会计英语英文版

会计英语词汇英文解释

1.Accounting(会计)The process of indentifying, recording, summarizing and reporting economic information to decision makers.2.Financial accounting(财务会计)The field of accounting that serves external decision makers, such as stockholders, suppliers, banks and government agencies.3.Management accounting(管理会计)The field of accounting that serves internal decision makers, such as top executives, department heads and people at other management levels within an organization.4.Annual report(年报)A combination of financial statements, management discussion and analysis and graphs and charts that is provided annually to investors.5.Balance sheet (statement of financial position, statement of financial condition)(资产负债表)A financial statement that shows the financial status of a business entity at a particular instant in time.6.Balance sheet equation(资产负债方程式)Assets = Liabilities + Owners' equity.7.Assets(资产)Economic resources that are expected to help generate future cash inflows or help reduce future cash outflows.8.Liabilities (负债)Economic obligations of the organization to outsiders ,or claims against its assets by outsiders.9.Owners’ equity (所有者权益)The residual interest in the organization’s assets after deducting liabilities.10.Notes payable (应付票据)Promissory notes that are evidence of a debt and state the terms of payment.11.Entity (实体)An organization or a section of an organization that stands apart from other organization and individuals as a separate economics unit.12.Transaction (交易)Any event that both affects the financial position of an entity and be reliably recorded in money terms.13.Inventory (存货)Goods held by a company for the purpose of sale to customers.14.Account (帐户)A summary record of the changes in a particular assets, liability, or owne r’ equity.15. Account payable (应付帐款)A liability that results from a purchase of goods or services on account.17.Creditor (债权人)A person or entity to whom money is owed.18.Debtor (债务人)A person or entity that owes money to another.19.Sole proprietorship (个体经营、独资经营)A separate organization with a single owner.20.Partnership (合伙)A form of organization that joins two or more individuals together as co-owners(共有人).21.Corporation (公司)A business organization that is created by individual state laws.22.Limited liability (有限责任)A feature of the corporate form of organization whereby corporate creditors ordinarily have claims against the corporate assets only.23.Publicly owned (公有)A corporation in which shares in the ownership are sold to the public.24.Privately owned (私有)A corporation owned by a family, a small group of shareholders, or a single individual, in which shares of ownership are not publicly sold.25.Stockholders’ equity (shareholders’ equi ty) (股东权益)Owners’ equity of a corporation.The excess of assets over liabilities of a corporation.26.Paid-in capital(实际投入资本)The total capital investment in a corporation by its owners both at and subsequent to the inception of business.27.Par value(票面值)The nominal dollar amount printed on stock certificates.29.Auditor (审计师)A person who examines the information used by managers to prepare the financial statements and attests to the credibility of those statements.31.Audit (审计)An examination of transactions and financial statement made in accordance with generally accepted auditing standards.33. Fiscal year (会计、财政年度)The year established for accounting purposes.34.Interim periods (中期)The time spans established for accounting purposes that are less than a year.35.Revenues(sales) (收入OR商品销售收入)Increases in owners’ equity arising from increases in assets received in exchange for the delivery of goods or services to customers.36.Expenses (费用)Decreases in owners’ equity that arise be cause goods or services are delivered to customers.37.Income (profit ,earnings) (收益、利润)The excess of revenues over expenses.39.Accrual basis (应计制、权责发生制)Accounting method that recognizes the impact of transactions on the financial statements in the time periods when revenues and expenses occur.40.Cash basis (收付实现制)Accounting method that recognizes the impact of transactions on the financial statements only when cash is received or disbursed.43.Cost of goods sold (cost of sales) (销售成本)The original acquisition cost of the inventory that was sold to customers during the reporting period.44.Matching (配比)The recording of expenses in the same time period as the related revenues are recognized.47.Depreciation (折旧)The systematic allocation of the acquisition cost of long-lived of fixed assets to the expenses accounts of particular periods that benefit from the use of the assets. income (净利润)The remainder after all expenses has been deducted from revenues.49.Income statement (statement of earnings, operating statement) (收益表)A report of all revenues and expenses pertaining to a specific time period.50.Statement of cash flows (cash flow statement) (现金流量表)A required statement that reports the cash receipts and cash payments of an entity during a particular period. loss (净损失)The difference between revenues and expenses when expenses exceed revenues.52.Cash dividends (现金股利)Distribution of cash to stockholders that reduce retained income.53.Statement of retained income (利润分配表)A statement that lists the beginning balance in retained income, followed by a description of any changes that occurred during the period, and the ending balance.54.Statement of income and retained income (收入及利润分配表)A statement that included a statement of retained income at the bottom of an income statement.55.Earnings per share (EPS) (每股收益)Net income divided by average number of common shares outstanding.56.Price-earnings ratio (P-E) (市盈率)Market price per share of common stock divided by earnings per share of common stock.57.Dividend-yield ratio (股息率)Common dividends per share dividend by market price per share.58.Dividend-payout ratio (派息率)Common dividends per share dividend by earnings per share.59.Double-entry system (复试记账法)The method usually followed for recording transactions, whereby at least two accounts are always affected by each transaction.60.Ledger (分类账)The records for a group of related accounts kept current in a systematic manner.61.General ledger (总分类账)The collection of accounts that accumulates the amounts reported in the major financial statements.62.T-account (T形账户)Simplified version of ledger accounts that takes the form of the capital letter T.63.Balance (余额)The difference between the total left-side and right-side amounts in an account at any particular time.64.Debit (借方)An entry or balance on the left side of an account.65.Credit (贷方)An entry or balance on the right side of an account.66.Charge (Debit)A word often used instead of debit.67.Source documents (原始凭证)The supporting original records of any transactions.68.Book of original entry (原始分录帐本)A formal chronological record of how the entity’s transactions affect the balances in pertinent accounts.69.General journal (普通日记账)The most common example of a book of original entry; a complete chronological record of transactions.70.Trial balance (试算表)A list of all accounts in the general ledger with their balance.71.Journalizing (记入分类帐)The process of entering transactions into the journal.72.Journal entry (日记帐分录)An analysis of the affects of a transaction on the accounts, usually accompanied by an explanation.81.Accumulated depreciation (allowance for depreciation) (累计折旧)The cumulative sum of all depreciation recognized since the date of acquisition of the particular assets described.82.Data processing 数据处理The totality to the procedures used to record, analyze store, and report on chosen activities.83.Explicit transactions (显性交易)Events such as cash receipts and disbursements, credit purchases, and credit sales that trigger nearly all day-to-day routine entries.84.Implicit transactions (非显性交易)Events (such as the passage of time) that do not generate source documents or visible evidence of the event and are not recognized in the accounting records until the end of an accounting period.85.Adjustments (adjusting entries) (调帐)End-of-period entries that assign the financial effects of implicit transactions to the appropriate time periods.86.Accrue (应计)To accumulate a receivable or payable during a given period even though no explicit transactions occurs.87.Unearned revenue (revenue received in advance, deferred revenue, deferred credit) (未实现收入)Revenue received and recorded before it is earned.88.Pretax income (税前利润)Income before income taxes.89.Classified balance sheet (分类资产负债表)A balance sheet that groups the accounts into subcategories to help readers quickly gain a perspective on the company’s financial position.90.Current assets (流动资产)Cash plus assets that are expected to be converted to cash or sold or consumed during the next 12 months or within the normal operating cycle if longer that a year.91.Current liabilities (流动负债)Liabilities that fall due within the coming year or within the normal operating cycle if longer than a year.92.Working capital (营运资金、资本)The excess of current assets over current liabilities.93.Solvency (偿付能力)An entity’s ability to meet its immediate financial obligations as they become due.94.Current ratio (working capital ratio) (流动比率)Current assets divided by current liabilities.Current ratio = Current assets / Current liabilities.95.Report format (报表格式之一)A classified balance sheet with the assets at the top. Example:Balance Sheet, January 31,20X2Assets 1999 1998Current assetsCashAccounts receivable……Total current assetsLong-term assetsStore equipmentAccumulated depreciationTotal assetsLiabilities and Owners’ Equity 1999 1998 Current liabilitiesNote payableAccounts payable…Total current liabilities Stockholder’s equityPaid-in capitalRetained incomeTotal liabilities and owners’ equity96.Account format (报表格式之二)A classified balance sheet with the assets at the left. Example:Balance Sheet, January 31,20X2Assets Liabilities and Owners’ EquityCurrent assets Current liabilitiesCash Note payableAccounts receivable Accounts payable… …Total current assets Total current liabilitiesLong-term assets Stockholder’s equityStore equipment Paid-in capitalAccumulated depreciation Retained incomeTotal Total97.Single-step income statement (单一步骤收入表)An income statement that groups all revenues together and then lists and deducts all expenses together without drawing any intermediate subtotals.98.Multiple-step income statement (复合步骤收入表)An income statement that contains one or more subtotals that highlight significant relationships.99.Gross profit (gross margin) (毛利)The excess of sales revenue over the cost of the inventory thatwas sold.100.Operating income (operating profit) (营业收入)Gross profit less all operating expenses.101.Profitability (收益能力)The ability of a company to provide investors with a particular rate of return on their investment.102.Gross profit percentage (gross margin percentage) (毛利率)Gross profit divided by sales.Gross profit percentage=Gross profit / Sales103.Return on sales ratio (销售收益率)Net income divided by sales,104.Return on stockholders’ equity ratio (股东权益收益率)Net income divided by invested capital (measured by average stockholder’s equity)。

