会计英语第三版(叶建芳)翻译

会计英语 第三版

temporary investment

短期投资

lower of cost or market

成本与市价孰低

allowance to reduce temporary investments to markets

短期投资市价下跌准 备

bad debts 坏账

write off 注销

cash in bank 银行存款

receivable 应收款项

prepaid expense 预付费用

payable 应付款项

investment 投资

unearned revenue 预收收入

withdrawal 提存

temporary account 暂时账户

fiscal year 财政年度

calendar year 日历年度

natural business year

自然经营年度

adjustments 账项调整

cash basis 现金制、收付实现制

accrual basis

prepaid items

应计制、权责发生制 预付项目

general journal 普通日记账

posting 过账

accounting cycle 会计循环

trial balance 试算表

adjustment 账项调整

adjusted trial balance

调整后试算表

closing 结账

post-closing trail balance

tangible fixed asset shareholders’ equity

固定资产

股东权益

intangible fixed asset

叶建芳会计英语中文版1-4

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

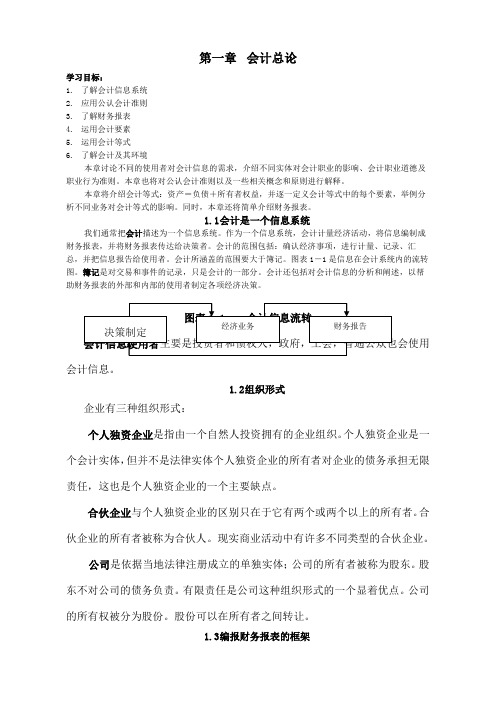

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

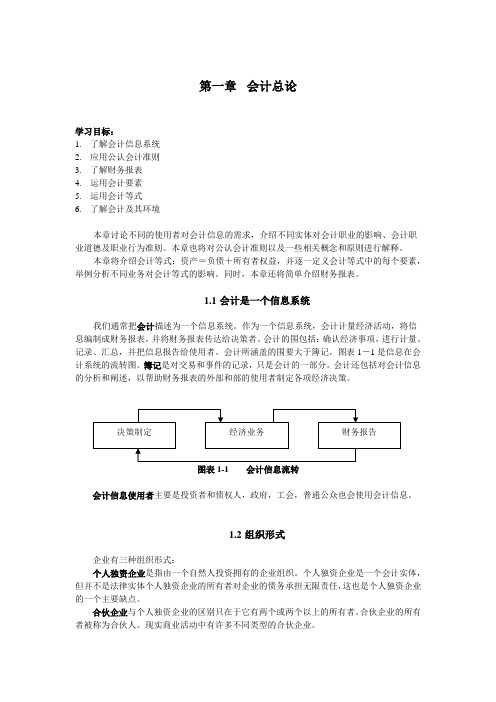

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

叶建芳会计英语中文版

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显着优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

为满足上述需求,国际会计准则委员会(IASC)于1973年成立,并致力于国际公认的会计准则的制定。

会计英语6-10章 中文翻译(叶建芳 孙红星)

制造企业主要包括以下三类存货: 1. 原材料,指企业取得的并将用于生产过程的物品。 2. 在产品,指正在各个生产工序加工的产品。记入在产品的成本包括原材料的成本, 直接人工成本和制造费用。 3. 产成品,指已经完工待售的产品。 在出售时,将产成品的成本确认为销售成本。成本确认的一个大致规则是,工厂内部发 生的成本确认为存货的成本,而工厂外部发生的成本记为销售费用或管理费用。 存货成本包括购买成本以及使存货达到预定可销售状态所发生的一切成本。 合理地计算 存货成本对于企业正确制定其产量, 定价以及战略决策是非常关键的。 生产过程的全部成本 以及使存货达到预定可销售状态的成本都应记入存货成本。与销售相关的成本作为期间费 用。 我们按存货的原始成本记录存货。 存货成本包括为使存货达到目前状态与位置的一切支 出。因此成本包括发票价格,运输费,运输途中保险费,以及其他相关费用。 对于生产制造企业来讲,存货的成本包括原材料成本,生产过程的人工成本,以及其他 相关制造费用。因此资本化的存货成本包括三类不同的存货:原材料,在产品和产成品。 ◇谁拥有存货? 一般地,只有企业拥有存货的法定所有权,才可以将其作为存货列示在资产负债表中。 在离岸价格交货的情况下,在途商品的所有权归买方所有。因为在这种情况下,商品的 所有权已于商品装上运输工具时转移给买方。若采用目的地交货,卖方支付运输费用,并拥 有商品的所有权,当商品抵达目的地后,其所有权才转移给买方。 在委托代销的情况下,商品的所有者(委托人)将商品转给零售商(受托人) 。受托人 为委托人销售商品,但并不享有商品的所有权。 只有在满足以下两个条件时,存货才能被确认: (a)与该存货有关的经济利益很可能流 入企业;(b)该存货的成本能够可靠计量。

6.3 存货成本流转假设

当存货的单位成本一直不变时,确定期末存货的单位成本是很容易的。但现实生活中, 存货的单位成本一直在变。 如果我们可以确定期末存货中每一件存货的取得成本, 那么就可 以很容易地确定期末存货的总成本。 这种确定期末存货成本的方法称为个别认定法。 个别认 定法按存货的实物流转来分配成本。从理论角度,个别认定法较受青睐,尤其是对于单位价 值比较高的单一存货。但若企业存货数量较多时,采用个别认定法,一一认定每件存货的取 得成本会使成本计算任务繁重,费时费力,且核算成本非常高。对于存货数量多,且存货单 价较低的企业一般采用下面三种存货成本流转假设: (注意存货成本流转假设只是出于会计 目的,与存货实物流转无关。 ) 1.平均成本流转假设 按平均成本确定每件存货的成本。这种方法假设所销售的商品 的成本等于平均成本,即每次购入存货的成本的加权平均。 2.先进先出法 假设先购入的存货先发出。先进先出法的假设有一定的道理,因为我 们认为企业都想不断地更新自己的存货,并将最先购入的存货最先售出。通货膨胀时,使用 先进先出法计算出的净利润比其他方法下计算出的高, 因为此时根据先进先出法的假定, 售 出的是最先购入的存货,而在通货膨胀存在的情况下,最先购入的存货的单价较低,所以企 业的销售成本较低。若企业在通货膨胀,物价水平较高时,不断地补充存货,则由此所产生 的高利润一般被成为“存货利润”或“虚假利润” 。在通货紧缩时,使用先进先出法的影响 与上述相反,会使净利润偏低。 3.后进先出法 假设后购入的存货先发出。当物价上涨时,使用后进先出法计算的当 期净利润会比其他方法少。因此在物价上涨时,使用后进先出法是比较稳健的做法。因为近 期购入的存货的成本接近于企业存货的重置成本。 因此, 后进先出法把当期成本与当期收入 很好地进行配比。同时,由于净利润相对偏低,后进先出法还具有减少企业所得税的优点。 在通货紧缩,物价水平下降时,后进先出法的影响与上述相反。在物价水平下降时,使用后

