Balance Sheet and Statement of Cash Flows

关于财务管理的英文单词

记帐:Bookkeeping Service对帐:Auditing Service联行:Associated Banks Service 或Affiliated Banks Service(我还是不明白这与5有何区别,但Associated和Affiliated不是动词原形,是形容词)代理业务: Agency Service银行卡接柜:Inter-Bank Bankcard Business Service现金审批:Cash Approval Service开销户: Account Opening/Closing Service开户的标牌还可以用:New Account/New Clientbig macs, big/large-cap stock, mega-issue 大盘股offering, list 上市bourse 证交所Shanghai Exchange 上海证交所pension fund 养老基金share 股票valuation 股价underwriter 保险商government bond 政府债券saving account 储蓄账户equity market 股市shareholder 股东delist 摘牌inventory 存货traded company, trading enterprise 上市公司market fundamentalist 市场经济基本规则damage-control machinery 安全顾问efficient market 有效市场opportunistic practice 投机行为entrepreneur 企业家cook the book 做假账regulatory system 监管体系portfolio 投资组合money-market 短期资本市场capital-market 长期资本市场volatility 波动diversification 多元化real estate 房地产option 期权call option 看涨期权put option 看跌期权merger 并购arbitrage 套利Securities and Exchange Commission 〈美〉证券交易委员会dollar standard 美元本位制budget 预算deficit 赤字bad debt 坏账macroeconomic 宏观经济fiscal stimulus 财政刺激a store of value 保值transaction currency 结算货币forward exchange 期货交易intervention currency 干预货币Treasury bond 财政部公债pickup in price 物价上涨Federal Reserve 美联储inflation 通货膨胀deflation 通货紧缩tighter credit 紧缩信贷monetary policy 货币政策foreign exchange 外汇spot transaction 即期交易forward transaction 远期交易quote 报价常见银行英语词汇account number 帐目编号depositor 存户pay-in slip 存款单a deposit form 存款单a banding machine 自动存取机to deposit 存款deposit receipt 存款收据private deposits 私人存款certificate of deposit 存单deposit book, passbook 存折credit card 信用卡principal 本金overdraft, overdraw 透支to endorse 背书endorser 背书人to cash 兑现to honor a cheque 兑付to dishonor a cheque 拒付to suspend payment 止付cheque,check 支票cheque book 支票本crossed cheque 横线支票blank cheque 空白支票rubber cheque 空头支票cheque stub, counterfoil 票根cash cheque 现金支票traveler's cheque 旅行支票cheque for transfer 转帐支票outstanding cheque 未付支票canceled cheque 已付支票forged cheque 伪支票Bandar's note 庄票,银票banker 银行家president 行长savings bank 储蓄银行Chase Bank 大通银行National City Bank of New York 花旗银行Hongkong Shanghai Banking Corporation 汇丰银行Chartered Bank of India, Australia and China 麦加利银行Banque de I'IndoChine 东方汇理银行central bank, national bank, banker's bank 中央银行bank of issue, bank of circulation 发行币银行commercial bank 商业银行,储蓄信贷银行member bank, credit bank 储蓄信贷银行discount bank 贴现银行exchange bank 汇兑银行requesting bank 委托开证银行issuing bank, opening bank 开证银行advising bank, notifying bank 通知银行negotiation bank 议付银行confirming bank 保兑银行paying bank 付款银行associate banker of collection 代收银行consigned banker of collection 委托银行clearing bank 清算银行local bank 本地银行domestic bank 国内银行overseas bank 国外银行unincorporated bank 钱庄branch bank 银行分行trustee savings bank 信托储蓄银行trust company 信托公司financial trust 金融信托公司unit trust 信托投资公司trust institution 银行的信托部credit department 银行的信用部commercial credit company(discount company) 商业信贷公司(贴现公司)neighborhood savings bank, bank of deposit 街道储蓄所credit union 合作银行credit bureau 商业兴信所self-service bank 无人银行land bank 土地银行construction bank 建设银行industrial and commercial bank 工商银行bank of communications 交通银行mutual savings bank 互助储蓄银行post office savings bank 邮局储蓄银行mortgage bank, building society 抵押银行industrial bank 实业银行home loan bank 家宅贷款银行reserve bank 准备银行chartered bank 特许银行corresponding bank 往来银行merchant bank, accepting bank 承兑银行investment bank 投资银行import and export bank (EXIMBANK) 进出口银行joint venture bank 合资银行money shop, native bank 钱庄credit cooperatives 信用社clearing house 票据交换所public accounting 公共会计business accounting 商业会计cost accounting 成本会计depreciation accounting 折旧会计computerized accounting 电脑化会计general ledger 总帐subsidiary ledger 分户帐cash book 现金出纳帐cash account 现金帐journal, day-book 日记帐,流水帐bad debts 坏帐investment 投资surplus 结余idle capital 游资economic cycle 经济周期economic boom 经济繁荣economic recession 经济衰退economic depression 经济萧条economic crisis 经济危机economic recovery 经济复苏inflation 通货膨胀deflation 通货收缩devaluation 货币贬值revaluation 货币增值international balance of payment 国际收支favourable balance 顺差adverse balance 逆差hard currency 硬通货soft currency 软通货international monetary system 国际货币制度the purchasing power of money 货币购买力money in circulation 货币流通量note issue 纸币发行量national budget 国家预算national gross product 国民生产总值public bond 公债stock, share 股票debenture 债券treasury bill 国库券debt chain 债务链direct exchange 直接(对角)套汇indirect exchange 间接(三角)套汇cross rate, arbitrage rate 套汇汇率foreign currency (exchange) reserve 外汇储备foreign exchange fluctuation 外汇波动foreign exchange crisis 外汇危机discount 贴现discount rate, bank rate 贴现率gold reserve 黄金储备money (financial) market 金融市场stock exchange 股票交易所broker 经纪人commission 佣金bookkeeping 簿记bookkeeper 簿记员an application form 申请单bank statement 对帐单letter of credit 信用证strong room, vault 保险库equitable tax system 等价税则specimen signature 签字式样banking hours, business hours 营业时间(Consumer Price Index) 消费者物价指数business 企业商业业务financial risk 财务风险sole proprietorship 私人业主制企业partnership 合伙制企业limited partner 有限责任合伙人general partner 一般合伙人separation of ownership and control 所有权与经营权分离claim 要求主张要求权management buyout 管理层收购tender offer 要约收购financial standards 财务准则initial public offering 首次公开发行股票private corporation 私募公司未上市公司closely held corporation 控股公司board of directors 董事会executove director 执行董事non- executove director 非执行董事chairperson 主席controller 主计长treasurer 司库revenue 收入profit 利润earnings per share 每股盈余return 回报market share 市场份额social good 社会福利financial distress 财务困境stakeholder theory 利益相关者理论value (wealth) maximization 价值(财富)最大化common stockholder 普通股股东preferred stockholder 优先股股东debt holder 债权人well-being 福利diversity 多样化going concern 持续的agency problem 代理问题free-riding problem 搭便车问题information asymmetry 信息不对称retail investor 散户投资者institutional investor 机构投资者agency relationship 代理关系net present value 净现值creative accounting 创造性会计stock option 股票期权agency cost 代理成本bonding cost 契约成本monitoring costs 监督成本takeover 接管corporate annual reports 公司年报balance sheet 资产负债表income statement 利润表statement of cash flows 现金流量表statement of retained earnings 留存收益表fair market value 公允市场价值marketable securities 油价证券check 支票money order 拨款但、汇款单withdrawal 提款accounts receivable 应收账款credit sale 赊销inventory 存货property,plant,and equipment 土地、厂房与设备depreciation 折旧accumulated depreciation 累计折旧liability 负债current liability 流动负债long-term liability 长期负债accounts payout 应付账款note payout 应付票据accrued espense 应计费用deferred tax 递延税款preferred stock 优先股common stock 普通股book value 账面价值capital surplus 资本盈余accumulated retained earnings 累计留存收益hybrid 混合金融工具treasury stock 库藏股historic cost 历史成本current market value 现行市场价值real estate 房地产outstanding 发行在外的a profit and loss statement 损益表net income 净利润operating income 经营收益earnings per share 每股收益simple capital structure 简单资本结构dilutive 冲减每股收益的basic earnings per share 基本每股收益complex capital structures 复杂的每股收益diluted earnings per share 稀释的每股收益convertible securities 可转换证券warrant 认股权证accrual accounting 应计制会计amortization 摊销accelerated methods 加速折旧法straight-line depreciation 直线折旧法statement of changes in shareholders’equity 股东权益变动表source of cash 现金来源use of cash 现金运用operating cash flows 经营现金流cash flow from operations 经营活动现金流direct method 直接法indirect method 间接法bottom-up approach 倒推法investing cash flows 投资现金流cash flow from investing 投资活动现金流joint venture 合资企业affiliate 分支机构financing cash flows 筹资现金流cash flows from financing 筹资活动现金流time value of money 货币时间价值simple interest 单利debt instrument 债务工具annuity 年金future value 终至present value 现值compound interest 复利compounding 复利计算pricipal 本金mortgage 抵押credit card 信用卡terminal value 终值discounting 折现计算discount rate 折现率opportunity cost 机会成本required rate of return 要求的报酬率cost of capital 资本成本ordinary annuity普通年金annuity due 先付年金financial ratio 财务比率deferred annuity 递延年金restrictive covenants 限制性条款perpetuity 永续年金bond indenture 债券契约face value 面值financial analyst 财务分析师coupon rate 息票利率liquidity ratio 流动性比率nominal interest rate 名义利率current ratio 流动比率effective interest rate 有效利率window dressing 账面粉饰going-concern value 持续经营价值marketable securities 短期证券liquidation value 清算价值quick ratio 速动比率book value 账面价值cash ratio 现金比率marker value 市场价值debt management ratios 债务管理比率intrinsic value 内在价值debt ratio 债务比率mispricing 给……错定价格debt-to-equity ratio 债务与权益比率valuation approach 估价方法equity multiplier 权益乘discounted cash flow valuation 折现现金流量模型long-term ratio 长期比率undervaluation 低估debt-to-total-capital 债务与全部资本比率overvaluation 高估leverage ratios 杠杆比率option-pricing model 期权定价模型interest coverage ratio 利息保障比率contingent claim valuation 或有要求权估价earnings before interest and taxes 息税前利润promissory note 本票cash flow coverage ratio 现金流量保障比率contractual provision 契约条款asset management ratios 资产管理比率par value 票面价值accounts receivable turnover ratio 应收账款周转率maturity value 到期价值inventory turnover ratio 存货周转率coupon 息票利息inventory processing period 存货周转期coupon payment 息票利息支付accounts payable turnover ratio 应付账款周转率coupon interest rate 息票利率cash conversion cycle 现金周转期maturity 到期日asset turnover ratio 资产周转率term to maturity 到期时间profitability ratio 盈利比率call provision赎回条款gross profit margin 毛利润call price 赎回价格operating profit margin 经营利润sinking fund provision 偿债基金条款net profit margin 净利润conversion right 转换权return on asset 资产收益率put provision 卖出条款return on total equity ratio 全部权益报酬率indenture 债务契约return on common equity 普通权益报酬率covenant 条款market-to-book value ratio 市场价值与账面价值比率trustee 托管人market value ratios 市场价值比率protective covenant 保护性条款dividend yield 股利收益率negative covenant 消极条款dividend payout 股利支付率positive covenant 积极条款financial statement财务报表secured deht担保借款profitability 盈利能力unsecured deht信用借款viability 生存能力creditworthiness 信誉solvency 偿付能力collateral 抵押品collateral trust bonds 抵押信托契约debenture 信用债券bond rating 债券评级current yield 现行收益yield to maturity 到期收益率default risk 违约风险interest rate risk 利息率风险authorized shares 授权股outstanding shares 发行股treasury share 库藏股repurchase 回购right to proxy 代理权right to vote 投票权independent auditor 独立审计师straight or majority voting 多数投票制cumulative voting 积累投票制liquidation 清算right to transfer ownership 所有权转移权preemptive right 优先认股权dividend discount model 股利折现模型capital asset pricing model 资本资产定价模型constant growth model 固定增长率模型growth perpetuity 增长年金mortgage bonds 抵押债券。

