国际会计英国会计报告共33页文档

英国 会计准则

英国会计准则(原创版)目录1.英国会计准则的概述2.英国会计准则的发展历程3.英国会计准则的特点4.英国会计准则与我国会计准则的比较5.英国会计准则对国际会计准则的影响正文一、英国会计准则的概述英国会计准则是指在英国境内适用的会计规范,其主要目的是为了保证企业财务报告的准确性、可靠性和一致性,以便于投资者、债权人、政府监管部门等各方进行经济决策。

英国会计准则包括一系列具体的会计处理方法和披露要求,涵盖了企业的资产、负债、收入、费用等各个方面。

二、英国会计准则的发展历程英国会计准则的发展历程可以追溯到 20 世纪初,当时主要依赖于各类会计职业团体发布的指导性文件。

随着经济的发展和会计职业化程度的提高,英国会计准则逐渐形成了以英国会计准则委员会(Accounting Standards Board,简称 ASB)为核心的制定体系。

ASB 成立于 1970 年,负责制定和修订会计准则,以适应市场经济的需求。

进入 21 世纪,英国会计准则又经历了一系列改革。

2005 年,英国政府成立了财务报告局(Financial Reporting Council,简称 FRC),取代了 ASB,成为英国会计准则的主要制定机构。

FRC 对会计准则的制定过程进行了改革,加强了与其他国家和地区会计准则制定机构的合作,推动了会计准则的国际化进程。

三、英国会计准则的特点英国会计准则具有以下特点:1.遵循国际会计准则:英国会计准则在很大程度上遵循了国际会计准则(International Financial Reporting Standards,简称 IFRS),力求与国际会计准则保持一致。

2.强调实质重于形式:英国会计准则强调企业应当根据经济实质进行会计处理,而不仅仅是按照法律形式。

3.鼓励披露:英国会计准则鼓励企业充分披露与财务报告使用者相关的信息,以提高财务报告的透明度。

四、英国会计准则与我国会计准则的比较英国会计准则与我国会计准则在很多方面存在相似之处,但在一些具体处理方法和披露要求上仍存在差异。

国际会计英国会计报告

日本

一、会计惯例与会计准则

惯例与准则联系又区别,会计准则是筛选出 来的“标准”会计惯例,会计惯例一般地说 是当时流行的会计准则。

宏观

英国是一个不成文法系国家,在会计 上“真实与公允”是至高无上的,无 论是公司法还是会计准则的执行都不 能违背这一准则

英国会计模式特征

1、《公司法》对会计行为的规范;

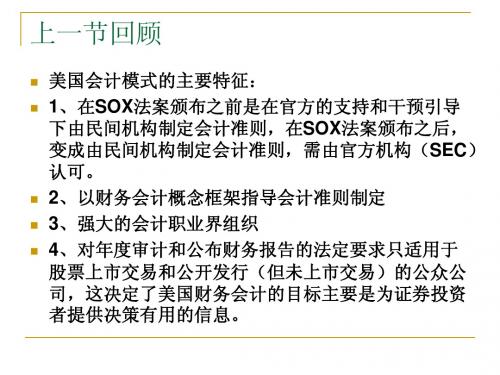

美英会计模式的差异处

1、会计规范形式不同。美国有数量庞大、规定细致的准则体系,英国受 《公司法》制约制定的会计准则数量较少,规定较粗,重视运用会计人员 的专业判断。 2、会计准则制定框架不同。英国是通过《公司法》管理公司事务,包括 对公司财务会计和报告的要求,而美国是以财务会计概念框架指导会计准 则的制定。 3、会计准则的制定方面。美国是在官方的支持和干预引导下由民间机构 制定会计准则,而英国的会计职业界民间组织在会计法规定方面所起的作 用和权威性 4、从会计核算及信息披露来看。美国的会计核算方法偏向乐观,不断创 新,在信息披露上强调保护股东的利益,提倡正是反映,并素以充分披露 而闻名;英国着重强调“真实与公允”的观念,是以保护公司的利益为主 要目的。

英国GAAP与IASC各个具体准则的差异分 析(只列举4个)

各个会计准则 收益 固定资产 英国概念框架 国际会计准则 在资产负债表优先的基础上 IAS18“收益”:在损益表优先 制定的 的基础上制定的

无形资产

FRS 15在资产重估时要求运 IAS 16要求对资产重估时运用 用与业务相关的价值,重估中 市场价值,发生重估盈余时不计 发生的损失计入损益表 入损益表 IAS 38只允许较 FRS 10允许无形资产采用无 长的折旧期限,协同中应予以统 限期的折旧期限 一规范

英国渐受“欧盟”的影响

英国财务报表

1.债券借款 2.银行借款及透支 3.预收款 4.应付商业账款 5.应付汇票 6.欠集团内公司账款 7.欠在其中参股的公司的账款 8.其他债务,包括税金和社会保险 9.应计及递延收益 F.净流动资产(负债) G.资产总额减流动负债 H.债务:一年后到期的金额 1.债券借款 2.银行借款及透支 3.预收款 4.应付商业账款 5.应付汇票 6.欠集团内公司账款 7.欠在其中参股的公司的账款 8.其他债务,包括税金及社会保险 9.应计及递延收益 I.备付负债及费用 1.养老金及类似债券 2.税金,包括递延所得税 3.其他准备 J.应计及递延收益 K 资本及公积金. Ⅰ.已缴股本 Ⅱ.股本溢价 Ⅲ.重估价储备 Ⅳ.其他公积金 1.资产赎回公积金 2.自由股份公积金 3.按公司章程提供的公积金 4.其他公积金 Ⅴ.损益 注:对集团会计来说,少数股权可插入在 K 上或 K 下

财务报表财务报表分析财务报表模板上市公司财务报表财务报表下载合并财务报表公司财务报表

英国财务报表——资产负债表

A.未付催缴股本 B.固定资产 Ⅰ无形资产 1.开发成本 2.特许权、专利权、许可权、商标及诸 如此类的权利和资产 3.商誉 4.暂付款 Ⅱ有形资产 1.土地及建筑物 2.厂房及机器 3.装置、配件、工具和设备 4.暂付款及在建资产 Ⅲ投资 1.集团内公司股份 2.对集团内公司的贷款 3.参股 4.对在其中参股的公司的贷款 5.除贷款外的其他投资 6.其他贷款 7 自有股份 C.流动资产 Ⅰ.存货 1.原材料及消耗品 2.在品 3.成品及待销商品 4.暂付款 Ⅱ债权 1.应收商业账款 2.集团内公司欠款 3.在其中参股的公司的欠款 4.其他应收款 5.未付催缴股本 6.预付款及应计收益 Ⅲ投资 1.集团内公司股份 2.总有股份 3.其他投资 Ⅳ.银行存款及库存现金 D 预付款及库存现金 E.债务:一年内到期的金额

