会计学:企业决策的基础exercises-chapter4答案

基础会计学——第四章课后练习参考答案

第四章课后习题复习思考题1.会计科目就是对会计要素的具体内容进行科学分类的项目为了准确的记录每一项经济业务发生后引起的会计要素中个别数量发生的数量变动必须对会计要素包括的具体内容进行科学分类并赋予每个类别一个特定的名称这个名称就是会计科目所以会计科目就是对会计要素的具体内容进行科学分类的项目2.第一必须结合会计要素的特点全面反映会计要素的内容第二既要符合企业内部经济管理的要求又要符合对外报告满足宏观经济管理的要求第三会计科目的设臵既要保持统一性又要考虑灵活性第四会计科目的设臵既要适应社会发展的需要又要保障持相应的稳定性第五会计科目的设臵应保持会计科目总体上的完整性和会计科目之间的互斥性3.可将其分为资产类会计科目所有者权益类会计科目负债类会计科目共同类会计科目损益类会计科目成本类会计科目4.账户是对会计要素的具体内容进行科学分类反应和监督并具有一定格式的工具它是用来分类连续系统的记录和反映各种会计要素增减变化情况及其结果的一种手段如果把企业发生的经济业务连续系统全面的反映和监督下来提供各种会计信息就需要一个记录的载体这个载体就是按照会计科目所规范的内容而设臵的会计账户5.会计账户与会计科目二者既有区别又有联系二者都是对会计要素具体内容的分类会计科目是账户的名称两者分类的口径和反映的经济内容一致区别表现在会计科目只有名称仅说明反映的经济内容是什么而账户既有名称又有结构具有一定的格式既能说明账户反映的经济内容是什么又系统的监督和反映经济业务的增减变化会计科目主要是为了开设账户和填制会计凭证之用而账户则是系统的提供某一个具体会计要素的会计资料是为了编制会计报表和经济管理之用6.账户的经济内容是指会计核算和核算的具体内容按经济内容可以分为资产类账户所有者权益类账户负债类账户成本费用类账户收入类账户利润类账户7.账户的用途是指通过在账户中的记录能够提供哪些会计核算指标也是设臵和运用账户的目的账户的结构是指在账户中怎样记录经济业务如何取得所需的会计核算资料也就是账户的借方登记什么贷方登记什么期末账户有没有余额在一般情况下余额在哪一方描述什么样的经济内容意义为了正确的运用账户来记录经济业务掌握账户在提供核算指标方面的规律性有必要在账户按会计要素分类的基础上进一步对账户按用途和结构分类8.账户按用途和结构可以分为盘存类账户财务成果类账户计价对比类账户成本呢计算类账户调整类账户跨期摊提类账户资本类账户结算类账户练习题一填空题1.会计科目格式会计科目企业实际2.账户性质3.会计要素4.财政部资产类负债类共同类所有者权益类成本类损益类5.会计科目增加减少增加额减少额6.财务成果形成财务成果计算7.债权结算债务结算债权债务结算8.是截至到本月至的利润或亏损“本年利润”“利润分配”9.抵减附加抵减附加10.借二单项选择题1.D2.D3.B4.A (5700+800-5600=900)5.B6.B7.A8.A9.A10.B11.C12.D13.A14.D三多项选择题1.A B C D2.A C3.A C E4.A B C D E5.A B C D E6.A D E7.A B C8.A B C9.B C10.A B D11.A C12.A C13.A B C四判断改错题1.错2.错3.对4.错(会计科目没有格式)5.错6.错7.对8.错(可以编多借多贷的会计分录尽量不编多借多贷会计分录)9.对10.对11.错12.错13.对14.对15.错(年终结转后。

会计学 企业决策的基础 财务会计分册 版 章答案

Chapter 6Merchandising Activitie s Ex. 6.41PROBLEM 6.1AClaypool earned a gross profit rate of 32%, which is significantly higher than the industry average. Claypool’s sales were above the industry average, and it earned $77,968 more gross profit than the “average” store of its size. This higher gross profit was earned even though its cost of goods sold was $18,000 to $20,000 higher than the industry average because of the additional transportation charges.To have a higher-than-average cost of goods sold and still earn a much larger-than-average amount of gross profit, Claypool must be able to charge substantially higher sales prices than most hardware stores. Presumably, the company could not charge such prices in a highly competitive environment. Thus, the remote location appears to insulate it from competition and allow it to operate more profitably than hardware stores with nearby competitors.PROBLEM 6.5Ac. Yes. Sole Mates should take advantage of 1/10, n/30 purchase discounts, even if itmust borrow money for a short period of time at an annual rate of 11%. Bytaking advantage of the discount, the company saves 1% by making payment 20 days early. At an interest rate of 11% per year, the bank charges only 0.6%interest over a 20-day period (11% X 20/365 = 0.6%). Thus, the cost of passing up the discount is greater than the cost of short-term borrowing.Chapter 7 Financial assetsChapter 8 Inventories and the cost of goods soldSupplementary ProblemChapter 91617。

会计学 企业决策的基础 课后习题答案 chapter

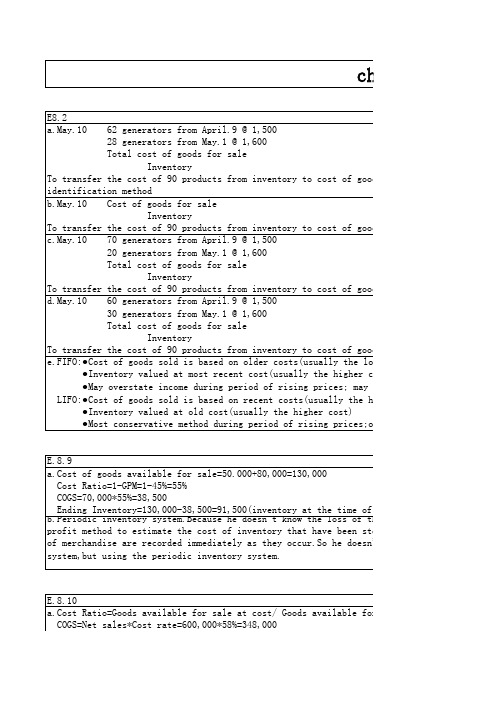

20 generators from May.1 @ 1,600 Total cost of goods for sale

chapter8

st of goods sold account by the specific

st of goods sold account by the average-cost

st of goods sold account by the FIFO method

500 generators from January 9 @ 32

Total cost of goods for sale

Inventory

To transfer the cost of 1000 products from inventory to cost of goods sold account by the

Inventory To transfer the cost of 90 products from inventory to cost of goods sold account by the LI e.FIFO:●Cost of goods sold is based on older costs(usually the lower costs)

Inventory To transfer the cost of 90 products from inventory to cost of goods sold account by the FI d.May.10 60 generators from April.9 @ 1,500

会计学原理基础会计第4章完整习题答案ppt课件精选ppt

09.06.2020

.

2.会计分录的概念:

在登记账簿前,根据记账规则,通过对经济 业务的分析而确定的应计入账户的名称、方 向及其金额的一个简明的记账公式

包括三项要素: 一是账户名称;二是账户 方向(应借或应贷);三是记账金额。

09.06.2020

.

会计分录的编制步骤:

1、分析经济业务的双重影响,并确定所具体影响的账户名称。

例如,以银行存款 50000元偿还银行短期借款。

银行存款

期初余额 200000

50000

短期借款

期初余额 80000

50000

09.06.2020

.

共同规律:有借同时有贷,借贷相等。

总结: 以上四种类型的经济业务,发生以后,总能表现为:对 一个账户的借方影响和对另一个账户的贷方影响(双重 影响),而且影响的金额相等。

第四章 复式记账法

09.06.2020

借

贷

.

第四章 复式记账法

[内容提示]

第一节 复式记账原理 第二节 借贷记账法 第三节 总分类账户和明细分类

账户的平行登记

09.06.2020

.

第一节 复式记账原理

一、记账方法的概念

所谓记账方法,就是根据一定的原理、记账符号、记 账规则,采用一定的计量单位,利用文字和数字在账 簿中登记经济业务的方法。

09.06.2020

.

(3)试算平衡表的作用:

1)通过检查借方余额合计和贷方余 额总计是否相等来检验记账是否正 确;

2)为正式编制财务报表提供一个帐 户余额,方便检索;

3)粗略显示财务状况和经营成果。

09.06.2020

.