财务管理基础英文版选择题

第一章1 CORRECTWhich of the following are microeconomic variables that help define and explain the discipline of finance? DA) risk and returnB) capital structureC) inflationD) all of the aboveFeedback: All of the above are relevant in explaining finance.2 CORRECTOne primary macroeconomic variable that helps define and explain the discipline of finance? CA) capital structureB) inflationC) technologyD) riskFeedback: Technology is very important in explaining the field of finance.3 CORRECTThe money markets deal with _________. BA) securities with a life of more than one yearB) short-term securitiesC) securities such as common stockD) none of the aboveFeedback: The money markets are concerned with short-term securities, those with a life less than one year.4 CORRECTThe ability of a firm to convert an asset to cash is called ___A_________.A) liquidityB) solvencyC) returnD) marketabilityFeedback: Liquidity also means how close an asset is to cash.5 CORRECTEarly in the history of finance, an important issue was: AA) liquidityB) technologyC) capital structureD) financing optionsFeedback: Maintaining liquidity was a major concern historically.6 INCORRECTThe __________C_________ is the most common form of business organization in the U.S.A) corporationB) partnershipC) sole proprietorshipD) none of the aboveFeedback: There are more sole proprietorships than any other form of business organization.7 CORRECTThe _________C___________ has more sales in dollars than any other form of business organization.A) sole proprietorshipB) partnershipC) corporationD) none of the aboveFeedback: The corporation is the most important in terms of dollars.8 CORRECTOne major disadvantage of the sole proprietorship is _____B___________.A) simplicity of decision-makingB) unlimited liabilityC) low operational costsD) none of the aboveFeedback: The owners of a sole proprietorship are personally liable.9 CORRECTThe appropriate firm goal in a capitalist society is ______B__________.A) profit maximizationB) shareholder wealth maximizationC) social responsibilityD) none of the aboveFeedback: The goal is to maximize the wealth of shareholders.10 CORRECTThe agency problem will occur in a business firm if the goals of ______C______ and shareholders do not agree.A) investorsB) the publicC) managementD) none of the above第二章Feedback: The goals of management may be different from those of shareholders.The accounting statements that a firm is required to file include all but one of these. BA) Balance SheetB) Statement of Accounts ReceivableC) Income StatementD) Statement of Cash FlowsFeedback: The required statements include the income statement, balance sheet and statement of changes in cash flows. The statement of changes in owners equity (or retained earnings) is also required by Generally Accepted Accounting Principles but is not covered in this text.2 CORRECTThe _______A________ shows the firm's operating results over a period of time.A) Income StatementB) Statement of Cash FlowsC) Balance SheetD) None of the aboveFeedback: The Income Statement represents a moving picture of a firm's revenues and expenses.3 CORRECTAll of the following except one are tax-deductible expenses. CA) interest expenseB) depreciationC) common stock dividendsD) income taxesFeedback: Common stock dividends are not tax deductible to a firm.4 CORRECTAll of the following are non-operating expenses except ______B_______.A) interest expenseB) cost of goods soldC) preferred stock dividendsD) taxesFeedback: The cost of goods sold is an operating expense.5 CORRECTBondholders receive _____C________ from the business firm.A) preferred dividend paymentsB) common stock paymentsC) interest paymentsD) royaltiesFeedback: Bondholders are typically paid interest semi-annually.6 CORRECTThe ratio of net income to common shares outstanding is called _____B_________.A) price/earnings ratioB) earnings per shareC) dividends per shareD) none of the aboveFeedback: This is called the earnings per share (EPS).7 CORRECTUsually, firms with high price/earnings ratios are _____A_______ firms.A) growthB) decliningC) matureD) none of the aboveFeedback: A high p/e ratio indicates a firm with strong growth prospects8 CORRECTOne of the limitations of the _____C_______ is that it is based on historical costs.A) income statementB) statement of cash flowsC) balance sheetD) none of the aboveFeedback: The balance sheet uses historical costs.9 INCORRECTA source of funds is a: DA) decrease in a current assetB) decrease in a current liabilityC) increase in a current liabilityD) a and c aboveFeedback: A decrease in current assets is equivalent to an increase in current liabilities.10 INCORRECTShort-term financing for a business firm includes: BA) bondsB) accounts payableC) stockholder's equityD) mortgagesFeedback: The other three answers represent long-term financing.第三章Trend analysis allows a firm to compare its performance to: DA) other firms in the industryB) other time periods within the firmC) other industriesD) all of the aboveFeedback: Trend analysis gives an analyst a long-term perspective. As a security analyst and a portfolio manager with Oppenheimer Capital, Dick Glasebrook spoke to a Senior Finance Managers’ Meeting at the Boeing Company on May 4, 1999. He said it is one thing to compare afirm’s performan ce against competitors within the same industry. But investors are not limited to specific industries. In fact, investors seek to diversify their investments across many different industries. So management should also compare performance to any well run company--both in and outside of their industry.2Ratio analysis allows a firm to compare its performance to: DA) other firms in the industryB) other time periods within the firmC) other industriesD) all of the aboveFeedback: Trend analysis gives an analyst a long-term perspective. As a security analyst and a portfolio manager with Oppenheimer Capital, Dick Glasebrook spoke to a Senior Finance Managers’ Meeting at the Boeing Company on May 4, 1999. He said it is one thing to compare a firm’s performance against competitors within the same industry. But investors are not limited to specific industries. In fact, investors seek to diversify their investments across many different industries. So management should also compare performance to any well run company--both in and outside of their industry.3Usually, a firm's suppliers are most interested in its ___D_____ ratios.A) profitabilityB) debtC) asset utilizationD) liquidityFeedback: The suppliers are most interested in getting paid, as shown by the liquidity of the firm.4 CORRECT__________D_____ would be most interested in a firm's debt utilization ratios.A) bondholdersB) stockholdersC) short-term creditorsD) Both A and BFeedback: Debt is indicated by a firm issuing bonds but is also a function of the debt to equity relationship or the degree of financial leverage. Both bond holders and stockholders are interested in this relationship although frof opposing viewpoints.5 CORRECTThe _______C______ ratio indicates the return firm shareholders are earning.A) return on assetsB) return on investmentC) return on equityD) net profit marginFeedback: The shareholders represent equity, or ownership in the firm.6 CORRECTWhich of the following is an example of a profitability ratio? CA) Quick ratioB) Average collection periodC) Return on equityD) Times interest earnedFeedback: This is the only profitability ratio that is listed. All profitability ratios have net income in the denominator.7Total asset turnover will indicate if there is a problem with the ___C______ ratio.A) debt to assetsB) times interest earnedC) fixed asset turnoverD) currentFeedback: Fixed asset turnover is part of total asset turnover.8 CORRECTAll of the following are asset utilization ratios except: DA) average collection periodB) inventory turnoverC) receivables turnoverD) return on assetsFeedback: Return on assets is a profitability ratio. Any ratio with net income in the denominator is a profitability ratio.9 CORRECTIf a firm's debt ratio is 55%, this means ____C__ of the firm's assets are financed by equity financing.A) 55%B) 50%C) 45%D) not enough information to answer questionFeedback: The equity portion plus the debt portion must add up to 100%.10 CORRECTAll of the following can present problems for ratio analysis except: DA) inflationB) inventory accounting methodsC) disinflationD) all of the aboveFeedback: These all may cause problems.