Midterm for IT auditing.doc

Auditing

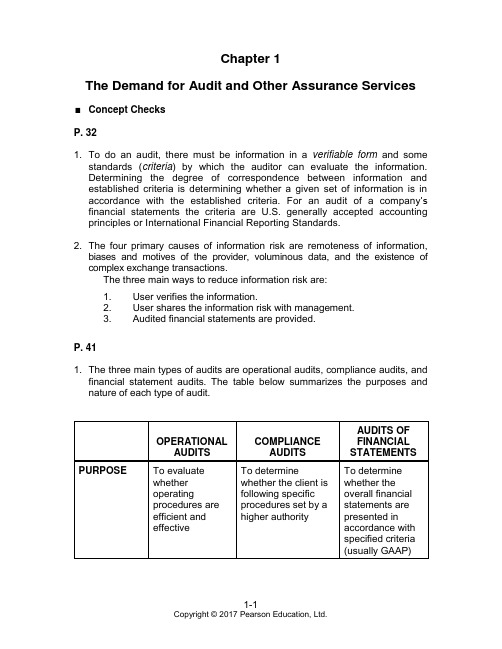

Chapter 1The Demand for Audit and Other Assurance ServicesConcept ChecksP. 321. To do an audit, there must be information in a verifiable form and somestandards (criteria) by which the auditor can evaluate the information.Determining the degree of correspondence between information and established criteria is determining whether a given set of information is in accordance with the established criteria. For an audit of a compan y’s financial statements the criteria are U.S. generally accepted accounting principles or International Financial Reporting Standards.2. The four primary causes of information risk are remoteness of information,biases and motives of the provider, voluminous data, and the existence of complex exchange transactions.The three main ways to reduce information risk are:1. User verifies the information.2. User shares the information risk with management.3. Audited financial statements are provided.P. 411. The three main types of audits are operational audits, compliance audits, andfinancial statement audits. The table below summarizes the purposes and nature of each type of audit.Concept Checks (continued)* Internal auditors may assist CPAs in the audit of financial statements. Internal auditors may also audit internal financial statements for use by management. 2. The major differences in the scope of audit responsibilities for CPAs, GAOauditors, IRS agents, and internal auditors are:•CPAs perform audits of financial statements prepared using U.S.GAAP or IFRS in accordance with auditing standards.•GAO auditors perform compliance or operational audits in order to assure the Congress of the expenditure of public funds in accordancewith its directives and the law.•IRS agents perform compliance audits to enforce the federal tax laws as defined by Congress, interpreted by the courts, and regulated by theIRS.•Internal auditors perform compliance or operational audits in order to assure management or the board of directors that controls and policiesare properly and consistently developed, applied, and evaluated.Review Questions1-1 Aishah should have information about the tax laws that are relevant to the case allocated to her. The established criteria are found in the Tax Audit Framework.1-2This apparent paradox arises from the distinction between the function of auditing and the function of accounting. The accounting function is the recording, classifying, and summarizing of economic events to provide relevant information to decision makers. The rules of accounting are the criteria used by the auditor for evaluating the presentation of economic events for financial statements and he or she must therefore have an understanding of accounting standards, as well as auditing standards. The accountant need not, and frequently does not, understand what auditors do, unless he or she is involved in doing audits, or has been trained as an auditor.1-3 An independent audit is a means of satisfying the need for reliable information on the part of decision makers. Recent changes in accounting and business operations include:1. Increased global activities of many businessesa. Multiple product lines and transaction locationsb. Foreign exchange affects transactions2. Complex accounting and exchange transactionsa. Increasing use of derivatives and hedging activitiesb. Increasingly complex accounting standards in areas such asrevenue recognition3. More complex information systemsa. Possibly millions of transactions processed daily through on-line and traditional sales channelsb. Voluminous data requires interpretation1-4 1. Risk-free interest rate This is approximately the rate the bank could earn by investing in U.S. treasury notes for the same length of timeas the business loan.2. Business risk for the customer This risk reflects the possibility thatthe business will not be able to repay its loan because of economicor business conditions such as a recession, poor managementdecisions, or unexpected competition in the industry.3. Information risk This risk reflects the possibility that the informationupon which the business risk decision was made was inaccurate. Alikely cause of the information risk is the possibility of inaccuratefinancial statements.Auditing has no effect on either the risk-free interest rate or business risk. However, auditing can significantly reduce information risk.1-5The three main ways to reduce information risk are:1. User verifies the information.2. User shares the information risk with management.3. Audited financial statements are provided.The advantages and disadvantages of each are as follows:1-6 Information risk is the risk that information upon which a business decision is made is inaccurate. Fair value accounting is often based on estimates and requires judgment. Fair value can be estimated using multiple methods with some estimates being more subjective than others. Fair value estimates are made at a point in time, but can also change rapidly, depending on market conditions. All of these factors increase information risk.1-7An assurance service is an independent professional service to improve the quality of information for decision makers. An attestation service is a form of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party. Audit services are a form of attestation service in which the auditor expresses a written conclusion about the degree of correspondence between information and established criteria.The most common form of audit service is an audit of historical financial statements, in which the auditor expresses a conclusion as to whether the financial statements are presented in accordance with an applicable financial reporting framework such as U.S. GAAP or IFRS. An example of an attestation service is a report on the effectiveness of an entit y’s internal control over financial reporting. There are many possible forms of assurance services, including services related to business performance measurement, health care performance, and information system reliability.1-8The following are examples of the different forms of evidence that Aisha, the tax auditor, will require for the audit process:▪Electronic and documentary data about transactions▪Written and electronic communication with outsiders▪Observations by the auditor▪Oral testimony of the auditee (client)1-11 The four parts of the Uniform CPA Examination are: Auditing and Attestation, Financial Accounting and Reporting, Regulation, and Business Environment and Concepts.Multiple Choice Questions From CPA Examinations1-12 a. (3) b. (2) c. (1)1-13 a. (2) b. (4) c. (2)Discussion Questions And Problems1-14 a. Audit services are a form of attestation service, and attestation services are a form of assurance service. In a diagram, auditservices are located within the attestation service area, andattestation services are located within the assurance service area.b. 1. (2) An attestation service other than an audit service2. (1) An audit of historical financial statements3. (3) An assurance or nonassurance service that is not anattestation service4. (2) An attestation service other than an audit service5. (2) An attestation service other than an audit service6. (2) An attestation service other than an audit service7. (2) An attestation service other than an audit service8. (2) An attestation service other than an audit service9. (2) An attestation service other than an audit service(Review services are a form of attestation, but areperformed according to Statements on Standards forAccounting and Review Services.)10. (2) An attestation service other than an audit service11. (3) An assurance or nonassurance service that is not anattestation service1-15 a. The interest rate for the loan that requires a review report is lower than the loan that did not require a review because of lowerinformation risk. A review report provides moderate assurance tofinancial statement users, which lowers information risk. An auditreport provides further assurance and lower information risk. As aresult of reduced information risk, the interest rate is lowest for theloan with the audit report.b. Given these circumstances, Busch should select the loan from FirstCity Bank that requires an annual audit. In this situation, theadditional cost of the audit is less than the reduction in interest dueto lower information risk. The following is the calculation of totalcosts for each loan:c. Busch should select the loan from United National Bank due to thehigher cost of the audit and the reduced interest rate for the loanfrom United National Bank. The following is the calculation of totalcosts for each loan:d. Busch may desire to have an audit because of the many otherbenefits that an audit provides. The audit will provide Busch’smanagement with assurance about annual financial information usedfor decision-making purposes. The audit may detect errors or fraud, andprovide management with information about the effectiveness ofcontrols. In addition, the audit may result in recommendations tomanagement that will improve efficiency or effectiveness.e. The auditor must have a thorough understanding of the client and itsenvironment, including the client’s e-commerce technologies, industry,regulatory and operating environment, suppliers, customers, creditors,and business strategies and processes. This thorough analysis helpsthe auditor identify risks associated with the client’s strategies thatmay affect whether the financial statements are fairly stated. Thisstrategic knowledge of the client’s business often helps the auditoridentify ways to help the client improve business operations, therebyproviding added value to the audit function.1-16 a. Top Gear presenters conduct races to test a wide variety of cars and report their strengths and weaknesses in the programme. Theprogramme provides information to help potential car buyers makeintelligent decisions about the cars they buy. Many car enthusiastsconsider the reviews in Top Gear to be more reliable thaninformation provided by the product manufacturers. This is becausethe Top Gear television series has been giving independent adviceon cars for years.b. The concepts of information risk for potential car buyers and for theusers of financial statements are essentially the same. They areboth concerned with the problem of unreliable information beingprovided. In the case of the auditor, the user is concerned aboutunreliable information being provided in the financial statements.The potential car buyers are likely to be concerned about themanufacturer or dealer providing unreliable information.c. The four causes of information risk are essentially the same for abuyer of a car and a user of financial statements:(1) Remoteness of information It is difficult for a user to obtainmuch information about either a car manufacturer or the caritself without incurring considerable cost. The car buyer doeshave the advantage of possibly knowing other users who aresatisfied or dissatisfied with a similar car, and the ability toperform online research of new vehicles.