会计英语 第四版 叶建芳05

会计英语第四版参考答案

会计英语第四版参考答案Chapter 1: Introduction to Accounting1. What is accounting?- Accounting is the systematic recording, summarizing, and reporting of financial transactions and events of a business entity.2. What are the main functions of accounting?- The main functions of accounting are to providefinancial information for decision-making, ensure compliance with laws and regulations, and facilitate the management of a business.3. What are the two main branches of accounting?- The two main branches of accounting are financial accounting and management accounting.4. What is the purpose of financial accounting?- The purpose of financial accounting is to provide an accurate and fair representation of an entity's financial position and performance to external users.5. What is the double-entry bookkeeping system?- The double-entry bookkeeping system is a method of recording financial transactions in which every transactionis recorded twice, once as a debit and once as a credit, to maintain the equality of the accounting equation.Chapter 2: Accounting Concepts and Principles1. What are the fundamental accounting concepts?- The fundamental accounting concepts include the accrual basis of accounting, going concern, consistency, and materiality.2. What is the accrual basis of accounting?- The accrual basis of accounting records transactions when they occur, regardless of when cash is received or paid.3. What is the going concern assumption?- The going concern assumption is the premise that a business will continue to operate for the foreseeable future.4. What is the principle of consistency?- The principle of consistency requires that an entity should apply accounting policies consistently over time.5. What is the principle of materiality?- The principle of materiality states that only items that could potentially affect the decisions of users of financial statements are included in the financial statements.Chapter 3: The Accounting Equation and Financial Statements1. What is the accounting equation?- The accounting equation is Assets = Liabilities +Owner's Equity.2. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, statement of changes in equity, and cashflow statement.3. What is the purpose of the balance sheet?- The balance sheet provides a snapshot of an entity's financial position at a specific point in time.4. What is the purpose of the income statement?- The income statement reports the revenues, expenses, and net income of an entity over a period of time.5. What is the purpose of the cash flow statement?- The cash flow statement reports the cash inflows and outflows of an entity over a period of time.Chapter 4: Recording Transactions1. What is a journal entry?- A journal entry is the initial recording of atransaction in the general journal.2. What are the steps in the accounting cycle?- The steps in the accounting cycle are analyzing transactions, journalizing, posting, preparing a trial balance, adjusting entries, preparing financial statements, and closing entries.3. What is the difference between a debit and a credit?- A debit is an increase in assets or a decrease inliabilities or equity, while a credit is an increase in liabilities or equity or a decrease in assets.4. What are adjusting entries?- Adjusting entries are made at the end of an accounting period to ensure that revenues and expenses are recorded in the correct period.5. What is the purpose of closing entries?- Closing entries are made to transfer the balances of temporary accounts to the owner's equity account and to prepare the accounts for the next accounting period.Chapter 5: Accounting for Merchandising Businesses1. What is a merchandise inventory?- A merchandise inventory is the stock of goods held by a business for sale to customers.2. What is the cost of goods sold?- The cost of goods sold is the direct cost of producing the merchandise sold during an accounting period.3. What is the gross profit?- The gross profit is the difference between the sales revenue and the cost of goods sold.4. What is the difference between a perpetual and a periodic inventory system?- A perpetual inventory system updates inventory records in real-time with each sale or purchase, while a periodicinventory system updates inventory records at specific intervals, such as at the end of an accounting period.5. What is the retail method of inventory pricing?- The retail method of inventory pricing is a method of estimating the cost of ending inventory by applying a cost-to-retail ratio to the retail value of the inventory.Chapter 6: Accounting for Service Businesses1. What are the main differences in accounting for service businesses compared to merchandise businesses?- Service businesses do not have inventory and their primary expenses are typically labor and overhead costs.2. What is the main source of revenue for service businesses? - The main source of revenue for service businesses is the fees charged for the services provided.3. What are the typical expenses。

会计英语_第四版_叶建芳09

Company Name Statement of Cash Flows Period Covered Cash flows from operating activities: [List of individual inflows and outflows] Net cash provided (used) by operating activities

Direct Method Cash Paid for Merchandise

How much did Lug Lite pay for inventory in 1999?

