Accounting and Finance

英国会计与金融专业Top-up推荐

目前,很多本科毕业生选择出国读研,部分选择就业,还有部分选择国内考研等等,对于本科生来说可选择面大些。

但是,对于专科生来说呢,毕业后出去找工作,可能学历这块不占优势,然后国内专升本也不容易。

那么,专科生应该怎样去提升自己呢?其实,专科生还有一个选择,那就是去读一个Top-up 课程。

先读个Top-up 课程过渡下,打好基础,之后好好努力申请更好的大学去读研究生,这也是提升自己的一个很好的途径。

接下来李益老师就给大家说一说会计与金融专业Top-up 的英国大学。

Coventry University 考文垂大学Coventry 考文垂大学BA Accounting and Finance for International Business (Top-Up) 侧重于国际会计与金融方面的知识,采用多学科教学方式,涵盖经济学、商业策略、市场营销、财务规划和会计等领域,学生可选择9 月或 1 月入学。

学校是EFMD 欧洲管理发展基金会和CABS 特学商学院学会的成员之一,并且和行业机构联系紧密,比如伦敦证券交易所、英格兰银行等。

该专业曾有学生拿到了一等学位,成功入读University of Glasgow 格拉斯哥大学MA International Accounting and Financial Management 专业开设的课程有:国际金融、会计与金融学术英语1&2 、商业决策管理会计、金融理论、企业报告与分析等,考核方式:考试、课程作业、测试、小论文、小组作业/presentation 等。

Coventry 考文垂大学伦敦校区也开设有BA Accounting and Finance for International Business (Top-Up) ,可在18 年10 月入学,和Coventry 校区的课程设置不太一样,开设的必修课有:财务管理、国际企业报告、审计与内部控制、商业研究方式、实习/ 论文/ 全球商业模拟/ 创业计划、发展商业技能等,考核方式:课程作业、实践作业等;以上专业均要求:相关专业背景。

