cpa Canada FA3 第10章作业

国际会计第九版第十章答案

国际会计第九版第十章答案10-1交易日会计:(1)交易日:20x1年8月14日借:债券期货投资100,000贷:应付债券期货合同款100,000借:存出保证金10,000贷:银行存款10,000(2)8月30日借:存出保证金400贷:银行存款400借:债券期货投资4000贷:债券期货投资损益4000(3)结算日借:债券期货投资损益2000贷:债券期货投资2000借:应付债券期货合同款100,000财务费用(交易费)600银行存款11800贷:债券期货投资102,000存出保证金10,400结算日会计(1)交易日:8月14日借:存出保证金10,000贷:银行存款10,000(2)8月30日借:存出保证金400贷:银行存款400借:债券期货投资4000贷:债券期货投资损益4000(3)结算日借:债券期货投资损益2000贷:债券期货投资 2000借:财务费用 600银行存款 11800贷:债券期货投资 2000存出保证金 1040010—2会计分录:1(1)交易日借:股票期货期权投资应收款 40,000贷:股票期权投资 40,000借:股票期权投资期权费 2,000 贷:银行存款 2,000 (注意:这时的股票期权投资属于负债类的。

)(2)6月30日借:股票期权投资 4000贷:股票期权投资损益 4000(3)结算日借:股票期权投资 2000贷:股票期权投资期权费 2000借:股票期权投资 3400财务费用(交易费) 300银行存款 5700贷:股票期权投资应收款 40,0002 共获利:6000-2000-300=3700 美元3执行价值低于期权费时,将亏损4执行价值为负值时,选择不执行期权合同10—3(1)发行债券时借:银行存款 100,000贷:应付债券 100,000(2)计提1—6月份的债券利息和互换交易费借:财务费用—债券利息费用 2750贷:应付债券利息 2750 借:应计费用 250贷:互换交易费 250计提7—12月份的债券利息和互换交易费借:财务费用-债券利息费用 2400贷:应付债券利息 2400 借:互换交易费 100贷:应计费用 100(3)20x1年末支付利息和互换交易费借:应付债券利息 5150贷:银行存款 5000应计费用 15010—4(1)20x1年1月1日借;债券投资 20,000贷:银行存款 20.000(2)20x1年末借:债券投资 2,000贷:债券投资损益 2,000(3)20x2年1月1日借:出售债券远期合同应收款 22,000贷;出售远期合同 22,000(4)20x2年末被套期项目公允价值下降借:债券投资损益 1,000贷:债券投资 1,000套期工具跌价:借:出售债券远期合同 1,000贷;套期损益 1,00010—5(1)20x1年10月17日,未发生成本,采用结算日会计,故不作记录 20x1年12月31日:借:购入存货远期合同 600贷:递延套期损益 500远期合同损益 100(2)假设情况一发生借:递延套期损益 500贷:套期损益 500同时,等待机会,转手这项远期合同(3)假设情况二发生借:递延套期损益 80贷:购入存货远期合同 80借:递延套期损益 420银行存款 49700贷:购入存货远期合同 520销货收入 49600。

加拿大会计及证书详细介绍(CA和CPA,CMA的区别)

审计1(AU1)及案例2 (BC2):

该课程适用于所有内部和外部审计的原理和程序。其内容包括报告,专业标准和执业规范,法律责任,审计证据,计划编制与分析,内部控制等知识。

加拿大税1(TX1):

主要讲述加拿大税法基本原则。

财务会计4(FA4):

这是一门高级财务会计课程。将为学员提供以下六个专业领域的更深入的学习:加拿大及国际会计准则,会计方法,收入税的分配,长期联合投资,外汇兑换与外国业务的转让和合并以及非盈利公共部门会计。

以上是对于你在加拿大读会计的一些建议。如果你以后打算回国发展,尽管会计师资格很难通用,但是,如果你有在四大或者其他大企业(比如银行或者保险公司)的比较有价值的工作经历的话(如果能做到中层基本上就所向披靡了),回国找好工作基本上是没问题的。因为一般的会计师,在奋斗几年之后,都是转到企业里做高级财务或者给企业做咨询,只有少数是继续在事务所打拼做合伙人的(因为这条路太累了),做财务和咨询对于行驶签字权都不是必须的,所以并不一定需要你再考CICPA。

国际金融2(FN2):

这是一门有助于财务经理决策分析的高级金融学课程。内容主要包括不确定因素下资金预算,基金的长期资源,资本结构,股利政策,特殊财务和投资决策,财产风险管理,财务计划以及长期计划与战略问题等。

管理信息系统2(MS2):

这是一门以计算机为基础的满足管理最终使用者需要的信息系统分析、设计和完善的高级课程。内容包括计算机信息系统的主要组成,系统需要确认,系统发展的生命周期,具体的系统分析、系统设计、系统完善和管理等。

