成本核算-4(常用Excel模板)

成本核算表格范例

成本核算表格范例1、生产部/车体总装科部门名称生产部/车体总装科填表日期 2001年1月30日资源名称计划数(实际数)总金额动因名称计量单位总动因数量分配权数成本对象名称分配金额100000 人工小时小时 20000 3000 WMC100/M1 15000.00 工资4000 WMC125/M4 20000.005000 WMC150/M6 25000.001000 质量预防成本 5000.003000 质量内部故障损失成本 15000.001500 非正常效率损失成本 7500.002500 正常效率损失成本 12500.003000 按金额分配人民币 3000 3000 废品质量内部故障损失成本 3000.00 次品 1000 按金额分配人民币 1000 1000 质量内部故障损失成本 1000.00半成品占用利息 5000 按金额分配人民币 5000 5000 资金占用成本 5000.00 说明:填表人审核人部门负责人生产部/车体总装科成本汇总:helping build the team, set up an accurate poverty alleviation mechanisms, implementing the requirements of accurate poverty alleviation. Four is the enterprise attaches great importance topeople's livelihood. More limited financial resources on the people's livelihood, actively promote the development of social undertakings suchas education, medical and health, completed the "ten's project" strengthening of low-income housing, public rental housing, renovate rural and earthquake resistant housing projects to improve people's housing conditions; further prosperity and development of cultural undertakings and cultural inheritance, protection, rescue and development. Five is fully engaged in the urban and rural environment. Working casually parked vehicles, trash, littering or abandoning, noise is disturbing, and so on. Completed the Township resident Street solar street lights, clear drains sludge, construction of latrines, waste incineration pool, advancing street lighting, landscaping, cleaning, hardening, improve rural human settlement environment. The six are working together to fight against natural disasters. To respond calmly and properly "8.05" wangji du Village and "8.20" ancient village torrent debris flow disasters. Before the disaster, and township Party Committee team members, party members and cadres reserve militia, armed police officers and men, the courage to dash the danger zone, dared to 合计项目计划金额实际金额金额差异(计划-实际)WMC100/M1 15000.00 15000.00 0.00WMC125/M4 20000.00 20000.00 0.00WMC150/M6 25000.00 25000.00 0.00质量预防成本 5000.00 5000.00 0.00质量内部故障损失成本 19000.00 19000.00 0.00非正常效率损失成本 7500.00 7500.00 0.00正常效率损失成本 12500.00 12500.00 0.00资金占用成本 5000.00 5000.00 0.00合计 109000.00 109000.00 0.002、生产部/发动机装配科部门名称生产部/发动机装配科填表日期 2001年1月30日资源名称计划数(实际数)总金额动因名称计量单位总动因数量分配权数成本对象名称分配金额43000 人工小时小时 10000 1000 100发动机 4300.00 工资2000 125发动机 8600.003000 150发动机 12900.00500 质量预防成本 2150.001000 质量内部故障损失成本 4300.001500 非正常效率损失成本 6450.001000 正常效率损失成本 4300.00废品 2000 按金额分配人民币 2000 2000 质量内部故障损失成本 2000.00 次品 500 按金额分配人民币 500 500 质量内部故障损失成本 500.00 helping build the team, set up an accurate poverty alleviation mechanisms, implementing the requirements of accurate poverty alleviation. Four is the enterprise attaches great importance topeople's livelihood. More limited financial resources on the people's livelihood, actively promote the development of social undertakings such as education, medical and health, completed the "ten's project" strengthening of low-income housing, public rental housing, renovate rural and earthquake resistant housing projects to improve people's housing conditions; further prosperity and development of culturalundertakings and cultural inheritance, protection, rescue and development. Five is fully engaged in the urban and rural environment. Working casually parked vehicles, trash, littering or abandoning, noise is disturbing, and so on. Completed the Township resident Street solar street lights, clear drains sludge, construction of latrines, waste incineration pool, advancing street lighting, landscaping, cleaning, hardening, improve rural human settlement environment. The six are working together to fight against natural disasters. To respond calmly and properly "8.05" wangji du Village and "8.20" ancient village torrent debris flow disasters. Before the disaster, and township Party Committee team members, party members and cadres reserve militia, armed police officers and men, the courage to dash the danger zone, dared to 半成品占用利息 3000 按金额分配人民币 3000 3000 资金占用成本 3000.00 说明:填表人审核人部门负责人生产部/发动机装配科成本汇总:合计项目计划金额实际金额金额差异(计划-实际)100发动机 4300.00 