会计专业基础英语

财务英语会计必背知识点

财务英语会计必背知识点是会计领域最为重要的一种语言。

对于从事财务工作的人员来说,掌握是必不可少的。

下面将介绍一些中必须要掌握的会计知识点。

一、会计基础知识1. 资产 (Assets):公司所拥有的有价值的资源或权益。

2. 负债 (Liabilities):公司对外部债权人所承诺的经济利益的义务。

3. 所有者权益 (Owner's Equity):指公司股东对公司和其资产净值所享有的权益。

4. 收入 (Revenue):公司在正常经营过程中获得的经济利益。

5. 费用 (Expense):公司在正常经营过程中为获取收入所发生的成本或支出。

6. 利润 (Profit):收入减去费用后的净收益。

7. 账户 (Account):用来记录公司的交易和财务状况的记录单元。

8. 会计方程 (Accounting Equation):资产=负债+所有者权益,表示了会计事务的基本平衡关系。

二、会计报表1. 资产负债表 (Balance Sheet):展示了公司在特定日期的负债、资产和所有者权益。

2. 利润表 (Income Statement):展示了特定时间段内公司的收入和费用,计算出利润。

3. 现金流量表 (Cash Flow Statement):展示了公司特定时间段内现金流动的情况,包括现金的来源和使用。

4. 所有者权益变动表 (Statement of Changes in Owner's Equity):展示了特定时间段内公司的所有者权益的变动情况。

三、会计分录和账务处理1. 会计分录 (Accounting Entry):用于记录每笔会计事务的方法,包括借方和贷方。

2. 借方 (Debit):用于记录增加资产、费用和减少负债、所有者权益的金额。

3. 贷方 (Credit):用于记录减少资产、费用和增加负债、所有者权益的金额。

4. 借贷平衡 (Debit-Credit Balance):每笔会计分录中借方金额必须等于贷方金额,以保持会计方程的平衡。

625个财务会计专业常用英语单词汇总

625个财务会计专业常用英语单词汇总基本词汇A (1)account 账户,报表A (2)accounting postulate 会计假设A (3)accounting valuation 会计计价A (4)accountability concept 经营责任概念A (5)accountancy 会计职业A (6)accountant 会计师A (7)accounting 会计A (8)agency cost 代理成本A (9)accounting bases 会计基础A (10)accounting manual 会计手册A (11)accounting period 会计期间A (12)accounting policies 会计方针A (13)accounting rate of return 会计报酬率A (14)accounting reference date 会计参照日A (15)accounting reference period 会计参照期间A (16)accrual concept 应计概念A (17)accrual expenses 应计费用A (18)acid test ratio 速动比率(酸性测试比率)A (19)acquisition 收购A (20)acquisition accounting 收购会计A (21)adjusting events 调整事项A (22)administrative expenses 行政管理费A (23)amortization 摊销A (24)analytical review 分析性复核A (25)annual equivalent cost 年度等量成本法A (26)annual report and accounts 年度报告和报表A (27)appraisal cost 检验成本A (28)appropriation account 盈余分配账户A (29)articles of association 公司章程细则A (30)assets 资产A (31)assets cover 资产担保A (32)asset value per share 每股资产价值A (33)associated company 联营公司A (34)attainable standard 可达标准A (35)attributable profit 可归属利润A (36)audit 审计A (37)audit report 审计报告A (38)auditing standards 审计准则A (39)authorized share capital 额定股本A (40)available hours 可用小时A (41)avoidable costs 可避免成本B (42)back-to-back loan 易币贷款B (43)backflush accounting 倒退成本计算B (44)bad debts 坏帐B (45)bad debts ratio 坏帐比率B (46)bank charges 银行手续费B (47)bank overdraft 银行透支B (48)bank reconciliation 银行存款调节表B (49)bank statement 银行对账单B (50)bankruptcy 破产B (51)basis of apportionment 分摊基础B (52)batch 批量B (53)batch costing 分批成本计算B (54)beta factor B (市场)风险因素BB (55)bill 账单B (56)bill of exchange 汇票B (57)bill of lading 提单B (58)bill of materials 用料预计单B (59)bill payable 应付票据B (60)bill receivable 应收票据B (61)bin card 存货记录卡B (62)bonus 红利B (63)book-keeping 薄记B (64)Boston classification 波士顿分类B (65)breakeven chart 保本图B (66)breakeven point 保本点B (67)breaking-down time 复位时间B (68)budget 预算B (69)budget center 预算中心B (70)budget cost allowance 预算成本折让B (71)budget manual 预算手册B (72)budget period 预算期间B (73)budgetary control 预算控制B (74)budgeted capacity 预算生产能力B (75)business center 经营中心B (76)business entity 营业个体B (77)business unit 经营单位B (78)by-product 副产品C (79)called-up share capital 催缴股本C (80)capacity 生产能力C (81)capacity ratios 生产能力比率C (82)capital 资本C (83)capital assets pricing model 资本资产计价模式C (84)capital commitment 承诺资本C (85)capital employed 已运用的资本C (86)capital expenditure 资本支出C (87)capital expenditure authorization 资本支出核准C (88)capital expenditure control 资本支出控制C (89)capital expenditure proposal 资本支出申请C (90)capital funding planning 资本基金筹集计划C (91)capital gain 资本收益C (92)capital investment appraisal 资本投资评估C (93)capital maintenance 资本保全C (94)capital resource planning 资本资源计划C (95)capital surplus 资本盈余C (96)capital turnover 资本周转率C (97)card 记录卡C (98)cash 现金C (99)cash account 现金账户C (100)cash book 现金账薄C (101)cash cow 金牛产品C (102)cash flow 现金流量C (103)cash flow budget 现金流量预算C (104)cash flow statement 现金流量表C (105)cash ledger 现金分类账C (106)cash limit 现金限额C (107)CCA 现时成本会计C (108)center 中心C (109)changeover time 变更时间C (110)chartered entity 特许经济个体C (111)cheque 支票C (112)cheque register 支票登记薄C (113)classification 分类C (114)clock card 工时卡C (115)code 代码C (116)commitment accounting 承诺确认会计C (117)common cost 共同成本C (118)company limited by guarantee 有限担保责任公司C (119)company limited by shares 股份有限公司C (120)competitive position 竞争能力状况C (121)concept 概念C (122)conglomerate 跨行业企业C (123)consistency concept 一致性概念C (124)consolidated accounts 合并报表C (125)consolidation accounting 合并会计C (126)consortium 财团C (127)contingency plan 应急计划C (128)contingent liabilities 或有负债C (129)continuous operation 连续生产C (130)contra 抵消C (131)contract cost 合同成本C (132)contract costing 合同成本计算C (133)contribution centre 贡献中心C (134)contribution chart 贡献图C (135)control 控制C (136)control account 控制账户C (137)control limits 控制限度C (138)controllability concept 可控制概念C (139)controllable cost 可控制成本C (140)conversion cost 加工成本C (141)convertible loan stock 可转换为股票的贷款C (142)corporate appraisal 公司评估C (143)corporate planning 公司计划C (144)corporate social reporting 公司社会报告C (145)cost 成本C (146)cost account 成本账户C (147)cost accounting 成本会计C (148)cost accounting manual 成本手册C (149)cost adjustment 成本调整C (150)cost allocation 成本分配C (151)cost apportionment 成本分摊C (152)cost attribution 成本归属C (153)cost audit 成本审计C (154)cost benefit analysis 成本效益分析C (155)cost center 成本中心C (156)cost driver 成本动因C (157)cost of capital 资本成本C (158)cost of goods sold 销货成本C (159)cost of non-conformance 非相符成本C (160)cost of sales 销售成本C (161)cost reduction 成本降低C (162)cost structure 成本结构C (163)cost unit 成本单位C (164)cost-volume-profit analysis(CVP) 本量利分析C (165)costing 成本计算C (166)credit note 贷项通知C (167)credit report 信贷报告书C (168)creditor 债权人C (169)creditor days ratio 应付账款天数率C (170)creditors ledger 应付账款分类账C (171)critical event 关键事项C (172)critical path 关键路线C (173)cumulative preference shares 累积优先股C (174)current asset 流动资产C (175)current cost accounting 现时成本会计C (176)current liabilities 流动负债C (177)current purchasing power accounting 现时购买力会计C (178)current ratio 流动比率C (179)cut-off 截止C (180)CVP 本量利分析C (181)cycle time 周转时间D (182)debenture 债券D (183)debit note 借项通知D (184)debit capacity 举债能力D (185)debt ratio 债务比率D (186)debtor 债务人;应收账款D (187)debtor days ratio 应收账款天数率D (188)debtors ledger 应收账款分类账D (189)debtor' age analysis 应收账款账龄分析D (190)decision driven costs 决策连动成本D (191)decision tree 决策树D (192)defects 次品D (193)deferred expenditure 递延支出D (194)deferred shares 递延股份D (195)deferred taxation 递延税款D (196)delivery note 交货单D (197)departmental accounts 部门报表D (198)departmental budget 部门预算D (199)depreciation 折旧D (200)dispatch note 发运单D (201)development cost 开发成本D (202)differential cost 差别成本D (203)direct cost 直接成本D (204)direct debit 直接借项D (205)direct hours yield 直接小时产出率D (206)direct labour cost percentage rate 直接人工成本百分比D (207)direct labour hour rate 直接人工小时率D (208)directs on indirect work 间接工作事项上的工时D (209)discount rate 贴现率D (210)discounted cash flow 现金流量贴现D (211)discretionary cost 酌量成本D (212)distribution cost 摊销成本D (213)diversions 移用D (214)diverted hours 移用小时D (215)diverted hours ratio 移用工时比率D (216)dividend 股利D (217)dividend cover 股利产出率D (218)dividend per share 每股股利D (219)dog 疲软产品D (220)double entry accounting 复式会计D (221)double-entry book-keeping 复式薄记D (222)doubtful debts 可疑债务D (223)down time 停工时间D (224)dynamic programming 动态规划E (225)earning per share 每股盈利E (226)earning ratio 市盈率E (227)economic order quantity(EOQ) 经济订购批量E (228)efficient market hypothesis 有效市场假设E (229)efficiency ration 效率性比率E (230)element of cost 成本要素E (231)entity 经济个体E (232)environmental audit 环境审计E (233)environmental impact assessment 环境影响评价E (234)EOQ 经济订购批量E (235)equity 权益E (236)equity method of accounting 权益法会计计算E (237)equity share capital 权益股本E (238)equivalent units 当量E (239)event 事项E (240)exceptional items 例外事项E (241)expected value 期望值E (242)expenditure 支出E (243)expenses 费用E (244)external audit 外部审计E (245)external failure cost 外部损失成本E (246)extraordinary items 非常事项F (247)factory goods 让售商品F (248)factoring 应收帐款让售F (249)fair value 公允价值F (250)feedback 反馈F (251)FIFO 先近先出法F (252)final accounts 年终报表F (253)finance lease 融资租赁F (254)financial accounting 财务会计F (255)financial accounts calendar adjustment 财务报表的日历时间调整F (256)financial management 财务管理F (257)financial planning 财务计划F (258)financial statement 财务报表F (259)finished goods 完成品F (260)fixed asset 固定资产F (261)fixed overhead 固定制造费用F (262)fixed asset turnover 固定资产周转率F (263)fixed assets register 固定资产登记薄F (264)fixed cost 固定成本F (265)flexed budget 变动限额预算F (266)flexible budget 弹性预算F (267)float time 浮动时间F (268)floating charge 流动抵押F (269)flow of funds statement 资金流量表F (270)forecasting 预测F (271)founder's shares 发起人股份F (272)full capacity 满负荷生产能力F (273)function costing 职能成本计算F (274)functional budget 职能预算F (275)fund accounting 基金会计F (276)fundamental accounting concept 基础会计概念F (277)fungible assets 可互换资产F (278)futuristic planning 远景计划G (279)gap analysis 间距分析G (280)gearing 举债经营比率(杠杆)G (281)goal congruence 目标一致性G (282)going concern concept 持续经营概念G (283)goods received note 商品收讫单G (284)goodwill 商誉G (285)gross dividend yield 总股息产出率G (286)gross margin 总边际G (287)gross profit 毛利润G (288)gross profit percentage 毛利润百分比G (289)group 企业集团G (290)group accounts 集团报表H (291)high-geared 高结合杠杆(比例)H (292)hire purchase 租购H (293)historical cost 历史成本H (294)historical cost accounting 历史成本会计H (295)hours 小时H (296)hurdle rate 最低可接受的报酬率I (297)ideal standard 理想标准I (298)idle capacity ration 闲置生产能力比率I (299)idle time 闲置时间I (300)impersonal accounts 非记名账户I (301)imprest system 定额备用制度I (302)income and expenditure account 收益和支出报表I (303)incomplete records 不完善记录I (304)incremental cost 增量成本I (305)incremental yield 增量产出率I (306)indirect cost 间接成本I (307)indirect hours 间接小时I (308)insolvency 无力偿付I (309)intangible asset 无形资产I (310)integrated accounts 综合报表I (311)interdependency concept 关联性概念I (312)interest cover 利息保障倍数I (313)interlocking accounts 连锁报表I (314)internal audit 内部审计I (315)internal check 内部牵制I (316)internal control system 内部控制体系I (317)internal failure cost 内部损失成本I (318)internal rate of return(IRR) 内含报酬率I (319)inventory 存货I (320)investment 投资I (321)investment center 投资中心I (322)invoice register 发票登记薄I (323)issued share capital 已发行股本J (324)job 定单J (325)job card 工作卡J (326)job costing 工作成本计算J (327)job sheet 工作单J (328)joint cost 联合成本J (329)joint products 联产品J (330)joint stock company 股份公司J (331)joint venture 合资经营J (332)journal 日记账J (333)just-in-time(JIT) 适时制度J (334)just-in-time production 适时生产J (335)just-in-time purchasing 适时购买K (336)key factor 关键因素L (337)labour 人工L (338)labour transfer note 人工转移单L (339)leaning curve 学习曲线L (340)ledger 分类账户L (341)length of order book 定单平均周期L (342)letter of credit 信用证L (343)leverage 举债经营比率L (344)liabilities 负债L (345)life cycle costing 寿命周期成本计算L (346)LIFO 后近先出法L (347)limited liability company 有限责任公司L (348)limiting factor 限制因素L (349)line-item budget 明细支出预算L (350)liner programming 线性规划L (351)liquid assets 变现资产L (352)liquidation 清算L (353)liquidity ratios 易变现比率L (354)loan 贷款L (355)loan capital 借入资本L (356)long range planning 长期计划L (357)lost time record 虚耗时间记录L (358)low geared 低结合杠杆(比例)L (359)lower of cost or net realizable value concept 成本或可变净价孰低概念M (360)machine hour rate 机器小时率M (361)machine time record 机器时间记录M (362)managed cost 管理成本M (363)management accounting 管理会计M (364)management accounting concept 管理会计概念M (365)management accounting guides 管理会计指导方针M (366)management audit 管理审计M (367)management buy-out 管理性购买产权M (368)management by exception 例外管理原则M (369)margin 边际M (370)margin of safety ration 安全边际比率M (371)margin cost 边际成本M (372)margin costing 边际成本计算M (373)mark-down 降低标价M (374)mark-up 提高标价M (375)market risk premium 市场分险补偿M (376)market share 市场份额M (377)marketing cost 营销成本M (378)matching concept 配比概念M (379)materiality concept 重要性概念M (380)materials requisition 领料单M (381)materials returned note 退料单M (382)materials transfer note 材料转移单M (383)memorandum of association 公司设立细则M (384)merger 兼并M (385)merger accounting 兼并会计M (386)minority interest 少数股权M (387)mixed cost 混合成本N (388)net assets 净资产N (389)net book value 净账面价值N (390)net liquid funds 净可变现资金N (391)net margin 净边际N (392)net present value(NPV) 净现值N (393)net profit 净利润N (394)net realizable value 可变现净值N (395)net worth 资产净值N (396)network analysis 网络分析N (397)noise 干捞N (398)nominal account 名义账户N (399)nominal share capital 名义股本N (400)nominal holding 代理持有股份N (401)non-adjusting events 非调整事项N (402)non-financial performance measurement 非财务业绩计量N (403)non-integrated accounts 非综合报表N (404)non-liner programming 非线性规划N (405)non-voting shares 无表决权的股份N (406)notional cost 名义成本N (407)number of days stock 存货周转天数N (408)number of weeks stock 存货周转周数O (409)objective classification 客体分类O (410)obsolescence 陈旧O (411)off balance sheet finance 资产负债表外筹资O (412)offer for sale 标价出售O (413)operating budget 经营预算O (414)operating lease 经营租赁O (415)operating statement 营业报表O (416)operation time 操作时间O (417)operational control 经营控制O (418)operational gearing 经营杠杆O (419)operating plans 经营计划O (420)opportunity cost 机会成本O (421)order 定单O (422)ordinary shares 普通股O (423)out-of-date cheque 过期支票O (424)over capitalization 过分资本化O (425)overhead 制造费用O (426)overhead absorption rate 制造费用分配率O (427)overhead cost 制造费用O (428)overtrading 超过营业资金的经营P (429)paid cheque 已付支票P (430)paid-up share capital 认定股本P (431)parent company 母公司P (432)pareto distribution 帕累托分布P (433)participating preference shares 参与优先股P (434)partnership 合伙P (435)payable ledger 应付款项账户P (436)payback 回收期P (437)payments and receipts account 收入和支出报表P (438)payments withheld 保留款额P (439)payroll 工资单P (440)payroll analysis 工资分析P (441)percentage profit on turnover 利润对营业额比率P (442)period cost 期间成本P (443)perpetual inventory 永续盘存P (444)personal account 记名账户P (445)PEPT 项目评审法P (446)petty cash account 备用金账户P (447)petty cash voucher 备用金凭证P (448)physical inventory 实地盘存P (449)planning 计划P (450)planning horizon 计划时限P (451)planning period 计划期间P (452)policy cost 政策成本P (453)position audit 状况审计P (454)post balance sheet events 资产负债表编后事项P (455)practical capacity 实际生产能力P (456)pre-acquisition losses 购置前损失P (457)pre-acquisition profits 购置前利润P (458)preference shares 优先股P (459)preference creditors 优先债权人P (460)preferred creditors 优先债权人P (461)prepayments 预付款项P (462)present value 现值P (463)prevention cost 预防成本P (464)price ratio 市盈率P (465)prime cost 主要成本P (466)prime entry-books of 原始分录登记薄P (467)principal budget factor 主要预算因素P (468)prior charge capital 优先股P (469)prior year adjustments 以前年度调整P (470)priority base budgeting 优先顺序体制的预算P (471)private company 私人公司P (472)pro-forma invoice 预开发票P (473)problem child 问号产品P (474)process costing 分步成本计算P (475)process time 加工时间P (476)product cost 产品成本P (477)Product life cycle 产品寿命周期P (478)production cost 生产成本P (479)production cost of sales 售货成本P (480)production volume ratio 生产业务量比率P (481)profit center 利润中心P (482)profit per employee 每员工利润P (483)profit retained for the year 年度利润留存P (484)profit to turnover ratio 利润对营业额比率P (485)profit-volume graph 利量图P (486)profitability index 盈利指数P (487)programming 规划P (488)project evaluation and review technique 项目评审法P (489)projection 预计P (490)promissory note 本票P (491)prospectus 募债说明书P (492)provisions for liabilities and charges 偿债和费用准备P (493)prudent concept 稳健性概念P (494)public company 公开公司P (495)purchase order 订购单P (496)purchase requisition 请购单P (497)purchase ledger 采购账户Q (498)quality related costs 质量有关成本Q (499)queuing time 排队时间R (500)rate 率R (501)ratio 比率R (502)ration pyramid 比率金字塔R (503)raw material 原材料R (504)receipts and payments account 收入和支付报表R (505)receivable ledger 应收款项账户R (506)redeemable shares 可赎回股份R (507)redemption 赎回R (508)registered share capital 注册资本R (509)rejects 废品R (510)relevancy concept 相关性概念R (511)relevant costs 相关成本R (512)relevant range 相关范围R (513)reliability concept 可靠性概念R (514)replacement price 重置价格R (515)report 报表R (516)reporting 报告R (517)research cost, applied 应用性研究成本R (518)research cost, pure or basic 理论或基础研究成本R (519)reserves 留存收益R (520)residual income 剩余收益R (521)responsibility center 责任中心R (522)retention money 保留款额R (523)return on capital employed 运用资本报酬率R (524)returns 退回R (525)revenue 收入R (526)revenue center 收入中心R (527)revenue expenditure 收益支出R (528)revenue investment 收入性投资R (529)right issue 认股权发行R (530)rolling budget 滚动预算R (531)rolling forecast 滚动预测S (532)sales ledger 销售分类账S (533)sales order 销售定单S (534)sales per employee 每员工销售额S (535)scrap 废料S (536)scrip issue 红股发行S (537)secured creditors 有担保的债权人S (538)segmental reporting 分部报告S (539)selling cost 销售成本S (540)semi-fixed cost 半固定成本S (541)semi-variable cost 半变动成本S (542)sensitivity analysis 敏感性分析S (543)service cost center 服务成本中心S (544)service costing 服务成本计算S (545)set-up time 安装时间S (546)shadow prices 影子价格S (547)share 股票S (548)share capital 股份资本S (549)share option scheme 购股权证方案S (550)share premium 股票溢价S (551)sight draft 即期汇票S (552)single-entry book-keeping 单式薄记S (553)sinking fund 偿债基金S (554)slack time 松弛时间S (555)social responsibility cost 社会责任成本S (556)sole trader 独资经营者S (557)source and application of funds statement 资金来源和运用表S (558)special order costing 特殊定单成本计算S (559)staff costs 职工成本S (560)statement of account 营业账单S (561)statement of affairs 财务状况表S (562)statutory body 法定实体S (563)stock 存货S (564)stock control 存货控制S (565)stock turnover 存货周转率S (566)stocktaking 盘点存货S (567)stores requisition 领料申请单S (568)strategic business unit 战略性经营单位S (569)strategic management accounting 战略管理会计S (570)strategic planning 战略计划S (571)strategy 战略S (572)subjective classification 主体分类S (573)subscribed share capital 已认购的股本S (574)subsidiary undertaking 子公司S (575)sunk cost 沉没成本S (576)supply estimate 预算估计S (577)supply expenditure 预算支出S (578)suspense account 暂记账户S (579)SWOT analysis 长处和短处,机会和威胁分析S (580)system 制度,体系T (581)tactical planning 策略计划T (582)tactics 策略T (583)take-over 接收T (584)tangible asset 有形资产T (585)tangible fixed asset statement 有形固定资产表T (586)target cost 目标成本T (587)terotechnology 设备综合工程学T (588)throughput accounting 生产量会计T (589)time 时间T (590)time sheet 时间记录表T (591)total assets 总资产T (592)total quality management 全面质量管理T (593)total stocks 存货总计T (594)trade creditors 购货客户(应付账款)T (595)trade debtors 销货客户(应收账款)T (596)trading profit and loss account 营业损益表T (597)transfer price 转让价格T (598)transit time 中转时间T (599)treasurership 财务长制度T (600)trail balance 试算平衡表T (601)turnover 营业额U (602)uncalled share capital 未催缴股本U (603)under capitalization 不足资本化U (604)under or over-absorbed overhead 少吸收或多吸收的制造费用U (605)uniform accounting 统一会计U (606)uniform costing 统一成本计算U (607)unissued share capital 未发行股本V (608)value 价值V (609)value added 增值V (610)value analysis 价值分析V (611)value for money audit 经济效益审计V (612)vote 表决V (613)voucher 凭证W (614)waiting time 等候时间W (615)waste 废品(料)W (616)wasting asset 递耗资产W (617)weighted average cost of capital 资本的加权平均成本W (618)weighted average price 加权平均价格W (619)with resource 有追索权W (620)without recourse 无追索权W (621)working capital 营运资本W (622)write-down 减值Z (623)zero base budgeting 零基预算Z (624)zero coupon bond 无息债券Z (625)Z score 破产预测计分法。