会计英语课后习题答案作者叶建芳会计英语课后习题参考答案

Suggested SolutionChapter 11.3.4.5.(a)(b) net income = 9,260-7,470=1,790(c) net income = 1,790+2,500=4,290Chapter 21.a.To increase Notes Payable -CRb.To decrease Accounts Receivable-CRc.To increase Owner, Capital -CRd.To decrease Unearned Fees -DRe.To decrease Prepaid Insurance -CRf.To decrease Cash - CRg.To increase Utilities Expense -DRh.To increase Fees Earned -CRi.To increase Store Equipment -DRj.To increase Owner, Withdrawal -DR2.a.Cash 1,800Accounts payable ................................................. 1,800 b.Revenue ................................................................. 4,500Accounts receivable ..................................... 4,500c.Owner’s withdrawals............................................... 1,500Salaries Expense ........................................... 1,500 d.Accounts Receivable (750)Revenue (750)3.Prepare adjusting journal entries at December 31, the end of the year.Advertising expense 600Prepaid advertising 600Insurance expense (2160/12*2) 360Prepaid insurance 360Unearned revenue 2,100Service revenue 2,100Consultant expense 900Prepaid consultant 900Unearned revenue 3,000Service revenue 3,000 4.1. $388,4002. $22,5203. $366,6004. $21,8005.1. net loss for the year ended June 30, 2002: $60,0002. DR Jon Nissen, Capital 60,000CR income summary 60,0003. post-closing balance in Jon Nissen, Capital at June 30, 2002: $54,000Chapter 31. Dundee Realty bank reconciliationOctober 31, 2009Reconciled balance $6,220 Reconciled balance $6,2202. April 7 Dr: Notes receivable—A company 5400Cr: Accounts receivable—A company 540012 Dr: Cash 5394.5Interest expense 5.5Cr: Notes receivable 5400June 6 Dr: Accounts receivable—A company 5533Cr: Cash 553318 Dr: Cash 5560.7Cr: Accounts receivable—A company 5533Interest revenue 27.73. (a) As a whole: the ending inventory=685(b) applied separately to each product: the ending inventory=6254. The cost of goods available for sale=ending inventory + the cost of goods=80,000+200,000*500%=80,000+1,000,000=1,080,0005.(1) 24,000+60,000-90,000*0.8=12000(2) (60,000+24,000)/( 85,000+31,000)*( 85,000+31,000-90,000)=18828Chapter 41. (a) second-year depreciation = (114,000 – 5,700) / 5 = 21,660;(b) second-year depreciation = 8,600 * (114,000 – 5,700) / 36,100 = 25,800;(c) first-year depreciation = 114,000 * 40% = 45,600second-year depreciation = (114,000 – 45,600) * 40% = 27,360;(d) second-year depreciation = (114,000 – 5,700) * 4/15 = 28,880.2. (a) weighted-average accumulated expenditures (2008) = 75,000 * 12/12 + 84,000 * 9/12 + 180,000 * 8/12 + 300,000 * 7/12 + 100,000 * 6/12 = 483,000(b) interest capitalized during 2008 = 60,000 * 12% + ( 483,000 –60,000) * 10% =49,5003. (1) depreciation expense = 30,000(2) book value = 600,000 – 30,000 * 2=540,000(3) depreciation expense = ( 600,000 – 30,000 * 8)/16 =22,500(4) book value = 600,000 – 30,000 * 8 – 22,500 = 337,5004. Situation 1:Jan 1st, 2008 Investment in M 260,000Cash 260,000June 30 Cash 6000Dividend revenue 6000Situation 2:January 1, 2008 Investment in S 81,000Cash 81,000June 15 Cash 10,800Investment in S 10,800December 31 Investment in S 25,500Investment Revenue 25,5005. a. December 31, 2008 Investment in K 1,200,000Cash 1,200,000June 30, 2009 Dividend Receivable 42,500Dividend Revenue 42,500December 31, 2009 Cash 42,500Dividend Receivable 42,500b. December 31, 2008 Investment in K 1,200,000Cash 1,200,000 December 31, 2009 Cash 42,500Investment in K 42,500Investment in K 146,000Investment revenue 146,000 c. In a, the investment amount is 1,200,000net income reposed is 42,500In b, the investment amount is 1,303,500Net income reposed is 146,000Chapter 51.a. June 1: Dr: Inventory 198,000Cr: Accounts Payable 198,000 June 11: Dr: Accounts Payable 198,000Cr: Notes Payable 198,000 June 12: Dr: Cash 300,000Cr: Notes Payable 300,000b. Dr: Interest Expenses (for notes on June 11) 12,100Cr: Interest Payable 12,100Dr: Interest Expenses (for notes on June 12) 8,175Cr: Interest Payable 8,175c. Balance sheet presentation:Notes Payable 498,000 Accrued Interest on Notes Payable 20,275d. For Green:Dr: Notes Payable 198,000 Interest Payable 12,100Interest Expense 7,700Cr: Cash 217,800For Western:Dr: Notes Payable 300,000Interest Payable 8,175Interest Expense 18,825Cr: Cash 327,0002.(1) 20⨯8 Deferred income tax is a liability 2,400Income tax payable 21,600 20⨯9 Deferred income tax is an asset 600Income tax payable 26,100(2) 20⨯8: Dr: Tax expense 24,000Cr: Income tax payable 21,600 Deferred income tax 2,400 20⨯9: Dr: Tax expense 25,500Deferred income tax 600Cr: Income tax payable 26,100 (3) 20⨯8: Income statement: tax expense 24,000Balance sheet: income tax payable 21,600 20⨯9: Income statement: tax expense 25,500 Balance sheet: income tax payable 26,1003.a. 1,560,000 (20000000*12 %* (1-35%))b. 7.8% (20000000*12 %* (1-35%)/20000000)5.Notes Payable 14,400 Interest Payable 1,296 Accounts Payable 60,000 +Unearned Rent Revenue 7,200 Current Liabilities 82,896Chapter 61. Mar. 1Cash 1,200,000Common Stock 1,000,000Paid-in Capital in Excess of Par Value 200,000Mar. 15Organization Expense 50,000Common Stock 50,000Mar. 23Patent 120,000Common Stock 100,000Paid-in Capital in Excess of Par Value 20,000The value of the patent is not easily determinable, so use the issue price of $12 per share on March 1 which is the issuing price of common stock.2. July.1Treasury Stock 180,000Cash 180,000The cost of treasury purchased is 180,000/30,000=60 per share.Nov. 1Cash 70,000Treasury Stock 60,000Paid-in Capital from Treasury Stock 10,000Sell the treasury at the cost of $60 per share, and selling price is $70 per share. The treasury stock is sold above the cost.Dec. 20Cash 75,000Paid-in Capital from Treasury Stock 15,000Treasury Stock 90,000The cost of treasury is $60 per share while the selling price is $50 which is lower than the cost.3. a. July 1Retained Earnings 24,000Dividends Payable—Preferred Stock 24,000b.Sept.1Dividends Payable—Preferred Stock 24,000Cash 24,000c. Dec.1Retained Earnings 80,000Dividends Payable—Common Stock 80,000d. Dec.31Income Summary 350,000Retained Earnings 350,0004.a. Preferred stock gives its owner certain advantages over common stockholders. These benefits include the right to receive dividends before the common stockholders and the right to receive assets before the common stockholders if the corporation liquidates. Corporation pay a fixed amount of dividends on preferred stock.The 7% cumulative term indicates that the investors earn 7% fixed dividends.b. 7%*120%*20,000=504,000c. If corporation issued debt, it has obligation to repay principald. The date of declaration decrease the stockholders’ equity; the date of record and the date of payment have no effect on stockholders.5.a. Jan. 15Retained Earnings 35,000Accumulated Depreciation 35,000To correct error in prior year’s depreciation.b. Mar. 20Loss from Earthquake 70,000Building 70,000c. Mar. 31Retained Earnings 12,500Dividends Payable 12,500d. Apirl.15Dividends Payable 12,500Cash 12,500e. June 30Retained Earnings 37,500Common Stock 25,000Additional Paid-in Capital 12,500To record issuance of 10% stock dividend: 10%*25,000=2,500 shares;2500*$15=$37,500f. Dec. 31Depreciation Expense 14,000Accumulated Depreciation 14,000Original depreciation: $40,000/40=$10,000 per year. Book value on Jan.1, 2009 is $350,000(=$400,000-5*$10,000). Deprecation for 2009 is $14,000(=$350,000/25).g. The company does not need to make entry in the accounting records. But the amount of Common Stock ($10 par value) decreases 275,000, while the amount of Common Stock ($5 par value) increases 275,000.Chapter 71.Requirement 1If revenue is recognized at the date of delivery, the following journal entries would be used to record the transactions for the two years:Year 1Inventory .................................................................................... 480,000 Cash/Accounts payable ........................................................ 480,000 To record purchase of inventoryInventory .................................................................................... 124,000 Cash/Accounts payable ........................................................ 124,000 To record refurbishment of inventoryAccounts receivable ................................................................... 310,000 Sales revenue ...................................................................... 310,000 To record sale of goods on accountCost of goods sold...................................................................... 220,000 Inventory .............................................................................. 220,000 To record the cost of the goods sold as an expenseSales returns (I/S) ...................................................................... 15,500* Allowance for sales returns (B/S).......................................... 15,500 To record provision for return of goods sold under 30-day return period* 5% of $310,000Warranty expense ...................................................................... 31,000* Provision for warranties (B/S) ............................................... 31,000 To record provision, at time of sale, for warranty expenditures* 10% of $310,000Allowance for sales returns......................................................... 12,400 Accounts receivable ............................................................. 12,400 To record return of goods within 30-day return period.It is assumed the returned goods have no value and are disposed of.Provision for warranties (B/S) ..................................................... 18,600 Cash/Accounts payable ........................................................ 18,600 To record expenditures in year 1 for warranty workCash .......................................................................................... 297,600*Accounts receivable ............................................................. 297,600 To record collection of Accounts Receivable* $310,000 – $12,400Year 2Provision for warranties (B/S) ..................................................... 8,400 Cash/Accounts payable ........................................................ 8,400 To record expenditures in year 2 for warranty workRequirement 2If revenue is recognized only when the warranty period has expired, the following journal entries would be used to record the transactions for the two years:Year 1Inventory .................................................................................... 480,000 Cash/Accounts payable ........................................................ 480,000 To record purchase of inventoryInventory .................................................................................... 124,000 Cash/Accounts payable ........................................................ 124,000 To record refurbishment of inventoryAccounts receivable ................................................................... 310,000 Inventory .............................................................................. 220,000 Deferred gross margin .......................................................... 90,000 To record sale of goods on accountDeferred gross margin ................................................................ 12,400 Accounts receivable ............................................................. 12,400 To record return of goods within the 30-day return period. It is assumed the goods haveno value and are disposed of.Deferred warranty costs (B/S)..................................................... 18,600 Cash/Accounts payable ........................................................ 18,600 To record expenditures for warranty work in year 1. The warranty costs incurred are deferred because the related revenue has not yet been recognizedCash .......................................................................................... 297,600* Accounts receivable ............................................................. 297,600 To record collection of Accounts receivable* $310,000 – $12,400Year 2Deferred warranty costs ............................................................. 