Inventory, 1/1/99 Inventory, 12/31/99 COGS, 12/31/99 $ 130,000 $ 165,000 $ 900,000 A/P, 1/1/99 A/P, 12/31/99 $ 23,000 $ 35,000

_

Cash Flows from Financing Activities

7

YE SUN AccountingEnglish

Cash and Cash Equivalents

Cash Equivalents

Cash

Currency

Short-term, highly liquid investments. Readily convertible into cash. So near maturity that market value is unaffected by interest rate changes.

Acquire plant assets. Purchase debt or equity investments. Make loans.

会计英语叶建芳第四版课后题

会计英语叶建芳第四版课后题摘要:一、引言1.会计英语的重要性2.叶建芳第四版教材的特点二、课后题概述1.题型分类2.难度分析3.解题技巧与策略三、重点题型详解1.选择题a.解题步骤b.常见错误分析c.答题技巧2.填空题a.解题方法b.易错点提示c.解题策略3.判断题a.判断标准b.解题技巧c.错误判断分析四、课后题练习与解答1.练习题一:会计基本概念2.练习题二:财务报表与分析3.练习题三:会计分录与账户4.练习题四:计量、估计与披露5.练习题五:财务决策与控制五、总结与展望1.课后题学习成果总结2.提高会计英语能力的建议3.叶建芳第四版教材在教学中的应用与评价正文:一、引言随着全球化进程的不断推进,会计英语在国际贸易、企业交流等领域发挥着越来越重要的作用。

