会计学-企业决策的基础 答案

会计学:企业决策的基础Chap019

19 COSTING AND THE VALUE CHAIN Chapter SummaryThe value chain is used to organize the discussion of several aspects of strategic cost management. These include activity-based management, target costing, just-in-time inventory procedures, and total quality management.Activity based management utilizes cost information from ABC systems to identify and eliminate non-value-added activities. While Chapter 17 focused on activity-based product costs, this chapter develops an extensive illustration to demonstrate the management of activities associated with period costs. This is done to emphasize the application of activity-based management across all phases of the value chain.Target costing begins with planning and market analysis of customer needs, then proceeds to product development to generate a target price. Value engineering leads to the most economically efficient combination of resources to create the product. Finally, the target cost is attained through production and continuous improvement. A straightforward example illustrates the execution of the four phases of the target costing process.The development of just-in-time inventory and production systems was one of the earliest efforts of management to identify non-value-adding activities. The realization that investment of resources in inventory added no value to the customer initiated the development of the just-in-time philosophy. This philosophy emphasizes that all production is driven by customer demand. The chapter centers on the importance of supplier relationships, product quality, and flexible manufacturing in achieving the JIT objective of controlling product costs.The chapter concludes with a discussion of the components of quality costs and the tradeoffs between prevention and appraisal costs on one hand and the costs of internal and external failure on the other.Learning Objectives1.Define the value chain and describe its basic components.2.Distinguish between non-value-added and value-added activities.3.Explain how activity-based management is related to activity-based costing (ABC).4.Describe the target costing process and list its components.5.Identify the relationship between target costing and the value chain.6.Explain the nature and goals of a just-in-time (JIT) manufacturing system.7.Identify the components of the cost of quality.8.Describe the characteristics of quality measures.Brief Topical OutlineA The value chain1 International financial reporting standards and the value chain2Value- and non-value-added activities - see Your Turn (page 845)B Activity-based management1Activity-based management across the value chaina Managing activities: an illustration (pages 846 - 848) - see Case inPoint (page 849)2 ABC: A subset of activity-based managementC The target costing process1Components of the target costing process2 Target costing: an illustration - see Your Turn (page 852)3Characteristics of the target costing processD Just-in-time inventory procedures1 JIT, supplier relationships, and product quality2Measures of efficiency in a JIT systema Measuring qualityE Total quality management and the value chain1Components of the cost of quality - see Case in Point (page 857)2Measuring the cost of quality3Productivity and quality –see Ethics, Fraud & Corporate Governance (page 858)F Concluding remarksTopical coverage and suggested assignmentComments and observationsTeaching objectives for Chapter 19Our goal in presenting this material is to help students to begin to think strategically about the development and use of cost information. In so doing our objectives are to:1 Introduce the value chain as a structure for strategic cost management.2Explain the distinction between value-added and non-value-added activities across the value chain.3 Show that activity-based costs are important to reducing and eliminating non-value-addedactivities.4 Explain how activity-based costs can be used to manage not only production, but alsoactivities across all components of the value chain.5 Introduce target costing and its components.6 Explain the JIT approach to identifying and reducing non-value-added activities.7 Present measures of efficiency in a JIT manufacturing system.8 Explain the trade-offs that exist among components of quality costs, and how thosetrade-offs change with technical progress.General commentsManaging activities across the value chain represents a comprehensive integrated approach to the traditional management functions of planning and control. Eliminating non-value-added activities from the chain is central to this strategic approach to cost management. Exercise 3 is designed to acquaint students with the value chain and the identification of non-value-added activities in the chain.We have emphasized that the ABC model developed in a previous chapter can be usefully extended beyond product costing to a wide variety of period costs. Doing so provides an opportunity to use ABC information to manage across the entire value chain. This can be illustrated using Exercise 4. Although Problem 2requires the calculation of target costs, it provides a comprehensive opportunity for students to use cost information to address activity- based management issues. We highly recommend reviewing this problem in class. Case 1 is a more extensive alternative.Target costing illustrates the use of cost information in planning and designing new products as well as reengineering existing ones. Problem 3 captures the use of cost estimates and budgets in the planning process. It also addresses the issue of process design to minimize production costs.Quality costing, like ABM, emphasizes activity management across the value chain. Prevention costs apply to the research and design phase, as well as in working with suppliers and vendors. Appraisal costs and internal failures are most closely identified with the suppliers and production component. Finally, external failure costs exert a significant impact on customer service. Managing quality activities across the value chain highlights the tradeoffs among these costs.Supplemental ExercisesInternet ExerciseDid you ever stop to notice that all the credit, debit, and ATM cards that you carry have exactly the same thickness. This is true worldwide and is crucial to transactions processing. How did this worldwide coordination come to be? Explore the website of the International Organization for Standardization at What are the goals of this organization? Write a brief report describing the information you are able to obtain from this site.CHAPTER 19 NAME #10-MINUTE QUIZ A SECTIONIndicate the best answer for each question in the space provided.1Examples of value-added activities include all of the following except:a Product design.b Material movement.c Assembly activities.d Establish an effective distribution network.2Of the following components of total quality cost, which is most damaging to a company attempting to achieve a reputation as a world-class manufacturer?a Prevention costs.b Appraisal costs.c Internal failure costs.d External failure costs3Of the following processes, which is chiefly concerned with products and services that have not yet been developed?a Just-in-time manufacturing.b Activity-based management.c Target costing.d Total quality management.4For a furniture manufacturer, which of the following activities could not be eliminated without changing the customer’s perception of the product’sdesirability?a Inspection of incoming shipments of wood and fabrics.b Movement of work-in-process from one work station to another.c Set-up of machinery to produce different pieces of furniture.d Reducing the product’s distribution network.5The cost borne by the customer of disposing of nickel-cadmium batteries is a component of the batteries’:a Life-cycle cost.b Overhead cost.c Cost of quality.d Direct production cost.CHAPTER 19 NAME #10-MINUTE QUIZ B SECTIONListed below are eight technical accounting terms introduced or emphasized in this chapter: Activity-based management Life-cycle costingValue-added activity Non-value-added activityTarget costing Total quality managementJust-in-time manufacturing system Cycle timeEach of the following statements may (or may not) describe one of these technical terms. In the space provided below each statement, indicate the accounting term described, or answer “None” if the statement does not correctly describe any of the terms.a The process of using activity-based costs to help reduce or eliminate non-value-addedactivities.______________________________b Can be eliminated without affecting the desirability of the product from the perspectiveof the customer.______________________________c The length of time for a product to pass completely through a specific manufacturingprocess.______________________________d If eliminated, the desirability of the product to consumers is decreased.______________________________e Consideration of all potential resources that will be consumed by a product fromdevelopment through disposal.______________________________f A method in which a product’s selling price is determined by adding a fixed profitmargin to its production cost.______________________________g An approach that explicitly monitors quality costs and rewards quality enhancingbehavior.______________________________CHAPTER 19 NAME # ______ 10-MINUTE QUIZ C SECTIONListed below are eight components of the total cost of quality. In the space provided identify each as a cost of prevention, appraisal, internal failure, or external failure.1.Product design2.Product returns due to defects3.Inspection of raw materials shipments4.Employee training5.Rework of defective units prior to shipment6.Estimated lost sales due to poor quality7.Warranty expense8.Inspection of finished goods9.ScrapCHAPTER 19 NAME #10-MINUTE QUIZ D SECTIONResourceful Corporation is considering the implementation of a JIT inventory system. The company recently analyzed its cycle time to determine the average number of days spent in each activity of its production process. A summary of the analysis is shown below:Production Activity Number of Days Receiving materials 1Inspecting materials 4Storing materials 9Moving materials into production 6Setting-up production equipment 7Cutting materials 6Assembling materials 7Painting finished products 4Packaging finished products 1a Resourceful’s value-adding production activities include:b Resourceful’s total cycle time is __________ days.c Resourceful’s manufacturing efficiency ratio is __________%.d Which activities might be reduced or eliminated should Efficient implement a JITsystem?SOLUTIONS TO CHAPTER 19 10-MINUTE QUIZZESQUIZ A1 B2 D3 C4 D5 ALearning Objective: 2, 3, 4. 6, 7QUIZ Ba Activity based managementb Non-value-added activitiesc Cycle timed Value-added activitye Life cycle costingf Target costingg Total quality managementLearning Objective: 1 - 8QUIZ CPreventionExternal failureAppraisalPreventionInternal failureExternal failureExternal failureAppraisalInternal failureLearning Objective: 7, 8QUIZ Da Cutting materials, Assembling materials, Painting finished products, Packaging finished products.b 45 daysc 18/45 = 40%d Receiving materials, storing materials, moving materials into productionLearning Objective: 6Chapter 19 - Costing and The Value ChainAssignment Guide to Chapter 1919-10 Instructor’s Resource Manual Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.。