会计金融英文复习资料 introduction to accounting and finance

INT0006: INTRODUCTION TO ACCOUNTING & FINANCERevision1: ROLE OF ACCOUNTING IN BUSINESSUSERS OF ACCOUNTING INFORMATION (STAKEHOLDERS)MANAGERSAs those responsible for planning the activities of thebusiness, managers are major users of accounting information.Types of management decisions requiring accountinginformation include: ∙ the pricing of goods [& services] ∙ the quantity of goods to produce∙ investment in new equipment ∙ raising of finance to maintain/expand the business∙ production capacity ∙ purchase of stock These are many of the stakeholders in any business, butthere will be others. Many of these groups are external to the business itself; however they have an interest in the success or failure of the business.Business organisationnCompetitors Lenders Managers OwnersCustomers Suppliers Investment analystsCommunity representative s Government Employees and theirrepresentativesRULES, REGULATIONS AND STANDARDSETHICAL RULESThere are four main ethical rules which accountants should follow. These are NOT legal requirements, but principles of good practice.Prudence –when estimates of the future need to be made –for example over the creditworthiness of a debtor, managers are likely to be optimistic, it is the responsibility of theConsistency –in a company’s accounts. Accountants must keep to the same methods in subsequent accounting periods, to ensure that one year’s figures can be compared to previous periods.Objectivity– Accounts should be prepared with the minimum of bias. This is often not easy, as owners may want to adopt policies which would result in higher profit figures, or in disguising poor results. Often it is wise to resort to the prudence rule, but each case must be considered individually.Relevance– The amount of information which could be disclosed to any stakeholder is virtually limitless. It is important to limit what is provided to that which is relevant to the user’s needs. MEASUREMENT RULESThere are six main measurement rules which govern how data is recorded in accounting in an accounting system.Money measurement– All information should be presented in monetary terms. For example in the accounting records for a farm, we would not wish to know how many cattle the farm had bought and sold, it would be more useful to know the monetary value of the stock transactions.Historic cost–Transactions should be recorded at their original cost. Changes in value are ignored until an asset is disposed of.Realisation– Transactions should be accounted for in the accounting period in which legal title for them has been transferred fro the seller to the buyer.Matching– Can be referred to as the accruals convention. Expenses should be matched to the revenue that they helped generate. Difficulties occur when a business pays in advance or in arrears for an expense. A business will usually be required to pay rent in advance. An adjustment is made to the amount actually paid, so that in the final accounts the figure shown for rent is only that portion of what has been paid which actually relates to the accounting period being reported.Dual Aspect– Every time a transaction takes place there is a twofold effect. For example if a business receives money from a debtor, the amount of cash in the bank will go up and the amount of debtors will go down. This is the basis of double-entry bookkeeping.Materiality – This rule allows us to apply common sense to what is reported in accounts. If an item is insignificant then it can be ignored. It should be remembered that what may be an insignificant amount for a large business, may well be significant to a small business. Large companies usually report figures in £000, whereas a small business will report in whole pounds.Inventories(stock)BOUNDARY RULESBusiness Entity – For accounting purposes a business and its owner(s) are treated as being quite separate and distinct. This means that the owner cannot charge personal expenditure to the business, and any money invested in the business by the owner(s)is treated as a claim against the business.Going concern – financial statements should be produced on the assumption that the business will continue into the foreseeable future. If the accountant thinks that the business is not a going concern then the accounts would be prepared as if the business were to be closed.2: Statement of Financial Position (The Balance Sheet)THE MAJOR FINANCIAL STATEMENTSThe three main financial statements produced by a business are:The Cash Flow statement – showing cash movements over the accounting periodThe Income Statement (also known as the profit and loss account) which shows how much wealth was generated over the accounting period The Balance Sheet – showing the accumulated wealth at the end of the accounting periodTHE BALANCE SHEETThe balance sheet shows the financial position of a business at a particular moment of time. It shows the assets of a business and the claims against the business (liabilities and owners capital ).Assets – An asset must arise from a past transaction or event, they must be capable of measurement in monetary terms, they must be under the exclusive control of the business and be held for a probable future benefit.Claims – A claim must arise from a past transaction or event, it must be capable of measurement in monetary terms and will result in an obligation to the business to provide cash or benefit at a future time. Capital – this is the claim that the owners have against the business. Liabilities – The claims of all other parties against the businessTYPES OF ASSETAssets are listed on a balance sheet in a logical order depending on what type of asset they are.Non-current assets are held for the long term benefit of the business. They are the tools of the business.Current assets are held for the short term. The most common current assets are: Inventories (stock), trade receivables (debtors) and cash . They are listed in order of liquidity , with the least liquid being shown first. Most sales are made on credit so current assets can be shown as acycle.TYPES OF CLAIMClaims are normally classified into capital (owner’s claim) and liabilities.Liabilities can be further divided into:Current liabilities – amounts due for settlement in the short term – usually within 12 monthsNon-current liabilities – amounts due to outside parties which are not current liabilities. VALUATION OF ASSETSTangible non-current assets – Normally valued at historic cost – less depreciation. It is possible to decide to re-value these assets to a current fair value or market value. The main consequence of this is that the business must revalue all similar assets at the same time, and then regularly throughout the lives of the assets.Impairment of non-current assets – if an asset is impaired it is worth less than the balance sheet value. This could be caused by changes in market values, obsolescence or factors such as fire.The business must show the impaired value on the balance sheet.Inventories – stock must be valued at the lower of cost and net realisable value. DEPRECIATION AND VALUE OF ASSETS.VALUATION OF ASSETS ON THE BALANCE SHEETNon-current assetsThe historic cost convention means that assets are normally valued at the price paid for them. Most assets lose value over their lifetime. In accountancy this reduction in value is referred to as depreciation. The total depreciation to date of an asset is recorded on the balance sheet. The accumulated depreciation is deducted from the historic cost (or fair value) to show the written down value.To calculate depreciation four factors need to be considered:∙the cost (or fair value) of the asset;∙the useful life of the asset;∙the residual value of the asset (what it will be worth when the business has finished with it);∙the depreciation methodThe cost (fair value) of the assetThe cost figure will include al of the expenses necessary to bring the asset to the business and make it ready for use. This will include delivery costs, legal costs, installation costs and the cost of improvements or alterations.The useful life of the assetA business should estimate the useful life of each asset this will probably be shorter tan the assets actual life. Advances in technology will make computer equipment obsolete long before the equipmentactually stops working.The residual value of the asset Example 3.7Cost of machine £40,000 Estimated residual value at the end of its useful lifeWhen a business disposes of an asset, at the end of its useful life, it may be that the asset will still be of use to someone else and can be sold.Depreciation methodThere are two main methods of depreciation:∙straight line method∙reducing balance methodStraight line methodThis is the most straightforward method.Deduct residual value from the cost of the asset anddivide by the useful life of the assetCost £40,000Residual value £ 1,024£38,97638,976 / 4 = £9,744Depreciation would be charged at £9,744 each yearfor four yearsReducing balance methodThis method is more complicated to calculate,but results in a more accurate depreciationfigure each year. Assets use most of their valuein the early years of their useful life. Thereducing balance method takes account of this.It applies a fixed percentage to the writtendown value of the asset each year to calculateannual depreciation.Current assetsInventories (stock)Changing prices of stock make it more difficult to decide what the value of a business’s inventories should be reported as. Both accounting standards and the prudence convention tell us to value inventory at the lower of cost and net realisable value. However, if the business buys stock regularly throughout the year then the cost will be different for each batch purchased.There are three common methods used to value inventories, all of which make an assumption about the order in which inventories are used:∙FIFO (First in first out) – assumes that the business uses the oldest stock first∙LIFO (Last in first out) – assumes that the business uses the newest stock first∙AVCO (weighted average cost) – assumes that all stock is treated as equal, and recalculates cost based on the quantity purchased at each price.LIFO method is NOT acceptable to use in final accounts.Normally net realisable value will be higher than cost. If for any reason the realisable value is lower than cost, for example inventories have suffered damage, then the balance sheet valuation should be the net realisable value.Trade receivables (debtors)When a business sells goods or services on credit, the amounts owed to the business are shown on the balance sheet as trade receivables or debtors.There is always the risk that some of these debtors may not pay. When it becomes certain that a debt is not going to be paid, the business must reduce the debtors and write off the bad debt as an expense in the financial period.Some businesses assume that a percentage of their debtors will not pay each year, and make a provision for bad debts every year.3: INCOME STATEMENTSTHE INCOME STATEMENT (PROFIT AND LOSS ACCOUNT)The income statement measures how much wealth has been generated by a business over a specified period.It deducts expenses from revenues to arrive at a profit figure.RECOGNITION OF REVENUERevenue should only be recognised when it has been realised. In practice this means that the business should only show revenue:–When it can be measured;–When it is probable that it will be received; and–The associated costs can be measured.ACCRUALS AND PREPAYMENTSThe expenses shown on the income statement are those incurred in the accounting period. In the normal course of business some expenses are paid in advance and some are paid in arrears.EXPENSES PAID IN ADVANCEWhen a business pays in advance, it will usually have paid for some of next years expenses. For example, rent is often paid in advance. The amount paid which relates to next year’s rent is NOT shown as an expense this year. Instead it appears on the balance sheet as a prepayment.EXPENSES PAID IN ARREARSIf an expense has not yet been paid for, the total amount incurred in the accounting period is shown as an expense on the income statement, with the amount not yet paid appearing on the balance sheet as an accrual4: SHARE CAPITALSHARE CAPITALAll Companies issue ordinary shares. The people who hold these shares own the business, they are known as shareholders or members. Ordinary shares are also known as equities.A company is formed by at least one person –the subscriber– that person agrees to buy a number of shares in the company. The money paid for those shares is the company’s share capital. The share capital will be made up of a number of shares of a certain denomination, such as 10p, 50p and £1 this is known as the nominal value.Limited Liability CompaniesA limited liability company is an artificial person in law. It has many of the same rights and responsibilities as a real person. A limited company is incorporated.It is a straightforward task to create a company. The subscriber, or promoter, fills in some simple forms and pays a small fee to the Registrar of Companies, who then issues a Certificate of Incorporation which evidences that the company exists.The company is quite separate from its owners. If the company is sued, the most that any owner (shareholder) can lose is limited to the amount they have paid, or agreed to pay, for their shareholding. In order to show stakeholders that a company has the right to limited liability the company must include in its name the word limited if it is a private limited company or plc if it is a public limited company.The main difference between private andpublic limited companies is that publiccompanies can offer their shares for saleto the general public.Types of sharesWhen a company is formed theincorporation documents state themaximum value of shares which thecompany will issue. This is called theauthorised share capital. Normally thecompany will not issue all of its authorisedshare capital at incorporation, it will onlyissue as much as it needs for immediate requirements. The amount of shares actually issued to shareholders is called the issued share capital. This allows the company to raise more capital in the future by issuing more shares.Sometimes shareholders have the right to pay for their shares by instalments. Until the whole amount has been paid, these shares will be known as partly paid. When the final instalment has been paid, the shares are known as fully paid.There are two main types of shares: ordinary shares and preference shares. Ordinary shareholders are not entitled to any dividend. The board of directors will decide each year if a dividend is to be paid, and how much that dividend will be. Preference shareholders are normally entitled to a specified amount of dividend. The preference shareholders dividend is paid before any ordinary shareholders dividend. Sometimes preference shares are cumulative, meaning that if a company cannot pay a dividend one year, the dividend unpaid will be added to the following year’s divid end.Raising capitalAs a company grows it may wish to raise more capital. It can then issue some more of its authorised share capital to new or existing shareholders.A private company can only issue shares to people it knows. Public companies can advertise a share issue, and often will take out a large advert in the main newspapers.Issues of new shares will normally be at a price higher than the nominal value of the shares. This is because its existing shares will be valued at a higher price. The extra that is paid for these new shares is called share premium.Methods of issuing new shares:∙Rights issues, made to existing shareholders, in proportion to their existing shareholdings∙Public issues, made to the general public∙Private placings, made to selected individuals, who are approached and asked if they would be interested in investing.A company may, under specific circumstances, buy back its own shares. This is rare, and the procedure laid out in the Companies Acts must be followed.Bonus issuesA company may issue shares to its existing shareholders, without raising capital. Companies frequently issue bonus shares as a method of reorganising its capital. The shareholders will each gain extra shares, but their ownership of the business will remain unchanged. Since there are more shares in issue, the value of each individual share will go down, making the shares more attractive to potential new investors.SOURCES OF FINANCEINTERNAL SOURCES OF FINANCEThese are sources which do not require the agreement of anyone outside the business. They are quick and easy to access, cheaper than external sources and flexible.Short term finance can be obtained by:∙ Reducing the levels of stock.∙ Arranging longer credit periods with suppliers ∙ Ensuring debtors pay more quickly Long term finance can be provided by retained profits. All of the profits of the business which have not been distributed to shareholders by dividend can be made available to invest in the business. It would also be possible to raise funds internally by selling un-used assets.EXTERNAL SOURCES OF FINANCEExternal sources of finance are more expensive to raise, and more time consuming. In the short term the most common form of externalfinance in the bank overdraft . Most businesses will have an overdraft agreement in place with their bankers.Debt factoring – a factoring company will take over the debts of a business, for a cash advance, usually less than 80% of the total debts. The factor will then collect the debts of the business, and repay the remaining 20% (less charges and interest) to the business.Invoice discounting is where a financial institution loans a percentage of the total debtors of a business, but without agreeing to collect the debts for thebusiness. In the longer term a business may raise finance byissuing new shares, either ordinary shares orpreference shares.Most businesses will also rely on long term loans .The details of the loan will be set out at the beginning, whether the loan is from a bank obtained through the issue of loan stock.Long term bank loans will normally be secured against the property of the business. If the business fails to repay the loan, the bank has the right to take the property of the business and sell it to repay the loan.5: WORKING CAPITAL CONTROLDEFINITIONTotal internal financeTighter credit controlDelayed payment to trade payablesReduced inventories levels Long-termShort-term Retained profitsOrdinary sharesBankoverdraft Debt factoringPreference shares Loans Total finance Long- term Short-termLeases Hire purchase agreementsInvoice discountingWorking capital is defined as current assets less current liabilities.The cash cycle shows the circulation of working capital in a business. This show how creditors (suppliers) provide stock, which is sold to debtors, who will eventually pay cash and so on.MANAGING WORKING CAPITALA business’s financial health depends on effective management of working capital.Managing inventories (stock) ∙ know stock levels, and perform physical checks (stocktakes) to make sure the information is correct.∙ re-order stock at appropriate times to make sure that the business does not run out, or hold too much. If prices are expected to rise then it may be wise to stockpile to save money in the future ∙ Monitor actual stock against budgeted stock as part of the budgetary control systemJust in time inventories managementJust in time (JIT) inventories management can help avoid the need to hold stock. Businesses must develop excellent relationships with their suppliers and their customers, so that customers give them notice of when they intend to order goods, and suppliers guarantee to fulfil orders in the minimum possible time.Managing receivables (debtors)Selling goods on credit will result in costs for a business. These include the administrative costs, bad debts and opportunity costs . However selling on credit is widespread, and so most businesses will offer credit terms to some of their customers.A business must have clear policies about who to give credit to, the amount and term of credit it will offer, how it will collect debts and how to reduce the risk of non-payment. Managing CashA cash flow forecast allows managers to monitor cash balances, so that surplus funds can be invested and borrowing facilities can be arranged if necessary.Managing payables (creditors)A business should negotiate suitable credit terms with its suppliers, and make prompt payment according to those terms. Businesses which obtain a reputation for slow payment will often impair their credit rating, and find further credit difficult to obtain.6: RATIO ANALYSISFINANCIAL RATIOSFinancial ratios are a quick and simple way of assessing the financial health of a business.STOCKCASHTYPES OF FINANCIAL RATIOSProfitabilityProfitability ratios relate profit to other key figures in the financial statements. Profit measures are the central measures of operating achievement.Activity (Efficiency)Activity ratios measure the efficiency with which the business utilises its assets, providing insights into management policy and operational efficiency.LiquidityLiquidity ratios examine the ability of the business to meet its short-term commitments. It is vital that a firm has the capacity to pay debts when they fall due. Poor liquidity can undermine the confidence of creditors/lendersGearing (Leverage)Gearing is important in the assessment of financial risk. Gearing ratios examine the relative contributions of investors and lenders, and the capacity of the business to service and repay loans.InvestmentSome ratios are calculated for the benefit of investors. They measure the performance of the business as it applies to the owners of the business. These investor ratios are often quoted in the financial press. Profitability ratiosActivity/Efficiency ratiosLiquidity ratiosGearing ratiosInvestor ratiosOverheads budgetTrade receivablesbudgetTrade payablesbudgetCapital expenditure budget Raw materials purchases budgetSales budget Direct labour budgetCash budgetLIMITATIONS OF FINANCIAL RATIOSAlthough ratios are a quick and easy to understand method of analysing the financial state of abusiness, there are some important limitations.∙ Quality of financial statements – if the prudence concept has been applied to reduce the stated value of an asset, then the ratios using that value will be lower. If the financial statements have been produced with the intention to mislead, then the ratios will be incorrect. ∙ Limited focus – it is important not to rely only on ratio analysis. Looking at the actual data can help to show a better picture of the business ∙ Comparison – ratios mean nothing on their own. They must be compared with something. It is important to compare ‘like with like’. Ideally we can compare across several years in the same business. Alternatively comparisons can be made with ‘industry standard’ figures. ∙ Balance sheet ratios – remember that the balance sheet represents one moment in the life of the business. The figures on the balance sheet may not reflect the true financial position of the business. ∙ Qualitative information – there is a lot that can be found out about a business by examining information which is NOT involved with numbers. How happy are the staff? Can the directors be trusted?7: BUDGETING AND BUDGETARY CONTROL AND PREPARATIONBUDGETINGEvery successful business plans for the future. Typically a business will produce a long-term plan aimed at achieving its business objectives. In order to achieve this plan, shorter term plans, for 12 months at a time will be produced. An important part of the short term plan will be a financial budget.TYPES OF BUDGETThere are many parts to a budget, all of which involve predicting future business conditions.Normally the process will begin with the sales budget . The business will forecast how many sales it will make, and at what selling price.Having decided on the level of sales, a production budget can be prepared, which will take into account the opening and closing inventories which the business wishes to maintain. The production budget then leads to materials purchases budget , direct labour budget and overheads budget.During this process the business can calculate the expected costs of all items in the budgets, and decide whether there is a need to purchase non-current assets.All of the information in these individual budgets will be put together into a budgeted income statement, balance sheet and cash flow statement.Limiting factors.It is possible that some of the items necessary to achieve budget are not available in the required quantities. Often a supplier of raw materials will be unable to meet increased orders, or there will be insufficient skilled labour available. These limiting factors may mean that the budget must be amended.BUDGETARY CONTROLBudgets allow managers to control the business. It allows them to check, on a regular basis, that the business is performing according to the budget. If things are not going according to plan, something can be done to put things right.Often managers will only receive information about items which are not going according to budget This is a form of exception reporting.When actual figures do not equal budgeted figures the difference is known as a variance. Variances can be favourable or adverse. Both adverse and favourable variance must be investigated so that they can be explained.FLEXING THE BUDGETThe budgets discussed so far have been fixed budget. They are based on a best estimate of the future. Usually as the business carries on, things will change. If, for example, production was budgeted at 10,000 units, but an unexpected order arrived which meant that production increased to 12,000 units, it would be necessary to change the budget figures to show this increased activity. This process is known as flexing the budget.QUALITY OF BUDGETSIn order to make sure that the budget is a useful tool it should be prepared carefully. The figures used to estimate costs should be achievable. Some businesses use an ideal budget which in practice is not achievable. If a business is trying to work with a budget which is not achievable staff will be demotivated.Budget holders should be involved in the production of the budget, as they will be able to estimate figures for their particular areas of the business.8: BREAKEVEN ANALYSISTHE BEHAVIOUR OF COSTSCosts in a business behave in different ways as the volume of activity changes. There are three ways that the costs could behave within a range of activity levels:Variable costs – These are costs where the cost varies in proportion to the activity level. For example if a carpentry workshop makes two tables, it will use twice as much wood.Fixed costs – These are costs which do not normally change when levels of activity change. The cost of rental for the carpentry workshop will normally remain the same whether they produce 1 or 100tables.Eventually, if business expanded a lot, the carpentry business may need to expand its operation, and rent another workshop. In this event this fixed cost would become a stepped cost.Semi variable costs – Some costs are a mixture of the two, they have a part of the cost which is fixed and the remainder which is variable. Some mobile phone bills will charge a set amount per month, but will charge more depending on how many calls are made.MARGINAL COSTINGMarginal costing requires us to classify all costs as variable, fixed or semi-variable. As we have seen all businesses must meet their fixed costs, whether or not they produce and sell goods. The selling price of a unit, less its variable costs will contribute towards the fixed costs. His gives us the marginal costing equation:contribution = selling price per unit BREAK-EVEN ANALYSISThe break-even point of a business is when it makes neither a profit nor a loss . This can be calculated by dividing the total fixedcosts of the business, by the contribution per unit, giving the number of unit sales needed to break-even.Multiply the number of units by the selling price to give the break-even point (BEP) in monetary terms.If a target profit is required, then this can be added to fixed costs, and the total divided by the contribution per units to show total sales required in order to achieve the target profit.USES OF BREAK-EVEN ANALYSISBusinesses use break-even analysis when forecasting future levels of activity. This is a useful tool to show the effects of changes in costs, and also changes in selling price. Managers can clearly identify sales levels to achieve predicted profit figuresRent cost (£)R。