我国著名会计学家叶建芳教授所著的《会计英语》教材,历经多次修订,已成为会计专业学生的必备书籍。

本篇文章将针对叶建芳第四版《会计英语》教材的课后题进行详细解析,以帮助读者提高会计英语水平。

二、课后题概述1.题型分类叶建芳第四版《会计英语》的课后题主要包括选择题、填空题、判断题等。

这些题型涵盖了会计英语的基本概念、财务报表、会计分录、计量、估计与披露、财务决策等方面,全面检测读者对会计英语知识的掌握程度。

2.难度分析总体来说,课后题的难度适中,既适合初学者巩固基础知识,又能锻炼有一定基础的读者提高解题能力。

其中,部分题目具有一定的挑战性,需要读者对相关知识点有较深入的理解。

3.解题技巧与策略为提高解题效率,读者需要掌握一定的解题技巧。

以下为针对不同题型的解题策略:(1)选择题:仔细阅读题干,分析选项差异,运用排除法缩小答案范围,最后根据知识点选择正确答案。

注意审题,避免粗心大意。

(2)填空题:根据题干信息,填入合适的知识点。

注意检查答案是否符合题意和语法规范。

(3)判断题:明确判断标准,分析题干中的关键信息,避免盲目判断。

对于存疑的题目,可以借助教材或其他资料进行查证。

叶建芳会计英语中文版1-5(精编文档).doc

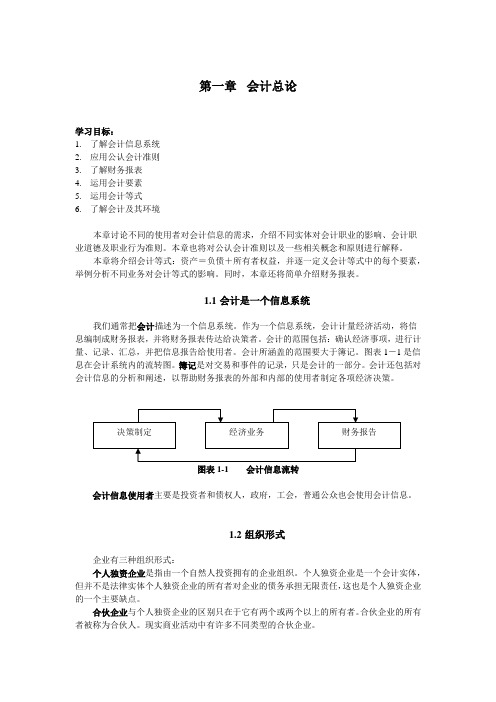

【最新整理,下载后即可编辑】第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

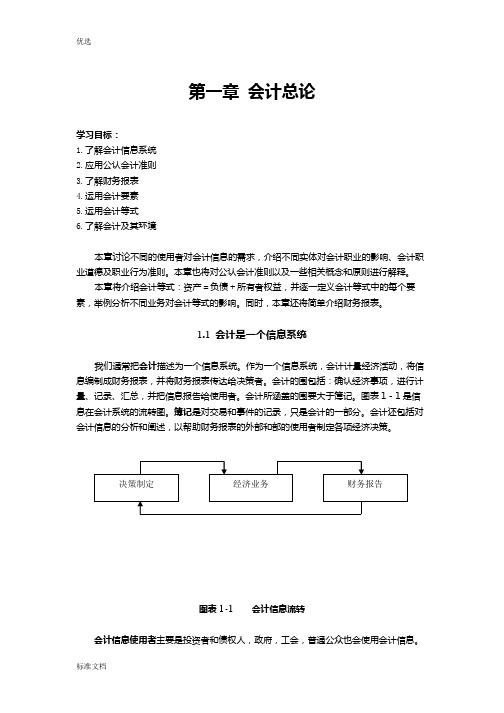

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计英语叶建芳第四版课后题

会计英语叶建芳第四版课后题Section 1: Introduction to Accounting1.1 What is accounting?Accounting is the process of identifying, measuring, summarizing, and communicating financial information to interested users.It involves recording transactions, preparing financial statements, and providing financial analysis.1.2 Why is accounting important?Accounting is important because it provides essential information for decision-making by management, investors, creditors, and other stakeholders.It helps in evaluating the financial performance and position of a business, and ensures transparency and accountability.1.3 Types of accounting.There are several types of accounting, including financial accounting, cost accounting, and management accounting.Financial accounting focuses on preparing financial statements for external users, while cost accounting is used for internal decision-making.Management accounting provides information for planning, controlling, and decision-making by management.Section 2: Financial Statements2.1 What are financial statements?Financial statements are written records prepared by a company that convey its financial performance and financial position.They include the balance sheet, income statement, statement of cash flows, and statement of changes in equity.2.2 What is the balance sheet?The balance sheet is a financial statement that shows the company"s assets, liabilities, and shareholders" equity at a specific point in time.It provides a snapshot of the company"s financial position.2.3 What is the income statement?The income statement, also known as the profit and loss statement, shows the company"s revenues, expenses, and net income or loss for a specific period of time.It demonstrates the company"s ability to generate profit.2.4 What is the statement of cash flows?The statement of cash flows shows the inflows and outflows of cash from operating, investing, and financing activities during a specific period of time.It provides information about the company"s cash flow position and its ability to meet short-term obligations.Section 3: Accounting Principles and Concepts3.1 What are accounting principles?Accounting principles are rules and guidelines that govern the preparation of financial statements.They provide a framework forconsistent and comparable financial reporting.Some common accounting principles include the accrual basis of accounting, the going concern concept, and the monetary unit assumption.3.2 What is the accrual basis of accounting?The accrual basis of accounting recognizes revenues and expenses when they are earned or incurred, regardless of when cash is received or paid.This provides a more accurate representation of the company"s financial performance.3.3 What is the going concern concept?The going concern concept assumes that the company will continue its operations in the foreseeable future.This allows for the valuation of assets and liabilities on a long-term basis.3.4 What is the monetary unit assumption?The monetary unit assumption assumes that the value of money is stable over time and that financial information can be measured in a common unit of currency.This simplifies the accounting process and allows for meaningful comparison of financial data.Section 4: Accounting Records and Journal Entries4.1 What are accounting records?Accounting records are detailed records of all financial transactions of a company.They provide a chronological record of transactions and serve as the basis for preparing financial statements.4.2 What are journal entries?Journal entries are the means by which accounting transactions are recorded in the accounting records.They involve debiting one account and crediting another account to maintain the balance of the accounting equation.4.3 What is the accounting equation?The accounting equation, Assets = Liabilities + Shareholders" Equity, serves as the foundation of the double-entry bookkeeping system.It ensures that every transaction has equal and opposite effects on the accounting equation.Section 5: Financial Analysis5.1 What is financial analysis?Financial analysis is the process of evaluating the financial performance and position of a company.It involves interpreting financial statements and using ratios, trends, and other financial indicators to assess the company"s liquidity, solvency, and profitability.5.2 What are financial ratios?Financial ratios are calculations used to analyze the relationships between different financial values.They provide insights into the company"s performance and financial mon financial ratios include the current ratio, debt-to-equity ratio, and return on assets.5.3 What is the current ratio?The current ratio is a liquidity ratio that compares a company"s current assets to its current liabilities.It indicates the company"s ability to cover its short-term obligations.5.4 What is the debt-to-equity ratio?The debt-to-equity ratio is a leverage ratio that compares a company"s total debt to its shareholders" equity.It indicates the company"s level of financial risk and its。

