实用会计英语Chapter 4 Accounts

会计专业英语名词解释

会计专业英语名词解释Chapter 11. Accounting: Accounting is the process of identifying, measuring, recording, andcommunicating economic information to permit informed judgments and decisions by users of the information.2. Accrual basis accounting: Accrual basis accounting refers to an accounting methodthat records financial events based on economic activity rather than financial activity.Under accrual accounting, revenue is recorded when it is earned and realized, regardless of when actual payment is received. Similarly, expenses are matched with revenue regardless of when they are actually paid.3. Balance sheet: Balance sheet is the financial statement showing the financial positionof an entity by summarizing its assets, liabilities, and owner’s equity at one sp ecific date.4. Business entity: Business entity refers to an economic unit that controls resources,incurs obligations, and engages in business activities.5. CAS: Chinese Accounting Standards refer to the accounting concepts, measurementtechniques, and standards of presentation used in financial statements made by the PRC Financial Apartment.6. Cash basis accounting: Cash basis accounting is a method of bookkeeping thatrecords financial events based on cash flows and cash position. Revenue is recognized when cash is received and expense is recognized when cash is paid out.7. Conservatism: Conservatism states that when alternative accounting valuations areequally possible, the accountant should select the one that is least likely to overstate assets and income in the current period.8. Consistency: Consistency means that a company uses the same accountingprinciples and methods from year to year.9. Continuity: Continuity refers to an accounting assumption, also known as thegoing-concern assumption, that the company will continue to operate in the near future, unless substantial evidence to the contrary exists.10. Corporation: Corporation is a business organized as a separate legal entity understate corporation law and having ownership divided into transferable shares of stock.11. Cost principle: Cost principle is a widely used principle of accounting for assets at theiroriginal cost to the current owner.12. Financial accounting: Financial accounting refers to the development and use ofaccounting information describing the financial position of an entity and the results of its operations.13. Financial position: Financial position refers to the financial resources and obligationsof an organization, as described in a balance sheet.14. Financial reporting: Financial reporting refers to the process of periodically providing“general-purpose”financial information (such as financial statements) to persons outside the business organization.15. Financial statements: Financial statements refer to the four related accounting reportsthe summarize the current financial position of an entity and the results of its operations for the preceding year ( or other time period).16. Full disclosure principle: Full disclosure principle requires that circumstances andevents that make a difference to financial statement users be disclosed.17. Going-concern assumption: Go-concern assumption is an assumption by accountantsthat a business will operate indefinitely unless specific evidence to the contrary, such as impending bankruptcy, exists.18. Historical cost: The historical cost of an asset is the exchange price in the transactionin which the asset was acquired.19. Matching principle: Matching principle is an accounting principle that dictates thatexpenses be matched with revenue in the period in which efforts are made to generate revenue.20. Materiality: Materiality refers to the magnitude of an omission or misstatement ofaccounting information that, considering the circumstances, makes it likely that the judgment of a reasonable person relying on the information would have been influenced by the omission or misstatement.21. Market value: Market value is the estimated amount for which a property shouldexchange on the date of valuation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion,22. Net realizable value: The net realizable value of an asset is the amount of cash (or theequivalent) that could be obtained on the date of the balance sheet by selling the asset in its present condition, in an orderly liquidation.23. Income statement: Income statement is a financial statement indicating theprofitability of a business over a preceding time period.24. Partnership: Partnership is a business owned by two or more persons associated aspartners.25. Present value: The present value of an asset is the net amount of discounted futurecash inflows less the discounted future cash outflows relating to the asset.26. Proprietorship: Partnership is a business owned by one person.27. Relevance: Accounting information is relevant if it can make a difference in a decisionby helping users predict the outcomes of past, present, and future events or confirm or correct prior expectations. To be relevant, accounting information should have either predictive or feedback value, or both. In addition, it should be timely,28. Reliability: Reliable information is reasonably free from error and bias, and faithfullyrepresents what it is intended to represent. That is, to be reliable, information should be verifiable, neutral, and possess representational faithfulness,29. Revenue recognition principle: An accounting principle that dictates that revenue berecognized in the accounting period in which it is earned.30. Statement of cash flow: A financial statement summarizing the cash receipts and cashpayments of the business over the same time period covered by the income statement.31. Statement of owner’s equity: A financial statement explaining certain changes in theamount of the owner’s equity (investment) in the business.1. Asset: Assets mean the entire property of a person, association, corporation, or estateapplicable or subject to the payment of debts.2. Operating cycle: The operating cycle is the time span from when cash is used toacquire goods and service and until cash is received from the sale of goods and service.3. Cash: cash refers to an exchange medium launched into circulation which is availablefor any ordinary use and can be used to purchase goods or services or repay debts.4. Cash equivalents: Cash equivalents are short-term, highly liquid investments or otherassets that readily convertible to cash and sufficiently close to their due date.5. Internal control: Internal control means all policies and procedures used to protectassets, ensure reliable accounting, promote efficient operations, and urge adherence to company policies.Chapter 31. Receivables: Receivables refer to the monetary claims against business, individualsand other debtors.2. Accounts receivable: Accounts receivables are amounts due from customers for creditsales. This section begins by describing how accounts receivables occur. It includes receivables that occur when customers use credit cards issued by third parties and when a company gives credit directly to customers.3. Installment accounts receivables: Installment accounts receivables are amounts overan extended time period.4. Commercial discounts: Commercial discounts refer to a certain sum of moneydeducted from listed prices.5. Cash discounts: Cash discounts refer to a deduction from gross invoice price, whichare an inducement offered to the buyer to encourage the payments of goods within a specific period of time.6. The percentage-of-sale method: The percentage-of-sale method estimates somepercentage of credit sales would turn out to be uncollectible, in which the percentage of bad debts to credit sales should be properly estimated with the past experience. 