会计学原理英文课件 (4)

会计学原理英文ppt课件Chapter_01ACCOUNTING IN BUSINESS共41页文档

McGraw-Hill/Irwin

•Managers

•Sales Staff

•Officers/Directors •Budget Officers

•Internal Auditors •Controllers

Slide 2

C2

USERS OF ACCOUNTING

INFORMATION

External Users

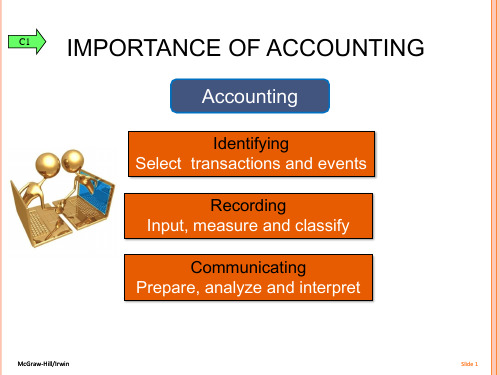

C1 IMPORTANCE OF ACCOUNTING

Accounting

Identifying Select transactions and events

Recording Input, measure and classify

Communicating Prepare, analyze and interpret

•Consultants

•Market researchers

•Analysts

•Systems designers

•Traders

•Merger services

•Directors

•Business valuation

•Underwriters

•Human services

•Planners

•Litigation support

Internal Users

Financial accounting provides external users with financial

statements.

McGraw-Hill/Irwin

Managerial accounting provides information needs for internal decision makers.

会计学原理英文课件4

earned.

4-2

Expenses are recorded when

incurred.

Because transactions occur over time, ADJUSTMENTS are required at the end of each fiscal period to get the revenues

External Transactions

Adjusting Entries

Start of Accounting

Period

End of Accounting

Period

4-7

Adjusting Entries

There are two types of adjusting entries.

DEFERRALS (递延)

4-6

Adjusting Process

At the end of the accounting period, adjusting journal entries are recorded for internal transactions that have a direct and

measurable effect on the accounting entity, particularly for revenue and expense recognition.

Interest Receivable 12/31 150

Bal. 150

Interest Revenue 12/31 150 Bal. 150

4-19

Chart for Deferred and Accrued Revenues

会计学原理英文ppt课件Chapter_05Accounting for Merchandising Operations

After we post these entries, the accounts involved look like this:

Merchandise Inventory

11/2 1,200 11/12 24 Bal. 1,176

Accounts Payable

11/12 1,200 11/2 1,200

PURCHASE DISCOUNTS

2/10,n/30

Discount Percent

McGraw-Hill/Irwin

Number of Days

Discount Is Available

Otherwise, Net (or All) Is Due in 30

Days

Credit Period

Slide 12

Credit sales

Slide 5

C3

INVENTORY SYSTEMS

Beginning inventory

+

Net cost of purchases

= Merchandise available for sale

Ending inventory

McGraw-Hill/Irwin

+

Cost of goods sold

Slide 6

C3

PERPETUAL AND PERIODIC

INVENTORY SYSTEMS

➢ Perpetual systems

➢ continually update accounting records for merchandising transactions

➢ Periodic systems

Merchandise Inventory Accounts Payable

会计学原理(英文)

