会计英语(第三版)

会计英语Chapter 3 The Accounting Cycle

会计英语

出版社 经管分社

The ledger is an accounting record that includes all the ledger accounts—that is, a separate account for each item included in the company’s financial statements.

1

会计英语

出版社 经管分社

8.Prepare adjusted trial balance. 9.State the rules of debit and credit for balance sheet accounts. 10.Explain the double-entry system of accounting. 11.Prepare financial statements. 12.Explain the purposes of closing entries; prepare these entries. 13.Prepare post-closing trial balance.

会计英语

出版社 经管分社

Chapter 3 The Accounting Cycle

1.Explain what accounting cycle is. 2.Describe the steps in the accounting cycle. 3.Describe a ledger account and a ledger. 4.Post journal entries to ledgers. 5.Explain the purpose of a journal and its relationship to the ledger. 6.Prepare a trial balance. 7.Make adjusting entries and explain the nature of adjusting entries.

会计英语课后习题参考答案

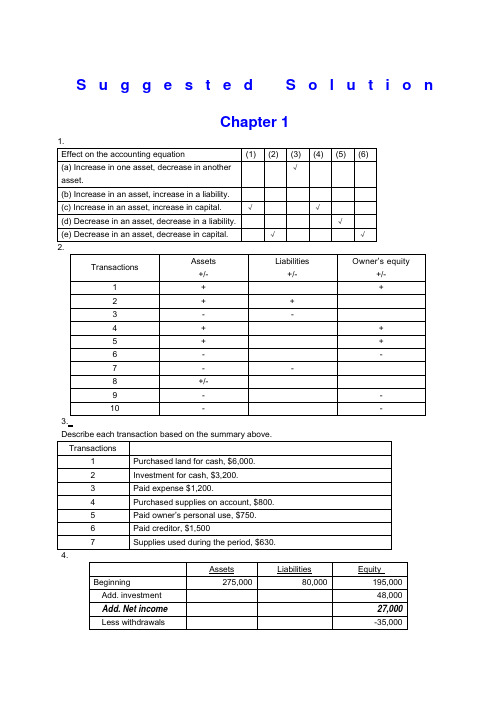

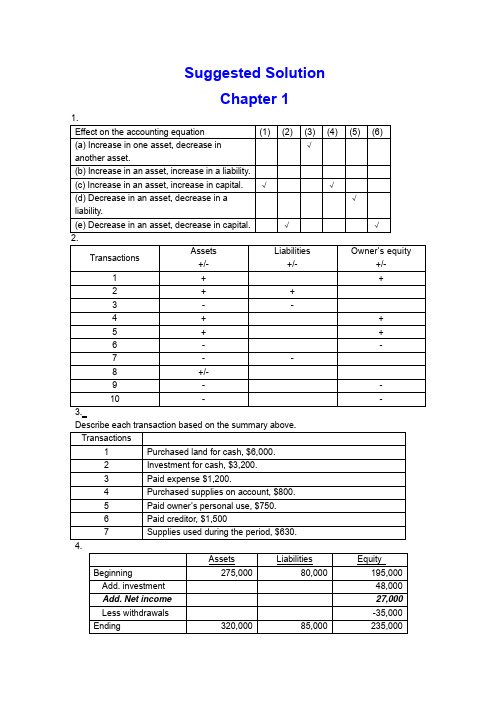

S u g g e s t e d S o l u t i o nChapter 12.3.4.5.(b) net income = 9,260-7,470=1,790(c) net income = 1,790+2,500=4,290Chapter 21.a.To increase Notes Payable -CRb.To decrease Accounts Receivable-CRc.To increase Owner, Capital -CRd.To decrease Unearned Fees -DRe.To decrease Prepaid Insurance -CRf.To decrease Cash - CRg.To increase Utilities Expense -DRh.To increase Fees Earned -CRi.To increase Store Equipment -DRj.To increase Owner, Withdrawal -DR2.Cash 1,800Accounts payable ...................................................... 1,800 Revenue ...................................................................... 4,500Accounts receivable .......................................... 4,500 Owner’s withdrawals .................................................... 1,500Salaries Expense ................................................ 1,500 Accounts Receivable (750)Revenue (750)3.Prepare adjusting journal entries at December 31, the end of the year.Advertising expense 600Prepaid advertising 600Insurance expense (2160/12*2) 360Prepaid insurance 360Unearned revenue 2,100Service revenue 2,100Consultant expense 900Prepaid consultant 900Unearned revenue 3,000Service revenue 3,000 4.1. $388,4002. $22,5203. $366,6004. $21,8005.1. net loss for the year ended June 30, 2002: $60,0002. DR Jon Nissen, Capital 60,000CR income summary 60,0003. post-closing balance in Jon Nissen, Capital at June 30, 2002: $54,000Chapter 31. Dundee Realty bank reconciliationOctober 31, 2009Reconciled balance $6,220 Reconciled balance $6,2202. April 7 Dr: Notes receivable—A company 5400Cr: Accounts receivable—A company 540012 Dr: Cash 5394.5Interest expense 5.5Cr: Notes receivable 5400June 6 Dr: Accounts receivable—A company 5533Cr: Cash 553318 Dr: Cash 5560.7Cr: Accounts receivable—A company 5533Interest revenue 27.73. (a) As a whole: the ending inventory=685(b) applied separately to each product: the ending inventory=6254. The cost of goods available for sale=ending inventory + the cost ofgoods=80,000+200,000*500%=80,000+1,000,000=1,080,0005.(1) 24,000+60,000-90,000*0.8=12000(2) (60,000+24,000)/( 85,000+31,000)*( 85,000+31,000-90,000)=18828Chapter 41. (a) second-year depreciation = (114,000 – 5,700) / 5 = 21,660;(b) second-year depreciation = 8,600 * (114,000 – 5,700) / 36,100 = 25,800;(c) first-year depreciation = 114,000 * 40% = 45,600second-year depreciation = (114,000 – 45,600) * 40% = 27,360;(d) second-year depreciation = (114,000 – 5,700) * 4/15 = 28,880.2. (a) weighted-average accumulated expenditures (2008) = 75,000 * 12/12 + 84,000 * 9/12 + 180,000 * 8/12 + 300,000 * 7/12 + 100,000 * 6/12 = 483,000(b) interest capitalized during 2008 = 60,000 * 12% + ( 483,000 – 60,000) * 10% =49,5003. (1) depreciation expense = 30,000(2) book value = 600,000 – 30,000 * 2=540,000(3) depreciation expense = ( 600,000 – 30,000 * 8)/16 =22,500(4) book value = 600,000 – 30,000 * 8 – 22,500 = 337,5004. Situation 1:Jan 1st, 2008 Investment in M 260,000Cash 260,000June 30 Cash 6000Dividend revenue 6000Situation 2:January 1, 2008 Investment in S 81,000Cash 81,000June 15 Cash 10,800Investment in S 10,800December 31 Investment in S 25,500Investment Revenue 25,5005. a. December 31, 2008 Investment in K 1,200,000Cash 1,200,000June 30, 2009 Dividend Receivable 42,500Dividend Revenue 42,500December 31, 2009 Cash 42,500Dividend Receivable 42,500b. December 31, 2008 Investment in K 1,200,000Cash 1,200,000December 31, 2009 Cash 42,500Investment in K 42,500Investment in K 146,000Investment revenue 146,000c. In a, the investment amount is 1,200,000net income reposed is 42,500In b, the investment amount is 1,303,500Net income reposed is 146,000Chapter 51.a. June 1: Dr: Inventory 198,000Cr: Accounts Payable 198,000 June 11: Dr: Accounts Payable 198,000Cr: Notes Payable 198,000 June 12: Dr: Cash 300,000Cr: Notes Payable 300,000b. Dr: Interest Expenses (for notes on June 11) 12,100Cr: Interest Payable 12,100Dr: Interest Expenses (for notes on June 12) 8,175Cr: Interest Payable 8,175c. Balance sheet presentation:Notes Payable 498,000 Accrued Interest on Notes Payable 20,275d. For Green:Dr: Notes Payable 198,000 Interest Payable 12,100Interest Expense 7,700Cr: Cash 217,800For Western:Dr: Notes Payable 300,000Interest Payable 8,175Interest Expense 18,825Cr: Cash 327,0002.(1) 20?8 Deferred income tax is a liability 2,400Income tax payable 21,600 20?9 Deferred income tax is an asset 600Income tax payable 26,100(2) 20?8: Dr: Tax expense 24,000Cr: Income tax payable 21,600 Deferred income tax 2,400 20?9: Dr: Tax expense 25,500Deferred income tax 600Cr: Income tax payable 26,100 (3) 20?8: Income statement: tax expense 24,000Balance sheet: income tax payable 21,600 20?9: Income statement: tax expense 25,500 Balance sheet: income tax payable 26,1003.a. 1,560,00012 %* (1-35%))12 %5.Notes Payable 14,400Interest Payable 1,296Accounts Payable 60,000+Unearned Rent Revenue 7,200Current Liabilities 82,896Chapter 61. Mar. 1Cash 1,200,000Common Stock 1,000,000Paid-in Capital in Excess of Par Value 200,000Mar. 15Organization Expense 50,000Common Stock 50,000Mar. 23Patent 120,000Common Stock 100,000Paid-in Capital in Excess of Par Value 20,000The value of the patent is not easily determinable, so use the issue price of $12 per share on March 1 which is the issuing price of common stock.2. July.1Treasury Stock 180,000Cash 180,000The cost of treasury purchased is 180,000/30,000=60 per share.Nov. 1Cash 70,000Treasury Stock 60,000Paid-in Capital from Treasury Stock 10,000Sell the treasury at the cost of $60 per share, and selling price is $70 per share. The treasury stock is sold above the cost.Dec. 20Cash 75,000Paid-in Capital from Treasury Stock 15,000Treasury Stock 90,000The cost of treasury is $60 per share while the selling price is $50 which is lower than the cost.3. a. July 1Retained Earnings 24,000Dividends Payable—Preferred Stock 24,000b.Sept.1Dividends Payable—Preferred Stock 24,000Cash 24,000c. Dec.1Retained Earnings 80,000Dividends Payable—Common Stock 80,000d. Dec.31Income Summary 350,000Retained Earnings 350,0004.a. Preferred stock gives its owner certain advantages over common stockholders. These benefits include the right to receive dividends before the common stockholders and the right to receive assets before the common stockholders if the corporation liquidates. Corporation pay a fixed amount of dividends on preferred stock.The 7% cumulative term indicates that the investors earn 7% fixed dividends.b. 7%*120%*20,000=504,000c. If corporation issued debt, it has obligation to repay principald. The date of declaration decrease the stockholders’ equity; the date of record and the date of payment have no effect on stockholders.5.a. Jan. 15Retained Earnings 35,000Accumulated Depreciation 35,000To correct error in prior year’s depreciation.b. Mar. 20Loss from Earthquake 70,000Building 70,000c. Mar. 31Retained Earnings 12,500Dividends Payable 12,500d. Apirl.15Dividends Payable 12,500Cash 12,500e. June 30Retained Earnings 37,500Common Stock 25,000Additional Paid-in Capital 12,500To record issuance of 10% stock dividend: 10%*25,000=2,500 shares;2500*$15=$37,500f. Dec. 31Depreciation Expense 14,000Accumulated Depreciation 14,000Original depreciation: $40,000/40=$10,000 per year. Book value on Jan.1, 2009 is$350,000(=$400,000-5*$10,000). Deprecation for 2009 is $14,000(=$350,000/25).g. The company does not need to make entry in the accounting records. But the amount of Common Stock ($10 par value) decreases 275,000, while the amount of Common Stock ($5 par value) increases 275,000.Chapter 71.Requirement 1If revenue is recognized at the date of delivery, the following journal entries would be used to record the transactions for the two years:Year 1Inventory ............................................................................................ 