7. The percentage-of-receivable method: The percentage-of-receivable methodestimates the uncollectible with a percentage of the ending balance of accounts receivables rather than credit sales.8. The aging method: The aging method analyzes the age structure of the accountbalance. In this method, an aging schedule is prepared, classifying the length of time that has passes since the sale that gave rise to them.9. The allowance method: The allowance method is the most usual way that companiesuse to record uncollectible accounts. In calculating uncollectible accounts, an account allowances for uncollectible receivable is set up.10. Promissory note: A promissory note is a written promise to pay a certain sum ofmoney on demand or at a fixed and determinable future time, generally over 30 or 60 days.1. Inventory: Inventory is the total amount if goods and/or materials contained in a storeor factory at any given.2. Product costs: Product costs are those costs that “attach”to the inventory. Suchcharges include freight charges on goods purchased, other direct costs of acquisition, and labor and other production costs incurred in processing the goods up to the time of sale.3. The perpetual inventory system: The perpetual inventory system requires thatseparate inventory ledger be maintained for each goods.4. The periodic inventory system: The periodic inventory system requires a companydetermines the quantity of inventory on hand only periodically, under which the cost of ending inventory is subtracted from the cost of goods available for sale, then the cost of goods sold are determined.5. The specific identification method: The specific identification method can be usedwhen units in the ending inventory can be identified as coming from specific purchases.6. The weighted average cost method: The weighted average cost method assumes thatthe goods available for sale have the same cost per unit. Under this method, the cost of goods available for sale is allocated on the basis of the weighted-average unit c0st.7. The first-in, first-out (FIFO) method: The first-in, first-out (FIFO) method is base on theassumption that the costs of the first items acquired should be assigned to the first item sold.Chapter 51. Accelerated depreciation: Accelerated depreciation is a method of depreciation thatcall for recognition of relatively large amounts if depreciation in the early years of an asset’s useful life and relatively small amounts in the later years.2. Depreciable value: Depreciable value is the amount of the acquisition cost to beallocated as depreciation over the total useful life of an asset. It is the difference between the total acquisition cost and the estimated residual value.3. Depreciation: Depreciation is the systematic allocation of the cost of an asset toexpress over the years of its estimated useful life.4. Fair market value: Fair market value is the value of an asset based on the price forwhich a company could sell the asset to an independent third party.5. Impairment: Impairment is a change in economic conditions which reduces theeconomic usefulness of an asset.6. Residual value: Residual value is the amount a company expects to receive fromdisposal of an asset at the end of its useful life.7. Useful life: Useful life refers to the shorter of the physical life or the economic life of anasset.1. Amortization: The systematic write-off to expense of the cost of an intangible assetover the period of its economic usefulness.2. Copyright: A grant by the state government covering the right to publish, sell, orotherwise control literary or artistic products for the life of the author plus 50 years. 3. Franchises: Agreements entered into by two parties in which, for a fee, one party (thefranchisor) gives the other party (the franchisee) rights to perform certain functions or sell certain products or services.4. Goodwill: The present value of expected future earnings of a business in excess of theearnings normally realized in the industry.5. Identifiable intangible asset: Intangibles that can be purchased or sold separately fromthe other assets of the company.6. Intangible assets: Those assets which are used in the operation of a business butwhich have no physical substance and are not current.7. Leases (or leaseholds): Intangible assets because a right to use the property is heldby the lessee.8. Patent: An exclusive right granted by the state government giving the owner control ofthe manufacturing, sale, or other use of an invention for a period of years from the date of filling.9. Research and development costs: Expenditures that may lead to patent, copy rights,new processes and new products.10. Trademarks: Distinctive identifications of a manufactured product or of a service,taking the form of a name, a sign, a slogan, a logo, or an emblem.Chapter 71. Available-for-sale securities: Securities that may be sold in the future.2. Consolidated financial statements: Financial statements that present the assets andliabilities controlled by the parent company and the aggregate profitability of the affiliated companies.3. Cost method: An accounting method in which the investment in common stock isrecorded at cost and revenue is recognized only when cash dividends are received.4. Debt investments: Investments in government and corporation bonds.5. Equity method: An accounting method in which the investment in common stock isinitially recorded at cost and the investment account is then adjusted annually to show the investor’s equity in the investee.6. Fair value: Amount for which a security could be sold in a normal market.7. Held-to-maturity securities: Debt securities that investor has the intent and ability tohold to maturity.8. Investment portfolio: A group of stocks in different corporations held for investmentpurposes.9. Long-term investments: Investments that are not readily marketable and thatmanagement does not intend to convert into cash within the next year or operating cycle, whichever is longer.10. Parent company: A company that owns more than 50% of the common stock ofanother entity.11. Short-term investments: Investments that are readily marketable and intend to convertinto cash within the next year or operating cycle, whichever is longer.12. Stock investments: Investments in the capital stock of corporations.13. Subsidiary (affiliated) company: A company in which more than 50% of its stock isowned by another company.14. Trading securities: Securities bought and held primarily for sale in the near term togenerate income on short-term price differences.Chapter 81. Amortization table: A schedule that indicates how installment payments are allocatedbetween interest expense and repayments of principal.2. Capital lease: A lease contract which, in essence, finances the eventual purchase bythe lessee of leased property. The lessor accounts for a capital lease as a sale of property; the lessee records an asset and a liability equal to the present value of the future lease payments. A capital lease is also called a financing lease.3. Commercial paper: Very short-term notes payable issued by financially strongcorporations. They are highly liquid from the investor’s point of view.4. Commitments: Contracts for the future transactions.5. Contra-liability account: A ledger account which is deducted from or offset against arelated liability account in the balance sheet; for example, Discount on Notes Payable.6. Convertible bond: One which may be changed at the option of the bondholder for aspecific number of shares of common stock.7. Deferred income taxes: Income taxes upon income which already has been reportedfor financial reporting purposes, but which will not be reported in income tax returns until future periods.8. Discount on notes payable: A contra-liability account representing any interestcharges applicable to future periods included in the face amount of a note payable.Over the life of the note, the balance of the Discount on Notes Payable account is amortized into Interest Expense.9. Deducted bond: Debenture bonds refer to an unsecured bond.10. Estimated liabilities: Liabilities which appear in financial statements at estimatedamounts.11. Long-term liabilities: Obligations that are not due for at least a year.12. Loss contingency: A possible loss, or expense, stemming from past events, that willbe resolved as to existence and amount by some future event.13. Mortgage bonds: Bonds secured by the pledge of specific assets.14. Operating lease: A lease contract which is in essence a rental agreement. The lesseehas the use of the leased property, but the lessor retains the usual risks and rewards of ownership. The periodic lease payments are accounted for as rent expense by the lessee and as rental revenue by the lessor.Chapter 91. Income: Income is defined as increases in economic benefits during the reportingperiod in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants. Income encompasses both revenue and gains.2. Revenue: Revenue is income that arises in the course of ordinary activities of anentity and is referred to by a variety of different names including sales, fees, interest, dividends and royalties.3. Gains: Gains represent other items that meet the definition of income and may, or maynot arise in the course of the ordinary activities of an entity.4. Accrued revenue: Accrued revenue is the revenue that has been earned but not yetcollected.5. Trade discounts: Trade discounts depend on the volume of the business or size oforder from the customer.6. Cash discounts: Cash discounts are offered to customers by some companies toencourage prompt payment of bills.7. Expenses: Expenses are outflows or using up of assets as part of operations of abusiness to generate sales.8. Employee expenses: Employee expenses are the entitlements which employeesaccumulate as a result of rendering their services to an employer.9. Depreciation (amortization): Depreciation is a periodic expense of operations and isassociated with the consumption or loss of service potential of non-current assets. 