1997年金融危机(英文)

97年亚洲金融危机大事记

97年亚洲金融危机大事记在1997年亚洲金融危机以前,东南亚国家的经济已经连续10年高速增长。

伴随着经济的高速增长,这些国家的银行信贷额以更快的速度增加,短期外债也达到前所未有的水平。

其中相当部分投向房地产。

投资的增加导致资产价格膨胀(主要是泰国和马来西亚)。

此外,汇率制度缺乏弹性也使得大量外债没有考虑汇率风险。

这些都为危机的发生埋下了伏笔。

危机首先从泰国爆发。

1997年3月至6月期间,泰国66家财务公司秘密从泰国银行获得大量流动性支持。

此外,还出现了大量资本逃离泰国。

泰国中央银行将所有的外汇储备用于维护钉住汇率制度,但仍然以失败告终。

7月2日,泰国财政部和中央银行宣布,泰币实行浮动汇率制,泰铢价值由市场来决定,放弃了自1984年以来实行了14年的泰币与美元挂钩的一揽子汇率制。

这标志着亚洲金融危机正式爆发。

很快,危机开始从泰国向其它东南亚国家蔓延,从外汇市场向股票市场蔓延。

7月9日,马来西亚股市指数下跌至18个月来最低点。

菲律宾、马来西亚等国中央银行直接干预外汇市场,支持本国货币。

7月11日,印度尼西亚、菲律宾扩大本国货币的浮动范围。

8月4日,泰国央行行长被迫辞职,新的央行行长猜瓦特上任。

8月13日,印尼财政部和印尼银行联合宣布,放弃钉住美元的汇率政策,实行自由浮动汇率制度,印尼盾大幅下跌55%。

随着危机的发展,以国际货币基金组织为首的国际社会开始向危机国家提供了大量援助。

但这些国家的金融市场仍在恶化,并波及香港和美国市场。

危机国家在采取措施稳定金融市场和金融体系时,也开始进行经济和金融改革。

8月11日,由国际货币基金组织主持的援助泰国国际会议在东京举行。

经过协商,确定对泰国提供约为160亿美元的资金援助,以稳定泰国的经济和金融市场秩序。

香港特区政府首次动用外汇基金,提供10亿美元,参与泰国的贷款计划。

9月1日,菲律宾股票市场继续下跌,菲股综合指数击穿2000点防线,最后以1975.20点收盘,是四年来最低记录。

年泰国金融危机

危机应对措施

b. 紧缩政策

为了控制通货膨胀和偿还外债,泰国实施了一系列的紧缩政策。这些政策包括提高利率、减少政府开支等。然而,这些政策也导致了经济的进一步衰退

危机应对措施

c. 国际援助

为了稳定国内金融市场,泰国接受了国际货币基金组织(IMF)和其他国家的援助。这些援助为泰国提供了急需的外部资金,帮助其稳定经济

危机爆发的原因

b. 房地产泡沫破裂

在泰国经济繁荣时期,房地产市场出现了严重的泡沫。随着经济的降温,房地产需求下降,房价大幅下跌,导致许多投资者破产

危机爆发的原因

c. 汇率波动

在危机爆发前,泰铢与美元的汇率被高估。当市场意识到泰国的经济状况开始恶化时,投资者开始抛售泰铢,导致其汇率大幅下跌

危机的影响

泰国危机的教训

5

泰国危机的教训

-

24

THE PROFESSIONAL TEMPLATE

这种经济发展模式在短期内确实带来了经济增长,但同时也为未来的危机埋下了隐患

2

3

危机爆发的原因

2

危机爆发的原因

泰国危机的爆发主要是由于以下几个原因

危机爆发的原因

a. 过度借贷

在经济发展的高峰期,泰国的企业和个人大量借入外债,而这些债务主要被用于投资房地产和股票市场。当经济环境发生变化时,这些高价值的资产迅速贬值,导致债务无法偿还

危机的影响

c. 国际影响

由于泰国是亚洲重要的经济体之一,其危机迅速波及到周围国家和地区。投资者开始对亚洲其他地区的经济产生疑虑,导致亚洲其他国家的货币和股票市场也出现了大幅波动

危机应对措施

4

危机应对措施

面对这场危机,泰国政府采取了以下措施

危机应对措施

the asian financial crisis(亚洲金融危机)()

IMF对危机的影响

1 IMF有利的影响

国际货币基金组织对发生金融危机国家的款项援助,缓 解了遭遇危机国家的金融、经济的进一步危机,在短时 间内对恢复投资者信心、稳定经济形势发挥了重要作用。

1997年,IMF向泰国提供172亿美元的贷款,向印尼 政府提供400亿美元的贷款。

流程

Introdction Analaysis

Reasons

Influence

IMF evaluation

分

析

导火索

泰铢盯住 美元,经常 账户逆差

经济衰退

经常账户 逆差

吸引外资

流入,利用 资本项目弥 补

国外资本 涌入

抑制投资 消费不足

货币紧缩 利率上升

资产价格 泡沫

银行巨额 不良资产

对世界经济的影响

1 对亚洲经济、社会及政治等方面的影响

首先,亚洲国家出现严重的经济衰退。 其次,亚洲国家的贫困现象加剧。 此外,危机国家还付出了社会动乱甚至政 治危机的沉重代价。

2 多数国家受影响,全球经济增长速度放慢

拉美国家受亚洲金融危机的影响日益明显。

美欧经济也难以独善其身。

其一,亚洲地区经济增长停滞或衰退,对外需求疲弱,必然导致其它国家, 特别是与该区贸易关系较密切的美国的出口减少,在该区投资的公司利 润下降,这些都直接影响到其它国家的经济增长。

