商业银行管理第2章习题答案

商业银行业务与经营综合练习题-附答案

《商业银行业务与经营》综合练习题第一章商业银行导论第一部分选择题1、最早进入中国的外国银行是()A、浙江兴业银行B、交通银行C、东方银行D、通商银行2、()是商业银行最基本,也是最能反映其经营活动特征的职能。

A、信用中介B、信用创造C、支付中介D、金融服务3、我国的商业银行实行的是(),而世界上大部分国家都实行此种组织形式。

A、单一银行制B、分行制C、银行控股公司制D、非银行控股公司制4、股份制商业银行的组织形式中,()是商业银行的最高权力机构。

A、董事会B、监事会C、总稽核D、股东大会5、现代股份制商业银行的内部组织结构可以分为()A、决策机构B、执行机构C、监管机构D、监督机构6、商业银行的管理系统由()方面组成。

A、全面管理B、财务管理C、人事管理D、经营管理E、市场营销管理7、世界各国在对银行业进行监管时,主要内容包括()A、银行业的准入B、银行资本的充足性C、银行的清偿能力D、银行业务活动的范围E、贷款的集中程度第二部分填空题1、在英国,早期的银行业是由发展而来的。

2、1694年,英国建立了历史上第一家资本主义股份制商业银行——,它的出现宣告了高利贷性质的银行业在社会信用领域垄断地位的结束。

3、商业银行的信用创造职能是在与职能的基础上产生的。

4、从全球商业银行来看,商业银行的外部组织形式主要有三种类型,即、和。

5、政府对银行监管的“CAMEL(骆驼)原则”具体指、、、和。

6、目前各国存款保险制度的组织形式主要有三种,即、和。

7、1894年我国的成立以后,开始正式行使对商业银行的监管职能。

而2003年12月27日,《中华人民共和国银行业监督管理法》,明确是银行业的监督管理机构。

第三部分名词解释1、信用创造2、银行控股公司制3、商业银行的外部组织形式4、商业银行的内部组织形式5、存款保险制度第四部分问答题1、商业银行在一国经济发展过程中发挥了什么样的作用?2、商业银行单一银行制有哪些优缺点?商业银行分行制有哪些优缺点?3、政府为什么要对银行业实施监管?我国政府如何对银行业实施监管?第二章商业银行的资本管理第一部分选择题1、一家银行在发展过程中,会遇到各种各样的风险,例如()A、信用风险B、利率风险C、汇率风险D、经营风险E、流动性风险2、(),国际清算银行通过了《关于统一国际银行资本衡量和资本标准的协议》(即《巴塞尔协议》),规定12个参加国应以国际可比性及一致性为基础制定各自银行资本标准。

商业银行经营学第二章练习

商业银行经营学第二章一、单项选择题(每个题目只有一个正确答案,请选择正确答案)1. 发行优先股对商业银行的不足之处不包括()。

A.股息税后支付,增加了资金成本B.总资本收益率下降时,会发生杠杆作用,影响普通股股东的权益C.不会稀释控制权D.可以在市场行情变动时对优先股进行有利于自己的转化,增大了经营的不确定性2. 一旦银行破产、倒闭时,对银行的资产的要求权排在最后的是()。

A.优先股股东B.普通股股东C.债权人D.存款人3. 发行普通股对商业银行的不足之处不包括()。

A.发行成本比较高B.对商业银行的股东权益产生稀释作用C.资金成本总要高于优先股和债券D.总资本收益率下降时,会发生杠杆作用4. 资本盈余是指发行普通股时发行的实际价格高于()的部分A.发行的预计价格B.票面价值C.实际价值D.每股净资产5. 下列各项不属于发行资本债券特点的有()。

A.不稀释控制权B.能大量发行,满足融资需求C.利息税前支付,可降低税后成本D.利息固定,会发生杠杆作用6. 资本与总资产比率和资本与存款比率相比,克服了()的不足。

A.没考虑资金运用B.没反映银行资产结构C.没考虑风险D.没考虑商业银行经营管理水平7. 下列关于纽约共识的说法中正确的有()。

A.它根据商业银行资本风险程度的不同,将全部资本分做六类B.其中的无风险资产包括:库存现金、同业拆借、国债、优质商业票据等C.亏损了的资产或固定资产也叫有问题资产,需要100%的资本保证D.商业银行只要将各类资产额分别乘以各自的资本资产比率要求,并进行加总,便可以求得商业银行所需的最低资本量8. 下列各项不属于综合分析法特点的有()。

A.非数量性B.不确定性C.繁琐D.客观性9. 下列各项不属于非公开储备特点的有()。

A.是指不在银行的资产负债表上公开标明的储备B.包括在核心资本中C.与公开储备具有相同的质量D.可以自由、及时地被用于应付未来不可预见的损失10. 下列关于资本需要量的说法中正确的是()。

商业银行课后习题及答案

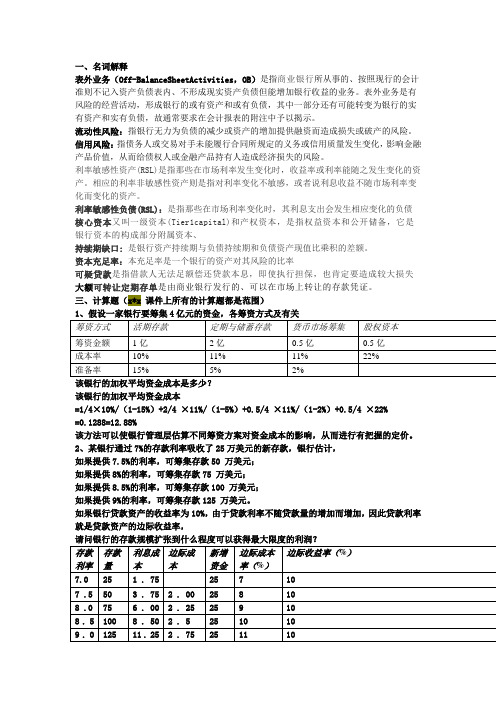

一、名词解释表外业务(Off-BalanceSheetActivities,OB)是指商业银行所从事的、按照现行的会计准则不记入资产负债表内、不形成现实资产负债但能增加银行收益的业务。

表外业务是有风险的经营活动,形成银行的或有资产和或有负债,其中一部分还有可能转变为银行的实有资产和实有负债,故通常要求在会计报表的附注中予以揭示。

流动性风险:指银行无力为负债的减少或资产的增加提供融资而造成损失或破产的风险。

信用风险:指债务人或交易对手未能履行合同所规定的义务或信用质量发生变化,影响金融产品价值,从而给债权人或金融产品持有人造成经济损失的风险。

利率敏感性资产(RSL)是指那些在市场利率发生变化时,收益率或利率能随之发生变化的资产。

相应的利率非敏感性资产则是指对利率变化不敏感,或者说利息收益不随市场利率变化而变化的资产。

利率敏感性负债(RSL):是指那些在市场利率变化时,其利息支出会发生相应变化的负债核心资本又叫一级资本(Tier1capital)和产权资本,是指权益资本和公开储备,它是银行资本的构成部分附属资本、持续期缺口: 是银行资产持续期与负债持续期和负债资产现值比乘积的差额。

资本充足率:本充足率是一个银行的资产对其风险的比率可疑贷款是指借款人无法足额偿还贷款本息,即使执行担保,也肯定要造成较大损失大额可转让定期存单是由商业银行发行的、可以在市场上转让的存款凭证。

三、计算题(x*x 课件上所有的计算题都是范围)该银行的加权平均资金成本是多少?该银行的加权平均资金成本=1/4×10%/(1-15%)+2/4 ×11%/(1-5%)+0.5/4 ×11%/(1-2%)+0.5/4 ×22%=0.1288=12.88%该方法可以使银行管理层估算不同筹资方案对资金成本的影响,从而进行有把握的定价。

2、某银行通过7%的存款利率吸收了25万美元的新存款,银行估计,如果提供7.5%的利率,可筹集存款50 万美元;如果提供8%的利率,可筹集存款75 万美元;如果提供8.5%的利率,可筹集存款100 万美元;如果提供9%的利率,可筹集存款125 万美元。

《商业银行管理学》课后习题答案及解析

《商业银行管理学》课后习题及题解第一章商业银行管理学导论习题一、判断题1. 《金融服务现代化法案》的核心内容之一就是废除《格拉斯-斯蒂格尔法》。

2. 政府放松金融管制与加强金融监管是相互矛盾的。

3. 商业银行管理的最终目标是追求利润最大化。

4. 在金融市场上,商业银行等金融中介起着类似于中介经纪人的角色。

5. 商业银行具有明显的企业性质,所以常用于企业管理的最优化原理如边际分享原理、投入要素最优组合原理、规模经济原理也适用于商业银行。

6. 金融市场的交易成本和信息不对称决定了商业银行在金融市场中的主体地位。

7. 企业价值最大化是商业银行管理的基本目标。

8. 商业银行管理学研究的主要对象是围绕稀缺资源信用资金的优化配置所展开的各种业务及相关的组织管理问题。

9. 商业银行资金的安全性指的是银行投入的信用资金在不受损失的情况下能如期收回。

二、简答题1. 试述商业银行的性质与功能。

2. 如何理解商业银行管理的目标?3. 现代商业银行经营的特点有哪些?4. 商业银行管理学的研究对象和内容是什么?5. 如何看待“三性”平衡之间的关系?三、论述题1. 论述商业银行的三性目标是什么,如何处理三者之间的关系。

