会计学原理(英文) principle of accounting

clj会计学原理第17讲

Principle of Accounting CLJ

三、补充登记法

在记账以后,如果 发现原编会计分录中 应借、应贷账户虽然 没有错误,但所写金 额小于正确的金额, 可用补充登记法进行 更正。

将少记的金额编制 一笔与原编会计分 录应借、应贷账户 相同的分录,并注 明补记某月某日某 笔业务的金额,将

Principle of Accounting CLJ

练习:错账更正

1.开出转账支票一张200元,支付管理部门零星开支。 原凭证为:

借:管理费用 200

贷:现金

200

2.用银行存款支付所欠供应单位货款3600元。原编 记账凭证为: 借:应付账款 2 600

贷:银行存款 2 600

Principle of Accounting CLJ

一、记账凭证核算程序

(四)步骤 1.根据原始凭证或原始凭证汇总表填制记账凭证。 2.根据现金收、付款凭证逐笔序时登记现金日记账;根

据银行存款收、付款凭证及其所附的银行结算凭证逐 笔序时登记银行存款日记账。 3.根据原始凭证、原始凭证汇总表及各种记账凭证逐笔 登记各种明细分类账。

Principle of Accounting CLJ

记,还可以每天或定期就科目汇总表进行试算平衡, 以便于及时发现问题,采取措施。 缺点:科目汇总表反映不出账户的对应关系,不便于了 解经济业务的内容。

Principle of Accounting CLJ

练习

1、会计核算形式中最基本、最简单的会计核算形式是( )。

A记账凭证核算形式

B科目汇总表核算形式

其补记入账。

Principle of Accounting CLJ

三、补充登记法

例:销售商品一批,计价款50 000元,货款尚未收到( 不考虑增值税),原编会计分录把金额误写为5000元 ,并已登记入账。

Chapter_01会计学原理答案 principles of accounting 19th edition john j.wild 人大出版社

Importance: GAAP are the rules that specify acceptable accounting

practices.

SEC:

Securities and Exchange Commission

Importance: The SEC is charged by Congress to set reporting rules for

To illustrate, many companies base compensation of managers on the amount of reported income. When the choice of an accounting method affects the amount of reported income, the amount of compensation is also affected. Similarly, if workers in a division receive bonuses based on the division’s income, its computation has direct financial implications for these individuals.

Quick Study 1-7

Assets

=

$375,000 (b) $250,000

$185,000

Liabilities (a) $125,000

$ 90,000 $ 60,000

+

Equity

$250,000

$160,000

(c) $125,000

Quick Study 1-8

Assets

会计学原理PrinciplesofAccounting

两权分离

产生职业会计师 这一时期,向外部关系人提供企业财务状况和盈利及分配情况是企 业会计的中心任务,因而形成了“ 财务会计”概念。

15

‹#›

1.2 会计的概念、会计的内容与特点

1.2.1会计的基本概念

什么是会计?多年来通俗的说法,会计就是记账、算账和 报账。 我国古代“会计”一词产生于西周,主要指对收支活动的 记录、计算、考察和监督。 中国最早对会计进行论述与评价的著名人物的孔子,他曾 主管仓库,提出“会计当而已矣”的名言。 清代学者焦循在《孟子正义》一书中,对“会”和“计” 作过概括性的解释:“零星算为之计,总合算为之会”,

4、文化、教育因素 从文化内容方面讲,一般包括语言、文字、书写工具、计量工 具、数字及经济理论、管理理论等 从教育方面来讲,包括基础文化教育、职业道德教育、会计专 业教育 。

8

1.1.2 会计演进的历史阶段与成就

1、会计的产生 会计萌芽

•

据考证,人类极为简单的原始记录、计量行为(如结绳记事)产生于原始社会末期。

11

1.1.2 会计演进的历史阶段与成就

3)明末清初,设计和创立了一种较为完善的会计核算方法,称为“龙 门账”。 要点是:将全部账目划分为“进、缴、存、该”四大类。 进:收入 缴:支出 存:资产包括债权 该:负债包括业主投资 四类账目的关系是 进- 缴=存- 该

12

1.1.2 会计演进的历史阶段与成就

20

1.3 会计的职能与目标

1.3.1会计的职能

会计的职能,指会计作 为一种管理经济的活动, 本身所具有的功能。会计 的职能有三: 一是会计核算 二是会计监督 三是会计参与经营决策 会计的三种职能的关 系:反映是监督、参与决 策的基础。监督必须借助 于反映,决策更是离不开 反映职能所提供的信息。 1. 反映客观的经济活动情 况,为管理经济提供所 需的信息。 2. 两层含义:会计监督与 监督会计 3、参与经营决策,谋求最优 效益 一个单位要进行经营决策, 会计信息是不可缺少的 依据

会计学原理约翰·J·怀尔德版上海交通大学

Information useful to help the enterprise achieve its goal, objectives and mission.

Types of Accounting Information

Financial Tax

Managerial

Integrity of Accounting Information

提供商品或服务所有者雇员和供应商顾顾客客债权人人目标和战略投资融资经营短期项目?现金?应收账款?存货长期项目?土地?建筑物?设备?专利?股票和债券短期项目?银行?供应商?员工?政府长期项目?长期债权人?股东采购销售生产管理企业活动概述importanceofaccounting

课程要求--教材与辅助资料

Financial Statements

Internal Users

• • • • • • • •

Board of Directors (董事会) Chief Executive Officer Chief Financial Officer Vice Presidents Business Unit Managers Plant Managers Store Managers Line Supervisors

• Conceptual Chapter Objectives • Analytical Chapter Objectives • Procedural Chapter Objectives

The Accounting Process

Economic Activities

Accounting links decision makers with economic activities and with the results of their decisions.

