irwin

© The McGraw-Hill Companies, Inc., 2005

中级财务会计英文课程授课教案

中级财务会计英文课程授课教案第一章:财务会计基础1.1 教学目标了解财务会计的基本概念、目的和重要性掌握会计要素、会计等式和会计原则熟悉会计术语和会计记录的基本方法1.2 教学内容财务会计的定义和作用会计要素:资产、负债、所有者权益、收入、费用会计等式:资产= 负债+ 所有者权益会计原则:会计基础、会计周期假设、货币计量原则、历史成本原则会计记录方法:日记账、总账、明细账1.3 教学活动引入财务会计的实例,引导学生思考财务会计的重要性通过PPT展示和讲解会计要素、会计等式和会计原则练习会计记录方法,让学生动手操作1.4 作业与评估要求学生完成课后习题,巩固所学内容评估学生的理解程度,检查会计等式的应用第二章:会计记录和账务处理2.1 教学目标掌握会计记录的方法和技巧学会使用会计软件进行账务处理理解会计分录和会计账簿的关系2.2 教学内容会计记录的方法:手工会计记录和会计软件会计分录的编制:借贷记账法会计账簿的设置和登记:日记账、总账、明细账会计软件的使用:会计软件的功能和操作2.3 教学活动讲解会计记录的方法和技巧,展示会计软件的操作界面通过案例分析,让学生练习编制会计分录和登记账簿引导学生使用会计软件进行账务处理2.4 作业与评估要求学生完成课后习题,巩固会计记录和账务处理的知识评估学生的操作能力,检查会计分录和账簿的登记第三章:财务报表的编制3.1 教学目标了解财务报表的种类和作用学会编制资产负债表、利润表和现金流量表掌握财务报表编制的步骤和方法3.2 教学内容财务报表的种类:资产负债表、利润表、现金流量表、所有者权益变动表财务报表编制的步骤:收集数据、编制试算平衡表、编制财务报表资产负债表的编制:资产、负债和所有者权益的分类和计算利润表的编制:收入、费用和利润的计算现金流量表的编制:现金流入和现金流出的计算3.3 教学活动讲解财务报表的种类和作用,展示财务报表的编制过程通过案例分析,让学生练习编制资产负债表、利润表和现金流量表引导学生理解财务报表编制的步骤和方法3.4 作业与评估要求学生完成课后习题,巩固财务报表编制的知识评估学生的理解程度,检查财务报表的编制质量第四章:财务分析与评价4.1 教学目标掌握财务分析的基本方法和指标学会使用财务比率进行企业评价4.2 教学内容财务分析的方法:比较分析法、比率分析法、趋势分析法财务比率的种类:偿债能力比率、运营能力比率、盈利能力比率、成长能力比率财务分析报告的编制:报告格式和内容的规范4.3 教学活动讲解财务分析的方法和指标,展示财务比率的计算和分析过程通过案例分析,让学生练习计算和分析财务比率4.4 作业与评估要求学生完成课后习题,巩固财务分析和评价的知识评估学生的分析能力,检查财务分析报告的质量第五章:国际财务报告准则(IFRS)5.1 教学目标了解国际财务报告准则(IFRS)的背景和重要性掌握IFRS的基本原则和会计政策学会应用IFRS进行财务报告的编制和分析5.2 教学内容IFRS的背景和目的:国际会计准则委员会(IASC)的成立、全球会计标准的趋同IFRS的基本原则:公平呈现、一致性、可比性、实质重于形式IFRS会计政策的选择和应用:固定资产的折旧、无形资产的摊销第六章:财务报告的翻译与解读6.1 