《会计学原理(英文)》教学大纲王燕祥编写工商管理专业课程教学大纲610 目录Chapter 1 Accounting in Action 第一章会计实践活动 (613)学习目标 (613)Teaching and homework hours 教学与作业时间 (613)Reading and References 学生必读和参考书目 (613)Chapter 2 The Recording Process 第二章记录过程 (615)学习目标 (615)Teaching and homework hours 教学与作业时间 (615)Reading and References 学生必读和参考书目 (615)Chapter 3 Adjusting the Accounts 第三章调整账户 (617)学习目标 (617)Teaching and homework hours 教学与作业时间 (617)Reading and References 学生必读和参考书目 (617)Chapter 4 Completion of the Accounting Cycle 第四章完成会计循环 (619)学习目标 (619)Teaching and homework hours 教学与作业时间 (619)Reading and References 学生必读和参考书目 (619)Chapter 5 Accounting for Merchandising Operations 第五章商品经营活动的会计核算 (621)学习目标 (621)Teaching and homework hours 教学与作业时间 (621)Reading and References 学生必读和参考书目 (621)Chapter 6 Inventories 第六章存货 (623)学习目标 (623)Teaching and homework hours 教学与作业时间 (624)Reading and References 学生必读和参考书目 (624)Chapter 7 Accounting Information Systems 第七章会计信息系统 (626)学习目标 (626)Teaching and homework hours 教学与作业时间 (626)Reading and References 学生必读和参考书目 (626)Chapter 8 Internal Control and Cash 第八章内部控制和现金 (628)学习目标 (628)Teaching and homework hours 教学与作业时间 (628)Reading and References 学生必读和参考书目 (628)Chapter 9 Accounting for Receivables 第九章应收款项的会计核算 (630)学习目标 (630)Teaching and homework hours 教学与作业时间 (630)Reading and References 学生必读和参考书目 (630)Chapter 10 Plant Assets, Natural Resources, and Intangible Assets 第十章厂场资产、自然资源和无形资产 (632)会计学原理(英文)学习目标 (632)Teaching and homework hours 教学与作业时间 (632)Reading and References 学生必读和参考书目 (633)Chapter 11 Current Liabilities and Payroll Accounting 第十一章流动负债和工资的核算 (634)学习目标 (634)Teaching and homework hours 教学与作业时间 (634)Reading and References 学生必读和参考书目 (634)Chapter 12 Accounting Principles 第十二章会计原则 (636)学习目标 (636)Teaching and homework hours 教学与作业时间 (636)Reading and References 学生必读和参考书目 (636)Chapter 13 Accounting for Partnerships 第十三章合伙企业的会计核算 (638)学习目标 (638)Teaching and homework hours 教学与作业时间 (638)Reading and References 学生必读和参考书目 (638)Chapter 14 Corporations: Organization and Capital Stock Transactions 第十四章公司:组织和股本交易 (640)学习目标 (640)Teaching and homework hours 教学与作业时间 (640)Reading and References 学生必读和参考书目 (640)Chapter 15 Corporations: Dividends, Retained Earnings, and Income Reporting 第十五章股利、保留盈余和收益报告 (642)学习目标 (642)Teaching and homework hours 教学与作业时间 (642)Reading and References 学生必读和参考书目 (642)Chapter 16 Long-Term Liabilities 第十六章长期负债 (644)学习目标 (644)Teaching and homework hours 教学与作业时间 (644)Reading and References 学生必读和参考书目 (644)Chapter 17 Investments 第十七章投资 (646)学习目标 (646)Teaching and homework hours 教学与作业时间 (646)Reading and References 学生必读和参考书目 (646)Chapter 18 The Statement of Cash Flows 第十八章现金流量表 (648)学习目标 (648)Teaching and homework hours 教学与作业时间 (648)Reading and References 学生必读和参考书目 (648)Chapter 19 Financial Statement Analysis 第十九章财务报表分析 (650)学习目标 (650)Teaching and homework hours 教学与作业时间 (650)Reading and References 学生必读和参考书目 (650)Chapter 20 Managerial Accounting 第二十章管理会计 (652)611工商管理专业课程教学大纲612 学习目标 (652)Teaching and homework hours 教学与作业时间 (652)Reading and References 学生必读和参考书目 (652)Chapter 21 Job Order Cost Accounting 第二十一章分批成本法 (654)学习目标 (654)Teaching and homework hours 教学与作业时间 (654)Reading and References 学生必读和参考书目 (654)Chapter 22 Process Cost Accounting 第二十二章分步成本法 (656)学习目标 (656)Teaching and homework hours 教学与作业时间 (656)Reading and References 学生必读和参考书目 (657)Chapter 23 Cost-V olume-Profit Relationships 第二十三章本量利分析 (658)学习目标 (658)Teaching and homework hours 教学与作业时间 (658)Reading and References 学生必读和参考书目 (659)Chapter 24 Budgetary Planning 第二十四章编制预算 (660)学习目标 (660)Teaching and homework hours 教学与作业时间 (660)Reading and References 学生必读和参考书目 (660)Chapter 25 Budgetary Control and Responsibility Accounting 第二十五章预算控制和责任会计 662 学习目标 (662)Teaching and homework hours 教学与作业时间 (662)Reading and References 学生必读和参考书目 (662)Chapter 26 Performance Evaluation through Standard Costs 第二十六章利用标准成本进行业绩评价 (664)学习目标 (664)Teaching and homework hours 教学与作业时间 (664)Reading and References 学生必读和参考书目 (664)Chapter 27 Incremental Analysis and Capital Budgeting 第二十七章增量分析和资本预算 (666)学习目标 (666)Teaching and homework hours 教学与作业时间 (667)Reading and References 学生必读和参考书目 (667)会计学原理(英文)Chapter 1 Accounting in Action第一章会计实践活动STUDY OBJECTIVESAfter studying this chapter you should be able to:1.Explain what accounting is.2.IDENTIFY THE USERS AND USES OF ACCOUNTING.3.UNDERSTAND WHY ETHICS IS A FUNDAMENTAL BUSINESS CONCEPT.4.EXPLAIN THE MEANING OF GENERALLY ACCEPTED ACCOUNTING PRINCIPLESAND THE COST PRINCIPLE.5.EXPLAIN THE MEANING OF THE MONETARY UNIT ASSUMPTION AND THE ECONOMIC ENTITY ASSUMPTION.6.STATE THE BASIC ACCOUNTING EQUATION AND EXPLAIN THE MEANING OF ASSETS, LIABILITIES, AND OWNER’S EQUITY.7.ANALYZE THE EFFECT OF BUSINESS TRANSACTIONS ON THE BASIC ACCOUNTING EQUATION.8.Understand what the four financial statements are and how they are prepared.学习目标学完本章之后,学生应该能够达到以下目标:1.解释什么是会计。