10. Bad (doubtful) debts expense: Bad debts expense is, in effect, a reduction of the“receivables” asset.11. Income taxes expense: Income taxes expense is the expense recognized in theaccounting records on an accrual basis that applies to income from continuing operations.12. Profit: Profit is the ultimate result of various operating activities of the enterprise in areporting period.13. Accounting policies: Accounting policies are the specific principles, bases,conventions, rules and practices adopted by an entity in preparing and presenting financial statements.14. Applicable profit: Applicable profit is assets that can be distributed to all kinds ofbeneficiaries.Chapter 101. Owner’s equity: Owner’s equity refers to the sources invested by owners or formed inthe course of the production and operation or other sourced shared by owners.2. Par value: The par value is an arbitrary dollar amount assigned to each share.3. Treasury stock: Treasury stock may be defined as shares of a corporation’s owncapital stock that have been issued and later reacquired by the issuing company but that have not been canceled or permanently retired.4. Capital reserve: Capital reserve refers to the capital which isn’t viewed as the paid-incapital or capital stock.5. Undistributed profit: Undistributed profit is the profit that is not distributed toshareholders but retained to the later years.Journal entries1. A company had the following transactions during January: Using the net method ofrecording purchases, prepare the journal entries to record these January transactions.Jan.2 Purchased merchandise, invoice price of $20 000, with terms 2/10, n/30.4 Received a credit memorandum for $4 000, the invoice price on merchandisereturned from the purchase of January 2.12 Purchased merchandise, invoice price of $15 000, with terms 3/15, n/30.26 Paid for the merchandise purchased on January 12.30 paid for the merchandise purchased on January 2.Answer:Jan.2 Merchandise …………………………………………………….19 600Accounts payable………………………………………………………19 6004 Accounts payable…………………………………………………3 920Merchandise………………………………………………………………3 92012 Merchandise……………………………………………………..14 550Accounts payable………………………………………………………14 55026 Accounts payable………………………………………………..14 550Cash……………………………………………………………………..14 55030 Accounts payable………………………………………………..15 680Expense (400)Cash………………………………………………………………………16 0802. The following series of transactions occurred during 2010 and 2011, when LinwoodCo. sold merchandise to John Moore. Linwood’s annual accounting period ends on December 31.10/01/2010 Sold $12 000 of merchandise to John Moore, terms 2/10, n/3011/15/2010 Moore reports that he cannot pay the account until the early next year. He agrees to exchange the account for a 120-day, 12% note receivable.12/31/2010 Prepared the adjusting journal entry to record accrued interest on the note.03/15/2011 Linwood receives a check from Moore for the maturity value (with interest) of the note.03/22/2011 Linwood receives notification that Moore’s check is being returned for nonsufficient funds (NSF).12/31/2011 Linwood writes off Moore’s account as uncollectible.Prepared Linwood Co.‘s journal entries to record the above transactions.The company uses the allowance method to account for its bad debt expenses.Answer:Oct.1, 2010 Accounts receivable—Moore……………………………..12 000Sales……………………………………………………………..12 000 Nov.15, 2010 Notes receivable……………………………………………12 000Accounts receivable—Moore........................................12 000 Dec.31,2010 Interest receivable (184)Interest revenue (184)($12 000 x 0.12 x 46/360 = $184)Mar.15, 2011 Cash…………………………………………………………..12 480Notes receivable………………………………………………...12 000Interest receivable (184)Interest earned (296)($12 000 x 0.12 x 74/360 = $296)Mar.22, 2011 Accounts receivable—Moore……………………………….12 480Cash…………………………………………………………….12 480 Dec.31, 2011 Allowance for doubtful accounts……………………………12 480Accounts receivable—Moore…………………………………12 4803. (a) A company purchased a patent on January 1, 2006, for $2 500 000. The patent’slegal life is 20 years but the company estimates that the patent’s useful life will only be5 years from the date of acquisition. On June 30, 2006, the company paid legal costsof $162 000 in successfully defending the patent in an infringement suit. Prepare the journal entry to amortize the patent at year end on December 31, 2006.(b) Suxia Company purchased a franchise from Yanyan Food Company for $400 000on January 1, 2006. The franchise is for an indefinite time period and gives Suxia Company the exclusive rights to sell Yanyan Wings in a particular territory. Prepare the journal entry to record the acquisition of the franchise and any necessary adjusting entry at year end on December 31, 2006.(c) Chenghe Company incurred research and development costs of $500 000 in 2006in developing a new product. Prepare the necessary journal entries during 2006 to record these events and any adjustments at year end on December 31, 2006.Answer:JOURNAL ENTRIES(a) December 31, 20×6Amortization Expense …………………………………………..518 000Patent………………………………………………………………… 518 000 (To record patent amortization.)$2 500 000 ÷ 5 years ……………………..$500 000$162 000 ÷ 54 months = …………………….$3 000$3 000×6……………………………………. $18 000$518 000(b) January 1, 20×6Franchise ………………………………………………………..400 000Cash………………………………………………………………. 400 000(To record acquisition of T astee Food franchise.)December 31, 20×6No amortization of the franchise is required since its life is indefinite.(c) 20×6Research and Development Expense……………………….. 500 000Cash………………………………………………………………. 500 000 (To record research and development expense for the Current year.)December 31—no entry.4. Suxia Company had the following transactions pertaining to short-term investments inequity securities.Jan.1 Purchased 900 shares of Chenghe Company stock for $9 450 cash plus brokerage fees of $ 270June.1 Received cash dividends of $0.50 per share on Chenghe Company stock.Sept.15 Sold 400 shares of Chenghe Company stock for $ 4 300 less brokerage fees of $100Dec.1 Received cash dividends of $0.50 per share on Chenghe Company stock.(a) Journalize the transactions.(b) Indicate the income statement effects of the transactions.Answer:(a) Jan. 1 Stock Investments……………………………………….. 9 720Cash..................................................................... 9 720 June 1 Cash (900 × $0.50) .. (450)Dividend Revenue (450)Sept. 15 Cash ($4 300 – $100)…………………………………. 4 200Loss on Sale of Stock Investments (120)Stock Investments (400 × ($9 720 ÷ 900)) ......................4 320 Dec. 1 Cash (500 × $0.50). (250)Dividend Revenue (250)(b) Dividend Revenue is reported under Other Revenues and Gains on theincome statement. Loss on Sale of Stock Investments is reported under Other Expenses and Losses on the income statement.5. Presented below are the three independent situations:(a) Henry Corporation purchased $ 400 000 of its bonds on June 30, 2005 at 102 andimmediately retired them. The carrying value of the bonds on the retirement date was $ 367 200. The bonds pay semiannual interest and the interest payment due on June 30, 2005 has been made and recorded.(b) Rose, Inc., purchased $600 000 of its bonds at 96 on June 30, 2005 andimmediately retired them. The carrying value of the bonds on the retirement date was $ 590 000. The bonds pay semiannual interest and the interest payment due on June 30, 2005 has been made and recorded.(c) Sealy Company has $200 000, 10%, 12-year convertible bonds outstanding.These bonds were sold at face value and pay semiannual interest on June 30 and December 31 of each year. The bonds are convertible into 80 shares of Sealy $ 5 par value common stock for each $ 1 000 par value bond. On December 31, 2005 after the bond interest has been paid, $ 50 000 par value of bonds were converted.The market value of Sealy’s common stock was $ 48 per share on December 31, 2005.Instruction: For each of the independent situations, prepare the journal entry to record the retirement or conversion of the bonds.Answer:(a) June 30 Bonds Payable……………………………………………. 400 000Loss on Bond Redemption……………………………….. 40 800Discount on Bonds Payable ………………………………………...32 800Cash …………………………………………………………………408 000($400 000 – $367 200 = $32 800)($400 000 × 102% = $408 000)(b) June 30 Bonds Payable……………………………………………. 600 000Discount on Bonds Payable………………………………………... 10 000Gain on Bond Redemption ………………………………………….14 000Cash………………………………………………………………… 576 000($600 000 – $590 000 =$10 000)($600 000 × 96% =$576 000)(c) Dec. 31 Bonds Payable………………………………………………. 50 000Common Stock…………………………………………………….. 20 000Paid-in Capital in Excess of Par …………………………………..30 000($5 × 80 × 50 =$20 000)6. Maia’s Bike Shop uses the perpetual inventory system and had the followingtransactions during the month of May:May 3 Sold merchandise to a customer on credit for $ 600, terms 2/10, n/30. The cost of the merchandise sold was $ 350.May 4 Sold merchandise to a customer for cash of $ 425. The cost of themerchandise was $ 250.May 6 Sold merchandise to a customer on credit for $ 1 300, terms 2/10, n/30. The cost of the merchandise sold was $ 750.May 8 The customer from May 3 returned merchandise with a selling price of $ 100.The cost of the merchandise returned was $ 55.May 15 The customer from May 6 paid the full amount due, less any appropriate discounts earned.May 31 The customer from May 3 paid the full amount due, less any appropriate discounts earned.Prepare the required journal entries that Maia’s Bike Shop must make to record these transactions.。