(4)试算平衡表的缺点

会计学-企业决策的基础 答案教学资料

会计学-企业决策的基础答案管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based on machine-hours:Manufacturing Overhead= $420,000= $35 per machine-hourMachine-Hours 12,000Department Two overhead application rate based on direct labor hours:Manufacturing Overhead= $337,500= $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct laborhours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probablyexplains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costingsystem include: (1) a better identification of its operating inefficiencies, (2) a betterunderstanding of its overhead cost structure, (3) a better understanding of theresource requirements of each product line, (4) the potential to increase the sellingprice of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability todecrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1a. job costing (each project of a construction company is unique)B. Ex.18.1b. both job and process costing (institutional clients may represent uniquejobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d. process costing (the dog houses are uniformly manufactured in highvolumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Ab4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target Operating IncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学-企业决策的基础答案

管理会计作业(chapter16-20 ) Chapter 16 P757b. HILLSDALE MANUFACTURING CORP.Schedule of the Cost of Fini shed Goods Man ufacturedChapter 16 P761Costs of fini shed goods man ufactured:Total inven tor y$ 149,00Chapter 17 P802a.Department One overhead application rate based onmachi ne-hours:Departme nt Two overhead applicati on rate based on direct labor hours:Manu facturi ng Overhead = $337,500= $ per direct labor hourDirect Labor Hours15,000Manu facturi ngOverheadMachi ne-Hours =$420,000 12,000= $35 per machi ne-hourChapter 17 P805d. The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company s current practice of using direct labor hours to allocate overhead results in the assig nment of a disproporti on ate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed perce ntage above the manu facturi ng costs assig ned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line iscurre ntly priced at an artificially low price in the marketplace. This probably expla ins why sales of Basic Chunks remai n strong while sales of Custom Cuts are on the decline.e. The ben efits the compa ny would achieve by impleme nting an activity-based costi ngsystem include: (1) a better identification of its operating inefficiencies, (2)a better understanding of its overhead cost structure, (3) a better understanding of the resourcerequireme nts of each product line, (4) the pote ntial to in crease the selling price of BasicChunks to makeit more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price of Custom Cuts without having tosacrifice product quality.Chapter 18 P835a job costi ng (each project of a con struct ion compa ny is unique)B. Ex.b both job and process costi ng (in stituti onal clie nts may represe nt unique jobs)c job cost ing (each set of equipme nt is uniq uely desig ned and manu factured)d process costing (the dog houses are uniformly manufactured in high volumes)e process costi ng (the vitam ins and suppleme nts are uni formly manu factured inhigh volumes)Chapter 18 P841b4,000 EU @ $ = $54,000Chapter 18 P845a. (1) $49 [($192,000 + $48,000 + $54,000) - 6,000 un its](2) $109 [($480,000 + $108,000 + $66,000) - 6,000 un its](3) $158 ($49 + $109)(4) $32 ($192,000 - 6,000 un its)(5) $18 ($108,000 - 6,000 un its)b. In evaluating the overall efficiency of the Engine Department, managementwould look at the mon thly per- unit cost in curred by that departme nt, which is the cost of assembli ng and in stalli ng an engine ($109 in part a).Chapter 20 P918d. No. With a unit sales price of $94, the break-even sales volume in units is 54,000un its:Un it co ntributio n margin = $94 - $84 variable costs = $10$540,000 Break-eve n sales volume (in un its) =—' ) $10= 54,000 un its Uni ess Thermal Tent has the ability to manufacture 54,000 un its (or lower fixedand/or variable costs), setting the unit sales price at $94 will not enableThermal Tent to break eve n.Chapter 20 P918Chapter 20 P920Sales volume required to maintain curre nt operati ng in come:$390,000 + $350,000=$20,000 un its。

会计学企业决策的基础 课后习题 答案 chapter

Total paid-in capital=15,000,000+20,000,000+44,000,000=79,000,000 e.Book value per share of common stock=(total stockholders' equity-preferred stock)/shares stock=(143,450.000-15,000,000)/4,000,000≈32.11

会计第四章课后习题及答案

会计第四章课后习题及答案会计第四章课后习题及答案在学习会计的过程中,课后习题是非常重要的一部分,可以帮助我们巩固所学的知识,提高解决问题的能力。

本文将为大家提供会计第四章的课后习题及答案,希望能对大家的学习有所帮助。

一、选择题1. 会计的基本任务是什么?A. 记账B. 做账C. 核算D. 预测答案:C. 核算2. 会计的基本原则包括以下哪些?A. 实体性原则B. 会计平衡原则C. 成本原则D. 所有选项都对答案:D. 所有选项都对3. 会计的记账方法有哪几种?A. 单式记账法B. 复式记账法C. 摊销记账法D. 所有选项都对答案:D. 所有选项都对4. 会计的账簿有哪几种?A. 总账B. 明细账C. 日记账D. 所有选项都对答案:D. 所有选项都对5. 会计的账户分为哪几类?A. 资产类账户B. 负债类账户C. 所有者权益类账户D. 所有选项都对答案:D. 所有选项都对二、填空题1. 会计的基本任务是对企业的经济活动进行_________和_________。

答案:核算、监督2. 会计的基本原则是_________原则、_________原则和_________原则。

答案:实体性、会计平衡、成本3. 会计的记账方法包括_________记账法、_________记账法和_________记账法。

答案:单式、复式、摊销4. 会计的账簿包括_________、_________和_________。

答案:总账、明细账、日记账5. 会计的账户分为_________类账户、_________类账户和_________类账户。

答案:资产、负债、所有者权益三、简答题1. 请简述会计的基本任务是什么?答案:会计的基本任务是对企业的经济活动进行核算和监督。

核算是指对企业的经济业务进行分类、计量、记录和汇总,以便形成财务报表。

监督是指对企业的经济活动进行监督和检查,确保企业的财务活动合法、规范和真实。

2. 请简述会计的基本原则有哪些?答案:会计的基本原则包括实体性原则、会计平衡原则和成本原则。

4第四章基础会计学课后练习题参考答案

第四章练习参考答案一、填空题1.现金收付制(现金收付基础)、权责发生制(应计基础)、应计基础2.资产类,实际采购成本3.采购成本,生产成本,销售成本4.根据市场经济需要组织产品生产,满足社会生产与消费的需要,同时根据生产经营活动获取利润,为国家提供财政收入并满足企业自身发展的需要。

5.本期发生的、不能直接或间接归入某种产品成本的各项费用,管理费用,财务费用和销售费用6.营业利润,投资收益,营业外收支净额,所得税费用7.买价,其他采购费用8.已销产品的实际生产成本,产品销售成本=产品销售数量×产品单位生产成本9.产品生产过程中发生的与产品生产有关的一切生产费用的总和,直接材料、直接人工、制造费用二、单项选择1.B2.B3.C4.C5.B6.D7.C8.A三、多项选择1.ABCD2.ABC3.ABC4.ABCD5.AC6.CD7.ACD四、判断改错1.F应贷记“长期借款”账户。

2.F不应计入,不构成3.F删除“制造费用”4.F营业利润=主营业物利润+其他业务利润—营业税金及附加—销售费用—财务费用—管理费用—资产减值损失±公允价值变动损益±投资收益5.T6.T7.T8.F除主营业物以外的其他经营活动实现的收入。