国际会计准则融合的代表性经济变化结果:英国 (英文版)

Cross-sectional variation in the economicconsequences of international accountingharmonization:The case of mandatory IFRSadoption in the UK ☆Hans B.Christensen,Edward Lee ⁎,Martin WalkerManchester Accounting and Finance Group,Manchester Business School,Crawford House,Oxford Rd,Manchester,M139PL,UKAbstractThis study examines the economic consequences for UK firms of the European Union's decision to impose mandatory IFRS.We hypothesize that the impact varies across firms and is conditional on the perceived benefit.We estimate a counter-factual proxy for a UK firm's willingness to adopt IFRS from the prior GAAP choices of German firms.We show that this proxy predicts cross-sectional variations in both the short-run market reactions and the long-run changes in cost of equity that are associated with the decision.This implies that mandatory IFRS adoption does not benefit all firms in a uniform way but results in relative winners and losers.©2007University of Illinois.All rights reserved.Keywords:International Financial Reporting Standards;Mandatory adoption;Economic consequencesAvailable online at The International Journal of Accounting42(2007)341–379☆The authors are from the Manchester Accounting and Finance Group,Manchester Business School.We would like to thank Rashad Abdel-khalik,Willem Buijink (our discussant),Kevin Chen,Ole-Kristian Hope,William Rees and other participants at the Illinois Accounting Symposium 2006,an anonymous referee,and Christian Leuz for their valuable comments.⁎Corresponding author.E-mail address:Edward.lee@ (E.Lee).0020-7063/$30.00©2007University of Illinois.All rights reserved.doi:10.1016/j.intacc.2007.09.007342H.B.Christensen et al./The International Journal of Accounting42(2007)341–3791.IntroductionThe mandatory adoption of IFRS1in the European Union(EU)is one of the largest regulatory experiments in financial reporting ever undertaken,and may eventually prove to be a vital step towards global GAAP harmonization.2The EU and European Economic Area(EEA)include30countries with integrated financial markets and more than7000 listed firms.Almost all EU/EEA listed firms are legally required to adopt IFRS in their consolidated statements no later than2005.3In this paper,we examine the economic consequences of mandatory IFRS adoption for United Kingdom(UK)listed firms.We study both the short-term price response to news about IFRS adoption,and the changes in the implied cost of equity for a large sample of firms between a date before the mandatory adoption was expected and a date by which mandatory adoption was effectively certain.The short-run share-price response and long-run implied cost of equity methods complement each other when testing the effect of mandatory IFRS adoption.The potential advantage of focusing on short-run abnormal returns is that we are able to isolate specific days when news affects all firms in the sample.The disadvantage is that it is reliant on precise identification of the event days.In particular it assumes that there has been no leakage of the policy deliberations to the market.Unfortunately the dates on which the probability of mandatory adoption of IFRS changed are debatable.In contrast,an advantage of using the implied cost of equity method is that it is not sensitive to the identification of specific dates—we simply exclude the period of uncertainty and test the difference between the implied cost of equity before and after the announcement period.However,the estimation of the implied cost of equity is also potentially problematic,because it is often difficult to control for all factors affecting the implied cost of equity over a long period of time.Thus we view the two methodologies as being complementary and we believe that their joint use should increase the robustness of our conclusions.We hypothesize that UK firms vary in their willingness to adopt IFRS,because the costs and benefits of IFRS adoption are likely to vary across firms.In terms of the literature on accounting choice,the decision to mandate IFRS for UK quoted firms was unusual in the sense that it cannot be simply portrayed as the imposition of a restriction on the accounting choices of UK firms.Prior to2005UK firms were not permitted to adopt IFRS for UK financial-reporting purposes.After2005,UK firms are not allowed to use pre-2005UK GAAP in their consolidated statements for financial reporting purposes.Thus the EU decision changed the choice set for UK firms by mandating a new set of rules for financial 1International Financial Reporting Standards(IFRS)is the name of accounting standards produced by the International Accounting Standards Board(IASB).2The EU's motive for adopting the regulation is the creation of a more transparent and efficient capital market that will facilitate a lower cost of capital for EU firms(EC16/06/2002).3EC16/06/2002requires all listed firms in a regulated market to comply with IFRS in their consolidated statements no later than2005unless they are listed in non-member state and have been using internationally accepted standards prior to September2002.Member countries can allow adoption to be postponed until2007for firms that comply with US-GAAP.The UK has decided not to use this option and all listed firms in a regulated market are,therefore,required to comply with IFRS from2005.reporting that some UK firms might have adopted voluntarily,if they had been given the choice.If UK firms had been given a choice between UK GAAP and IFRS it is logically possible that some would have chosen not to adopt IFRS,and some would have chosen to abandon UK GAAP in favor of IFRS.Thus it is possible that some UK firms would have been constrained by the EU's decision,while others would have been liberated.For the purposes of this paper we need a counter-factual proxy for what choices UK firms would have made,if they had been given an option to choose between UK GAAP and IFRS.One possibility,which we explore in this paper,is to exploit the information in the choices made by firms in an economy similar to the UK,but where firms had the choice to adopt IFRS before 2005.In particular Germany is a major EU economy that allowed early adoption of IFRS and that also experienced extensive early adoption.This combination of Germany and the UK as two major EU economies,but with very different IFRS adoption processes,produces a unique setting for testing the factors affecting the economic consequences of mandatory IFRS adoption.We hypothesize that the characteristics of voluntary/early adopters of IFRS or US-GAAP 4in an EU jurisdiction that allowed voluntary adoption of international accounting standards (IFRS or US-GAAP)might serve as a viable proxy for how UK firms might have behaved given the same choice.In particular we focus on the choices made by German firms.5In Germany,listed firms have had the option to choose between an international accounting regime (IFRS or US-GAAP)and domestic standards for their consolidated statements since 1998.6Economic theory predicts that firms committing to an international accounting regime are those that perceive the greatest net-benefit.We measure the degree of similarity to German voluntary adopters by estimating a logistic choice-model using German data and calculating the probability of voluntary adoption in the UK based on this model.We use the estimated probability of voluntary adoption from our model based on German firms as a counter-factual proxy for the probability of voluntary adoption by UK firms.The advantage of this approach is that it focuses on actual observed choices,there is no potential for response bias,and it is based on a large population of firms.The disadvantage of this approach is that the German GAAP and financial disclosure regime is not the same as UK GAAP.The choice between UK GAAP and IFRS for UK firms is not the same as the choice between German GAAP and IFRS for German firms.For example,German IFRS adopters will typically experience a greater leap in disclosure quality.Due to these differences one might expect two sets of determinants for firms'willingness to switch to IFRS,i.e.,one set that is common across both countries and another set that is country-4For brevity we describe German firms that comply with either IFRS or US-GAAP in 2002as voluntary adopters in this paper.5An alternative approach might be to ask firms directly what they might have done if they had been given a choice.However this approach is also problematic for the following reasons:1)firms may not know what they would have done given the choice,2)many firms may be unwilling to respond to the survey (typical response rates are 20–30%),3)some firms may not tell the truth.6In April 1998KapAEG was adopted in Germany allowing listed firms the option only to comply with either IFRS or US-GAAP in there consolidated statements.343H.B.Christensen et al./The International Journal of Accounting 42(2007)341–379344H.B.Christensen et al./The International Journal of Accounting42(2007)341–379 specific.For instance,factors that correlate with corporate governance may be less transferable from Germany to the UK.Convincing outside investors that the firm is committed to improved corporate governance may be an underlying motive that is more important to firms in Germany due to the ownership and legal system they operate in.The implications of this fact for our research design is that we run the risk of identifying some determinants from the German adopters that are not necessarily relevant to the UK firms, which would add noise and reduce the power of the tests based on the UK sample.Thus our analysis reports two sets of results for the UK.One set