会计专业词汇

该单元属于单词书:会计专业英语词汇表查看accounting period 会计期会计年度accoungting process:会计程序budget n. 预算vt. 编预算,为…做预算accounting n. 会计accrual basis n. 权责发生制,应计制,权责发生基础,应计基础annual report n. 年度报告audit n. 查帐,审计vt. 审计,旁听balance sheet 决算表, 资产负债表, 资金平衡表;cash and cash equivalents 现金及现金等价物cash basis n. 现金制(以现金为依据的记帐法);cash flow statement 现金流量表CPA 注册会计师Certified Public Accountantcorporation n. 公司, 法人, 集团cost accounting n.成本会计;financial accounting 财务会计;economic entity 经济实力forecast n. 预测,预报vt. &vi. 预测;geenral purpose financial statements 通用财务报表GAAP abbr. 一般公认会计原则(=generally accepted accounting principles)going concern 继续盈利的企业; 持续经营income statement 收益表,损益表,利润表;internal auditing 内部审计;International Accounting Standard Board 国际会计准则理事会management accounting n. 管理会计(学), 管理计算, 簿记处理;unit of measurement 货币计量;not-for-profits 非盈利组织partnership n. 合伙, 合股performance n.业绩prospectus n.招股说明书;内容说明书;(即将出版的书等的)内容介绍,简介;计划书,意见书;(讲义等的)大纲sole proprietorship 独资;stewardship of management 管理当局的受托责任asset n. 资产,有用的东西,优点,长处;balance between benefit and cost 权衡成本效益comparability n. 相似性,可比较性;completeness 完整性;confirmatory role 确证作用;current cost 现行成本equity n. 权益,产权,(无固定利息的)股票n. 公平, 公正expense n. 消费,支出;faithful representation 如实反映;framework for the preparation and presentation of financial statements 编报财务报表的框架gain 利得;accrued liability 应计负债administrative expense 管理费用行政事务费amortization 摊销;n. 分期偿还;available-for-sale security 可供出售证券bond n. 债券borrowing n. 借款, 贷款;comprehensive income 综合收益cost of sales 销售成本;current item 流动性项目;current liability 流动负债;(capital)reserve (资本)公积depreciation n. 折旧direct method n.直接法;discontinued operation 终止营业;equity method 权益法;indirect method 间接法distribution cost 销售费用n. 发行成本, 经销成本finance cost 财务费用;finished good 产成品goodwill n. 商誉, 信誉.;foreign currency translation adjustment 外币折算差额intangible asset n. 无形资产investing activities 投资活动investment n. 投资,投入,投资额mortgage 抵押借款;vt. 抵押n. 抵押;房屋抵押贷款;multiple-step form 多步式;non-current asset 非流动资产notes payable [经] 应付账款operating activities 经营活动;operating cycle 营业周期;prepaid expense 预付费用;raw material 原材料,素材;property plant and equipment 固定资产;report form 报告式retained earnings 留存收益share capital 股本;short-term investment 短期投资;single-step form 单步式;taxes payable 应交税金treasury bill 短期国库券treasury note n. (美国的)中期国库券, ;wages payable 应付工资work in progress n. 在产品account 账户accounting equation 会计等式accrual 应计;accrued asset 应计资产accumulated depreciation n. 累计折旧;adjusted trail balance 调整后的试算平衡表;adjusting entry 调整分录cash n. 现金allowance for doubtful accounts 坏账准备;cash dividend 现金股利closing entry 结账分录common stock 普通股contra account n. 抵减帐户credit n. 贷项,信贷debit n. 借方,借项deferral n. 递延;deferred expense 递延费用;deferred revenue 递延收入dividend n. 红利,股息,意外之财, 彩金, 被除数;double-entry bookkeeping system 复式记账entry n. 分录;income summary account 本年利润账户journal n. 日记账ledger 分类帐par value 平价, 票面价值;permanent account 永久性账户post n.过账;post-closing trail balance 结账后试算平衡;sales discount 销售折扣salvage value 残值;sales returns and allowance 销售退回与折让;temporary account 暂时性账户;trail balance 试算平衡表unearned adj. 不劳而获的, 不应得到的;unearned revenue 预计收入;valuation asjustments 计价调整T-account T型账户count 盘存;administrative overhead 管理间接费用;aging receivable 应收账款账龄分析Average cost 平均费用平均成本bad debt n. 呆账, 坏账,死帐bank reconciliation 银行存款余额调节表bank statement 银行结单,银行对账单;cash book 现金账cash on hand n. 库存现金;cash short and over 现金尾差,现金短溢;cost flow assumption 成本流转假说demand deposit 活期存款;deposit in transit 在途存款;deposit to guarantee contract performance 合同履行保证金;direct labor 直接人工;direct material 直接材料IOU (=I owe you) n. 借据;dividend receivable 应收股利;equity investment 权益投资;first-in first-out 先进先出法maturity n. 成熟(支票等的)到期;maturity date 到期日;moving or cumulative weighted average 移动加权平均;net realizable value 可变现净值overdraft n. 透支notes receivable [经] 应收票据;overtime premium 加班津贴;past due 过期;periodic system 定期盘存制;perpetual system 永续盘存制rebate n. 回扣;petty cash fund 备用金;prudence concept 谨慎性原则;redeemable preference shares 可赎回优先股retail n. 零售;retail method 零售价法reverse n转回;selling cost 销售费用;specific identification 个别认定法;standard cost 标准成本supply n. 无聊,价值较低的材料;subsidiary record 明细记录trade discount n.商业折扣,同行折扣,批发折扣;trade receivable 应收账款write down 减记;variable production overhead 可变制造费用;amortize vt. 摊销;amortize cost 摊销成本capitalize 资本化;arm‘s length transaction 公平交易control 控制;carrying amount 账面价值;consolidated financial statements 合并财务报表;depreciable amount 应计折旧额;derecognize 终止确认fair value 公允价值;effective interest rate method 实际利率法;estimated residual value 预计残值financial instrument n. 金融工具,金融证券;financial asset 金融资产identifiable 可辨认;held on freehold 拥有所有权;held on leasehold 拥有使用权;held-to-maturity investiments 持有至到期投资impairment n. 减值;internally generated 自创;investee 被投资方investment income 投资收入;investment property 投资性房地产parent company 母公司,总公司;knowledgeable willing parties 熟悉情况,自愿的双方ordinary shares 普通股;physical substance 实物形态;quoted market price 市场报价recoverable amount 可收回金额;reducing balance method 余额递减折旧法;research and development costs 研究和开发支出evaluation n. 重估;revaluation surplus 重估增值significant 重大影响;straight-line-method 直线法或年限平均法subsidiary company n.子公司,附属公司;sum-of-the-year digits method 年数综合法;surplus cash 现金盈余write off 注销记为费用;adjunct account 附属账户at par 平价, 按票面价格bonus n. 红利, 奖金book value 帐面价值Callable bond 可提前赎回债券;compound instrument 混合股利discount rate 贴现率discount n. 折扣, 贴现率vt. 打折扣, 贴现, 不重视,不全信vi. 贴现, 减息贷款face value n. 票面价值, 表面价值;good&service tax 货物和劳务税;gross price method 总价法indirect taxation n. 间接税制installment n. 分期付款(安装, 一期);interest-bearing 带息,附息leverage n. 杠杆作用,lien n. 扣押权, 留置权mortgage bond [经] 抵押债券net price 净价实价payroll tax 就业税,薪工税,工资薪金税premium n. (商)溢价provision 准备retained earning 留存收益sales tax n. 营业税,销售税;social security and unemployment insurance 社会保障税和失业保险金;tax authorities 税务机关tax deduction n.税前抵扣(指在计算所得税时可从纳税者所得总额中扣除的款项,如子女抚养费等)value added tax n. 增值税warrant 认股权warranty n. 产品质保yield 收益率;zero-coupon bond 零息债券;additional paid-in capital 股本溢价;callability 可赎回优先权convertibility n.可转换(优先股)cumulative 积累(优先股);declaration date 股权宣告日fair market value 公允市价;legal capital 法定资本limited liability n. 有限责任liquidate 清算participation 参加(优先股);payment day 股利支付日;securities law 证券法stockholder n. 股东=shareholder(英);shares outstanding 流通在外的股份;stock dividend distributable 应付股票股利stock option 股票期权;优先认股权stock split 股份分割,分股treasury stock n.[商]库存股份commission 销售佣金;associating cause and effect 因果关系对比cash discount n. 现金折扣consideration 对价dealer n. 经销商;商人;发牌者,庄家;[俚语]毒品贩子,贩毒者department store 百货公司n. 百货商店;gross amount 总额;immediate recognition 立即确认;installment sales 分期收款销售matching 配比nominal value 名义价值;ordinary operating activities 经常经营活动refund 退款;sales allowance 销售折让;sales returns 销售退回;shipping cost 运费volume volume rebate 数量折扣accounting policy 会计政策;asset turnover 资产周转率;auditor’s report 审计报告;base amount 基数base year 基期或基年;business risk 商业风险;chairman's statement 董事长报告common-size statement 统一量度式财务报表;comparative statement 比较报表scoring c redit scoring 信用评级cross-sectional comparison 同行业比较;director‘s report 董事会报告DuPont system 杜邦分析系统economic environment 经济环境financial asset 财务资产financial leverage 财务杠杆作用;financial ratio 财务比率government statistics 政府统计数据net income to sales 销售净利润;net profit margin 边际净利率ratio analysis 比率分析;return on assets 资产回报率roe return on equity 权益资产报酬率;return on sales 销售资产报酬率time-series comparison 时间序列比较trend analysis 趋势分析working capital 营运资本allocation rate 分配率clock card 工时卡;cost allocation 成本分配department overhead 部门制造费用manufacturing overhead 制造费用payroll system 工资系统reciprocal method 交互分配法step-down method 顺序分配法budgeted balance sheet 预算资产负债表budgeted statement of cash flows 预算现金流量表capital expenditures budget 资本支出预算cost center 成本中心cost of goods sold budget 产品销售成本预算efficiency variance 效率差异favorable variance 有利差异fixed overhead capacity variance 固定性制造费用能量差异fixed overhead expenditure variance 固定性制造费用耗费差异fixed overhead variance 固定性制造费用差异labor cost variance 人工成本差异labor efficiency variance 人工效率差异labor rate variance 人工工资率差异material price variance 材料价格差异material usage variance 材料使用差异operating budget 经营预算price standards 价格标准production budget 生产预算profit center 利润中心。