会计专业英语-Chapter4 Inventory and cost of goods sold

Chapter4 Inventory and cost of goods sold SpotlightDanny opened a supermarket named Happy Mall. There are variety kinds of inventories in the supermarket. The merchandise inventory is Happy Mall’s largest asset while the cost of goods sold is the largest expense. How to manage these inventories is the most important issue for the company. However, the cost of the purchase of each batch may be different. The different cost of goods sold may lead to different net income. So how to measure the cost of the inventory sold? How to measure the ending inventory?The management of inventory has significant impact to an entity, especially commercial enterprise. Reasonable inventory management can help the enterprise to calculate the profit and report the assets correctly. Through the control of the inventory, the enterprise can achieve the ultimate goal of inventory management-Improvement of economic benefit.Text1 Classifications of inventoryInventories are also called merchandise inventories. Inventories can include any of the followings:•Finished Goods product•Work in progress being produced•Materials•Purchased goods2 Inventory and cost of goods soldExhibit 4-1Financial statement Account StatusBalance sheet Inventory On handIncome statement Cost of goods sold Sold3 Gross profitFor merchandising firms, an initial step in assessing profitability is gross profit. Gross profit, also called gross margin, is the excess of sales revenue over cost of goods sold. It is the difference between sales revenues and the cost of goods sold.Gross profit= Sales revenue-cost of goods sold4 Accounting for inventoryThere are 2 main types of inventory accounting systems:•Periodic inventory system•Perpetual inventory system4.1 Periodic inventory systemThis system in which the cost of goods sold is computed periodically by relying solely on physical counts without keeping day-to-day records of units sold or on hand.The periodic inventory system does not involve a day-to-day record of inventories or of the cost of goods sold. Instead we compute the cost of goods sold and an updated inventory balance only at the end of an accounting period, when we take a physical count of inventory.Beginning balance+ Newly purchase-Cost of goods sold=Ending balanceCost of goods sold=Beginning balance+ Newly purchase-Ending balanceExhibit 4-2Goods available for sale -Inventory left over = Cost of goods sold 4.2 Perpetual inventory systemIt is a system that keeps a running, continuous record that tracks inventories and the cost of goods sold on a day-to-day basis. The daily record helps managers control inventory levels and prepare interim financial statements. In addition to this continuous record-keeping process, companies periodically physically count and value the inventory.No matter which method a company choose to manage its inventory, it should conduct a physical count at least once a year to check on the accuracy of the continuous record.Journal entry:①Inventory is purchased:Dr: Inventory. . . . . . . . . . . . . . . . . . . . .. . . . . . . . . .XXXCr: Cash. . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . XXX②Inventory is soldDr: Cash. . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . XXXCr: Sales revenue. . . . . . . . . . . . . . . . . . . . .. . . . .XXXDr: Cost of goods sold. . . . . . . . . . . . . . . . . . . . .. .XXXCr: Inventory. . . . . . . . . . . . . . . . . . . . .. . . . . . . . .XXX5 The various inventory costing methodThere is a challenge to recognize the cost of goods sold. Because the unit price is different every time when purchase inventory.There are four accepted inventory method•Specific identification method•Average cost method•First-in, first out•Last in, first out5.1 Specific identification methodIt is also called specific identification method. Specific identification method concentrates on physically linking the particular items sold with the cost of goods sold that we report. Business cost their inventories at the specific cost of the particular unit. This method is relatively easy to use for expensive, low volume。