assumes that the choice model for the UK is the same as for Germany.The other set attempts to isolate the Germany-specific choice drivers from the common drivers.We find that the common-driver set produces consistent results both for implied cost of capital changes and for the short-run market responses.In both cases we find a significant positive cross-sectional association between the economic response to mandatory IFRS adoption and our counter-factual proxy for the probability of voluntary adoption by UK firms.The study makes two main contributions.First,understanding that the costs and benefits of IFRS adoption varies systematically across firms is important not only to countries that have already decided to make IFRS mandatory,but also to countries that are currently considering taking this step.7Second,the study also makes a novel methodological contribution,by showing that under certain circumstances the information contained in voluntary GAAP choices in one economy can predict the economic responses to a mandatory GAAP change in a similar economy.The remainder of the paper is organized as follows.Section2reviews the literature in the area and Section3develops the testable hypotheses of the paper.Section4describes the methodology and sample including the key dates that changed the likelihood of mandatory IFRS in the EU and the calculation of the counter-factual proxy for voluntary adoption in the UK.Section5presents the results and discusses the implications.Section6summarizes the paper.2.Literature review2.1.Voluntary adoptionUntil recently,empirical studies on the connection between GAAP changes and the cost of capital have focused on voluntary adoption of either IFRS or US-GAAP over domestic standards.The assumption is that the accounting regime affects the quality of information and that the quality of information in turn affects the cost of capital.One stream of research examines proxies for the cost of capital either within an event study around the adoption of IFRS or US-GAAP,or cross-sectionally between firms that have adopted IFRS or US-GAAP and firms that use local-GAAP.Leuz and Verrecchia (2000)and Leuz(2003)take this approach by examining bid/ask-spreads,trading volume7According to GAAP convergence(2002)over90%of the59countries surveyed intend to convert national standards to IFRS.and share price volatility as proxies for the information asymmetry component of the cost of capital.They find reduced information asymmetry when firms change from German GAAP (HGB)to either IFRS or US-GAAP,but no significant difference between IFRS and US-GAAP.Contrary to this conclusion,Daske (2006)finds no evidence of a reduced cost of capital when using both the residual-income valuation model and the Ohlson and Juettner-Nauroth (2005)abnormal earnings growth model to estimate the implied cost of equity.These three studies limit their sample to German firms,thus keeping the institutional settings constant.Cuijpers and Buijink (2005)use a European sample to test the affect of changing from local-GAAP to either IFRS or US-GAAP.They examine information asymmetry proxied by analyst following,forecast dispersion and stock return volatility and the implied cost of capital estimated using the method suggested by Easton,Taylor,Shroff,and Sougiannis (2002).They document a positive effect of adopting IFRS or US-GAAP on analyst following,but fail to find support for a lower implied cost of equity.Dargenidou,McLeay,and Raonic (2006)also use a European sample to test how the change from local GAAP to international accounting standards (IFRS or US-GAAP)affected the estimated cost of capital using the Ohlson and Juettner-Nauroth (2005)abnormal earnings growth model.Contrary to Daske (2006)and Cuijpers and Buijink (2005)they find that the cost of capital increased by more than 4%after voluntary adoption but that the effect is smaller for large firms.Daske,Hail,Leuz,and Verdi (2007)extend these studies by focussing on whether the impact varies with the degree of compliance.Survey evidence documents that compliance varies considerably among voluntary adopters (Cairns,1999,2000).Daske et al.(2007)show that the cost of capital is only reduced when adoption is serious (i.e.,leads to improved accounting quality).The heterogeneity that they document in the voluntary setting arises from differences in compliance level.The heterogeneity that we explore in the mandatory setting arises because the willingness to adopt varies across firms.To summarize,prior research that uses proxies for either the cost of capital or components of the cost of capital have produced mixed results.Another stream of research looks at the market reaction to the announcement of future compliance with IFRS or US-GAAP.The idea is that the market reaction around the announcement contains the change in the required risk premium,and thus impounds the change in the cost of capital.Pellens and Tomaszewski (1999)find insignificant market reactions to the announcement of future compliance with either IFRS or US-GAAP in Germany.The statistical power of their test is,however,low due to a sample size of only 16firms.Karamanou and Nishiotis (2005)use an international sample of 54firms adopting IFRS and show that firms experience abnormal positive returns around the announcement of future compliance with IFRS.They also find evidence that the positive market reaction is not identical among firms with different characteristics.Thus,firms with low valuations and high growth opportunities experience a stronger market reaction.Karamanou and Nishiotis suggest that firms use the adoption of IFRS to signal to the market that they are undervalued.This signalling motive does not apply to the mandatory-adoption setting as in the case of the UK.Indeed,the study of mandatory adoption differs from voluntary adoption in two ways.First,mandatory adoption eliminates the self-selection issues inherent in voluntary adoption.Second,the choice to voluntarily adopt is a signal that includes information in itself,which could be difficult to disentangle from the underlying issue a study seeks to examine.345H.B.Christensen et al./The International Journal of Accounting 42(2007)341–379346H.B.Christensen et al./The International Journal of Accounting42(2007)341–3792.2.Mandatory adoptionThree prior studies examine mandatory rather that voluntary adoption of IFRS. Comprix,Muller and Stanford-Harris(2003)examine abnormal returns around the dates of public announcements that increase the likelihood of mandatory IFRS in the EU.They apply the Sefcik and Thompson(1986)approach to evaluate the relationship between announcement returns and a number of firm and country characteristics.They find that firms that are a)audited by a big5auditor,b)located in countries that will experience the greatest increase in quality of financial information as a consequence of IFRS,and c)are subject to the highest level of legal enforcement experience significant positive returns.Apart from the nature of the auditor these characteristics are all country specific.Although the methodology of Comprix et al.(2003)is similar to the market-reaction test we conduct in our study,the underlying research question is different. While they predominantly examine differences among country characteristics we investigate the role of firm characteristics within one country,which keeps the institutional framework constant.Armstrong,Barth,Jagolinzer,and Riedl(2006)also investigate market reactions to events that they argue would affect the likelihood of mandatory IFRS in the EU. Unlike Comprix et al.(2003),which studies the events from2000to2002,they analyze later events between2003and2004that are related to the endorsement of the IFRS standards in general and IAS32/39in particular.In general,they find positive(negative)market reactions to events they classify as increasing(decreasing) the likelihood of mandatory IFRS and interpret this as evidence that investors perceive benefits of harmonized accounting standards under IFRS.The focus of Armstrong et al.(2006)is on whether mandatory IFRS is good or bad as perceived by investors.In our study,the focus is instead on the differences in the economic consequences of mandatory IFRS between firms that are likely to incur relative benefits and costs due to the decision.Differences in economic consequences are of particular interest when evaluating a mandatory policy change.Since all firms by definition are treated equally by such a policy,those that are disadvantaged by the policy are still forced to comply.Instead of examining the short-term market reactions,Pae,Thornton,and Welker (2006)investigate the consequences of mandatory IFRS by looking at Tobin's Q.They show that firms with high agency cost measured by concentration of control and excess of the largest shareholder's voting rights over cash flow rights experience relative increases in valuation as a consequence of mandatory IFRS.The underlying idea in the study is that the shares of some firms trade at a discount due to weaker protection for minority shareholders and that mandatory IFRS force these firms to improve their disclosure,which in turn reduces the discount.Pae et al.