会计共享服务中心全球网络外文文献

数字化会计外国文献

数字化会计外国文献

以下是有关数字化会计外国文献的推荐:

•《会计领域的大数据:概述》,作者:Ali Alnodel。

这篇文章对大数据在会计行业的影响进行了广泛概述,深入探讨了大数据分析如何改变会计实践,并强调了在会计中使用大数据相关的挑战和机遇。

•《大数据分析在会计和审计中的作用》,作者:Syed Liaquat Hussain等。

该文探讨了大数据分析在会计和审计领域的潜在应用,详细讨论了大数据如何改变会计师的角色,并提供了在会计和审计中使用大数据分析的实例。

•《大数据及其对会计行业的影响》,作者:迈克尔·克拉滕。

这篇文章深入讨论了在会计中使用大数据所带来的挑战和机遇,并探讨了大数据如何改变会计师的角色,同时提供了一些大数据在会计和审计中应用的实例。

•《大数据、分析与会计职业的未来》,作者:小约瑟夫·R·科因。

这篇文章着重探讨了大数据分析对会计行业未来的潜在影响,对会计行业的未来发展提供了深刻的见解。

这些文献从不同的角度探讨了大数据在会计领域的应用和影响,为读者提供了全面而深入的理解。

如有更多需要,建议查阅国外文献资料获取。

财务共享外文参考文献

财务共享外文参考文献当谈到财务共享方面的外文参考文献时,我们可以从不同角度来考虑这个问题。

首先,我们可以从财务共享的概念和原则出发,寻找相关的外文参考文献。

其次,我们可以关注财务共享在不同行业和领域的应用,以及相关的国际经验和案例。

最后,我们也可以从技术和政策的角度来探讨财务共享的外文文献。

在财务共享概念和原则方面,一些经典的外文参考文献可能涉及到财务数据共享的隐私和安全性,以及共享经济对传统财务模式的冲击。

例如,可以参考M. D. Myers和N. S. Majluf在1984年发表的《Corporate financing and investment decisions when firms have information that investors do not have》一文,探讨了信息不对称对公司融资决策的影响。

此外,还可以查阅J. Bradford DeLong和A. Shleifer在1993年发表的《Princes and merchants: European city growth before the industrial revolution》一文,探讨了中世纪欧洲城市的财务共享和经济增长。

在财务共享在不同行业和领域的应用方面,可以关注一些特定行业的案例和国际经验。

例如,可以研究金融科技领域的财务共享模式,可以参考A. G. Akerlof和R. J. Shiller在2009年发表的《Animal spirits: How human psychology drives the economy, and why it matters for global capitalism》一书,探讨了金融市场中的信息共享和市场波动。

此外,也可以关注医疗健康领域的财务共享模式,可以参考L. B. Sheiner在2015年发表的《Sharing the costs: The impact of telemedicine ontraditional Medicare costs》一文,探讨了远程医疗对传统医疗成本的影响。

2023财务信息化国外文献综述

2023财务信息化国外文献综述一、引言在当今信息化发展迅速的时代,财务信息化已经成为了各个行业中不可或缺的部分。

随着全球经济一体化的加速推进,对于财务信息化的需求也在不断增加。

本文将从国外文献的角度出发,对2023年财务信息化的相关内容进行一次综述,旨在为读者提供一次全面、深入的了解。

二、财务信息化的概念1. 财务信息化的定义财务信息化是指在财务管理过程中采用信息技术手段进行数据的采集、处理、传递和利用,以提高财务管理效率和质量,改善公司治理结构,促进企业财务管理的现代化和规范化。

2. 财务信息化的重要性财务信息化可以使企业实现财务部门的数字化管理,提高工作效率,减少人为错误,提高财务数据的准确性和真实性,为企业决策提供更加准确的数据支持,从而对企业的经营管理起到了极大的促进作用。

三、财务信息化的发展现状1. 国外财务信息化的发展趋势根据国外文献的调查和研究,当前国外财务信息化的发展已经趋向于智能化、集成化。

各国企业纷纷引入人工智能、大数据分析等先进技术,提高财务信息化的水平,实现财务信息的自动化处理和预测分析。

2. 国外财务信息化的应用实例国外许多企业已经在财务信息化领域取得了丰硕的成果。

例如美国的谷歌公司通过引入人工智能技术,成功实现了财务数据的自动分析和预测,为企业决策提供了更为准确的数据支持,大大提高了财务管理的效率和质量。

四、财务信息化的未来发展1. 人工智能在财务信息化中的应用随着人工智能技术的不断发展,将更加深入地应用于财务信息化领域。

预计未来财务信息化将实现更高水平的自动化处理和智能化决策,为企业提供更为准确、及时的财务决策支持。

2. 数据安全在财务信息化中的重要性随着财务信息化的推进,数据安全问题也日益凸显。

未来,财务信息化需要更加重视数据的安全保障,加强对财务数据的加密和防护,确保财务信息不受到非法侵入和篡改。

五、结论通过对国外财务信息化的文献综述,我们可以看到,财务信息化已经成为企业管理的必然趋势,对企业的经营管理产生了深远的影响。

企业财务信息化国内外文献综述范文

企业财务信息化国内外文献综述近年来,随着科技的发展和全球化的趋势,企业财务信息化在国内外得到了广泛的应用和研究。

本文将就企业财务信息化的国内外文献进行综述,以期对该领域的研究有更深入的了解和认识。

一、企业财务信息化的概念和发展1.1 企业财务信息化的概念企业财务信息化是指利用信息技术手段对企业内部和外部的财务管理进行自动化和信息化处理,以提高管理效率和决策能力的过程。

企业财务信息化包括财务数据的采集、存储、处理和分析等方面,是企业管理中不可或缺的一部分。

1.2 企业财务信息化的发展随着信息技术的快速发展,企业财务信息化逐渐成为企业管理的重要趋势。

在国内外,越来越多的企业意识到财务信息化对企业管理和竞争力的重要性,纷纷进行相关的应用和研究。

一些学者和专家也对企业财务信息化进行了深入的研究和探讨,提出了许多有价值的观点和方法。

二、国外企业财务信息化的研究与应用2.1 美国企业财务信息化的研究美国作为全球经济的引领者,其企业财务信息化方面的研究和应用处于领先地位。

美国的一些知名企业如IBM、思科等早在80年代就开始了财务信息化的探索和实践,其经验和成果对全球范围内的企业财务信息化发展产生了积极的影响。

2.2 德国企业财务信息化的应用作为欧洲的经济强国,德国企业财务信息化的研究和应用也非常活跃。

德国的一些大型企业如戴姆勒、西门子等在财务信息化方面拥有丰富的经验,其在企业管理和风险控制方面的成功案例为国内企业提供了许多借鉴和启示。

三、国内企业财务信息化的研究与实践3.1 我国企业财务信息化的现状近年来,我国企业财务信息化取得了长足的发展。

随着信息技术的普及和应用,越来越多的我国企业意识到财务信息化对企业管理的重要性,并开始进行相关的研究和实践。

国内的一些大企业如阿里巴巴、腾讯等在财务信息化方面展现出了较高的水平,其成功经验值得其他企业借鉴和学习。

3.2 我国企业财务信息化的研究成果在我国,许多学者和专家也对企业财务信息化进行了深入的研究和探讨,并取得了不少研究成果。

会计学外文经典文献

会计学外文经典文献摘要:一、引言1.会计学的重要性2.外文经典文献的意义二、会计学外文经典文献概述1.文献分类2.重要学术观点与贡献三、代表性外文经典文献解析1.文献一:《会计学原理》2.文献二:《财务会计理论》3.文献三:《管理会计》四、我国会计学外文经典文献的研究现状1.研究概况2.研究热点与趋势五、外文经典文献对我国会计学研究的启示1.理论体系建设2.研究方法与技术3.实践应用与创新六、结论1.外文经典文献在会计学领域的价值2.我国会计学研究的未来发展正文:一、引言会计学作为一门重要的经济管理学科,其理论体系和实践应用在全球范围内得到了广泛认可。