国家的外债结构不合理。

在中期、短期债务较多的情况下,一旦外资流出超过外资流入,而本国的外汇储 备又不足以弥补其不足,这个国家的货币贬值便是不可避免的了。

2 内在基础性因素

透支性经济高增长和不良资产的膨胀。

Financial crisis of 2007-2009金融危机 金融风暴 英文介绍

Financial crisis of 2007–2009From Wikipedia, the free encyclopediaThis article is about background financial market events dating from July 2007. For the financial market conditions of 2008 and 2009, see Global financial crisis of 2008–2009. For an overview of all economic problems during the late 2000s, see Late 2000s recession.The financial crisis of 2007–2009 has been called the most serious financial crisis since the Great Depression by leading economists,[1] with its global effects characterized by the failure of key businesses, declines in consumer wealth estimated in the trillions of U.S. dollars, substantial financial commitments incurred by governments, and a significant decline in economic activity.[2] Many causes have been proposed, with varying weight assigned by experts.[3] Both market-based and regulatory solutions have been implemented or are under consideration,[4] while significant risks remain for the world economy.[5] [edit] BackgroundThe immediate cause or trigger of the crisis was the bursting of the United States housing bubble which peaked in approximately 2005–2006.[6][7] High default rates on "subprime" and adjustable rate mortgages (ARM), began to increase quickly thereafter. An increase in loan incentives such as easy initial terms and a long-term trend of rising housing prices had encouraged borrowers to assume difficult mortgages in the belief they would be able to quickly refinance at more favorable terms. However, once interest rates began to rise and housing prices started to drop moderately in 2006–2007 in many parts of the U.S., refinancing became more difficult. Defaults and foreclosure activity increased dramatically as easy initial terms expired, home prices failed to go up as anticipated, and ARM interest rates reset higher.Share in GDP of U.S. financial sector since 1860.[8]In the years leading up to the start of the crisis in 2007, significant amounts of foreign money flowed into the U.S. from fast-growing economies in Asia and oil-producing countries. This inflow of funds made it easier for the Federal Reserve to keep interest rates in the United States too low (by the Taylor rule) from 2002–2006 which contributed to easy credit conditions, leading to the United States housing bubble. Loans of various types (e.g., mortgage, credit card, and auto) were easy to obtain and consumers assumed an unprecedented debt load.[9][10] As part of the housing and credit booms, the amount of financial agreements called mortgage-backed securities (MBS), which derive their value from mortgage payments and housing prices, greatly increased. Such financial innovation enabled institutions and investors around the world to invest in the U.S. housing market. As housing prices declined, major global financialFrom 2000 to 2003, the Federal Reserve lowered the federal funds rate target from 6.5% to 1.0%.[25] This was done to soften the effects of the collapse of the dot-com bubble and of the September 2001 terrorist attacks, and to combat the perceived risk of deflation.[26] The Fed then raised the Fed funds rate significantly between July 2004 and July 2006.[27] This contributed to an increase in 1-year and 5-year adjustable-rate mortgage (ARM) rates, making ARM interest rate resets more expensive for homeowners.[28] This may have also contributed to the deflating of the housing bubble, as asset prices generally move inversely to interest rates and it became riskier to speculate in housing.[29][30]U.S. Current Account or Trade DeficitIn 2005, Ben Bernanke addressed the implications of the USA's high and rising current account (trade) deficit, resulting from USA imports exceeding its exports.[31] Between 1996 and 2004, the USA current account deficit increased by $650 billion, from 1.5% to 5.8% of GDP. Financing these deficits required the USA to borrow large sums from abroad, much of it from countries running trade surpluses, mainly the emerging economies in Asia and oil-exporting nations. The balance of payments identity requires that a country (such as the USA) running a current account deficit also have a capital account (investment) surplus of the same amount. Hence large and growing amounts of foreign funds (capital) flowed into the USA to finance its imports. This created demand for various types of financial assets, raising the prices of those assets while lowering interest rates. Foreign investors had these funds to lend, either because they had very high personal savings rates (as high as 40% in China), or because of high oil prices. Bernanke referred to this as a "saving glut."[32] A "flood" of funds (capital or liquidity) reached the USA financial markets. Foreign governments supplied funds by purchasing USA Treasury bonds and thus avoided much of the direct impact of the crisis. USA households, on the other hand, used funds borrowed from foreigners to finance consumption or to bid up the prices of housing and financial assets. Financial institutions invested foreign funds in mortgage-backed securities. USA housing and financial assets dramatically declined in value after the housing bubble burst.[33][34][edit] Sub-prime lendingU.S. Subprime lending expanded dramatically 2004-2006In addition to easy credit conditions, there is evidence that both government and competitive pressures contributed to an increase in the amount of subprime lending during the years preceding the crisis. Major∙As early as 1997, Fed Chairman Alan Greenspan fought to keep the derivatives market unregulated.[citation needed] With the advice of the President's Working Group on Financial Markets,[62] the U.S. Congress and President allowed the self-regulation of the over-the-counter derivatives market when they enacted the Commodity Futures Modernization Act of 2000. Derivatives such as credit default swaps (CDS) can be used to hedge or speculate against particular credit risks. The volume of CDS outstanding increased 100-fold from 1998 to 2008, with estimates of the debt covered by CDS contracts, as of November 2008, ranging from US$33 to $47 trillion. Total over-the-counter (OTC) derivative notional value rose to $683 trillion by June 2008.[63]Warren Buffett famously referred to derivatives as "financial weapons of mass destruction" in early 2003.[64][65][edit] Increased debt burden or over-leveragingLeverage Ratios of Investment Banks Increased Significantly 2003-2007U.S. households and financial institutions became increasingly indebted or overleveraged during the years preceding the crisis. This increased their vulnerability to the collapse of the housing bubble and worsened the ensuing economic downturn. Key statistics include:∙USA household debt as a percentage of annual disposable personal income was 127% at the end of 2007, versus 77% in 1990.[66]∙U.S. home mortgage debt relative to gross domestic product (GDP) increased from an average of 46% during the 1990s to 73% during 2008, reaching $10.5 trillion.[67]∙In 1981, U.S. private debt was 123% of GDP; by the third quarter of 2008, it was 290%.[68]∙From 2004-07, the top five U.S. investment banks each significantly increased their financial leverage (see diagram), which increased their vulnerability to a financial shock. These five institutions reported over $4.1 trillion in debt for fiscal year 2007, about 30% of USA nominal GDP for 2007. Lehman Brothers was liquidated, Bear Stearns and Merrill Lynch were sold at fire-sale prices, and Goldman Sachs and Morgan Stanley became commercial banks, subjecting themselves to more stringent regulation. With the exception of Lehman, these companies required or received government support.[69]∙Fannie Mae and Freddie Mac, two U.S. Government sponsored enterprises, owned or guaranteed nearly $5 trillion in mortgage obligations at the time they were placed into conservatorship by the U.S. government in September 2008.[70][71]These seven entities were highly leveraged and had $9 trillion in debt or guarantee obligations, an enormous concentration of risk, yet were not subject to the same regulation as depository banks.[edit] Financial innovation and complexityA protester on Wall Street in the wake of the AIG bonus payments controversy is interviewed by news media.The term financial innovation refers to the ongoing development of financial products designed to achieve particular client objectives, such as offsetting a particular risk exposure (such as the default of a borrower) or to assist with obtaining financing. Examples pertinent to this crisis included: the adjustable-rate mortgage; the bundling of subprime mortgages into mortgage-backed securities (MBS) or collateralized debt obligations (CDO) for sale to investors, a type of securitization; and a form of credit insurance called credit default swaps(CDS). The usage of these products expanded dramatically in the years leading up to the crisis. These products vary in complexity and the ease with which they can be valued on the books of financial institutions.In a Peabody Award winning program, NPR correspondents argued that a "Giant Pool of Money" (represented by $70 trillion in worldwide fixed income investments) sought higher yields than those offered by U.S. Treasury bonds early in the decade. Further, this pool of money had roughly doubled in size from 2000 to 2007, yet the supply of relatively safe, income generating investments had not grown as fast. Investment banks on Wall Street answered this demand with the MBS and CDO, which were assigned safe ratings by the credit rating agencies. In effect, Wall Street connected this pool of money to the mortgage market in the U.S., with enormous fees accruing to those throughout the mortgage supply chain, from the mortgage broker selling the loans, to small banks that funded the brokers, to the giant investment banks behind them. By approximately 2003, the supply of mortgages originated at traditional lending standards had been exhausted. However, continued strong demand for MBS and CDO began to drive down lending standards, as long as mortgages could still be sold along the supply chain. Eventually, this speculative bubble proved unsustainable.[72]The CDO in particular enabled financial institutions to obtain investor funds to finance subprime and other lending, extending or increasing the housing bubble and generating large fees. A CDO essentially places cash payments from multiple mortgages or other debt obligations into a single pool, from which the cash is allocated to specific securities in a priority sequence. Those securities obtaining cash first received investment-grade ratings from rating agencies. Lower priority securities received cash thereafter, with lower credit ratings but theoretically a higher rate of return on the amount invested.[73][74]For a variety of reasons, market participants did not accurately measure the risk inherent with this innovation or understand its impact on the overall stability of the financial system.[75] For example, the pricing model for CDOs clearly did not reflect the level of risk they introduced into the system. The average recovery rate for "high quality" CDOs has been approximately 32 cents on the dollar, while the recovery rate for mezzanine CDO's has been approximately five cents for every dollar. These massive, practically unthinkable, losses have dramatically impacted the balance sheets of banks across the globe, leaving them with very little capital to continue operations.[76]Another example relates to AIG, which insured obligations of various financial institutions through the usage of credit default swaps. The basic CDS transaction involved AIG receiving a premium in exchangefor a promise to pay money to party A in the event party B defaulted. However, AIG did not have the financial strength to support its many CDS commitments as the crisis progressed and was taken over by the government in September 2008. U.S. taxpayers provided over $180 billion in government support to AIG during 2008 and early 2009, through which the money flowed to various counterparties to CDS transactions, including many large global financial institutions.[77][78]The limitations of a widely-used financial model also were not properly understood.[79][80] This formula assumed that the price of CDS was correlated with and could predict the correct price of mortgage backed securities. Because it was highly tractable, it rapidly came to be used by a huge percentage of CDO and CDS investors, issuers, and rating agencies.[80] According to one article[80]: "Then the model fell apart. Cracks started appearing early on, when financial markets began behaving in ways that users of Li's formula hadn't expected. The cracks became full-fledged canyons in 2008—when ruptures in the financial system's foundation swallowed up trillions of dollars and put the survival of the global banking system in serious peril... Li's Gaussian copula formula will go down in history as instrumental in causing the unfathomable losses that brought the world financial system to its knees."As financial assets became more and more complex, and harder and harder to value, investors were reassured by the fact that both the international bond rating agencies and bank regulators, who came to rely on them, accepted as valid some complex mathematical models which theoretically showed the risks were much smaller than they actually proved to be in practice [81]. George Soros commented that "The super-boom got out of hand when the new products became so complicated that the authorities could no longer calculate the risks and started relying on the risk management methods of the banks themselves. Similarly, the rating agencies relied on the information provided by the originators of synthetic products. It was a shocking abdication of responsibility." [82]Certain financial innovation may also have the effect of circumventing regulations, such as off-balance sheet financing that affects the leverage or capital cushion reported by major banks. For example, Martin Wolf wrote in June 2009: "...an enormous part of what banks did in the early part of this decade – theoff-balance-sheet vehicles, the derivatives and the 'shadow banking system' itself – was to find a way round regulation."