会计专业英语资料

会计专业英语复习资料.doc

会计专业英语复习资料.doc会计专业英语复习资料⼀、短语中英互译1、会计分录2、投资活动3、后进先出法4、客观性原则5、注册会计师6、权责发⽣制7、累计折旧8、资产负债表9、经营决策10、银⾏存款11、到期⽇12、历史成本13、source document14、nominal rate15、credit sale16、sum-of-years-digits method17、economic entity assumption18、financial position19、fixed assets20、public hearing21、income statement22、sales discount23、value added tax24、trade mark25、bank overdraft⼆、从下列选项中选出最佳答案1、Generally,revenue is recorded by a business enterprise at a point when :( )A、Management decides it is appropriate to do soB、The product is available for sale to consumersC、An exchange has taken place and the earning process is virtually completeD、An order for merchandise has been received2、Why are certain costs capitalized when incurred and then depreciated or amortized over subsequent accounting periods?( )A、To reduce the income tax liabilityB、To aid management in making business decisionsC、To match the costs of production with revenue as earnedD、To adhere to the accounting concept of conservatism3、What accounting principle or concept justifies the use of accruals and deferrals?( )A、Going concernB、MaterialityC、ConsistencyD、Stable monetary unit4、An accrued expense can best be described as an amount ( )A、Paid and currently matched with revenueB、Paid and not currently matched with revenueC、Not paid and not currently matched with revenueD、Not paid and currently matched with revenue5、Continuation of a business enterprise in the absence of contrary evidence is an example of the principle or concept of ( )A、Business entityB、ConsistencyC、Going concernD、Substance over form6、In preparing a bank reconciliation,the amount of checks outstanding would be:( )A、added to the bank balance according to the bank statement.B、deducted from the bank balance according to the bank statement.C、added to the cash balance according to the depositor’s records.D、deducted from the cash balance according to the depositor’s records.7、Journal entries based on the bank reconciliation are required for:( )A、additions to the cash balance according to the depositor’s records.B、deductions from the cash balance according to the depositor’srecords.C、Both A and BD、Neither A nor B8、A petty cash fund is :( )A、used to pay relatively small amounts。

会计专业英语

会计专业英语-CAL-FENGHAI.-(YICAI)-Company One1一、words and phrases1.残值 scrip value2.分期付款 installment3.concern 企业4.reversing entry 转回分录5.找零 change6.报销 turn over7.past due 过期8.inflation 通货膨胀9.on account 赊账10.miscellaneous expense 其他费用11.charge 收费12.汇票 draft13.权益 equity14.accrual basis 应计制15.retained earnings 留存收益16.trad-in 易新,以旧换新17.in transit 在途18.collection 托收款项19.资产 asset20.proceeds 现值21.报销 turn over22.dishonor 拒付23.utility expenses 水电费24.outlay 花费25.IOU 欠条26.Going-concern concept 持续经营27.运费 freight二、Multiple-choice question1.Which of the following does not describe accounting( C )A. Language of businessB. Useful ofr decision makingC. Is an end rathe than a means to an end.ed by business, government, nonprofit organizations, and individuals.2.An objective of financial reporting is to ( B )A. Assess the adequacy of internal control.B.Provide information useful for investor decisions.C.Evaluate management results compared with standards.D.Provide information on compliance with established procedures.3.Which of the following statements is(are) correct( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.A company may use different depreciation methods in its financial statements and its income tax return.C.The cost of a machine includes the cost of repairing damage to the machine during the installation process.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method.4. Which of the following is(are) correct about a company’s balance sheet( B )A.It displays sources and uses of cash for the period.B.It is an expansion of the basic accounting equationC.It is not sometimes referred to as a statement of financial position.D.It is unnecessary if both an income statement and statement of cash flows are availabe.5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A )rmation used to determine which products to poducermation about economic resources, claims to those resources, and changes in both resources and claims.rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows.rmation that is useful in making ivestment and credit decisions.6.Each of the following measures strengthens internal control over cash receipts except. ( C )A.The use of a petty cash fund.B.Preparation of a daily listing of all checks received through the mail.C.The use of cash registers.D.The deposit of cash receipts in the bank on a daily basis.7.The primary purpose for using an inventory flow assumption is to. ( A )A.Offset against revenue an appropriate cost of goods sold.B.Parallel the physical flow of units of merchandise.C.Minimize income taxes.D.Maximize the reported amount of net income.8.In general terms, financial assets appear in the balance sheet at. ( B )A.Current valueB.Face valueC.CostD.Estimated future sales value.9.If the going-concem assumption is no longer valid for a company except. ( C )nd held as an ivestment would be valued at its liquidation value.B.All prepaid assets would be completely written off immediately.C.Total contributed capital and retained earnings would remain unchanged.D.The allowance for uncollectible accounts would be eliminated.10.Which of the following explains the debit and credit rules relating to the recording of revenue and expenses( C )A.Expenses appear on the left side of the balance sheet and are recorded by debits;revenue appears on the right side of the balance sheet and is reoorded by credits.B. Expenses appear on the left side of the income statement and are recorded by debits; Revenue appears on the right side of the income statement and is recorded by credits.C.The effects of revenue and expenses on owners’ equity.D.The realization principle and the matching principle.11.Which of the following statements is(are) correct( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.The cost of a machine do not includes the cost of repairing damage to the machine during the installation prcess.C.A company may use same depreciation methods in its finacial statements and its income tax return.