企业增值税纳税筹划外文文献翻译最新

税收筹划的外文翻译

外文文献翻译2011 届译文一:企业税收筹划的有效性:基于对报酬的激励作用(上)译文二:企业税收筹划的有效性:基于对报酬的激励作用(下)学生姓名周伟学号********院系经济与管理学院专业会计指导教师许庆高完成日期2010年12月2日Corporate Tax-Planning Effectiveness: The Role of Compensation-Based Incentives (Ⅰ)John D. Phillips University of ConnecticutABSTRACTThis study investigates whether compensating chief executive officers and business-unit managers using after-tax accounting-based performance measures leads to lower effective tax rates, the empirical surrogate used for tax-planning effectiveness. Utilizing proprietary compensation data obtained in a survey of corporate executives, the relation between effective tax rates and after-tax performance measures is modeled and estimated using a two-step approach that corrects for the endogeneity bias associated with firms' decisions to compensate managers on a pre- versus after-tax basis. The results are consistent with the hypothesis that compensating business-unit managers, but not chief executive officers, on an after-tax basis leads to lower effective tax rates.KEYWORDS tax planning; performance measures; endogenous treatment effects.I. INTRODUCTIONEffective tax planning, defined by Scholes et al. (2002) as tax planning that maximizes the firm's expected discounted after-tax cash flows, requires managers to consider their decisions' after-tax consequences. In this paper, I investigate whether after-tax accounting-based performance measures lead to lower effective tax rates (ETR), my empirical surrogate for tax planning effectiveness.1 The ETR, an income-statement-based outcome measure calculated as the ratio of total income tax expense to pre-tax income, generally measures the effectiveness of tax reduction strategies that lead to higher after-tax income. A lower ETR, however, can only proxy for tax savings and does not always imply that after-tax income and/or cash flows have been maximized.2 Despite this limitation, the ETR has been used to measure the effectiveness of spending on the tax function (Mills et al. 1998) and corporate tax department performance (Douglas et al. 1996). Also, lowering the ETR is frequently cited as a way to increase earnings(e.g., Ziegler 1997) and increase share price (e.g., Mintz 1999; Swenson 1999).Accounting research has addressed the relation between accounting-based compensation and managers' actions (e.g., Larcker 1983; Healy 1985; Wallace 1997). This paper is the first to address whether after-tax accounting-based performance measures motivate managers to take actions that help lower their firms' ETR and does so at both the chief executive officer (CEO) and business-unit (SBU) manager levels. Prior after-tax performance measure research has focused only on the determinants of compensation CEOs using pre- versus after-tax earnings (e.g., Newman 1989; Carnes and Guffey 2000; Atwood et al. 1998; Dhaliwal et al. 2000) and provides no evidence concerning after-tax compensation's effectiveness in lowering a firm's tax liability. Extending this investigation to the SBU level is motivated out of the apparent conflict between arguments that taxes should be allocated to SBU for incentive compensation purposes (e.g., McLemore 1997) with empirical observations that a majority of firms do not do so (e.g., Douglas et al. 1996).4 The current investigation provides evidence concerning the incremental effectiveness of explicitly motivating CEOs and SBU managers to incorporate tax consequences into their operating and investment decisions.A common issue in cross-sectional studies that attempt to link a particular management accounting choice to an outcome measure is that all sample firms may be optimizing with respect to the choice being investigated (Ittner and Larcker 2001). Without addressing the endogeneity of a firm's choice, it is difficult to provide evidence consistent with this choice leading to an improved outcome. To address this issue, the relation between ETR and CEO and SBU-manager after-tax performance measures is estimated using a two-step approach that helps correct for the potential endogeneity bias associated with these two choice variables. As a first step in implementing this approach, the Antle and Demski (1988) controllability principle is used to model a firm's decisions to adopt after-tax CEO and SBU-manager performance measures. To include a particular measure in a manager's compensation contract, this principle requires that the expected benefits from holding a manager responsible for a measure must be greater than the additional wage that must be paid to compensate the manager for the resulting additional risk and effort. Accordingly, an after- tax performance measure should be used as a contracting variable in a manager's incentive compensation contract only if the manager's involvement in tax-planning efforts leads to a difference between pre-tax and after-tax accounting results, which is generally reflected in the ETR. Consistent with prior research, the pre- versus after-tax CEO and SBU-manager selection models include variables that control for a firm's tax-planning opportunities because the presence of such opportunities reflect the extent to which a manager's actions can be expected to lower the ETR.Even if a manager's efforts are expected to lead to a lower ETR, a firm will use an after-tax performance measure only if the expected benefits exceed the expected costs of doing so. An after-tax performance measure is expected to lead to a lower ETR because it motivates the manager's increased cooperation with tax professionals to help identify, develop, and execute tax-planning strategies. McLemore (1997, 1) cites Hewlett Packard's tax director to support the need for SBU-manager involvement in tax-planning efforts:Tax planning is only as good as being involved in the early stages of such things as business planning, strategic planning, and merger and acquisition work....Your tax department has to be represented at the table when those decisions are made. The evolving model for the future is the tight integration of tax people with business unit planning.Costs associated with using after-tax performance measures include the additional wage that must be paid to compensate the manager for the increased risk due to potential tax law changes and the increased effort that results from including income tax expense in the compensation contract. Other potential costs associated with after-tax compensation include the administrative cost of allocating tax expense to a firm's SBU, increased tax examination costs, and increased tax authority scrutiny. Contrary to measuring after-tax compensation's benefits via observed ETR, there are no clear empirical surrogates for after-tax performance measures' costs. This study thus focuses on the realized benefits of compensating managers on an after-tax basis but does not provide evidence of the associated costs' magnitude.Proprietary data obtained in a survey of corporate executives are used to construct certain test variables, including those indicating whether CEOs and SBU managers are compensated using after-tax accounting-based performance measures. Publicly available data are used to construct ETR and other test variables. The results are consistent with the hypothesis that compensating SBU managers, but not CEOs, on an after-tax basis leads to lower ETR, resulting in an estimated median tax savings of $13.3 million annually. Sensitivity tests performed on a subsample of firms with high simulated MTR (Graham 1996) provide further evidence that low-MTR firms' potential ETR-lowering actions that could have ambiguous effects on cash flows and after-tax profits are not driving this result. Further sensitivity tests help rule out the proportion of tax function outsourcing as an alternative explanation for the statistically and economically significant negative relation between after- tax SBU-manager compensation and ETR.The results contribute to the accounting-based compensation literature by linking after- tax accounting-based performance measures to SBU-manager involvement that is incrementally effective in lowering firms' ETR. Consistent with Guidry et al. (1999) who documentbonus-induced earnings management at the SBU level, this finding provides additional insight into the effect that SBU-manager accounting-based incentives have on managers' actions. Also, the estimated explicit tax savings resulting from after-tax performance measures provide corporate decision makers with information relevant to the design of SBU-manager incentive compensation plans.The paper proceeds as follows. The next section sets forth the hypotheses tested in this study. Section III outlines the empirical models and estimation procedures used in testing these hypotheses. Section IV provides a discussion of the data and sample, including a brief overview of the survey used to obtain proprietary compensation data. Results are presented in Section V. The final section provides the conclusion and a discussion of the study's limitations.II. HYPOTHESIS DEVELOPMENTNewman (1989), Cares and Guffey (2000), and Atwood et al. (1998) investigate firms' choices of after-tax earnings as the contracting variable in CEO bonus plans. These studies hypothesize that firms with greater tax-planning opportunities, consistent with the Antle and Demski (1988) controllability principle, are more likely to use after-tax performance measures. Using proxies for tax-planning opportunities, these studies collectively find that multinational status, number of operating segments, firm size, and capital intensity are positively associated with after-tax CEO compensation. Atwood et al. (1998) also presents evidence that leverage is negatively associated with this choice.企业税收筹划的有效性:基于对报酬的激励作用(上)约翰D·菲利普斯康涅狄格大学摘要本研究探讨首席执行官是否修正主管和业务部门经理利用税后会计为基础的绩效措施,导致较低的实际税率,以报酬激励用于税收筹划的有效性。