会计专业英语词汇

会计专业英语词汇会计专业英语词汇大全会计专业的'基础词汇会计accounting会计职能accountingfunction会计核算financialaccounting会计控制accountingcontrol会计学科accountingscience会计职业accountingprofession非营利组织会计non-profitorganizationaccounting 企业会计enterpriseaccounting财务会计financialaccounting成本会计costaccounting管理会计managementaccounting税务会计taxaccounting审计audit电算化会计computerizedaccounting会计信息accountinginformation会计目标accountingobjective企业会计准则accountingcriteriaforenterprises存货会计准则inventoryaccounting长期股权投资会计准则accountingstandards,long-termequityinvestment投资性房地产会计准则investmentpropertyaccountingstandards固定资产会计准则fixedassetsaccountingstandards生物资产会计准则biologicalassetsaccountingstandards无形资产会计准则intangibleassetsaccountingstandards非货币性资产交换会计准则ofnon-monetaryassets,theexchangeofaccountingstandards部门的称谓市场部MarketingDepartment销售部SalesDepartment客户服务CustomerService人事部HumanResourcePersonnelDepartment行政部AdministrationDepartment财务部MinistryofFinance/FinancialDepartment产品供应ProductSupply人员的称谓助理Assistant秘书Secretary前台接待小姐Receptionist文员clerk会计文员为AccountingClerk主任supervisor经理Manager总经理GM,GeneralManager总监Director总会计师FinanceControllerSeniorManager高级经理VP(VicePresident)副总裁FVP(FirstVicePresident)第一副总裁AVP(AssistantVicePresident)副总裁助理CEO(ChiefExecutiveOfficer)首席执行官COO(ChiefOperationsOfficer)首席运营官CFO(ChiefFinancialOfficer)首席财务官CIO(ChiefInformationOfficer)首席信息官HRD(HumanResourceDirector)人力资源总监OD(OperationsDirector)运营总监(MarketingDirector)市场总监OM(OperationsManager)运作经理PM(ProductionManager)生产经理(ProductManager)产品经理。