2. 试结合我国实际论述商业银行在金融体系中的作用。

第一章习题参考答案一、判断题1.√2.×3.×4.√5.×6.√7.×8.√9.√二、略;三、略。

第二章商业银行资本金管理习题一、判断题1. 新巴塞尔资本协议规定,商业银行的核心资本充足率仍为4%。

2. 巴塞尔协议规定,银行附属资本的合计金额不得超过其核心资本的50%。

3. 新巴塞尔资本协议对银行信用风险提供了两种方法:标准法和内部模型法。

4. 资本充足率反映了商业银行抵御风险的能力。

5. 我国国有商业银行目前只能通过财政增资的方式增加资本金。

6. 商业银行计算信用风险加权资产的标准法中的风险权重由监管机关规定。

二、单选题1. 我国《商业银行资本充足率管理办法》规定,计入附属资本的长期次级债务不得超过核心资本的。

商业银行经营习题(含答案)1-5章

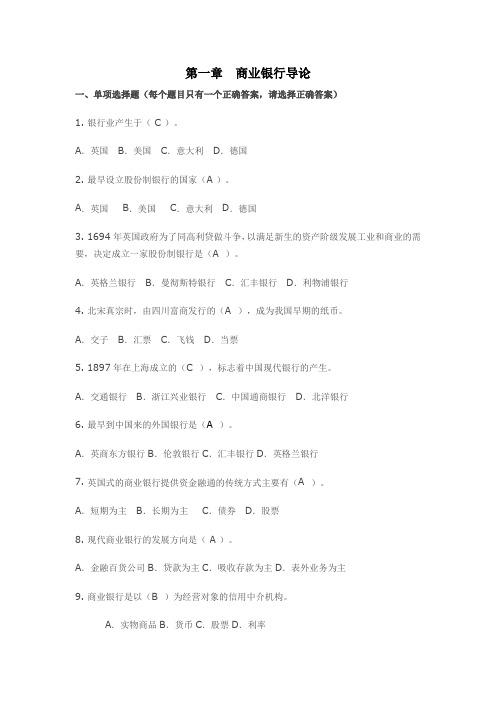

第一章商业银行导论一、单项选择题(每个题目只有一个正确答案,请选择正确答案)1.银行业产生于(C)。

A.英国B.美国C.意大利D.德国2.最早设立股份制银行的国家(A)。

A.英国B.美国C.意大利D.德国3.1694年英国政府为了同高利贷做斗争,以满足新生的资产阶级发展工业和商业的需要,决定成立一家股份制银行是(A)。

A.英格兰银行B.曼彻斯特银行C.汇丰银行D.利物浦银行4.北宋真宗时,由四川富商发行的(A),成为我国早期的纸币。

A.交子B.汇票C.飞钱D.当票5.1897年在上海成立的(C),标志着中国现代银行的产生。

A.交通银行B.浙江兴业银行C.中国通商银行D.北洋银行6.最早到中国来的外国银行是(A)。

A.英商东方银行B.伦敦银行C.汇丰银行D.英格兰银行7.英国式的商业银行提供资金融通的传统方式主要有(A)。

A.短期为主B.长期为主C.债券D.股票8.现代商业银行的发展方向是(A)。

A.金融百货公司B.贷款为主C.吸收存款为主D.表外业务为主9.商业银行是以(B)为经营对象的信用中介机构。

A.实物商品B.货币C.股票D.利率10.商业银行的(D)被称为第一级准备。

A.贷款资产B.证券资产C.股票资产D.现金资产11.商业银行的性质主要归纳为以追求(B)为目标。

A.追求最大贷款额B.追求最大利润C.追求最大资产D.追求最大存款12.(C)是国家的金融管理当局和金融体系的核心,具有较高的独立性,它不对客户办理具体的信贷业务,不以营利为目的。

A.工商银行B.股份制银行C.中央银行D.专业银行13.(A)是商业银行最基本也最能反映其经营活动特征的的职能。

A.信用中介B.支付中介C.清算中介D.调节经济的职能14.金融市场上利率的变动使经济体在筹集或运用资金时可能遭受到的损失是指(A)。

A.国家风险B.利率风险C.信用风险D.流动性风险15.借贷双方产生借贷行为后,借款方不能按时归还贷款方的本息而使贷款方遭受损失的可能性是指(C)。

商业银行经营管理第2章 商业银行资本管理

8

《巴塞尔协议》将银行的资本划分为两类:一类是 核心资本(一级资本);另一类是附属资本(二 级资本)。 1、核心资本(一级资本) 核心资本包括股本和公开储备。 股本包括已经发行并全额缴付的普通股和永久 性非累积的优先股; 公开储备指以公开的形式,通过保留盈余和其 他盈余,例如股票发行溢价、保留利润(凭国家 自行处理,包括在整个过程中用当年保持利润向 储备分配或储备提取)、普通准备金和法定准备 金的增值而创造和增加的反映在资产负债表上的 储备。

3.发行资本票据和债券 债务资本是 70 年代起被西方发达国家的银行广 泛使用的一种外源资本。这种债务资本所有者的求 偿权排在各类银行存款所有者之后,并且其原始期 限较长。债务资本通常有资本票据和债券两类。资 本票据是一种以固定利率计息的小面额证券,该证 券的期限为 7—15 年不等。它可以在金融市场上出 售,也可向银行的客户推销。债券的形式较多,通 常而言,银行债券性资本包括可转换后期偿付债券、 浮动利率后期偿付债券、选择性利率后期偿付债券 等等。

26

发行资本票据和债券筹资的优点在于: 1)由于债务的利息可以从银行税前收益中支出,而不必 缴纳所得税,因此,尽管长期债务的利息看上去比发行 股票的成本高,但考虑税收因素后,长期债务反而更便 宜; 2)在通过投资银行发行股票或债券时,通常发行股票的 成本要比发行债券的成本高一些; 3)虽然在西方的商业银行管理中,一般存款要缴存一定 比率的准备金,但商业银行通过发行资本票据和债券吸 收到资金,不必缴存准备金,这实际上增加了商业银行 可以运用的资金量,也就降低了商业银行的融资成本; 4)发行资本票据和债券可以强化财务杠杆效应。

22

商业银行通过发行普通股筹资有以下缺点: 1)发行成本高。 2)会削弱原股东对银行的控制权。 3)会影响股票的收益。 4)如果市场利率比较低,通过债务方式进行 融资的成本较低,此时,发行新股会降低银 行的预期收益,这样将使普通股股东的收益 降低。

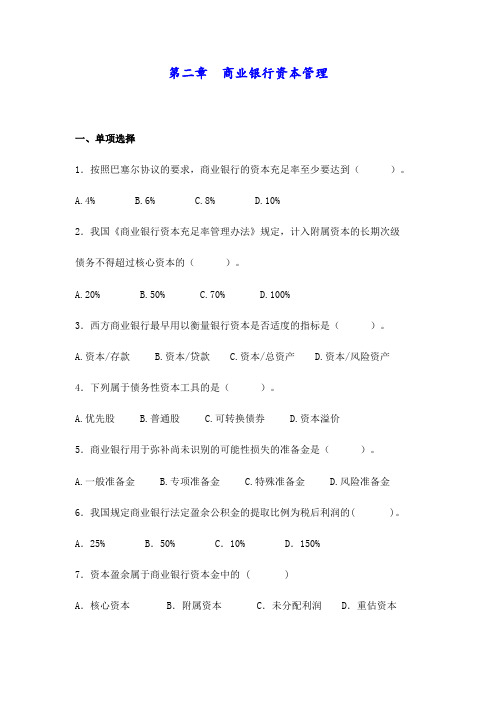

第二章商业银行资本管理习题

第二章商业银行资本管理一、单项选择1.按照巴塞尔协议的要求,商业银行的资本充足率至少要达到()。

A.4%B.6%C.8%D.10%2.我国《商业银行资本充足率管理办法》规定,计入附属资本的长期次级债务不得超过核心资本的()。

A.20%B.50%C.70%D.100%3.西方商业银行最早用以衡量银行资本是否适度的指标是()。

A.资本/存款B.资本/贷款C.资本/总资产D.资本/风险资产4.下列属于债务性资本工具的是()。

A.优先股B.普通股C.可转换债券D.资本溢价5.商业银行用于弥补尚未识别的可能性损失的准备金是()。

A.一般准备金B.专项准备金C.特殊准备金D.风险准备金6.我国规定商业银行法定盈余公积金的提取比例为税后利润的( )。

A.25% B.50% C.10% D.150%7.资本盈余属于商业银行资本金中的 ( )A.核心资本 B.附属资本 C.未分配利润 D.重估资本8.《巴塞尔协议》规定商业银行的核心资本与风险加权资产的比例关系是( )。

A.≥8% B.≤8% C.≤4% D.≥4%9.票据贴现的期限最长不超过 ( )。

A.6个月 B.9个月 C.3个月 D.1个月10.下列哪一个不属于银行的权益资本 ( )。

A.普通股 B.优先股 C.权益承诺票据 D.盈余公积金二、多项选择1.下列各项中属于商业银行核心资本的是()。

A.实收资本B.资本公积C.未分配利润D.重估储备E.公开储备2.下列各项中属于商业银行附属资本的是()。

A.一般准备B.优先股C.盈余公积D.可转换债券E.永久性非累计优先股3.根据巴塞尔《新资本协议》,银行可以采用的信用风险计量方法有()。

A.标准法B.内部评级初级法C.内部评级高级法D.基本指标法E.内部模型法4.巴塞尔《新资本协议》对商业银行的()提出了资本拨备要求。

A.流动性风险B.信用风险C.市场风险D.操作风险E.道德风险5.次级债券是商业银行发行的、本金和利息的清偿顺序列于()的债券。

第二章-商业银行经营与管理

第二章商业银行经营与管理第一节商业银行经营与管理概述一、商业银行经营与管理的涵义商业银行是以货币和信用为经营对象的金融中介机构。

商业银行的经营是指商业银行对所开展的各种业务活动的组织和营销;商业银行的管理是商业银行对所开展的各种业务活动的控制与监督。

【例题·单选题】商业银行的经营是指对其所开展的各项业务活动的()。

A.组织和控制B.组织和营销C。

控制和监督D.计划和组织『正确答案』B二、商业银行经营与管理的内容1。

商业银行的经营主要包括以下内容:(1)负债业务的组织和营销;(2)资产业务的组织和营销;(3)中间业务和表外业务的组织和营销2。

商业银行的管理主要包括以下内容:(1)资产负债管理;(2)财务管理;(3)风险管理;(4)人力资源开发与管理三、商业银行经营与管理的关系经营是现代商业银行生存发展的根本,管理是为了确保经营的效率,服务于经营,为了更好地经营。