(2) Biases and motives of provider There is a conflict betweenthe car buyer and the manufacturer. The buyer wants to buya high quality product at minimum cost whereas the sellerwants to maximize the selling price and quantity sold.(3) Voluminous data There is a large amount of availableinformation about cars that users might like to have inorder to evaluate a car. Either that information is notavailable or too costly to obtain.(4) Complex exchange transactions The acquisition of a car isexpensive and certainly a complex decision because of allthe components that go into making a good car andchoosing from a large number of alternatives.d. The three ways users of financial statements and buyers ofcars reduce information risk are also similar:(1) User verifies information him or herself That can be obtainedby driving different cars, examining the specifications of thecars, talking to other users, and doing research in variousmagazines.(2) User shares information risk with management Themanufacturer of a product has a responsibility to meet itswarranties and to provide a reasonable product. The buyerof a car can return it for correction of defects. In some casesa refund may be obtained.(3) Examine the information prepared by Consumer ReportsThis is similar to an audit in the sense that independentinformation is provided by an independent party. Theinformation provided by Consumer Reports is comparableto that provided by a CPA firm in an audit of financialstatements.1-17 a. The following parts of the definition of auditing are related to the narrative:(1) Haraldsson is being asked to issue a report about qualitativeand quantitative information for the buses. The buses andtheir value are therefore the information with which she isconcerned.(2) There are four established criteria which must be evaluatedand reported by Haraldsson: existence of the buses on thenight of August 31, 2008, ownership of each bus by DanvilleBus Services, physical condition of each bus and fair marketvalue of each bus.(3) Annaliese Haraldsson will accumulate and evaluate fourtypes of evidence:(a) Count the buses to determine their existence.(b) Use registrations documents held by Olson forcomparison to the serial number on each bus todetermine ownership.(c) Examine the buses to determine each bus's physicalcondition. She can examine the bus’s conditionherself or hire an expert to do so.(d) Examine the blue book to determine the fair marketvalue of each bus.(4) Annaliese Haraldsson, CPA, appears qualified, as acompetent, independent person. She is a CPA, and shespends most of her time auditing used automobile, bus, andtruck dealerships, and has experience that is consistent withthe nature of the engagement.(5) The report results are to include:(a) which of the 20 buses are parked in Danville'sparking lot the night of August 31.(b) whether all of the buses are owned by Danville BusServices.(c) the condition of each bus, using establishedguidelines.(d) fair market value of each bus using the current bluebook for buses.b. The only parts of the audit that will be difficult for Haraldsson are:(1) Evaluating the condition, using the guidelines of poor, good,and excellent. It is highly subjective to do so. One method isto find the “blue book” value. (Note: Kelley Blue Book is aUnited States automotive vehicle valuation company thatgives used vehicle pricing information. Because of itspopularity, the term “blue book” has become synonymouswith the car’s market value.) If she uses a differe nt criterionthan the "blue book," the fair market value will not bemeaningful. Her experience will be essential in using thisguideline.(2) Determining the fair market value, unless it is clearly definedin the blue book for each condition.1-18 a. The major advantages and disadvantages of a career as an CAO auditor, tax authority agent, CPA, or internal auditor are:1-18 (continued)b. Other auditing careers that are available are:Auditors within many of the branches of the federalgovernment (e.g., Atomic Energy Commission)Auditors for many state and local government units (e.g., stateinsurance or bank auditors)1-19 The most likely type of auditor and the type of audit for each of the examples are:1-20 a. Financial statement audits reduce information risk, which lowers borrowing costs. An audit also provides assurances to managementabout information used for decision-making purposes, and may alsoprovide recommendations to improve efficiency or effectiveness ofoperations.b. Czarnecki and Hogan likely provide tax services, accountingservices, and management advisory services. They may also provideadditional assurance and attestation services other than audits offinancial statements.c. Student answers will vary. They may identify new types of informationthat require assurance, such as environmental or corporateresponsibility reporting. Students may also identify opportunitiesfor consulting or management advisory services, such as assistancewith the adoption of International Financial Reporting Standards.1-21 a. Assurance related to financial statements are the most likely forms of assurance that are likely to be provided only by public accountingfirms. Examples include audits of historical financial statements,reviews of historical financial statements, audits of internal controlover financial reporting, and compliance auditing such as thatrequired by the Single Audit Act and OMB Circular A-133 (althoughthese audits may also be provided by government auditors).b. There are many types of information that are assured by providersother than public accounting firms. Some of these assurances areprovided by government entities, such as food inspections, elevatorinspections, and pumps at gasoline stations. Other assurances areprovided by nonprofit and for-profit assurance providers, such asISO 9000 certifications.c. Table 1-1 on p. 35 includes some examples of assurance that may beprovided by public accounting firms or other assurance providers. Forexample, assurance on corporate responsibility and sustainability maybe provided by public accounting firms or other assurance providers.Other examples included assurance on Web site controls, andinformation such as Web site traffic or newspaper circulation.1-22 a. The vision of the Global Reporting Initiative (GRI) is a sustainable global economy where organizations manage their economic,environmental, social and governance performance and impactsresponsibly, and report transparently. Its mission is to makesustainability reporting standard practice by providing guidance andsupport to organizations.b. According to the GRI “A sustainability report is a report publishedby a company or organization about the economic, environmental,and social impacts caused by its everyday activities. Asustainability report also presents the organization's values andgovernance model, and demonstrates the link between its strategyand its commitment to a sustainable global economy.”In an integrated report, sustainability information is included along with financial information. These reports emphasize the linksbetween financial and non-financial performance. An integrated reportalso presents the risks and opportunities the company faces, integratedwith disclosure of environmental, social, and governance issues.c. GRI offers two “in accordance” reporting options, Core andComprehensive. The Core report provides the essential elementsof a sustainability report. The Comprehensive report includesadditional d isclosures of the organization’s strategy and analysis,governance, and ethics and integrity. The GRI recommendsexternal assurance, but it is not required for either type of “inaccordance” report.1-23 a. Answers will vary by state. Most states require 150 hours of education, with specific requirements for number of accounting hoursand credit hours in other subject areas.b. Answers will vary by state. Many states require one or two years ofwork experience gained in public practice, or possibly government,academia or industry, depending on the state. In many states,experience in industry or internal audit is sufficient, depending on thetype of work performed.c. Most states have frequently addressed questions. Many of theseaddress education requirements, as well as information on how toprepare for the exam, as well as information on applying for licensure.d. The Elijah Watt Sells award program was established in 1923by the American Institute of Certified Public Accountants(AICPA) to recognize outstanding performance on the UniformCPA Examination. The award is presented to candidates whoobtained a cumulative average score above 95.50 across all foursections of the Uniform CPA Examination, completed testing duringthe previous calendar year, and passed all four sections of theExamination on their first attempt.e. Passing information is available on the CPA Examination portion ofthe AICPA web site. Recent passing rates have ranged fromapproximately 44% to 59% across the four sections.。

