Internal audit report 16 mar 2011

管理评审输入报告中英文对照版

XX公司2012年质量环境管理评审输入报告The input report to management review during 2012Y1.2012年公司目标完成情况分析报告(包括顾客满意度) (2)2.2011-2012年环境目标指标和管理方案完成情况统计分析 (5)The report on the status of environment objective achieved during 20123.2012年进料质量分析报告 (8)The analysis report of incoming material quality in 2012Y4.2012Y客户抱怨处理汇总 (12)Claim Information analysis in 2012Y5.2012年公司生产过程质量分析报告 (14)The report on the product process quality in 2012 year6.生产工艺和产品质量改进报告 (17)The report on the technical and product improvements7.2012公司环境绩效 (19)Environmental performance in 20128.合规性评价结果报告 (29)The report of evaluation of legal compliance9.2012年人力资源状况分析及培训效果评价 (30)Human resource status analysis and training effectiveness appraisal of year 201210.管理体系内部审核报告 (33)Management system internal audit report11.上年(2011年)管理评审输出跟踪验证 (34)Following-up and verification the output for management review last year12.2012年TLC认证管理评审输入报告 (35)Input report for TLC in 201213.纠正预防措施执行状况 (36)The implementation of corrective and preventive actions表格编号:A-PQEO-26/1-2/001. 2012年公司目标完成情况分析报告The report on the status of quality objective achieved during 2012 The status of Quality objective公司质量目标完成状况统计图(2012年)1.1. XX1.1.2.Negative plate scrap:原因Stat. the reason for scrap in front the third for plates1.1.3. 原因占前三位的统计Stat. the reason for scrap in front the third for Pos.platesexplanation 分析说明:a. 2012年1月-11月XX 报废率平均值为0.12%,在目标值0.40%内,较去年同期升高0.02%。

Audit Report审计报告

Audit ReportDFNS Zi.: (2007) No.64 To all the shareholders of Dalian Changhai Fengyi Aquaculture Co., Ltd:We audited the attached financial statement of Dalian Changhai Fengyi Aquaculture Co., Ltd: (from below abbreviation as “your company”), balance sheet on Dec.31st, 2005, and on Dec.31st, 2006, and profit statement in 2005 and 2006 and its annotations.1, administers’ responsibility for the financial statementAccording to Enterprise Accounting Principles and “Enterprise Accounting Regulation” , the administrators have the responsibility of compiling the financial statement, including: 1, to design, implement, and maintain the internal control related to financial statement complication in order to avoid the big mistakes caused by embezzlement and errors. 2, to choose and to apply suitable accounting policies. 3, to make reasonable accounting estimates.2,The Responsibility of Registered AccountantOur responsibility is to give suggestions on financial form on the base of executing the audit work. We have carried out the audit work according to the rule of “Chinese Certified Public Accountant Audit Principle”. There is a requirement in “Chinese Certified Public Accountant Audit Principle” that we should obey the professional ethical standard. And we should plan and carry out the audit work in order to obtain the reasonable promise whether there are any big mistakes or not.The audit work is related to the execution of audit procedure in order to obtain the related sum of money of financial form and the announced audit evidence. The registered accountant will judge which audit procedure should be chosen, including the evaluation of the big mistake of financial form caused by embezzlement and mistakes. While we are carrying out the risk evaluation, we will take a consideration of the inner control related to the financial form organization in order to design a proper audit procedure. But we do not have the purpose to give suggestions to the validity of the inner control. The audit work also includes the evaluation of theappropriation of the accountant policy that the managers use to choose an accountant and the rationality of an account decision that they make. And it also includes the whole list of estimating the financial form.3, Audit OpinionWe think that the provided accounting statements are in conformity with the regulations of <<Company Accounting Principles and Copmany Accounting Regulation>>, which can objectively reflect the financial status as from Dec. 31, 2005 to Dec. 31, 2006, and business achievements of Year 2005 and Year 2006 of the company.Enclosed:1.Balance Sheet of Dec. 31, 2005 and Profit Statement of Year 20052.Balance Sheet of Dec. 31, 2006 and Profit Statement of Year 2006Dalian FundYuan Certified Public Accountants Co., Ltd. (Seal)Dalian ChinaCertified Public Accountant of the People’s Republic of China: Yuan Shichun (Seal)Certified Public Accountant of the People’s Republic of China: Yu Hongwei (Seal)Jun.20th, 2007。