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the straight-line method.12.A set of financial statements ( B ) except.A.Is intended to assist users in evaluating the financial position, profitability, and future prospects of an entity.B.Is intended to assist the Intemal Revenue Service in detemining the amount of income taxes owed by a business organization.C.Includes notes disclosing information necessary for the proper interpretation of the statements.D.Is intended to assist investors and creditors in making decisions inventory the allocation of economic resources.13.The primary purpose for using an inventory flow assumption is to. ( B )A.Parallel the physical flow of units of merchandise.B.Offset against revenue an appropriate cost of goods soldC.Minimize income taxes.D.Maximize the reported amount of net income.14.Indicate all correct answers. In the accounting cycle. ( D )A.Transactions are posted before they are journalized.B.A trial balance is prepared after journal entries haven’t been posted.C.The Retained Earnings account is not shown as an up-to-date figure in the trial balance.D.Joumal entries are posted to appropriate ledger accounts.15.According to text, Objectives of Financial Reporting by Business Enterprises. ( D )A.Extemal users have the ability to prescribe information they want.rmation is always based on exact measures.C.Financial reporting is usually based on industries or the economy as a whole.D.Financial accounting does not directly measure the value of a business enterprise.16.Indicate all correct answers. Dividends except ( A )A.Decrease owners’ equity.B.Decrease net incomeC.Are recorded by debiting the Cash accountD.Are a business expense17.Which of the following practices contributes to efficient cash management ( C )A.Never borrow money-maintain a cash balance sufficient to make all necessary payments.B.Record all cash receipts and cash payments at the end of the month when reconciling the bank statements.C.Prepare monthly forecasts of planned cash receipts, payments, and anticipated cash balances up to a year in advance.D.Pay each bill as soon as the invoice arrives.18.Which of the following would you expect to find in a correctly prepared income statement ( A )A.Revenues earned during the period.B.Cash balance at the end of the period.C.Contributions by the owner during the period.D.Expenses incurred during the next period to earn revenues.19.Which of the following are important factors in ensuring the integrity of accounting information ( D )A.Institutional factors, such as standards for preparing information.B.Professional organizations, such as the American Institute of CPAs.petence’ judgment’ and ethical behavior of individual accountants’D.All of the above.三、Practices11.On Jan.1, 2000, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $40,000 for 2000, calculated under the sum-of –the-years’–digits method. Required: Determine the acquisition cost of the equipment. ( C )A.$210,000B.$250,000C.$225.000D.$200,0002. On Jan.2, 2002, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $24,000 for 2004, calculated under the sum-of –the-years’–digits method (4%). Required: Determine the acquisition cost of the equipment. ( C )A.$220,000B.$250,000C.$224.000D.$200,0003. October 1, 2005, Coast Financial Ioaned Bart Corporation $3000,000, receiving in exchange a nine-month, 12 percent note receivable. Coast ends its fiscal year on December 31 and makes adjusting entries to accrue interest earned on all notes receivable. The interest earned on the note receivable from Bart Corporation during 2006 will amount to. ( A )A.$9,000B.$18,000C.$27.000D.$36,000Question: What is the reconciled balance ( B )A.$4,187B.$4,085C.$4,090D.$4,000Required: Choose the reconciled balance. ( D )A.$3,220B.$3,250C.$3,200D.$3,225Required:Calculate the cost of goods available for sale(C)A.$475,000B.$474,000C.$470,000D.$473,000Required: Calculate the cost of goods sold ( D )A.$225,000B.$254,000C.$250,000D.$253,0008.At the end of the current year, the accounts receivable account has a debit balance of $60,000 and net sales for the year total $100,000. The allowance account before adjunstment has adebit balance of a $500, and uncollectible accounts expense is estimated at 1% of net sales. Question: The entry for the above bad debts is ( A )A.Dr. Bad Debt Accts. $1,500B.Dr. Bad Debt Accts. $500Cr. Allowance Doubtful Accts. $1,500 Cr. Allowance Doubtful Accts. $500C. Dr. Bad Debt Accts. $1,000D. Dr. Bad Debt Accts. $1,500Cr. Accts Rec. $1,000 Cr. Accts Rec. $1,5009.The balance sheet items to The Oven Bakery(arranged in alphabetical order)were as follows at August 1,2005.(You are to compute the missing figure for retained earnings.)(4%)REQUIRED:Find Retained earnings at August 1 2005(D)A.$420,000B.$44,000C.$40,000D.$48,000Practices2Sue began a public accounting practice and completed these transactions during first month of the current year.Required: Choose the entries to record the following transactons.1.Invested $50,000 cash in a public accounting practice begun this day. ( A )A.Dr. Cash $50,000B.Dr. Capital Stock $50,000Cr. Capital Stock $50,000 Cr. Cash $50,0002.Paid cash for three monts’ office rent in advance $900(B)A.Dr. Rent Exp. $900B.Dr. Prepaid Rent $900Cr. Cash $900 Cr. Cash $9003.Paid the premium on two insurance policies, $300. ( )A.Dr. Prepaid Insurance $300B.Dr. Insurance Exp $300Cr. Cash $300 Cr. Cash $300pleted accounting work for Sun Bank on credit $1000. ( A )A.Dr. Accts Rec $1000B.Dr. Cash $1000Cr.Accounting Revenue $1000 Cr.Accounting Revenue $10005.Paid the monthly utility bills of the accounting office $300 ( A )A.Dr Utility Exp $300B.Dr office Exp $300Cr. Cash $300 Cr. Cash $300Linda began a public accounting practice and completed these transactons during first month of the current year.Required: Choose the entries to record the following transactons.6.Invested $20,000 cash in a public accounting practice begun this day. ( A )A.Dr Cash $20,00B.Dr Capital Stock $20,000Cr. Capital Stock $20,000 Cr. Cash $20,007.Paid cash for three months’ office rent in advance $1200.( B )A.Dr. Rent Exp $1200B.Dr. Prepaid Rent $1200Cr. Cash $1200 Cr. Cash $12008.Purchased offfice supplies $100 and office equipment $2,000 on credit. ( B )A.Dr. Office Equipment $2,000B.Dr.Office Equipment $2,000Office Supplies $100 Office Supplies $100Cr. Accts Rec. $2,100 Cr.Accts Pay. $2,100pleted accounting work for Jack Hall and collected $2000 cash therefore. ( B )A.Dr. Accts Rec $2000B.Dr. Cash $2000Cr.Accounting Revenue $2000 Cr.Accounting Revenue $200010.Purchase additional office equipment on credit $2500.( A )A.Dr.Office equipment $2500B.Dr. Office equipment $2500Cr.Accts Pay $2500 Cr.Accts Rec $2500四、Translation:1)The mechanics of double-entry accounting are such that every transaction is recorded in the debit side of one or more accounts and in the credit side of one or more accounts with equal debits and credits. Such form of combination is called accounting entry. Where there are only two accounts affected. 2)the debit and credit amounts are equal. If more than two accounts are affceted, the total of the debit entries must equal the total of the credit entries. The double-entry accounting is used by virtually every business organization, regardless of whether the company’s accounting records are maintained manually or by computer.1.The mechanics of double-entry accounting.( B )A.会计两次记账的制度B.复式记账机制C.会计的重复记账体制2.the debit and credit amounts are equal. ( A )A.借方金额与贷方金额是相等的B.借出金额与贷款金额是相等的C.借入金额与贷款金额是相等的Most accounting methods are based on the assumption that the business enterprise will have a long life. Experience indicates that.1)inspite of numerous business failures, companies have a fairly highcontinuance rate. Accountants do not believe that business firms will last indefinitely, but they do expect them to last long enouthto 2)fulfill their objectives and commitments.3.in spite of numerous business failures, companies have a fairly high continuance rate. ( B )A.可惜有许多企业失败,但公司仍有较高的持续经营比率。