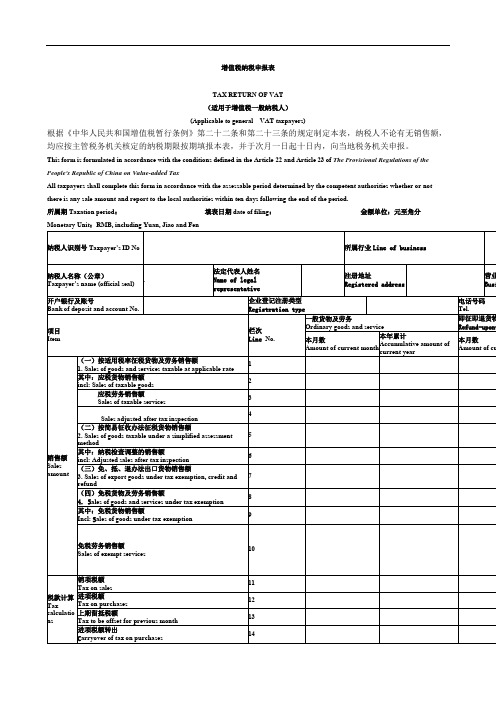

增值税纳税申报表中英对照精译版

增值税纳税申报表TAX RETURN OF VAT(适用于增值税一般纳税人)(Applicable to general VAT taxpayers)根据《中华人民共和国增值税暂行条例》第二十二条和第二十三条的规定制定本表,纳税人不论有无销售额,均应按主管税务机关核定的纳税期限按期填报本表,并于次月一日起十日内,向当地税务机关申报。

This form is formulated in accordance with the conditions defined in the Article 22 and Article 23 of The Provisional Regulations of the People's Republic of China on Value-added TaxAll taxpayers shall complete this form in accordance with the assessable period determined by the competent authorities whether or not there is any sale amount and report to the local authorities within ten days following the end of the period.所属期Taxation period:填表日期date of filing:金额单位:元至角分Monetary Unit:RMB, including Yuan, Jiao and Fen以下由税务机关填写:Only for the use of the taxation institution only below:收到日期:接收人:主管税务部门签章:Date of receipt: Receiver: Seal of competent taxation institution。

企业增值税纳税筹划外文文献翻译最新

企业增值税纳税筹划外文文献翻译最新This article discusses the importance of value-added tax (VAT) XXX is a tax on the value added to a product or service at each stage of n and n。