会计学-企业决策的基础 问题详解

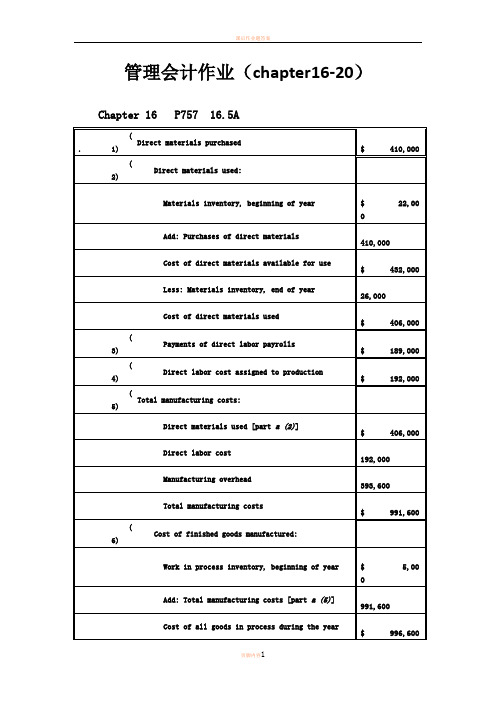

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22.50 per direct laborhourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line. Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1a. job costing (each project of a construction company is unique)b . both job and process costing (institutional clients may represent unique jobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d . process costing (the dog houses are uniformly manufactured in high volumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Aa4,000 EU $61.50 = $246,000 b4,000 EU $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target OperatingIncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学 企业决策的基础 财务会计分册 版 章答案