会计的基本英语知识点汇总

会计的基本英语知识点汇总1. Introduction to Accounting会计简介Accounting is the systematic process of identifying, recording, measuring, classifying, summarizing, interpreting, and communicating financial information. It plays a crucial role in the management and decision-making processes of businesses and organizations.会计是一种系统性的流程,用于识别、记录、度量、分类、总结、解释和传达财务信息。

它在企业和组织的管理和决策过程中发挥着至关重要的作用。

2. Basic Accounting Principles基本会计原则There are several fundamental principles that underpin the field of accounting:有几个基本原则支撑着会计领域:a) Accrual Principle: This principle states that financial transactions should be recorded when they occur and not when the cash is received or paid out.应计原则:该原则规定财务交易应在其发生时记录,而不是在现金收到或支付时记录。

b) Matching Principle: This principle states that expenses should be recognized in the same accounting period as the revenues they help generate.配比原则:该原则规定支出应在与其相关的收入产生的同一会计期间内确认。

会计专业英语知识点

会计专业英语知识点作为一门重要的商科专业,会计在各行各业中都扮演着重要的角色。

对于学习会计的学生来说,掌握好会计专业的英语知识点是非常必要的。

本文将介绍一些与会计专业相关的英语知识点,以帮助学生在学习和实践中更好地应用。

一、会计基础术语1. Assets(资产):在会计中,资产指的是公司拥有的具有现金价值的资源,包括现金、存货、房地产等。

2. Liabilities(负债):负债是指公司对外的债务或应付款项,在会计中包括借款、应付账款等。

3. Equity(所有者权益):也被称为净资产或股东权益,表示公司的所有者对于其资产净值的权益。

4. Revenue(收入):收入是指公司通过销售产品或提供服务而获得的资金流入。

5. Expenses(费用):费用是指公司为经营活动而发生的支出,包括租金、工资、税金等。

6. Balance Sheet(资产负债表):资产负债表是一份会计报表,以资产、负债和所有者权益的形式显示公司的财务状况。

二、会计报表1. Income Statement(利润表):利润表显示了公司在一定期间内的收入、费用和净利润。

2. Cash Flow Statement(现金流量表):现金流量表反映了公司在一定期间内现金收入、现金支出以及现金净增加额。

3. Statement of Retained Earnings(留存收益表):留存收益表展示了公司在一定期间内的净利润和分红情况。

4. Statement of Changes in Equity(权益变动表):权益变动表展示了公司在一段时间内所有者权益的变化情况,包括净利润、股东投资等。

三、审计和税务1. Audit(审计):审计是对公司财务报表和财务记录的全面审核和检查。

2. Taxation(税务):税务是指涉及支付税款和申报纳税义务的活动,包括个人所得税、企业所得税等。

3. Tax Return(纳税申报表):纳税申报表是个人或企业向税务机关报告收入和纳税情况的文件。

会计专业英语

资产负债表Balance Sheet As at Dec. 31, 2007损益表Income StatementFor the year ended Dec. 31, 2007现金流量表Cash Flow StatementFor the year ended Dec. 31 2007所有者权益变动表Statement of Changes in Equity For the year ended Dec. 31 2007会计确认reorganization计量measurement 表述presentation 揭示(附注)disclosureChap. 1会计基本假设underlying assumptions 会计主体假设separate-entity assumption 持续经营假设continuity assumption Going-concern assumption会计分期accounting period 货币计量unit-of-measure assumption币值稳定Nominal dollar capital maintenance assumption会计信息质量要求qualitative criteria 可靠性reliability相关性relevance 可理解性understandability可比性comparability 实质重于形式substance over form历史成本historical cost重置成本replacement cost可实现净值net-realizable value现值present value公允价值fair value财务报告financial statement资产负债表Balance Sheet利润表Income Statement现金流量表Cash Flow Statement所有者权益变动表Statement of Changes in Equity附注notesDisclosure notesChap. 2货币资金monetary assets现金cash银行账户bank account现金等价物cash equivalentChap. 3金融资产financial instruments以公允价值计量且变动计入当期损益的金融资产Measure at fair value through profit or loss交易性金融资产held for trading指定为以公允价值计量且变动计入当期损益的金融资产Identified as at fair value through profit or loss持有到期投资Held-to –maturity investment贷款和应收账款Loans and receivables可供出售金融资产available-for-sale financial assets减值impairment减值损失impairment lossChap. 4存货inventory存货的种类:Classification of inventory原材料raw materials inventory在产品work-in-progress inventory半成品component parts产成品finished goods inventory商品merchandise inventory周转材料supplies inventory发出存货的计量cost flow assumption先进先出法first-in-first-out (FIFO)后进先出法last-in-first-out (LIFO)移动加权平均法moving-average unit cost全月一次加权平均法weighted-average system个别计价法(具体辨认法)specific identification期末存货的计量ending balance of inventory成本与可变现净值孰低lower-of –cost-or-market valueNet-realizable value存货跌价准备Allowance to reduce inventory to LCM资产减值损失—存货减值损失loss of impairment on assets ---- loss of impairment on inventory Chap. 5长期股权投资long-term investment –shareInvestment in subsidiary ***成本法cost method权益法equity method投资收益investment income可转换convertibleChap. 6固定资产capital assets在建工程wok-in-progress construction折旧amortization平均年限法straight-line-method工作量法unit-of- production双倍余额递减法declining-balance method年数总和法sum-of-the-years-digits method后续支出subsequent expenditure资本化capitalized cost费用化expensed cost处置retirement and disposal持有待售的固定资产capital assets held for sale固定资产清理disposal of capital assets固定资产减值准备allowance of impairments on capital assetsChap. 7无形资产intangible assets专利权patents非专利技术industrial design registration商标权trademarks and trade name著作权copyright特许权franchise rights土地使用权rights of using landChap. 8投资性房地产investment property / profitable estateChap. 9非货币性资产交换non-monetary assets exchange商业实质commercial substanceChap. 10资产减值assets impairment估计evaluation资产组assets group cash generate unit商誉goodwillChap. 11负债liabilities流动负债current liabilities非流动负债non-current liabilities初始计量initial measurement辞退福利fire fringe进口import出口export可转换公司债券convertible bondChap. 12所有者权益equity实收资本issued capital资本公积capital reserve股本溢价share premium留存收益retained earnings未分配利润distributed profitChap. 13完工百分比法percentage of completion method建造合同construction contract直接法direct method间接法indirect method分部报告segment report关联方related party租赁lease担保guaranteeChap. 15或有事项contingencies或有资产contingent assets或有负债contingent liabilities亏损合同onerous contractChap.16重组reorganization /resutructionChap. 18借款费用borrowing costs borrowing expenditure溢价premium折价discount资本化capitalize costsChap. 20所得税income tax计税基础tax base永久性差别permanent difference暂时性差别temporary difference应纳税暂时性差异taxable temporary differences可抵扣暂时性差异deductible temporary difference递延所得税资产deferred tax assets递延所得税负债deferred tax liabilitiesChap. 21外币折算translation of foreign currency外币交易foreign currency transactions外币财务报表折算translation of foreign currency financial statement 即期汇率current exchange rate远期汇率future exchange rate通货膨胀inflationChap. 22出租人lessor承租人lessee经营租赁operating lease融资租赁finance lease / capital lease售后租回sale and leasebackChap. 23会计政策、会计估计变更和差错更正Changes in accounting policies, changes in accounting estimates and corrections of errors 会计估计Accounting estimatesChap. 24资产负债表日后事项Events after the balance sheet date调整事项Adjusting event非调整事项Unadjusting event利润分配profit allocation以前年度损益调整retained earnings--prior year adjustmentUndistributed profit—prior year adjustmentChap. 25企业合并corporate combination长期股权投资long-term investment--shareInvestment in subsidiary ***Chap. 26合并财务报表consolidated financial statementConsolidated Balance SheetConsolidated Income StatementConsolidated Cash Flow StatementConsolidated Statement of Changes in Equity。

会计专业读的英语书

会计专业读的英语书1. "Accounting for Managers: Interpreting Accounting Information for Decision Making" by Robert N. Anthony and Leslie K. Breitner:这本书是一本经典的会计入门教材,用通俗易懂的方式解释了会计基本概念和财务报表分析,适合初学者阅读。

2. "Financial Accounting: An Introduction to Concepts, Methods, and Uses" by Robert F. Meigs and Walter B. Meigs:这本书涵盖了财务会计的基本概念和原则,以及财务报表的编制和分析,是一本广泛使用的会计教材。

3. "Intermediate Accounting" by Donald E. Kieso, Jerry J. Weygandt, and TerryD. Warfield:这是一本中级会计教材,深入探讨了财务会计的各个方面,包括资产、负债、所有者权益、收入和费用等。

4. "Cost Accounting: A Managerial Emphasis" by Charles T. Horngren, Srikant M. Datar, and George Foster:这本书专注于成本会计,介绍了成本核算、成本分析和成本管理的概念和方法。

5. "Advanced Accounting" by Floyd A. Beams, Joseph H. Anthony, Kenneth R. Peach, and Michael F. Ragatz:这本书是高级会计的教材,涵盖了复杂的会计议题,如合并报表、合伙企业会计和国际会计等。

会计专业英语汇总

会计专业英语汇总Introduction to Accounting Profession (会计专业介绍)Accounting is the practice of recording, analyzing, and interpreting financial transactions of a business or organization. It is an essential function for business success as it provides information about the financial position, performance, and cash flow of an entity. In the accounting profession, professionals use a set of standards and principles to ensure accuracy and consistency in financial reporting.Accounting Principles and Concepts (会计原则和概念)There are several widely accepted accounting principles and concepts that guide the preparation of financial statements. The most significant principles include the accrual principle, revenue recognition principle, matching principle, and consistency principle. These principles ensure that financial information is reported accurately and fairly.Financial Statements (财务报表)Financial statements are the primary output of the accounting process. They provide a snapshot of a company's financial position and performance over a specific period. The three main financial statements are the balance sheet, income statement, and cash flow statement. The balance sheet shows a company's assets, liabilities, and equity at a specific point in time. The income statement shows a company's revenue, expenses, and net income or loss over a period. The cash flow statement shows the inflows and outflows of cash during a specific period.Auditing (审计)Auditing is the examination of financial statements to ensure theirreliability and compliance with accounting standards and principles. Auditors play a crucial role in providing assurance to stakeholders that the financial statements are free from material misstatement or fraud. They assess the internal controls of an organization and gather evidence to support the financial information provided in the statements.Taxation (税务)Taxation is an essential aspect of accounting, as professionals need to understand the tax laws and regulations to provide accurate tax planning and compliance services. Accountants prepare tax returns for individuals and businesses, ensuring that they pay the correct amount of taxes according tothe applicable laws.Cost Accounting (成本会计)Cost accounting focuses on the analysis and control of costs in a business. It involves determining the cost of producing goods or services and analyzing the profitability of different products or services. Cost accountants provide valuable information for decision-making, such as pricing strategies, budgeting, and cost reduction initiatives.Management Accounting (管理会计)Management accounting involves the use of financial information to support managerial decision-making. Management accountants provide reports and analysis to help managers make informed decisions about resource allocation, performance evaluation, and strategic planning. They may also be involved in budgeting, forecasting, and variance analysis.International Financial Reporting Standards (国际财务报告准则)International Financial Reporting Standards (IFRS) is a set of accounting standards developed by the International Accounting Standards Board (IASB). IFRS is widely adopted in many countries around the world, with the aim of promoting transparency and comparability of financial statements globally. Knowledge of IFRS is essential for accountants working in multinational organizations or those seeking international opportunities.Ethics in Accounting (会计伦理)Ethics play a crucial role in the accounting profession. Accountants are expected to maintain integrity, objectivity, and professional skepticism in their work. They must adhere to ethical codes and standards set by professional accounting bodies, such as the American Institute of Certified Public Accountants (AICPA) or the Association of Chartered Certified Accountants (ACCA).Conclusion (结论)Accounting is a dynamic and challenging profession that requires bothtechnical knowledge and ethical behavior. Professionals in the field play a critical role in helping businesses make informed financial decisions and ensuring compliance with accounting standards. The knowledge and skills gained through studying accounting and mastering accounting English are valuable assets that can open doors to a variety of career opportunities.。