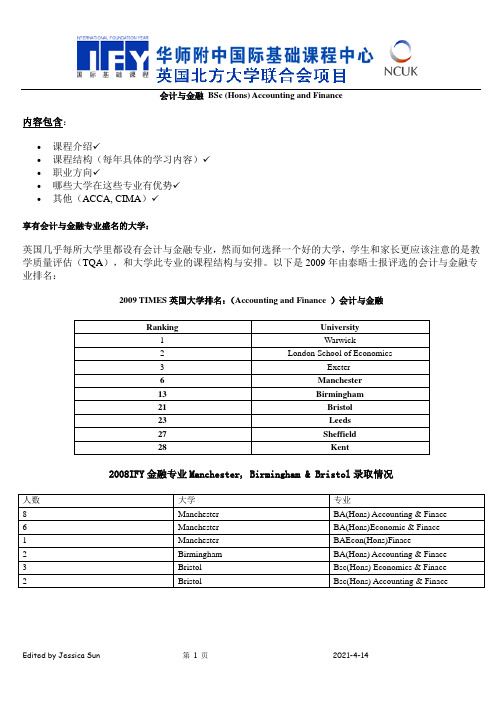

会计与金融 BSc (Hons) Accounting and Finance

Ranking

University

1

Warwick

2

LondonSchoolof Economics

3

Exeter

6

Manchester

13

Birmingham

21

Bristol

23

Leeds

27

Sheffield

2

Birmingham

BA(Hons) Accounting & Finace

3

Bristol

Bsc(Hons) Economics & Finace

2

Bristol

Bsc(Hons) Accounting & Finace

课程介绍与结构(/undergraduate/courses/search/atoz/course/?code=05151):