Chapter 6Merchandising Activitie s Ex. 6.41PROBLEM 6.1AClaypool earned a gross profit rate of 32%, which is significantly higher than the industry average. Claypool’s sales were above the industry average, and it earned $77,968 more gross profit than the “average” store of its size. This higher gross profit was earned even though its cost of goods sold was $18,000 to $20,000 higher than the industry average because of the additional transportation charges.To have a higher-than-average cost of goods sold and still earn a much larger-than-average amount of gross profit, Claypool must be able to charge substantially higher sales prices than most hardware stores. Presumably, the company could not charge such prices in a highly competitive environment. Thus, the remote location appears to insulate it from competition and allow it to operate more profitably than hardware stores with nearby competitors.PROBLEM 6.5Ac. Yes. Sole Mates should take advantage of 1/10, n/30 purchase discounts, even if itmust borrow money for a short period of time at an annual rate of 11%. Bytaking advantage of the discount, the company saves 1% by making payment 20 days early. At an interest rate of 11% per year, the bank charges only 0.6%interest over a 20-day period (11% X 20/365 = 0.6%). Thus, the cost of passing up the discount is greater than the cost of short-term borrowing.Chapter 7 Financial assetsChapter 8 Inventories and the cost of goods soldSupplementary ProblemChapter 91617。

会计学企业决策的基础 答案

管理会计作业(chapter16-20) Chapter 16 P757 16、5AChapter 16 P761 16、4BChapter 17 P802 17、3Aa、Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22、50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17、8Ad、The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line、Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line、If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace、This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline、e、The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality、Chapter 18 P835 18、1B、Ex、a、job costing (each project of a construction company is unique)18、1b、both job and process costing (institutional clients may representunique jobs)c、job costing (each set of equipment is uniquely designed andmanufactured)d、process costing (the dog houses are uniformly manufactured inhigh volumes)e、process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18、3A4,000 EU @ $61、50 = $246,000b4,000 EU @ $13、50 = $54,000Chapter 18 P845 18、2Ba、(1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b、In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a)、Chapter 20 P918 20、1Ad、No、With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even、Chapter 20 P918 20、2AChapter 20 P920 20、6ASales volume required to maintain current operating income:Sales Volume = Fixed Costs + Target OperatingIncomeUnit Contribution Margin= $390,000 + $350,000= $20,000 units $37。

会计学企业决策的基础

会计学企业决策的基础会计学作为现代企业管理的基本学科,对企业决策具有重要的支撑作用。

在企业运营过程中,会计学有助于企业管理者更加准确地把握企业的经营状况,制定科学的决策方案。

本文将从会计学对企业决策的作用、职能以及核算体系等方面进行探讨。

会计学对企业决策的作用1.提供信息支持:会计学的主要职责是收集、处理和汇报企业财务信息,通过财务报表、经营分析报告等形式,为企业管理者提供准确、全面的信息支持,帮助管理者把握企业经营状况,制定决策方案。