9.T10.T五、业务核算题习题一1借:其他应收款—张三400贷:银行存款4002借:材料采购—甲材料4500—乙材料2000应交税费—应交增值税1105贷;银行存款76053借:材料采购—甲材料300—乙材料200贷:银行存款5004借:材料采购—丙材料5000应交税费—应交增值税850贷:应付账款58505借:材料采购—丙材料500贷:银行存款5006借:应付账款—南湖工厂5850贷:银行存款58507借:材料采购—丁材料5200应交税费—应交增值税850贷:应付票据—中南工厂5850库存现金2008借:管理费用—差旅费365库存现金35贷:其他应收款——张三4009借:原材料—甲材料4800—乙材料2200—丙材料5500—丁材料5200贷:材料采购—甲材料4800—乙材料2200—丙材料5500—丁材料5200习题二1借:生产成本—A产品7125—B产品8225制造费用500贷:原材料—甲材料8200—乙材料76502借:管理费用600贷:银行存款6003借:生产成本—A产品25000—B产品25000制造费用2000管理费用8000贷:应付职工薪酬600004借:生产成本—A产品3500—B产品3500制造费用280管理费用1120贷:应付职工薪酬—职工福利费8400 5借:库存现金60000贷:银行存款600006借:应付职工薪酬60000贷:库存现金600007借:管理费用1000贷:银行存款10008借:管理费用800贷:银行存款8009借:制造费用300贷:银行存款30010借:管理费用1000制造费用2500贷:银行存款350011借:银行存款100000贷:短期借款10000012借:管理费用1000制造费用3500贷:累计折旧450013借:财务费用1000贷:应付利息100014借:生产成本—A产品4540—B产品4540贷:制造费用908015借:库存商品—A产品40165—B产品41265贷;生产成本—A产品40165—B产品41265习题三1借:银行存款93600贷:主营业务收入80000应交税费—应交增值税136002借:应收账款56160贷:主营业务收入48000应交税费—应交增值税81603借:销售费用—广告费1000贷:银行存款10004借:财务费用—汇兑手续费900贷:银行存款9005借:主营业务成本—A产品40000—B产品35000贷:库存商品—A产品40000—B产品350006借:银行存款56160贷:应收账款561607借:销售费用5000贷:银行存款50008借:银行存款7020贷:其他业务收入6000应交税费—应交增值税10209借:其他业务成本5000贷:原材料—丙材料500010借:营业税金及附加—城市维护建设税500—教育费附加80贷:应交税费—城市维护建设税500—教育费附加80 11借:银行存款10000贷:投资收益1000012借:主营业务收入128000投资收益10000其他业务收入6000贷:本年利润14400013借:本年利润97680贷:主营业务成本75000营业税金及附加580销售费用6000管理费用10200财务费用—汇兑手续费900其他业务成本5000 14借:所得税费用13896贷:应交税费—应交所得税1389615借:利润分配—提取法定盈余公积3242.4—提取任意盈余公积1621.2贷:盈余公积—法定盈余公积3242.4—任意盈余公积1621.216借:利润分配5000贷:应付股利5000习题四1借:材料采购—甲材料30000应交税费—应交增值税5100贷:银行存款351002借:材料采购—乙材料9000应交税费—应交增值税1530贷:应付账款—光明工厂105303借:材料采购—甲材料400—乙材料180贷:银行存款5804借:应付账款—光明工厂10530贷:银行存款10530 5借:材料采购—甲材料100—乙材料45贷:库存现金1456借:原材料—甲材料30500—乙材料9225贷:材料采购—甲材料30500—乙材料9225 7借:生产成本—A产品18300—B产品6150贷:原材料—甲材料18300—乙材料61508借:应收账款—红星工厂46800贷:主营业务收入40000应交税费—应交增值税6800 9借:销售费用—广告费800贷:银行存款80010借:应付职工薪酬15800贷:银行存款1580011借:其他应收款——王立300贷:库存现金300 12借:管理费用280库存现金20贷:其他应收款——王立300 13借:管理费用5000贷:银行存款500014借:财务费用200贷;应付利息20015借:管理费用600制造费用1800贷:累计折旧240016借:管理费用1000制造费用1288贷:银行存款228817借:银行存款58500贷:主营业务收入50000应交税费—应交增值税8500 18借:生产成本—A产品8000—B产品5000制造费用800管理费用2000贷:应付职工薪酬1580019借:生产成本—A产品1120—B产品700制造费用112管理费用280贷:应付职工薪酬—福利费316—养老保险费1896 20借:生产成本—A产品3000—B产品1000贷:制造费用400021借:库存商品—A产品29300—B产品12150贷:生产成本—A产品29300—B产品1215022借:销售费用—运杂费6000贷:银行存款600023借:主营业务成本—A产品32700—B产品9256贷:库存商品—A产品32700—B产品9256 24借:银行存款1404贷:其他业务收入1200应交税费—应交增值税20425借:其他业务成本1000贷:原材料100026借:营业外支出20000贷:银行存款2000027借:营业外支出1000贷:库存现金100028借:银行存款10000贷:投资收益1000029借:主营业务收入90000其他业务收入1200投资收益10000贷:本年利润10120030借:本年利润80116贷:主营业务成本41956营业外支出21000其他业务成本1000销售费用6800管理费用9160财务费用20031.利润总额=101200-80116=21084所得税费用=21084*33%=6957.72借:所得税费用6957.72贷:应交税费——应交所得税6957.7232.税后利润=21084-6957.72=14126.28法定盈余公积=14126.28*10%=1412.63任意盈余公积=14126.28*5%=706.31借:利润分配——法定公益金1412.63——任意公益金706.31贷:盈余公积——法定公益金1412.63——任意公益金706.3133.借:利润分配——应付股利10000贷:应付股利10000参考答案的提供感谢侯露、杨其瑞同学。

会计学 企业决策的基础 16版 1-5章 课后习题答案

Ex. 1.7i. Financial accountingh. Management accountingb. Financial reportingf. Financial statementsg. General-purpose assumptionc. Integritye. Internal controld. Public accountinga. BookkeepingCASE 1.1FANNIE MAESeveral factors prevent a large publicly owned corporation such as Fannie Mae from issuing misleading financial statements, no matter how desperately the company needs investors’ capital. To begin with, there is the basic honesty and integrity of the company’s management and its accounting personnel. Many people participate in the preparation of the financial statements of a large corporation. For these statements to be prepared in a grossly misleading manner, all of these people would have to knowingly participate in an act of criminal fraud.Next, there is the audit of Fannie Mae's financial statements by a firm of independent CPAs. These CPAs, too, would have to participate in a criminal conspiracy if the company were to supply creditors and investors with grossly misleading financial statements.If personal integrity is not sufficient to deter such an act of fraud, the federal securities laws provide for criminal penalties as well as financial liability for all persons engaged in the preparation and distribution of fraudulent financial statements. All that would be necessary for the SEC to launch an investigation would be a “tip” from but one individual within the company’s organization or its auditing firm. An investigation also would be launched automatically if the company declared bankruptcy or became insolvent shortly after issuing financial statements that did not indicate a shaky financial position.Problem 2.1 AProblem 3.8AExercise 4.2Exercise 4.14Problem 4.5AProblem 5.2AProblem 5.5A。

会计学基础 第四章习题参考答案

第四章借贷记账法的应用二、基础练习题(一)单项选择题:1. B2. A3. C4. A5. C6. B7.B 8. B(二)多项选择题:1.ABC2. BCD3. ABDE4. ABCDE5. BCDE(三)判断题:1. Y2. Y3. N4. N5. N6. Y章后作业习题参考答案:习题一会计分录1、借:在途物资——甲材料 5 000应交税费——应交增值税850贷:应付账款 5 8502、借:库存现金800贷:银行存款8003、借:其他应收款 1 000贷:库存现金 1 0004、借:在途物资——乙材料50 000应交税费——应交增值税8 500贷:银行存款58 5005、借:原材料——甲材料5000——乙材料50000贷:在途物资550006、借:在途物资——丙材料 2 500应交税费——应交增值税425贷:银行存款 2 925借:原材料--------丙材料 2 500贷:在途物资---丙材料 2 5007、借:应付账款 5 850贷:银行存款 5 8508、借:管理费用 1 200贷:其他应收款 1 000库存现金200习题二采购成本(1)采购费用:分配率:2500÷5000=0.5水陆——甲:4000×0.5=2000 ——乙:1000×0.5=500分配率:500÷5000=0.1 装卸——甲:4000×0.1=400——乙:1000×0.1=100 (2)编制材料采购成本计算表:习题三1、借:应付职工薪酬26 080贷:库存现金26 0802、借:在途物资----乙材料81 000应交税费——应交增值税(进项税额)13 430贷:应付账款94 4303、借:原材料----乙材料81 000贷:在途物资----乙材料81 0004、借:生产成本——A产品40 000——B产品48 000贷:原材料——甲40 000——乙48 0005、借:财务费用800贷:应付利息8006、借:生产成本——A产品 4 000——B产品8 000制造费用9 000管理费用 5 080贷:应付职工薪酬26 0807、借:银行存款60 000贷:短期借款60 0008、借:制造费用7 900管理费用 4 100贷:累计折旧12 0009、借:管理费用 2 450贷:银行存款 2 45010、借:应付利息 2 400贷:银行存款 2 40011、借:应付账款94 430贷:银行存款94 43012、借:生产成本——A产品 4 225——B产品12 675 贷:制造费用16 90013、借:库存商品——A 48 225——B 68 675贷:生产成本——A 48 225——B 68 675习题四1、借:生产成本——丙产品52 000——丁产品12 000制造费用8 000管理费用 1 500贷:原材料73 5002、借:生产成本——丙产品10 000——丁产品 2 000制造费用9 800管理费用 4 400贷:应付职工薪酬26 2003、借:生产成本——丙产品 6 000——丁产品 1 400贷:银行存款7 4004、借:制造费用 6 200管理费用 2 300贷:累计折旧8 500(2)电费分配表2003年7月分配率=7400÷74000=0.1(3)制造费用总额=8000+6200=24000(元)生产工人工资总额=10000+2000=12000(元)分配率=24000÷12000=2∴丙产品制造费用=10000×2=20000(元)丁产品制造费用=2000×2=4000(元)制造费用分配表2003年7月(4)产品成本计算表2003年7月习题五会计分录1、借:应收账款93 600贷:主管业务收入80 000 应交税费——应交增值税(销项税额)13 6002、借:销售费用 3 200贷:银行存款 3 2003、借:银行存款93 600贷:应收账款93 6004、借:银行存款70 200贷:主营业务收入60 000 应交税费——应交增值税(销项税额)10 2005、借:销售费用 1 200贷:银行存款 1 2006、借:主营业务成本87 000贷:库存商品——A 52 000——B 35 0007、借:应交税费——应交增值税12 000贷:银行存款12 0008、借:营业税金及附加 1 200贷:应交税费–城建税840---附加费3609、借:管理费用 1 500贷:库存现金 1 50010、借:银行存款 2 000贷:营业外收入 2 00011、借:财务费用 3 000贷:应付利息 3 00012、借:本年利润97 100贷:主营业务成本87 000销售费用 4 400营业税金及附加 1 200财务费用 3 000管理费用 1 50013、借:主营业务收入140 000营业外收入 2 000贷:本年利润142 00014、借:所得税费用11 225贷:应交税费---所得税11 225借:本年利润11 225贷:所得税费用11 225习题六(2)会计分录1、借:在途物资——甲 4 000——乙9 000应交税费——应交增值税(进项税额) 2 210 贷:银行存款15 2102、借:原材料——甲 4 000——乙9 000贷:在途物资——甲 4 000——乙9 0003、借:在途物资——乙材料30 000应交税费——应交增值税(进项税额)5 100 贷:应付账款35 100借:原材料——乙材料30 000贷:在途物资——乙材料30 0004、借:应付账款35 100贷:银行存款35 1005、借:库存现金12 100贷:银行存款12 1006、借:应付职工薪酬12 100贷:库存现金12 1007、借:预付账款12 000贷:银行存款12 0008、借:银行存款187 200贷:主管业务收入160 000 应交税费——应交增值税(销项税额)27 2009、借:销售费用 4 000贷:银行存款 4 00010、借:生产成本——A 5 550——B 3 330制造费用 2 110管理费用 1 110贷:应付职工薪酬12 10011、借:制造费用 3 000管理费用 1 000贷:累计折旧 4 00012、借:财务费用900贷:应付利息90013、借:制造费用 1 400管理费用600贷:预付账款 2 00014、借:生产成本——A 28 450——B 13 670制造费用 1 590管理费用590贷:原材料——甲材料30 000——乙材料14 30015、制造费用总额=2 110+3 000+1 400+1 590=8 100(元)生产总工时=10 125+6 075=16 200(元)分配率=0.5∴A为5 062.50,B为3 037.50借:生产成本—A 5 062.5—B 3 037.5贷:制造费用8 10016、借:库存商品----A 39 062.5贷:生产成本——A 39 062.517、借:主营业务成本80 000贷:库存商品80 00018、借:应交税费——应交增值税16 000贷:银行存款16 00019、借:营业税金及附加 1 600贷:应交税费——应交城市维护建设税 1 120 应交税费——教育费附加48020、借:主营业务收入160 000贷:本年利润160 00020、借:本年利润89 800贷:主营业务成本80 000营业税金及附加 1 600管理费用 3 300财务费用900销售费用 4 00021、借:所得税费用17 550贷:应交税费——应交所得税费用17 550借:本年利润17 550贷:所得税费用17 550(1)总分类账户:借库存现金贷借银行存款贷借原材料贷借固定资产贷借预付账款贷借库存商品贷借累计折旧贷借 短期借款贷借 应付利息 贷借 实收资本 贷借 盈余公积 贷借 本年利润 贷借 在途物资贷借 应付账款贷借 应交税费 贷贷借 主营业务收入 贷借 销售费用借 生产成本 贷借 制造费用贷借财务费用贷借管理费用贷借 主营业务成本 贷借营业税金及附加贷借所得税费用贷发生额及余额试算平衡表2003年7月30日。