以下是曼彻斯特大学关于会计金融的课程安排:

Level1第一年(/undergraduate/courses/modules/)

Code(s)课程号码

Course Module Title课程名称

Credits学分

BMAN10501

会计与金融BSc (Hons)Accounting andFinance

内容包含:

课程介绍

课程结构(每年具体的学习内容)

职业方向

哪些大学在这些专业有优势

其他(ACCA,CIMA)

享有会计与金融专业盛名的大学:

英国几乎每所大学里都设有会计与金融专业,然而如何选择一个好的大学,学生和家长更应该注意的是教学质量评估(TQA),和大学此专业的课程结构与安排。以下是2009年由泰晤士报评选的会计与金融专业排名:

英国留学国际金融专业

英国留学国际金融专业英国留学金融专业详解分类及介绍国外关于金融专业的设置,是两方面都有。

一、以微观为主,也就是研究与公司个体有关的投资、融资等行为。

另一方面就是和国内类似的宏观金融的研究。

专业细分英国大学的金融专业按细分不同通常设置在商学院、经济学院或数学学院。

在参考专业排名时需要考虑会计与金融、经济、商学三个方向。

金融专业细分可分为:金融学、公司金融、金融与投资、国际金融、银行与金融、金融与管理、会计与金融、风险管理、房地产金融与投资、金融与经济、金融工程。

金融学:对金融各个细分领域的综合介绍。

下面以曼彻斯特大学为例来看下金融学专业的课程设置:第一学期必修课:Introductory Research Methods for Accounting and Finance; 会计与金融学方法导论Essentials of Finance;金融学精要Derivative Securities衍生证券选修一门:Portfolio Investment证券投资International Macroeconomics and Global Capital Markets国际宏观经济学与全球资本市场Foundations of Finance Theory金融学基础第二学期Financial Econometrics金融计量经济学Advanced Empirical Finance高级实证金融学Corporate Finance; 公司金融选修一门International Finance国际金融Financial Statement Analysis财务报表分析Real Options in Corporate Finance公司金融中的实物期权Mergers and Acquisitions: Economic and Financial Aspects关于企业并购的经济金融思考Dissertation毕业论文公司金融:解决以公司财务、公司融资、公司治理为核心的公司治理结构方面的问题,综合运用各种形式的金融工具与方法,进行风险管理和财富创造。

英文财务管理

3- 7

The Balance sheet is prepared depend by the basic accounting equation: Asset =Liability +Owner’s equity So the amount of total assets is always equal to the total amount of liabilities and owner’s equity. This is the reason why the statement of financial position called a balance sheet.

3- 15

Common Size Balance Sheet

3- 16

Market Value vs. Book Value

Book Values are determined by GAAP Market Values are determined by current values

Generally Accepted Accounting Principles (GAAP) Procedures for preparing financial statements.

McGraw McGraw Hill/Irwin Hill/Irwin

Copyright ©Copyright 2009 by The McGraw-Hill Companies, Inc. All rights reserved © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Accts payable Notes payable Accruals Total CL Long-term debt Common stock Retained earnings Total Equity Total L & E

Unit 1 Finance and Accounting

Unit 1 Finance and AccountingText A Accounting and Accounting ProfessionAccounting is often called the language of business because all organizations set up an accounting information system to communicate data to help people make decisions. It records the past growth or decline of the business. Careful analysis of these results and trends may suggest the ways in which the business may grow in the future. Expansion or reorganization should not be planned without the proper analysis of the accounting information; a new product and the campaign to advertise and sell them should not be launched without the help of accounting expertise(专门技术或知识). Accounting information affects many aspects of our lives. When we earn money, pay taxes, invest savings, budget earnings, and plan for the future, we are influenced by accounting.DISTICNTION BETWEEN BOOKKEEPING(记账)AND ACCOUNTING. Earlier accounting procedures were simple in comparison with modern methods. The simple bookkeeping procedures of a hundred years ago have been replaced in many cases by the data-processing computer. In the past, a bookkeeper kept the books of accounts for an organization. Today, a sharp distinction is made between the relatively unchanged work performed by a bookkeeper and the more sophisticated duties of the accountants. The bookkeeper simply enters data in financial record books; this is just one part of accounting. Accounting also identifies and communicates information on transactions and events, and it includes the crucial processes of analysis and interpretation. Accountants must understand the entire system of records so that they can analyze and interpret business transactions and events. Because interpretation of the figures is such an important part of the accou ntant’s function, accounting has often been described as an art.DIVISIONS OF ACCOUNTING. The field of accounting is divided into three broad divisions: public, governmental, and private.Public accounting. Public accounting is the field of accounting that provides a variety of accounting services to clients for a fee. A professional accountant who works in a public accounting firm usually is a Certified Public Accountant (CPA注册会计师). The British equivalent for a CPA is CA, representing chartered accountants(特许会计师).The scope of services offered by public accounting firms is expending in the information age. Auditing(审计), which is a typical type of assurance services(鉴证服务), is one of the main functions of a CPA firm. Among audit services, the most common is the financial statement audit. Other types of audit services include operational audits(经营审计)and compliance audits(合规审计). Tax preparation and planning is another function of a public accountant. Because tax factors are important to most major financial decisions, CPAs are often asked for advice about the possible tax consequences of a particular decision. Also, CPAs often are asked to prepare income tax returns(所得税申报单). Management advisory services are among the fastest growing practice areas in accounting firms. In addition, many firms are expanding the traditional bounds of services to include such areas as organization design, information processing, employee benefits, and human resource management.Governmental accounting. The management of governmental affairs requires the use of accounting for record keeping, planning, and controlling operations. Many accountants work in government offices or for nonprofit organizations. These two areas are often joined together under the term governmental and institutional accounting(政府和事业单位会计). The two are similarbecause of legal restrictions in the way in which they receive and spend funds. Therefore, a legal background is sometimes necessary for this type of accounting practice. All branches of governments employ accountants. In addition, government-owned corporations have accountants on their staffs. All of these accountants, like those in private industry, work on a salary basis. They tend to become specialists in limited fields like transportation or public utilities(公共事业).Nonprofit organizations are, of course, in business for some purpose other than making money. They include cultural organizations, charitable organizations(慈善组织), religious groups and etc. Although they are limited in the manner in which they can raise and spend their funds, they usually benefit from special provisions in the tax laws.Private accounting. Private accountants, also called management accountants, work for a single business and are responsible for collecting, processing, and reporting financial information. Private accountants are employed in a variety of capacities. For example, the chief accounting officer for a private enterprise typically is known as the controller(会计主任), and the head financial officer is often called the treasurer(财务主任). Others working in accounting departments perform such tasks as determining the cost of items produced by the enterprise, budgeting, internal auditing, taxation, and financial reporting. Like those who work for the government or nonprofit organizations, they are salaried rather than paid a fee. Those who work for manufacturing concerns(制造业)are sometimes called industrial accountant.(763 words)Text B Information UsersAccounting information system serves many kinds of users who can be divided into two groups: external users and internal users.EXTERNAL USERS. Financial accounting is the area of accounting aimed at serving external users by providing them with financial statements(财务报表). These statements are known as general-purpose financial statements(通用财务报表). The term general-purpose refers to the broad range of purposes for which external users rely on these statements.External users of accounting information are not directly involved in running the organization. Almost all of us are users of accounting information. They include shareholders (investors), lenders, directors, customers, suppliers, regulators(监管部门、主管部门), lawyers, brokers, and the press. Each external user has special information needs depending on the types of decisions to be made. External users have limited access to an organization’s information. Yet their business decisions depend on information that is reliable, relevant, and comparable.Present and potential investors. Shareholders are the owners (present investors) of a corporation and the public are the potential investors. They use financial statements and other information about an enterprise to make decisions about increasing (to buy stock), decreasing (to sell stock), or maintaining (to hold stock) their investment in the entity. Shareholders typically elect a board of directors(董事会) to oversee(监督)their interests in an organization. Since directors are responsible to shareholders, their information needs are similar.Creditors(债权人). Creditors or lenders loan money or other resources to an organization. They use the same financial statements to evaluate whether the corporation can repay its debts or obligations. For example, a bank will analyze company’s f inancial statements to determinewhether to make a new loan or to extend a current loan.Government agencies. Government agencies (the regulators) are another major user of financial information about a firm. Regulators often have legal authority over certain activities of organizations. For example, the Internal Revenue Service (IRS美国国内税务署) and other tax authorities require organizations to file accounting reports in computing taxes. Other regulators include utility boards(公用事业管理委员会)that use accounting information to set utility rates (公用事业费收费标准)and securities regulators(证券监管部门)that require reports for companies that sell their stock to the public. In many circumstances, this information is based on the same accounting principles that govern the financial statements presented to investors and creditors. However, it does not necessarily have to be the same, and in some cases there are significant differences. The concepts, standards, and practice of accounting as it relates particularly to government organizations is called governmental accounting.Other external users. Accounting serves the needs of many other external users. For example, employees and labor unions use financial statements to judge the fairness of wages, assess job prospects(前景), and bargain for better wages. The financial information contained in a firm’s financial statements often is used in negotiations. Potential employees may use financial information to evaluate the long-range prospects of the firm before deciding to accept an employment offer. Suppliers use accounting information to judge the soundness of a customer before making sales on credit(赊账), and customers use financial reports to assess the staying power of potential suppliers. V oters, legislators(立法者), and government officials use accounting information to monitor and evaluate government receipts and expenses. Contributors to nonprofit organizations use accounting information to evaluate the use and impact of their donations.INTERNAL USERS. Internal users of accounting information are those directly involved in managing and operating an organization. Company managers are the primary internal users of accounting information. Managers need an information system that will identify problems, such as possible cost overruns(超支)or a department’s inability to implement(实行)a plan properly. The selection and implementation of solutions can occur only after problems have been identified. Accounting information is used to pinpoint(精确定位)problems and to help select appropriate solutions. Managers also use accounting information as they make business decisions. For example, research and development managers need information about projected costs and revenues of any proposed changes in products and services. Purchasing managers need to know what, when, and how much to purchase. Human resource mangers need information about employees’ payroll, benefits, performance, and compensation. Production managers depend on information to monitor costs and ensure quality. Distribution manager need reports for timely, accurate, and efficient delivery of products and services. Marketing managers user reports about sales and costs to target consumers, set prices, and monitor consumer needs, tastes, and price concerns. Service managers require information on the costs and benefits of looking after products and services. Decisions of these and other internal users depend on accounting reports.(745 words)。