教学目标理解财务报告翻译的重要性学会将财务报告中的专业术语翻译成中文掌握财务报告解读的技巧6.2 教学内容财务报告翻译的原则和方法:准确性、忠实原文、符合中文表达习惯财务报告中的专业术语:资产、负债、所有者权益、收入、费用等财务报告解读的步骤:了解企业背景、分析财务指标、评估企业财务状况6.3 教学活动讲解财务报告翻译的原则和方法,让学生练习翻译财务报告术语通过案例分析,让学生解读财务报告,评估企业财务状况引导学生运用翻译技巧,提高财务报告解读能力6.4 作业与评估要求学生完成课后习题,巩固财务报告翻译和解读的知识评估学生的翻译和解读能力,检查翻译和解读的准确性第七章:公司合并与合并财务报表7.1 教学目标理解公司合并的概念和类型掌握合并财务报表的编制方法学会分析公司合并对财务报表的影响7.2 教学内容公司合并的类型:横向合并、纵向合并、多元化合并合并财务报表的原则:统一会计政策、公平呈现、一致性合并财务报表的编制步骤:合并资产负债表、合并利润表、合并现金流量表7.3 教学活动讲解公司合并的类型和合并财务报表的原则,展示合并财务报表的编制过程通过案例分析,让学生练习编制合并财务报表引导学生理解公司合并对财务报表的影响7.4 作业与评估要求学生完成课后习题,巩固公司合并和合并财务报表的知识评估学生的理解程度,检查合并财务报表的编制质量第八章:审计与财务报告的可靠性8.1 教学目标理解审计的概念和目的掌握审计过程和审计方法学会评估财务报告的可靠性8.2 教学内容审计的概念和目的:独立验证财务报告的真实性和公正性审计过程:计划审计、实施审计、完成审计、审计报告审计方法:检查、观察、询问、分析8.3 教学活动讲解审计的概念和目的,展示审计过程和审计方法引导学生评估财务报告的可靠性8.4 作业与评估要求学生完成课后习题,巩固审计和财务报告可靠性的知识第九章:税务会计与财务报告9.1 教学目标理解税务会计的概念和作用掌握税收法律法规和税收计算学会将税务会计信息纳入财务报告9.2 教学内容税务会计的概念和作用:遵守税收法律法规,合理避税税收法律法规:税种、税率、税收优惠政策税收计算:所得税、增值税、个人所得税等9.3 教学活动讲解税务会计的概念和作用,展示税收法律法规和税收计算方法通过案例分析,让学生练习税收计算和税务会计的处理引导学生将税务会计信息纳入财务报告9.4 作业与评估要求学生完成课后习题,巩固税务会计和财务报告的知识评估学生的计算能力,检查税务会计处理的准确性第十章:财务报告的伦理与道德10.1 教学目标理解财务报告伦理的重要性学会识别和处理财务报告中的伦理问题提高财务报告编制和解读的道德水平10.2 教学内容财务报告伦理的原则:真实性、公正性、透明度财务报告中的伦理问题:虚假报告、利益冲突、信息安全财务报告伦理的实践:企业内部控制、审计监管、职业道德10.3 教学活动讲解财务报告伦理的原则和伦理问题,引导学生思考和实践财务报告伦理通过案例分析,让学生了解财务报告伦理的实践和职业道德的要求引导学生提高财务报告编制和解读的道德水平10.4 作业与评估要求学生完成课后习题,巩固财务报告伦理和道德的知识评估学生的理解程度,检查财务报告伦理实践的规范性重点和难点解析1. 会计记录和账务处理(第二章):会计记录的方法和技巧,以及会计软件的使用是学生需要重点掌握的内容。