(2006)use a European sample where early adoption is allowed in several countries and national disclosure quality generally is lower than IFRS.In this setting it makes sense to test whether the restrictions imposed by mandatory adoption of IFRS have benefited some investors. Contrary to this we restrict our test to a UK setting where firms have not had the option to comply with IFRS voluntarily.Furthermore,the disclosure quality in our UK setting is generally high and it is unsure whether IFRS is an improvement for all firms.Oursample is more relevant for an investigation into whether or not relative benefits differ across firms than whether or not it enhances protection of minority investors.The key contribution of our study to the literature is the focus on firm-specific cross-sectional differences in the economic consequences of mandatory IFRS.We define the firm-specific differences through a counter-factual proxy for willingness to adopt.The idea is that heterogeneity in the economic consequences of mandatory IFRS arises because some firms are forced to comply against their will,while others have net benefits and would have complied voluntarily had they been given the opportunity.We are not aware of any prior studies that connect the voluntary accounting GAAP commitment of firms in one country to the economic consequences of a mandatory policy in another country.3.Hypotheses developmentThe starting point of our analysis is the assumption that the costs and benefits of IFRS adoption,relative to firm value,will vary across firms.The mandatory adoption of IFRS imposes two kinds of changes on the financial-reporting practices of firms.First,firms are required to adopt a new set of accounting-measurement rules that in some cases will have a material effect on a firm's reported earnings and balance-sheet values,and in other cases will not.Second,IFRS introduces a new set of required disclosures that in some cases will be greater than the original disclosure requirements and in other cases less.Empirical research suggests that the cost of capital is related to both disclosure and measurement policies.Examples of such studies are Botosan (1997),that examines the association between disclosure levels and the implied cost of equity,and Francis,LaFond,Olsson,and Schipper (2004),that examines the relationship between earnings attributes and the implied cost of equity.Both studies find that a lower quality of information is associated with a higher cost of capital.The main hypothesis of this paper is (stated in alternative form):H 1.The cross-sectional variations in the economic consequences of mandatory IFRS adoption by UK firms are related to the probability that the firm would have adopted IFRS voluntarily if it had been given the choice.In order to convert H 1into an empirically testable proposition we need to identify specific,measurable,economic consequences,and we need to specify how to model the probability of (counter-factual)voluntary adoption by UK firms.For the purposes of this paper we focus on two,potentially related,types of economic consequences.First we consider the market response to news about the decision by the EU to mandate IFRS.Second we consider the relative change in implied cost of equity between the time when the EU started to consider IFRS adoption and the time when the decision to adopt IFRS was effectively final and binding on all member states.The main hypothesis is divided into two testable hypotheses (stated in alternative form):H 1A.The stock price reaction of UK firms to announcements that increased (decreased)the likelihood of mandatory IFRS adoption is positively (negatively)related to their degree of similarity to the characteristics of German voluntary IFRS adopters.347H.B.Christensen et al./The International Journal of Accounting 42(2007)341–379348H.B.Christensen et al./The International Journal of Accounting42(2007)341–379H1B.The change in the implied cost of equity of UK firms before and after the mandatory IFRS adoption decision is negatively related to their degree of similarity to characteristics of German voluntary IFRS adopters.Both hypotheses exploit the fact that an informationally efficient market should rapidly incorporate the expected costs and benefits of IFRS adoption into share prices.That is to say,that if the market expects UK firms with characteristics similar to German early adopters to derive a relative benefit from IFRS adoption over other firms then such firms should experience a reduction in their relative cost of capital after future mandatory IFRS adoption became known,and a relatively positive(negative)response to news indicating that mandatory IFRS adoption was more(less)likely.Hypothesis H1A tests how the market initially received the news of mandatory IFRS adoption.Hypothesis H1B tests how the market perceives mandatory IFRS adoption in the longer run.Consistent results for H1A and H1B should increase the robustness of the conclusion with regard to the main hypothesis.In thinking about these hypotheses it is important to recognize that our focus is on the possibility that some firms may benefit more than others from the implementation of IFRS. In particular we do not deny the possibility that the value of IFRS adoption could be relatively greater in Germany than in the UK.Indeed,while there does seem to be a common perception that IFRS could be beneficial for German firms(Leuz and Verrecchia, 2000),the general perception of IFRS seems less favourable for UK firms.Studies such as Ginger and Rees(2001)show that UK-GAAP and IFRS are generally assumed to be very close.Some practitioners hold the belief that UK GAAP is of higher quality than IFRS.8 However,despite such perceptions recent empirical evidence has found that the investment decisions of fund managers in the UK have been affected by the transition to IFRS.9 Furthermore,we are not concerned in this paper with testing the overall effect of mandatory IFRS adoption on the cost of capital of UK firms.It could be that the median level of accounting information quality decreases in the UK due to IFRS being of a lower quality than UK accounting standards,but at the same time the effect of IFRS adoption could be smaller for UK firms similar in characteristics to German volunteer adopters.In this case our main alternative hypothesis would be accepted in the UK even though the overall affect of introducing IFRS was to decrease the quality of financial statements and increase the cost of capital.Another issue we face in relation to the changes to measurement and disclosure policies due to IFRS is the differences between Germany and the UK.Economic intuition suggest that a firms'accounting policy choice is driven by it's perception of net benefits.If the perceived net-benefits are at least partly determined by a function of measurement and disclosure issues then it is unlikely to be identical for Germany and the UK due to their institutional differences.Ball(2006)and Nobes(2006)both analyse how differences in 8See Accountancy,January1999,p.6,and Accountancy,May1999,p.77,for examples.9In a PwC/MORI(2005)survey of fund managers,70%said that they found the first IFRS information fairly useful or very useful,29%reported that the disclosure had influenced them to disinvest from a company,and21% said that they had been influenced to not invest in a company and13%had been influenced to invest.financing,ownership,legal,and taxation systems across countries influence the development of their domestic accounting regulations and suggest that this is likely to have effects on the implementation of IFRS.Thus,to the extent that these institutional differences affect the decision of IFRS adoption,there will be country-specific factors in Germany that are not transferable to the UK context and therefore induce noise into our counter-factual proxy for a UK firm's willingness to adopt IFRS.That is to say,our research design potentially underestimates the differences in economic consequences and therefore we run the risk of failing to reject that no differences exist when differences actually exist.Thus this issue,in effect,loads the dice in favor of our null hypothesis.The fact that we are able to reject the null,in spite of this issue,suggests that even stronger results in support of our alternative hypotheses could be found if a more powerful counter-factual proxy could be designed than the one we use here.4.Methodology and sample4.1.Development of the counter-factual proxyIn this section we explain the development of the counter-factual proxy for UK firms'willingness to adopt IFRS based on their degree of characteristics similar to German voluntary IFRS adopters.We use the observed voluntary GAAP choices of German firms to predict which UK firms would be more likely to adopt IFRS given the same choice.The following logistic regression models are used to explain the choice of German firms:Adopter i ¼a 0þa 1FS i þa 2DTM i þa 3LMV i þe ið1ÞAdopter i ¼b 0þb 1FS i þb 2DTM i þb 3LMV i þX 10k ¼4b k INDDUM k ;i þe i ð2ÞAdopter i ¼g 0þX7k ¼1g k INDDUM k ;i þe ið3ÞThe dependent variable (Adopter)is assigned the value of one if firm i complies with an international accounting regime in 2002and the value of zero otherwise.10FS is the foreign sales divided by total sales,DTM is the long-term debt divided by the sum of its long-term debt and market value,LMV is the natural logarithm of the market value,and INDDUM are seven industry dummies set equal to one for the industry for which the firm belongs and zero otherwise.Model 1(Eq.(1))only includes the three firm-characteristic variables that measures foreign sales,leverage,and size.To capture the long-run norm,we 10We do not distinguish between IFRS and US-GAAP.The reason is that we are interested in firms that have net-benefit of committing to an international accounting regime regardless which one.We do,however,re-run the models excluding firms complying with US-GAAP.The results are consistent in all material aspects,which is also consistent with the result of Leuz (2003).349H.B.Christensen et al./The International Journal of Accounting 42(2007)341–379。