TheNotificationf...

TheNotificationf...第一篇:The Notification for joint annual inspection of FIE 关于开展2011年外商投资企业年检通知大全关于开展2011年外商投资企业联合年检工作的通知The Notification for joint annual inspection of foreign investment enterprise in 2011各有关单位:The relevant units:根据《商务部、财政部、税务总局、工商总局、统计局、外汇局关于开展2011年外商投资企业联合年检工作的通知》(商资函〔2011〕75号)的要求,现将广州市2011年外商投资企业联合年检工作通知如下:Industrial and commercial bureauAccording toindustry and commerce, the statistics bureau, the safe develop the notificationforeign investment enterprise joint annual inspection about 2011 >(commercial letter [2011] no.75)requirement, now the work of Guangzhouforeign investment enterprise joint annual inspection notification of 2011 is the following:一、联合年检工作的参检部门The inspection department ofjoint annual inspection广州市联合年检工作的参检部门包括市外经贸局、市财政局、市国税局、市地税局、市工商局、市统计局、国家外汇管理局广东省分局。

The inspection department which should joinjoint annual inspection : 1﹑Foreign Economy & Trade 2﹑Local bureau of finance3﹑National Tax Bureau 4﹑Local Taxation Bureau 5﹑Industrial and commercial bureau 6﹑Statistics Department;7 SAFE State Administration of Foreign Exchange注:各区、县级市统计局在市统计局的领导下直接参与并负责对各自辖区外商投资企业的网上年检工作。

离职审计 英语

离职审计英语As an auditor, one of the key responsibilities is to conduct exit audits when an employee leaves the organization. Exit audits are crucial in ensuring that all assets, information, and responsibilities are properly accounted for and transferred to the appropriate individuals. 。

During an exit audit, the auditor will review the employee's departure process, including the return of company property such as laptops, access cards, and confidential documents. It is important to verify that all items are returned in good condition and that there are no outstanding liabilities or obligations.In addition to physical assets, the auditor will also review the employee's access to sensitive information and systems. This includes revoking access to company databases, email accounts, and other digital platforms to prevent any unauthorized access after the employee leaves.Furthermore, the auditor will conduct a thorough review of the employee's work performance and responsibilities. This includes assessing the completion of assigned tasks, projects, and any pending deadlines. It is important to ensure that all work is properly documented and transferred to other team members to avoid any disruptions in workflow.Another important aspect of an exit audit is to review the employee's compliance with company policies and procedures. This includes reviewing any signed agreements, confidentiality agreements, and non-compete clauses to ensure that the employee is not in violation of any contractual obligations.Overall, exit audits play a critical role in safeguarding the organization's assets, information, and reputation. By conducting a thorough review of the employee's departure process, the auditor helps to mitigate risks and ensure a smooth transition for both the departing employee and the organization as a whole.In conclusion, exit audits are essential for maintaining the integrity and security of an organization. By conducting a comprehensive review of the employee's departure process, the auditor helps to protect the organization from potential risks and liabilities. It is important for auditors to be thorough, detail-oriented, and objective in their approach to exit audits to ensure a successful transition for all parties involved.。

第三方服务提供商

IT CONTROLS: S11/ 4

IT audit training

for

利益

专家 经验与专门知识 义务 新系统的快速实现

March 2007

IT CONTROLS: S11/ 5

IT audit training

for

世界上的外包/FM

你的国家中情况怎样? IT是否比其它服务更受关注? 例子

March 2007

IT CONTROLS: S11/ 9

IT audit training

for

关注的原因(II)

柔性的缺失

合同限制 变更需求 变更条款 High cost高成本 性能审计问题 变更率

变更的成本

March 2007

IT CONTROLS: S11/ 10

IT audit trainingIT来自CONTROLS: S11/ 2

IT audit training

for

第三方服务

设备管理 外包 市场测试

March 2007

IT CONTROLS: S11/ 3

IT audit training

for

为什么使用第三方服务? 有什么好处?

成本 现金流 员工 调度

March 2007

IT audit training

for

外部审计访问权限

理解内部控制系统 很多审计师审计一个服务提供商是不切 实际的 可能需要直接访问

March 2007

IT CONTROLS: S11/ 8

IT audit training

会计英语审计流程中的七个环节英语

会计英语审计流程中的七个环节英语The audit process is an important part of accounting and ensures the accuracy and integrity of financial records. There are seven key stages in the audit process, each with its own significance and purpose. In this article, we will explore each of these stages in detail to provide a comprehensive understanding of the audit process in accounting.1. Engagement PlanningThe first stage of the audit process is engagement planning. This involves the auditor and the client setting the scope and objectives of the audit, as well as establishing the timeline and resources required for the audit. During this stage, the auditor gains an understanding of the client's business and the industry in which they operate. This helps the auditor to identify potential risksand areas of focus for the audit. Additionally, the auditor will assess the client's internal controls and identify any potential areas of weakness or areas for improvement.2. Risk AssessmentOnce the engagement planning is complete, the auditorwill move on to the risk assessment stage. During this stage, the auditor will identify and assess the risks associated with the client's financial statements. This involves understanding the nature of the client's business, analyzing the internal and external factors that may impact the financial statements, and identifying any potential areas of concern. The auditor will also consider the likelihood and potential impact of these risks on the financial statements.3. Testing Internal ControlsTesting internal controls is an important stage of the audit process as it allows the auditor to evaluate the effectiveness of the client's internal controls in mitigatingthe identified risks. This involves testing the design and implementation of the client's internal controls, as well as performing tests of control to assess whether the controls are operating effectively. The auditor will also consider any deficiencies or weaknesses in the client's internal controls and provide recommendations for improvement.4. Substantive TestingSubstantive testing is a critical stage of the audit process as it involves testing the financial transactions and account balances that make up the client's financial statements. This includes examining the evidence supporting the transactions and account balances, as well as performing analytical procedures to assess the reasonableness and accuracy of the financial information. The auditor will also consider any potential misstatements or errors in the financial statements and assess their impact on the overall financial position of the client.5. Audit DocumentationThroughout the audit process, the auditor is required to maintain comprehensive audit documentation that supports the findings and conclusions of the audit. This includes documenting the auditor's understanding of the client's business and internal controls, the results of the risk assessment and testing, and any significant findings or issues identified during the audit. The audit documentation serves as a historical record of the audit and provides evidence of the work performed by the auditor.6. ReportingOnce the substantive testing and audit documentation are complete, the auditor will move on to the reporting stage. During this stage, the auditor will communicate the findings and conclusions of the audit to the client in the form of an audit report. The audit report includes the auditor's opinion on the fairness and accuracy of the client's financialstatements, as well as any significant issues or recommendations identified during the audit. The audit report provides valuable information to the client's stakeholders, such as investors, creditors, and regulators, about the reliability of the financial statements.7. Follow-upThe final stage of the audit process is follow-up, where the auditor will communicate any outstanding issues or recommendations to the client and ensure that they are addressed in a timely manner. This may involve discussing the audit findings with the client's management and providing guidance on implementing any recommended improvements to the client's internal controls or financial reporting processes. The auditor will also consider any changes in circumstances or events that may impact the client's financial statements and assess the need for additional audit procedures.In conclusion, the audit process in accounting involves several key stages that are critical to ensuring the accuracy and integrity of financial records. From engagement planning and risk assessment to substantive testing and reporting, each stage plays an important role in identifying and addressing potential risks and issues in the client's financial statements. By following a structured and comprehensive audit process, auditors can provide valuable assurance to the client and their stakeholders about the reliability of the financial information.。