480,000 Cash/Accounts payable .............................................................. 480,000To record purchase of inventoryInventory ............................................................................................ 124,000 Cash/Accounts payable .............................................................. 124,000To record refurbishment of inventoryAccounts receivable .......................................................................... 310,000 Sales revenue ............................................................................. 310,000To record sale of goods on accountCost of goods sold ............................................................................. 220,000 Inventory ..................................................................................... 220,000To record the cost of the goods sold as an expenseSales returns (I/S) .............................................................................. 15,500* Allowance for sales returns (B/S)................................................ 15,500To record provision for return of goods sold under 30-day return period* 5% of $310,000Warranty expense ............................................................................. 31,000* Provision for warranties (B/S) ..................................................... 31,000To record provision, at time of sale, for warranty expenditures* 10% of $310,000Allowance for sales returns ............................................................... 12,400 Accounts receivable .................................................................... 12,400To record return of goods within 30-day return period.It is assumed the returned goods have no value and are disposed of.Provision for warranties (B/S) ............................................................ 18,600 Cash/Accounts payable .............................................................. 18,600To record expenditures in year 1 for warranty workCash .................................................................................................. 297,600* Accounts receivable .................................................................... 297,600To record collection of Accounts Receivable* $310,000 – $12,400Year 2Provision for warranties (B/S) ............................................................ 8,400 Cash/Accounts payable .............................................................. 8,400To record expenditures in year 2 for warranty workRequirement 2If revenue is recognized only when the warranty period has expired, the following journal entries would be used to record the transactions for the two years:Year 1Inventory ............................................................................................ 480,000 Cash/Accounts payable .............................................................. 480,000To record purchase of inventoryInventory ............................................................................................ 124,000 Cash/Accounts payable .............................................................. 124,000To record refurbishment of inventoryAccounts receivable .......................................................................... 310,000 Inventory ..................................................................................... 220,000 Deferred gross margin ................................................................ 90,000To record sale of goods on accountDeferred gross margin ....................................................................... 12,400 Accounts receivable .................................................................... 12,400To record return of goods within the 30-day return period. It is assumed the goods have no value and are disposed of.Deferred warranty costs (B/S) ........................................................... 18,600 Cash/Accounts payable .............................................................. 18,600To record expenditures for warranty work in year 1. The warranty costs incurred are deferred because the related revenue has not yet been recognizedCash .................................................................................................. 297,600* Accounts receivable .................................................................... 297,600To record collection of Accounts receivable* $310,000 – $12,400Year 2Deferred warranty costs .................................................................... 8,400 Cash/Accounts payable .............................................................. 8,400To record warranty costs incurred in year 2 related to year 1 sales. The warranty costs incurred are deferred because the related revenue has not yet been recognized.Deferred gross margin ....................................................................... **77,600Cost of goods sold ............................................................................. 220,000 Sales revenue ............................................................................. 297,600*To record recognition of sales revenue from year 1 sales and related cost of goods sold at expiry of warranty period* $310,000 – $12,400** ($90,000 – $12,400)Warranty expense ............................................................................. 27,000* Deferred warranty costs .............................................................. 27,000To record recognition of warranty expense at same time as related sales revenue recognition* $18,600 + $8,400Requirement 3Allied Auto Parts Inc. might choose to recognize revenue only after the warranty period has expired if they are not able to make a good estimate, at the time of sale, of the amount of warranty work that willbe required under the terms of the one-year warranty. If Allied is not able, at the time of sale, to make a good estimate of the warranty work that will be required, then the measurability criterion of revenue recognition is not met at the time of sale. The measurability criterion means that the amount of revenue can be reliably measured. If the seller is not able to estimate the amount of work that will have to be done under the warranty agreement, then it is not able to reasonably measure the profit that it will eventually earn on the sales. The performance criteria might also be invoked here. The performance criterion means that the seller has transferred the significant risks and rewards of ownership to the buyer. As long as there is warranty work to be performed after the sale that is the responsibility of the seller, you might argue that performance is not substantially complete. However, if the seller was able to reliably estimate the amount of warranty work, then performance would be satisfied on the assumption that we could measure the risk that remains with the seller, and make a provision for it.2.Percentage-of-completion method:The first step in applying revenue recognition using the percentage-of-completion method (using costs incurred to date compared to estimated total costs to determine the percentage of completion) is to estimate the percentage of completion of the project at the end of each year. This is done in the following table (in $000s):End of 2005 End of 2006 End of 2007Total costs incurred $ 5,400 $ 12,950 $ 18,800 Total estimated costs 18,000 18,500 18,800% completed 30% 70% 100% Once the percentage of completion at the end of each year has been calculated as above, the next step is to allocate the appropriate amount of revenue to each year, based on the percentage completed to date, less what has previously been recorded in revenue. This is done in the following table (in $000s):2005 2006 20072005 $20,000 × 30% $ 6,0002006 $20,000 × 70% $ 14,0002007 $20,000 × 100% $ 20,000 Less: Revenue recognized in prior years (0) (6,000) (14,000) Revenue for year $ 6,000 $ 8,000 $ 6,000 Therefore, the profit to be recognized each year on the construction project would be:2005 2006 2007 TotalRevenue recognized $ 6,000 $ 8,000 $ 6,000 $ 20,000 Construction costs incurred (expenses) (5,400) (7,550) (5,850) (18,800) Gross profit for the year $ 600 $ 450 $ 150 $ 1,200 The following journal entries are used to record the transactions under the percentage-of-completion method of revenue recognition:2005 2006 20071. Costs of construction:Construction in progress ..................... 