第四章Planning for future growth is called: CA) capital budgetingB) working capital managementC) financial forecastingD) none of the aboveFeedback: This involves looking ahead to the future.2 INCORRECTWhich one of the following is NOT a tool of financial forecasting? BA) cash budgetB) capital budgetC) pro forma balance sheetD) pro forma income statementFeedback: The other three are all tools used by an analyst.3 CORRECTThe first step in developing a pro forma income statement is to: AA) build a sales forecastB) determine the production scheduleC) determine cost of goods soldD) none of the aboveFeedback: A sales forecast begins the process.4 INCORRECTPro forma statements are _B______ statements.A) actualB) projectedC) a previous year'sD) none of the aboveFeedback: Pro forma statements are based on estimates or projections.5 INCORRECTAll of the following compose cost of goods sold except ______D__________.A) raw materialB) laborC) overheadD) all of the above are part of cost of goods soldFeedback: The cost of good sold involves all three of these items.6 INCORRECTFinancial managers use the ______B_______ to plan for monthly financing needs.A) capital budgetB) cash budgetC) pro forma income statementD) none of the aboveFeedback: The cash budget allows for planning cash needs.7 INCORRECTThe payments that a firm collects from its customers are called _______C________.A) cash disbursementsB) cash outflowsC) cash receiptsD) none of the aboveFeedback: Cash receipts represent cash coming into the firm.8 INCORRECTExamples of cash disbursements are all but _________B________.A) payment for materials purchasedB) collection of accounts receivableC) payment of dividendsD) payment of taxesFeedback: The collection of accounts receivable is an example of a cash receipt, not a cash disbursement.9 CORRECTIn developing the pro forma balance sheet, we get common stock from __________A_______.A) the firm's previous balance sheetB) the firm's cash budgetC) the firm's income statementD) none of the aboveFeedback: Common stock appears on the balance sheet.10 INCORRECTThe percent of sales method of financial forecasting shows us the relationship between________D___ and financing needs.A) changes in the level of liabilitiesB) changes in the level of assetsC) changes in debtD) changes in the level of salesFeedback: It compares the relationship between balance sheet items and sales.第五章An example of a semi-variable cost is: DA) rentB) raw materialC) depreciationD) utilitiesFeedback: The other three represent fixed or variable costs.2 CORRECT_________A____ is the point at which firm profit is equal to zero.A) breakevenB) operating breakevenC) financial leverageD) combined breakevenFeedback: This is the point where the firm's revenues equal its expenses.3 INCORRECTIn breakeven analysis, if fixed costs rise, then the breakeven point will _____B_____.A) fallB) riseC) stay the sameD) none of the aboveFeedback: This implies that a larger quantity will have to be sold in order to break even.4 INCORRECTIn the breakeven formula, Price - Variable Cost is called the___C__________.A) breakeven pointB) leverageC) contribution marginD) none of the aboveFeedback: This implies that a larger quantity will have to be sold in order to cover the additional fixed costs and still break even.5 INCORRECTWhich of the following types of firms may operate with high operating leverage? BA) a doctor's officeB) an auto manufacturing facilityC) a mental health clinicD) none of the above would have high operating leverageFeedback: This implies a high break-even point and high operating expenses.6 INCORRECTThe __________C__________ is the percentage change in operating income that results from a percentage change in sales.A) degree of financial leverageB) breakeven pointC) degree of operating leverageD) degree of combined leverageFeedback: This is called the degree of operating leverage (DOL).7 CORRECTIf interest expenses for a firm rise, we know that firm has taken on more ______A________.A) financial leverageB) operating leverageC) fixed assetsD) none of the aboveFeedback: Financial leverage refers to interest expense on debt.8 INCORRECTThe ________B________ is the percentage change in earnings per share that results from a percentage change in operating income.A) degree of combined leverageB) degree of financial leverageC) breakeven pointD) degree of operating leverageFeedback: This is known as the degree of financial leverage (DFL).9 INCORRECTCombined leverage is the percentage change in relationship between sales and ______C______.A) operating incomeB) operating leverageC) earnings per shareD) breakeven pointFeedback: This combines operating leverage and financial leverage.10 INCORRECTA highly leveraged firm is ____B______ risky than its peers.A) lessB) moreC) the sameD) none of the aboveFeedback: Leverage is equivalent to risk, because it implies a higher level of fixed costs.第六章Working capital management involves the financing and management of the __C_____ assets of the firm.A) fixedB) totalC) currentD) none of the aboveFeedback: Working capital management deals with the financing and management of currentassets.2 INCORRECTAn asset sold at the end of a specified time period is called a ______B_______ asset.A) temporary currentB) self-liquidatingC) currentD) permanent currentFeedback: A self-liquidating asset is one that will be sold after a certain amount of time.3 CORRECTFixed assets are usually financed with _______A______ funds.A) long-termB) short-termC) permanentD) none of the aboveFeedback: Fixed assets are by definition long-term assets.4 INCORRECT_________B_____ is usually used to finance self-liquidating assets.A) Long-term financingB) Short-term financingC) Permanent financingD) none of the aboveFeedback: These are short-term or temporary assets.5 INCORRECTShort-term interest rates, in a normal economy, are generally ____C____ than long-term rates.A) higherB) the sameC) lowerD) none of the aboveFeedback: Long-term interest rates are normally higher than short-term interest rates to compensate for uncertainty or risk.6 INCORRECTThe expectations hypothesis says that _____B____ interest rates are a function of _______ interest rates.A) short-term; long-termB) long-term; short-termC) short-term; short-termD) none of the aboveFeedback: This theory says that long-term interest rates reflect the average of short-term expected rates.7 INCORRECTInsurance companies would tend to invest in ______C____ securities.A) short-termB) intermediate termC) long-termD) not enough information to answerFeedback: An insurance company would prefer long-term securities because they are more conservative or safer.8 INCORRECTThe _________D_____ theory says that investors must be paid a premium to hold long-term securities.A) expectations hypothesisB) time value theoryC) segmentationD) liquidity premiumFeedback: This is the liquidity premium.9 INCORRECTShort-term financing plans with high liquidity have: BA) high return and high riskB) moderate return and moderate riskC) low profit and low riskD) none of the aboveFeedback: This is known as a "middle-of-the-road" approach.10 INCORRECTLong-term financing plans with low liquidity have: BA) high return and high riskB) moderate return and moderate riskC) low return and low riskD) none of the aboveFeedback: This is also known as a "middle-of-the-road" approach.第七章The transaction motive for holding cash is for BA) a safety cushionB) daily operating requirementsC) compensating balance requirementsD) none of the aboveFeedback: This is money for everyday transactions.2 CORRECTWhich of the following motives for holding cash is required by the bank before loaning money? AA) compensating balance motiveB) transactions motiveC) precautionary motiveD) none of the aboveFeedback: This can be considered a form of collateral.3 INCORRECTThe difference between the cash balance on the firm's books and the balance shown on the bank's books is called: BA) the compensating balanceB) floatC) a safety cushionD) none of the aboveFeedback: Float implies that it takes time for checks to clear.4 CORRECTElectronic funds transfer has _____A_____ the use of float.A) reducedB) increasedC) had no effect onD) none of the aboveFeedback: Electronic funds transfer (EFT) has moved cash more quickly and reduced float.5 INCORRECTThe most utilized marketable security by most firms is the: DA) Treasury bondB) Agency securityC) Certificate of DepositD) Treasury billFeedback: Treasury bills (T-Bills) are very safe, popular investments.6 INCORRECTOf the following marketable securities, which are guaranteed by the Federal government? DA) agency securitiesB) negotiable certificates of depositC) banker's acceptancesD) none of the aboveFeedback: None of these are backed by the government.7 INCORRECTThe 5 C's of credit include: DA) conditionsB) collateralC) characterD) all of the aboveFeedback: The other two C's of credit are capacity and capital.8 INCORRECT BThe use of safety stock by a firm will:A) reduce inventory costsB) increase inventory costsC) have no effect on inventory costsD) none of the aboveFeedback: Safety stock is extra inventory a firm keeps in case of unforseen circumstances.9 INCORRECTAll of these factors are used in credit policy administration except: CA) credit standardsB) terms of tradeC) dollar amount of receivablesD) collection policyFeedback: The other three choices are the primary policy variables to consider.10 CORRECTFirms aim to hold ___A___ cash balances since cash is a non-interest earning asset.A) lowB) averageC) highD) none of the aboveFeedback: A firm does not want to keep too much cash on hand because it will lose interest (by not keeping the money in a bank).