8,400 Cash/Accounts payable ........................................................ 8,400 To record warranty costs incurred in year 2 related to year 1 sales. The warranty costs incurred are deferred because the related revenue has not yet been recognized.Deferred gross margin ................................................................ **77,600Cost of goods sold...................................................................... 220,000 Sales revenue ...................................................................... 297,600* To record recognition of sales revenue from year 1 sales and related cost of goods sold at expiry of warranty period* $310,000 – $12,400** ($90,000 – $12,400)Warranty expense ...................................................................... 27,000* Deferred warranty costs ....................................................... 27,000 To record recognition of warranty expense at same time as related sales revenue recognition* $18,600 + $8,400Requirement 3Allied Auto Parts Inc. might choose to recognize revenue only after the warranty periodhas expired if they are not able to make a good estimate, at the time of sale, of the amount of warranty work that will be required under the terms of the one-year warranty. If Allied is not able, at the time of sale, to make a good estimate of the warranty work that will be required, then the measurability criterion of revenue recognition is not met at the time of sale. The measurability criterion means that the amount of revenue can be reliably measured. If the seller is not able to estimate the amount of work that will have to be done under the warranty agreement, then it is not able to reasonably measure the profit that it will eventually earn on the sales. The performance criteria might also be invoked here.The performance criterion means that the seller has transferred the significant risks and rewards of ownership to the buyer. As long as there is warranty work to be performed after the sale that is the responsibility of the seller, you might argue that performance is not substantially complete. However, if the seller was able to reliably estimate the amount of warranty work, then performance would be satisfied on the assumption that we could measure the risk that remains with the seller, and make a provision for it.2.Percentage-of-completion method:The first step in applying revenue recognition using the percentage-of-completion method (using costs incurred to date compared to estimated total costs to determine the percentage of completion) is to estimate the percentage of completion of the project at the end of each year. This is done in the following table (in $000s):End of 2005 End of 2006 End of 2007Total costs incurred $ 5,400 $ 12,950 $ 18,800 Total estimated costs 18,000 18,500 18,800 % completed 30% 70% 100%Once the percentage of completion at the end of each year has been calculated as above, the next step is to allocate the appropriate amount of revenue to each year, based on the percentage completed to date, less what has previously been recorded in revenue. This is done in the following table (in $000s):2005 2006 20072005 $20,000 × 30% $ 6,0002006 $20,000 × 70% $ 14,0002007 $20,000 × 100% $ 20,000 Less: Revenue recognized in prior years (0) (6,000) (14,000) Revenue for year $ 6,000 $ 8,000 $ 6,000Therefore, the profit to be recognized each year on the construction project would be:2005 2006 2007 TotalRevenue recognized $ 6,000 $ 8,000 $ 6,000 $ 20,000 Construction costs incurred (expenses) (5,400) (7,550) (5,850) (18,800) Gross profit for the year $ 600 $ 450 $ 150 $ 1,200The following journal entries are used to record the transactions under thepercentage-of-completion method of revenue recognition:2005 2006 20071. Costs of construction:Construction in progress................. 5,400 7,550 5,850 Cash, payables, etc. ..... 5,400 7,550 5,850 2. Progress billings:Accounts receivable ........... 3,100 4,900 12,000 Progress billings ........... 3,100 4,900 12,000 3. Collections on billings:Cash .................................. 2,400 4,000 12,400 Accounts receivable ..... 2,400 4,000 12,400 4. Recognition of profit:Construction in progress..... 600 450 150Construction expense ......... 5,400 7,550 5,850 Revenue from long-termcontract..................... 6,000 8,000 6,000 5. To close construction in progress:Progress billings ................. 20,000 Construction in progress 20,0002005 2006 2007Balance sheetCurrent assets:Accounts receivable $ 700 $ 1,600 $ 1,200 Inventory:Construction in process 6,000 14,000 Less: Progress billings (3,100) (8,000)Costs in excess of billings 2,900 6,000Income statementRevenue from long-term contracts $ 6,000 $ 8,000 $ 6,000 Construction expense (5,400) (7,550) (5,850) Gross profit $ 600 $ 450 $ 1503.a. The three criteria of revenue recognition are performance, measurability, andcollectibility.Performance means that the seller or service provider has performed the work.Depending on the nature of the product or service, performance may mean quitedifferent points of revenue recognition. For example, for the sale of products, IAS18 defines performance as the point when the seller of the goods has transferred therisks and rewards of ownership to the buyer. Normally, this means that performance is done at the time of sale. Although the seller may have performed much of the work prior to the sale (production, selling efforts, etc.), there is still significant risk to theseller that a buyer may not be found. Therefore, from a reliability point of view,revenue recognition is delayed until the point of sale. Also, there may be significant risks remaining with the seller of the product even after the sale. Warranties given by the seller are a risk that remains with the seller. However, if this risk can be reliably estimated at the time of sale, revenue can be recognized at the point of sale.Performance is quite different under a long-term construction contract. Here,performance really is considered to be a measure of the work done. Revenue isrecognized over the production period as the work is performed. It is intended toreflect the amount of effort expended by the seller (contractor). Although legal titlewon’t transfer to the buyer until the project is completed, revenue can be recognized because there is a known and committed buyer. If the contractor is not able toestimate how much of the work has been done (perhaps because he or she can’treliably estimate how much work must still be done), then profit would not berecognized until the extent of performance is known.Measurability means that the seller or service provider must be able to reliablyestimate the amount of the revenue from the sale or service. For the sale of products this is generally known at the time of sale (the sales price is set). However, if the seller provides a return period, it may be necessary to estimate the volume of returns at the time of sale in order to measure the revenue that will be recognized.Collectibility means that the seller or the service provider has reasonable assurance that the sales price will actually be collected. In most cases for the sales of products, the seller is able to recognize revenue at the time of sale even if the sale is on account.This is because the seller has experience with its customers and is able to estimate reliably the risk of non payment. As long as the seller is able to make this estimate, it is appropriate to recognize the revenue but to offset it with a provision for possible non collection. If the seller is unable to make reliable estimates of future collection ofamounts owing, the recognition of revenue would be delayed until the cash is actually received. This is what is done using the instalment sales method of revenuerecognition.b. Because of the performance criterion of revenue recognition, it would seem to bemost appropriate to recognize most revenue as the seller or service provider per forms the work. This would be the best measure of performance. This would mean, for example,that sellers of products would recognize their revenue over the whole production, selling, and post sales servicing periods. As we saw above, this is not commonly done because,in many cases, there are still significant risks that are retained by the seller (risk of not being able to sell the product, for example). There are also measurement risks (knowingthe selling price) that exist prior to the sale. The percentage-of-completion method of revenue used for some long-term construction contracts would seem to most closely recognize revenue as the work is performed. As mentioned in Part 1, we are able to recognize revenue on this basis since a contract exists which commits the purchaser tobuy the project (assuming certain conditions are met) and the sales price is known because of the existence of the contract.4.If all revenue is recognized when a student registers for the course, profit for 2007 would be:Sales Revenue1:Manuals and initial lessons (200 × $100) $ 20,000 Additional lessons ((200 × 8) × $30) 48,000 Examinations ((200 × 80%) × $130) 20,800 Total sales revenue 88,800Cost of sales:Manuals and initial lessons (200 × ($15 + $3)) 3,600 Additional lessons ((200 × 8) × $3)) 4,800Examinations ((200 × 80%) × $30) 4,800 Total cost of sales 13,200Depreciation of development costs:$180,000 × (200/1,000) 36,000Profit $ 39,6005.FINISH ENTERPRISESIncome Statementfor the year ending December 31, 2005Continuing operations (excluding the chemical division)Sales ($35,000,000 – $5,500,000) $ 29,500,000Cost of sales ($15,000,000 – $2,800,000) (12,200,000)Gross profit 17,300,000Selling & administration expenses($18,000,000 – $3,200,000) (14,800,000)Profit from operations 2,500,000Income tax expense (40%) 1,000,000Profit after tax $ 1,500,000Discontinuing operations (Chemical division)Sales 5,500,000Cost of sales (2,800,000)Gross profit 2,700,000Selling & administration expenses (3,200,000)Loss from operations (500,000)Income tax expense(40%) 200,000Loss after tax (300,000) Gain on discontinuance of the Chemical division 3,500,000Tax thereon (1,400,000)After-tax gain on discontinuance of the Chemical division 2,100,000 Enterprise net profit $ 3,300,000Chapter 81.Payment of account payable. operatingIssuance of preferred stock for cash. financingPayment of cash dividend. financingSale of long-term investment. investingAmortization of bond discount. no effectCollection of account receivable. operatingIssuance of long-term note payable to borrow cash. financing Depreciation of equipment. no effectPurchase of treasury stock. financingIssuance of common stock for cash. financingPurchase of long-term investment. investingPayment of wages to employees. operatingCollection of cash interest. investingCash sale of land. InvestingDistribution of stock dividend. no effectAcquisition of equipment by issuance of note payable. no effect Payment of long-term debt. financingAcquisition of building by issuance of common stock. no effect Accrual of salary expense. no effect2.(a) Cash received from customers = 816,000(b) Cash payments for purchases of merchandise. =468,000(c) Cash payments for operating expenses. = 268,200(d) Income taxes paid. =36,9003.Cash sales …………………………………………... $9,000 Payment of accounts payable ……………………….-48,000 Payment of income tax ………………………………-13,000 Payment of interest ……………………………..…..-16,000 Collection of accounts receivable ……………………93,000 Payment of salaries and wages ……………………….. -34,000 Cash flows from operating activitiesby the direct method -9,0004.Operating activities:Net loss -200,000 Add: loss on sale of land 250,000 Add: depreciation 300,000Add: amortization of patents 20,000Less: increases in current assets other than cash -750,000Add: increases in current liabilities 180,000Net cash flows from operating -200,000Investing activitiesSale of land -50,000Purchase of PPE -1,500,000Net cash flows from investing -1,550,000Financing activitiesIssuance of common shares 400,000Payment of cash dividend -50,000Issuance of non-current liabilities 1,000,000Net cash flows from financing 1,350,000 Net changes in cash -400,000 5.。

