Bond Graphs II

交易网关Binary接口规格说明书(新债券技术开发稿)

上海证券交易所交易网关Binary接口规格说明书(新债券技术开发稿)2021年62月文档版本目录第一章前言 (6)1.1 目的 (6)1.2 术语和定义 (6)1.3 参考文档 (6)1.4 联系方式 (7)第二章系统简介 (8)2.1系统接入 (8)2.2业务范围 (8)第三章交互机制 (10)3.1会话机制 (10)3.1.1建立会话 (10)3.1.2关闭会话 (10)3.1.3维持会话 (11)3.1.4其他约定 (11)3.2申报与回报 (11)3.2.1业务类型 (12)3.2.2消息流图 (13)3.2.3平台状态 (14)3.2.4重复订单 (15)3.2.5执行报告 (16)3.3 恢复场景 (17)3.4 订阅机制 (18)第四章消息定义 (19)4.1消息结构与约定 (19)4.1.1消息序号 (19)4.1.2消息扩展 (19)4.1.3数据类型 (20)4.2会话消息 (20)4.2.1登录Logon (20)4.2.2注销Logout (21)4.2.3心跳Heartbeat (21)4.3应用消息 (22)4.3.1新订单申报New Order Single (22)4.3.2撤单申报Order Cancel (23)4.3.3执行报告Execution Report (24)4.3.4申报拒绝Order Reject (27)4.3.5平台状态PlatformState (28)4.3.6执行报告信息ExecRptInfo (28)4.3.7分区序号同步ExecRptSync (28)4.3.8分区序号同步响应ExecRptSyncRsp (29)4.3.9分区执行报告结束ExecRptEndOfStream (29)第五章附录 (31)5.1附一计算校验和 (31)5.2附二PBU及说明 (31)5.3附三错误代码说明 (32)5.4附四UserInfo说明 (32)第一章前言1.1 目的本接口规范描述了上海证券交易所(以下称本所)交易网关与市场参与者系统之间进行交易数据交换时所采用的交互机制、消息格式、消息定义和数据内容。

cfa 2级 notes

cfa 2级 notesCFA Level 2 NotesThe CFA (Chartered Financial Analyst) Level 2 exam is a highly prestigious and challenging examination that tests candidates' knowledge and understanding of investment analysis, asset valuation, portfolio management, and ethical and professional standards. To succeed in this exam, candidates need comprehensive and well-organized study materials, such as CFA Level 2 notes.CFA Level 2 notes are instrumental in helping candidates review and understand the vast amount of information covered in the exam curriculum. These notes serve as study guides, condensing and organizing the material in a concise and easily digestible format. In this article, we will explore the importance of CFA Level 2 notes and discuss the key features that make them effective study tools.First and foremost, CFA Level 2 notes provide a comprehensive overview of the exam curriculum, ensuring that candidates cover all the necessary topics. The exam curriculum includes a wide range of subjects, including financial reporting and analysis, equity investments, fixed income, derivatives, alternative investments, portfolio management, and ethics. These notes help candidates navigate through these subjects, highlighting the most important concepts and principles.One of the major advantages of CFA Level 2 notes is their ability to condense vast amounts of information into easily understandable summaries. The exam curriculum is extensive, and candidates often find it challenging to retain and comprehend everything they study. Well-structured notes break down complex topics into simpler, more manageable chunks, facilitating easier understanding and retention of the material.Furthermore, CFA Level 2 notes offer a systematic and organized approach to studying for the exam. They provide a clear outline of the topics and their interrelationships, allowing candidates to establish a structured study plan. With the help of these notes, candidates can prioritize their study efforts, focusing on areas where theyneed more practice and review. This targeted approach enhances efficiency and effectiveness in exam preparation.Another crucial aspect of CFA Level 2 notes is their ability to clarify and reinforce concepts and principles. The exam questions often require a deep understanding of the underlying theories and frameworks. Comprehensive notes help candidates comprehend these concepts by providing explanatory examples, illustrations, and practice questions. By reinforcing the fundamental principles, candidates can better apply their knowledge to real-life investment scenarios, increasing their chances of success in the exam.In addition, CFA Level 2 notes play a vital role in exam revision. As the exam date approaches, candidates need to review and consolidate their knowledge quickly. The well-organized structure of these notes facilitates efficient revision, enabling candidates to swiftly navigate through the topics and identify areas that require additional focus. With concise summaries and key points, these notes serve as a valuable last-minute review tool.Lastly, CFA Level 2 notes are designed to align with the official CFA Institute curriculum and exam format. This ensures that candidates are focusing on the relevant content and are well-prepared for the exam. By using high-quality and up-to-date notes, candidates can confidently approach the exam, knowing that they have covered all the necessary material.In conclusion, CFA Level 2 notes are indispensable study resources for candidates preparing for the exam. These notes provide a comprehensive overview of the exam curriculum, condense complex topics, offer a systematic approach to studying, clarify and reinforce concepts, aid in exam revision, and align with the official CFA Institute curriculum. By incorporating these notes into their study routine, candidates can enhance their understanding, retention, and application of the knowledge needed to excel in the CFA Level 2 exam.。

Bond Graphs I

Start Presentation

M athematic M odeling of Physic S ystems al al

Energy and Power III

• In all physical systems, energy flows can be written as products of two different physical variables, one of which is extensive (i.e., proportional to the amount), whereas the other is intensive (i.e., independent of the amount). • In the case of coupled energy flows, it may be necessary to describe a single energy flow as the sum of products of such adjugate variables.