会计英语第四版叶建芳

Interpretation of the Income Statement

要点一

Revenue

Revenue reports the total amount of income generated by a company through its normal business operations This can include sales of products or services, interest income, and other sources of income

Accounting Definition and Function

Preparing financial statements

Recording business transactions

Functions of Accounting

01

03 02

Accounting Definition and Function

Owner's Equity

Owner's equity reports the residual interest in the assets of the company after conducting its liabilities It reflects the amount of capital contributed by the owners and the retained earnings over time

Cash Flow from Operating AThcistsievctiiotnieofsthe cash flow

statement shows how much cash is generated from a company's normal business operations It includes cash received from customers and cash paid to suppliers, employees, and for other operating expenses

叶建芳会计英语中文版1-5

学习目标:1.2.3.编制多步式利润表4.5.编制特种日记账6.本章购货折扣和运输成本。

◇服务企业◇商品流通企业批发商和零售商是商品还会因商品存货的购买和销售而存在其他会计问题。

销售商品带来的收益叫销售收入,为出售而购买和准备商品存货的费用叫做销售成本。

在商品流通活动中使用的两个常见的等式是:净销售收入-销售成本=毛利毛利-经营费用=净利润(或净损失)商品存货是商品流通企业在正常商业过程中为出售而持有的货物。

◇定期盘存制和永续盘存制定期盘存制只在存货(通常年末)盘点时提供存货和销售成本数据。

永续盘存制持续地,不断更新存货和销售成本数据。

因此,定期盘存制和永续盘存制的区别在于如何记录商品存货的采购和销售。

比如定期盘存制使用一个暂时账户---采购账户记录购买商品的成本。

在定期盘存制下,企业根据对存货的盘点确定销售成本和和期末存货成本,进而编制财务报表。

永续盘存制企业在每次采购和商品销售时都及时更新销售成本和商品存货记录。

以前,销售量大且商品单价较低的企业多采用定期盘存制。

随着科技发展,目前这些企业也多采用永续盘存制。

实际盘点也必须在一个永续的制度下完成来使实际手头商品数目与会计记录的余额相一致。

4.2 采购、销售收入和销售成本◇商品采购——永续盘存制在永续盘存制下,所有的商品存货的赊购都要在购买时借记入商品存货账户中,例如:商品存货 xxx应付账款 xxx注意购货净额和总购买额不同。

要计算购货净额,我们需要用总采购额减去供应商提供的购货折扣,购货退回以及对供货商提供的不满意的商品的购货折让。

◇购货退回和折让在日记账中对购货退回和折让的处理如下:应付账款 xxx 商品存货 xxx◇商业折扣商业折扣是买卖双方在确定商品销售价格的谈判中达成的对价目表中所列价格的减让。

实际价格(发票价格)是用价目表中的价格减去商业折扣后得到的。

价目表中的原价和商业折扣均不出现在购销双方的账簿上,以发票价格记录交易。

商业折扣的使用使批发商和零售商节省了频繁更改价目表的成本。

会计英语(第四版)(叶建芳)05

On July 15, Play Clothes pays the full amount due to Kid’s Clothes.

Prepare the journal entry for Play Clothes.

credit terms are stated in the invoice.

2/10, n/30

Read as: “Two ten, net thirty”

YE SUN AccountingEnglish

18

Credit Terms and Cash Discounts

2/10, n/30

Percentage of Discount

• Record discount when taken.

• Net of discount

• Charge discounts not taken when paid.