会计AF和DF

会计AF和DF

AF是金融与会计专业的简称,即Accounting and Finance。

金融与会计专业是高等院校开设的专业之一,旨在培养金融会计人才。

该专业的培养目标是掌握企业会计信息系统与设计的基本原理、电算化会计软件初始化的设置、总帐系统、报表系统以及工资核算、固定资产核算有关业务核算子系统的操作方法。

金融与会计专业会涉及会计、财政、税收、金融、保险、工商企业管理专业的有关内容。

DF应该是复利现值指数系数。

复利现值系数亦称折现系数或贴现系数,是指按复利法计算利息的条件下,将未来不同时期一个货币单位折算为现时价值的比率。

它直接显示现值同已知复利终值的比例关系,与复利终值系数互为倒数。

进行固定资产投资的时间颇长,项目投产和投资回收的年限更长,因此,在筹划拟建项目,预测其投资经营成本与投产效益时,必须考虑资金的时间价值,确切地测定项目的效益,办法是把项目寿命期内迟早不同时间发生的成本与收益,逐一按折现系数折算成同一时点 (通常选定在开始建设的年份) 上的成本与收益,然后进行指标计算和成本效益分析。

中英文职位对照表-AccountingandFinance(会计与财务部分)

Certified Public Accountant 注册会计师 Senior Accoutant 高级会计

Chief Financial Officer 首席财务官 Audit Manager 审计经理

Vice-President of Finance 财务副总裁 Financial Consultant 财务顾问

Loan Servicer 贷款服务 Financial Manager 财务经理

Financial Planner 财务计划员 Bank Clerk 银行出纳

Management A文员

Mortgage Underwriter 抵抻保险员 Billing Supervisor 票据管理员

Payroll Manager 工资经理 Bookkeeper 档案管理

Staff Auditor 审计员 Bookkeeping Clerk 档案管理助理

Stock Broker 股票经纪人 Budget Analyst 预算分析

Tax Accountant 税务会计 Credit Analyst 信用分析

Tax Inspector 税务检查员 Credit Manager 信用管理经理

Vice-President of Administration and Finance 财务行政副总裁 Financial Analyst 财务分析

下载word文档到电脑方便收藏和打印全文共913字

Accounting and Finance(会计与财务部分)

Accounting Payable Clerk 应付帐款文员 Accounting Assistant 会计助理

英国巴斯大学金融类硕士专业解析

英国巴斯大学金融类硕士专业解析学校名称:英国巴斯大学 University of Bath所在位置:英国学费:9000-28000英镑/学年录取率:0.28英国巴斯大学是不错的大学,很多人会选择去巴斯大学留学,那么去巴斯大学学习金融专业到底怎么样呢?跟着来看看吧!欢迎阅读。

英国巴斯大学金融类硕士专业解析金融专业一直是留学生关注度最高的黄金专业,巴斯大学头4个金融方向的专业。

分别是MSc in Accounting and Finance会计与金融硕士、MSc in Finance金融硕士、MSc in Finance with Banking 金融银行硕士和MSc in Finance with Risk Management金融风险管理硕士。

课程设置Bath的金融硕士专业十分抢手,录取标准也是很高的。

总结以往申请的经验,虽然对商科专业不作要求,但需要均分达到85分以上,对数学的要求也比较高,跨专业(特别是文科生)的学生需要提供学过高数课程的证明。

对语言的要求并不是很高,IETLS达到6.5单项不低于6.0就可以了。

虽然录取条件中对数学的要求比较高,但专业课程还是比较常规,只是选修中的一些课程要求较高的数学能力,总体来说学习的难度不是很大。

专业申请截止日期一般在6月尾,需要缴纳60胖子的报名费。

Bath的金融硕士课程同样是开展为期12个月全日制课程,分为2个学期和论文期,并由核心课程和选修课程组成。

需要讲授的课程都将在前2个学期完成,而论文则需要在夏季那几个月完成。

每节理论课程学分为6分,理论课共60个学分,而论文共30个学分。

学院为留学生提供十个价值3,000英镑的奖学金,童鞋们要加油了。

毕业生未来可进入四大会计师事务所工作,起薪比较高,而随着职位的提升薪水还会大幅增加。

而已拿到国际认可证书的毕业生未来可进入银行、投资公司、投资银行、保险公司等工作。

MSc in Accounting and Finance会计与金融硕士第一学期必修课(4门)Econometrics for Economics and FinanceTheory of Financial Decision MakingFinancial Accounting 1Management Accounting 1选修课(1门)BankingInvestment ManagementCorporate Governance第二学期必修课(4门)Financial EconometricsCorporate FinanceFinancial Accounting 2Management Accounting 2选修课(1门)International FinanceFinancial Statement Analysis论文完成一篇9,00012,000字数的论文MSc in Finance金融硕士第一学期必修课(3门)Econometrics for Economics and FinanceTheory of Financial Decision-MakingInvestment Management选修课(2门)BankingCorporate GovernanceIntroduction to Quantitative Finance第二学期必修课(3门)Corporate FinanceInternational FinanceFinancial Econometrics选修课(2门)Risk ManagementFinancial EngineeringFinancial Statement Analysis Contemporary Finance Issues论文完成一篇9,00012,000字数的论文MSc in Finance with Banking金融银行硕士第一学期必修课(3门)Econometrics for Economics and Finance Theory of Financial Decision Making Banking选修课(2门)Financial DerivativesInvestment Management Introduction to Quantitative Finance Corporate Governance第二学期必修课(3门)Financial EconometricsCorporate Finance选修课(2门)International FinanceRisk ManagementFinancial Statement AnalysisContemporary Finance Issues论文完成一篇9,00012,000字数的论文MSc in Finance with Risk Management金融风险管理硕士第一学期必修课(3门)Econometrics for Economics and FinanceTheory of Financial Decision-MakingIntroduction to Quantitative Finance选修课(2门)Financial DerivativesInvestment ManagementBankingCorporate Governance第二学期必修课(3门)Financial EconometricsCorporate FinanceRisk Management选修课(2门)Financial EngineeringInternational FinanceFinancial Statement AnalysisContemporary Finance Issues论文完成一篇9,00012,000字数的论文从上面四个金融课程中不难发现,课程设置都偏向数理计量等方向,对数学要求比较高,本科数学成绩不好的确实很容易杯具。