ns pliance.The first step in XXX includes identifying the VAT rates。

ns。

XXX。

It is also XXX.Once the VAT rules are understood。

ns XXX and report VAT。

as well as training XXX.XXX。

This can include taking advantage of VAT ns and ced rates。

as well as optimizing the timing of VAT payments and refunds.Overall。

XXX their financial performance。

It requires a thorough understanding of the VAT rules and ns。

as well as a XXX.译文本文讨论了对于公司而言,增值税规划的重要性。

增值税是对于每个生产和分销阶段所增加的产品或服务价值的税收。

公司可以通过增值税规划来最小化其税务责任,并避免违规行为的罚款。

增值税规划的第一步是了解公司运营所在国家的增值税规则和法规。

这包括确定增值税率、免税和门槛。

同样重要的是确定增值税注册要求和截止日期。

一旦了解了增值税规则,公司可以制定增值税合规策略。

这包括实施系统和程序来准确计算和报告增值税,以及培训员工以确保合规性。

增值税规划还涉及识别增值税节省的机会。

这可以包括利用增值税免税和减税,以及优化增值税支付和退款的时机。

企业纳税筹划外文文献翻译

文献出处:MUCAI G P, KINYA G S, NOOR A I, et al. Tax Planning and Financial Performance of Small Scale Enterprises in Kenya[J].2014:3:1236-1243.原文Tax Planning and Financial Performance of Small Scale Enterprises in KenyaMUCAI G P, KINYA G S, NOOR A IAbstractIn order to ensure the efficiency and effectiveness of activities, reliability and compliance with applicable laws, small scale enterprises need to have adequate tax controls. The study sought to find out the extent to which expenditure on capital assets in tax planning, to determine how tax planning by Capital Structure influence performance of small enterprises, find out how tax planning through Advertisement expenditure influence performance of small enterprises and to assess how tax planning through Legal Forms of enterprise influence performance of small enterprises in Embu CBD. The study had a total population of one hundred and forty nine respondents and a sample of 30 percent was drawn from each stratum. The data was then presented in form of Percentages and Tables. The study found the influence of tax planning by capital structure, tax planning in investment, capital asset planning through advertisement expenditure and found that the Legal Forms of small enterprises in Embu CBD has no significant relationship. The study recommends that small scale enterprises should be ready to seek advice on tax planning. Further to this, the study recommends that there is need to have NGOs to sensitize the respondents as to the need to do formal tax planning as it could increase their Business profitability. Key Words: Tax Avoidance, Tax Evasion, Tax Planning, Capital Structure.IntroductionThe concept of taxation has been a concern of global significance as it affects every economy irrespective of national differences (Oboh et al., 2012). Within thecontext of Africa, tax, a concept as old as mankind can be described as an amount, effort, contribution or service rendered either in kind (goat, cow, farm produce, clearing of grass etc.) or monetary value contributed into a common purse for the running of the society. According to Omotoso (2001), in his definition of the modern taxes, defined tax as a compulsory charge imposed by a public authority on the income of individuals and companies as stipulated by the government decrees, acts or case laws irrespective of the exact amount of services rendered to the payer in return. Thus, taxes constitute the principal source of government revenue and the beauty of any government is for its citizen to voluntarily execute their tax obligations without much coercion and harassment (Adedeji and Oboh, 2012).Tax evasion and fiscal corruption have been a general and persistent problem throughout history with serious economic consequences, not only in transition economies, but also in countries with developed tax systems (Raza, 2011). In general, tax evasion and corruption can have ambiguous effects on Economic growth: tax evasion increases the amount of resources accumulated by entrepreneurs, but it also reduces the amount of public services supplied by the government, thus leading to negative Consequences for economic growth (Roy and Raffaella, 2011). Previous studies highlight reports of declining effective tax rates and a rising proportion of firms that report little or no tax liability. To date, the maintained assumption in much of the literature is that aggressive tax behavior, rather than economic trends, is the driving factor behind this decline (Desai and Dharmapala 2009).The Kenya Revenue Authority (K.R.A) is the tax collection agency of Kenya. It was formed July 1, 1995 to enhance tax collection on behalf of the Government of Kenya. It collects a number of taxes and duties, including: value added tax, income tax and customs. Since KRA's inception, revenue collection has increased dramatically, enabling the government to provide much needed services to its citizenry like free primary education and Health Services to all. Over 90% of annual national budget funding comes from local taxes collected by the KRA (GOK, 2010).It is however important to establish whether the observed increased revenue collection effectiveness has resulted from aggressive tax management by Kenya Revenue Authority (KRA) or whether it is, in part, due to increased use of the new economy business model. This is important because the sources of tax avoidance have distinct policy implications. The policy response to tax avoidance arising from aggressive tax schemes and investments in tax planning is likely to be very different from the response to tax avoidance stemming from a shift in many firms' organizational, operating, and financing attributes, which enable them to exploit their operating flexibility to naturally align with tax incentives that generate tax savings (Drucker 2006).The decreasing trend in effective tax rates may not be solely due to aggressive tax management but Rather, firms' modifications to their business models resulting from changing economic trends potentially enabling them to reduce tax burdens without additional investments in tax planning (Blouin, and Larcker 2011). Performance of Small EnterprisesDifferent approaches are used for performance evaluation in which goal approach, time frame approach, balanced scorecard , system approach, and ineffectiveness approach are included (Jean-Francois, 2004). In stakeholder approach, centre of attention is the ability of a business to meet the needs and expectations of its stakeholders (Daft, 1995).Competing values approach expands the range of other approaches.By using competing values approach, four other models are developed in which rational goal; internal process, open system and human relations are included (Quinn and Rohrbaugh, 1983). Performance of an organization can be evaluated by focusing on problems and retarding factors that inhibit the performance of organizations (Camaron, 1984). Out of the above mentioned approaches, goal approach is the superlative approach to evaluate the performance due to its straightforwardness (Pfeffer and Salancik 1978). Most trendy approach of performance evaluation ofSME's is balanced scorecard approach. Balanced scorecard has four dimensions in which