4300.00 0.00125发动机 8600.00 8600.00 0.00150发动机 12900.00 12900.00 0.00质量预防成本 2150.00 2150.00 0.00质量内部故障损失成本 6800.00 6800.00 0.00非正常效率损失成本 6450.00 6450.00 0.00正常效率损失成本 4300.00 4300.00 0.00资金占用成本 3000.00 3000.00 0.00合计 48500.00 48500.00 0.003、品质管理部helping build the team, set up an accurate poverty alleviation mechanisms, implementing the requirements of accurate poverty alleviation. Four is the enterprise attaches great importance topeople's livelihood. More limited financial resources on the people's livelihood, actively promote the development of social undertakings such as education, medical and health, completed the "ten's project" strengthening of low-income housing, public rental housing, renovate rural and earthquake resistant housing projects to improve people's housing conditions; further prosperity and development of cultural undertakings and cultural inheritance, protection, rescue and development. Five is fully engaged in the urban and rural environment. Working casually parked vehicles, trash, littering or abandoning, noise is disturbing, and so on. Completed the Township resident Street solar street lights, clear drains sludge, construction of latrines, waste incineration pool, advancing street lighting, landscaping, cleaning, hardening, improve rural human settlement environment. The six are working together to fight against natural disasters. To respond calmly and properly "8.05" wangji du Village and "8.20" ancient village torrent debris flow disasters. Before the disaster, and township Party Committee team members, party members and cadres reserve militia, armed police officers and men, the courage to dash the danger zone, dared to部门名称: 品质管理部填表日期: 2001年1月30日资源名称计划数(实际数)总金额动因名称计量单位总动因数量分配权数成本对象名称分配金额工资 57270.24 按比例分配比例 100 40 质量预防成本 22908.1060 质量鉴定成本 34362.141467 按金额分配人民币 1467 0 差旅费质量预防成本 0.001467 质量鉴定成本 1467.00试验检验费 595.3 按金额分配人民币 595.3 595.3 质量鉴定成本 595.30 其他 12571.64 按金额分配人民币 12571.64 12571.64 质量鉴定成本12571.64按金额分配人民币 20000 20000 20000 质量内部故障损失成本 20000.00 处理质量事故费用说明:1、质量管理直接费用/工资(应发)= 部室 + 车体品质科 + 发动机测功室 + 发动机品质科 + 发动机收货组 + 返聘 + 附加2、质量管理直接费用/其他= 折旧+文具+办公费+电话+业务招待+公务车+低值品+劳动保护填表人: 审核人部门负责人品质管理部成本汇总:项目计划金额实际金额金额差异(计划-实际)质量预防成本 22908.10 22908.10 0.00质量鉴定成本 48996.08 48996.08 0.00质量内部故障损失成本 20000.00 20000.00 0.00合计 91904.18 91904.18 0.004、配套部(表1)helping build the team, set up an accurate poverty alleviation mechanisms, implementing the requirements of accurate poverty alleviation. Four is the enterprise attaches great importance topeople's livelihood. More limited financial resources on the people's livelihood, actively promote the development of social undertakings such as education, medical and health, completed the "ten's project" strengthening of low-income housing, public rental housing, renovate rural and earthquake resistant housing projects to improve people's housing conditions; further prosperity and development of cultural undertakings and cultural inheritance, protection, rescue and development. Five is fully engaged in the urban and rural environment. Working casually parked vehicles, trash, littering or abandoning, noise is disturbing, and so on. Completed the Township resident Street solar street lights, clear drains sludge, construction of latrines, waste incineration pool, advancing street lighting, landscaping, cleaning, hardening, improve rural human settlement environment. The six are working together to fight against natural disasters. To respond calmly and properly "8.05" wangji du Village and "8.20" ancient village torrent debris flow disasters. Before the disaster, and township Party Committee team members, party members and cadres reserve militia, armed police officers and men, the courage to dash the danger zone, dared to 部门名称配套部填表日期 2001年1月30日资源名称计划数(实际数) 总金额动因名称计量单位总动因数量分配权数成本对象名称分配金额工资 36000 按比例分配比例 100 20 发动机零部件采购 7200.0080 车体零部件采购 28800.0010000 按比例分配人民币 100 20 发动机零部件采购 2000.00 其他80 车体零部件采购 8000.00质量管理差旅费 4000 按金额分配人民币 4000 1000 质量预防成本 1000.00 3000 质量内部故障损失成本 3000.0020000 按金额分配人民币 20000 20000 原材料占用利息资金占用成本20000.00填表人审核人部门负责人配套部(表2)部门名称配套部填表日期 