accounting and finance专业介绍-概述说明以及解释

accounting and finance专业介绍-概述说明以及解释1.引言1.1 概述概述部分的内容可以包括对accounting and finance专业的定义和简要介绍。

可以着重强调该专业的重要性和它在商业领域中的作用。

概述:accounting and finance是一门研究财务管理和会计原理的学科,其目的是培养学生具备在财务和会计领域工作所需的技能和知识。

这个领域的专业人士负责管理和监督组织的财务活动,确保其财务健康并为未来的决策提供有关财务数据和信息。

会计和财务专业具有深远的影响力,无论是在商业机构还是在非营利组织。

它们为决策制定者提供了必要的财务信息,以便他们能够作出明智的决策,规划战略并管理资源。

通过学习会计和财务知识,学生将掌握财务报告、预算编制、投资决策和风险管理等方面的技能。

在现代商业环境中,会计和财务专业人士扮演着关键的角色。

他们需要具备分析能力、问题解决能力和沟通能力,以便能够理解和解释复杂的财务数据,并为管理者和其他利益相关者提供准确的报告和建议。

因此,accounting and finance专业对于那些想要在商业领域取得成功的学生来说是非常有吸引力的选择。

无论是在投资银行、会计师事务所、企业财务部门还是其他金融机构,这个专业都提供了广阔的就业机会和职业发展空间。

在接下来的章节中,我们将更详细地介绍会计专业和财务专业,以便更全面地了解这两个领域的特点和要求。

1.2 文章结构文章结构部分的内容可以描述整篇文章的组织结构和各个章节的主要内容。

可以按照以下方式编写:在本文中,将介绍accounting and finance专业的相关知识和领域。

文章主要分为引言、正文和结论三个部分。

引言部分将为读者提供一个概述,简单介绍accounting and finance 专业的背景和重要性。

同时,还会阐述本文的目的,为读者提供一个清晰的阅读指南。

正文部分将详细介绍会计专业和财务专业。

财会中英文职位对照表

中英文职位对照_Accounting and Finance(会计与财务部分)Accounting Payable Clerk应付帐款文员Accounting Assistant会计助理Assistant Portfolio Manager组合基金经理助理Accounting Manager会计经理Accounts Receivable Clerk应收帐款文员Accounting Clerk会计文员Certified Public Accountant注册会计师Senior Accoutant高级会计Chief Financial Officer首席财务官Audit Manager审计经理Collections Officer收款负责人Actuarial Anaylst保险分析员Insurance Underwriter 保险承销商Auditor审计师Bank Administrator银行事务管理员Junior Accountant 初级会计Loan Administrator贷款管理员Bank Treasurer资金调拨Management Accountant管理会计Billing Clerk票据文员Mortgage Underwriter抵抻保险员Billing Supervisor票据管理员Payroll Manager工资经理Bookkeeper档案管理Staff Auditor审计员Bookkeeping Clerk档案管理助理Stock Broker股票经纪人Budget Analyst预算分析Tax Accountant税务会计Credit Analyst信用分析Tax Inspector 税务检查员Credit Manager信用管理经理Vice-President of Administration and Finance财务行政副总裁Financial Analyst财务分析Vice-President of Finance 财务副总裁Financial Consultant财务顾问Loan Servicer贷款服务Financial Manager 财务经理Financial Planner财务计划员Bank Clerk银行出纳Human Resources(人力资源部分)Assistant Personnel Officer人事助理Benefits Coordinator员工福利协调员Assistant Vice-President of Human Resources 人力资源副总裁助理Compensation Manager 薪酬经理Director of Human Resources 人力资源总监Employment Consultant招募顾问Employer Relations Representative员工关系代表Facility Manager后勤经理Job Placement Officer人员配置专员Personnel Consultant员工顾问Labor Relations Specialist劳动关系专员Personnel Manager职员经理Training Coordinator培训协调员Recruiter招聘人员Vice-President of Human Resources 人力资源副总裁Training Specialist培训专员Administration(行政部分)Administrative Director行政主管File Clerk档案管理员Executive Assistant行政助理Office Manager办公室经理Executive Secretary行政秘书Receptionist接待员General Office Clerk办公室文员Secretary秘书Inventory Control Analyst存货控制分析Staff Assistant助理Mail Room Supervisor信件中心管理员Stenographer速记员Order Entry Clerk订单输入文员Telephone Operator电话操作员Shipping/Receiving Expediter收发督导员Ticket Agent票务代理Vice-President of Administration行政副总裁Typist打字员中英文职位对照。

发表accounting and finance

发表accounting and finance全文共四篇示例,供读者参考第一篇示例:财务与会计学是现代商业社会中不可或缺的重要学科,它们通过对财务数据进行分析和解释,帮助企业制定决策、评估绩效和规划未来。

在当今全球化和数字化的经济环境下,在财务与会计领域取得成功变得越来越具有挑战性和重要性。

财务与会计是紧密相关的两个学科,它们在企业管理中起着至关重要的作用。

财务是指企业运作中涉及现金流量的一切方面,包括筹措资金、投资、运营和风险管理等。

而会计是负责记录和报告企业财务活动的学科,它为决策者提供了有关企业财务状况和绩效的信息。

财务和会计的结合为企业提供了一个全面的财务管理框架,帮助企业做出明智的财务决策。

在当今竞争激烈的商业环境中,企业面临着种种挑战,如全球化竞争、技术革新、市场波动等。

在这些复杂的环境中,正确的财务与会计战略显得尤为重要。

通过高效的财务管理,企业可以优化资源利用,提高效率和生产力,实现盈利最大化。

准确的会计信息也可以帮助企业了解自身的财务状况,及时发现问题和改进不足之处。

对于个人而言,了解财务与会计知识也是非常重要的。

无论是作为企业管理者、投资者还是普通消费者,都需要具备一定的财务与会计知识来做出明智的决策。

作为企业管理者,了解财务数据可以帮助他们更好地制定战略和控制成本;而作为投资者,了解公司的财务报表可以帮助他们评估投资风险和回报;作为普通消费者,了解自己的财务状况可以帮助他们做出理性的消费决策。

财务与会计学不仅在商业领域中发挥重要作用,同时也对社会发展具有深远影响。

通过财务与会计信息的准确记录和披露,可以有效监督企业的经营活动,防止欺诈行为的发生,保护投资者和消费者的利益。

透明的财务信息也有助于政府和监管机构更好地监管和规范市场,维护金融秩序和社会稳定。

在未来,随着经济全球化和数字化的加速发展,财务与会计学将面临更多挑战和机遇。

新兴技术如人工智能、大数据、区块链等的应用将改变财务与会计领域的传统模式,为企业提供更高效、准确和安全的财务管理工具。

应聘职位名称 —— Accounting and Finance(会计与财务部分)