会计专业英语(超实用}

一、企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流动资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due within one year 减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivable due within one year减:短期投资跌价准备Less: Impairment for current investment短期投资净额Net bal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账准备Less: Bad debt provision for Account receivable 应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账准备Less: Bad debt provision for Other receivable 其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less: Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due within one year一年内到期的应收融资租赁款Finance lease receivables due within one year其他流动资产Other current assets流动资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment委托贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值准备Less: Impairment for long-term equity investment减:长期债权投资减值准备Less: Impairment for long-term debt investment减:委托贷款减值准备Less: Provision for entrusted loan receivable长期投资净额Net bal of long-term investment其中:合并价差Include: Goodwill (Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less: Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less: Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值准备Less: Impairment for construction in progress 在建工程净额Net bal of construction in progress固定资产清理Fixed assets to be disposed of固定资产合计Total fixed assets无形资产及其他资产Other assets & Intangible assets无形资产Intangible assets减:无形资产减值准备Less: Impairment for intangible assets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease –Unguaranteed residual values融资租赁——应收融资租赁款Finance lease –Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets & intangible assets递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability & Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advance from customers应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Other payable预提费用Accrued Expense预计负债Provision递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year 其他流动负债Other current liability流动负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants & Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益)Owners’Equity实收资本(或股本)Paid in capital减;已归还投资Less: Capital redemption实收资本(或股本)净额Net bal of Paid in capital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include: Statutory reserves未确认投资损失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include: Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability & Equity三、利润及利润分配表Income statement and profit appropriation一、主营业务收入Revenue减:主营业务成本Less: Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit ( - means loss) 加:其他业务收入Add: Other operating income减:其他业务支出Less: Other operating expense减:营业费用Selling & Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列)Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列)Add: Investment income补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less: Non-operating expense四、利润总额(亏损总额以“—”填列)Profit before Tax减:所得税Less: Income tax少数股东损益Minority interest加:未确认投资损失Add: Unrealised investment losses五、净利润(净亏损以“—”填列)Net profit ( - means loss)加:年初未分配利润Add: Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution( - means loss) 减:提取法定盈余公积Less: Appropriation of statutory surplus reserves 提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and welfare fund提取储备基金Appropriation of reserve fund提取企业发展基金Appropriation of enterprise expansion fund利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners' distribution 减:应付优先股股利Less: Appropriation of preference share's dividend 提取任意盈余公积Appropriation of discretionary surplus reserve应付普通股股利Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses from natural disaster3.会计政策变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting policies4.会计估计变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting estimates5.债务重组损失Losses from debt restructuringaccount payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表Accounting period 会计期间accounting year 或financial year 会计年度accountant genaral 会计主任account balancde 结平的帐户account bill 帐单account books 帐account classification 帐户分类account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐Accounting period(会计期间)are related to specific time periods ,typically one year(通常是一年) 资产负债表:balance sheet 可以不大写b利润表:income statements (or statements of income)利润分配表:retained earnings现金流量表:cash flows1、部门的称谓市场部Marketing销售部Sales Department (也有其它讲法,如宝洁公司销售部叫客户生意发展部CBD)客户服务Customer Service ,例如客服员叫CSR,R for representative人事部Human Resource行政部Admin.财务部Finance & Accounting产品供应Product Supply,例如产品调度员叫P S Planner2、人员的称谓助理Assistant秘书secretary前台接待小姐Receptionist文员clerk ,如会计文员为Accounting Clerk主任supervisor经理Manager总经理GM,General Manager入场费admission运费freight小费tip学费tuition价格,代价charge制造费用Manufacturing overhead 材料费Materials管理人员工资Executive Salaries 奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare 会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance 油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees总监Director总会计师Finance Controller高级Senior 如高级经理为Senior Manager 营业费用Operating expenses代销手续费Consignment commission charge 运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license plate tax(VVULPT) 土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost帐目名词一、资产类Assets流动资产Current assets货币资金Cash and cash equivalents现金Cash银行存款Cash in bank其他货币资金Other cash and cash equivalents 外埠存款Other city Cash in bank银行本票Cashier''s cheque银行汇票Bank draft信用卡Credit card信用证保证金L/C Guarantee deposits存出投资款Refundable deposits短期投资Short-term investments股票Short-term investments - stock债券Short-term investments - corporate bonds基金Short-term investments - corporate funds其他Short-term investments - other短期投资跌价准备Short-term investments falling price reserves 应收款Account receivable应收票据Note receivable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable其他应收款Other notes receivable坏账准备Bad debt reserves预付账款Advance money应收补贴款Cover deficit by state subsidies of receivable库存资产Inventories物资采购Supplies purchasing原材料Raw materials包装物Wrappage低值易耗品Low-value consumption goods材料成本差异Materials cost variance自制半成品Semi-Finished goods库存商品Finished goods商品进销差价Differences between purchasing and selling price委托加工物资Work in process - outsourced委托代销商品Trust to and sell the goods on a commission basis受托代销商品Commissioned and sell the goods on a commission basis存货跌价准备Inventory falling price reserves分期收款发出商品Collect money and send out the goods by stages待摊费用Deferred and prepaid expenses长期投资Long-term investment长期股权投资Long-term investment on stocks股票投资Investment on stocks其他股权投资Other investment on stocks长期债权投资Long-term investment on bonds债券投资Investment on bonds其他债权投资Other investment on bonds长期投资减值准备Long-term investments depreciation reserves股权投资减值准备Stock rights investment depreciation reserves债权投资减值准备Bcreditor''s rights investment depreciation reserves委托贷款Entrust loans本金Principal利息Interest减值准备Depreciation reserves固定资产Fixed assets房屋Building建筑物Structure机器设备Machinery equipment运输设备Transportation facilities工具器具Instruments and implement累计折旧Accumulated depreciation固定资产减值准备Fixed assets depreciation reserves房屋、建筑物减值准备Building/structure depreciation reserves机器设备减值准备Machinery equipment depreciation reserves工程物资Project goods and material专用材料Special-purpose material专用设备Special-purpose equipment预付大型设备款Prepayments for equipment为生产准备的工具及器具Preparative instruments and implement for fabricate在建工程Construction-in-process安装工程Erection works在安装设备Erecting equipment-in-process技术改造工程Technical innovation project大修理工程General overhaul project在建工程减值准备Construction-in-process depreciation reserves 固定资产清理Liquidation of fixed assets无形资产Intangible assets专利权Patents非专利技术Non-Patents商标权Trademarks, Trade names著作权Copyrights土地使用权Tenure商誉Goodwill无形资产减值准备Intangible Assets depreciation reserves专利权减值准备Patent rights depreciation reserves商标权减值准备trademark rights depreciation reserves未确认融资费用Unacknowledged financial charges待处理财产损溢Wait deal assets loss or income待处理财产损溢Wait deal assets loss or income待处理流动资产损溢Wait deal intangible assets loss or income 待处理固定资产损溢Wait deal fixed assets loss or income二、负债类Liability短期负债Current liability短期借款Short-term borrowing应付票据Notes payable银行承兑汇票Bank acceptance商业承兑汇票Trade acceptance应付账款Account payable预收账款Deposit received代销商品款Proxy sale goods revenue应付工资Accrued wages应付福利费Accrued welfarism应付股利Dividends payable应交税金Tax payable应交增值税value added tax payable进项税额Withholdings on V AT已交税金Paying tax转出未交增值税Unpaid V AT changeover减免税款Tax deduction销项税额Substituted money on V AT出口退税Tax reimbursement for export进项税额转出Changeover withnoldings on V AT出口抵减内销产品应纳税额Export deduct domestic sales goods tax转出多交增值税Overpaid V AT changeover未交增值税Unpaid V AT应交营业税Business tax payable应交消费税Consumption tax payable应交资源税Resources tax payable应交所得税Income tax payable应交土地增值税Increment tax on land value payable应交城市维护建设税Tax for maintaining and building cities payable应交房产税Housing property tax payable应交土地使用税Tenure tax payable应交车船使用税Vehicle and vessel usage license platetax(VVULPT) payable应交个人所得税Personal income tax payable其他应交款Other fund in conformity with paying其他应付款Other payables预提费用Drawing expense in advance其他负债Other liabilities待转资产价值Pending changerover assets value预计负债Anticipation liabilities长期负债Long-term Liabilities长期借款Long-term loans一年内到期的长期借款Long-term loans due within one year一年后到期的长期借款Long-term loans due over one year应付债券Bonds payable债券面值Face value, Par value债券溢价Premium on bonds债券折价Discount on bonds应计利息Accrued interest长期应付款Long-term account payable应付融资租赁款Accrued financial lease outlay一年内到期的长期应付Long-term account payable due within one year一年后到期的长期应付Long-term account payable over one year 专项应付款Special payable一年内到期的专项应付Long-term special payable due within one year一年后到期的专项应付Long-term special payable over one year 递延税款Deferral taxes三、所有者权益类OWNERS'' EQUITY资本Capita实收资本(或股本) Paid-up capital(or stock)实收资本Paicl-up capital实收股本Paid-up stock已归还投资Investment Returned公积资本公积Capital reserve资本(或股本)溢价Cpital(or Stock) premium接受捐赠非现金资产准备Receive non-cash donate reserve 股权投资准备Stock right investment reserves拨款转入Allocate sums changeover in外币资本折算差额Foreign currency capital其他资本公积Other capital reserve盈余公积Surplus reserves法定盈余公积Legal surplus任意盈余公积Free surplus reserves法定公益金Legal public welfare fund储备基金Reserve fund企业发展基金Enterprise expension fund利润归还投资Profits capitalizad on return of