a primary purpose of audit working papers -回复

a primary purpose of audit working papers -回复Audit working papers serve as a critical tool for auditors during the audit process. They provide a comprehensive record of the auditor's work, procedures performed, evidence gathered, and conclusions reached. The primary purpose of audit working papers is to document the audit engagement from planning to completion. In this article, we will explore the different steps involved in creating audit working papers and discuss their significance in ensuring the quality and integrity of the audit.Step 1: Planning and PreparationThe first step in creating audit working papers is to identify the objectives of the audit engagement and plan the audit approach. The planning phase involves understanding the client's business, assessing the risk and materiality levels, and determining the audit scope. During this stage, auditors gather relevant information about the client, such as financial statements, internal controls, and previous audit documentation.Step 2: Risk AssessmentOnce the planning phase is complete, auditors conduct a riskassessment to identify and evaluate potential risks that may impact the financial statements. This step involves analyzing the internal controls, assessing inherent risks, and testing the design and effectiveness of controls. The findings from this stage are documented in the working papers, including any identified weaknesses or areas requiring further examination.Step 3: Performing Audit ProceduresThe next step is the execution of audit procedures to gather sufficient and appropriate evidence to support the auditor's opinion. Auditors employ various methods, such as substantive testing, analytical procedures, and inquiries, to obtain the necessary evidence. Each audit procedure is recorded in the working papers, along with the associated findings, explanations, and calculations.Step 4: Cross-referencing and IndexingTo maintain organization and easy accessibility, auditorscross-reference their working papers to link related information. This helps to establish the logical flow of the audit documentation and facilitates tracking of the audit procedures performed and evidence obtained. Additionally, auditors create index sheets tosummarize the contents of the working papers, enabling easy reference to specific areas.Step 5: Documentation ReviewOnce the audit procedures are performed and the working papers are complete, a reviewing process is conducted to ensure consistency, accuracy, and compliance with auditing standards. This step involves a detailed review of the working papers by a supervising auditor or team lead, who examines the documentation for completeness, relevance, and appropriate conclusions. Any identified deficiencies or areas requiring clarification are addressed and amended accordingly.Step 6: Retention and ConfidentialityAudit working papers are crucial records that provide evidence of the audit work performed and support the auditor's opinion. Therefore, it is essential to retain these documents for a specified period, usually based on legal or regulatory requirements. Additionally, auditors must ensure the confidentiality of the working papers, as they may contain sensitive information about the client's operations and financials.The significance of audit working papers lies in their ability to demonstrate the auditor's professional judgment, due care, and compliance with auditing standards. They allow for effective planning, execution, and review of the audit engagement, contributing to the overall quality and reliability of the audit opinion. Moreover, working papers serve as a valuable reference for subsequent audits and enable auditors to address any queries or challenges that may arise in the future.In conclusion, audit working papers play a vital role in the audit process, serving as a comprehensive record of the audit engagement. They document the planning, execution, and review of the audit procedures, enabling auditors to support their findings and conclusions. By following the steps outlined above, auditors can create well-organized, reliable, and easily understandable working papers, ensuring the highest level of professionalism during the audit engagement.。

审读工作标准和尺度

审读工作标准和尺度It is essential for organizations to establish clear and comprehensive work standards and measurements to ensure the quality and efficiency of their operations. 审读工作标准和尺度对于组织来说至关重要,可以确保其运营质量和效率。

First and foremost, clear work standards provide employees with aset of expectations and guidelines to follow in their daily tasks. Without clear standards, employees may struggle to understand what is expected of them, leading to confusion and decreased productivity. 明确的工作标准可以为员工提供一套日常任务的期望和指导。

没有清晰的标准,员工可能会难以理解所期望的工作,导致混乱和降低的生产率。

Additionally, work standards help to ensure consistency and qualityin the deliverables of an organization. By detailing the specific steps and requirements for each task, standards enable employees to maintain a high level of quality in their work, ultimately contributing to the overall success of the organization. 此外,工作标准有助于确保组织交付成果的一致性和质量。