[83][edit] Boom and collapse of the shadow banking systemIn a June 2008 speech, U.S. Treasury Secretary Timothy Geithner, then President and CEO of the NY Federal Reserve Bank, placed significant blame for the freezing of credit markets on a "run" on the entities in the "parallel" banking system, also called the shadow banking system. These entities became critical to the credit markets underpinning the financial system, but were not subject to the same regulatory controls. Further, these entities were vulnerable because they borrowed short-term in liquid markets to purchase long-term, illiquid and risky assets. This meant that disruptions in credit markets would make them subject to rapid deleveraging, selling their long-term assets at depressed prices. He described the significance of these entities: "In early 2007, asset-backed commercial paper conduits, in structured investment vehicles, in auction-rate preferred securities, tender option bonds and variable rate demand notes, had a combined asset size of roughly $2.2 trillion. Assets financed overnight in triparty repo grew to $2.5 trillion. Assets held in hedge funds grew to roughly $1.8 trillion. The combined balance sheets of the then five major investment banks totaled $4 trillion. In comparison, the total assets of the top five bank holding companies in the United States at that point were just over $6 trillion, and total assets of the entire banking system were about $10 trillion." He stated that the "combined effect of these factors was a financial system vulnerable to self-reinforcing asset price and credit cycles."[12]2007 bank run on Northern Rock, a UK bankOne of the first victims was Northern Rock, a medium-sized British bank.[98] The highly leveraged nature of its business led the bank to request security from the Bank of England. This in turn led to investor panic and a bank run in mid-September 2007. Calls by Liberal Democrat Shadow Chancellor Vince Cable to nationalise the institution were initially ignored; in February 2008, however, the British government (having failed to find a private sector buyer) relented, and the bank was taken into public hands. Northern Rock's problems proved to be an early indication of the troubles that would soon befall other banks and financial institutions.Initially the companies affected were those directly involved in home construction and mortgage lending such as Northern Rock and Countrywide Financial, as they could no longer obtain financing through the credit markets. Over 100 mortgage lenders went bankrupt during 2007 and 2008. Concerns that investment bank Bear Stearns would collapse in March 2008 resulted in its fire-sale to JP Morgan Chase. The crisis hit its peak in September and October 2008. Several major institutions either failed, were acquired under duress, or were subject to government takeover. These included Lehman Brothers, Merrill Lynch, Fannie Mae, Freddie Mac, and AIG.[99]See also: Federal takeover of Fannie Mae and Freddie Mac[edit] Credit markets and the shadow banking systemTED spread and components during 2008During September 2008, the crisis hits its most critical stage. There was the equivalent of a bank run on the money market mutual funds, which frequently invest in commercial paper issued by corporations to fund their operations and payrolls. Withdrawal from money markets were $144.5 billion during one week, versus $7.1 billion the week prior. This interrupted the ability of corporations to rollover (replace) their short-term debt. The U.S. government responded by extending insurance for money market accounts analogous to bank deposit insurance via a temporary guarantee[100] and with Federal Reserve programs to purchase commercial paper. The TED spread, an indicator of perceived credit risk in the general economy, spiked up in July 2007, remained volatile for a year, then spiked even higher in September 2008,[101] reaching a record 4.65% on October 10, 2008.In a dramatic meeting on September 18, 2008 Treasury Secretary Henry Paulson and Fed Chairman Ben Bernanke met with key legislators to propose a $700 billion emergency bailout. Bernanke reportedly tells them: "If we don't do this, we may not have an economy on Monday."[102] The Emergency Economic Stabilization Act also called the Troubled Asset Relief Program (TARP) is signed into law on October 3, 2008.[103]Economist Paul Krugman and U.S. Treasury Secretary Timothy Geithner explain the credit crisis via the implosion of the shadow banking system, which had grown to nearly equal the importance of the traditional commercial banking sector as described above. Without the ability to obtain investor funds in exchange for most types of mortgage-backed securities or asset-backed commercial paper, investment banks and other entities in the shadow banking system could not provide funds to mortgage firms and other corporations.[12][58]This meant that nearly one-third of the U.S. lending mechanism was frozen and continued to be frozen into June 2009.[104] According to the Brookings Institution, the traditional banking system does not have the capital to close this gap as of June 2009: "It would take a number of years of strong profits to generate sufficient capital to support that additional lending volume." The authors also indicate that some forms of securitization are "likely to vanish forever, having been an artifact of excessively loose credit conditions." While traditional banks have raised their lending standards, it was the collapse of the shadow banking system that is the primary cause of the reduction in funds available for borrowing.[105][edit] Wealth effectsThere is a direct relationship between declines in wealth, and declines in consumption and business investment, which along with government spending represent the economic engine. Between June 2007 and November 2008, Americans lost an estimated average of more than a quarter of their collective net worth. By early November 2008, a broad U.S. stock index the S&P 500, was down 45 percent from its 2007 high. Housing prices had dropped 20% from their 2006 peak, with futures markets signaling a30-35% potential drop. Total home equity in the United States, which was valued at $13 trillion at its peak in 2006, had dropped to $8.8 trillion by mid-2008 and was still falling in late 2008. Total retirement assets, Americans' second-largest household asset, dropped by 22 percent, from $10.3 trillion in 2006 to $8 trillion in mid-2008. During the same period, savings and investment assets (apart from retirement savings) lost $1.2 trillion and pension assets lost $1.3 trillion. Taken together, these losses total a staggering $8.3 trillion.[106]Further, U.S. homeowners had extracted significant equity in their homes in the years leading up to the crisis, which they could no longer do once housing prices collapsed. Free cash used by consumers from home equity extraction doubled from $627 billion in 2001 to $1,428 billion in 2005 as the housing bubble built, a total of nearly $5 trillion over the period.[16][107][108] U.S. home mortgage debt relative to GDP increased from an average of 46% during the 1990s to 73% during 2008, reaching $10.5 trillion.[109]To offset this decline in consumption and lending capacity, the U.S. government and U.S. Federal Reserve have committed $13.9 trillion, of which $6.8 trillion has been invested or spent, as of June 2009.[110] In effect, the Fed has gone from being the "lender of last resort" to the "lender of only resort" for a significant portion of the economy. In some cases the Fed can now be considered the "buyer of last resort."The New York City headquarters of Lehman Brothers.Economist Dean Baker explained the reduction in the availability of credit this way:"Yes, consumers and businesses can't get credit as easily as they could a year ago. There is a really good reason for tighter credit. Tens of millions of homeowners who had substantial equity in their homes two years ago have little or nothing today. Businesses are facing the worst downturn since the Great Depression. This matters for credit decisions. A homeowner with equity in her home is very unlikely to default on a car loan or credit card debt. They will draw on this equity rather than lose their car and/or have a default placed on their credit record. On the other hand, a homeowner who has no equity is a serious default risk. In the case of businesses, their creditworthiness depends on their future profits. Profit prospects look much worse in November 2008 than they did in November 2007 (of course, to clear-eyed analysts, they didn't look too good a year ago either). While many banks are obviously at the brink, consumers and businesses would be facing a much harder time getting credit right now even if the financial system were rock solid. The problem with the economy is the loss of close to $6 trillion in housing wealth and an even larger amount of stock wealth. Economists, economic policy makers and economic reporters virtually all missed the housing bubble on the way up. If they still can't notice its impact as the collapse of the bubble throws into the worst recession in the post-war era, then they are in the wrong profession."[111]At the heart of the portfolios of many of these institutions were investments whose assets had been derived from bundled home mortgages. Exposure to these mortgage-backed securities, or to the credit derivatives used to insure them against failure, caused the collapse or takeover of several key firms such as Lehman Brothers, AIG, Merrill Lynch, and HBOS.[112][113][114][edit] Global contagionThe crisis rapidly developed and spread into a global economic shock, resulting in a number of European bank failures, declines in various stock indexes, and large reductions in the market value of equities[115] and commodities.[116] Moreover, the de-leveraging of financial institutions, as assets were sold to pay back obligations that could not be refinanced in frozen credit markets, further accelerated the liquidity crisis and caused a decrease in international trade.World political leaders, national ministers of finance and central bank directors coordinated theirefforts[117] to reduce fears, but the crisis continued. At the end of October 2008 a currency crisis developed, with investors transferring vast capital resources into stronger currencies such as the yen, the dollar and the Swiss franc, leading many emergent economies to seek aid from the International Monetary Fund.[118][119][edit] Effects on the global economy[edit] Official economic projectionsOn November 3, 2008, the EU-commission at Brussels predicted for 2009 an extremely weak growth of GDP, by 0.1 percent, for the countries of the Euro zone (France, Germany, Italy, etc.) and even negative number for the UK (-1.0 percent), Ireland and Spain. On November 6, the IMF at Washington, D.C., launched numbers predicting a worldwide recession by -0.3 percent for 2009, averaged over the developed economies. On the same day, the Bank of England and the Central Bank for the Euro zone, respectively, reduced their interest rates from 4.5 percent down to three percent, and from 3.75 percent down to 3.25 percent. Economically, mainly the car industry seems to be involved. As a consequence, starting from November 2008, several countries launched large "help packages" for their economies.The U.S. Federal Reserve Open Market Committee release in June 2009 stated: "...the pace of economic contraction is slowing. Conditions in financial markets have generally improved in recent months. Household spending has shown further signs of stabilizing but remains constrained by ongoing job losses, lower housing wealth, and tight credit. Businesses are cutting back on fixed investment and staffing but appear to be making progress in bringing inventory stocks into better alignment with sales. Although economic activity is likely to remain weak for a time, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability."[136] Economic projections from the Federal Reserve and Reserve Bank Presidents include a return to typical growth levels (GDP) of 2-3% in 2010; an unemployment plateau in 2009 and 2010 around 10% with moderation in 2011; and inflation that remains at typical levels around 1-2%.[137][edit] Responses to financial crisis[edit] Emergency and short-term responsesMain article: Subprime mortgage crisis#ResponsesThe U.S. Federal Reserve and central banks around the world have taken steps to expand money supplies to avoid the risk of a deflationary spiral, in which lower wages and higher unemployment lead to aself-reinforcing decline in global consumption. In addition, governments have enacted large fiscal stimulus packages, by borrowing and spending to offset the reduction in private sector demand caused by the crisis. The U.S. executed two stimulus packages, totaling nearly $1 trillion during 2008 and 2009.[138] This credit freeze brought the global financial system to the brink of collapse. The response of the USA Federal Reserve, the European Central Bank, and other central banks was immediate and dramatic. During the last quarter of 2008, these central banks purchased US$2.5 trillion of government debt and troubled private assets from banks. This was the largest liquidity injection into the credit market, and the largest monetary policy action, in world history. The governments of European nations and the USA also raised the capital of their national banking systems by $1.5 trillion, by purchasing newly issued preferred stock in their major banks.[99]Governments have also bailed-out a variety of firms as discussed above, incurring large financial obligations. To date, various U.S. government agencies have committed or spent trillions of dollars in loans, asset purchases, guarantees, and direct spending. For a summary of U.S. government financial commitments and investments related to the crisis, see CNN - Bailout Scorecard.。