会计英语第四版参考答案

会计英语第四版参考答案Chapter 1: Introduction to Accounting1. What is accounting?- Accounting is the systematic recording, summarizing, and reporting of financial transactions and events of a business entity.2. What are the main functions of accounting?- The main functions of accounting are to providefinancial information for decision-making, ensure compliance with laws and regulations, and facilitate the management of a business.3. What are the two main branches of accounting?- The two main branches of accounting are financial accounting and management accounting.4. What is the purpose of financial accounting?- The purpose of financial accounting is to provide an accurate and fair representation of an entity's financial position and performance to external users.5. What is the double-entry bookkeeping system?- The double-entry bookkeeping system is a method of recording financial transactions in which every transactionis recorded twice, once as a debit and once as a credit, to maintain the equality of the accounting equation.Chapter 2: Accounting Concepts and Principles1. What are the fundamental accounting concepts?- The fundamental accounting concepts include the accrual basis of accounting, going concern, consistency, and materiality.2. What is the accrual basis of accounting?- The accrual basis of accounting records transactions when they occur, regardless of when cash is received or paid.3. What is the going concern assumption?- The going concern assumption is the premise that a business will continue to operate for the foreseeable future.4. What is the principle of consistency?- The principle of consistency requires that an entity should apply accounting policies consistently over time.5. What is the principle of materiality?- The principle of materiality states that only items that could potentially affect the decisions of users of financial statements are included in the financial statements.Chapter 3: The Accounting Equation and Financial Statements1. What is the accounting equation?- The accounting equation is Assets = Liabilities +Owner's Equity.2. What are the four main financial statements?- The four main financial statements are the balance sheet, income statement, statement of changes in equity, and cashflow statement.3. What is the purpose of the balance sheet?- The balance sheet provides a snapshot of an entity's financial position at a specific point in time.4. What is the purpose of the income statement?- The income statement reports the revenues, expenses, and net income of an entity over a period of time.5. What is the purpose of the cash flow statement?- The cash flow statement reports the cash inflows and outflows of an entity over a period of time.Chapter 4: Recording Transactions1. What is a journal entry?- A journal entry is the initial recording of atransaction in the general journal.2. What are the steps in the accounting cycle?- The steps in the accounting cycle are analyzing transactions, journalizing, posting, preparing a trial balance, adjusting entries, preparing financial statements, and closing entries.3. What is the difference between a debit and a credit?- A debit is an increase in assets or a decrease inliabilities or equity, while a credit is an increase in liabilities or equity or a decrease in assets.4. What are adjusting entries?- Adjusting entries are made at the end of an accounting period to ensure that revenues and expenses are recorded in the correct period.5. What is the purpose of closing entries?- Closing entries are made to transfer the balances of temporary accounts to the owner's equity account and to prepare the accounts for the next accounting period.Chapter 5: Accounting for Merchandising Businesses1. What is a merchandise inventory?- A merchandise inventory is the stock of goods held by a business for sale to customers.2. What is the cost of goods sold?- The cost of goods sold is the direct cost of producing the merchandise sold during an accounting period.3. What is the gross profit?- The gross profit is the difference between the sales revenue and the cost of goods sold.4. What is the difference between a perpetual and a periodic inventory system?- A perpetual inventory system updates inventory records in real-time with each sale or purchase, while a periodicinventory system updates inventory records at specific intervals, such as at the end of an accounting period.5. What is the retail method of inventory pricing?- The retail method of inventory pricing is a method of estimating the cost of ending inventory by applying a cost-to-retail ratio to the retail value of the inventory.Chapter 6: Accounting for Service Businesses1. What are the main differences in accounting for service businesses compared to merchandise businesses?- Service businesses do not have inventory and their primary expenses are typically labor and overhead costs.2. What is the main source of revenue for service businesses? - The main source of revenue for service businesses is the fees charged for the services provided.3. What are the typical expenses。

会计英语,第四章

C4 - 14

Advantages of Using Periodic Inventory

• The accounting records for inventory and

cost of goods sold are updated only at the end of the accounting period (month, year, etc.). • Thus, in the middle of the period, there is no record that shows how much inventory is on hand or how much has been sold (COGS). • This is an easy, inexpensive method.

C4 - 10

COGS Schedule

Assume that each unit cost $6

Units

Beg. Inventory + Purchases = Goods Available - End. Inventory = Cost of Goods Sold 3 8 11 5 6

Cost

C4 - 12

4-2 Two inventory systems

P110

• Two main systems for keeping merchandise inventory records:

–Perpetual inventory system - a system that keeps a running, continuous record that tracks inventories and the cost of goods sold on a day-to-day basis –Periodic inventory system - a system in which the cost of good sold is computed periodically by relying solely on physical counts without keeping day-to-day records of units sold or on hand.

《会计英语》Accounting04解读

4

Coins (硬币)

currency (纸币)

Cash is defined as any deposit banks will accept.

Checks

Money orders (汇票)

A cash equivalent is an investment that is readily convertible to a known amount of cash and is sufficiently close to its maturity date so that its market value is relatively insensitive to interest rate changes. 现金等价物是指企业持有至到期,容易兑换成确定金额的现 金,并且市场价值不随利率的变化有较大波动的一项投资。

June 15, 200x Petty Cash 250 Cash To open the petty cash fund

250

13

Example of Petty Cash Payments

• Jose is the petty cash custodian responsible for the fund. • On June 20, he purchased supplies in the amount of $70. • For each disbursement, he prepares a petty cash ticket. • At all times the amount of cash in the petty cash fund plus the petty cash tickets must equal $250.

会计英语PPT(完成版) Chapter 4-The Accounting Cycle

5

of

11

Posting to the General Ledger

The last step is to insert the ledger account number in the Posting Reference column (POST REF.) of the journal.

The last two steps both serve as a cross-reference, which enables us to trace a transaction from the journal to the ledger or from the ledger to the journal quickly. After the process of posting to the general ledger, the journal and the ledger should contain the same information

The accounting cycle usually can be divided into the following steps: ① analyzing transactions from source documents; ② posting journal entries to ledger accounts; ③ preparing a trial balance; ④ completing a work sheet; ⑤ preparing financial statements.

6

of

11Trial Balan来自eThe trial balance is a two- column schedule listing the names and balances of all the accounts appearing in the ledger with the purpose of verifying clerical accuracy and preparing financial statements. The debit balances are listed in the left-hand column and the credit balances in the right-hand column. Because the amounts of debits and credits are equal, the sum of all the debits in the ledger must be the same as the sum of all the credits.

实用会计英语unit4简明教程PPT课件

4-2

实用会计英语 / Practical Accounting English

Guidance 学习指导

Contents

04

【Unit 04】

Accounting for Manufacturing Business

1 2 3

4-3

【 LESSON 】

MANUFACTURING BUSINESS AND ITS OPERATING CYCLE

MODULE 1

A. Reading material

1. Operation cycle of a manufacturing business The major operational activities of manufacturing businesses are purchase, manufacturing and sale of products. Examples of manufacturing business include General Motors produces automobiles, Nike produces Athletic shoes, Coca-cola produces beverages and Sony produces stereos, televisions and radios, etc. Most of the accounting procedure discussed in previous lessons applies equally to manufacturing business.