financial growth, quality, customers and learning growth is built-in (Kaplan and Norton, 1992).Balance scorecard actually focuses on maintaining symmetry between monetary and non monetary measures (Neely et al. 1996).Book-tax differences, on average, are systematically related to earnings growth, future stock returns, and earnings persistence (Hanlon, 2005) and among other implications, book-tax differences are useful measures in evaluating firm performance. Consistent with these studies, Shevlin (2002) and Hanlon, Laplante, and Shevlin (2005) find that while book income explains a firm's annual stock returns better than estimated taxable income, estimated taxable income, on average, has incremental explanatory power for book income. However , there is little evidence regarding taxable income as an alternative performance measure and, in particular, cross-sectional differences in firms that mitigates or enhances the ability of taxable income to inform investors regarding firm performance (Lev and Nissim, 2004).Some SME's compare their performance with that of other SME's. They evaluate their performance by means of comparative analysis. Performance can also be evaluated by means of ineffectiveness approach. In ineffectiveness approach, focus is on the factors that hampers the feat of organizations. Therefore this study seeks to investigate the extent to which Tax Planning influences Financial Performance of Small Enterprises in Embu town CBDTax PlanningThe implementation situation of SME income tax planning is distorted tax planning, that is to say, on the one hand, more and more SME pay tax in accordance with the law, and on the other hand, because of the role of the interest mechanism and other various reasons, more and more SME tax-related cases appear (Karing and Wanjala, 2005). According to the survey, the vast majorities SME have not yet started or are considering carrying out tax planning, which can not fight for the legitimate tax interests and ruin financial interests leading to a large number of emerging additionaltax burden (Fjeldstad and Rakne, 2003). In addition, SME tax planning is treated unreasonable. Due to the limitations of the concept, SME tax planning activities often encounter misunderstanding, punishment and censor from some basic taxation law enforcement agencies (Karing and Wanjala, 2005).Tax law is said to be barely connected with the universe and with universal law as we understand it. However, tax law is founded not only on principles but also on practicality. There is no element of perpetuity about tax law, only the constant clash of the immediate and semi permanent (Kibua and Nziok, 2004). A State cannot run a democracy well without taxation and a taxation system cannot be run well without democracy. Oliver Wendell Holmes has said on one occasion, "Taxes are what we pay for civilized society" (Neely et al. 1996).Statement of the ProblemTax reform today has been moving towards considering new legislation, such as whole new taxes or reliefs, rather than patching of existing taxes by either increasing or decreasing the amount of taxation. This breaks down into the fact that there are ongoing considerations of widening the tax base. Kenya is no exception to this and there are ongoing considerations into taxing the informal or "jua kali' sector including the taxation of the "mitumba', the second hand clothing industry as well as the taxation of all informal tax payers of small amounts.A question that appears to generate surprisingly little debate in Kenya is the scope for legally mitigating taxes payable by individuals and corporate entities. Tax planning is bound to gain increasing significance with the ever greater aggressiveness and sophistication of the Kenya Revenue Authority and other tax collecting bodies. The trend of increased aggressiveness and sophistication in tools and methods is occurring against a backdrop of a public policy of domestic sources being the primary sources of revenues for budgetary purposes. This results in governmental pressure on tax collecting agencies to improve their revenue collection performance. The result of this trend is the more stringent enforcement of taxation laws. The past and presentpractice by many of outright evasion is, and likely will continue to be, fraught with risk.Examining the relation between the new economy business model, tax avoidance and investments in tax planning is important as previous Studies in the tax avoidance literature generally examine how specific firm attributes are related to tax avoidance independently, rather than investigating how firms' overall business models facilitate or hinder effective tax planning (Frank, Lynch, and Rego 2009). Hanlon and Heitzman (2010) argue that despite the much literature, these do not explain the variation in tax avoidance very well. Therefore due to this and such seemingly inexorable trends, the question of tax mitigation by legitimate avoidance naturally occurs. This study intends to find out the influence of small Enterprises tax planning within the current legal environment so as so minimize their tax burden. ConclusionDue to the corruption levels, low business growth, and management of public finances in the economy, where there is a great extent of corruption, has a related to a high level of tax evasion and the study concluded that there was no relationship between tax planning in investment in capital asset and performance of small enterprises in Embu CBD. The study concludes no significant relationship. The study concludes also that no significant relationship exists between tax planning through advertisement expenditure and performance of small enterprises in Embu CBD and also concluded there was no significant relationship the Legal Forms of enterprise tax planning and performance of small enterprises in Embu CBD. RecommendationsThe tax authorities should address the lack of formal tax planning as this may be a way of evading taxation in the name of tax avoidance. The small scale enterprises should also be ready to open up to advice on tax planning to make savings lather than playing a hide and seek game with tax authorities. Further to this, the study recommends that there is need to have NGOs to sensitize the respondents as to theneed to do formal tax planning as it could increase their Business profitability Implications on Policy Theory and PracticeThis study though confined to investigate the influence of tax planning on financial performance of small scale enterprises has established that little tax planning take place among the small enterprises and therefore tax Authorities and the chamber of commerce should write a position paper to address the awareness and use of tax planning by small scale enterprises. This would improve the growth rate of the small enterprises and there after the growth of the economy.译文肯尼亚小规模企业的纳税筹划与财务业绩保罗,萨洛姆,努尔摘要为了确保活动的效率和有效性,适用性法律的可靠性与遵从性,小规模企业需要有足够的税收管制。