2.帮助评估经营结果:会计学通过记录和反映企业经济活动的历史,反映和评价企业的经营状况,判断企业各项事务的优劣,帮助管理者做出合理的经营决策。

3.辅助经营风险管理:通过会计核算,可以实现对企业不同部门、不同环节的财务状况监控,帮助管理者识别、分析和评估风险,及时采取措施控制或缓解风险。

4.促进企业治理:会计学通过财务报告等信息披露,监督企业管理行为,维护股东、投资者等人的合法权益,促进企业的良性治理。

会计职能对企业决策的支持1.记账职能:会计的首要职责是记录企业的经济业务活动,通过会计帐簿的形式,反映企业的经济状况,为企业决策提供准确的信息支持。

2.核算职能:会计核算是会计学的核心内容,贯穿整个会计工作,在企业决策中具有举足轻重的地位。

经过核算,企业能够准确、全面地了解自己的财务状况,制定合理的决策方案。

3.处理职能:会计处理职能是指利用会计方法和技术,对企业的财务信息进行分析和处理,在企业决策中发挥重要作用。

通过处理,会计人员能够对经济事务进行有序管理,优化企业的决策效果。

4.报告职能:会计报告包括财务报表、经营分析报告等,是向企业管理者、股东等外部人员提供的信息。

会计人员通过报告,向外部用户传达企业的财务状况,以便他们能够了解企业的经营状况,做出相应的决策。

会计核算体系对企业决策的支持1.资产负债表:资产负债表反映企业的资产、负债和所有者权益状况,是企业财务状况的总结表。

会计学-企业决策的基础 答案教学资料

会计学-企业决策的基础答案管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based on machine-hours:Manufacturing Overhead= $420,000= $35 per machine-hourMachine-Hours 12,000Department Two overhead application rate based on direct labor hours:Manufacturing Overhead= $337,500= $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct laborhours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probablyexplains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costingsystem include: (1) a better identification of its operating inefficiencies, (2) a betterunderstanding of its overhead cost structure, (3) a better understanding of theresource requirements of each product line, (4) the potential to increase the sellingprice of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability todecrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1a. job costing (each project of a construction company is unique)B. Ex.18.1b. both job and process costing (institutional clients may represent uniquejobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d. process costing (the dog houses are uniformly manufactured in highvolumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Ab4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target Operating IncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37。

会计学企业决策的基础财务会计分册第17版

会计学企业决策的基础财务会计分册第17版下载提示:该文档是本店铺精心编制而成的,希望大家下载后,能够帮助大家解决实际问题。

文档下载后可定制修改,请根据实际需要进行调整和使用,谢谢!本店铺为大家提供各种类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by this editor. I hope that after you download it, it can help you solve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you! In addition, this shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts, other materials and so on, want to know different data formats and writing methods, please pay attention!企业决策在当前竞争激烈的市场环境中显得尤为重要。

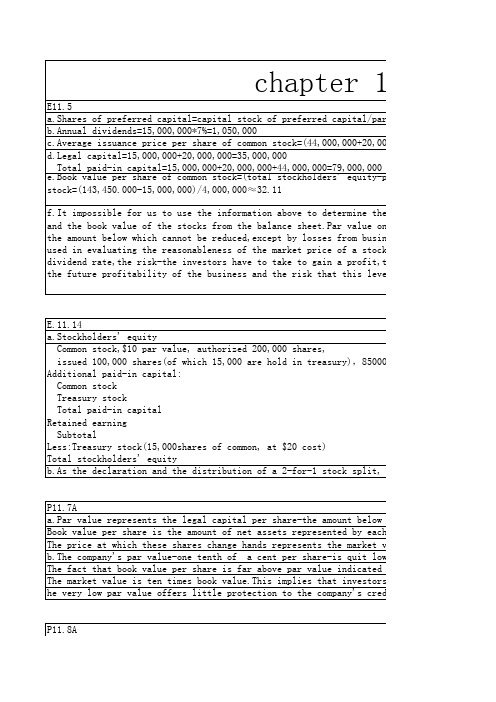

会计学企业决策的基础 课后习题 答案 chapter

Total paid-in capital=15,000,000+20,000,000+44,000,000=79,000,000 e.Book value per share of common stock=(total stockholders' equity-preferred stock)/shares stock=(143,450.000-15,000,000)/4,000,000≈32.11

会计学企业决策的基础chapter2 答案

(5)(6)(7)(8)(9)Owner’s equity is not valued at either the original amountinvested or at the estimated market value of the business. In fact, owner’s equity cannot be valued independently of the values assigned to assets and liabilities. Rather, it is a residual figure—the excess of total assets over totalliabilities. (If liabilities exceed assets, owners' equity would be a negative amount.) Thus the amount of Berkeley's capital should be determined by subtracting the corrected figure for total liabilities ($23,100) from the corrected amount of total assets ($51,500). This indicates owners'equity of $28,400.The $22,400 described as “Other assets” is not an asset,because there is no valid legal claim or any reasonable expectation of recovering the income taxes paid. Also, the payment of federal income taxes by Pippin was not abusiness transaction by Big Screen Scripts. If a refund were obtained from the government, it would come to Pippin personally, not to the business entity.The proper valuation for the land is its historical cost of$39,000, the amount established by the transaction in which the land was purchased. Although the land may have acurrent fair value in excess of its cost, the offer by the friend to buy the land if Pippin would move the building appears to be mere conversation rather than solid, verifiable evidence of the fair value of the land. The "cost principle," although less than perfect, produces far more reliable financial statements than would result if the owners could "pull figures out of the air" in recording asset values.The accounts payable should be limited to the debts of the business, $32,700, and should not include Pippin’s personal liabilities.The amount owed to stagehands for work done throughSeptember 30 is the result of completedtransactions and should be included among the liabilities of the business. Even if agreement hasbeen reached with Mario Dane for her to perform in a future play, he has not yet performedand therefore, is not yet owed any money. Thus, this $25,000 is not yet a liability of thebusiness.therefore cannot be included in the assets. To do so would cause an overstatement of both assets and owners’ equity.The “Office furniture” amount must be reduced by $2,525.invested or at the estimated market value of the business. In fact, owner’s equity cannot be valued independently of the values assigned to assets and liabilities. Rather, it is a residual figure—the excess of total assets over total liabilities. (If liabilities exceed assets, owners' equity would be a negative amount.) Thus the amount of Berkeley's capital should be determined by subtracting the corrected figure for total liabilities ($23,100) from the corrected amount of total assets ($51,500). This indicates owners' equity of $28,400.。