叶建芳会计英语中文版

由于各个国家的法律和经济环境不同,各国有不同的会计模式。在一个国家可行的会计实务在另一个国家并不一定可行。由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

为满足上述需求,国际会计准则委员会(IASC)于1973年成立,并致力于国际公认的会计准则的制定。2001年4月1日,根据题为《关于重塑国际会计准则委员会未来的建议》的报告中的提议,国际会计准则委员会(IASC)改组为国际会计准则理事会(IASB)。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。合伙企业的所有者被称为合伙人。现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。股东不对公司的债务负责。有限责任是公司这种组织形式的一个显著优点。公司的所有权被分为股份。股份可以在所有者之间转让。

个人独资企业编制的四种财务报表有:

-利润表(又称为损益表);

-所有者权益变动表(又称为资本变动表,以及以后章节介绍的留存收益表);

-资产负债表;

-现金流量表。

◇资产负债表(财务状况报告)

资产负债表反映一个企业在某一特定日期的所有资产,负债和所有者权益。资产负债表中资产等于负债加所有者权益。

IASB框架对资产的定义如下:

除了1989年发布的国际会计准则外,国际会计准则委员会还发布了财务报表编报的框架,并将其作为建立会计准则的概念基础。

框架主要包括以下内容:

1.财务报表的目的及基础假设;

2.ﻩ财务报表的质量特征;

3.ﻩ财务报表的要素;

4.资本和资本保全概念。

图表1-2概括地介绍了一些重要的会计原则。

图表1-2

会计英语(第三版)

Chapter 6

specific identification method

个别认定法

first-in, first-out method

(FIFO)

last-in, first-out method

(LIFO) 后进先出法

replacement costs 重置成本

复式记账

American Institute of Certified Public Accountants

(AICPA)

Chinese Institute of Certified Public Accountants

(CICPA)

中国注册会计师协 会

Managerial accounting

留存收益

流动性

Chapter 4

service enterprise wholesales

服务企业

批发商

merchandising enterprise

商品流通企业

retailers 零售商

sales revenue 销售收入

gross profit 毛利

cost of good sold 销售成本

bookkeeping procedures

账务处理程序

summarized vouchers

汇总记账凭证

categorized accounts summary

科目汇总表

columnar journal 多栏式日记账

Advance from customers

预收账款

unearned revenue

Cash flow statement

现金流量表

Asset 资产

会计英语

Accounting English

6

International financial reporting standards & GAAP

Accounting concepts and principles include:

business entity (会计主体) time period (会计分期) going-concern (持续经营) monetary unit (货币计量) objectivity principle (客观性原则) cost principle (成本原则) revenue recognition or realization principle (收入确 认原则) materiality principle(重要性原则) matching principle (匹配原则) consistency principle (一致性原则) conservatism principle (稳健性原则) full-disclosure principle (充分披露原则)

Accounting English

17

2. Purchased equipment for $5,000 cash. Liabilities Assets Accounts Accounts + Receivable + Equipment = Payable +5,000 Stockholders’ Equity