税收筹划分析英文外文

Tax planning refers to the extent permitted by laws and regulations, through business, investment, financial activities and arrangements in advance planning to minimize tax costs, to maximize the tax benefits of an economic act. The expectation of any taxpayer to reduce tax burden because they often require a minimum of input, maximum output, in order to achieve the goal of maximizing enterprise value, which is the demand for tax planning motives and economic base. In recent years, people have come to understand that although the importance of tax planning, but often as a result of tax planning provisions in the tax laws of the edge of the operation, and the state’s tax policy, tax laws and regulations and changing risk estimates of tax planning not enough, resulting in a tax were economic, such as a waste of time, more harm than good, and they even find stolen, the abyss of tax fraud. Therefore, the risk of all times.For enterprises, the only fully aware of the existence of tax planning risks and understand their motives have, in accordance with the current tax law, combined with their own conditions, with the preferential policies the state fully in order to make effective tax planning measures, The ultimate goal to reduce corporate tax burden, improving economic efficiency.。

企业税收筹划外文翻译文献

企业税收筹划外文翻译文献企业税收筹划外文翻译文献(文档含中英文对照即英文原文和中文翻译)Corporate Tax-Planning Effectiveness: The Role of Compensation-BasedIncentives (Ⅰ)John D. Phillips University of ConnecticutABSTRACTThis study investigates whether compensating chief executive officers andbusiness-unit managers using after-tax accounting-based performance measures leads to lower effective tax rates, the empirical surrogate used for tax-planning effectiveness. Utilizing proprietary compensation data obtained in a survey of corporate executives, the relation between effective tax rates and after-tax performance measures is modeled and estimated using a two-step approach that corrects for the endogeneity bias associated with firms' decisions to compensate managers on a pre- versus after-tax basis. The results are consistent with the hypothesis that compensating business-unit managers, but not chief executive officers, on an after-tax basis leads to lower effective tax rates.KEYWORDS tax planning; performance measures; endogenous treatment effects.I. INTRODUCTIONEffective tax planning, defined by Scholes et al. (2002) as tax planning that maximizes the firm's expected discounted after-tax cash flows, requires managers to consider their decisions' after-tax consequences. In this paper, I investigate whether after-tax accounting-based performance measures lead to lower effective tax rates (ETR), my empirical surrogate for tax planning effectiveness.1 The ETR, an income-statement-based outcome measure calculated as the ratio of total income tax expense to pre-tax income, generally measures the effectiveness of tax reduction strategies that lead to higher after-tax income. A lower ETR, however, can only proxy for tax savings and does not always imply that after-tax income and/or cash flows have been maximized.2 Despite this limitation, the ETR has been used to measure the effectiveness of spending on the tax function (Mills et al. 1998) and corporate tax department performance (Douglas et al. 1996). Also, lowering the ETR is frequently cited as a way to increase earnings (e.g., Ziegler 1997) and increase share price (e.g., Mintz 1999; Swenson 1999).Accounting research has addressed the relation between accounting-based compensation and managers' actions (e.g., Larcker 1983; Healy 1985; Wallace 1997). This paper is the first to address whether after-tax accounting-based performance measures motivate managers to take actions that help lower their firms' ETR and does so at both the chief executive officer (CEO) and business-unit (SBU) manager levels.Prior after-tax performance measure research has focused only on the determinants of compensation CEOs using pre- versus after-tax earnings (e.g., Newman 1989; Carnes and Guffey 2000; Atwood et al. 1998; Dhaliwal et al. 2000) and provides no evidence concerning after-tax compensation's effectiveness in lowering a firm's tax liability. Extending this investigation to the SBU level is motivated out of the apparent conflict between arguments that taxes should be allocated to SBU for incentive compensation purposes (e.g., McLemore 1997) with empirical observations that a majority of firms do not do so (e.g., Douglas et al. 1996).4 The current investigation provides evidence concerning the incremental effectiveness of explicitly motivating CEOs and SBU managers to incorporate tax consequences into their operating and investment decisions.A common issue in cross-sectional studies that attempt to link a particular management accounting choice to an outcome measure is that all sample firms may be optimizing with respect to the choice being investigated (Ittner and Larcker 2001). Without addressing the endogeneity of a firm's choice, it is difficult to provide evidence consistent with this choice leading to an improved outcome. To address this issue, the relation between ETR and CEO and SBU-manager after-tax performance measures is estimated using a two-step approach that helps correct for the potential endogeneity bias associated with these two choice variables. As a first step in implementing this approach, the Antle and Demski (1988) controllability principle is used to model a firm's decisions to adopt after-tax CEO and SBU-manager performance measures. To include a particular measure in a manager's compensation contract, this principle requires that the expected benefits from holding a manager responsible for a measure must be greater than the additional wage that must be paid to compensate the manager for the resulting additional risk and effort. Accordingly, an after- tax performance measure should be used as a contracting variable in a manager's incentive compensation contract only if the manager's involvement in tax-planning efforts leads to a difference between pre-tax and after-tax accounting results, which is generally reflected in the ETR. Consistent with prior research, the pre- versus after-tax CEO and SBU-manager selection models include variables that control for a firm's tax-planning opportunities because the presence of such opportunities reflect the extent to which a manager's actions can be expected to lower the ETR.Even if a manager's efforts are expected to lead to a lower ETR, a firm will use an after-tax performance measure only if the expected benefits exceed the expectedcosts of doing so. An after-tax performance measure is expected to lead to a lower ETR because it motivates the manager's increased cooperation with tax professionals to help identify, develop, and execute tax-planning strategies. McLemore (1997, 1) cites Hewlett Packard's tax director to support the need for SBU-manager involvement in tax-planning efforts:Tax planning is only as good as being involved in the early stages of such things as business planning, strategic planning, and merger and acquisition work....Your tax department has to be represented at the table when those decisions are made. The evolving model for the future is the tight integration of tax people with business unit planning.Costs associated with using after-tax performance measures include the additional wage that must be paid to compensate the manager for the increased risk due to potential tax law changes and the increased effort that results from including income tax expense in the compensation contract. Other potential costs associated with after-tax compensation include the administrative cost of allocating tax expense to a firm's SBU, increased tax examination costs, and increased tax authority scrutiny. Contrary to measuring after-tax compensation's benefits via observed ETR, there are no clear empirical surrogates for after-tax performance measures' costs. This study thus focuses on the realized benefits of compensating managers on an after-tax basis but does not provide evidence of the associated costs' magnitude.Proprietary data obtained in a survey of corporate executives are used to construct certain test variables, including those indicating whether CEOs and SBU managers are compensated using after-tax accounting-based performance measures. Publicly available data are used to construct ETR and other test variables. The results are consistent with the hypothesis that compensating SBU managers, but not CEOs, on an after-tax basis leads to lower ETR, resulting in an estimated median tax savings of $13.3 million annually. Sensitivity tests performed on a subsample of firms with high simulated MTR (Graham 1996) provide further evidence that low-MTR firms' potential ETR-lowering actions that could have ambiguous effects on cash flows and after-tax profits are not driving this result. Further sensitivity tests help rule out the proportion of tax function outsourcing as an alternative explanation for the statistically and economically significant negative relation between after- tax SBU-manager compensation and ETR.The results contribute to the accounting-based compensation literature by linking after- tax accounting-based performance measures to SBU-manager involvement that is incrementally effective in lowering firms' ETR. Consistent with Guidry et al. (1999) who document bonus-induced earnings management at the SBU level, this finding provides additional insight into the effect that SBU-manager accounting-based incentives have on managers' actions. Also, the estimated explicit tax savings resulting from after-tax performance measures provide corporate decision makers with information relevant to the design of SBU-manager incentive compensation plans.The paper proceeds as follows. The next section sets forth the hypotheses tested in this study. Section III outlines the empirical models and estimation procedures used in testing these hypotheses. Section IV provides a discussion of the data and sample, including a brief overview of the survey used to obtain proprietary compensation data. Results are presented in Section V. The final section provides the conclusion and a discussion of the study's limitations.II. HYPOTHESIS DEVELOPMENTNewman (1989), Cares and Guffey (2000), and Atwood et al. (1998) investigate firms' choices of after-tax earnings as the contracting variable in CEO bonus plans. These studies hypothesize that firms with greater tax-planning opportunities, consistent with the Antle and Demski (1988) controllability principle, are more likely to use after-tax performance measures. Using proxies for tax-planning opportunities, these studies collectively find that multinational status, number of operating segments, firm size, and capital intensity are positively associated with after-tax CEO compensation. Atwood et al. (1998) also presents evidence that leverage is negatively associated with this choice.企业税收筹划的有效性:基于对报酬的激励作用(上)约翰D·菲利普斯康涅狄格大学摘要本研究探讨首席执行官是否修正主管和业务部门经理利用税后会计为基础的绩效措施,导致较低的实际税率,以报酬激励用于税收筹划的有效性。