YE SUN AccountingEnglish

11

Terminology

Purchase = receipt of merchandise not to placing of a purchase order.

• Tangible items that will be consumed in the course of normal operations.

• e.g., office supplies, lubricants, repair parts.

• Not sold and not accounted for as part of cost of goods sold.

• 3 types of inventories;

• Materials. • Work-in-process. • Finished goods.

会计英语(第四版)

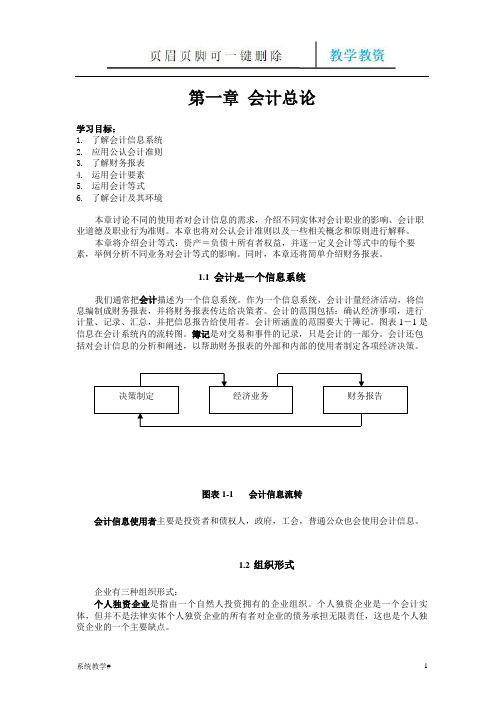

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1 会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的围要大于簿记。

图表1-1是信息在会计系统的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2 组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3 编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计英语概述

2019/2/13

Decision Making

Economic Events

Reports

Exhibit 1-1

Financial statements report accounting information about resources, earning prospects, expected cash collections, incurred expenses, repayment ability, tax collection and negotiating wage agreements.

1、transaction n.交易;处理 Related transactions 关联交易 Transactions cost 交易成本 Business transactions 经济业务;商业交易 2、accounts n.帐目;会计账户;会计账簿 Accounts manager 会计部经理 Accounts receivables 应收账款 Accounts payable应付账款 Accounts department 会计部 3、Statements n.报告;报表 Accounting statement 会计报表=financial statement=statements Financial statements analysis 财务报表分析 Combination statements 汇总报表;合并报表 Suppliers statements 供应商对账单

【 LESSON 】

Recording Transactions

【 LESSON 】

Adjusting the Accounts, Preparing the Statements, and Completing the Accounting Cycle

会计英语叶建芳第四版课后题

会计英语叶建芳第四版课后题以下为您提供 20 个关于会计英语的示例,包含英语释义、短语、单词、用法和双语例句:1. **Asset**- 英语释义:Something valuable that a business or person owns, such as property, equipment, or money owed to them.- 短语:Fixed asset(固定资产);Current asset(流动资产)- 单词用法:Assets are recorded on the balance sheet.- 双语例句:The company's assets include land and buildings.(公司的资产包括土地和建筑物。

)2. **Liability**- 英语释义:A debt or obligation that a business or person owes.- 短语:Long-term liability(长期负债);Current liability(流动负债)- 单词用法:Liabilities must be paid in the future.- 双语例句:The company has a large liability for outstanding loans.(公司有大量未偿还贷款的负债。

)3. **Revenue**- 英语释义:The income that a business receives from its normal activities, such as selling goods or services.- 短语:Operating revenue(营业收入);Non-operating revenue (非营业收入)- 单词用法:Revenue increased significantly this year.- 双语例句:The company's revenue comes mainly from product sales.(公司的收入主要来自产品销售。

叶建芳会计英语中文版1-5

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计英语(第四版)(完整教资)

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1 会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

决策制定经济业务财务报告图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2 组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3 编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

实用会计英语(第四版) (5)

10 5.2 Inventory System

Periodic inventory system

▲ Steps under Periodic inventory system

(1) Recording cost of goods purchased (2) Purchase returns and allowances (3) Determining cost of goods purchased (4) Recording sales of merchandise (5) Determining cost of goods on hand (ending inventory) (6) Computing cost of goods sold

Unit 5 Inventory

1

葛军 吴晓华

高等教育出版社

2

Outline of Unit 5

5.1 The Concept of Inventory 5.2 Inventory System 5.3 Inventory Measurement Methods

高等教育出版社

3

5.1 The Concept of Inventory

The importance of inventory: ▲ Inventories are particularly significant because inventories affect both the balance sheet and the income statement.