第八章The largest provider of short-term credit for a business is: BA) banking organizationsB) suppliers to the firmC) commercial paperD) EurodollarsFeedback: This is also known as trade credit.2 INCORRECTThe number of days until the firm is past due to a supplier is called the: CA) discount periodB) term to creditC) payment periodD) none of the aboveFeedback: The payment period is the number of days a firm has to pay its bill.3 INCORRECTIf a firm is given trade credit terms of 2/10, net 30, then the cost of the firm failing to take the discount is: CA) 2%B) 30%C) 36.72%D) 10%Feedback: This is calculated using formula 8-1 in this chapter.4 CORRECTThe interest rate given by a bank to its most creditworthy customers is the: AA) prime rateB) LIBOR rateC) federal funds rateD) discount rateFeedback: This is the "best" interest rate charged to people with excellent credit.5 INCORRECTWhich of the following types of bank loans generally have the highest effective rate of interest? DA) simple interest loanB) discount interest loanC) loan with a compensating balanceD) installment loanFeedback: Installment loans tend to be the most expensive.6 INCORRECTIf a firm needs to borrow $100,000, at 8% interest, to finance working capital needs and a 20% compensating is required, then the firm should borrow ____C______.A) $100,000B) $80,000C) $125,000D) $108,000Feedback: The formula to calculate this is: amount needed/(1-c), where c = the compensating balance percentage.7 CORRECTIf a bank offers a firm a simple interest loan of $1000 for 120 days at a cost of $60 interest, what is the effective rate of interest on the loan? AA) 18.00%B) 6.00%C) 20.00%D) none of the aboveFeedback: This is calculated by using formula 8-2 in this chapter.8 INCORRECTIf a company raises money to finance short-term needs by selling its accounts receivable to another party, this is called ___________. CA) pledgingB) warehousingC) factoringD) none of the aboveFeedback: Factoring means selling the accounts receivable outright.9 INCORRECTThe most restrictive policy for using inventory as collateral for short-term borrowing is called: BA) blanket inventory lienB) warehousing inventoryC) trust receiptD) factoringFeedback: This is a complex method of inventory financing wherein the lender takes control of the inventory.10 CORRECTA type of accounts receivable financing where a firm uses its receivables as collateral is called: AA) pledgingB) securitizationC) factoringD) warehousingFeedback: Pledging means using accounts receivable as collateral.第九章Both the future and present value of a sum of money are based on: CA) interest rateB) number of time periodsC) both a and bD) none of the aboveFeedback: These two factors are used in time value of money calculations.2 INCORRECTAn annuity is ___________________. CA) more than one paymentB) a series of unequal but consecutive paymentsC) a series of equal and consecutive paymentsD) a series of equal and non-consecutive paymentsFeedback: An annuity is a stream of equal payments to be received in the future.3 CORRECTIf you have $1000 and you plan to save it for 4 years with an interest rate of 10%, what is the future value of your savings? AA) $1464.00B) $1000.00C) $1331.00D) cannot be determinedFeedback: This is calculated by using formua 9-1 in this chapter.4 INCORRECTTime value of money is an important finance concept because: DA) it takes risk into accountB) it takes time into accountC) it takes compound interest into accountD) all of the aboveFeedback: Time value of money incorporates all of these concepts.5 INCORRECTThe present value of a dollar to be received in the future is: CA) more than a dollarB) equal to a dollarC) less than a dollarD) none of the aboveFeedback: The reason is because you can earn interest on the money.6 CORRECTThe future value of a dollar that you invest today is: AA) more than a dollarB) equal to a dollarC) less than a dollarD) none of the aboveFeedback: Again, the reason is because the money can earn interest.7 INCORRECTThe future value of an annuity is: CA) less than each annuity paymentB) equal to each annuity paymentC) more than each annuity paymentD) none of the aboveFeedback: The reason has to do with compound interest (or interest earning more interest).8 INCORRECTThe concepts of present value and future value are:DA) directly related to each otherB) not related to each otherC) proportionately related to each otherD) inversely related to each otherFeedback: They are essentially opposite sides of a coin.9 INCORRECTIf you win the lottery and you choose to have your proceeds distributed to you over atwenty-year time period, with the first payment coming to you one year from today, which calculation would you use to calculate the worth of those proceeds to you today? DA) future value of a lump sumB) future value of an annuityC) present value of a lump sumD) present value of an annuityFeedback: This is shown by formula 9-4 in this chapter. But this is not a typical situation. Most lotteries (let’s say $1 Million over 20 years), will pay you the first payment today and $50,000 each year for the next 19 years. This is actually an “annuity due” which is not covered in this text. Y ou’d have to calculate the present value of the annuity for 19 years and add the initial $50,000 you received today.10 CORRECTYou have $1000 you want to save. If four different banks offer four different compounding methods for interest, which method should you choose to maximize your $1000? AA) compounded dailyB) compounded quarterlyC) compounded semi-annuallyD) compounded annuallyFeedback: The more often interest is compounded the faster it will grow because you will begin to earn interest on the interest sooner.第十章In valuing a financial asset, you use these variables: DA) present value of future cash flowsB) discount rateC) required rate of returnD) all of the aboveFeedback: All of these are needed in order to value an asset.2 CORRECTThe principal amount of a bond at issue is called: AA) par valueB) coupon valueC) present value of an annuityD) present value of a lump sumFeedback: This is also known as the face value or stated value.3 INCORRECT BIf a bond's value rises above its par value during its life, interest rates have:A) gone upB) gone downC) stayed the sameD) there is no correlation with interest ratesFeedback: There is an inverse relationship between bond prices and interest rates (or yields).4 INCORRECTThe basic "rent" that you are charged when you borrow money is called: CA) inflation premiumB) risk premiumC) real rate of returnD) none of the aboveFeedback: This is known as the opportunity cost in economics.5 INCORRECTAs time to maturity draws near, a bond's value approaches: BA) zeroB) parC) the coupon paymentD) none of the aboveFeedback: The bond price gets closer to its face value the closer it is to maturity (see figure 10-2 in this chapter).6 INCORRECTOne characteristic of preferred stock is that:DA) it has no maturity dateB) it is a hybrid security with characteristics of both common stock and debtC) it pays a fixed dividend paymentD) all of the aboveFeedback: Preferred stock is described by all of the above characteristics.7 CORRECTCommon stock that has no growth in dividends is valued as if it were: AA) preferred stockB) a bondC) an optionD) none of the aboveFeedback: It is treated the same as preferred stock.8 INCORRECT。