investment利润Profits本年利润Current year profits利润分配Profit distribution其他转入Other chengeover in提取法定盈余公积Withdrawal legal surplus提取法定公益金Withdrawal legal public welfare funds提取储备基金Withdrawal reserve fund提取企业发展基金Withdrawal reserve for business expansion提取职工奖励及福利基金Withdrawal staff and workers'' bonus andwelfare fund利润归还投资Profits capitalizad on return of investment应付优先股股利Preferred Stock dividends payable提取任意盈余公积Withdrawal other common accumulation fund 应付普通股股利Common Stock dividends payable转作资本(或股本)的普通股股利Common Stock dividends change toassets(or stock)未分配利润Undistributed profit四、成本类Cost生产成本Cost of manufacture基本生产成本Base cost of manufacture辅助生产成本Auxiliary cost of manufacture制造费用Manufacturing overhead材料费Materials管理人员工资Executive Salaries 奖金Wages退职金Retirement allowance补贴Bonus外保劳务费Outsourcing fee福利费Employee benefits/welfare 会议费Coferemce加班餐费Special duties市内交通费Business traveling通讯费Correspondence电话费Correspondence水电取暖费Water and Steam税费Taxes and dues租赁费Rent管理费Maintenance车辆维护费Vehicles maintenance 油料费Vehicles maintenance培训费Education and training接待费Entertainment图书、印刷费Books and printing 运费Transpotation保险费Insurance premium支付手续费Commission杂费Sundry charges折旧费Depreciation expense机物料消耗Article of consumption劳动保护费Labor protection fees季节性停工损失Loss on seasonality cessation劳务成本Service costs五、损益类Profit and loss收入Income业务收入OPERATING INCOME主营业务收入Prime operating revenue产品销售收入Sales revenue服务收入Service revenue其他业务收入Other operating revenue材料销售Sales materials代购代售包装物出租Wrappage lease出让资产使用权收入Remise right of assets revenue 返还所得税Reimbursement of income tax其他收入Other revenue投资收益Investment income短期投资收益Current investment income长期投资收益Long-term investment income计提的委托贷款减值准备Withdrawal of entrust loans reserves 补贴收入Subsidize revenue国家扶持补贴收入Subsidize revenue from country其他补贴收入Other subsidize revenue营业外收入NON-OPERATING INCOME非货币性交易收益Non-cash deal income现金溢余Cash overage处置固定资产净收益Net income on disposal of fixed assets出售无形资产收益Income on sales of intangible assets固定资产盘盈Fixed assets inventory profit罚款净收入Net amercement income支出Outlay业务支出Revenue charges主营业务成本Operating costs产品销售成本Cost of goods sold服务成本Cost of service主营业务税金及附加Tax and associate charge营业税Sales tax消费税Consumption tax城市维护建设税Tax for maintaining and building cities 资源税Resources tax土地增值税Increment tax on land value5405 其他业务支出Other business expense销售其他材料成本Other cost of material sale其他劳务成本Other cost of service其他业务税金及附加费Other tax and associate charge 费用Expenses营业费用Operating expenses代销手续费Consignment commission charge运杂费Transpotation保险费Insurance premium展览费Exhibition fees广告费Advertising fees管理费用Adminisstrative expenses职工工资Staff Salaries修理费Repair charge低值易耗摊销Article of consumption办公费Office allowance差旅费Travelling expense工会经费Labour union expenditure研究与开发费Research and development expense福利费Employee benefits/welfare职工教育经费Personnel education待业保险费Unemployment insurance劳动保险费Labour insurance医疗保险费Medical insurance会议费Coferemce聘请中介机构费Intermediary organs咨询费Consult fees诉讼费Legal cost业务招待费Business entertainment技术转让费Technology transfer fees矿产资源补偿费Mineral resources compensation fees排污费Pollution discharge fees房产税Housing property tax车船使用税Vehicle and vessel usage license plate tax(VVULPT) 土地使用税Tenure tax印花税Stamp tax财务费用Finance charge利息支出Interest exchange汇兑损失Foreign exchange loss各项手续费Charge for trouble各项专门借款费用Special-borrowing cost营业外支出Nonbusiness expenditure捐赠支出Donation outlay减值准备金Depreciation reserves非常损失Extraordinary loss处理固定资产净损失Net loss on disposal of fixed assets 出售无形资产损失Loss on sales of intangible assets固定资产盘亏Fixed assets inventory loss债务重组损失Loss on arrangement罚款支出Amercement outlay所得税Income tax以前年度损益调整Prior year income adjustmentabacus算盘Abandonment废弃,报废;委付abandonment value废弃价值ability to service debt偿债能力abnormal cost异常成本abnormal spoilage异常损耗above par超过票面价值above the line线上项目absolute amount绝对数,绝对金额absolute endorsement绝对背书absolute insolvency绝对无力偿付absolute priority绝对优先求偿权absolute value绝对值absorb摊配,转并absorption account摊配账户,转并账户absorption costing摊配成本计算法abstract摘要表abuse滥用职权abuse of tax shelter滥用避税项目ACCA特许公认会计师公会accelerated cost recovery system加速成本收回制度accelerated depreciation method加速折旧法,快速折旧法acceleration clause加速偿付条款,提前偿付条款acceptance bill承兑票据acceptance register承兑票据登记簿acceptance sampling验收抽样access time存取时间accommodation融通accommodation bill融通票据accommodation endorsement融通背书accountability经营责任,会计责任accountability unit责任单位Accountancy 《会计》杂志accountancy会计accountant会计员,会计师accountant general会计主任,总会计accounting in charge主管会计师accountant,s legal liability会计师的法律责任accountant,s report会计师报告accountant,s responsibility会计师职责account form账户式,账式accounting assumption会计假定,会计假设accounting basis会计基准,会计基本方法accounting changes会计变更accounting concept会计概念accounting control会计控制accounting convention会计常规,会计惯例accounting corporation会计公司accounting cycle会计循环accounting data会计数据accounting doctrine会计信条accounting elements会计要素accounting entity会计主体,会计个体accounting entry会计分录accounting equation会计等式accounting event会计事项accounting exposure会计暴露,会计暴露风险accounting firm会计事务所Accounting Hall of Fame会计名人堂accounting harmonization会计协调化accounting identity会计恒等式accounting income会计收益accounting information会计信息accounting information system会计信息系统accounting internationalization会计国际化accounting journals会计杂志accounting legislation会计法规accounting manual会计手册accounting objective会计目标accounting period会计期accounting policies会计政策accounting postulate会计假设accounting principle会计原则Accounting Principle Board会计原则委员会accounting procedures会计程序accounting profession会计职业,会计专业accounting rate of return会计收益率accounting records会计记录,会计簿籍Accounting Review 《会计评论》accounting rules会计规则Accounting Series Release 《会计公告文件》accounting service会计服务accounting software会计软件accounting standard会计标准,会计准则accounting standardization会计标准化Accounting Standards Board会计准则委员会(英) Accounting Standards Committee会计准则委员会(英) accounting technique会计技术accounting theory会计理论accounting transaction会计业务,会计账务Accounting Trend and Techniques 《会计趋势和会计技术》accounting unit会计单位accounting valuation会计计价accounting year会计年度accounts会计账簿,会计报表account sales承销清单,承销报告单Account 账户Accounting system 会计系统American Accounting Association 美国会计协会Audit 审计Balance sheet 资产负债表bookkeeping 簿记cash folw prospects 现金流量预测certificate in Internal Auditing 内部审计证书certificate in Management Accounting 管理会计证书Certificate Public Accountant 注册会计师cost accounting 成本会计external users 外部使用者financial accounting 财务会计financial accounting standards board 会计准则委员会financial forecast 财务预测generally accepted accounting principles 会计公认原则general-purpose information 通用目的信息government accounting office 政府会计办公室income statement 损益表institute of internal auditors 内部审计师协会institute of management accountants 管理会计师协会integrity 整合性internal auditing 内部审计internal control structure 内部控制结构internal revenue service 国内收入暑internal users 内部使用者management accounting 管理会计return of investment 投资回报securities ans exchange commission 证券交易委员会statement of cash flow 现金流量表statement of financial position 财务状况表tax accounting 税务会计accounting equation 会计等式articulation 勾稽关系assets 资产business entity 企业个体capital stock 股本corporation 公司cost principle 成本原则creditor 债权人deflation 通货紧缩disclosure 披露expenses 费用financial statement 财务报表financial activities 筹资活动going-concern assumption 持续经营假设inflatiion 通货膨胀investing activities 投资活动owner's equity 所有者权益parternership 合伙企业negative cash flow 负现金流量operating activities 经营活动liabilities 负债positive cash folw 正现金流retained earning 留存利润revenue 收入sole proprietorship 独资企业slovency 清偿能力stable-dollar assumption 稳定货币假设stockholders 股东stockholders' equity 股东权益window dressing 门面粉饰account format 账户式account payable 应付账款account receivabla 应收账款accounting cycle 会计循环accounting equation 会计等式accounting receivable turnover 应收账款周转率accrual basis accounting 债权发生制accrued dividend 应计股利accrued expenseaccrued revenueaccumulated depreciation 累计折旧acid-test ratio 、quick ratio 速动资产与流动负债比例acquisition cost 购置成本adjusted trial balance 调整后试算表adjusting entry 调整分录adverseaging of accounts receivable 应收账款的账龄分类allocable 应分配的allowance for bad debts 备抵坏账allowance for depreciationallowance for doubtful accounts 呆账备抵allowance for uncollectible accounts 呆账备抵amortization 摊销、清偿annuity due 期初年金allowance method 备抵法annuity method 年金法appraisal method 估价法bad debt 坏账bad debts expensebank discount 银行贴现折扣bank reconciliation 银行调节表bank statement 银行对账单barter 易货交易benchmarking 基准board of directors 董事会bond 证券bonds payable 应付债券book value 账面价值budget 预算callable bonds 可赎回债券capital 资金,资本capital expenditures 资本支出capital lease 资本租赁capital paid in 缴入资本capital stock 股本capitalize 资本化carry back 抵前carry forward 递延、结转cash basis accounting 现收现付制cash disbursements journal 现金支出簿cash in hand 库存现金cash receipts journal 现金收入日记账chart of accounts 会计科目表classified balance sheet 分类资产负债表closing entries 结账分录closing the accounts 结账collateral 抵押品common stock 普通股compound interest 复利comprehensive income 综合收入conservatism 谨慎性consistency principle 一致性consolidated statements 汇总报表contingent liability 或有负债contra account 抵消账户contract interest rate 约定利率contribute capital 缴入资本control account 控制账户controlling interest 控制股权权益convertible bond 可转换债券convertible preferred stock 可转换优先股copyright 版权cost of capital 资本成本cost of goods sold 销售成本coupon 息票,减价优待券credit 信用,贷方cumulative preferred stock 累积优先股current assets 流动资产current liability 流动负债fair market value 公平市价FIFO 先进先出法fixed assets 固定资产FOB price 离岸价footnotes 表下注释franchise 特许权freight-in 进货运费freight-out 销货运费general journal 普通日记账general ledger 总分类账gross book value 账面价值gross profit 毛利hedge 套期交易incremental cost 增值成本installment 分期付款instruments 证券,票据intangible assets 无形资产interest 利息inventory 存货invoice 发票issued capital stock 已发行股本journal entry 日记账LIFO 后进先出long-term debt 长期负债Lower of cost or market 成本市价孰低法lump sum 一次性付款market value 市场价值markup 涨价mortgage 抵押,债券net assets 净资产obsolete inventory 作废存货partnership 合伙企业par value 面值patent 专利权payroll 工资单pension fund 养老基金pension plan 养老金计划physical inventory 实地盘点pledged assets 抵押资产posting 过账P&E 固定资产preference shares 优先股preferred stock 优先股premium 溢价present value 现值principal 本金refinance 再筹资refund 退还,再筹资retained earnings 留存收益salvage value 挽救价值(残值)security 证券,担保品segment 分部service life 使用年限stockholders equity 股东权益stock discount 股票折价straight line method 直线法subsidiary ledger 明细分类账sum-of-the-year-digits methods 年数总和法tangible assets 有形资产voucher check 凭单支票withholding 预扣worksheets 工作底稿write down 减计write off 转销,注销year-end-adjustment 年终调整。