会计英语分录中英对照

2 负债 liabilities21~ 22 流动负债 current liabilities211 短期借款 short-term borrowings(debt)2111 银行透支 bank overdraft2112 银行借款 bank loan2114 短期借款 -业主 short-term borrowings - owners 2115 短期借款 -员工 short-term borrowings - employees 2117 短期借款-关系人 short-term borrowings- related parties2118 短期借款 -其它 short-term borrowings - other 212 应付短期票券 short-term notes and bills payable 2121 应付商业本票 commercial paper payable2122 银行承兑汇票 bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价 discount on short-term notes and bills payable213 应付票据 notes payable2131 应付票据 notes payable2137 应付票据-关系人 notes payable - related parties 2138 其它应付票据 other notes payable214 应付帐款 accounts pay able2141 应付帐款 accounts payable2147 应付帐款-关系人 accounts payable - related parties 216 应付所得税 income taxes payable2161 应付所得税 income tax payable217 应付费用 accrued expenses2171 应付薪工 accrued payroll2172 应付租金 accrued rent payable2173 应付利息 accrued interest payable2174 应付营业税 accrued VAT payable2175 应付税捐 -其它 accrued taxes payable- other2178 其它应付费用 other accrued expenses payable218~219 其它应付款 other payables2181 应付购入远汇款 forward exchange contract payable 2182 应付远汇款-外币forward exchange contract payable - foreign currencies2183 买卖远汇溢价 premium on forward exchange contract 2184 应付土地房屋款payables on land and building purchased2185 应付设备款 Payables on equipment2187 其它应付款-关系人 other payables - related parties 2191 应付股利 dividend payable2192 应付红利 bonus payable2193 应付董监事酬劳 compensation payable to directors and supervisors2198 其它应付款 -其它 other payables - other226 预收款项advance receipts2261 预收货款 sales revenue received in advance2262 预收收入 revenue received in advance2268 其它预收款 other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债 corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款 long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债 other current liabilities2281 销项税额 VAT received(or output tax) 2283 暂收款 temporary receipts2284 代收款 receipts under custody2285 估计售后服务/保固负债estimated warranty liabilities2291 递延所得税负债 deferred income tax liabilities 2292 递延兑换利益 deferred foreign exchange gain 2293 业主(股东)往来 owners' current account2294 同业往来 current account with others2298 其它流动负债-其它 other current liabilities - others23 长期负债 long-term liabilities231 应付公司债 corporate bonds payable2311 应付公司债 corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款 long-term loans payable2321 长期银行借款 long-term loans payable - bank 2324 长期借款 -业主 long-term loans payable - owners 2325 长期借款 -员工 long-term loans payable - employees 2327 长期借款-关系人 long-term loans payable - related parties2328 长期借款 -其它 long-term loans payable - other 233 长期应付票据及款项 long-term notes and accounts payable2331 长期应付票据 long-term notes payable2332 长期应付帐款 long-term accounts pay-able2333 长期应付租赁负债long-term capital lease liabilities2337 长期应付票据及款项-关系人 Long-term notes and accounts payable - related parties2338 其它长期应付款项 other long-term payables234 估计应付土地增值税 accrued liabilities for land value increment tax2341 估计应付土地增值税 estimated accrued land value incremental tax pay-able235 应计退休金负债 accrued pension liabilities2351 应计退休金负债 accrued pension liabilities238 其它长期负债 other long-term liabilities2388 其它长期负债-其它 other long-term liabilities - other28 其它负债 other liabilities281 递延负债 deferred liabilities2811 递延收入 deferred revenue2814 递延所得税负债 deferred income tax liabilities 2818 其它递延负债 other deferred liabilities286 存入保证金 deposits received2861 存入保证金 guarantee deposit received288 杂项负债 miscellaneous liabilities2888 杂项负债-其它 miscellaneous liabilities – other3 业主权益 owners' equity31 资本 capital311 资本(或股本) capital3111 普通股股本 capital - common stock3112 特别股股本 capital - preferred stock3113 预收股本 capital collected in advance3114 待分配股票股利 stock dividends to be distributed 3115 资本 capital32 资本公积 additional paid-in capital321 股票溢价 paid-in capital in excess of par3211 普通股股票溢价 paid-in capital in excess of par- common stock3212 特别股股票溢价 paid-in capital in excess of par- preferred stock323 资产重估增值准备capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积 capital surplus from gain ondisposal of assets3241 处分资产溢价公积 capital surplus from gain on disposal of assets325 合并公积 capital surplus from business combination 3251 合并公积capital surplus from business combination326 受赠公积 donated surplus3261 受赠公积 donated surplus328 其它资本公积 other additional paid-in capital 3281 权益法长期股权投资资本公积 additional paid-in capital from investee under equity method3282 资本公积- 库藏股票交易additional paid-in capital - treasury stock trans-actions33 保留盈余(或累积亏损) retained earnings (accumulated deficit)331 法定盈余公积 legal reserve3311 法定盈余公积 legal reserve332 特别盈余公积 special reserve3321 意外损失准备 contingency reserve3322 改良扩充准备 improvement and expansion reserve3323 偿债准备special reserve for redemption of liabilities3328 其它特别盈余公积 other special reserve335 未分配盈余(或累积亏损)retained earnings-unappropriated (or accumulated deficit)3351 累积盈亏 accumulated profit or loss3352 前期损益调整 prior period adjustments3353 本期损益 net income or loss for current period 34 权益调整 equity adjustments341 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments 3411长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments 342累积换算调整数cumulative translation adjustment 3421 累积换算调整数cumulative translation adjustments343 未认列为退休金成本之净损失net loss not recognized as pension cost3431 未认列为退休金成本之净损失net loss not recognized as pension costs35 库藏股 treasury stock351 库藏股 treasury stock3511 库藏股 treasury stock36 少数股权 minority interest361 少数股权 minority interest3611 少数股权 minority interest4 营业收入 operating revenue41 销货收入 sales revenue411 销货收入 sales revenue4111 销货收入 sales revenue4112 分期付款销货收入 installment sales revenue 417 销货退回 sales return4171 销货退回 sales return419 销货折让 sales allowances4191 销货折让 sales discounts and allowances46 劳务收入 service revenue461 劳务收入 service revenue4611 劳务收入 service revenue47 业务收入 agency revenue471 业务收入 agency revenue4711 业务收入 agency revenue48 其它营业收入 other operating revenue488 其它营业收入-其它 other operating revenue 4888 其它营业收入-其它 other operating revenue - other 5 营业成本 operating costs51 销货成本 cost of goods sold511 销货成本 cost of goods sold5111 销货成本 cost of goods sold5112 分期付款销货成本 installment cost of goods sold 512 进货 purchases5121 进货 purchases5122 进货费用 purchase expenses5123 进货退出 purchase returns5124 进货折让 charges on purchased merchandise513 进料 materials purchased5131 进料 material purchased5132 进料费用 charges on purchased material5133 进料退出 material purchase returns5134 进料折让 material purchase allowances514 直接人工 direct labor5141 直接人工 direct labor515~518 制造费用 manufacturing overhead5151 间接人工 indirect labor5152 租金支出 rent expense, rent5153 文具用品 office supplies (expense)5154 旅费 travelling expense, travel5155 运费 shipping expenses, freight5156 邮电费 postage (expenses)5157 修缮费 repair(s) and maintenance (expense )5158 包装费 packing expenses5161 水电瓦斯费 utilities (expense)5162 保险费 insurance (expense)5163 加工费 manufacturing overhead - outsourced5166 税捐 taxes5168 折旧 depreciation expense5169 各项耗竭及摊提 various amortization5172 伙食费 meal (expenses)5173 职工福利 employee benefits/welfare5176 训练费 training (expense)5177 间接材料 indirect materials5188 其它制造费用 other manufacturing expenses56 劳务成本制 ervice costs561 劳务成本 service costs5611 劳务成本 service costs57 业务成本 gency costs571 业务成本 agency costs5711 业务成本 agency costs58 其它营业成本 other operating costs588 其它营业成本-其它 other operating costs-other 5888 其它营业成本-其它 other operating costs - other 6 营业费用 operating expenses61 推销费用 selling expenses615~618 推销费用 selling expenses6151 薪资支出 payroll