会计学-企业决策的基础答案

会计学-企业决策的基础答案(总14页)--本页仅作为文档封面,使用时请直接删除即可----内页可以根据需求调整合适字体及大小--管理会计作业(chapter16-20)Chapter 16 P757Chapter 16 P761Chapter 17 P802a.Department One overhead application rate based onmachine-hours:Manufacturing Overhead=$420,000 =$35 per machine-hourMachine-Hours12,000Department Two overhead application rate based on direct labor hours:Manufacturing Overhead=$337,500=$ per direct labor hourDirect Labor Hours15,000Chapter 17 P805d.The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct labor hours to allocate overhead results in the assignment of a disproportionateamount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e.The benefits the company would achieve by implementing an activity-basedcosting system include: (1) a better identification of its operating inefficiencies,(2) a better understanding of its overhead cost structure, (3) a betterunderstanding of the resource requirements of each product line, (4) thepotential to increase the selling price of Basic Chunks to make it morecomparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price ofCustom Cuts without having to sacrifice product quality.Chapter 18 P835B. Ex. a.job costing (each project of a construction company is unique)b.both job and process costing (institutional clients may representunique jobs)c.job costing (each set of equipment is uniquely designed andmanufactured)d.process costing (the dog houses are uniformly manufactured in highvolumes)e.process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841b4,000 EU @ $ = $54,000Chapter 18 P845a.(1)$49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2)$109 [($480,000 + $108,000 + $66,000) ÷?6,000 units](3)$158 ($49 + $109)(4)$32 ($192,000 ÷ 6,000 units)(5)$18 ($108,000 ÷ 6,000 units)b.In evaluating the overall efficiency of the Engine Department, managementwould look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918d.No. With a unit sales price of $94, the break-even sales volume in units is 54,000units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units)=$540,000$10=54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918Chapter 20 P920Sales volume required to maintain current operating income:Sales Volume ?Fixed Costs + Target Operating IncomeUnit Contribution Margin?$390,000 + $350,000= $20,000 units$37。