October 1, 2009

© Prof. Dr. François E. Cellier

Start Presentation

M athematic M odeling of Physic S ystems al al

A-causal Bond Graphs

U0

va

i

+ U0

vb

⇔

Se

U0

i

Energy is being Voltage and current added to the system have opposite directions

Energy Flow

基于松弛预留策略的连续双向拍卖模型

[ sr c]Ai n tea e sraino r suc, ni rvdc niu u o beacinmo ei po oe . h o cp fea e me Abtat migarl dr ev t f i r o re a o e o t o s u l u t d ls rp sd T e ne t lxdt x e o g de mp n d o c or i

Co tn m u h c i n M e O i uo SDo b eAu t o l n uO U l U o t d Ba e n Re a e s r a i n S r t g s d 0 l x d Re e v to t a e y

HU Z i a g S N Qi-u, h uj n h- n , HE uh iHU Z o - g u

接纳率 。在 用户出价 和要价策略 中,买方通过剩余 时间和剩余资源 量出价 ,卖方根据 负载情 况要价 。仿真 实验结果表 明,对于具有费用约

束 的网格任 务,该模型能增加约 2%的资源 总收益 ,提高约 1%的资源利 用率 。 1 5 关健词 :网格 计算 ;提前预留 ;松弛预 留;连 续双 向拍卖 ;资源利用率 ・

预 留机制下 网格资源 定价策 略和用户出价策略并以此进行资 源预 留。

prc j ma i e, x

_

p ie L 其中 ,r — u ni , r jD c, e qa t 表示资源 的数 s 砂

Bond Basics 2

Amortizing A Bond Premium

Adidas will make the following entry every six months to record the cash interest payment and the amortization of the discount.

Date 1/1/2009 6/30/2009 12/31/2009 6/30/2010 12/31/2010

* Rounded.

Issuing Bonds At A Premium

Adidas issues bonds with the following features on January 1, 2009: Par Value = $100,000 Issue Price = 103.546% of par value Stated Interest Rate = 12% Bond will sell at a premium. Market Interest Rate = 10% Interest Dates = 6/30 and 12/31 Bond Date = Jan. 1, 2009 Maturity Date = Dec. 31, 2010 (2 years)

Bond Pricing

The present value(现值 ) the value of future-day assets today. The future value (终值) the value of present-day assets at a future date.

Present Value Of A Discount Bond

96,454

Maturity Value Carrying Value

cfa 二级 课后题 2024

CFA二级课后题2024随着金融市场的不断发展,CFA(Chartered Financial Analyst)资格证书的价值日益凸显,成为越来越多金融从业者和机构的追求。