(1) In the balance sheet of merchandising companies, inventory is frequently the most significant current asset.

会计英语叶建芳答案

会计英语叶建芳答案【篇一:《会计英语》考试大纲】>一、课程性质与目标(一)课程性质《会计英语》是会计学专业的学科基础课程之一,是为培养既具备国际相关专业知识和业务技能又具备熟练运用专业英语从事专业工作的人才而开设的一门专业限选课。

本课程的先修课程为会计学原理,大学英语等。

(二)课程目标本课程讲授内容基于国际会计准则之下的会计概念、财务报表、流动资产、长期资产、负债与或有事项、所有者权益以及会计的其他领域如成本会计,管理会计和审计的概况等。

通过本课程的学习,要求学生了解中国和美国会计处理的相同和不同,掌握基本的会计处理的英文表达方式,熟练掌握专业的英文术语。

通过考核,检查学生是否具备阅读会计英语文献,基础的专业交流能力,基础的专业做账能力。

为学生今后在外企工作,从事外贸工作打下良好的基础。

二、考试内容与考核目标chapter 1 conceptual framework underlying accounting (一)考试内容1. definition of accounting2. objectives of financial accounting3. the qualitative characteristics of accounting information4. the basic elements of financial statements and equations.5. the basic accounting assumptions(二)考核目标1. to learn objectives of financial accounting2. to learn the basic accounting assumptions3. master the basic elements of financial statements and equations4. proficiency in the qualitative characteristics o faccounting information.chapter 2 the accounting information system(一)考试内容1. the basic terminology in collecting accounting data.2. the double-entry system3. the procedures of accounting cycle(二)考核目标1. proficency the basic terminology in collecting accounting data.2. understand the double-entry system3. understand the procedures of accounting cyclechapter 3 financial reporting(一)考试内容1. the elements of balance sheet and how to prepare the balance sheet2. the elements of income statement and how to prepare the income statement3. the elements of the statement of cash flows4. the five sections of full disclosure.(二)考核目标1. proficency the elements of balance sheet and how to prepare the balance sheet.2. prjoficency the elements of income statement and how to prepare the income statement.3. master the elements of the statement of cash flows4. to learn the five sections of full disclosure.chapter 4 current assets(一)考试内容1. the definition of cash and cash equivalents2. the definition of receivables and classification of receivables.3. the definition of account receivables, two discounts, and two methods used to calculate the exchange price under cash discount—the gross method and the net method4. two methods to deal with un-collectible accounts receivables—the direct write-off method and the allowance method5. two methods to determine the inventory quantity—periodic inventory system and perpetual inventory system6. master four methods available to account for the flow of goods from purchase to sale:(1) specific identification,(2) first in, first out,(3) last in, first out,(4) averaging7. three methods to report temporary investment-- historical cost, market value, and the lower of cost or market(二)考核目标1. understand the definition of cash and cash equivalents2. learn the definition of receivables and classification of receivables.3. understand the definition of account receivables, two discounts, and two methods used to calculate the exchange price under cash discount—the gross method and the net method4. figure out two methods to deal with un-collectible accounts receivables—the direct write-off method and the allowance method5. identify two methods to determine the inventory quantity—periodic inventory system and perpetual inventory system6. master four methods available to account for the flow of goods from purchase to sale:(1) specific identification,(2) first in, first out,(3) last in, first out,(4) averaging7. understand three methods to report temporary investment-- historical cost, market value, and the lower of cost or marketchapter 5 long-term assets(一)考试内容1. the characteristics of property, plant, and equipment, and how to record ppe under different situations.2. the methods of depreciation.3. capitalization expenditure and revenue expenditure of the fixed assets.4. the disposition of fixed assets5. three circumstances of investment of equity securities.6. three different debt securities.7. the characteristics of intangible assets.8. the different kinds of intangible assets(二)考核目标1. to identify the characteristics of property, plant, and equipment, and how to record ppe under different situations.2. to understand the methods of depreciation.3. to figure out capitalization expenditure and revenue expenditure of the fixed assets.4. to learn how to deal with the disposition of fixed assets5. to understand the three circumstances of investment of equity securities.6. to learn the three different debt securities.7. to understand the characteristics of intangible assets.8. to learn the different kinds of intangible assetschapter 6 liabilities and contingencies(一)考试内容1. the definition of current liabilities and related elements, especially notes payable2. the classification of bonds payable.3. the definition of par value, premium, discount, stated interest rate, the effective yield, and the method to deal with amortization of premium and discount.4. the characteristics of contingency(二)考核目标1. understand the definition of current liabilities related elements, especially notes payable2. identify the classification of bonds payable.3. comprehend the definition of par value, premium, discount, stated interest rate, the effective yield, and the method to deal with amortization of premium and discount.4. understand the characteristics of contingencychapter 7 stockholders’ equity(一)考试内容1. the definition and characteristics of equity2. the sole proprietorships’ characteristics.3. the partnerships’ characteristics.4. the corporation’s characteristics.5. the difference between common stock and preferred stock.6. two methods to record treasury stock(二)考核目标1. understand the definition and characteristics of equity2. identify the sole proprietorships’ charact eristics.3. learn the partnerships’ characteristics.4. understand the corporation’s characteristics.5. figure out the difference between common stock and preferred stock.6. master two methods to record treasury stockchapter8 the other fields of accounting---cost accounting, managerialaccounting, auditing(一)考试内容1. the two principles of cost accounting systems2. the characteristics of managerial accounting3. the characteristics of auditing and sevral audit reports (二)考核目标1. understand the essential of costing accounting and its scope2. learn the characteristics of managerial accounting3. figure out the difference between auditing and accounting三、教材及参考资料(一)本课程使用的教材《会计英语简明教程》 [英文版] 李越冬编著西南财经大学出版社2005年5月第1版(二)参考资料1.叶建芳,孙红星,何瑞丰.会计英语.上海:复旦大学出版社,2007年2.于久洪. 会计英语.北京:中国人民大学出版社,2007年3. 张国华,王晓巍著.财会专业英语.北京:科学出版社,2007年四、考试题(样题)本试题包括填空(考查对定义的理解)、调整分录(会计循环)、会计处理、完成资产负债表(考查资产负债表的要素分类)、编制利润表。