常用会计英语词汇

常用会计英语词汇基本词汇1. account账户,报表2. account ing postula te 会计假设3. account ing valuati on 会计计价4. account abilit y concept经营责任概念5. account ancy 会计职业6. account ant 会计师7. account ing 会计8. agencycost 代理成本9. account ing bases 会计基础10. account ing manual会计手册11. account ing period会计期间12. account ing policie s 会计方针13. account ing rate of return会计报酬率14. account ing referen ce date 会计参照日15. account ing referen ce period会计参照期间16. accrual concept应计概念17. accrual expense s 应计费用18. acid test ratio 速动比率(酸性测试比率)19. acquisi tion 收购20. acquisi tion account ing 收购会计21. adjusti ng events调整事项22. adminis trativ e expense s 行政管理费23. amortiz ation摊销24. analyti cal review分析性复核25. annualequival ent cost 年度等量成本法26. annualreportand account s 年度报告和报表27. apprais al cost 检验成本28. appropr iation account盈余分配账户29. article s of associa tion 公司章程细则30. assets资产31. assetscover 资产担保32. asset value per share 每股资产价值33. associa ted company联营公司34. attaina ble standar d 可达标准35. attribu tableprofit可归属利润36. audit 审计37. audit report审计报告38. auditin g standar ds 审计准则39. authori zed share capital额定股本40. availab le hours 可用小时41. avoidab le costs 可避免成本42. back-to-back loan 易币贷款43. backflu sh account ing 倒退成本计算44. bad debts 坏帐45. bad debts ratio 坏帐比率46. bank charges银行手续费47. bank overdra ft 银行透支48. bank reconci liatio n 银行存款调节表49. bank stateme nt 银行对账单50. bankrup tcy 破产51. basis of apporti onment分摊基础52. batch 批量53. batch costing分批成本计算54. beta factorB (市场)风险因素B55. bill 账单56. bill of exchang e 汇票57. bill of lading提单58. bill of materia ls 用料预计单59. bill payable应付票据60. bill receiva ble 应收票据61. bin card 存货记录卡62. bonus 红利63. book-keeping薄记64. Bostonclassif icatio n 波士顿分类65. breakev en chart 保本图66. breakev en point 保本点67. breakin g-down time 复位时间68. budget预算69. budgetcenter预算中心70. budgetcost allowan ce 预算成本折让71. budgetmanual预算手册72. budgetperiod预算期间73. budgeta ry control预算控制74. budgete d capacit y 预算生产能力75. busines s center经营中心76. busines s entity营业个体77. busines s unit 经营单位78. by-product副产品79. called-up share capital催缴股本80. capacit y 生产能力81. capacit y ratios生产能力比率82. capital资本83. capital assetspricing model 资本资产计价模式84. capital commitm ent 承诺资本85. capital employe d 已运用的资本86. capital expendi ture 资本支出87. capital expendi ture authori zation资本支出核准88. capital expendi ture control资本支出控制89. capital expendi ture proposa l 资本支出申请90. capital funding plannin g 资本基金筹集计划91. capital gain 资本收益92. capital investm ent apprais al 资本投资评估93. capital mainten ance 资本保全94. capital resourc e plannin g 资本资源计划95. capital surplus资本盈余96. capital turnove r 资本周转率97. card 记录卡98. cash 现金99. cash account现金账户100. cash book 现金账薄101. cash cow 金牛产品102. cash flow 现金流量103. cash flow budget现金流量预算104. cash flow stateme nt 现金流量表105. cash ledger现金分类账106. cash limit 现金限额107. CCA 现时成本会计108. center中心109. changeo ver time 变更时间110. charter ed entity特许经济个体111. cheque支票112. chequeregiste r 支票登记薄113. classif icatio n 分类114. clock card 工时卡115. code 代码116. commitm ent account ing 承诺确认会计117. commoncost 共同成本118. company limited by guarant ee 有限担保责任公司119. company limited by shares股份有限公司120. competi tive positio n 竞争能力状况121. concept概念122. conglom erate跨行业企业123. consist ency concept一致性概念124. consoli datedaccount s 合并报表125. consoli dation account ing 合并会计126. consort ium 财团127. conting ency plan 应急计划128. conting ent liabili ties 或有负债129. continu ous operati on 连续生产130. contra抵消131. contrac t cost 合同成本132. contrac t costing合同成本计算133. contrib utioncentre贡献中心134. contrib utionchart 贡献图135. control控制136. control account控制账户137. control limits控制限度138. control labili ty concept可控制概念139. control lablecost 可控制成本140. convers ion cost 加工成本141. convert ible loan stock 可转换为股票的贷款142. corpora te apprais al 公司评估143. corpora te plannin g 公司计划144. corpora te socialreporti ng 公司社会报告145. cost 成本146. cost account成本账户147. cost account ing 成本会计148. cost account ing manual成本手册149. cost adjustm ent 成本调整150. cost allocat ion 成本分配151. cost apporti onment成本分摊152. cost attribu tion 成本归属153. cost audit 成本审计154. cost benefit analysi s 成本效益分析155. cost center成本中心156. cost driver成本动因157. cost of capital资本成本158. cost of goods sold 销货成本159. cost of non-conform ance 非相符成本160. cost of sales 销售成本161. cost reducti on 成本降低162. cost structu re 成本结构163. cost unit 成本单位164. cost-volume-profitanalysi s(CVP) 本量利分析165. costing成本计算166. creditnote 贷项通知167. creditreport信贷报告书168. credito r 债权人169. credito r days ratio 应付账款天数率170. credito rs ledger应付账款分类账171. critica l event 关键事项172. critica l path 关键路线173. cumulat ive prefere nce shares累积优先股174. current asset 流动资产175. current cost account ing 现时成本会计176. current liabili ties 流动负债177. current purchas ing power account ing 现时购买力会计178. current ratio 流动比率179. cut-off 截止180. CVP 本量利分析181. cycle time 周转时间182. debentu re 债券183. debit note 借项通知184. debit capacit y 举债能力185. debt ratio 债务比率186. debtor债务人;应收账款187. debtordays ratio 应收账款天数率188. debtors ledger应收账款分类账189. debtor' age analysi s 应收账款账龄分析190. decisio n drivencosts 决策连动成本191. decisio n tree 决策树192. defects次品193. deferre d expendi ture 递延支出194. deferre d shares递延股份195. deferre d taxatio n 递延税款196. deliver y note 交货单197. departm entalaccount s 部门报表198. departm entalbudget部门预算199. depreci ation折旧200. dispatc h note 发运单201. develop ment cost 开发成本202. differe ntialcost 差别成本203. directcost 直接成本204. directdebit 直接借项205. directhours yield 直接小时产出率206. directlabourcost percent age rate 直接人工成本百分比207. directlabourhour rate 直接人工小时率208. directs on indirec t work 间接工作事项上的工时209. discoun t rate 贴现率210. discoun ted cash flow 现金流量贴现211. discret ionary cost 酌量成本212. distrib utioncost 摊销成本213. diversi ons 移用214. diverte d hours 移用小时215. diverte d hours ratio 移用工时比率216. dividen d 股利217. dividen d cover 股利产出率218. dividen d per share 每股股利219. dog 疲软产品220. doubleentry account ing 复式会计221. double-entry book-keeping复式薄记222. doubtfu l debts 可疑债务223. down time 停工时间224. dynamic program ming 动态规划225. earning per share 每股盈利226. earning ratio 市盈率227. economi c order quantit y(EOQ) 经济订购批量228. efficie nt markethypothe sis 有效市场假设229. efficie ncy ration效率性比率230. element of cost 成本要素231. entity经济个体232. environ mental audit 环境审计233. environ mental impactassessm ent 环境影响评价234. EOQ 经济订购批量235. equity权益236. equitymethodof account ing 权益法会计计算237. equityshare capital权益股本238. equival ent units 当量239. event 事项240. excepti onal items 例外事项241. expecte d value 期望值242. expendi ture 支出243. expense s 费用244. externa l audit 外部审计245. externa l failure cost 外部损失成本246. extraor dinary items 非常事项247. factory goods 让售商品248. factori ng 应收帐款让售249. fair value 公允价值250. feedbac k 反馈251. FIFO 先近先出法252. final account s 年终报表253. finance lease 融资租赁254. financi al account ing 财务会计255. financi al account s calenda r adjustm ent 财务报表的日历时间调整256. financi al managem ent 财务管理257. financi al plannin g 财务计划258. financi al stateme nt 财务报表259. finishe d goods 完成品260. fixed asset 固定资产261. fixed overhea d 固定制造费用262. fixed asset turnove r 固定资产周转率263. fixed assetsregiste r 固定资产登记薄264. fixed cost 固定成本265. flexedbudget变动限额预算266. flexibl e budget弹性预算267. float time 浮动时间268. floatin g charge流动抵押269. flow of funds stateme nt 资金流量表270. forecas ting 预测271. founder's shares发起人股份272. full capacit y 满负荷生产能力273. functio n costing职能成本计算274. functio nal budget职能预算275. fund account ing 基金会计276. fundame ntal account ing concept基础会计概念277. fungibl e assets可互换资产278. futuris tic plannin g 远景计划279. gap analysi s 间距分析280. gearing举债经营比率(杠杆)281. goal c ongrue nce 目标一致性282. going concern concept持续经营概念283. goods receive d note 商品收讫单284. goodwil l 商誉285. gross dividen d yield 总股息产出率286. gross margin总边际287. gross profit毛利润288. gross profitpercent age 毛利润百分比289. group 企业集团290. group account s 集团报表291. high-geared高结合杠杆(比例)292. hire purchas e 租购293. histori cal cost 历史成本294. histori cal cost account ing 历史成本会计295. hours 小时296. hurdlerate 最低可接受的报酬率297. ideal standar d 理想标准298. idle capacit y ration闲置生产能力比率299. idle time 闲置时间300. imperso nal account s 非记名账户301. imprest system定额备用制度302. incomeand expendi ture account收益和支出报表303. incompl ete records不完善记录304. increme ntal cost 增量成本305. increme ntal yield 增量产出率306. indirec t cost 间接成本307. indirec t hours 间接小时308. insolve ncy 无力偿付309. intangi ble asset 无形资产310. integra ted account s 综合报表311. interde penden cy concept关联性概念312. interes t cover 利息保障倍数313. interlo ckingaccount s 连锁报表314. interna l audit 内部审计315. interna l check 内部牵制316. interna l control system内部控制体系317. interna l failure cost 内部损失成本318. interna l rate of return(IRR) 内含报酬率319. invento ry 存货320. investm ent 投资321. investm ent center投资中心322. invoice registe r 发票登记薄323. issuedshare capital已发行股本324. job 定单325. job card 工作卡326. job costing工作成本计算327. job sheet 工作单328. joint cost 联合成本329. joint product s 联产品330. joint stock company股份公司331. joint venture合资经营332. journal日记账333. just-in-time(JIT) 适时制度334. just-in-time product ion 适时生产335. just-in-time purchas ing 适时购买336. key factor关键因素337. labour人工338. labourtransfe r note 人工转移单339. leaning curve 学习曲线340. ledger分类账户341. lengthof order book 定单平均周期342. letterof credit信用证343. leverag e 举债经营比率344. liabili ties 负债345. life cycle costing寿命周期成本计算346. LIFO 后近先出法347. limited liabili ty company有限责任公司348. limitin g factor限制因素349. line-item budget明细支出预算350. liner program ming 线性规划351. liquidassets变现资产352. liquida tion 清算353. liquidi ty ratios易变现比率354. loan 贷款355. loan capital借入资本356. long range plannin g 长期计划357. lost time record虚耗时间记录358. low geared低结合杠杆(比例)359. lower of cost or net realiza ble value concept成本或可变净价孰低概念360. machine hour rate 机器小时率361. machine time record机器时间记录362. managed cost 管理成本363. managem ent account ing 管理会计364. managem ent account ing concept管理会计概念365. managem ent account ing guides管理会计指导方针366. managem ent audit 管理审计367. managem ent buy-out 管理性购买产权368. managem ent by excepti on 例外管理原则369. margin边际370. marginof safetyration安全边际比率371. margincost 边际成本372. margincosting边际成本计算373. mark-down 降低标价374. mark-up 提高标价375. marketrisk premium市场分险补偿376. marketshare 市场份额377. marketi ng cost 营销成本378. matchin g concept配比概念379. materia lity concept重要性概念380. materia ls requisi tion 领料单381. materia ls returne d note 退料单382. materia ls transfe r note 材料转移单383. memoran dum of associa tion 公司设立细则384. merger兼并385. mergeraccount ing 兼并会计386. minorit y interes t 少数股权387. mixed cost 混合成本388. net assets净资产389. net book value 净账面价值390. net liquidfunds 净可变现资金391. net margin净边际392. net present value(NPV) 净现值393. net profit净利润394. net realiza ble value 可变现净值395. net worth 资产净值396. network analysi s 网络分析397. noise 干捞398. nominal account名义账户399. nominal share capital名义股本400. nominal holding代理持有股份401. non-adjusti ng events非调整事项402. non-financi al perform ance measure ment 非财务业绩计量403. non-integra ted account s 非综合报表404. non-liner program ming 非线性规划405. non-votingshares无表决权的股份406. notiona l cost 名义成本407. numberof days stock 存货周转天数408. numberof weeks stock 存货周转周数409. objecti ve classif icatio n 客体分类410. obsoles cence陈旧411. off balance sheet finance资产负债表外筹资412. offer for sale 标价出售413. operati ng budget经营预算414. operati ng lease 经营租赁415. operati ng stateme nt 营业报表416. operati on time 操作时间417. operati onal control经营控制418. operati onal gearing经营杠杆419. operati ng plans 经营计划420. opportu nity cost 机会成本421. order 定单422. ordinar y shares普通股423. out-of-date cheque过期支票424. over capital izatio n 过分资本化425. overhea d 制造费用426. overhea d absorpt ion rate 制造费用分配率427. overhea d cost 制造费用428. overtra ding 超过营业资金的经营429. paid cheque已付支票430. paid-up share capital认定股本431. parentcompany母公司432. paretodistrib ution帕累托分布433. partici pating prefere nce shares参与优先股434. partner ship 合伙435. payable ledger应付款项账户436. payback回收期437. payment s and receipt s account收入和支出报表438. payment s withhel d 保留款额439. payroll工资单440. payroll analysi s 工资分析441. percent age profiton turnove r 利润对营业额比率442. periodcost 期间成本443. perpetu al invento ry 永续盘存444. persona l account记名账户445. PEPT 项目评审法446. petty cash account备用金账户447. petty cash voucher备用金凭证448. physica l invento ry 实地盘存449. plannin g 计划450. plannin g horizon计划时限451. plannin g period计划期间452. policycost 政策成本453. positio n audit 状况审计454. post balance sheet events资产负债表编后事项455. practic al capacit y 实际生产能力456. pre-acquisi tion losses购置前损失457. pre-acquisi tion profits购置前利润458. prefere nce shares优先股459. prefere nce credito rs 优先债权人460. preferr ed credito rs 优先债权人461. prepaym ents 预付款项462. present value 现值463. prevent ion cost 预防成本464. price ratio 市盈率465. prime cost 主要成本466. prime entry-books of 原始分录登记薄467. princip al budgetfactor主要预算因素468. prior chargecapital优先股469. prior year adjustm ents 以前年度调整470. priorit y base budgeti ng 优先顺序体制的预算471. private company私人公司472. pro-forma invoice预开发票473. problem child 问号产品474. process costing分步成本计算475. process time 加工时间476. product cost 产品成本477. Product life cycle 产品寿命周期478. product ion cost 生产成本479. product ion cost of sales 售货成本480. product ion volumeratio 生产业务量比率481. profitcenter利润中心482. profitper employe e 每员工利润483. profitretaine d for the year 年度利润留存484. profitto turnove r ratio 利润对营业额比率485. profit-volumegraph 利量图486. profita bility index 盈利指数487. program ming 规划488. project evaluat ion and reviewtechniq ue 项目评审法489. project ion 预计490. promiss ory note 本票491. prospec tus 募债说明书492. provisi ons for liabili ties and charges偿债和费用准备493. prudent concept稳健性概念494. publiccompany公开公司495. purchas e order 订购单496. purchas e requisi tion 请购单497. purchas e ledger采购账户498. quality related costs 质量有关成本499. queuing time 排队时间500. rate 率501. ratio 比率502. rationpyramid比率金字塔503. raw materia l 原材料504. receipt s and payment s account收入和支付报表505. receiva ble ledger应收款项账户506. redeema ble shares可赎回股份507. redempt ion 赎回508. registe red share capital注册资本509. rejects废品510. relevan cy concept相关性概念511. relevan t costs 相关成本512. relevan t range 相关范围513. reliabi lity concept可靠性概念514. replace ment price 重置价格515. report报表516. reporti ng 报告517. researc h cost, applied应用性研究成本518. researc h cost, pure or basic 理论或基础研究成本519. reserve s 留存收益520. residua l income剩余收益521. respons ibilit y center责任中心522. retenti on money 保留款额523. returnon capital employe d 运用资本报酬率524. returns退回525. revenue收入526. revenue center收入中心527. revenue expendi ture 收益支出528. revenue investm ent 收入性投资529. right issue 认股权发行530. rolling budget滚动预算531. rolling forecas t 滚动预测532. sales ledger销售分类账533. sales order 销售定单534. sales per employe e 每员工销售额535. scrap 废料536. scrip issue 红股发行537. secured credito rs 有担保的债权人538. segment al reporti ng 分部报告539. selling cost 销售成本540. semi-fixed cost 半固定成本541. semi-variabl e cost 半变动成本542. sensiti vity analysi s 敏感性分析543. service cost center服务成本中心544. service costing服务成本计算545. set-up time 安装时间546. shadowprices影子价格547. share 股票548. share capital股份资本549. share optionscheme购股权证方案550. share premium股票溢价551. sight draft 即期汇票552. single-entry book-keeping单式薄记553. sinking fund 偿债基金554. slack time 松弛时间555. socialrespons ibilit y cost 社会责任成本556. sole trader独资经营者557. sourceand applica tion of funds stateme nt 资金来源和运用表558. special order costing特殊定单成本计算559. staff costs 职工成本560. stateme nt of account营业账单561. stateme nt of affairs财务状况表562. statuto ry body 法定实体563. stock 存货564. stock control存货控制565. stock turnove r 存货周转率566. stockta king 盘点存货567. storesrequisi tion 领料申请单568. strateg ic busines s unit 战略性经营单位569. strateg ic managem ent account ing 战略管理会计570. strateg ic plannin g 战略计划571. strateg y 战略572. subject ive classif icatio n 主体分类573. subscri bed share capital已认购的股本574. subsidi ary underta king 子公司575. sunk cost 沉没成本576. supplyestimat e 预算估计577. supplyexpendi ture 预算支出578. suspens e account暂记账户579. SWOT analysi s 长处和短处,机会和威胁分析580. system制度,体系581. tactica l plannin g 策略计划582. tactics策略583. take-over 接收584. tangibl e asset 有形资产585. tangibl e fixed asset stateme nt 有形固定资产表586. targetcost 目标成本587. terotec hnolog y 设备综合工程学588. through put account ing 生产量会计589. time 时间590. time sheet 时间记录表591. total assets总资产592. total quality managem ent 全面质量管理593. total stocks存货总计594. trade credito rs 购货客户(应付账款)595. trade debtors销货客户(应收账款)596. trading profitand loss account营业损益表597. transfe r price 转让价格598. transit time 中转时间599. treasur ership财务长制度600. trail balance试算平衡表601. turnove r 营业额602. uncalle d share capital未催缴股本603. under capital izatio n 不足资本化604. under or over-absorbe d overhea d 少吸收或多吸收的制造费用605. uniform account ing 统一会计606. uniform costing统一成本计算607. unissue d share capital未发行股本608. value 价值609. value added 增值610. value analysi s 价值分析611. value for money audit 经济效益审计612. vote 表决613. voucher凭证614. waiting time 等候时间615. waste 废品(料)616. wasting asset 递耗资产617. weighte d average cost of capital资本的加权平均成本618. weighte d average price 加权平均价格619. with resourc e 有追索权620. without recours e 无追索权621. working capital营运资本622. write-down 减值623. zero base budgeti ng 零基预算624. zero couponbond 无息债券625. Z score 破产预测计分法。