Accounting English

8

The balance sheet

details assets, liabilities, and equity A specific date of the business entity Two columns The definition of an asset : tangible and intangible Sources of assets The definition of liability: present obligation, outflow of economic benefits Definition of equity : residual amount. Assetsliabilities

叶建芳会计英语中文版1-5

学习目标:1.2.3.编制多步式利润表4.5.编制特种日记账6.本章购货折扣和运输成本。

◇服务企业◇商品流通企业批发商和零售商是商品还会因商品存货的购买和销售而存在其他会计问题。

销售商品带来的收益叫销售收入,为出售而购买和准备商品存货的费用叫做销售成本。

在商品流通活动中使用的两个常见的等式是:净销售收入-销售成本=毛利毛利-经营费用=净利润(或净损失)商品存货是商品流通企业在正常商业过程中为出售而持有的货物。

◇定期盘存制和永续盘存制定期盘存制只在存货(通常年末)盘点时提供存货和销售成本数据。

永续盘存制持续地,不断更新存货和销售成本数据。

因此,定期盘存制和永续盘存制的区别在于如何记录商品存货的采购和销售。

比如定期盘存制使用一个暂时账户---采购账户记录购买商品的成本。

在定期盘存制下,企业根据对存货的盘点确定销售成本和和期末存货成本,进而编制财务报表。

永续盘存制企业在每次采购和商品销售时都及时更新销售成本和商品存货记录。

以前,销售量大且商品单价较低的企业多采用定期盘存制。

随着科技发展,目前这些企业也多采用永续盘存制。

实际盘点也必须在一个永续的制度下完成来使实际手头商品数目与会计记录的余额相一致。

4.2 采购、销售收入和销售成本◇商品采购——永续盘存制在永续盘存制下,所有的商品存货的赊购都要在购买时借记入商品存货账户中,例如:商品存货 xxx应付账款 xxx注意购货净额和总购买额不同。

要计算购货净额,我们需要用总采购额减去供应商提供的购货折扣,购货退回以及对供货商提供的不满意的商品的购货折让。

◇购货退回和折让在日记账中对购货退回和折让的处理如下:应付账款 xxx 商品存货 xxx◇商业折扣商业折扣是买卖双方在确定商品销售价格的谈判中达成的对价目表中所列价格的减让。