会计学原理Accounting Principle

3、唐宋时期:流水账和眷清账,“四 柱结算法”。 旧管+新收-开除 = 实 在

4、明清时期:“四柱清册” 进-缴 = 存-该

5、近代:引进复式记账方法

二、西方会计的产生

1、起源:中世纪地中海沿岸。 标志——复式记账 卢卡.巴其阿勒—— 《算术、几何与比例概要》

2、演变:佛罗伦萨式、热那亚式、威尼斯式。 3、发展:产业革命。

§1.5 会计假设 assumption

1、会计主体 accounting entity 2、持续经营 going concern 3、会计期间 accounting period 4、货币计量 measuring unit

§1.6 会计信息质量要求

1、客观性 企业应当以实际发生的交易或 事项为依据进行会计确认、计量和报告,如 实反映符合确认核计量要求的各项会计要素 及其他相关信息,保证会计信息真实可靠、 内容完整。

6、重要性 企业提供的会计信息应当反映与 企业财务状况、经营成果和现金流量等有关的 所有重要交易或者事项。

7、谨慎性 企业对交易或事项进行会计确、 计量和报告应当保持应有的谨慎,不应高估 资产或收益、低估负债或费用。

会计学原理(英文)

《会计学原理(英文)》教学大纲王燕祥编写工商管理专业课程教学大纲610 目录Chapter 1 Accounting in Action 第一章会计实践活动 (613)学习目标 (613)Teaching and homework hours 教学与作业时间 (613)Reading and References 学生必读和参考书目 (613)Chapter 2 The Recording Process 第二章记录过程 (615)学习目标 (615)Teaching and homework hours 教学与作业时间 (615)Reading and References 学生必读和参考书目 (615)Chapter 3 Adjusting the Accounts 第三章调整账户 (617)学习目标 (617)Teaching and homework hours 教学与作业时间 (617)Reading and References 学生必读和参考书目 (617)Chapter 4 Completion of the Accounting Cycle 第四章完成会计循环 (619)学习目标 (619)Teaching and homework hours 教学与作业时间 (619)Reading and References 学生必读和参考书目 (619)Chapter 5 Accounting for Merchandising Operations 第五章商品经营活动的会计核算 (621)学习目标 (621)Teaching and homework hours 教学与作业时间 (621)Reading and References 学生必读和参考书目 (621)Chapter 6 Inventories 第六章存货 (623)学习目标 (623)Teaching and homework hours 教学与作业时间 (624)Reading and References 学生必读和参考书目 (624)Chapter 7 Accounting Information Systems 第七章会计信息系统 (626)学习目标 (626)Teaching and homework hours 教学与作业时间 (626)Reading and References 学生必读和参考书目 (626)Chapter 8 Internal Control and Cash 第八章内部控制和现金 (628)学习目标 (628)Teaching and homework hours 教学与作业时间 (628)Reading and References 学生必读和参考书目 (628)Chapter 9 Accounting for Receivables 第九章应收款项的会计核算 (630)学习目标 (630)Teaching and homework hours 教学与作业时间 (630)Reading and References 学生必读和参考书目 (630)Chapter 10 Plant Assets, Natural Resources, and Intangible Assets 第十章厂场资产、自然资源和无形资产 (632)会计学原理(英文)学习目标 (632)Teaching and homework hours 教学与作业时间 (632)Reading and References 学生必读和参考书目 (633)Chapter 11 Current Liabilities and Payroll Accounting 第十一章流动负债和工资的核算 (634)学习目标 (634)Teaching and homework hours 教学与作业时间 (634)Reading and References 学生必读和参考书目 (634)Chapter 12 Accounting Principles 第十二章会计原则 (636)学习目标 (636)Teaching and homework hours 教学与作业时间 (636)Reading and References 学生必读和参考书目 (636)Chapter 13 Accounting for Partnerships 第十三章合伙企业的会计核算 (638)学习目标 (638)Teaching and homework hours 教学与作业时间 (638)Reading and References 学生必读和参考书目 (638)Chapter 14 Corporations: Organization and Capital Stock Transactions 第十四章公司:组织和股本交易 (640)学习目标 (640)Teaching and homework hours 教学与作业时间 (640)Reading and References 学生必读和参考书目 (640)Chapter 15 Corporations: Dividends, Retained Earnings, and Income Reporting 第十五章股利、保留盈余和收益报告 (642)学习目标 (642)Teaching and homework hours 教学与作业时间 (642)Reading and References 学生必读和参考书目 (642)Chapter 16 Long-Term Liabilities 第十六章长期负债 (644)学习目标 (644)Teaching and homework hours 教学与作业时间 (644)Reading and References 学生必读和参考书目 (644)Chapter 17 Investments 第十七章投资 (646)学习目标 (646)Teaching and homework hours 教学与作业时间 (646)Reading and References 学生必读和参考书目 (646)Chapter 18 The Statement of Cash Flows 第十八章现金流量表 (648)学习目标 (648)Teaching and homework hours 教学与作业时间 (648)Reading and References 学生必读和参考书目 (648)Chapter 19 Financial Statement Analysis 第十九章财务报表分析 (650)学习目标 (650)Teaching and homework hours 教学与作业时间 (650)Reading and References 学生必读和参考书目 (650)Chapter 20 Managerial Accounting 第二十章管理会计 (652)611工商管理专业课程教学大纲612 学习目标 (652)Teaching and homework hours 教学与作业时间 (652)Reading and References 学生必读和参考书目 (652)Chapter 21 Job Order Cost Accounting 第二十一章分批成本法 (654)学习目标 (654)Teaching and homework hours 教学与作业时间 (654)Reading and References 学生必读和参考书目 (654)Chapter 22 Process Cost Accounting 第二十二章分步成本法 (656)学习目标 (656)Teaching and homework hours 教学与作业时间 (656)Reading and References 学生必读和参考书目 (657)Chapter 23 Cost-V olume-Profit Relationships 第二十三章本量利分析 (658)学习目标 (658)Teaching and homework hours 教学与作业时间 (658)Reading and References 学生必读和参考书目 (659)Chapter 24 Budgetary Planning 第二十四章编制预算 (660)学习目标 (660)Teaching and homework hours 教学与作业时间 (660)Reading and References 学生必读和参考书目 (660)Chapter 25 Budgetary Control and Responsibility Accounting 第二十五章预算控制和责任会计 662 学习目标 (662)Teaching and homework hours 教学与作业时间 (662)Reading and References 学生必读和参考书目 (662)Chapter 26 Performance Evaluation through Standard Costs 第二十六章利用标准成本进行业绩评价 (664)学习目标 (664)Teaching and homework hours 教学与作业时间 (664)Reading and References 学生必读和参考书目 (664)Chapter 27 Incremental Analysis and Capital Budgeting 第二十七章增量分析和资本预算 (666)学习目标 (666)Teaching and homework hours 教学与作业时间 (667)Reading and References 学生必读和参考书目 (667)会计学原理(英文)Chapter 1 Accounting in Action第一章会计实践活动STUDY OBJECTIVESAfter studying this chapter you should be able to:1.Explain what accounting is.2.IDENTIFY THE USERS AND USES OF ACCOUNTING.3.UNDERSTAND WHY ETHICS IS A FUNDAMENTAL BUSINESS CONCEPT.4.EXPLAIN THE MEANING OF GENERALLY ACCEPTED ACCOUNTING PRINCIPLESAND THE COST PRINCIPLE.5.EXPLAIN THE MEANING OF THE MONETARY UNIT ASSUMPTION AND THE ECONOMIC ENTITY ASSUMPTION.6.STATE THE BASIC ACCOUNTING EQUATION AND EXPLAIN THE MEANING OF ASSETS, LIABILITIES, AND OWNER’S EQUITY.7.ANALYZE THE EFFECT OF BUSINESS TRANSACTIONS ON THE BASIC ACCOUNTING EQUATION.8.Understand what the four financial statements are and how they are prepared.学习目标学完本章之后,学生应该能够达到以下目标:1.解释什么是会计。