中级财务会计英文版.课后答案(chap2)word精品文档15页

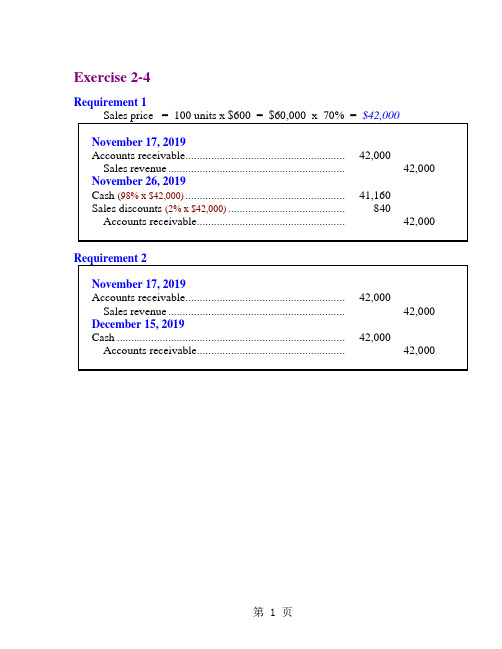

Exercise 2-4 Requirement 1Exercise 7-4 (concluded)Requirement 3Exercise 2-7Requirement 1Estimated returns = 4% x $11,500,000 = $460,000 Less: Actual returns (450,000)Exercise 2-7 (continued)Requirement 2Beginning balance in allowance account $300,000 Add: Year-end estimate 460,000 Less: Actual returns (450,000) Ending balance in allowance account $310,000Exercise 2-8Requirement 1Bad debt expense = $67,500 (1.5% x $4,500,000)Requirement 2Allowance for uncollectible accountsBalance, beginning of year $42,000 Add: Bad debt expense for 2019 (1.5% x $4,500,000) 67,500 Less: End-of-year balance (40,000) Accounts receivable written off $69,500 Requirement 3$69,500 — the amount of accounts receivable written off.Exercise 2-9Requirement 1Balance, beginning of year $32,000 Deduct: Receivables written off (21,000) Add: Collection of receivable previously written off 1,200 Balance, before adjusting entry for 2019 bad debts 12,200 Required allowance: 10% x $625,000 (62,500) Bad debt expense $50,300Requirement 2Current assets:Accounts receivable, net of $62,500 allowancefor uncollectible accounts $562,500Exercise 2-10Using the direct write-off method, bad debt expense is equal to actual write-offs. Collections of previously written-off receivables are recorded as revenue.Allowance for uncollectible accounts:Balance, beginning of year $17,280Deduct: Receivables written off (17,100)Add: Collection of receivables previously written off 2,200Less: End of year balance (22,410)Bad debt expense for the year 2019 $20,030 Exercise 2-11($ in millions)Allowance for uncollectible accounts:Balance, beginning of year $16Add: Bad debt expense 14Less: End of year balance (18)Write-offs during the year $ 12*Accounts receivable analysis:Balance, beginning of year ($1,084 + 16)$ 1,100Add: Credit sales 4,271Less: Write-offs* (12)Less: Balance end of year ($953 + 18) (971)Cash collections $4,388 Exercise 2-12Requirement 22019 income before income taxes would be understated by $900 2019 income before income taxes would be overstated by $900.Exercise2-13Requirement 2$ 1,800 interest for 9 months÷ $28,200 sales price= 6.383% rate for 9 monthsx 12/9to annualize the rate_______= 8.511% effective interest rateExercise 2-14Requirement 1Book value of stock $16,000Plus gain on sale of stock 6,000= Note receivable $22,000Interest reported for the year= 10% rate Divided by value of note $ 22,000 Requirement 2Exercise 2-18Mountain High retains significant risks and rewards and therefore must treat the transfer as a secured borrowing. The accounts receivable stay on the balance sheet ofExercise 2-19Step 3: Deduct discount to calculate cash proceeds.Exercise 2-21Step 3: Deduct discount to calculate cash proceeds.Exercise 7-21 (continued)Step 4: To record a loss for the difference between the cash proceeds and theExercise 2-21 (concluded) Requirement 2。

中级会计学英文课件 (2)

2-4

LO 1 Describe the usefulness of a conceptual framework.

Conceptual Framework

Question

(true or false):

A conceptual framework underlying financial accounting is important because it can lead to consistent standards and it prescribes the nature, function, and limits of financial accounting and financial statements.

2-3

Conceptual Framework

The Need for a Conceptual Framework

u u

To develop a coherent set of standards and rules. To solve new and emerging practical problems.