外文经典文献在会计学领域的研究成果丰富,为我国会计学研究提供了宝贵的理论依据和实践经验。

本文将对会计学外文经典文献进行梳理,以期为我国会计学研究提供参考。

二、会计学外文经典文献概述1.文献分类会计学外文经典文献主要包括财务会计、管理会计、审计、税收等方面的著作。

这些文献涵盖了会计学的理论体系、方法论、实践应用等各个方面。

2.重要学术观点与贡献在外文经典文献中,许多学者提出了具有影响力的学术观点,如会计要素、会计等式、财务报表分析、现金流量预测等。

这些观点为会计学理论体系的构建奠定了基础,并对实际应用产生了深远影响。

三、代表性外文经典文献解析1.文献一:《会计学原理》这本书是由美国会计学家佩顿(Paton)和利特尔顿(Littleton)共同撰写的。

该书系统地阐述了会计学的基本原理和方法,强调了会计信息的真实性和可靠性。

这本书对我国会计学研究的理论体系建设具有重要的指导意义。

2.文献二:《财务会计理论》该书由美国学者布里曼(Bromwich)和瓦茨(Watts)合著。

该书对财务会计理论进行了全面梳理,对会计准则、会计信息质量、会计假设等方面进行了深入探讨。

这本书对我国会计学研究具有很高的参考价值。

3.文献三:《管理会计》这本书是由英国学者亨德里克森(Hendrickson)所著。

关于企业财务共享服务研究的文献综述

关于企业财务共享服务研究的文献综述近年来,随着信息技术的快速发展以及企业规模的不断扩大,企业财务共享服务成为提高企业财务效率、降低成本的重要手段。

本文将对关于企业财务共享服务的研究文献进行综述。

企业财务共享服务是指在同一集团内的不同企业之间,通过共享财务资源、共同使用财务系统和数据,实现财务业务的集中处理和管理。

具体来说,财务共享服务包括财务业务处理、会计核算、财务报表编制、财务分析等方面。

在企业财务共享服务研究方面,许多学者从不同的角度和层面进行了深入研究。

以下是一些典型的研究文献:1. 《企业财务共享服务模式研究》该文献系统地分析了企业财务共享服务的概念、特点、模式和实施方法。

研究发现,财务共享服务可以提高财务效率、降低成本,但实施过程中也存在一些挑战,如信息安全风险、人员管理问题等。

研究者提出了一些解决方案和建议,以促进企业财务共享服务的顺利实施。

3. 《云计算在企业财务共享服务中的应用研究》该文献从云计算的角度,研究了企业财务共享服务中云计算的应用。

研究发现,云计算可以提供灵活、可扩展的财务共享服务平台,帮助企业实现财务数据的共享和共同使用。

云计算还可以提高系统的安全性、可靠性和可用性,为企业财务共享服务的实施创造更有利的条件。

4. 《企业财务共享服务对企业绩效的影响研究》该文献研究了企业财务共享服务对企业绩效的影响。

研究发现,通过财务共享服务,企业可以实现财务数据的集中管理和处理,提高财务分析和决策的准确性和及时性。

研究还发现,在实施财务共享服务的企业中,财务绩效普遍较好,公司价值也有所提升。

企业财务共享服务作为提高企业财务效率和降低成本的重要手段,受到了广泛的关注。

目前,相关研究主要集中在财务共享服务的概念、模式、实施方法以及对企业绩效的影响等方面。

未来的研究可以从更深入的角度探讨财务共享服务的实施机制、影响因素以及解决实施过程中的问题和挑战。

2024年会计论文外文参考文献

[18] 王斌,李苹莉. 关于企业预算目标确定及其分解的理论分析[J]. 会计研究. 2001(08)

[19] 《管理会计应用与发展的典型案例研究》课题组,林斌,刘运国,谭光明,张玉虎. 作业成本法在我国铁路运输企业应用的案例研究[J]. 会计研究. 2001(02)

[6] 余绪缨. 关于培养高层次管理会计人才的认识与实践[J]. 财会月刊. 2007(22)

[7] 余绪缨. 管理会计学科建设的方向及其相关理论的新认识[J]. 财会通讯(综合版). 2007(02)

[8] 于增彪,王竞达,袁光华. 中国管理会计的未来发展:研究方法、热点实务和人才培养[J]. 首都经济贸易大学学报. 2006(01)

2024年会计论文外文参考文献

会计论文外文参考文献1

[1]徐静.我国企业社会责任会计信息披露探析[J].企业导报.2012(15) :22-25.

[2]张明霞.李云鹏.企业社会责任会计信息披露问题研究[J].经济研究导刊.2011(20):40-43.

[3] 路秀平.任会来.我国社会责任会计信息披露模式现实选择 [J]. 会计之友 (上旬刊).2012(12):89-92.

[20] 胡玉明. 21世纪管理会计主题的转变--从企业价值增值到企业核心能力培植[J]. 外国经济与管理. 2001(01)

本文来源:网络收集与整理,如有侵权,请联系作者删除,谢谢!

[4]林斌,饶静.上市公司为什么自愿披露内部控制鉴证报告.一基于信号传递理论的实证研宄[J].会计研究,2009 (2): 45-52.

会计专业研究生必看外文文献

1. Introduction, Course Overview and the Examples for PresentationBall R., and P. Brown. 1968. An Empirical Evaluation of Accounting Income Numbers. Journal of Accounting Research 6: 159-178.Beaver W.H., 1968. The Information Content of Annual Earnings Announcements. Journal of Accounting Research 6: 67-92.2. The Information Content of Accounting Earnings: ERCEaston, P., and M. Zmijewski. 1989. Cross-Sectional Variation in the Stock Market Response to Accounting Earnings Announcements. Journal of Accounting and Economics 11: 117-141.Collins, D.W., and S.P. Kothari. 1989. An Analysis of Intertemporal Cross-Sectional Determinants of Earnings Response Coefficients. Journal of Accounting and Economics 11: 143-181.Lipe, C., 1986. The Information Contained in the Components of Earnings. Journal of Accounting Research 24: 37-64.3. Other Accounting Information and Stock PricesBowen, R.M., D. Burgstahler, and L. A. Daley. 1986. Evidence on the Relationships between Earnings and Various Measures of Cash Flow. The Accounting Review 61: 713-725.Jegadeesh N., and J. Livnat. 2006. Revenue Surprises and Stock Returns. Journal of Accounting and Economics 41: 147-171.Kothari S.P., and R. G. Sloan. 1992. Information in Price about Future Earnings: Implications for Earnings Response Coefficients. Journal of Accounting and Economics 15: 143-171.4. Time-Series Properties of Accounting InformationFoster, G., 1977. Quarterly Accounting Data: Time-Series Properties and Predictive-Ability Results. The Accounting Review 52: 1-21.Brooks, L., and D. Buckmaster. 1976. Further Evidence of the Time Series Properties of Accounting Income. The Journal of Finance 31: 1359-1373.Freeman, R., J. Ohlson, and S. Penman. 1982. Book Rate-of-Return and Prediction of Earnings Changes: An Empirical Investigation. Journal of Accounting Research 20: 639-653.5. Analyst ForecastsO’ Brien, P., 1988. Analysts’ Forecasts as Earnings Expectations. Journal of Accounting and Economics 10: 538-.Dechow, P., A. Hutton, and R. Sloan. 2000. The Relation between Analysts’Long-TermEarnings Forecasts and Stock Price Performance Following Equity Offering. Contemporary Accounting Research 17: 1-32.Irvine, P.J. 2004. Analysts’ Forecasts and Brokerage-Firm Trading. The Accounting Review 79: 125-149.6. Earning Management: Part IBurgstahler, D., and I.D.Dichev. 1997. Earnings Management to Avoid Earnings Decreases and Losses. Journal of Accounting and Economics 24: 99-126.Matsumoto, D. 2002. Management’s Incentives to Avoid Negative Earning Surprises. The Accounting Review 77: 483-514.Jones, J. 1991. Earnings Management during Import Relief Investigations. Journal of Accounting Research 29: 193-228.7. Earning Management: Part IIDeFond, M.L., and J. Jiambalvo. 1994. Debt Covenant Violation and Manipulation of Accruals. Journal of Accounting and Economics 17: 145-176.Gramlich, J.D., M.L. McAnally, and J. Thomas. 2001. Balance Sheet Management: The Case of Short-Term Obligations Reclassified ad Long-Term Debt. Journal of Accounting Research 39: 283-295.Daniel, N.D., D.J. Denis, and L. Naveen. 2008. Do Firms Manage Earnings to Meet Dividend Thresholds? Journal of Accounting and Economics 45: 2-26.8. Management Disclosures and Disclosure QualityBotosan, C., 1997. Disclosure Level and the Cost of Equity Capital. The Accounting Review 72: 323-349.Skinner, D. 1994. Why Do Firms V oluntarily Disclose Bad News? Journal of Accounting Research 32: 38-60.Lang M.H., and R.J. Lundholm. 1996. Corporate Disclosure Policy and Analyst Behavior. The Accounting Review 71: 467-492.9. Financial Accounting: an International View(3学时)Ball, R., S.P. Kothari, and A. Robin. 2000. The Effect of International Institutional Factors on Properties of Accounting Earnings. Journal of Accounting and Economics 29: 1-51.Morck, R., B. Yeung, and W. Yu. 2000. The information Content of Stock Markets: Why DoEmerging Markets Have Synchronous Stock Price Movements? Journal of Financial Economics 58: 215-260.Lang, M., J.S. Ready, and M.H. Yetman. 2003. How Representative Are Firms that Are Cross-Listed in the United States? An Analysis of Accounting Quality. Journal of Accounting Research 41: 363-386.参考书目[加]威廉姆·司可脱著,陈汉文译,《财务会计理论》,机械工业出版社。