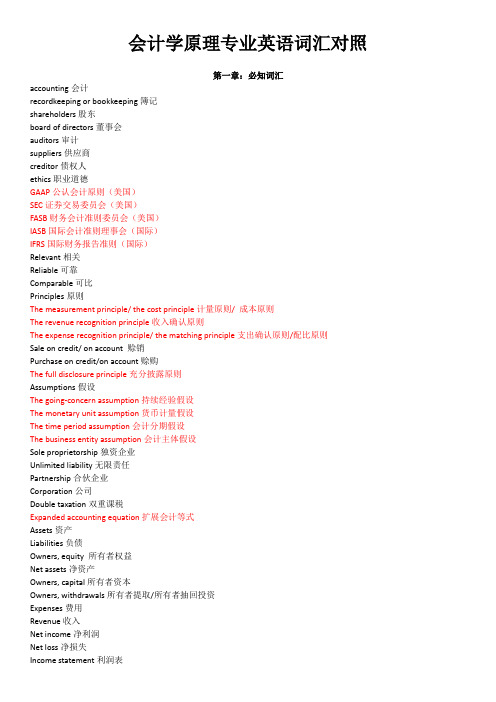

会计学原理专业英语词汇对照(第一二章)

会计学原理专业英语词汇对照第一章:必知词汇accounting会计recordkeeping or bookkeeping簿记shareholders股东board of directors董事会auditors审计suppliers供应商creditor债权人ethics职业道德GAAP公认会计原则(美国)SEC证券交易委员会(美国)FASB财务会计准则委员会(美国)IASB国际会计准则理事会(国际)IFRS国际财务报告准则(国际)Relevant相关Reliable可靠Comparable可比Principles原则The measurement principle/ the cost principle计量原则/ 成本原则The revenue recognition principle收入确认原则The expense recognition principle/ the matching principle支出确认原则/配比原则Sale on credit/ on account 赊销Purchase on credit/on account赊购The full disclosure principle充分披露原则Assumptions假设The going-concern assumption持续经验假设The monetary unit assumption货币计量假设The time period assumption会计分期假设The business entity assumption会计主体假设Sole proprietorship独资企业Unlimited liability无限责任Partnership合伙企业Corporation公司Double taxation双重课税Expanded accounting equation扩展会计等式Assets资产Liabilities负债Owners, equity 所有者权益Net assets净资产Owners, capital所有者资本Owners, withdrawals所有者提取/所有者抽回投资Expenses费用Revenue收入Net income净利润Net loss净损失Income statement利润表Statement of owners, equity所有者权益表/所有者权益变动表Balance sheet资产负债表Statement of cash flows现金流量表第二章:必知词汇(上文有的不再重复)Accounting books/books会计帐簿Source documents原始凭证Account账户General ledger总分类账Ledger分类账Account receivable应收账款Note receivable应收票据Prepaid accounts/ prepaid expenses预付账款/待摊费用Account payable应付账款Note payable应付票据Unearned revenue预收账款Accrued liabilities应计负债Increase增加Decrease减少Chart of accounts会计科目表T-account T形账户Debit借方(Dr.)Credit贷方(Cr.)Account balance账户余额Normal balance正常余额Double entry accounting 复式记账法Journalizing登记日记账Journal日记账General journal普通日记账Journal entry日记账分录Posting过账Balance column account三栏式账户PR(posting reference)过账索引Trial balance试算平衡表Unadjusted statements调整前的财务报表必记口诀:有借必有贷,借贷必相等。