(7)初级的课程一般每年都有4次考试,中高级课程每年出题次数也不少于2次。

以下是CGA中文网站

CGA网站:

法律1(LW1):

cpa Canada FA3作业 第一章

LESSON 1AssignmentQuestion 1 (25 marks)Computer questionThe following is observed in the United States:Spot rate for British pounds sterling £0.7009/US$Yield on 90-day treasury bill 1.00%90-day forward rate for pounds sterling £0.6999/US$In the U.K., 90-day government securities yield 1.20%.RequiredUsing the partially completed worksheet in the file I-FN1L1Q1, assume that the amount of investment is US$1,000, and that 90 days represent 3 months of the year. Also, assume that the T-bill yields given in the question are effective annual yields.a. (10 marks)Enter appropriate formulas in the following cells:D8 to calculate the effective 90-day interest rate in the U.S.D10 to calculate the effective 90-day interest rate in the U.K.E20 to calculate the amount of the investment with interest at maturity in British currency F20 to calculate the effective yield if invested in the U.K.b. (5 marks)Based on the above, should a U.S. investor invest in U.S. T-bills or in British T-bills?c. (5 marks)Enter an appropriate formula in the following cell:C22 to calculate the 90-day forward rate (US$/£) such that the effective yield is the same for both the U.K. and the U.S.A.d. (5 marks)What is the 90-day forward rate for British funds calculated in part (c)?You should review Computer illustration 1-1 before attempting this question. Note that in contrast to illustration 1-1, this question uses reciprocal spot and forward exchange rates.Procedure1. Open the file I-FN1L1Q1. The file contains one worksheet, L1Q1.2. Enter appropriate values in cells D7, D9, B20, C20, and B22 as given in the problem.3. Note that the U.K. effective yield for part (c) in cell F22 is set to the effective 90-day interestrate in the U.S. (cell D8), thus making the effective yield the same whether the funds are invested in the U.K. or in the United States.4. Enter an appropriate formula in cell D8 to calculate the effective 90-day interest rate in theU.S., using the annualized rate for 90-day U.S. T-bills in cell D7. To compute the effective 90-day interest rate, you should add 1 to the annual interest rate, then raise the sum to the power (1/4 or 3/12 ), and lastly subtract 1 from the result.5. Enter an appropriate formula in cell D10 to calculate the effective 90-day interest rate in theU.K, using the annualized rate for 90-day U.K. government securities in cell D9.6. Enter an appropriate formula in cell E20 to calculate the amount of investment with interestat maturity (after 90 days) in U.K. currency.7. Enter an appropriate formula in cell F20 to calculate the U.K. effective interest yield, usingthe value calculated in cell E20.8. Enter an appropriate formula in cell C22 to calculate the 90-day forward rate (expressed in£/US$), based on the U.K. effective yield specified in cell F22, which is the same as the effective rate for 90-day U.S. T-bills.9. Save a copy of your completed worksheet.10. Copy and paste cells A1 to F23 into your Word document.11. Prepare your answers to parts (a) to (d).12. Display the formulas in your completed worksheet. Copy and paste the formulas in cells B5to F23 into your Word document.Question 2 (20 marks)Multiple choice (2 marks each)a. Which of the following does not usually constitute a possible conflict of interest?1) Shareholder vs. government2) Shareholder vs. creditors3) Shareholder vs. managers4) Shareholder vs. auditorsb. Which of the following statements about conflicts of interest is false?1) Creditors insert covenants in loan agreements to protect their interests.2) One of the most important types of conflicts is the one between management andshareholders.3) The government can identify all potential conflicts of interests affectingshareholders.4) Tax avoidance and industrial pollution are common types of conflicts of interestsbetween government and shareholders.c. Which of the following is the main concern from the point of view of a company’sshareholders?1) The internal rate of return of the best division when an investment is analyzed2) Preservation of the firm when risk is concerned3) Accounting return on investment when performance is appraised4) Market prices when performance is appraisedd. Which of the following is an example of an agency cost?1) A company always buys the latest computer equipment for its employees2) Senior management receives stock options enabling them to buy company stockat an exercise price well above the current stock price3) Managers use the company float plane to fly to their cottages on weekends4) Sales reps are provided with company cars to use when visiting clientse. What is the framework for analyzing investment or asset decisions known as?1) income management analysis2) capital budgeting analysis3) capital aligning analysis4) asset allocation analysisf. What is the main difference between exchanges and dealer/OTC (over the counter) markets?1) Exchanges are a part of the primary market, while dealer and OTC markets arepart of the secondary market.2) Transactions in dealer markets are conducted entirely by humans, notelectronically.3) Exchanges have a physical location, while dealer and OTC markets do not.4) All of these are differences between exchanges and dealer markets.g. Which of the following is the primary objective of the financial manager?1) Maximize profit2) Maximize dividend payments3) Maximize shareholder wealth4) Maximize revenueh. Which of the following is an example of a capital structure decision?1) Buying a new factory2) Reducing inventory levels3) Issuing new preferred shares4) Increasing purchases on crediti. Which of the following statements regarding bonds and preference shares is true?1) Only preference shares