企业会计信息化研究外文文献翻译最新译文

文献出处: T Vatuiu. The study of enterprise accounting information [J]. Annals of the University of Petrosani, Economics, 2015, 5: 201-208.原文The study of enterprise accounting informatizationT VatuiuAbstractThe development of information technology is accompanied by the rise and popularization of computer and the emergence and development, the original computer is applied to the finance department handling accounting business, enterprise information since birth is the accounting information into the center, that is to say, the success of accounting informationization construction is directly related to the success of the enterprise informationization strategy. In the enterprise implementation of accounting information system is conducive to further standardize the operation of the enterprise funds, for the enterprise management decision makers to provide real and effective reference data, in a rapidly changing market competition to accurately grasp the market changes, better management combined with the actual enterprise decision-making, to achieve the optimal allocation of resources and benefits.Keywords: enterprise; Accounting informationization; ERP1 IntroductionWith the development of computer information technology and penetration in the social each domain, the information technology is more and more attention, so information technology is also naturally become the important driving force of economic development. At present, the world has become a global village, networking and globalization has become the main trend of world development, starting in the 1980 s, countries began to make the informatization development strategy adjustment and as an important support power, promote the development of national economy, also took to the formal information construction development road, national policies, the informationization construction as an important part for a period of time in the future of the country's development goals, and to promote and facilitate the process ofthe country's enterprise information construction, to lay a solid position in the market competition.Enterprise as the important pillar of national economy growth, closely related to the development and growth of the national economy informatization as the subsystem of the national informatization, is the surest way to achieve modernization of the enterprise, therefore, only to promote the enterprise information, to better promote the national economic information.2 The concept and related theories of enterprise informatization2.1 The meaning of enterprise informationAccounting information is the wide application of information technology in the accounting work, the development of information resources, the use of information technology to promote enterprise to develop the economy and improve the economic benefit, and to provide comprehensive information services to various aspects of the process. The main content of the accounting information is to establish a system of accounting information and accounting information system is the main part of enterprise information system, the basic law of development is consistent with the enterprise information system. Accounting informationization is popular in recent years a noun, it is different from the accounting computerization, is to cater to the information society and the application of a new word, it has realized the accounting and the integration of information technology, is the enterprise management in the new period of main channel of information for policy makers, and effectively solve the accounting computerization existence island phenomenon is an important way, is conducive to standardize the procedures of accounting management and enhancing the market competitiveness of the enterprise. Accounting information is the key of enterprise informatization construction and most important, to the enterprise overall information-based construction and implementation plays an important role in success.2.2 ERP concepts and related theoriesERP (Enterprise Resource Planning) refers to an Enterprise Resource Planning system, it is GartnerGrouP companies in the United States in 1990.It will enterpriseplanning, management, marketing, finance, purchasing set at an organic whole, to the customer's needs and the activities of the enterprise goal to unify, to all the enterprise resources integration into a dynamic complete supply chain. The core of the ERP is the management of the enterprise is an organic whole, emphasized the ERP is an enterprise's lean management and lean production, realized the unity of advance planning and afterwards. Use of ERP software system to realize the coordination and control of each department, make the business process tends to rationalize, to better achieve department the input for the optimization of the reconstruction to lay the work, is the enterprise continuously self-assessment and important way to improve management.ERP has experienced four stages of development, its core is to realize the management thoughts of the entire supply chain comprehensive dynamic effective management and control. In particular, mainly includes three aspects of thought. One is reflect of the whole supply chain resources comprehensive management thoughts. Today is the era of win-win cooperation, enterprise competition is, in fact, to a certain extent has evolved into a competition between the supply chain and another supply chain problems, enterprises should not only know the optimal configuration of their resources, also need to coordinate the advantage of other resources, such as with suppliers, customers, and the relationship between the sales network and so on, thus to the all-round development of the enterprise into a dynamic system, and to effectively implement the management of the enterprise supply chain is a dynamic and control. Tt is to embody the lean production, concurrent engineering and virtual manufacturing management thinking. The core of the ERP system shown above all is lean production. Is all supply chain partners into the overall production process, to establish the enterprise and the interests of customers, suppliers and other partners sharing mechanism, form an integral part of the supply chain. Followed by agile manufacturing, when there is new on the market opportunities and business partners can't meet, can rapidly form a virtual factory, thus realize products in the limited time and resources optimization configuration, enterprise in market activity, high quality and diverse and flexible. Then, it is reflected in advance plan to control the overallmanagement of thoughts later. ERP enterprise production planning, logistics demand plan, sales plan, budget and human resources plan integrated into a whole system, and successfully realized the centralization and unification of various plans for formal management. In addition, the ERP system of the transaction to the relevant accounting synchronous records, ensure the cash flow and logistics of synchronization and consistent, can understand the ins and outs of money thus to control and management in a timely manner.3 Enterprise informatization development present situationFrom the perspective of the development of accounting information system, the early of the accounting information system is mainly the financial and reporting software, solve and manage the daily accounting and report processing, the financial department are introduced corresponding accounts receivable and payroll data system. But the period of the establishment of the accounting information system often do not pay attention to economic benefits, in the process of actual operation on data processing is also a lack of control, as a result, the user for the accounting information system is still in the stage stay at a respectful distance from sais the further development of the computer in the world and popular, wins initial success in accounting information system in the financial sector, then gradually developed, and the accounting information system in other department managers also begin to pay close attention to the information system of investment benefit, at this point, an enlarged the scope of information system, in addition to the accounting information system, also including the personnel information system, marketing information system and logistics information system, after that, the accounting information system to the widespread popularity and spread of development stage, the stage by the managers convene the different functions of the overall planning, and set up a special information management center of internal control activities, to start the project management system, since then, the accounting information system on the right track.3.1 Accounting network systematization degree is lowAccounting information is the premise of accounting network, according to relevant data shows: enterprise all serious resource waste. This is mainly because thenetwork degree applied in enterprise accounting system is too low. Enterprise data submitted too many mistakes. This is mainly because the typing errors in the process of data transmission, computer fault, and other factors. Enterprise cannot very good coordination between different departments. Only in the financial sector, mainly because the accounting software applications cannot be good coordination with other departments.3.2 Insufficient understanding of ERP systemFirst, many enterprise ERP system is regarded as the common office software, rather than use it as an integral part of the management system to run, the myth has led to many enterprises will be the construction of the ERP investment focus in ERP software system, and neglect to personnel training and the adjustment of the system process. Second, insufficient understanding of ERP's return on investment. Many small and medium-sized enterprise knowledge of ERP system there is a big deviation, either the ERP system is considered to be the panacea to solve the problem of enterprise all, don't think it's not much value to the enterprise, can objectively evaluate the value of the ERP system makes the ERP investment return expectations appeared larger gap. Third, the lack of understanding of the function of ERP system, think that ERP system is the simple use of inventory, logistics and financial system, not the whole development of the enterprise management planning together, through the system dynamic adjustment to realize the unification of the whole enterprise management.3.3 The accounting business process is not standardEnterprise accounting information system from accounting subject classification, the accounting information collection, selection, summary, but the current implementation, accounting information system provides information far cannot satisfy the needs of corporate decision makers, so that the accounting activities became independent departments in operation, the data generated by the natural and the business sector has been out of line. Enterprise after the implementation of accounting information system, simply by using the computer instead of manual accounting, and failed to change from the whole enterprise accounting businessprocess, did not realize the fundamental process reengineering. And in practice, enterprise capital is seriously lagging behind the logistics information, thus causes the enterprise business process can't satisfy the need of real-time control in time, nature of accounting information and enterprise management state of point-to-point statistics, provide to the enterprise information management and the policy makers also loses the relative authenticity, the reliability of the information quality decline.4 ConclusionAccounting informationization is the enterprise informatization of the central nervous, many enterprises in the construction of informatization, often based on accounting information into a breakthrough, the accounting information is the core of enterprise informatization enterprise accounting information is an ongoing process, the goal is to set up the enterprise decision support system, decision-making for real-time, accurate and complete the production and transmission of information, realize the optimal allocation of resources, the rational flow of value; Help enterprises to quickly make the right decisions, in the harsh competition environment to survive and continue to grow stronger. Companies must also be on the outer and inner risk of the enterprise effective management and control, only through the implementation of the strategy analysis in the process of small and medium-sized enterprise accounting information system analysis, and can effectively deal with accounting information, accounting information system, internal control and external risk management, and to better promote the small and medium-sized enterprise accounting information system to realize healthy and sustainable development.译文企业会计信息化问题研究T Vatuiu摘要信息化的发展是伴随着计算机的兴起和普及而出现和发展的,最初计算机是应用于财务部门处理会计业务的,企业信息化从诞生开始就是以会计信息化为中心的,也就是说会计信息化建设的成功与否直接关系到企业信息化战略的成功。