Principle of Accounting 英中互译

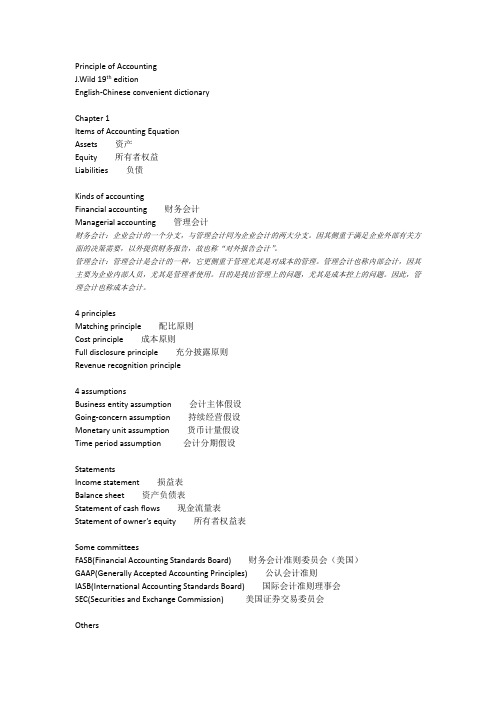

Principle of AccountingJ.Wild 19th editionEnglish-Chinese convenient dictionaryChapter 1Items of Accounting EquationAssets 资产Equity 所有者权益Liabilities 负债Kinds of accountingFinancial accounting 财务会计Managerial accounting 管理会计财务会计:企业会计的一个分支,与管理会计同为企业会计的两大分支。

因其侧重于满足企业外部有关方面的决策需要,以外提供财务报告,故也称“对外报告会计”。

管理会计:管理会计是会计的一种,它更侧重于管理尤其是对成本的管理。

管理会计也称内部会计,因其主要为企业内部人员,尤其是管理者使用。

目的是找出管理上的问题,尤其是成本控上的问题。

因此,管理会计也称成本会计。

4 principlesMatching principle 配比原则Cost principle 成本原则Full disclosure principle 充分披露原则Revenue recognition principle4 assumptionsBusiness entity assumption 会计主体假设Going-concern assumption 持续经营假设Monetary unit assumption 货币计量假设Time period assumption 会计分期假设StatementsIncome statement 损益表Balance sheet 资产负债表Statement of cash flows 现金流量表Statement of owner’s equity 所有者权益表Some committeesFASB(Financial Accounting Standards Board) 财务会计准则委员会(美国)GAAP(Generally Accepted Accounting Principles) 公认会计准则IASB(International Accounting Standards Board) 国际会计准则理事会SEC(Securities and Exchange Commission) 美国证券交易委员会OthersCommon stock 普通股股票Ethics 伦理External users 外部使用者Internal users 内部使用者Chapter 2~4Compound journal entry 复合分录T-account T型账户Posting reference (PR) column 过账根据栏Interim financial statements 期中财务报表LedgerLedger 分类账General ledger 总分类账Subsidiary ledger 辅助分类账(chpt7)AdjustingAdjusting entry 调整分录。

会计学原理双语142AccountingPrinciplesSYLLABUS

Jiangxi University of Finance and EconomicsSchool of International Trade and Economics SYLLABUSCourse Title: Principles of AccountingCourse Code: 02016Semester: 142Class No.: AE1Credits: 6Teaching Hours: 64Class Times: Tuesday 8:00am-9:40am, Friday 10:20am-12:00pm Prerequisites: NoneLecturer's InformationName: Dr. Ling JiangEmail : ljiang@Course Description and ObjectivesThis is an introductory financial accounting course. In today's economy, basic accountingknowledge is useful to students of various disciplines, especially those who are in the businessfield. This course is an opportunity of gaining an understanding of the many details ofoperation of a business entity from a financial information perspective. The focus is on thepreparation of corporate financial statements and interpreting the information by simple analyses.It is a prerequisite to more advanced accounting and business courses.Learning OutcomesUpon completion of the course, a student should achieve the following learning outcomes:Understand the operation of the accounting cycle.Understand how to account for business transactions.Understand how to prepare financial statements.Understand how to analyze a business entity's financial condition and operating results by usingfinancial statement information.Develop accounting-related critical thinking, problem solving, and ethical reasoning skills.1Teaching MethodsTeaching methods include formal lecture, group work, individual exercise, and class discussion.AssessmentFinal Examination 50%20% Mid-Term Examination10% Test 110% Test 210% Homework assignments, attendance, and class participation100%TotalTo obtain a passing grade, a student should achieve at least 60% in total.Tests and ExaminationsTests and Examinations will be held when the related learning content has been completed. Test1 covers chapters 1-4, Mid-Term Exam covers chapter 1-7, Test2 covers chapters 8-11, and theFinal Exam will focus on chapters 8-14, plus limited coverage on chapters 1-7. Homework, Attendance, and Class ParticipationIn-class exercises are opportunities to put chapter knowledge to practice. These can includegroup work, individual exercises, and case discussions. Homework problems are assigned toprovide additional exercises.Your InputYou will be expected to:Participate actively in group work, individual exercises, and class discussions. Complete homework assignments, and submit printed copies when they are due. Review textbook chapters, PowerPoint slides, and other study materials.Course outlineChapter 1 Accounting in BusinessChapter 2 Analyzing and Recording Transactions2Chapter 3 Adjusting Accounts and Preparing Financial StatementsChapter 4 Completing the Accounting CycleChapter 5 Accounting for Merchandising OperationsChapter 6 Inventories and Cost of SalesChapter 7 Accounting Information SystemChapter 8 Cash and Internal ControlsChapter 9 Accounting for ReceivablesChapter 10 Plant Assets, Natural Resources, and IntangiblesChapter 11 Current Liabilities and Payroll AccountingChapter 12 Long-Term LiabilitiesChapter 13 Investments and International OperationsChapter 14 Accounting for CorporationsTextbookJohn J. Wild, Ken W. Shaw, and Barbara Chiappetta, “Fundamental Accounting Principles,”21stedition, revised by Xuegang Cui and Qing Rao, English language reprint edition, McGraw-HillEducation (Asia) Co. and China Renmin University Press, 2013.Tentative Schedule34。