2001年1月30日作业名称计划数(实际数)总金额动因名称计量单位总动因数量分配权数成本对象名称分配金额发动机零部件采购 9200 人工小时小时 3000 600 100发动机 1840.00 900 125发动机 2760.001500 150发动机 4600.00车体零部件采购 36800 人工小时小时 20000 3000 WMC100/M1 5520.004000 WMC125/M4 7360.005000 WMC150/M6 9200.00填表人审核人部门负责人配套部成本汇总:helping build the team, set up an accurate poverty alleviation mechanisms, implementing the requirements of accurate poverty alleviation. Four is the enterprise attaches great importance topeople's livelihood. More limited financial resources on the people'slivelihood, actively promote the development of social undertakings such as education, medical and health, completed the "ten's project" strengthening of low-income housing, public rental housing, renovate rural and earthquake resistant housing projects to improve people's housing conditions; further prosperity and development of cultural undertakings and cultural inheritance, protection, rescue and development. Five is fully engaged in the urban and rural environment. Working casually parked vehicles, trash, littering or abandoning, noise is disturbing, and so on. Completed the Township resident Street solar street lights, clear drains sludge, construction of latrines, waste incineration pool, advancing street lighting, landscaping, cleaning, hardening, improve rural human settlement environment. The six are working together to fight against natural disasters. To respond calmly and properly "8.05" wangji du Village and "8.20" ancient village torrent debris flow disasters. Before the disaster, and township Party Committee team members, party members and cadres reserve militia, armed police officers and men, the courage to dash the danger zone, dared to 合计项目计划金额实际金额金额差异(计划-实际)WMC100/M1 5520.00 5520.00 0.00WMC125/M4 7360.00 7360.00 0.00WMC150/M6 9200.00 9200.00 0.00100发动机 1840.00 1840.00 0.00125发动机 2760.00 2760.00 0.00150发动机 4600.00 4600.00 0.00质量预防成本 1000.00 1000.00 0.00质量内部故障损失成本 3000.00 3000.00 0.00资金占用成本 20000.00 20000.00 0.00合计 55280.00 55280.00 0.005、营业部/销售一科部门名称营业部/销售一科填表日期 2001年1月30日资源名称计划数(实际数)总金额动因名称计量单位总动因数量分配权数成本对象名称分配金额工资 8000 按比例分配比例 100 20 销售地区/江西 1600.0020 销售地区/江苏 1600.0020 销售地区/山东 1600.0020 销售地区/浙江 1600.0020 销售地区/安徽 1600.00促销奖 12000 按比例分配比例 100 15 销售地区/江西 1800.00 helping build the team, set up an accurate poverty alleviation mechanisms, implementing the requirements of accurate poverty alleviation. Four is the enterprise attaches great importance to people's livelihood. More limited financial resources on the people's livelihood, actively promote the development of social undertakings such as education, medical and health, completed the "ten's project" strengthening of low-income housing, public rental housing, renovate rural and earthquake resistant housing projects to improve people's housing conditions; further prosperity and development of cultural undertakings and cultural inheritance, protection, rescue and development. Five is fully engagedin the urban and rural environment. Working casually parked vehicles, trash, littering or abandoning, noise is disturbing, and so on. Completed the Township resident Street solar street lights, clear drains sludge, construction of latrines, waste incineration pool, advancing street lighting, landscaping, cleaning, hardening, improve rural human settlement environment. The six are working together to fight against natural disasters. To respond calmly and properly "8.05" wangji du Village and "8.20" ancient village torrent debris flow disasters. Before the disaster, and township Party Committee team members, party members and cadres reserve militia, armed police officers and men, the courage to dash the danger zone, dared to20 销售地区/江苏 2400.0010 销售地区/山东 1200.0045 销售地区/浙江 5400.0010 销售地区/安徽 1200.00广告费 180000 按比例分配比例 100 15 销售地区/江西 27000.0020 销售地区/江苏 36000.0010 销售地区/山东 18000.0045 销售地区/浙江 81000.0010 销售地区/安徽 18000.00 销售费用/运杂费 16000 按金额分配人民币16000 2000 销售地区/江西 2000.005000 销售地区/江苏 5000.004000 销售地区/山东 4000.002000 销售地区/浙江 2000.001000 销售地区/安徽 1000.002000 非正常效率损失成本 2000.00 成品占用利息 6000 按比例分配比例100 100 资金占用成本 6000.00 说明:促销奖的分配权数按实际发生数构成分配,该实际发生数与当地销售数量从正比。