会计英语章叶建芳and孙红星

业提供服务等实现的义务。 负债包括应付账款,应付票据,应付工资,应付税款,应付利息和应付债券。 权益(独资企业的所有者权益,合伙企业的合伙人权益,及公司的股东权益)是剩余权益。IASB

税务* - 编制纳税表 - 计划 - 规范控制 - 调研 - 咨询

相关会计活动 - 债权人 - 顾问 - 分析员 - 商人 - 经理 - 董事 - 证券包销商 - 计划者

1.6 会计要素和会计等式使用

◇什么是会计等式 会计要素是会计实务的基本分类。会计要素是反映企业财务状况和经营结果的基本元素。我们已 经介绍了资产负债表。资产和对资产的要求权之间的关系可以用如下等式表示:

决策制定

经济业务

财务报告

会计信息使用者主要是投资者和债权人,政府,工会和普通公众也会使用会计信息。

1.2 组织形式

企业有三种组织形式: 独资企业是指由一个自然人投资拥有的企业组织。独资企业是一个会计实体,但并不是法律实体。 所有者对企业的债务承担无限责任,这也是独资企业的一个主要缺点。 合伙企业与独资企业的区别只是在于它有两个或两个以上的所有者。合伙企业的所有者被称为合 伙人。现实商业活动中有许多不同类型的合伙企业。 公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。股东不对公司的债务负责。 有限责任是公司这种组织形式的一个显著优点。公司的所有权被分为股份。股票可以在所有者之间转 让。

交易对会计等式的影响 所有的经济交易,无论是最简单的还是最复杂的,都可以用会计等式中三类基本要素的变化来表示。 会计等式应用于所有经济和法律实体——即用于独资企业,也用于大公司。我们必须理解的要点: 1. 每笔交易至少影响会计等式中的两个项目(复式记账)。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

May have materials inventories.