企业税收筹划中英文对照外文翻译文献

中英文对照外文翻译文献(文档含英文原文和中文翻译)1、Enterprises of the major means of tax planningTax planning is the premise of strict enforcement of tax laws to minimize tax, customs tax called. Enterprises to carry out the correct tax, the need for the adoption of the following major route of transmission.First, reasonable means of financing options. In accordance with the provisions of China's current tax law, corporate interest payments on the loan within a certain range can be pre-tax expenses, and dividends can only be spending the after-tax profits of enterprise expenses. From a tax point of view, appropriate to the bank business loans and financing between enterprises, rather than directly to thefund-raising benefits.Second, a reasonable choice of trading partners. China's existing value-added tax system has a general taxpayers and small-scale taxpayers on the points, choose a different supplier object, the tax burden on enterprises is not the same. For example, when the Department of suppliers of value-added tax general taxpayer, the businessafter the purchase of goods, according to the amount of tax deduction of input tax amount of the corresponding balance after payment of value-added tax; if the purchase of goods for small-scale taxpayers, VAT can not be achieved Its not contain the amount of input tax deduction, the tax burden more than the former. Such as open invoices can also be part of deduction.Third, "the easy way out" tax conversion. Enterprises will be converted tohigh-tax low-tax, refers to economic activities in the same, there are a variety of revenue options to choose from, the taxpayers to avoid "high-tax point", choose the "low tax" and reduce the tax liability . The most typical example of this is to runnon-taxable to the tax planning services. From the tax point of view, run mainly two: First, the same taxes, different tax rates. Systems such as supply and marketing enterprises, the general operating tax rate is 17% of the means of subsistence, but also the operating value-added tax rate of 13% of the agricultural means of production and so on. Second, different taxes, different tax rates. This usually refers to types of enterprises in their business activities, both value-added business project, the project also involves the business tax.Fourth, the cost of reasonable expenses. Enterprises does not violate tax laws and financial system under the premise of the full cost of the reasonable expenses, that may occur on the full estimated losses and narrow the tax base and reduce the amount of taxable income. Countries allow for costs incurred in the projects, such as wages, respectively, the total amount of tax by 2%, 14%, 1.5% extracts of trade union funds, staff welfare, staff education funding should be sufficient to mention as much as possible to the whole. For some of the losses that may occur, such as bad debt losses, businesses should be fully expected in the tax law as far as possible the extent permitted by the cap enough to reserve. This is in line with the national tax law and financial system, can receive the tax effect.Fifth, to reduce tax liability. Factors that affect the tax liability there are two, namely, tax base and tax rates, the smaller the tax base, lower tax rates, tax liability is also smaller. Tax planning can start from these two factors to find legitimate ways to reduce tax liability. For example, an enterprise December 30, 2005 estimated taxableincome amounted to 100,200 yuan, the enterprise income tax liability 25050 yuan (100200 ×25%). If the corporate tax planning, tax consulting fees to pay 200 yuan, the corporate taxable income 100,000 (100200-200), income tax liability 27,000 yuan (100000 × 27%), can be found by comparing, for tax planning to pay only 200 yuan, 6066 yuan tax is (33066-27000).Sixth, to weigh the severity of the overall tax burden. For example, manyvalue-added tax planning programs have the general taxpayer and the taxpayer to choose small-scale planning. If an enterprise is a non-tax-year sales of about 900,000 yuan of production enterprises and enterprises to buy the materials each year the price of non-value-added tax of 70 million or less. The company's accounting system, the conditions identified as the general taxpayers. If that is the general taxpayer, the company's products are value-added tax rate applies to 17% capital gains tax liability 34,000 yuan (90 × 17% -70 × 17%); If it is small-scale taxpayers, the rate is 6%, 5.4 VAT liability million (90 × 6%)> 3.4 million. Therefore, from the perspective of value-added tax general taxpayer should be selected. But, in fact, althoughsmall-scale VAT taxpayers pay 20,000 yuan, but the input tax amount of 119,000 yuan (70 × 17%), although it can not offset the costs, thereby increasing the cost of 119,000 yuan, the income tax reduction of 2.975 million (11.9 × 25%), than pay a 20,000 yuan of value-added tax. Therefore, the business tax planning in the selection of programs, not only to look in a certain period of time watching the program on tax less, and to consider business development goals, to choose to increase their overall revenue program.Seventh, take full advantage of preferential taxation policies. For taxpayers, the use of tax incentives for tax planning focuses on how the rational use of tax policies and regulations shall apply to the lower or more favorable tax rates, a well-planned production and operation activities, the actual tax burden to a minimum in order to achieve Festival tax effect. For example, according to China's Law of the State Council for approval of high-tech industrial development zone of the high-tech enterprises, since the production from the fiscal year income tax exemption for 2 years. To-business use of wastewater, waste gas, waste residue and other waste as themain raw materials for production, 5 years in the income tax reduction or exemption. In addition, to support agriculture and the development of UNESCO Wei investment, countries have different tax incentives. Business operators should refer to policy, comparing the investment environment, investment income, investment risks and other factors, decided to invest in the region, investment direction, as well as investment projects, a reasonable tax planning, in order to reduce the corporate tax burden.企业税收筹划的主要途径纳税筹划是在严格执行税法前提下,尽量减少缴税,习惯称其为节税。