expense6152 租金支出 rent expense, rent6153 文具用品 office supplies (expense)6154 旅费 travelling expense, travel6155 运费 shipping expenses, freight6156 邮电费 postage (expenses)6157 修缮费 repair(s) and maintenance (expense)6159 广告费 advertisement expense, advertisement 6161 水电瓦斯费 utilities (expense)6162 保险费 insurance (expense)6164 交际费 entertainment (expense)6165 捐赠 donation (expense)6166 税捐 taxes6167 呆帐损失 loss on uncollectible accounts6168 折旧 depreciation expense6169 各项耗竭及摊提 various amortization6172 伙食费 meal (expenses)6173 职工福利 employee benefits/welfare6175 佣金支出 commission (expense)6176 训练费 training (expense)6188 其它推销费用 other selling expenses62 管理及总务费用 general & administrative expenses 625~628 管理及总务费用general & administrative expenses6251 薪资支出 payroll expense6252 租金支出 rent expense, rent6253 文具用品 office supplies6254 旅费 travelling expense, travel6255 运费 shipping expenses,freight6256 邮电费 postage (expenses)6257 修缮费 repair(s) and maintenance (expense)6259 广告费 advertisement expense, advertisement 6261 水电瓦斯费 utilities (expense)6262 保险费 insurance (expense)6264 交际费 entertainment (expense)6265 捐赠 donation (expense)6266 税捐 taxes6267 呆帐损失 loss on uncollectible accounts6268 折旧 depreciation expense6269 各项耗竭及摊提 various amortization6271 外销损失 loss on export sales6272 伙食费 meal (expenses)6273 职工福利 employee benefits/welfare6274 研究发展费用 research and development expense 6275 佣金支出 commission (expense)6276 训练费 training (expense)6278 劳务费 professional service fees6288 其它管理及总务费用other general and administrative expenses63 研究发展费用 research and development expenses 635~638 研究发展费用research and development expenses6351 薪资支出 payroll expense6352 租金支出 rent expense, rent6353 文具用品 office supplies6354 旅费 travelling expense, travel6355 运费 shipping expenses, freight6356 邮电费 postage (expenses)6357 修缮费 repair(s) and maintenance (expense)6361 水电瓦斯费 utilities (expense)6362 保险费 insurance (expense)6364 交际费 entertainment (expense)6366 税捐 taxes6368 折旧 depreciation expense6369 各项耗竭及摊提 various amortization6372 伙食费 meal (expenses)6373 职工福利 employee benefits/welfare6376 训练费 training (expense)6378 其它研究发展费用 other research and development expenses7 营业外收入及费用 non-operating revenue and expenses, other income(expense)71~74 营业外收入 non-operating revenue711 利息收入 interest revenue7111 利息收入 interest revenue/income712 投资收益 investment income7121 权益法认列之投资收益investment income recognized under equity method7122 股利收入 dividends income7123 短期投资市价回升利益gain on market price recovery of short-term investment713 兑换利益 foreign exchange gain7131 兑换利益 foreign exchange gain714 处分投资收益 gain on disposal of investments 7141 处分投资收益 gain on disposal of investments 715 处分资产溢价收入 gain on disposal of assets7151 处分资产溢价收入 gain on disposal of assets748 其它营业外收入 other non-operating revenue7481 捐赠收入 donation income7482 租金收入 rent revenue/income7483 佣金收入 commission revenue/income7484 出售下脚及废料收入 revenue from sale of scraps 7485 存货盘盈 gain on physical inventory7486 存货跌价回升利益 gain from price recovery of inventory7487 坏帐转回利益 gain on reversal of bad debts7488 其它营业外收入-其它 other non-operating revenue- other items75~ 78 营业外费用 non-operating expenses751 利息费用 interest expense7511 利息费用 interest expense752 投资损失 investment loss7521 权益法认列之投资损失investment loss recog- nized under equity method7523 短期投资未实现跌价损失unrealized loss on reduction of short-term investments to market753 兑换损失 foreign exchange loss7531 兑换损失 foreign exchange loss754 处分投资损失 loss on disposal of investments7541 处分投资损失 loss on disposal of investments755 处分资产损失 loss on disposal of assets7551 处分资产损失 loss on disposal of assets788 其它营业外费用 other non-operating expenses7881 停工损失 loss on work stoppages7882 灾害损失 casualty loss7885 存货盘损 loss on physical inventory7886 存货跌价及呆滞损失 loss for market price decline and obsolete and slow-moving inventories7888 其它营业外费用-其它 other non-operating expenses- other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax expense (or benefit) 811 所得税费用(或利益) income tax expense (or benefit) 8111 所得税费用(或利益) income tax expense ( or benefit) 9 非经常营业损益 nonrecurring gain or loss91 停业部门损益gain(loss) from discontinued operations911 停业部门损益-停业前营业损益 income(loss) from operations of discontinued segments9111 停业部门损益-停业前营业损益 income(loss) from operations of discontinued segment912 停业部门损益-处分损益 gain(loss) from disposal of discontinued segments9121 停业部门损益-处分损益 gain(loss) from disposalof discontinued segment92 非常损益 extraordinary gain or loss921 非常损益 extraordinary gain or loss9211 非常损益 extraordinary gain or loss93 会计原则变动累积影响数 cumulative effect of changesin accounting principles931 会计原则变动累积影响数cumulative effect of changes in accounting principles9311 会计原则变动累积影响数 cumulative effect of changes in accounting principles94 少数股权净利 minority interest income941 少数股权净利 minority interest income9411 少数股权净利 minority interest income中英文资产负债表资产 ASSETS流动资产: CURRENT ASSETS:现金 Cash on hand银行存款 Cash in bank有价证券 Marketable securities 应收票据 Notes receivable 应收账款 Accounts receivable 减:坏账准备 Less:Provision for bad debts 预付帐款 Advances to suppliers 其他应收款 Other receivables待摊费用 Deferred and prepaid expenses 存货 Inventories减:存货变现损失准备Less:Provision for loss on realization of inventories一年内到期的长期投资 Long-term investments maturing within one year其他流动资产 Other current assets流动资产合计 Total current assets长期投资: LONG TERM INVESTMENTS 长期投资 Long-term investments一年以上的应收款项 Receivables collectable after one year固定资产: FIXED ASSETS:固定资产原价 Fixed assets-cost减:累计折旧 Less:Accumulated depreciationcost固定资产净值 Fixed assets-net value 固定资产清理 Disposal of fixed assets 在建工程: CONSTRUCTION IN PROGRESS 在建工程 Construction in progress 无形资产: INTANGIBLE ASSETS:场地使用权 Land occupancy righ工业产权及专有技术 Industary property rights and proprietary technology其它无形资产 Other intangible assets无形资产合计 Total intangibles assets:其它资产: OTHER ASSETS:开办费 Organization expenses筹建期间汇兑损失 Exchange loss during start-up period递延投资损失 Deferred loss on investm递延税款借项 Deferred taxes debi其它递延支出 Other deferred expense待转销汇兑损失 Unamortized cxehangs loss负债及所有者权益 LIABILITIES AND OWNER'S EQUITY 流动负债: CURRENT LIABILITIES:短期借款 Short-term loans应付票据 Notes payable应付账款 Accounts payable应付工资 Accrued payroll应交税金 Taxes payable应付股利 Dividends payable预收货款 Advances from customers其它应付款 Other payables预提费用 Accrued expense职工奖励及福利基金 Staff and worker's bonus and welfare fund一年内到期的长期负债 Long-term liabilities due within one year其他流动负债 Other current liabilities 流动负债合计 Total current liabilities 长期负债: LONG-TERM LIABILITIES:长期借款 Long-term loans应付公司债 Dividends payable应付公司债溢价(折价) Premium(discount)on debentures payable一年以上的应付款项 Payables due after one year长期负债合计Total long-term liabilities其他负债: OTHER LIABILITIES筹建期间汇兑收益 Exchange gain during start-up period递延投资收益Deferred gain on investments递延税款贷项 Deferred tax credits 其他递延贷项 Other deferred credits 待转销汇兑收益 Unamortized exchange gain 其他负债合计Total other liabilities负债合计 Total liabilities所有者权益: OWNER'S EQUITY资本总额 Registered capital (货币名称及金额currency and amount___)实收资本 Paid-in capital (非人民币资本期末金额amount of non-RMB currency at end of period___)其中:中方投资 Chinese investments(非人民币资本期末金额amount of non-RMB currency at end of period___)外方投资 Foreign investments(非人民币资本期末金额amount of non-RMB currency at end of period___)减:已归还投资 Less:Investments returned资本公积 Capital surplus储备基金 Reserve fund企业发展基金 Enterprise expansion fund利润归还投资Profit capitalised on return of investments本年利润 Current year net income未分配利润 Undistributed profit所有者权益总计 Total owner's equity负债及所有者权益总计 TOTAL LIABILITIES AND OWNER'S EQUITY。