会计学:企业决策的基础

20 COST-VOLUME-PROFIT ANALYSISChapter SummaryThe relationship between costs and revenue and the level of business activity is the foundation of profit planning. We begin our presentation of cost-volume-profit analysis with an introduction to cost behavior relationships. Fixed, variable and semivariable cost functions are illustrated graphically and numerically. The distinction between the behavior of total and unit costs is explained and graphically illustrated as well.With the various cost behavior patterns established, the chapter turns to the development of the basic CVP model. This analysis is initially presented graphically. Following discussion of the contribution margin concept the same results are established numerically. The model is solved for target levels of operating income and the margin of safety. A number of comparative static experiments illustrate the usefulness of the CVP model in a realistic planning situation. This example is developed from the point of view of managers of several different functional areas.The chapter concludes with an examination of the significance of sales mix and the high-low method of estimating fixed and variable components of mixed costs. Learning Objectives1.Explain how fixed, variable, and semivariable costs respond to changes in the volumeof business activity.2.Explain how economies of scale can reduce unit costs.3.Prepare a cost-volume-profit graph.pute contribution margin and explain its usefulness.5.Determine the sales volume required to earn a desired level of operating income.e the contribution margin ratio to estimate the change in operating income causedby a change in sales volume.e CVP relationships to evaluate a new marketing strategy.e CVP when a company sells multiple products.9.Determine semivariable cost elements.Brief topical outlineA Cost-volume relationships1Fixed costs (and fixed expenses)2Variable costs (and variable expenses)3Semivariable costs (and semivariable expenses) - see Case in Point(page 883)4 Cost-volume relationships: a graphic analysis5The behavior of per-unit costs - see Your Turn (page 886)6Economies of scale - see Case in Point (page 886)7Additional cost behavior patternsB Cost behavior and operating income1Cost-volume-profit analysis: an illustration2 Preparing and using a cost-volume-profit graph3Contribution margin: a key relationshipa Contribution margin ratio4How many units must we sell?5How many dollars in sales must we generate?6What is our margin of safety?7What change in operating income do we anticipate?8Business applications of CVPa Director of advertisingb Plant manager - see Your Turn (page 894)c Vice president of sales9Additional considerations in CVP10CVP analysis when a company sells many productsa Improving the "quality" of the sales mix11Determining semivariable cost elements: the high-low method12Assumptions underlying cost-volume-profit relationships13Summary of basic cost-volume-profit relationships – see Ethics, Fraud & Corporate Governance (page 898)C Concluding remarksTopical coverage and suggested assignmentComments and observationsTeaching objectives for Chapter 20In this chapter, we explain the patterns of cost behavior and cost-volume-profit relationships. In discussing cost behavior patterns and cost-volume-profit analysis, our teaching objectives are to:1Explain the importance of understanding cost-volume-profit relationships in planning and controlling business operations.2Define and provide examples of fixed costs, variable costs, and semivariable costs.3Contrast the behavior of a cost expressed on per-unit basis with that of the total cost.4Explain that cost behavior patterns (and cost-volume-profit analysis) serve only as useful approximations. (As part of this discussion, explore other cost behaviorpatterns and introduce the concept of the relevant volume range.)5 Illustrate the preparation of a break-even graph, and explain its usefulness.6Define contribution margin, contribution margin ratio,and contribution margin per unit. (Stress that these concepts form the cornerstone of cost-volume-profitanalysis, and also will be used extensively in later chapters.)7Show how contribution margin ratio and/or contribution margin per unit are used to determine the sales volume necessary to earn a specified level of operating income.8Illustrate the importance of sales mix and the relative contribution margin ratios of different products.9Illustrate and explain the high-low method of determining the fixed and variable components of a semivariable cost.10Review the assumptions underlying cost-volume-profit analysis.11Review the summary of basic cost-volume-profit relationships.General commentsWe find that the challenge in successfully presenting cost-volume-profit analysis is to get students to understand the significance of contribution margin, rather than to commit numerous formulas to memory. Memorizing formulas serves little purpose beyond the next exam; an understanding of the concept of contribution margin, however, can serve students well through a lifetime of managerial and personal financial decisions.Contribution margin is merely that portion of revenue that "contributes" to fixed costs and (after covering the fixed costs) to operating income. In short, all revenue except for the contribution margin is consumed by the variable costs relating to the revenue. Once students grasp the fact that only the contribution margin "contributes" to covering fixed costs and to providing a profit, most of the formulas presented in this chapter will "fall into place."We recommend that in approaching any cost-volume-profit problem (homework assignment or exam question), students jot down in the margin of the paper the contribution margin ratio and contribution margin per unit. One of these measurements is usually the key to solving the problem.Supplemental ExercisesGroup ExerciseSuppose a company faces two technologies for manufacturing its single product. The first requires significantly higher fixed costs but much smaller unit variable costs than does the second. Prepare a cost-volume-profit graph for each of the technologies. Using the graphs, discuss the economic circumstances that would lead to a choice of one technology over the other.Internet ExerciseResearch the Dell Computer website at /and the Hewlett Packard website at / to see how these corporations differ in their approach to manufacturing and selling personal computers.10-MINUTE QUIZ A SECTIONInformation regarding a product manufactured and sold by Schiffman is shown below:Maximum capacity with existing facilities 4,000 unitsTotal fixed costs per month ......................................................................... $50,000Variable cost per unit ................................................................................... $42.00Sales price per unit ....................................................................................... $56.001Refer to the above data. The contribution margin ratio for this product is:a20%.c30%.b25%.d40%.2Refer to the above data. The number of units Schiffman must sell to break even is: (rounded)a3,927.c4,823.b3572. d5,140.3Refer to the above data. The dollar sales volume necessary to produce monthly operating income of $12,000 before taxes is:a$188,000.c$288,000.b$186,000.d$248,000.Use the following data for questions 4 and 5.The monthly high and low levels of units and total manufacturing overhead for RatnereCompany are shown below:ManufacturingUnits Overhead Highest observed level .................................................... 117,000 $306,000Lowest observed level .................................................... 81,000 234,0004Refer to the above data. The cost formula for Ratnere’s monthly overhead cost can be expressed as:a$2.65 average cost per unit.b$1.75 average cost per unit.c$24,000 fixed cost plus $1.00 per unit.d$72,000 fixed cost + $2.00 per unit.5Refer to the above data.In a month in which 30,000 equivalent full units are produced, Ratnere’s manufacturing overhead should be approximately:a $52,500.c$ 132,000.b$79,500.d$ 90,500.10-MINUTE QUIZ B SECTION1Management predicts total sales for June to be $3,000,000, yielding a margin of safety of $1,000,000 and a contribution margin ratio of 25%. Which of thefollowing amounts is not consistent with this information?a Fixed costs, $500,000.b Variable costs, $750,000.c Operating income, $250,000.d Break-even sales volume, $2,000,000.Use the following data for questions 2 through 4.The recent high and low levels of hours operated and monthly repair cost for heavy equipment for Universal Mfg. are shown below:Hours Operated Repair Cost Highest observed level 24,000 $7,450Lowest observed level .................................................... 21,500 6,7002Refer to the above data. Using the high-low method, compute the variable element of repair cost per hour of operation for Universal’s equipment:a $750c$0.30.b$3.33.d$0.34.3Refer to the above data. Using the high-low method, compute the fixed element of Universal’s monthly repair cost:a $150.c$6,300.b$250.d$6,450.4Refer to the above data.The total estimated repair cost for a month in which Universal operates equipment for 19,000 hours is:a$5,950.c$6,450.b$6,300.d$5,700.5Perkins Corporation manufactures two products; data are shown below:Contribution RelativeMargin Ratio Sales Mix Product A ........................................................................ 40% 40%Product B......................................................................... 30% 60%If Perkins’ monthly fixed costs average $425,000, what is its break-even pointexpressed in sales dollars?a$1,320,000.c$1,250,000.b$1,400,000.d$990,000.CHAPTER 20 NAME _____________________#10-MINUTE QUIZ C SECTIONPaulsen Company sells only one product. The regular selling price is $50. Variable costs are 70% of this selling price, and fixed costs are $7,500 per month.Management decides to increase the selling price from $50 to $55 per unit. Assume that the cost of the product and the fixed operating expenses are not changed by this pricing decision. 1Refer to the above data. At the original selling price of $50 per unit, what is the contribution margin ratio?2Refer to the above data. At the original selling price of $50 per unit, how many units must Paulsen sell to break even?3Refer to the above data. At the original selling price of $50 per unit, what dollar volume of sales per month is required for Paulsen to earn a monthly operating income of $5,000?4Refer to the above data.At the increased selling price of $55 per unit, what is the contribution margin ratio?5Refer to the above data. At the increased selling price of $55 per unit, what dollar volume of sales per month is required to break-even?CHAPTER 20 NAME #10-MINUTE QUIZ D SECTIONRhinefold brews reduced calorie beer and regular beer. Sales of its reduced calorie beer represent 25% of the company’s total revenue. Sales of regular beer represent the remaining 75%. Reduced calorie beer has a contribution margin ratio of 80%, whereas the contribution margin ratio of regular beer is only 60%. Rhinefold’s monthly fixed costs average $609,500. 1What is the company’s monthly break-even point expressed in sales dollars? $__________2What monthly sales level must be achieved for Rhinefold to earn a monthly operating income of $350,000? $__________3If Rhinefold generates $1,400,000 in monthly sales, it will earn a monthly operating income of $__________.4Assume Rhine fold’s margin of safety was $300,000 in May. What was the company’s operating income in May? $__________.5If Rhinefold’s monthly fixed costs increase by $8,500, what level of monthly sales revenue will be required to break-even? $__________.SOLUTIONS TO CHAPTER 20 10-MINUTE QUIZZESQUIZ A QUIZ B1B1 B2B2 C3D3 B4D4 A5C5 CLearning Learning Objectives: 1, 4, 5, 6, 8, 9 Objectives: 4, 5, 6QUIZ C1Sales price (100%) minus variable costs (70%) = 30%2Sales volume (units) = fixed costs / contribution margin$7,500 / ($50 x 30%) = 500 units3fixed costs + operating incomeSales volume (dollars) = ___________________________contribution margin ratio$7,500 + $5,000= ______________ = $41,66730%4$55 sales price - $35 variable cost per unit ($50 x 70%)___________________________________________________ = 36.4%$55 sales price5Sales volume (dollars) = fixed costs / contribution margin ratio= $7,500 / 30% = $25,000Learning Objective: 7QUIZ D1$609,500/[(75% x 60%) + (25% x 80%)] = $937,6922($609,500 + $350,000)/[75% x 60%) + (25% x 80%)] = $1,476,154 3$1,400,000 x [(75% x 60%) + $1,400,000 (25% x 80%)] = $910,000; Thus, operating income = $910,000 - $609,500 = $300,5004$300,000 x [(75% x 60%) + (25% x 80%)] = $195,0005($609,500 + $8,500)/[(75% x 60%) + (25% x 80%)] = $950,769 Learning Objective: 4, 5, 6, 8Chapter 20 - Cost-Volume-Profit AnalysisAssignment Guide to Chapter 20Financial and Managerial Accounting, 17/e 20-11 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.。

基础会计——第四章课后测试答案解析

基础会计——第四章课后测试答案解析座位号: [填空题] *_________________________________姓名: [填空题] *_________________________________1.下列会计分录中,属于简单会计分录的是()的会计分录. [单选题] *A.一借多贷B.一贷多借C.一借一贷(正确答案)D.多借多贷答案解析:简单会计分录是指每一项经济业务只涉及两个对应账户的分录,即一借一贷的会计分录。

复合会计分录是指一项经济业务涉及两个或两个以上有对应关系账户的分录,即一借多贷、一贷多借或多借多贷的会计分录。

2.资产类账户贷方记减少数,借方记增加数,其余额(). [单选题] *A.在贷方B.在借方C.一般在借方,其备抵调整账户的余额在贷方(正确答案)D.期末无余额3.甲企业购进材料100吨,货款计1000000元,途中发生定额内损耗1000元,并以银行存款支付该材料的运杂费1000元,保险金5000元,增值税进项税额为130000元.则该材料的采购成本为()元. [单选题] *A.1000000B.1005000C.1006000(正确答案)D.1175000答案解析:采购成本包括材料货款、运杂费和保险金,定额损耗包含在成本中,增值税进项税计入应交税费-应交增值税(进项税额)中,故为1 000 000+1 000+5 000=1 006 000元。

4.下列各项目中,应记入“制造费用”账户的是(). [单选题] *A.生产产品耗用的材料B.机器设备的折旧费(正确答案)C.生产工人的工资D.行政管理人员的工资答案解析:选项AC计入生产成本;选项D计入管理费用。