PREVIEW OF CHAPTER

2

Intermediate Accounting 15th Edition Kieso Weygandt Warfield

2-2

2

1. 2. 3. 4.

Conceptual Framework for Financial Reporting

LEARNING OBJECTIVES

2-8

Development of Conceptual Framework

The FASB has issued seven Statements of Financial Accounting Concepts (SFAC) for business enterprises.

中级财务会计英文ch07.ppt

3. Effects of obsolescence, customer demand, competition, rate of technological change, and other economic factors.

The holder is allowed to use, manufacture, sell, and control the item, process, or activity without interference or infringement by others.

Chapter 7-18

Intangible Assets Amortization of Cost

Factors to consider when estimating the useful life of an intangible asset:

1. Legal, regulatory, or contractual provisions that place a limit on the maximum economic life.

costs. 10. Indicate the presentation of intangible assets and related items.

Chapter 7-2

Intangible Assets

Intangible assets are those noncurrent economic resources that are used in the operations of the business but have no physical existence.

中级财务会计英文版.课后答案(chap06)

Exercise 6-11. Straight-line:$33,000 - 3,000= $6,000 per year5 years2. Sum-of-the-years’ digits:Exercise 6-1 (concluded)3. Double-declining balance:Straight-line rate of 20% (1 ÷ 5 years) x 2 = 40% DDB rate.4. Units-of-production:$33,000 - 3,000= $.30 per mile depreciation rate 100,000 milesExercise 6-21. Straight-line:$115,000 - 5,000= $11,000 per year10 years2. Sum-of-the-years’ digits:Sum-of-the-digits is ([10 (10 + 1)] ÷2) = 552011 $110,000 x 10/55 = $20,0002012 $110,000 x 9/55 = $18,0003. Double-declining balance:Straight-line rate is 10% (1 ÷ 10 years) x 2 = 20% DDB rate2011 $115,000 x 20% = $23,0002012 ($115,000 - 23,000) x 20% = $18,4004. One hundred fifty percent declining balance:Straight-line rate is 10% (1 ÷ 10 years) x 1.5 = 15% rate2011 $115,000 x 15% = $17,2502012 ($115,000 - 17,250) x 15% = $14,6635. Units-of-production:$115,000 - 5,000= $.50 per unit depreciation rate220,000 units2011 30,000 units x $.50 = $15,0002012 25,000 units x $.50 = $12,500Exercise 6-31. Straight-line:$115,000 - 5,000= $11,000 per year10 years2011 $11,000 x 3/12 = $ 2,7502012 $11,000 x 12/12 = $11,0002. Sum-of-the-years’ digits:Sum-of-the-digits is {[10 (10 + 1)]/2} = 552011 $110,000 x 10/55 x 3/12 = $ 5,0002012 $110,000 x 10/55 x 9/12 = $15,000+ $110,000 x 9/55 x 3/12 = 4,500$19,5003. Double-declining balance:Straight-line rate is 10% (1 ÷ 10 years) x 2 = 20% DDB rate2011 $115,000 x 20% x 3/12 = $5,7502012 $115,000 x 20% x 9/12 = $17,250+ ($115,000 - 23,000) x 20% x 3/12 = 4,600$21,850 or,2012 ($115,000 - 5,750) x 20% = $21,8504. One hundred fifty percent declining balance: Straight-line rate is 10% (1 ÷ 10 years) x 1.5 = 15% rate 2011 $115,000 x 15% x 3/12 =$ 4,313 2012 $115,000 x 15% x 9/12 = $12,937 + ($115,000 - 17,250) x 15% x 3/12 = 3,666$16,603Or,2012 ($115,000 - 4,313) x 15% = $16,603Exercise 6-3 (concluded)5. Units-of-production:$115,000 - 5,000= $.50 per unit depreciation rate220,000 units2011 10,000 units x $.50 =$ 5,0002012 25,000 units x $.50 =$12,500Exercise 6-4Building depreciation:$5,000,000 - 200,000= $160,000 per year30 yearsBuilding addition depreciation:Remaining useful life from June 30, 2011 is 27.5 years.