会计专业英语

会计专业英语-CAL-FENGHAI.-(YICAI)-Company One1一、words and phrases1.残值 scrip value2.分期付款 installment3.concern 企业4.reversing entry 转回分录5.找零 change6.报销 turn over7.past due 过期8.inflation 通货膨胀9.on account 赊账10.miscellaneous expense 其他费用11.charge 收费12.汇票 draft13.权益 equity14.accrual basis 应计制15.retained earnings 留存收益16.trad-in 易新,以旧换新17.in transit 在途18.collection 托收款项19.资产 asset20.proceeds 现值21.报销 turn over22.dishonor 拒付23.utility expenses 水电费24.outlay 花费25.IOU 欠条26.Going-concern concept 持续经营27.运费 freight二、Multiple-choice question1.Which of the following does not describe accounting( C )A. Language of businessB. Useful ofr decision makingC. Is an end rathe than a means to an end.ed by business, government, nonprofit organizations, and individuals.2.An objective of financial reporting is to ( B )A. Assess the adequacy of internal control.B.Provide information useful for investor decisions.C.Evaluate management results compared with standards.D.Provide information on compliance with established procedures.3.Which of the following statements is(are) correct( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.A company may use different depreciation methods in its financial statements and its income tax return.C.The cost of a machine includes the cost of repairing damage to the machine during the installation process.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method.4. Which of the following is(are) correct about a company’s balance sheet( B )A.It displays sources and uses of cash for the period.B.It is an expansion of the basic accounting equationC.It is not sometimes referred to as a statement of financial position.D.It is unnecessary if both an income statement and statement of cash flows are availabe.5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A )rmation used to determine which products to poducermation about economic resources, claims to those resources, and changes in both resources and claims.rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows.rmation that is useful in making ivestment and credit decisions.6.Each of the following measures strengthens internal control over cash receipts except. ( C )A.The use of a petty cash fund.B.Preparation of a daily listing of all checks received through the mail.C.The use of cash registers.D.The deposit of cash receipts in the bank on a daily basis.7.The primary purpose for using an inventory flow assumption is to. ( A )A.Offset against revenue an appropriate cost of goods sold.B.Parallel the physical flow of units of merchandise.C.Minimize income taxes.D.Maximize the reported amount of net income.8.In general terms, financial assets appear in the balance sheet at. ( B )A.Current valueB.Face valueC.CostD.Estimated future sales value.9.If the going-concem assumption is no longer valid for a company except. ( C )nd held as an ivestment would be valued at its liquidation value.B.All prepaid assets would be completely written off immediately.C.Total contributed capital and retained earnings would remain unchanged.D.The allowance for uncollectible accounts would be eliminated.10.Which of the following explains the debit and credit rules relating to the recording of revenue and expenses( C )A.Expenses appear on the left side of the balance sheet and are recorded by debits;revenue appears on the right side of the balance sheet and is reoorded by credits.B. Expenses appear on the left side of the income statement and are recorded by debits; Revenue appears on the right side of the income statement and is recorded by credits.C.The effects of revenue and expenses on owners’ equity.D.The realization principle and the matching principle.11.Which of the following statements is(are) correct( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.The cost of a machine do not includes the cost of repairing damage to the machine during the installation prcess.C.A company may use same depreciation methods in its finacial statements and its income tax return.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the straight-line method.12.A set of financial statements ( B ) except.A.Is intended to assist users in evaluating the financial position, profitability, and future prospects of an entity.B.Is intended to assist the Intemal Revenue Service in detemining the amount of income taxes owed by a business organization.C.Includes notes disclosing information necessary for the proper interpretation of the statements.D.Is intended to assist investors and creditors in making decisions inventory the allocation of economic resources.13.The primary purpose for using an inventory flow assumption is to. ( B )A.Parallel the physical flow of units of merchandise.B.Offset against revenue an appropriate cost of goods soldC.Minimize income taxes.D.Maximize the reported amount of net income.14.Indicate all correct answers. In the accounting cycle. ( D )A.Transactions are posted before they are journalized.B.A trial balance is prepared after journal entries haven’t been posted.C.The Retained Earnings account is not shown as an up-to-date figure in the trial balance.D.Joumal entries are posted to appropriate ledger accounts.15.According to text, Objectives of Financial Reporting by Business Enterprises. ( D )A.Extemal users have the ability to prescribe information they want.rmation is always based on exact measures.C.Financial reporting is usually based on industries or the economy as a whole.D.Financial accounting does not directly measure the value of a business enterprise.16.Indicate all correct answers. Dividends except ( A )A.Decrease owners’ equity.B.Decrease net incomeC.Are recorded by debiting the Cash accountD.Are a business expense17.Which of the following practices contributes to efficient cash management ( C )A.Never borrow money-maintain a cash balance sufficient to make all necessary payments.B.Record all cash receipts and cash payments at the end of the month when reconciling the bank statements.C.Prepare monthly forecasts of planned cash receipts, payments, and anticipated cash balances up to a year in advance.D.Pay each bill as soon as the invoice arrives.18.Which of the following would you expect to find in a correctly prepared income statement ( A )A.Revenues earned during the period.B.Cash balance at the end of the period.C.Contributions by the owner during the period.D.Expenses incurred during the next period to earn revenues.19.Which of the following are important factors in ensuring the integrity of accounting information ( D )A.Institutional factors, such as standards for preparing information.B.Professional organizations, such as the American Institute of CPAs.petence’ judgment’ and ethical behavior of individual accountants’D.All of the above.三、Practices11.On Jan.1, 2000, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $40,000 for 2000, calculated under the sum-of –the-years’–digits method. Required: Determine the acquisition cost of the equipment. ( C )A.$210,000B.$250,000C.$225.000D.$200,0002. On Jan.2, 2002, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $24,000 for 2004, calculated under the sum-of –the-years’–digits method (4%). Required: Determine the acquisition cost of the equipment. ( C )A.$220,000B.$250,000C.$224.000D.$200,0003. October 1, 2005, Coast Financial Ioaned Bart Corporation $3000,000, receiving in exchange a nine-month, 12 percent note receivable. Coast ends its fiscal year on December 31 and makes adjusting entries to accrue interest earned on all notes receivable. The interest earned on the note receivable from Bart Corporation during 2006 will amount to. ( A )A.$9,000B.$18,000C.$27.000D.$36,000Question: What is the reconciled balance ( B )A.$4,187B.$4,085C.$4,090D.$4,000Required: Choose the reconciled balance. ( D )A.$3,220B.$3,250C.$3,200D.$3,225Required:Calculate the cost of goods available for sale(C)A.$475,000B.$474,000C.$470,000D.$473,000Required: Calculate the cost of goods sold ( D )A.$225,000B.$254,000C.$250,000D.$253,0008.At the end of the current year, the accounts receivable account has a debit balance of $60,000 and net sales for the year total $100,000. The allowance account before adjunstment has adebit balance of a $500, and uncollectible accounts expense is estimated at 1% of net sales. Question: The entry for the above bad debts is ( A )A.Dr. Bad Debt Accts. $1,500B.Dr. Bad Debt Accts. $500Cr. Allowance Doubtful Accts. $1,500 Cr. Allowance Doubtful Accts. $500C. Dr. Bad Debt Accts. $1,000D. Dr. Bad Debt Accts. $1,500Cr. Accts Rec. $1,000 Cr. Accts Rec. $1,5009.The balance sheet items to The Oven Bakery(arranged in alphabetical order)were as follows at August 1,2005.(You are to compute the missing figure for retained earnings.)(4%)REQUIRED:Find Retained earnings at August 1 2005(D)A.$420,000B.$44,000C.$40,000D.$48,000Practices2Sue began a public accounting practice and completed these transactions during first month of the current year.Required: Choose the entries to record the following transactons.1.Invested $50,000 cash in a public accounting practice begun this day. ( A )A.Dr. Cash $50,000B.Dr. Capital Stock $50,000Cr. Capital Stock $50,000 Cr. Cash $50,0002.Paid cash for three monts’ office rent in advance $900(B)A.Dr. Rent Exp. $900B.Dr. Prepaid Rent $900Cr. Cash $900 Cr. Cash $9003.Paid the premium on two insurance policies, $300. ( )A.Dr. Prepaid Insurance $300B.Dr. Insurance Exp $300Cr. Cash $300 Cr. Cash $300pleted accounting work for Sun Bank on credit $1000. ( A )A.Dr. Accts Rec $1000B.Dr. Cash $1000Cr.Accounting Revenue $1000 Cr.Accounting Revenue $10005.Paid the monthly utility bills of the accounting office $300 ( A )A.Dr Utility Exp $300B.Dr office Exp $300Cr. Cash $300 Cr. Cash $300Linda began a public accounting practice and completed these transactons during first month of the current year.Required: Choose the entries to record the following transactons.6.Invested $20,000 cash in a public accounting practice begun this day. ( A )A.Dr Cash $20,00B.Dr Capital Stock $20,000Cr. Capital Stock $20,000 Cr. Cash $20,007.Paid cash for three months’ office rent in advance $1200.( B )A.Dr. Rent Exp $1200B.Dr. Prepaid Rent $1200Cr. Cash $1200 Cr. Cash $12008.Purchased offfice supplies $100 and office equipment $2,000 on credit. ( B )A.Dr. Office Equipment $2,000B.Dr.Office Equipment $2,000Office Supplies $100 Office Supplies $100Cr. Accts Rec. $2,100 Cr.Accts Pay. $2,100pleted accounting work for Jack Hall and collected $2000 cash therefore. ( B )A.Dr. Accts Rec $2000B.Dr. Cash $2000Cr.Accounting Revenue $2000 Cr.Accounting Revenue $200010.Purchase additional office equipment on credit $2500.( A )A.Dr.Office equipment $2500B.Dr. Office equipment $2500Cr.Accts Pay $2500 Cr.Accts Rec $2500四、Translation:1)The mechanics of double-entry accounting are such that every transaction is recorded in the debit side of one or more accounts and in the credit side of one or more accounts with equal debits and credits. Such form of combination is called accounting entry. Where there are only two accounts affected. 2)the debit and credit amounts are equal. If more than two accounts are affceted, the total of the debit entries must equal the total of the credit entries. The double-entry accounting is used by virtually every business organization, regardless of whether the company’s accounting records are maintained manually or by computer.1.The mechanics of double-entry accounting.( B )A.会计两次记账的制度B.复式记账机制C.会计的重复记账体制2.the debit and credit amounts are equal. ( A )A.借方金额与贷方金额是相等的B.借出金额与贷款金额是相等的C.借入金额与贷款金额是相等的Most accounting methods are based on the assumption that the business enterprise will have a long life. Experience indicates that.1)inspite of numerous business failures, companies have a fairly highcontinuance rate. Accountants do not believe that business firms will last indefinitely, but they do expect them to last long enouthto 2)fulfill their objectives and commitments.3.in spite of numerous business failures, companies have a fairly high continuance rate. ( B )A.可惜有许多企业失败,但公司仍有较高的持续经营比率。

会计的英文是什么

会计的英文是什么会计是以货币为主要计量单位,以提高经济效益为主要目标,运用专门方法对企业,机关,事业单位和其他组织的经济活动进行全面,综合,连续,系统地核算和监督,提供会计信息。

那么你知道会计的英文是什么吗?一起来学习一下吧!会计的英文说法1:accounting会计的英文说法2:accountancy会计的英文说法3:accountant会计的英文例句:1. The accounting firm deliberately destroyed documents to thwart government investigators.会计事务所故意毁坏文件,阻挠政府调查工作。

2. How do accounting records operate?账目是如何记录的?3. The debate revolves around specific accounting techniques.这场争论的焦点是具体的会计技术。

4. a career in accounting会计职业5. There was no love lost between the sales and the accounting departments.销售部门与财务部门之间关系很坏.6. A company's accounting records must be open for inspection at all times.公司的会计账目必须随时可以公开以备检查.7. A job fell vacant in the accounting department.财会部出现了一个空缺.8. We offer accounting as a subsidiary course.我们开设会计课,作为副修课程.9. Accounting principles are also referred to as standards.会计原则也可称作会计标准.10. There is no accounting for tastes.趣味是说不明白的.11. There's an accounting error in this entry.这笔账目里有差错.12. August registrations have gone ballistic, accounting now for a quarter of the annual total.8月份的注册人数突然暴涨,现在已经达到了年注册量的四分之一。