实际价格(发票价格)是用价目表中的价格减去商业折扣后得到的。

价目表中的原价和商业折扣均不出现在购销双方的账簿上,以发票价格记录交易。

商业折扣的使用使批发商和零售商节省了频繁更改价目表的成本。

会计英语 课后习题答案 作者 叶建芳 会计英语课后习题参考答案

Suggested SolutionChapter 13.4.5.(b) net income = 9,260-7,470=1,790(c) net income = 1,790+2,500=4,290Chapter 21.a.To increase Notes Payable -CRb.To decrease Accounts Receivable-CRc.To increase Owner, Capital -CRd.To decrease Unearned Fees -DRe.To decrease Prepaid Insurance -CRf.To decrease Cash - CRg.To increase Utilities Expense -DRh.To increase Fees Earned -CRi.To increase Store Equipment -DRj.To increase Owner, Withdrawal -DR2.a.Cash 1,800Accounts payable ................................................... 1,800 b.Revenue ................................................................... 4,500Accounts receivable ...................................... 4,500c.Owner’s withdrawals ................................................ 1,500Salaries Expense ............................................ 1,500 d.Accounts Receivable (750)Revenue (750)3.Prepare adjusting journal entries at December 31, the end of the year.Advertising expense 600Prepaid advertising 600Insurance expense (2160/12*2) 360Prepaid insurance 360Unearned revenue 2,100Service revenue 2,100Consultant expense 900Prepaid consultant 900Unearned revenue 3,000Service revenue 3,000 4.1. $388,4002. $22,5203. $366,6004. $21,8005.1. net loss for the year ended June 30, 2002: $60,0002. DR Jon Nissen, Capital 60,000CR income summary 60,0003. post-closing balance in Jon Nissen, Capital at June 30, 2002: $54,000Chapter 31. Dundee Realty bank reconciliationOctober 31, 2009Reconciled balance $6,220 Reconciled balance $6,2202. April 7 Dr: Notes receivable—A company 5400Cr: Accounts receivable—A company 540012 Dr: Cash 5394.5Interest expense 5.5Cr: Notes receivable 5400June 6 Dr: Accounts receivable—A company 5533Cr: Cash 553318 Dr: Cash 5560.7Cr: Accounts receivable—A company 5533Interest revenue 27.73. (a) As a whole: the ending inventory=685(b) applied separately to each product: the ending inventory=6254. The cost of goods available for sale=ending inventory + the cost of goods=80,000+200,000*500%=80,000+1,000,000=1,080,0005.(1) 24,000+60,000-90,000*0.8=12000(2) (60,000+24,000)/( 85,000+31,000)*( 85,000+31,000-90,000)=18828Chapter 41. (a) second-year depreciation = (114,000 – 5,700) / 5 = 21,660;(b) second-year depreciation = 8,600 * (114,000 – 5,700) / 36,100 = 25,800;(c) first-year depreciation = 114,000 * 40% = 45,600second-year depreciation = (114,000 – 45,600) * 40% = 27,360;(d) second-year depreciation = (114,000 – 5,700) * 4/15 = 28,880.2. (a) weighted-average accumulated expenditures (2008) = 75,000 * 12/12 + 84,000 * 9/12 + 180,000 * 8/12 + 300,000 * 7/12 + 100,000 * 6/12 = 483,000(b) interest capitalized during 2008 = 60,000 * 12% + ( 483,000 –60,000) * 10% =49,5003. (1) depreciation expense = 30,000(2) book value = 600,000 – 30,000 * 2=540,000(3) depreciation expense = ( 600,000 – 30,000 * 8)/16 =22,500(4) book value = 600,000 – 30,000 * 8 – 22,500 = 337,5004. Situation 1:Jan 1st, 2008 Investment in M 260,000Cash 260,000June 30 Cash 6000Dividend revenue 6000Situation 2:January 1, 2008 Investment in S 81,000Cash 81,000June 15 Cash 10,800Investment in S 10,800December 31 Investment in S 25,500Investment Revenue 25,5005. a. December 31, 2008 Investment in K 1,200,000Cash 1,200,000June 30, 2009 Dividend Receivable 42,500Dividend Revenue 42,500December 31, 2009 Cash 42,500Dividend Receivable 42,500b. December 31, 2008 Investment in K 1,200,000Cash 1,200,000 December 31, 2009 Cash 42,500Investment in K 42,500Investment in K 146,000Investment revenue 146,000 c. In a, the investment amount is 1,200,000net income reposed is 42,500In b, the investment amount is 1,303,500Net income reposed is 146,000Chapter 51.a. June 1: Dr: Inventory 198,000Cr: Accounts Payable 198,000 June 11: Dr: Accounts Payable 198,000Cr: Notes Payable 198,000 June 12: Dr: Cash 300,000Cr: Notes Payable 300,000b. Dr: Interest Expenses (for notes on June 11) 12,100Cr: Interest Payable 12,100Dr: Interest Expenses (for notes on June 12) 8,175Cr: Interest Payable 8,175c. Balance sheet presentation:Notes Payable 498,000 Accrued Interest on Notes Payable 20,275d. For Green:Dr: Notes Payable 198,000 Interest Payable 12,100Interest Expense 7,700Cr: Cash 217,800For Western:Dr: Notes Payable 300,000Interest Payable 8,175Interest Expense 18,825Cr: Cash 327,0002.(1) 20⨯8 Deferred income tax is a liability 2,400Income tax payable 21,600 20⨯9 Deferred income tax is an asset 600Income tax payable 26,100(2) 20⨯8: Dr: Tax expense 24,000Cr: Income tax payable 21,600 Deferred income tax 2,400 20⨯9: Dr: Tax expense 25,500Deferred income tax 600Cr: Income tax payable 26,100 (3) 20⨯8: Income statement: tax expense 24,000Balance sheet: income tax payable 21,600 20⨯9: Income statement: tax expense 25,500 Balance sheet: income tax payable 26,1003.a. 1,560,000 (20000000*12 %* (1-35%))b. 7.8% (20000000*12 %* (1-35%)/20000000)5.Notes Payable 14,400 Interest Payable 1,296 Accounts Payable 60,000 +Unearned Rent Revenue 7,200 Current Liabilities 82,896Chapter 61. Mar. 1Cash 1,200,000Common Stock 1,000,000Paid-in Capital in Excess of Par Value 200,000Mar. 15Organization Expense 50,000Common Stock 50,000Mar. 23Patent 120,000Common Stock 100,000Paid-in Capital in Excess of Par Value 20,000The value of the patent is not easily determinable, so use the issue price of $12 per share on March 1 which is the issuing price of common stock.2. July.1Treasury Stock 180,000Cash 180,000The cost of treasury purchased is 180,000/30,000=60 per share.Nov. 1Cash 70,000Treasury Stock 60,000Paid-in Capital from Treasury Stock 10,000Sell the treasury at the cost of $60 per share, and selling price is $70 per share. The treasury stock is sold above the cost.Dec. 20Cash 75,000Paid-in Capital from Treasury Stock 15,000Treasury Stock 90,000The cost of treasury is $60 per share while the selling price is $50 which is lower than the cost.3. a. July 1Retained Earnings 24,000Dividends Payable—Preferred Stock 24,000b.Sept.1Dividends Payable—Preferred Stock 24,000Cash 24,000c. Dec.1Retained Earnings 80,000Dividends Payable—Common Stock 80,000d. Dec.31Income Summary 350,000Retained Earnings 350,0004.a. Preferred stock gives its owner certain advantages over common stockholders. These benefits include the right to receive dividends before the common stockholders and the right to receive assets before the common stockholders if the corporation liquidates. Corporation pay a fixed amount of dividends on preferred stock.The 7% cumulative term indicates that the investors earn 7% fixed dividends.b. 7%*120%*20,000=504,000c. If corporation issued debt, it has obligation to repay principald. The date of declaration decrease the stockholders’ equity; the date of record and the date of payment have no effect on stockholders.5.a. Jan. 15Retained Earnings 35,000Accumulated Depreciation 35,000To correct error in prior year’s depreciation.b. Mar. 20Loss from Earthquake 70,000Building 70,000c. Mar. 31Retained Earnings 12,500Dividends Payable 12,500d. Apirl.15Dividends Payable 12,500Cash 12,500e. June 30Retained Earnings 37,500Common Stock 25,000Additional Paid-in Capital 12,500To record issuance of 10% stock dividend: 10%*25,000=2,500 shares;2500*$15=$37,500f. Dec. 31Depreciation Expense 14,000Accumulated Depreciation 14,000Original depreciation: $40,000/40=$10,000 per year. Book value on Jan.1, 2009 is $350,000(=$400,000-5*$10,000). Deprecation for 2009 is $14,000(=$350,000/25).g. The company does not need to make entry in the accounting records. But the amount of Common Stock ($10 par value) decreases 275,000, while the amount of Common Stock ($5 par value) increases 275,000.Chapter 71.Requirement 1If revenue is recognized at the date of delivery, the following journal entries would be used to record the transactions for the two years:Year 1Inventory ....................................................................................... 480,000 Cash/Accounts payable .......................................................... 480,000 To record purchase of inventoryInventory ....................................................................................... 124,000 Cash/Accounts payable .......................................................... 124,000 To record refurbishment of inventoryAccounts receivable ...................................................................... 310,000 Sales revenue ......................................................................... 310,000 To record sale of goods on accountCost of goods sold ........................................................................ 220,000 Inventory ................................................................................. 220,000 To record the cost of the goods sold as an expenseSales returns (I/S) ......................................................................... 15,500* Allowance for sales returns (B/S) ........................................... 15,500 To record provision for return of goods sold under 30-day return period* 5% of $310,000Warranty expense ......................................................................... 31,000* Provision for warranties (B/S) ................................................. 31,000 To record provision, at time of sale, for warranty expenditures* 10% of $310,000Allowance for sales returns .......................................................... 12,400 Accounts receivable ............................................................... 12,400 To record return of goods within 30-day return period.It is assumed the returned goods have no value and are disposed of.Provision for warranties (B/S) ....................................................... 18,600 Cash/Accounts payable .......................................................... 18,600 To record expenditures in year 1 for warranty workCash .............................................................................................. 297,600*Accounts receivable ............................................................... 297,600 To record collection of Accounts Receivable* $310,000 – $12,400Year 2Provision for warranties (B/S) ....................................................... 8,400 Cash/Accounts payable .......................................................... 8,400 To record expenditures in year 2 for warranty workRequirement 2If revenue is recognized only when the warranty period has expired, the following journal entries would be used to record the transactions for the two years:Year 1Inventory ....................................................................................... 480,000 Cash/Accounts payable .......................................................... 480,000 To record purchase of inventoryInventory ....................................................................................... 124,000 Cash/Accounts payable .......................................................... 124,000 To record refurbishment of inventoryAccounts receivable ...................................................................... 310,000 Inventory ................................................................................. 220,000 Deferred gross margin ............................................................ 90,000 To record sale of goods on accountDeferred gross margin .................................................................. 12,400 Accounts receivable ............................................................... 12,400 To record return of goods within the 30-day return period. It is assumed the goods haveno value and are disposed of.Deferred warranty costs (B/S) ...................................................... 18,600 Cash/Accounts payable .......................................................... 18,600 To record expenditures for warranty work in year 1. The warranty costs incurred are deferred because the related revenue has not yet been recognizedCash .............................................................................................. 297,600* Accounts receivable ............................................................... 297,600 To record collection of Accounts receivable* $310,000 – $12,400Year 2Deferred warranty costs ................................................................ 