因此,两者是相互联系、互为依托的。

四、商业银行经营与管理的原则(一)商业银行经营与管理的原则通常把安全性、流动性、盈利性归纳为商业银行经营与管理的三大原则.1。

安全性原则资金经营安全是商业银行生存发展的基础,也是实现资金流动和盈利、保持银行良好信誉的前提,被视为三大原则的首要原则。

2。

流动性原则银行的流动性体现在资产和负债两个方面:(1)资产的流动性,即银行资产在不受损失的条件下能够迅速变现的能力;(2)负债的流动性,即银行在需要时能够及时以较低的成本获得所需资金的能力。

3.盈利性原则盈利性是指商业银行获得利润的能力。

商业银行作为企业,追求盈利是其经营的核心目标,也是其不断改进服务,扩大业务经营的内在动力。

(二)商业银行经营与管理原则之间的关系商业银行经营管理的三原则既有联系又有矛盾。

一般说来流动性与安全性成正比,流动性越强,风险越小,安全就越有保障。

然而,流动性、安全性与盈利性成反比,流动性越高,安全性越好,而银行盈利水平则会越低,反之则相反。

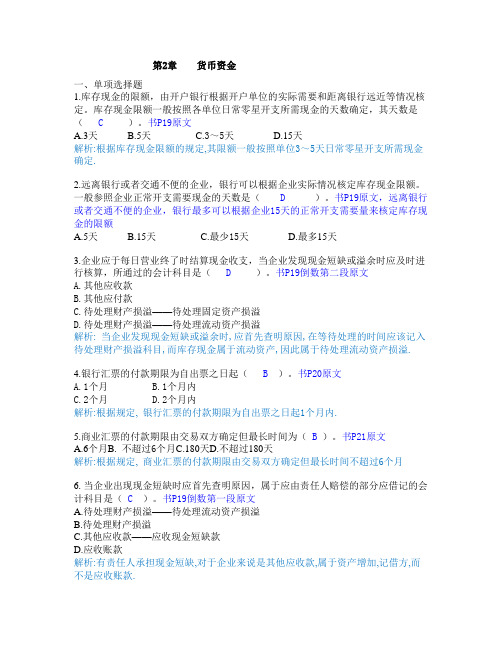

(完整版)第2章习题货币资金(答案完整版)

第2章货币资金一、单项选择题1.库存现金的限额,由开户银行根据开户单位的实际需要和距离银行远近等情况核定。

库存现金限额一般按照各单位日常零星开支所需现金的天数确定,其天数是( C )。

书P19原文A.3天B.5天C.3~5天D.15天解析:根据库存现金限额的规定,其限额一般按照单位3~5天日常零星开支所需现金确定.2.远离银行或者交通不便的企业,银行可以根据企业实际情况核定库存现金限额。

一般参照企业正常开支需要现金的天数是( D)。

书P19原文,远离银行或者交通不便的企业,银行最多可以根据企业15天的正常开支需要量来核定库存现金的限额A.5天B.15天C.最少15天D.最多15天3.企业应于每日营业终了时结算现金收支,当企业发现现金短缺或溢余时应及时进行核算,所通过的会计科目是( D )。

书P19倒数第二段原文A.其他应收款B.其他应付款C.待处理财产损溢——待处理固定资产损溢D.待处理财产损溢——待处理流动资产损溢解析:当企业发现现金短缺或溢余时,应首先查明原因,在等待处理的时间应该记入待处理财产损溢科目,而库存现金属于流动资产,因此属于待处理流动资产损溢.4.银行汇票的付款期限为自出票之日起( B )。

书P20原文A.1个月B.1个月内C.2个月D.2个月内解析:根据规定,银行汇票的付款期限为自出票之日起1个月内.5.商业汇票的付款期限由交易双方确定但最长时间为( B)。

书P21原文A.6个月B.不超过6个月C.180天D.不超过180天解析:根据规定,商业汇票的付款期限由交易双方确定但最长时间不超过6个月6.当企业出现现金短缺时应首先查明原因,属于应由责任人赔偿的部分应借记的会计科目是(C )。

书P19倒数第一段原文A.待处理财产损溢——待处理流动资产损溢B.待处理财产损溢C.其他应收款——应收现金短缺款D.应收账款解析:有责任人承担现金短缺,对于企业来说是其他应收款,属于资产增加,记借方,而不是应收账款.7.现金的管理和控制要先从企业内部着手建立相应的( D)书P18第一段原文A.现金管理制度B.现金控制制度C.企业管理制度D.内部控制制度解析:现金的管理和控制要先从企业内部着手,建立相应的内部控制制度,同时应严格遵守国家的相关规定.8.银行本票的适用范围是( D )。