trade in the secondary market.2) The periodic payments that issuing firms are contractually obligated to make toinvestors are set at a fixed rate for both bonds and preference shares.3) Neither payments on bonds nor on preference shares are allowable tax expensesfor the issuing firm.4) Only bonds have a stated face or par value that must be repaid at maturity.j. Which of the following actions by a company could create a conflict between shareholders and creditors?1) Downplaying negative information and promoting positive news when thecompany is preparing to issue new securities2) Undertaking highly risky projects3) Taking steps to defer and minimize taxes payable4) Passing up profitable projects because they are viewed as too riskyQuestion 3 (15 marks)Assume that an Italian firm needs to borrow €500,000 for 1 year. The one year interest rate in Italy is 3%. In the U.S., the one year interest rate is 2%. The current exchange rate for the United States dollar in Italy is €0.728/US$. The one year forward rate is €0.737/US$. Would it be cheaper for the firm to borrow in Italy or arrange a loan in the U.S. and fully hedge using the forward market?Question 4 (10 marks)The corporation has been defined as a nexus of contracts. Identify four potential sources of conflict that can arise due to market imperfections and give an example of each.Question 5 (30 marks)Computer questionIn 20X2, ANZ Ltd. negotiated compensation schemes with two new managers, Mr. Top and Mr. Bottom. In 20X3, ANZ Ltd. renegotiated compensation schemes with both managers.The following personal data is available.Mr. Top Mr. Bottom20X220X320X220X3 Federal tax rate ($0 – $35,000) 15% 15% 15% 15% Federal tax rate ($35,001 – $70,000) 22% 22% 22% 22% Provincial tax rate ($0 – $35,000) 7% 7% 7% 7% Provincial tax rate ($ 35,001 – $70,000) 10% 10% 10% 10% Dividend income is grossed up by 45%. A federal tax credit of 18.97% applies to the grossed-up amount, while the associated provincial tax credit is 6.5% of the grossed-up amount.Investment income:Interest $ 1,500 $ 500 $ 1,000 $ 750 Capital gains $ 4,000 $ 5,000 $ 3,000 $ 2,500 ANZ Ltd. offered each manager the following possible compensation packages:Package #1 Annual salary $ 52,000 $ 52,000 $ 45,000 $ 45,000 Package #2 Annual salary $ 40,000 $ 42,000 $ 40,000 $ 42,000 Annual dividend $ 12,000 $ 10,000 $ 5,000 $ 3,000 The dividend is provided from ANZ's preference stock that will never involve capital gains to the holder, only dividend income. ANZ has a corporate tax rate of 40%.The after-tax costs to ANZ of the two packages are shown as follows. Note that salaries are tax deductible but dividends are not.RequiredUse Excel file I-FN1L1Q2 to calculate the actual after-tax personal income of Mr. Top and Mr. Bottom under each compensation package for 20X2 and 20X3, given their personal data. Which compensation package would each of the managers have chosen in 20X2? Which compensation package would each of the managers have chosen in 20X3? Explain your conclusions.Remember to allocate the taxable income in accordance with the corresponding rates following the progressive tax system. For this example, assume the federal tax rate applicable to a taxable income of $50,000 earned during 20X2 is 15% for the first $35,000 and 22% for the remainder.You will use Excel file I-FN1L1Q2 and Excel’s Scenario Manager feature for your analysis.Procedure1.Open Excel file I-FN1L1Q2.2.Cells A5 to B23 form the input data area. Observe that the data entered in these cells isfor Mr. Top, under compensation package #2 for 20X2. Cells C8 to D18 form thesummary of income and taxes. Examine cells D8 to D18 and observe theinterrelationships between these cells and the detailed tax calculations in rows 29 to 45.Note the formula in cell D18, which calculates the average tax rate.3.Study the completed detailed personal income tax calculations in rows 29 to 45 and theformulas in cells B29 to B45. Note the following:o These formulas refer to the input data area in rows 8 to 23.o The total income amount in cell D8 is not the same as the taxable income amount in cell B34 due to the gross-up of dividend income for tax purposes in cell B32and the inclusion of only the 50% taxable portion of capital gains in cell B33.Creating scenariosUse Scenario Manager to create the required scenarios to analyze the various compensation packages for Mr. Top and Mr. Bottom:1.Select Data, What-if Analysis, Scenario Manager and click Add. In the Scenario namebox, enter Mr. Top, 20X2, #2 to name the particular compensation package for Mr. Top.2.Select the Changing cells box. Hold down the Ctrl key and click each of the cells thathave changing inputs: B5, B6, D5, B18, B21, B22, and B23. Click OK.3.In the Scenario Values dialog box, enter the relevant cell values for this scenario, thenclick OK.4.Repeat steps 1 to 3 for the remaining compensation package for Mr. Top and the fourcompensation packages for Mr. Bottom.5.With the Scenario Manager dialog box on-screen (or choose Data, What-if Analysis,Scenario Manager to display this dialog box if it is not currently on-screen), clickSummary.6.In the Report Type box, select Scenario Summary. In the Result cells box, hold down theCtrl key and enter D8, D11, D12, D14, D16, and D18. Click OK.7.Excel creates a new worksheet called Scenario Summary that displays the scenarios, thechanging cells, and the results cells for each scenario. Select the Scenario Summaryworksheet tab.8.Cut and paste the Scenario Summary into your assignment Word file. To fit the wholesummary into your Word document, cut and paste it in two steps. Step 1, select cells B2 to H19 to include the data for Mr.Top up to 20X3. Step 2, select the range I2:L19 toinclude the data for Mr. Bottom.。