CFA考试分为三个级别,涵盖了投资组合、财务报表分析、估值等多个领域的知识和技能。

本文将针对2024年CFA二级课后题进行分析和解答,帮助考生更好地备战CFA考试。

一、估值理论1. 企业价值估算在进行企业价值估算时,需要考虑公司的未来盈利能力、成长潜力、市场风险等因素。

主要的估值方法包括比较公司估值法、折现现金流量法和权益残值法。

2. 股票估值股票估值是考察投资者对公司未来盈利的预期,主要的估值方法包括市盈率法、股利折现模型和自由现金流量估值法。

二、固定收益1. 市场利率市场利率对固定收益证券的价格有着重要的影响。

假设市场利率上升,债券价格会下降,反之亦然。

2. 利率风险管理债券组合的利率风险管理至关重要,可以通过套期保值和利率互换等方法来降低利率风险。

三、风险管理1. 风险测度风险测度是评估投资组合风险的重要工具,主要包括标准差、协方差和价值atr-risk等方法。

2. 风险管理策略风险管理策略包括对冲、多元化和风险控制等方法,有助于降低投资组合的波动性和损失。

四、衍生品1. 期货合约期货合约是一种标准化的金融工具,包括商品期货和金融期货,能够用于对冲和投机。

2. 期权合约期权合约分为认购期权和认沽期权,可以通过标的资产的价格涨跌来获利,是一种灵活的金融工具。

五、投资组合管理1. 资产配置资产配置是指在不同资产类别之间进行分配,以达到投资组合的最佳风险收益平衡。

2. 绩效评估投资组合的绩效评估是评估投资经理的能力和投资策略的有效性,主要包括夏普比率、特雷诺比率和信息比率等指标。

六、伦理和专业标准1. CFA准则CFA准则包括道德准则、专业准则和继续教育准则,要求CFA持有人遵守职业道德和专业标准进行工作。

2. 道德决策框架道德决策框架主要包括辨别、分析、决策和行动四个步骤,帮助CFA持有人正确处理道德问题和纠纷。

AMD FirePro W7100 8GB 高端工作站图形卡说明书

AMD FirePro W7100 8GB GraphicsAMD FirePro W7100 8GB Graphics J3G93AA INTRODUCTIONThe AMD FirePro™ W7100 workstation graphics delivers great performance, superb visual quality, and outstandingmulti-display capabilities. It is an excellent high-end solution for professionals who work with advanced visualization,complex models, large data sets, video editing and production.The AMD FirePro W7100 features AMD Eyefinity technology support for up to 4 directly attached independent monitors from a single graphics card. Also, the AMD FirePro W7100 is backed by 8GB of ultra-fast GDDR5 memory. PERFORMANCE AND FEATURES∙AMD Graphics Core Next (GCN) architecture designed to effortlessly balance GPU compute and 3D workloads efficiently∙Blazing compute performance powered by latest AMD GCN architecture yielding up to 3.0 TFLOPS of peak single precision and up to 200 GFLOPS peak double precision∙Optimized and certified for leading workstation ISV applications. The AMD FirePro™ professional graphic s family is certified on more than 100 different applications for reliable performance.∙GeometryBoost technology with dual primitive engines∙Four (4) native display DisplayPort 1.2a (with Adaptive-Sync) outputs with 4K resolution support∙AMD Eyefinity technology (see Note 1) support managing up to 6 displays seamlessly as though they were one display∙New Ultra HD Media Engine with more than 8x decode and 3x encode performance than the prior generation anddedicated Audio DSP’s enabling low power decode of t wo streams H.264 4K resolution at 60Hz content and 4Kencoding∙AMD PowerTune and AMD ZeroCore Power technologies that allow for state of the art dynamic power management of the GPU∙8GB of high speed GDDR5 memory∙PCI Express® 3.0 compliantCOMPATIBILITYThe AMD FirePro W7100 is supported on the following HP Z Workstations:- Z230 CMT, Z440, Z640, Z840SERVICE AQND SUPPORTThe AMD FirePro W7100 has a one-year limited warranty or the remainder of the warranty of the HP product in which it is installed. Technical support is available seven days a week, 24 hours a day by phone, as well as online support forums.Parts and labor are available on-site within the next business day. Telephone support is available for parts diagnosis and installation. Certain restrictions and exclusions apply.TECHNICAL SPECIFICATIONSForm Factor Full height, single slot (9.5” X 4.376”)Graphics Controller AMD FirePro W7100 graphicsGPU: 1792 Stream Processors organized into 28 Compute UnitsPower: <75 WattsCooling: ActiveBus Type PCI Express® x16, Generation 3.0Memory 8GB GDDR5 memoryMemory Bandwidth: up to 176 GB/sMemory Width: 256 bitConnectors 4x Display Port 1.2a connectors with HBR2 and MST support.Factory Configured: No video cable adapter includedAfter market option kit: No video cable adapter includedAdditional DisplayPort-to-VGA or DisplayPort-to-DVI adapters are available as FactoryConfiguration or Option Kit accessories.Maximum Resolution DisplayPort:- 4096x2160 @24bpp 60HzDual Link DVI:- 2560x1600 (requires DP to DL-DVI adapter)Single Link DVI:- 1920x1200 (requires DP to DVI adapter)VGA:- 1920x1200 (requires DP to VGA adapter)Image Quality Features Advanced support for 8-bit, 10-bit, and 16-bit per RGB color component.High bandwidth scaler for high quality up and downscalingDisplay Output Max number of monitors supported using DisplayPort 1.2a:- 4 direct attached monitors- 6 using DP 1.2a with MST and HBR2 enabled monitorsMonitor chaining from a single DisplayPort (subject to a max of 6 total monitors across alloutputs, requires use of DisplayPort enabled monitors supporting MST and HBR2):- one 4096x2160 display- two 2560x1600 displays- four 1920x1200 displaysShading Architecture Shader Model 5.0Supported Graphics APIs OpenGL 4.4OpenCL 1.2 and 2.0DirectX 11.2 / 12AMD MantleAvailable Graphics Drivers Windows 8.1 / 8 (64-bit and 32-bit)Windows® 7 (64-bit and 32-bit)LinuxHP qualified drivers may be preloaded or available from the HP support Web site:/country/us/en/support.htmlNotes 1. AMD Eyefinity technology supports up to six DisplayPort™ monitors on an enabled graphicscard. Supported display quantity, type and resolution vary by model and board design; confirmspecifications with manufacturer before purchase. To enable more than two displays, or multipledisplays from a single output, additional hardware such as DisplayPort-ready monitors orDisplayPort 1.2 MST-enabled hubs may be required. See /eyefinityfaq for fulldetails.2. OpenGL 4.4 support available with driver 14.301.xxx or later.3. OpenCL 2.0 support planned in driver updates for early 2015.4. For HP Z440 Workstation configurations, the HP Z4 Fan and Front Card Guide Kit, which isavailable both CTO (G8T99AV) and AMO (J9P80AA), is required.Summary of ChangesDescription of change: Date of change: VersionHistory:© Copyright 2014 Hewlett-Packard Development Company, L.P.The only warranties for HP products and services are set forth in the express warranty statements accompanying such products and services. Nothing herein should be construed as constituting an additional warranty. HP shall not be liable for technical or editorial errors or omissions contained herein. The information contained herein is subject to change without notice.。

cfa2024年二级原版书课后题

CFA 2024年二级原版书课后题一、公司金融和财务报告分析1.1 企业金融报告的意义企业金融报告是企业向外界公开披露的财务信息,包括企业的资产负债状况、经营成果、现金流量以及股东权益等信息。

通过对企业金融报告的分析,可以帮助投资者了解企业的财务状况,评估企业的经营风险和盈利能力,为投资决策提供重要的参考依据。

1.2 企业金融报告分析的方法企业金融报告分析主要采用财务比率分析、财务趋势分析、现金流量分析、股票市场指标分析等方法。

其中,财务比率分析是最常用的方法之一,通过计算企业的财务比率,包括盈利能力、偿债能力、运营能力、收益能力等指标,来评估企业的财务状况。

1.3 财务报表分析的注意事项在进行财务报表分析时,需要注意一些问题,包括财务信息的准确性和真实性、企业的会计政策和会计估计的合理性、行业和竞争对手的情况、宏观经济环境等因素对企业财务状况的影响。