会计专业英语

accounting会计 financial position财务状况 stockholder股东investor 投资者 creditor 债务人 financial strength财务实力financial report财务报告 accounting process会计过程financial accounting财务会计 managerial accounting管理会计auditing 审计cost accounting 成本会计 tax returns纳税申报单Financial statement财务报表 balance sheet资产负债表Income statement 收益表 statement of cash flow现金流量表Liabilities 负债 asset 资产 owners’ equity 所以者权益Accounting equation 会计等式 current asset 流动资产Long-term asset 长期资产 cash 现金 liquidity 变现能力Accounts receivable 应收账款 fixed assets 固定资产Depreciable asset 应折旧资产 original cost 原始成本Accumulated depreciation 累计折旧 intangible asset 无形资产Goodwill 商誉 Notes payable 应付票据 current liability流动负债Accounts payable应付账款 bonds payable 应付债券 partnership 合伙Sole proprietorship 独资 corporation股份有限公司 capital stock股本Retained earnings留存收益 undistributed earnings 未分配收益Board of directors 董事会 dividend payable 应付股利 revenue 收入Expense 费用 Cost of goods sold销货成本 operating result 经营成本Operating Expense营业费用 sales returns and allowances 销货退回及折让Sales discounts 销货折扣 gross sales 销售总额 net sales 销售净额Beginning inventory期初存货 net purchase购货净额Ending inventory期末存货 purchase discounts购货折让purchase returns and allowances购货退还及折让transportation in购货运费 transportation out 销货运费cost of goods available for sale 可供销售的商品成本gross profit on sales 销售毛利 selling expense销售费用advertising expense 广告费用 administration expense 管理费用depreciation expense 折旧费 ledger 分类账 account 账户double-entry bookkeeping system 复式记账法source document 原始凭证 check stub 支票存根 journal 日记账post 过账 chart of accounts 账户一览表 subsidiary ledger明细分类账perpetual inventory system 永续盘存制uncollectible accounts expense 坏账费用loss from uncollectible accounts坏账损失loss from doubtful accounts 呆账损失bad debts expense 坏账费用 direct write-off method 直接销账法allowance method 备抵法allowance for uncollectible accounts备抵坏账specific identification 具体辨认weighted average 加权平均 first-in,first-out 先进先出last-in,first-out 后进先出 periodic inventory system 定期盘存制depletion折耗 amortization 摊销 equivalent 等同straight-line method 直线折旧法sum-of-the-year’s digits method 年数总和法double-declining-balance method 双倍递减法accelerated depreciation method 加速折旧法authorized stock 额定股本 issued stock 已发股本treasury stock 库存股本 outstanding stock 外发股本common stock 普通股 preferred stock优先股stock-option 股票期权 cash dividend 现金股利stock dividend 股票股利job order cost accounting分批成本会计process cost accounting 分步成本会计cost center 成本中心 conversion cost加工成本equivalent units 约当产量。

会计英语 Accounting English

会计英语 Accounting English2011年07月28日 13:24一:ACCOUNTING ENTIY㈠资产(Asset)1.应收账款:Accounts receivable会计操作:收到应收账款 Dr:Cash Cr:Accounts receivable外欠帐款收到:Dr:Accounts receivable Cr:Unearn receivable ;2.现金:Cash 会计操作:收到现金:Dr:Cash Cr:Accounts receivable 支付现金:Dr:Furniture Cr:Cash Dr:Accounts Payable Cr:Cash3.广告:Advertisement 会计操作:计提广告费用:Dr:Advertisement Expent Cr:Advertisement4.折旧:Depreciation 会计处理:计提折旧: Dr:Depreciation Expent Cr:Accumulated Depreciation5. 存货:Inventory6.应收票据:Note receivable 会计处理:Dr:Cash Cr:Note receivable7.办公用品:Office supplies 会计处理:购买办公用品: Dr:Officesupplies Cr:Cash8.预付租金:Prepaid rent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent9.家具:Furniture 会计处理:购买家具: Dr:Fueniture Cr:Cash10.土地:Land 会计处理:出售土地: Dr:Cash Cr:Land11.预付租金:Prepaid rent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent㈡负债(liability)1.应付账款:Accounts Payable 会计处理:支付账款:Dr:AccountsPayable Cr:Cash2.累计折旧:Accumulated Depreciation 会计处理:计提折旧:Dr:Depreciation Expent Cr:Accumulated Depreciation3.应付工资:Salary payable 会计处理:计提工资费用:Dr:Salary Expent Cr:Salary payable 支付工资:Dr:Salary Payable Cr:Cash㈢所有者权益(Owner's equity)1.Withdrawal (撤资) 会计处理:期末过度到本年利润2.投资:Investment 会计处理:投资:Dr:Investment Cr:Cash3.资本:Captial 会计处理:期初+本期过度的资本=期末资本余额㈣收入(Revenue)1. 服务收入:Service revenue 会计处理:计提服务收入:Dr:Accountsreceivable Cr:Service renenue收到:Dr:Cash Cr:Accounts receivable Dr:Unearned Servicerenenue Cr:Service renenue2.保险收入:Commission revenue 会计处理:计提:Dr:Unearned commission revenue Cr:Commission revenue3.销售收入:Sales revenue 会计处理:现金收到:Dr:Cash Cr:Sales revenue销售收入赊账处理:Dr:Accounts receivable Cr:Sales revenue㈤费用(Expent)1.公用事业费用:Utilities Expent2.租金费用:Rent Expent 会计处理:计提:Dr:Rent Expent Cr:Prepaid rent3.工资费用:Salary Expent 会计处理:计提工资费用:Dr:Salary Expent Cr:Salary payable4.办公费用:Supplies Expend 会计处理:计提:Dr:Supplies Expent Cr:Supplies5.折旧费用:Depreciation Expent 会计处理:计提折旧: Dr:Depreciation Expent Cr:Accumulated Depreciation㈥过户:Dr:Income Summary Cr:费用类科目Dr:收入类科目 Cr:Income SummaryDr:Withdrawal Cr:Income SummaryDr:Income Summary Cr:Captial二:THE ACCOUNTING CYCLEA→→→→→→→→→↓↓Transaction source document→Joural→Ledger→Worksheet→Finacial statementsB→→→Closing→→→→↓↓Analyzing→Recording→Posting→Adjusting→Preparing三:存货(Inventory)---会计处理1.购买存货:Dr:Purchase Cr:Cash OR Accounts Payable2.购货折扣与退回折让:Dr:Accounts Payable Cr:CashPurchase DiscountsPurchase returns and allowances3.Purchase(Dr) ---Purchase Discounts(Cr)---Purchase returnsand allowances(Cr) =Net purchase(Dr)4.运输成本:Dr:Freight In Cr :Cash5.销售折扣与销售折让、退回:Dr:Sales DiscountSales Returnsand allowancesCr:Accounts receivable6.Sales revenue (Cr) ---Sales Discount (Dr)--- Sales Returnsand allowances(Dr)=Net Sales (Cr)7.Beginning inventory(Dr)+Net purchase(Dr)+Freight In =Cost of inventory ---Ending inventory=Cost of goods sold。