注会应试指南会计第十章综合题第二题

注会应试指南会计第十章综合题第二题下载提示:该文档是本店铺精心编制而成的,希望大家下载后,能够帮助大家解决实际问题。

文档下载后可定制修改,请根据实际需要进行调整和使用,谢谢!本店铺为大家提供各种类型的实用资料,如教育随笔、日记赏析、句子摘抄、古诗大全、经典美文、话题作文、工作总结、词语解析、文案摘录、其他资料等等,想了解不同资料格式和写法,敬请关注!Download tips: This document is carefully compiled by this editor. I hope that after you download it, it can help you solve practical problems. The document can be customized and modified after downloading, please adjust and use it according to actual needs, thank you! In addition, this shop provides you with various types of practical materials, such as educational essays, diary appreciation, sentence excerpts, ancient poems, classic articles, topic composition, work summary, word parsing, copy excerpts, other materials and so on, want to know different data formats and writing methods, please pay attention!注会应试指南会计第十章第二题:综合题。

注册会计师综合阶段职业能力综合测试第三套A卷及答案解析

1.45%:20071. 442. 3333. 32011 2201070%70%53%70% :2011 1020121212 1201200100 /17.72 /10%5130%302070%3012%14 1.12% 10%2.3.14 17.72 26.6%4.:HenryAlbertAlbert20120.8018%///1.AlbertAlbert85%2.Albert3.Albert4.AlbertAlbert 5.Albert 6.7.2008Albert8.AlbertA25B12%20AB=12%=12%1 3 2.7 9 82 4 3.2 8 6.434 2.8 8 5.7 4 4 2.56 3.8 5 5 2.8 6 3.4 6 7.4 3.7 6.6 3.3 78 3.6 4 1.8 8 8 3.2 4 1.69 8 2.9 3 1.1 108 2.6 2.6 0.959.43057.236AlbertAlbertP/E Price-to-earnings ratio model5Adjusted P/E ratio model Albert20121 A 20.10 16%2 B 16.00 13%3 C 15.40 12%4 D 11.20 9% 5E 12.30 10%15.0012%Albert16Albert)12345678Albert9 Based on the information provided in Material Four(), indicate the payback period( ) for Project A and Project B, respectively, and briefly describe the advantages and disadvantages of using the payback period method.10 Based on the information provided in Material Four(), calculate the net present value() and present valueindex()for Project A and Project B, respectively, and decide whether the net present value method and the presentvalue index method is more appropriate for the project evaluation in terms of the efficiency of investment, given the same project period. Please provide a reason to support your answer. 11 Based on the information provided in Material Four(), (i)identify the three driving factors that affect the P/E ratio((ii)with the related financial information provided for 2012, calculate the share values of Albert Company u singthe P/E ratio model()and the adjusted P/E ratio model()respectively, and evaluate whether thetransaction price of USD 16 per share was over-priced or under-priced using each model;(iii)briefly explain why Henry Company finally decided to use the adjusted P/E ratio model when evaluating Albert Company.1.1. 1①②③④⑤2①②③④⑤⑥2. 1 42 13 44519 51/33//()()1/3567 3 183. 12 :①②③3 :①②③4. 13201525. 1236. 1 12/32 263 320%~30% 4 47. 125 112 50008. 1Albert2Albert385%4Albert5Albert6Albert7Albert89Albert10 20082008 Albert9.The payback period for Project A is: 4+(20-3-4-4-4) ÷5= 5 yearsThe payback period for Project B is: 2+(25-9-8) ÷8=3 yearsAdvantages of using the payback period method:1The calculation is simple;2It is easy for decision makers to understand;3It gives a higher level indication of the projects’ liquidity and risk.Disadvantages of using the payback period method:1This method ignores time value of money by assuming values are the same at different times;2This method does not consider cash flows after the payback period, therefore giving no indication of the profitability; 3This method tends to encourage companies to accept short-term projects and to abandon long-term projects that are of strategic value.A 4+ 20-3-4-4-4 /5=5B 2+ 25-9-8 /8=3123123A Bing the net present value methodNet present value for Project A is 30-20=USD 10 millionNet present value for Project B is 36-25=USD 11 millionUnder net present value method, Project B should be selected for investment.Using the present value index methodPresent value index for Project A is 30÷20=1.5Present value index for Project B is 36÷25=1.44Under present value index method, Project A should be selected for investment.The decision made using the present value index method is more appropriate.Reason: Compared to net present value method, the present value index method eliminated the differences caused by different amounts of investment.A 30-20=10B36-25=11BA 30/20=1.5B36/25=1.44AA B11. 1 The three driving factors affecting P/E ratio are the enterprise’s sustainable growth rate, dividend payout ratio, and risks (share capital cost).2The value per share of Albert Company computed using the P/E ratio model is: 15×0.80=USD 12/shareThe transaction price of USD 16 per share was over-priced.The value per share of Albert Company computed using the adjusted P/E ratio model is: 15÷12%×18%×0.80=USD 18/share The transaction price of USD 16 per share was under-priced.3Among the many driving factors affecting P/E ratio, the crucial variable is the growth rate. As there is a large difference between the growth rate of Albert Company and the growth rate of these comparable companies, it will result a large variance in the outcome. Therefore, using the adjusted P/E ratio model could minimize the impact of growth rate when these companies are in the same industry but with different growth rates.12 Albert 15×0.80=1216Albert =15/12%×18%×0.80=18////163 Alberti ii 2012Albert 16iii Henry Albert。