1997年与2008年两次国际金融危机比较分析解析

1997年与2008年两次国际金融危机成因、特征和影响比较分析及对中国企业的影响摘要近几十年来,随着人类经济发展的速度加快,随之而来的问题也日益凸现,随着全球化的发展,金融危机也开始向全球蔓延.1997年爆发于泰国、后迅速扩散到整个东南业井波及世界的东南亚金融危机,使许多东南亚国家和地区的汇市、股市轮番暴跌,金融系统乃至整个社会经济受到严重创伤.2008年由美国华尔街引爆的世界金融危机有如巨风海啸,迅速波及全球。

不管是同属发达国家的欧洲联盟国家,还是经济尚未开放的非洲,以及是坐享石油美元的中东,或者说是新兴崛起的一系列国家,都在感受着这场金融巨风带来的狂扫与震撼。

从1997年泰铢引发的亚洲金融危机到2008 年美国次贷危机引发的全球金融危机的全面爆发,我国面临外部需求萎缩带来的经济下滑的风险。

本课题通过比较1997年与2008年国际金融危机成因、特征和影响,旨在透过近十几年来两次金融危机的表象,把握经济运行的规律。

通过分析比较这两次金融危机的成因,总结出其内在的相同点,再分析我国现阶段经济运行的形式,找出我国经济发展中存在的问题,提出相应的合理化的建议。

以及通过比较两次经济危机的特征和影响,总结出金融危机爆发后对中国企业的的影响,并提出合理化的防措施,有利于提早做准备,防患于未然。

In rece nt decades, with the developme nt of the econo mic , a series of questi ons is coming up .with the development of globalization, the financial crisis are spreadingacross the world .Southeast Asian financial crisis, which broke out in Thailand, quicklyspread throughout the en tire southeast of the world, made the stock market tumbli ng in many southeast Asian countries , , repeatedly trading financial system and even the entire social economy suffered serious wounds. the world financial crisis in 2008 det on ated by Wall Street like gia nt wind tsu nami, quickly spread arou nd the world. Whether the cou ntries of the Europea n Un io n, or Africa n ,in which economy have not been open, or the countries of Middle East, or rather, a series of new countries all felt this financial giant wind brings the crazy esau and shock.from world financial crisis caused by the Thai baht in 1997 to the subprime mortgage crisis triggered in Amercia in2008, Chi na faces the risk of econo mic dow ntur n atrophy due to the exter nal dema nd withered .This topic compared the causes , characteristics and in flue nce of the in ter nati onal financial crisis in 1997 and 2008,through the study on the appearance of the financial crisis past doze ns of years, grasp the econo mic operati on of the law. An alysize and comparied the causes of the financial crisis, the author sums up their inner similarities, then an alyzes the curre nt form of econo mic operati on of the econo mic developme nt of our cou ntry, find out the problems existed in the develop ing of our econo mic. propose corresp onding rati on alizati on suggesti on. And through compari ng the two econo miccrisis, summarized the characteristics and effects of the financial crisis after the outbreak of the in flue nce of Chin ese en terprises, and puts forward some precauti onary measures, which is helpful for the rati on alizati on of prepari ng early.正文」、两次金融危机演变过程比较分析(一)1997年亚洲金融危机的演变过程分析1997年6月,一场金融危机在亚洲爆发,这场危机的发展过程十分复杂。

亚洲金融风暴

亚洲金融风暴免费编辑添加义项名B添加义项?所属类别:其他经济相关亚洲金融危机指发生于1997年的一次世界性金融风波。

1997年7月2日,亚洲金融风暴席卷泰国。

不久,这场风暴波及马来西亚、新加坡、日本和韩国、中国等地。

泰国、印尼、韩国等国的货币大幅贬值,同时造成亚洲大部分主要股市的大幅下跌;冲击亚洲各国外贸企业,造成亚洲许多大型企业的倒闭,工人失业,社会经济萧条。

打破了亚洲经济急速发展的景象。

亚洲一些经济大国的经济开始萧条,一些国家的政局也开始混乱。

泰国,印尼和韩国是受此金融风暴波及最严重的国家。

新加坡,马来西亚,菲律宾和香港也被波及,中国大陆和台湾则几乎不受影响。

∙∙1997Asian financial crises∙∙1997年7月2日∙∙∙∙折叠编辑本段爆发原因亚洲国家的经济形态导致;美国经济利益和政策的影响;乔治·索罗斯的个人及一些支持他的资本主义集团的因素;亚洲国家的经济形态导致:新马泰日韩等国都为外向型经济的国家,他们对世界市场的依附很大。