会计学专业英语第一章

D

Unit 4 Information Users

Words and Expressions

Unit 1 Accounting and Accounting Profession

• 1.accounting 会计(核算); 会计学 • 2.accountant 会计师;会计人 员

• 6.operational audits 经营审计 • pliance audits 合规审计 • 8.income tax returns 所得税申 报单 • 9.nonprofit organizations 非盈 利组织 • ptroller 会计主任

• 3.bookkeeping 簿记;簿记学

• 4.chartered accountants 特许会 计师 • 5.auditing 审计;审计学

• 11.professional ethics 职业道德

• 12.proprietorship 独资企业 • 13.partnership 合伙企业 • 14.double-entry accounting

of these accountants work on a salary basis.

Unit 1 Accounting and Accounting Profession

Private accounting

Private

accountants, also called executive or administrative accountants,

Accountingபைடு நூலகம்is

often known as one of the most useful tools of business because all

《会计专业英语》Chapter 1 Introduction to Accounting

▪ 1.1 What is accounting ▪ 1.2 Forms of business entities ▪ 1.3 Business activities ▪ 1.4 Users of accounting information ▪ 1.5 Types of accounting ▪ 1.6 Careers in accounting

12

Internal users

➢ Internal users are employees of an enterprise and are directly involved in managing and operating the business.

➢ From basic labor categories to chief executive officers, all employees are paid, and their paychecks are generated by the accounting information system.

➢ Resources owned by a business are called capital assets. ➢ Assets have different types and names. Various, non-current,

and tangible assets are called property, plant, and equipment (PPE).

9

Investing activity

➢ Investing activities involve the purchase of the resources a company needs in order to operate.

《会计学专业英语》PPT课件

Accounting: Information for Decision Making

• The primary objective of accounting – to provide information that is useful for making decisions.

Users of Accounting Information

why they need the information; • Understand the types of accounting information; • Have a general idea of the professional fields of

accounting and their duties. • Learn the accounting terms in this chapter and use them

Suggestions for study

• Previewing the text is very important.

• 《An English –Chinese Dictionary of Accounting》,《英汉双解财会词典》,外 语教学与研究出版社, [英] P.H. Collin, Adrian Joliffe 编,张炜等译,2002年9 月第1版

– Company – Corporation

Definition of Accounting

• Accounting is an information system designed to record, classify and summarize systematically significant financial and other economic information about business firms, and analyses and interprets its results, with monetary unit as its main criterion.