国际会计_第3章-2英国

3.2.1 通过《公司法》管理公司事务,包 括对公司财务会计和报告的要求

通过《公司法》对会计行为进行规范 ,是 英国会计模式区别于美国会计模式的最主 要特征。

《公司法》是全国性的法律,目前执行的 是2006年全面修订的《公司法》。 英国也像大多数欧洲国家一样,主要通过 法律规范来约束企业的会计行为。

英国传统文化的不强求统一和一致性也使得英 国会计实务处理具有可选择性,而不是生搬硬 套某些法律条文。 不列颠民族虽然某些方面相对美利坚民族比较 保守,但较之与东方民族他们更具有冒险精神 和乐观主义态度,表现在会计处理上,英国人 更侧重于激进的方法,而不是采取稳健主义原 则,比如对存货的处理,不同批次购进的存货 项目,税法和会计准则允许采用先进先出法确 定成本,但不允许后进先出法。

英国与爱尔兰共和国于1973年加入欧洲经济共同体, 此后,英国公司法的修订,就反映出与欧洲经济共同 体理事会指令的协调趋向。

3.2.1 通过《公司法》管理公司事务,包括对 公司财务会计和报告的要求

2、1981年修订的《公司法》

规定了资产负债表和损益表的格式,提出了与欧共体第4号指令提 出的十分类似的5项会计原则(1)持续经营假设;(2)一致性; (3)谨慎;(4)应用权责发生制;(5)分开确定任何总数的组 成部分

英国的文化因素

英国崇尚民主、自由、博爱、平等的价值观,倡导自 由灵活和个人主义。相对于集体主义倾向的国家来说, 英国会计理论和会计准则由会计职业团体阐释和发布, 政府控制很宽松,基本上不予干预。 比如对固定资产计量,英国会计有较大弹性。会计准 则建议企业至少每 5年对固定资产进行一次重新估价 并重新核定经济使用年限;重估增值列为业主权益, 不能作为当年收益;重估减值先从该项资产以前列为 业主权益的重估增值账户中抵补,不足部分再计入当 年损益。很多会计准则对会计实务的指导只是建议性 的意见,并不一定强制执行,这就为会计职业团体和 职业会计师执业提供了依据个人职业判断的充分空间。

英国会计实习报告总结

一、前言随着我国经济的快速发展,会计行业在全球范围内的影响力日益增强。

为了拓宽视野,提升自己的专业技能,我选择了在英国某知名会计师事务所进行为期三个月的实习。

在这三个月的时间里,我不仅深入了解了英国会计行业的运作模式,还积累了丰富的实践经验。

以下是我在实习过程中的总结与感悟。

二、实习单位及岗位实习单位:英国某知名会计师事务所实习岗位:财务实习生三、实习内容1. 参与公司日常财务工作在实习期间,我主要负责协助会计师处理日常财务工作,包括但不限于:(1)整理和归档财务凭证;(2)核对财务报表;(3)协助编制月度、季度、年度财务报表;(4)参与税务申报及筹划。

2. 参与审计项目在实习期间,我参与了多个审计项目,包括但不限于:(1)了解客户行业特点、经营状况及财务状况;(2)协助会计师收集、整理审计证据;(3)参与编制审计工作底稿;(4)协助会计师与客户沟通,解答客户疑问。