5.“期间费用”类账户期末应(). [单选题] *A.有借方余额B.有贷方余额C.有时在借方,有时在贷方出现余额D.无余额(正确答案)答案解析:“期间费用”类账户期末转入“本年利润”,结转后无余额。

6.“生产成本”账户的期末借方余额表示(). [单选题] *A.完工产品成本B.半成品成本C.本月生产成本合计D.期末在产品成本(正确答案)答案解析:“生产成本”账户期末余额在借方,表示尚未加工完成的各项在产品成本。

会计学基础第四章练习题答案

姓名班别学号:得分第四章练习题答案一、单选题(每题1分,共30分)1。

企业接受其他单位或个人捐赠固定资产时,应贷记的账户是( A )。

A 营业外收入B 实收资本C 资本公积D 盈余公积2。

( A )是指为筹集生产经营所需资金而发生的费用。

A 财务费用B 借入资本C 投入资本D 管理费用3. 企业计提短期借款的利息支出应借记的账户是( A )。

A 财务费用B 短期借款C 应付利息D 在建工程4. 企业设置“固定资产”账户是用来反映固定资产的( A )。

A 原始价值B 磨损价值C 累计折旧D 净值5. 某制造企业为增值税一般纳税人,本期外购原材料一批,发票注明买价20000元,增值税税额3400元,入库前发生的挑选整理费用为1000元,则该批原材料的入账价值为( C )元。

A 20000B 23400C 21000D 244006. 下列费用中,不构成产品成本,而应直接计入当期损益的是( C ).A 直接材料费用B 直接人工费用C 期间费用D 制造费用7。

下列不属于期间费用的是( A )。

A 制造费用B 管理费用C 财务费用D 销售费用8。

“固定资产”科目所核算的固定资产的原始价值是( B )。

A 该固定资产投入市场初期价格B 购建当时的买价和附属支出C 不包括运杂费、安装费的买价D 现行的购置价格和附属支出9. 固定资产因损耗而减少的价值,应记入( A )账户的贷方。

A 累计折旧B 固定资产C 管理费用D 制造费用10。

不影响本期营业利润的项目是( D ).A 主营业务成本B 主营业务收入C 管理费用D 所得税费用11。

下列不属于营业外支出的项目是( D )。

A 固定资产盘亏损失B 非常损失C 捐赠支出D 坏账损失12。

下列属于营业外收入的项目是( D ).A 固定资产盘盈收益B 出售原材料的收入C 出售无形资产收益D 收到包装物押金13. 企业购入材料发生的运杂费等采购费用,应计入( B )。

A 物资采购B 材料采购C 生产D 管理费用14。

会计学-企业决策的基础 答案

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line. Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1a. job costing (each project of a construction company is unique)b . both job and process costing (institutional clients may represent unique jobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d . process costing (the dog houses are uniformly manufactured in high volumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3A4,000 EU @ $61.50 = $246,000 b4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume ?Fixed Costs + Target OperatingIncomeUnit Contribution Margin?$390,000 + $350,000= $20,000 units$37。