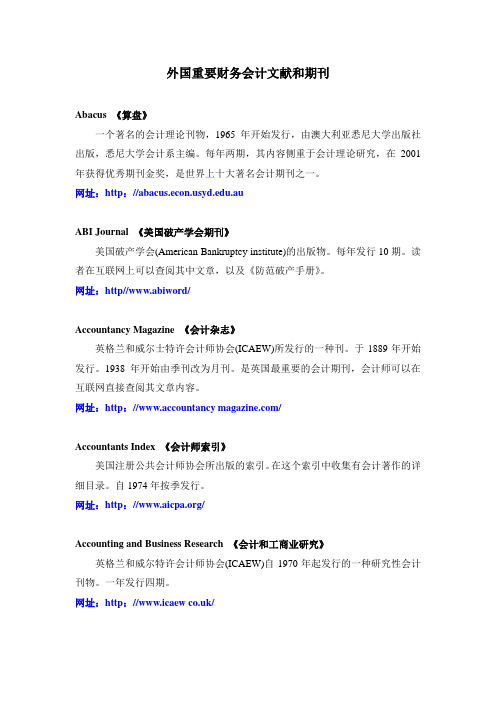

外国重要财务会计文献和期刊

外国重要财务会计文献和期刊Abacus 《算盘》一个著名的会计理论刊物,1965年开始发行,由澳大利亚悉尼大学出版社出版,悉尼大学会计系主编。

每年两期,其内容侧重于会计理论研究,在2001年获得优秀期刊金奖,是世界上十大著名会计期刊之一。

网址:http://.auABI Journal 《美国破产学会期刊》美国破产学会(American Bankruptcy institute)的出版物。

每年发行10期。

读者在互联网上可以查阅其中文章,以及《防范破产手册》。

网址:http//www.abiword/Accountancy Magazine 《会计杂志》英格兰和威尔士特许会计师协会(ICAEW)所发行的一种刊。

于1889年开始发行。

1938年开始由季刊改为月刊。

是英国最重要的会计期刊,会计师可以在互联网直接查阅其文章内容。

网址:http://www.accountancy /Accountants Index 《会计师索引》美国注册公共会计师协会所出版的索引。

在这个索引中收集有会计著作的详细目录。

自1974年按季发行。

网址:http:///Accounting and Business Research 《会计和工商业研究》英格兰和威尔特许会计师协会(ICAEW)自1970年起发行的一种研究性会计刊物。

一年发行四期。

网址:http://www.icaew /Accounting and the Public Interest 《会计和公众利益》美国会计学会(AAA)出版的一种学术性期刊。

其主要内容包括财务会计和审计,社会和环境会计、职业道德、信息技术、会计教育,以及会计机构的管理等内容。

网址:http:///Accounting Evolution to1900《1900年以前的会计发展演变》美国著名会计学家利特尔顿(A.C.Limeton)在1993年出版的一本著作。

其中详细地阐述了会计理论的历史发展过程。

关于会计的英文文献原文(带中文翻译)

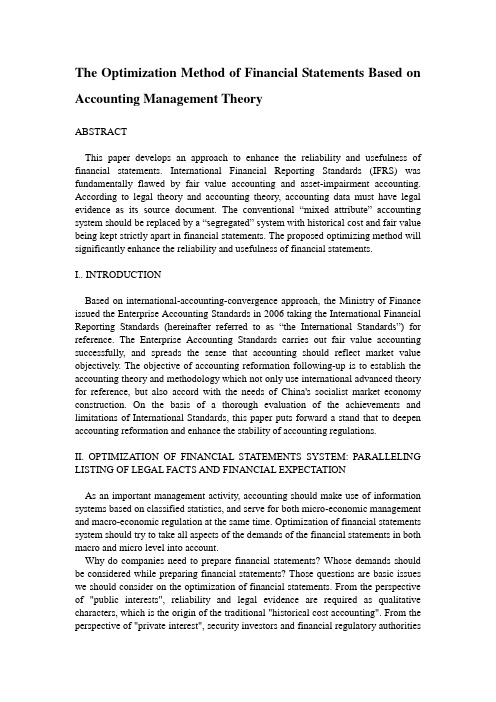

The Optimization Method of Financial Statements Based on Accounting Management TheoryABSTRACTThis paper develops an approach to enhance the reliability and usefulness of financial statements. International Financial Reporting Standards (IFRS) was fundamentally flawed by fair value accounting and asset-impairment accounting. According to legal theory and accounting theory, accounting data must have legal evidence as its source document. The conventional “mixed attribute” accounting system should be re placed by a “segregated” system with historical cost and fair value being kept strictly apart in financial statements. The proposed optimizing method will significantly enhance the reliability and usefulness of financial statements.I.. INTRODUCTIONBased on international-accounting-convergence approach, the Ministry of Finance issued the Enterprise Accounting Standards in 2006 taking the International Financial Reporting Standards (hereinafter referred to as “the International Standards”) for reference. The Enterprise Accounting Standards carries out fair value accounting successfully, and spreads the sense that accounting should reflect market value objectively. The objective of accounting reformation following-up is to establish the accounting theory and methodology which not only use international advanced theory for reference, but also accord with the needs of China's socialist market economy construction. On the basis of a thorough evaluation of the achievements and limitations of International Standards, this paper puts forward a stand that to deepen accounting reformation and enhance the stability of accounting regulations.II. OPTIMIZA TION OF FINANCIAL STATEMENTS SYSTEM: PARALLELING LISTING OF LEGAL FACTS AND FINANCIAL EXPECTA TIONAs an important management activity, accounting should make use of information systems based on classified statistics, and serve for both micro-economic management and macro-economic regulation at the same time. Optimization of financial statements system should try to take all aspects of the demands of the financial statements in both macro and micro level into account.Why do companies need to prepare financial statements? Whose demands should be considered while preparing financial statements? Those questions are basic issues we should consider on the optimization of financial statements. From the perspective of "public interests", reliability and legal evidence are required as qualitative characters, which is the origin of the traditional "historical cost accounting". From the perspective of "private interest", security investors and financial regulatory authoritieshope that financial statements reflect changes of market prices timely recording "objective" market conditions. This is the origin of "fair value accounting". Whether one set of financial statements can be compatible with these two different views and balance the public interest and private interest? To solve this problem, we design a new balance sheet and an income statement.From 1992 to 2006, a lot of new ideas and new perspectives are introduced into China's accounting practices from international accounting standards in a gradual manner during the accounting reform in China. These ideas and perspectives enriched the understanding of the financial statements in China. These achievements deserve our full assessment and should be fully affirmed. However, academia and standard-setters are also aware that International Standards are still in the process of developing .The purpose of proposing new formats of financial statements in this paper is to push forward the accounting reform into a deeper level on the basis of international convergence.III. THE PRACTICABILITY OF IMPROVING THE FINANCIAL STATEMENTS SYSTEMWhether the financial statements are able to maintain their stability? It is necessary to mobilize the initiatives of both supply-side and demand-side at the same time. We should consider whether financial statements could meet the demands of the macro-economic regulation and business administration, and whether they are popular with millions of accountants.Accountants are responsible for preparing financial statements and auditors are responsible for auditing. They will benefit from the implementation of the new financial statements.Firstly, for the accountants, under the isolated design of historical cost accounting and fair value accounting, their daily accounting practice is greatly simplified. Accounting process will not need assets impairment and fair value any longer. Accounting books will not record impairment and appreciation of assets any longer, for the historical cost accounting is comprehensively implemented. Fair value information will be recorded in accordance with assessment only at the balance sheet date and only in the annual financial statements. Historical cost accounting is more likely to be recognized by the tax authorities, which saves heavy workload of the tax adjustment. Accountants will not need to calculate the deferred income tax expense any longer, and the profit-after-tax in the solid line table is acknowledged by the Company Law, which solves the problem of determining the profit available for distribution.Accountants do not need to record the fair value information needed by security investors in the accounting books; instead, they only need to list the fair value information at the balance sheet date. In addition, because the data in the solid line table has legal credibility, so the legal risks of accountants can be well controlled. Secondly, the arbitrariness of the accounting process will be reduced, and the auditors’ review process will be greatly simplified. The independent auditors will not have to bear the considerable legal risk for the dotted-line table they audit, because the risk of fair value information has been prompted as "not supported by legalevidences". Accountants and auditors can quickly adapt to this financial statements system, without the need of training. In this way, they can save a lot of time to help companies to improve management efficiency. Surveys show that the above design of financial statements is popular with accountants and auditors. Since the workloads of accounting and auditing have been substantially reduced, therefore, the total expenses for auditing and evaluation will not exceed current level as well.In short, from the perspectives of both supply-side and demand-side, the improved financial statements are expected to enhance the usefulness of financial statements, without increase the burden of the supply-side.IV. CONCLUSIONS AND POLICY RECOMMENDATIONSThe current rule of mixed presentation of fair value data and historical cost data could be improved. The core concept of fair value is to make financial statements reflect the fair value of assets and liabilities, so that we can subtract the fair value of liabilities from assets to obtain the net fair value.However, the current International Standards do not implement this concept, but try to partly transform the historical cost accounting, which leads to mixed using of impairment accounting and fair value accounting. China's accounting academic research has followed up step by step since 1980s, and now has already introduced a mixed-attributes model into corporate financial statements.By distinguishing legal facts from financial expectations, we can balance public interests and private interests and can redesign the financial statements system with enhancing management efficiency and implementing higher-level laws as main objective. By presenting fair value and historical cost in one set of financial statements at the same time, the statements will not only meet the needs of keeping books according to domestic laws, but also meet the demand from financial regulatory authorities and security investorsWe hope that practitioners and theorists offer advices and suggestions on the problem of improving the financial statements to build a financial statements system which not only meets the domestic needs, but also converges with the International Standards.基于会计管理理论的财务报表的优化方法摘要本文提供了一个方法,以提高财务报表的可靠性和实用性。