《特殊目的审计报告》 的英文专业说法

《特殊目的审计报告》的英文专业说法全文共3篇示例,供读者参考篇1Special Purpose Audit ReportIntroductionA Special Purpose Audit Report is a type of audit report specifically tailored to meet the specific needs of a particular user of financial statements. Unlike a general purpose audit report, which is conducted in accordance with generally accepted auditing standards, a special purpose audit report is focused on specific aspects of an organization's financial statements or operations. This type of audit report is often requested by stakeholders who have a specific interest in certain elements of an organization's financial information.Objectives of a Special Purpose Audit ReportThe main objectives of a special purpose audit report are as follows:- To provide assurance on specific aspects of an organization's financial statements or operations.- To meet the specific needs of a particular user of financial statements.- To provide reliable and relevant information to stakeholders who have a specific interest in certain elements of an organization's financial information.Key Features of a Special Purpose Audit ReportSome key features of a special purpose audit report include:- Limited Scope: A special purpose audit report typically has a limited scope, focusing on specific aspects of an organization's financial statements or operations.- Specific Criteria: The auditor may use specific criteria or benchmarks to evaluate the information provided in the audit report.- Tailored Reporting: The audit report is tailored to meet the specific needs of the user and may include additional information or analysis not typically found in a general purpose audit report.Example of a Special Purpose Audit ReportBelow is an example of a special purpose audit report:Independent Auditor's ReportTo the Board of DirectorsABC CompanyWe have audited the balance sheet of ABC Company as at December 31, 20XX, and the related statements of income, changes in equity, and cash flows for the year then ended. This audit was conducted in accordance with the specific criteria agreed upon by management and the Board of Directors.In our opinion, the financial statements present fairly, in all material respects, the financial position of ABC Company as at December 31, 20XX, and the results of its operations and its cash flows for the year then ended, in accordance with the specific criteria agreed upon by management and the Board of Directors.[Signature][Name of Audit Firm][Date]ConclusionSpecial Purpose Audit Reports play a key role in providing stakeholders with specific information tailored to meet their needs. By focusing on specific aspects of an organization's financial statements or operations, these reports can providerelevant and reliable information to stakeholders who have a specific interest in certain elements of an organization's financial information.篇2Special Purpose Audit ReportIntroductionA special purpose audit report is a type of audit report that is tailored to meet the specific needs and requirements of a particular client or situation. Unlike a standard audit report, which is conducted in accordance with generally accepted auditing standards, a special purpose audit report is conducted based on the specific requirements agreed upon between the auditor and the client.Purpose of a Special Purpose Audit ReportThe purpose of a special purpose audit report is to provide assurance on specific financial information or aspects of an organization's operations. This type of audit report is often requested by clients who have specific concerns or needs that go beyond the scope of a standard audit.Key Components of a Special Purpose Audit Report1. Scope of the Audit: The scope of a special purpose audit report is defined by the specific requirements agreed upon between the auditor and the client. This may include specific financial information, operational processes, or internal controls.2. Compliance with Applicable Standards: While a special purpose audit report is not conducted in accordance with generally accepted auditing standards, the auditor is still required to comply with other relevant standards, such as the International Standards on Auditing.3. Opinion: The special purpose audit report will typically include an opinion on the specific financial information or aspects of operations that were audited. This opinion will be based on the audit procedures performed by the auditor.4. Management's Responsibilities: The report may also include a section outlining management's responsibilities in relation to the audit, such as providing access to relevant information and cooperating with the auditor.ConclusionIn conclusion, a special purpose audit report is a tailored audit report that is conducted to meet the specific needs and requirements of a particular client or situation. While it may notfollow the same standards as a standard audit report, a special purpose audit report still provides valuable assurance on specific financial information or aspects of an organization's operations. If you have any further questions about special purpose audit reports, please feel free to reach out to us for more information.篇3Special Purpose Audit ReportIntroductionA special purpose audit report is a type of audit report that is tailored to meet the specific needs of a particular client or situation. Unlike a general purpose audit report, which is intended for a wider audience, a special purpose audit report is typically prepared for the entity's management, investors, creditors, or other parties with a specific interest in the entity's financial statements.Purpose of a Special Purpose Audit ReportThe purpose of a special purpose audit report is to provide assurance on specific aspects of the entity's financial statements. This may include verifying the accuracy of certain items, such as revenue, expenses, or assets, in order to address concerns raised by management, investors, or creditors. The scope of a specialpurpose audit report is limited to the specific areas identified by the client, and the auditor's procedures are designed to meet the client's specific needs.Key Components of a Special Purpose Audit ReportA special purpose audit report typically includes the following key components:1. Introduction: This section provides an overview of the purpose and scope of the audit, as well as the responsibilities of the auditor and management.2. Management's Representations: In this section, management confirms its responsibility for the financial statements and acknowledges its role in preparing and presenting the information.3. Auditor's Opinion: The auditor provides an opinion on the specific items or aspects of the financial statements that were audited, based on the procedures performed.4. Findings and Recommendations: The audit report may include findings and recommendations related to the specific areas examined, as well as any weaknesses or deficiencies identified during the audit.5. Appendices: Additional information, such as supporting documentation or audit evidence, may be included in appendices to the report.ConclusionIn conclusion, a special purpose audit report is a tailored audit report that is prepared to meet the specific needs of a client or situation. The report provides assurance on specific aspects of the entity's financial statements, as identified by the client, and is designed to address the concerns of management, investors, creditors, or other interested parties. By focusing on the specific areas of interest, a special purpose audit report can provide targeted insights and recommendations to help the client achieve its objectives.。

奥迪特个人工作总结英文

Introduction:As an auditor, I have completed a variety of audit projects over the past year, which have allowed me to gain valuable experience and enhance my professional skills. In this personal work summary, I will discuss the key achievements, challenges, and insights I have gained during my audit work.1. Key Achievements:a. Successful Completion of Audit Projects:I have successfully completed multiple audit projects, including financial statement audits, internal control assessments, and compliance audits. These projects have been completed within the stipulated timeframes and budgets, and the audit reports have been well-received by clients.b. Enhanced Technical Skills:Through my audit work, I have developed a strong understanding of various accounting standards and auditing practices. I have gained expertise in financial statement analysis, risk assessment, and internal control evaluation. This has enabled me to provide accurate andinsightful audit opinions.c. Effective Communication:I have honed my communication skills by working closely with clients, colleagues, and other stakeholders. I have effectively communicated audit findings, recommendations, and conclusions, ensuring that all parties are well-informed and engaged in the audit process.2. Challenges:a. Time Management:Managing multiple projects simultaneously has been a challenge. I have had to prioritize tasks, allocate resources efficiently, and meet tight deadlines. This has required me to develop strong time management skills and adaptability.b. Handling Complex Issues:Occasionally, I have encountered complex accounting and auditing issues that required extensive research and analysis. Navigating these challenges has helped me expand my knowledge base and develop problem-solving skills.c. Adapting to Client Expectations:Different clients have varying expectations regarding audit processesand outcomes. Balancing client needs with professional standards has been a challenge. I have learned to be flexible and communicate effectively to meet client expectations while maintaining the integrity of the audit process.3. Insights and Learning:a. The Importance of Professional Judgment:Throughout my audit work, I have realized that professional judgment plays a crucial role in providing accurate audit opinions. It isessential to exercise sound judgment when assessing risks, evaluating evidence, and forming conclusions.b. Continuous Improvement:Audit work is dynamic, and new challenges arise regularly. To stay ahead, I have learned the importance of continuous learning and professional development. I have attended various training programs and workshops to enhance my knowledge and skills.c. Teamwork and Collaboration:Audit projects often require collaboration with colleagues and other stakeholders. I have learned the value of teamwork and effective communication in achieving common goals and delivering high-qualityaudit services.Conclusion:As an auditor, I have gained valuable experience and developed a strong skill set over the past year. The challenges I have faced have helped me grow both professionally and personally. I am committed to continuous improvement and look forward to contributing further to the success of my organization.。

审计五要素 英语作文

审计五要素英语作文Audit Five Elements。

Introduction。

Audit is an essential process that ensures the accuracy and reliability of financial statements. There are five key elements of an audit, which include planning, internal control evaluation, substantive procedures, reporting, and follow-up. In this essay, we will discuss each of these elements in detail and highlight their importance in the auditing process.Planning。

The first element of an audit is planning. This involves setting objectives, identifying risks, and developing an audit plan. During the planning phase, auditors gather information about the client's business, industry, and regulatory environment. They also assess theclient's internal controls to determine the extent oftesting required. Proper planning is crucial as it helps auditors allocate resources efficiently and effectively.Internal Control Evaluation。