国际会计专业英语课程参考词汇

Vocabulary Unit 1accounting principle 会计原则accounting element 会计要素accounting equation 会计等式shareholder n. 股东asset n. 资产liability n. 负债owner’s equity 所有者权益revenue n. 收益,收入expense n. 费用accounting period 会计期间cash n. 现金accounts receivable 应收账款inventory n. 存货notes payable 应付票据accounts payable 应付账款salaries payable 应付工资shareholders’ equity 股东权益capital n. 资本ledger n . 总账chart of accounts 会计科目表ledger account 总账账户prepaid insurance 预付保险费bank deposit 银行存款cash receipt 现金收入financial position 财务状况creditor n. 债权人creditors’ account 债权人账户transaction n. 经济业务T account 丁字账户debit n. & vt. 借方;借记credit n. & vt. 贷方;贷记enter vt. 登录,记账entry n. 分录double-entry a. 复式的,复式记账的supplies expense 材料费用miscellaneous expense 其他费用debit balance 借方余额credit balance 贷方余额posting n. 过账accounting cycle 会计循环/周期journal n. 日记账journalizing n. 登日记账payroll n. 工资表cash disbursements 现金支出sales on account 赊销purchases on account 赊购adjusting and closing entries 调整及结账分录Unit 2cash n. 现金cash in bank 银行存款cash equivalents 现金等价物bank draft 银行汇票credit card 信用卡short-term investments 短期投资stock n. 股票bonds / debentures n. 债券funds n. 基金accounts receivable 应收账款notes receivable 应收票据bank acceptance 银行承兑汇票trade acceptance 商业承兑汇票dividend receivable 应收股利interest receivable 应收利息allowance for bad debts 坏账准备prepaid n. 预付项目inventory n. 存货raw materials 原材料low-value consumption goods 低值易耗品semi-finished goods 半成品finished goods 产成品periodic 实地盘存制the Lower of Cost or Market Rule 成本与市价孰低specific identification 个别认定法weighted average 加权平均法FIFO 先时先出法LIFO 后进先出法limited company 有限公司principal n. 本金marketable securities 有价证券common stocks 普通股preferred stock 优先股dividend n. 股息,红利interest n. 利息listed companies 上市公司Securities/stock exchange 证券交易所Unit 3enterprise n. 企业tangible assets 有形资产rental n. 租赁,租金额administrative 管理的,行政的fixed assets (PPE) 固定资产property n. 财产,地产plant 工厂,重型机械equipment 设备warehouse n. 库房issuance of securities 发行股票donation n. 捐助long-term assets 长期资产useful life 使用寿命original cost 原始成本historical cost 历史成本actual cost 实际成本additional cost 附加费用expenditure n. 支出,花费,开销intended use 预定可使用状态installation cost 安装费professional fees 专业人员服务费building permit fee 建设许可费acquisition cost 购置成本fair value 公允价值non-monetary assets 非货币性资产debt restructuring transaction 债务重组abandoning cost 弃置费用recognition criteria 确认条件measurement bases 计量基础depreciation n. 折旧estimated net residual value 预计净残值net salvage value 净残值depreciation rate 折旧率amortization n. 摊销impairment test 减值测试depreciable amount 应计折旧额disposal proceeds 处置收益disposal expenses 处置费用straight-line method 年限平均法(直线法)double declining balance method 双倍余额递减法sum-of-the-years-digits method 年数总和法depreciation expense/ charge 折旧费wear and tear 磨损,损耗units of production method 工作量法intangible assets 无形资产identifiable a. 可以确认的physical substance 实物形态privilege n. 特权,特别待遇finite intangibles 寿命有限的无形资产indefinite intangibles 寿命不确定的无形资产franchise n. 特许经营权,公民权license n. 营业执照,许可证Internet domain name 互联网域名construction permit 建筑许可证assessed value 评估价格Unit 4current liability 短期负债notes payable 应付票据account payabl e 应付账款unearned revenue 预收账款accrued wages 应付工资dividends payable 应付股利tax payable 应交税金value added tax payable 应交增值税consumption tax payable 应交消费税income tax payable 应交所得税personal income tax payable 应交个人所得税Drawing expense in advance 预提费用Long-term Liabilities/loans 长期负债/借款Long-term loans due within one year 一年内到期长期借款Long-term loans due over one year 一年后到期长期借款debentures , bonds 债券bonds payable 应付债券face value, par value 债券面值the maturity date 到期日premium on bonds 债券溢价discount on bonds 债券折价accrued interest 应计利息contingent liability 或有负债Unit 5Partnership/partner n. 合伙/合伙人amortize v. 分期清偿distribution n. 分配combine v. 联合recognize v. 承认,认可consolidate v. 巩固,加固share v. 分配,分享evidence n /v. 证实,证明subtotal n. 小计dividend 股利股息preemptive right n. 优先权owner’s equity 所有者权益stockholders’ equity 股东权益par value stock 有面值股票no-par value stock 无面值股票paid-in capital 实收资本additional paid-in capital 多收资本,增收资本capital surplus 资本公积issuing corporation 发行公司retained earnings 留存收益cash dividend 现金股利stock dividend 股票股利declaration of dividend 股利宣告dividend distribution 股利分配reserve 计提准备金,准备金reserve found 盈余公积appropriated retained earnings 核定的留存收益stock split 股票分割bylaw 附则、细则、公司章程Unit 6sales revenue 销售收入service revenue 劳务收入prime operating revenue 主营业务收入render 提供(服务等)period expense 期间费用direct material cost 直接材料成本direct labor cost 直接人工成本manufacturing overhead 制造费用leasing charge 租赁费maintenance 维修费freight charges 运输费advertising expenses 广告费Unit 7markup n. 成本加成projected adj. 预期的drawings n. 提款alternatively adv. 替代地summarize v. 汇总multiple-step n. 多步式single-step n. 单步式deduct v. 扣减subtract n. 减去,扣除subtotals n. 小计liquid adj. 流动的maturity n. 到期financial position 财务状况operating results 经营成果the balance sheet 资产负债表the income statement 利润表the statement of cash flows 现金流量表net income 净收益net loss 净损失multiple-step income statement 多步式利润表single-step income statement 单步式利润表the cost of goods sold 商品销售成本gross profit 毛利income tax expenses 所得税费用cash receipts 现金收入cash payments 现金支出operating activities 经营活动financing activities 筹资活动(融资行为)Unit 8profitability 获利能力solvency 偿付能力financial analysis 财务分析current ratio 流动比率quick ratio 速动比率return on stockholders’ equity 股东权益收益率return on owner’s equity 所有者权益收益率return on assets 资产收益率assets turnover 资产周转率return on investment 投资收益率earnings per share (EPS)每股收益price/earning ratio 市盈率book value per share 每股账面价值equity ratio 权益比率times interest earned 已获利息倍数receivable turnover 应收账款周转率inventory turnover 存货周转率operating cycle 营业周期operating cash flows/current debts ratio 营业现金流量与流动负债比率debt ratio 负债比率average collection period 平均收款期dividend cover 股利报酬率profit margin 销售利润率。

会计专业英语

D D

会计循环

单选题

C

现金

单选题

中

C

银行余额 调节

单选题

中

A bank reconciliation should be prepared periodically because ( )

C

银行余额 调节

单选题

现金

单选题

坏账

单选题

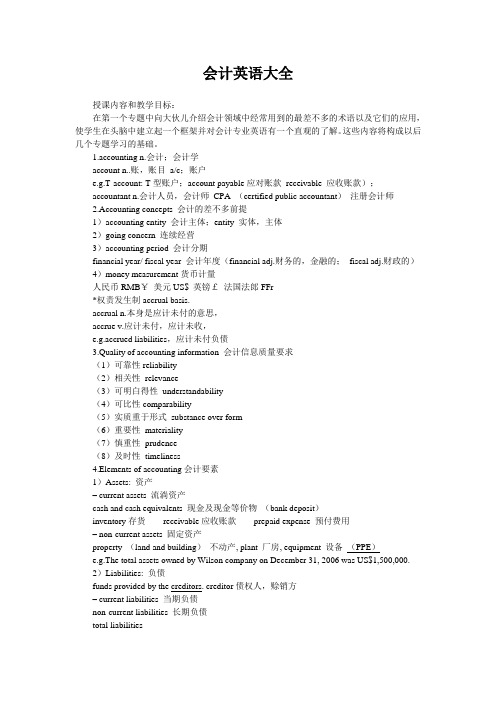

deduction from the balance per depositor's records##addition to the balance per bank statement##deduction from the balance per bank statement##addition to the balance per depositor's records are illegal in some company##will be converted to cash within 中 Cash equivalents( ) two years##will be converted to cash within 90 days##will be converted to cash within 120 days Uncollectible accounts expense for the year##total of the On the balance sheet, the amount shown for accounts receivables written-off during the year ##total 中 the Allowance for Doubtful Accounts is equal estimated uncollectible accounts as of the end of the to the ( ) year##sum of all accounts that are past due. The amount of the outstanding checks is 中 included on the bank reconciliation as a(n) ( ) 中 What is the type of account and normal balance of Allowance for Doubtful Accounts? ) Contra asset, credit##Asset, debit##Asset, credit##Contra asset, debit merchandise held for sale in the normal course of business##materials in the process of production or held for production##supplies##both A and B net income is understated##net income is overstated##cost of merchandise sold is understated##merchandise inventory reported on the balance sheet is overstated average cost##last-in, first-out##first-in, firstout##weighted average FIFO##LIFO##average##specific identification

会计英语大全

会计英语大全授课内容和教学目标:在第一个专题中向大伙儿介绍会计领域中经常用到的最差不多的术语以及它们的应用,使学生在头脑中建立起一个框架并对会计专业英语有一个直观的了解。

这些内容将构成以后几个专题学习的基础。

1.accounting n.会计;会计学account n..账,账目a/c;账户e.g.T-account: T型账户;account payable应对账款receivable 应收账款);accountant n.会计人员,会计师CPA (certified public accountant)注册会计师2.Accounting concepts 会计的差不多前提1)accounting entity 会计主体;entity 实体,主体2)going concern 连续经营3)accounting period 会计分期financial year/ fiscal year 会计年度(financial adj.财务的,金融的;fiscal adj.财政的)4)money measurement货币计量人民币RMB¥美元US$ 英镑£法国法郎FFr*权责发生制accrual basis.accrual n.本身是应计未付的意思,accrue v.应计未付,应计未收,e.g.accrued liabilities,应计未付负债3.Quality of accounting information 会计信息质量要求(1)可靠性reliability(2)相关性relevance(3)可明白得性understandability(4)可比性comparability(5)实质重于形式substance over form(6)重要性materiality(7)慎重性prudence(8)及时性timeliness4.Elements of accounting会计要素1)Assets: 资产– current assets 流淌资产cash and cash equivalents 现金及现金等价物(bank deposit)inventory存货receivable应收账款prepaid expense 预付费用– non-current assets 固定资产property (land and building)不动产, plant 厂房, equipment 设备(PPE)e.g.The total assets owned by Wilson company on December 31, 2006 was US$1,500,000.2)Liabilities: 负债funds provided by the creditors. creditor债权人,赊销方– current liabilities 当期负债non-current liabilities 长期负债total liabilitiesaccount payable应对账款loan贷款advance from customers 预收款bond债券(由政府发行, government bond /treasury bond政府债券,国库券)debenture债券(由发行)3)Owners’ equity: 所有者权益(Net assets)funds provided by the investors. Investor 投资者– paid in capital (contributed capital)实收资本– shares /capital stock (u.s.)股票retained earnings 留存收益同时记住几个单词dividend 分红beginning retained earnings ending retained earnings– reserve 储备金(资产重估储备金,股票溢价账户)e.g.The company offered/issued 10,000 shares at the price of US$2.30 each.4)Revenue: 收入sales revenue销售收入interest revenue利息收入rent revenue租金收入5)Expense: 费用cost of sales销售成本, wages expense工资费用6)Profit (income, gain):利润net profit, net income5.Financial statement 财务报表1)balance sheet 资产负债表2)income statement 利润表3)statement of retained earnings 所有者权益变动表4)cash flow statement 现金流量表6.Accounting cycle1)journal entries 日记账general journal总日记账general ledger总分类账trial balance试算平稳表adjusting entries 调整分录adjusted trial balance调整后的试算平稳表Financial statements 财务报表closing entry 完结分录2)Dr.—Debit 借Cr.—Credit 贷Double-entry system 复式记账7.Exercise 练习1)purchases of inventory in cash for RMB¥3,000 现金人民币3,000元购买存货Dr.inventory 3,000借:存货3,000Cr.cash 3,000 贷:现金3,0002)sales on account of US$10,000 赊销方式销售,收入10,000美元Dr.account receivable 10,000借:应收账款10,000 Cr.sales revenue 10,000 贷:销售收入10,0003)paid RMB¥50,000 in salaries & wages 支付工资人民币50,000元Dr.wages & salaries expense 50,000 借:职工薪酬50,000Cr.bank deposit 50,000贷:银行存款50,0004)cash sale of US$1,180 销售收入现金1,180美元Dr.cash 1,180 借:现金1,180 Cr.sales revenue 1,180贷:销售收入1,1805)pre-paid insurance for US$12,000 预付保险费12,000美元Dr.prepaid insurance 12,000借:预付保险12,000Cr.bank deposit 12,000贷:银行存款12,000第二讲存货授课内容和教学目标:本专题要紧讲授与存货有关的英文术语,如期初和期末的存货的表达方式,以及不同的企业中的各种存货形式。