毕业论文——财务共享服务中心模式分析与研究

财务共享服务中心模式分析与研究【摘要】当前财务共享服务中心(FinancialSharedServiceCenter, 简称FSSC。

)模式已成为跨国公司的一种新型管理模式, 其通过一种有效的运作模式来解决跨国公司财务职能建设中的效率低下和重复投入的缺点, 并充分整合相关资源建立统一、快捷的财务信息共享平台, 实现企业的战略目标和价值提升。

本文通过对财务共享服务模式的介绍, 并结合当前的实践经验, 具体分析该模式的优势和劣势, 为我国大型集团公司提供可供参考的信息。

【关键词】财务共享服务中心优缺点发展建议共享服务中心模式起源于20世纪80年代的西方发达国家, 经历的20多年的快速发展,现已在跨国公司得以广泛应用, 而财务服务共享是共享服务最主要的内容之一。

福特公司是世界公认的第一个建立共享服务中心的公司, 在20 世纪80年代初, 其在欧洲第一个建立财务共享服务中心, 将其下属公司共同的、简单的、标准化的财务业务集中到该中心, 实施全集团的财务共享服务。

近年来, 共享服务的管理思想迅速传入我国。

在理论界和实务界的共同努力下, 已经取得的一定的进展,并在国内实务界积极开展共享服务管理模式的实践工作。

在实践中,我们获得了具有中国大型企业自身特色的实践经验, 并在实际管理运作中取得了巨大成就, 同时也为理论界提供了大量的研究资料, 为未来该模式在我国的成功运用提供了基础。

一、财务共享服务中心模式的含义BryanBergeron在《共享服务精要》一书中提出了共享服务的定义:“共享服务是一种将一部分现有的经营职能集中到一个新的半自主的业务单元的合作战略, 这个业务单元就像在公开市场展开竞争的企业一样, 设有专门的管理结构, 目的是提高效率、创造价值、节约成本以及提高对内部客户的服务质量。

”作为一种管理创新, 共享服务管理模式被广泛用于现代企业的不同领域。

共享服务管理模式不同于传统的集中式或分散式的管理模式, 在共享服务的管理模式下, 企业将各个职能部门或各个分支机构中能够共享的服务部分独立出来, 作为一个专门的运营机构来向企业提供共享服务。

会计学外文经典文献

会计学外文经典文献会计学作为一门学科,有许多经典的外文文献。

以下是其中一些:1. "Accounting Principles" by Jerry J. Weygandt, DonaldE. Kieso, and Paul D. Kimmel: 这本书是会计学的经典教材,涵盖了会计学的基本原理和概念,适用于初学者和专业人士。

2. "Financial Accounting: Tools for Business Decision Making" by Paul D. Kimmel, Jerry J. Weygandt, and Donald E. Kieso: 这本书探讨了财务会计的理论和实践,重点关注如何用财务信息做出商业决策。

3. "Management Accounting: Information for Decision-Making and Strategy Execution" by Anthony A. Atkinson, Robert S. Kaplan, Ella Mae Matsumura, and S. Mark Young: 这本书涵盖了管理会计的理论和实践,讨论了如何为决策制定和战略执行提供信息。

4. "Cost Accounting: A Managerial Emphasis" by CharlesT. Horngren, Srikant M. Datar, and Madhav V. Rajan: 这本书介绍了成本会计的概念和方法,重点关注如何计算和控制成本以支持管理决策。

5. "Auditing and Assurance Services" by Alvin A. Arens, Randal J. Elder, and Mark S. Beasley: 这本书详细介绍了审计和保证服务的原理和实践,讨论了审计的目的、过程和责任。

关于企业财务共享服务研究的文献综述

关于企业财务共享服务研究的文献综述

企业财务共享服务是指多个公司共享同一套财务系统的服务。

随着云计算技术的日益成熟,企业财务共享服务已经成为了许多企业降低成本和提高效率的重要途径。

本文将针对企业财务共享服务进行文献综述。

首先,2018年Jun Hyup Lee等人在《Measurement model for business process performance in Korean shared service centers》中探讨了韩国共享服务中心业务流程绩效的测量模型。

作者采用了结构方程模型和多元回归分析方法,通过对多个韩国公司进行调研和数据分析,得出了一套适用于韩国共享服务中心业务流程绩效测量的模型,并展示了该模型的实用性。

其次,2019年Clara Garcia-Martinez等人在《Exploring the factors that drive the adoption of financial shared service centers from the perspective of accounting professionals》中研究了会计专业人士对于财务共享服务采用的因素。

作者采用了一个定量问卷调查的方法,选择了西班牙的公司作为研究对象。

研究结果显示,对于财务共享服务的采用,会计专业人士的优先考虑因素为降低成本、提高效率和加强内部控制。

总之,以上文献综述表明,财务共享服务已经成为了许多企业降低成本和提高效率的重要途径。

采用合适的模型和方法来测量业务流程绩效、考虑会计专业人士的优先考虑因素、分析采用模式和驱动因素以及研究成功决定因素,可以为企业实现财务共享服务提供新的思路和方法。

关于企业财务共享服务研究的文献综述

关于企业财务共享服务研究的文献综述随着企业规模的不断扩大和财务共享服务的需求不断增加,企业财务共享服务成为当前财务管理领域的热点话题。

此类服务在运营过程中涉及的内容广泛,包括会计、预算、报告和其他财务职能等。

本篇综述将对现有的关于企业财务共享服务研究的文献进行概述,并探讨其研究方向和研究成果。

1. 前言企业财务共享服务是指一个企业将会计、预算、报告和其他财务职能给予财务共享中心处理,以提高工作效率,实现财务数据的整合。

此外,这种服务能够在全球统一财务体系下,提供高质量的财务报告和数据。

2. 研究背景在过去的几十年中,很多企业发现本部门内部财务管理成本太高,效率受到限制。

由于企业的成长、收购和并购以及全球化的扩张,企业内部的财务管理面临愈来愈多的挑战。

这些企业将精力集中于其核心业务,这意味着削减和优化非核心业务的领域,如财务管理、会计和人力资源等。

于是企业财务共享服务因其低成本、高效率、一致的标准和最佳实践而得到广泛的关注。

3. 研究现状目前,国内外对企业财务共享服务的研究方向主要集中于以下几个方面:(1) 财务共享中心的创建和管理财务共享中心的创建和管理是企业财务共享服务发展的重要组成部分。

相关研究聚焦于财务共享中心的组织架构、服务内容设计、流程改进和绩效评估。

例如,林育强和林小玲(2011)研究发现,创建和管理财务共享中心能够降低企业的财务成本,提高财务业务处理效率。

Joshi和Gupta(2014)则聚焦于财务共享中心运营过程中的挑战和解决方案,并提出了如何提高财务共享中心运营效率的建议。

(2) 财务共享对企业绩效的影响财务共享服务通过提高财务管理和流程的效率和一致性,来促进企业的财务绩效提升。

目前,研究者普遍认为财务共享服务可以降低企业财务成本,并提高其绩效。

例如,Huq和Turley(2015)通过对英国的银行业进行研究,发现企业财务共享服务可以降低银行的非财务成本,并提高客户满意度和员工满意度。

财务共享模式国外研究现状文献

财务共享模式国外研究现状文献一、引言财务共享模式是指企业将财务数据、信息和流程通过云计算、大数据、人工智能等技术手段进行共享,以实现财务管理的高效性、准确性和安全性。

近年来,财务共享模式在国内外得到了广泛的应用和研究。

本文将介绍国外财务共享模式的研究现状文献。

二、国外财务共享模式的研究现状1. 《财务共享服务模式研究》该文献是由中国财政科学研究院的研究人员撰写的,主要介绍了财务共享服务模式的概念、特点和优势,并分析了其在国内外的应用情况。