会计学企业决策的基础《会计学企业决策的基础》

§ 负债(Liabilities)是由过去的交易、事项形 成的现有义务,履行该义务预期会导致经济 利益流出企业。

§ 负债的特征是:

§ (1)负债是由于过去的交易或事项所引起的企 业的现有义务。企业预期在将来要发生的交 易或事项可能产生的债务,不能作为会计上 的负债处理;

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

PPT文档演模板

•成本和收入决定: • 分批成本法 • 分步成本法 • 作业成本法 •销售:收入和利润 •资产和负债 •厂房和设备 •贷款和资产 •应收和应付款项 •现金和存款 •现金流: • 经营活动现金流 • 筹资活动现金流 • 投资活动现金流

•决策支持 •本-量-利分析 •业绩评估 •增值分析 •预算 •资本分配 •每投收益 •比率分析

会计学企业决策的基础《会计学企业 决策的基础》

三、所有者权益

§所有者权益(owner‘s equity),是所有者在企 业资产中享有的经济利益,其金额为资产减 去负债后的余额。它表明企业的资产总额在 抵偿了现存的一切债务后的差额,所有者享 有的份额。

§ 所有者权益就其形成看,除投入资本与资本 公积外,主要来源于企业的经营积累。

会计行为可分为三类:

§ (一)会计核算行为 § 即以货币为主要的计量单位,采用专门方法,

通过计量、计算、记录、分类、汇总等程序, 对单位的经济活动进行连续、系统、完整的 反映,以提供会计信息的活动。

PPT文档演模板

会计学企业决策的基础《会计学企业 决策的基础》

(二)会计监督行为

§ 即从单位内部和外部对单位会计核算本身, 以及纳入经济核算范围之内的经济业务事项 进行监督的活动。

公布等,特别是对其中的会计信息进行监督,以防 欺骗投资人。 § (4)财税部门——对纳税额的监督核实。 § (5)工会、职工、社会公众、专业分析师等。

会计学基础试题及答案(1-3章)

第一章练习题1.会计主体是〔〕A.企业单位B.企业法人C.法律主体D.独立核算的特定单位正确答案:D解析:D、会计主体是指企业会计确认、计量和报告的空间范围,即会计核算和监督的特定单位或组织。

2.企业会计分期假设是以〔〕假设为前提的。

A.会计主体B.持续经营C.历史本钱D.货币计量正确答案:B解析: B、会计分期是对企业持续经营的生产经营活动人为划分为一个个连续的、长短相同的期间。

3.〔〕假设明确了会计工作的空间范围A.会计主体B.持续经营C.会计客体D.会计分期正确答案:A解析:A、会计主体这一会计根本假设,对会计确认、计量和报告范围从空间上作了有效界定。

4.会计核算的内容是特定会计主体的〔〕A.经济资源B.经济活动C.资金运动D.劳动成果正确答案:C解析: C、会计的对象是指会计所核算和监督的内容。

但凡特定主体能够以货币表现的经济活动,都是会计对象。

以货币表现的经济活动通常又称为资金运动。

因此,会计核算和监督的内容即会计对象就是资金运动。

5.以下哪一项描述会计的含义是不正确的?A.商业语言B.是目的而不是到达目的的手段C.决策有用的D.信息系统正确答案:B解析: B、会计是一种商业语言,但它不是目的,它是一种工具,具有核算和监督两项根本职能,并且也具有预测经济前景、参与经济决策、评价经济业绩等拓展职能,因此它是决策有用的,并且是一个信息系统。

6.以下有关会计主体假设的表达中,正确的〔〕A.界定会计主体是开展会计确认,计量和报告工作的重要前提B.明确会计主体,才能划定会计所要处理的各项事项的空间范围C.会计主体也等同于法律主体D.法律主体通常也是会计主体正确答案:A、B、D解析: C、会计主体是指企业会计确认、计量和报告的空间范围,即会计核算和监督的特定单位或组织。