《会计学原理》课程教学大纲

《会计学原理》课程教学大纲课程代码:ABGS0380课程中文名称:会计学原理英文英文名称:Accounting Principles课程性质:必修课程学分数:3课程学时:48授课对象:信息管理与信息系统本课程的前导课程:管理学一、课程简介《初级会计学》课程是会计学、财务管理专业学生学习会计学知识的入门课程,该课程重点讲解会计学的基本原理以及在企业当中会计职能展开的基本方法和程序。

要求学生明确会计的基本职能和特点,掌握会计核算的基本原理和方法,认识到做好会计工作对加强经济管理,提高经济效益的重要意义。

《基础会计》是一门实用性很强的课程,学习时要着重掌握会计核算各种基本原理和方法,既要知其然,又要知其所以然。

既学会独立操作整个账务处理程序,又理解其中的基本理论,学习《初级会计学》为进一步学习其它会计课程和财务管理课程打下坚实的基础。

二、教学基本内容和要求(一)总论课程教学内容:会计的基本概念:会计的产生和发展,会计职能,会计特点,会计的含义。

会计对象:会计对象的一般要求,企业经营资金运动过程。

会计的目的与任务:会计的目的,会计的任务。

会计假设:会计主体,持续经营,会计分期,货币计量。

会计的一般原则:客观性原则,相关性原则,可比性原则,一贯性原则,及时性原则,明晰性原则,权责发生制原则,配比性原则,谨慎性原则,实际成本原则,划分收益性支出和资本性支出的原则,重要性原则,实质重于形式原则。

会计的基本方法(会计核算的方法):设置账户,复式记账,填制和审核凭证,登记账簿,成本计算,财产清查,财务会计报告。

课程的重点、难点:本章重点:会计的涵义、会计假设、会计的一般原则、会计的基本方法。

本章难点:会计假设、会计的一般原则。

课程教学要求:了解会计的基本概念;理解会计概念框架各概念之间的逻辑关系,尤其是每项会计假设和原则的含义,以及如何将经济活动信息转化成会计语言的方法体系;掌握会计基本概念框架。

(二)账户与复式记账的基本原理课程教学内容:会计要素:会计要素定义,会计要素构成及各要素的定义。

会计学原理(英文)