会计学原理23版 英文版课件Wild_FAP23e_Ch12_PPT_091117

800 800

11 Learning Objective P1: Prepare entries for partnership formation.

Learning Objective P2:

Allocate and record income and loss among partners.

Accounting for Partnerships

Chapter 12

Wild, Shaw, and Chiappetta Fundamental Accounting Principles 23rd Edition

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

H. Perez, Capital 10,000

• Protects innocent partners from malpractice or negligence claims.

• Most states hold all partners personally liable for partnership debts.

Learning Objective C1: Identify characteristics of partnerships and similar organizations.

their shares of net income (or net loss) when closing the accounts at the end of the period. 3. Each partner’s withdrawal account is closed to that partner’s capital account. Separate capital and withdrawals accounts are kept for each partner.

会计学原理23版 英文版课件WildFAP23eCh18PPT

7 Learning Objective C1: Explain the purpose and nature of, and the role of ethics in, managerial accounting.

statements.

2

Learning Objective

C1: Explain the purpose and nature

of, and the role of ethics in, managerial accounting.

3

18 - 4

Managerial Accounting Basics

Fraud affects all business and it is costly: The 2016 Report to the Nations from the Association of Certified Fraud Examiners (ACFE) estimates the average U.S. business loses 5% of its annual revenues to fraud.

Activity

• Total fixed costs do not change when activity changes.

Cost

Cost

• Total variable costs change

Activity

in proportion

会计学原理23版 英文版课件WildFAP23eCh11PPT

16 Learning Objective P1: Prepare entries to account for short-term notes payable.

11 - 17

When Note Extends over Period-End

11 - 16

Note Given To Borrow From Bank

On Sept. 30, a company borrows $2,000 from a bank at 12% interest for 60 days.

On Nov. 29, the company repays the principal of the note plus interest.

whichever is longer.

5 Learning Objective C1: Describe current and long-term liabilities and their characteristics.

11 - 6

Current and Lone Given to Extend Credit Period

On October 22, Brady pays the note plus interest to McGraw.

Interest expense = $500 × 12% × (60 ÷ 360) = $10

15 Learning Objective P1: Prepare entries to account for short-term notes payable.

Jun. 30

会计学原理PrinciplesofAccountingppt课件

24

1.3.2会计目标

(一) 企业信息的外部使用者 (1)投资者——最主要的使用人。企业盈利能力如何?是否值得投资。 (2)债权人。是否要贷款给这家公司?利息收取多少?该公司能否根据合

约还本付息?是否需要提供担保? (3)税务部门。公司依法应缴多少税?是否依法纳税?来年的纳税前景如

赖程度如何?能否根据合约按时支付货款? (7)客户。公司能否继续生存?产品定价是否合理?产品更新换代的打算

如何? (8)中介机构

25

1.3.2会计目标

(二)会计信息的内部使用者 指企业内部各阶层的管理人员,包括公司董事会成员,公司经理、 公司计划、财务、供应、市场等方面的管理人员以及车间部门的负 责人等。 公司职工也属于内部使用者,他们需要考虑的问题是公司是否有 能力按劳付酬?公司的财务状况与获利能力是否足以保障就业?公 司是否在劳动保护方面花了必要或足够的钱?公司是否有能力不断 提高职工福利待遇?