该文献认为,财务共享服务模式可以提高企业的财务管理效率和准确性,降低成本和风险,是一种具有广阔发展前景的新型财务服务模式。

2. 《财务共享服务模式的实践与思考》该文献是由德勤会计师事务所的研究人员撰写的,主要介绍了财务共享服务模式在企业实践中的应用情况,并分析了其优缺点。

该文献认为,财务共享服务模式可以提高企业的财务管理效率和准确性,降低成本和风险,但同时也存在一些挑战和风险,需要企业在实践中加以注意和解决。

3. 《财务共享服务模式的实践与创新》该文献是由美国普华永道会计师事务所的研究人员撰写的,主要介绍了财务共享服务模式在企业实践中的应用情况,并分析了其优缺点。

该文献认为,财务共享服务模式可以提高企业的财务管理效率和准确性,降低成本和风险,但同时也需要企业在实践中加以注意和创新,以适应不断变化的市场和技术环境。

4. 《财务共享服务模式的风险管理》该文献是由英国安永会计师事务所的研究人员撰写的,主要介绍了财务共享服务模式的风险管理策略和方法,并分析了其在企业实践中的应用情况。

该文献认为,财务共享服务模式可以提高企业的财务管理效率和准确性,降低成本和风险,但同时也需要企业在实践中加强风险管理,以确保财务共享服务的安全性和可靠性。

三、结论国外财务共享模式的研究现状文献表明,财务共享服务模式可以提高企业的财务管理效率和准确性,降低成本和风险,是一种具有广阔发展前景的新型财务服务模式。

国外的财务共享研究报告

国外的财务共享研究报告

以下是国外财务共享研究报告的一些例子。

1. 《Leveraging the Power of Financial Data Sharing: A Global Perspective》 - 这份报告由Accenture撰写,研究了全球范围

内金融数据共享的潜力和机会。

报告分析了金融机构如何通过共享数据来改善业务决策、创新产品和服务,并为消费者提供更好的金融体验。

2. 《The Future of Financial Services: How FinTech is Transforming the Financial Industry》 - 这份报告由World Economic Forum撰写,研究了金融科技如何改变金融业。

报告探讨了财务共享的趋势,以及新兴技术如人工智能、区块链和大数据分析等如何推动财务共享的发展。

3. 《Open Banking: A Canadian Perspective》 - 这份报告由PwC Canada撰写,研究了加拿大的开放银行和财务共享。

报告分析了加拿大金融监管机构推动开放银行的进展和影响,以及金融机构和科技公司如何在这个新生态系统中合作。

4. 《The State of Open Banking in the United Kingdom》 - 这份报告由Deloitte UK撰写,研究了英国的开放银行现状。

报告评估了过去几年英国开放银行政策的影响,以及金融机构和创新科技公司如何应对这些变化。

这些报告提供了关于全球范围内财务共享的最新研究和趋势分

析。

您可以通过搜索报告名称或相关关键词,找到更多关于国外财务共享的研究报告。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

文献信息标题: Creating a global network of shared service centres for accounting作者: Lindvall, Jan; Iveroth, Einar出版物名称: Journal of Accounting & Organizational Change卷: 7期: 3页: 278-305出版年份: 2011年份: 2011出版商: Emerald Group Publishing, Limited出版物地点: Bradford出版物国家/地区: United KingdomISSN: 18325912DOI: /10.1108/18325911111164213ProQuest 文档ID: 893892014文档URL: /docview/893892014?accountid=38235联系ProQuest版权 2015 ProQuest LLC。