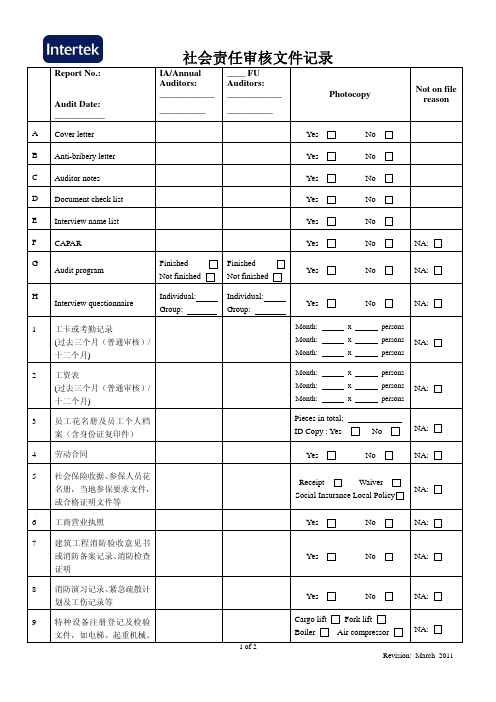

Document Checklist _China_ -Mar 2011

H

Interview questionnaire 工卡或考勤记录 (过去三个月(普通审核)/ 十二个月)

Yes

Month: Month: Month: Month: Month: Month: x x x x x x

No

persons persons persons persons persons persons

NA:Leabharlann 9特种设备注册登记及检验 文件,如电梯、起重机械、

NA:

Revision: March 2011

社会责任审核文件记录

机动叉车、 锅炉及压力容器 (含气瓶、压力表及安全 阀)等 10 特种作业人员操作证, 如电 工、焊接工等; 特种设备作业人员操作证, 如电梯司机、 叉车司机、 起 重机械操作工、司炉工等。 11 厨房餐饮服务许可证 厨工健康证 12 职业健康体检记录及化学 品安全培训记录 13 环保文件(如建设项目环 评、 环评批复、 建设项目竣 工环境验收报告, 排放污染 物申报登记表等) 14 危险废物处置商的经营许 可证, 危险废物转移联单等 15 16 企业规章制度或员工手册 政府有关当地最低工资标 准文件 17 当地劳动局关于综合计算 工时工作制批文或延长加 班批文 18 未成年工体检及劳动局登 记记录 19 20 建筑平面图 劳务派遣工的考勤及工资 表记录, 劳动合同, 社会保 险收据及合格证明, 与劳务 派遣单位签订的合同及劳 务派遣单位的营业执照 21 22 (危险)化学品清单 其他文件 Yes Production Material Other: No Quality Administration NA: NA: Yes No NA: YW health examination YW registration Yes No NA: NA: Electrician Cargo lift Boiler Other Catering Service License Health certificate Health examination records Training records EIA Report EIA Approval Final acceptance check NA: Declaration Form Duplicated form BL of waste collector Service agreement Yes Yes No No NA: NA: NA: NA: NA: Welder Forklift NA: Crane Other

Internal Audit Report 内审报告2014.12

Audit Report审计报告

Audit ReportDFNS Zi.: (2007) No.64 To all the shareholders of Dalian Changhai Fengyi Aquaculture Co., Ltd:We audited the attached financial statement of Dalian Changhai Fengyi Aquaculture Co., Ltd: (from below abbreviation as “your company”), balance sheet on Dec.31st, 2005, and on Dec.31st, 2006, and profit statement in 2005 and 2006 and its annotations.1, administers’ responsibility for the financial statementAccording to Enterprise Accounting Principles and “Enterprise Accounting Regulation” , the administrators have the responsibility of compiling the financial statement, including: 1, to design, implement, and maintain the internal control related to financial statement complication in order to avoid the big mistakes caused by embezzlement and errors. 2, to choose and to apply suitable accounting policies. 3, to make reasonable accounting estimates.2,The Responsibility of Registered AccountantOur responsibility is to give suggestions on financial form on the base of executing the audit work. We have carried out the audit work according to the rule of “Chinese Certified Public Accountant Audit Principle”. There is a requirement in “Chinese Certified Public Accountant Audit Principle” that we should obey the professional ethical standard. And we should plan and carry out the audit work in order to obtain the reasonable promise whether there are any big mistakes or not.The audit work is related to the execution of audit procedure in order to obtain the related sum of money of financial form and the announced audit evidence. The registered accountant will judge which audit procedure should be chosen, including the evaluation of the big mistake of financial form caused by embezzlement and mistakes. While we are carrying out the risk evaluation, we will take a consideration of the inner control related to the financial form organization in order to design a proper audit procedure. But we do not have the purpose to give suggestions to the validity of the inner control. The audit work also includes the evaluation of theappropriation of the accountant policy that the managers use to choose an accountant and the rationality of an account decision that they make. And it also includes the whole list of estimating the financial form.3, Audit OpinionWe think that the provided accounting statements are in conformity with the regulations of <<Company Accounting Principles and Copmany Accounting Regulation>>, which can objectively reflect the financial status as from Dec. 31, 2005 to Dec. 31, 2006, and business achievements of Year 2005 and Year 2006 of the company.Enclosed:1.Balance Sheet of Dec. 31, 2005 and Profit Statement of Year 20052.Balance Sheet of Dec. 31, 2006 and Profit Statement of Year 2006Dalian FundYuan Certified Public Accountants Co., Ltd. (Seal)Dalian ChinaCertified Public Accountant of the People’s Republic of China: Yuan Shichun (Seal)Certified Public Accountant of the People’s Republic of China: Yu Hongwei (Seal)Jun.20th, 2007。