cpa Canada FA3 第10章作业

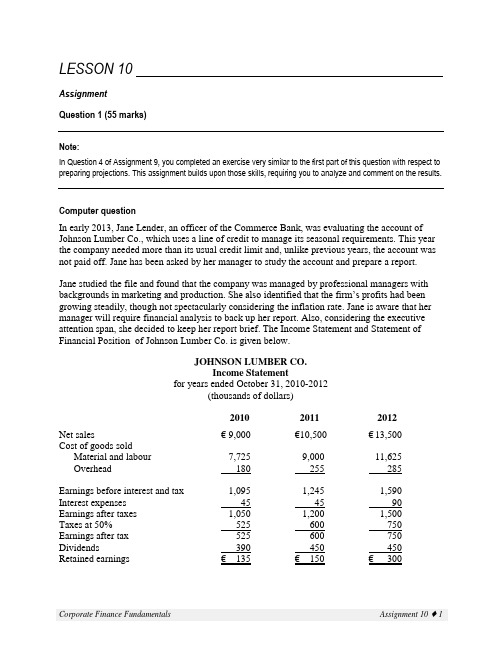

LESSON 10AssignmentQuestion 1 (55 marks)Note:In Question 4 of Assignment 9, you completed an exercise very similar to the first part of this question with respect to preparing projections. This assignment builds upon those skills, requiring you to analyze and comment on the results.Computer questionIn early 2013, Jane Lender, an officer of the Commerce Bank, was evaluating the account of Johnson Lumber Co., which uses a line of credit to manage its seasonal requirements. This year the company needed more than its usual credit limit and, unlike previous years, the account was not paid off. Jane has been asked by her manager to study the account and prepare a report. Jane studied the file and found that the company was managed by professional managers with backgrounds in marketing and production. She also identified that the firm’s profits had been growing steadily, though not spectacularly considering the inflation rate. Jane is aware that her manager will require financial analysis to back up her report. Also, considering the executive attention span, she decided to keep her report brief. The Income Statement and Statement of Financial Position of Johnson Lumber Co. is given below.JOHNSON LUMBER CO.Income Statementfor years ended October 31, 2010-2012(thousands of dollars)201020112012Net sales € 9,000 €10,500 €13,500Cost of goods soldMaterial and labour 7,725 9,000 11,625Overhead 180 255 285 Earnings before interest and tax 1,095 1,245 1,590 Interest expenses 45 45 90 Earnings after taxes 1,050 1,200 1,500Taxes at 50% 525 600 750 Earnings after tax 525 600 750 Dividends 390 450 450 Retained earnings €135 €150 €300The net sales is arrived after a quantity discount of €90, €105, and €160 respectively i n 2010, 2011, and 2012. Overhead includes the following depreciation.Plant 120 135 165Equipment 52 60 75JOHNSON LUMBER CO.Statement of Financial Positionas at October 31, 2010-2012201020112012 ASSETSCash €271 €241 €121 Marketable securities 315 15 0 Accounts receivable 1,410 1,515 1,785 Inventories 1,515 1,725 1,965Total current assets 3,511 3,496 3,871 Loans to dealers 150 150 225Plant (net of depreciation) 1,650 1,800 2,700 Equipment (net of depreciation) 1,350 1,425 1,515 Total fixed assets 3,150 3,375 4,440Total assets € 6,661 € 6,871 €8,311 LIABILITIES AND EQUITYAccounts payable € 1,305 € 1,515 €1,680 Notes payables 150 0 0Bank loan 0 0 975Total current liabilities 1,455 1,515 2,655 Ordinary shares 1,206 1,206 1,206 Retained earnings 4,000 4,150 4,450Total Liabilities and equity € 6,661 € 6,871 €8,311 There are two sections to this question: Section 1 pertains to the financial analysis as specified in the appendix; Section 2 is an additional analysis specified in this assignment.RequiredSection 1 (5 marks)Prepare an analysis of the financial performance of the three years (2010-2012), and comment on Johnson’s current financial situation. Your analysis should be bas ed on the statement of cash flows (SCF) for the period from October 31, 2010 to October 31, 2012 and basic ratios for the three years of data, as supplied below. This section requires your skills with financial ratios and working capital management.JOHNSON LUMBER CO.Statement of cash flowstwo years ended October 31, 2012(000s)Net income from operations € 1,350 OPERATING ACTIVITIESAdjustments to convert to cash basisAccounts receivable increase (375)Inventories increase (450)Accounts payable increase 375€ (450) Depreciation 435€(15)€ 1,335 FINANCING ACTIVITIESNotes payable decrease € (150)Bank loan increase 975Dividends (900)€(75) INVESTING ACTIVITIESLoans to dealers increase €(75)Plant increase (1,350)Equipment increase (300)(1,725)Decrease in cash € (465)Cash and cash equivalents at October 31, 2010 586Cash and cash equivalents at October 31, 2012 €121RATIO ANALYSIS2010 2011 2012 Liquidity ratios:Current 2.41 2.31 1.46 Quick 1.37 1.17 0.72 Inventory turnover1 5.22 5.71 6.46 Accounts receivable turnover2 6.38 7.18 8.18 Profitability ratios:Times-interest-earned 24.33 27.67 17.67 Asset turnover3 1.35 1.53 1.62Net operating margin 0.12 0.12 0.12 Earnings power ratio 0.16 0.18 0.19 1The calculation for 2010 was based on the 2010 inventory number not the average inventory as the 0211 and 2012 were2The calculation for 2010 Accounts receivable turnover was based on the 2010 Accounts receivable number and not the average accounts receivable as the 2011 and 2012 were.3The calculation for asset turnover for 2010 was based on the Total assets for 2010 and not the average total assets as was done used for the asset turnover calculation for 2011and2012.Note:No worksheet has been provided for analyzing Section 1. You may wish to construct your own, or answer the question manually.Section 2 (50 marks total)Use a worksheet to develop pro forma financial