3. 参与内部培训实习期间,我还参加了会计师事务所举办的内部培训,包括会计准则、审计方法、税务筹划等方面的培训,提升了自己的专业素养。

四、实习收获1. 熟悉英国会计行业运作模式通过实习,我对英国会计行业的运作模式有了深入了解,包括会计准则、审计准则、税务筹划等方面。

这为我今后的职业发展奠定了基础。

2. 提升专业技能在实习过程中,我熟练掌握了财务软件的使用,如SAP、Oracle等;掌握了财务报表编制、审计工作底稿编制等技能;提高了自己的英语水平。

3. 培养团队合作精神在实习期间,我学会了与不同背景、不同文化的人合作,培养了良好的沟通能力和团队协作精神。

4. 增强抗压能力在实习过程中,我遇到了许多困难和挑战,如语言障碍、工作压力等。

通过努力克服,我增强了抗压能力,学会了如何在压力下保持冷静、高效地完成任务。

五、实习感悟1. 实习让我认识到,理论知识与实际操作相结合的重要性。

在实习过程中,我将所学知识运用到实际工作中,提高了自己的实践能力。

英国财报格式

英国财报格式一、引言财务报表是企业向外界传递其经济活动和财务状况的主要手段。

在全球范围内,各个国家或地区都有其特定的财报格式和会计准则。

本文将重点探讨英国的财报格式,分析其特点、具体内容以及与其他国家或地区的异同。

二、英国财报格式的特点英国的财报格式具有以下特点:1.遵循国际会计准则(IFRS):自2005年起,英国开始采用国际财务报告准则(IFRS),使得英国的财报格式更加国际化和标准化。

这也有助于投资者更好地理解和比较不同国家或地区的公司财务状况。

2.强调真实与公允原则:英国的财报格式强调提供真实、公允的财务信息,以帮助投资者做出明智的决策。

这意味着在编制财报时,公司需要充分披露所有重要信息,避免误导性陈述或遗漏。

3.结构化逻辑:英国的财报格式具有清晰的逻辑结构,主要包括财务报表、附注、管理层讨论与分析等部分。

这种结构有助于投资者快速获取关键信息,并对公司的财务状况有全面的了解。

4.详尽的附注和说明:英国的财报格式强调附注和说明的重要性,要求企业提供足够的信息以解释其财务数据。

这有助于增加财报的可读性和可理解性,降低信息不对称。

三、英国财报格式的具体内容英国的财报格式主要包括以下内容:1.财务报表:主要包括资产负债表、利润表和现金流量表。

这些报表反映了公司的财务状况、经营成果和现金流量。

2.附注:附注是对财务报表中列示的数字进行的详细解释和说明。

附注可能包含会计政策、计量基础、报表项目明细等重要信息。

此外,还包括管理层讨论与分析,这是对企业的财务状况和经营成果进行的详细讨论和分析,有助于投资者了解公司的未来前景和战略规划。

3.其他重要信息:除了财务报表和附注外,英国的财报格式还包括其他重要信息,如公司治理报告、合规声明、社会责任报告等。

这些信息有助于投资者了解公司的治理结构、合规情况和社会责任等方面的信息。

四、结论通过上述分析可知,英国的财报格式具有鲜明的特点,强调真实与公允原则、结构化逻辑和详尽的附注和说明等,以确保财务报告的透明度和可理解性。

比较国际会计研究———英国会计

比较国际会计研究——英国会计关于《比较国际会计研究-------- 英国会计》,是我们特意为大家整理的,希望对大家有所帮助。

一、英国格鲁•萨克逊会计体系。

盎格鲁•萨克逊会计体系可以明确地与大陆欧洲、拉丁美洲、亚洲以及世界上其他国家或地区的会计区分开来。

它不仅在英美推行,而且了相当一部分国家和地区的会计制度和实务。

与其他国家集群会计相比,盎格鲁・萨克逊会计信息披露的透明度较高。

英国是第一个建立意义上会计职业团体的国家,在会计中具有悠久的传统。

鉴于殖民时期的广泛的商业贸易,英国的会计通过英联邦及其范例,对世界各国早期的会计实务有着深刻的影响。

尽管随着大英帝国的衰落以及国际间剧烈的竞争,英国正面临新的挑战,但无可否认,英国有着丰富的会计思想。

1973年,英国加入了欧洲共同体(Eureopean Community, 1993 年改称欧盟European Union )o 作为欧盟的成员国,必须遵守相应的法规。

例如欧盟发布的第4、7、8号指令都是有关会计审计协调的专题规定。

无疑地,欧盟在成员国会计协调上的积极举措将影响英国会计未来的发展方向,使其逐渐向大陆欧洲模式靠拢;同样,英国会计对欧洲其他国家的影响也会有所增加。

(一)会计的规范与监管英国会计的立法依据主要是公司法。

公司法的基本原则是适用于在管辖区内组建的所有股份有限公司。

1948年颁布的公司法为英国会计模式奠定了重要的基础。

它不但规定了公司(包括公开招股和不公开招股)必须公布资产负债表和损益表,而且第一次提出了关于财务报表和会计信息披露的指导思想一一真实与公允的观点。

其后英国一直强调全部帐目应按“真实与公允〃的观点予以提供。

但"真实与公允〃在英国并无官方的确切定义。

一般认为, 〃真实与公允〃是指以诚实的态度披露所有真实的、可信的重要信息,不抱偏见,不隐瞒或忽略重大事实;必要时可超出规定要求披露有关细节。

自1948年公司法颁布以来,英国立法经历了几次修订和补充,除1948年文本外,2967、2976、2980、1981 年(实施欧盟第4号指令)历次修订的文本都作为单独的立法存在,公司在执行或引用时,必须相互参照才能决定取舍,很不方便。

最新英国会计模式综述

1国际会计结课论文2345英国会计模式综述678910111213班级:经1105-3班14姓名:随宇宇15学号: 201114451617181920212223中文摘要:英国作为近代工业革命和现代会计的发源地,是会计理论与实务24最发达的国家之一。

著名的真实与公允观念就起源于英国,其会计理论和实务25经验在国际会计界具有重要的影响。

26关键字:《公司法》真实与公允社会经管责任现行成本会计会计职业界27英国是第一个建立现代意义上会计职业团体的国家,在会计的发展中具有悠28久的历史传统,有着丰富的会计思想。

其会计实物体系在英联邦国家有广泛的29影响,对世界各国早期的会计实务也有着深刻的影响,被称为英国(不列颠)30会计模式。

在历史上,英国的会计曾对美国会计的发展有过重大的影响,而美国会计的3132发展在20世纪60年代又推动了英国的会计发展,因此,英国会计模式与美国33会计模式颇有类似之处。

嗣后,英国会计模式又在欧洲经济共同体(现欧洲联34盟)的努力下处于与欧洲大陆国家的会计模式相互协调的过程中。

35以下概述英国会计模式的基本特征。

36一、通过《公司法》管理公司事务,包括对公司财务会计和报告的要求这是英国会计模式区别于美国会计模式的最主要特征。

公司法是全国性的法3738律,目前执行的是2006年全面修订的《公司法》。

1948年颁布的《公司法》为39英国会计模式奠定了基础。

该法规定,所有注册的公司,不论是股份公开发行的还是不公开发行的,都要公布它们的损益表和资产负债表,因此英国公司法4041的基本原则适用于在管辖区内组建的所有股份有限公司(包括公开招股和不公42开招股)。