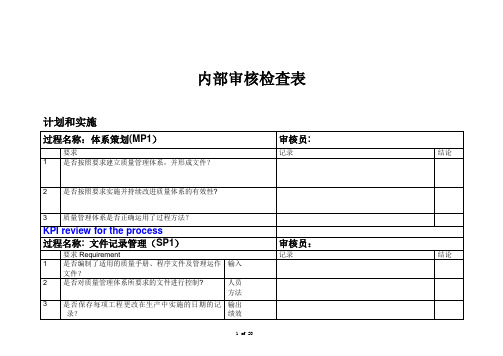

内审检查表internal-audit-checklist

识别任何问题并提出必要的措施

输出

绩效

8

是否保持评审结果及任何必要措施的记录?

人员

输出

9

为确保设计和开发输出满足输入的要求,组织是否依据所策划的安排对设计和开发进行验证?并保持验证结果及任何必要措施的记录?

输出

10

为确保产品能够满足规定的使用要求或已知的预期用途的要求,是否依据所策划的安排对设计和开发进行确认并在产品交付或实施之前完成?

内部实验室设施是否有定义的范围,包括有能力进行的检验,试验或校准服务?

设施

10

组织的实验室范围是否包括在质量管理体系中,并符合规定的技术要求?

方法

11

为组织提供检验,试验或校准服务的外部实验室是否有定义的范围、能力并符合下列要求

—通过ISO/IEC17025或相等的国家标准认可

—必须有证据证明外部实验室可以被顾客接受

过程名称:管理评审(MP2)

审核员:

要求Requirement

记录

结论

1

是否按计划评审质量管理体系,以确保其持续的适宜性,充分性和有效性?,并保持记录?

方法

输入

2

管理评审是否包括过程绩效/质量目标的评审?

绩效

3

组织的管理评审输入是否包括所有必要内容?

输入

4

组织的管理评审的输出是否包括改进与相关资源需求。

设施

8

是否采用多方论证的方法制定工厂,设施及设备的计划,以尽量减少材料的转移和搬运,优化对场地空间的增值利用,便于材料的同步流动?

输出

9

是否制定评价现有操作和过程有效性的方法?

绩效

10

是否为达到产品符合要求所需的工作环境?

内部审计报告综述

内部审计报告综述The internal audit report provides a comprehensive overview of the financial health and operational efficiency of an organization. It serves as a crucial tool for identifying risks, evaluating compliance, and ensuring accountability within the organization. This report offers insights into the effectiveness of internal controls, identifies areas of improvement, and recommends strategies for enhancing overall performance.内部审计报告是对组织财务状况和运营效率的全面概述,是识别风险、评估合规性和确保组织内部问责制的重要工具。

这份报告提供了对内部控制有效性的深入见解,确定了改进领域,并提出了提高整体业绩的策略。

The audit process begins with a thorough understanding of the organization's structure, operations, and objectives. Auditors review financial records, policies, and procedures to assess their accuracy and compliance with applicable regulations. They also conduct interviews with staff members to gain insights intoday-to-day operations and challenges faced.审计过程始于对组织结构、运营和目标的深入了解。

内部审计流程及问题分析

内部审计流程及问题分析Internal auditing is a critical process for any organization to ensure compliance with policies, procedures, and regulations, as well as to evaluate the effectiveness of internal controls. 内部审计是任何组织确保遵守政策、流程和法规,并评估内部控制有效性的关键过程。

It involves systematically reviewing and analyzing an organization's operations to identify areas of potential risk and improvement. 它涉及系统性地审查和分析组织的运营,以识别潜在风险和改进的领域。

Internal auditors play a crucial role in providing independent and objective assessments of an organization's processes and controls. 内部审计师在提供组织流程和控制的独立客观评估方面发挥着至关重要的作用。

One of the key challenges in internal auditing is the management of the audit process itself. 内部审计中的一个关键挑战是审计流程本身的管理。

This includes planning and scheduling audits, conducting fieldwork and testing, and preparing audit reports. 这包括规划和安排审计、开展实地工作和测试,以及准备审计报告。

InternalAudit

•

Internal control review for the following processes

– Purchase to pay cycle – Order to receive cycle

•

Review of IT Systems/ Processes

– Role conflicts in IT – MIS Functionality used vs. EXCEL reports – Review of IT Organization/ roles

• •

Customer satisfaction processes Purchase Transaction audit

8

Sundar & Co

• IT Strategy vs. Business growth • Data conversion • Mapping business processes to IT • Marrying standard operating procedures to Oracle functionalities • IT Organization • IT Controls – authorization

5

Sundar & Co

New dimensions add to the complexity of audit and skills required in executing such assignments Illustrative audit scope

Review of Corporate Governance Machinery

Internal Audit - A Comprehensive Risk Management tool Understanding Document

英文内部审计报告

英文内部审计报告Internal Audit Report;[Date][To:][From:]Subject: Internal Audit ReportIntroduction:This internal audit report provides an overview of the audit findings, observations, and recommendations resulting from the audit conducted at [Name of Company/Organization] during the period [Audit Period].Scope of the Audit:The audit focused on [specific area or process audited], with the objective of assessing compliance with internal policies, procedures, and regulations, as well as identifying areas for improvement and risk mitigation.Audit Findings:1. [Finding 1]: Provide a detailed description of the first audit finding, including any deviations from policies or procedures, potential risks, and impacts on the organization.2. [Finding 2]: Describe the second audit finding in a similar manner, highlighting anynon-compliance issues, weaknesses in controls, or areas of concern.3. [Finding 3]: Outline the third audit finding, emphasizing key findings, root causes, and recommendations for corrective actions.Recommendations:Based on the audit findings, the following recommendations are proposed to address the identified issues and improve the effectiveness of internal controls:1. [Recommendation 1]: Provide a specific recommendation to address the first audit finding, including actions to be taken, responsible parties, and timelines for implementation.2. [Recommendation 2]: Suggest measures to rectify the second audit finding, such as process improvements, training initiatives, or policy revisions.3. [Recommendation 3]: Offer guidance on how to address the third audit finding, outlining steps to be taken to mitigate risks and enhance control mechanisms.Conclusion:In conclusion, the internal audit report highlights areas of concern, non-compliance issues, and opportunities for improvement identified during the audit. It is essential that management takes prompt action to implement the recommended corrective measures to strengthen internal controls and mitigate risks effectively.Please feel free to contact [Name of Internal Auditor] at [Contact Information] for further clarification or assistance in implementing the audit recommendations.Sincerely,[Name of Internal Auditor][Title][Company/Organization][Date]。

审计报告AuditReport

审计署国外贷援款项目审计服务中心Audit Service Center of China National Audit Office for Foreign Loan and Assistance Projects审计报告Audit Report审外中报〔2016〕23号AUDIT REPORT〔2016〕NO. 23项目名称:世界银行贷款中国节能融资项目–中国进出口银行Project Name:China Energy Efficiency Financing Project Financed by the World Bank –the Export-Import Bank ofChina贷款编号:7529–CNLoan No.:7529–CN项目执行单位:中国进出口银行Project Entity: The Export-Import Bank of China会计年度:2015Accounting Year: 2015目录Contents一、审计师意见 (1)Ⅰ. Auditor’s Opinion (3)二、财务报表及财务报表附注 (5)II. Financial Statements and Notes to the Financial Statements (5)(一)资金平衡表 (5)i. Balance Sheet (5)(二)项目进度表 (7)ii. Summary of Sources and Uses of Funds by Project Component (7)(三)贷款协定执行情况表 (11)iii. Statement of Implementation of Loan Agreement (11)(四)财务报表附注 (12)iv. Notes to the Financial Statements (15)三、审计发现的问题及建议 (18)III. Audit Findings and Recommendations (20)一、审计师意见审计师意见中国进出口银行:我们审计了世界银行贷款中国节能融资项目2015年12月31日的资金平衡表及截至该日同年度的项目进度表、贷款协定执行情况表等特定目的财务报表及财务报表附注(第5页至第17页)。

审计术语——内部审计报告

审计术语——内部审计报告审计术语——内部审计报告审计术语——内部审计报告内部审计报告(Internal Audit Reports)[1] 什么是内部审计报告内部审计报告是指内部审计人员,根据审计计划对被审计单位实施必要的审计程序后,就被审计单位经营活动和内部控制的适当性、合法性和有效性出具的书面文件。

[2] 内部审计报告撰写的基本原则客观性原则《内部审计具体准则第7号——审计报告》第四条规定:“内部审计人员应在审计实施结束后,以经过核实的审计证据为依据,形成审计结论与建议,出具审计报告”。

即审计报告应实事求是、不偏不倚地反映审计事项。

审计依据、标准不明确的事项,以及由各种原因导致模棱两可,事实不清的问题都不应该在审计报告中评价。

重要性原则审计报告应突出重点,以点采面,充分考虑审计风险水平,不遗漏审计中发现的重大事项。

审计评价要围绕预定的审计目标开展,不可扩大审计范围。

简洁易懂原则审计报告文字措辞要“明确、简练”。

从内部审计报告的利用来看,“明确”是指写出的报告要让大多数人能看懂,所提出的审计意见或建议具有可操作性,被审计单位一看就知道怎么做,“简练”是指内部审计报告一定要主次分明,繁简得体,能短则短,把主要方面讲清楚则可。

说明审计立项依据、审计目的和范围、审计重点和审计标准等内容。

[2] 内部审计报告的结构和主要内容1(审计概况说明审计立项依据、审计目的和范围、审计重点和审计标准等内容。

2(审计依据说明在审计过程中遵守的国家制定的相关法律、法规、上级单位制定的制度等外部依据。

3(审计结论根据已查明的事实,对被审计单位经营活动和内部控制所作的评价,结论要正确、客观、公正、实事求是,该肯定就肯定,该否定就否定,不能含糊不清,更不能掺杂任何个人意志。

4(审计决定及审计建议针对审计发现的主要问题提出的处理、处罚意见或合理化建议。

审计建议要确保可行性,不仅要体现一定的政策性和指导性,符合有关法规和制度要求,同时也要结合实际情况有较强的针对性和可操作性,否则被审计单位难以达到整改要求。

Internal Audit procedure内部审核程序(中英文)

1.0 Purpose 目的This procedure describes how internal audits of the Management System (including QualityManagement System and Environmental Management System) are conducted, how Non-conformances are recorded and how corrective actions are agreed, implemented and verified.本程序描述了如何对公司管理体系(包括质量管理体系和环境管理体系)进行内部审核,如何记录不符合事项以及如何制定、实施和验证纠正措施2.0 Scope 范围This procedure applies to Management System (including Quality Management System andEnvironmental Management System) internal audit, process audit and product audit in ***.本程序适用于本公司与管理体系(包括质量管理体系和环境管理体系)有关的审核活动,包括质量管理体系审核、环境管理体系审核、过程审核、产品审核。

3.0 Definitions 定义3.1 IMSA Jnternal Management System Audit/内部管理体系审核;3.2 Internal Auditor: Based on training, a person who is capable and qualified to audit the performanceof Management System.内审员:经过相应培训,具有能力和资格对公司管理体系状况进行审核的员工3.3 Audit Team Leader: A person who is recommended to take charge in the internal audit.内审组长:指定的负责全程内审的人员3.4 Audit Criteria: A series of policies, procedures and requirements, which are used as basis for audit.审核准则:所依据的一系列的方针、程序或要求3.5 Audit Evidence: Any fact, record or other information that can be got during audit.审核证据:与审核有并能够证实的记录、事实陈述或其他信息3.6 Audit Finding: The result after evaluating the audit evidence based on the audit criteria.审核发现:所收集到的审核证据对照审核准则进行评价的结果3.7 System Audits: Systematic assessment for quality and environmental management to verify theeffectiveness.体系审核:对质量和环境管理体系进行审核,以确认体系运行的有效性。

编写内部审计报告英语

编写内部审计报告英语Internal Audit Report。

Introduction。

This internal audit report aims to provide an overview of the findings and recommendations resulting from the recent audit conducted within our organization. The purpose of this report is to identify areas of improvement, assess the effectiveness of internal controls, and make recommendations for enhancing operational efficiency and risk management.Executive Summary。

The internal audit focused on various key areas, including financial processes, compliance with regulations, and operational effectiveness. The audit team conducted thorough examinations, reviewed documentation, interviewed staff members, and analyzed data to gather sufficient evidence for their findings.Findings and Recommendations。

1. Financial Processes。

1.1 Accounts Payable。

The audit revealed inconsistencies in the accounts payable process, including delays in invoice processing and inadequate documentation. To address this issue, it is recommended to implement an automated accounts payable system that can streamline the process, improve accuracy, and enhance overall efficiency.1.2 Budgeting and Forecasting。

internal auditor job description

internal auditor job description [Internal Auditor Job Description]Introduction:Internal auditing is a crucial function within any organization. It involves evaluating and monitoring an organization's internal controls, processes, and financial operations to ensure they are efficient, effective, and compliant with relevant regulations. This article will delve into the various aspects of an internal auditor's job description, providing a step-by-step analysis of their responsibilities, skills, qualifications, and career prospects.Step 1: Defining the role of an internal auditorAn internal auditor is responsible for assessing an organization's risk management strategies, internal control systems, and financial reporting processes. They conduct independent and objective evaluations to help the organization achieve its objectives and improve its operations. The role requires thorough understanding and application of auditing principles, ethical codes, and professional standards.Step 2: Assessing the responsibilities of an internal auditora) Risk assessment: Internal auditors evaluate the organization's vulnerabilities and potential risks. They identify areas where control weaknesses exist or where fraud, waste, or abuse may occur.b) Audit planning: Internal auditors develop audit plans, which outline the scope, objectives, audit procedures, and timeframes for each audit engagement. They ensure that audits are conducted in a systematic and efficient manner.c) Gathering evidence: Internal auditors collect and analyze relevant data, records, and documents to support their audit findings and recommendations. They may need to interview staff and review policies and procedures.d) Testing controls: Internal auditors assess the effectiveness of control activities implemented by the organization to mitigate identified risks. They may perform control tests, including process walk-throughs, sample testing, and IT system reviews.e) Reporting findings: Internal auditors prepare detailed reports summarizing audit findings, including control deficiencies, process inefficiencies, and areas of non-compliance. These reports are submitted to management and other stakeholders.f) Follow-up and monitoring: Internal auditors track the implementation of their recommendations and assess whether the suggested improvements have been effectively adopted by the organization. They may conduct periodic follow-up audits to ensure sustainability.Step 3: Highlighting essential skills for internal auditorsa) Analytical skills: Internal auditors need to analyze complex information and data to identify patterns, trends, and irregularities. They must possess strong problem-solving skills to identify risks and weaknesses and propose appropriate solutions.b) Communication skills: Internal auditors must effectively communicate audit findings, recommendations, and their rationale to diverse stakeholders, including management, staff, and external auditors. Both written and oral communication skills are crucial.c) Integrity and ethics: Internal auditors must adhere to ethical principles and maintain a high level of integrity while conducting audits. They should be impartial, objective, and independent in their evaluations.d) Technical expertise: Internal auditors are expected to have a solid understanding of auditing standards, regulations, andindustry-specific knowledge. Proficiency in financial analysis, accounting principles, and data analytics is highly desirable.Step 4: Outlining necessary qualifications and certificationsa) Education: A bachelor's degree in accounting, finance, or a related field is typically required for a career in internal auditing. Some organizations may prefer a master's degree or professional certifications such as Certified Internal Auditor (CIA) or Certified Public Accountant (CPA).b) Experience: Entry-level internal auditor positions may require1-3 years of relevant experience in auditing, accounting, or financial analysis. Higher-level positions often necessitate severalyears of progressive experience in internal auditing or a related field.c) Certifications: Professional certifications such as CIA, CPA, or Certified Information Systems Auditor (CISA) are highly regarded in the internal auditing profession. These certifications validate the auditor's knowledge and expertise in specific areas.Step 5: Discussing career prospects in internal auditingInternal auditors often have diverse career progression opportunities. They can advance within their organization, take on managerial roles, or specialize in specific areas such as IT auditing or fraud examination. Additionally, internal auditing experience can serve as a stepping stone to executive positions such as Chief Audit Executive or Chief Financial Officer.Conclusion:The role of an internal auditor is vital in providing independent and objective assessments of an organization's internal controls,processes, and financial operations. By identifying risks, recommending improvements, and monitoring implementation, internal auditors contribute significantly to the overall efficiency, effectiveness, and compliance of the organization. Strong analytical, communication, and ethical skills, along with relevant qualifications and certifications, are essential for success in this profession.。

chapter 5 Internal audit

2020/11/2

4

1.4 Internal audit activities

The tasks of an internal audit department includes: • Review of the accounting and internal control systems; • Examination of financial and operating information; • VFM audits (3E); • Compliance audits; • Review of the safeguarding of assets; • Review of the implementation of cor objectives; • Risk assessments; • Special investigations; • Stress tests.

• Scope of work; • Authority; • Independence; • Resources.

2020/11/2

12

6 The internal audit committee

• An internal audit committee of independent non-executive directors should liaise with external audit, supervise internal audit, and review the annual accounts and internal controls.

• Its objective is to assist management in the effective discharge of their responsibilities. It furnishes them with analysis, appraisals, recommendations…and information concerning the activities reviewed.

Internal Audit Program - 财务中心

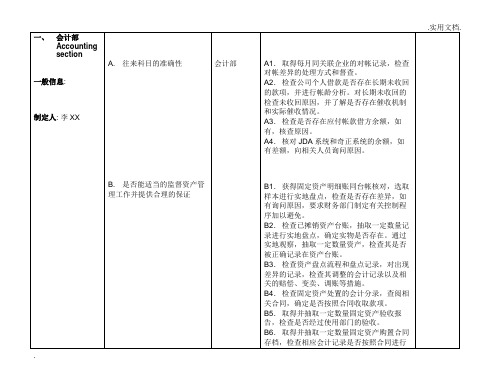

C1.检查合同是否经过审核,是否经过审核人批准。

D1.针对所有通过接口过账的科目,例如银行存款、成本等,检查审计期间JDA和齐正系统的发生额和余额是否相符。不相符的查明原因。

A1.取得税务部工作流程,了解税务工作重点及战略;

E1.审查资产负债表及现金流量表,检查其负债和融资规模是否在允许的范畴内,是否对融资风险进行有效的控制和调整

F1.检查外部融资的合同条款是否合法、合理;抵押质押物是否合理,是否经过审批;询问公司律师,是否存在未经授权的担保行为

G1.检查盘点计划制定的是否完善、可靠,盘点的基础是否可靠,实施的方法是否对数字的准确有保证。

一、会计部

Accounting section

一般信息:

制定人:李XX

二、税务部

Tax section

一般信息:

制定人:吴XX

三、资金部

Treasury section

一般信息:

制定人:王XX

四、账单部

Billing section

一般信息:

制定人:李XX

五、报告部

Reporting section

A2.检查、分析并评价报表预测数据基本假设的合理性。

A3.抽取一定数量报表,对报表数据作趋势分析和比率分析,查找异常项目,追踪异常项目已发现其原因和性质。

B1.向报表使用部门发送意见收集表,了解他们对报表数据的格式、质量、可用性的意见。

A1。调查了解编制预算的假设,并做分析、评估;

B1。调查了解预算引用数据的来源,并评价其可靠、真实、合理性

B1.检查年度支出计划中是否包含了被批准执行的资本性支出计划和预计的股利支付计划,检查该计划的制定是否挤占了日常经营所需要的资金,检查在上述计划下的外部融资计划是否在允许的范畴内

编写内部审计报告

编写内部审计报告(中英文实用版)英文文档内容:Internal Audit ReportIntroduction:This report presents the findings and recommendations of the internal audit conducted on [Name of Department/Area] within the organization [Name of Organization].The audit was conducted to assess the effectiveness and efficiency of the department"s operations, risk management practices, and compliance with relevant policies and procedures.Scope:The audit covered a period from [Start Date] to [End Date] and included a review of financial records, operational processes, and internal control systems.The audit was performed in accordance with the generally accepted auditing standards and the organization"s internal audit policy.Findings:1.Financial Management:- The department"s financial records were incomplete and inaccurate.Recommendation: Implement a robust financial management system to ensure accurate and complete records.- Expenditures were not properly authorized, and there was a lack of segregation of duties.Recommendation: Establish clear authorization procedures and segregation of duties to prevent misappropriation of funds.2.Operational Processes:- The department"s operational processes were inefficient, leading to delays and increased costs.Recommendation: Streamline operational processes to improve efficiency and reduce costs.- There was a lack of documentation and record-keeping practices.Recommendation: Develop and implement comprehensive documentation and record-keeping policies.3.Internal Control Systems:- The internal control systems were weak, with gaps in access controls and monitoring procedures.Recommendation: Strengthen internal control systems by implementing effective access controls and monitoring procedures.- There was a lack of employee training and awareness regarding compliance requirements.Recommendation: Provide regular training sessions to employees to enhance their understanding of compliance requirements.Recommendations:Based on the findings of the audit, the following recommendationsare made:1.Implement a robust financial management system to ensure accurate and complete financial records.2.Establish clear authorization procedures and segregation of duties to prevent misappropriation of funds.3.Streamline operational processes to improve efficiency and reduce costs.4.Develop and implement comprehensive documentation and record-keeping policies.5.Strengthen internal control systems by implementing effective access controls and monitoring procedures.6.Provide regular training sessions to employees to enhance their understanding of compliance requirements.Conclusion:The internal audit revealed several areas of improvement within the [Name of Department/Area].Implementation of the recommendations will enhance the department"s effectiveness and efficiency, improve risk management practices, and ensure compliance with relevant policies and procedures.Management is requested to review this report and take necessary actions to address the identified issues.Date: [Date of Report]中文文档内容:内部审计报告引言:本报告总结了组织[组织名称]内部审计小组对[部门名称]进行的内部审计的结果和建议。

企业内部审计报告范文

企业内部审计报告范文n:As part of our plan for internal audit for the year 2003.we conducted on-site audits of the business management res。

procurement plans and pricing control。

relevant contracts。

and inventory management system of the Planning and Control Department of the company。

The audit covered the d from January 1.2002 to September 30.2003.XXX:The scope of this audit covered the timely。

effective。

reasonable。

XXX and Control Department from January 1.2002 to September 30.2003.as well as the efficiency of inventory cost management and the effectiveness of internal control。

The audit was based on the n provided by the Planning and Control Department。

During the audit process。

XXX:Audit findings XXX:During the audit of the Planning and Control Department。

we identified the following key audit findings:1.The procurement r is not specific and standardized。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Ben / Peter

3

SO090928004HK 5-May SR101007001

Fixed the flow switch 29-Nov

(Product quality) 4

Analysis of quality objective

Supplier Cole Parmer

• ask 8 week commitment Including especial case • Changing note (SO101202005HK 00180VG 5718-37)

A & P INSTRUMENT CO., LTD. 科 藝 儀 器 有 限 公 司

香港九龍灣宏冠道8號金漢工業大厦1樓1 室 Unit 1, 1/F., Kam Hon Ind. Bldg., 8 Wang Kwun Rd., Kowloon Bay, Kln., H.K. Tel: (852) 27556578 Fax: (852) 27554549 E-mail: anpcohk@

QA action

Remind engineers in weekly service meeting on 14-Mar

Remark Discipline

Improve cognition

Discipline

Improve cognition

In MR meeting

Logistic

Michael Sandy

AC/DC adaptor connector corroded - replaced 15-Sep

Rate

SO /SR no.

Unsatisfied item

HOMETEK (IKA MIXER + HOTPLATE)

Cole Parmer

3

SO100629007HK 19-Aug

• Wrong accessory • Packing • SVC response time

(Product quality)

• Arrangement of pump system installation

HKU dept of P&A medicine (DRIVE + PUMPHEAD) OCEANUS

(OPTICAL PWR METER SYSTEM 840-C)

(Service quality) Communication

SO / PO

SO100628004HK PO100706001 SO100716004HK PO100721002 SO100723002HK PO100802002 SO100805009HK PO100811002 SO100813001HK PO100816006 SO100817007HK PO100817007 SO100827001HK PO100830005 SO100921005HK PO100922004 SO1001116001HK PO101117002 SO101216003HK PO101220006

Objective: 1. Discipline monitoring 2. Emphasize continual improvement

Conclusion of audit: 1. Company operation is running smooth 2. More discipline in operation (Sales and Service) 3. More communication / quality information distribution (Quality) 4. Conduct “Act” in PDCA improvement loop

2

Result of internal audit

Department Service Auditor Michael Sandy Auditee Lok Peter John Order deck Admin Account Sales Michael Sandy Tony Mabel Barry QA Rayo Michael Sandy 9-Mar 9-Mar Michael Sandy Bonnie Peggy 8-Mar Date 8-Mar Finding

Top three MOTIC

SO100712012HK PO100712001 SO100914001HK PO100914001

PASCO • better schedule

SO100730001HK PO100806004 SO100819002HK PO100819001 SO100823002HK PO100827002 SO101125003HK PO101126007

Internal audit report

16-Mar-2011 By quality department

1

Summary of internal audit

Scope: 1. Operating level of all departments in HK office 2. Cognition of company quality objective 3. Quality manual

Wrong MQ expand Missing SR update Lack of quality objective cognition Well operation Lack of improvement cognition Missing mark /chop on outgoing document Lack of information of customer satisfaction rate Unclear definition of on time delivery Remind engineers in MR meeting Emphasize customer satisfaction rate as sales KPI Discuss definition of on time delivery Start date Close date Quarterly review delivery status and send out result

Reason of delay delivery Non-catalog item need longer time b/o Special item need longer time b/o Out of stock Out of stock Item need a cert. Item need calibration Non-catalog item need longer time Not the manufacturer of the item b/o Out of stock b/o Out of stock b/o Out of stock 5

• Sales didn’t contact customer actively

Newport

?? / Lok

(Sales performance)

• Lab condition affected Laser performance

HKU dept of CHEM (YAG LASER)

Spec Phy

Raymond 黑仔

11-Mar

Well operation Lack of quality objective cognition

More quality objective propagation

Improvis of quality objective

Customer Supplier Sales / SVC Barry / Peter SR100820005 RMA 518486 Replaced 7-Sep Cole Parmer Ronald / Peter (Lok) 2 SO100813002HK 25-Aug SR100831011 Demo & Train 2-Sep 3 SO100722001HK -SR100719003