$1,650,000= $60,000 per year27.5 years2011 $60,000 x 6/12 = $30,0002012 $60,000 x 12/12 =$60,000Exercise 6-6Requirement 11. Straight-line:$260,000 - 20,000= $40,000 per year6 years2011 $40,000 x 8/12 = $26,667 2012 $40,000 x 12/12 = $40,0002. Sum-of-the-years’ digits:Sum-of-the-yea rs’ digits is ([6 (6 + 1)] ÷2) = 212011 $240,000 x 6/21 x 8/12 = $45,7142012 $240,000 x 6/21 x 4/12 = $22,857+ $240,000 x 5/21 x 8/12 =38,095$60,9523. Double-declining balance:1/6 (the straight-line rate) x 2 = 1/3 DDB rate2011 $260,000 x 1/3 x 8/12 = $57,7782012 $260,000 x 1/3 x 4/12 = $28,889+ ($260,000 – 86,667) x 1/3 x 8/12 = 38,518$67,407 or,2012 ($260,000 – 57,778) x 1/3 = $67,407Exercise 6-9Requirement 1$5,675Group depreciation rate = = 17.2% (rounded)$33,000Group life = $28,500= 5.02 years (rounded)$5,675Requirement 2To record the purchase of new refrigerators.To record the sale of old refrigerators.Exercise 6-10Requirement 1Cost of the equipment:Purchase price $154,000Freight charges 2,000Installation charges 4,000$160,000Straight-line rate of 12.5% (1 ÷ 8 years) x 2 = 25% DDB rate.Requirement 2For plant and equipment used in the manufacture of a product, depreciation is a product cost and is included in the cost of inventory. Eventually, when the product is sold, depreciation will be included in cost of goods sold.Exercise 6-15To record the purchase of a patent.To record amortization of a patent for the year 2011.To record amortization of the patent for the year 2012.To record costs of successfully defending a patent infringement suit.Exercise 6-15 (concluded)To record amortization of patent for the year 2013.Calculation of revised annual amortization:($ in thousands)$500 Cost$62.5 Previous annual amortization ($500 ÷ 8 years) x 2 years 125 Amortization to date (2011-2012)375 Unamortized cost (balance in the patent account)45Add420 New unamortized cost÷ 6 Estimated remaining life(8 years – 2 years)$ 70 New annual amortizationExercise 6-21Requirement 1Analysis:Correct Incorrect(Should Have Been Recorded) (As Recorded)2008 Machine 350,000 Expense 350,000Cash 350,000 Cash 350,0002008 Expense 70,000 Depreciationentry omittedAccum. deprec. 70,0002009 Expense 70,000 Depreciationentry omittedAccum. deprec. 70,0002010 Expense 70,000 Depreciationentry omittedAccum. deprec. 70,000During the three-year period, depreciation expense wasunderstated by $210,000, but other expenses were overstated by$350,000, so net income during the period was understated by$140,000, which means retained earnings is currently understatedby that amount.During the three-year period, accumulated depreciation wasunderstated, and continues to be understated by $210,000.To correct incorrect accountsMachine ............................................................ 350,000Accumulated depreciation ($70,000 x 3 years) .. 210,000 Retained earnings ($350,000 – 210,000) ............ 140,000 Requirement 2Correcting entry:Assuming that the machine had been disposed of, no correctingentry would be required because, after five years, the accountswould show appropriate balances.。

中级财务会计(双语)第二章

Gross Method V.S. Net Method • In America, most companies use the gross method because it’s easier than the net method. • But in China, only the gross method is allowed to use.

• Trade discounts only has one way to record: use the net price to record the accounts receivable and the revenue. • Cash discounts has two ways to record: gross method & net method.

▪ Notes receivable are supported by the note and an invoice.

• Accounts receivable are classified as current assets, because their collection period (收款期) is usually less than one year. • AR are recognized on the day when we deliver the goods/services.