生产成本核算Excel模板(1)

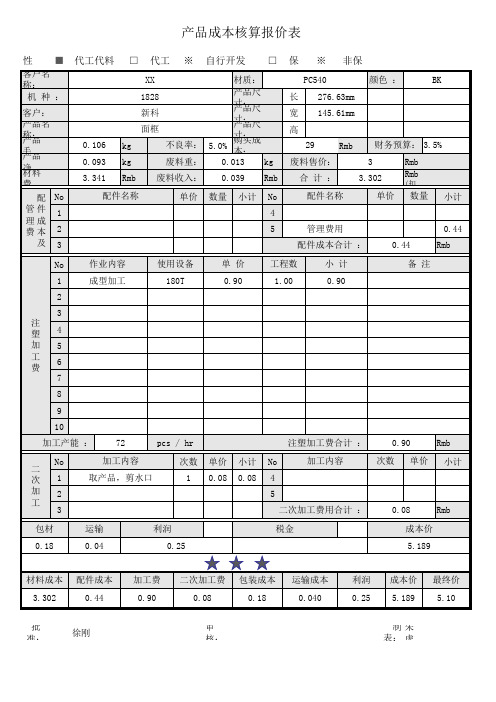

制朱 表: 虎

kg

废料重: 0.013 kg

Rmb 废料收入: 0.039 Rmb

配件名称

单价 数量 小计 No 4 5

保 ※ 非保

PC540

颜色 :

BK

长 276.63mm

宽 145.61mm

高

29

Rmb 财务预算: 3.5%

废料售价: 合计: 配件名称

3 3.302

单价

Rmb Rmb

(扣

数量

小计

管理费用 配件成本合计 :Βιβλιοθήκη 加工内容45

二次加工费用合计 :

次数 单价 小计

0.08

Rmb

包材 0.18

运输 0.04

利润 0.25

税金

成本价 5.189

材料成本 配件成本

3.302

0.44

加工费 0.90

二次加工费 包装成本

0.08

0.18

运输成本 0.040

批 准:

徐刚

审 核:

利润 0.25

成本价 5.189

最终价 5.10

0.44

0.44 Rmb

No

作业内容

1

成型加工

2

3 注 塑4

加5

工 费

6

7

8

9

10

加工产能 : 72

使用设备 180T

单价 0.90

工程数 1.00

小计 0.90

备注

pcs / hr

注塑加工费合计 :

0.90

Rmb

No 二 次1

加2 工

3

加工内容 取产品,剪水口

次数 1

单价 0.08

小计 0.08

生产型企业成本核算表格模板-概述说明以及解释

生产型企业成本核算表格模板-范文模板及概述示例1:生产型企业成本核算表格模板在生产型企业中,成本核算是一个非常重要的管理工具,它可以帮助企业管理者全面了解企业的生产成本情况,从而做出合理的决策。

为了帮助生产型企业进行成本核算工作,我们提供了一个成本核算表格模板,帮助企业管理者快速准确地进行成本核算。

成本核算表格模板包括以下内容:1.直接材料成本:列出所用的直接材料名称、单位价格、使用数量以及总成本。

2.直接人工成本:列出所用的直接人工工种、工资标准及时间、使用工时以及总成本。

3.制造费用:列出制造费用项目,包括设备折旧、设备维护、生产设备租赁等费用,以及总成本。

4.产品成本汇总:将直接材料成本、直接人工成本和制造费用汇总,得出产品总成本。

5.单位产品成本:将产品总成本除以生产数量,得出单位产品成本。

通过以上成本核算表格模板,生产型企业管理者可以清晰地了解生产成本的构成和相关数值,从而形成合理的成本控制和利润提升策略。

希望这份模板能够帮助到您的企业,提升管理效率和经济效益。

示例2:生产型企业成本核算表格模板是为了帮助企业有效地管理和控制成本,提高生产效率和盈利能力而设计的一种工具。

通过填写成本核算表格,企业可以清晰地了解生产过程中的各个环节的成本情况,从而及时调整生产计划和控制成本。

该模板通常包括以下内容:1. 生产成本分类:包括直接材料成本、直接人工成本、制造费用等各项成本的分类。

2. 成本计算公式:根据企业个别情况,可以设置不同的成本计算公式,用于计算各类成本。

3. 成本占比分析:通过计算各项成本的占比,帮助企业了解各项成本在总成本中的比重,以便及时调整成本结构。

4. 成本控制措施:根据成本核算表格的分析结果,制定相应的成本控制措施,以降低成本、提高效益。

5. 成本核算结果:最终得出生产过程中的总成本和单位产品成本,帮助企业进行经营决策。

通过使用生产型企业成本核算表格模板,企业可以更加科学地管理成本,提高生产效率,增加盈利能力,更好地适应市场竞争的激烈情况。

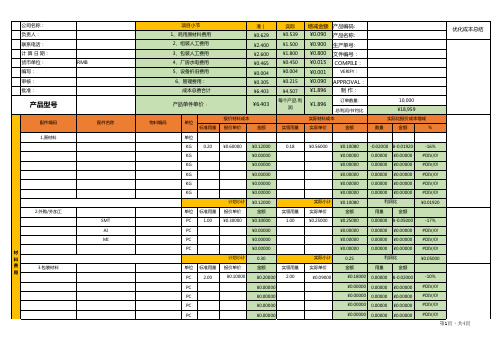

产品成本预算核算表excel模板

物料编码

单位 标准用量

计划(标 准)

¥0.629 ¥2.400 ¥2.600 ¥0.465 ¥0.004 ¥0.305 ¥6.403

¥6.403

报价材料成本 报价单价

金额

实际 ¥0.539 ¥1.500 ¥1.800 ¥0.450 ¥0.004

增减金额 产品编码:

¥0.090 产品名称:

-38% #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! ¥0.90000

单位

报价组装制造成本

标准工时 每小时成本

金额

实际组装制造成本

实际工时

每小时成本

金额

实际比标准增减

工时差额 金额

%

H 0.13000 ¥20.00000

H

H

单位

报价包装费用总计 报价成本

面积/用量

0.00 0.00 0.00 0.00 0.00 0.00 ¥0.00350

0.00000 ¥-0.00050 0.00000 ¥0.00000 0.00000 ¥0.00000 0.00000 ¥0.00000 0.00000 ¥0.00000 0.00000 ¥0.00000 总材料节约/利润比

¥0.00000

0.00000 ¥0.00000 #DIV/0!