会计专业基础英语

Accounting- 1 -Unit 4 AccountingPART I Fundamentals to Accounting第一部分 会计基本原理1.accounting [ə'ka ʊnt ɪŋ]n. 会计会计2.double-entry system 复式记账法复式记账法 2-1 Dr.(Debit) 借记借记借记 2-2 Cr.(Credit) 贷记贷记贷记3.accounting basic assumption 会计基本假设会计基本假设4.accounting entity 会计主体会计主体5.going concern 持续经营持续经营6.accounting periods 会计分期会计分期7.monetary measurement 货币计量货币计量8.accounting basis 会计基础会计基础9.accrual [ə'kr ʊəl] b asis basis 权责发生制权责发生制 【讲解】【讲解】accrual n. 自然增长,权责发生制原则,应计项目自然增长,权责发生制原则,应计项目自然增长,权责发生制原则,应计项目 accrual concept 应计概念应计概念应计概念 accrue [ə'kruː] v. 积累,自然增长或利益增加,产生积累,自然增长或利益增加,产生积累,自然增长或利益增加,产生 10.accounting policies 会计政策会计政策 11.substance over form 实质重于形式实质重于形式12.accounting elements 会计要素会计要素 13.recognition [rek əg'n ɪʃ(ə)n] n.确认确认 13-1 initial recognition [rek əg'n ɪʃ(ə)n] 初始确认初始确认 【讲解】【讲解】recognize ['r ɛk əg'na ɪz] v.确认确认确认14.measurement ['me ʒəm(ə)nt] n.计量计量计量 14-1 subsequent ['s ['s ʌbs ɪkw(ə)nt] measurement 后续计量后续计量后续计量 15.asset ['æset] n. 资产资产资产 16.liability [la ɪə'b ɪl ɪt ɪ] n. 负债负债负债 17.owners’ equity 所有者权益所有者权益 18.shareholder’s equity 股东权益股东权益股东权益 19.expense [ɪk'spens; ek-] n. 费用费用费用 20.profit ['pr ɒf ɪt] n.利润利润利润 21.residual [r ɪ'z ɪdj ʊəl] equity 剩余权益剩余权益 22.residual claim 剩余索取权剩余索取权 23.capital ['kæpɪt(ə)l] n.资本资本资本 24.gains [ɡeinz] n. 利得利得利得 25.loss [l ɒs] n.损失损失损失 26.Retained earnings 留存收益留存收益 27.Share premium 股本溢价股本溢价股本溢价28.historical cost 历史成本历史成本 【讲解】【讲解】historical [h ɪ'st ɒr ɪk(ə)l] adj. 历史的历史的历史的,,历史上的历史上的 historic [h ɪ'st ɒr ɪk] adj.有历史意义的有历史意义的有历史意义的,,历史上著名的历史上著名的28-1 replacement [r [r ɪ'ple ɪsm(ə)nt] cost重置成本重置成本 29.Balance Sheet/Statement of Financial Position 资产负债表资产负债表 29-1 Income Statement 利润表利润表 29-2 Cash Flow Statement 现金流量表现金流量表29-3 Statement of changes in owners’equity (or shareholders’shareholders’equity) equity) 所有者权益(股东权益)变动表东权益)变动表29-4 notes [n [n əʊts] n.附注附注附注PART II Financial Assets*第二部分 金融资产*30.financial assets 金融资产金融资产e.g. A financial instrument is any contract that gives rise to a financial asset ofone enterprise and a financial liability or equity instrument of another enter 【讲解】【讲解】give rise to 引起,导致引起,导致31.cash on hand 库存现金库存现金 32.bank deposits [d ɪ'p ɒz ɪt] 银行存款银行存款 33.A/R, account receivable 应收账款应收账款 34.notes receivable 应收票据应收票据 35.others receivable 其他应收款项其他应收款项 36.equity investment 股权投资股权投资 37.bond investment 债券投资债券投资38.derivative financial instrument 衍生金融工具衍生金融工具 39.active market 活跃市场活跃市场40.quotation [kw ə(ʊ)'te ɪʃ(ə)n]n.报价报价 41.financial assets at fair value through profit or loss 以公允价值计量且其变动计入当期损益的金融资产入当期损益的金融资产41-1 those designated as at fair value through profit or loss 指定为以公允价值计量且其变动计入当期损益的金融资产且其变动计入当期损益的金融资产41-2 financial assets held for trading 交易性金融资产交易性金融资产 42.financial liability 金融负债金融负债 43.transaction costs 交易费用交易费用43-1 incremental external cost 新增的外部费用新增的外部费用 【讲解】【讲解】incremental [ɪnkr ə'm əntl] adj.增量的增量的增量的,,增值的增值的44.cash dividend declared but not distributed 已宣告但尚未发放的现金股利已宣告但尚未发放的现金股利 投资收益投资收益45.profit and loss arising from fair value changes 公允价值变动损益公允价值变动损益 46.Held-to-maturity investments 持有至到期投资持有至到期投资 47.amortized cost 摊余成本摊余成本 【讲解】【讲解】amortized [ə'm ɔ:taizd]adj. 分期偿还的分期偿还的,,已摊销的已摊销的48.effective interest rate 实际利率实际利率 49.loan [l əʊn] n.贷款贷款贷款 50.receivables [ri'si:v əblz] n.应收账款应收账款应收账款 51.available-for-sale financial assets 可供出售金融资产可供出售金融资产 52.impairment of financial assets 金融资产减值金融资产减值52-1 impairment loss of financial assets 金融资产减值损失金融资产减值损失 53.transfer of financial assets 金融资产转移金融资产转移53-1 transfer of the financial asset in its entirety 金融资产整体转移金融资产整体转移 53-2 transfer of a part of the financial asset 金融资产部分转移金融资产部分转移 54.derecognition [diː'rekəg'n ɪʃən] n.终止确认,撤销承认终止确认,撤销承认54-1 derecognize [diː'rekə[diː'rekəgna ɪz] v.撤销承认撤销承认撤销承认 e.g. An enterprise shall derecognize a financial liability (or part of it) only w the underlying present obligation (or part of it) is discharged /cancelled . 【译】金融负债的现时义务全部或部分已经解除的,才能终止确认该金融负债或其一部分。

会计英语基础试题及答案

会计英语基础试题及答案一、单项选择题(每题2分,共20分)1. The term "accounting" refers to:A. The process of recording, summarizing, analyzing, and interpreting financial informationB. The science of cookingC. The study of plantsD. The practice of law答案:A2. Which of the following is not a financial statement?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Payroll Report答案:D3. The process of identifying, measuring, and communicating economic information is known as:A. AuditingB. BudgetingC. AccountingD. Taxation答案:C4. What is the purpose of an income statement?A. To show the financial position of a company at a specific point in timeB. To show the changes in equity of a company over a period of timeC. To show the results of a company's operations over a period of timeD. To show the cash inflows and outflows of a company over a period of time答案:C5. The accounting equation is:A. Assets = Liabilities + EquityB. Assets - Liabilities = EquityC. Liabilities - Equity = AssetsD. Equity - Assets = Liabilities答案:A6. Which of the following is an example of a tangible asset?A. GoodwillB. PatentsC. MachineryD. Trademarks答案:C7. The term "double-entry bookkeeping" refers to the practice of:A. Recording transactions in two different accountsB. Recording transactions in two different ledgersC. Recording each transaction with a corresponding debit and creditD. Recording each transaction with a corresponding increase and decrease答案:C8. The accounting principle that requires companies to match expenses with revenues in the same period is known as:A. The matching principleB. The accrual basis of accountingC. The cash basis of accountingD. The historical cost principle答案:A9. What is the purpose of depreciation?A. To increase the value of an assetB. To reduce the value of an asset over timeC. To dispose of an assetD. To sell an asset答案:B10. The process of adjusting the accounts at the end of an accounting period to ensure they reflect the actual financial position of the company is called:A. Closing the booksB. Adjusting entriesC. AuditingD. Budgeting答案:B二、多项选择题(每题3分,共15分)1. Which of the following are considered current assets? (Choose all that apply)A. CashB. Accounts ReceivableC. InventoryD. Land答案:A, B, C2. The following are examples of liabilities except:A. Accounts PayableB. Bonds PayableC. Common StockD. Long-term Debt答案:C3. The accrual basis of accounting is different from the cash basis of accounting in that it:A. Recognizes revenues when cash is receivedB. Recognizes revenues when earnedC. Recognizes expenses when cash is paidD. Recognizes expenses when incurred答案:B, D4. Which of the following are considered as equity accounts? (Choose all that apply)A. Retained EarningsB. Common StockC. DividendsD. Treasury Stock答案:A, B, D5. The following are examples of adjusting entries except:A. Accrued RevenueB. Accrued ExpensesC. Prepaid ExpensesD. Depreciation Expense答案:C三、填空题(每题2分,共20分)1. The basic accounting equation is _______ = _______ +_______.答案:Assets, Liabilities, Equity2. The two main types of business entities are _______ and_______.答案:Sole Proprietorship, Corporation3. The process of preparing financial statements is known as _______.答案:Accounting Cycle4. The term used to describe the cost of an asset is _______.答案:Historical Cost5. The accounting principle that requires companies to provide full disclosure in financial reports is known as_______.答案:Full Disclosure Principle6. The _______ statement shows the changes in equity of a company over a period of time.答案:Statement of Changes in Equity7. The _______ statement shows the cash inflows and outflows of a company over a period of time.答案:Cash Flow Statement8. The process of determining the value of an asset is called _______.答案:Valuation9. The _______ principle states that a company should not anticipate revenues or expenses before they are earned or incurred.答案:Cons。