亚洲经济的动摇难免会出现牵一发而动全身的状况。

以泰国为例,泰铢在国际市场上是否要买卖不由政府来主宰,而泰国本身并没有足够的外汇储备量,面对金融家的炒作,该国经济不堪一击。

而经济决定政治,所以,泰国政局也就动荡了。

国内学者的分析:直接触发因素、内在基础因素和世界经济因素。

折叠编辑本段发展阶段折叠第一阶段1997年7月2日,泰国宣布放弃固定汇率制,实行浮动汇率制,引发一场遍及东南亚的金融风暴。

当天,泰铢兑换美元的汇率下降了17%,外汇及其他金融市场一片混乱。

在泰铢波动的影响下,菲律宾比索、印度尼西亚盾、马来西亚林吉特相继成为国际炒家的攻击对象。

1997年8月,马来西亚放弃保卫林吉特的努力。

一向坚挺的新加坡元也受到冲击。

印尼虽是受"传染"最晚的国家,但受到的冲击最为严重。

1997年10月下旬,国际炒家移师国际金融中心香港,矛头直指香港联系汇率制。

关于1997年亚洲金融风暴的探析

关于1997年亚洲金融风暴的探析一、亚洲金融风暴概述1997年亚洲金融风暴是亚洲金融史上最严重的一次金融危机,它从发生到结束用时约为两年时间。

该危机开始于1997年7月泰国的货币和股票市场崩溃,随后蔓延到韩国、印尼、菲律宾等亚洲国家。

本场危机的影响远不止于亚洲地区,其对世界经济的冲击仍在影响着人们。

二、亚洲金融风暴的原因1997年亚洲金融风暴的根本原因是亚洲国家采取了宽松的货币政策和扩张性的信贷政策,导致泡沫和债务的快速增长。

同时,亚洲金融体系脆弱,国内金融监管不力,外资流入过度依赖短期外债、银行信用担保和外汇套利等方式,导致危机爆发。

三、危机对亚洲各国的影响亚洲金融风暴对亚洲各国经济的影响十分严重,2000年前后的亚洲,几乎所有的亚洲国家经济增长都出现了明显的下降趋势,且相应的失业率呈增长趋势。

其中又以泰国、印尼等国家受到影响最为严重。

四、国际金融机构对危机的反应在亚洲金融危机中,国际货币基金组织(IMF)和世界银行(WB)等国际金融机构通过向危机国家提供金融援助和技术协助等形式来缓解亚洲金融危机的影响。

但是这些救助行动对于危机的根本解决并没有太大的作用,还引发了亚洲的反弹。

从这场危机中我们可以看出,IMF等国际机构的应对危机措施还需要进一步完善。

五、亚洲金融风暴对国际金融市场的影响亚洲金融危机影响最大的除了亚洲各国之外,还有世界其他地区的金融市场。

危机的爆发导致亚洲股市、货币和债券市场惨遭抛售,国际投资者纷纷把资金转移到其他地区市场,这也使得许多国家的经济形势雪上加霜。

六、案例1:泰国1997年7月,泰铢的汇率开始暴跌,导致了国内的银行破产和意大利银行等外国机构的巨额损失,泰国经济陷入严重的经济危机。

政府随后采取了对泰铢贬值、禁止银行外汇交易等措施,但这只加剧了泰国的经济萎缩。

七、案例2:韩国韩国的崩溃是1997年末至1998年初,在韩美银行宣布破产后,韩元突然贬值。

韩国政府随后颁布了一系列措施,如向IMF组织申请救助、向银行注入资金等来缓解金融风险带来的影响。

97金融危机

至此,与8月份最高点相比,香港股市跌幅几乎过 半。

六、97危机的主要过程——第三阶段

全球股市股市在大跌之后都有回升现象,亚洲市场 也一度呈现出向好的趋势。在人们认为东南亚金融 危机最危险的时刻已经过去,金融风暴渐趋平息之 际,韩国金融危机的爆发却再次将东南亚卷入了第 三轮金融风波之中。

1987~1990年为外国对泰投资高峰期,1991年后投资势 头有所减缓。 1993年外资又大幅回升,全年申请扶助项目为 1252宗,总投资额2788亿铢,超过最好时期的1990年。 其中日本和欧洲的投资增长速度最快。

泰国的对外贸易出口增长传统上是一直是泰国经济增长的动力, 并对泰国工业结构的多元化起了积极的促进作用。1991- 1997年间,出口额增长了一倍,由282亿美元增长到567亿 美元。

自1997年初起,韩国许多大财团先后陷入了破产 倒闭的绝境,经济受到极大的冲击,加上东南亚金 融动荡的影响,韩国经济负增长跌至多年来的最低 点。

11月17日,由于政府金融改革法案未获通过,韩 圆兑美元的比价突破1000:1大关,股票综合指 数跌至500点以下。

11月20日,韩国中央银行决定将韩圆汇率 浮动范围由2.25%扩大到10%,至此韩 国开金融管理局一方面动用外汇储备在 外汇市场进行积极干预,另一方面只得提高银 行间市场短期利率。而香港股市在汇价和银行 短期利率高企的影响下,受投机沽售力量冲击 大幅滑落。

10月23日,同业隔夜拆借利率一度由7%上 升至300%,港元兑美元汇价也一度升至联 系汇率制实施14年来最高水平(7.6150)。

1.2更加极端的例子---新加坡

金融危机对全球经济的影响中英文对照外文翻译文献

金融危机对全球经济的影响中英文对照外文翻译文献(文档含英文原文和中文翻译)金融危机对全球商业的影响目前,新的经济只是在部分工业化经济高度发达的国家初露端倪,在全球范围还属于萌芽状态。

不过这种经济的发展肯定对于世界政治和经济将产生越来越大的影响。

日本经济审议会1999年向日本政府提出对未来十年日本新经济计划的建议时说:“当前,世界文明正在发生变化,这一变化不是一般的‘进步’与“高度化”,而是要创造新的历史发展阶段的变化。

一直支撑战后增长的现代工业社会的规范已跟不上人类文明的巨大潮流。

在今后存在多种智慧的社会中,必须通过不断创造出新的智慧来搞活经济与文化。

为此,就必须能够更加容易地吸收世界的信息和知识,还要有更加容易向世界传递信息的环境。

同时,还必须拥有能够培养富于个性和创造性的组织和人才的计划和社会气氛”。

如果把上面所说的世界经济的变化加以概括,似乎可以说,未来经济有两大趋势:一个是经济知识化,表现为知识和信息成为经济发展最活跃、最重要的因素;另一个是经济全球化,表现为商品、劳务、资本、技术和人才在全球流动的加速。

这两大趋势相互联系、互相影响。

也可以说,新的经济将是以知识与技术创新为基础,以全球为市场的时代。

它将促使各国的增长模式、产业构成、经济体制、社会结构、教育制度、文化取向等产生深刻的变化,也将对各国的对内、对外政策提出新课题。

三、经济全球化的大趋势及其两重性经济全球化的发端似可溯源到二次世界大战后期布雷顿森林体制的创建。

世界银行、国际货币基金组织和关贸总协定三大机构的建立与发展,给全球金融、贸易与投资活动以极大的推动。

美元与黄金挂钩使美元成为国际流通与储备的手段,首先便利了美国企业向全球的拓展。

不过,冷战时期两个世界市场的划分又使经济全球化受到一定限制。

冷战结束后,经济全球化得到进一步发展。

主要有两股力量推动:一股力量是信息技术革命和高新技术成长的大大促进了商品、劳务、资本、人才、技术的全球交流。

1997~1998年亚洲金融风暴,的前因后果Microsoft Word 文档

1997~1998年亚洲金融风暴,的前因后果金融风暴启示录对冲基金(HedgeFund)意为“风险对冲过的基金”,起源于上世纪50年代初的美国,原指广泛利用金融衍生产品进行投资保值的一类基金,现今指利用各种金融衍生产品的杠杆效用,承担高风险、追求高收益的一种投资模式。