5,400 7,550 5,850Cash, payables, etc. ....... 5,400 7,550 5,8502. Progress billings:Accounts receivable .............. 3,100 4,900 12,000Progress billings .............. 3,100 4,900 12,0003. Collections on billings:Cash ...................................... 2,400 4,000 12,400Accounts receivable ........ 2,400 4,000 12,4004. Recognition of profit:Construction in progress........ 600 450 150Construction expense ............ 5,400 7,550 5,850Revenue from long-termcontract ....................... 6,000 8,000 6,0005. To close construction in progress:Progress billings .................... 20,000Construction in progress ... 20,0002005 2006 2007Balance sheetCurrent assets:Accounts receivable $ 700 $ 1,600 $ 1,200 Inventory:Construction in process 6,000 14,000Less: Progress billings (3,100) (8,000)Costs in excess of billings 2,900 6,000Income statementRevenue from long-term contracts $ 6,000 $ 8,000 $ 6,000 Construction expense (5,400) (7,550) (5,850) Gross profit $ 600 $ 450 $ 1503.a. The three criteria of revenue recognition are performance, measurability, and collectibility.Performance means that the seller or service provider has performed the work. Depending on the nature of the product or service, performance may mean quite different points of revenuerecognition. For example, for the sale of products, IAS18 defines performance as the point when the seller of the goods has transferred the risks and rewards of ownership to the buyer. Normally, this means that performance is done at the time of sale. Although the seller may have performed much of the work prior to the sale (production, selling efforts, etc.), there is still significant risk to the seller that a buyer may not be found. Therefore, from a reliability point of view, revenuerecognition is delayed until the point of sale. Also, there may be significant risks remaining with the seller of the product even after the sale. Warranties given by the seller are a risk that remains with the seller. However, if this risk can be reliably estimated at the time of sale, revenue can be recognized at the point of sale. Performance is quite different under a long-term construction contract. Here, performance really is considered to be a measure of the work done. Revenue is recognized over the production period as the work is performed. It is intended to reflect theamount of effort expended by the seller (contractor). Although legal title won’t transfer to the buyeruntil the project is completed, revenue can be recognized because there is a known andcommitted buyer. If the contractor is not able to estimate how much of the work has been done (perhaps because he or she can’t reliably estimate how much work must still be done), then profit would not be recognized until the extent of performance is known.Measurability means that the seller or service provider must be able to reliably estimate theamount of the revenue from the sale or service. For the sale of products this is generally known at the time of sale (the sales price is set). However, if the seller provides a return period, it may be necessary to estimate the volume of returns at the time of sale in order to measure the revenue that will be recognized.Collectibility means that the seller or the service provider has reasonable assurance that the sales price will actually be collected. In most cases for the sales of products, the seller is able torecognize revenue at the time of sale even if the sale is on account. This is because the seller has experience with its customers and is able to estimate reliably the risk of non payment. As long as the seller is able to make this estimate, it is appropriate to recognize the revenue but to offset it with a provision for possible non collection. If the seller is unable to make reliable estimates of future collection of amounts owing, the recognition of revenue would be delayed until the cash is actually received. This is what is done using the instalment sales method of revenue recognition.b. Because of the performance criterion of revenue recognition, it would seem to be most appropriate to recognize most revenue as the seller or service provider performs the work. This would be the best measure of performance. This would mean, for example, that sellers of products would recognize their revenue over the whole production, selling, and post sales servicing periods. As we saw above, this is not commonly done because, in many cases, there are still significant risks that are retained by the seller (risk of not being able to sell the product, for example). There are also measurement risks (knowing the selling price) that exist prior to the sale. Thepercentage-of-completion method of revenue used for some long-term construction contracts would seem to most closely recognize revenue as the work is performed. As mentioned in Part 1, we are able to recognize revenue on this basis since a contract exists which commits the purchaser to buy the project (assuming certain conditions are met) and the sales price is known because of the existence of the contract.4.If all revenue is recognized when a student registers for the course, profit for 2007 would be:Sales Revenue1:Manuals and initial lessons (200 × $100) $ 20,000 Additional lessons ((200 × 8) × $30) 48,000 Examinations ((200 × 80%) × $130) 20,800 Total sales revenue 88,800 Cost of sales:Manuals and initial lessons (200 × ($15 + $3)) 3,600 Additional lessons ((200 × 8) × $3)) 4,800 Examinations ((200 × 80%) × $30) 4,800 Total cost of sales 13,200 Depreciation of development costs:$180,000 × (200/1,000) 36,000 Profit $ 39,6005.FINISH ENTERPRISESIncome Statementfor the year ending December 31, 2005Continuing operations (excluding the chemical division)Sales ($35,000,000 – $5,500,000) $ 29,500,000Cost of sales ($15,000,000 – $2,800,000) (12,200,000)Gross profit 17,300,000Selling & administration expenses($18,000,000 – $3,200,000) (14,800,000)Profit from operations 2,500,000Income tax expense (40%) 1,000,000Profit after tax $ 1,500,000 Discontinuing operations (Chemical division)Sales 5,500,000Cost of sales (2,800,000)Gross profit 2,700,000Selling & administration expenses (3,200,000)Loss from operations (500,000)Income tax expense(40%) 200,000Loss after tax (300,000) Gain on discontinuance of the Chemical division 3,500,000Tax thereon (1,400,000)After-tax gain on discontinuance of the Chemical division 2,100,000 Enterprise net profit $ 3,300,000Chapter 81.Payment of account payable. operatingIssuance of preferred stock for cash. financingPayment of cash dividend. financingSale of long-term investment. investingAmortization of bond discount. no effectCollection of account receivable. operatingIssuance of long-term note payable to borrow cash. financing Depreciation of equipment. no effectPurchase of treasury stock. financingIssuance of common stock for cash. financingPurchase of long-term investment. investingPayment of wages to employees. operatingCollection of cash interest. investingCash sale of land. InvestingDistribution of stock dividend. no effectAcquisition of equipment by issuance of note payable. no effectPayment of long-term debt. financingAcquisition of building by issuance of common stock. no effectAccrual of salary expense. no effect2.(a) Cash received from customers = 816,000(b) Cash payments for purchases of merchandise. =468,000(c) Cash payments for operating expenses. = 268,200(d) Income taxes paid. =36,9003.Cash sales …………………………………………... $9,000Payment of accounts payable ……………………….-48,000Payment of income tax ………………………………-13,000Payment of interest ……………………………..…..-16,000Collection of accounts receivable …………………… 93,000Payment of salaries and wages ………………………..-34,000Cash flows from operating activitiesby the direct method -9,0004.Operating activities:Net loss -200,000 Add: loss on sale of land 250,000 Add: depreciation 300,000Add: amortization of patents 20,000 Less: increases in current assets other than cash -750,000 Add: increases in current liabilities 180,000Net cash flows from operating -200,000 Investing activitiesSale of land -50,000Purchase of PPE -1,500,000Net cash flows from investing -1,550,000 Financing activitiesIssuance of common shares 400,000Payment of cash dividend -50,000Issuance of non-current liabilities 1,000,000Net cash flows from financing 1,350,000 Net changes in cash -400,000 5.。