27

1.4.2会计核算前提(会计假设)

是对会计领域中某些无法加以论证的事物,根据客观、正常的 情况作出的判断,是全部会计工作的基础,是组织会计核算工作的 前提。 一、会计主体

1.可反映代理理论中的受托责任 2.会计所服务的特定对象,空间范围 3.凡是实行独立核算的经济实体 4.与法人的区别

二、持续经营 1.时间无限性 2.可合理确定六要素的内容

某一历史阶段的会计发展状况、水平与进步,从始到终受到 这一历史阶段会计环境的推动和制约。

6

1.1.1会计环境变化对会计的影响

会计环境的构成要素

经济因素

政治法律因素 科学技术因素 文化教育因素

7

1.1.1会计环境变化对会计的影响

会计学原理英文课件 (4)

Permanent Accounts

Income Summary

The closing process applies only to temporary accounts.

4-6

P2

Recording Closing Entries

Close Credit Balances in Revenue Accounts to Income Summary. Close Debit Balances in Expense accounts to Income Summary. Close Income Summary account to Owner’s Capital. Close Withdrawals to Owner’s Capital.

Depreciation Expense- Eq. 375 375 -

Rent Expense 1,000 1,000 Income Summary 4,365 8,150 3,785

Salaries Expense 1,610 1,610 Insurance Expense 100 100 -

Supplies Expense 1,050 1,050 Utilities Expense 230 230 -

P2

Close Income Summary to Owner’s Capital

4 - 16

C. Taylor, Capital 30,000 3,785 33,785

Income Summary 4,365 8,150 3,785 -

4 - 17

P2

FastForward Adjusted Trial Balance December 31, 2013 Debit Cash $ 4,350 Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-Equip. Accounts payable Salaries payable Unearned consulting revenue C. Taylor, Capital C. Taylor, Withdrawals 200 Consulting revenue Rental revenue Depreciation expense-Equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals $ 47,685

会计学原理23版 英文版课件WildFAP23eCh20PPT

EUP for Materials and Conversion Costs

11 Learning Objective C2: Define and compute equivalent units and explain their use in process costing.

Weighted Average versus FIFO Weighted Average versus FIFO

Learning Objective A1:

Compare process costing and job order costing.

5

Comparing Process and Job Order Costing Systems

Job Order Systems

Process Systems

Goods Sold.

2

Learning Objective C1:

Explain process operations and the way they differ from job order operations.

3

Process Operations

▪ Used for production of identical, low-cost items. ▪ Mass produced in automated continuous

12 Learning Objective C2: Define and compute equivalent units and explain their use in process costing.

Learning Objective

C3: Describe accounting for production activity and preparation of a process cost summary using weighted

会计学原理英文ppt课件Chapter_05Accounting for Merchandising

Quantity sold Price per unit Total Less 30% discount Invoice price

1,000 $ 5.25

5,250 (1,575) $ 3,675

Slide 9

P1

Invoice

Main Source, Inc.

Invoice

614 Tech Avenue Nashville, TN 37651

McGraw-Hill/Irwin

Slide 7

P1 November 2, Z-Mart purchased $1,200 of merchandise inventory for cash.

Nov 2

Merchandise Inventory Cash

ACCOUNTING FOR MERCHANDISING OPERATIONS

Chapter 5

© 2009 The McGraw-Hill Companies, Inc.,

SERVICE COMPANIES

Service organizations sell time to earn revenue.

C3

PERPETUAL AND PERIODIC

INVENTORY SYSTEMS

➢ Perpetual systems

➢ continually update accounting records for merchandising transactions

➢ Periodic systems

➢ accounting records relating to merchandise transactions are updated only at the end of the accounting period

会计学原理(英文) principle of accounting

15-4

C1

Basics of Investments

Motivation for Investments

panies transfer excess cash into investments to produce higher income. 2.Some companies (e.g. mutual funds etc.) are set up to produce income from investments. panies make investments for strategic reasons (control).