企业所得税税收筹划研究外文翻译文献

企业所得税税收筹划研究外文翻译文献(文档含中英文对照即英文原文和中文翻译)Study on the Tax Planning of Enterprise Income TaxHongceng Cao & Xiaohui XuCollege of Economics, Shenyang UniversityShenyang 110044, ChinaGuojie AoDepartment of Accounting and Financial Affairs, Shenyang UniversityShenyang 110044, ChinaAbstractThe enterprise income tax occupies is very important status in the tax paying of enterprise, and it has large space of tax planning. Under the background that the new enterprise income tax law was issued, we discussed the problem how to use tax planning to reduce the tax burden of enterprise and realize the maximization of the total profit for the enterprise. In this article, we studied the tax financing in the stage of enterprise financing from the selection of financing mode and the confirmation of financing channel, and put forward that the enterprise should select the liability financing mode to the largest extent in the critical risk range of equity structure. We studied the tax planning in the stage of investment of enterprise from three aspects including correctly selecting theinvestment direc tion, confirming proper enterprise organization form and selecting tax saving investment subject. We studied the tax planning from two aspects such as income and charge deduction. We studied the tax planning in the distribution stage of enterprise management result from first utilizing taxable income to compensate the loss, the loss recovering sequence of domestic investment profit return and the profit distribution strategy in the low tax region. For above aspects, we all put forward our own new theoretical opinions.Keywords: Enterprise income tax, Tax planning, Tax preferenceComparing with the old enterprise income law, the new enterprise income law changed in many aspects such as the taxpayer, the pre-tax deduction, and the tax preference, which put forward new task for the tax planning of the enterprise income tax. Under the background of new enterprise income tax, we will discuss the tax planning in the main stages such as the enterprise financing, investment, management and distribution.1. Tax planning in the stage of enterprise financingThe tax planning of the income tax in the stage of enterprise financing mainly includes the contents about the financing mode and the financing channel.1.1 Tax planning of financing modeThe financing modes of enterprise mainly include the equity financing and liability financing, and two different financing modes will produce different tax results. Generally speaking, under the fixed tax rate level, the liability financing can produce the interest rigid cost which can be reported before tax. When the account profit is adjusted as the taxable income, the tax law allows that the interest expenditure induced by the liability can be deducted before tax in the same interest rate regulated by the Bank in the same period, which equals that the state finance assumes a quarter of interest cost fro the enterprise. The equity financing is the flexi ble cost of bonus stock which can be reported after tax. The mode that the enterprise provides bonus stock and dividend to the investors is only one item of the distraction of post-tax profit (net profit), and it must be distributed after tax. The tax saving difference between two financing modes is very obvious. In the equity structure of enterprise, the proportion of the liability equity is higher, and the saving effectof the tax cost is more significant. So under the prem ise that the rate of or return on inv estment is higher than the liability cost rate, enhancing the proportion of liability financing will bring extra economic benefits for the owner of the enterprise, and finally increase the value of the enterprise. But we should also pay attention to that will increase the financial risk of the enterprise, and excessive liability will even induce the ab normality of the enterprise equity structure, and the liability crisis will make the financial status of the enterprise fall into collapse. Therefore, before the enterprise makes the tax planning of financing mode, it must ensure that the equity structure is in the critical risk range.1.2 Tax planning of enterprise financing channelThe financing channels of enterprise mainly include bank loan, self-accumulation of enterprise, inter-enterprise lending interior collection of en terprise, bond or stock issuance and commercial credit. Under usual situation, the sequence of the tax burden from heavy to light is self-accumulation of enterprise, bank loan, inter-enterprise lending and interio collection of enterprise. The prin ciple of tax planning of financing channel is that under the premise that the equity structure is to select the channel with higher profit and lower harm in the critical risk range, through comparing the advantages and disadvantages of various financing channels.2. Tax planning in the investment stage of enterpriseFor the tax planning in the investment stage of enterprise, we mainly consider three aspects, i.e. the selection of investment direction, the selection of enterprise organization form and the selection ofinvestment mode.2.1 Selecting correct investment directionThe new enterprise income tax established the new tax preference which gave priority to the industrial preference assisted by the regional preference, giving attention to the social advancement . Investors should select the investmen industry to reduce the tax burden according to the regulations about the national industrial policies and tax preference and response the industrial policy gui dance of the government. First, because the industrial select possesses strategicmeanings for the development trend of the enterprise, so when the investors make the decision of industrial investment they should scientifically demonstrate the investment and carefully make the decision, and they should consider not only their own industrial advantages, but also national industrial support policies, industrial tax preference policies, and make the rare resources of the enterprise to the green sunrise industries such as the agriculture, scientific technology environment protection and energy saving. Second, the enterprise income tax regulated regional preference for Chinese western regions, minority regions and special economic zones, and the enterp rise should study out multiple selectable investment programs in possible investment regions, and it should not only compare the cost incomes of various regional investment programs, but compare the tax levels of various programs, and make the comprehensive evaluation for the comprehensive benefits of variou s regional investment programs, which can not only reduce the tax burden, but find the regional investment program with maximum economic benefit.2.2 Selecting proper enterprise organization formThe tax planning of enterprise organization form should mainly consider four parts including establishment, expansion, division and merger. First, we will study the tax planning when the enterprise is established and select the organization form. According to the organization form, the enterprise types include individual proprietorship enterprise, partnership enterprise and limited corporation which can be divided into limited liability company and joint stock limited partnership, and because the tax system regulates different tax burden levels for the enterprises with different organization forms, so the establishment costs and advantages of different organization forms are different, and the tax is one of factors we should consider when we select the organization form of the enterprise. Especially when the organization form of the enterprise has large influence to the production and management, the tax will be the important factor which we should consider, and investors can select the organization form of the ent erprise to reduce the tax burden for the enterprise. Second, we will research the tax planning when the enterprise is expanded and needs to select the organization form. Enterprise always actualizes the scale expansion by increasing branches, but the tax policies for the branches with different forms in the tax law are obviously different, so enterprise should select the organization form of the branch. For the filiale and the subsidiary company, they respectively have their advantages and disadvantages for the tax, so the loss of the branch can counteract the gain of the parent company and reduce the total taxable income of the company. The subsidiary company and the parent company are regarded as two entities in the law, but the subsidiary company can obtain various tax preference policies regulated by the laws or local government. So the enterprise should comprehen sively consider the profit ability of the branch when it selects the form of the branch, and it should adopt the form of filiale when the branch is in the loss period, and adopt the form of subsidiary company when the branch is in the profit period. Third, we will study the tax planning in the division and merger of the enterprise. According to the regulations of the enterprise income law, enterprises should pay the income tax by 25%, but it also regulates that the small-sized profit-mak ing enterprise can pay the income tax by 20%, so the middle and small-sized enterprise can adopt the division measure to separate the branch from th e enterprise to reduce the taxable income and the tax burden. Theenterprise income tax regulates that the profitable enterprise a nnexes unprofitable enterprise, it can use the accumulated loss of the unprofitable enterprise to counteract the profit of the profitab le enterprise and reduce the taxable income and the tax burden. Therefore, in the merger of enterprises, the profitable enterprise can reduce the enterprise income tax by annexing unprofitable enterprises.2.3 Selecting the investment subject of tax savingAccording to different forms of investment subject, the investment of enterprise can be divided into monetary investment, tangible investment and im material investment. The monetary investment doesn’t increase the tax burden of investors, but it w ill influence the cash flux and payment ability of the enterprise. Different tax regulations aim at different tangible investment types, for example, fo r the estate investment, investors need not pay relative sales tax (if investor belongs to the real estate enterprise, the land value increment tax needs not be paid temporarily), and the depreciation of the estate can be deducted before tax to reduce the tax base of the en terprise income tax. For the sock-in-trade investment, the tax law will regard it as the sales goods and increase the tax bases of the value increment tax and the enterprise income tax, and the enterprise need pay the increment tax and the enterprise income tax. The immaterial investment can deduct the withholding income tax for the enterprise, and realize the deduction before tax through amortization year by year, which can reduce the tax base of the enterprise income tax. So when the enterprise selects the investment subject, it can select the tangible investment and immaterial investment which are better than the monetary investment from the view of the invested enterprise. Certainly, for