PC

¥0.00000

计划小计

0.30

实际小计

¥0.00000 0.25

0.00000 ¥0.00000 利润比

#DIV/0! ¥0.05000

单位 标准用量 报价单价

金额

实领用量 实际单价

金额

用量

金额

PC

2.00

完整成本核算表模板

完整成本核算表模板

温馨提示:文档内容仅供参考

以下是一个基本的完整成本核算表模板:

成本项目金额

原材料成本

直接人工成本

制造费用

- 间接人工费用

- 工厂租金

- 设备折旧

- 能源消耗

销售费用

- 广告费用

- 销售人员工资

- 物流费用

管理费用

- 行政人员工资

- 办公用品费用

- 保险费用

其他费用

- 税金及附加费

- 利息费用

- 其他杂项费用

总成本

这个模板列出了常见的成本项目,你可以根据你的具体业务需求进行调整和添加。

在每个成本项目的金额栏中填写实际的成本金额。

最后,计算所有成本项目的金额总和,得到总成本。

请注意,这只是一个基本的模板,你可能需要根据你的业务需要进行自定义调整。

另外,确保你按照适用的会计准则和法规进行成本核算,以确保准确性和合规性。

excel成本核算表格

excel成本核算表格

成本核算是企业管理中非常重要的一部分,Excel是一个非常

好的工具来创建和管理成本核算表格。

在Excel中,你可以使用各

种函数和工具来进行成本核算,比如SUM函数来计算总成本,AVERAGE函数来计算平均成本,以及PMT函数来计算贷款利息等等。

首先,你可以在Excel中创建一个表格,列出所有的成本项目,比如原材料成本、人工成本、制造成本、销售成本等等。

然后,在

每个成本项目下面创建相应的单元格来输入具体的成本数据。

你可

以使用公式来自动计算一些成本项目,比如总成本等。

另外,你也可以使用Excel的图表功能来可视化成本数据,比

如创建成本分布图、成本趋势图等,这样可以更直观地展示成本的

变化和分布情况。

除此之外,你还可以利用Excel的筛选和排序功能来对成本数

据进行分析和比较,比如找出成本最高的项目、最低的项目,或者

按照时间进行成本的趋势分析等。

总的来说,Excel是一个非常强大的工具,可以帮助你创建和

管理成本核算表格,同时进行各种成本数据的分析和展示。

希望这些信息对你有所帮助。

用Excel做成本核算

用Excel做成本核算成本练习1 - 原材料入库加权平均单价的计算任务背景1.《原材料进销存汇总表》12月库存是根据上年度核算的年末库存,同时作为2018年1月份期初库存,作为已知数据给出。

2.本例中的存货单价采用月底一次加权平均法计算。

3.入库单序时簿是根据1月份库房的入库单及发票序时整理而来,本例中作为已知数据而给出。

01只在月末一次计算加权平均单价,比较简单,有利于简化成本计算工作。

02发出存货的单位成本与期末存货的单位成本一致。

03平时无法从账上提供发出和结存存货的单价及金额,因此不利于存货成本的日常管理与控制。

12月初库存+12月入库-12月出库=12月底库存1月初库存+1月入库-1月出库=1月底库存2月初库存+2月入库-2月出库=2月底库存入库数量单价金额出库数量单价金额库存数量单价金额任务要求1.将《1月份入库单序时簿》中材料的“数量”及“金额”用sumif函数引入至《原材料进销存汇总表》中1月入库“数量”及“金额”里。