© The McGraw-Hill Companies, Inc., 2010

15-10

C2

Basics of Accounting for Investments

Accounting Basics for Debt Securities Debt securities are recorded at cost when purchased. Interest revenue for investments in debt securities is recorded when earned.

Cash Equivalents, Short-Term versus Long-Term Investments

Short-term investments:

are securities that management intends to convert to cash with one year or the operating cycle, whichever is longer. are readily convertible to cash.

会计学原理英文版

会计学原理英文版Accounting Principles。

Accounting is the language of business. It is a system of recording, analyzing, and summarizing financial transactions for the purpose of providing financial information to external users for decision making. In this document, we will discuss the fundamental principles of accounting, which form the foundation of the accounting process.1. Entity Concept。

The entity concept states that a business is separate and distinct from its owners. This means that the business's financial transactions should be recorded and reported separately from the personal transactions of its owners. This concept is important because it ensures that the financial position and performance of the business are accurately reflected without any personal bias or influence.2. Going Concern Concept。

The going concern concept assumes that a business will continue to operate indefinitely. This means that the financial statements are prepared under the assumption that the business will not be liquidated in the near future. This concept is important because it allows for the proper valuation of assets and liabilities, as well as the preparation of accurate financial statements.3. Monetary Unit Concept。

会计学原理Accounts Receivable英文PPT

Jan. 18 Dr Allowance for Doubtful Accounts $250

Cr Accounts Receivable

$250

- Leonardo Dicaprio

Valuing Accounts Receivable

• If on May 11 Leonardo Dicaprio pays full his account previously written off,the entries are:

• Accounts receivable is a legally enforceable claim for payment from a bussiness to its customer for goods supplied and services rendered in execution of the customer's order.

$480

Cr Accounts Receivable $480

Valuing Accounts Receivable

• Direct Write-Off Method/直接核销法/

Eg: If Dreamwork determines on June 24 that it cannot collect $250 owed to it by its customer Johnny Depp, it recognizes the loss using the direct write-off method as follows:

ቤተ መጻሕፍቲ ባይዱstimating bad debts

• Percent of Receivables Method/应收账款百分 比法/

会计学原理英文课件Chapter04ACCOUNTING CYCLE

1,000

1,000

Supplies expense

1,050

1,050

Utilities expense

230

230

Totals

47,685

47,685

4,365

8,150

43,320

39,535

Net income

3,785

3,785

8,150

8,150

43,320

43,320

McGraw-Hill/Irwin

$ 7,850

Statement.

Rental revenue

300

Total revenues Operating expenses:

8,150 A work sheet

Depr. expense - Equip. $ 375

Salaries expense

1,610

does not

Insurance expense Rent expense

Depr. expense - Equip. $ 375

Salaries expense

1,610

Insurance expense

100

Rent expense

1,000

Supplies expense

1,050

Utilities expense

230

Total expenses

4,365

Net income

375

Accounts payable

6,200

Salaries payable

210

Unearned consulting revenue

2,750

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Illustration 4-2

2. ENTER THE ADJUSTMENTS IN THE ADJUSTMENTS COLUMNS

Account Titles Cash Supplies Prepaid Insurance Equipment Notes Payable Accounts Payable Unearned Revenue Share Capital-Ordinary Dividends Service Revenue Salaries and Wages Exp. Rent Expense Totals Supplies Expense Insurance Expense Accumulated Depreciation Depreciation Expense Accounts Receivable Interest Expense Interest Payable Salaries and Wages Payable Totals Statement of Financial Position Dr. Cr.

WILEY

IFRS EDITION

Prepared by Coby Harmon University of California, Santa Barbara 4-1 Westmont College

PREVIEW OF CHAPTER 4

Financial Accounting

IFRS 3rd Edition Weygandt ● Kimmel ● Kieso

4-2

CHAPTER

4

Completing the Accounting Cycle

LEARNING OBJECTIVES

After studying this chapter, you should be able to: 1. Prepare a worksheet.