会计英语

一、Translation(English to Chinese)(1'*8)Separate legal entity 独立法人主体Relevance 相关性Statement of comprehensive income 综合收益报表Reliability 可靠性Statement of financial position 财务状况报表Comparability 可比性Underlying assumption 基本假设Materiality 重要性Statement of changes in equity 权益变动表Prudence 稳健性Statement of cash flows 现金流量表Invoice 发票Historical cost 历史成本Understandability 可理解性Replacement cost 重置成本IASs 国际会计准则Net realizable value 可变现净值IFRSs 国际财务报告准则Economic value 经济价值Journal 账簿Accounting period 会计分期ledger 账户Accounting cycle 会计循环Posting 过账Accrual basis 权责发生制Liquidity 流动性Going Concern 持续经营Contra-assets 抵消资产Credit note 贷方通知单Inventory 存货Goods received note 收货单Depreciation 折旧Source document 原始凭证Goodwill 商誉Double-entry accounting 复式记账Patent 专利权Adjusting entry 调整分录Bond 债券Trial balance 试算平衡表Dividend 股利Prepaid expense 预付费用Reserve 公积金Unearned revenue 未赚得收入Fraud 舞弊Accrued expense 应计费用Net book value 账面净值Accrued revenue 应计收入Residual Value 残值Revenue-recognition principle 收入确认原则Accumulated depreciation 累计折旧Cash equivalent 现金等价物Intangible assets 无形资产Petty cash fund 备用金Trade mark 商标Bank statement 银行对账单Amortization 摊销Bank reconciliation 银行余额调节表Accounts payable 应付账款Deposit in transit 在途存款Current liability 流动负债Outstanding checks 未兑现支票Contingent liability 或有负债Non-sufficient funds checks 存款不足退票Product warranty 产品质量保证Irrecoverable debts 无法收回的账款Short-term loan 短期贷款Allowance method 备抵法Net profit 净利润Direct write-off method 直接冲销法Bad debt 坏账Trade securities 证券交易Warranty liability 质保负债Constructive obligation 推定责任Paid up share 已缴股本Raw material 原材料Owner’s equity 所有者权益Work in process 生产成本Shareholders’ equity 股东权益Authorised share capital 核定股本Share capital 股本Work-in-process inventory 在产品Maturity date 到期日Straight Line method 直线法Finished goods 完成品Reducing balance method 余额递减法Adjusting events 调整事项Statement of changes in equity 股东权益变动表Non-adjusting events 非调整事项Called up shares 认缴股本(催缴股本)Preference shares 优先股Retained earnings 留存收益Share premium 股本溢价Revaluation reserve 重估公积金General reserve 一般公积金Ordinary shares 普通股二、True or false (2'*8)1.The principle financial statements of a business are the statement of financial position (Balance sheet) and the statement of comprehensive income ( Income statement).2.The definition of "Going concern"The F.Ss are normally prepared on the assumption that an entity is a going concern and will continue in operation for the foreseeable future(at least the next 12 months). realizable value: at the expected selling price less any costs that need to be incurred before the item can be sold.4.Some errors will not be discovered by Trial BalanceComplete omission of a transaction, because neither a debit nor a credit is madeThe posting of a debit or credit to the correct side of the ledger, but to a wrong accountCompensating error(e.g. an error of $100 is exactly cancelled by another $100 error elsewhere)Errors of principle, such as cash from receivables being debited toaccounts receivables and credited to cash instead of the other way round5.A note is a writtenpromise to pay a specific amount at a specific future date.Interest Computation:principal of the note*annual interest rate*time expressed in years=interest6.The cost of inventory consists the following costs:Purchase priceCost of conversionOther costs incurred in bringing the inventories to their present location and condition7.Inventory should be valued at the lower of cost and net realizable value(NRV)8.Tangible non-current assets1)are held for use2)are expected to be used during more than one periodnd normally has unlimited useful life and is therefore not depreciated.10.Criteria--Development cost capitalised PIRATEProbable future economic benefitsIntention to complete and use/sell assetResources adequate and available to completeAbility to use/sell the assetTechnical feasibility of completing asset for use/saleExpenditure can be measured reliably11.Definition of LiabilitiesA present obligation of the entity arising from past events, the settlement of which is expected to result in outflow of economic benefits12.A provision is a liability of uncertain timing or amount Recognition:A provision should only be recognised whenAn entity has a present obligation (legal or constructive)as a result of a past eventA reliable estimate can be made of the amount of the obligation Unless all three conditions are met, no provision can be recognised 13.Dividends are charged directly to retained earnings as they are an appropriation of profits earned to date.They are not an expense of the income statementDr Retained earnings (SOFP)Cr Dividends payable (SOFP)三、Multi-Choice (2'*15)1.A business entity is owned and run by A, B and C. What type of business is this an example of?( b )A.Sole traderB.PartnershipC.Limited liability company2.XY Co bought a machine five years ago for $15,000. it is now worn out and needs replacing. An identical machine can be purchased for $20,000Historical cost is _$15,000_________Replacement cost is___$20,000_____3.XY Co’s machine from the example above can be restored to working order at a cost of $5,000. It can then be sold for $10,000. What is its net realisable value?NRV=___5,000__________________4.Suppose XY Co buy the new machine for $20,000. It is estimated that the new machine will generate profits of $4,000 per year for its useful life of 8 years. What is its economic value?Economic value=______32,000______5.Which of the following is an example of a liability?( d )A.InventoryB.ReceivablesC.Plant and machineryD.Loan6.Only items which have a monetary value can be included in accounts. Which of the following is a basis valuation?( a )A.Historical costB.Monetary measurementC.RealisationD.Business entity7.Making an allowance for receivables is an example of which concept?( d )A.AccrualsB.Going concernC.MaterialityD.Prudence8.An item of inventory was purchased for $10. however, due to a fall in demand, its selling price will be only $8. In addition further costs will be incurred prior to sale of $1. What is the net realisable value.( a )A.$7B.$8C.$10D.$119.How is closing inventory incorporated in the financial statements?(B)A Debit: income statementCredit: Statement of financial positionB Debit: Statement of financial positionCredit: income statement10.on 10 Dec 20x8 an entity bought a machine.The breakdown on the invoice showed:$Cost of machine 20,000Delivery costs 200One-year maintenance contract 90021,100further installation costs of $500 were also incurredAt what amount should the machine be capitalised in the entity's records?( b )A.$20,000B. $20,700C. $20,200D. $21,600SolutionCost capitalised should includePurchase price 20,000All directly attibutable costsDelivery cost 200Installation cost 50020,700The cost of the maintenance contract should be shown as an expense in the SOCI11.What is an asset’s net book value?( b )A.Its cost less annual depreciationB.Its cost less accumulated depreciationC.Its net realised valueD.Its replacement value12.A non current asset( cost $10,000, depreciation $7,500) is given in part exchange for a new asset costing $20,500. The agreed trade in value was $3,500. The income statement will include:( b )A.A loss on disposal $1,000B.A profit on disposal $1,000C.A loss on purchase of a new asset $3,500D.A profit on disposal $3,5013.What is the required accounting treatment for expenditure on research?( a )A.Write off as an expense in the period it is incurredB.Capitalise and carry forward as an asset14.Which of the following items is an intangible asset?( b )ndB.PatentC.BuildingD.Van15.Research expenditure is incurred in the application of knowledge for the production of new products.( b )A .True B.False16.XY Co has development expenditure of $500,000. its policy is to amortise development expenditure at 2% per annum. Accumulated amortisation brought forward is $20,000. What is the charge in the income statement for the year’s amortisation?( a )A.$10,000B.$400C.$20,000D.$9,60017.Given the facts above, what is the amount shown in the statement of financial position for development expenditure?( c )A.$500,000B.$480,000C.$470,000D.490,00018.A company is being sued for $10,000 by a customer. The company’s lawyers reckon that it is likely that the claim will be upheld. How should the company account for this?( a )A.ProvisionB.Contingent liability19.Given the fact above,how much of a provision should be made if further legal fees of $2,000 are likely to be incurred?( a )A.10,000B.$5,000C.$15,000D.$12,00020.A company issues 50,000 $1 shares at a price of $1.25 per share. How much should be posted to the share premium account?( b )A.$50,000B.$12,500C.62,500D.$60,00021.Which of the following items impact on the statement of changes in Equity?( d )⑴Issue of ordinary shares ⑵Revaluation of a building⑶Profit for the period ⑷Revaluation of a non-current asset investmentA.1)B.1) 2)C.2) 3)D.All of the above22.Which of the following events after the reporting period would normally qualify asa non-adjusting event?(b )①A fall in the market price of shares held by the entity as investments②Insolvency of a trade receivable with a balance of $200,000 outstanding at the end of the reporting period③Declaration of the year-end dividend by the directors④Confirmation of the amount of damages awarded to an employee who sued for unfair dismissal after being sacked two months before the year endA.② onlyB.① and ③C.①,③ and ④D.② and ④四、Calculation(8'*2\15'*1)(1)Two methods to account for uncollectible accounts 1.direct write-off methodeg.On January 23, TechCom determines it cannot collect $520 from Jack Kent, a credit customer.Dr : Bad debts expense 520Cr :Accounts receivable 520If Jack Kent later pays the $520, the previous entry is simply reversed and the cash collection is recorded.Dr :Accounts receivable 520Cr :Bad debts expense 520Dr :Cash 520Cr :Accounts receivable 5202.allowance methodrequires an estimate of the total irrecoverable debts expected to result from that period's saleswrite off bad debtsDr Bad debts expense (SOCI)Cr Trade receivables (SOFP)Make entries for specific allowancesDr Doubtfull debts expense (SOCI)Cr Allowance for receivables (SOFP)Total trade receivables 100Less: specific allowances (20)80General allowance@5% 4Total allowance:specific 20general 424(2)Interest Computationprincipal of the note*annual interest rate*time expressed in years=interest1.eg.Record the receipt of a $1,000, 12%, 90-day note in exchange for goods.July 10th Dr:notes receivable 1,000Cr :sales 1,000Interest Computation:1,000*12%*90/365=29.592.At the maturity date, the following journal entry is required:Oct 8th Dr :cash 1029.59Cr :notes receivable 1,000Interest revenue 29.593.End-of-Period AdjustmentsWhen a note receivable is outstanding at the end of an accounting period, the company must prepare an adjusting entry to accrue interest income.Dec 31st Dr :Interest receivable XXCr :Interest revenue XXThe accrued interest is equal to the number of days from the start of the note to the end of the year.Example - $3,000, 12% note dated December 16th. Due: June 16thDec 31st Dr :Interest receivable 14.79Cr :Interest revenue 14.79( $3,000 x 12% x 15/365)(4)A business’s trade receivables account showed a year end balance of $47,440. It was decided that amounts totalling $340 should be written off as irrecoverable, a specific allowance was to be made against an amount of $400 due from Dodgy Co, a customer, and a general allowance of 2% was to be made against remaining debts.Requireda)Calculate the allowance for receivables shown in the statementof financial position.b)Calculate the bad debt and doubtful debts expense shown in the income statement.Answer:36500(5)FIFO (先进先出法)Date Purchase Cost of goods sold Inventory blance Aug 1 10 @ $91 = $910 $ 910Aug 3 15 @ $106=$1,590 $ 2,500Aug 14 10 @ $91=$910$ 53010@ $106=$1060Aug 17 20 @ $115=$2,300 $ 2,830Aug 28 10 @ $119=$1,190 $ 4,020Aug 31 5@$106=$530$ 1,42018@$115=$2070Cost of goods sold for Aug 31=($530+$2,070)=$2,600Cost of goods sold Inventory balance$910$2,50010 @ $91=$910 $53010@ $106=$1060$2,830$4,020$1,4205@$106=$53018@$115=$2070Income statement COGS=$4570Balance sheet inventory=$1,420(6)weight average (加权平均法)Date Purchase Cost of goods sold Inventory blance Aug 1 10 @ $91 = $910 $ 910Aug 3 15 @ $106=$1,590 $ 2,500Aug 14 20@$100=$2000 $ 500Aug 17 20 @ $115=$2,300 $ 2,800Aug 28 10 @ $119=$1,190 $ 3990Aug 31 23@$114=$2622 $ 1,368 Purchase 8/1 10 cost of goods availablePurchase 8/3 15 for sale $3,990Sale 8/14 (20) total units in inventory 35 Purchase 8/17 10 weighted average costPurchase 8/28 20 per unit $114Units available for sale 35Cost of goods sold Inventory balance$910$2,50020 @ $100=$2000$500$2,800$3,99023@$114=$2,622$1,368Income statement COS =$4,622Balance sheet inventory=$1,368(7)On Jan 20x6, the Grand Union Food Stores had goods in inventory valued at $6,000. During 20x6 its proprietor purchased supplies costing $5,000. sales for the year to 31 Dec 20x6 amounted to $80,000. The cost of goods in inventory at 31 Dec 20x6 was $12,500.Sales 80,000 Opening inventories 6,000Add purchases 50,00056,000Less closing inventories (12,500)Cost of goods sold (43,500) Gross profit 36,500(8)Jessie is trying to value her inventory. she has the following informationavailable: $ Selling price 35 Cost incurred to date 20Cost of work to complete item 12 Selling costs per item 1 RequiredWhat is the net realisable value of Jessie's inventory?Answer:Net realisable value is: $Estimated selling price 35Less: costs of completion (12)Less: selling costs (1)22(9)Two methods of depreciation(1)Straight line methodThe depreciation charge is the same every yearDepreciation=(Cost-residual value)/useful life(years)or (cost-residual value)x%Residual value=expected proceeds/scrap value at the end of the assets's useful lifeUseful life=the number of years the business expects to make use of the assetEg.A business buys a machine for $2500. it is expected to have a useful life of three years after which time it will have a scrap value of $250.RequiredCalculate the annual depreciation charge.answer:Depreciation charge=(Cost-Residual value)/useful life=(2500-250)/3yrs=$750 per annumReducing balance depreciationeg.A business buys a machine costing $6000. The depreciation rate is 40% on a reducing balance basisRequiredCalculate depreciation expense, accumulated depreciation and net book value of the asset for the first three years.solutionyear NBVb/f Dep rate Dep exp Acc Dep NBV c/d 1 6000 40% 2400 2400 36002 3600 40% 1440 3840 21603 2160 40% 864 4704 1296 (10)Grass Co is reviewing its warranty obligations. Based on sales during 20x7 it has established that if all products sold required minor repairs this would cost $1m whereas if major repairs were required this would cost $6mGrass Co expects that 75% of products sold will have no faults, 20% will need minor repairs and 5% major repairs.required:What provision should be made in 20x7 and what accounting entry is needed to record it?Solution:A provision should be made using expected values$1m x 20%+$6m x 5%=$0.5mDr Warranty cost expense (I/S) 0.5mCr Provisions (SOFP) 0.5m(11)On 1 June 20x6 Rab Co. issued a further 200,000 ordinary shares of 50c each for 80c per share.Required:Show how this issue of shares would be accounted for and what the SOFP would look like immediately after the issue. Solution:Dr cash (200,000x80c) 160,000Cr Share capital (200,000x50c) 100,000Cr Share premium account (200,000x30c) 60,000Rab Co. statement of financial position (extract) as at 1June 20x6Equity $Share capital-50c ordinary shares (50,000+100,000) 150,000Share premium account 60,000210,000 (12)ABC Co has the following share capital:100,000 6% $1 preference shares200,000 50c ordinary sharesRetained earnings at the beginning of the year were $125,000 During the year ended 31 Dec 20x7 it made the following profit: Profit before tax 60,000Income tax expense (10,000)Profit for the period 50,000Dividends paid and declared during the year were as follows: Interim dividend paid 5c per shareFinal dividend declared on 20 January 20x8 10c per share Required Show the movement in retained earnings for ABC Co. for the year ended 31 Dec 20x7Solution $ $Retained earnings at beginning of year 125,000Profit for the period 50,000Dividends-Preference(6%x100,000) 6,000-Ordinary(5cx200,000) 10,000(16,000)Retained earnings at end of year 159,000五、Discussion(15'*1)(1)Development is the application of research findings or other knowledge to plan or design for the production of new or substantially improve materials, devices, products, process, systems or services prior to the commencement of commercial production or use.Components of research and development costs:Salaries, wages,Depreciation,Overhead costs, eg. Administration cost,Other cost, eg. amortisation,(2)DevelopmentFuture profits are expectedMust capitalise as an intangible non-current asset if all of the relevant criteria are satisfiedDr Intangible NCA (SOFP)Cr Bank/ payablesAmortise asset over its useful life once asset is ready for use.(3)Criteria--Development cost capitalisedPIRATEProbable future economic benefitsIntention to complete and use/sell assetResources adequate and available to completeAbility to use/sell the assetTechnical feasibility of completing asset for use/sale Expenditure can be measured reliably。