它还首次提出了“真实和公允”观点,这一观点成为英国《公司法》对公司财务会计和报告要求的指导思想。

4344英国(联合王国)与爱尔兰共和国在1973年1月1日加入欧洲经济共同体,自45此以后,英国公司法的修订,就反映出与欧洲经济共同体理事会指令的协调趋46向。

国际比较会计英国

一·公司法对会计行为的规范

3.关于损益表。公司法规定: (1)格式。可以从三种格式中选择,即横式或竖式的或两种都采用, 项目的分类可以按费用的性质分,也可以按其职能分。(在美国,损 益表的格式一般是竖式的,费用项目系按职能分类) (2)提供的信息。公司法要求企业必须提供下列有关信息: 营业额,其中年营业额超过一百万英镑的公司还应提供营业额的计算 过程;租金收入或投资收入;董事报酬,包括以前任董事的养老金和 给董事的补偿金,以及年报酬为五干英镑的董事人数(董事年报酬不 超过四万英镑的不须遵守这一要求);董事长报酬;应计利息;折旧 费用包括折旧的计算方法等;其它费用包括审计费用;纳税信息(分 别按联合王国公司税,联合王国所得税和海外税类单独反映);股利 总额(包括未分配股利);非常交易事项收支。会计政策的变动情况。

案通过,除92名留任外,600多名世袭贵族失去上院议员资格,非政

治任命的上院议员将由专门的皇家委员会推荐。下院也叫平民院,议

员由普选产生,采取最多票当选的小选区选举制度,任期5年。但政

府可决定提前大选。政府实行内阁制,由女王任命在议会选举中获多

数席位的政党领袖出任首相并组阁,向议会负责。

政党

(1)工党(Labour Party):执政党。2001年6月大选后蝉联执政。工党近年来更多倾向于中产 阶级的利益,与工会关系有所疏远。布莱尔当选工党领袖后,政治上提出“新工党、新英国”的口 号,取消党章中有关公有制的第四条款,经济上主张减少政府干预,严格控制公共开支,保持宏观 经济稳定增长,建立现代福利制度。对外主张积极参与国际合作,对欧洲一体化持积极态度,主张 加入欧元,主张同美国保持特殊关系。现有党员近40万名,是英国第一大党。

英国公司财务报告分析(3篇)

第1篇摘要:本文旨在对英国某知名公司的财务报告进行深入分析,通过对其财务报表的解读,评估公司的财务状况、盈利能力、偿债能力、运营效率和未来发展潜力。

分析过程中,我们将结合财务比率、现金流量分析等方法,对公司的财务健康状况进行综合评价。

一、公司简介(以下以某知名英国公司为例)某知名英国公司成立于XX年,主要从事XX行业,业务遍布全球。

公司致力于为客户提供高品质的产品和服务,在行业内享有较高的声誉。

近年来,公司业绩稳步增长,市场份额不断扩大。

二、财务报表分析1. 资产负债表分析(1)资产结构分析根据公司资产负债表,我们可以看到,公司资产主要由流动资产、非流动资产和无形资产构成。

流动资产主要包括现金、应收账款和存货等,非流动资产主要包括固定资产、无形资产和长期投资等。

从资产结构来看,公司流动资产占总资产的比例较高,说明公司具有较强的短期偿债能力。

同时,公司非流动资产占比也相对较高,表明公司具有较强的长期发展潜力。

(2)负债结构分析公司负债主要由流动负债和非流动负债构成。

流动负债主要包括短期借款、应付账款和预收账款等,非流动负债主要包括长期借款、应付债券和长期应付款等。

从负债结构来看,公司流动负债占比相对较高,说明公司在短期内需要支付一定的债务。

但考虑到公司流动资产充足,短期内偿债压力不大。

2. 利润表分析(1)收入分析公司收入主要来源于主营业务收入和其他业务收入。

近年来,公司主营业务收入稳步增长,表明公司在行业内具有较强的竞争力。

(2)成本分析公司成本主要包括主营业务成本、销售费用、管理费用和财务费用等。

从成本结构来看,公司主营业务成本占比较高,但近年来成本控制能力有所提高。

(3)盈利能力分析通过计算毛利率、净利率等指标,我们可以看出公司盈利能力较强。

近年来,公司净利润逐年增长,表明公司具有较强的盈利能力。

3. 现金流量表分析(1)经营活动现金流量分析公司经营活动现金流量主要来源于主营业务收入和投资收益。

英国财务报告分析模板(3篇)

第1篇一、引言财务报告是企业对外展示其财务状况、经营成果和现金流量的重要工具。

通过对英国企业的财务报告进行分析,可以帮助投资者、债权人、监管机构等利益相关者了解企业的经营状况和财务风险。

以下是一份针对英国企业财务报告的分析模板,旨在帮助分析者全面、系统地评估企业的财务状况。

二、分析框架1. 基本财务指标分析2. 营业收入分析3. 成本费用分析4. 资产负债分析5. 现金流量分析6. 盈利能力分析7. 偿债能力分析8. 发展能力分析9. 行业对比分析10. 总结与建议三、基本财务指标分析1. 毛利率2. 净利率3. 资产回报率4. 股东权益回报率5. 流动比率6. 速动比率7. 负债比率8. 股东权益比率分析目的:通过分析这些指标,评估企业的盈利能力、偿债能力和发展能力。

四、营业收入分析1. 营业收入增长率2. 主营业务收入占比3. 地区分布4. 行业分布分析目的:了解企业的收入来源、增长速度以及市场分布情况。

五、成本费用分析1. 销售费用率2. 管理费用率3. 财务费用率4. 成本费用控制能力分析目的:分析企业的成本费用构成,评估其成本控制能力。

六、资产负债分析1. 总资产增长率2. 总负债增长率3. 资产结构4. 负债结构分析目的:了解企业的资产和负债状况,评估其财务风险。

七、现金流量分析1. 经营活动现金流量净额2. 投资活动现金流量净额3. 筹资活动现金流量净额4. 现金流量比率分析目的:评估企业的现金流量状况,了解其偿债能力和支付能力。