《会计学原理(英文)》教学大纲王燕祥编写工商管理专业课程教学大纲610 目录Chapter 1 Accounting in Action 第一章会计实践活动 (613)学习目标 (613)Teaching and homework hours 教学与作业时间 (613)Reading and References 学生必读和参考书目 (613)Chapter 2 The Recording Process 第二章记录过程 (615)学习目标 (615)Teaching and homework hours 教学与作业时间 (615)Reading and References 学生必读和参考书目 (615)Chapter 3 Adjusting the Accounts 第三章调整账户 (617)学习目标 (617)Teaching and homework hours 教学与作业时间 (617)Reading and References 学生必读和参考书目 (617)Chapter 4 Completion of the Accounting Cycle 第四章完成会计循环 (619)学习目标 (619)Teaching and homework hours 教学与作业时间 (619)Reading and References 学生必读和参考书目 (619)Chapter 5 Accounting for Merchandising Operations 第五章商品经营活动的会计核算 (621)学习目标 (621)Teaching and homework hours 教学与作业时间 (621)Reading and References 学生必读和参考书目 (621)Chapter 6 Inventories 第六章存货 (623)学习目标 (623)Teaching and homework hours 教学与作业时间 (624)Reading and References 学生必读和参考书目 (624)Chapter 7 Accounting Information Systems 第七章会计信息系统 (626)学习目标 (626)Teaching and homework hours 教学与作业时间 (626)Reading and References 学生必读和参考书目 (626)Chapter 8 Internal Control and Cash 第八章内部控制和现金 (628)学习目标 (628)Teaching and homework hours 教学与作业时间 (628)Reading and References 学生必读和参考书目 (628)Chapter 9 Accounting for Receivables 第九章应收款项的会计核算 (630)学习目标 (630)Teaching and homework hours 教学与作业时间 (630)Reading and References 学生必读和参考书目 (630)Chapter 10 Plant Assets, Natural Resources, and Intangible Assets 第十章厂场资产、自然资源和无形资产 (632)会计学原理(英文)学习目标 (632)Teaching and homework hours 教学与作业时间 (632)Reading and References 学生必读和参考书目 (633)Chapter 11 Current Liabilities and Payroll Accounting 第十一章流动负债和工资的核算 (634)学习目标 (634)Teaching and homework hours 教学与作业时间 (634)Reading and References 学生必读和参考书目 (634)Chapter 12 Accounting Principles 第十二章会计原则 (636)学习目标 (636)Teaching and homework hours 教学与作业时间 (636)Reading and References 学生必读和参考书目 (636)Chapter 13 Accounting for Partnerships 第十三章合伙企业的会计核算 (638)学习目标 (638)Teaching and homework hours 教学与作业时间 (638)Reading and References 学生必读和参考书目 (638)Chapter 14 Corporations: Organization and Capital Stock Transactions 第十四章公司:组织和股本交易 (640)学习目标 (640)Teaching and homework hours 教学与作业时间 (640)Reading and References 学生必读和参考书目 (640)Chapter 15 Corporations: Dividends, Retained Earnings, and Income Reporting 第十五章股利、保留盈余和收益报告 (642)学习目标 (642)Teaching and homework hours 教学与作业时间 (642)Reading and References 学生必读和参考书目 (642)Chapter 16 Long-Term Liabilities 第十六章长期负债 (644)学习目标 (644)Teaching and homework hours 教学与作业时间 (644)Reading and References 学生必读和参考书目 (644)Chapter 17 Investments 第十七章投资 (646)学习目标 (646)Teaching and homework hours 教学与作业时间 (646)Reading and References 学生必读和参考书目 (646)Chapter 18 The Statement of Cash Flows 第十八章现金流量表 (648)学习目标 (648)Teaching and homework hours 教学与作业时间 (648)Reading and References 学生必读和参考书目 (648)Chapter 19 Financial Statement Analysis 第十九章财务报表分析 (650)学习目标 (650)Teaching and homework hours 教学与作业时间 (650)Reading and References 学生必读和参考书目 (650)Chapter 20 Managerial Accounting 第二十章管理会计 (652)611工商管理专业课程教学大纲612 学习目标 (652)Teaching and homework hours 教学与作业时间 (652)Reading and References 学生必读和参考书目 (652)Chapter 21 Job Order Cost Accounting 第二十一章分批成本法 (654)学习目标 (654)Teaching and homework hours 教学与作业时间 (654)Reading and References 学生必读和参考书目 (654)Chapter 22 Process Cost Accounting 第二十二章分步成本法 (656)学习目标 (656)Teaching and homework hours 教学与作业时间 (656)Reading and References 学生必读和参考书目 (657)Chapter 23 Cost-V olume-Profit Relationships 第二十三章本量利分析 (658)学习目标 (658)Teaching and homework hours 教学与作业时间 (658)Reading and References 学生必读和参考书目 (659)Chapter 24 Budgetary Planning 第二十四章编制预算 (660)学习目标 (660)Teaching and homework hours 教学与作业时间 (660)Reading and References 学生必读和参考书目 (660)Chapter 25 Budgetary Control and Responsibility Accounting 第二十五章预算控制和责任会计 662 学习目标 (662)Teaching and homework hours 教学与作业时间 (662)Reading and References 学生必读和参考书目 (662)Chapter 26 Performance Evaluation through Standard Costs 第二十六章利用标准成本进行业绩评价 (664)学习目标 (664)Teaching and homework hours 教学与作业时间 (664)Reading and References 学生必读和参考书目 (664)Chapter 27 Incremental Analysis and Capital Budgeting 第二十七章增量分析和资本预算 (666)学习目标 (666)Teaching and homework hours 教学与作业时间 (667)Reading and References 学生必读和参考书目 (667)会计学原理(英文)Chapter 1 Accounting in Action第一章会计实践活动STUDY OBJECTIVESAfter studying this chapter you should be able to:1.Explain what accounting is.2.IDENTIFY THE USERS AND USES OF ACCOUNTING.3.UNDERSTAND WHY ETHICS IS A FUNDAMENTAL BUSINESS CONCEPT.4.EXPLAIN THE MEANING OF GENERALLY ACCEPTED ACCOUNTING PRINCIPLESAND THE COST PRINCIPLE.5.EXPLAIN THE MEANING OF THE MONETARY UNIT ASSUMPTION AND THE ECONOMIC ENTITY ASSUMPTION.6.STATE THE BASIC ACCOUNTING EQUATION AND EXPLAIN THE MEANING OF ASSETS, LIABILITIES, AND OWNER’S EQUITY.7.ANALYZE THE EFFECT OF BUSINESS TRANSACTIONS ON THE BASIC ACCOUNTING EQUATION.8.Understand what the four financial statements are and how they are prepared.学习目标学完本章之后,学生应该能够达到以下目标:1.解释什么是会计。

会计学原理课程课程简介(02704)

中文名称:会计学原理

英文名称:Principles of Accounting

开课学院:会计学院

课程代码:02704学分:4开课学期:1/2/3学期预修课程:无

课程类别:学科基础课

内容简介:会计学原理是一门融理论性与实践性为一体的带有较强应用技术的学科,是学习后续课程中级财务会计、成本管理会计、财务管理和高级财务会计等专业课程的基础,2006年评为省级精品课程。主要讲述四个模块:一是会计基本概念及基本理论,包括会计概念、特点、职能、对象、会计假设、会计原则;二是会计核算方法及其应用,包括账户与复式记账、主要经济业务核算、账户分类、会计凭证、会计账簿、财产清查、会计报表;三是会计循环与组织,包括会计循环、会计核算组织程序、会计工作组织;四是电算化会计简介;重点讲述前两个模块。本课程在内容和方法上尽量将会计理论分析揉合在会计实务过程中,侧重理论与实际相结合,不断规范教学内容及教学手段,主要通过课堂教学、案例分析、练习等环节,让学生全面了解、掌握会计的基本原理、基本方法和基本技能,完善学生的专业知识结构,拓展学生的视野,提高其理论水平和思辨能力,为进一步学习其他会计课程和有关管理课程打下坚实基础。

会计学原理(英文) principle of accounting

15-4

C1

Basics of Investments

Motivation for Investments

panies transfer excess cash into investments to produce higher income. 2.Some companies (e.g. mutual funds etc.) are set up to produce income from investments. panies make investments for strategic reasons (control).

© The McGraw-Hill Companies, Inc., 2010

15-10

C2

Basics of Accounting for Investments

Accounting Basics for Debt Securities Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is recorded when earned.

Cash Equivalents, Short-Term versus Long-Term Investments

Short-term investments:

are securities that management intends to convert to cash with one year or the operating cycle, whichever is longer. are readily convertible to cash.

会计学原理 Fundamentals of Accounting

财政部颁发了新《企业会计准则》,并要求 自07年1月1日起在上市公司范围内施行,并

鼓励其他企业执行。新准则的出台标志着与

国际会计准则趋同的中国会计准则体系正式

建立,这在我国会计发展史上将成为新的里 程碑。

• 补充:我国会计法规体系可以从法律来源 上划分为三个层次:一是由全国人民代表 大会统一制定的会计法律如《会计法》; 二是由国务院或财政部制定的会计行政法 规如《企业会计准则》 ;三是由企业根据 《企业会计准则》的规定制定的会计核算 办法。

• 《企业会计制度》由国家财政部和地方财 政部统一制定的.