会计专业英语(超实用}

一、企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流动资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due within one year 减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivable due within one year减:短期投资跌价准备Less: Impairment for current investment短期投资净额Net bal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账准备Less: Bad debt provision for Account receivable 应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账准备Less: Bad debt provision for Other receivable 其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less: Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due within one year一年内到期的应收融资租赁款Finance lease receivables due within one year其他流动资产Other current assets流动资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment委托贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值准备Less: Impairment for long-term equity investment减:长期债权投资减值准备Less: Impairment for long-term debt investment减:委托贷款减值准备Less: Provision for entrusted loan receivable长期投资净额Net bal of long-term investment其中:合并价差Include: Goodwill (Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less: Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less: Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值准备Less: Impairment for construction in progress 在建工程净额Net bal of construction in progress固定资产清理Fixed assets to be disposed of固定资产合计Total fixed assets无形资产及其他资产Other assets & Intangible assets无形资产Intangible assets减:无形资产减值准备Less: Impairment for intangible assets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease –Unguaranteed residual values融资租赁——应收融资租赁款Finance lease –Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets & intangible assets递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability & Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advance from customers应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Other payable预提费用Accrued Expense预计负债Provision递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year 其他流动负债Other current liability流动负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants & Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益)Owners’Equity实收资本(或股本)Paid in capital减;已归还投资Less: Capital redemption实收资本(或股本)净额Net bal of Paid in capital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include: Statutory reserves未确认投资损失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include: Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability & Equity三、利润及利润分配表Income statement and profit appropriation一、主营业务收入Revenue减:主营业务成本Less: Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit ( - means loss) 加:其他业务收入Add: Other operating income减:其他业务支出Less: Other operating expense减:营业费用Selling & Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列)Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列)Add: Investment income补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less: Non-operating expense四、利润总额(亏损总额以“—”填列)Profit before Tax减:所得税Less: Income tax少数股东损益Minority interest加:未确认投资损失Add: Unrealised investment losses五、净利润(净亏损以“—”填列)Net profit ( - means loss)加:年初未分配利润Add: Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution( - means loss) 减:提取法定盈余公积Less: Appropriation of statutory surplus reserves 提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and welfare fund提取储备基金Appropriation of reserve fund提取企业发展基金Appropriation of enterprise expansion fund利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners' distribution 减:应付优先股股利Less: Appropriation of preference share's dividend 提取任意盈余公积Appropriation of discretionary surplus reserve应付普通股股利Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses from natural disaster3.会计政策变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting policies4.会计估计变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting estimates5.债务重组损失Losses from debt restructuringaccount payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表Accounting period 会计期间accounting year 或financial year 会计年度accountant genaral 会计主任account balancde 结平的帐户account bill 帐单account books 帐account classification 帐户分类account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐Accounting period(会计期间)are related to specific time periods ,typically one year(通常是一年) 资产负债表:balance sheet 可以不大写b利润表:income statements (or statements of income)利润分配表:retained earnings现金流量表:cash flows1、部门的称谓市场部Marketing销售部Sales Department (也有其它讲法,如宝洁公司销售部叫客户生意发展部CBD)客户服务Customer Service ,例如客服员叫CSR,R for representative人事部Human Resource行政部Admin.财务部Finance & Accounting产品供应Product Supply,例如产品调度员叫P S Planner2、人员的称谓助理Assistant秘书secretary前台接待小姐Receptionist文员clerk ,如会计文员为Accounting Clerk主任supervisor经理Manager总经理GM,General Manager入场费admission运费freight小费tip学费tuition价格,代价charge制造费用Manufacturing overhead 材料费Materials管理人员工资Executive Salaries 奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare 会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance 油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees总监Director总会计师Finance Controller高级Senior 如高级经理为Senior Manager 营业费用Operating expenses代销手续费Consignment commission charge 运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license plate tax(VVULPT) 土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost帐目名词一、资产类Assets流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents 外埠存款Other city Cash in bank银行本票Cashier''s cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments - stock债券Short-term investments - corporate bonds基金Short-term investments - corporate funds其他Short-term investments - other短期投资跌价准备Short-term investments falling price reserves 应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrappage低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process - outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investment长期股权投资Long-term investment on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investment on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investments depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备Bcreditor''s rights investment depreciation reserves委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves 固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or income 待处理固定资产损溢Wait deal fixed assets loss or income二、负债类Liability短期负债Current liability短期借款Short-term borrowing应付票据Notes payable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应付账款Account payable预收账款Deposit received代销商品款Proxy sale goods revenue应付工资Accrued wages应付福利费Accrued welfarism应付股利Dividends payable应交税金Tax payable应交增值税value added tax payable进项税额Withholdings on V AT已交税金Paying tax转出未交增值税Unpaid V AT changeover减免税款Tax deduction销项税额Substituted money on V AT出口退税Tax reimbursement for export进项税额转出Changeover withnoldings on V AT出口抵减内销产品应纳税额Export deduct domestic sales goods tax转出多交增值税Overpaid V AT changeover未交增值税Unpaid V AT应交营业税Business tax payable应交消费税Consumption tax payable应交资源税Resources tax payable应交所得税Income tax payable应交土地增值税Increment tax on land value payable应交城市维护建设税Tax for maintaining and building cities payable应交房产税Housing property tax payable应交土地使用税Tenure tax payable应交车船使用税Vehicle and vessel usage license platetax(VVULPT) payable应交个人所得税Personal income tax payable其他应交款Other fund in conformity with paying其他应付款Other payables预提费用Drawing expense in advance其他负债Other liabilities待转资产价值Pending changerover assets value预计负债Anticipation liabilities长期负债Long-term Liabilities长期借款Long-term loans一年内到期的长期借款Long-term loans due within one year一年后到期的长期借款Long-term loans due over one year应付债券Bonds payable债券面值Face value, Par value债券溢价Premium on bonds债券折价Discount on bonds应计利息Accrued interest长期应付款Long-term account payable应付融资租赁款Accrued financial lease outlay一年内到期的长期应付Long-term account payable due within one year一年后到期的长期应付Long-term account payable over one year 专项应付款Special payable一年内到期的专项应付Long-term special payable due within one year一年后到期的专项应付Long-term special payable over one year 递延税款Deferral taxes三、所有者权益类OWNERS'' EQUITY资本Capita实收资本(或股本) Paid-up capital(or stock)实收资本Paicl-up capital实收股本Paid-up stock已归还投资Investment Returned公积资本公积Capital reserve资本(或股本)溢价Cpital(or Stock) premium接受捐赠非现金资产准备Receive non-cash donate reserve 股权投资准备Stock right investment reserves拨款转入Allocate sums changeover in外币资本折算差额Foreign currency capital其他资本公积Other capital reserve盈余公积Surplus reserves法定盈余公积Legal surplus任意盈余公积Free surplus reserves法定公益金Legal public welfare fund储备基金Reserve fund企业发展基金Enterprise expension fund利润归还投资Profits capitalizad on return of investment利润Profits本年利润Current year profits利润分配Profit distribution其他转入Other chengeover in提取法定盈余公积Withdrawal legal surplus提取法定公益金Withdrawal legal public welfare funds提取储备基金Withdrawal reserve fund提取企业发展基金Withdrawal reserve for business expansion提取职工奖励及福利基金Withdrawal staff and workers'' bonus andwelfare fund利润归还投资Profits capitalizad on return of investment应付优先股股利Preferred Stock dividends payable提取任意盈余公积Withdrawal other common