statements for the next five years (2013-2017) for Johnson. Then perform what-if analyses with the pro forma financial statements. Modify the LXQ1 worksheet in the file I-FN1LXQ1 to complete this section.Base plan(14 marks)The following additional information is required to complete this section, using the worksheet LXQ1. (All dollar amounts are expressed in €000s.)1. The corporate tax rate is 40% effective November 1, 2006. Previously it was 50%.2. Depreciation is calculated by applying the depreciation rate on non-current assets. The averagedepreciation rate is 5%. In the year of acquisition, depreciation is allowed only for a half year, for new capital expenditures (row 34). [Note that these instructions differ from those given in Question 4 of Assignment 9.]3. Cost of goods sold is 83% of sales for the same year.4. Salaries and administration costs are 8% of sales for the same year.5. Inventory is maintained at 15% of next year’s sales.6. Accounts payable is 15% of cost of goods sold for the same year.7. Accounts receivable is 15% of sales for the same year.8. Johnson’s target level of cash and marketable securities is 2% of sales for the same year.9. Johnson projects its sales to grow at 20% per year over the preceding year for both 2013 and2014, and slow to 5% per year for 2015 to 2017.10. Interest rates are forecasted at 9% for 2013, 10% for 2014, and 12% thereafter.11. Johnson plans to incur no long-term debt for the five years starting 2013.12. No new equity issues have been planned for the five years starting 2013.13. New capital expenditures for the five years from 2013 to 2017 will be €800, €1,400, €1,000,€1,000, and €1,000 respectively.14. Dividends will be maint ained at €300 for 2013 to 2017.After entering the preceding information in the worksheet, analyze the pro forma financial information. Comment on Johnson’s financial plan, and discuss some of the financial ratios and key financial information.Procedure1. Open the file I-FN1LXQ1. The file has only one worksheet, LXQ1.2. Before making any changes to this worksheet, print out a copy (including column and rowheaders) of the worksheet and analyze it. You may find the printed copy useful in working through various parts of the question.3. Examine the layout of the worksheet. It resembles the worksheet used in Computer illustration10-1 of the Lesson Notes and Question 4 of Assignment 9. The current data pertaining to 2012 has been pre-entered in cells B13 to B20. Most parts of the pro forma financial statements and ratio analysis have also been pre-entered.4. Enter appropriate information or formulas in the following cells:B8 Corporate tax rateB9 Depreciation rateG10 to G20 The various percentagesB26 to G26 Sales growth multiple for calculating projected salesB27 to G27 Projected salesB28 to G28 Interest ratesC32 to G32 Long-term debtC33 to G33 New equityC34 to G34 New capital expendituresC35 to G35 DividendsB41 to G41 Target cash and marketable securitiesB43 to G43 Accounts receivableB48 to G48 Accounts payableC60 to G60 Depreciation5. After completing the worksheet, save a copy. This copy will be used as a basis for each of thescenarios in the next section.6. Copy and paste cells A5 to G66 into your Word document. Then copy and paste cells A69 toG76 into your Word document.7. Display the formulas in your completed worksheet. Copy and paste the formulas in cells A38to D76 to your Word document.What-if analysis(36 marks, 6 marks each)After reviewing the five-year financial forecast, Ms. Lender of the Commercial Bank makes several suggestions for Johnson.Use your completed worksheet to analyze the following independent scenarios suggested by Ms. Lender. Assume long-term debt is incurred at the beginning of a year.Note:6 marks for each part’s analysis and conclusions.a.Cut growth. By reducing the firm’s optimal capital budget, Johnson can reduce new capitalexpenditures to €200 for all years, which in turn will change the firm’s sales. Instead of the original growth rate, 2013 net sales will increase 10% over 2012, and then grow at an annual rate of only 2% thereafter.b. Finance growth through long-term debt. Instead of cutting growth, Johnson can try tofinance growth by incurring long-term debt, with year-end balances of €2,500, €2,500, €3,500, €4,000, €4,000 for 2013 to 2017 respectively.c. Finance growth through new equity financing. Rather than financing growth using long-term debt, Johnson can issue new equity of €3,500 (net proceeds) in 2013.d. Finance growth using a mix of long-term debt and new equity. Johnson can try to financegrowth by issuing new equity of €1,750 in 2013, and long-term debt with year-end balances of €1,500, €1,800, €2,500, and €3,000 in th e years 2014 to 2017 respectively.e. Finance growth by improving cash receipts. Instead of issuing new equity and/or new long-term debt, Johnson can