the view of investing enterprise, it will assume more tax burdens such as the enterprise income tax, the increment tax and the consump tion tax when it selects the tangible investment and immaterial investment, so the investing enterprise should comprehensively consider the tax burdens of two parties to select the proper investment form.3. Tax planning in the production and management stage of enterpriseThe tax base of the enterprise income tax is the taxable income amount which equals to that an enterprise’s total income amount of each tax year deducts the tax-free incomes, tax-exempt incomes, each deduction items as well as the permitted remedies for losses of the previous years. And the income items, tax-free incomes and tax-exempt incomes and each deduction items are all generated in the production and management of the enterprise. So the tax planning of the enterprise income tax in the production and management can be implemented from two items such as the income items and the deduction items.3.1 Tax planning of incomeThe total income amount of the enterprise in the present term is decided by the sales amount of the product, the unit sales price of the product and the selected sales mode of the product, so the tax planning of the enterprise income tax about the income mainly includes the scale of production and sale, the sales price and the sales mode. First, for the planning of production and sale scale, under the premise of certain sale unit price, the income scale of the enterprise is decided by the sales amount. The scale of production and sale belongs to the item independently controlled by the enterprise, and the scale of production and sale will influence the tax burden of the enterprise which will influence the scale of production and sale in the same way. Therefore, when the enterprise confirms the scale of production and sale, it must consider the tax burden at term. According to the en terprise’s self management ability, the enterprise should find the critical point of profit and loss, and seek the scale of production and sale with maximum profits. Second, for the planning of sales price, under the premise of certain production and sale amount, the income scale of the enterprise is decided by the price level which is also the item independently controlled by the enterprise. The enterprise should consider many factors such as the cost level, the market de mand and thecompetition strategy, and the tax burden level is the important factor which should be considered by the enterprise, and the confirmation of the sales price can not only include the pre-tax income and income tax of the enterprise, but will directly influence the increment tax and other relative taxes. In the tax planning of income, we should take the sales price as the factor we should mainly considered. Third, for the planning of sales mode, in the sales proce ss of the product, the enterp rise possesses the independent selection right to the sales mode, and different sales mode always apply in different tax policies, i.e. the treatment difference of tax exists in this aspect, which offers the possibility to utilize different sales mode to plan the income tax. In a word, under the premise disobeying the tax law, the enterprise should compress the income scale which has exceeded the critical point of the tax rate from the sales scale and the sales price, and make the enterprise obtain the preference policies of low tax rate. For the selection of sales mode, the enterprise should delay the implementation of the income and the tax obligation to the best, which will not only compress the income scale in the present term to make the enterprise obtain the preference policy of low tax rate, but also make the enterprise obtain the profit of interest-free loan because of delaying the implementation of tax obligation.3.2 Tax planning of cost charge deductionThe payout of the enterprise can be divided into the profitable payout and the capital payout according to the time of the profitable term. The profitable payout should be reported in th e present cost charge, and the capital payout is divided and respectively reported in the cost charges of the present and future terms. For these two sorts of payout, the planning of the enterprise income tax should treat them differently.3.2.1 Tax planning of profitable payoutBecause different situations of profit and loss, and different tax preferences will differently influence the tax planning of enterprise, so we should respectively plan the tax of the profitable payout aiming at different situations of profit and loss. First, suppose the enterprise is profitable, because the profit able payout can be deducted from the enterprise income tax, the enterprise should select the planning method with large prophase cost. To make the tax deduction effect of the cost exert its function as soon as possible, and delay the realization of the pr ofit, then enterprise should delay the tax obligation time of the income tax. Second, suppose the enterprise is in loss, the planning method should be combined with the loss remedy of the enterprise. The enterprise should try to make the cost charge in the year with pretax loss remedy higher and make the cost charge in the year w ithout or incompletely with pretax loss remedy lower, and accordingly ensure the tax reduction effect of the cost charge will be exerted to the largest extent. Finally, suppose the enterprise is enjoying th e preference policy of the enterprise income tax, because the taxdeduction effect of the cost charge in the tax deduction period will completely or pa rtly be deducted through the deduction preference, so the enterprise should select the planning method which has few costs in the tax deduction period and has more costs in the non-tax-deduction period.3.2.2 Tax planning of capital payoutAs the modernization degree of enterprise is gradually enhanced, the proportion of the purchase payout of the long-term assets such as the fixed assets and immaterial assets which reflect the progress of the technology of the enterprise is higher and higher, and the tax planning of the fixed assets depreciation and the immaterial assets salesmanship possesses special importance in the tax planning of th e enterprise income tax. First, the tax law doesn’t recognize the devaluation preparation of long-term assets which the enterprise picks up, but the taxpayer can utilize the relative regulations about the subseq uent expenses of the long-term assets to adjust the depreciation base. The enterprise should combine the long-term development, rebuild the fixed assetsdesignedly, enhance the technical level of the enterprise, and improve the comprehensive competition strengthen of the enterprise. At the same time , the enterprise can put the subsequent expenses acco rding with the capitalization cond itions into the fixed assets cost, increase the depreciation picking base, and accordingly increase the depreciation amount of the deduction, reduce the taxable inco me of the present term and save the tax. For various payouts which don’t accord with the confirmation conditions of long-term assets, they should be counted into the profit and loss of th e present term. Second, the “Chinese Enterprise Income Tax Law” regu lated that the fixed assets of the enterprise needed to be depreciated quickly because of technical progress, the enterprise could reduce the depreciation fixed number of year or adopt the method of quick depreciation. To reduce the depreciation year can quicken the withdrawal of the costs, move the anaphase cost charges to the anterior period, and move the prophase account profit to the latter period. When the tax rate is fixed, the delayed payment of the income tax equals to obtain an interest-free loan from the country. When the tax rate is not fixed, the extension of the depreciation term can also reduce the tax burden for the enterprise. And the selection of the depreciation method of the long-term assets should be scientific, reasonable and legal. Finally, when the enterprise is in the non-deduction period of the income tax, taxpayer should apply for reducing the residual proportion for the tax department in time according to the characters of the assets. When the residual proportion is reduced , the depreciation tax de duction will increase, which could not only maintain the taxpayer’s right, but bring large tax benefit for the taxpayer.4. Tax planning in the management result distribution stage of enterprise4.1 First utilizing the taxable income to compensate the lossFor the yearly loss of the enterprise, the tax law regulates to allow the enterprise uses the pretax profit in the next year to compensate it. And if the profit in the next year is not enough to compensate, the enterprise is allowed to compensate the loss year after year, but the longest term should be limited in 5 years. In this way, the enterprise can use the selection right of the assets price counting and amortization method allowed by the tax law, and the selection right of the expenses reported range standard to more report the pretax deduction items and deduction amount, and continue to induce the loss before the term of five years is at term, accordingly to prolong the term of the preference policy.4.2 Arranging the domestic investment return to compensate the loss according to the sequence from low tax rate to high tax rateAccording to the enterprise income tax, the investors’ after-tax profits returned from the associated enterprise should pay the income tax, but if the enterprise which is the investor has loss or past yearly loss which has not be remedied, the returned profit can be used to remedy the loss, and for the surplus part, the enterprise should pay the income tax. Therefore, if the investor is the enterprise which can be applicable for different income tax rates, the enterprise can select the sequence from low tax rate to high tax rate, to use th e returned investment profit remedy the loss and make the taxpayer’s income tax reduce to the least level.4.3 Keepin g that the investment return in the low tax region doesn’t be distributedIn the existing enterprise income tax, for the taxpayer’s profit returned from other enterprise which has paid the income tax, the tax amount of the tax payment can be adjusted when computing the income tax of the enterprise. If the profit of the invested enterprise has not be distributed to the investors, the investors need not to pay the income tax, and in this way, to keep that the investment return in the low tax region doesn’t be distributed and turn it into the investment capital can reduce investors’ tax burden.ReferencesChinese CPA Association. (2008). Tax Law. Beijing: Economic Science Press.The Fifth Session of the Tenth NPC. (2007). Enterpri se Income Tax Law of China. Mar. 16, 2007.Wang, Xinjian. (2006). The Method of Enterprise Tax Planning. Shandong Commercial Accounting. No.2.Zhou, Yan. (2008). Influences of New Enterprise Income Tax Law on Enterprise Tax Planning. Friends of Accounting.No.15.Zhuang, Fenrong. (2007). Hundred Classic Practical Examples of Tax Planning.Beijing: Mechanical Industry Press.企业所得税税收筹划研究曹宏层、徐晓慧(沈阳工业大学经济学院)、敖国杰(沈阳工业大学会计财务部)摘要企业所得税的税收空间很大,在企业的纳税额中占有很大的比重。

增值税中英文对照外文翻译文献