accumulation fund 应付普通股股利Common Stock dividends payable转作资本(或股本)的普通股股利Common Stock dividends change toassets(or stock)未分配利润Undistributed profit四、成本类Cost生产成本Cost of manufacture基本生产成本Base cost of manufacture辅助生产成本Auxiliary cost of manufacture制造费用Manufacturing overhead材料费Materials管理人员工资Executive Salaries 奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare 会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance 油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing 运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees季节性停工损失Loss on seasonality cessation劳务成本Service costs五、损益类Profit and loss收入Income业务收入OPERATING INCOME主营业务收入Prime operating revenue产品销售收入Sales revenue服务收入Service revenue其他业务收入Other operating revenue材料销售Sales materials代购代售包装物出租Wrappage lease出让资产使用权收入Remise right of assets revenue 返还所得税Reimbursement of income tax其他收入Other revenue投资收益Investment income短期投资收益Current investment income长期投资收益Long-term investment income计提的委托贷款减值准备Withdrawal of entrust loans reserves 补贴收入Subsidize revenue国家扶持补贴收入Subsidize revenue from country其他补贴收入Other subsidize revenue营业外收入NON-OPERATING INCOME非货币性交易收益Non-cash deal income现金溢余Cash overage处置固定资产净收益Net income on disposal of fixed assets出售无形资产收益Income on sales of intangible assets固定资产盘盈Fixed assets inventory profit罚款净收入Net amercement income支出Outlay业务支出Revenue charges主营业务成本Operating costs产品销售成本Cost of goods sold服务成本Cost of service主营业务税金及附加Tax and associate charge营业税Sales tax消费税Consumption tax城市维护建设税Tax for maintaining and building cities 资源税Resources tax土地增值税Increment tax on land value5405 其他业务支出Other business expense销售其他材料成本Other cost of material sale其他劳务成本Other cost of service其他业务税金及附加费Other tax and associate charge 费用Expenses营业费用Operating expenses代销手续费Consignment commission charge运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license plate tax(VVULPT) 土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost营业外支出Nonbusiness expenditure捐赠支出Donation outlay减值准备金Depreciation reserves非常损失Extraordinary loss处理固定资产净损失Net loss on disposal of fixed assets 出售无形资产损失Loss on sales of intangible assets固定资产盘亏Fixed assets inventory loss债务重组损失Loss on arrangement罚款支出Amercement outlay所得税Income tax以前年度损益调整Prior year income adjustmentabacus算盘Abandonment废弃,报废;委付abandonment value废弃价值ability to service debt偿债能力abnormal cost异常成本abnormal spoilage异常损耗above par超过票面价值above the line线上项目absolute amount绝对数,绝对金额absolute endorsement绝对背书absolute insolvency绝对无力偿付absolute priority绝对优先求偿权absolute value绝对值absorb摊配,转并absorption account摊配账户,转并账户absorption costing摊配成本计算法abstract摘要表abuse滥用职权abuse of tax shelter滥用避税项目ACCA特许公认会计师公会accelerated cost recovery system加速成本收回制度accelerated depreciation method加速折旧法,快速折旧法acceleration clause加速偿付条款,提前偿付条款acceptance bill承兑票据acceptance register承兑票据登记簿acceptance sampling验收抽样access time存取时间accommodation融通accommodation bill融通票据accommodation endorsement融通背书accountability经营责任,会计责任accountability unit责任单位Accountancy 《会计》杂志accountancy会计accountant会计员,会计师accountant general会计主任,总会计accounting in charge主管会计师accountant,s legal liability会计师的法律责任accountant,s report会计师报告accountant,s responsibility会计师职责account form账户式,账式accounting assumption会计假定,会计假设accounting basis会计基准,会计基本方法accounting changes会计变更accounting concept会计概念accounting control会计控制accounting convention会计常规,会计惯例accounting corporation会计公司accounting cycle会计循环accounting data会计数据accounting doctrine会计信条accounting elements会计要素accounting entity会计主体,会计个体accounting entry会计分录accounting equation会计等式accounting event会计事项accounting exposure会计暴露,会计暴露风险accounting firm会计事务所Accounting Hall of Fame会计名人堂accounting harmonization会计协调化accounting identity会计恒等式accounting income会计收益accounting information会计信息accounting information system会计信息系统accounting internationalization会计国际化accounting journals会计杂志accounting legislation会计法规accounting manual会计手册accounting objective会计目标accounting period会计期accounting policies会计政策accounting postulate会计假设accounting principle会计原则Accounting Principle Board会计原则委员会accounting procedures会计程序accounting profession会计职业,会计专业accounting rate of return会计收益率accounting records会计记录,会计簿籍Accounting Review 《会计评论》accounting rules会计规则Accounting Series Release 《会计公告文件》accounting service会计服务accounting software会计软件accounting standard会计标准,会计准则accounting standardization会计标准化Accounting Standards Board会计准则委员会(英) Accounting Standards Committee会计准则委员会(英) accounting technique会计技术accounting theory会计理论accounting transaction会计业务,会计账务Accounting Trend and Techniques 《会计趋势和会计技术》accounting unit会计单位accounting valuation会计计价accounting year会计年度accounts会计账簿,会计报表account sales承销清单,承销报告单Account 账户Accounting system 会计系统American Accounting Association 美国会计协会Audit 审计Balance sheet 资产负债表bookkeeping 簿记cash folw prospects 现金流量预测certificate in Internal Auditing 内部审计证书certificate in Management Accounting 管理会计证书Certificate Public Accountant 注册会计师cost accounting 成本会计external users 外部使用者financial accounting 财务会计financial accounting standards board 会计准则委员会financial forecast 财务预测generally accepted accounting principles 会计公认原则general-purpose information 通用目的信息government accounting office 政府会计办公室income statement 损益表institute of internal auditors 内部审计师协会institute of management accountants 管理会计师协会integrity 整合性internal auditing 内部审计internal control structure 内部控制结构internal revenue service 国内收入暑internal users 内部使用者management accounting 管理会计return of investment 投资回报securities ans exchange commission 证券交易委员会statement of cash flow 现金流量表statement of financial position 财务状况表tax accounting 税务会计accounting equation 会计等式articulation 勾稽关系assets 资产business entity 企业个体capital stock 股本corporation 公司cost principle 成本原则creditor 债权人deflation 通货紧缩disclosure 披露expenses 费用financial statement 财务报表financial activities 筹资活动going-concern assumption 持续经营假设inflatiion 通货膨胀investing activities 投资活动owner's equity 所有者权益parternership 合伙企业negative cash flow 负现金流量operating activities 经营活动liabilities 负债positive cash folw 正现金流retained earning 留存利润revenue 收入sole proprietorship 独资企业slovency 清偿能力stable-dollar assumption 稳定货币假设stockholders 股东stockholders' equity 股东权益window dressing 门面粉饰account format 账户式account payable 应付账款account receivabla 应收账款accounting cycle 会计循环accounting equation 会计等式accounting receivable turnover 应收账款周转率accrual basis accounting 债权发生制accrued dividend 应计股利accrued expenseaccrued revenueaccumulated depreciation 累计折旧acid-test ratio 、quick ratio 速动资产与流动负债比例acquisition cost 购置成本adjusted trial balance 调整后试算表adjusting entry 调整分录adverseaging of accounts receivable 应收账款的账龄分类allocable 应分配的allowance for bad debts 备抵坏账allowance for depreciationallowance for doubtful accounts 呆账备抵allowance for uncollectible accounts 呆账备抵amortization 摊销、清偿annuity due 期初年金allowance method 备抵法annuity method 年金法appraisal method 估价法bad debt 坏账bad debts expensebank discount 银行贴现折扣bank reconciliation 银行调节表bank statement 银行对账单barter 易货交易benchmarking 基准board of directors 董事会bond 证券bonds payable 应付债券book value 账面价值budget 预算callable bonds 可赎回债券capital 资金,资本capital expenditures 资本支出capital lease 资本租赁capital paid in 缴入资本capital stock 股本capitalize 资本化carry back 抵前carry forward 递延、结转cash basis accounting 现收现付制cash disbursements journal 现金支出簿cash in hand 库存现金cash receipts journal 现金收入日记账chart of accounts 会计科目表classified balance sheet 分类资产负债表closing entries 结账分录closing the accounts 结账collateral 抵押品common stock 普通股compound interest 复利comprehensive income 综合收入conservatism 谨慎性consistency principle 一致性consolidated statements 汇总报表contingent liability 或有负债contra account 抵消账户contract interest rate 约定利率contribute capital 缴入资本control account 控制账户controlling interest 控制股权权益convertible bond 可转换债券convertible preferred stock 可转换优先股copyright 版权cost of capital 资本成本cost of goods sold 销售成本coupon 息票,减价优待券credit 信用,贷方cumulative preferred stock 累积优先股current assets 流动资产current liability 流动负债fair market value 公平市价FIFO 先进先出法fixed assets 固定资产FOB price 离岸价footnotes 表下注释franchise 特许权freight-in 进货运费freight-out 销货运费general journal 普通日记账general ledger 总分类账gross book value 账面价值gross profit 毛利hedge 套期交易incremental cost 增值成本installment 分期付款instruments 证券,票据intangible assets 无形资产interest 利息inventory 存货invoice 发票issued capital stock 已发行股本journal entry 日记账LIFO 后进先出long-term debt 长期负债Lower of cost or market 成本市价孰低法lump sum 一次性付款market value 市场价值markup 涨价mortgage 抵押,债券net assets 净资产obsolete inventory 作废存货partnership 合伙企业par value 面值patent 专利权payroll 工资单pension fund 养老基金pension plan 养老金计划physical inventory 实地盘点pledged assets 抵押资产posting 过账P&E 固定资产preference shares 优先股preferred stock 优先股premium 溢价present value 现值principal 本金refinance 再筹资refund 退还,再筹资retained earnings 留存收益salvage value 挽救价值(残值)security 证券,担保品segment 分部service life 使用年限stockholders equity 股东权益stock discount 股票折价straight line method 直线法subsidiary ledger 明细分类账sum-of-the-year-digits methods 年数总和法tangible assets 有形资产voucher check 凭单支票withholding 预扣worksheets 工作底稿write down 减计write off 转销,注销year-end-adjustment 年终调整。