Trade receivables 商业应收款: resulting from the sale of goods or services. Receivables Exp. Accounts Receivable Nontrade receivables 非商业应收款: not resulting from the sale of goods or services.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2/10,n/30

Discount percent Number of days discount is available Otherwise, net (or all) is due Credit period

7 - 10

Cash Discounts

Gross Method

Sales are recorded at the invoice amounts.

7 - 13

Sales Returns

During the first year of operations, Hawthorne sold $2,000,000 of merchandise that had cost them $1,200,000 (60%). Industry experience indicates 10% return rate. During the year $130,000 was returned prior to customer payment. Record the returns and the end of the year adjustment.

Checks should be signed only by authorized individuals.

Restricted Cash and Compensating Balances

Restricted Cash

Management’s intent to use a certain amount of cash for a specific purpose – future plant expansion, future payment of debt.

Actual Returns Sales returns Accounts receivable Inventory Cost of goods sold (60%) Adjusting Entries Sales returns Allowance for sales returns Inventory-estimated returns Cost of goods sold (60%)

To avoid misstating the financial statements, sales revenue and accounts receivable should be reduced by the amount of returns in the period of sale if the amount of returns is anticipated to be material.

Are recorded net of trade discounts.

7-8

Cash Discounts

increase sales

Cash discounts

encourage early payment increase likelihood of collections

7-9

Cash Discounts

• Bank overdrafts may be offset against other cash accounts.

7-7

Accounts Receivable

Result from the credit sales of goods or services to customers.

Are classified as current assets.

Enhances the reliability and accuracy of accounting data

7-4

Internal Control Procedures

Cash Receipts • Separate responsibilities for receiving cash, recording cash transactions, and reconciling cash balances. • Match the amount of cash received with the amount of cash deposited. • Close supervision of cash-handling and cash-recording activities. Cash Disbursements

◦ Composite Rate

◦ Aging of Receivables

7 - 17

Income Statement Approach

• Focuses on past credit sales to make estimate of bad debt expense.

• Emphasizes the matching principle by estimating the bad dee current period’s credit sales.

7 - 11

Sales discounts forfeited are recorded as interest revenue if payment is received after the discount period.

Cash Discounts

On October 5, Hawthorne sold merchandise for $20,000 with terms 2/10, n/30. On October 14, the customer sent a check for $13,720 taking advantage of the discount to settle $14,000 of the amount. On November 4, the customer paid the remaining $6,000.

7 - 16

xxx xxx

Allowance for Uncollectible Accounts

Accounts Receivable

Less: Allowance for Uncollectible Accounts

Net Realizable Value

Net realizable value is the amount of the accounts receivable that the business expects to collect. Income Statement Approach Balance Sheet Approach

Money market funds

7-3

Treasury bills

Commercial paper

Internal Control

Encourages adherence to company policies and procedures

Promotes operational efficiency Minimizes errors and theft

Normally classified as a selling expense and closed at year-end.

Contra asset account to Accounts Receivable.

Bad debt expense Allowance for uncollectible accounts

7 - 12

Sales Returns

Merchandise may be returned by a customer to a supplier. A special price reduction, called an allowance, may be given as an incentive to keep the merchandise.

7 - 15

PAST DUE

Uncollectible Accounts Receivable

Most businesses record an estimate of the bad debt expense by an adjusting entry at the end of the accounting period.

• • •

7-5

All disbursements, except petty cash, made by check.

Separate responsibilities for cash disbursement documents, check authorization, check signing, and record keeping.

7 - 14

130,000 130,000 78,000

78,000

70,000 70,000

42,000

42,000

Uncollectible Accounts Receivable

Bad debts result from credit customers who are unable to pay the amount they owe, regardless of continuing collection efforts. In conformity with the matching principle, bad debt expense should be recorded in the same accounting period in which the sales related to the uncollectible account were recorded.

Cash and Receivables

7

Cash and Receivables

PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA