2015年ACCA考试《F6税务》公式解析六

特许公认会计师 F6考试常用计算公式与答题方法介绍

特许公认会计师 F6考试常用计算公式与答题方法介绍ACCA F6的标准格式的确很复杂,所以有很多同学就会自己创造一种新的格式,或者是直接使用恒等式得出计算结果。

确实最后那个数字是正确的,但是在F6的考试中那个数字恰巧不是很重要。

那么临考前有什么办法能够帮助自己多拿几分呢?浦江财经为你介绍特许公认会计师F6考试常用计算公式与答题方法。

大家在做题的时候发现考官给的标准答案后面附带了很多的“NOTE”。

这些“NOTE”其实并不是ACCA考试答案的一部分,而只是考官关于题目考点的解释。

那么我们应该在什么时候写“NOTE”呢?通常情况下在计算中遇到“exempt income”, “exempt benefit”以及capital gain计算的“exempt asset”的时候才需要写“NOTE”。

NOTE不需要写的长篇大论,通常推荐用一句话把事情表达清楚就可以了,毕竟通常这些条目只有half Mark。

Adjustment of trading profit Trading profit 的调整是考试当中的重要考点,但是考生的得分率通常都不尽人意,为什么会这样呢?1、格式书写不符合规范如下是案列trading profit 调整的固定提问方式:Where a question requires the adjustment of profits, candidates will be told in there quire ments what figure to start their computation with (normally the net profit figure for an unincorporated business, or the profit before taxation figure for a limited company). They will also be told that they should list all of the items referred to in the notes to the question, indicating by the use of zero (0) any items, which do not require adjustment. Please see the end of this article for different wording used in variant papers.考生会被要求从一个固定的数字开始调整。

2015年6月ACCA考试F6mock答案

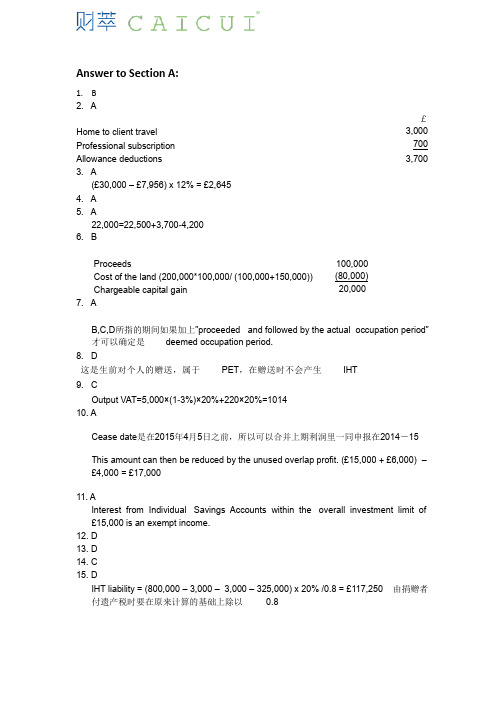

Answer to Section A:1. B2. A£ 3,000 700 Home to client travel Professional subscription Allowance deductions 3,7003. A(£30,000 – £7,956) x 12% = £2,645 4. A5. A22,000=22,500+3,700-4,200 6. BProceeds100,000 (80,000) 20,000Cost of the land (200,000*100,000/ (100,000+150,000)) Chargeable capital gain 7. AB,C,D 所指的期间如果加上”proceeded and followed by the actual occupation period” 才可以确定是 deemed occupation period. 8. D这是生前对个人的赠送,属于 PET ,在赠送时不会产生IHT 。

9. COutput VAT=5,000×(1-3%)×20%+220×20%=1014 10. ACease date 是在2015年4月5日之前,所以可以合并上期利润里一同申报在2014-15 This amount can then be reduced by the unused overlap profit. (£15,000 + £6,000) – £4,000 = £17,00011. AInterest from Individual Savings Accounts within the overall investment limit of £15,000 is an exempt income. 12. D 13. D 14. C 15. DIHT liability = (800,000 – 3,000 – 3,000 – 325,000) x 20% /0.8 = £117,250 付遗产税时要在原来计算的基础上除以 0.8由捐赠者Answer to Section B1. Flick Pick (TX 06/12 Q1)Answer: all figures are in one pound, unless indicated otherwise (a)Other income (Total income)Trading profit (W2)(W3)(W4) Employment income (W1) Property income (W5) Total (net) income8,220 34,388 5,940 48,548 -10,000 38,548Less: Personal allowance (W6) Taxable incomeWorking 1 Employment income Salary 25,665 Benefit:-accommodation benefit (W1.1) -furniture benefit 9,400*0.2 Total6,843 1,880 34,388 Working 1.1 accommodation benefit basic rate: annual value4,600 2,243 6,843additional charge: (144,000-75,000)*3.25% taxable benefit:Working 2 tax-adjusted trading profitYear ended 30 April 2015=29,700- 300 (W2.1) =29,400 Working 2.1 capital allowanceprivate-used carsBusiness use %Capital allowanceTWDV B/D addition 0 18,750 18,750 -500 Balance WDA (8%*4/12) Total60%300 30018,250Working 3 Partnership profit allocationFlickArtTotalTotal29,400 (W2)-2,000less: salary to art Remaining 6,000*4/12=2,00016,44027,400 profit sharing10,960-27,400ratio(4:6) Total10,960 18,440 Working 4 sole trader basis tax year Basis periodProfit2014/15from 1/1/2015-6/4/201510,960 (W3)*3/4=8,220Working 5 property income Rental 660*12 7,920 council tax -1,320 -660 W&T allowance Total(7,920-1,320)*10%5,940Working 6 Personal allowances Adjusted net income= 49,065Born on or after 6 April 1948, so the standard PA of 10,000 should be used(b)3D Ltd will be responsible for paying class 1 NIC (both primary and secondary contributions) in respect of Flick’s salary.3D Ltd will be responsible for paying class 1A NIC in respect of Flick’s taxable benefits. Flick will be responsible for paying class 2 NIC in respect of her trading income. Flick will be responsible for paying class 4 NIC in respect of her trading incomeTutorials:1.第一个税务年度所对应的 basis period 应该为公司成立日至第一个税务年度日(06/04/20XX) 2. For accommodation benefit, since the property was acquired more than 6 years before being provided to Flick, the market value at the date it was provided to her is used as the cost of providing the benefit, instead of the original cost.3. Cost of replacing furniture 和 wear & tear allowance 只能选其一抵减,本题中 flick 选择 使用 wear & tear allowance.4.对于求 trading income 的综合题,必须按照规定步骤按顺序计算:1.先求 tax-adjustedtrading profit. 2. Partnership profit allocation 3. Basis period assessment.2. Neung Ltd(a ) Associates● ● Second Ltd and Fourth Ltd are not associated companies as Neung Ltd has ashareholding of less than 50% in Second Ltd, and Fourth Ltd is dormant. Third Ltd and Fifth Ltd is associated companies as Neung Ltd has ashareholding of over 50% in each case, and both are trading companies. (b )Neung Ltd – Corporation tax computation for the year ended 31 March2015£Trading profit(W1) 358,766(25,200 + 12,600) 37,800396,566Interest income Taxable total profitFranked investment income Augmented profits(37,800/90%) 42,000438,566Corporation tax at marginal rate £396,566 at 21% 83,279(139) Marginal relief1/400 * (500,000 – 438,566) x396,566/438,566 Corporation tax liability83,140(W1) Trading profit£622,536 11,830 Operating profit Depreciation Amortisation7,000 Less: Deduction for lease premium (w2) Capital allowances (w3) Trading profit(4,340) (278,260) 358,766(W2) Deduction for lease premium£140,000 (53,200 86,800 4,340Premium paidLess: £140,000*2%*(20-1)) Assessment on landlordAllowable deduction per year(£86,800/20)(W3) Capital allowancesMain poolSpecial rate pool AllowanceTWDV b/f4,800 12,700Additional (no AIA ) Motor car (1) Motor car (2) Additional ( with AIA)15,40028,600Ventilation system Less: AIA 270,000 (270,000) 28,100 270,000Balance 33,400 (6,012) WDA (18%) WDA (8%) 6,012 2,248 (2,248) 25,852TWDV C/F Total allowance27,388278,260 (W4) Corporation tax rateNeung Ltd has two associated companies; therefore there are three associated companies in total. £ 500,000 100,000Upper limit (£1,500,000/3) Lower limit (£ 300,000/3)3. TomOrdinary shares in Kapook plc(W1)Ordinary shares in Jooba Ltd (no gain no loss transfer between spouses) Antique table (W2)13,600- 3,500- UK Government securities (exempt) Chargeable gains 17,100 (6,100) 11,000 (11,000)Less: losses b/f (W3) Net chargeable gainsLess: annual exempt amount Taxable gainsTom therefore has a nil liability to capital gains tax in 2014/15 and capital losses carried forward of £ (15,900 – 6,100) = £9,800.(w1) The shares in Kapook plc are valued at the lower of: (a) 3.70 + ¼ × (3.90 – 3.70) = 3.75; (b) (3.60 + 3.80)/2 = 3.70The disposal is first matched against the purchase on 24 July 2014 (this is within the following 30 days) and then against the shares in the share pool. The cost of the shares disposed of is, therefore, £23,400 (5,800 + 17,600).No. of sharesCost£ £ Purchase 19 February 2004 Purchase 6 June 20098,000 6,00016,200 14,600 30,800 (17,600) 13,20014,000 (8,000) 6,000 Disposal 20 July 2014 £30,800 × 8,000/14,000 Balance c/f£ Deemed proceeds (10,000 × £3.70) Less: cost 37,000 (23,400) 13,600Chargeable gains(w2) The antique table is a non-wasting chattel. £ proceeds 8,700 (5,200) 3,500Less: cost Chargeable gainsThe maximum gain is 5/3 × £(8,700 − 6,000) = £4,500. The chargeable gain is the lower of £3,500 and £4,500, so it is £3,500.(w3)The set off of the brought forward capital losses is restricted to £6,100 (17,100 – 11,000) so that chargeable gains are reduced to the amount of the annual exempt amount.4. IHT£CLT (20/06/2007) 280,000 Less annual exemption - - 2007/08 2006/07 (3,000) (3,000) 274,000IHT liability274,000 x 0% = 0£PET (05/10/2013)255,000 Less annual exemption - - 2013/14 2012/13(3,000) (3,000) 249,000The PET is initially exemption from IHT liability.Death date: 12/03/2015CLT (20/06/2007) was made more than 7 years ago, so there is no additional IHT liability incurred.£PET (05/10/2013)249,0000 422,500 (W1) – 274,000 = 148,500 x 0% 249,000 – 148,500 = 100,500 x 40% IHT liability40,200 40,200Value of death estate£850,000 460,000 275,000 PropertyBuilding society depositsProceeds of life assurance policy Less Funeral cost(18,000) 1,567,000422,500 – 249,000 = 173,500 x 0%1,567,000 – 173,500 = 1,393,500 x 40% 557,400557,400IHT liability(W1)Nil rate band for Nicola in tax year 2014/15 is 325,000 + 325,000 x (1 – 70%) = £422,500.5.(a) (1) Wind can use both schemes because its expected taxable turnover for the next 12month does not exceed £1,350,000 exclusive of VAT; in addition, for both of theschemes the company is up to date with its VAT returns.(2) With the cash accounting scheme, output VAT will be accounted for one monthlater than at present since the scheme will result in the tax point becoming the datethat payment is received from customers and the recovery of input VAT will not beaffected as these are paid in cash.(3) With the annual accounting scheme, the reduced administration in only having tofile one VAT return each year should have save overtime costs.此处的考点为special scheme,注意三种不同的scheme的使用条件以及各自的优缺点,在回答优缺点时注意结合题目所给具体条件答题(b) (1) from suppliers situated outside EUWind Ltd will have to pay VAT of £8,000 (40,000×20%) to HM Revenue and Customsat the time of importation, and this will be reclaimed as input VAT on the VAT return for the period during which the equipment is imported.(2) From supplier situated within EUVAT will have to be accounted for according to the date of acquisition. This will be theEarlier of date that a VAT invoice is issued or the 15th day of the month following theMonth in which the equipment transported to UK.The VAT charged of £8,000 will be declared on Wind Ltd’ VAT return as output VAT,But will then be reclaimed as input VAT on the same VAT return.6.(a) Sophie Shape – Schedule of tax paymentsDue date Tax year Payment £31 July 2015 2014–15 Second payment on account 3,240 6,480 (5,240 + 1,240) x 50%31 January 2016 2014–15 Balancing payment 5,98012,460 (6,100 + 1,480 + 4,880) – 6,480 (3,240 x 2)31 January 2016 2015–16 First payment on account 3,790 7,580 (6,100 + 1,480) x 50%(b) (1) If Sophie’s payments on account for 2014–15 were reduced to nil, then she would be charged intereston the payments due of £3,240 from the relevant due date to the date of payment.(2) A penalty based on the amount of underpaid tax will be charged as the claim to reduce the payments on account to nil would appear to be made fraudulently or negligently.(c) (1) Unless the return is issued late, the latest date when Sophie can file a paperself-assessment tax return for 2014–15 is 31 October 2015.(d) (1) If HM Revenue and Customs (HMRC) intend to carry out a compliance check into Sophie’s 2014-15 tax return they will have to notify her within 12 months of the date when they receive the return.(2) HMRC has the right to carry out a compliance check as regards the completeness and accuracy of any return, and such a check may be made on a completely random basis.(3) However, compliance checks are generally carried out because of a suspicion that income has been undeclared or because deductions have been incorrectly claimed. For example, where accounting ratios are out of line with industry norms.。

2015年6月ACCA考试《税务》真题及详解

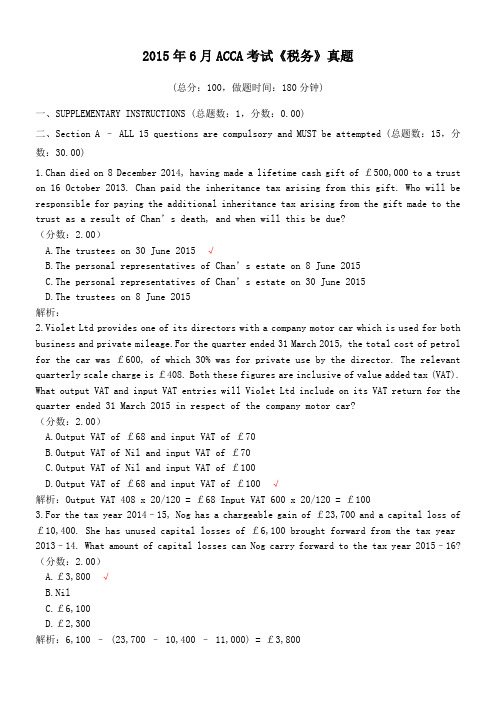

2015年6月ACCA考试《税务》真题(总分:100,做题时间:180分钟)一、SUPPLEMENTARY INSTRUCTIONS (总题数:1,分数:0.00)二、Section A – ALL 15 questions are compulsory and MUST be attempted (总题数:15,分数:30.00)1.Chan died on 8 December 2014, having made a lifetime cash gift of £500,000 to a trust on 16 October 2013. Chan paid the inheritance tax arising from this gift. Who will be responsible for paying the additional inheritance tax arising from the gift made to the trust as a result of Chan’s death, and when will this be due?(分数:2.00)A.The trustees on 30 June 2015 √B.The personal representatives of Chan’s estate on 8 June 2015C.The personal representatives of Chan’s estate on 30 June 2015D.The trustees on 8 June 2015解析:2.Violet Ltd provides one of its directors with a company motor car which is used for both business and private mileage.For the quarter ended 31 March 2015, the total cost of petrol for the car was £600, of which 30% was for private use by the director. The relevant quarterly scale charge is £408. Both these figures are inclusive of value added tax (VAT). What output VAT and input VAT entries will Violet Ltd include on its VAT return for the quarter ended 31 March 2015 in respect of the company motor car?(分数:2.00)A.Output VAT of £68 and input VAT of £70B.Output VAT of Nil and input VAT of £70C.Output VAT of Nil and input VAT of £100D.Output VAT of £68 and input VAT of £100 √解析:Output VAT 408 x 20/120 = £68 Input VAT 600 x 20/120 = £1003.For the tax year 2014–15, Nog has a chargeable gain of £23,700 and a capital loss of £10,400. She has unused capital losses of £6,100 brought forward from the tax year 2013–14. What amount of capital losses can Nog carry forward to the tax year 2015–16? (分数:2.00)A.£3,800 √B.NilC.£6,100D.£2,300解析:6,100 – (23,700 – 10,400 – 11,000) = £3,8004.For the year ended 30 November 2014, Mixiness Ltd has taxable total profits of £1,380,000 and franked investment income (FII) of £240,000. Mixiness Ltd does not have any associated companies. What is Mixiness Ltd’s corporation tax liab ility for the year ended 30 November 2014?(分数:2.00)A.£351,000B.£299,000 √C.£308,200D.£289,800解析:5.Which of the following statements correctly explains the difference between tax evasion and tax avoidance?(分数:2.00)A.Both tax evasion and tax avoidance are illegal, but tax evasion involves providing HM Revenue and Customs with deliberately false informationB.Tax evasion is illegal, whereas tax avoidance involves the minimisation of tax liabilities by the use of any lawful means √C.Both tax evasion and tax avoidance are illegal, but tax avoidance involves providing HM Revenue and Customs with deliberately false informationD.Tax avoidance is illegal, whereas tax evasion involves the minimisation of tax liabilities by the use of any lawful means解析:6.Quinn will not make the balancing payment in respect of her tax liability for the tax year 2013–14 until 17 October 2015. What is the total percentage of penalty which Quinn will be charged by HM Revenue and Customs (HMRC) in respect of the late balancing payment for the tax year 2013–14?(分数:2.00)A.15%B.10% √C.5%D.30%解析:7.Which classes of national insurance contribution is an employer responsible for paying? (分数:2.00)A.Both class 2 and class 4B.Class 1 onlyC.Both class 1 and class 1A √D.Class 2 only解析:8.Alice is in business as a sole trader. On 13 May 2014, she sold a freehold warehouse for £184,000, and this resulted in a chargeable gain of £38,600. Alice purchased a replacement freehold warehouse on 20 May 2014 for £143,000.Where possible, Alice always makes a claim to roll over gains against the cost of replacement assets. Both buildings have been, or will be, used for business purposes by Alice. What is the base cost of the replacement warehouse for capital gains tax purposes?(分数:2.00)A.£181,600B.£104,400C.£143,000 √D.£102,000解析:(184,000 – 143,000) > 38,600 The base cost is the actual cost of £143,000. There is no rollover relief because the proceeds not reinvested are greater than the chargeable gain.9.For the tax year 2013–14, Willard filed a paper self-assessment tax return on 10 August 2014. What is the deadline for Willard to make an amendment to his tax return for the tax year 2013–14, and by what date will HM Revenue and Customs (HMRC) have to notify Willard if they intend to carry out a compliance check into this return? Amendment Compliance check (分数:2.00)A.10 August 2015 31 January 2016B.10 August 2015 10 August 2015C.31 January 2016 10 August 2015 √D.31 January 2016 31 January 2016解析:10.For the tax year 2014–15, Chi has a salary of £53,000. She received child benefit of £1,771 during this tax year. What is Chi’s child benefit income tax charge for the tax year 2014–15?(分数:2.00)A.£1,771B.NilC.£1,240D.£531 √解析:1,771 x 30% ((53,000 – 50,000)/100) = £53111.Samuel is planning to leave the UK to live overseas, having always previously been resident in the UK. He will not automatically be treated as either resident in the UK or not resident in the UK. Samuel has several ties with the UK and will need to visit the UK for 60 days each tax year. However, he wants to be not resident after he leaves the UK. For the first two tax years after leaving the UK, what is the maximum number of ties。

ACCA F6《税务》常用公式汇总

ACCA F6《税务》常用公式汇总

企业所得税

1、年税工薪扣标准=年员工平均数×政府定均月税工资×12

2、招待费扣标=销(营)收净×级扣例+速增数

销收比例速增数

小于1500万5‰ 0

大于1500万元3‰ 3万

3、某年可补被并企亏得额=并企某年未补亏前得额×(被并企净资公允价/并后并企业全部净资产的公允价值)

4、纳税=纳得额×税率

5、纳得额=收入总额-准予扣除项目金额

6、核定所得率,所得税=纳得额×率

纳得额=收入额×应税所得率或=本费支/(1-应税所得率)×应税所得率

(应税所得率一般题目都会给出。

因此,以下这个表估计做综合题时没什么用处。

在做选择题时可能会有用处:)

应税所得率表

工交商7-20%

建、房10-20%

饮服10-25%。

ACCA F6 纳税时间点 罚款快速总结

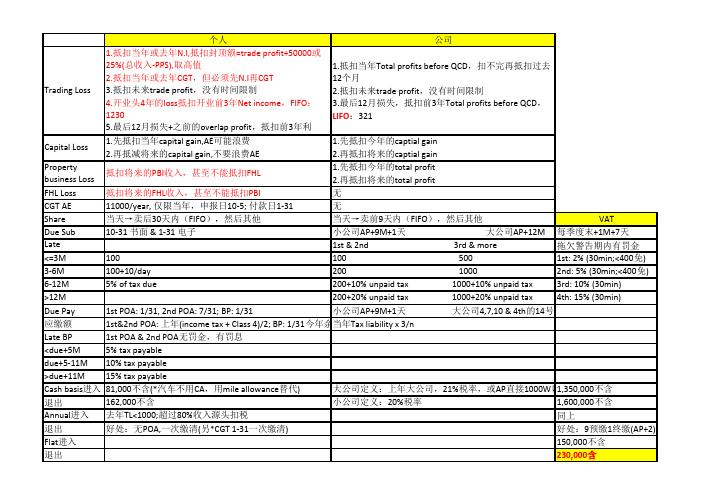

个人公司Trading Loss 1.抵扣当年或去年N.I,抵扣封顶额=trade profit+50000或25%(总收入‐PPS),取高值2.抵扣当年或去年CGT,但必须先N.I再CGT3.抵扣未来trade profit,没有时间限制4.开业头4年的loss抵扣开业前3年Net income,FIFO:12305.最后12月损失+之前的overlap profit,抵扣前3年利1.抵扣当年Total profits before QCD,扣不完再抵扣过去12个月2.抵扣未来trade profit,没有时间限制3.最后12月损失,抵扣前3年Total profits before QCD,LIFO:321Capital Loss 1.先抵扣当年capital gain,AE可能浪费2.再抵减将来的capital gain,不要浪费AE1.先抵扣今年的captial gain2.再抵扣将来的captial gainProperty business Loss 抵扣将来的PBI收入,甚至不能抵扣FHL1.先抵扣今年的total profit2.再抵扣将来的total profitFHL Loss抵扣将来的FHL收入,甚至不能抵扣PBI无CGT AE11000/year, 仅限当年,申报日10‐5; 付款日1‐31无Share当天→卖后30天内(FIFO),然后其他当天→卖前9天内(FIFO),然后其他VATDue Sub10‐31 书面 & 1‐31 电子小公司AP+9M+1天 大公司AP+12M每季度末+1M+7天Late1st & 2nd 3rd & more拖欠警告期内有罚金<=3M100100 5001st: 2% (30min;<400免) 3‐6M100+10/day200 10002nd: 5% (30min;<400免) 6‐12M5% of tax due200+10% unpaid tax 1000+10% unpaid tax3rd: 10% (30min)>12M200+20% unpaid tax 1000+20% unpaid tax4th: 15% (30min)Due Pay1st POA: 1/31, 2nd POA: 7/31; BP: 1/31小公司AP+9M+1天 大公司4,7,10 & 4th的14号应缴额1st&2nd POA: 上年(income tax + Class 4)/2; BP: 1/31今年余当年Tax liability x 3/nLate BP1st POA & 2nd POA无罚金,有罚息<due+5M5% tax payabledue+5‐11M10% tax payable>due+11M15% tax payableCash basis进入81,000不含(*汽车不用CA,用mile allowance替代)大公司定义:上年大公司,21%税率,或AP直接1000W以1,350,000不含退出162,000不含小公司定义:20%税率1,600,000不含Annual进入去年TL<1000;超过80%收入源头扣税同上退出好处:无POA,一次缴清(另*CGT 1‐31一次缴清)好处:9预缴1终缴(AP+2) Flat进入150,000不含退出230,000含Income Tax CGT NISAs dividend / interest exempt exemptPremium exempt exempt政府securities No need to gross up exemptGaming exempt exemptNSIB interest No need to gross upMotor计算benefits exemptScholarships exempt工伤补贴exempt。

ACCA F6知识要点汇总

F6知识点:第一章UK TAX SYSTEMTaxation function: encourage economic, social and environmental behaviour Structure: 税务由HMRC管理Human revenue and customs 英国税务及海关总署Source of law 立法Finance Act每年更新税率Tax year: April 6th to April 5thTax evasion is illegal 逃税非法 & Tax avoidance is legal 合理避税合法第二章Computation of taxable income and income tax liability1.Resident判定UK resident individuals UK & oversea income都交税Non‐UK resident individuals 仅UK income交税5 UK Ties:▲考试提供表格:Days inUK Previously resident Not previously resident < 16 Automatically not resident Automatically not resident 16 to 45 Resident if 4 UK ties(or more) Automatically not resident 46 to 90 Resident if 3 UK ties(or more) Resident if 3 UK ties(or more) 91 to 120 Resident if 2 UK ties(or more) Resident if 2 UK ties(or more) 121 to 182 Resident if 1 UK ties(or more) Resident if 1 UK ties(or more) 183 Automatically resident Automatically resident1. Types of incomeNon ‐saving income Trade incomeEmployment incomeProperty incomeSavings income Taxed income (20% tax 已扣)Bank interestBuilding society interest Interest received gross (未扣税)Government stocks (gilts 债券) interestNational saving & invest bank interest Dividend income 10% tax 已扣This tax credit is not refundable. Exempt income 免税收入,回答题目时必须注明时免税收入,不写没分Interest from Saving Certificates issued by National Savings and InvestmentBank(UK 国民储蓄和投资银行:储蓄账户免税,投资账户收税)国民储蓄券 Statutory redundancy money 裁员补偿Betting and gaming winnings 博彩奖金(收其他税,不收个税) Scholarships 奖学金Interest on damages for personal injuries 个人受伤赔偿,包括工资补贴等 in UK < 16Din UK < 46D, not resident in past 3 tax yearsFull time oversea work & in UK < 90Din UK >183D only home in UK Full time work in UK UK House in useSubstantive work in UK > 90D in either two past tax years more time in UK than oversea FamilyLocal authority grant 地方补助Income from investments made through new individual savings accounts (NISAs) NISA有3种, 每个Tax year overall subscription limit is 15,000。

ACCA F6 2015 June specimen 答案

P a p e r F 6 ( U K )SUPPLEMENTARY INSTRUCTIONS1.Calculations and workings need only be made to the nearest £.2.All apportionments should be made to the nearest month.3.All workings should be shown in Section B.TAX RATES AND ALLOWANCESThe following tax rates and allowances are to be used in answering the questions.Income taxNormal Dividendrates ratesBasic rate£1 – £31,86520%10%Higher rate£31,866 to £150,00040%32·5% Additional rate£150,001 and over45%37·5%A starting rate of 10% applies to savings income where it falls within the first £2,880 of taxable income.Personal allowancePersonal allowanceBorn on or after 6 April 1948£10,000Born between 6 April 1938 and 5 April 1948£10,500Born before 6 April 1938 £10,660Income limitPersonal allowance£100,000Personal allowance (born before 6 April 1948)£27,000Residence statusDays in UK Previously resident Not previously residentLess than 16Automatically not resident Automatically not resident16 to 45Resident if 4 UK ties (or more)Automatically not resident46 to 90Resident if 3 UK ties (or more)Resident if 4 UK ties91 to 120Resident if 2 UK ties (or more)Resident if 3 UK ties (or more)121 to 182Resident if 1 UK tie (or more)Resident if 2 UK ties (or more)183 or more Automatically resident Automatically residentChild benefit income tax chargeWhere income is between £50,000 and £60,000, the charge is 1% of the amount of child benefit received for every £100 of income over £50,000.Car benefit percentageThe relevant base level of COemissions is 95 grams per kilometre.2The percentage rates applying to petrol cars with COemissions up to this level are:275 grams per kilometre or less5%76 grams to 94 grams per kilometre11%95 grams per kilometre12%2Car fuel benefitThe base figure for calculating the car fuel benefit is £21,700.New individual savings accounts (NISAs)The overall investment limit is £15,000.Pension scheme limitAnnual allowance –2014–15£40,000–2011–12 to 2013–14£50,000 The maximum contribution that can qualify for tax relief without any earnings is £3,600.Authorised mileage allowances: carsUp to 10,000 miles45p Over 10,000 miles25pCapital allowances: rates of allowancePlant and machineryMain pool18% Special rate pool8% Motor carsNew cars with CO2emissions up to 95 grams per kilometre100%CO2emissions between 96 and 130 grams per kilometre18%CO2emissions over 130 grams per kilometre8%Annual investment allowanceRate of allowance100% Expenditure limit£500,000Cap on income tax reliefsUnless otherwise restricted, reliefs are capped at the higher of £50,000 or 25% of income.Corporation taxFinancial year201220132014Small profits rate20%20%20%Main rate24%23%21%Lower limit£300,000£300,000£300,000Upper limit£1,500,000£1,500,000£1,500,000Standard fraction1/1003/4001/400Marginal reliefStandard fraction x (U –A) x N/A3[P.T.O.Value added tax (VAT)Standard rate20% Registration limit£81,000 Deregistration limit£79,000Inheritance tax: tax rates£1 –£325,000Nil Excess–Death rate40%–Lifetime rate20%Inheritance tax: taper reliefYears before death Percentagereduction Over 3 but less than 4 years20% Over 4 but less than 5 years40% Over 5 but less than 6 years60% Over 6 but less than 7 years80%Capital gains taxRates of tax–Lower rate18%–Higher rate28% Annual exempt amount£11,000 Entrepreneurs’ relief–Lifetime limit£10,000,000–Rate of tax 10%National insurance contributions(Not contracted out rates)%Class 1Employee£1 – £7,956 per year Nil£7,957 – £41,865 per year12·0£41,866 and above per year12·0Class 1Employer£1 – £7,956 per year Nil£7,957 and above per year13·8Employment allowance£2,000Class 1A13·8Class 2£2·75 per weekSmall earnings exemption limit£5,885Class 4£1 – £7,956 per year Nil£7,957 – £41,865 per year9·0£41,866 and above per year2·0Rates of interest (assumed)Official rate of interest 3·25%Rate of interest on underpaid tax 3%Rate of interest on overpaid tax0·5%4Section A – ALL 15 questions are compulsory and MUST be attemptedPlease use the space provided on the inside cover of the Candidate Answer Booklet to indicate your chosen answer to each multiple-choice question.Each question is worth 2 marks.1During the tax year 2014–15, William was paid a gross annual salary of £82,700. He also received taxable benefits valued at £5,400.What amount of class 1 national insurance contributions (NIC) will have been suffered by William for the tax year 2014–15?A£4,994B£8,969C£4,886D£4,0692You are a trainee Chartered Certified Accountant and your firm has a client who has refused to disclose a chargeable gain to HM Revenue and Customs (HMRC).From an ethical viewpoint, which of the following actions could be expected of your firm?(1)Reporting under the money laundering regulations(2)Advising the client to make disclosure(3)Ceasing to act for the client(4)Informing HMRC of the non-disclosure(5)Warning the client that your firm will be reporting the non-disclosure(6)Notifying HMRC that your firm has ceased to act for the clientA2, 3 and 5B1, 2, 3 and 6C2, 3 and 4D1, 4, 5 and 63Martin was born on 28 June 1965. He is self-employed, and for the year ended 5 April 2015 his trading profit was £109,400. During the tax year 2014–15, Martin made a gift aid donation of £800 (gross) to a national charity.What amount of personal allowance will Martin be entitled to for the tax year 2014–15?A£10,000B£5,700C£5,300D Nil5[P.T.O.4For the year ended 31 March 2015, Halo Ltd made a trading loss of £180,000.Halo Ltd has owned 100% of the ordinary share capital of Shallow Ltd since it began trading on 1 July 2014. For the year ended 30 June 2015, Shallow Ltd will make a trading profit of £224,000.Neither company has any other taxable profits or allowable losses.What is the maximum amount of group relief which Shallow Ltd can claim from Halo Ltd in respect of the trading loss of £180,000 for the year ended 31 March 2015?A£180,000B£168,000C£45,000D£135,0005For the year ended 31 March 2014, Sizeable Ltd had a corporation tax liability of £384,000, and for the year ended31 March 2015 had a liability of £456,000.Sizeable Ltd is a large company, and is therefore required to make instalment payments in respect of its corporation tax liability.The company’s profits have accrued evenly throughout each year.What is the amount of each instalment payable by Sizeable Ltd in respect of its corporation tax liability for the year ended 31 March 2015?A£228,000B£114,000C£96,000D£192,0006For the year ended 31 December 2014, Lateness Ltd had a corporation tax liability of £60,000, which it did not pay until 31 March 2016. Lateness Ltd is not a large company.How much interest will Lateness Ltd be charged by HM Revenue and Customs (HMRC) in respect of the late payment of its corporation tax liability for the year ended 31 December 2014?A£900B£2,250C£300D£4507On 26 November 2014 Alice sold an antique table for £8,700. The antique table had been purchased on 16 May 2011 for £3,800.What is Alice’s chargeable gain in respect of the disposal of the antique table?A£4,500B£1,620C£4,900D Nil68On 14 November 2014, Jane made a cash gift to a trust of £800,000 (after deducting all available exemptions).Jane paid the inheritance tax arising from this gift. Jane has not made any other lifetime gifts.What amount of lifetime inheritance tax would have been payable in respect of Jane’s gift to the trust?A£95,000B£190,000C£118,750D£200,0009During the tax year 2014–15, Mildred made the following cash gifts to her grandchildren:(1)£400 to Alfred(2)£140 to Minnie(3) A further £280 to Minnie(4)£175 to WinifredWhich of the gifts will be exempt from inheritance tax under the small gifts exemption?A1, 2, 3 and 4B2, 3 and 4 onlyC 2 and 4 onlyD 4 only10For the quarter ended 31 March 2015, Zim had standard rated sales of £59,700 and standard rated expenses of £27,300. Both figures are inclusive of value added tax (VAT).Zim uses the flat rate scheme to calculate the amount of VAT payable, with the relevant scheme percentage for her trade being 12%.How much VAT will Zim have to pay to HM Revenue and Customs (HMRC) for the quarter ended 31 March 2015?A£6,396B£3,888C£6,480D£7,16411Which of the following assets will ALWAYS be exempt from capital gains tax?(1) A motor car suitable for private use(2) A chattel(3) A UK Government security (gilt)(4) A houseA 1 and 3B 2 and 3C 2 and 4D 1 and 47[P.T.O.12Winston has already invested £8,000 into a cash new individual savings account (NISA) during the tax year 2014–15. He now wants to invest into a stocks and shares NISA.What is the maximum possible amount which Winston can invest into a stocks and shares NISA for the tax year 2014–15?A£15,000B£7,000C NilD£7,50013Ming is self-employed. How long must she retain the business and non-business records used in preparing her self-assessment tax return for the tax year 2014–15?Business records Non-business recordsA31 January 201731 January 2017B31 January 201731 January 2021C31 January 202131 January 2021D31 January 202131 January 201714Moon Ltd has had the following results:Period Profit/(loss)£Year ended 31 December 2014 (105,000)Four-month period ended 31 December 201343,000Year ended 31 August 2013 96,000The company does not have any other income.How much of Moon Ltd’s trading loss for the year ended 31 December 2014 can be relieved against its total profits of £96,000 for the year ended 31 August 2013?A£64,000B£96,000C£70,000D£62,00015Nigel has not previously been resident in the UK, being in the UK for less than 20 days each tax year. For the tax year 2014–15, he has three ties with the UK.What is the maximum number of days which Nigel could spend in the UK during the tax year 2014–15 without being treated as resident in the UK for that year?A90 daysB182 daysC45 daysD120 days8Section B – ALL SIX questions are compulsory and MUST be attempted1(a)On 10 June 2014, Delroy made a gift of 25,000 £1 ordinary shares in Dub Ltd, an unquoted trading company, to his son, Grant. The market value of the shares on that date was £240,000. Delroy had subscribed for the 25,000 shares in Dub Ltd at par on 1 July 2004. Delroy and Grant have elected to hold over the gain as a gift of a business asset.Grant sold the 25,000 shares in Dub Ltd on 18 September 2014 for £240,000.Dub Ltd has a share capital of 100,000 £1 ordinary shares. Delroy was the sales director of the company from its incorporation on 1 July 2004 until 10 June 2014. Grant has never been an employee or a director of Dub Ltd.For the tax year 2014–15 Delroy and Grant are both higher rate taxpayers. Neither of them has made any other disposals of assets during the year.Required:(i)Calculate Grant’s capital gains tax liability for the tax year 2014–15.(3 marks)(ii)Explain why it would have been beneficial for capital gains tax purposes if Delroy had instead sold the 25,000 shares in Dub Ltd himself for £240,000 on 10 June 2014, and then gifted the cash proceedsto Grant.(2 marks)(b)On 12 February 2015, Marlon sold a house for £497,000, which he had owned individually. The house hadbeen purchased on 22 October 1999 for £146,000. Marlon incurred legal fees of £2,900 in connection with the purchase of the house, and legal fees of £3,700 in connection with the disposal.Throughout the period of ownership the house was occupied by Marlon and his wife, Alvita, as their main residence. One-third of the house was always used exclusively for business purposes by the couple.Entrepreneurs’ relief is not available in respect of this disposal.For the tax year 2014–15 Marlon is a higher rate taxpayer, but Alvita did not have any taxable income. Neither of them has made any other disposals of assets during the year.Required:(i)Calculate Marlon’s chargeable gain for the tax year 2014–15.(3 marks)(ii)Calculate the amount of capital gains tax which could have been saved if Marlon had transferred 50% ownership of the house to Alvita prior to its disposal.(2 marks)(10 marks)9[P.T.O.2You should assume that today’s date is 15 March 2015.Opal Elder, aged 71, owns the following assets:(1)T wo properties respectively valued at £374,000 and £442,000. The first property has an outstanding repaymentmortgage of £160,000, and the second property has an outstanding endowment mortgage of £92,000.(2)Vintage motor cars valued at £172,000.(3)Investments in new individual savings accounts (NISAs) valued at £47,000, savings certificates from NS&I(National Savings and Investments) valued at £36,000, and government stocks (gilts) valued at £69,000.Opal owes £22,400 in respect of a personal loan from a bank, and she has also verbally promised to pay legal fees of £4,600 incurred by her nephew.Under the terms of her will, Opal has left all of her estate to her children. Opal’s husband is still alive.On 14 August 2005, Opal had made a gift of £100,000 to her daughter, and on 7 November 2014, she made a gift of £220,000 to her son. Both these figures are after deducting all available exemptions.The nil rate band for the tax year 2005–06 is £275,000.Required:(a)(i)Calculate Opal Elder’s chargeable estate for inheritance tax purposes were she to die on20 March 2015.(5 marks)(ii)Calculate the amount of inheritance tax which would be payable in respect of Opal Elder’s chargeable estate, and state who will be responsible for paying the tax. (3 marks)(b)Advise Opal Elder as to why the inheritance tax payable in respect of her estate would alter if she were tolive for another seven years until 20 March 2022, and by how much.Note: You should assume that both the value of Opal Elder’s estate and the nil rate band will remain unchanged.(2 marks)(10 marks)103Glacier Ltd runs a business providing financial services. The following information is available in respect of the company’s value added tax (VAT) for the quarter ended 31 March 2015:(1)Invoices were issued for sales of £44,600 to VAT registered customers. Of this figure, £35,200 was in respectof exempt sales and the balance in respect of standard rated sales. The standard rated sales figure is exclusive of VAT.(2)In addition to the above, on 1 March 2015 Glacier issued a VAT invoice for £8,000 plus VAT of £1,600 to aVAT registered customer. This was in respect of a contract for financial services which will be completed on15 April 2015. The customer paid for the contract in two instalments of £4,800 on 31 March 2015 and30 April 2015.(3)Invoices were issued for sales of £289,100 to non-VAT registered customers. Of this figure, £242,300 was inrespect of exempt sales and the balance in respect of standard rated sales. The standard rated sales figure is inclusive of VAT.(4)The managing director of Glacier Ltd is provided with free fuel for private mileage driven in her company motorcar. During the quarter ended 31 March 2015, this fuel cost Glacier Ltd £260. The relevant quarterly scale charge is £408. Both these figures are inclusive of VAT.For the quarters ended 30 September 2013 and 30 June 2014, Glacier Ltd was one month late in submitting its VAT returns and in paying the related VAT liabilities. All of the company’s other VAT returns have been submitted on time.Required:(a)Calculate the amount of output VAT payable by Glacier Ltd for the quarter ended 31 March 2015.(4 marks)(b)Advise Glacier Ltd of the default surcharge implications if it is one month late in submitting its VAT returnfor the quarter ended 31 March 2015 and in paying the related VAT liability.(3 marks)(c)State the circumstances in which Glacier Ltd is and is not required to issue a VAT invoice, and the periodduring which such an invoice should be issued.(3 marks)(10 marks)4Sophie Shape has been a self-employed sculptor since 1996, preparing her accounts to 5 April. Sophie’s tax liabilities for the tax years 2013–14 and 2014–15 are as follows:2013–142014–15££Income tax liability5,2406,100Class 2 national insurance contributions143143Class 4 national insurance contributions1,2401,480Capital gains tax liability04,880No income tax has been deducted at source.Required:(a)Prepare a schedule showing the payments on account and balancing payment which Sophie Shape will havemade, or will have to make, during the period from 1 April 2015 to 31 March 2016.Note: Your answer should clearly identify the relevant due date of each payment.(4 marks)(b)State the implications if Sophie Shape had made a claim to reduce her payments on account for the tax year2014–15 to nil without any justification for doing so.(2 marks)(c)Advise Sophie Shape of the latest date by which she can file a paper self-assessment tax return for the taxyear 2014–15.(1 mark)(d)State the period during which HM Revenue and Customs (HMRC) will have to notify Sophie Shape if theyintend to carry out a compliance check in respect of her self-assessment tax return for the tax year 2014–15, and the possible reasons why such a check would be made.Note: You should assume that Sophie will file her tax return by the filing date.(3 marks)(10 marks)5On 6 April 2014, Simon Bass, who was born on 14 June 1991, commenced employment with Echo Ltd as a music critic. On 1 January 2015, he commenced in partnership with Art Beat running a small music venue, preparing accounts to 30 April. The following information is available for the tax year 2014–15:Employment(1)During the tax year 2014–15, Simon was paid a gross annual salary of £23,700.(2)During May 2014, Echo Ltd paid £11,600 towards Simon’s removal expenses when he permanently moved totake up his new employment with the company, as he did not live within a reasonable commuting distance. The £11,600 covered both his removal expenses and the legal costs of acquiring a new main residence.(3)Throughout the tax year 2014–15, Echo Ltd provided Simon with living accommodation. The company hadpurchased the property in 2004 for £89,000, and it was valued at £143,000 on 6 April 2014. The annual value of the property is £4,600. The property was furnished by Echo Ltd during March 2014 at a cost of £9,400.Partnership(1)The partnership’s tax adjusted trading profit for the four-month period ended 30 April 2015 is £29,700. Thisfigure is before taking account of capital allowances.(2)The only item of plant and machinery owned by the partnership is a motor car which cost £18,750 on1 February 2015. The motor car has a CO2emission rate of 155 grams per kilometre. It is used by Art, and40% of the mileage is for private journeys.(3)Profits are shared 40% to Simon and 60% to Art. This is after paying an annual salary of £6,000 to Art. Property income(1)Simon owns a freehold house which is let out furnished. The property was let throughout the tax year 2014–15at a monthly rent of £660.(2)During the tax year 2014–15, Simon paid council tax of £1,320 in respect of the property, and also spent£2,560 on purchasing new furniture.(3)Simon claims the wear and tear allowance.Required:(a)Calculate Simon Bass’s taxable income for the tax year 2014–15.(13 marks)(b)State TWO advantages for the partnership of choosing 30 April as its accounting date rather than 5 April.(2 marks)(15 marks)6You are a trainee accountant and your manager has asked you to correct a corporation tax computation which has been prepared by the managing director of Naive Ltd, a company which manufactures children’s board games. The corporation tax computation is for the year ended 31 March 2015 and contains a significant number of errors: Naive Ltd – Corporation tax computation for the year ended 31 March 2015£T rading profit (working 1)494,200 Loan interest received (working 2)32,100–––––––––526,300 Dividends received (working 3)28,700–––––––––555,000–––––––––Corporation tax (555,000 at 21%)116,550–––––––––Working 1 – Trading profit£Profit before taxation395,830 Depreciation15,740 Donations to political parties400 Qualifying charitable donations900 Accountancy2,300 Legal fees in connection with the issue of loan notes (the loan was used to financethe company’s trading activities) 5,700 Entertaining suppliers3,600 Entertaining employees1,700 Gifts to customers (pens costing £40 each and displaying Naive Ltd’s name)920 Gifts to customers (food hampers costing £45 each and displaying Naive Ltd’s name)1,650 Capital allowances (working 4)65,460–––––––––T rading profit494,200–––––––––Working 2 – Loan interest received£Loan interest receivable32,800 Accrued at 1 April 201410,600 Accrued at 31 March 2015(11,300)–––––––––Loan interest received32,100–––––––––The loan was made for non-trading purposes.Working 3 – Dividends received£From unconnected UK companies20,700 From a 100% UK subsidiary company8,000–––––––––Dividends received28,700–––––––––These figures were the actual cash amounts received.Working 4 – Capital allowancesMain Motor Special Allowancespool car rate pool££££Written down value (WDV) brought forward12,40013,600AdditionsMachinery 42,300Motor car [1] 13,800Motor car [2] 14,000––––––––68,500Annual investment allowance (AIA)(68,500)68,500 Disposal proceeds(9,300)––––––––4,300Balancing allowance(4,300)(4,300)––––––––Writing down allowance (WDA) – 18%(2,520) x 50%1,260––––––––––––––––WDV carried forward 011,480––––––––––––––––––––––––T otal allowances65,460––––––––(1)Motor car [1] has a CO2emission rate of 110 grams per kilometre.(2)Motor car [2] has a CO2emission rate of 155 grams per kilometre. This motor car is used by the sales managerand 50% of the mileage is for private journeys.(3)All of the items included in the special rate pool at 1 April 2014 were sold for £9,300 during the year ended31 March 2015. The original cost of these items was £16,200.Other informationFrom your files, you note that Naive Ltd has one associated company (the 100% UK subsidiary company mentioned in working 3).Required:Prepare a corrected version of Naive Ltd’s corporation tax computation for the year ended 31 March 2015. Note: You should indicate by the use of zero any items in the computation of the trading profit for which no adjustment is required.(15 marks)End of Question PaperFundamentals Level – Skills Module, Paper F6 (UK)Specimen Exam Answers Taxation (United Kingdom)and Marking Scheme Section A1C(33,909 (41,865 –7,956) at 12%) + (40,835 (82,700 –41,865) at 2%) = £4,8862B3B£Personal allowance10,000Restriction (109,400 – 800 – 100,000 = 8,600/2)(4,300)––––––Restricted personal allowance5,700––––––4DLower of:£135,000 (180,000 x 9/12)£168,000 (224,000 x 9/12)5B456,000/4 = £114,0006A60,000 x 3% x 6/12 = £900 (period 1 October 2015 to 31 March 2016)7A2,700 (8,700 –6,000) x 5/3 = £4,500This is less than £4,900 (8,700 – 3,800)8C475,000 (800,000 – 325,000) x 20/80 = £118,7509D10D59,700 x 12% = £7,16411A12B15,000 – 8,000 = £7,00013CMarks 14D105,000 – 43,000 = £62,00015 A–––2 marks each30–––Section B Marks 1(a)Delroy and Grant(i)Grant – Capital gains tax liability 2014–15£Ordinary shares in Dub LtdDisposal proceeds240,000½Cost (25,000)1––––––––215,000 Annual exempt amount(11,000)½––––––––204,000––––––––Capital gains tax: 204,000 at 28%57,1201–––––––––––3–––Tutorial notes:(1)Because the whole of Delroy’s chargeable gain has been held over, Grant effectively took over theoriginal cost of £25,000.(2)The disposal does not qualify for entrepreneurs’ relief as Grant was neither an officer nor anemployee of Dub Ltd.(ii)(1)The disposal would have qualified for entrepreneurs’ relief as Delroy was the sales director of Dub Ltd, and his shareholding of 25% (25,000/100,000 x 100) was more than the minimum requiredholding of 5%.1(2)The capital gains tax liability would therefore have been calculated at the rate of 10%.½(3) There are no capital gains tax implications regarding a gift of cash. ½–––2–––(b)Marlon and Alvita(i)Marlon – Chargeable gain 2014–15££HouseDisposal proceeds497,000½Cost 146,000½Incidental costs (2,900 + 3,700)6,6001––––––––(152,600)––––––––344,400Principal private residence exemption (229,600)1–––––––––––114,8003–––––––––––(1)One-third of Marlon’s house was always used exclusively for business purposes, so the principalprivate residence exemption is restricted to £229,600 (344,400 x 2/3).(ii)(1)The capital gains tax saving if 50% ownership of the house had been transferred to Alvita prior to its disposal would have been £6,266, calculated as follows:£Annual exempt amount11,000 at 28%3,0801Lower rate tax saving31,865 at 10% (28% –18%)3,1861–––––––––6,2662–––––––––10–––Tutorial note:Transferring 50% ownership of the house to Alvita prior to its disposal would haveenabled her annual exempt amount and lower rate tax band of 18% for 2014–15 to be utilised.Marks 2(a)(i)Opal Elder – Chargeable estate££Property (374,000 + 442,000)816,000½Repayment mortgage160,000½Endowment mortgage01––––––––(160,000)––––––––656,000 Motor cars172,000½Investments (47,000 + 36,000 + 69,000)152,0001––––––––980,000 Bank loan22,400½Legal fees01––––––––(22,400)–––––––––––Chargeable estate 957,6005–––––––––––Tutorial notes:(1)There is no deduction in respect of the endowment mortgage as this will be repaid upon death bythe life assurance element of the mortgage.(2)The promise to pay the nephew’s legal fees is not deductible as it is not legally enforceable.(ii)Opal Elder – Inheritance tax on death estate£Chargeable estate957,600––––––––IHT liability 105,000 (working) at nil%0W 852,600 at 40% 341,040½––––––––341,040––––––––(1)The personal representatives of Opal’s estate will be responsible for paying the inheritance tax.1Working – Available nil rate band£Nil rate band325,000½Potentially exempt transfers – 14 August 20050½–7 November 2014(220,000)½––––––––––––105,0003––––––––––––Tutorial note:The potentially exempt transfer on 14 August 2005 is exempt from inheritance tax as itwas made more than seven years before 20 March 2015.(b)(1)If Opal were to live for another seven years, then the potentially exempt transfer on 7 November 2014would become exempt.1(2)The inheritance tax payable in respect of her estate would therefore decrease by £88,000 (220,000 at40%).1–––2–––10–––。

2015年ACCA考试F6科目大解析

2015年ACCA考试F6科目大解析科目介绍:F6《税法》的大纲为学员介绍税法科目的核心知识点和主要的税法计算部分,它们影响着个人和商业活劢。

首先大纲介绍了英国的税法系统;其次介绍作为一名会计师必须详绅理解开掌握各种税收及其义务,例如个体所得税义务,公司所得税义务,应税利得,遗产税,国民保险制度,增值税和纳税人义务及其代理人。

除了掌握基础税法的核心部分,学员还应该能够计算应纳税义务,解释计算的依据,应用避税计划技巧为个体和公司避税,仍商业或者个人案例中识别各种税的合规问题。

近几年考试通过率趋势图:知识结构:科目关联性:F6课程是ACCA基础阶段唯一的一门税务科目,在整个ACCA课程体系中相对来说比较独立,和它直接相关的科目只有与业阶段的P6(高级税务)。

相关知识掌握:学习f6之前应该要有财务报表有基本的学习认知,因为在个人所得税和企业所得税的计算中需要懂得财务利润是怎么得来的,权责发生制和收付实现制的差别。

考试形式:今年f6暂时不做考题的变化。

F6的考试时长为3小时。

考试题共有五道全为必选题,以计算为主。

第一题主要是考察的是个人所得税和第事题主要考察的是公司税,这两道题一共55分,一题30分,另一题25分。

第三题主要考察的是个人戒者公司的应税利得,15分。

第四第五题考察的是大纲的其他部分,每题15分。

至少10分的内容会涉及增值税的考察,通常会包含在第一或第二题,但是增值税也有可能单独作为一题进行考察。

遗产税会出现在第三,第四或者第五题中考察,分值为5分至15分。

社会保险不会单独作为一题,一般在个人所得税戒公司税中考察。

集团的公司税可能会在第事题或第四,第五题中考察。

除了第三题之外,应税利得还可能会在其他题目中涉及一小部分。

关于税负最小化或者递延纳税义务的相关事项可能会在五道题目中任何一道出现。

ACCAF6常用计算及格式

Income tax 计算格式Non‐savings income Savings income Dividend income Trading profit X X Employment income X X Property business income X X Savings (x100/80)X X Dividends (x100/90)X X Total income X X X X Less: qualifying interest paid(X)(X) Net income X X X X Less: personal allowance(10000+‐)(X) Txable income X X X X Income tax liability X Less tax suffered at sourceDividends (10%)XSavings (20%)XPAYE (20‐45%)X(X) Income tax payable X Trading Profit(only for self‐employed)个税Profit Before Taxation X Add: Non‐deductible expenditure X Less: Income under other schedules(X)Interest Income(X)Dividend Income(X)Rent Income(X)Profit on disposal of non‐current(X) Less: Capital Allowance (私用扣WDA; AIA asset; FYA; BC/BA(X) Tax adjusted Trading Profit X Employment Income X Salary货币收入X Bonus货币收入XCommission货币收入X Add:Benefit in kind非货币收入X Less: Allowable deduction如OPC职位养老金(X) Employment Income XTaxable benefit on not‐job related living accommodation X General Charge = Annual value & Rent paid by the employer,取高值X Add:Additional charge = (Cost ‐ £75,000) * official interest rate X这里,如购买日‐第一次出租<6年,取Cost;>6年,取第一次出租时MV Less: Job related part(X) Less: Rent paid by employee(X)XMileage AllowanceEmployer Paid X Less: HMRC 10,000 at 45p; > 10,000 at 25p(X) Taxable benefit X Or Allowable deduction(X) Capital Gain TaxGross proceeds X Less: Incidental costs of disposal(X) Net proceeds X Less: Cost(X) Less: Enhancement expenditure包括诉讼费,建围栏(X) Capital gain/(capital loss) X/(X) Less: Individual annual exemptio11000如果已经为loss,不再扣(X) Taxable gain X/0 Capital LossCurrent gains XCY capital losses先抵扣当年损失(X)1X Capital losses b/fwd再抵扣去年损失(X)2X Less: Individual annual exemptio11000(X) Taxable gain如net loss,可带去次年X Part disposalProceeds of part disposal A Less: selling costs(X) Net proceeds X Less: Original cost of whole asseA/(A+B) = C(C) Chargeable gain X Gift Relief (纯赠送)A: Disposal proceeds MVLess: Cost(X)Capital Gain X'Less: Gift Relief(X')Chargeable Gain (Donor No gain/No loss) 00 B:Base cost of asset = MV – Gift Relief(Rest of the gain is rolled over into the base cost for a subsequent disposal of the asset) Gift Relief for sale under value (半卖半送)A: Disposal proceeds MVLess: Cost (X)Capital Gain X1先算X2,倒退得X1X1Less: Gift Relief for sale at under value (Balancing Figure)(X)Chargeable Gain X2(X2=Actual consideration ‐ cost)X2 B:Base cost of asset = MV – Gift Relief for sale at under value = consideration(Rest of the gain is rolled over into the base cost for a subsequent disposal of the asset)Gift of shares 难点!Free hold property CBA & CALeasehold property CBA & CAStock流动资产,都不是Debtors T/R,流动资产,都不是Investments CAPlant (cost & proceeds <6000Non wasting chattel, exemptCreditors T/P, Liability,都不是Lifetime tax: proformaGift X Less: AE (X) Less: AE b/f (X) Net gift after exemptions X Less: Nil band remaining:Nil band at date of gift X*less: CLTs in last 7 years be(X)(X)X Tax@20% (or 20/80) X * Nil band for 2014/15 is 325,000Death tax: proformaGross CLT/PET X Less: nil band remaining: Nil band on death325000Less: GCTs in 7 years before gift(X)Nil band remaining(X)X Tax @ 40% IHT IHT Less: taper relief% × IHT (X)(X)XLess: lifetime tax (on CLT) (X) Death tax due X Death estate: proformaCHARGEABLE ESTATE XLess: nil band remaining: Nil band on death325000Less: GCTs in 7 years before death(X)Nil band remaining(X)X Tax @ 40% IHT IHT Corporation tax 计算格式Trading Profits(accruals)X Investment Income (accruals)(accruals)X Property Business Income (accruals)(accruals)X Net chargeable gains (receipts)(cash basis)X Less: Qualifying charitable donations (payments)(cash basis)(X) Taxable total profits X PLUS: Franked Investment In非关联企业(<50%)分红X Augmented Profits (for tax rate only)X Trading profit企税Profit before taxation X Add: Non‐deductible expenditure X Less:Income under other schedules(X) Less: Capital allowance – P&M(X) Trading Profit X Investment IncomeInterest income (actual cash amount received gross by companies)Less: Interest payable for underpaid / overdue taxLess: Property loan interest*所有非经营活动产生的利息,都从Invest income下减去Chargeable Gains ₤Proceeds X Less: Incidental cost on disposal (X) Allowable expenditure X Less: cost (X) Less: incidental cost on purchase(X) Less: improvement (X) Unindexed Gain X Less: Indexation allowance (IA)(% increase in RPI to 3 d.p. x Allowable expenditure) (X) Indexed gain X Less: Rollover relief (X) Less: Capital loss – current period (X) – carried forward (X) Chargeable Gain X PAYE tax codeAllowances:Personal allowances XHigher rate relief XExpense deductions X X Less: DeductionsBenefits XUntaxed income XTax under payments b/f gross up (x100/20 or 100/4上一年少交的税X(X) Allowance to set against pay XL ‐ Tax code for born after 5 Apr 1948P ‐ Tax code for born between 6 Apr 1938 ‐ 5 Apr 1948Y ‐ Tax code for born before 6 Apr 1938。

ACCA F6 Taxation (UK) Introduction

ACCA F6 Taxation (UK)Introduction本文由高顿ACCA整理发布,转载请注明出处F6 Taxation是一门关于税法的科目,在教材中,同学们会陆续接触到UK tax system, Income tax and notional insurance contributions, Chargeable gains for individuals, Tax administration for individuals, Inheritance tax, Corporation tax和Value added tax这七部分不同的知识。

针对于2015年6月份的F6考试来说,同学们仍可以按照老一套的考试标准来进行学习和复习,因为考试模式仍然是五道大计算简答题的样式。

第一道题是有关于个人所得税,第二道题是有关于公司所得税,第三道大题是资本利得税,第五道大题是遗产税,第四道大题每年都会出不同的类型,比如2014年6月份出的题目就是个人的资本利得税计算的。

在UK tax system中,学员们会学习到英国的税法体制,包括还会了解到一些有关税法制度的知识。

在Income tax and notional insurance contributions中,学员们会学习到有关个人的样工资、养老金、房产收入的核算,还会再利用一些抵减来减免自己的收入,然后以最后的金额去计算应缴纳的税款。

除了个人税以外,还有一项比较重要的知识就是国民保险也会在这个板块中进行深入的了解。

在Chargeable gains for individuals中,同学们会了解到有关个人税中另一个大板块,就是资本利得税。

这一部分是独立于所得税而存在的,所以同学们要记得在学习过程当中一定要分清它们的界限,这样在最后做综合大题的时候就不会犹豫哪个数据该往哪里放了。

在Tax administration for individuals中,同学们看到更多的是文字的叙述,主要讲解了什么时候交税和晚纳税时产生的一系列的弥补措施等。

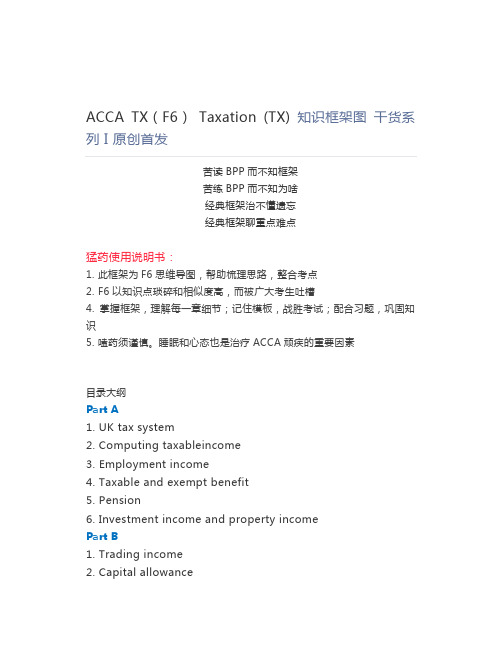

ACCA TX(F6) Taxation (TX) 知识框架图 干货系列 I 原创首发

ACCA TX(F6)Taxation (TX) 知识框架图干货系列 I 原创首发苦读BPP而不知框架苦练BPP而不知为啥经典框架治不懂遗忘经典框架聊重点难点猛药使用说明书:1. 此框架为F6思维导图,帮助梳理思路,整合考点2. F6以知识点琐碎和相似度高,而被广大考生吐槽4. 掌握框架,理解每一章细节;记住模板,战胜考试;配合习题,巩固知识5. 嗑药须谨慎。

睡眠和心态也是治疗ACCA顽疾的重要因素目录大纲Part A1. UK tax system2. Computing taxableincome3. Employment income4. Taxable and exempt benefit5. Pension6. Investment income and property incomePart B1. Trading income2. Capital allowance3. Assessable trading income4. Trading loss5. Partnership6. National insurance contributionPart C1. Chargeable capital gain2. Reliefs3. Share and securities4. Self assessment and payment of tax5. Inheritance taxPart D1. Computing taxable total profitfor company2. Chargeable gains for companies3. Losses4. Groups5. Self assessment and payment of tax by company6. Value add tax。

ACCA考试复习回顾《税务F6》辅导6

ACCA考试复习回顾《税务F6》辅导6本文由高顿ACCA整理发布,转载请注明出处OVERSEAS ASPECTS OF CORPORATION TAXRELATED LINKSThis article is relevant to candidates sitting Paper F6 (UK)in either June or December 2013, and is based on tax legislation as it applies to the tax year 2012–13 (Finance Act 2012)。

Overseas aspects of corporation tax may be examined as part of Question 2, or it could be examined in Questions 4 or 5.Company residence Companies that are incorporated in the UK are resident in the UK. Companies that are incorporated overseas are only treated as being resident in the UK if their central management and control is exercised in the UK. Companies that are resident in the UK (or treated as being resident in the UK)are subject to UK corporation tax on their worldwide profits (including chargeable gains)。

Example 1 Crash-Bash Ltd is incorporated overseas, although its directors are based in the UK and hold their board meetings in the UK.· Companies that are incorporated overseas are only treated as being resident in the UK if their central management and control is exercised in the UK.· Since the directors are UK based and hold their board meetings in the UK, this would indicate that Crash-Bash Ltd is managed and controlled from the UK, and therefore it is resident in the UK.· If the directors were to be based overseas and to hold their board meetings overseas, the company would probably be treated as resident overseas since the central management and control would then be exercised outside the UK.Overseas dividends As far as Paper F6 (UK)is concerned all overseas dividends are exempt from UK corporation tax.Exempt overseas dividends are included as franked investment income when calculating a company’s augmented profits in exactl y the same way as UK dividends, unless they are group income. In this case they are completely ignored for tax purposes.Example 2 During the year ended 31 March 2013 Various Ltd, a UK resident company, received an overseas dividend of ?67,500 (net)。

ACCAF6税法——收入的分类和计算

ACCA F6税法——收入的分类和计算本文由高顿ACCA整理发布,转载请注明出处

为在英国的税法中,对于不同类别的收入有不同的计算方法和税率,所以同学们要格外注意,一定要记住什么样的收入在什么样的类别里面。

在F6中,会学习到的收入大致分为以下一个类别:

①来自于工作收入和退休金或养老金的收入;

②来自于贸易的利润;

③房租的收入;

④来自于投资的收入。

首先,建议学员们要先从这些收入中挑出什么是Savings income和Dividend income这样剩下来的项目就都在Other/Non-saving income中进行相应的计算。

1. Savings income

能进入Savings income这个项目中的就是之前谈到的利息。

这些利息来自于银行,政府债券等,但是学员们一定要注意,这些利息在支付的时候都是支付的金额,而在计算的时候都要进行还原,还原为100%的金额。

但是又不是所有的项目都需要进行还原,例如来自银行和房屋互助协会的利息就需要还原或者来自公司股票的利息也是需要还原的。

同时,也建议学员在平时做练习的时候多做积累,因为这样的知识点没有办法在考试的时候体现在试卷前几页的位置,只能靠多做练习题来巩固记忆。

2. Dividend income

同样的问题也出现在股利收益中。

但不同的是在股利收益中,只有10%的金额需要在计算的过程中进行还原。

而具体返还的操作流程学员们也会在后续的复习篇中看到。

那么剩下的项目就可以划分在Other/Non-saving income中进行相应的计算。

更多ACCA资讯请关注高顿ACCA官网:。

ACCA F6 知识点总结 2015年

Chapter 1 Introduction to the UK tax system1.HMRC:Her Majesty ’s Rvenue and Customs 英国税务海关总署2.factors affect tax policies:①econmic:whole;factors;behavior(donation,investment,saving,build own business,drink,fuel);②social:缩小贫富差距;③environment3.progressive taxation:income tax 随财富增加税率变高Regressive taxation:fuel duty 随财富减少税率变高Proportional taxation:财富增加比率不变,是固定数 Ad Valorem :增值税4.direct and indirect (VAT) taxes .5.treasure(财政局),chancellor of the exchequer,HMRC,Tribunal(first,upper),遵从欧盟规则6.避收两次税:避收两次;避免歧视;避免逃税漏税7.tax evasion(illegal) and tax avoidance(legal:abusive arrangement,tax mitigation)8.出现违反:告知;不改的话不予受理;报告单不能透露信息9.ISA :限额15000,存款投资股票免税(利息不用交个人所得,资产利得不用交税),亏损不能抵减。

Chapter 2 Introduction to Crporation Taxpany residence:place of incorporation 注册地:①UK;②Overseas(central management in UK)2.period of account(会计期,可长于/短于12个月) and chargeable accounting period(应税会计期,不能超过12个月,会计期大于12月时拆分)★3.financial year:FY 2014 01/04/2014-31/03/2015▲4.proforma of corporation tax computationFII:免税投资收入:①dividend(另一UK 公司,海外公司,unconected company(<50% share holding);②FII=dividends received from unconnected companies/90%★5.MR=standard fraction*(upper limit-augmented profit)*TTP/augmented profit6.大于12个月的拆分:①按期间:trading profit,property business income②按具体发生日期:interest income,chargeable gain,qualifying charitable donation,FIICapital allowance:计算每一个期间的capital allowance 后加总7.小于12个月:按比例:upper limit and lower limit 同样按比例减小8. associatied company:>50% share capital,>50% voting rights,>50% profit pr netAsset on winding up(结束).注意:Both UK and overseas,dormant companies excluded,一段时间为associated company 视为整个期间都是associated;Associated company dividend is not include FIIChapter 3 trading profit▲1.proforma for tax adjusted trading profits★2.decutible and non-decuctible(完全,唯一) 两个目的中有一个目的与金融无关,不可扣 ①fine 罚款(停车除外);②depreciation;③capital expenditure(性能有提升,不可扣),revenue expenditure(无提升,可扣)买破房,不翻新无法使用,CE;翻新前也可以使用RE,换烟囱,RE④lease car(租车):≤130g/km 全可扣,>130:15%不可扣⑤entertain and gift:employee deductible;customer(不可扣,除非:一年一人不超过50磅/不是实务研究代金券/gift 有给公司打广告⑥donation:可扣减三要素:trading purpose,local,给教育宗教文化慈善组织不满足三条件时,放在QCD 里面扣掉政治捐款不可扣,也不能放在QCD 里面扣★⑦legal fee:可扣:应收账款的催付,贷款用于经营,商标注册,短租续租,保护域名,起诉违约,会计审计费,版税不可扣:发行股票,被别人起诉,初次短期租约,与capital expenditure 相关的⑧debt:only 赊销未还可扣(即staff 不行),确认坏账又收到了算在other income 里⑨other:培训,商业会费,经营前7年内,裁员补偿,咨询服务3.Capital allowance:a businesstax relief for capital expenditure on qualifying asset.It coverd for expenditure on plant and machinery,and is given to the net cost of asset(original cost-disposal value)4.plant and machinery:land building and structures are not plant.so as walls,floors,ceilings,doors,gates,shutters,windows.①main pool:大多数资产,car with CO2 96g/km-130g/km②special rate pool :long life asset(≥25years,total cost of at least 100000 for 12 month),房间自带体系,cars with CO2>130g/km③short-life asset:预备8年内出售;购买资产的accounting period结束后两年内去税务局做认定(对unincorporate business,会计期结束后的1年内的1月31日之前);计算CA时单列,使用结束后计算balancing charge or balancing allowance;8年后仍在用转化为main pool;AIA5.WDA(writing down value.for still use,reducing balance basis余额递减法)Main pool-18% special pool-8% short life asset-18%(年折旧比率)6.AIA(annual investment allowance,for newly required) exception of motor carsProvide alloance of 100% for the first 500000 of expenditure(针对12个月)抵减顺序:SP→MP→SLA★7.motor car:针对于低排量(≤95g/km)汽车。

ACCAF6知识点总结2015年

Chapter 1 Introduction to the UK tax system1.HMRC:Her Majesty ’s Rvenue and Customs 英国税务海关总署2.factors affect tax policies:①econmic:whole;factors;behavior(donation,investment,saving,build own business,drink,fuel);②social:缩小贫富差距;③environment3.progressive taxation:income tax 随财富增加税率变高Regressive taxation:fuel duty 随财富减少税率变高Proportional taxation:财富增加比率不变,是固定数 Ad Valorem :增值税4.direct and indirect (VAT) taxes .5.treasure(财政局),chancellor of the exchequer,HMRC,Tribunal(first,upper),遵从欧盟规则6.避收两次税:避收两次;避免歧视;避免逃税漏税7.tax evasion(illegal) and tax avoidance(legal:abusive arrangement,tax mitigation)8.出现违反:告知;不改的话不予受理;报告单不能透露信息9.ISA :限额15000,存款投资股票免税(利息不用交个人所得,资产利得不用交税),亏损不能抵减。

Chapter 2 Introduction to Crporation Taxpany residence:place of incorporation 注册地:①UK;②Overseas(central management in UK)2.period of account(会计期,可长于/短于12个月) and chargeable accounting period(应税会计期,不能超过12个月,会计期大于12月时拆分)★3.financial year:FY 2014 01/04/2014-31/03/2015▲4.proforma of corporation tax computationFII:免税投资收入:①dividend(另一UK 公司,海外公司,unconected company(<50% share holding);②FII=dividends received from unconnected companies/90%★5.MR=standard fraction*(upper limit-augmented profit)*TTP/augmented profit6.大于12个月的拆分:①按期间:trading profit,property business income②按具体发生日期:interest income,chargeable gain,qualifying charitable donation,FIICapital allowance:计算每一个期间的capital allowance 后加总7.小于12个月:按比例:upper limit and lower limit 同样按比例减小8. associatied company:>50% share capital,>50% voting rights,>50% profit pr netAsset on winding up(结束).注意:Both UK and overseas,dormant companies excluded,一段时间为associated company 视为整个期间都是associated;Associated company dividend is not include FIIChapter 3 trading profit▲1.proforma for tax adjusted trading profits★2.decutible and non-decuctible(完全,唯一) 两个目的中有一个目的与金融无关,不可扣 ①fine 罚款(停车除外);②depreciation;③capital expenditure(性能有提升,不可扣),revenue expenditure(无提升,可扣)买破房,不翻新无法使用,CE;翻新前也可以使用RE,换烟囱,RE④lease car(租车):≤130g/km 全可扣,>130:15%不可扣⑤entertain and gift:employee deductible;customer(不可扣,除非:一年一人不超过50磅/不是实务研究代金券/gift 有给公司打广告⑥donation:可扣减三要素:trading purpose,local,给教育宗教文化慈善组织不满足三条件时,放在QCD 里面扣掉政治捐款不可扣,也不能放在QCD 里面扣★⑦legal fee:可扣:应收账款的催付,贷款用于经营,商标注册,短租续租,保护域名,起诉违约,会计审计费,版税不可扣:发行股票,被别人起诉,初次短期租约,与capital expenditure 相关的⑧debt:only 赊销未还可扣(即staff 不行),确认坏账又收到了算在other income 里⑨other:培训,商业会费,经营前7年内,裁员补偿,咨询服务3.Capital allowance:a businesstax relief for capital expenditure on qualifying asset.It coverd for expenditure on plant and machinery,and is given to the net cost of asset(original cost-disposal value)4.plant and machinery:land building and structures are not plant.so as walls,floors,ceilings,doors,gates,shutters,windows.①main pool:大多数资产,car with CO2 96g/km-130g/km②special rate pool :long life asset(≥25years,total cost of at least 100000 for 12 month),房间自带体系,cars with CO2>130g/km③short-life asset:预备8年内出售;购买资产的accounting period结束后两年内去税务局做认定(对unincorporate business,会计期结束后的1年内的1月31日之前);计算CA时单列,使用结束后计算balancing charge or balancing allowance;8年后仍在用转化为main pool;AIA5.WDA(writing down value.for still use,reducing balance basis余额递减法)Main pool-18% special pool-8% short life asset-18%(年折旧比率)6.AIA(annual investment allowance,for newly required) exception of motor carsProvide alloance of 100% for the first 500000 of expenditure(针对12个月)抵减顺序:SP→MP→SLA★7.motor car:针对于低排量(≤95g/km)汽车。

ACCA《F6 税务》难点分析:准予扣除项目的分类

ACCA《F6 税务》难点分析:准予扣除项目的分类一. 差旅费用其实,在雇佣收入中能够抵扣的项目少之又少,但是差旅费就是其中的一项。

不过学员们需要注意的是,也不是所有的差旅费用否是可以抵扣的,即只有符合规定的差旅费用是可以抵扣的。

当一位员工被迫发生某项差旅费,且此笔费用是有助于完成业务本身或者公司目的的,那么这笔差旅费就是符合规定的费用,即可以抵扣。

比如,某员工需要从家到非公司地办理公司业务,那么发生的费用就是可以抵扣的差旅费。

然而,经常往来的成本是不在这个范围内的,所谓经常往来的成本就是从员工家到公司之间产生的费用。

在这之中,有两项需要学员们格外注意的就是没有固定工作地的员工和工作于临时工作地的员工。

针对于前者来说,不管去哪里工作,所产生的费用都是符合规定的差旅费,可以进行抵扣。

针对于后者来说,在税法中,存在一个“24个月”的规定,如果在临时工作地的工作时长超过了24个月,那么就会像对待永久工作地的性质一样,差旅费不能进行抵扣,如果工作时长没有超过24个月,那么其中产生的费用可以进行抵扣。

二. 行车津贴当员工家是自己的车办理公事的时候,雇主会付给员工行车津贴,这个津贴是可以在雇佣收入中进行相应的减免的。

学员们在这里需要注意的是,英国税法中规定对于轿车和卡车来说在不高于1万英里的情况下,每英里有45便士的津贴,高于1万英里的情况,每公里有25便士的津贴;对于摩托车来说每英里有24便士的津贴;对于自行车来说,每英里有20便士的津贴可以享受。

不过,可以享受的津贴和雇主给员工的津贴是两回事。

当雇主给员工的津贴大于法律规定的限制的时候,多余出来的津贴就要被视为应纳税福利在雇佣收入中进行纳税,如果雇主给员工的津贴少于法律规定的限制,那么未达部分可以当作准予扣除项目在雇佣收入中进行抵扣。

三. 在工资扣款方案中的慈善捐款这里提到的慈善捐款类似于之前提到的gift aid donation,但是在计算中却有很大的不同。

2015年12月份ACCA F6税法知识点总结

2015年12月份ACCA F6税法知识点总结ACCA12月的考试就要到了,为了方便大家更好地复习,小编在百度文库定期传一些考试资料,如有需要请关注我的百度文库。

类似于中国的税法体系一样,在英国的税法体系中,也会出现有一些免税收入,就这篇文章和学员们一起回顾一下F6的考试中会考到的内容。

一.投资类收入对于投资类的收入,在F6的考试中涉及的比较少,只有在某些税务筹划的题目中才会出现某些特定类别的投资收入是免税收入。

学员们也不要紧张,考试的时候学员们会从考卷中读出这项投资收入是不是免税收入。

如果是免税收入,那么学员也必须在作答的时候,在自己的答案中提到为什么该项目调整为0,或者因为该项目是免税收入么,才做了相应的税务筹划。

二.个人储蓄账户 (Individual savings accounts/ISAs)这个中个人储蓄账户是比较特殊的一个种类,大多数在英国本土留学的学生都会办理这样的账户。

在这个个人储蓄账户中,最高可以存入11,520英镑,其中组成这11,520英镑可以有现金和其他的等价物组成。

并且这个源于这个账户中的资本利得也会和其他的项利息收入或者股票收入一样是免税收入。

三.储蓄存单 (Savings certificates)这章储蓄存单也是英国一个比较独特的存单,是有英国National Savings and Investment (NS&I)发出的。

这张储蓄存单的年限一般是2-5年不等,但是一般是一固定的税率返还利息,这是倍返还的利息就是免税收入。

四.政府有奖债券这一项学员们应该算比较熟悉,因为在中国也会有同样的项目出现,不过税务处理也不太一样。

在中国,例如彩票中奖所得到的收入,在1万元以上是需要交个人所得税,但是在英国此项收入就是免税收入。

五.儿童补助金顾名思义,设置儿童补助金的目的就是为了给孩子一个保证,但是这一部分钱一般都会直接付给孩子的母亲。

但是,学员们要注意,在这里有一个特殊情况有可能出现,那就是当接收儿童补助金的一方如果年调整金收入超过了5万英镑的话,那么这时候接收的儿童补助金就是需要被征收税的,如果低于这个标准,那就是免税收入。

ACCAF6常用计算及格式

ACCAF6常用计算及格式1.个人所得税计算:个人所得税计算的公式为:个人所得税=(收入-免税额)×税率-速算扣除数免税额和税率可以根据题目给出的信息计算得出。

速算扣除额可以根据税率表查得。

2.企业所得税计算:企业所得税计算的公式为:企业所得税=应纳税所得额×税率-速算扣除数应纳税所得额可以根据税前利润减去各种扣除项计算得出。

税率和速算扣除数可以根据税率表查得。

3.增值税计算:增值税计算的公式为:增值税=销售额×税率/(1+税率)销售额是指不含增值税的销售金额,税率可以根据题目给出的信息计算得出。

4.税务报告的格式:税务报告是向税务机关申报纳税信息的文件,需要按照一定的格式填写。

一般包括以下部分:-公司基本信息:包括公司名称、注册地址、税务登记号等。

-申报期间:报告涉及的时间段。

-资产负债表:列出公司的资产和负债情况。

-利润表:列出公司的收入和支出情况。

-现金流量表:列出公司的现金流动情况。

-补充资料:根据需要,可以包括其他相关的资料和解释。

5.税务文件的保存期限:税务文件是跟纳税有关的文件,需要妥善保管并保存一定的时间。

一般来说,税务文件的保存期限为5年,但对于一些特殊情况会有不同的规定,如重大税务案件保存期限为15年。

6.税务罚款计算:税务罚款是对违反税法规定的行为进行处罚的一种方式,罚款的金额可以根据题目给出的信息计算得出,一般为违规金额×罚款率。

这些是ACCAF6考试中常用的计算和格式,考生需要熟练掌握并在实际题目中灵活运用。

在备考过程中,可以多做练习题和模拟考试,提高自己的计算和应用能力。