try to finance growth by cutting the percentage of credit sales so that accounts receivable is only at 5% of its total sales for each year, and reduce inventory to 5% of the next year’s sale by reducing dealer inventories.f. Ms. Lender points out that if Johnson is successful in financing the desired growth,shareholders may want a higher level of dividends. Therefore, she suggests an analysis of the impact of a higher level of dividends on its financial plan: using the financial growth plan specified in (d), increase the total dividend payout to €450 for 2015 and beyond.Procedure1. For each of the six scenarios suggested by Ms. Lender, retrieve the copy of the worksheetsaved in step 5 of the previous section. (Base plan)2. Enter appropriate information for each scenario. Modify cell A6 to indicate “SCENARIO A,”“SCENARIO B,” and so on and cell A69 to indicate “RATIO ANALYSIS: SCENARIO A”and so on.3. Use the worksheet to provide the appropriate analysis and conclusions.4. Submit the Ratio Analysis for each scenario by pasting cells A69 to G76 into your Worddocument.Question 2 (20 marks)Multiple choice (2 marks each)Statement of cash flowsUse the information that follows for questions a – g.a.Referring to the company data above, what is the firm’s operating margin?1) 3.00%2) 4.10%3) 4.90%4) 15.31%b. Referring to the company data above, what is the market-to-book ratio of the firm’s equity?1) 0.472) 1.003) 1.164) 1.50c.Referring to the company data above, what is the firm's price-earnings ratio?1) 2.32) 3.03) 5.04) 15.0d.Referring to the company data above, what is the firm's return on common equity?1) 11%2) 22%3) 30%4) 43%e.Referring to the company data above, what is the firm's total debt-to-assets ratio?1) 0.692) 0.723) 0.764) 1.31f.Referring to the company data above, what is the times-interest-earned ratio?1) 1.002) 2.733) 3.734) 4.45g.Referring to the following company data above, what is the firm's debt-to-equity ratio?1) 1.542) 1.773) 2.204) 3.14h.Acquirer Inc. a firm specialized in buying other firms, announced that it was going to acquireSpecialize Cars Ltd., a carmaker. What type of merger would this be?1) Cross-border merger2) Conglomerate merger3) Horizontal merger4) Vertical mergeri.Which of the following firms would be a good target for a leveraged buyout (LBO)?1) A firm that uses well-known, mature production technology2) A firm that is highly levered and has difficulty meeting loan payments3) A firm that is in a new and specialized business4) A firm whose primary assets are trademarks and patentsj.External growth can occur by which of the following means?1) Increasing research and development into new products2) Purchasing another firm's debt3) Purchasing either another firm's assets or shares4) Expanding a production line by purchasing new production equipment Question 3 (5 marks)Pal-Lee Foods (PLF) is a processor of baking ingredients such as dried fruits, chocolate chips, and nuts. Wow Foods Inc. (WFI) has diversified production facilities for making a wide variety of food products that use PLF’s products. Following discussions with its investment bankers, WFI's management is considering a merger of equals to take advantage of some strategic synergies between the two companies.a.What type of merger would this be? (2 marks)b.What reasons might management of PLF and WFI have for wanting to merge their businessoperations? (3 marks)Question 4 (5 marks)One of the features that make a company a good target for a leveraged buyout is a diversified product line. Explain why this feature is important.Question 5 (15 marks)Answer the following independent questions.a.Financial ratios use the relative value of various items on the financial statements to assess afirm’s financial position. Typically, these financial ratios are divided into five types. One of these types is valuation (market-value) ratios. Identify the remaining four types of ratios and, for each, briefly describe the information it conveys. (4 marks)b.The senior management of Pyramid Inc. is currently developing its marketing strategy for thenext two years. A potential input into this process is confidential information on themarketing plans of its nearest competitor, which has been provided to Pyramid by a new staff member who recently resigned from a position with the competitor. Briefly explain why it is important for the senior management of Pyramid to consider how they have acquired this information as well as the content of the information itself in a situation such as this one.(4 marks)c.External expansion of a business can occur in several different ways. Briefly explain thedifference between an acquisition and a statutory amalgamation (merger). (3 marks)d.Briefly describe what a leveraged buyout (LBO) (also known as a management buyout) isand how an LBO is typically undertaken. (4 marks)。