使用SUMIF函数可以对报表范围中符合指定条件的值求和。

sumif函数的参数如下:第一个参数:用于条件判断的单元格区域。

第二个参数:由数字、逻辑表达式等组成的判定条件。

第三个参数:为实际求和区域,需要求和的单元格、区域或引用。

2.计算《原材料进销存汇总表》1月份入库单价(月底一次加权平均法),计算公式为:(12月库存金额+1月份入库金额)/(12月库存数量+1月份入库数量)。

3.将计算的一次加权平均单价复制粘贴到出库单价及库存单价里,作为核算出库单位成本及库存材料单位成本的依据。

成本练习2 - 原材料入库单汇总表的制作及会计分录任务背景1.入库单序时簿是根据1月份库房的入库单及发票序时整理而来,本例子作为已知数据而给出。

任务要求1.根据《1月份入库单序时簿》,原材料名称为行标签汇总统计每种原材料的不含税入库金额。

2.根据《1月份入库单序时簿》,以供应商名称为行标签汇总统计每家供应商1月份供货的含税金额。

公司成本核算表格模板

管理费用小计: 成本费用小计:

计划分摊制造成本

标准工时 分摊额

金额

实际分摊制造成本

实际工时 分摊额

金额

实际比标准成本增减

工时

金额

%

计划分摊管理成本

标准工时 分摊额

金额

实际分摊管理成本

实际工时 分摊额

Байду номын сангаас

金额

实际比标准成本增减

工时

金额

%

XXX公司成本核算表

标准

公司成本核算表模板 耗用原材料小计: 花费工资小计: 制造费用小计:

管理费用小计:

项 目 单件成品净重g

料工费合计: 单件单价:

配件编码

配件名称

物料批号

物料编码

单位

标准材料成本 标准重量 单价

金额

1.原材料

单位

实际

增减金额

产品编码: 产品名称: 生产单号: 订单数量: 完工数量: 货币单位:

金额 金额

实际工时 分摊额

金额

实际人工成本

实际时间 单价

金额

工时

金额

%

实际比标准成本增减

数量

金额

金额

直

接

人

工

费 用

直接人工费用小 计:

制造费用分摊

三 、 制 造 费 用

工作中心

材料组 车床部 五金部 磨光部 包装部 塑胶部

制造费用小计:

管理费用分摊

四 、 管 理 费 用

工作中心

材料组 车床部 五金部 磨光部 包装部 塑胶部

实际材料成本

实际重量 单价

金额

实际比标准成本增减

数量

单价

%

成本核算格式excel模版

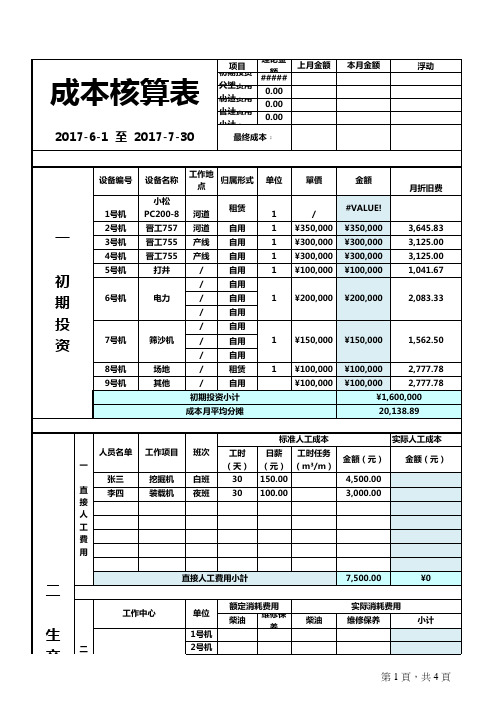

金額 #VALUE! ¥350,000 ¥300,000 ¥300,000 ¥100,000 ¥200,000

月折旧费 3,645.83 3,125.00 3,125.00 1,041.67 2,083.33

河道 河道 产线 产线 / / / / /

租赁 自用 自用 自用 自用 自用 自用 自用 自用 自用 自用 租赁 自用

成本核算表

2017-6-1 至 2017-7-30

设备编号 1号机 2号机

项目

理论金额 上月金额

本月金额

浮动

##### 初期投资分摊: 0.00 人工费用小计﹕ 0.00 制造费用小计﹕ 0.00 管理費用小计﹕ 最终成本﹕

设备名称 工作地点 归属形式

小松PC200-8

单位 1 1 1 1 1 1

單價 / ¥350,000 ¥300,000 ¥300,000 ¥100,000 ¥200,000

晋工757 晋工755 晋工755 打井 电力

一 初 期 投 资

3号机 4号机 5号机 6号机

7号机 8号机 9号机

筛沙机 场地 其他

/ / / /

1 1

¥150,000 ¥100,000 ¥100,000

¥150,000 ¥100,000 ¥100,000

1,562.50 2,777.78 2,777.78

二

工作中心

直接人工費用小計 额定消耗费用 柴油 维修保 养 柴油

7,500.00 实际消耗费用 维修保养

¥0

单位 1号机

生 产 过 程

小计

二 制 造 費

2号机 设备耗材费用 3号机

第 1 頁,共 4 頁

生 产 过 程 成 本

成本核算系统excel模板

11月4日

11月5日

11月6日

11月7日

11月8日

计划 实际 计划 实际 计划 实际 计划 实际 计划 实际 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 投入 投入 投入 投入 投入 投入 投入 投入 投入 投入

11月9日

11月10日

11月30日

12月1日

合计

计划 实际 计划 实际 计划 实际 报废 差值 产出 报废 差值 产出 报废 差值 产出 计划投入 实际投入 报废 投入 投入 投入 投入 投入 投入

产出

理论在制

11月11日

11月12日

11月13日

计划 实际 计划 实际 计划 实际 计划 实际 计划 实际 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 投入 投入 投入 投入 投入 投入 投入 投入 投入 投入

11月14日

11月15日

11月16日

11月17日

11月24日

11月25日

11月26日

11月27日

11月28日

计划 实际 计划 实际 计划 实际 计划 实际 计划 实际 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 投入 投入 投入 投入 投入 投入 投入 投入 投入 投入

11月29日

11月18日

计划 实际 计划 实际 计划 实际 计划 实际 计划 实际 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 投入 投入 投入 投入 投入 0日

11月21日

11月22日

11月23日

计划 实际 计划 实际 计划 实际 计划 实际 计划 实际 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 报废 差值 产出 投入 投入 投入 投入 投入 投入 投入 投入 投入 投入

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

序号 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

费用支出明细 材料消耗费

人工工资 社保

公积金 福利费 折旧费 设备采购费 修理费 交通费 差旅费 办公费 通信费 广告费 招待费 劳务外包费 水电费 利息费 咨询费 诉讼费 其它费用

费用情况 费用增加 费用增加 费用增加 费用增加 费用减少 费用减少 费用减少 费用减少 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加 费用增加

备注

总计

¥

1,860,024.00 ¥

1,818,364.00

2.29%

费用增加

¥

25,000.00 ¥

35,000.00

-28.57%

¥

200,000.00 ¥

235,000.00

-14.89%

¥

50,000.00 ¥

52,352.00

-4.49%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

本年

去年

费用增减

¥

250,000.00 ¥

220,000.00

13.64%

¥

1,200,000.00 ¥

1,160,000.00

3.45%

¥

50,000.00 ¥

45,000.00

11.11%

¥

60,000.00 ¥

45,000.00

33.33%

¥

25,000.00 ¥

26,000.00

-3.85%

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%

¥

2.00 ¥

1.00

100.00%¥来自2.00 ¥1.00

100.00%