会计学:企业决策的基础exercises-chapter4答案

SOLUTIONS TO EXERCISESEx 4–1 a. Book valueb. Materialityc. Matching principled. Unrecorded revenuee. Adjusting entriesf. Unearned revenueg. Prepaid expensesh. None (This is an example of “depreciation expense.”)Ex. 4–2 Income Statement Balance SheetAdjustingEntryab NE I D NE I Dc I NE I I NE Id NE I D NE I De NE I D D NE Df I NE I NE D I Ex. 4–3 a. Rent Expense ......................................................... 240,000Prepaid Rent .................................................. 240,000 To record rent expense for May ($1,200,000 ÷ 5 months =$240,000 per month).b. Unearned Ticket Revenue ......................................... 148,800Ticket Revenue .............................................. 148,800 To record earning portion of season ticket revenuerelating to May home games.Ex. 4–4 a. (1) Interest Expense (375)Interest Payable (375)$50,000 x 9% annual rate x 1/12 = $375.(2) Accounts Receivable ............................................ 10,000Consulting Fees Earned ................................ 10,000 To record ten days of unbilled consulting fees at$1,000 per day.b. $2,250 ($50,000 x 9% x 6/12 = $2,250)c. $15,000 ($25,000 - $10,000 earned in December, 2002)Ex. 4–5 a. The balance of TWA’s Advance Ticket Sales account represents unearned revenue—that is, amounts collected from customers prior to rendering therelated services (air travel). As TWA has an obligation to render these services,the Advanced Ticket Sales account appears among the liabilities in TWA’sbalance sheet.b. TWA normally reduces the balance of this liability account by renderingservices to customers—that is, by providing flights for which the customershave purchased tickets. On some occasions, however, TWA reduces the balanceof this liability by making cash refunds to customers.Ex. 4–6 a. 1. I nterest Expense ..................................................... 1,200Interest Payable .............................................. 1,200 To record interest accrued on bank loan duringDecember.2. D epreciation Expense: Office Building .......................... 1,100Accumulated Depreciation: Office Building ............ 1,100 To record depreciation on office building ($330,000 ÷ 25years ⨯1/12 = $1,100).3. A ccounts Receivable ................................................ 64,000Marketing Revenue Earned ................................ 64,000 To record accrued Marketing revenue earned inDecember.4. I nsurance Expense (150)Prepaid Insurance (150)To record insurance expense (1,800 ÷ 12 months =$150).5. U nearned Revenue .................................................. 3,500Marketing Revenue Earned ................................ 3,500 To record portion of unearned revenue that had becomeearned in December.6. S alaries Expense ..................................................... 2,400Salaries Payable .............................................. 2,400 To record accrued salaries in December.b. $62,650 ($64,000 + $3,500 - $1,200 - $1,100 - $150 - $2,400).Ex. 4–7 a. The total interest expense over the life of the note is $5,400 ($120,000 ⨯ .09 ⨯6/12 = $5,400).The monthly interest expense is $900 ($5,400 ÷ 6 = $900).b. The liability to the bank at December 31, 2002, is $121,800 (Principal, $120,000+ $1,800 accrued interest).c. 2002Oct. 31 Cash ......................................................... 120,000Notes Payable ..................................... 120,000 Obtain from bank six-month loan with interest at9% a year.d. Dec. 31 Interest Expense (900)Interest Payable (900)To accrue interest expense for December on notepayable ($120,000 ⨯ 9% ⨯1/12).e. The liability to the bank at March 31, 2003, is $124,500, consisting of $120,000principal plus $4,500 accrued interest for five months.Ex. 4–8 a. May 1 Cash ......................................................... 300,000Notes Payable ..................................... 300,000 Obtained a three-month loan from National Bankat 12% interest per year.May 31 Interest Expense ......................................... 3,000Interest Payable .................................. 3,000 To record interest expense for May on notepayable to National Bank ($300,000 ⨯ 12% ⨯1/12 =$3,000).b. May 1 Prepaid Rent .............................................. 180,000Cash ................................................ 180,000 Paid rent for six months at $30,000 per month.May 31 Rent Expense ............................................. 30,000Prepaid Rent ...................................... 30,000 To record rent expense for the month of May.c. May 2 Cash ......................................................... 910,000Unearned Admissions Revenue ................ 910,000 Sold season tickets to the 70-day racing season.May 31 Unearned Admissions Revenue ........................ 260,000Admissions Revenue ............................. 260,000 To record admissions revenue from the 20 racingdays in May ($910,000 ⨯ 20/70 = $260,000).d. May 4 No entry required.e. May 6 Prepaid Printing .......................................... 12,000Cash ................................................ 12,000 Printed racing forms for first 30 racing days.May 31 Printing Expense ......................................... 8,000Prepaid Printing .................................. 8,000 To record printing expense for 20 racing days inMay.f. May 31 Concessions Receivable ................................. 16,500Concessions Revenue............................ 16,500 Earned 10% of refreshment sales of $165,000during May.- --Something to Consider:Effects of omission of May 31 adjusting entry for rent expense on May 31financial statements:Revenue Not affectedExpenses Understated (by May’s rent of $30,000)Net Income Overstated (because May rent expense was not recognized)Assets Overstated (Prepaid Rent should be reduced by portionexpired in May)Liabilities Not affectedOwners’ Equity Overstated (because net income is overstated)Ex. 4–9 a. Materiality refers to the relative importance of an item. An item is material if knowledge of it might reasonably influence the decisions of users of financialstatements. If an item is immaterial, by definition it is not relevant to decisionmakers.Accountants must account for material items in the manner required bygenerally accepted accounting principles. However, immaterial items may beaccounted for in the most convenient and economical manner.b. Whether a specific dollar amount is “material” depends upon the (1) size of theamount and (2) nature of the item. In evaluating the size of a dollar amount,accountants consider the amount in relation to the size of the organization.Based solely upon dollar amount, $2,500 is not material in relation to thefinancial statements of a large, publicly owned corporation. For a smallbusiness however, this amount could be material.In addition to considering the size of a dollar amount, accountants must alsoconsider the nature of the item. The nature of an item may make the item“material” to users of the financial statements regardless of its dollar amount.Examples might include bribes paid to government officials, or theft ofcompany assets or other illegal acts committed by management.In summary, one cannot say whether $2,500 is a material amount. The answerdepends upon the related circumstances.c. Two ways in which the concept of materiality may save time and effort foraccountants are:1. Adjusting entries may be based upon estimated amounts if there is little orno possibility that the use of an estimate will result in material error. Forexample, an adjusting entry to reflect the amount of supplies used may bebased on an estimate of the cost of supplies remaining on hand.2. Adjusting entries need not be made to accrue immaterial amounts ofunrecorded expenses or unrecorded revenue. For example, no adjustingentries normally are made to record utility expense payable at year-end.Ex. 4–10 a. None (or Materiality). Accounting for immaterial items is not “wrong” or a “violation” of generally accepted accounting prin ciples; it is merely a waste oftime. The bookkeeperis failing to take advantage of the concept of materiality, which permits chargingimmaterial costs directly to expense, thus eliminating the need to recorddepreciation in later periods.b. Matching.c. Realization.Ex. 4–11 a. Accounts likely to have required an adjusting entry are:1. Investments2. Accounts Receivable3. Inventories4. Prepaid Expenses5. Deferred Income Taxes6. Buildings7. Machinery and Equipment8. Intangible Assets9. Accounts Payable10. Accrued Liabilities11. Income Taxes Payable12. Deferred Compensation and Other LiabilitiesNote to the Instructor:The adjustments required for many of the accountslisted above are discussed in subsequent chapters. Some are beyond the scopeof an introductory course.SOLUTIONS TO PROBLEMS20 Minutes, Easy PROBLEM 4–1FLORIDA PALMS COUNTRY CLUBPROBLEM 4–1FLORIDA PALMS COUNTRY CLUB (concluded)b.1. Accruing unpaid expenses.2. Accruing uncollected revenue.3. Converting liabilities to revenue.4. Converting assets to expenses.5. Accruing unpaid expenses.6. Converting assets to expenses.7. No adjusting entry required.8. Accruing unpaid expenses.c. The clubhouse was built in 1925 and has been fully depreciated for financial accountingpurposes. The net book value of an asset reported in the balance sheet does not reflect the asset’s fair market value. Likewise, depreciation expense rep orted in the income statement does not reflect a decline in fair market value, physical obsolescence, or wear-and-tear.40 Minutes, Medium PROBLEM 4–2PROBLEM 4–2ENCHANTED FOREST (concluded)b.1. Accruing uncollected revenue.2. Accruing unpaid expenses.3. Converting assets to expenses.4. No adjusting entry required.5. Accruing unpaid expenses.6. Accruing uncollected revenue.7. Converting liabilities to revenue.8. Accruing unpaid expenses.9. Accruing unpaid expenses.c. Income Statement Balance SheetAdjustment Revenue Expenses =NetIncome Assets = Liabilities +Owners’Equity1. I NE I I NE I2. NE I D NE I D3. NE I D D NE D4. NE NE NE NE NE NE5. NE I D NE I D6. I NE I I NE I7. I NE I NE D I8. NE I D NE I D9. NE I D NE I Dd. $340 ($12,000 x 0.85% x 4/12)e. Original cost of buildings .......................................................$600,000 Accumulated depreciation: buildings (prior to adjusting entry 3in part a) ...........................................................................$310,000 December depreciation expense from part a ..............................2,000 Accumulated depreciation, buildings, 12/31 ...............................(312,000) Net book value at December 31 ..............................................$288,00SEA CAT a. (1) Age of the catamaran in months = accumulated depreciation monthlydepreciation. Useful life is given as 10 years, or 120 months.Cost $46,200 120 months = $385 monthly depreciation expense.Accumulated depreciation of $9,240 $385 monthly depreciation = 24 months.(2) Tickets used in June (14)5Tickets outstanding on June 30 ($825$15) (55)Tickets sold to resort hotel on June 1 (20)(3) Prepaid rent of $6,000 5 months remaining = $1,200 monthlyrental expense.(4) $1,400 x 12/8 = $2,100 original cost.Since 4 months of the 12-month life of the policy have expired, the $1,400 ofunexpired insurance applies to the remaining 8 months. This indicates a monthlycost of $175, computed as $1,400 8. Therefore, the 12-month policy originallycost $2,100, or 12 x $175.PROBLEM 4–4CAMPUS THEATER (concluded) b. (1) Eight months (bills received January through August). Utilities bills are recorded asmonthly bills are received. As of August 31, eight monthly bills should have beenreceived.(2) Seven months (January through July). Depreciation expense is recorded only inmonth-end adjusting entries. Thus, depreciation for August is not included in theAugust unadjusted trial balance.(3) Twenty months ($14,000 $700 per month).c. Corporations must pay their income taxes in several installment payments throughoutthe year. The balance in the Income T axes Expense account represents the total amount of income taxes expense recognized since the beginning of the year. But Income T axes Payable represents only the portion of this expense that has not yet been paid. In the example at hand, the $4,740 in income taxes payable probably represents only theincome taxes expense accrued in July, as Pickwood should have paid taxes accrued in the first two quarters by June 15.50 Minutes, Strong PROBLEM 4–5KEN HENSLEY ENTERPRISES, INC.PROBLEM 4–5KEN HENSLEY ENTERPRISES, INC. (continued)c. Monthly rent expense for the last two months of 2002 was $2,000 ($6,000 3months). The $21,000 rent expense shown in the studio’s trial balance includes a$2,000 rent expense for November, which means that total rent expense for January through October was $19,000 ($21,000 - $2,000). The monthly rent expense in these months must have been $1,900 ($19,000 10 months). Thus, it appears that thestudio’s monthly rent increased by $100 (from $1,900 t o $2,000) in November andDecember.15 Minutes, Medium PROBLEM 4–6KOYNE CORPORATION。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