1. 制造企业的经营活动 制造业企业的主要经营 活动包括采购、生产和销售 产品。前面课程中所讲到的 大部分内容对制造业的会计 核算都适用。4ຫໍສະໝຸດ 7MODULE 2 手不释卷

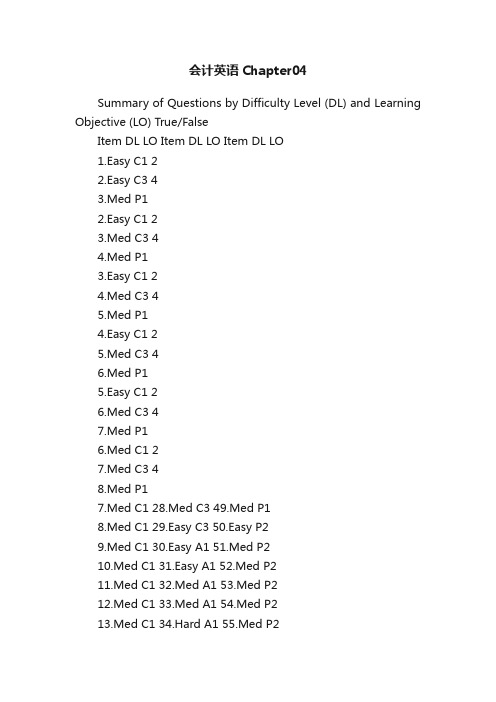

会计英语Chapter04

会计英语Chapter04Summary of Questions by Difficulty Level (DL) and Learning Objective (LO) True/FalseItem DL LO Item DL LO Item DL LO1.Easy C1 22.Easy C3 43.Med P12.Easy C1 23.Med C3 44.Med P13.Easy C1 24.Med C3 45.Med P14.Easy C1 25.Med C3 46.Med P15.Easy C1 26.Med C3 47.Med P16.Med C1 27.Med C3 48.Med P17.Med C1 28.Med C3 49.Med P18.Med C1 29.Easy C3 50.Easy P29.Med C1 30.Easy A1 51.Med P210.Med C1 31.Easy A1 52.Med P211.Med C1 32.Med A1 53.Med P212.Med C1 33.Med A1 54.Med P213.Med C1 34.Hard A1 55.Med P214.Hard C1 35.Easy P1 56.Med P215.Easy C2 36.Easy P1 57.Hard P216.Easy C2 37.Easy P1 58.Hard P217.Med C2 38.Easy P1 59.Easy P318.Hard C2 39.Easy P1 60.Easy P319.Easy C3 40.Med P1 61.Med P320.Easy C3 41.Med P1 62.Easy P421.Easy C3 42.Med P1 63.Easy P4Multiple ChoiceItem DL LO Item DL LO Item DL LO64.Easy C1 81. Hard A1 98. Med P265.Easy C1 82. Easy P1 99. Med P266.Med C1 83. Med P1 100. Med P267.Med C1 84. Med P1 101. Med P268.Med C1 85. Med P1 102. Hard P269.Med C1 86. Med P1 103. Med P270.Med C1 87. Med P1 104. Hard P271.Med C1 88. Med P1 105. Hard P272.Med C1 89. Med P1 106. Hard P273.Med C2 90. Med P1 107. Med P374.Med C2 91. Med P1 108. Med P375.Easy C3 92. Med P1 109. Med P376.Easy C3 93. Med P1 110. Med P377.Med C3 94. Hard P1 111. Med P478.Med C3 95. Med P2 112. Med P479.Med C3 96. Med P2 113. Med P480.Med A1 97. Med P2 114. Med P4MatchingItem DL LO Item DL LO Item DL LO 115. Med C1,C2 116. Med C1-C3 117. Med C3 P1-P3 A1Short EssayItem DL LO Item DL LO Item DL LO 118. Med C1 122. Med A1 126. Med P2 119. Med C1 123. Med P1 127. Med P3 120. Med C2 124. Hard P1 128. Hard P4 121. Med C3 125. Med P2 ProblemsItem DL LO Item DL LO Item DL LO 129. Med C1 136. Hard P1 143. Med P2 130. Med C1 137. Hard P1 144. Hard P2,P3 131. Med C2 138. Hard P1 145. Hard P2,P3 132. Hard C3 139. Easy P2 146. Easy P4 133. Hard C3,A1 140. Med P2 147. Med P4 134. Med A1 141. Med P2135. Med P1 142. Med P2Completion ProblemsItem DL LO Item DL LO Item DL LO 148. Easy C1 152. Easy C2 156. Easy P1 149. Easy C1 153. Med C3 157. Med P3 150. Easy C1 154. Med C3 158. Hard P4 151. Easy C1 155. Med A1 ProblemsItem DL LO Item DL LO Item DL LO 159. Hard P1 161. Hard C3, A1 163. Hard P4 160. Hard C3 162. Hard P4True / False Questions1. Accounts that appear in the balance sheet are often called temporary (nominal) accounts. FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C12. Income Summary is a temporary account only used for the closing process.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C13. Revenue accounts should begin each accounting period with zero balances.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C14. Closing revenue and expense accounts at the end of the accounting period serves to make the revenue and expense accounts ready for use in the next period.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C15. The closing process takes place after financial statements have been prepared.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C16. Revenue and expense accounts are permanent (real)accounts and should not be closed at the end of the accounting period.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C17. Closing entries result in revenues and expenses being reflected in the owner's capital account.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C18. The closing process is a step in the accounting cycle that prepares accounts for the next accounting period.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C19. The closing process is a two-step process. First revenue, expense, and withdrawals are set toa zero balance. Second, the process summarizes a period's assets and expenses.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C110. Closing entries are required at the end of each accounting period to close all ledger accounts.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C111. Closing entries are designed to transfer the end-of-period balances in the revenue accounts, the expense accounts, and the withdrawals account to owner's capital.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C112. The Income Summary account is a permanent account that will be carried forward period after period.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C113. Closing entries are necessary so that owner's capital willbegin each period with a zero balance.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C114. Permanent accounts carry their balances into the next accounting period. Moreover, asset, liability and revenue accounts are not closed as long as a company continues in business. FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: HardLearning Objective: C115. The first step in the accounting cycle is to analyze transactions and events to prepare for journalizing.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C216. The accounting cycle refers to the sequence of steps in preparing the work sheet. FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: C217. The first five steps in the accounting cycle include analyzing transactions, journalizing, posting, preparing an unadjusted trial balance, and recording adjusting entries.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: C218. The last four steps in the accounting cycle include preparing the adjusted trial balance, preparing financial statements and recording closing and adjusting entries.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: HardLearning Objective: C219. A classified balance sheet organizes assets and liabilities into important subgroups that provide more information to decision makers.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: EasyLearning Objective: C320. An unclassified balance sheet provides more information to users than a classified balance sheet.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: EasyLearning Objective: C321. Current assets and current liabilities are expected to be used up or come due within one year or the company's operating cycle whichever is longer.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: EasyLearning Objective: C322. Intangible assets are long-term resources that benefit business operations that usually lack physical form and have uncertain benefits.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: EasyLearning Objective: C323. Assets are often classified into current assets, long-term investments, plant assets, and intangible assets.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: C324. Current liabilities are cash and other resources that are expected to be sold, collected or used within one year or the company's operating cycle whichever is longer.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: C325. Long-term investments can include land held for future expansion.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: C326. Plant assets and intangible assets are usually long-term assets used to produce or sell products and services.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: C327. Current liabilities include accounts receivable, unearned revenues, and salaries payable. FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: C328. Cash and office supplies are both classified as current assets.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: C329. Plant assets are also called fixed assets or property, plant, and equipment.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: EasyLearning Objective: C330. The current ratio is used to help assess a company's ability to pay its debts in the near future.TRUEAACSB: AnalyticAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: EasyLearning Objective: A131. The current ratio is computed by dividing current liabilities by current assets.FALSEAACSB: AnalyticAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: EasyLearning Objective: A132. Harley-Davidson's current assets are $400 million and its current liabilities are $250 million. Its current ratio is 0.63.FALSE$400/$250 = 1.6AACSB: AnalyticAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: MediumLearning Objective: A133. A company has current assets of $15,000 and current liabilities of $9,500. Its current ratio is 1.6TRUE$15,000/$9,500 = 1.6AACSB: AnalyticAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: MediumLearning Objective: A134. Harley-Davidson's current ratio is 1.3. The industry average for the current ratio is 1.2. This indicates that Harley-Davidson can cover its short term liabilities with its short term assets. TRUEAACSB: AnalyticAICPA BB: IndustryAICPA FN: Risk AnalysisDifficulty: HardLearning Objective: A135. A work sheet is a tool to help bring together information needed in adjusting the accounts and preparing the financial statements.TRUEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: EasyLearning Objective: P136. Adjustments must be entered in the journal and posted to the ledger after the work sheet is prepared.TRUEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: EasyLearning Objective: P137. The work sheet is a book of original entry used to record transactions and events as they occur.FALSEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: EasyLearning Objective: P138. The work sheet is a required financial statement.FALSEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: EasyLearning Objective: P139. A work sheet is a substitute for the set of financial statements.FALSEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: EasyLearning Objective: P140. All necessary numbers to prepare the income statement can be taken from the income statement columns of the work sheet, including the net income or net loss.TRUEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P141. On a work sheet, a loss is indicated if the total of the Income Statement Debit column exceeds the total of the Income Statement Credit column.TRUEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P142. If all columns balance upon completion of a work sheet, you can be sure that no errors were made in preparing the work sheet.FALSEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P143. Closing entries are normally entered in the general journal and then posted to the work sheet.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P144. Adjusting entries are normally entered in the general journal before they are posted to the work sheet.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P145. On a work sheet, the adjusted balances of revenues and expenses are sorted to the Income Statement columns of the work sheet.TRUEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P146. On the work sheet, net income is entered in the Income Statement Credit column as well as the Balance Sheet or Statement of Owner's Equity Debit column.FALSEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P147. All necessary numbers to prepare the balance sheet can be found in the balance sheet columns of the work sheet including ending owner's capital.FALSEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P148. A worksheet can be helpful in showing the effects of proposed or "what if" transactions, as well as being useful in helping to prepare end-of-period financial statements.TRUEAACSB: TechnologyAICPA BB: IndustryAICPA FN: Leveraging TechnologyDifficulty: MediumLearning Objective: P149. Since it is an important financial statement, the trial balance must be prepared according to specified accounting procedures.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: ReportingDifficulty: MediumLearning Objective: P150. An expense account is normally closed by debiting Income Summary and crediting the expense account.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: P251. The withdrawals account is normally closed by debiting it.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P252. After posting the entries to close all revenue accounts and all expense accounts, the Income Summary account of Waif Services has a $4,000 debit balance. This result implies that WaifServices earned a net income of $4,000.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P253. After posting the entries to close all revenue and expense accounts, Hatfield Company's Income Summary account has a credit balance of $6,000, and its Hatfield, Withdrawals account has a debit balance of $2,500. These balances indicate that net income for the current accounting period amounted to $3,500.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P254. The Income Summary account is closed to the owner's capital account.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P255. When expenses exceed revenues, there is a net loss and the Income Summary account would have a credit balance.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P256. The Income Summary account is used to close the permanent accounts at the end of an accounting period.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P257. The steps in the closing process are (1) close credit balances in revenue accounts to Income Summary; (2) close credit balances in expense accounts to Income Summary; (3) close Income Summary to Owner's Capital; (4) close Withdrawals to Owner's Capital.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: HardLearning Objective: P258. The usual third closing entry is to close Owner's Capital to the Owner's Withdrawals account.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: HardLearning Objective: P259. A post-closing trial balance is a list of permanent accounts and their balances from the ledger after all closing entries are journalized and posted.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: P360. The aim of a post-closing trial balance is to verify that (1) total debits equal total credits for temporary accounts, and (2) all temporary accounts have zero balances.FALSEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: P361. A company's post-closing trial balance has a debit total of $40,350 and a credit total of $40,650. Accordingly, the company should review for errors in the closing process.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: MediumLearning Objective: P362. Reversing entries are optional.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: P463. Reversing entries adjust the accrued assets and accrued liabilities that were created by adjusting entries at the end of the prior accounting period.TRUEAACSB: CommunicationsAICPA BB: IndustryAICPA FN: Decision MakingDifficulty: EasyLearning Objective: P4。