二、固定收益投资2.1 固定收益投资的特点固定收益投资是指投资者通过购物债券、债务工具等金融资产获得固定的利息收入。

与股票投资相比,固定收益投资具有收益稳定、风险较低的特点,适合风险偏好较低的投资者。

2.2 债券投资的评价指标在进行固定收益投资时,债券的评价指标是十分重要的。

包括债券的到期收益率、债券的久期和凸性、信用评级等指标,可以帮助投资者评估债券的风险和回报。

2.3 固定收益投资组合的管理固定收益投资组合的管理包括资产配置、收益再投资、久期匹配等内容,通过对固定收益投资组合的管理,可以实现风险的分散和收益的最大化。

三、权益投资3.1 权益投资的特点权益投资是指投资者通过购物股票等金融资产获得股息收入和资本收益。

权益投资具有较高的收益潜力,但也伴随着较高的风险。

3.2 股票投资的评价指标在进行权益投资时,股票的评价指标包括市盈率、市净率、股息率、股票的盈利增长率等指标,可以帮助投资者评估股票的估值和风险。

3.3 权益投资组合的管理权益投资组合的管理包括资产配置、股票选择、风险控制等内容,通过对权益投资组合的管理,可以实现风险的分散和收益的最大化。

cfa二级中文notes

cfa二级中文notes 资产估值

固定收益证券

现值模型

久期和凸性

股票

贴现现金流模型

股利贴现模型

残余收益模型

相对估值

权益投资组合管理

投资组合构成

分散化

风险回报权衡

投资组合业绩衡量

回报率

风险度量

资产配置

战略性资产配置

战术性资产配置固定收益投资组合管理免疫组合

久期中性

凸性对冲

主动久期和凸性管理

市场利率预期

利率风险管理替代投资

对冲基金

策略类型

业绩衡量

私募股权

投资阶段

退出途径

行为金融学

认知偏差

锚定效应

框架效应

过度自信

情绪影响

贪婪和恐惧

羊群效应

行为金融学投资策略

价值投资

动量投资

衍生品

期货和期权

合约类型

估值和风险管理掉期

利率掉期

外汇掉期

财务分析

财务报表分析

资产负债表

利润表

现金流量表财务比率分析

流动性比率

偿债能力比率

盈利能力比率公司治理

公司董事会

董事会结构

董事会职责代理问题

委托代理关系

代理成本

公司治理结构

内部控制

外部审计

道德与专业责任

CFA道德准则

诚信

利益冲突

职业行为

专业责任

客户义务

利益冲突管理量化方法

统计描述

均值

标准差

相关性

假设检验

正态分布

t检验

回归分析。

(完整版)博易大师函数、语法指令与指标公式大全

取当前周期结算价

注意:该函数适用于期货行情

TURNOVER

成交金额

取当前周期成交金额

V

成交量

取当前周期成交量。同VOL

VOL

成交量

取当前周期成交量。简写为:V

ZBS

成交总笔数

取当前周期成交总笔数

函数

功能

解释

示例

专业财务

扩展数据

数据引用

ALTFILTER(X1,X2)

交换信号过滤

X1与X2信号交替过滤

委买量二

取得动态行情:委买量二

DYNAINFO(43)

委买量三

取得动态行情:委买量三

DYNAINFO(44)

委买量四

取得动态行情:委买量四

DYNAINFO(45)

委买量五

取得动态行情:委买量五

DYNAINFO(51)

委买价一

取得动态行情:委买价一

DYNAINFO(52)

委买价二

取得动态行情:委买价二

权的标的股票。

函数

功能

解释

示例

主力资金

FLZJ(Side,Attr,Index)

主力资金

取由参数指定的分类主力资金数据细项。Side为买卖方向:0-买,1-卖;Attr为资金分层:0-庄单,1-大单,2-中单,3-小单;Index为数据类型:0-累计成交量,1-累计成交金额,2-累计成交笔数。

FLZJ(0,0,0),表示庄单累计买入量。

DYNAINFO(07)

最新价

取得动态行情:最新价

DYNAINFO(08)

总成交量

取得动态行情:总成交量

DYNAINFO(09)

最新成交量

取得动态行情:最新成交量

上海证券交易所Level-2行情发布系统接口说明书_3_01_

V3.01

发布

第一章 前言..................................................................................................................................... 4 1 目的....................................................................................................................................... 4 2 阅读对象............................................................................................................................... 4 3 参考文档............................................................................................................................... 4 4 术语说明............................................................................................................................... 4 5 文档变动说明...........................................................................................

固定收益证券课后习题答案

) r

(.5)

⎞

⎛

f (1) ⎞

⎜⎜⎝1 +

2 ⎟⎟⎠ = ⎜⎜⎝1+

2

⎟⎟⎠

⎜1+ ⎝

2

⎟ ⎠

⎛ ⎜⎜⎝1 +

Байду номын сангаас

) r

(1.5)

⎞3

2 ⎟⎟⎠

⎛ = ⎜⎜⎝1+

) r

(1)

2

⎞2 ⎟⎟⎠

⎛ ⎜1 ⎝

+

f

(1.5) ⎞

2

⎟ ⎠

to

get

) r

(.5)

=

.25%

;

) r

(1)

=

.3250%

;

) r

(1.5)

.5 [.998752 + .996758] + 99.6758 = 100.17468

2

Chapter 3

3.1 The price of the 3/4s of May 31, 2012 was 99.961 as of May 31, 2010. Calculate its

price using the discount factors in Table 2.3. Is the bond trading cheap or rich to those

of .5%. If over the subsequent six months the term structure remains unchanged, will

the price of the .5% bond increase, decrease, or stay the same? Try to answer the