应聘职位名称—— Accounting and Finance(会计与财务部分) Accounting Assistant 会计助理Accounting Clerk 会计文员Accounting Manager 会计经理Accounting Payable Clerk 应付帐款文员Accounts Receivable Clerk 应收帐款文员Actuarial Anaylst 保险分析员Assistant Portfolio Manager 组合基金经理助理Audit Manager 审计经理Auditor 审计师Bank Administrator 银行事务管理员Bank Clerk 银行出纳Bank Treasurer 资金调拨Billing Clerk 票据文员Billing Supervisor 票据管理员Bookkeeper 档案管理Bookkeeping Clerk 档案管理助理Budget Analyst 预算分析Certified Public Accountant 注册会计师Chief Financial Officer 首席财务官Collections Officer 收款负责人 Credit Analyst 信用分析Credit Manager 信用管理经理Financial Analyst 财务分析Financial Consultant 财务顾问Financial Manager 财务经理Financial Planner 财务计划员Insurance Underwriter 保险承销商Junior Accountant 初级会计Loan Administrator 贷款管理员Loan Servicer 贷款服务Management Accountant 管理会计Mortgage Underwriter 抵抻保险员Payroll Manager 工资经理Senior Accoutant 高级会计Staff Auditor 审计员Stock Broker 股票经纪人Tax Accountant 税务会计Tax Inspector 税务检查员Vice-President of Finance 财务副总裁Vice-President of Administration and Finance 财务行政副总裁。

SSCI检索国际顶级商业金融期刊

SOCIAL SCIENCES CITATION INDEX—BUSINESS, FINANCE–JOURNAL LISTSSCI检索的商业金融类,一共84篇,加下划线的为著名的期刊1.ABACUS-A JOURNAL OF ACCOUNTING FINANCE AND BUSINESS STUDIES2.ACCOUNTING AND BUSINESS RESEARCH3.ACCOUNTING AND FINANCE4.ACCOUNTING HORIZONS5.ACCOUNTING ORGANIZATIONS AND SOCIETY英国会计学会发行的会计学术期刊,简称AOS,通常与AR、JAR、JAE、CAR并称为会计五大期刊。

AOS偏好刊登field study类型的研究文章,且内容常常饶富哲学意涵(会计学顶级)6.ACCOUNTING REVIEW美国会计学会(AAA)发行的会计学术期刊,为会计三大期刊之一,简称AR(会计学顶级)-PACIFIC JOURNAL OF ACCOUNTING & ECONOMICS-PACIFIC JOURNAL OF FINANCIAL STUDIES9.AUDITING-A JOURNAL OF PRACTICE & THEORYAAA发行的会计学术期刊(AAA审计部门的section journal),专门刊登以审计相关议题为探讨主题的研究文章(会计学优良)10.AUSTRALIAN ACCOUNTING REVIEW11.CONTEMPORARY ACCOUNTING RESEARCH加拿大会计学会发行的会计学术期刊,已与三大期刊并列first-tier之列,简称CAR (会计学顶级)12.EMERGING MARKETS REVIEW13.EUROPEAN ACCOUNTING REVIEW14.EUROPEAN FINANCIAL MANAGEMENT15.EUROPEAN JOURNAL OF FINANCE16.FEDERAL RESERVE BANK OF ST LOUIS REVIEW17.FINANCE A UVER-CZECH JOURNAL OF ECONOMICS AND FINANCE18.FINANCE AND STOCHASTICS19.FINANCE RESEARCH LETTERS20.FINANCIAL ANALYSTS JOURNAL21.FINANCIAL MANAGEMENT22.FINANZARCHIV23.FISCAL STUDIES24.FORBES25.GENEVA PAPERS ON RISK AND INSURANCE-ISSUES AND PRACTICE26.GENEVA RISK AND INSURANCE REVIEW27.IKTISAT ISLETME VE FINANS28.IMF ECONOMIC REVIEW29.INTERNATIONAL FINANCE30.INTERNATIONAL INSOLVENCY REVIEW31.INTERNATIONAL JOURNAL OF CENTRAL BANKING32.INTERNATIONAL JOURNAL OF FINANCE & ECONOMICS33.INTERNATIONAL JOURNAL OF HEALTH CARE FINANCE & ECONOMICS34.INTERNATIONAL REVIEW OF ECONOMICS & FINANCE35.INVESTMENT ANALYSTS JOURNAL36.JASSA-THE FINSIA JOURNAL OF APPLIED FINANCE37.JOURNAL OF ACCOUNTING & ECONOMICSRochester大学发行的会计学术期刊,为会计三大期刊之一,简称JAE(会计学顶级)38.JOURNAL OF ACCOUNTING AND PUBLIC POLICY39.JOURNAL OF ACCOUNTING RESEARCH (1.1)芝加哥大学发行的会计学术期刊,为会计三大期刊之一,简称JAR(会计学顶级)40.JOURNAL OF BANKING & FINANCE41.JOURNAL OF BEHAVIORAL FINANCE42.JOURNAL OF BUSINESS FINANCE & ACCOUNTINGBlackwell发行的财务及会计学术期刊,2005年列入SSCI(会计学不错)43.JOURNAL OF COMPUTATIONAL FINANCE44.JOURNAL OF CORPORATE FINANCE45.JOURNAL OF CREDIT RISK46.JOURNAL OF DERIVATIVES47.JOURNAL OF EMPIRICAL FINANCE48.JOURNAL OF FINANCE (2.8)(金融学最顶级)49.JOURNAL OF FINANCIAL AND QUANTITATIVE ANALYSIS50.JOURNAL OF FINANCIAL ECONOMETRICS51.JOURNAL OF FINANCIAL ECONOMICS (1.9)(金融学最顶级)52.JOURNAL OF FINANCIAL INTERMEDIATION53.JOURNAL OF FINANCIAL MARKETS54.JOURNAL OF FINANCIAL SERVICES RESEARCH55.JOURNAL OF FINANCIAL STABILITY56.JOURNAL OF FUTURES MARKETS57.JOURNAL OF INDUSTRIAL ECONOMICS58.JOURNAL OF INTERNATIONAL FINANCIAL MANAGEMENT &ACCOUNTING59.JOURNAL OF INTERNATIONAL MONEY AND FINANCE60.JOURNAL OF MONETARY ECONOMICS61.JOURNAL OF MONEY CREDIT AND BANKING62.JOURNAL OF OPERATIONAL RISK63.JOURNAL OF PENSION ECONOMICS & FINANCE64.JOURNAL OF PORTFOLIO MANAGEMENT65.JOURNAL OF REAL ESTATE FINANCE AND ECONOMICS66.JOURNAL OF REAL ESTATE RESEARCH67.JOURNAL OF RISK68.JOURNAL OF RISK AND INSURANCE69.JOURNAL OF RISK AND UNCERTAINTY70.JOURNAL OF RISK MODEL VALIDATION71.MANAGEMENT ACCOUNTING RESEARCH72.MATHEMATICAL FINANCE73.NATIONAL TAX JOURNAL全美租税学会(NT A)发行的租税学术期刊,专门刊登以政府财政相关议题为探讨主题的研究文章(会计学不错)74.NORTH AMERICAN JOURNAL OF ECONOMICS AND FINANCE75.PACIFIC-BASIN FINANCE JOURNAL76.QUANTITATIVE FINANCE77.REAL ESTATE ECONOMICS78.REVIEW OF ACCOUNTING STUDIES由南加大发行的新兴会计学术期刊(公元1996年创刊),以刊登分析性及实验的研究文章为主,已被认可为first-tier之列(会计学顶级)79.REVIEW OF DERIVATIVES RESEARCH80.REVIEW OF FINANCE81.REVIEW OF FINANCIAL STUDIES (1.3)(金融学最顶级)82.REVISTA ESPANOLA DE FINANCIACION Y CONTABILIDAD-SPANISHJOURNAL OF FINANCEAND ACCOUNTING83.WORLD BANK ECONOMIC REVIEW84.WORLD ECONOMY。

顶级英文期刊-会计方面的杂志

顶级英文期刊-会计方面的杂志一,国际公认的最顶尖(first-tier)的6本会计学术期刊(搜索看,至今中国大陆只有1人(上海财大教授)以第2作者发过文章)1,Accounting Review (SSCI检索):美国会计学会(AAA)发行的会计学术期刊,为会计三大期刊之一,简称AR。

会计评论2,Journal of Accounting Research (SSCI):芝加哥大学发行的会计学术期刊,为会计三大期刊之一,简称JAR。

会计研究3,Journal of Accounting and Economics (SSCI):Rochester 大学发行的会计学术期刊,为会计三大期刊之一,简称JAE。

会计与经济学杂志4,Contemporary Accounting Research(SSCI):加拿大会计学会发行的会计学术期刊,已与三大期刊并列first-tier之列,简称CAR。