会计专业英语课件Chapter 4

(1) Acquisition

▪ Classified as measured at FVTOCI, an investment in debt or equity instruments is recorded at its cost at initial recognition, including the purchase price and transaction costs that are directly attributable to the acquisition of the financial asset.

【Example 4-3】

▪ Take the bonds purchased by company W on June 30, 2019 for illustration. Assume that company W classified these bonds at FVTOCI. On December 31, 2019, the quoted market price of the bonds was $1,030,000. On acquisition, company W should make the following entry:

• Only investments in debt, such as bonds, satisfy the recognition requirements for financial instruments measured at amortized cost since investments in stocks do not produce interest or refund the principal.

• is prepared to amortize bond discount or premium for each interest receipt.

会计实用英语

会计实用英语第一篇:会计实用英语account current 往来帐account form of balance sheet 帐户式资产负债表account form of profit and loss statement 帐户式损益表account payable 应付帐款account receivable 应收帐款account of payments 支出表account of receipts 收入表account title 帐户名称,会计科目accounting year 或financial year 会计年度accounts payable ledger 应付款分类帐Accounting period(会计期间)are related to specifictime periods ,typically one year(通常是一年)资产负债表:balance sheet 可以不大写b利润表: income statements(or statements of income)利润分配表:retained earnings现金流量表:cash flowsAccounting system 会计系统American Accounting Association 美国会计协会American Institute of CPAs 美国注册会计师协会Audit 审计Balance sheet 资产负债表Bookkeepking 簿记Cash flow prospects 现金流量预测Certificate in Internal Auditing 内部审计证书Certificate in Management Accounting 管理会计证书Certificate Public Accountant注册会计师Cost accounting 成本会计External users 外部使用者Financial accounting 财务会计Financial Accounting Standards Board 财务会计准则委员会Financial forecast 财务预测Generally accepted accounting principles 公认会计原则General-purpose information 通用目的信息Government Accounting Office 政府会计办公室accountant genaral 会计主任 account balancde 结平的帐户 account bill 帐单account books 帐account classification 帐户分类Income statement 损益表 Institute of Internal Auditors 内部审计师协会Institute of Management Accountants 管理会计师协会Integrity 整合性Internal auditing 内部审计Internal control structure 内部控制结构Internal Revenue Service 国内收入署Internal users 内部使用者Management accounting 管理会计Return of investment 投资回报Return on investment 投资报酬Securities and Exchange Commission 证券交易委员会 Statement of cash flow 现金流量表 Statement of financial position 财务状况表Tax accounting 税务会计Accounting equation 会计等式Articulation 勾稽关系 Assets 资产 Business entity 企业个体 Capital stock 股本 Corporation 公司 Cost principle 成本原则 Creditor 债权人Deflation 通货紧缩Disclosure 批露Expenses 费用Financial statement 财务报表Financial activities 筹资活动Going-concern assumption 持续经营假设 Inflation 通货膨涨 Investing activities 投资活动Liabilities 负债Negative cash flow 负现金流量 Operating activities 经营活动 Owner's equity 所有者权益 Partnership 合伙企业Positive cash flow 正现金流量Retained earning 留存利润Revenue 收入Sole proprietorship 独资企业Solvency 清偿能力Stable-dollar assumption 稳定货币假设 Stockholders 股东Stockholders' equity 股东权益Window dressing 门面粉饰Account 帐第二篇:会计常用英语现金 Cash in hand银行存款 Cash in bank其他货币资金-外埠存款Other monetary assetscashier‘s check其他货币资金-银行汇票 Other monetary assetscredit cards 其他货币资金-信用证保证金Other monetary assetscash for investment短期投资-股票投资 Investmentsstocks短期投资-债券投资 Investmentsbonds短期投资-基金投资 Investmentsfunds短期投资-其他投资 Investmentsothers短期投资跌价准备 Provision for short-term investment长期股权投资-股票投资 Long term equity investmentothers长期债券投资-债券投资 Long term securities investemntothers长期投资减值准备 Provision for long-term investment应收票据 Notes receivable应收股利 Dividends receivable应收利息 Interest receivable应收帐款 Trade debtors坏帐准备-应收帐款 Provision for doubtful debtsother debtors 其他流动资产 Other current assets物资采购 Purchase原材料 Raw materials包装物 Packing materials低值易耗品 Low value consumbles材料成本差异 Material cost difference自制半成品 Self-manufactured goods库存商品 Finished goods商品进销差价Difference between purchase & sales of commodities委托加工物资 Consigned processiong material 委托代销商品 Consignment-out受托代销商品 Consignment-in分期收款发出商品 Goods on instalment sales存货跌价准备 Provision for obsolete stocks待摊费用 Prepaid expenses待处理流动资产损益 Unsettled G/L on current assets待处理固定资产损益 Unsettled G/L on fixed assets委托贷款-本金 Consignment loaninterest委托贷款-减值准备 Consignment loanBuildings固定资产-机器设备Fixed assetsElectronic Equipment, furniture and fixtures固定资产-运输设备Fixed assetsspecific materials工程物资-专用设备 Project materialprepaid for equipment工程物资-为生产准备的工具及器具 Project materialpatent无形资产-非专利技术 Intangible assetstrademark rights无形资产-土地使用权 Intangible assetsgoodwill无形资产减值准备 Impairment of intangible assets长期待摊费用 Deferred assets未确认融资费用 Unrecognized finance fees其他长期资产 Other long term assets递延税款借项 Deferred assets debits应付票据 Notes payable应付帐款 Trade creditors预收帐款 Adanvances from customers代销商品款 Consignment-in payables其他应交款 Other payable to government其他应付款 Other creditors应付股利 Proposed dividends待转资产价值 Donated assets预计负债 Accrued liabilities应付短期债券 Short-term debentures payable其他流动负债 Other current liabilities预提费用 Accrued expenses应付工资 Payroll payable应付福利费 Welfare payable短期借款-抵押借款 Bank loanspledged短期借款-信用借款 Bank loanscredit短期借款-担保借款 Bank loansguaranteed一年内到期长期借款 Long term loans due within one year一年内到期长期应付款 Long term payable due within one year 长期借款 Bank loansPar value应付债券-债券溢价 Bond payableDiscount应付债券-应计利息 Bond payableincome tax应交税金-增值税 Tax payablebusiness tax应交税金-消费税 Tax payableothers递延税款贷项 Deferred taxation credit股本 Share capital已归还投资 Investment returned利润分配-其他转入Profit appropriationstatutory surplus reserve利润分配-提取法定公益金 Profit appropriationreserve fund利润分配-提取企业发展基金Profit appropriationstaff bonus and welfare fund利润分配-利润归还投资Profit appropriationpreference shares dividends利润分配-提取任意盈余公积Profit appropriationordinary shares dividends利润分配-转作股本的普通股股利Profit appropriationshare premium资本公积-接受捐赠非现金资产准备Capital surpluscash donation资本公积-股权投资准备 Capital surplussubsidiary资本公积-外币资本折算差额 Capital surplusothers盈余公积-法定盈余公积金Surplus reserveother surplus reserve盈余公积-法定公益金 Surplus reservereserve fund盈余公积-企业发展基金Surplus reservereture investment by investment主营业务收入 Sales主营业务成本 Cost of sales主营业务税金及附加 Sales tax营业费用 Operating expenses管理费用 General and administrative expenses财务费用 Financial expenses投资收益 Investment income其他业务收入 Other operating income营业外收入 Non-operating income补贴收入 Subsidy income其他业务支出 Other operating expenses营业外支出 Non-operating expenses所得税 Income tax一、资产类 assets现金 cash on hand银行存款 cash in bank其他货币资金 other cash and cash equivalent短期投资 short-term investment短期投资跌价准备short-term investments falling price reserve应收票据 notes receivable应收股利 dividend receivable应收利息 interest receivable应收帐款 accounts receivable坏帐准备 bad debt reserve预付帐款 advance money应收补贴款 cover deficit receivable from state subsidize其他应收款 other notes receivable在途物资 materials in transit原材料 raw materials包装物 wrappage低值易耗品 low-value consumption goods库存商品 finished goods委托加工物资 work in process-outsourced委托代销商品trust to and sell the goods on a commission basis受托代销商品commissioned and sell the goods on a commission basis存货跌价准备 inventory falling price reserve 分期收款发出商品 collect money and send out the goods by stages待摊费用 deferred and prepaid expenses长期股权投资 long-term investment on stocks长期债权投资 long-term investment on bonds长期投资减值准备 long-term investment depreciation reserve 固定资产 fixed assets累计折旧 accumulated depreciation工程物资 project goods and material在建工程 project under construction固定资产清理 fixed assets disposal无形资产 intangible assets开办费 organization/preliminary expenses长期待摊费用 long-term deferred and prepaid expenses待处理财产损溢 wait deal assets loss or income二、负债类 debts短期借款 short-term loan应付票据 notes payable应付帐款 accounts payable预收帐款 advance payment代销商品款 consignor payable应付工资 accrued payroll应付福利费 accrued welfarism应付股利 dividends payable应交税金 tax payable其他应交款 accrued other payments 其他应付款 other payable预提费用 drawing expenses in advance 长期借款 long-term loan应付债券 debenture payable长期应付款 long-term payable递延税款 deferred tax住房周转金 revolving fund of house 三、所有者权益 owners equity股本 paid-up stock资本公积 capital reserve盈余公积 surplus reserve本年利润 current year profit利润分配 profit distribution四、成本类 cost生产成本 cost of manufacture制造费用 manufacturing overhead 五、损益类 profit and loss(p/l)主营业务收入 prime operating revenue 其他业务收入 other operating revenue 折扣与折让 discount and allowance投资收益 investment income补贴收入 subsidize revenue营业外收入 non-operating income主营业务成本 operating cost主营业务税金及附加tax and associate charge其他业务支出other operating expenses存货跌价损失 inventory falling price loss营业费用 operating expenses管理费用 general and administrative expenses财务费用 financial expenses营业外支出 non-operating expenditure所得税 income tax以前损益调整 adjusted p/l for prior year第三篇:会计英语求职信在外企上班用英语的求职信是不是会跟合适点呢?来看看如何写一篇好的英语求职信吧。

《实用会计英语》课件

积极互动

与同学和老师积极互动,主 动参与讨论和演练。

实用技能和应用

财务报表分析

学会分析财务报表,评估公司 的财务状况和经营绩效。

预算编制与监控ห้องสมุดไป่ตู้

掌握预算编制和监控的技巧, 有效管理公司的财务资源。

税务筹划

了解税务规定,为公司进行税 务筹划,合法降低税负。

总结和要点

掌握专业英语表达能力

熟悉会计领域的英语术语,流利地与国际同行交流。

深入了解会计知识

掌握财务报表分析、预算编制等核心会计技能。

应用于实际工作

将所学知识应用到实际会计工作中,提高工作效率。

《实用会计英语》PPT课 件

本课程将帮助您掌握实用会计英语的关键知识和技能,从而能够更好地应对 会计工作中的各种挑战。

课程目标

1 强化英语能力

提高对会计领域英语表 达的理解和运用能力。

2 丰富会计知识

深入学习会计相关的词 汇、概念和原则。

3 提升职场竞争力

使您能够流利地与国际 客户、同事和合作伙伴 沟通。

课程大纲

1. 会计基础知识 2. 财务报表的分析和解读 3. 预算和成本管理 4. 税务法规和会计准则

课程重点

1 会计术语

掌握会计领域的专业术语,如资产、负债、利润等。

2 财务报表

了解并学会分析、解读财务报表,如利润表、资产负债表等。

3 会计信息系统

学习使用会计软件和工具,提高工作效率。

课程难点

1 专业词汇

理解和运用会计领域的专业术语和词汇。

2 复杂概念

掌握财务会计和管理会计中的复杂概念和原则。

3 实际应用

将所学知识应用到实际会计工作中。

学习方法和技巧

会计英语实训教程(第四章)

10. money order

11. electronic funds transfer

落后,缓慢 快递 补充,补足 即时支付 汇票 电子资金转账

Section 1 Cash and Accounts Receivable

9

Part 2 Intensive Reading

Cash

New Words and Special Terms

Section 1 Cash and Accounts Receivable

4

Part 1 Workplace Spoken English

Follow the Samples

Dialogue 1

A:Lucy, perhaps you need to set up a petty cash fund. B:Why? A:All businesses should have a petty cash fund for small various purchases. B:How much should we keep in it? A:There should not be a lot of money kept in the petty cash and it should

Section 1 Cash and Accounts Receivable

8

会计英语ACCOUNTING

Assets =

$52,800

9. -$400(cash) Bal.$52,400

Liabilities + Owner’s Equity

$300

$52,500

-$400(expense)

$300

$52,100

10. John hasn’t paid the bill of utility expense of $300.

Kinds of assets:current assets, fixed assets and intangible assets.