会计英语

Separate Entity Assumption(会计主体)Going Concern Assumption(持续经营)Time-period Assumption(会计分期)Monetary Unit Assumption(货币计量)2.Corporation does not adjust amounts in its financial statements for the effects of inflation. ——Monetary unit3.firm reports current and noncurrent classifications in its balance sheet ——Going Concern4.The economic activities of D corporation and its subsidiaries are merged for accounting and reporting purposes.——accounting Entity Cost principle历史成本原Matching Principle配比原则 Conservatism谨慎性原则Materiality重要性原则 capital and revenue expenditure资本性与权益性支出 Substance over form实质重于形式(a) Crimson Tide Corporation does not accrue a contingent lawsuit gain of $650,000.——Conservatism(b) Yahoo, Inc. recognizes depreciation expense for a machine over the 2-year period during which that machine helps the company earn revenue.——Matching(c) Sun Devil Corporation expenses the cost of wastebaskets in the year they are acquired.——Materiality(d) Eastman Kodak Company reports land on its balance sheet at the amount paid to acquire it, even though the estimated fair market value is greater.——Historical CostMateriality 重要性原则的四个小点1.A large bad-debt write-off would usually be a material event. —— large2. A very low inventory figure, but reflects the firm’s liquidity. ——Small but important3. A small bad-debt write-off is twice as large as normal. —— significantly different4. The sales figure. —— natureCost principle历史成本原则• This principle means that accounting information is based on actual cost(实际成本).• Cost is reliable, and information based on cost is considered objective.• The cost principle provides guidance primarily at the initial acquisition date(初始获得日). And it is the depreciation(折旧)base.•Measurement bases(计量基础)五个计量属性1. Historical cost历史成本2. Replacement cost 重置成本3. Net realizable value 可变现净值4. Current value现值5. Fair value公允价值Quality characteristics of accounting information(会计信息质量特征)Relevance (相关性) Reliability(可靠性) Understandability(可理解性)Comparability(可比性)Trade-off(权衡利弊)happens between relevance and reliability Accounting cycleAccounting equation 会计等式Double-entry 复式记账Accounting cycle 会计循环Journals 日记账Ledgers 分类账Adjusting procedures 调整程序Closing process 结账程序The trial balance 余额试算表Rules of The Double-Entry System复式记账1.Each transaction affects at least two accounts. (每项交易至少影响两个账户)2. Total debits must equal total credits.(借方总额等于贷方总额)Debits and Credits in the AccountsAssets(Dr+,Cr-) = liabilities(Dr-,Cr+) + equity(Dr-,Cr+)Revenues(Dr-,Cr+) - Expenses(Dr+,Cr-) = Net IncomeTwo words about journals (简答)1.Journalize 登记日记账The process of recording a transaction in a journal is called journalizing the transaction.2.post 过账Transferring the information from the journals to the ledger is called posting .and is usually done monthly.Advantages of using journals(使用日记账的优点)见书P48日记账与分类账的比较1-1.the debits and credits for a transaction are recorded together in journals.1-2.the debits and credits for a transaction are recorded in different accounts in ledger.So, we can see the complete story of a transaction in the journal.2. It is a record in a chronological order.So, if we want to look up the transaction several years ago, we only need the data of the transaction in the journal.3. a journal can help to prevent errors .such as: Omitting the debitor credit. Entering the debit or credit twiceDeferrals (递延)Deferred(prepaid) expenses (递延费用)mean items paid for in advance of receiving their benefits.Prepaid expenses are assets. When these assets are used, their costs become expenses.Examples include prepaid insurance, prepaid rent , supplies ,and depreciation.例:• 1.On April 1Dr. prepaid insurance 1200Cr. cash 1200• 2.At the end of AprilDr. insurance expense 100Cr. Prepaid insurance 100Unearned revenues(预收(递延)收入)• Unearned revenues are the liabilities account used to record cash received from customers in advance.• By the end of the accounting period, as products or services are provided ,it become earned revenues.例:• 1.On January 1Dr. cash 240 000Cr. Unearned consulting revenue 240 000• 2.At the end of JanuaryDr. Unearned consulting revenue 20 000Cr. Consulting revenue 20 000Accruals(应计)Accrued expenses (应计费用)— costs that are incurred in a period but are both unpaid and unrecorded.Such as : salaries , interest , rent, taxes例:1.At the end of AprilDr. salaries expense 1000Cr. Salaries payable 10002.On May 3Dr. salaries payable 1000salaries expense 1500Cr.cash 2500Accruals(应计)Accrued revenues (应计收入)— revenue that has been earned but not received.For example :a technician who bills customers only when the job is done .If one-third of a job is complete by the end of a period ,then the technician must record one-third of the billing as revenue in that period —even though there is no billing or collection.ExampleDr. accounts receivable 1800Cr. consulting revenue 1800Purpose of closing entries(结账程序的目的)To reset the revenue, expense, and dividends accounts (the temporary accounts) to a zero balance.The second purpose of closing entries is to move the balance of all revenue, expense, and dividends accounts to the retained earnings account, because they affect stockholders’ equity.An Example of Balance Sheet (account form)Assets Liabilities and Stockholder’s EquityCash $ 20,000 LiabilitiesAccounts receivable 2,000 Accounts payable $ 200 Supplies 500 Stockholder’s equityLand 11,000 Capital stock 20,000Total assets $ 33,500 Retained earnings 13,300Total liabilities andowner’s equity $33,500Retained Earnings留存收益借方:Net loss 贷方: Net incomeAdjustments for overstatement Adjustments for understatementDividendsDisposals of treasury stockReporting Cash Flows(现金流量表)The statement of cash flows reports cash flows by three types of activities:1. Cash flows from operating activities – transactions that affect netincome.现金流入①.Sales of goods and services ②.Interest revenue③.dividend revenue。