一般而言,法律主体必然是一个会计主体,但是会计主体不一定是法律主体。

会计主体既可以是法人,如股份或有限责任公司,也可以是不具备法人资格的实体,如独资企业或合伙企业、集团公司、事业部、分公司、工厂的分部等。

会计学企业决策的基础管理会计分册作业答案19.2A培训资料

会计学企业决策的基础管理会计分册作业答案19.2AProblem19.2Aa.The target cost for KAP1= target price-profit margin=$120-15%×$120=$120×85%=$102The target cost for QUIN=$220×85%=$187b. Total manufacturing for KAP1=($30+$24)×25,000+(24÷2×3×25,000)+[2,000,000÷(25,000+15,000)×25,000]=$2,750,000b.So the total manufacturing cost per unit of KAP1=$2,750,000÷25,000=$110>$102 The same as KAP1, the total manufacturing cost for QUIN=$2,550,000So the total manufacturing cost per unit of QUIN=$2,550,000÷15,000=$170<$187 So QUIN is earning the desired return.c. Because the overhead costs are assigned on the basis of the direct labor hours, so we need to recalculate it.The total manufacturing cost for KAP1=($30+$24)×25,000+(24÷2×3×25,000)+ [2,000,000÷(24/12×25,000+60/12×15,000)*24/12×25,000=$2,300,000c.So the total manufacturing cost per unit of KAP1=$2,300,000÷25,000=$92<$102 The same as KAP1, the total manufacturing cost for QUIN=$3,000,000So the total manufacturing cost per unit of QUIN=$3,000,000÷15,000=$200>$187 So QUIN is earning the desired return.d. Using the activity-based costing method, the total manufacturing cost for KAP1= 400,000*1/5+600,000*2/3+500,000*2/6+200,000*5/8+300,000*3/5+($30+$24)×25,0 00+(24÷2×3×25,000)=$910,000d.So the total manufacturing cost per unit of KAP1=$96.4<$102The same as the KAP1, the total manufacturing cost for QUIN=$2,890,000So the total manufacturing cost per unit of QUIN=$2,890,000÷15,000=$192.67>$187 So KAP1 is earning the desired return.e. Because the activities of machining, purchase orders and shipping to customers are value-added activities, so the proportion of fixedoverhead=(600,000+500,000+300,000)÷2,000,000=70%In attempting to reach the target cost for QUIN, we would like to improve the activity of machine set-ups first because its proportion of all overhead cost is relatively big and it is easiest for the manufacturer to make the adjustment to lower down the target cost.f. Impact: the manufacturing cost of KAP1 increased and that of QUIN decreased. The new manufacturing cost per unit of KAP1=$106>$102The new manufacturing cost per unit of QUIN=$176.67<$187So QUIN is earning the desired return.g. If the machine was purchased, the manufacturing cost of KAP1=$2,370,000and the new manufacturing cost per unit of KAP1=$2,370,000÷25,000=$94.8<$102 And the manufacturing cost of QUIN=$2,730,000The new manufacturing cost per unit of QUIN=$2,730,000÷15,000=$183<$187 Both of the KAP1 and QUIN are earning the desired return, so the machine should be purchased.。

会计学-企业决策的基础 答案

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa.Department One overhead application ratebased on machine-hours:Manufacturing Overhead$420,000=$35 per machine-hourMachine-Hours 12,00 0Department Two overhead application rate based on direct labor hours:Manufacturing Overhead$337,500=$22.50 per direct laborhourDirect Labor Hours 15,00 0Chapter 17 P805 17.8Ad .The Custom Cuts product line is very labor intensive in comparison to theBasic Chunks product line. Thus, the company’s current practice of using direct labor hours to allocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e .The benefits the company would achieve by implementing an activity-basedcosting system include: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex. 18.1a.job costing (each project of a construction company is unique)b.both job and process costing (institutional clients may represent unique jobs)c.job costing (each set of equipment is uniquely designed and manufactured)d.process costing (the dog houses are uniformly manufactured in high volumes)e.process costing (the vitamins and supplements are uniformly manufactured in high volumes)Chapter 18 P841 18.3AInputs:•Beginning WIP•StartedOutputs:•Units completed•Ending WIP•Beginning WIP•Units started•Units completed•Ending WIP•Cost of beginning WIP•Cost added during the period•Cost of goods transferredtransferred•Add ending WIP$246,000b4,000 EU @ $13.50 =$54,000Chapter 18 P845 18.2Ba .(1)$49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2)$109 [($480,000 + $108,000 + $66,000) ÷6,000 units] (3)$158 ($49 + $109)(4)$32 ($192,000 ÷ 6,000 units)(5)$18 ($108,000 ÷ 6,000 units)b .In evaluating the overall efficiency of the Engine Department, managementwould look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad .No. With a unit sales price of $94, the break-even sales volume in unitsis 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units)$540,000$1054,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales VolumeFixed Costs + TargetOperating IncomeUnit Contribution Margin$390,000 + $350,000= $20,000 units $37。