Economic resources are referred to as assets and creditors’ equities are referred to as liabilities.

Cash Salaries Payable Accounts Receivable Johnson, Capital

Land Accounts Payable Supplies

Classroom exercises:

1. Identify the following transactions by type of owner’s equity transaction by marking each as either an owner’s investment (I), owner’s withdrawal (W), revenue (R), expense (E) or not an owner’s equity transaction (NOE).

performed.

Part 2 ILLUSTRATIVE TRANSACTIONS

Transactions

大学课程《会计英语》PPT课件:Chapter 4 Unit 2

Types of Receivables

To reflect important differences among receivables, they are frequently classified as accounts eivable, notes receivable, and other receivables.

Specify the key controls over accounts receivable.

Key Terms

Credit Policy 信用政策 Contra-asset Account 资产备抵账户,资产

抵消账户。 Valuation Account 计价对比账户 Credit Memo 贷项通知单。也写作credit

Two Methods for Uncollectible Accounts

(1) the direct write-off method (2) the allowance method

Recognizing Accounts Receivable

Initial recognition of accounts receivable is relatively straightforward. A service organization records a receivable when it provides service on account. A merchandiser records accounts receivable at the point of sale of merchandise on account. When a merchandiser sells goods, it increases both the Accounts Receivable and Sales accounts.

会计英语词汇

Chapter1Accounting 会计,会计学Accountant 会计师,会计人员Accounting information 会计信息Financial data 财务数据Business 企业,经营,商业,业务Business transaction 经济业务,经济交易Enterprise 企业Economic information 经济信息Business organization 经济组织Financial activity 财务活动,筹资活动Profitability 获利能力,盈利能力End product 最终产品Creditor 债权人Performance 业绩Favorable 有利的Unfavorable 不利的Accounting system 会计系统,会计制度Financial condition 财务状况Investor 投资人Result of operations 经营成果Financial report 财务报告To make decision 制定决策Accounting principles 会计原则Business activity 经济活动Accounting concepts 会计概念Financial accounting 财务会计Economic unit 经济单位Owner 业主,拥有者Governmental agency 政府机构Generally accepted accounting principles 公认会计原则Employ 采用Prepare 准备,编制Annual report 年度报告Stockholder 股东Audit 审计,审查,查帐Auditing 审计,审计学Accounting records 会计记录Public accountant 公共会计师Fairness 公正性,公允性Reliability 可靠性Periodic audit 定期审计Corporation 股份有限公司Internal auditor 内部审计人员Cost accounting 成本会计Cost data 成本数据Management accounting 管理会计Selling price 销售价格Management advisory service 管理咨询服务Management service 管理服务Tax accounting 税务会计Tax returns 纳税申报单,税单Budgetary accounting 预算会计International accounting 国际会计International trade 国际贸易Not-for-profit accounting 非盈利组织会计Not-for-profit organization 非盈利组织Social accounting 社会会计Measurement 计量Chapter2Accounting practice 会计实务Accounting theory 会计理论Decline 方针,指南Assumption 假设Business entity 经济主体Accounting entity 会计主体Economic activity 经济活动Bookkeeping 簿记Double-entry bookkeeping system 复试记账系统Entry分录,记录Single proprietorship独资Partnership合伙Accounting purpose会计目的Separate entity独立主体Asset资产Going-concern持续经营Historical cost历史成本Current market value 当前市场价值Accounting period会计期间Stable-monetary-unit货币计量单位Objective principle客观性原则Operating result经营成果Cost principle成本原则Actual cost实际成本Book value账面价值Equivalent当量,约当量Depreciation折旧Consistency principle一贯性原则Accounting method会计方法Financial statement 财务报告Comparability可比性Materiality principle重要性原则Conservatism principle谨慎性原则Revenue收入Expense费用Cost of goods商品成本Net income净收入Net loss净损失Accrual-basis 权责发生制Cash-basis 现金收付制Journal 日记账Realization principle 实现原则Matching principle 配比原则Recognize 确认Transfer转让,转帐,过户Income statement收益表,损益表Full-disclosure principle充分揭示原则Chapter3Accounting element会计要素Accounting equation会计等式Liability负债Owner s’ equity业主权益,所有者权益Current asset长期资产Long-term asset长期资产Operating cycle 经营周期Bank deposit 银行存款Short-term investment短期投资Long-term investment长期投资Accounts receivable应收账款Note receivable应收票据Prepayment 预付款项Inventory 存货Fixed asset 固定资产Plant and equipment 厂房和设备Intangible asset 无形资产Store fixtures店面装置Office equipment办公设备Delivery equipment运输设备Creditors’ equity债权人权益Obligation责任,义务Debt债务Current liability流动负债Long-term liability长期负债Short-time loans payable应付短期贷款Long-term loans payable长期应付贷款Notes payable应付票据Accounts payable应付账款Accrued expense应计费用Bonds payable应付债券Long-term accounting payable长期应付账款Interest 股份,利息Claim 要求权Net assets 净资产Capital资本Stockholder’s equity 股东权益Cost of goods sold 商品销售成本Administrative expenses 管理费用Selling expenses销售费用Financial expense 财务费用Occur 发生Dividend payable 应付股利Retained earnings留存收益Chapter4Classification分类,分级Day-to-day 随时Account title 账户名称Ledger 分类帐Debit side 借方Credit side 贷方Charge借记,收取费用Memorandum 摘要,备忘录Insert 插入,嵌入,写入Cash on hand 库存现金subgrouping子目,细目supplies 物料用品prepaid expenses 预付费用face value 面值check 支票bank draft 银行汇票money order 汇款单debtor 债务人bearer 持票人salaries payable 应付工资taxes payable 应付税费interest payable 应付利息long-term notes payable 长期应付票据mortgage payable 应付抵押借款bonds payable 应付公司债券drawing提款income summary收益汇总professions fees职业服务费commissions revenues 佣金收入interest income利息收入chart of accounts账户一览表executive salaries主管人员薪金office salaries办公人员薪金sales salaries销售人员薪金prepaid rent预付租金accumulated depreciation累计折旧depreciation expense折旧费用sales销售收入sales returns and allowance销售退回与折让purchases returns and allowance购买退回与折让Chapter5Accounting cycle会计循环Accounting procedures会计程序,会计方法Trial balance试算平衡表Post-closing trial balance结算后试算平衡表Journalize 做分录,记账Post to the ledger过入分类帐Assemble汇集Work sheet工作底表Adjusting entry调整分录close结账,结清,关闭ledger accounts分类账户general ledger总分类帐two-column account两栏式账户source document原始凭证check stub支票存根journal日记帐journal entry日记帐分录records(book) of original entry原始记录簿transcribe抄录post过账,誊帐manually手工的chronological按时间顺序的enter登记,计入general journal普通日记账special journal特殊日记帐sales journal销售日记帐purchases journal购买日记帐cash receipts journal现金收入日记帐cash disbursements journal现金支出日记帐division of labor分工Chapter6Adjusting procedures调整程序Accrual(basis) accounting权责发生制Align调整,使成一线,(转做)使一致Apportion(按比例)分配,摊配Accrue自然积累(如利息等),计提Outlay支出Expire期满,耗尽,失效Insurance expense保险费用Prepaid insurance 预付保险费Supplies expense物料用品费Supplies on hand在用物料Subscription预订Deferred credit递延贷项Accrued salaries payable应计应付工薪Accrued revenue应计收入Closing entry结账分录Closing procedure结账程序Temporary account临时性账户,名义账户,虚账户Permanent account 永久性账户,实账户Withdrawals提款Statement of cash flow现金流量表Financial position财务状况Portray描绘Dispose处理Inflows流入Outflows流出Chapter7Working paper工作底稿Adjusted trial balance调整后试算平衡表Cross-reference交叉参考Occasion需要,机会,工作场合Salaries accrued应计薪金Combine结合,联合Extend(会计)将数字转入。

实用会计英语大全