商业银行管理第2章习题答案

Chapter 2Analyzing Bank PerformanceChapter Objectives1.Introduce bank financial statements, including the basic balance sheet and income statement, and discuss theinterrelationship between them.2.Provide a framework for analyzing bank performance over time and relative to peer banks. Introduce key financial ratios that can be used to evaluate profitability and the different types of risks faced by banks. Focus on the trade-off between bank profitability and risk.3.Identify performance measures that differentiate between small, independent banks (specialty banks) and largerbanks that are part of multibank holding companies or financial holding companies.4. Distinguish between types of bank risk; credit, liquidity, interest rate, capital, operational, and reputational.5. Describe the nature of and meaning of regulatory CAMELS ratings for banks.6.Provide applications of data analysis to sample banks’ financial information.7.Describe performance characteristics of different-sized banks.8. Describe how banks can manipulate financial information to ‘window-dress’ performance.Key Concepts1. Bank managers must balance banking risks and returns because there is a fundamental trade-off between profitability, liquidity, asset quality, market risk and solvency. Decisions that increase banking risk must offer above average profits. The more liquid a bank is and the more equity capital used to fund operations, the less profitable is a bank, ceteris paribus.2. Banks face five basic types of risk in day-to-day operations: credit risk, liquidity risk, market risk, capital/solvency risk, and operational risk. Market risk encompasses interest rate risk, foreign exchange risk and price risk. Each type of risk refers to the potential variation in a ba nk's net income or market value of stockholders’ equity resulting from problems that affect that part of the bank's activities.3. Banks also face risks in the areas of country risk associated with loans or other activity with foreign government units and off-balance sheet activities, which create contingent liabilities. More recently, banks have focused on reputation risk. For example, from 2002-2005 Citigroup, JP Morgan Chase, and Bank of America found that even though they continued to report strong pro fits, they experienced strong criticism for 1) their roles in facilitating strategies to disguise Enron’s true financial status, 2) problems in sub-prime lending programs via the Associates Corp. and their own internal finance company activities, 3) problems with underwriting subsidiaries with analyst conflicts between stock reports and the firm’s investment banking relationships; facilitating market timing of stock trades to their detriment of their own mutual fund holders, 4) lack of supervision of trading groups, and 5) facilitating improper borrowing at Parmalat.4. A bank's return on equity (ROE) can be decomposed in terms of the duPont system of financial ratio analysis. This examination of historical balance sheet and income statement data enables an analyst to evaluate the comparative strengths and weaknesses of performance over time and versus peer banks. The Uniform Bank Performance Report (UBPR) data reflect the basic ratios from this return on equity model.5. Different-sized commercial banks exhibit different operating characteristics and thus performance measures. Small banks typically report a higher return on assets (ROA) than large banks because they earn higher gross yields on assets and pay less interest on liabilities.6. High performance banks generally benefit from lower interest and non-interest expense and limit credit risk so that loan losses are relatively low. They also operate with above average stockholders' equity.7. Many banks can successfully "window-dress" performance by manipulating the reporting of financial data. They may accelerate revenue recognition and defer expenses or selectively alter when they take securities gains or losses and time when to charge off loans or report loans as non-performing. As such, they may inappropriately smooth earnings with provisions for loan losses or by other means. Analysts must be careful when evaluating extraordinary transactions that have one-time gain or loss features.Answers to End of Chapter Questions1. For a large bank, assets consist approximately of marketable securities (20%), loans (70%), and other assets (10%). Liabilities consist of core deposits (40%-60%), noncore, purchased liabilities (20%-40%), and other liabilities (5 %-10%) as a fraction of assets. Small banks typically obtain more funds in the form of core deposits and less in the form of noncore, purchased liabilities. Small banks often invest more in securities as well. Of course, the actual percentages for any bank depend on that bank’s business strategy, mark et competition, and ownership.2. A bank's interest income consists of interest earned on loans and securities while noninterest income includes revenues from deposit service charges, trust department fees, fees from nonbank subsidiaries, etc. Interest expense consists of interest paid on interest-bearing core deposits and noncore liabilities while noninterest expense is comprised of overhead costs, personnel costs, and other costs. A bank’s net interest income equals its interest income minus interest expense. Note that interest income may be calculated on a tax-equivalent basis in which tax-exempt interest is converted to its pre-tax equivalent. A bank’s burden is defined as its noninterest expense minus noninterest income. This is often quoted as a fract ion of total assets. A bank’s efficiency ratio is calculated as noninterest expense divided by the sum of net interest income and noninterest income. The denominator effectively measures net operating revenue after subtracting interest expense. The efficiency ratio measure the noninterest cost per $1of operating revenue generated. Analysts often interpret the efficiency ratio as a measure of a bank’s ability to control overhead relative to its ability to generate noninterest income (and overall revenue). A lower number is presumably better because it reflects better cost control compared with revenue generation.3. Balance sheet accounts:a. Increase liability: money market deposit account (+$5,000)Increase asset: federal funds sold (+$5,000)b. Decrease asset: real estate loanIncrease asset: mortgage loanc. Increase equity: common stock (common and preferred capital)Increase asset: commercial loans4. Income statementInterest on U.S. Treasury & agency securities $44,500Interest on municipal bonds 60,000Interest and fees on loans 189,700Interest income = $294,200Interest paid on interest-checking accounts $33,500Interest paid on time deposits 100,000Interest paid on jumbo CDs 101,000Interest expense = $234,500Net interest income = $59,700Provisions for loan losses = $ 18,000Net interest income after provisions = $41,700Fees received on mortgage originations $23,000Service charge receipts 41,000Trust department income 15,000Non-interest income = $79,000Employee salaries and benefits $145,000Occupancy expense 22,000Non-interest expense = $167,000Income before income taxes -$46,300Income taxes 15,742Net income = -$30,558Cash dividends declared 2,500Retained earnings = -$33,058This assumes that expenses associated with the purchase of the new computer are included in occupancy expense. If not, the computer expense (depreciation) will increase the loss for the period. Also, the bank can receive a tax refund from prior tax payments if the bank made a taxable profit within recent years.5. The primary risks faced by banks are credit risk, liquidity risk, interest rate risk, foreign exchange risk (the latter two represent market risk), operational risk, reputational risk, and capital solvency. In general, promised, or expected, returns should be higher for banks that assume increased risk. There should also be greater volatility in returns over time.a. Credit risk: Net loan charge-offs/LoansHigh risk - high ratio; Low risk - low ratioHigh risk manifests itself in occasional high charge-offs, which requires above average provisions for loan lossses to replenish the loan loss reserve. Thus, net income is volatile over time.b. Liquidity risk: Core deposits/AssetsHigh risk - low ratio; Low risk - high ratioHigh risk manifests itself in less stable funding as a bank relies more on noncore, purchased liabilities thatfluctuate over time. These noncore liabilities are also higher cost, which raises interest expense.c. Interest rate risk: (|Repriceable assets-repriceable liabilities|)/AssetsHigh risk - high ratio; Low risk - low ratioHigh risk banks do not closely match the amount of repriceable assets and repriceable liabilities. Largedifferences suggest that net interest income may vary sharply over time as the level of interest rates changes.d. Foreign exchange risk: Assets denominated in a foreign currency minus liabilities denominated in the same foreign currency.High risk – a large difference; Low risk – a small differenceHigh risk manifests itself when exchange rates change adversely and the value of the bank’s net position of assets versus liabilities denominated in a currency changes sharply.e. Operational risk: total assets/number of employeesHigh risk – low ratio; Low risk – high ratioHigh risk manifests itself when the bank operates at low productivity measured by more employees per amount of assetsf. Capital/solvency risk: Stockholders’ equity/AssetsHigh risk - low ratio; Low risk - high ratioHigh risk manifests itself because fewer assets must go into default before a bank is insolvent and can be closed down by regulators.g. Reputational risk is difficult to measure ex ante. It is more observable by announced problems and issues.6. Equity multiplierBank L: Equity/Assets = 0.06 indicates Assets/Equity = 16.67XBank S: Equity/Assets = 0.10 indicates Assets/Equity = 10XIf each bank earns 1.5% on assets (ROA = 0.015), then the ROEs will equal 25% (Bank L) and 15% (Bank S). If, instead, each bank reports a loss with ROA = -0.012, then the ROEs will equal -20% (Bank L) and -15% (Bank S). When banksare profitable, financial leverage has the positive effect of increasing ROE; when banks report losses, financial leverage increases the magnitude of loss in terms of a negative ROE.7. ROE= net income/stockholders' equityROA = net income/total assetsEM = total assets/stockholders' equityER = total operating expense/total assetsAU = total revenue/total assetsBalance sheet figures should be measured as averages over the period of time the income number is generated.ROE = ROA x EM ROA = AU – ER – TAXwhere TAX = applicable income tax/total assets.8. Profitability ratios differ across banks of different size as measured by assets. The primary reasons are that different size banks have different asset and liability compositions and engage in different amounts of off-balance sheet activities. Typically, small banks report higher net interest margins because their average asset yields are relatively high while their average cost of funds is relatively low. This reflects loans to higher risk borrowers, on average, and proportionately more funding from lower cost core deposits. ROEs, in turn, are often lower because small banks operate with more capital relative to assets, that is with lower equity multipliers, so that even with comparable ROAs the ROEs are lower. Large banks ROAs are increasing faster over time because large banks operate with lower efficiency ratios as they have been more successful in generating fee income.9. CAMELSa. C =capital adequacy: equity/assetsb. A = asset quality: nonperforming loans/loans; loan charge-offs/loansc. M = management: no single ratio is good, although all ratios indicate overall strategyd. E = earnings: aggregate profit ratios; ROE, ROA, net interest margin, burden, efficiencye. L = liquidity: core deposits/assets; noncore, purchased liabilities/assets; marketable securities/assetsf. S = sensitivity to market risk; |repriceable assets-repriceable liabilities|/assets; difference in assets and liabilitiesdenominated in the same currency; size of trading positions in commodities, equities and other tradeable assets.10. Lowest to highest liquidity risk: 3-month T-bills, 5-year Treasury bond, 5-year municipal bond (if high quality and from a known issuer), 4-year car loan with monthly payments (receive some principal monthly, may be saleable), 1-year construction loan, 1-year loan to individual, pledged 3-month T-bill. As stated, the 3-month T-bill that is pledged as collateral is illiquid unless the bank can change its collateral status.11. Comparative credit riska. loan to a comer grocery store representing a little known borrower with uncertain financialsb. loan collateralized with inventory (work in process) because the collateral is less liquid and more difficult to value;this assumes that the receivables are still viable and not too aged.c. normally the Ba-rated municipal bond, unless the agency bond is an "exotic" mortgage backed security, because theagency bond carries an implied guarantee in that Freddie Mac is a quasi-public borrower.d. 1-year car loan because the student loan is typically government guaranteed12. For the balance sheet: high core deposits/assets; high equity/assets; low noncore, purchased liabilities/assets; high investment securities/assets; high agriculture loans/assets (the value refers to that for small banks); For the income statement: net interest margin (high); burden/assets (high), efficiency ratio (high); (the descriptor in parentheses refers to the relationship for small banks versus larger banks).13. Extending a loana. the new loan is typically not classified as nonperforming because no payments are past dueb. often a bank recognizes that the loan is in the problem stage and the borrower renegotiates the terms in its favor;rationale is that the borrower may default if the loan is not restructured. Note that this restructuring gives theappearance that asset quality is higher.c. the primary risk is that the bank is throwing more money down a sink hole and will never recover any of its loan.14. Dividend payment: For: the loss is temporary and stockholders expect the dividend payment. Failure to make the payment will sharply lower the stock price because stockholders will be alienated. Against: the bank has not generated sufficient cash to make the payment from normal operations. By paying the cash dividend, the bank is self-liquidating. The cash dividend will lower the bank’s capital. What normally decides the issue is whether the loss is truly temporary or more permanent. Management typically errs by assuming that losses are temporary, and thus continues to make dividend payments when it should be reducing or eliminating them.15.Liquidity risk:a.Securities classified as held-to-maturity cannot be sold unless there has been an unusual change in the underlyingcredit quality of the security issuer. A high fraction indicates low liquidity because few securities (just 5% of the total) can be sold.b. A low core deposit base indicates a bank that relies proportionately more on noncore, volatile liabilities that are lessstable and more likely to leave the bank if rates change. This makes a bank’s funding sources less reliable and the bank subject to greater liquidity risk.c. A bank that holds long-term securities (8 years is long term) has assumed significant price risk even if the securitiescan be readily sold because they are classified as available-for-sale. Such securities will fall in value if interest rates rise. This indicates high liquidity risk.d.Assuming that $10 million in securities is sufficient, the fact that none are pledged makes them more liquid and isindicative of lower liquidity risk than if any securities were pledged.Problems1. Community National Bank (CNB)1. Profitability analysis for 2004 using UBPR figures:RATIO Community National Bank Peer BanksROE 8.67% 11.72%ROA 0.63 1.09EM 13.97X 10.67XAU 5.91 6.23ER 4.94 4.73TAX 0.34 0.41a.Aggregate profitability for CNB is substantially lower measured both by both ROE and ROA. Because CNB has less equity relative to assets, it has greater financial leverage. Thus, the greater financial leverage increases CNB’s ROE relative to peer banks. The fact that its ROE is lower, despite the greater leverage, indicates that the higher risk does not produce higher overall profitability. CNB has assumed a riskier profile with its greater financial leverage in that fewer assets can default before the bank is insolvent. CNB’s ROA is lower because it earns a lower average yield on assets (AU), pays more in operating expense (ER), offset somewhat by the fact that it pays less in taxes (TAX).b.Risk ComparisonCredit risk: same net charge-offs, much lower nonperforming (more than 90 days past due) and nonaccrual loans, higher provisions for loan losses (.30% versus 0.18%); loan loss reserve is a greater fraction of total loans and leases and a much greater fraction of noncurrent loans. Overall, the ratios indicate below-average risk. Of course, these figures represent only one year of data.Liquidity risk: lower equity to assets suggests higher liquidity risk from a funding perspective, higher available for sale securities and lower pledged securities suggests lower liquidity risk from the asset sale perspective; very high core deposits, low noncore funding (liabilities), low loans and leases and high ST securities suggest lowerliquidity risk. Overall, liquidity risk appears lower because the bank has a strong core deposit base, fewer loans and more securities can be readily sold. Still, the bank might have difficulty borrowing if loans exhibit low qualityand deposit outflows arise. Conclusion: below-average liquidity risk.Capital Risk: low capital to asset ratios; low equity to assets indicate above average capital risk; bank pays less out in dividends and its growth rate in equity capital is lower. Overall, the bank exhibits greater capital risk. Thissituation is offset by the bank’s apparent higher quality assets.Operational risk: low assets to employees ratio, high personnel expense to employees and high efficiency ratio indicate high operational risk. Of course, these data do not capture the likelihood of fraud and other potentialoperational problems.c.Recommendations:1)Impro ve the bank’s capital position; slow asset growth and pursue greater profits.2)Evaluate credit risk carefully; ensure that loans are adequately diversified and that any default of a single loan ortype of loans cannot place the bank’s capital at risk to where regulators will restrict the bank’s activities. Slow loan growth until capital base is at target. Implement a formal credit risk review process.3)Improve operating efficiency. Review noninterest expense sources and cut costs where possible.4)The first t wo suggestions will have the impact of lowering the bank’s earnings, ceteris paribus. Therefore,management should focus on growing sources of noninterest income that currently are not being pursued.2.Citibank UBPRa.In 2004, Citibank’s ROE equaled 15.26% while its ROA equaled 1.49% versus peers’ figures of 14.58% and 1.31%,respectively. Citibank’s equity multiplier (EM = ROE/ROA) equaled approximately 10.24X versus 11.13X for peers. Citibank’s AU is higher at 8.83% (5.25% + 3.58%) versus 7.69% (4.46% + 3.23%) at peers. Citibank clearly generated higher gross revenues from both interest and noninterest sources. Citibank’s expense ratio (ER), in turn, equaled 6.27% while ER for peers was much lower for each type of expense and in total at 4.23%. Based on the profit figures alone, Citibank appears to be a high performance bank and achieves that by generating greater relative revenues.b.Citibank’s credit risk (as evidenced only by the ratios provided) appears high as net losses to loans is higher thanPeers (1.58% versus 0.25%), as is noncurrent loans and leases as a fraction of loans (1.78% versus 0.59%). The loss allowance (reserve) is a higher fraction of loans, but a much smaller fraction of net losses (charge-offs) andnoncurrent loans indicating that more reserves might be appropriate.c.Citibank’s liquidity risk appears high as the bank has a lower equity to asset (tier 1 leverage capital) ratio and reliesmuch more on noncore liabilities (noncore fund dependence). With its greater credit risk, you might expect it to operate with greater equity capital. Similarly, the bank is growing at a fast pace which generally increases overall risk because management cannot easily control risk from growth.d.Recommendations:Carefully assess credit risk; realign portfolio where appropriate.Increase the loan loss reserve.Slow loan growth and/or shift loans to less risky classes.Line up additional sources of liquidity.Review pricing of loans and deposits; identify sources of fees/noninterest income to see if they are sustainable.。