2020年本科会计英语章后习题答案-光盘1

新世纪会计学专业精品教材国家级双语教学示范课程会计专业英语教程(第三版)章后习题答案马建威编著东北财经大学出版社大连ContentsChapter 1 (3)Chapter 2 (5)Chapter 3 (7)Chapter 4 (10)Chapter 5 (12)Chapter 6 (14)Chapter 7 (17)Chapter 8 (19)Chapter 9 (22)Chapter 10 (25)Chapter 11 (26)Chapter 12 (28)Chapter 13 (29)Chapter 14 (30)Chapter 15 (32)Chapter 16 (34)Chapter 11. True or false1.1 T1.2 T1.3 T1.4 T1.5 F1.6 F1.7 F1.8 F1.9 F2. Short answer questions2.1 Accounting may be described as the process of identifying, measuring, recording, and communicating economic information to permit informed judgments and decisions by users of that information.2.2 The simplest answer to this question is that financial accounting provides information for managers to use in operating the business. In addition, financial accounting provides information to other stakeholders to use in assessing the economic performance and the condition of the business.2.3 A set of financial statements consists of four related accounting reports that summarize in a few pages the financial resources, obligations, profitability, and cash transactions of a business. A complete set of financial statements includes: A balance sheet, an income statement, a statement of owner s’ equity and a statement of cash flow.2.4 There are several objectives of financial reporting. The Financial Accounting Standards Board (FASB) concluded that the objectives of the financial reporting are to provide information that:is useful to those making investment and credit decisions;is helpful in assessing future cash flows; andidentifies the economic resources (assets), the claims to those resources(liabilities), and the changes in those resources and claims.2.5 Using cash-basis accounting, income and expenses are recognized only when cash is received or paid out. Using accrual-basis accounting, receivables and payables are recognized when a sale is agreed to, even though no cash has been received or paid out as yet.3. Problem solvingA L OE(a) + +(b) + +(c) - -(d) + +(e) - -(f) +,-(g) - -(h) + +(i) - -(j) +,-(k) - -(l) - -(m) + -(n) - -(o) +,-4. Case studyOmitted.Chapter 21. True or false1.1 T1.2 F1.3 F1.4 T1.5 F1.6 F1.7 F1.8 T1.9 T1.10 T2. Short answer questions2.1 An internal control system refers to the policies and procedures designed to protect the firm's assets and to ensure reliable accounting. It also should promote efficient operations and urge employees to comply with company policies. Internal control systems can help prevent losses, help mangers plan operations, and monitor company and employer performance.2.2 A bank reconciliation is a report explaining any differences between the balance according to a depositor's records and the balance on the company's bank statement. The reconciliation procedure examines the differences based on the information available to the company and adjusts for the differences. It also serves as a format for the discovery and correction of errors.2.3 The net method assumes that a firm will take all cash discounts offered for prompt payment. Any discounts missed are recorded in a discounts lost account. Discounts lost is considered to be an operating expense, and to be a record of presumed inefficiencies in managing cash (of course, further analysis may reveal that the discounts lost reflect purchase discounts at unfavorable terms). The net method of accounting for purchases is used to assist in the internal control function.2.4 Accounts receivable arise from credit sales to customers. Accounts receivable are reported at their realizable value, which is their total amount less an estimate for the amount of uncollectible accounts. Accounts receivable are also recorded into an accounts receivable subsidiary ledger that separately lists amounts owed by individual customers.2.5 A company’s receivables are normally converted to cash as the customers pay off their accounts. However, there are at least three options available to a company that wishes to convert its receivables before they are at least due. First a company can sell the receivables to a factor. Second, a company can use its receivables as collateral for a loan. Third, a company can discount the receivables to a bank in return for cash.3. Problem solvingYear 1: ($49,000/$285,000) ×365 = 63 daysYear 2: ($85,000/$575,000) ×365 = 54 daysThe decrease of 9 days means that this company has improved its management of receivables and its liquidity position.4. Case studyOn December 31, of the current year, a company's unadjusted trial balance revealed the following: Accounts receivable of $185,600; Sales Revenue of $1,280,000; (75% were on credit), and Allowance for Doubtful Accounts of $1,600 (credit balance).Chapter 31. True or false1.1 F1.2 T1.3 T1.4 T1.5 F1.6 F1.7 F1.8 T1.9 T1.10 T2. Short answer questions2.1 Merchandise inventory consists of goods owned by a company and held for resale. Three special cases involving ownership decisions are goods in transit, consigned goods, and damaged goods. Goods in transit are included in the inventory of the company that owns the goods. Consigned goods are included in the inventory of the consignor. Damaged goods are valued at net realizable value.2.2 The specific identification method exactly identifies the costs of the inventory items sold. The weighted average method smoothes out changes in costs by ―averaging‖ inventory costs. However, LIFO and FIFO provide different amounts in periods of rising or falling costs. For example, in periods of rising costs, LIFO provides a lower income and thus lower taxes. In periods of falling costs, LIFO provides a higher income and thus higher taxes. FIFO calculations provide both higher income and taxes in periods of rising costs and lower income and taxes in periods of declining costs.2.3 An inventory error causes misstatements in cost of good sold, gross profit, net income, current assets, and equity. It also causes misstatements in the next period's cost of goods sold and net income. However, the inventory error is said to be self-correcting because the error in the first period is offset by the error in the second period.2.4 A merchandiser's ability to pay its short term obligations depends, among other factors, on how quickly it sells its merchandise inventory. The inventory turnover ratio reveals how many times a company turns over (sells) its inventory during a period. A low ratio compared to competitors suggests the company may be holding more inventory than necessary to support its sales volume. On the other hand, a ratio that is too high compared to competitors may suggest that the inventory level is too low and customers may have to back order merchandise.The days' sales in inventory ratio helps to better interpret inventory turnover. It can be interpreted as the number of days one can sell from inventory if no new items are purchased, and can be viewed as a measure of the buffer against out-of-stock inventory.2.5 The retail method is generally used to prepare interim statements. It uses the cost to retail ratio to give an estimated ending inventory at cost. The gross profit method is typically used to reconstruct the value of lost, stolen, or destroyed inventory. It uses the (historical) gross profit ratio to estimate cost of goods sold and the value of ending inventory.3. Problem solving(1)(2)4. Case study(2) LCM, applied separately to each product = $3,470Chapter 41. True or false1.1 F1.2 F1.3 T1.4 F1.5 F1.6 T1.7 F1.8 T1.9 T1.10 T2. Short answer questions2.1 The cost of plant and equipment includes all expenditures reasonable and necessary in acquiring an asset and placing it in a position and condition for use in the operation of the business. Only reasonable and necessary expenditures should be included.2.2 Depreciation, as the term is used in accounting, is the allocation of the cost of a tangible plant asset to expense in the periods in which services are received from the asset. In short, the basic purpose of depreciation is to achieve the matching principle — that is, to offset the revenue of an accounting period with the costs of the goods and services being consumed in the effort to generate that revenue.2.3 The term accelerated depreciation means recognition of relatively large amounts of depreciation in the early years of use and reduced amounts in the later years. This is consistent with the basic accounting concept of matching costs with related revenue. Accelerated depreciation methods have been widely used in income tax returns because they reduce the current year’s tax burden by recognizing a relatively large amount of depreciation expense.2.4 (1) the expected life of the asset; (2) the expected useful life of another asset that is related to the life of the intangible asset, such as the mineral rights that relate to adepleting