保留所有权利。

- 条款与条件Creating a global network of shared service centres for accountingAbstractThe purpose of this paper is to contribute to the understanding of the practice of IT-enabled management control change, in particular how IT-driven change is made possible from a practical perspective in a global context. It does so by investigating the redesign of the telecommunications company Ericsson's global finance and accounting function from an independent structure of numerous national chief financial officer units into one interdependent global network of shared service centres. Ericsson's transformation was followed by drawing mainly on interviews and documents. The data were analysed using narrative and temporal bracketing strategies for theorising from process data. The paper illustrates how IT-enabled management control change unfolds as a continuous interaction between a dynamic organisational structure (social dimension) and a less, but still, dynamic IT (material dimension) across time. The study also highlights how such a process is metaphorically similar to the form of a hermeneutic spiral rather than the common perspective of an arrow from the present to the future. This paper stresses the importance of pre-understanding, an openness to trials and learning, and a dynamic stance towards the moving targets of IT and organisation.IntroductionGlobalisation and access to new information technology (IT) are two interdependent forces, creating both opportunities and threats for individuals, companies and nations ([9] Bhimani, 2003; [89] Scapens and Jazayeri, 2003). Opportunities can include opening up new markets and expanding the customer base for many companies. Threats can include the development of new and innovative business models that increase the possibilities for new competitors to enter a given market. Such changes have consequences not only for an organisation's strategy, structure, culture, and management control ([8] Berger, 2006; [45] Granlund and Malmi, 2002), but also for competencies and work ([63] Malone, 2004).If, due to different institutional arrangements, cultural differences and technological restrictions, it was previously necessary to manage a multinational company strategically as a portfolio of independent and vertically oriented subsidiaries, globalisation creates possibilities for integration among the subsidiaries. It is now possible to design an interdependent, horizontally oriented and more standardised management model ([26] Chenhall, 2008). Such change is largely enabled by the use of new integrating IT, such as enterprise resource planning (ERP) ([83] Pollock and Williams, 2009).Integrated IT increases a company's capacity to create, store, distribute, and use information, at the same time as relational databases make it possible to re-arrange work in time and space ([25] Chapman, 2005; [85] Quattrone and Hopper, 2005). Work that previously needed to be sequential can now be performed in parallel. Data, once entered, are immediately accessible as information all over the company. In this way, work that was formerly highly bound to a specific physical place can now be visualised, virtualised, reconfigured and replaced in a new geographical location ([77] Overby, 2008). Realising all this potential, however, requires combining IT solutions with organisational change(s) ([39] Dedrick et al. , 2003). In addition to adopting a new management philosophy - with a stronger focus on integration, the whole company and the creation of a common global mindset - it is often important to create new organisational routines, rules and roles ([17] Burns and Baldvinsdottir, 2005; [18] Burns and Scapens, 2000; [21] Caglio, 2003). If well designed, these new structural solutions can support and strengthen IT solutions in a number of ways, such as reducing costs and time and improving quality. However, without change, much of the potential of integrated IT will not be realised, and IT investments will result in failure, disappointment and frustration.An important example of the extensive change required - often referred to as transformation - is the creation of a new organisational unit: in this case, a shared services centre (SSC). For staff functions such as finance and accounting (F&A), human resources (HR) and IT, this new support solution is presented as an answer to the existing criticism that such units often lack value-adding capabilities. Often, these supporting units have been seen as a disturbing and costly burden for the operating units. The SSC solution, however, creates an opportunity and the desire to reorganise these often large units and change them from being perceived as passive, reactive and costly bystanders into more embedded and proactive actors within the organisation. This ambition is often expressed in terms of a will to be more of a partner to managers and employees ([44] Granlund and Lukka, 1998; [99] Walther et al. , 1997). With an SSC solution, the pressure and possibilities for generating increased efficiency and effectiveness is high ([48] IBM, 2005). For example, the chief financial officer (CFO) function must spend the same or less in resources, but at the same time be prepared to deliver a broader array of services. The integrating ERP system in an SSC solution is often of vital importance to resolve this problem ([91] Schulman et al. , 1999).Among a large number of international companies working to realise SSC initiatives, the global telecommunications company Ericsson is one of the forerunners. Using one common integrated IT platform (SAP R/3), in just a few years they have successfully created a global network of ten interdependent F&A functions (this claim is supported by the empirical data sources that were collected over two years after the transformation was finished). With this new organisation, Ericsson has managed to transform a situation that was characterised by hundreds of dispersed, independent and locally oriented CFO units and systems, into one common governance structure and one IT system. This paper explores and analyses this successful transformation from fragmentation to standardisation from a managerial point of view.The research objective is to contribute to the understanding of the practice of IT-enabled management control change, in particular how IT-driven change is made possible from a practical perspective in a global context. In doing so, we employ the practice-based perspective ([1] Ahrens and Chapman, 2007; [90] Schatzki et al. , 2001): our focus is on how change is implemented. More specifically, we have organised the paper in accordance to our research questions: when did Ericsson change (Section 4), why did Ericsson change (Section 5), how did they do it (Section 6), and finally, so what (Section 7). Such straightforward issues may seem too simple for research, yet they are vital when the focus of interest is on a new phenomenon such asIT-enabled management control change in a global context ([100] Van De Ven, 2007).2 Theoretical and analytical considerationsGeneral management research, specifically management control research, is dominated by a structural perspective. For example, in management control the main focus is on the control system and less on the creators, users and actors of such a system ([55] Jönsson, 1998). Of course, there are some classic exceptions ([47] Hopwood, 1973; [93] Simon et al. , 1954) but overall, during the last few decades of management control research has been pre-occupied with general abstract structures at the cost of human actors and groups ([28] Chua, 1986; [82] Pihlanto, 2003). In other words, there is a lack of a balanced view in management control research that integrates both actor and structure perspectives.Recently, there has been increased interest in the existence of a duality between structure(s) and actor(s) ([13] Briers and Chua, 2001). An increasing number of researchers have begun to pay attention to the interaction between structures and actors ([29] Coad and Herbert, 2009). An individual (actor) or group of individuals can influence a common structure or system, while the structure or system can simultaneously influence one or many individuals ([43] Englund and Gerdin, 2008). Over time and during a process of creation, an actor's ability to influence the common structure (e.g. routines in a management control system) varies. In the early phase, with less formalised routines, rules and roles (less structure), the actor's opportunities for changing structures are greater. In the later phase, however, actor's ability to change structures is more difficult because of the process of institutionalization (e.g. individual behaviour becomes part of the "the way of doing things" in an organisation ([18] Burns and Scapens, 2000). For example, and as [88] Scapens (2006) illustrates, this means that if the control system is initially more open to design and creation, later on it will be more or less taken for granted among the many users, and therefore more difficult to change.In this context, an SSC is analytically seen as a dynamic structural solution. It is dynamic insofar as a solution today will not be the same as one tomorrow. On the other hand, it will not (and cannot) be completely different as there is often a path dependency in a chosen solution ([38] Dechow and Mouritsen, 2005; [88] Scapens, 2006). This structural dynamism is partly the result of individual and collective knowledge and experience, which can be both a restriction and a resource for the company. One important aspect of such knowledge, as relatedto an SSC solution, is the experience and learning of using an integrating IT system ([65] Markus et al. , 2000). Therefore, IT is an important structural concept for the present study. Traditionally, IT is often black-boxed and seen as a given, static and narrowly defined concept ([3] Barley, 1986; [72] Orlikowski, 1992; [103] Zammuto et al. , 2007). This study, however, applies a broader perspective in which IT includes and is related to a number of organisational solutions. This is what [75] Orlikowski and Iacono (2001) call the ensemble view of technology, which ascribes dynamic and fluid features to the IT artefact that are dependent on time, use and space. With an ensemble view of technology, IT is both a social and a material artefact. It is a socially constructed artefact because the creation of, for example, supporting processes, roles and routines is open to idiosyncratic definitions ([57] Lamb and Kling, 2003). Therefore, every IT implementation initiative can be regarded asopen-ended and unique ([12] Boudreau and Robey, 2005; [81] Piccoli and Ives, 2005). Still, many important aspects of IT are material ([60] Leonardi and Barley, 2008) and thus a chosen IT solution also consists of a number of more general, driving and deterministic aspects. For example, a single company cannot change the technical standard for communication, the internet protocol ([104] Zittrain, 2008). Or, when a financial routine is firmly embedded in the IT system, it is difficult for an individual actor to change it ([33] Costello, 2000). Consequently, IT is seen here as a socio-material phenomenon ([53] Iveroth, 2011; [74] Orlikowski, 2007).The socio-material phenomenon specifically discussed in this paper is an integrated ERP solution, which is of utmost importance for a global company ([23] Campbell-Kelly, 2003; [25] Chapman, 2005; [38] Dechow and Mouritsen, 2005; [45] Granlund an d Malmi, 2002; [92] Sennett, 2006; [102] Véron et al. , 2006). An ERP system is a type of modularised IT system built on a horizontal business logic, which aims to support and strengthen organisational integration and interdependencies among a company's different sub-units ([38] Dechow and Mouritsen, 2005; [83] Pollock and Williams, 2009). With an ERP solution, the previously functional and standalone parts of a system are integrated into a number of modules within a single system. By handling a company's transactional data in one common relational database, it is possible to improve the horizontal flow of information, products and services ([56] Klaus et al. , 2000; [70] O'Leary, 2000). The system creates a more or less frictionless interface of information between different parts of the company, making it easier to move from aggregated to detailed information (drilling down). Ultimately, a modern, integrating ERP system can support both horizontal and vertical transparency and accountability, which are important for management control of a modern company ([67] Mero et al. , 2007).An ERP system has the capacity to manage large amounts of transactional data and can be seen as the backbone of a company's information capabilities. Information can be created, distributed and used throughout the entire organisation. However, since the information is designed and managed within an organisational centre, the system, the organisation and management control can be described as a distributed solution - it is neither centralised nor decentralised, since it has characteristics of both approaches ([11] Boland et al. , 1994). In addition to this transactional system, it is common to use a data warehouse, or some other form of business intelligence (BI) solution. With this complementary IT application, it is possible to create knowledge out of the large amount of data and information stored and managed by the ERP system ([36] Davenport and Harris, 2007).To organisationally match these two types of IT - ERP and BI - it is common to divide accounting work and CFO activities into transactional and analytical work. Transactional work is defined as relatively standardised, less complex, and consisting of frequent work with high volumes. Owing to these characteristics, the work can be standardised, automated, rationalised and centralised, which in turn can lead to increased efficiency.Transactional work is strongly related to the greater use of supporting tools such as computers and integrated systems. Because these tools are designed to support the standardised administrative flow of transactional work, and due to their connection to an information system, maintaining a geographical proximity to the primary operation is no longer necessary. Work can be managed, allocated, and coordinated from a distant geographical place ([91] Schulman et al. , 1999). Typical examples of transactional work in a traditional CFO department include working with a general ledger (bookkeeping), accounts payable (A/P) and accounts receivable (A/R).Analytical work, by contrast, is more bounded and related to a unique situation or place. Interpretations of the situation and the localisation of place - the situated practice - are important here. These interpretations are more dependent on human aspects, such as expertise and engagement in work, and the specific context where analytical work is conducted ([14] Brown and Duguid, 2001). To gain access to explicit and tacit knowledge for better interpretations, but also to create important social relationships, emotional