亚洲金融危机,又称亚洲金融风暴,是指1997年发源于泰国,之后进一步影响到临近亚洲国家,甚至全球货币、股票市场和其他资产价值的一场金融大危机。

其过程十分复杂,大致可分为三个阶段:第一阶段:1997年7月,以索罗斯为代表的国际金融投机者瞄准泰铢注入大量热钱,迫使泰国政府于7月2日宣布放弃实行了14年的泰币与美元挂钩的一揽子汇率制,实行浮动汇率制。

亚洲金融危机正式爆发,并很快波及菲律宾、印尼、马来西亚等其它东南亚国家;10月下旬,国际炒家移师香港,香港恒生指数自1996年以来首次跌破10000点;11月中旬,韩国爆发金融风暴,随之日本一系列银行和证券公司破产,东南亚金融风暴演变为亚洲金融危机。

第二阶段:1998年初,印尼金融风暴再起,由此陷入政治经济大危机。

受其影响,东南亚汇市再起波澜,新元、马币、泰铢、菲律宾比索等纷纷下跌,随之日元也大幅贬值,亚洲金融危机继续深化。

第三阶段:1998年8月初,国际炒家对香港发动新一轮进攻,香港特区政府予以回击,使其遭遇失利。

继而因俄罗斯国家政策的突变,在俄股市投下巨额资金的国际炒家再次大伤元气,并带动美欧国家股市、汇市的全面剧烈波动,由此亚洲金融危机具有了全球性的意义。

到1998年底,俄罗斯经济仍没有摆脱困境。

1999年,亚洲金融危机结束。

胡进、张才进:“全球金融动荡加剧的四大成因”, 《港澳经济》,1997年第3期。

而且过分集中于简单加工业。

结果在国际竞争日益加剧的冲击下,以劳动密集型产业为主体的东南亚国家出口扩张势头放缓,带动经济增长下降,从而导致经常项目赤字、外汇储备减少,进而对固定汇率产生压力,最终使金融风暴在区内广泛爆发。

20世纪90年代以来四次世界性金融危机的比较分析

第一,亚洲金融风暴(1997年)亚洲金融风暴始于东南亚国家的货币贬值和金融体系崩溃。

此次危机引发了东南亚地区经济下滑,导致泰国、印度尼西亚和韩国等国家放弃固定汇率制度。

危机的原因包括外债积累、固定汇率政策、资本市场的不稳定和金融监管问题。

第二,俄罗斯金融危机(1998年)俄罗斯金融危机爆发在亚洲金融风暴之后,导致俄罗斯卢布贬值和债务违约。

危机的原因主要是俄罗斯债务问题和严重的经济问题,包括宏观经济政策失误和金融机构的腐败。

第三,全球金融危机(2024年)全球金融危机是2024年爆发的一场由美国次贷危机引发的全球性金融危机。

此次危机加剧了银行系统流动性问题,导致了全球范围内的金融机构倒闭和经济衰退。

危机的主要原因是次贷危机暴露了全球金融体系的风险管理问题,以及银行和金融机构的过度杠杆。

第四,欧洲主权债务危机(2024年)欧洲主权债务危机爆发在全球金融危机之后,主要涉及希腊、爱尔兰、葡萄牙、西班牙和意大利等欧洲国家。

危机的主要原因是这些国家的高度负债、低增长和缺乏竞争力的经济结构。

此次危机引发了欧元区的稳定问题,威胁到了整个欧洲经济。

这四次世界性金融危机的比较分析如下:首先,这四次危机都起源于不同的国家或地区,但危机的影响是全球性的。

它们都是由于经济和金融问题的加剧导致的,但其具体原因和特点各有不同。

其次,这四次危机都给全球经济带来了巨大的冲击。

危机爆发后,全球范围内的金融市场出现动荡,经济增长放缓,失业率上升,企业和家庭面临债务问题。

再次,这四次危机都揭示了金融市场的系统性风险和风险管理的重要性。

亚洲金融风暴和俄罗斯金融危机暴露了金融体系脆弱性和监管不力的问题。

全球金融危机和欧洲主权债务危机则揭示了金融机构过度杠杆和风险管理不善的问题。

最后,这四次危机都促使各国和国际机构采取了行动来应对危机。

国家采取了货币政策、财政政策和金融监管的措施来稳定金融市场和促进经济复苏。

国际机构如国际货币基金组织和世界银行也提供了贷款和援助来帮助受危机影响的国家。

1997年金融危机(中英对照)

1997年金融危机(中英对照)The Asian Financial Crisis was a period of financial crisis that gripped much of Asia beginning in July 1997, and raised fears of a worldwide economic meltdown . 亚洲金融危机是从1997年7月开始的困扰许多亚洲国家的金融危机并令许多人担心起全球经济崩溃。

The crisis started in Thailand with the financial collapse of the Thai baht caused by thedecision of the Thai government to float the baht, cutting its peg to the USD, after exhaustive efforts to support it in the face of a severe financial overextension that was in part real estate driven. 这场金融危机始于泰国泰铢的倒塌是因为泰国政府做出的使泰铢浮动的决定切断其对美元的汇率来尽力维持它在面临严重的受部分房地产驱使的财政过度外延。

At the time, Thailand had acquired a burden of foreign debt that made the country effectively bankrupt even before the collapse of its currency. As the crisis spread, most of Southeast Asia and Japansaw slumping currencies, devalued stock markets and other asset prices, and a precipitous rise in private debt. 当时泰国已负担了沉重的外债甚至在其货币崩溃之前已使该国实际上已经破产。

1997年与2008年两次国际金融危机比较分析解析

1997年与2008年两次国际金融危机成因、特征和影响比较分析及对中国企业的影响摘要近几十年来,随着人类经济发展的速度加快,随之而来的问题也日益凸现,随着全球化的发展,金融危机也开始向全球蔓延.1997年爆发于泰国、后迅速扩散到整个东南业井波及世界的东南亚金融危机,使许多东南亚国家和地区的汇市、股市轮番暴跌,金融系统乃至整个社会经济受到严重创伤.2008年由美国华尔街引爆的世界金融危机有如巨风海啸,迅速波及全球。

不管是同属发达国家的欧洲联盟国家,还是经济尚未开放的非洲,以及是坐享石油美元的中东,或者说是新兴崛起的一系列国家,都在感受着这场金融巨风带来的狂扫与震撼。

从1997年泰铢引发的亚洲金融危机到2008年美国次贷危机引发的全球金融危机的全面爆发,我国面临外部需求萎缩带来的经济下滑的风险。

本课题通过比较1997年与2008年国际金融危机成因、特征和影响,旨在透过近十几年来两次金融危机的表象,把握经济运行的规律。

通过分析比较这两次金融危机的成因,总结出其内在的相同点,再分析我国现阶段经济运行的形式,找出我国经济发展中存在的问题,提出相应的合理化的建议。

以及通过比较两次经济危机的特征和影响,总结出金融危机爆发后对中国企业的的影响,并提出合理化的防措施,有利于提早做准备,防患于未然。

In recent decades, with the development of the economic , a series of questions is coming up .with the development of globalization, the financial crisis are spreading across the world .Southeast Asian financial crisis, which broke out in Thailand, quickly spread throughout the entire southeast of the world, made the stock market tumbling in many southeast Asian countries , , repeatedly trading financial system and even the entire social economy suffered serious wounds. the world financial crisis in 2008 detonated by Wall Street like giant wind tsunami, quickly spread around the world. Whether the countries of the European Union, or African ,in which economy have not been open, or the countries of Middle East, or rather, a series of new countries all felt this financial giant wind brings the crazy esau and shock.from world financial crisis caused by the Thai baht in1997 to the subprime mortgage crisis triggered in Amercia in2008, China faces the risk of economic downturn atrophy due to the external demand withered . This topic compared the causes , characteristics and influence of the international financial crisis in 1997 and 2008,through the study on the appearance of the financial crisis past dozens of years, grasp the economic operation of the law. Analysize andcomparied the causes of the financial crisis, the author sums up their inner similarities, then analyzes the current form of economic operation of the economic development of our country, find out the problems existed in the developing of our economic. propose corresponding rationalization suggestion. And through comparing the two economic crisis, summarized the characteristics and effects of the financial crisis after the outbreak of the influence of Chinese enterprises, and puts forward some precautionary measures, which is helpful for the rationalization of preparing early.正文一、两次金融危机演变过程比较分析(一)1997年亚洲金融危机的演变过程分析1997年6月,一场金融危机在亚洲爆发,这场危机的发展过程十分复杂。