会计报表项目中英文对照(三张主表)

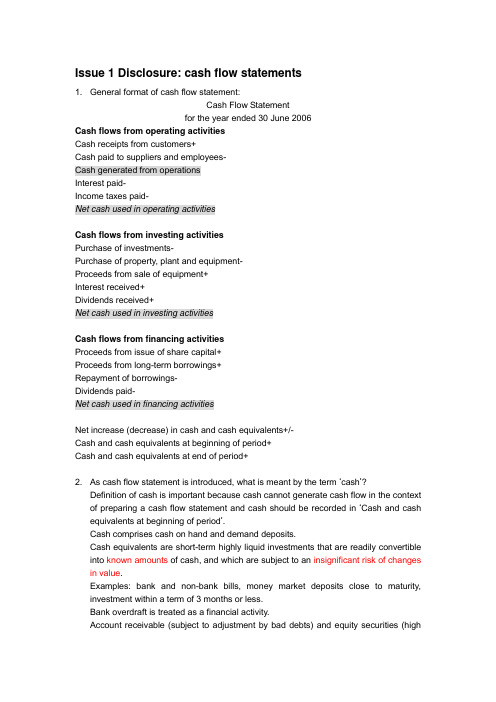

会计报表工程中英文对照(三张主表)1、Balance sheet(audited) 资产负债表Assets 资产Current assets 流动资产、Cash 货币资金Short-term investment 短期投资Notes receivable 应收票据Dividends receivable 应收股利Interest receivable 应收利息Account receivable 应收帐款Other receivable 其他应收款Advanced to suppliers 预付帐款Subsidies receivable 应收补贴款Inventories 存货Prepaid expenses 待摊费用Long-term investments maturing within one year 一年内到期的长期投资Other current assents 其他流动资产Total current assets 流动资产合计Long-term investments 长期投资Long-term equity investment 长期股权投资Long-term debt investment 长期债权投资Total long-term investment 长期投资合计Fixed assets 固定资产Fixed assets-cost 固定资产原价Less: accumulated depreciation 减:累计折旧Fixed assets net value 固定资产净值Less: impairment of fixed assets 减:固定资产减值准备Fixed asset-book value 固定资产净值Materials for projects 工程物资Construction in progress 在建工程Disposal of fixed assets 固定资产清理Total fixed assets 固定资产合计Intangible assets and other assets 无形资产及其他资产Intangible assets 无形资产Long-term deferred expenses 长期待摊费用Other long-term assets 其他长期资产Total intangible assets and other assets 无形资产及其他资产合计Deferred tax:递延税项Deferred tax debit 递延税款借项Total assets 资产总计Liabilities and owners’ equity负债及所有者权益Current liabilities : 流动负债Short-term loans 短期借款Notes payable 应付票据Account payable 应付帐款Advance from customers 预收帐款Accrued payroll 应付工资Accrued employee’s welfare expenses应付福利费Dividends payable 应付股利Taxes payable 应交税金Other taxes and expense payable 其他应交款Other payable 其他应付款Accrued expenses 预提费用Provisions 预计负债Long-term liabilities due within one year 一年内到期的长期负债Other current liabilities 其他流动负债Total current liabilities 流动负债合计Long-term liabilities:长期负债Long-term loans 长期借款Bonds payable 应付债券Long-term accounts payable 长期应付款Specific account payable 专项应付款Other long-term liabilities 其他长期负债Total long-term liabilities 长期负债合计Deferred tax: 递延税项Deferred tax credits 递延税款贷项Total other liabilities : 负债合计Owner’s equity:所有者权益〔股东权益〕Paid-in capital 实收资本Less :investment returned 减:已归还投资Pain-in capital-net 实收资本净额Capital surplus 资本公积Surplus from profits 盈余公积Including: statutory public welfare fund 其中:法定公益金Undistributed profit 未分配利润Total owner’s equity所有者权益〔股东权益〕Total liabilities and owner’s equities负债及所有者权益Total liabilities and owner’s equiti es 负债及所有者权益2、Income statement (audited) 利润表Item 工程Sales 产品销售收入Including :export sales 其中:出口产品销售收入Less: sales discounts and allowances 减:销售折扣与折让Net sales 产品销售净额Less: sales tax 减:产品销售税金Cost of sales 产品销售本钱Including :cost of export sales 出口产品销售本钱Gross profit 产品销售毛利Less : selling expense 减:销售费用General and administrative expense 管理费用Financial expense 财务费用Including :interest expense(less interest income) 其中:利息支出〔减利息收入〕Exchange loss (less exchange gain) 汇兑损失〔减汇兑收益〕Income from main operation 产品销售利润Add :income from other operations 加:其他业务利润Operating income 营业利润Add : investment income 加:投资收益Non-operating expense 营业外收入Less: non-operating expense 减:营业外支出Add: adjustment to pripr year’s income and expense加:以前年度损益调整Income before tax 利润总额Less: income tax 减:所得税Net income 净利润Statement of profit apropriation and distribution (audited) 利润分配表Item 工程Net income 净利润Add: undistributed profit at beginning of year 加:年初未分配利润Other transferred in 其他转入Profit available for distribution 可供分配的利润Less: statutory surplus from profits 减:提取法定盈余公积Statutory public welfare fund 提取法定公益金Staff and workers’ bonus and welfare fund职工奖励及福利基金Reserve fund 提取储藏基金Enterprise expansion fund 提取企业开展基金Profit capitalized on return of investments 利润归还投资Profit available for distribution to owners 可供投资者分配的利润Less: dividends payable for preferred stock 应付优先股股利V oluntary surplus from profits 提取任意盈余公积Dividends payable for common stock 应付普通股股利Dividends transferred to capital 转作股本的普通股股利Undistributed profit 未分配利润3、Cash flows statement 现金流量表工程 Item NO。

四大财务报表中英文对照

四大财务报表中英文对照全文共四篇示例,供读者参考第一篇示例:四大财务报表是每家公司每年都要制作的重要财务文件,它们记录着公司在一定期间内的财务业绩和资产负债状况。

这四大财务报表分别是资产负债表(Balance Sheet)、损益表(Income Statement)、现金流量表(Cash Flow Statement)和股东权益变动表(Statement of Changes in Equity)。

下面将为您详细介绍这四大财务报表的中英文对照。

一、资产负债表(Balance Sheet)资产负债表是衡量公司财务状况的重要指标,它展示了公司在特定日期的资产、负债和所有者权益的情况。

资产负债表的中英文对照如下:中文:资产负债表英文:Balance Sheet资产(Assets):1. 流动资产(Current Assets)2. 非流动资产(Non-current Assets)负债和所有者权益(Liabilities and Equity):1. 流动负债(Current Liabilities)2. 非流动负债(Non-current Liabilities)3. 所有者权益(Equity)资产负债表将公司的资产按照流动性和长期性分类,并将公司的负债和所有者权益细分为流动负债、非流动负债和所有者权益,以展示公司的资产负债结构。

二、损益表(Income Statement)损益表是公司在一定期间内的收入、成本和利润情况的总结,展示了公司的盈利能力。

损益表的中英文对照如下:中文:损益表英文:Income Statement收入(Revenue):1. 销售收入(Sales Revenue)2. 其他收入(Other Revenue)成本(Expenses):1. 销售成本(Cost of Goods Sold)2. 营业费用(Operating Expenses)3. 税前利润(Profit Before Tax)利润(Profit):1. 税后利润(Net Profit)损益表记录了公司在一段时间内的总收入、总成本和净利润,帮助投资者和管理层了解公司的盈利能力。