asset; (3) any legal, regulatory, or contractual provisions that enable renewal or extension of the asset’s legal or contractual life w ithout substantial economic cost;(4) the effects of obsolescence, demand, competition, and other economic factors; and(5) the level of maintenance costs required to obtain the expected future cash flows from the asset.2.5 Intangible assets are separated into three categories to determine whether or not they are amortized, and how they are reviewed for impairment. The three categories are: (1) intangible assets with a finite (limited) life, (2) intangible assets with an indefinite life, and (3) goodwill.3. Problem solving2014 July 1Computer Equipment 2,700Cash 2,700Nov.3 Repairs Expense 140Cash 140Dec.31 Depreciation Expense 275Accumulated Depreciation 275[($2,700 – $500) ÷ 4 × 1/2]2015 Dec.31 Depreciation Expense 550Accumulated Depreciation ($2,200 ÷ 4) 5502016 Jan.1 Computer Equipment 500Cash 5004. Case studyOmitted.Chapter 51. True or false1.1 T1.2 F1.3 F1.4 T1.5 T1.6 T1.7 F1.8 T1.9 F1.10 T2. Short answer questions2.1 For purposes of valuation and reporting at a financial statement date, debt and stock investments are classified into three categories of securities:(1)Trading securities are securities bought and held primarily for sale in the near term to generate income on short-term price differences.(2)Available-for-sale securities are securities that may be sold in the future.(3)Held-to-maturity securities are debt securities that the investor has the intent and ability to hold to maturity.2.2 Corporations purchase investments in debt or stock securities generally for one of three reasons. First, a corporation may have excess cash that it does not need for the immediate purchase of operation assets. Second, some companies such as banks, purchase investments to generate earnings from investment income. Third, some companies invest for strategic purposes.2.3 Reporting the unrealized gain or loss in the stockholders’ equity sections serves two important purposes: (1) it reduces the volatility of net income due to fluctuations in fair value. (2) it informs the financial statement user of the gain or loss that would occur if the securities were sold at fair value.2.4 Short-term investments are securities held by a company that are (1) readilymarketable, and (2) intended to be converted into cash within the next year or operating cycle, whichever is longer. Investments that do not meet both criteria are classified as long-term investments.2.5 Consolidated financial statements present the total assets and liabilities controlled by the parent company. They also present the total revenues and expenses of the subsidiary companies. Consolidated statements are prepared in addition to the financial statements for the parent and individual subsidiary companies.3. Problem solving(1) Jan.1 Stock Investments ..................................................................9,720Cash ....................................................................... 9,720 June 1 Cash (900 × $.50) .. (450)Dividend Revenue (450)Sep.15 Cash ($4,300 – $100) ..........................................................4,200Loss on Sale of Stock Investments (120)Stock Investments .................................................. 4,320[400 × ($9,720 ÷ 900)]Dec.1 Cash (500 × $.50) (250)Dividend Revenue (250)(2) Dividend Revenue is reported under Other Revenues and Gains on the incomestatement. Loss on Sale of Stock Investments is reported under Other Expenses and Losses on the income statement.4. Case studyJan. 2 Debt Investments .................................................................................... 32,000Cash ................................................................................... 32,000July 1 Cash ($30,000 × 10% × 1/2) ................................................................... 1,500Interest Revenue ................................................................ 1,500Chapter 61. True or false1.1 T1.2 F1.3 T1.4 T1.5 T1.6 F1.7 T1.8 T1.9 F1.10 F2. Short answer questions2.1 Current liabilities are obligations that must be paid within one year or within the operating cycle, whichever is longer. Another requirement for classification as a current liability is the expectation that the debt will be paid from current assets (or through the rendering of service). Liabilities that do not meet these conditions are classified as long-term liabilities.2.2 Bonds usually are very long-term notes, maturing in perhaps 30 or 40 years. The bonds are transferable; however, so individual bond-holders may sell their bonds to other investors at any time. Most bonds call for semi-annual interest payments to the bond-holders, with interest computed at a specified contract rate throughout the life of the bond. Thus, investors often describe bonds as ―fixed income‖ investments.2.3 Bonds payable differ from capital stock in several ways. First, bonds payable are a liability; thus, bond-holders are creditors of the corporation, not owners. Bond-holders generally do not have voting rights and do not participate in the earnings of the corporation beyond receiving contractual interest payments. Next, bond interest payments are contractual obligations of the corporation. Dividends, on the other hand, do not become legal obligations of the corporation until they have been formally declared by the board of directors. Finally, bonds have a specific maturing date, upon which the corporation must redeem the bonds at their face amount. Capital stock, onthe other hand, does not have a maturing date and may remain outstanding indefinitely.2.4 A principal advantage of raising money by issuing bonds instead of stock is that interest payments are deductible in determining income subject to corporate income taxes. Dividends paid to stockholders, however, are not deductible in computing taxable income.2.5 Bonds are sometimes retired before the maturity date. The principal reason for retiring bonds early is to relieve the issuing corporation of the obligation to make future interest payments. If interest rates decline to the point that a corporation can borrow at an interest rate below that being paid on a particular bond issue, the corporation may benefit from retiring those bonds and issuing new bonds at a lower interest rate.3. Problem solving(1) June 30 Bonds Payable ......................................................400,000Loss on Bond Redemption ...................................40,800Discount on Bonds Payable ............................... 32,800Cash .................................................................... 408,000($400,000 – $367,200 = $32,800)($400,000 × 102% = $408,000)(2) June 30 Bonds Payable ........................................................600,000Discount on Bonds Payable ............................... 10,000Gain on Bond Redemption ................................. 14,000Cash .................................................................... 576,000($600,000 – $590,000 = $10,000)($600,000 × 96% = $576,000)(3) Dec. 31 Bonds Payable ........................................................50,000Common Stock ................................................... 20,000Paid-in Capital in Excess of Par ......................... 30,000($5 × 80 × 50 = $20,000)4. Case studyThe alternative effects on net income and earnings per share are as follows:Issue Stock Issue BondsIncome before interest and taxes $1,500,000 $1,500,000 Interest (10% × $2,500,000) —(250,000) Income before income taxes 1,500,000 1,250,000 Income tax expense (450,000) (375,000) Net income $1,050,000 $ 875,000Outstanding shares 250,000 200,000Earnings per share $4.20 $4.38Net income is higher if the equipment is financed through the issuance of stock. However, earnings per share is lower because of the additional number of shares of common stock that are outstanding.Chapter 71. True or false1.1 T1.2 F1.3 T1.4 F1.5 F1.6 T1.7 F1.8 T1.9 T1.10 F2. Short answer questions2.1 Common stockholders generally have the right to vote at stockholders' meetings, sell or otherwise dispose of their stock, receive the same dividend, if any on each common share, and share in any assets remaining after creditors are paid when and if the corporation is liquidated. Stockholders generally also have a preemptive right, which is the right to purchase their proportional share of any common stock later issued by the corporation.2.2 Stockholders' equity consists of two main parts, paid-in capital and retained earnings. Paid-in capital consists of funds raised by the issuance of stock, either common or preferred. Paid-in capital is the total amount of cash and other assets the corporation receives in exchange for stock. Paid-in capital in excess of par value represents