会计专业英语

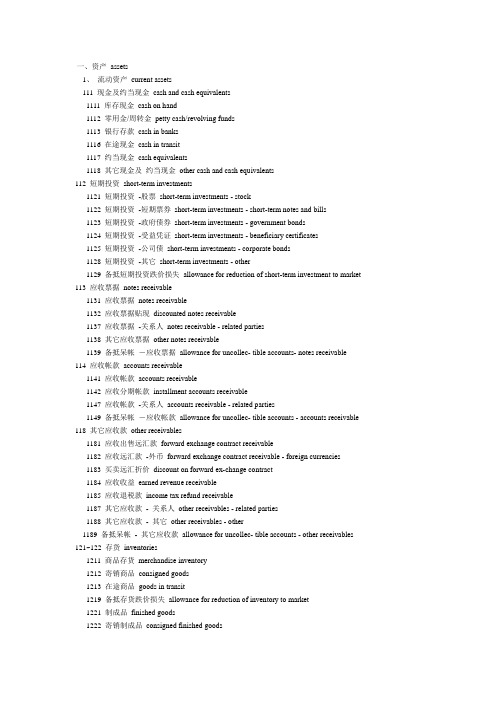

一、资产assets1、流动资产current assets111 现金及约当现金cash and cash equivalents1111 库存现金cash on hand1112 零用金/周转金petty cash/revolving funds1113 银行存款cash in banks1116 在途现金cash in transit1117 约当现金cash equivalents1118 其它现金及约当现金other cash and cash equivalents112 短期投资short-term investments1121 短期投资-股票short-term investments - stock1122 短期投资-短期票券short-term investments - short-term notes and bills1123 短期投资-政府债券short-term investments - government bonds1124 短期投资-受益凭证short-term investments - beneficiary certificates1125 短期投资-公司债short-term investments - corporate bonds1128 短期投资-其它short-term investments - other1129 备抵短期投资跌价损失allowance for reduction of short-term investment to market 113 应收票据notes receivable1131 应收票据notes receivable1132 应收票据贴现discounted notes receivable1137 应收票据-关系人notes receivable - related parties1138 其它应收票据other notes receivable1139 备抵呆帐-应收票据allowance for uncollec- tible accounts- notes receivable 114 应收帐款accounts receivable1141 应收帐款accounts receivable1142 应收分期帐款installment accounts receivable1147 应收帐款-关系人accounts receivable - related parties1149 备抵呆帐-应收帐款allowance for uncollec- tible accounts - accounts receivable 118 其它应收款other receivables1181 应收出售远汇款forward exchange contract receivable1182 应收远汇款-外币forward exchange contract receivable - foreign currencies1183 买卖远汇折价discount on forward ex-change contract1184 应收收益earned revenue receivable1185 应收退税款income tax refund receivable1187 其它应收款- 关系人other receivables - related parties1188 其它应收款- 其它other receivables - other1189 备抵呆帐- 其它应收款allowance for uncollec- tible accounts - other receivables 121~122 存货inventories1211 商品存货merchandise inventory1212 寄销商品consigned goods1213 在途商品goods in transit1219 备抵存货跌价损失allowance for reduction of inventory to market1221 制成品finished goods1222 寄销制成品consigned finished goods1223 副产品by-products1224 在制品work in process1225 委外加工work in process - outsourced1226 原料raw materials1227 物料supplies1228 在途原物料materials and supplies in transit1229 备抵存货跌价损失allowance for reduction of inventory to market125 预付费用prepaid expenses1251 预付薪资prepaid payroll1252 预付租金prepaid rents1253 预付保险费prepaid insurance1254 用品盘存office supplies1255 预付所得税prepaid income tax1258 其它预付费用other prepaid expenses126 预付款项prepayments1261 预付货款prepayment for purchases1268 其它预付款项other prepayments128~129 其它流动资产other current assets1281 进项税额V A T paid (or input tax)1282 留抵税额excess V A T paid (or overpaid V A T)1283 暂付款temporary payments1284 代付款payment on behalf of others1285 员工借支advances to employees1286 存出保证金refundable deposits1287 受限制存款certificate of deposit-restricted1291 递延所得税资产deferred income tax assets1292 递延兑换损失deferred foreign exchange losses1293 业主(股东)往来owners^(stockholders^)current account1294 同业往来current account with others1298 其它流动资产-其它other current assets - other2、基金及长期投资funds and long-term investments131 基金funds1311 偿债基金redemption fund (or sinking fund)1312 改良及扩充基金fund for improvement and expansion1313 意外损失准备基金contingency fund1314 退休基金pension fund1318 其它基金other funds132 长期投资long-term investments1321 长期股权投资long-term equity investments1322 长期债券投资long-term bond investments1323 长期不动产投资long-term real estate in-vestments1324 人寿保险现金解约价值cash surrender value of life insurance1328 其它长期投资other long-term investments1329 备抵长期投资跌价损失allowance for excess of cost over market value of long-term investments3、固定资产property , plant, and equipment141 土地land1411 土地land1418 土地-重估增值land - revaluation increments142 土地改良物land improvements1421 土地改良物land improvements1428 土地改良物-重估增值land improvements - revaluation increments1429 累积折旧-土地改良物accumulated depreciation - land improvements143 房屋及建物buildings1431 房屋及建物buildings1438 房屋及建物-重估增值buildings -revaluation increments1439 累积折旧-房屋及建物accumulated depreciation - buildings144~146 机(器)具及设备machinery and equipment1441 机(器)具machinery1448 机(器)具-重估增值machinery - revaluation increments1449 累积折旧-机(器)具accumulated depreciation - machinery151 租赁资产leased assets1511 租赁资产leased assets1519 累积折旧-租赁资产accumulated depreciation - leased assets152 租赁权益改良leasehold improvements1521 租赁权益改良leasehold improvements1529 累积折旧- 租赁权益改良accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments forequipment 1561 未完工程construction in progress1562 预付购置设备款prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation - miscellaneous property, plant, and equipment 16 递耗资产depletable assets161 递耗资产depletable assets1611 天然资源natural resources1618 天然资源-重估增值natural resources -revaluation increments1619 累积折耗-天然资源accumulated depletion - natural resources17 无形资产intangible assets171 商标权trademarks1711 商标权trademarks172 专利权patents1721 专利权patents173 特许权franchise1731 特许权franchise174 著作权copyright1741 著作权copyright175 计算机软件computer software1751 计算机软件computer software cost176 商誉goodwill1761 商誉goodwill177 开办费organization costs1771 开办费organization costs178 其它无形资产other intangibles1781 递延退休金成本deferred pension costs1782 租赁权益改良leasehold improvements1788 其它无形资产-其它other intangible assets - other18 其它资产other assets181 递延资产deferred assets1811 债券发行成本deferred bond issuance costs1812 长期预付租金long-term prepaid rent1813 长期预付保险费long-term prepaid insurance1814 递延所得税资产deferred income tax assets1815 预付退休金prepaid pension cost1818 其它递延资产other deferred assets182 闲置资产idle assets1821 闲置资产idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables1841 长期应收票据long-term notes receivable1842 长期应收帐款long-term accounts receivable1843 催收帐款overdue receivables1847 长期应收票据及款项与催收帐款-关系人long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产assets leased to others1851 出租资产assets leased to others1858 出租资产-重估增值assets leased to others - incremental value from revaluation1859 累积折旧-出租资产accumulated depreciation - assets leased to others186 存出保证金refundable deposit1861 存出保证金refundable deposits188 杂项资产miscellaneous assets1881 受限制存款certificate of deposit - restricted1888 杂项资产-其它miscellaneous assets - other二、负债liabilities21~ 22 流动负债current liabilities211 短期借款short-term borrowings(debt)2111 银行透支bank overdraft2112 银行借款bank loan2114 短期借款-业主short-term borrowings - owners2115 短期借款-员工short-term borrowings - employees2117 短期借款-关系人short-term borrowings- related parties2118 短期借款-其它short-term borrowings - other212 应付短期票券short-term notes and bills payable2121 应付商业本票commercial paper payable2122 银行承兑汇票bank acceptance2128 其它应付短期票券other short-term notes and bills payable2129 应付短期票券折价discount on short-term notes and bills payable213 应付票据notes payable2131 应付票据notes payable2137 应付票据-关系人notes payable - related parties2138 其它应付票据other notes payable214 应付帐款accounts pay able2141 应付帐款accounts payable2147 应付帐款-关系人accounts payable - related parties216 应付所得税income taxes payable2161 应付所得税income tax payable217 应付费用accrued expenses2171 应付薪工accrued payroll2172 应付租金accrued rent payable2173 应付利息accrued interest payable2174 应付营业税accrued V A T payable2175 应付税捐-其它accrued taxes payable- other2178 其它应付费用other accrued expenses payable218~219 其它应付款other payables2181 应付购入远汇款forward exchange contract payable2182 应付远汇款-外币forward exchange contract payable - foreign currencies2183 买卖远汇溢价premium on forward exchange contract2184 应付土地房屋款payables on land and building purchased2185 应付设备款Payables on equipment2187 其它应付款-关系人other payables - related parties2191 应付股利dividend payable2192 应付红利bonus payable2193 应付董监事酬劳compensation payable to directors and supervisors2198 其它应付款-其它other payables - other226 预收款项advance receipts2261 预收货款sales revenue received in advance2262 预收收入revenue received in advance2268 其它预收款other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债other current liabilities2281 销项税额V A T received(or output tax)2283 暂收款temporary receipts2284 代收款receipts under custody2285 估计售后服务/保固负债estimated warranty liabilities2291 递延所得税负债deferred income tax liabilities2292 递延兑换利益deferred foreign exchange gain2293 业主(股东)往来owners^ current account2294 同业往来current account with others2298 其它流动负债-其它other current liabilities - others23 长期负债long-term liabilities231 应付公司债corporate bonds payable2311 应付公司债corporate bonds payable2319 应付公司债溢(折)价premium(discount)on corporate bonds payable232 长期借款long-term loans payable2321 长期银行借款long-term loans payable - bank2324 长期借款-业主long-term loans payable - owners2325 长期借款-员工long-term loans payable - employees2327 长期借款-关系人long-term loans payable - related parties2328 长期借款-其它long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据long-term notes payable2332 长期应付帐款long-term accounts pay-able2333 长期应付租赁负债long-term capital lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties2338 其它长期应付款项other long-term payables234 估计应付土地增值税accrued liabilities for land value increment tax2341 估计应付土地增值税estimated accrued land value incremental tax pay-able235 应计退休金负债accrued pension liabilities2351 应计退休金负债accrued pension liabilities238 其它长期负债other long-term liabilities2388 其它长期负债-其它other long-term liabilities - other28 其它负债other