通过内部审核英语作文

通过内部审核英语作文Internal Audit。

Internal audit is a crucial function within an organization that helps ensure the effectiveness of its operations, risk management, and internal controls. It involves the independent and objective examination of an organization's activities to provide assurance that they are being carried out in accordance with established policies and procedures.The internal audit process typically involves the following steps:1. Planning: This involves determining the scope and objectives of the audit, as well as the resources and time required to complete it.2. Fieldwork: This is where the audit team collects and analyzes information, tests controls, and identifies areasof risk and potential improvement.3. Reporting: The audit team presents its findings and recommendations to management, highlighting anydeficiencies or areas of concern that need to be addressed.4. Follow-up: Management is responsible for implementing the audit recommendations and monitoring progress to ensure that the necessary changes are made.Internal audit plays a critical role in helping organizations achieve their objectives by providing independent and objective assurance on the effectiveness of their governance, risk management, and internal controls.It helps organizations identify areas of improvement, mitigate risks, and enhance overall performance.In addition to providing assurance to management and the board of directors, internal audit also serves as a valuable resource for external stakeholders, such as regulators, investors, and customers. By demonstrating that the organization has effective internal controls in place,internal audit can help build trust and credibility with these stakeholders.Overall, internal audit is an essential function that helps organizations operate more efficiently, effectively, and ethically. By conducting regular audits and providing actionable recommendations, internal audit can help organizations identify and address issues before they escalate into major problems. It is a key component of good governance and risk management, and organizations that invest in internal audit are better positioned to achieve their strategic objectives and maintain long-term success.。

confirmation for undergoing the remote audit -回复

confirmation for undergoing the remote audit-回复中括号内的主题是“确认参加远程审计”。

远程审计是指通过远程技术手段进行审计活动,而不需要审计师到现场进行实地检查和测试。

尤其在当前全球爆发的COVID-19疫情下,远程审计成为一种主要的审计方式,以确保安全、高效地完成审计工作。

本文将详细介绍远程审计的步骤和回答一些常见问题。

一、了解远程审计的背景和目的(约200字)远程审计是近年来随着技术的发展而兴起的一种审计方式。

通过远程技术手段,审计师能够远程访问被审计单位的系统、数据、文件等信息。

远程审计的目的是确保审计工作的准确性和有效性,并促进审计过程的高效率。

二、核实并确认远程审计的安排和要求(约300字)在确认参加远程审计之前,需要核实并确认远程审计的具体安排和要求。

首先,审计师需与被审计单位的相关负责人进行沟通,了解被审计单位的信息系统架构、访问权限、安全措施等。

其次,审计师和被审计单位需要协商并确定远程审计的时间安排、审计范围和审计目标。

三、准备远程审计所需的技术设备和软件(约400字)远程审计需要准备相应的技术设备和软件。

首先,审计师需要具备一台稳定的电脑或笔记本电脑,并安装远程访问软件。

其次,被审计单位需要提供远程访问的权限和账号,以便审计师能够远程登录被审计单位的系统。

此外,为了保证通信质量,稳定的互联网连接也是必需的。

四、开展远程审计前的准备工作(约400字)在进行远程审计之前,需要进行一些准备工作。

首先,审计师需要了解被审计单位的业务特点和风险情况,并制定相应的审计方案。

其次,审计师需与被审计单位的相关人员进行会议或电话沟通,明确审计过程中可能涉及的问题和需要提供的信息。

最后,审计师和被审计单位需要签订远程审计的合同或协议,明确双方的权利和义务。

五、开展远程审计并记录审计结果(约400字)在进行远程审计时,审计师使用远程访问软件登录被审计单位的系统,并通过远程方式对被审计单位的数据、文件、程序等进行审查和测试。

Chapter01TheDema...

Chapter01 The Demand for Audit and Other Assurance Services(审计学-英文版)The Demand for Audit and Other Assurance ServicesChapter 1Learning Objective 1Describe auditing4>>.Nature of AuditingAuditing is the accumulation and evaluationof evidence about information to determineand report on the degree of correspondencebetween the information and established criteria>.Auditing should be done by 7><a competent,independent person>.Information and Established CriteriaTo do an audit, there must be information in <averifiable form and some standards (criteria)by which the auditor can evaluate the information>.Accumulating Evidence and Evaluating EvidenceEvidence is any information used by the auditorto determine whether the information beingaudited is stated in accordance with theestablished criteria>.Competent, Independent PersonThe auditor must be qualified to understand thecriteria used and must be competent to knowthe types and amount of evidence to accumulateto reach the proper conclusion after theevidence has been examined>.The competence of the individual performingthe audit is of little value if he or she is biased in the accumulation and evaluation of evidence>. ReportingThe final stage in the auditing process is preparing the Audit Report, which is the communicationof the auditor’s findings to users>.Audit of <a Tax Return ExampleInternalrevenueagentCompetent,independentpersonExamines cancelledchecks and othersupporting recordsAccumulates andevaluates evidenceDeterminescorrespondenceFederal taxreturns filedby taxpayerInformationInternal RevenueCode and allinterpretationsEstablished criteriaReport on taxdeficienciesReport on resultsLearning Objective 2Distinguish betweenauditing and accounting>.Distinguish BetweenAuditing and AccountingAccounting is the recording, classifying, and summarizing of economic eventsfor the purpose of providing financial information used in decision making>. Auditing is determining whetherrecorded information properlyreflects the economic events that occurred during the accounting period>. Learning Objective 3Explain the importanceof auditing in reducinginformation risk>.Economic Demandfor AuditingInformation risk reflects the possibility that the information upon which the businessrisk decision was made was inaccurate>. Auditing can have <a significant effecton information risk>.Learning Objective 4List the causes of informationrisk, and explain how thisrisk may be reduced>.Causes of Information RiskRemoteness of informationBiases and motives of the providerVoluminous dataComplex exchange transactionsReducing Information RiskUser verifies information>.User shares information risk with management>. Audited financial statements are provided>. Capital Costs to Shrink: Elliott’s Example Assuming <a cost of capital of 13%, Elliottestimates this rate is composed of the following: 5>.5% risk-free interest rate3>.5% economic risk premium (business risk)4>.0% information cost (information risk)Capital Costs to Shr ink: Elliott’s ExampleElliott believes the following factors will drastically reduce information risk:Advanced technologyNew accounting and auditing standardsAuditors finding more efficient ways to audit Learning Objective 5Describe assurance servicesand distinguish audit servicesfrom other assurance andnonassurance servicesprovided by CPAs>.Assurance ServicesAssurance services are professionalservices that improve the quality ofinformation for decision makers>.Assurance services can beperformed by CPAs or by<a variety of other professionals>.Attestation ServicesAn attestation service is <a type of assuranceservice in which the CPA firm issues <areport about the reliability of an assertionthat is the responsibility of another party>.Attestation Services1>. Audit of historical financial statements2>. Effectiveness of internal control overfinancial reporting3>. Review of historical financial statements4>. Other attestation servicesRelationships Among Auditors, Client, and External Users ClientAuditorClient or auditcommittee hiresauditorExternalUsersAuditor issuesreport reliedupon by usersOther Assurance ServicesMost of the other assurance services that CPAsprovide do not meet the formal definitionof attestation services>.The CPA is not required to issue <a written report>.The assurance does not have to be about the reliability of another party’s assertion about compliance with specified criteria>.AICPA Assurance ServicesThe AICPA formed the Special Committeeon Assurance Services (SCAS)>.Assurance Services on Information Technology The growth of the Internet and new waysof conducting business electronically(e-commerce) is driving the demandfor other assurance services>.Assurance Services on Information Technology WebTrust is an attestation service, and the WebTrust seal is <a symbolic representationof the CPA’s report on management’s assertions about its disclosure ofelectronic commerce practices>.Assurance Services on Information Technology SysTrust is an attest-type engagementto evaluate and test system reliability in areas such as security and data integrity>. Principles for WebTrust and SysTrust Services1>. Online privacy2>. Security3>. Processing integrity4>. Availability5>. Confidentiality6>. Certification authorities (WebTrust only) Other AssuranceServices ExamplesControls over and risks related to investments, including policies related to derivatives…assessing the processes in <a company’s investment practices to identify risks and to determine the effectiveness of those processes>. Other AssuranceServices ExamplesAssess risks of accumulation, distribution,and storage of digital information…assessing security risks and relatedcontrols over data and other informationstored electronically, including theadequacy of backup and off-site storage>.Other AssuranceServices ExamplesFraud and illegal acts risk assessment…developing fraud risk profiles and assessing the adequacy of company systems and policies in preventing and detecting fraud and illegal acts>. Other AssuranceServices ExamplesCompliance with trading policies and procedures Compliance with entertainment royalty agreements ISO 900 certificationEnvironmental auditAssurance, Attestation, and Nonassurance Services Other Assurance ServicesCertainManagementConsultingOther Attestation Services(e>.g>., WebTrust, SysTrust)ATTESTATION SERVICESAuditsReviewsInternal Controlover Financial ReportingASSURANCE SERVICESAssurance, Attestation, and Nonassurance Services CertainManagementConsultingNONASSURANCE SERVICESOther ManagementConsultingTaxServicesAccounting andBookkeepingLearning Objective 6Differentiate the threemain types of audits>.Types of AuditsOperational AuditExampleEvaluate computerized payroll system for efficiency and effectiveness InformationNumber of records processed, costs of the department, and number of errors EstablishedCriteriaCompany standards for efficiency and effectiveness in payroll department AvailableEvidenceError reports, payroll records, and payroll processing costsCompliance AuditExampleDetermine whether bank requirements for loan continuation have been met InformationCompany recordsEstablishedCriteriaLoan agreement provisionsAvailableEvidenceFinancial statements and calculations by the auditor Financial Statement AuditExampleAnnual audit of Boeing’sfinancial statementsInformationBoeing's financial statements EstablishedCriteriaGenerally accepted accounting principlesAvailableEvidenceDocuments, records, and outside sources of evidenceLearning Objective 7Identify the primarytypes of auditors>.Types of AuditorsInternal auditorsCertified public accounting firms Internal revenue agentsGeneral accounting office auditors Learning Objective 8Describe the requirementsfor becoming <a CPA>.Three Requirements forBecoming <a CPAEducational requirementUniform CPA examination requirement Experience requirementCPA Examination SectionsAuditing and AttestationFinancial Accounting and Reporting RegulationBusiness Environments and Concepts End of Chapter 1。