财会专业英语-中英文对照

AAbsorption costing 完全成本法Accelerated Depreciation Method 加速折旧法Account 科目,账户Account form 账户式Account payable 应付账款Account receivable 应收账款Accounting 会计Accounting cycle 会计循环Accounting equation 会计等式资产 Assets= 负债 Liabilities + 所有者权益Owner’s EquityAccounting period concept 会计期间Accounting system 会计制度Account payable subsidiary ledger 应付款明细分类账Accounts receivable analysis 应收账款分析Accounts receivable subsidiary ledger 应收账款明细分类账Accounts receivable turnover 应收账款周转率Accrual basis accounting 应记制,债权发生制Accrued expenses 应记费用Accrued revenues 应记收入Accumulated depreciation 累计折旧Accumulated other comprehensive income 累计其他综合收入Activity base drive 作业基础/动因Activity—based costing ABC 作业成本计算法Adjusted trial balance调整后试算平衡表Adjusting entries调整分录Adjusting process调整过程Administrative expenses general expenses管理费用一般费用Aging the receivables应收账款账龄分析Allowance for doubtful accounts 坏账准备Allowance method备抵法Amortization摊销Annuity年金Assets资产Available—for—sale securities可供出售证券Average inventory cost flow method 平均库存成本流法Average cost method平均成本法Average rate of return平均回报率BBad debt expense 坏账费用Balance of the account账户余额Balance sheet资产负债表Balanced scorecard平衡记分卡Bank reconciliation银行存款余额调节表Bank statement 银行报表Bond债券Bond indenture债券契约Book value账面价值Book value of the asset资产的账面价值Boot补价Break-even point盈亏临界点Budget预算Budget performance report预算业绩报告Budgetary slack预算松弛Budgeted variable factory overhead 预算变量工厂开销Business企业Business combination 企业合并Business entity concept企业主体概念Business stakeholder企业利益相关者Business strategy企业战略Business transaction经济业务CCapital account 资本性账户Capital expenditures资本性支出Capital expenditures budget资本支出预算Capital investment analysis资本投资分析Capital leases资本性租赁Capital rationing资本分配Carrying amount账面金额Cash现金Cash basis of accounting现金制;收付实现制Cash budget现金预算Cash dividend现金股利Cash equivalents现金等价物Cash flow per share 每股现金流量Cash flows from financing activities筹资活动现金流量Cash flows from investing activities投资活动现金流量Cash flows from operating activities经营活动现金流量Cash payback period现金回收期Cash payments journal现金付款日记账Cash receipts journal现金收款日记账Cash short and over account现金余缺账户Certified public accountant CPA注册会计师Chart of accounts会计科目表Clearing account 清理账户Closing entries结账分录Closing process结账程序Closing the books 结账Common stock普通股Common—size statement通用报表Compensating balance 补偿性余额Comprehensive income全面收益Consigned inventory 寄售库存Consignee 收货人承销人Consignor 发货人寄件人Consolidated financial statements合并财务报表Contingent liabilities 不确定债务Continuous budgeting滚动预算Continuous process improvement 持续过程改进Contra accountor contra asset account抵减账户Contract rate约定利率Contribution margin 贡献毛益Contribution margin ratio贡献毛益率Contribution margin ratio 边际贡献率Controllable expenses可控费用Controllable revenues 可控收入Controllable variance可控差异Controller主计长Controlling 管理控制Controlling account控制账户Conversion costs加工成本Copyright版权Corporation公司Correcting journal entry 调整分录Cost成本Cost accounting system成本会计系统Cost allocation成本分配Cost behavior成本性态Cost center成本中心Cost concept 成本概念Cost method 成本法Cost object 成本对象Cost of finished goods available 已完工产品的成本Cost of goods manufactured 产品成本Cost of goods sold产品销售成本Cost of goods sold budget产品销售成本预算Cost of merchandise sold商品销售成本:商业企业所销售商品的成本.Cost of merchandise purchased 产品购买成本Cost of merchandise sold 销货成本Cost of production report 生产成本报告Cost per equivalent unit单位约当产量成本Cost price approach成本价格法Cost variance成本差异Cost-volume-profit analysis本-量-利分析Cost-volume-profit chart本-量-利图Credit memorandumcredit memo贷项通知单Credit period 贷款期限Credit terms 赊销付款条件,信用证条款Credits 贷记Cumulative preferred stock累积优先股Currency exchange rate货币汇率Current assets流动资产Current liabilities流动负债Current position analysis 流动财务状况分析Current ratio流动比率Currently attainable standards当前可达标准DDebit memorandum 借项通知单Debits借记debt securities债务证券,债券decision making 决策,判定;作出判定Deficiency 亏损Deficit 亏损Defined benefit plan 固定收益计划:Defined contribution plan 固定缴款计划:Depletion 折耗:Depreciate:贬值Depreciation 资产等折旧;货币贬值;跌价Depreciation expense 折旧费用Differential analysis 差异分析Differential income or less 差别收入或更少Differential cost 差异成本Differential revenue 差异收入Differential strategy 差异化战略Direct labor cost 直接人工成本Direct labor cost budget 直接人工成本预算Direct labor rate variance 直接人工工资率差异Direct labor time variance 直接人工工时差异Direct materials cost 直接材料成本Direct materials price variance 直接材料价格差异Direct materials purchases budget 直接材料采购预算Direct materials quantity variance 直接材料数量差异Direct method 直接法:Direct write—off method 直接注销法:Directing 指导Discount 贴现息;折价:Dishonored note receivable 拒付应收票据:Dividend yield 股利收益率:Dividends 股息,红利Dividends per share每股股利Double-declining—balance method双倍余额递减法Double—entry accounting system 复式会计模式:Drawing 提款:DuPont formula 杜邦公式EEarnings per common share EPS on common stock 普通股每股收益E—commerce 电子商务:Effective interest rate method 实际利率法Effective rate of interest 实际利率:债券发行时的市场利率。

会计实务英语

会计实务英语以下是一些在会计实务中常用的英语词汇和短语:1. Accounting Principles (会计原则)2. Balance Sheet (资产负债表)3. Income Statement (利润表/损益表)4. Cash Flow Statement (现金流量表)5. Trial Balance (试算平衡表)6. General Ledger (总账)7. Journal Entry (日记账分录)8. Debit (借方)9. Credit (贷方)10. Asset (资产)11. Liability (负债)12. Equity (所有者权益)13. Revenue (收入)14. Expense (费用)15. Accrual Basis Accounting (权责发生制会计)16. Cash Basis Accounting (现金收付制会计)17. Accounts Payable (应付账款)18. Accounts Receivable (应收账款)19. Inventory (库存)20. Depreciation (折旧)21. Amortization (摊销)22. Budget (预算)23. Cost of Goods Sold (销售成本)24. Financial Statement Analysis (财务报表分析)25. Audit (审计)26. Internal Control (内部控制)27. GAAP (Generally Accepted Accounting Principles,公认会计原则)28. IFRS (International Financial Reporting Standards,国际财务报告准则)29. Taxation (税收)30. Bookkeeping (记账)在实际的会计实务中,这些词汇和相关的表达会频繁出现,理解和掌握它们对于进行英文环境下的会计工作非常重要。

财会英语词汇

在财务和会计领域,有一些专业术语和词汇是经常使用的。

以下是一些常用的财会英语词汇:1. Accountant -会计师2. Accounting -会计3. Bookkeeping -记账4. Budget -预算5. Cash flow -现金流量6. Chart of accounts -账户表7. Cost accounting -成本会计8. Credit -信用9. Debit -借方10. Equity -股东权益11. Expense -费用12. Financial statement -财务报表13. Fixed asset -固定资产14. Income -收入15. Journal entry -日记账目16. Ledger -分户账17. Liability -负债18. Net income -净收入19. Payroll -工资单20. Profit -利润21. Tax -税收22. Trial balance -试算平衡表23. Audit -审计24. Bank reconciliation -银行对账25. Depreciation -折旧26. Earnings per share -每股收益27. Financial ratio -财务比率28. Forecasting -预测29. Internal controls -内部控制30. Journal -日志31. Noncurrent asset -非流动资产32. Nonoperating income -非经常性收入33. Operating expense -营业费用34. Operating income -营业收入35. Owner's equity -所有者权益36. Payable -应付账款37. Receivable -应收账款38. Revenue -营业收入39. Statement of cash flows -现金流量表40. Statement of financial position -财务状况表41. Statement of income -收入表42. Statement of retained earnings -未分配利润表43. Transaction -交易44. Trial balance sheet -试算平衡表这些词汇是财务和会计专业的基础词汇,对于从事这一领域的工作的人来说非常重要。

会计英语1(词汇,会计)

Accounting English学习会计英语,词汇是基础。

以下是一些经常用到的词汇。

第一篇(词汇篇上——结构篇)第一部分:基础的会计词汇CPA (Certified Public Accountant)注册会计师AICPA (American Institute Of CPA)美国注册会计师CICPA (Chinese Institute Of CPA)中国注册会计师ACCA (the Association of Chartered Certified Accountants)特许公认会计师协会“四大”指的是世界四大会计师事务所,分别为普华永道(Price Waterhouse Coopers, PwC)毕马威(KPMG)德勤(Deloitte Touche Tohmatsu,DTT)安永(Ernst&Young,E&Y)Management Accountants 管理会计师•The Institute of Management Accountants(美国管理会计师协会,IMA)•Certified Management Accountant(美国注册管理会计师,CMA)Controller 总会计师,会计主管CFO(Chief Financial Officer)财务总监,首席财务官Financial position 财务状况Result of operation 经营成果Cash flow 现金流Income tax returns 纳税申报Prepare income tax returns 编制纳税申报Audit v.审计Controller 总会计师,会计主管Treasurer 财务主管CFO(Chief Financial Officer) 首席财务官Financial statement 财务报表(Statement:结算单,报表)Internal control 内部控制Internal auditing 内部审计Bookkeeping 簿记Professional ethics 职业道德Transaction 交易,事务Conceptual framework of financial accounting 财务会计概念框架Objectives of financial reporting by business enterprise 企业编制财务报告的目标Qualitative characteristics of accounting information 会计信息的质量特征Basic assumptions of accounting 会计的基本假设Basic principles of accounting 会计的基本原则Prescribe v.规定,开处方Coherent system 协调一致的系统Interrelated objectives 相互联系的目标Fundamental 基本原理,基本原则Consistent standards 一致的标准New and emerging practical problems 新的和突出的问题Securities 有价证券Securities and Exchange Commission (SEC) 美国证券交易委员会Acquiesce v.默许Stock 股票Statement of Financial Accounting Concepts (SFAC) 美国财务会计概念公告Statement of Financial Accounting Standards (SFASs) 美国财务会计准则公告Interpretation of the SFASs 美国财务会计准则公告解释Facilitate v.促进,帮助Evenhanded 公平的Allocate v.分配Scarce resource 稀有资源Adopt v.采取Constraints 制约因素Hierarchy 等级制度Pervasive 普遍的Threshold 门槛,起点,开端Criterion 评判的标准,尺度Decision-making 有关决策制定的Sequence 顺序Accounting procedure 会计程序Interval n.间隔、间距、幕间休息第二部分:专业的会计词汇Entry 分录Make an accounting entryClosing entry 结账分录Contra entry 抵消分录(contra n.相反,对立面)Adjusting entry 调整分录Entry price 入账价值Entry document 记账凭证Journalize v.登记日记账Journal n.日记账,序时账Journal entry 日记账分录Cash journal 现金日记账Post v.过账Posting is the process that debits and credits are transferred from the journal to the ledger accounts.Ledger accounts n.分类账Account n.账户Trial balance 试算平衡表Item n.项目Double-entry accounting 复式记账法Single-entry accounting 单式记账法Bookkeeping 簿记Debit (Dr.) v.借记n.借方Debit balance 借方余额Credit (Cr.) v.贷记n.贷方Credit balance 贷方余额Credit card 信用卡T-account T字形账户Accounting equation 会计等式,会计方程式Chronological adj.依时间前后排列而记载的Source document 原始凭证Verify v.核实,查证Format 格式General journal 普通日记账Special journal 特殊日记账Column 纵队,列;专栏;圆柱,柱形物Enter v.记账Premium 保险费;(正常价格或费用以外的)加付款,加价;额外补贴,津贴;奖金Ref. =reference 摘要Subsidiary ledger account 辅助分类账subsidiary adj.辅助的Trial balance 试算平衡表Erroneous adj.错误的,不正确的Balance sheet accounts 资产负债表账户Permanent (real) accounts 实账户Income statement accountsTemporary (nominal) accounts 虚账户Close sth to sth = transfer sth to sth 转移,转账Rental 租金Plus 加Less 减Add 加Deduct 减Minus 减Financial statements include:1. The balance sheet 资产负债表2. The income statement 利润表3. The statement of changes in owner ’s equity 所有者权益变动表4. The statement of cash flows 现金流量表(财务报表的编制内容十分复杂,尤其是现金流量表的编制,具体编制和内容将单独讲授,会尽量结合国际原则进行综合,同时应用中英双语。

常用会计英语词汇汇总