the amount a corporation receives from issuing stock when the market value exceeds the par value of the stock. Retained earnings is the cumulative net income and loss retained by the corporation less any dividends declared.2.3 Stock options are the rights to purchase common stock at a fixed price over a specified period. As the stock's price rises above the fixed price, the option's value increases. As a general rule, stock options motivate managers and employees to (1) focus on company performance, (2) take a long-term perspective, and (3) remain with the company. A stock option is like having an investment with no risk.2.4 The price-earnings ratio of a common stock is computed by dividing the stock's market value per share by its earnings per share. The price-earnings ratio represents the stock market's expectations of a company's future performance. Some analysts view a high PE (greater than 20 to 25, for instance) ratio as an indication that a stock is overvalued. A low ratio (less than 5 to 8) may indicate that a stock is undervalued.2.5 Dividend yield is the ratio of annual cash dividends per share divided by the market value per share of stock. The resulting dividend yield represents the percent of cash return investors receive from an investment in a company's stock. Dividend yield can be used to identify whether a stock is an income stock or a growth stock. Companies that pay large dividends on a regular basis are income stocks. Companies that distribute little or no cash but use the cash to finance expansion are known as growth stocks.3. Problem solving(1)Book value per preferred share:$560,000/5,000 shares = $112 per preferred share(2)Book value per common share:$2,550,000/150,000 shares = $17 per common share4. Case studyChapter 81. True or false1.1 T1.2 F1.3 T1.4 F1.5 T1.6 T1.7 F1.8 F1.9 F1.10 T2. Short answer questions2.1 The basic components of income begin with net sales. Cost of goods sold is subtracted from net sales to get gross profit (also called gross margin). Operating expenses are then subtracted from gross margin to determine net income.2.2 The gross margin ratio is calculated by dividing gross margin (or net sales less cost of goods sold) by net sales. The gross margin ratio measures a firm's profitability in selling its inventory. The gross margin must be large enough to cover operating expenses and provide sufficient net income to the owner(s).2.3 Selling expenses include the expenses of promoting sales by displaying and advertising merchandise, making sales, and delivering goods to customers. General and administrative expenses support a company's overall operations and include expenses related to accounting, human resource management, and financial management. Some expenses can relate to both areas and are allocated between them.2.4 The three important guidelines for revenue recognition include: (1) Revenue is recognized when earned. (2) Assets received from selling products and services do not need to be in cash. (3) Revenue recognized is measured by cash received plus the cash equivalent of other assets received.2.5 Revenues are the gross increases in equity from a company's earnings activities.Expenses are the costs of assets or services used to earn revenues. Net income is the excess of revenues over expenses.3. Problem solving(1)(2) Trico had the more favorable ratio for each year.(3) Unico's gross margin ratio is increasing, while Trico's is decreasing. Moreover, these changes appear significant and warrant further analysis.4. Case studyChapter 91. True or false1.1 F1.2 F1.3 T1.4 F1.5 T1.6 T1.7 T1.8 F1.9 T1.10 T2. Short answer questions2.1 Both stockholders and creditors use financial statement analysis to (1) predict their expected returns and (2) assess the risks associated with those returns.2.2 The analysis of financial data employs various techniques to emphasize the comparative and relative significance of the data presented and to evaluate the position of the firm. Three commonly used tools are as following.Horizontal analysis evaluates a series of financial statement data over a period of time.Vertical analysis evaluates financial statement data by expressing each item in a financial statement as a percent of a base amount.Ratio analysis expresses the relationship among selected items of financial statement data.2.3 For users of financial statements t o determine ―earning power‖ or regular income, the ―irregular‖ items are separately identified on the income statement. Three types of ―irregular‖ items are reported:(1) Discontinued operations.(2) Extraordinary items.(3) Changes in accounting principle.2.4 When two conditions are met (1) management can show that the new principle is preferable to the old principle, and (2) the effects of the change are clearly disclosed in the income statement.2.5 (1) Financial statements contain numerous estimates.(2) Traditional financial statements are based on cost.(3) Companies vary in the generally accepted accounting principles they use.(4) Fiscal year-end data may not be typical off the financial condition during the year.(5) Diversification within a global environment also limits the usefulness of financial analysis.3. Problem solving(1) Current = 1.45:1 ($160,000 ÷ $110,000)(2) Acid-test = 0.77:1 ($85,000 ÷ $110,000)4. Case study(1) Credit salesReceivables turnover = —————————————Average accounts receivable= $5,110,000 ÷ $700,000= 7.3 times365 daysAverage collection period = ——————————Receivables turnover= 365 ÷ 7.3 times= 50 days(2) Inventory turnover = Cost of goods sold ÷ Average inventoryFirst calculate ending inventory.Beginning Inventory $ 482,000+ Purchases 4,146,000– Cost of Goods Sold (4,088,000)*Ending Inventory $ 540,000*Since the gross profit ratio is 20%, the cost of goods sold ratio is 80%.80% × $5,110,000 (net sales) = $4,088,000.Ending Inventory = $540,000 (per above)Average Inventory = ($482,000 + $540,000) ÷ 2 = $511,000Inventory Turnover = $4,088,000 ÷ $511,000 = 8 timesDays to Sell = 365 days ÷ 8 times = 45.6 days(3) Net incomeReturn on common stockholders' equity = —————————————————Average common stockholders' equity =$490,000 ÷ $3,500,000 = 14%Chapter 101. True or false1.1 T1.2 T1.3 T1.4 F1.5 T1.6 T1.7 F1.8 T1.9 F2. Short answer questionsOmitted.3. Problem solving(1) Direct-labor-hour basisOverhead recovery rate=£50,000/2000=£25 per machine-hour.A £25×1500=£37500B £25×500=£12500(2) Machine-hour basisOverhead recovery rate=£50,000/1200=£41.6667 per machine-hour.A £41.6667×800=£33333B £41.6667×400=£166674. Case studyThe relevant costs to be included in the minimum price are:Stock item: A1 £6×500=£3,000B2 £8×800=£6,400We are told that the stock of item A1 is in frequent use and so, if it is used on the contract, it will need to be replaced. We are told the stock of item B2 will never be used by the business unless the contract is undertaken. Thus, if the contract is not undertaken, the only reasonable thing for the business to do is sell the stock. This means that the opportunity cost is £8 a unit.Chapter 111. True or false1.1 T1.2 T1.3 F1.4 F1.5 F1.6 T1.7 T1.8 T1.9 F2. Short answer questionsOmitted.3. Problem solvingThe original budget, the flexed budget and the actual are as follows:Budget Actual Flexed budget Output (production and sales) 1,000 units 1050 units 1050 units£££Sale revenue 100,000 104,300 105,000 Raw materials 40,000 41,200 42,000 Labor 20,000 12,300 21,000 Fixed overheads 20,000 19,400 20,000 Operating profit 20,000 22,400 22,000 Reconciliation of the budgeted and actual operating profits for JulyBudgeted profit 20,000Add favorable variances:Sales volume (22,000-20,000) 2,000Direct materials usage {[(1050×40)-40,500]×£1} 1,500Direct labor efficiency{[(1050×2.5)-2,600]×£8} 200Fixed overhead spending (20,000-19,400) 60024,300Less Adverse variances:Sales price variance (105,000-104,300) 700Direct materials price[(40,500×£1)-41,200] 700Direct labor rate[(2,600×£8) -21,300] 500Actual profit 22,4004. Case studyPilot Ltd(1)and (2)BudgetActualOriginal FlexedOutput (units)(production and sales)5,000 5,400 5,400£££Sales revenue 25,000 27,000 26,460Raw materials (7,500) (8,100) (2,700 kg) (8,770) (2,830 kg) Labor (6,250) (6,750) (1,350 hr) 6,885 (1,300 hr) Fixed overheads (6,000) (6,000) (6,350)Operating profit 5,250 6,150 4,455£Manager accountableSales volume varianceSales price variance Materials usage variance Materials price variance Labor efficiency variance Labor rate variance Fixed overhead variance5250-615027000-26460[(5400×0.5)-2830]×£3(2830×3)-8770[(5400×0.25)-1300]×£5(1300×5)-68856000-6350900 (F)(540) (A)(280) (A)(390) (A)(385) (A)250(F)(350) (A)SalesSalesBuyerProductionPersonnelProductionDepends on the natureof the overheadsTotal net variances 795(A) Note: F—favorable; A—adverse.。

会计词汇(英语版)