1997~1998年亚洲金融风暴,的前因后果Microsoft Word 文档要点

1997~1998年亚洲金融风暴,的前因后果金融风暴启示录对冲基金(HedgeFund)意为“风险对冲过的基金”,起源于上世纪50年代初的美国,原指广泛利用金融衍生产品进行投资保值的一类基金,现今指利用各种金融衍生产品的杠杆效用,承担高风险、追求高收益的一种投资模式。

亚洲金融危机,又称亚洲金融风暴,是指1997年发源于泰国,之后进一步影响到临近亚洲国家,甚至全球货币、股票市场和其他资产价值的一场金融大危机。

其过程十分复杂,大致可分为三个阶段:第一阶段:1997年7月,以索罗斯为代表的国际金融投机者瞄准泰铢注入大量热钱,迫使泰国政府于7月2日宣布放弃实行了14年的泰币与美元挂钩的一揽子汇率制,实行浮动汇率制。

亚洲金融危机正式爆发,并很快波及菲律宾、印尼、马来西亚等其它东南亚国家;10月下旬,国际炒家移师香港,香港恒生指数自1996年以来首次跌破10000点;11月中旬,韩国爆发金融风暴,随之日本一系列银行和证券公司破产,东南亚金融风暴演变为亚洲金融危机。

第二阶段:1998年初,印尼金融风暴再起,由此陷入政治经济大危机。

受其影响,东南亚汇市再起波澜,新元、马币、泰铢、菲律宾比索等纷纷下跌,随之日元也大幅贬值,亚洲金融危机继续深化。

第三阶段:1998年8月初,国际炒家对香港发动新一轮进攻,香港特区政府予以回击,使其遭遇失利。

继而因俄罗斯国家政策的突变,在俄股市投下巨额资金的国际炒家再次大伤元气,并带动美欧国家股市、汇市的全面剧烈波动,由此亚洲金融危机具有了全球性的意义。

到1998年底,俄罗斯经济仍没有摆脱困境。

1999年,亚洲金融危机结束。

胡进、张才进:“全球金融动荡加剧的四大成因”, 《港澳经济》,1997年第3期。

而且过分集中于简单加工业。

结果在国际竞争日益加剧的冲击下,以劳动密集型产业为主体的东南亚国家出口扩张势头放缓,带动经济增长下降,从而导致经常项目赤字、外汇储备减少,进而对固定汇率产生压力,最终使金融风暴在区内广泛爆发。

1997亚洲金融危机ppt课件

• 1998年2月11日,印尼政府宣布将实行印尼盾与美元保持固定汇率的 联系汇率制,以稳定印尼盾。遭到国际货币基金组织及美国、西欧的 一致反对。国际货币基金组织扬言将撤回对印尼的援助,印尼陷入政 治经济大危机。

11

对中国的影响 对亚洲其他国家的影响 对世界的影响 教训和启示

12

对中国的影响

13

•房地产开发投资为例

14

•对香港经济的影响

股市:1997年10月20日,香港股市开始连续多日的下跌,恒生 指数由上周收盘的13601点一泻到23日的10426点,短短4天里 下降3175点。

15

3

发展过程

• 第一阶段

• 1997年7月2日,泰国宣布放弃固定汇率制,实行浮动பைடு நூலகம்率制,引发一 场遍及东南亚的金融风暴。

• 1997年8月,马来西亚放弃保卫林吉特的努力。一向坚挺的新加坡元 也受到冲击。

• 1997年10月下旬,国际炒家移师国际金融中心香港,矛头直指香港联 系汇率制。台湾当局突然弃守新台币汇率,加大了对港币和香港股市 的压力。

7

1.东亚模式中出口替代战略的缺陷 在东亚发展模式中,其产业定位与发展战略方面上是以劳 动密集型产业为最优发展产业,其推行出口导向型经济发展 战略,甚至有些国家还大量引进外部发达国家的资本。出口 替代战略曾经使得亚洲大多数国家实现了经济的繁荣与成功, 但是这一战略模式有着一定的缺陷。出口替代战略是指着重 发展出口导向工业,从而使工业品代替初级产品成为出口的 主要项目。然而,这一战略会使国家经济对于外部具有很严 重的依赖性。

8

AsianCrisis亚洲金融危机英文版

Southeast Asia in 1997

Russia in 1998 They faced sudden currency depreciations(贬值) due to

speculative attacks or large outflows of funds

IMF History and Background

What happened in East Asia is not peculiar(特殊的), but

has already happened to:

Many Latin American countries in 1980s Sweden and Norway in the early 1990s

1. A government should settle its own policies to protect its economy structure.

2. Speculators seek weakness

3. The IMF: an antiquated(陈旧的) system

Q A &?!

由于在出口的蓬勃发展,有必要的资金,以资助其 出口行业和其他经济活动的增加。 当时全球金融市 场的开放,对外部资金的来源提供了一个完美的途 径。 然而,最终这些借款将扩大的经常账户赤字。

当一个国家的经常账户赤字扩大,加上出口下降, 由于外国资金的流入,货币高估,它会吸引货币投 机者的关注。受影响rev的ers经e flo济w o体f fu政nds府’ 将试图捍卫其货 币,无论是通过提高利率或使用其外汇储备货币撑 起。 当他们提高利率,最终将带来银行业由于增加 国外借贷成本。 最终会有“逆转资金流动”-从外国 资金流入到流出。 有了这样的资金流出,将导致信 贷紧缩,加上高利率,它最终将影响房地产和银行

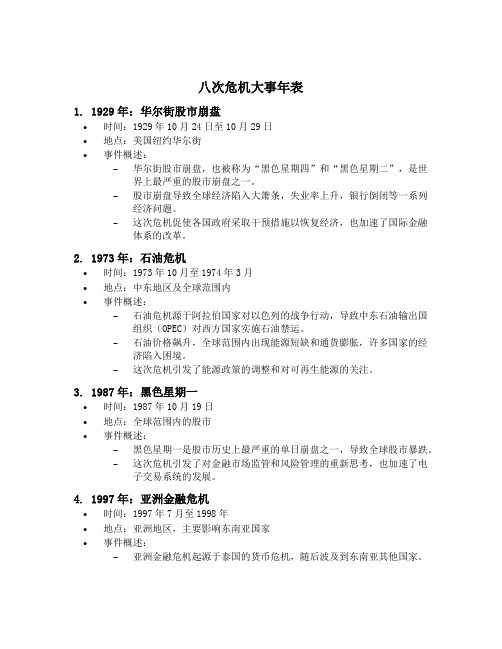

八次危机大事年表

八次危机大事年表1. 1929年:华尔街股市崩盘•时间:1929年10月24日至10月29日•地点:美国纽约华尔街•事件概述:–华尔街股市崩盘,也被称为“黑色星期四”和“黑色星期二”,是世界上最严重的股市崩盘之一。

–股市崩盘导致全球经济陷入大萧条,失业率上升,银行倒闭等一系列经济问题。

–这次危机促使各国政府采取干预措施以恢复经济,也加速了国际金融体系的改革。

2. 1973年:石油危机•时间:1973年10月至1974年3月•地点:中东地区及全球范围内•事件概述:–石油危机源于阿拉伯国家对以色列的战争行动,导致中东石油输出国组织(OPEC)对西方国家实施石油禁运。