2. Explain the process of closing the books.

5. TOTAL COLUMNS, COMPUTE NET INCOME (LOSS)

Account Titles Cash Supplies Prepaid Insurance Equipment Notes Payable Accounts Payable Unearned Revenue Share Capital-Ordinary Dividends Service Revenue Salaries and Wages Exp. Rent Expense Totals Supplies Expense Insurance Expense Accumulated Depreciation Depreciation Expense Accounts Receivable Interest Expense Interest Payable Salaries and Wages Payable Totals Net Income Totals Trial Balance Adjustments Dr. Cr. Dr. Cr. 15,200 (a) 1,500 2,500 (b) 600 50 5,000 5,000 2,500 1,200 (d) 400 10,000 500 (d) 400 10,000 (e) 200 (g) 4,000 1,200 900 28,700 28,700 (a)1,500 (b) 50 (c) 40 (c) 40 (e) 200 (f) 50 (f) 50 (g) 1,200 3,440 3,440 Adjusted Trial Balance Dr. Cr. 15,200 1,000 550 5,000 5,000 2,500 800 10,000 500 10,600 5,200 900 1,500 50 40 40 200 50 50 1,200 30,190 40 Income Statement Dr. Cr.

Adjusting Journal Entries

(Chapter 3)

4-7

Steps in Preparing a Worksheet

Trial Balance Adjustments Dr. Cr. Dr. Cr. 15,200 (a) 1,500 2,500 (b) 600 50 5,000 5,000 2,500 1,200 (d) 400 10,000 500 (d) 400 10,000 (e) 200 (g) 4,000 1,200 900 28,700 28,700 (a)1,500 (b) 50 (c) 40 (c) 40 (e) 200 (f) 50 (f) 50 (g) 1,200 3,440 3,440 Adjusted Trial Balance Dr. Cr. Income Statement Dr. Cr.

Enter adjustment amounts, total adjustments columns, and check for equality.

Add additional accounts as needed.

4-8

LO 1

Steps in Preparing a Worksheet

Trial Balance Adjustments Dr. Cr. Dr. Cr. 15,200 (a) 1,500 2,500 (b) 600 50 5,000 5,000 2,500 1,200 (d) 400 10,000 500 (d) 400 10,000 (e) 200 (g) 4,000 1,200 900 28,700 28,700 (a)1,500 b) 50 (c) 40 (c) 40 (e) 200 (f) 50 (f) 50 (g) 1,200 3,440 3,440 Adjusted Trial Balance Dr. Cr. 15,200 1,000 550 5,000 5,000 2,500 800 10,000 500 10,600 5,200 900 1,500 50 40 40 200 50 50 1,200 30,190 Income Statement Dr. Cr.

6. Identify the sections of a classified statement of financial position.

4-3

Using a Worksheet

Worksheet

Learning Objective 1

Prepare a worksheet.

Multiple-column form used in preparing

Illustration 4-2

1. PREPARE A TRIAL BALANCE ON THE WORKSHEET

Account Titles Cash Supplies Prepaid Insurance Equipment Notes Payable Accounts Payable Unearned Revenue Share Capital-Ordinary Dividends Service Revenue Salaries and Wages Exp. Rent Expense Totals Statement of Financial Position Dr. Cr.

Adjustments Key: (a) Supplies Used. (b) Insurance Expired. (c) Depreciation Expensed. (d) Service Revenue Recognized. (e) Service Revenue Accrued. (f) Interest Accrued. (g) Salaries Accrued.

30,190

4-9

Total the adjusted trial balance columns and check for equality.

LO 1

Steps in Preparing a Worksheet

Trial Balance Adjustments Dr. Cr. Dr. Cr. 15,200 (a) 1,500 2,500 (b) 600 50 5,000 5,000 2,500 1,200 (d) 400 10,000 500 (d) 400 10,000 (e) 200 (g) 4,000 1,200 900 28,700 28,700 (a)1,500 (b) 50 (c) 40 (c) 40 (e) 200 (f) 50 (f) 50 (g) 1,200 3,440 3,440 Adjusted Trial Balance Dr. Cr. 15,200 1,000 550 5,000 5,000 2,500 800 10,000 500 10,600 5,200 900 1,500 50 40 40 200 50 50 1,200 30,190 40 50 Income Statement Dr. Cr.

Illustration 4-2

4. EXTEND AMOUNTS TO FINANCIAL STATEMENT COLUMNS

Account Titles Cash Supplies Prepaid Insurance Equipment Notes Payable Accounts Payable Unearned Revenue Share Capital-Ordinary Dividends Service Revenue Salaries and Wages Exp. Rent Expense Totals Supplies Expense Insurance Expense Accumulated Depreciation Depreciation Expense Accounts Receivable Interest Expense Interest Payable Salaries and Wages Payable Totals Statement of Financial Position Dr. Cr.