8,400 Cash/Accounts payable .......................................................... 8,400 To record warranty costs incurred in year 2 related to year 1 sales. The warranty costs incurred are deferred because the related revenue has not yet been recognized.Deferred gross margin .................................................................. **77,600Cost of goods sold ........................................................................ 220,000 Sales revenue ......................................................................... 297,600* To record recognition of sales revenue from year 1 sales and related cost of goods sold at expiry of warranty period* $310,000 – $12,400** ($90,000 – $12,400)Warranty expense ......................................................................... 27,000* Deferred warranty costs ......................................................... 27,000 To record recognition of warranty expense at same time as related sales revenue recognition* $18,600 + $8,400Requirement 3Allied Auto Parts Inc. might choose to recognize revenue only after the warranty periodhas expired if they are not able to make a good estimate, at the time of sale, of the amount of warranty work that will be required under the terms of the one-year warranty. If Allied is not able, at the time of sale, to make a good estimate of the warranty work that will be required, then the measurability criterion of revenue recognition is not met at the time of sale. The measurability criterion means that the amount of revenue can be reliably measured. If the seller is not able to estimate the amount of work that will have to be done under the warranty agreement, then it is not able to reasonably measure the profit that itwill eventually earn on the sales. The performance criteria might also be invoked here.The performance criterion means that the seller has transferred the significant risks and rewards of ownership to the buyer. As long as there is warranty work to be performed after the sale that is the responsibility of the seller, you might argue that performance is not substantially complete. However, if the seller was able to reliably estimate the amount of warranty work, then performance would be satisfied on the assumption that we could measure the risk that remains with the seller, and make a provision for it.2.Percentage-of-completion method:The first step in applying revenue recognition using the percentage-of-completion method (using costs incurred to date compared to estimated total costs to determine the percentage of completion) is to estimate the percentage of completion of the project at the end of each year. This is done in the following table (in $000s):End of 2005 End of 2006 End of 2007Total costs incurred $ 5,400 $ 12,950 $ 18,800 Total estimated costs 18,000 18,500 18,800 % completed 30% 70% 100%Once the percentage of completion at the end of each year has been calculated as above, the next step is to allocate the appropriate amount of revenue to each year, based on the percentage completed to date, less what has previously been recorded in revenue. This is done in the following table (in $000s):2005 2006 20072005 $20,000 × 30% $ 6,0002006 $20,000 × 70% $ 14,0002007 $20,000 × 100% $ 20,000 Less: Revenue recognized in prior years (0) (6,000) (14,000) Revenue for year $ 6,000 $ 8,000 $ 6,000Therefore, the profit to be recognized each year on the construction project would be:2005 2006 2007 TotalRevenue recognized $ 6,000 $ 8,000 $ 6,000 $ 20,000 Construction costs incurred (expenses) (5,400) (7,550) (5,850) (18,800) Gross profit for the year $ 600 $ 450 $ 150 $ 1,200The following journal entries are used to record the transactions under thepercentage-of-completion method of revenue recognition:2005 2006 20071. Costs of construction:Construction in progress .................. 5,400 7,550 5,850 Cash, payables, etc. ..... 5,400 7,550 5,850 2. Progress billings:Accounts receivable ............ 3,100 4,900 12,000 Progress billings ............ 3,100 4,900 12,000 3. Collections on billings:Cash .................................... 2,400 4,000 12,400 Accounts receivable ...... 2,400 4,000 12,400 4. Recognition of profit:Construction in progress ..... 600 450 150Construction expense.......... 5,400 7,550 5,850 Revenue from long-termcontract ...................... 6,000 8,000 6,000 5. To close construction in progress:Progress billings .................. 20,000 Construction in progress .20,0002005 2006 2007Balance sheetCurrent assets:Accounts receivable $ 700 $ 1,600 $ 1,200 Inventory:Construction in process 6,000 14,000 Less: Progress billings (3,100) (8,000)Costs in excess of billings 2,900 6,000Income statementRevenue from long-term contracts $ 6,000 $ 8,000 $ 6,000 Construction expense (5,400) (7,550) (5,850) Gross profit $ 600 $ 450 $ 1503.a. The three criteria of revenue recognition are performance, measurability, andcollectibility.Performance means that the seller or service provider has performed the work.Depending on the nature of the product or service, performance may mean quitedifferent points of revenue recognition. For example, for the sale of products, IAS18 defines performance as the point when the seller of the goods has transferred therisks and rewards of ownership to the buyer. Normally, this means that performance is done at the time of sale. Although the seller may have performed much of the work prior to the sale (production, selling efforts, etc.), there is still significant risk to theseller that a buyer may not be found. Therefore, from a reliability point of view,revenue recognition is delayed until the point of sale. Also, there may be significant risks remaining with the seller of the product even after the sale. Warranties given by the seller are a risk that remains with the seller. However, if this risk can be reliably estimated at the time of sale, revenue can be recognized at the point of sale.Performance is quite different under a long-term construction contract. Here,performance really is considered to be a measure of the work done. Revenue isrecognized over the production period as the work is performed. It is intended toreflect the amount of effort expended by the seller (contractor). Although legal titlewon’t transfer to the buyer until the project is completed, revenue can be recognized because there is a known and committed buyer. If the contractor is not able toestimate how much of the work has been done (perhaps because he or she can’treliably estimate how much work must still be done), then profit would not berecognized until the extent of performance is known.Measurability means that the seller or service provider must be able to reliablyestimate the amount of the revenue from the sale or service. For the sale of products this is generally known at the time of sale (the sales price is set). However, if the seller provides a return period, it may be necessary to estimate the volume of returns at the time of sale in order to measure the revenue that will be recognized.Collectibility means that the seller or the service provider has reasonable assurance that the sales price will actually be collected. In most cases for the sales of products, the seller is able to recognize revenue at the time of sale even if the sale is on account.This is because the seller has experience with its customers and is able to estimate reliably the risk of non payment. As long as the seller is able to make this estimate, it is appropriate to recognize the revenue but to offset it with a provision for possible non collection. If the seller is unable to make reliable estimates of future collection ofamounts owing, the recognition of revenue would be delayed until the cash is actually received. This is what is done using the instalment sales method of revenuerecognition.b. Because of the performance criterion of revenue recognition, it would seem to bemost appropriate to recognize most revenue as the seller or service provider performs the work. This would be the best measure of performance. This would mean, for example,that sellers of products would recognize their revenue over the whole production, selling, and post sales servicing periods. As we saw above, this is not commonly done because,in many cases, there are still significant risks that are retained by the seller (risk of not being able to sell the product, for example). There are also measurement risks (knowingthe selling price) that exist prior to the sale. The percentage-of-completion method of revenue used for some long-term construction contracts would seem to most closely recognize revenue as the work is performed. As mentioned in Part 1, we are able to recognize revenue on this basis since a contract exists which commits the purchaser tobuy the project (assuming certain conditions are met) and the sales price is known because of the existence of the contract.4.If all revenue is recognized when a student registers for the course, profit for 2007 would be:Sales Revenue1:Manuals and initial lessons (200 × $100) $ 20,000 Additional lessons ((200 × 8) × $30) 48,000 Examinations ((200 × 80%) × $130) 20,800 Total sales revenue 88,800Cost of sales:Manuals and initial lessons (200 × ($15 + $3)) 3,600 Additional lessons ((200 × 8) × $3)) 4,800Examinations ((200 × 80%) × $30) 4,800 Total cost of sales 13,200Depreciation of development costs:$180,000 × (200/1,000) 36,000Profit $ 39,6005.FINISH ENTERPRISESIncome Statementfor the year ending December 31, 2005Continuing operations (excluding the chemical division)Sales ($35,000,000 – $5,500,000) $ 29,500,000Cost of sales ($15,000,000 – $2,800,000) (12,200,000)Gross profit 17,300,000Selling & administration expenses($18,000,000 – $3,200,000) (14,800,000)Profit from operations 2,500,000Income tax expense (40%) 1,000,000Profit after tax $ 1,500,000Discontinuing operations (Chemical division)Sales 5,500,000Cost of sales (2,800,000)Gross profit 2,700,000Selling & administration expenses (3,200,000)Loss from operations (500,000)Income tax expense(40%) 200,000Loss after tax (300,000) Gain on discontinuance of the Chemical division 3,500,000Tax thereon (1,400,000)After-tax gain on discontinuance of the Chemical division 2,100,000 Enterprise net profit $ 3,300,000Chapter 81.Payment of account payable. operatingIssuance of preferred stock for cash. financingPayment of cash dividend. financingSale of long-term investment. investingAmortization of bond discount. no effectCollection of account receivable. operatingIssuance of long-term note payable to borrow cash. financing Depreciation of equipment. no effectPurchase of treasury stock. financingIssuance of common stock for cash. financingPurchase of long-term investment. investingPayment of wages to employees. operatingCollection of cash interest. investingCash sale of land. InvestingDistribution of stock dividend. no effectAcquisition of equipment by issuance of note payable. no effect Payment of long-term debt. financingAcquisition of building by issuance of common stock. no effect Accrual of salary expense. no effect2.(a) Cash received from customers = 816,000(b) Cash payments for purchases of merchandise. =468,000(c) Cash payments for operating expenses. = 268,200(d) Income taxes paid. =36,9003.Cash sales …………………………………………... $9,000 Payment of accounts payable ……………………….-48,000 Payment of income tax ………………………………-13,000 Payment of interest ……………………………..…..-16,000 Collection of accounts receivable ……………………93,000 Payment of salaries and wages ……………………….. -34,000 Cash flows from operating activitiesby the direct method -9,0004.Operating activities:Net loss -200,000 Add: loss on sale of land 250,000 Add: depreciation 300,000Add: amortization of patents 20,000Less: increases in current assets other than cash -750,000Add: increases in current liabilities 180,000Net cash flows from operating -200,000Investing activitiesSale of land -50,000Purchase of PPE -1,500,000Net cash flows from investing -1,550,000Financing activitiesIssuance of common shares 400,000Payment of cash dividend -50,000Issuance of non-current liabilities 1,000,000Net cash flows from financing 1,350,000 Net changes in cash -400,000 5.。