energy, commitment and trust, it is important to work physically close to the real-life situation. An information system, therefore, has limited capacity to fully substitute such a need ([10] Boland et al. , 2001). Typical examples of analytical work are profit analyses of products and customers, and proactive controller work ([61] Lindvall, 2009; [105] Zoni and Mercant, 2007). Analytical work can be enabled by data warehouse technologies and other BI solutions.In sum, this paper is informed by a sociomaterial perspective ([53] Iveroth, 2011; [60] Leonardi and Barley, 2008;[74] Orlikowski, 2007; [103] Zammuto et al. , 2007) that rests upon the notion of duality between structures and actors ([18] Burns and Scapens, 2000; [29] Coad and Herbert, 2009; [43] Englund and Gerdin, 2008). This theoretical lens is applied to the examination of Ericsson's integrated ERP system ([83] Pollock and Williams, 2009; [86] Rom and Rohde, 2007) that enables transactional and analytical work ([35] Davenport, 2005) in their construction of SSCs ([91] Schulman et al. , 1999) that is viewed as a dynamic and organizational solution ([64] Markus, 2004; [94] Simon, 2002). The examination of the transformation is done in order to attain the research objective of contributing to the understanding of the practice of IT-enabled management control change, in particular how IT-driven change is made possible from a practical perspective in a global context. The objective is achieved by addressing the research questions of when (Section 4), why (Section 5), and how (Section 6) Ericsson changed, and finally so what (Section 7). The article answers these questions by taking a process approach to change ([18] Burns and Scapens, 2000; [79] Pettigrew, 1993; [101] Weick and Quinn, 1999). Therefore, Ericsson's transformation programme was framed as an on-going evolutionary process rather than one disruptive revolutionary phenomenon. A more detailed explanation of the process approach and its methods follows in the subsequent section.3 Research methodology3.1 Data gatheringThe empirical data come mainly from documents and interviews. Documents were collected retrospectively between 2004 and 2006, and interviews and document collection took place between March 2006 and June 2009. The formal transformation process began in 2004 and ended in 2006. The broader time span of the data gathering was motivated by an intention to include the interviewees' reflection of the past change process ([78] Pettigrew, 1990).A total of 29 in-depth interviews were conducted with 17 respondents at the SSC offices in Stockholm and Beijing. Each interview was approximately one-and-a-half hours in duration, and was recorded and transcribed,and then analysed and discussed by the research team. The respondents were initially identified by snowball sampling, and later identified in the narratives of the respondents (i.e. actors who were recurrently brought upby the respondents), as well as identified in the documents (i.e. actors who recurred in different forms of documents). The majority of these respondents were seen as significant actors within the transformation process (however, six interviews were done with respondents with lower position). Most held key positions during the entire transformation programme and were experienced individuals in senior positions at Ericsson. Many of them were, in general, positive towards the transformation programme and we did not explicitly try to identify respondents who were negative towards it. This could be seen as a limitation since resistance is often related to change, but the focus here is on how the F&A transformation was managed and successfully carriedit out in practice. In doing so, the paper adds to the recently developed field of positive organisational change ([22] Cameron, 2008). The second source of empirical data consisted of the analysis of documentation (over1,000 pages) including monthly global newsletters, policy documents strategy documents, operational documents, and presentation material for external communication.3.2 Data analysisAmong the different strategies to theorise with a process perspective ([84] Pozzebon and Pinsonneault, 2005; [100] Van De Ven, 2007), the combination of narrative and temporal bracketing was selected ([58] Langley, 1999). The combination was chosen because they correspond with the research questions (e.g. when, why,how and so what), as [84] Pozzebon and Pinsonneault (2005, p. 1367) explain. "Temporal bracketing helps to recognize when and how changes are triggered; narrative strategies help to explain why". The joint answers to when, how (i.e. outcome of temporal bracketing, Sections 4 and 6) and why (i.e. outcome of narrative, Section 5) related questions attains the last research question (i.e. consequences, Section 7).The narrative strategy meant that we constructed a meta-story of the entire transformation process from the empirical data. In doing so, the narrative strategy provided in-depth descriptions that illuminated and clarified individual stories, events, practices and choices in Ericsson's transformation. The narrative strategy was then combined with a broad-ranging temporal bracketing strategy, which is recommended when dealing with large amounts of process data spread across time ([58] Langley, 1999; [84] Pozzebon and Pinsonneault, 2005; [100] Van De Ven, 2007). Temporal bracketing aims to make sense of and structure the empirical data by dividing the temporal change process into different broad-ranging brackets. Every bracket contains a certain continuity of activities and a discontinuity in regards to activities within neighbouring brackets. This enabled us to conduct, as [58] Langley (1999, p. 703) states "the explicit examination of how actions of one period lead to changes in the context that will affect action in subsequent period". More simply put, Ericsson's transformation process wassplit up into brackets that became the unit of analysis for comparison across time (for a similar use of temporal bracketing, see [4] Barrett and Walsham (1999) and [87] Rowe et al. (2008)). The temporal brackets were determined by the orientation of the CFO function at Ericsson over the last decade: a fragmented history (mainly Section 4); a more coordinated national SSC solution (Section 6.1); the transition into regional SSC solutions (Section 6.2); and finally, the existence of a global network of SSCs (Section 6.3; as noted Section 5 is the outcome of the narrative strategy).The validation strategy was threefold. First, the multiple sources of data enabled comparison across time between the transcribed interviews and the different forms of documents. The examination was performed within and across the different sources of data. Second, the whole research process was conducted in a teamof two, which limited the confirmatory bias. Third, there were opportunities to assess the validity of ourunderstanding by holding feedback meetings with the most significant respondents. These occasions involved discussions, validation and elaboration of the similarities and differences that emerged from the empirical data. In general, the research team and the significant actors within the case firm seemed to share a common understanding of the phenomena under investigation.4 When: case study backgroundEricsson was established in 1876 and today is one of the global leaders in the telecommunications industry consisting of 200 legal entities with operations in over 140 countries. The company has been able to maintain this strong market position for many decades despite the considerable changes in technology. These changes can be briefly described as a transition from mechanics to electronics, and from mainly physical products and large systems to software and services ([2] Asgard and Hellgren, 2001). Ericsson has extensive international business experience as they began to expand internationally as early as in the 1890s. Although during the majority of the twentieth century much of its competency and market position is historically due to a close relationship with the previously state-owned Swedish telephone company Televerket (later renamed Telia; [54] Jacobæus, 1976). Throughout most of this century, many of Ericsson's international markets had a similar structure: a nationally oriented market with one or a few large customers, most being state monopolies. The important buying criteria for such customers were less about strictly commercial criteria and more about investments in prestigious projects with high technological performance ([2] Asgard and Hellgren, 2001). Ericsson's competitive advantage in these types of markets has historically been based on its access to superior technology - technologies mainly developed in Sweden and then distributed to different national customers through local subsidiaries ([5] Bartlett and Ghoshal, 1989). Over the last three decades, the global telecommunications market has been characterised by deregulation, privatisations and important shifts in technology ([32] Cortada, 2004). As a result, the quantity and significance of for-profit customers has increased and the rules of competition have changed ([68] Meurling and Jeans, 2000, p. 398).In the 1980s and 1990s, Ericsson evolved from an international company into a multi-national company. One important reason for this, aside from market demands, was the existence of a management ideology that strongly emphasised decentralisation. In essence, it could be said that this management philosophy favoured effectiveness through local market adoption, at the cost of reduced efficiency from economies of scale. From an internal Ericsson perspective, this control philosophy created a large number of strong national entities (market units - MUs) through which the national CEO could manage "their subsidiary" as "their own kingdoms" ([42] Elvander and Elvander, 1995). From a corporate perspective, such a structure creates a lack of transparency, heavy governance structures, and major difficulties in implementing and coordinating change.To increase transparency and strengthen the corporate perspective in a globalising world, a matrix structure was implemented at Ericsson in the early 1990s. This new organisational form was driven by a demand for a structural solution that was capable of managing the intense complexities of a globalised company: a company characterised by operations in many markets, a large portfolio of products and services and a strong management ambition to handle this complexity in a balanced manner. However, due to its multi-dimensional structure and the existence of shared responsibilities, the matrix organisation created additional pressure for congruence among the company's different management control systems. More specifically, and according to the interviewees, Ericsson's management control system was based upon a traditional approach of planning, feedback and control that was initiated from the top and executed according to the formal lines of responsibilities ([76] Otley, 1999). Due to Ericsson's history of fragmented control, there have been recurringproblems with the distribution and feedback of information ([6] Beckérus and Edström, 1995, p. 151). A typical example of this was the lack of formalised follow-up procedures for the guidelines and corporate directives that were sent from its headquarters in Stockholm. As a result, headquarters often had limited knowledge of whether their corporate directives were being implemented or not. As a former CFO for one MU commented "If we thought it [the guideline/directive] was important for our company we followed it, otherwise we just ignored it". Moreover, much of the feedback was time-consuming and infrequent. Information from subsidiaries was sent back to headquarters by post or by fax, and often only on a quarterly basis. Further complicating the management control process was the lack of specific rules (such as a shortage of a common chart of accounts and common models for cost and profitability calculations). According to the respondents, every local company (LC) and MU had more or less their own management control system, customised to their language, local needs and historical standards. Since Ericsson's information platform(s) was (were) also highly heterogeneous, this obstructed important financial communication inside and outside the company.In 2001, Ericsson (as well as their competitors) experienced severe business and financial problems due to the bursting of the internet "bubble" ([96] Strömsten, 2006). After having lost SEK30 billion in 2001, the company began to cut down operations by as much as 50-70 per cent, and dismissed a large number of its employees. It was after this market turmoil that Ericsson finally decided to reorganise their F&A activities into a global network of shared service centres (SSC), which formally began in 2004 and was successfully completed in 2006. While the financial crisis had been a wake-up call, it was still only one trigger among others for this reorganisation. Simultaneous, increasing pressure from global customers, a more demanding financial and capital market, and new technologies such as SAP/R3 created both a need for and the possibility of coordinating Ericsson's F&A function on a global scale. However, there were also more specific reasons behind the transformation, which is the subject of the subsequent section.5 Why change: communicated reasons from Ericsson HQ about the need for a transformation of the CFO functionFrom the beginning of the transformation programme until its successful conclusion a number of motivating arguments for change was communicated in Ericsson, which recurred in the data across time. These arguments centred on the notion of a vision of a global organisation and was grouped into four areas: Cost (Section 5.1), Control (Section 5.2), Consistency (Section 5.3) and Competency (Section 5.4).The four Cs and their respective messages were a recurrent and important part in the extensive, on-going communication between the initiators of the transformation at the corporate level and the employees at the local level. By communicating these motives - through monthly newsletters, numerous face-to-face meetings, group presentations, interactive workshops and conferences with a global orientation - attention to the changes and a common understanding of why change was important spread throughout Ericsson.5.1 CostIn a world with greater competition and higher demands on financial performance from capital market, reducing costs will always be important for management. Nowadays it is always important for a service function to reduce head counts (i.e. to increase efficiency), while it is simultaneously of utmost importance to be able to serve customers well and in a timely manner (i.e. high effectiveness) ([49] IBM, 2008). Such a dual ambition was explained (with an MU perspective) in one of Ericsson's newsletters:Effectiveness relies on us having the right answer at the right time. Remember, the business often wants。