会计英语(第二版)第一章中英文互译

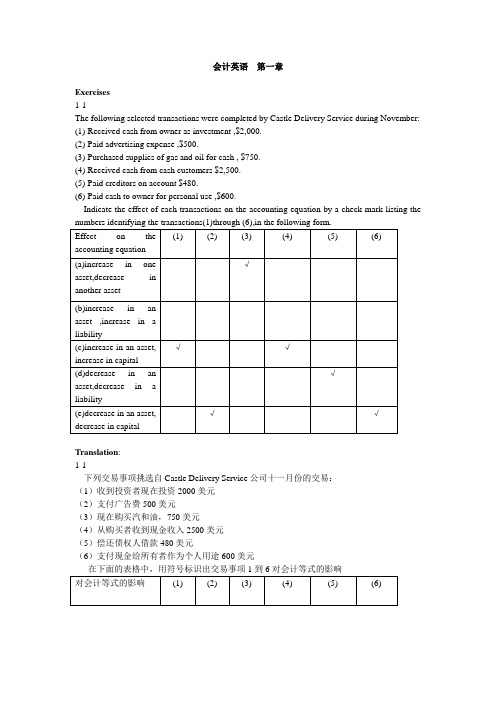

会计英语第一章Exercises1-1The following selected transactions were completed by Castle Delivery Service during November:(1)Received cash from owner as investment ,$2,000.(2)Paid advertising expense ,$500.(3)Purchased supplies of gas and oil for cash , $750.(4)Received cash from cash customers $2,500.(5)Paid creditors on account $480.(6)Paid cash to owner for personal use ,$600.Indicate the effect of each transactions on the accounting equation by a check mark listing theTranslation:1-1下列交易事项挑选自Castle Delivery Service公司十一月份的交易:(1)收到投资者现在投资2000美元(2)支付广告费500美元(3)现在购买汽和油,750美元(4)从购买者收到现金收入2500美元(5)偿还债权人借款480美元(6)支付现金给所有者作为个人用途600美元1-2Foreman Corporation, engaged in a service business , completed the following selected transactions during the period:1)Added additional investment, receiving cash2)Purchased supplies on account3)Returned defective supplies purchased on account and not yet paid for4)Received cash as a refund from the erroneous overpayment of an expense5)Charged customers for services sold on account6)Paid salary expense7)Paid a creditor on account8)Received cash on account from charge customer9)Paid cash for the owner’s personal use10)Determined the amount of supplies used during the monthTranslation :Foreman是一家从事服务行业的公司,以下是该公司在一段时间内的交易事项。

会计英语

Accounts Payable应付账款Accounts Receivable应收账款Accruals权责发生额Adjusting Entries调整分录Administrative Expenses行政开支Advertising Expenses广告费用Aging of Accounts Receivable应收账款到期时间表Assets资产Auditing审计Authorized Stock核准股本Average Cost Method平均成本法(库存)Bad Debts Expense坏账费用Balance Sheets资产平衡表Bank Accounts银行账户Bank Service Charge银行服务费用Bank Statements银行报表Bearer Bonds无记名债券Bond Certificates债券证书Bond Indenture债券契约Bonding, Employee雇员担保保险Bonds Payable应付债券Bonus奖金津贴Book Value账面价值Bookkeeping簿记Break-even Point盈亏平衡点Budget预算Buildings建筑物By-laws公司规章Calendar Year公历年Call Price赎回价格Callable Bonds可赎回债券Canceled Check被取消的支票Capital资本Capital Leases资本租赁Carrying Value库存账面价值Cash现金Cash-basis Accounting收付实现制Cash Equivalents现金等价物Cash Receipts现金收入Chart of Accounts会计科目表Charter for Corporations公司宪章Check Register支票登记簿Checks支票Closing Entries结账分录Collection 收款Common Stock普通股Compound Interest复利Consigned Goods寄售货物Consolidated Financial Statements合并财务报表Contingent Liabilities或有负债Contribution Margin边际收益贡献Controllers会计主任Controlling Interest控股权益Convertible Bonds可转换公司债券Copyrights版权Cost Accounting成本会计Cash Flow现金流量Collateral抵押品Cost of Capital资本成本Cost of Goods Sold销货成本Cost-volume-profit Analysis (CVP)成本数量利润分析Credit Cards信用卡Crediting贷记Creditors债权人Cross-footing交叉计算Cumulative Dividend累积股息Current Assets流动资产Current Liabilities短期负债Debenture Bonds信用债券(无抵押担保)Debiting借记Declaration Date宣布支付股息日Deferred Revenue递延收入Deficit赤字Depletion折耗Deposits in Transit在途存款Depreciation折旧Direct Labor直接人工成本Discount折扣Dividends股息Double-entry System复式计帐制Drawings提款Earnings盈利Effective-interest Method实际利息法Employees雇员Equipment设备Equity资本权益Expenses费用Face Value票面价值Factory Overhead工厂管理费用Fair Value公允价值Federal Unemployment Taxes联邦失业保障税FICA (Federal Insurance Contribution Acts)Taxes美国联邦保险税Financial Accounting Standards Board (FASB)财务会计准则委员会Financial Statements财务报表Financing Activities筹资行为Finished Goods制成品First-in, First-out Method (FIFO)先进先出法(存货)Fiscal Year财政年度Fixed Assets固定资产Footing合计Fraud欺诈行为Freight Costs运费Fringe Benefits附带福利Gains收益General Journal普通日记账General Ledgers总账Generally Accepted Accounting Principles (GAAP)通用会计准则Going Concern 持续经营企业Goodwill商誉Gross Profit毛利Income Statements收益表Income Taxes所得税Intangible Assets无形资产Interest利息Internal Control内部控制Internal Rate of Return内部收益率Inventory存货Investment投资Journals流水账Labor劳工Last-in, First-out Method (LIFO)后进先出法(存货)Liabilities负债Licenses执照Limited Liability Companies有限责任公司Limited Partners有限责任合伙人Liquidation清盘Liquidity Ratios流动资金比率Long-term Liabilities长期负债Losses on Investments投资亏损Lower of Cost or Market (LCM)取成本或市场价较低者Management管理层Manufacturing Operations制造业务Market Value市场价格Marketing市场营销Matching Principle收支对应原则Maturity Date到期日Medicare美国医疗保障制度Merchandise Inventory商品库存Mortgage抵押贷款Mutual Funds互助基金NASDAQ (National Association of Security Dealers ‘Automation Quotations)纳斯达克(全国证券交易商协会自动报价系统)Net Income净收入Net Loss净亏损Net Present Value净现值New York Stock Exchange (NYSE)纽约证券交易所Not-for-profit Organizations非盈利组织Notes Payable应付票据Notes Receivable应收票据NSF Check存款不足支票Obsolescence陈废Operating Activities经营活动Operating Expenses营业支出Operating Leases经营性租赁Opportunity Cost机会成本Outstanding Checks未付款的支票Overhead经常性管理开支Owner's Capital业主资本Paid-in Capital实收资本Parent Company母公司Partnerships合伙企业Patents专利权Payee收款人Payroll工资名单Pension Funds退休金基金Percentage-of-completion Method完工百分率法Periodic Inventory Systems定期盘存制度Permanent Accounts永久性账户Perpetual Inventory Systems永续盘存制度Petty Cash零用金Plant Assets工厂资产Posting记账Preferred Stock优先股Premium: on Bonds债券溢价Prepaid Expenses预付费用Price-Earnings (P-E) Ratio市盈率Process Cost Systems分步成本制度Profit Margin利润率Promissory Notes本票Property, Plant, and Equipment (PPE)物业,工厂及设备Proprietorships独资经营Ratio Analysis比率分析Raw Materials原材料Real Estate房地产Record Date股票所有人登记日期Redemption Price回购价格Research and Development (R&D) Costs研发费用Residual Value剩余价值Retailers零售商Retained Earnings留成收益Return on Investment (ROI)投资回报率Revenues收入Salaries薪水Sales销售额Sales Tax销售税Salvage Value残值Securities证券Selling Expenses销售费用Serial Bonds分期偿还债券Shareholder's Equity股东权益Short-term Investments短期投资Sinking Funds偿债基金Social Security Taxes社会保障税State Unemployment Taxes州失业保障税Stock Certificates股票凭证Stock Splits股票分股Straight-line Amortization Method直线摊销法Subsidiary Company子公司Sunk Cost沉没成本Suppliers供应商Supply Chain供应链Temporary Accounts暂记账户Term Bonds定期债券Time Value of Money货币时间价值Trademarks商标Transactions交易Treasurer财务主管Treasury Stock库存股份Trial Balance试算表Trustee受托管理人Unearned Revenue预收收入Unit Production Costs单位生产成本Unlimited Liability无限责任Useful Life of Assets资产使用寿命Variable Costs可变成本Vouchers凭单Wages Payable应付工资Weighted-average Method加权平均法Wholesalers批发商Work in Process在制品Work Sheet工作单Working Capital周转资金。

会计英语中英文对照