•

• 补充: 新准则大量借鉴了国际会计准 则的内容体系,包括公允价值的充分应用、 所得税会计、外币折算、职业判断的运用 等方面。

• 包括基本准则、38个具体准则

• 基本准则包括会计假设、会计信息质量要 求、会计要素、会计计量、财务会计报告

(2)国外

返回

• 五、会计对象

– 会计的对象是指会计核算和监督的内容。

• 只有能够以货币计量的经济活动才能纳入会计核算和监督的范 围。

• 能够以货币计量的经济活动通常被称为价值运动或资金运动。

– 因此,会计的对象可以高度概括为特定对象的资金运 动。

第二节 会计核算的基本前提

• 一、会计核算的基本前提: • 1、会计主体 • 2、持续经营 • 3、会计分期 • 4、货币计量

币计量。

三、会计的职能

• 1、反映职能

• 会计反映职能主要是 从价值量方面对会计 主体已经发生或已经 完成的各项经济活动 进行确认、计量、记 录和报告。它是会计 最基本的工作。

• 2、监督职能

• 会计监督职能主要是 利用会计资料和信息 对经济活动进行控制 和指导。监督的核心 是干预经济活动,使 之遵守国家有关法律 法规的规定。包括事 前监督、事中监督和 事后监督。

PrinciplesofAccounting实践教学指导书(精)

Principles of Accounting实践教学指导书一、教学目的会计学基础是经济管理各专业的一门专业基础课。

会计学原理课程设计的主要目的,是要明确会计的意义和任务,认识做好会计工作的重要性,掌握会计的基本原理和方法。

通过课程设计,可以更好地将教材所涉及的基本理论、基本知识和操作方法,自觉地与现实的会计实践结合起来。

重视课程设计这一环节,可以使学生巩固所学内容,掌握从事会计工作的基本技能。

二、教学时间1.设计任务部署阶段:第一天由指导教师向学生介绍课程设计的目的意义,下达设计任务书,讲解设计进程安排和设计要求等。

2.实施设计阶段:第二天至第十三天集体进行课程设计,并在指导教师的指导下,按照课程设计进程进行设计(自行设计某公司可能发生的30笔业务;编制日记账;过账;编制资产负债表(Balance Sheet)和利润表(Income Statement)。

3.上交课程设计作业阶段:第十四天学生必须完成并上交课程设计作业。

4.成绩评定阶段:实习周结束以后指导教师对学生的课程设计作业逐一审阅,并评定相应成绩(五级分制),写出审阅意见。

三、教学内容1. 资产负债表的相关问题2. 会计记录和系统的相关问题3. 收入和货币资产的相关问题4. 费用测量法的相关问题5. 存货出售的成本的相关问题6. 非流动性资产和贬值的相关问题7. 责任和公平的相关问题8. 现金流转的相关问题9. 财务声明分析的相关问题四、教学要求1.在指导教师指导下进行设计,按时独立完成任务。

对有抄袭他人设计或找他人代做课程设计等行为者,成绩一律按零分记。

2.学生要有勤于思考、刻苦钻研的学习精神和严肃认真的工作态度。

3.课程设计结束后要提交课程设计作业作为成绩考核的主要依据。

4.严格遵守学习纪律,遵守作息时间,不得迟到、早退或旷课。

如因事、因病不能上课,须按学校管理规定办理请假手续。

凡未请假或未获准假擅自缺勤者,均按旷课论处。

5.学生要注意安全、爱护公物,搞好环境卫生。

会计学原理PrinciplesofAccounts

Types of Company

• Sole Proprietorship

(個人公司)

• Partnership

(合夥公司)

• Limited Company

(有限公司)

Examinations

• HKCEE (香港中學會考)

• London Chamber of Commerce and Industry (英國倫敦商會 ) – Book-keeping (初級簿記) – Book-keeping and Accounts (中級會計及簿記)

Why Accounting? (I)

• HK is an international financial center

• CEPA • Different business

activities need different accounting knowledge

Why Accounting? (II)

Career Prospects (Accounting)

• If pass the professional examinations, you can be:

– Company’s accounting officer

– Tax officer

– Auditor

Am I eligible?

• Are you interested in business activities?

• If you are an accounting clerk • You need to know HOW to:

– Post the entries (入帳) – Calculate Profit or Loss (盈利或

虧損); – Prepare the Balance Sheet (資產

《财务管理学》课程中英文简介

《财务管理学》课程中英文简介Corporate Finance课程代码:040013A/040013B Course Code:040025A/040015A/040012B 040025A/040015A /040012B 040025A/040015A课程名称:财务管理学Course Name:Corporate Finance学时:48/32/80 Periods:48/32/80学分:3/2/5 Credits:3/2/5考核方式:考查/考试Assessment:Inspection/Examination先修课程:Preparatory Courses:成本管理会计学(上)MA1 Management AccountingⅠ本课程是国际会计专业方向的基础财务管理学课程,主要讲授的是财务经理在进行投资、筹资和日常营运管理过程中如何进行财务决策,才能实现股东财富最大化这一企业理财目标。