基于Moldflow摄像头支架热流道注塑成型模拟

基 于 Modlw摄 像 头 支 架 热 流 道 注 塑成 型模 拟 lf o

董 学敏 , 正 浩 ,张 凯 凯 , 韦 华 葛 刘

( 西科 技 大 学 机 电工 程 学 院 , 西 西安 70 2 ) 陕 陕 10 1

摘 要 : 于 Modlw 设 计 并确 定 了摄 像 头 支架模 具 的浇 注 系统和 冷却 系统 , 基 lf o 同时对 支架 的

1 制 件分 析

球 形摄 像 头 内侧 支架 产 品制件 图如 图 1所 示 . 品为 圆心 角 为 6 。 制 0 的环 形制 件 , 高度 小 于 1 8 mE, 体 积 小 , 面 有 4个不 规 则弧 形孔 , 面有 4个 装 配棱 柱 , 侧 有 3个 凸 起. 表 侧 外 塑料 材 料 为 AB , 型后 要 求 外 S成

第 2 9卷

可 以保 证注 塑过 程 的熔体 流 动 的平衡 性.

3 冷 却 +流动 +翘 曲分 析

本 设计 采用 热 流道 系统 , 以必 须要 设计 冷 却 系统 . 型 芯板 和 型 腔板 分 别 设 置 冷却 水 道 , Mod 所 在 用 l—

f w分 析模 具 的冷却 系 统 , l o 4 得到 模具 和制 品的冷却 效 果如 图 6所 示 , 具 温 度 范 围为 2 ~ 3 . 7℃ , 模 5 51 制 品 的最高 温度 为 2 . 0 5 6 7 8  ̄3 . 3℃. 由于 AB S的熔 点是 1 0℃ , 7 因此此 冷却 方案 完全 可 以保证 制 品 的冷 却

N 2 o.

陕西 科 技 大 学 学 报

J 0URNAL OF SHAANXIUNI VERS TY CI NCE & TE I OF S E CHNOLOGY

Level-2产品内容简述

成交总量 股票:股 权证:份 债券:手 成交总金额(元) 委托买入总量 股票:股 权证:份 债券:手 加权平均委买价格(元) 债券加权平均委买价格(元) 委托卖出总量 加权平均委卖价格(元) 债券加权平均委卖价格 ETF 净值估值 ETF 申购笔数 ETF 申购数量 ETF 申购金额 ETF 赎回笔数 ETF 赎回数量 ETF 申购金额 债券到期收益率 权证执行的总数量 权证跌停价格(元) 权证涨停价格(元) 买入撤单笔数 买入撤单数量 买入撤单金额 卖出撤单笔数 卖出撤单数量 卖出撤单金额 买入总笔数 卖出总笔数 买入委托成交最大等待时间 卖出委托成交最大等待时间 买方委托价位数 卖方委托价位数

TradeBuyNo 买方订单号

TradeSellNo 卖方订单号

内外盘标志:

TradeBSFlag

B – 外盘,主动买, S – 内盘,主动卖,

N – 未知

NoBidLevel

10147 PriceLevelOperator

44

Price

39

OrderQty

10067 NumOrders

73

NoOrders

10148 OrderQueueOperator

10149

OrderQueueOperatorEntryI D

38

OrderQty

NoOfferLevel

10147

44 39 10067 73

PriceLevelOperator

Price OrderQty NumOrders NoOrders

10148 OrderQueueOperator

10149

OrderQueueOperatorEntryI D

38

2021~2022 CFA二级笔记30-固收-信用风险模型分析

CFA二级笔记30-固收-信用风险模型分析图片版第一部分:第二部分:文字版1. 错题笔记错题1---结构化模型vs简约模型反思:简约模型基于外部数据和宏观数据分析,B项吻合,C项用到概率分布属于结构化模型错题2---解释信用基差期限结构的特征反思:这道题可以从两个角度解读(1)材料说了,DLL是个高质量的债券,只有A项符合高质量的定义(2)为什么高质量债券的信用基差曲线是斜向上的呢?1)本身利率曲线就是斜向上的2)高质量债券,目前大环境OK,但是所谓没有“常胜将军”,大环境是具有周期性的,现在好不代表未来就好,未来环境变差的话,高质量债券也可能变成低质量,这时要求的信用基差就比较大错题3---对比资产支持证券的信用分析方法反思:关键词-homogeneous(同质性),同质性强的,基础资产池分析哦错题4---了解exposure反思:低级错误!!!看成bond1比bond2了!!!Bond1和bond2 exposure一样的,LGD就看RR了,bond2RR低,那么LGD就大2. 本章框架Reading 1: The Term Structure and Interest Rate Dynamics★★★Rading 2: The Arbitrage-Free Valuation Framework★★Reading 3: Valuation and analysis: Bonds with Embedded Options★★★Reading 4: Credit Analysis Model★★Reading 5: Credit Default Swaps★★3. 信用风险建模A. E xpected loss信用风险定义:Credit risk is the risk associated with losses from the failure of aborrower to make timely and f u lly payments of interest or principal信用风险公式:Expected loss = Probability of default * Loss given defaulti. L oss given defaultExpected loss = Probability of default * Loss given defaultLoss given default (LGD) is the amount of loss if a default occursLoss given default (%) =100% - Recovery rateLoss given default ($) = Expected exposure - Recovery ($)Recovery rate is percentage of the loss recovered from a bond in defaultExpected exposure is the projected amount of money the investor couldL ose if an event of default occurs, before factoring in possible recoveryQuestion:Are the expected exposure equal to the fair value?答案是预期敞口不等于公允价值预期敞口等于未来现金流折现+此时此刻的现金流公允价值等于未来现金流折现ii. P robability of defaultexpected loss = Probability of defaul t * Loss given defaultProbability of default (POD) is the probability that he bond issuer will not meet its contractual obligations on schedule1)Actual probability of defaultThe actual default probability for the corporate bond can observed from historical data2)Risk-neutral probability of default“Risk-neutral” follows the usage of the term in option pricingIn the risk neutral option pricing methodology, the expected value for the payoffs is discounted using the risk-free interest rate违约概率分为实际违约概率(根据历史数据推出)和风险中性概率(计算得出)风险中性概率推导逻辑:假设一年期到期回收100元100/(1+YTM):分子100是有惊无险拿到,分母YTM包含了信用风险100*RR*POD+100*(1-POD):100*RR*POD,违约情况下拿到的钱;100*(1-POD),不违约情况下拿到的钱;分母Rf 代表无风险利率那么分子的POD就是风险中性概率通过公式推导,风险中性违约概率>实违约概率(YTM不仅仅含有信用风险,还有其他风险,如流动性风险等)Th initial POD, which is called the hazard rate in statistics, is used to calcu l ate the remain in PODsHazard rate is the conditional default rate,which mean the default rate under the condition that no default happens beforeProbability of survival (POS) is under the condition that no default happens beforePOD,站在0时刻看某个时间段的违约概率(死掉概率)H azard rate,站在当前时刻某个时间段的违约概率POS,站在0时刻看个时间段的不违约概率(活下来概率)几个问题:Hazard rate = 10%(风险率)At the end of Year1/Year2,Year3What is the POD?What is the POS?What is the general formula?What is the formula for POD?What is the formula for POS?POD i+ POS i= 1?(不等于1)答案如下:B. CVAFair value of corporate bond = VND -CVAVND: the value for the corporate bond assuming no de faultCredit valuation adjustment (CVA) is the value of the cr edit risk in present value termCVA is the sum of PV of expe cted loss整个公式串起来:4. 有风险债券估值A. 例题1(0息债券,水平利率)【重点例题】Considering a 5-year, zero-coupon corporate bond with following:A flat government b ond yield curve at 3.00%The initial POD is 1.25%, which is c alled the hazard rateDefault occurs only at year end (on dat es 1, 2, 3, 4, 5) and that default will not occur on date 0The par value is $100The recovery rate is 40%To determine:(1)Fair value given the credit risk求CVA=3.115VND = 100/1.035 = 86.2609Fair value= VND -CVA= 86. 2609- 3.1539 = 83.106(2)The rate of return(3)The spread over a maturity-matching government bondGiven a price of 83.1060, we can calculate its yield to maturi ty: 100/(1+YTM)5=83.1060 > YTM= 3.77%The yield on the 5-year, zero-coupon government bond is 3.00% So the credit spread is77 basis points: 3.77%- 3.00% = 0.77%B. 例题2(付息债券,水平利率)【次重点例题】A fixed-income trader observes a 3-year, 5% annual payment corporate bond trading at $104 p er $10O of par valueThe trader determines that the conditio nal POD for each date for the bond is 1.50% given a recover y rate of 40%The government bond yield curve is flat at 2.50%(1)Based on these assumptions, does the trader deem the cor porate bond to be overvalued or undervalued?CVA=2.72If this 3-year, 5% bond were default free, its price (VND) would be$1 07.14015/(1+2.5%)+5/(1+2.5%)^2+105/(1+2.5%)^3= 107.1 401Fair value = VND - CVA= 107.1401 -2.7222= $104.4178 Therefore, this corporate bond is under valued by $0.4178if it is trading at a price of $104(2)By how much?一共有4个收益率:第一年就违约的收益率;第二年就违约的收益率;第三年就违约的收益率;3年都没有违约的收益率(3) If the trader buys the bond at $104, what are the proj ected annual rates of return?C. 例题3(付息债券,利率二叉树)【非重点】The following table displays the data for the spot rate curve The 1-year government bond has a negative yield to reflect theco nditions seen in some financial marketsWe assumes 10% vo latility in benchmark interest ratesConsider a 5-year, 3.50% annual payment, $100 par value corporate bon dThe hazard rate is 1.25% and a recovery rate of 40%第一步,构建利率二叉树:第二步,算VND:Step 2: Determine VND 1)The binomial interest rate tree for benchmark rates can be used tocalculate the VND for the bond The VND is $103.54502) This co uld also have been obtained directly using the benchmark discount factorsV (3.50x 1.002506) + (3.50 x 0.985093) + (3. 50x 0.955848) +(3.50 x 0.913225) + (103.50 x 0.870016)= $1 03.5450第三步和第四步,算CVA和最终价值:重要结论:利率波动率从10%增加到20%带来的影响10% volatility fair value of the bond = 103. 5450-3.5394=100.005620% volatility: fair value of the bond =103 5450-3.5390=100.0060The fair value of the bond will increase with a higher interest ratevolatility The reason for the small volatility impact on the fa ir value is theasymmetry in the forward rates produced by the log norm ality assumption in the interest rate model利率波动性增加,使风险债券的价值增加,CVA减少(原因:利率二叉树不对称性——上涨利率比下跌利率幅度大——那么导致价格下跌幅度比上升幅度大——敞口变小——CVA减少)D. 例题4(付息债券,利率二叉树,浮动利息)【非重点】The spot rate curve is the same with Example 3So we constr uct the 1-Year binomial interest rate tree for 10% volatilityConsider a 5-year floater" that pays annually the 1-year benchmark rate plus 0.50%Assume that for the first th ree years the annual default probability(the hazard rate) is 0 .50% and the recovery rate 20%The credit risk of the issuer then worsens: For the final two yearsthe probability of default goes up to 0.75% and the recover y rate goes down to 10%第一步,计算VND:第二步,计算CVA:注意下,第4年和第5年POD和RR不一样难点,求exposure:。