liabilities281 递延负债deferred liabilities2811 递延收入deferred revenue2814 递延所得税负债deferred income tax liabilities2818 其它递延负债other deferred liabilities286 存入保证金deposits received2861 存入保证金guarantee deposit received288 杂项负债miscellaneous liabilities2888 杂项负债-其它miscellaneous liabilities - other三、业主权益owners^ equity31 资本capital311 资本(或股本)capital3111 普通股股本capital - common stock3112 特别股股本capital - preferred stock3113 预收股本capital collected in advance3114 待分配股票股利stock dividends to be distributed3115 资本capital32 资本公积additional paid-in capital321 股票溢价paid-in capital in excess of par3211 普通股股票溢价paid-in capital in excess of par- common stock3212 特别股股票溢价paid-in capital in excess of par- preferred stock323 资产重估增值准备capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积capital surplus from gain on disposal of assets3241 处分资产溢价公积capital surplus from gain on disposal of assets325 合并公积capital surplus from business combination3251 合并公积capital surplus from business combination326 受赠公积donated surplus3261 受赠公积donated surplus328 其它资本公积other additional paid-in capital3281 权益法长期股权投资资本公积additional paid-in capital from investee under equity method3282 资本公积- 库藏股票交易additional paid-in capital - treasury stock trans-actions33 保留盈余(或累积亏损)retained earnings (accumulated deficit)331 法定盈余公积legal reserve3311 法定盈余公积legal reserve332 特别盈余公积special reserve3321 意外损失准备contingency reserve3322 改良扩充准备improvement and expansion reserve3323 偿债准备special reserve for redemption of liabilities3328 其它特别盈余公积other special reserve335 未分配盈余(或累积亏损)retained earnings-unappropriated (or accumulated deficit)3351 累积盈亏accumulated profit or loss3352 前期损益调整prior period adjustments3353 本期损益net income or loss for current period34 权益调整equity adjustments341 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments 3411 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments342 累积换算调整数cumulative translation adjustment3421 累积换算调整数cumulative translation adjustments343 未认列为退休金成本之净损失net loss not recognized as pension cost3431 未认列为退休金成本之净损失net loss not recognized as pension costs35 库藏股treasury stock351 库藏股treasury stock3511 库藏股treasury stock36 少数股权minority interest361 少数股权minority interest3611 少数股权minority interest四、损益类4 营业收入operating revenue41 销货收入sales revenue411 销货收入sales revenue4111 销货收入sales revenue4112 分期付款销货收入installment sales revenue417 销货退回sales return4171 销货退回sales return419 销货折让sales allowances4191 销货折让sales discounts and allowances46 劳务收入service revenue461 劳务收入service revenue4611 劳务收入service revenue47 业务收入agency revenue471 业务收入agency revenue4711 业务收入agency revenue48 其它营业收入other operating revenue488 其它营业收入-其它other operating revenue4888 其它营业收入-其它other operating revenue - other 5 营业成本operating costs51 销货成本cost of goods sold511 销货成本cost of goods sold5111 销货成本cost of goods sold5112 分期付款销货成本installment cost of goods sold512 进货purchases5121 进货purchases5122 进货费用purchase expenses5123 进货退出purchase returns5124 进货折让charges on purchased merchandise513 进料materials purchased5131 进料material purchased5132 进料费用charges on purchased material5133 进料退出material purchase returns5134 进料折让material purchase allowances514 直接人工direct labor5141 直接人工direct labor515~518 制造费用manufacturing overhead5151 间接人工indirect labor5152 租金支出rent expense, rent5153 文具用品office supplies (expense)5154 旅费travelling expense, travel5155 运费shipping expenses, freight5156 邮电费postage (expenses)5157 修缮费repair(s)and maintenance (expense ) 5158 包装费packing expenses5161 水电瓦斯费utilities (expense)5162 保险费insurance (expense)5163 加工费manufacturing overhead - outsourced5166 税捐taxes5168 折旧depreciation expense5169 各项耗竭及摊提various amortization5172 伙食费meal (expenses)5173 职工福利employee benefits/welfare5176 训练费training (expense)5177 间接材料indirect materials5188 其它制造费用other manufacturing expenses56 劳务成本制ervice costs561 劳务成本service costs5611 劳务成本service costs56 劳务成本制ervice costs561 劳务成本service costs5611 劳务成本service costs57 业务成本gency costs571 业务成本agency costs5711 业务成本agency costs58 其它营业成本other operating costs588 其它营业成本-其它other operating costs-other5888 其它营业成本-其它other operating costs - other 6 营业费用operating expenses61 推销费用selling expenses615~618 推销费用selling expenses6151 薪资支出payroll expense6152 租金支出rent expense, rent6153 文具用品office supplies (expense)6154 旅费travelling expense, travel6155 运费shipping expenses, freight6156 邮电费postage (expenses)6157 修缮费repair(s)and maintenance (expense) 6159 广告费advertisement expense, advertisement6161 水电瓦斯费utilities (expense)6162 保险费insurance (expense)6164 交际费entertainment (expense)6165 捐赠donation (expense)6166 税捐taxes6167 呆帐损失loss on uncollectible accounts6168 折旧depreciation expense6169 各项耗竭及摊提various amortization6172 伙食费meal (expenses)6173 职工福利employee benefits/welfare6175 佣金支出commission (expense)6176 训练费training (expense)6188 其它推销费用other selling expenses62 管理及总务费用general & administrative expenses625~628 管理及总务费用general & administrative expenses6251 薪资支出payroll expense6252 租金支出rent expense, rent6253 文具用品office supplies6254 旅费travelling expense, travel6255 运费shipping expenses,freight6256 邮电费postage (expenses)6257 修缮费repair(s)and maintenance (expense)6259 广告费advertisement expense, advertisement6261 水电瓦斯费utilities (expense)6262 保险费insurance (expense)6264 交际费entertainment (expense)6265 捐赠donation (expense)6266 税捐taxes6267 呆帐损失loss on uncollectible accounts6268 折旧depreciation expense6269 各项耗竭及摊提various amortization6271 外销损失loss on export sales6272 伙食费meal (expenses)6273 职工福利employee benefits/welfare6274 研究发展费用research and development expense6275 佣金支出commission (expense)6276 训练费training (expense)6278 劳务费professional service fees6288 其它管理及总务费用other general and administrative expenses 63 研究发展费用research and development expenses635~638 研究发展费用research and development expenses6351 薪资支出payroll expense6352 租金支出rent expense, rent6353 文具用品office supplies6354 旅费travelling expense, travel6355 运费shipping expenses, freight6356 邮电费postage (expenses)6357 修缮费repair(s)and maintenance (expense)6361 水电瓦斯费utilities (expense)6362 保险费insurance (expense)6364 交际费entertainment (expense)6366 税捐taxes6368 折旧depreciation expense6369 各项耗竭及摊提various amortization6372 伙食费meal (expenses)6373 职工福利employee benefits/welfare6376 训练费training (expense)6378 其它研究发展费用other research and development expenses7 营业外收入及费用non-operating revenue and expenses, other income(expense)71~74 营业外收入non-operating revenue711 利息收入interest revenue7111 利息收入interest revenue/income712 投资收益investment income7121 权益法认列之投资收益investment income recognized under equity method7122 股利收入dividends income7123 短期投资市价回升利益gain on market price recovery of short-term investment713 兑换利益foreign exchange gain7131 兑换利益foreign exchange gain714 处分投资收益gain on disposal of investments7141 处分投资收益gain on disposal of investments715 处分资产溢价收入gain on disposal of assets7151 处分资产溢价收入gain on disposal of assets748 其它营业外收入other non-operating revenue7481 捐赠收入donation income7482 租金收入rent revenue/income7483 佣金收入commission revenue/income7484 出售下脚及废料收入revenue from sale of scraps7485 存货盘盈gain on physical inventory7486 存货跌价回升利益gain from price recovery of inventory7487 坏帐转回利益gain on reversal of bad debts7488 其它营业外收入-其它other non-operating revenue- other items75~ 78 营业外费用non-operating expenses751 利息费用interest expense7511 利息费用interest expense752 投资损失investment loss7521 权益法认列之投资损失investment loss recog- nized under equity method7523 短期投资未实现跌价损失unrealized loss on reduction of short-term investments to market 753 兑换损失foreign exchange loss7531 兑换损失foreign exchange loss754 处分投资损失loss on disposal of investments7541 处分投资损失loss on disposal of investments755 处分资产损失loss on disposal of assets7551 处分资产损失loss on disposal of assets788 其它营业外费用other non-operating expenses7881 停工损失loss on work stoppages7882 灾害损失casualty loss7885 存货盘损loss on physical inventory7886 存货跌价及呆滞损失loss for market price decline and obsolete and slow-moving inventories 7888 其它营业外费用-其它other non-operating expenses- other8 所得税费用(或利益)income tax expense (or benefit)81 所得税费用(或利益)income tax expense (or benefit)811 所得税费用(或利益)income tax expense (or benefit)8111 所得税费用(或利益)income tax expense (or benefit)9 非经常营业损益nonrecurring gain or loss91 停业部门损益gain(loss)from discontinued operations911 停业部门损益-停业前营业损益income(loss)from operations of discontinued segments 9111 停业部门损益-停业前营业损益income(loss)from operations of discontinued segment 912 停业部门损益-处分损益gain(loss)from disposal of discontinued segments 9121 停业部门损益-处分损益gain(loss)from disposal of discontinued segment92 非常损益extraordinary gain or loss921 非常损益extraordinary gain or loss9211 非常损益extraordinary gain or loss93 会计原则变动累积影响数cumulative effect of changes in accounting principles931 会计原则变动累积影响数cumulative effect of changes in accounting principles9311 会计原则变动累积影响数cumulative effect of changes in accounting principles94 少数股权净利minority interest income941 少数股权净利minority interest income9411 少数股权净利minority interest income。

会计英语复习资料