先修课程为管理会计基础(MA1)。

该课程主要包括以下内容:(1)财务管理学简介;(2)财务环境和其组成要素分析。

(3)证券估价。

(4)利息率和汇率的确定:利息率的影响因素和确定步骤、利率期限结构、风险溢价、汇率的影响因素、购买力平价理论和利率平价理论。

(5)战略决策——资本预算:主要讲授项目现金流的确定、资本预算方法和决策标准、内部报酬率法的优缺点分析、资本限额决策、资本预算决策中的风险分析。

(6)战略决策——资本成本:主要讲授资本结构、个别资本成本(包括债券、优先股、普通股)和综合资本成本的确定。

(7)经营决策——营运资本管理:主要讲授营运资本筹资决策、存货、应收帐款的管理。

(8)财务计划:主要讲授财务计划(或资金需求计划)的编制和分析。

Corporate Finance Fundamentals [FN1] is a fundamental course in managerial finance with an emphasis on the major decisions to be made by the financial executive of an organization. Topics introduced in FN1 include the following parts:Part 1 Introduction to the corporate finance; Part 2 The financial environment,including the financial system, the major intermediaries and the specialized markets; Part 3 Security valuation: Risk-free assets, including the interest rate as an opportunity cost, varying compound intervals and annuities; Part 4 The determinants of interest rates, including the determinants of interest rates, term structure effects; Part 5 Security valuation: Risk-adjusted discount rates, including the determinants of equity prices, the relationship between the price and the expected return; Part 6 Strategic decisions: Capital budgeting and cash flow estimation, including the capital budgeting process, estimating cash flows; Part 7 Strategic decisions: Capital budgeting evaluation criteria, including the NPV rule measures shareholder wealth, alternative capital budgeting criteria; Part 8 Financial planning, including Important elements in financial planning and the benefits of financial planning.《财务管理学》课程中英文简介Financial Management课程代码:040015A Course Code:040015A课程名称:财务管理学Course Name:Financial Management学时:80 Periods:80学分:5 Credits:5考核方式:考试Assessment:Examination先修课程:会计学基础Preparatory Courses:Accounting财务管理学是会计学和注册会计师专业的学科基础课,开设本课程的主要任务是加强学生对财务管理理论与实务的全面、深入了解,培养学生课堂讨论和课外阅读与写作的习惯,引导学生对有关现代企业财务管理问题进行思考,从而培养出适应市场经济需要的中级理财者。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Amortized Cost

Market Value Method

Equity Method

Consolidate

Reporting

Jun. 30 Cash Interest Revenue 30,000 30,000

To record receipt of interest on bonds

The same entry would be made on December 31, 2008.

© The McGraw-Hill Companies, Inc., 2010

© The McGraw-Hill Companies, Inc., 2010

15-11

C2

Basics of Accounting for Investments

Accounting Basics for Debt Securities Held-to-maturity (HTM) debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is recorded when earned.

© The McGraw-Hill Companies, Inc., 2010

15-3

Procedural Learning Objectives

P1: Account for trading securities(交易性金 融资产) P2: Account for held-to-maturity (HTM) securities(持有至到期日金融资产) P3: Account for available-for-sale (AFS) securities(可供出售金融资产) P4: Account for equity securities with significant influence(重大影响)

Jan. 1

Cash Long-Term Investment - HTM

1,000,000 1,000,000

Cash received at bond maturity.

© The McGraw-Hill Companies, Inc., 2010

15-14

Matrix Inc. Example: Cont’

© The McGraw-Hill Companies, Inc., 2010

15-8

C1

Basics of Investments

Debt securities versus Equity securities

Debt securities – investments in notes, bonds, etc

15-1

Chapter 13

Investments

© The McGraw-Hill Companies, Inc., 2008

15-2

Conceptual Learning Objectives

C1: Distinguish between debt and equity securities and between short-term and long-term investments C2: Identify and describe the different classes of investments in securities C3: Describe how to report equity securities with controlling influence

15-13

C2

Basics of Accounting for Investments

Accounting Basics for Debt Securities On January 1, 2010, the bonds mature and Matrix would make the following entry:

Accounting Basics for Debt Securities Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is recorded when earned.

Jan. 1

Long-Term Investment - HTM Cash

1,000,000 1,000,000

Purchased bonds to hold to maturity

© The McGraw-Hill Companies, Inc., 2010

15-12

C2

Basics of Accounting for Investments

On September 1, 2008, Matrix, Inc. paid Debt Inc. $1,000,000 for the bonds at par. The two-year Debt Inc. bonds have a stated rate of 6% annually. Interest is paid semi-annually on August 31 and February 28.

© The McGraw-Hill Companies, Inc., 2010

15-16

*Matrix Inc. Example: Try!

On September 1, 2008, Matrix, Inc. paid Debt Inc. $1,200,000 for the bonds with a $1,000,000. The two-year Debt Inc. bonds have a stated rate of 6% annually. Interest is paid semi-annually on August 31 and February 28.

Equity securities – investments in stocks, etc

© The McGraw-Hill Companies, Inc., 2010

15-9

C2

Classes of and Reporting for Investments

Class of Investment

© The McGraw-Hill Companies, Inc., 2010

15-10

C2

Basics of Accounting for Investments

Accounting Basics for Debt Securities Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is recorded when earned.

Cash Equivalents, Short-Term versus Long-Term Investments

Short-term investments:

are securities that management intends to convert to cash with one year or the operating cycle, whichever is longer. are readily convertible to cash.

© The McGraw-Hill Companies, Inc., 2010

15-7

C1

Basics of Investments

Cash Equivalents, Short-Term versus Long-Term Investments

Long-term investments: Short-term investments:

(1)Readily convertible to a known cash amount (2)Sufficiently close to due date (within 3 months)

© The McGraw-Hill Companies, Inc., 2010

15-6

C1

Basics of Investments

© The McGraw-Hill Companies, Inc., 2010

15-17

P1

Accounting Basics for Equity Securities (Non-influential)

Equity securities are recorded at cost when acquired, including commissions or brokerage fees paid. Any cash dividends received are credited to Dividend Revenue and reported in the income statement. When the securities are sold, sales proceeds are compared with cost, and any gain or loss is recorded.

© The McGraw-Hill Companies, Inc., 2010

15-4

C1

Basics of Investments

Motivation for Investments