现金流的直接和间接方法英文

Direct and Indirect Cash Flow MethodThe more commonly known balance sheet and income statement have been required for reporting in America for many years. However, the statement of cash flows is a more recent addition to requirements being introduced formally in 1988. Forms and alterations of the statement of cash flows have existed long before 1988 and one example is a statement released by the Northern Central Railroad in 1863 that documented cash receipts and cash payments for the year. In 1902, United States Steel Corporation produced the working capital funds statement which was essentially current assets minus accounts payable. In 1971, the Accounting Principles Board released Opinion No. 19 which required the funds statement to be part of the three major financial statements. Even with this requirement the statement was not emphasized and still there was not a formal difference between indirect and direct methods (Direct was commonly used). During the 1980’s FASB issued Statement No. 95 and Statement of Financial Accounting Concepts No. 5 which both implemented the statement of cash flows as we know it today.The introduction of Statement No. 95 was highly controversial in accounting circles and FASB because of the anticipated cost of implementation and disagreements over the permissibility of either the Direct Method or Indirect Method of reporting cash flow from operations. At the time of implementation of Statement No. 95 many outside stakeholders pushed for the Direct Method to be compulsory because it would give a better idea of a firm’s ability to pay back debt holders. Proponents of the Indirect Method were preparers and corporations that argued the cost of implementation was too high for the Direct Method and that it didn’t provide clear enough information to shareholders. In the end, Statement No. 95 encourages use of theDirect Method but allows use of the Indirect Method. Today 99% of companies preparing a statement of cash flows use the Indirect Method.The case we chose to examine shows a company that has an example of the statement of cash flows using the Direct Method and the Indirect Method. Both financial statements are exhibited at the end of the paper with the Direct Method being known as Exhibit A and the Indirect Method being known as Exhibit B. When looking at each statement of cash flows two things become apparent. First, the cash balance at the beginning and the end of the year are identical. Second, more importantly, the cash flow from operating activity section is different. In the operating activity section the Direct Method includes lines that directly coincide with specific amounts of cash received and paid for example in exhibit A there is cash received from customers and cash paid for wages. In exhibit B the statement of cash flows uses the Indirect Method there for cash flows are a function of net income, for example, the difference between expenses and cash payments is related to prepayments and expenses payable.Nowadays, cash flow can dictate a corporation’s development and survival. A corporation can maintain the ability to turn a profit temporarily but a quick look at the statement of cash flows can indicate a number of problems in the future that can affect normal operation. Therefore, in recent years the importance of being able to understand and analyze the statement of cash flow and deciding between using the Indirect and Direct Method has grown rapidly. Our paper looks at the benefits and weakness of both methods and also examines why GAAP and IASB prefer the direct cash flow method and on the contrary, why most corporations use the indirect method.In theory, the direct method is easier to understand theoretically and can be defined by cash being paid and cash being received. This looks easier, but for a big company that handles thousands of transactions per day using the direct method approach could be near impossible. Considering that most companies use the accrual method of accounting finding the required information for a direct method approach can be time consuming and costly. In addition the direct method could require the disclosure of sensitive information including the receipts and payments to suppliers and customers respectively that might be stolen by competitors. Another disadvantage of the direct method is that since cash payments and cash received numbers are used on a non-accrual basis extremely high numbers can formulate shown in Exhibit A. An advantage of the direct method is that the overall picture shown by the operating activities is a more accurate one than the one formulated by the indirect method and is preferred by GAAP as well as shareholders.The indirect method is used by more than 95% of corporations currently all while GAAP and FASB recommend using the direct method. The main advantage of the indirect method is the simple nature of preparing the statement of cash flows as compared to the direct method. When using the indirect method changes in accounts are recorded that affect cash. For example, the accounts receivable account increases goes up then cash flow is down. Another advantage of the indirect method is a more systematic view of the corporation as a whole. The indirect method creates a direct link between the statement of cash flows and a stakeholder can trace changes in accounts on the balance sheet back to the operating section on the statement of cash flows. In the indirect method stakeholders can also get a better idea of how non-cash transactions factor intonet income but not cash flow because it is required in the disclosure notes. The indirect method advantage is that it less costly to prepare because it is basically a reconciliation of already known numbers back to cash basis. There are some disadvantages for the indirect method; one is that stakeholder’s especially creditors have a harder time seeing if the company’s cash flow can cover debts and numbers can be bigger and less relevant compared to the direct method. Since the indirect method is not built from the ground up like the direct method accountants need to make adjustments to deferred accounts such as depreciation and so on which can present an additional challenge.Both the direct and the indirect method have their disadvantages as well as their advantages. However, it is telling that over 95% of corporations utilize the indirect method even while GAAP and FASB recommend the direct method. In the end, both final balances are the same but the operating sections differ and this can have a large affect depending on the stakeholder. It seems that the direct method provides are clearer easier to understand operating activity section but the costs of preparing it outweigh the benefit for most corporations. We recommend the each company be responsible and look at both the advantages and disadvantages while deciding which method to use. We also recommend that companies utilize disclosure notes to make the statement of cash flows more valuable to stakeholder whether they use the indirect or direct method. It will be interesting to see in the future if FASB or GAAP change regulations or rules and make the direct method required or start accepting that the indirect method is more relevant nowadays.Works Cited:"Deferred Revenue for the Indirect Method in Accounting." Small Business. Web. 26 Apr. 2015. </deferred-revenue-indirect-method-accounting-21787.html>."The Advantages of Preparing a Cash Flow Statement Using the Direct Method." Small Business. Web. 26 Apr. 2015. </advantages-preparing-cash-flow-statement-using-direct-method-23694.html>.Ori, Jack. "The Benefits of the Direct Method of Cash Flow." EHow. Demand Media, 22 July 2011. Web. 27 Apr. 2015. </info_8771641_benefits-direct-method-cash-flow.html>."Principles of Accounting." Principles of Accounting. Web. 27 Apr. 2015.</chapter16/chapter16.html>.Exhibits Exhibit A:Exhibit B:。

财务报表分析英文课件

Examines the purchase and redemption of treasury stock and its impact on the financial statements

Income statement analysis

Revenue Recognition

Examining the methods and timelines of revenue recognition to ensure it complies with Generally Accepted Accounting Principles (GAAP)

Distinguishing between direct and indirect costs to better understand the impact of each on the capability of specific products or services

Direct vs. Indirect Costs

Investment in Property, Plant, and Equipment: This category includes cash outflows related to the purchase of fixed assets, such as property, plant, and equipment