一些国外键合图的-bond-graph

R : Bmot

C :1/ ksh

u

Moteur

1

DC

Arbre

2

Pignon +

F

Piston

P

Cylindre +

-Penv

i

1

2

crémaill

V

Q

Orifice

Q0

13

Moteur DC arbre

Orifice

Pignon

Cylindre Piston

Crémaillère

u i

Représentation graphique des transferts de puissance Langage unifié pour tous les domaines physiques (analogie) Modèle BG d’un système :

entre le schéma physique et les modèles mathématiques visualisation de la causalité Hypothèse : paramètres localisés

de puissance)

m

f1 = f2 =...= fn ai ei = 0

e1 = m . e2 f2 = m . f1

même vitesse, débit vol, courant, …

levier, poulies embrayages, transfo elect. transducteur

volume nombre de moles

entropie

6

Introduction Principes et langage Applications Conclusion

上证level2数据发布业务技术文档

上证level2数据发布业务技术文档1. 引言本文档旨在介绍上证level2数据发布业务的技术实现细节。

上证level2数据是指上海证券交易所(Shanghai Stock Exchange,SSE)提供的股票市场深度行情数据,包括委托队列、逐笔成交等信息。

本文档将详细介绍上证level2数据的获取、处理和发布过程,以及相关技术要点和注意事项。

2. 数据获取上证level2数据的获取主要依赖于SSE提供的数据接口。

开发者可以通过以下步骤获取level2数据:1.注册并申请SSE的开发者账号;2.获取开发者API密钥;3.使用API密钥通过SSE提供的接口订阅level2数据。

SSE提供的level2数据接口支持多种协议,如TCP、UDP和HTTP等。

开发者可以根据自身需求选择合适的协议进行数据订阅。

3. 数据处理获取到的level2数据需要进行一系列的处理,以便提取有用的信息并进行进一步的分析。

以下是数据处理的主要步骤:1.数据解析:根据数据接口的协议,对接收到的数据进行解析,提取出各个字段的值。

解析过程需要注意数据的编码格式和字节顺序等问题。

2.数据校验:对解析后的数据进行校验,确保数据的完整性和准确性。

常见的校验方法包括校验和、CRC校验等。

3.数据存储:将解析后的数据存储到数据库或者其他数据存储系统中,以便后续的查询和分析。

数据存储可以采用关系型数据库、NoSQL数据库或者其他存储方式。

4.数据分析:对存储的level2数据进行分析,提取出各种市场指标和统计信息。

常见的分析方法包括计算股票的涨跌幅、计算成交量和成交额等。

4. 数据发布上证level2数据的发布主要涉及两个方面:实时数据推送和历史数据查询。

4.1 实时数据推送实时数据推送是指将最新的level2数据实时推送给订阅者。

为了实现实时推送,可以使用以下技术手段:1.推送协议:选择合适的推送协议,如WebSocket、MQTT等。

这些协议具有低延迟、高效率的特点,适合实时数据推送场景。

bond中的optional参数

bond中的optional参数Bond中的optional参数在编程中,optional参数是一种可选的参数,它允许函数或方法在调用时不需要提供该参数的值。

在Bond中,optional参数也扮演着重要的角色,它能够提高代码的灵活性和可扩展性。

本文将介绍Bond中的optional参数的使用方法和优势。

一、optional参数的定义和使用在Bond中,optional参数是通过在参数类型后面加上一个问号(?)来定义的。

例如,我们可以定义一个接受optional参数的函数:```bonddef foo(x: int32?, y: string?): bool;```在调用这个函数时,我们可以选择性地提供x和y的值,也可以不提供。

例如:```bondbool result = foo(10, "hello"); // 提供了x和y的值bool result = foo(10); // 只提供了x的值bool result = foo(); // 不提供任何值```通过使用optional参数,我们可以根据实际需要来选择性地传递参数值,而不需要为每个参数都提供一个默认值。

二、optional参数的优势1. 简化函数调用:通过使用optional参数,我们可以避免在调用函数时传递不必要的参数,从而简化函数调用的过程。

这对于具有大量参数的函数来说尤为有用。

2. 提高代码的灵活性:optional参数使得函数的参数可以根据实际情况进行扩展或缩减,而不需要修改函数的定义或调用。

这样,我们可以随时添加新的参数,而不会对现有的代码造成影响。

3. 降低函数的复杂性:通过使用optional参数,我们可以将一些参数的处理逻辑放在函数内部,而不需要在调用函数时处理。

这样,函数的接口和使用方式会变得更加简单和清晰。

4. 提高代码的可读性:optional参数可以使函数的调用更加直观和易于理解。

通过在函数定义中明确指定哪些参数是可选的,我们可以清楚地知道在调用函数时需要提供哪些参数,而不需要查看函数的实现细节。

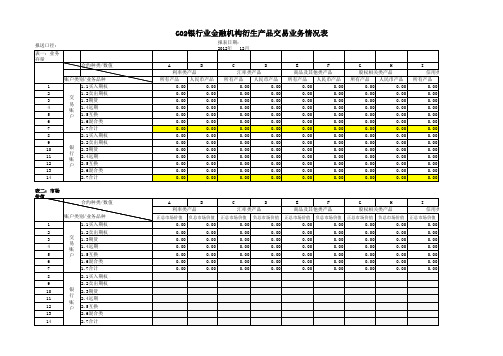

G02银行业金融机构衍生产品交易业务情况表

G H 股权相关类产品 所有产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 人民币产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