会计学-企业决策的基础答案

会计学-企业决策的基础答案(总14页)--本页仅作为文档封面,使用时请直接删除即可----内页可以根据需求调整合适字体及大小--管理会计作业(chapter16-20)Chapter 16 P757Chapter 16 P761Chapter 17 P802a.Department One overhead application rate based onmachine-hours:Manufacturing Overhead=$420,000 =$35 per machine-hourMachine-Hours12,000Department Two overhead application rate based on direct labor hours:Manufacturing Overhead=$337,500=$ per direct labor hourDirect Labor Hours15,000Chapter 17 P805d.The Custom Cuts product line is very labor intensive in comparison to the BasicChunks product line. Thus, the company’s current practice of using direct labor hours to allocate overhead results in the assignment of a disproportionateamount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line is overpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e.The benefits the company would achieve by implementing an activity-basedcosting system include: (1) a better identification of its operating inefficiencies,(2) a better understanding of its overhead cost structure, (3) a betterunderstanding of the resource requirements of each product line, (4) thepotential to increase the selling price of Basic Chunks to make it morecomparable to competitive brands and possibly do so without having to sacrifice significant market share, and (5) the ability to decrease the selling price ofCustom Cuts without having to sacrifice product quality.Chapter 18 P835B. Ex. a.job costing (each project of a construction company is unique)b.both job and process costing (institutional clients may representunique jobs)c.job costing (each set of equipment is uniquely designed andmanufactured)d.process costing (the dog houses are uniformly manufactured in highvolumes)e.process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841b4,000 EU @ $ = $54,000Chapter 18 P845a.(1)$49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2)$109 [($480,000 + $108,000 + $66,000) ÷?6,000 units](3)$158 ($49 + $109)(4)$32 ($192,000 ÷ 6,000 units)(5)$18 ($108,000 ÷ 6,000 units)b.In evaluating the overall efficiency of the Engine Department, managementwould look at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918d.No. With a unit sales price of $94, the break-even sales volume in units is 54,000units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units)=$540,000$10=54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918Chapter 20 P920Sales volume required to maintain current operating income:Sales Volume ?Fixed Costs + Target Operating IncomeUnit Contribution Margin?$390,000 + $350,000= $20,000 units$37。

(完整版)会计学基础试题及答案(1-3章)

第一章练习题1.会计主体是()A.企业单位B.企业法人C.法律主体D.独立核算的特定单位正确答案:D解析:D、会计主体是指企业会计确认、计量和报告的空间范围,即会计核算和监督的特定单位或组织。

2.企业会计分期假设是以()假设为前提的。

A.会计主体B.持续经营C.历史成本D.货币计量正确答案:B解析: B、会计分期是对企业持续经营的生产经营活动人为划分为一个个连续的、长短相同的期间。

3.()假设明确了会计工作的空间范围A.会计主体B.持续经营C.会计客体D.会计分期正确答案:A解析:A、会计主体这一会计基本假设,对会计确认、计量和报告范围从空间上作了有效界定。

4.会计核算的内容是特定会计主体的()A.经济资源B.经济活动C.资金运动D.劳动成果正确答案:C解析: C、会计的对象是指会计所核算和监督的内容。

凡是特定主体能够以货币表现的经济活动,都是会计对象。

以货币表现的经济活动通常又称为资金运动。

因此,会计核算和监督的内容即会计对象就是资金运动。

5.下列哪一项描述会计的含义是不正确的?A.商业语言B.是目的而不是达到目的的手段C.决策有用的D.信息系统正确答案:B解析: B、会计是一种商业语言,但它不是目的,它是一种工具,具有核算和监督两项基本职能,并且也具有预测经济前景、参与经济决策、评价经济业绩等拓展职能,因此它是决策有用的,并且是一个信息系统。

6.下列有关会计主体假设的叙述中,正确的()A.界定会计主体是开展会计确认,计量和报告工作的重要前提B.明确会计主体,才能划定会计所要处理的各项事项的空间范围C.会计主体也等同于法律主体D.法律主体通常也是会计主体正确答案:A、B、D解析: C、会计主体是指企业会计确认、计量和报告的空间范围,即会计核算和监督的特定单位或组织。