balance sheet 资产负债表

balance sheet 资产负债表income statement 收益表statement of cash flows 现金流量表operating expense 经营费用operating result 经营成果profitability 获利能力partnership 合伙reporting format 报告式statement of owner’s equity 业主权益表T-account format T形账户表accounting cycle 会计循环anually 每年adjust 调整close 结清inequality 不平衡list 列示post 过账reverse 转回temporary account 临时账户trail balance 试算平衡表transfer 转移columnar 多栏的closing entry 结账分录accounting period 会计期间accrue 计提apportion 分配benefit 利益earn 赚取expire 耗费indefinite 无限的insurance premium 保险费matching 配比portray 描述prepaid 预付precollected 预收time period assumption 会计分配假设closing procedure 结账程序eliminate 消除expedient 方便的facilitate 便于income summary 收益汇总interim 期中norminal account 虚帐户post closing trial balance 结账后试算平衡表reversing entry 转回分录temporary account 暂时性账户worksheet 工作底表abbreviate 略缩cash sales 现金销售cash discount 现金折扣credit sales 赊账销售credit period 信用期COD cash on delivery 付款交货credit memorandum 贷项通知书freight collect 货到付运费freight prepaid 运费预付fob shipping point 离岸价起运地交货价fob destination 到岸价目的地交货价grant 同意merchandising company 商业公司merchandise 商品multi-step format多不式operational activity 经营活动purchase 购买payment term 付款条件sales revenue 销货收入sales returns and allowances 销货退回于折让sales discount 销货折扣net sales revenue 销货净额trade discount 商业折扣1.Bookkeeping 簿记2.审计报告Auditors’ Report3.验资报告Capital Verification Report 2.Data-processing 数据处理3.Double-entry 复式记账4.Single-entry 单式记账5.Account 账户6.Journal 日记账7.Ledger 分类账general ledger 总分类账subsidiary ledger 明细分类账8.Capital 资本9.Stock(inventory) 存货10.Account receivable 应收账款11.Account payable 应付账款12.Posting 过账13.Assets 资产14.Liabilities 负债15.Net worth 净值16.Current liabilities 流动负债17.Long-term liabilities 长期负债18.Stockholders’ equity =proprietorship 业主(股东)权益19.Fiscal period会计期间20.Partnership 合伙经营21.Accounting equation /formula 会计等式/方程式22.Debit 借方23.Credit 贷方24.Cash in bank 银行存款25.Bank loan 银行存款26.To foot (footing) 加总27.Trial balance 试算平衡表28.Sales invoice 销售发票29.Negotiable instrument 流通票据30.Cost accounting 成本会计31.Selling price 销售价格32.Allowance 折让33.Discount 折扣34.Gross profit 毛利35.Sales returns 销售退回36.Current assets 流动资产37.Fixed assets 固定资产38.Intangible assets 无形资产39.Balance sheet 资产负债表40.Patent 专利权41.Copyright 版权42.Franchise 专营权,特许权43.Trade discount 商业折扣44.Depreciation 折旧45.Bonds payable 应付债券46.Mortgages payable 应付抵押借款47.Accrual basis(the produced authority system) 权责发生制48.Prepay 预付49.Cash basis(the realized receipt and payment system) 收付实现制50.Bill of loading 提单51.Physical inventory system 实地盘存制52.Perpetual inventory system 永续盘存制53.Allowance for uncollectible accounts 坏账准备54.Uncollectible accounts expense=bad debts 坏账损失55.Accumulated depreciation =allowance for depreciation 累计折旧56.Factory cost 工厂成本57.Overhead 间接费用58.Financial forecast 财务预测59.Retail outlet 零售渠道60.Summary account 汇总账户61.Close out 结清62.Closing entry 结账分录63.Depletive assets 折耗资产64.Credit note 贷项通知书65.Debit note 借项通知书66.Income statement 收益表67.Net income 净收益68.Capital statement 资本表69.Installment sales 分期付款销售70.Accounting cycle 会计循环71.Source document 原始凭证72.Worksheet 工作底稿73.Post-closing trial balance 结账后的试算表74.Drawing account 业主往来帐户75.Notes payable 应付票据76.Open account 未清帐户77.Notes receivable 应收票据78.Demand deposits 活期存款79.Petty cash funds 备用金80.Bank drafts 银行汇票81.Cashier’s drafts 本票82.Open the bank 开立账户83.Rule off 账户划线84.Outstanding checks 未兑现支票85.Deposit in trant 在途存款86.Nonsufficient fund check 空头支票87.Reconciliation statement 调节表88.Bank statement 银行对账单89.Service charges 银行服务费90.Merchandise inventory 库存商品91.Merchandise inventory turnover 存货周转率92.Net purchases 净购进93.Net sales 净销售94.Working capital 营运资金95.Audit 审计96.Internal control 内部控制97.Internal audit 内部审计98.Job-order cost accounting 分批成本会计99.Process cost accounting 分步成本会计100.Direct cost /prime cost 直接成本/主要成本101.Standard cost 标准成本102.Burden rate 负荷率103.Petty cash(fund) 零(备)用金104.Imprest cash(fund) 定额备用金105.Imprest system 定额备用制106.Physical count 实地盘存107.Retail inventory method 零售价盘存108.First-in, first-out(FIFO) 先进先出法109.Last-in, first-out(LIFO) 后进先出法110.Lower-of-cost-or-market rule(LCM) 成本与市价孰低法111.Moving average 移动加权平均112.Weighted average 加权平均113.Specific identification 具体确认114.FOB(free own bought) destination 目的地交货价115.FOB shipping point 起运点交货价116.Inventory cutoff 库存商品截至日期117.Gross margin 毛利118.Finished goods 产成品119.Work-in-process 在产品120.Acid-test ratio (quick ratio) 速动比率121.Cash over and short 现金溢缺122.Contingent liability 或有负债123.Discount period 贴现期,折扣限期124.Discount rate 贴现率,折现率125.Discounting a note receivable 应收票据折价126.Liquidity 变现性127.Maturity date 到期日128.Maturity value 到期值129.Amortization 摊销130.Book value 账面价值131.Capital expenditure 资本支出132.Declining –balance depreciation method 余额递减法133.Straight –line depreciation method 直线折旧法134.Sum-of-the-years-digits depreciation method 年数总和法135.Units-of-production depreciation method 工作量法136.Fair market value 公允市价137.Salvage(residual) value 残值138.Undepreciated cost 折余价值139.Amortization of bonds 债券摊销140.Annuity 年金141.Bond discount 债券折价142.Bond maturity date 债券到期日143.Bond premium 债券溢价144.Callable bonds 可赎回债券145.Consolidated financial statement 合并报表146.Convertible bonds 可调换债券147.Long-term investment 长期投资148.Market rate of interest 市场利率149.Present value of an annuity 年金现值150.Registered bonds 记名债券151.Bearer bond 无记名债券152.Secured bonds 担保债券153.Serial bonds 分期偿还债券154.Stated(nominal) rate of interest 设定利率(名义利率)155.Term bonds 定期债券156.Debt financing 负债融资157.Equity financing 权益融资158.Lease obligations 租赁融资159.Deferred income taxes 提延所得税160.Effective interest rate 实际利率161.Leveraging 杠杆作用162.Capital stock 股本163.Cash dividend 现金股利164.Articles of incorporation(charter) 公司章程165.Contribute capital 捐赠资本166.Cumulative-dividend preference 累计优先股利167.Current-dividend preference 现行优先股股利168.Date of declaration 公告日169.Dividends in arrears 积欠股利170.Issued stock 已发行股利171.Legal capital 法定资本172.Limited liability 有限责任173.Outstanding stock 发行在外的股票174.Participating-dividend preference 参加分红优先股股利175.Preemptive right 优先股176.Property dividend 财产股利177.Statement of retained earnings 留存收益表178.Stock dividend 股票股利179.Treasury stock 库藏股票180.Liquidation 清算181.Market value 市价182.Transportation in 购货运费183.Transportation out 销货运费184.Promissory note 本票,期票185.Marker 出票人186.Bearer 持票人187.Endorse 背书188.Endorser 背书人189.Dishonor (票据的)拒付。

Balance Sheet and Statement of Cash FlowsPPT课件

5-3

Balance Sheet and Statement of Cash Flows

Balance Sheet

Usefulness Limitations Classification

5-9

LO 2 Identify the major classifications of the balance sheet.

Classification in the Balance Sheet

Current Assets

Cash and other assets a company expects to convert into cash, sell, or consume either in one year or in the operating cycle, whichever is longer.

Balance Sheet

Classification

5-8

LO 2 Identify the major classifications of the balance sheet.

Balance Sheet

Classification

Illustration 5-1

In practice you usually see little departure from these major subdivisions.

5-11

LO 2 Identify the major classifications of the balance sheet.

管理会计双语版总结

Static budget Flexible budget Static budget variance

Sales volume variance Flexible budget variance

Favorable variance and unfavorable variance Management by exception

16

Types of Problems

A. Equipment Replacement

Sunk Costs & Depreciation

B. Special Order

Fixed Cost & Opportunity Costs

C. Outsourcing: Make or Buy Decision

Comparison of traditional and ABC overhead allocation

6

Major Points of Cost Allocation

1 2 3

4

Why allocate? How much to allocate?

Allocate to whom? How to allocate?

7

Chapter 5 : Cost Behavior

Common cost behavior patterns

Fixed costs : think as total Variable costs : think on a per-unit basis Relevant range