Mechanical Engineering Auditing (continued)

Mechanical Engineering Auditing(continued)As a mechanical engineering auditor, it is essential to approach the task with a meticulous and detail-oriented mindset. Auditing in this field involves evaluating the design, production, and maintenance of mechanical systems, ensuring compliance with industry standards and regulations. It requires a comprehensive understanding of mechanical principles, materials, and manufacturing processes. The role of a mechanical engineering auditor is crucial in upholding the safety, reliability, and efficiency of mechanical systems in various industries. One of the primary aspects of mechanical engineering auditing is to assess the design and specifications of mechanical components and systems. This involves reviewing technical drawings, materials selection, and adherence to engineering standards.It is imperative to verify that the design meets the functional requirements andis capable of withstanding the anticipated operating conditions. This aspect of auditing requires a keen eye for detail and a thorough understanding of mechanical design principles. In addition to design evaluation, mechanical engineering auditing also encompasses the assessment of manufacturing processes and quality control measures. This involves inspecting production facilities, reviewingquality assurance procedures, and ensuring compliance with relevant codes and standards. It is essential to identify any potential issues that could compromise the integrity or performance of mechanical components during the manufacturing process. Furthermore, as a mechanical engineering auditor, it is crucial to evaluate the maintenance and operation of mechanical systems. This involves reviewing maintenance records, conducting on-site inspections, and identifying any areas of concern or potential improvement. The goal is to ensure that the systems are being maintained in a manner that promotes longevity, reliability, and safety. From a broader perspective, mechanical engineering auditing plays a vital role in enhancing overall operational efficiency and risk management. By identifying and addressing potential design flaws, manufacturing defects, or maintenance deficiencies, auditors contribute to the optimization of mechanical systems. Moreover, thorough auditing can mitigate the risk of costly failures, downtime, orsafety hazards, ultimately contributing to the overall success and sustainability of the organization. Emotionally, the role of a mechanical engineering auditor can be both challenging and rewarding. It requires a sense of responsibility and accountability in upholding the highest standards of quality and safety. The satisfaction of knowing that thorough auditing efforts contribute to thereliability and safety of mechanical systems can be a driving force in this role. However, the attention to detail and the need for constant vigilance can also create pressure and a sense of burden. Nevertheless, the opportunity to make a tangible impact on the functionality and safety of mechanical systems can be incredibly fulfilling. In conclusion, mechanical engineering auditing is a multifaceted and critical aspect of ensuring the reliability, safety, and efficiency of mechanical systems. It encompasses design evaluation, manufacturing assessment, and maintenance review, all of which are essential in upholding industry standards and mitigating operational risks. The role of a mechanical engineering auditor requires not only technical expertise but also a strong sense of diligence and commitment to promoting the highest standards of quality and safety.。

Sample midterm

Sample Midterm forRisk Management: Applications to Financial FirmsMultiple Choice1.No matter what happens, a call option can never be worth more than the stock.a.Trueb. Falsec.Not if dividend yield is higher than the risk free rate2.DeadBeat stock has dropped from $100 to $3 in the last year, since its technology is now obsolete. Afriend is offering to sell you an at the money American put with maturity of 5 years for a premium of $4. Do you:a.Grab this opportunity and buy the putb.Pass on thi s opportunity (and never speak to this …friend‟ again)c.I‟m not sure, since the question setup doesn‟t talk about dividends at all3. A forward contract is usually tradeda.Over the counterb.On the Chicago Mercantile exchangec.On the NYMEX4.True or False. A forward is better than a future because it has lower credit risk.a.Trueb.False5.After a futures transaction the open interest:a.Increasesb.Decreasesc.Stays the samed.All of the above are possibleQuantitative Problems1.The spot price of oil is $80 per barrel and the cost of storing a barrel of oil for one year is $3,payable at the end of the year. The risk-free interest rate is 5% per annum, continuouslycompounded. What is an upper bound for the one-year futures price of oil?2. A trader owns 55,000 troy oz of silver and decides to hedge with 6-month silver futures contracts.Each futures contract is on 5,000 troy oz. The standard deviation of the change in the spot price of silver is 0.43. The standard deviation of the change in silver futures prices is 0.40. The coefficient of correlation between the two is 0.95.3.The LIBOR zero curve is flat at 5% (continuously compounded) out to 1.5 years. Swap rates for2- and 3-year semiannual pay swaps are 5.4% and 5.6%, respectively. Estimate the LIBOR zero rates for maturities of 2.0, 2.5, and 3.0 years. (Assume that the 2.5-year swap rate is the averageof the 2- and 3-year swap rates and use LIBOR discounting.) 4.Suppose that a corporate treasurer said: “I will have £1 million to sell in six months. If the exchange rate is less than 1.41, I want you to give me 1.41. If it is greater than 1.47 I will accept 1.47. If the exchange rate is between 1.41 and 1.47, I will sell the sterling for the exchange rate.” How could you use options to satisfy the treasurer? 5. Suppose that F 1 and F 2 are two futures contracts on the same commodity with times to maturity, t 1and t 2, where t 2>t 1. Prove that21()21r t t F Fe -≤ where r is the interest rate (assumed constant) and there are no storage costs. For the purposes of this problem, assume that a futures contract is the same as a forward contract.。