SOLUTIONS TO EXERCISESEx 4–1 a. Book valueb. Materialityc. Matching principled. Unrecorded revenuee. Adjusting entriesf. Unearned revenueg. Prepaid expensesh. None (This is an example of ―depreciation expense.‖)Ex. 4–2 Income Statement Balance SheetAdjustingEntryab NE I D NE I Dc I NE I I NE Id NE I D NE I De NE I D D NE Df I NE I NE D I Ex. 4–3 a. Rent Expense....................................................................................... 240,000Prepaid Rent ........................................................................... 240,000 To record rent expense for May ($1,200,000 ÷ 5 months =$240,000 per month).b. Unearned Ticket Revenue .................................................................. 148,800Ticket Revenue ....................................................................... 148,800 To record earning portion of season ticket revenue relating toMay home games.Ex. 4–4 a. (1) Interest Expense (375)Interest Payable (375)$50,000 x 9% annual rate x 1/12 = $375.(2) Accounts Receivable .................................................................... 10,000Consulting Fees Earned ................................................... 10,000 To record ten days of unbilled consulting fees at $1,000 perday.b. $2,250 ($50,000 x 9% x 6/12 = $2,250)c. $15,000 ($25,000 - $10,000 earned in December, 2002)Ex. 4–5 a. The balance of TWA’s Advance Ticket Sales account represents unearned rev enue—that is, amounts collected from customers prior to rendering the related services (airtravel). As TWA has an obligation to render these services, the Advanced Ticket Salesaccount appears among the liabilities in TWA’s balance sheet.b. TWA normally reduces the balance of this liability account by rendering services tocustomers—that is, by providing flights for which the customers have purchased tickets.On some occasions, however, TWA reduces the balance of this liability by making cashrefunds to customers.Interest Payable ...................................................................... 1,200 To record interest accrued on bank loan during December.2. D epreciation Expense: Office Building ............................................ 1,100Accumulated Depreciation: Office Building ........................ 1,100 To record depreciation on office building ($330,000 ÷ 25 years ⨯1/12 = $1,100).3. A ccounts Receivable ........................................................................... 64,000Marketing Revenue Earned................................................... 64,000 To record accrued Marketing revenue earned in December.4. I nsurance Expense (150)Prepaid Insurance (150)To record insurance expense (1,800 ÷ 12 months = $150).5. U nearned Revenue ............................................................................. 3,500Marketing Revenue Earned................................................... 3,500 To record portion of unearned revenue that had become earnedin December.6. S alaries Expense ................................................................................. 2,400Salaries Payable ...................................................................... 2,400 To record accrued salaries in December.b. $62,650 ($64,000 + $3,500 - $1,200 - $1,100 - $150 - $2,400).Ex. 4–7 a. The total interest expense over the life of the note is $5,400 ($120,000 ⨯ .09 ⨯6/12= $5,400).The monthly interest expense is $900 ($5,400 ÷ 6 = $900).b. The liability to the bank at December 31, 2002, is $121,800 (Principal, $120,000 + $1,800accrued interest).c. 2002Oct. 31 Cash .................................................................................... 120,000Notes Payable ........................................................ 120,000 Obtain from bank six-month loan with interest at 9%a year.d. Dec. 31 Interest Expense (900)Interest Payable (900)To accrue interest expense for December on notepayable ($120,000 ⨯ 9% ⨯1/12).e. The liability to the bank at March 31, 2003, is $124,500, consisting of $120,000 principalplus $4,500 accrued interest for five months.Notes Payable ........................................................ 300,000 Obtained a three-month loan from National Bank at12% interest per year.May 31 Interest Expense ................................................................ 3,000Interest Payable ..................................................... 3,000 To record interest expense for May on note payable toNational Bank ($300,000 ⨯ 12% ⨯1/12 = $3,000).b. May 1 Prepaid Rent ...................................................................... 180,000Cash ........................................................................ 180,000 Paid rent for six months at $30,000 per month.May 31 Rent Expense ..................................................................... 30,000Prepaid Rent .......................................................... 30,000 To record rent expense for the month of May.c. May 2 Cash .................................................................................... 910,000Unearned Admissions Revenue ............................ 910,000 Sold season tickets to the 70-day racing season.May 31 Unearned Admissions Revenue ........................................ 260,000Admissions Revenue ............................................. 260,000 To record admissions revenue from the 20 racing daysin May ($910,000 ⨯ 20/70 = $260,000).d. May 4 No entry required.e. May 6 Prepaid Printing ................................................................ 12,000Cash ........................................................................ 12,000 Printed racing forms for first 30 racing days.May 31 Printing Expense ............................................................... 8,000Prepaid Printing .................................................... 8,000 To record printing expense for 20 racing days in May.f. May 31 Concessions Receivable..................................................... 16,500Concessions Revenue ............................................ 16,500 Earned 10% of refreshment sales of $165,000 duringMay.Something to Consider:Effects of omission of May 31 adjusting entry for rent expense on May 31 financialstatements:Revenue Not affectedExpenses Understated (by May’s rent of $30,000)Net Income Overstated (because May rent expense was not recognized)Assets Overstated (Prepaid Rent should be reduced by portion expired inMay)Liabilities Not affectedOwners’ Equity Overstated (because net income is overstated)Ex. 4–9 a. Materiality refers to the relative importance of an item. An item is material if knowledge of it might reasonably influence the decisions of users of financial statements. If an itemis immaterial, by definition it is not relevant to decision makers.Accountants must account for material items in the manner required by generallyaccepted accounting principles. However, immaterial items may be accounted for in themost convenient and economical manner.b. Whether a specific dollar amount is ―material‖ depends upon the (1) size of the amountand (2) nature of the item. In evaluating the size of a dollar amount, accountants considerthe amount in relation to the size of the organization.Based solely upon dollar amount, $2,500 is not material in relation to the financialstatements of a large, publicly owned corporation. For a small business however, thisamount could be material.In addition to considering the size of a dollar amount, accountants must also considerthe nature of the item. The nature of an item may make the item ―material‖ to users ofthe financial statements regardless of its dollar amount. Examples might include bribespaid to government officials, or theft of company assets or other illegal acts committedby management.In summary, one cannot say whether $2,500 is a material amount. The answer dependsupon the related circumstances.c. Two ways in which the concept of materiality may save time and effort for accountantsare:1. Adjusting entries may be based upon estimated amounts if there is little or nopossibility that the use of an estimate will result in material error. For example, anadjusting entry to reflect the amount of supplies used may be based on an estimateof the cost of supplies remaining on hand.2. Adjusting entries need not be made to accrue immaterial amounts of unrecordedexpenses or unrecorded revenue. For example, no adjusting entries normally aremade to record utility expense payable at year-end.Ex. 4–10 a. None (or Materiality). Accounting for immaterial items is not ―wrong‖ or a ―violation‖ of generally accepted accounting principles; it is merely a waste of time. The bookkeeperis failing to take advantage of the concept of materiality, which permits charging im-material costs directly to expense, thus eliminating the need to record depreciation in laterperiods.b. Matching.c. Realization.Ex. 4–11 a. Accounts likely to have required an adjusting entry are:1. Investments2. Accounts Receivable3. Inventories4. Prepaid Expenses5. Deferred Income Taxes6. Buildings7. Machinery and Equipment8. Intangible Assets9. Accounts Payable10. Accrued Liabilities11. Income Taxes Payable12. Deferred Compensation and Other LiabilitiesNote to the Instructor: The adjustments required for many of the accounts listed aboveare discussed in subsequent chapters. Some are beyond the scope of an introductorycourse.SOLUTIONS TO PROBLEMS20 Minutes, Easy PROBLEM 4–1FLORIDA PALMS COUNTRY CLUBPROBLEM 4–1 FLORIDA PALMS COUNTRY CLUB (concluded)b.1. Accruing unpaid expenses.2. Accruing uncollected revenue.3. Converting liabilities to revenue.4. Converting assets to expenses.5. Accruing unpaid expenses.6. Converting assets to expenses.7. No adjusting entry required.8. Accruing unpaid expenses.c. The clubhouse was built in 1925 and has been fully depreciated for financial accounting purposes.The net book value of an asset reported in the balance sheet does not reflect the asset’s fair market value. Likewise, depreciation expense reported in the income statement does not reflect a decline in fair market value, physical obsolescence, or wear-and-tear.40 Minutes, Medium PROBLEM 4–2PROBLEM 4–2ENCHANTED FOREST (concluded)b.1. Accruing uncollected revenue.2. Accruing unpaid expenses.3. Converting assets to expenses.4. No adjusting entry required.5. Accruing unpaid expenses.6. Accruing uncollected revenue.7. Converting liabilities to revenue.8. Accruing unpaid expenses.9. Accruing unpaid expenses.c. Income Statement Balance SheetAdjustment Revenue Expenses =NetIncome Assets = Liabilities +Owners’Equity1. I NE I I NE I2. NE I D NE I D3. NE I D D NE D4. NE NE NE NE NE NE5. NE I D NE I D6. I NE I I NE I7. I NE I NE D I8. NE I D NE I D9. NE I D NE I Dd. $340 ($12,000 x 0.85% x 4/12)e. Original cost of buildings ......................................................................................$600,000Accumulated depreciation: buildings (prior to adjusting entry 3 in parta) ...............................................................................................................................$310,000December depreciation expense from part a ...................................................... 2,000Accumulated depreciation, buildings, 12/31 .......................................................(312,000) Net book value at December 31 ............................................................................$288,000SEA CAT a. (1) Age of the catamaran in months = accumulated depreciation÷monthly depreciation.Useful life is given as 10 years, or 120 months.Cost $46,200 ÷ 120 months = $385 monthly depreciation expense.Accumulated depreciation of $9,240 ÷ $385 monthly depreciation = 24 months.(2) Tickets used in June (145)Tickets outstanding on June 30 ($825 ÷ (55)Tickets sold to resort hotel on June 1 (200)(3) Prepaid rent of $6,000 ÷expense.(4) $1,400 x 12/8 = $2,100 original cost.Since 4 months of the 12-month life of the policy have expired, the $1,400 of unexpiredinsurance applies to the remaining 8 months. This indicates a monthly cost of $175,computed as $1,400 ÷ 8. Therefore, the 12-month policy originally cost $2,100, or 12 x $175.PROBLEM 4–4CAMPUS THEATER (concluded) b. (1) Eight months (bills received January through August). Utilities bills are recorded asmonthly bills are received. As of August 31, eight monthly bills should have been received.(2) Seven months (January through July). Depreciation expense is recorded only in month-endadjusting entries. Thus, depreciation for August is not included in the August unadjustedtrial balance.(3) Twenty months ($14,000 $700 per month).c. Corporations must pay their income taxes in several installment payments throughout the year.The balance in the Income Taxes Expense account represents the total amount of income taxes expense recognized since the beginning of the year. But Income Taxes Payable represents only the portion of this expense that has not yet been paid. In the example at hand, the $4,740 in income taxes payable probably represents only the income taxes expense accrued in July, as Pickwood should have paid taxes accrued in the first two quarters by June 15.50 Minutes, Strong PROBLEM 4–5KEN HENSLEY ENTERPRISES, INC.PROBLEM 4–5 KEN HENSLEY ENTERPRISES, INC. (continued)c. Monthly rent expense for the last two months of 2002 was $2,000 ($6,000 ÷ 3 months). The$21,000 rent expense shown in the studio’s trial balance includes a $2,000 rent expense forNovember, which means that total rent expense for January through October was $19,000($21,000 - $2,000). The monthly rent expense in these months must have been $1,900 ($19,000 ÷10 months). Thus, it appears that the studio’s monthly rent increased by $100 (from $1,900 t o$2,000) in November and December.15 Minutes, Medium PROBLEM 4–6KOYNE CORPORATION。