一般而言,法律主体必然是一个会计主体,但是会计主体不一定是法律主体。

会计主体既可以是法人,如股份有限公司或有限责任公司,也可以是不具备法人资格的实体,如独资企业或合伙企业、集团公司、事业部、分公司、工厂的分部等。

会计学-企业决策的基础 答案

管理会计作业(chapter16-20)Chapter 16 P757 16.5AChapter 16 P761 16.4BChapter 17 P802 17.3Aa. Department One overhead application rate based onmachine-hours:ManufacturingOverhead = $420,000 = $35 per machine-hour Machine-Hours 12,000Department Two overhead application rate based on direct labor hours:ManufacturingOverhead = $337,500 = $22.50 per direct labor hourDirect Labor Hours 15,000Chapter 17 P805 17.8Ad. The Custom Cuts product line is very labor intensive in comparison to the Basic Chunksproduct line. Thus, the company’s current practice of using direct labor hours toallocate overhead results in the assignment of a disproportionate amount of total overhead to the Custom Cuts product line. If pricing decisions are set as a fixed percentage above the manufacturing costs assigned to each product, the Custom Cuts product line isoverpriced in the marketplace whereas the Basic Chunks product line is currently priced at an artificially low price in the marketplace. This probably explains why sales of Basic Chunks remain strong while sales of Custom Cuts are on the decline.e. The benefits the company would achieve by implementing an activity-based costing systeminclude: (1) a better identification of its operating inefficiencies, (2) a better understanding of its overhead cost structure, (3) a better understanding of the resource requirements of each product line, (4) the potential to increase the selling price of Basic Chunks to make it more comparable to competitive brands and possibly do so without having to sacrificesignificant market share, and (5) the ability to decrease the selling price of Custom Cuts without having to sacrifice product quality.Chapter 18 P835 18.1B. Ex.18.1a. job costing (each project of a construction company is unique)b . both job and process costing (institutional clients may represent unique jobs)c. job costing (each set of equipment is uniquely designed andmanufactured)d . process costing (the dog houses are uniformly manufactured in high volumes)e. process costing (the vitamins and supplements are uniformlymanufactured in high volumes)Chapter 18 P841 18.3Ab4,000 EU @ $13.50 = $54,000Chapter 18 P845 18.2Ba. (1) $49 [($192,000 + $48,000 + $54,000) ÷ 6,000 units](2) $109 [($480,000 + $108,000 + $66,000) ÷ 6,000 units](3) $158 ($49 + $109)(4) $32 ($192,000 ÷ 6,000 units)(5) $18 ($108,000 ÷ 6,000 units)b. In evaluating the overall efficiency of the Engine Department, management wouldlook at the monthly per-unit cost incurred by that department, which is the cost of assembling and installing an engine ($109 in part a).Chapter 20 P918 20.1Ad. No. With a unit sales price of $94, the break-even sales volume in units is 54,000 units:Unit contribution margin = $94 - $84 variable costs = $10Break-even sales volume (in units) = $540,000$10= 54,000 unitsUnless Thermal Tent has the ability to manufacture 54,000 units (or lower fixed and/or variable costs), setting the unit sales price at $94 will not enable Thermal Tent to break even.Chapter 20 P918 20.2AChapter 20 P920 20.6ASales volume required to maintain current operating income:Sales Volume =Fixed Costs + Target OperatingIncomeUnit Contribution Margin=$390,000 + $350,000= $20,000 units$37c.Current AfterCapacity Expansion(20,000Units)(25,000 Units) Total contribution margin ($37 per unit) $ 740,000 $ 925,000Less: Fixed costs390,000530,000*Operating income at full capacity $ 350,000$ 395,000*$390,000 + additional depreciation per year on newmachinery, $140,000 (20% of $700,000).盛年不重来,一日难再晨。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Direct labor costs assigned to production

230,000

Manufacturing overhead applied to production

400,000

Total manufacturing costs charged to work in process

9,000

Cost of finished goods manufactured

$ 987,600

Chapter 16P761 16.4B

a.

Purchases of direct materials

$ 360,000

b.

Cost of direct materials used:

Materials inventory, beginning of year

Add: Total manufacturing costs [parta (5)]

991,600

Cost of all goods in process during the year

$ 996,600

Less: Work in process inventory, end of year

9,000

Units in the activity base (direct labor costs)

230,000

Overhead stated as a percentage of direct labor costs

($400,000 ÷ $230,000)

174%

f.

Direct materials used (partb)

管理会计作业(

Chapter 16P757 16.5A

a.

(1)

Direct materials purchased

$ 410,000

(2)

Direct materials used:

Materials inventory, beginning of year

$ 22,000

Add: Purchases of direct materials

410,000

Cost of direct materials available for use

$ 432,000

Less: Materials inventory, end of year

26,000

Cost of direct materials used

$ 406,000

(3)

Payments of direct labor payrolls

Manufacturing overhead

393,600

Total manufacturing costs

$ 991,600

(6)

Cost of finished goods manufactured:

Work in process inventory, beginning of year

$ 5,000

$ 364,000

c.

Direct labor payrolls paid during the year

$ 225,000

d.

Direct labor costs assigned to production

$ 230,000

e.

Overቤተ መጻሕፍቲ ባይዱead costs during the year

$ 400,000

987,600

Cost of goods available for sale

$ 1,025,600

Less: Ending inventory of finished goods

25,000

Cost of goods sold

$ 1,000,600

(8)

Total inventory:

Materials inventory

$ 406,000

Direct labor

192,000

Manufacturing overhead

393,600

Total manufacturing costs

991,600

Cost of all goods in process during the year

$ 996,600

Less: Work in process, end of year

Cost of finished goods manufactured

$ 987,600

(7)

Cost of goods sold:

Beginning inventory of finished goods

$ 38,000

Add: Cost of finished goods manufactured [parta (6)]

$ 189,000

(4)

Direct labor cost assigned to production

$ 192,000

(5)

Total manufacturing costs:

Direct materials used [parta (2)]

$ 406,000

Direct labor cost

192,000

$ 18,000

Add: Purchases of direct materials

360,000

Cost of materials available for use

$ 378,000

Less: Materials inventory, end of year

14,000

Cost of direct materials used

$ 26,000

Work in process inventory

9,000

Finished goods inventory

25,000

Total inventory

$ 60,000

b.

HILLSDALE MANUFACTURING CORP.

Schedule of the Cost of Finished Goods Manufactured

$ 994,000

g.

Costs of finished goods manufactured:

For the Year Ended December 31, 20__

Work in process inventory, beginning of year

$ 5,000

Add: Manufacturing costs assigned to production:

Direct materials used [parta (2)]