X139_Midterm Exam

University of California, Berkeley ExtensionIntegrated‐Circuit Design and Techniques ProgramX139: Advanced Analog MicroelectronicsMidterm Exam (Take‐home Exam)Midterm Instructions:A. Due dateThis midterm should be done and submitted within 120 days from your registration date.B. Answering format & grading philosophyRather than just give the value in your answer, you should write down a comprehensive reasoning process. Remember, showing your work—the reasoning process—is much more important than displaying an answer.Full credit: You will receive full credit only if both reasoning (either derivation or analysis‐by‐inspection) and answer are correct.Partial credit: You will receive partial credit if reasoning is correct and the answer is wrong.Zero credit: You won’t receive any credit if reasoning is wrong even though your final answer is correct.C. Submitting formatAcceptable format:•Submit assignments as attachments (not as in‐line text) using PDF or Word.• Hand‐writing answers first, scanning and converting into PDF format is acceptable.•Do not submit the homework separately via two or three emails.Preferable format: (See Homework Example)•PDF with the bookmarks indicating Prob.1, Prob.2, etc.•Display the bookmarks for the initial view.D. Special note about proctored final examAfter submitting this midterm, you should begin making arrangements for your proctored final exam, complete a Required Proctor Information Form, and then submit it to the office via email or fax.[X139: Advanced Analog Microelectronics Midterm Exam] Page 1Midterm problems:1. Noninverting Amplifier/Series ‐Shunt Feedback (20 points)For the OPAMP ‐based noninverting amplifier shown below, use the negative feedback theory to analyze the closed ‐loop characteristics .(a) Derive the expression for the input resistance .in R (b) Derive the expression for the output resistance .out R (c) Derive the expression for the close ‐loop voltage gain s o vf V V A /=.[X139: Advanced Analog Microelectronics Midterm Exam ] Page 2For the sinusoidal oscillator circuit shown in the figure, suppose )k 32,k 18(),(11ΩΩ=b a R R mA 11.0. Assume the diode 1N4148 presents at the forward current of V 5.0=D V =D I . (a) Calculate the value of the loop gain βA at the frequency of oscillation. (b) Estimate the amplitude of the steady state waveform at node A.[X139: Advanced Analog Microelectronics Midterm Exam ] Page 3For the noninverting bistable multivibrator shown in the figure, assume the rated output voltages of the op amp are . Sketch the voltage transfer characteristic ( vs. ) with the values marked on the break points.V 5±O v I v[X139: Advanced Analog Microelectronics Midterm Exam ] Page 44. Case Study: Circuit Identity (40%)Assume the op amp shown in the circuit is ideal,Ω=k 0,102R Ω=k 3R ,5=504e the Zener diode presents the forward voltage of 0.5V and the breakdown voltage of 5V. and Suppos Ωk R .(a) Let , what is the small ‐signal voltage gain Ω=k 201R I O v ?(b) Let , sketch the transfer characteristics v vs. . Specify the values at the breakpoints.Ω=k 51R O I v[X139: Advanced Analog Microelectronics Midterm Exam ] Page 5。

内审管理程序--中英文对照

TITLE : CORPORATE PROCEDURE FOR INTERNAL AUDIT内审之管制程序Document No.: QA20001 Rev. No. : A00 Page 1 of 12Revision HistoryREV DCN # INITIATEDBYEFFECTIVEDATE(MM/DD/YY)DESCRIPTIONA00 WilliamMagramoInitial ReleaseApproved DCN on File in Document ControlAPPROVED BY Motoaki Wakui AUTHORIZED BY SK LamCONFIDENTIALPROPERTY OF ZHONGSHAN SUNMING OPTICAL TECHNOLOGIES LIMITEDThis document, and the information it contains, are the property of Zhong shan Sunming Optical Technologies Limited and are protected by law. Both must be held in strict confidence at all times. No license expressed or implied, under any patent, copyright or other intellectual property right is granted or implied by the provision or possession of this document. No part of this document may be reproduced, transmitted, transcribed, stored in a retrieval system, translated into any language or computer language, in any form or by any means,whatsoever, without the prior written consent ofZhongshan Sunming Optical Technologies Limited.©2014 ZHONGSHAN SUNMING OPTICAL TECHNOLOGIES LIMITED1.0 PURPOSE 目的To establish a procedure in the planning, management, conduct and documenting of InternalAudits against SUNMING policies, procedures and work instructions in order to verify that they are effectively implemented and maintained and to identify areas for improvement.为规划,管理,引导及内审记录建立程序以对比SUNMING的政策,程序及作业指导书以便检验它们是否得到了有效的执行及维护,在确定的范围是否得到改善。

计算机类翻译案例中英对照

妙文翻译公司翻译样稿审计信息系统Audit Information System在计算机审计项目中,审计组以审前调查获取的信息为基础,以审计中间表数据构成的审计数据库为中心,涵盖与该审计项目相关的人员组织、工作安排等相关管理信息和其他信息,建立审计信息系统,作为审计项目资源的共享和管理平台。

审计信息系统主要由审前调查获取的信息、审计数据库和审计项目管理及其他信息三大部分组成,并随着审计项目资源信息的不断增加而不断丰富完善。

审计分析模型Audit Analysis Model审计分析模型是审计人员用于数据分析的数学公式或逻辑表达式,它是按照审计事项应该具有的性质或数量关系,由审计人员通过设定计算、判断或限制条件来建立起来的,用于验证审计事项实际的性质或数量关系,从而对被审计单位经济活动的真实、合法、效益情况做出科学的判断。

审计分析模型有多种表现形态:用在查询分析中,表现为一个或一组查询条件;用在多维分析中,表现为切片、切块、旋转、钻取、创建计算成员、创建计算单元等;用在挖掘分析中,表现为设定挖掘条件。

按照在审计中的不同功能,可以将审计分析模型具体划分为系统分析模型、类别分析模型和个体分析模型三大类型。

系统分析模型System Analysis Model系统分析模型是审计分析模型的一种,属于总体分析模型的范畴,主要用于对被审计单位的数据进行整体层次上的全面、系统分析,发现趋势、异常,帮助审计人员把握被审计单位的总体情况。

类别分析模型Classification Analysis model类别分析模型是审计分析模型的一种,属于总体分析模型的范畴,是系统分析模型的细化和延伸。

类别分析模型主要是按业务类别对审计数据进行分析,指引审计人员发现和锁定重点审计的内容、范围。

个体分析模型Specific-Issues-Oriented Analysis个体分析模型是审计分析模型的一种,是对审计重点的进一步深入分析,主要目的是通过不同角度的分析来核查问题,筛选线索,为下一步的延伸取证提供明确具体的目标。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。