商业银行管理学课后题答案(第三版全)

商业银行:商业银行是以追求利润最大化为目标,以多种金融负债筹集资金,以多种金融资产为其经营对象,能利用负债进行信用创造,并向客户提供多功能、综合性服务的金融企业。

信用中介:是指商业银行通过负债业务,把社会上各种闲散货币资金集中到银行,通过资产业务,把它投向需要资金的各部门,充当有闲置资金者和资金短缺者之间的中介人,实现资金的融通。

作用:使闲散的货币转化为资本、使闲置资本得到充分利用、续短为长,满足这会对长期资本的需要。

支付中介:是指商业银行利用活期存款账户,为客户办理各种货币结算、货币收付、货币兑换和转移存款等业务活动。

CAMELS:美国联邦储备委员会对商业银行监管的分类检查制度,这类分类检查制度的主要内容是把商业银行接受检查的范围分为六大类:资本(capital)、资产(asset)、管理(management)、收益(earning)、流动性(liquidity)和对市场风险的敏感性(sensitivity)。

分行制:分行制银行是指那些在总行之下,可在本地或外地设有若干分支机构,并可以从事银行业务的商业银行。

这种商业银行的总部一般都设在大都市,下属所有分支行须由总行领导指挥。

优点:第一,有利于银行吸收存款,有利于银行扩大资本总额和经营规模,能取得规模经济效益。

第二,便于银行使用现代化管理手段和设备,提高服务质量,加快资金周转速度。

第三有利于银行调节资金、转移信用、分散和减轻多种风险。

第四,总行家数少,有利于国家控制和管理,其业务经营受地方政府干预小。

第五,由于资金来源广泛,有利于提高银行的竞争实力。

缺点:容易加速垄断的形成;并且由于其规模大,内部层次较多,使银行管理的难度增加等。

流动性:指资产变现的能力,商业银行保持随时能以适当的价格去的可用资金的能力,以便随时应付客户提存以及银行其他支付的需要。

其衡量指标有两个:一是资产变现的成本,二是资产变现的速度。

4.建立商业银行制度的基本原则有哪些?为什么要确立这些原则?答:(一)有利于银行业竞争。

《商业银行经营与管理》(毛秋容)作业集答案(专本科函授)

1、商业银行具有信用创造功能,其信用创造功能有一定的限度。

答:正确。

商业银行信用创造要受诸多因素的制约,一是要以存款为基础,二是要受中央银行准备金率,自身现金准备率的制约,三是要以有贷款要求为前提,如果没有足够的贷款需求,存款贷不出去就不能信用创造。

2、现金结算发展到非现金结算。

3、从买卖双方的直接结算向以银行为中介的结算发展。

4、货物单据化、履约证书化。

5、国际结算的发展趋势:电子化、无纸化、标准化和一体化。

1、按照国际惯例进行国际结算。

2、国际结算使用可兑换货币进行结算。

3、实行“推定交货”的原理。

4、商业银行成为结算和融资的中心。

4、答:主要有三大类:(1)汇款方式(International Remittance)通过银行的汇兑来实现国与国之间的债权债务的清偿和国际资金的转移。

(2)托收方式(Collection)出口方委托本地银行,通过进口地银行向进口方提2、按照目前的法律规定,中国公民可以成为商业银行的股东。

答:在目前的条件下,中国政府允许民间借款的存在,但不允许私人钱庄的存在。

3、深圳发展银行属于公开发行股份的银行,因此其股份可以上市交易。

答:深圳发展银行股份由三部分组成,一是国家股,二是企业股,三是社会公众股,前两部分股份不参考答案第一章导论一、名词解释1、商业银行:是以追求最大利润为目标,以多种金融负债筹集资金,以多种金融资产为其经营对象,能利用负债进行信用创造,并向客户提供多功能、综合性服务的金融企业。

2、信用创造:指商业银行利用其可以吸收活期存款的有利条件,通过发放借款,从事投资业务,而衍生出更多存款,从而扩大社会货币供给量。

3、单元制银行:指那些不设立或不能设立分支机构的商业银行,这种银行主要集中在美国。

4、分行制银行:是指那些在总行之下,可在本地或外地设有若干分支机构,并都可从事银行业务的商业银行,这种商业银行的总部一般都设在大都市,下属所有分支行处须由总行领导指挥。

商业银行管理彼得S.罗斯第八版课后答案

商业银行管理彼得S.罗斯第八版课后答案第一章现代商业银行的概述1.解释现代商业银行的定义和特点。

商业银行是一种金融机构,主要从事存款、贷款、支付和其他与金融活动相关的业务。

其特点包括但不限于:收取利息和手续费、进行风险管理、提供信贷和储蓄服务、发行货币等。

2.列举现代商业银行的主要功能。

现代商业银行的主要功能包括但不限于:存款业务、贷款业务、国际业务、支付结算、外汇交易、信用和担保、投资银行业务、资金运作等。

3.商业银行与其他金融机构的区别是什么?和其他金融机构相比,商业银行的最大区别在于其可以发行货币,并具有相应的存储和支付功能。

此外,商业银行还可以从中央银行和其他金融机构获得流动性支持。

此外,商业银行还拥有广泛的客户群体和网络,可以提供多样化的金融产品和服务。

第二章商业银行的治理结构1.解释商业银行的治理结构。

商业银行的治理结构是指银行内各个决策层级和机构之间相互关系的安排和管理方式。

这包括董事会、监事会、高级管理层等。

2.详细描述商业银行治理结构中各种角色的职责和权力。

•董事会:负责制定银行的战略方向和政策,监督高级管理层的工作表现。

•监事会:负责审计和监督董事会和高级管理层的工作,确保其合法、合规。

•高级管理层:负责银行的日常经营管理,执行董事会决策,负责风险管理和业绩目标的实现。

•内部控制机构:负责制定和实施内部控制制度,保障银行运营的合规性和风险控制。

3.商业银行的治理结构有哪些挑战和改进措施?商业银行的治理结构面临的主要挑战包括:信息不对称、利益冲突、监管合规等。

为了改善这些问题,银行可以采取以下措施:加强内部控制机制、设立独立董事、加强风险管理和合规审查等。

第三章商业银行的资本管理1.商业银行为什么需要资本?商业银行需要资本来保证其业务的顺利运作。

资本可以用于覆盖银行风险、偿还债务、承担损失等。

同时,一定水平的资本也是银行移植的法定要求。

2.商业银行的资本可以来源于哪些渠道?商业银行资本的主要来源有:股东投资、利润留存、债务融资、政府注资等。

第二编第二章商业银行法

第二编第二章商业银行法字体:大中小打印全部打印客观题打印主观题本试卷在答题过程中可能要用到“公式编辑器”,请点击此处安装插件!一、单项选择题1.设立全国性商业银行的注册资本最低限额为人民币()。