当代会计研究5,Accounting, Organization, and Society (SSCI):英国会计学会发行的会计学术期刊,简称AOS,通常与AR、JAR、JAE、CAR并称为会计五大期刊。

AOS偏好刊登field study类型的研究文章,且内容常常饶富哲学意涵。

6,Review of Accounting Studies(SSCI):由南加大发行的新兴会计学术期刊(公元1996年创刊),以刊登分析性及实验的研究文章为主,已被认可为first-tier之列。

二,优良(second-tier)的会计期刊Auding: A Journal of Practice and Theory (SSCI):AAA发行的会计学术期刊(AAA审计部门的section journal),专门刊登以审计相关议题为探讨主题的研究文章。

Journal of Management Accounting Research:AAA发行的会计学术期刊(AAA管理会计部门的section journal),专门刊登以管理会计相关议题为探讨主题的研究文章,简称JMAR。

英国finance专业

/prospectus/pg/courses/dept/ec/baf/index.htm

MSc International Banking

/prospectus/pg/courses/dept/ec/ib/index.htm

MSc Finance and Management

/prospectus/pg/courses/dept/bs/fam/index.htm

MA Money, Banking and Finance

/prospectus/pg/courses/dept/ec/bfm/index.htm

/Study/courses/taught/mscbusinessfinance.aspx

MSc International Finance and Economics Development

/Study/courses/taught/mscinternationafinanceandecodevelop.aspx

雅思7,写作7

MSc Finance and Business Economics

50英镑申请费

MSc Finance and Economics

MSc Finance

MSc Mathematical Finance

雅思6.5,各单项不低于5

MSc Financial Engineering

MSc Risk Management

MSc in Quantitative Finance

/masters/courses/mscqf/index.html

MSc in Mathematical Trading and Finance

不需要GMAT

/masters/courses/mscmtf/index.html

PERSONALS TEMEN ccountingand Finance申请会计金融专业个人陈述

PERSONAL STATEMENTI would like to apply for the taught master degree programme about Accounting and Finance in your university. Having been studying Business Administration in xx College and International Business and Finance in xx University, which is one of the most famous business schools in China, I deeply realize the trend of economic globalization and the huge demand of talents in the field of accounting and finance in China. I also find myself quite obsessed with this subject and believe that admission into one of the best universities overseas will stimulate more reflects on financial convergence and divergence on a global basis.Looking back on my academic journey, I feel very confident in dealing with the complex nature of different subjects. At first, I chose Business as my major, but after engaging in Accounting and Finance, I became more interested in it instead, especially Financial System and Auditing, Business Decision Making, and managing Financial Resources and Decisions. I often spend time collecting financial information, trying to analyze some hot topics using the knowledge I have learnt. Comparing my analysis with the professional one is a good way to find out my weakness. My creativity and passion to Accounting and Finance is inspired. Learning to think and doubt about theories rather than directly believe or remember theories is the most important thing that these experts show to me.In addition to my academic diligence, I took every opportunity to put the theory into practice. I have taken an internship as a cashier in a big supermarket for2 months. My responsibility was to check whether the sales slip was correct. If it was correct, I would stamp it and input information in computer. In order to avoid mistakes, I and my colleagues worked hard and carefully and reminded each other. The job responsibility was simple, but it required us to be careful, honest and kind. Through this experience, I understood the importance of responsibility and team spirit, which would be very beneficial to my future life and career.In my opinion, English is very essential for students who want to go abroad and engage in Business field. From my sophomore year, all my courses were taught in English and most of teachers were foreigners. In the spare time, I often communicated with my foreign teachers and watched many English dramas and listened to English songs. Now I have handled the fundamental English skills and can make it no gap in communicating with others in many situations.Chinese financial institutions and companies nowadays are viewing their business from international perspective and need elites who are not only knowing the reality of China, but also armed with professional knowledge which can be applied to the international market. I am very interested in turning complex ideas to simple one, which can give me a sense of achievement. I always collect a lot of information and then summarize it to know the tendency and meaning of many affairs. After extensive research, I know the postgraduate programme in your university perfectly fit into my choice. Firstly, that many of your courses fall within the scope of my interests serves as an overwhelming reason. Moreover, your internationalreputation in planning education, the nourishing academic atmosphere, as well as the perfect combination of various cultures all attract me. I believe your programme will greatly enhance my grasp of theoretical frameworks and improve my research abilities towards fulfill my professional objectives. I sincerely hope that you can offer me with this precious opportunity.。

msc accounting and finance的理解

msc accounting and finance的理解

MSc Accounting and Finance是一个硕士学位课程,旨在为学

生提供深入的会计和金融知识,以培养他们在这两个领域中的专业能力和技能。

该课程涵盖了财务会计、管理会计、金融管理、投资决策、企业财务等方面的内容。

通过MSc Accounting and Finance课程,学生可以学习财务报告、预算编制、成本计算、绩效管理等会计方面的知识。

同时,他们也将了解投资组合管理、公司估值、风险管理、资本市场等金融领域的重要概念和技能。

该课程的目标是培养学生成为在会计和金融领域具备高级专业知识和技能的专业人士。

学生毕业后可以在金融机构、会计公司、投资银行、咨询公司等各种组织中从事高级财务分析、风险管理、投资决策等工作。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Ledger

Laptop £ Cash 500 Laptop Cash £ 500

Ledger accounts are often referred to as T accounts In the above transaction a laptop has been bought costing £500.

Accounting equation

Capital represents the value of resources introduced into the business by an owner plus profits retained in the business less drawings. Accounting equation is: Assets less liabilities = Capital, or Capital plus liabilities = Assets

Items owned by a business Items owed by a business Monies owed by individuals or businesses to whom goods or services have been supplied Monies owed to individuals or businesses from whom goods or services have been bought Goods bought for resale The amount of the owner’s stake in the business

The initial recording of financial transactions is generally referred to as bookkeeping Every financial transaction results in there being two entries made in the accounting records One entry is a DEBIT – on the left hand side One entry is a CREDIT – on the right hand side The debit entry and credit entry will be for exactly the same amount

Daybooks

Recording of accounting transactions in day books (books of prime entry)

Transfer of information from day books to ledger accounts

Ledger accounts

Double entry bookkeeping

DEBIT Increase in asset account Increase in expense account Decrease in liability account Decrease in income (revenue) account Increase in drawings account

Source documents

Sales invoices Purchase invoices Credit notes Cash receipts Till rolls Cheque stubs Bank paying-in slip counterfoils Bank statements

Daybooks

Sales day book Purchase day book Sales returns day book Purchase returns day book Cash book General journals

Double entry bookkeeping

Accounting terminology – an introduction cont.

Sales Purchases Credit (sales or purchases) Expenses Drawings

The value of sales of goods or services by a business The value of goods or services bought by a business Sales or purchases to be settled at some future agreed date Costs incurred in the operation of a business Cash or goods taken from the business by the owner for personal use

CREDIT Decrease in asset account Decrease in expense account Increase in liability account Increase in income account Increase in capital account

Ledger accounts

DEBIT

CREDIT

Expenses Assets Drawings DEAD

Liabilities Income Capital CLIC

Financial accounting process

Source documents

Processing of source documents

Accounting terminology – an introduction

Assets Liabilities Trade debtors or Accounts receivable

Trade creditors or Accounts payable Inventory or stock Capital

What is Accounting?

“The language of business” The recording of business transactions in financial terms The collection and classification of business transactions in such ways as meaningful information can be derived about the business

Financial accounting process cont.

Ledger accounts

Trialaccounts

Extraction of balances from ledger accounts to trial balance to check their accuracy Production of income statement (trading and profit and loss account), and a balance sheet

Accounting and Finance

The principles of Accounting covered by the course will apply to all types of business BUT the course will focus on how to produce the accounts for Sole Trader businesses

Why are accounts produced?

To quantify items such as sales, purchases and expenses To establish the profitability and financial position of the business To enable the owner of the business to understand the financial performance of the business To enable the owner to make decisions for the future

Accounting and Finance

Introduction to Accounting

Lecture 1

What is Accounting? Accounting terminology Why are accounts produced? Source documents Daybooks Double entry bookkeeping Ledger accounts Financial accounting process Accounting equation