会计英语第三(叶建芳)翻译

第一章会计总论本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍并列示财务报表。

学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.理解了解会计及其环境会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会和普通公众也会使用会计信息。

1.1组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体。

个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只是在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股票股份可以在所有者之间转让。

1.2编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

叶建芳会计英语中文版1-4

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

叶建芳会计英语中文版

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显着优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

为满足上述需求,国际会计准则委员会(IASC)于1973年成立,并致力于国际公认的会计准则的制定。

叶建芳会计英语中文版1_5

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的围要大于簿记。

图表1-1是信息在会计系统的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

会计英语概述

2019/2/13

Decision Making

Economic Events

Reports

Exhibit 1-1

Financial statements report accounting information about resources, earning prospects, expected cash collections, incurred expenses, repayment ability, tax collection and negotiating wage agreements.

1、transaction n.交易;处理 Related transactions 关联交易 Transactions cost 交易成本 Business transactions 经济业务;商业交易 2、accounts n.帐目;会计账户;会计账簿 Accounts manager 会计部经理 Accounts receivables 应收账款 Accounts payable应付账款 Accounts department 会计部 3、Statements n.报告;报表 Accounting statement 会计报表=financial statement=statements Financial statements analysis 财务报表分析 Combination statements 汇总报表;合并报表 Suppliers statements 供应商对账单

【 LESSON 】

Recording Transactions

【 LESSON 】

Adjusting the Accounts, Preparing the Statements, and Completing the Accounting Cycle

会计英语中文翻译(叶建芳孙红星)第二章

每天只看目标,别老想障碍

•

3、

。22.3 .2402:1 1:2002: 11Mar-2224-M ar-22

宁愿辛苦一阵子,不要辛苦一辈子

•

4、

。02:1 1:2002: 11:200 2:11Thursday, March 24, 2022

• •

积极向上的心态,是成功者的最基本要素 5、

。22.3 .2422.3 .2402:1 1:2002: 11:20M arch 24, 2022

M22.3.2422.3.24

Hale Waihona Puke 生活总会给你谢另一个谢机会,大这个机家会叫明天 6、

。2 022年3 月24日 星期四 上午2 时11分2 0秒02:1 1:2022. 3.24

人生就像骑单车,想保持平衡就得往前走

•

7、

。202 2年3月 上午2 时11分2 2.3.240 2:11Ma rch 24, 2022

•

8、业余生活要有意义,不要越轨。20 22年3 月24日 星期四2 时11分 20秒02 :11:202 4 March 2022

我们必须在失败中寻找胜利,在绝望中寻求希望

•

9、

。上 午2时11 分20秒 上午2 时11分0 2:11:20 22.3.24

• 10、一个人的梦想也许不值钱,但一个人的努力很值 钱。3/24/2022 2:11:20 AM02:11:202022/3/24

• 11、在真实的生命里,每桩伟业都由信心开始,并由 信心跨出第一步。3/24/2022 2:11 AM3/24/2022 2:11 A

每一个成功者都有一个开始。勇于开始,才能找到成

•

1、

功的路 。22.3.2422.3.24Thursday, March 24, 2022

会计英语(第三版)

nominal account 虚账户

chart of accounts 科目表

精选ppt

17

general ledger 总分类账

normal balance 正常余额

journalizing 记日记账

compound journal entry

复合分录

精选ppt

18

general journal 普通日记账

精选ppt

9

Chinese Institute of Certified Public Accountants

(CICPA) 中国注册会计师协会

Financial accounting 财务会计

Managerial accounting

管理会计

Tax accounting 税务会计

科目汇总表

精选ppt

28

columnar journal 多栏式日记账

unearned revenue 预收收入

Advance from customers

预收账款

Prepaid expense 待摊费用

精选ppt

Generally accepted accounting principles

公认会计准则

Financial Accounting Standards Board

(FASB) 财务会计准则委员会

精选ppt

6

Entity Concept 会计主体

Cost principle 成本原则

会计英语

第三版

精选ppt

1

Chapter 1

精选ppt

2

Accounting 会计

Bookkeeping 簿记

叶建芳会计英语中文版

第一章会计总论学习目标:1.了解会计信息系统2.应用公认会计准则3.了解财务报表4.运用会计要素5.运用会计等式6.了解会计及其环境本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍财务报表。

1.1会计是一个信息系统我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转会计信息使用者主要是投资者和债权人,政府,工会,普通公众也会使用会计信息。

1.2组织形式企业有三种组织形式:个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股份可以在所有者之间转让。

1.3编报财务报表的框架由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第一章会计总论

学习目标:

1.了解会计信息系统

2.应用公认会计准则

3.了解财务报表

4.运用会计要素

5.运用会计等式

6.理解了解会计及其环境

本章讨论不同的使用者对会计信息的需求,介绍不同实体对会计职业的影响、会计职业道德及职业行为准则。

本章也将对公认会计准则以及一些相关概念和原则进行解释。

本章将介绍会计等式:资产=负债+所有者权益,并逐一定义会计等式中的每个要素,举例分析不同业务对会计等式的影响。

同时,本章还将简单介绍并列示财务报表。

会计是一个信息系统

我们通常把会计描述为一个信息系统。

作为一个信息系统,会计计量经济活动,将信息编制成财务报表,并将财务报表传达给决策者。

会计的范围包括:确认经济事项,进行计量、记录、汇总,并把信息报告给使用者。

会计所涵盖的范围要大于簿记。

图表1-1是信息在会计系统内的流转图。

簿记是对交易和事件的记录,只是会计的一部分。

会计还包括对会计信息的分析和阐述,以帮助财务报表的外部和内部的使用者制定各项经济决策。

图表1-1 会计信息流转

会计信息使用者主要是投资者和债权人,政府,工会和普通公众也会使用会计信息。

1.1组织形式

企业有三种组织形式:

个人独资企业是指由一个自然人投资拥有的企业组织。

个人独资企业是一个会计实体,但并不是法律实体。

个人独资企业的所有者对企业的债务承担无限责任,这也是个人独资企业的一个主要缺点。

合伙企业与个人独资企业的区别只是在于它有两个或两个以上的所有者。

合伙企业的所有者被称为合伙人。

现实商业活动中有许多不同类型的合伙企业。

公司是依据当地法律注册成立的单独实体;公司的所有者被称为股东。

股东不对公司的债务负责。

有限责任是公司这种组织形式的一个显著优点。

公司的所有权被分为股份。

股票股份可以在所有者之间转让。

1.2编报财务报表的框架

由于各个国家的法律和经济环境不同,各国有不同的会计模式。

在一个国家可行的会计实务在另一个国家并不一定可行。

由于各国的会计模式不同,所以我们需要制定一个互相协调的会计标准:用全球通用的会计语言来传达相关的且可靠的会计信息。

为满足上述需求,国际会计准则委员会(IASC)于1973年成立,并致力于国际公认的会计准则的制定。

2001年4月1日,根据题为《关于重塑国际会计准则委员会未来的建议》的报告中的提议,国际会计准则委员会(IASC)改组为国际会计准则理事会(IASB)。

除了1989年发布的国际会计准则外,国际会计准则委员会还发布了财务报表编报的框架,并将其作为建立会计准则的概念基础。

框架主要包括以下内容:

1.财务报表的目的及基础假设;

2.财务报表的质量特征;

3.财务报表的要素;

4.资本和资本保全概念.

图表1-2概括地介绍了一些重要的会计原则。

图表1-2

2006年2月16日,中国的财政部宣布实行一项新的基本准则和38项新的具体会计准则,虽然这些准则和国际会计准则相比有一些例外,但很大程度上已经和国际会计准则一致。

新的基本准则类似于国际会计准则委员会发布的概念框架,并且这新的38项会计准则覆盖了国际财务报告准则下的所有问题。

1.3了解财务报表

会计信息必须满足使用者的需求。

主要使用者利用财务报表信息评价企业的盈利能力和偿债能力。

财务报表是会计程序的最终产品。

财务报表应按一定的格式编制,并提供与决策相关的信息。

个人独资企业编制的四种财务报表有:

-利润表(又称为损益表);

-所有者权益变动表(又称为资本变动表,以及以后章节介绍的留存收益表);。