Mixed costs and its separation

2

Chapter 2 :Classifying Costs

课上会计英语练习

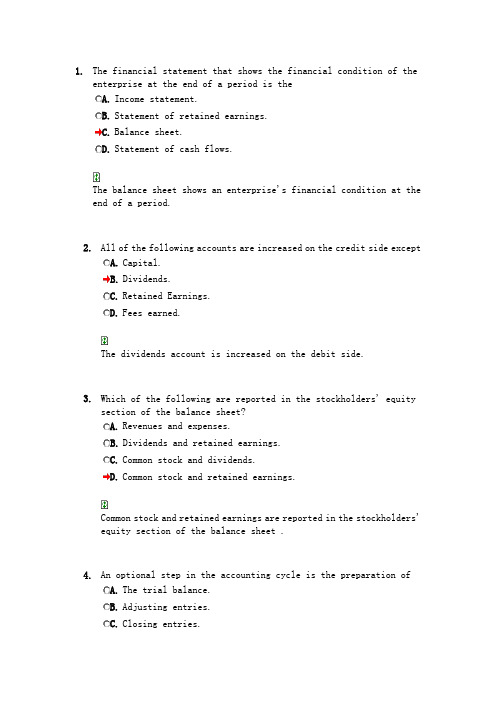

1.The financial statement that shows the financial condition of theenterprise at the end of a period is theA.Income statement.B.Statement of retained earnings.C.Balance sheet.D.Statement of cash flows.The balance sheet shows an enterprise's financial condition at the end of a period.2.All of the following accounts are increased on the credit side exceptA.Capital.B.Dividends.C.Retained Earnings.D.Fees earned.The dividends account is increased on the debit side.3.Which of the following are reported in the stockholders' equitysection of the balance sheet?A.Revenues and expenses.B.Dividends and retained earnings.mon stock and dividends.mon stock and retained earnings.Common stock and retained earnings are reported in the stockholders' equity section of the balance sheet .4.An optional step in the accounting cycle is the preparation ofA.The trial balance.B.Adjusting entries.C.Closing entries.D.The worksheet.The preparation of the work sheet is an optional part in theaccounting cycle.5.All of the following are external events exceptA.A transaction with another entity.B.Consuming raw materials in production processes.C.A change in the price of a good that an entity buys or sells.D.An improvement in technology by a competitor.Consuming raw materials in production processes is an internal event.6.Posting is the process of transferring items entered in a generaljournal to theA.Worksheet.B.Trial Balance.C.General ledger.D.Financial statements.Posting is transferring items in a general journal to the general ledger.7.Which of the following statements about a trial balance is incorrect?A.Its primary purpose is to prove the mathematical equality ofdebits and credits after postingB.It uncovers errors in journalizing and posting.C.It is useful in the preparation of financial statements.D.It proves that all transactions have been recorded.A trial balance does not prove that all transactions have beenrecorded.8.An adjusting entry would never include aA.Debit to an expense account and a credit to an asset account.B.Debit to an expense account and a credit to a liability account.C.Debit to a liability account and a credit to a revenue account.D.Debit to an asset account and a credit to a liability account.An adjusting entry including a debit to an asset account and a credit to a liability account would never occur because income statement amounts would not be adjusted.9.The adjusting entry to record revenue that has been earned, but waspreviously recorded as unearned results in a debit toA.An asset account and a credit to a revenue account.B.A liability account and a credit to a revenue account.C.An expense account and a credit to a revenue account.D.A revenue account and a credit to an asset account.The adjusting entry for unearned revenues includes a debit to a liability account and a credit to a revenue account.10.If the adjusting entry for an accrued expense is not madeA.Assets will be overstated.B.Expenses will be overstated.C.Liabilities will be understated.D.Owner's equity will be understated.Liabilities (and expenses also) will be understated if theadjusting entry for an accrued expense is not made.11.In the closing process all of the revenue and expense accountbalances aretransferred to theA.Capital account.B.Income Summary account.C.Retained Earnings account.D.Dividends account.All revenue and expense account balances are transferred to the Income Summary account.12.The post-closing trial balance consists only ofA.Asset and liability accounts.B.Nominal accounts.C.Revenue and expense accounts.D.Real accounts.Only real accounts are included on the post-closing trial balance.13. A work sheetA.Replaces financial statements.B.Is a required step in the accounting cycle.C.Causes the financial statements to be prepared on a delayedbasis.D.Is an informal device for accumulating and sorting informationneeded for the financial statements.The work sheet is an informal device for accumulating and sorting information.14.Which one of the following appears in both the income statement andbalance sheet columns of a work sheet?A.Merchandise Inventory. income.C.Retained Earnings.D.Sales.Net income appears in both the income statement and balance sheet columns of a work sheet.15.Depreciation and amortization policies are justifiable andappropriate because of theA.Economic entity assumption.B.Going concern assumption.C.Monetary unit assumption.D.Periodicity assumption.The going concern assumption is the justification for depreciation and amortization.16.The assumption that implies that the economic activities of anenterprise can be divided into artificial time periods is theA.Economic entity assumption.B.Going concern assumption.C.Monetary unit assumption.D.Periodicity assumption.The periodicity assumption implies that the economic activities of an enterprise can be divided into artificial timeperiods.17.Generally, revenue should be recognizedA.During production.B.At the end of production.C.At the time of sale.D.At the time cash is received.Usually, revenue is recognized at the time of sale.18.Generally, expenses are recognized when theA.Wages are paid.B.Work is performed.C.Product is produced.D.Work or product actually makes its contribution to revenue.Expenses are recognized when the work or product actually makes its contribution to revenue.1. Accounts that appear in the balance sheet are often called temporary (nominal) accounts. FALSE2. Income Summary is a temporary account only used for the closing process.TRUE3. Revenue accounts should begin each accounting period with zero balances.TRUE4. Closing revenue and expense accounts at the end of the accounting period serves to make the revenue and expense accounts ready for use in the next period.TRUE5. The closing process takes place after financial statements have been prepared.TRUE6. Revenue and expense accounts are permanent (real) accounts and should not be closed at the end of the accounting period.FALSE7. Closing entries result in revenues and expenses being reflected in the owner's capital account. TRUE8. The closing process is a step in the accounting cycle that prepares accounts for the next accounting period.TRUE9. The closing process is a two-step process. First revenue, expense, and withdrawals are set to a zero balance. Second, the process summarizes a period's assets and expenses.FALSE10. Closing entries are required at the end of each accounting period to close all ledger accounts. FALSE11. Closing entries are designed to transfer the end-of-period balances in the revenue accounts, the expense accounts, and the withdrawals account to owner's capital.TRUE12. The Income Summary account is a permanent account that will be carried forward period after period.FALSE13. Closing entries are necessary so that owner's capital will begin each period with a zero balance.FALSE14. Permanent accounts carry their balances into the next accounting period. Moreover, asset, liability and revenue accounts are not closed as long as a company continues in business. FALSE15. The first step in the accounting cycle is to analyze transactions and events to prepare for journalizing.TRUE16. The accounting cycle refers to the sequence of steps in preparing the work sheet.FALSE17. The first five steps in the accounting cycle include analyzing transactions, journalizing, posting, preparing an unadjusted trial balance, and recording adjusting entries.TRUE18. The last four steps in the accounting cycle include preparing the adjusted trial balance, preparing financial statements and recording closing and adjusting entries.FALSE1. Current assets and current liabilities are expected to be used up or come due within one year or the company's operating cycle whichever is longer.TRUE2. Intangible assets are long-term resources that benefit business operations that usually lack physical form and have uncertain benefits.TRUE3. Assets are often classified into current assets, long-term investments, plant assets, and intangible assets.TRUE4. Plant assets and intangible assets are usually long-term assets used to produce or sell products and services.TRUE5. Cash and office supplies are both classified as current assets.TRUE6. Plant assets are also called fixed assets or property, plant, and equipment.TRUE1. Which of the following would NOT be included in the cost of equipment?A. Sales taxB. Installation costsC. Repairs after the equipment is placed in serviceD. Insurance while in transit2. Depreciation:A. is a process of valuation that records the decline in market value of plant assets.B. sets aside cash to replace plant asset as they wear out.C. is a process of allocating a plant asset’s cost to expense over its life.D. covers all of the above.3. Which plant asset is NOT depreciated?A. LandB. Land improvementsC. Furniture and fixturesD. All plant assets are depreciated4. A company purchases a machine for $50,000. It is assigned a $5,000 residual value and a 10-year life. Compute annual depreciation expense using the straight-line method.A. $5,500B. $5,000C. $4,500D. $50,0005. A company purchased a truck for $42,000. Management estimated a residual value of $2,000 and that it would be driven 200,000 miles. Compute depreciation expense using the units-of-production method, assuming the truck is driven 25,000 miles in the first year.A. $25,000B. $5,250C. $5,000D. $1,6006. A company sells machinery for $25,000 cash. The machinery originally cost $100,000 and its accumulated depreciation balance is $80,000. The entry to record the sale would include a:A. loss of $75,000.B. gain of $20,000.C. gain of $5,000.D. loss of $5,000.4. Which inventory costing method is most consistent with the actual flow of goods?A. Specific-unitB. FIFOC. LIFOD. Average cost。

income+statement

• The allowances for damage or missing good reflect the situations in which the goods are damaged in transit or are not what the customer expected. Most companies also will offer discounts, especially on credit sales where the customer pays off the amount early, which reduces overall revenue and is the reason for its deduction from gross sales. All these deductions from the gross sales are represented in the net sales figure.

• Investors must remind themselves that the income statement recognize revenues when they are realized (i.e., when goods are shipped, services rendered, and expenses incurred). With accrual accounting(权责发生制), the flow of accounting events through the income statement doesn't necessarily coincide with the actual receipt and disbursement of cash; the income statement measures profitability, not cash flow.

balance sheet 资产负债表