八、盈利能力分析1. 净利润增长率2. 毛利率3. 净利率4. 营业利润率5. 股东权益回报率分析目的:分析企业的盈利能力,评估其盈利质量。

九、偿债能力分析1. 流动比率2. 速动比率3. 负债比率4. 股东权益比率分析目的:评估企业的偿债能力,了解其财务风险。

十、发展能力分析1. 总资产增长率2. 营业收入增长率3. 净利润增长率4. 研发投入占比分析目的:评估企业的发展能力,了解其成长潜力。

国际会计---英国会计

英国会计环境及其特征研究摘要:英国是创造“真实与公允反映〞概念的国家,目前这一概念已被欧盟国家正式承受,而且也对世界上许多其他国家产生了重要的影响。

英国在会计审计领域中作出了许多开创性奉献,奠定了形成广泛且长久的英国会计模式的根底。

英国会计模是以英国会计理论和实务为代表的、以要求公司财务报表给予“真实与公允反映〞为特征的一种国际会计模式。

英国会计模式是世界上产生较早、你是较久的一个模式。

英国工业革命以后,随着生产力的提高、生产规模的扩大,产生了许多不同以往的会计问题,在解决这些会计问题的过程中,英国会计师创造了许多新的会计理论、方法、技术和制度,从而逐渐传播到了其他许多国家,尤其是英联邦国家。

英国现代会计和审计的开展都曾经作出过重大的奉献。

英国是现代会计的发祥地,由于其在政治经济上的特殊地位,无论是在历史上还是现代,英国的会计理论和实务在世界X围内都具有重大的影响,其影响力不仅限于英联邦的40多个国家,而且扩展到英联邦以外的许多国家。

构成英国会计环境的两大组成局部是法律约束和行业自律。

法律约束主要是官方通过立法的形式,将政府的有关政策主X法制化,从而使会计活动在发来的框架内有序进展;行业自律这是通过会计职业界自我约束的各种方式对会计实务和会计职业界本身进展管理。

在英国,公司法一直是会计制度的主要法律依据,由公司对会计提出总括框架,再有会计职业团体制定会计准那么对会计实务进展具体规X。

这样,公司法的执行在很大程度上依靠会计职业团体通过制定具体规那么来完成。

关键词:会计准那么职业团体真实公允财务报告一、英国简况英国全称“大不列颠及北爱尔兰联合王国〞, 由大不列颠岛、爱尔兰岛北部及附近的很多小岛组成,领土总面积24 .4万平方公里。

其中大不列颠岛又分为英格兰、威尔士和苏格兰三局部。

它是典型的资产阶级议会制的君主立宪制国家, 实行的是“三权分立〞的政治体制。

英国政治法律制度影响市场经济运行的一个显著特点是政策法制化。

国际会计英国会计报告共33页文档

41、学问是异常珍贵的东西,从任何源泉吸 收都不可耻。——阿卜·日·法拉兹

国际会计英国会计报告

11、战争满足了,或曾经满足过人的 好斗的 本能, 但它同 时还满 足了人 对掠夺 ,破坏 以及残 酷的纪 律和专 制力的 欲望。 ——查·埃利奥 特 12、不应把纪律仅仅看成教育的手段 。纪律 是教育 过程的 结果, 首先是 学生集 体表现 在一切 生活领 域—— 生产、 日常生 活、学 校、文 化等领 域中努 力的结 果。— —马卡 连柯(名 言网)

42、只有在人群中间,才能认识自 己。——德国

43、重复别人所说的话,只需要教育; 而要挑战别人所说的话,则需要头脑。—— 玛丽·佩蒂博恩·普尔

44、卓越的人一大优点是:在不利与艰 难的遭遇里百折不饶。——贝多芬

45、自己的饭量自己知道。——苏联

涉外会计实务报告范文

涉外会计实务报告范文1. 简介涉外会计实务是指在进行与外国相关的财务活动时所涉及的会计实践和技术。

本报告将对涉外会计实务进行分析和总结,旨在提供指导和建议,以确保财务活动的准确性和合规性。

2. 国际会计准则涉外会计实务的核心是遵守国际会计准则(International Financial Reporting Standards,IFRS)。

IFRS是由国际会计准则理事会(International Accounting Standards Board,IASB)制定和发布的会计准则,旨在提供全球通用的财务报告框架。

IFRS的应用要求涉外企业对财务报表进行全面和准确的披露,确保透明度和可比性。

在准备涉外财务报表时,企业应根据IFRS的要求归类、评估和计量资产、负债、收入和费用。

此外,企业还需要披露与会计政策选择、估计和判断有关的信息,以增加财务报表的可理解性和可比性。

3. 外币核算与报告涉外会计实务还涉及外币核算与报告。

在跨国公司的运营中,经常需要处理多种货币,因此需要将外币转换为报告货币。

根据IFRS的要求,外币交易应按当期汇率折算,而外币货币性项目应按年末汇率重新计算。

企业在外币核算与报告过程中,还需要记录并披露外币兑换损益。

这些损益通常来自于外币财务报表与报告货币财务报表之间的折算差异。

对于企业而言,理解和控制外币风险是确保财务报表准确性的重要因素之一。

4. 跨国税务筹划涉外会计实务中的另一个重要方面是跨国税务筹划。

不同国家的税法和税率各有不同,企业可以通过合理的税务筹划来最大程度地减少税务负担。

跨国税务筹划涉及利用不同国家的税收协定和税收减免政策,以降低企业的税务成本。

企业在进行跨国税务筹划时,需要遵守各国的法律法规和国际税收准则,确保合规性和透明度。

此外,企业还需要进行风险评估和管理,以避免因税务筹划不当带来的负面影响。

5. 涉外会计审核涉外会计实务还涉及涉外会计审核。

企业的财务报表需要经过独立审计师的审核,以确保其准确性和合规性。

FRC发布英国会计业重要事实和趋势报告

龙源期刊网

FRC发布英国会计业重要事实和趋势报告作者:张宪光

来源:《财会信报》2016年第03期

英国财务报告委员会(FRC)近日发布了第14版《会计业重要事实和趋势》报告。

报告显示,英国职业会计组织的会员人数在英国和全球不断增长,但在过去2年,英国和爱尔兰境内的学员数量有所下降。

报告收集了过去4年各个会计组织的会员及其业务开展情况的相关数据。

主要包括以下几个方面。

第一,七大会计组织的会员人数稳步增长,英国和爱尔兰境内的会员总数为34.2万人(4年间增长了2.4%),全球范围的会员总数为49.7万人(4年间增长了3.2%)。

第二,注册登记的会计师事务所数量逐年下降,从2014年12月到现在,减少了304家,降幅为4.6%。

第三,与2014年相比,相较于其他为公共利益实体提供审计服务的事务所,规模最大的四家事务所的全部收费服务类项目均获得了增长。

所有事务所的审计服务收入均有所上升,而审计服务收入占总收入的比例保持稳定。

第四,“四大”在2015年审计的未纳入英国富时350指数(FTSE 350)的上市公司数量要多于往年。

FRC负责审计业务的执行理事梅勒妮·麦克拉伦说:“FRC是英国审计活动的主管部门,能够提供关于英国会计组织的独立观察。

FRC与相关会计组织通力合作,通过对各个组织的会员进行监管来提升审计质量。

今天发布的报告提供了不断发展的英国以及国际会计业的规模和特质的第一手资料。

”。