A.10亿元B.5亿元C.1亿元D.5千万元【本题1分,建议1.0分钟内完成本题】【加入打印收藏夹】【加入我的收藏夹】【隐藏答案】【正确答案】:A【答案解析】:《商业银行法》第13条第1款规定:“设立全国性商业银行的注册资本最低限额为10亿元人民币。

设立城市商业银行的注册资本最低限额为1亿元人民币,设立农村商业银行的注册资本最低限额为5千万元人民币。

注册资本应当是实缴资本。

”2.商业银行拨付各分支机构营运资金额的总和,不得超过总行资本金总额的()。

A.70%B.60%C.50%D.40%【本题1分,建议1.0分钟内完成本题】【加入打印收藏夹】【加入我的收藏夹】【隐藏答案】【正确答案】:B【答案解析】:《商业银行法》第19条第2款规定:“商业银行在中华人民共和国境内设立分支机构,应当按照规定拨付与其经营规模相适应的营运资金额。

拨付各分支机构营运资金额的总和,不得超过总行资本金总额的百分之六十。

”3.商业银行的“三性”经营原则不包括()。

A.安全性原则B.流动性原则C.法定性原则D.效益性原则【本题1分,建议1.0分钟内完成本题】【加入打印收藏夹】【加入我的收藏夹】【隐藏答案】【正确答案】:C【答案解析】:所谓商业银行的“三性”经营原则,是指商业银行的效益性原则、安全性原则和流动性原则。

4.依据我国《商业银行法》的规定,商业银行贷款,其资本充足率不得低于()。

A.5%B.7%C.8%D.10%【本题1分,建议1.0分钟内完成本题】【加入打印收藏夹】【加入我的收藏夹】【隐藏答案】【正确答案】:C【答案解析】:依据我国《商业银行法》第39条的规定,商业银行贷款,应当遵守下列资产负债比例管理的规定:(1)资本充足率不得低于8﹪;(2)贷款余额与存款余额的比例不得超过75﹪;(3)流动性资产余额与流动性负债余额的比例不得低于25﹪;(4)对同一借款人的贷款余额与商业银行资本余额的比例不得超过10﹪;(5)国务院银行业监督管理机构对资产负债比例管理的其他规定。

《商业银行管理学》课后习题参考答案

《商业银行管理学》课后习题参考答案第一章1.金融制度对现代经济体系的运行起到了什么作用?(1)配置功能(2)节约功能(3)激励功能(4)调节功能2.商业银行在整个金融体系中有哪些功能?(1)金融服务功能(2)信用创造功能3.美国、英国、日本和德国的商业银行制度特征是什么?比较英美和日德的银行制度差异。

美国:是金融制度创新和金融产品创新的中心,拥有健全的法律法规对银行进行管制;竞争的激烈,使得美国商业银行具有完善的管理体系和较高的管理水平;受到双重银行体系的管制,即联邦和州权力机构都掌握着管制银行的权利。

英国:成立最早,经验丰富,实行分支行制;银行系统种类齐全、数量众多,按英国的分类,英国的银行主要包括清算银行,商人银行,贴现行,其他英国银行和海外银行等机构;不存在正式的制度化的银行管理机构,惟一的监管机构是作为中央银行的英格兰银行;典型的实行分业经营的国家。

日本:货币的统一发行集中到中央银行-日本银行;商业银行按区域划分的,具体可分为两大类型,即都市银行和地方银行;受到广泛的政府管制;二战前仿效英国业务分离的做法,之后随着环境的变化和经济的发展日本银行从1998年开始实行混业经营。

德国:由统一的中央银行-德意志联邦银行,统一发行货币,且德意志联邦银行被认为是欧洲各国中最具有独立性的中央银行。

德国银行高度集中,实行全能化的银行制度,密集程度是欧盟各国中最高的。

区别:英美在其业务上侧重存款的管理,而日德则侧重在贷款方面。

英美制度完善,有利于银行之间的竞争,日德法律体系发展相对缓慢。

4.根据你对我国银行业的认识,讨论我国银行业在国民经济中的地位以及制度特征。

答:地位:(1)我国的商业银行已成为整个国民经济活动的中枢(2)我国的商业银行的业务活动对全社会的货币供给具有重要影响(3)商业银行已经成为社会经济活动的信息中心(4)商业银行已经成为国家实施宏观经济政策的重要途径和基础(5)商业银行成了社会资本运动的中心制度特征:建立商业银行原则,有利于银行竞争,有利于保护银行体系安全与稳定,使银行保持适当规模。

商业银行业务与经营第二章的形考题及答案

商业银行业务与经营第二章的形考题及答案商业银行业务与经营第二章的形考题及答案注意:选项(abcd)后面数字是一道题对这题的的评分,也就是答案,如果是0,是错误的,.就不要选择。

绿色为:单选题蓝色为:多选题紫色为:判断题top/第2章/判断题判断题银行通过发放普通股和优先股所形成的资本是最基本、最稳定的银行资本,属于商业银行的内源资本。

()对0错100判断题银行优先股构成银行资本的核心部分,它不仅代表对银行的所有权,而且具有永久性质。

()对0错100判断题.一般而言,银行优先股持有人按固定股息率取得股息,对银行清算的剩余资产的分配权优于普通股持有人,不拥有对银行的表决权。

()对100错0判断题留存收益的大小取决于银行盈利性大小、股息政策及税率等因素。

留存收益的多少是这些因素综合作用的结果。

通常,盈利性越强,留存收益越大,反之,则越小;股息支付率越高,留存收益越少;所得税率越高,企业留存越少。

()对100错0判断题储备金是为了应付未来回购、赎回资本债务或防止意外损失而建立的基金,包括放款与证券损失准备金和偿债基金等。

()对100错0判断题资本数量越大,盈利性越大。

()对0错100判断题资本结构的合理性是指普通股、优先股、留存盈余、债务资本等应在资本总额中占有合理的比重。

()对100错0判断题《巴塞尔协议》定义银行资本的逻辑和依据为:银行资本的构成部分应取决于银行资本的不同形式。

()对0错100判断题《巴塞尔协议I》未考虑利率、证券价格、汇率等不利变动给银行造成损失的市场风险。

()对100错0判断题《巴塞尔协议I》的不足在于对金融市场的创新不敏感以及用相同的方法估计风险并据此确定银行资本要求。

()对100错0判断题“分母对策”是针对《巴塞尔协议》中的资本计算方法,尽量地提高商业银行的资本总量,改善和优化资本结构。

()对0错100判断题外源资本策略为:对核心资本不足的银行来说,一般通过发行新股方式来增加资本,同时应充分考虑这种方式的可得性、能否为将来进一步筹集资本提供灵活性以及可能造成的金融后果。

商业银行经营管理练习题及答案

商业银行经营管理练习题及答案第一章商业银行概述一、单项选择题1、1694年,(D)的成立标志着现代商业银行制度的建立。

A、威尼斯银行B、阿姆斯特丹银行C、汉堡银行D、英格兰银行2、1897年在上海成立的(C)标志着中国现代银行的产生。

A、交通银行B、浙江兴业银行C、中国通商银行D、北洋银行3、商业银行把资金从盈余者手中转移到短缺者手中,使闲置资金得到充分的运用,这种职能被称为商业银行的(A)职能。

A、信用中介B、支付中介C、信用创造D、金融服务4、(A)是商业银行最基本也最能反映其经营活动特征的职能。

A、信用中介B、支付中介C、清算中介D、调节经济的职能5、商业银行利用活期存款账户,为客户办理货币结算、转账、兑换、转移存款等业务,这种功能被称为(B)功能。

A信用中介B支付中介C信用创造D金融服务6、商业银行利用吸收的活期存款,通过转账的方式发放贷款,从而衍生出更多存款,扩大社会货币供给量。

这种功能被称为(C)功能。

A信用中介B支付中介C信用创造D金融服务7、下列说法不正确的是(B)。

A、银行的普通股股东拥有表决权B、银行的优先股股东拥有表决权C、股东大会有权选举董事和监事D、股东大会可以决定银行的经营方针和投资计划8、商业银行经营活动的最终目标是(C)。