–石油价格飙升,全球范围内出现能源短缺和通货膨胀,许多国家的经济陷入困境。

–这次危机引发了能源政策的调整和对可再生能源的关注。

3. 1987年:黑色星期一•时间:1987年10月19日•地点:全球范围内的股市•事件概述:–黑色星期一是股市历史上最严重的单日崩盘之一,导致全球股市暴跌。

–这次危机引发了对金融市场监管和风险管理的重新思考,也加速了电子交易系统的发展。

4. 1997年:亚洲金融危机•时间:1997年7月至1998年•地点:亚洲地区,主要影响东南亚国家•事件概述:–亚洲金融危机起源于泰国的货币危机,随后波及到东南亚其他国家。

–危机导致货币贬值、股市崩盘、经济衰退等一系列问题,许多企业倒闭,失业率激增。

–国际货币基金组织(IMF)提供援助并推动了相关国家经济体制的改革。

5. 2000年:互联网泡沫破裂•时间:2000年3月至2002年10月•地点:美国及全球范围内的科技股市•事件概述:–互联网泡沫破裂是指因为投资者对互联网公司高估价值而导致股市崩盘。

–许多互联网公司破产,投资者损失惨重,科技股市陷入低迷。

–这次危机促使投资者更加审慎,也推动了科技行业的整合和重组。

6. 2008年:全球金融危机•时间:2008年9月至2010年•地点:全球范围内,主要影响美国和欧洲国家•事件概述:–全球金融危机起源于美国次贷危机,随后蔓延到全球金融体系。

1997亚洲金融危机

中国政府

2000亿美元外汇储备

香港特区政府

动用外汇储备进入市场干预

60余亿美元

卖股票

120亿美元

•影响

索罗斯等代表的国际投机资金并不可怕,只要你有实力,那 些投机者是不敢轻易动你的,哪怕你的金融体制确实有问题。既然 国际投机资金不可怕,而实行人民币自由兑换可以促进人民币早日 成为国际贸易结算和储备货币,这对我国的经济发展是大大有利的, 为何不尽早舍弃钉住美元的外汇管制制度,实行自由外汇制度呢? 实行自由外汇制度并不是政府真的对人民币汇率撒手不管。恰恰相 反,我国政府从那场危机得出相反的结论,认为国际投机资金太可 怕,必须实行外汇管制制度,从而错失了1999-2000年间外汇制度改 革的良机 。

0.2 1

0.4

0.6

0.8

1.2

0

1997M3 1997M4 1997M5 1997M6 1997M7 1997M8 1997M9 1997M10 1997M11 1997M12 1998M1 1998M2 1998M3 1998M4

泰国 印度尼西亚 马来西亚

汇率指数(1997年3月—1998年9月)

1.东亚模式中出口替代战略的缺陷 在东亚发展模式中,其产业定位与发展战略方面上是以劳 动密集型产业为最优发展产业,其推行出口导向型经济发展 战略,甚至有些国家还大量引进外部发达国家的资本。出口 替代战略曾经使得亚洲大多数国家实现了经济的繁荣与成功, 但是这一战略模式有着一定的缺陷。出口替代战略是指着重 发展出口导向工业,从而使工业品代替初级产品成为出口的 主要项目。然而,这一战略会使国家经济对于外部具有很严 重的依赖性。

菲律宾

1998M5 1998M6 1998M7

注:①美元对每种本币的汇率;②1997年3月=1

高分作文范文-1997年的一次金融危机使他破产了

生活就像一面镜子。

你对它哭,它也对你哭,如果你想要它对你微笑,你只有一种办法,就是对它——微笑。

微笑是最美好最迷人的一种表情。

诚、温馨、快乐。

人生中有成功就有失败,失败不意味着你是一个失败者,失败表明你尚未成功;失败不意味着你没有努力,失败表明你的努力还不够;失败不意味着你必须忏悔,失败表明你还要吸取教训;失败不意味着你一事无成,失败表明你得到了经验;失败不意味着你无法成功,失败表明你还需要一些时间;失败不意味着你会被打倒,失败表明你要微笑面对。

微笑面对你身边的一切。

失败是一道菜,一道难以下咽的苦菜,但你要把它吃下去。

当朋友离你而去,当苦苦追求的梦想屡受挫折,你便知道了人间的苦涩。

你徘徊,你失落,甚至想死,但你还是不想放弃,很不甘心。

同时,你也会意识到,失败不过是酸甜苦辣的人生中的一碟小菜。

凡真正大的智慧,往往源于失败的教训。

古今中外,大多数成功者都经历过失败,可贵的是他们的勇气。

马克。

吐温经商失意,弃商从文,结果一举成名。

因为他曾经微笑面对过失败。

巴尔扎克说:“世界上的事情永远不是绝对的,结果因人而异,苦难对于天才是一块垫脚石,对能干的人是一笔财富,对于弱者是一个万丈深渊。

”我们要在失败中吸取经验教训,体会方法,思考原因,这样,我们才会变地成熟,才会成功。

我们不能单单停留在失败上,要微笑着面对失败,迎接新一次的挑战,正如拿破仑所说的“避免失败的最好方法,就是决心获得下一次成功。

”如何面对失败?微笑着面对失败,失败并不意味着什么,失败只表明你需更加努力。

泰国商人施利华,是商界上拥有亿万资产的风云人物。

1997年的一次金融危机使他破产了,面对失败,他只说了一句:“好哇!又可以从头再来了!”他从容地走进街头小贩的行列叫卖三明治。

一年后,他东山再起。

然而他微笑面对了失败,他重生了。

失败是人生的熔炉。

它可以把人烤死,也可以使人变得坚强、自信。

如果我们曾经微笑面对过失败,那在我们年迈时,我们可以对自己的子孙后代说:“我们曾笑对失败。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

The reasons of the outbreak

2. Effects of American economic interests and policy;

3. Factors of George Soros's personal and some support his group of capitalism;

(中央坚持人民币不贬值)

The IMF created a series of bailouts

* structural adjustment package" (SAP).(结构调整计划) *There were to be adequate government controls set up to supervise all financial activities, ones that were to be independent, in theory, of private interest.(私人利益) *IMF and high interest rates(国际货币基金组织和高利率)

Background

The impacts of the Asian financial in Hong Kong

Methords

Effects

Background

1. In the second half of 1997, Soros(索罗斯), an American financial expert used his hedge fund to launch repeated attacks of Asian countries and regions, and he got a great success.

Measures of China and HongKong government resisting crisis

The outbreak of the Asian financial crisis

1. Asian countries’ economic patterns(Singapore, Malaysia, Thailand, Japan ,Korea are export-oriented economy countries.) ;

(1997年6-7月,索罗斯把矛头对准港元,开始有计划地向香港股市和期市发动冲击。)

Methords

accumulated a large amount of short positions

(国际投机者先在期指市场上积累大量淡仓)

bought forward dollar and put forward the Hong Kong dollar

(买上远期美元,沽远期港元)

then speculators would sell a lot of futures, so the price of futures declined substantially

(这时投机者便趁势大沽期指,令期指大跳水)

speculators could flat out short positions and obtain huge profits.

(1997年下半年,美国金融学家索罗斯旗下的对冲基金对亚洲各国和地区发起了连番 狙击,并获得了极大的成功。)

2. On June 1997, Soros aimed at the Hong Kong dollar and began to launch the impact to the Hong Kong stock market and futures market

1. Using the enormous reserves of foreign exchange to accept HK dollar

(动用庞大的外汇储备吸纳港元)

2. Increase interest rate and decrease money supply

(调高利息并抽紧银根)

3. the central government decided to keep the value of the RMB as it was.

(恐慌性地沽出股票,炒家就可平掉淡仓而获取丰厚的利润)

Effects

1.The slump of stock market 2.The falling of housing market 3.The reform of government policies

measures of China and HongKong government resisting crisis

The Asian Financial Crisis in 1997

---Hong Kong

The Asian financial crisis in 1997

The outbreak of the Asian nancial crisis

The impacts of the Asian financial crisis in Hong Kong