填表人:吴枫华 版本号:1210 无数据部分 数据库预留空间(暂不填报) 填报机构:81r00000000

货币单位:万元

J 信用类产品 人民币产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

K L 贵金属类产品 所有产品 人民币产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

所有产品 人民币产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

M 复合类产品 所有产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

N

O 合计

P

人民币产品 所有产品 人民币产品 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

velocity v = flow

October 8, 2009

© Prof. Dr. François E. Cellier

Start Presentation

M athematic M odeling of Physic S ystems al al

Passive Mechanical Elements in Bond Graph Notation

M athematic M odeling of Physic S ystems al al

Bond Graphs II

• In this class, we shall deal with the effects of algebraic loops and structural singularities on the bond graphs of physical systems. • We shall also analyze the description of mechanical systems by means of bond graphs.

October 8, 2009

© Prof. Dr. François E. Cellier

Start Presentation

M athematic M odeling of Physic S ystems al al

An Example I

The cutting forces are represented by springs and friction elements that are placed between bodies at a 0-junction.

v1

v1 FB2 v21 FB2

v2 FB2

Fk2 v2 v2 FBcv2 FI2

The sign rule follows here automatically, and the modeler rarely makes any mistake relating to it.

October 8, 2009

October 8, 2009

© Prof. Dr. François E. Cellier

Start Presentation

L1.e R2.f

M athematic M odeling of Physic S ystems al al

Bond Graphs of Mechanical Systems I

The D’Alembert principle is formulated in the bond graph representation as a grouping of all forces that attack a body around a junction of type 1.

October 8, 2009

October 8, 2009

© Prof. Dr. François E. Cellier

Start Presentation

M athematic M odeling of Physic S ystems al al

Table of Contents

• • • • • Algebraic loops Structural singularities Bond graphs of mechanical systems Selection of state variables Example

x

m

fI fB v1 v2 fB

fI = m · dv /dt

fI

v

I :m

B

fB = B · ∆ v

fB

∆v

R:B

fk x1

k

x2 fk

∆ x = fk / k ⇒ ∆v = (1 / k) · dfk /dt

© Prof. Dr. François E. Cellier

fk

∆v

C : 1/k

October 8, 2009

• The two adjugate variables of the mechanical translational system are the force f as well as the velocity v. • You certainly remember the classical question posed to students in grammar school: If one eagle flies at an altitude of 100 m above ground, how high do two eagles fly? Evidently, position and velocity are intensive variables and therefore should be treated as potentials. • However, if one eagle can carry one sheep, two eagles can carry two sheep. Consequently, the force is an extensive variable and therefore should be treated as a flow variable.

© Prof. Dr. François E. Cellier

Start Presentation

M athematic M odeling of Physic S ystems al al

An Example II

FI3 v3 v31 FBb v1 FBb v3 FBb F v3 v2 FBa FBa v3 FBa v32

Structural Singularities

Causality conflict

⇒ Structural

Singularity

U0.e C1.f

R1.e R1.f

U0.e R1.f U0.e U0.f

L1.e R1.f L1.e L1.f

U0 .e = f(t) U0 .f = C1 .f + R1 .f

•

October 8, 2009

© Prof. Dr. François E. Cellier

Start Presentation

Start Presentation

M athematic M odeling of Physic S ystems al al

Selection of State Variables

• The “classical” representation of mechanical systems makes use of the absolute motions of the masses (position and velocity) as its state variables. • The multi-body system representation in Dymola makes use of the relative motions of the joints (position and velocity) as its state variables. • The bond graph representation selects the absolute velocities of masses as one type of state variable, and the spring forces as the other.

October 8, 2009

U0.e R1.f U0.e U0.f Choice

R2.e R1.f R2.e R3.f

Start Presentation

© Prof. Dr. François E. Cellier

R2.e R2.f

M athematic M odeling of Physic S ystems al al

October 8, 2009

© Prof. Dr. François E. Cellier

Start Presentation

M athematic M odeling of Physic S ystems al al

Bond Graphs of Mechanical Systems II

• Sadly, the bond graph community chose the reverse definition. “Velocity” gives the impression of a movement and therefore of a flow. • We shall show that it is always possible mathematically to make either of the two assumptions (duality principle). force f = potential • Therefore:

October 8, 2009

© Prof. Dr. François E. Ceon

M athematic M odeling of Physic S ystems al al

Algebraic Loops

U0.e L1.f

R1.e R1.f

U0 .e = f(t) U0 .f = L1 .f + R1 .f dL1 .f /dt = U0 .e / L1 R3 .f = R1 .f – R2 .f R2 .e = R3 · R3 .f R2 .f = R2 .e / R2 R1 .f = R1 .e / R1 R1 .e = U0 .e – R2 .e

Fk1

v1 FI1v1 FBd

© Prof. Dr. François E. Cellier