A、安全性目标B、流动性目标C、盈利性目标D、合法性目标9、属于商业银行一级准备的是(C)。

A、短期证券B、短期票据C、库存现金D、存款更多精品文档.学习-----好资料10、商业银行是(B)。

A、事业单位B、特殊企业C、国家机关D、商业机构二、多项选择题1、商业银行的职能有(ABCD)。

A、信用中介职能B、支付中介职能C、信用创造职能D、金融服务职能2、现代商业银行产生途径有(AB)。

A、早期银行转变过来B、股份制形式组建C、货币兑换D、货币经营业3、商业银行的经营原则是(BCD)。

A、政策性B、安全性C、流动性D、盈利性4、商业银行面临的风险主要有(ABD ABCD)。

商业银行业务与经营第二章的形考题及答案

商业银行业务与经营第二章的形考题及答案注意:选项(abcd)后面数字是一道题对这题的的评分,也就是答案,如果是0,是错误的,.就不要选择。

绿色为:单选题蓝色为:多选题紫色为:判断题top/第2章/判断题判断题银行通过发放普通股和优先股所形成的资本是最基本、最稳定的银行资本,属于商业银行的内源资本。

()对0错100判断题银行优先股构成银行资本的核心部分,它不仅代表对银行的所有权,而且具有永久性质。

()对0错100判断题.一般而言,银行优先股持有人按固定股息率取得股息,对银行清算的剩余资产的分配权优于普通股持有人,不拥有对银行的表决权。

()对100错0判断题留存收益的大小取决于银行盈利性大小、股息政策及税率等因素。

留存收益的多少是这些因素综合作用的结果。

通常,盈利性越强,留存收益越大,反之,则越小;股息支付率越高,留存收益越少;所得税率越高,企业留存越少。

()对100错0判断题储备金是为了应付未来回购、赎回资本债务或防止意外损失而建立的基金,包括放款与证券损失准备金和偿债基金等。

()对100错0判断题资本数量越大,盈利性越大。

()对0错100判断题资本结构的合理性是指普通股、优先股、留存盈余、债务资本等应在资本总额中占有合理的比重。

()对100错0判断题《巴塞尔协议》定义银行资本的逻辑和依据为:银行资本的构成部分应取决于银行资本的不同形式。

()对0错100判断题《巴塞尔协议I》未考虑利率、证券价格、汇率等不利变动给银行造成损失的市场风险。

()对100错0判断题《巴塞尔协议I》的不足在于对金融市场的创新不敏感以及用相同的方法估计风险并据此确定银行资本要求。

()对100错0判断题“分母对策”是针对《巴塞尔协议》中的资本计算方法,尽量地提高商业银行的资本总量,改善和优化资本结构。

()对0错100判断题外源资本策略为:对核心资本不足的银行来说,一般通过发行新股方式来增加资本,同时应充分考虑这种方式的可得性、能否为将来进一步筹集资本提供灵活性以及可能造成的金融后果。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Chapter 2Analyzing Bank PerformanceChapter Objectives1.Introduce bank financial statements, including the basic balance sheet and income statement, and discuss theinterrelationship between them.2.Provide a framework for analyzing bank performance over time and relative to peer banks. Introduce key financial ratios that can be used to evaluate profitability and the different types of risks faced by banks. Focus on the trade-off between bank profitability and risk.3.Identify performance measures that differentiate between small, independent banks (specialty banks) and largerbanks that are part of multibank holding companies or financial holding companies.4. Distinguish between types of bank risk; credit, liquidity, interest rate, capital, operational, and reputational.5. Describe the nature of and meaning of regulatory CAMELS ratings for banks.6.Provide applications of data analysis to sample banks’ financial information.7.Describe performance characteristics of different-sized banks.8. Describe how banks can manipulate financial information to ‘window-dress’ performance.Key Concepts1. Bank managers must balance banking risks and returns because there is a fundamental trade-off between profitability, liquidity, asset quality, market risk and solvency. Decisions that increase banking risk must offer above average profits. The more liquid a bank is and the more equity capital used to fund operations, the less profitable is a bank, ceteris paribus.2. Banks face five basic types of risk in day-to-day operations: credit risk, liquidity risk, market risk, capital/solvency risk, and operational risk. Market risk encompasses interest rate risk, foreign exchange risk and price risk. Each type of risk refers to the potential variation in a ba nk's net income or market value of stockholders’ equity resulting from problems that affect that part of the bank's activities.3. Banks also face risks in the areas of country risk associated with loans or other activity with foreign government units and off-balance sheet activities, which create contingent liabilities. More recently, banks have focused on reputation risk. For example, from 2002-2005 Citigroup, JP Morgan Chase, and Bank of America found that even though they continued to report strong pro fits, they experienced strong criticism for 1) their roles in facilitating strategies to disguise Enron’s true financial status, 2) problems in sub-prime lending programs via the Associates Corp. and their own internal finance company activities, 3) problems with underwriting subsidiaries with analyst conflicts between stock reports and the firm’s investment banking relationships; facilitating market timing of stock trades to their detriment of their own mutual fund holders, 4) lack of supervision of trading groups, and 5) facilitating improper borrowing at Parmalat.4. A bank's return on equity (ROE) can be decomposed in terms of the duPont system of financial ratio analysis. This examination of historical balance sheet and income statement data enables an analyst to evaluate the comparative strengths and weaknesses of performance over time and versus peer banks. The Uniform Bank Performance Report (UBPR) data reflect the basic ratios from this return on equity model.5. Different-sized commercial banks exhibit different operating characteristics and thus performance measures. Small banks typically report a higher return on assets (ROA) than large banks because they earn higher gross yields on assets and pay less interest on liabilities.6. High performance banks generally benefit from lower interest and non-interest expense and limit credit risk so that loan losses are relatively low. They also operate with above average stockholders' equity.7. Many banks can successfully "window-dress" performance by manipulating the reporting of financial data. They may accelerate revenue recognition and defer expenses or selectively alter when they take securities gains or losses and time when to charge off loans or report loans as non-performing. As such, they may inappropriately smooth earnings with provisions for loan losses or by other means. Analysts must be careful when evaluating extraordinary transactions that have one-time gain or loss features.Answers to End of Chapter Questions1. For a large bank, assets consist approximately of marketable securities (20%), loans (70%), and other assets (10%). Liabilities consist of core deposits (40%-60%), noncore, purchased liabilities (20%-40%), and other liabilities (5 %-10%) as a fraction of assets. Small banks typically obtain more funds in the form of core deposits and less in the form of noncore, purchased liabilities. Small banks often invest more in securities as well. Of course, the actual percentages for any bank depend on that bank’s business strategy, mark et competition, and ownership.2. A bank's interest income consists of interest earned on loans and securities while noninterest income includes revenues from deposit service charges, trust department fees, fees from nonbank subsidiaries, etc. Interest expense consists of interest paid on interest-bearing core deposits and noncore liabilities while noninterest expense is comprised of overhead costs, personnel costs, and other costs. A bank’s net interest income equals its interest income minus interest expense. Note that interest income may be calculated on a tax-equivalent basis in which tax-exempt interest is converted to its pre-tax equivalent. A bank’s burden is defined as its noninterest expense minus noninterest income. This is often quoted as a fract ion of total assets. A bank’s efficiency ratio is calculated as noninterest expense divided by the sum of net interest income and noninterest income. The denominator effectively measures net operating revenue after subtracting interest expense. The efficiency ratio measure the noninterest cost per $1of operating revenue generated. Analysts often interpret the efficiency ratio as a measure of a bank’s ability to control overhead relative to its ability to generate noninterest income (and overall revenue). A lower number is presumably better because it reflects better cost control compared with revenue generation.3. Balance sheet accounts:a. Increase liability: money market deposit account (+$5,000)Increase asset: federal funds sold (+$5,000)b. Decrease asset: real estate loanIncrease asset: mortgage loanc. Increase equity: common stock (common and preferred capital)Increase asset: commercial loans4. Income statementInterest on U.S. Treasury & agency securities $44,500Interest on municipal bonds 60,000Interest and fees on loans 189,700Interest income = $294,200Interest paid on interest-checking accounts $33,500Interest paid on time deposits 100,000Interest paid on jumbo CDs 101,000Interest expense = $234,500Net interest income = $59,700Provisions for loan losses = $ 18,000Net interest income after provisions = $41,700Fees received on mortgage originations $23,000Service charge receipts 41,000Trust department income 15,000Non-interest income = $79,000Employee salaries and benefits $145,000Occupancy expense 22,000Non-interest expense = $167,000Income before income taxes -$46,300Income taxes 15,742Net income = -$30,558Cash dividends declared 2,500Retained earnings = -$33,058This assumes that expenses associated with the purchase of the new computer are included in occupancy expense. If not, the computer expense (depreciation) will increase the loss for the period. Also, the bank can receive a tax refund from prior tax payments if the bank made a taxable profit within recent years.5. The primary risks faced by banks are credit risk, liquidity risk, interest rate risk, foreign exchange risk (the latter two represent market risk), operational risk, reputational risk, and capital solvency. In general, promised, or expected, returns should be higher for banks that assume increased risk. There should also be greater volatility in returns over time.a. Credit risk: Net loan charge-offs/LoansHigh risk - high ratio; Low risk - low ratioHigh risk manifests itself in occasional high charge-offs, which requires above average provisions for loan lossses to replenish the loan loss reserve. Thus, net income is volatile over time.b. Liquidity risk: Core deposits/AssetsHigh risk - low ratio; Low risk - high ratioHigh risk manifests itself in less stable funding as a bank relies more on noncore, purchased liabilities thatfluctuate over time. These noncore liabilities are also higher cost, which raises interest expense.c. Interest rate risk: (|Repriceable assets-repriceable liabilities|)/AssetsHigh risk - high ratio; Low risk - low ratioHigh risk banks do not closely match the amount of repriceable assets and repriceable liabilities. Largedifferences suggest that net interest income may vary sharply over time as the level of interest rates changes.d. Foreign exchange risk: Assets denominated in a foreign currency minus liabilities denominated in the same foreign currency.High risk – a large difference; Low risk – a small differenceHigh risk manifests itself when exchange rates change adversely and the value of the bank’s net position of assets versus liabilities denominated in a currency changes sharply.e. Operational risk: total assets/number of employeesHigh risk – low ratio; Low risk – high ratioHigh risk manifests itself when the bank operates at low productivity measured by more employees per amount of assetsf. Capital/solvency risk: Stockholders’ equity/AssetsHigh risk - low ratio; Low risk - high ratioHigh risk manifests itself because fewer assets must go into default before a bank is insolvent and can be closed down by regulators.g. Reputational risk is difficult to measure ex ante. It is more observable by announced problems and issues.6. Equity multiplierBank L: Equity/Assets = 0.06 indicates Assets/Equity = 16.67XBank S: Equity/Assets = 0.10 indicates Assets/Equity = 10XIf each bank earns 1.5% on assets (ROA = 0.015), then the ROEs will equal 25% (Bank L) and 15% (Bank S). If, instead, each bank reports a loss with ROA = -0.012, then the ROEs will equal -20% (Bank L) and -15% (Bank S). When banksare profitable, financial leverage has the positive effect of increasing ROE; when banks report losses, financial leverage increases the magnitude of loss in terms of a negative ROE.7. ROE= net income/stockholders' equityROA = net income/total assetsEM = total assets/stockholders' equityER = total operating expense/total assetsAU = total revenue/total assetsBalance sheet figures should be measured as averages over the period of time the income number is generated.ROE = ROA x EM ROA = AU – ER – TAXwhere TAX = applicable income tax/total assets.8. Profitability ratios differ across banks of different size as measured by assets. The primary reasons are that different size banks have different asset and liability compositions and engage in different amounts of off-balance sheet activities. Typically, small banks report higher net interest margins because their average asset yields are relatively high while their average cost of funds is relatively low. This reflects loans to higher risk borrowers, on average, and proportionately more funding from lower cost core deposits. ROEs, in turn, are often lower because small banks operate with more capital relative to assets, that is with lower equity multipliers, so that even with comparable ROAs the ROEs are lower. Large banks ROAs are increasing faster over time because large banks operate with lower efficiency ratios as they have been more successful in generating fee income.9. CAMELSa. C =capital adequacy: equity/assetsb. A = asset quality: nonperforming loans/loans; loan charge-offs/loansc. M = management: no single ratio is good, although all ratios indicate overall strategyd. E = earnings: aggregate profit ratios; ROE, ROA, net interest margin, burden, efficiencye. L = liquidity: core deposits/assets; noncore, purchased liabilities/assets; marketable securities/assetsf. S = sensitivity to market risk; |repriceable assets-repriceable liabilities|/assets; difference in assets and liabilitiesdenominated in the same currency; size of trading positions in commodities, equities and other tradeable assets.10. Lowest to highest liquidity risk: 3-month T-bills, 5-year Treasury bond, 5-year municipal bond (if high quality and from a known issuer), 4-year car loan with monthly payments (receive some principal monthly, may be saleable), 1-year construction loan, 1-year loan to individual, pledged 3-month T-bill. As stated, the 3-month T-bill that is pledged as collateral is illiquid unless the bank can change its collateral status.11. Comparative credit riska. loan to a comer grocery store representing a little known borrower with uncertain financialsb. loan collateralized with inventory (work in process) because the collateral is less liquid and more difficult to value;this assumes that the receivables are still viable and not too aged.c. normally the Ba-rated municipal bond, unless the agency bond is an "exotic" mortgage backed security, because theagency bond carries an implied guarantee in that Freddie Mac is a quasi-public borrower.d. 1-year car loan because the student loan is typically government guaranteed12. For the balance sheet: high core deposits/assets; high equity/assets; low noncore, purchased liabilities/assets; high investment securities/assets; high agriculture loans/assets (the value refers to that for small banks); For the income statement: net interest margin (high); burden/assets (high), efficiency ratio (high); (the descriptor in parentheses refers to the relationship for small banks versus larger banks).13. Extending a loana. the new loan is typically not classified as nonperforming because no payments are past dueb. often a bank recognizes that the loan is in the problem stage and the borrower renegotiates the terms in its favor;rationale is that the borrower may default if the loan is not restructured. Note that this restructuring gives theappearance that asset quality is higher.c. the primary risk is that the bank is throwing more money down a sink hole and will never recover any of its loan.14. Dividend payment: For: the loss is temporary and stockholders expect the dividend payment. Failure to make the payment will sharply lower the stock price because stockholders will be alienated. Against: the bank has not generated sufficient cash to make the payment from normal operations. By paying the cash dividend, the bank is self-liquidating. The cash dividend will lower the bank’s capital. What normally decides the issue is whether the loss is truly temporary or more permanent. Management typically errs by assuming that losses are temporary, and thus continues to make dividend payments when it should be reducing or eliminating them.15.Liquidity risk:a.Securities classified as held-to-maturity cannot be sold unless there has been an unusual change in the underlyingcredit quality of the security issuer. A high fraction indicates low liquidity because few securities (just 5% of the total) can be sold.b. A low core deposit base indicates a bank that relies proportionately more on noncore, volatile liabilities that are lessstable and more likely to leave the bank if rates change. This makes a bank’s funding sources less reliable and the bank subject to greater liquidity risk.c. A bank that holds long-term securities (8 years is long term) has assumed significant price risk even if the securitiescan be readily sold because they are classified as available-for-sale. Such securities will fall in value if interest rates rise. This indicates high liquidity risk.d.Assuming that $10 million in securities is sufficient, the fact that none are pledged makes them more liquid and isindicative of lower liquidity risk than if any securities were pledged.Problems1. Community National Bank (CNB)1. Profitability analysis for 2004 using UBPR figures:RATIO Community National Bank Peer BanksROE 8.67% 11.72%ROA 0.63 1.09EM 13.97X 10.67XAU 5.91 6.23ER 4.94 4.73TAX 0.34 0.41a.Aggregate profitability for CNB is substantially lower measured both by both ROE and ROA. Because CNB has less equity relative to assets, it has greater financial leverage. Thus, the greater financial leverage increases CNB’s ROE relative to peer banks. The fact that its ROE is lower, despite the greater leverage, indicates that the higher risk does not produce higher overall profitability. CNB has assumed a riskier profile with its greater financial leverage in that fewer assets can default before the bank is insolvent. CNB’s ROA is lower because it earns a lower average yield on assets (AU), pays more in operating expense (ER), offset somewhat by the fact that it pays less in taxes (TAX).b.Risk ComparisonCredit risk: same net charge-offs, much lower nonperforming (more than 90 days past due) and nonaccrual loans, higher provisions for loan losses (.30% versus 0.18%); loan loss reserve is a greater fraction of total loans and leases and a much greater fraction of noncurrent loans. Overall, the ratios indicate below-average risk. Of course, these figures represent only one year of data.Liquidity risk: lower equity to assets suggests higher liquidity risk from a funding perspective, higher available for sale securities and lower pledged securities suggests lower liquidity risk from the asset sale perspective; very high core deposits, low noncore funding (liabilities), low loans and leases and high ST securities suggest lowerliquidity risk. Overall, liquidity risk appears lower because the bank has a strong core deposit base, fewer loans and more securities can be readily sold. Still, the bank might have difficulty borrowing if loans exhibit low qualityand deposit outflows arise. Conclusion: below-average liquidity risk.Capital Risk: low capital to asset ratios; low equity to assets indicate above average capital risk; bank pays less out in dividends and its growth rate in equity capital is lower. Overall, the bank exhibits greater capital risk. Thissituation is offset by the bank’s apparent higher quality assets.Operational risk: low assets to employees ratio, high personnel expense to employees and high efficiency ratio indicate high operational risk. Of course, these data do not capture the likelihood of fraud and other potentialoperational problems.c.Recommendations:1)Impro ve the bank’s capital position; slow asset growth and pursue greater profits.2)Evaluate credit risk carefully; ensure that loans are adequately diversified and that any default of a single loan ortype of loans cannot place the bank’s capital at risk to where regulators will restrict the bank’s activities. Slow loan growth until capital base is at target. Implement a formal credit risk review process.3)Improve operating efficiency. Review noninterest expense sources and cut costs where possible.4)The first t wo suggestions will have the impact of lowering the bank’s earnings, ceteris paribus. Therefore,management should focus on growing sources of noninterest income that currently are not being pursued.2.Citibank UBPRa.In 2004, Citibank’s ROE equaled 15.26% while its ROA equaled 1.49% versus peers’ figures of 14.58% and 1.31%,respectively. Citibank’s equity multiplier (EM = ROE/ROA) equaled approximately 10.24X versus 11.13X for peers. Citibank’s AU is higher at 8.83% (5.25% + 3.58%) versus 7.69% (4.46% + 3.23%) at peers. Citibank clearly generated higher gross revenues from both interest and noninterest sources. Citibank’s expense ratio (ER), in turn, equaled 6.27% while ER for peers was much lower for each type of expense and in total at 4.23%. Based on the profit figures alone, Citibank appears to be a high performance bank and achieves that by generating greater relative revenues.b.Citibank’s credit risk (as evidenced only by the ratios provided) appears high as net losses to loans is higher thanPeers (1.58% versus 0.25%), as is noncurrent loans and leases as a fraction of loans (1.78% versus 0.59%). The loss allowance (reserve) is a higher fraction of loans, but a much smaller fraction of net losses (charge-offs) andnoncurrent loans indicating that more reserves might be appropriate.c.Citibank’s liquidity risk appears high as the bank has a lower equity to asset (tier 1 leverage capital) ratio and reliesmuch more on noncore liabilities (noncore fund dependence). With its greater credit risk, you might expect it to operate with greater equity capital. Similarly, the bank is growing at a fast pace which generally increases overall risk because management cannot easily control risk from growth.d.Recommendations:Carefully assess credit risk; realign portfolio where appropriate.Increase the loan loss reserve.Slow loan growth and/or shift loans to less risky classes.Line up additional sources of liquidity.Review pricing of loans and deposits; identify sources of fees/noninterest income to see if they are sustainable.。