YE SUN AccountingEnglish

7

Types of Companies/Inventories (Cont.)

Professional service firms (accounting firms, legal firms)

GENERAL JOURNAL

Date Account Titles and Explanation Debit Credit

YE SUN AccountingEnglish

21

Recording Purchases at Gross Invoice Price

On July 6, Play Clothes purchased $4,000 of merchandise on credit with terms of 2/10, n/30 from Kid’s Clothes. Prepare the journal entry for Play Clothes.

Service company

Provides intangible services.

YE SUN AccountingEnglish

4

Types of Companies/Inventories

Merchandising

Sells goods in same form in which they are acquired. Inventory costs (and costs of goods sold) = acquisition costs.

YE SUN AccountingEnglish

9

Merchandise Inventory

Inventories accounted for at cost.

Cost includes cost of

Acquiring merchandise (invoice cost of goods, freight-in) Making goods ready for sale. ( unpacking and marking)

YE SUN AccountingEnglish

10

Methods of Accounting for Purchase (or cash) Discounts

Record at invoice price( in china)

Record discount when taken. Charge discounts not taken when paid.

Detailed record is useful. Built in check. Identifies shrinkage by item. Income statement can be prepared without taking a physical inventory.

YE SUN AccountingEnglish

YE SUN AccountingEnglish

3

Types of Companies

Merchandising company

Sells goods in same form as acquired. Converts raw material into finished goods.

Manufacturing company

Beginning inventory of current period = ending inventory of preceding period.

COGS = COGA - End. Inventory

YE SUN AccountingEnglish

15

Perpetual Inventory Method

20

Recording Purchases at Gross Invoice Price

On July 6, Play Clothes purchased $4,000 of merchandise on credit with terms of 2/10, n/30 from Kid’s Clothes. Prepare the journal entry for Play Clothes.

Count inventory (i.e., a physical inventory is taken) at the end of the period. Multiply count times cost for each item to determine total amount of inventory.

Tangible items that will be consumed in the course of normal operations.

e.g., office supplies, lubricants, repair parts.

Not sold and not accounted for as part of cost of goods sold.

Periodic inventory method. Perpetual inventory method.

YE SUN AccountingEnglish

14

Periodic Inventory Method

Determine amount of ending inventory and deduce costs of goods sold.

Lesson 5

Inventory and Cost of Goods Sales

YE SUN AccountingEnglish

1

Inventory Issues

What is inventory? What costs are included in inventory? How do we separate COGS from End. Inv?

Measure amount actually delivered to customers; deduce ending inventory. Perpetual inventory record is kept for each item in the inventory.

Advantages of perpetual inventory method:

Intangible inventory costs are costs incurred for client but not yet billed called jobs-in-progress or unbilled costs.

YE SUN AccountingEnglish

8

Supplies

19 YE SUN AccountingEnglish

Recording Purchases at Gross Invoice Price

Purchases are recorded at their gross amounts.

Gross Method

Purchase discounts taken are recorded when payment is made inside the discount period. YE SUN AccountingEnglish

பைடு நூலகம்

Net of discount

YE SUN AccountingEnglish

11

Terminology

Purchase = receipt of merchandise not to placing of a purchase order.

Usually title transfers when goods are shipped (FOB shipping point).

GENERAL JOURNAL

Date Account Titles and Explanation Accounts Payable (Kid's Clothes)

YE SUN AccountingEnglish

Debit 4,000

Credit 4,000

22

July 6 Inventory

Recording Purchases at Gross Invoice Price

16

Account for the purchase

YE SUN AccountingEnglish

17

Credit Terms and Cash Discounts

When manufacturers and wholesalers sell their products on account, the credit terms are stated in the invoice.

Net purchases = gross purchases -purchase returns and allowances + freight-in

YE SUN AccountingEnglish

13

Measurement Issue

Dividing goods available for sale between COGS and End. Inventory. 2 approaches:

2/10, n/30

Read as: “Two ten, net thirty”