高级会计学英文版第十版课后练习题含答案

高级会计学英文版第十版课后练习题含答案Chapter 1Multiple Choice Questions1.A primary reason for a business to organize as a corporationis to A. allow shareholders to limit their losses to the amount they have invested in the company. B. limit the amount of taxes the company pays. C. make it easier for the company to secureloans from banks and other lenders. D. ensure that the company’s management is not subject to legal liability.Answer: A2.Which of the following statements is true? A. A partnershipis a legal entity separate from its owners. B. A soleproprietorship has limited liability. C. A corporation is owned by its shareholders. D. A limited liability company is not taxed as a separate entity.Answer: CShort Answer Questions1.What is the definition of accounting? Accounting is theprocess of identifying, measuring, and communicating economicinformation to permit informed judgments and decisions by users of the information.2.What are the three primary financial statements produced byaccounting? The three primary financial statements produced byaccounting are the balance sheet, income statement, and cash flow statement.Chapter 2Multiple Choice Questions1.A transaction that increases an asset and decreases aliability is called a(n) A. expense. B. revenue. C. equity. D.none of the above.Answer: D2.Which of the following is an example of a prepd expense? A.Rent pd in advance B. Money borrowed from a bank C. Interest on a loan D. Salary pd to an employeeAnswer: AShort Answer Questions1.What is the purpose of the accounting equation? The purposeof the accounting equation is to show the relationship between a company’s assets, liabilities, and equity.2.What is the difference between an asset and a liability? Anasset is something that a company owns and has value, while a liability is something that a company owes to someone else. Chapter 3Multiple Choice Questions1.What is the difference between a perpetual inventory systemand a periodic inventory system? A. A perpetual inventory systemis based on physical counts of inventory, while a periodicinventory system is based on estimates of inventory levels. B. A perpetual inventory system updates inventory records continuously, while a periodic inventory system updates inventory records only periodically. C. A perpetual inventory system is used only bylarge companies, while a periodic inventory system is used bysmall companies. D. A perpetual inventory system is necessary for accurate financial statements, while a periodic inventory system is not.Answer: B2.When inventory is sold on credit, which accounts areaffected? A. The sales account and the cost of goods sold account.B. The accounts receivable account and the cost of goods soldaccount. C. The sales account and the inventory account. D. The accounts receivable account and the inventory account.Answer: BShort Answer Questions1.What is gross profit? Gross profit is the difference betweena company’s sales revenue and cost of goods sold.2.What is the difference between FIFO and LIFO? FIFO (First In,First Out) assumes that the first items purchased are the first items sold, while LIFO (Last In, First Out) assumes that the last items purchased are the first items sold.。

加拿大csc考试(3)

加拿大csc考试(3)加拿大csc考试某企业甲产品的单位成本为200元,其中,原材料60元,直接人工80元,制造费用60元。

则甲产品中原材料的构成比率为()。

A.30%B.40%C.6%D.70%正确答案:A,第 3 题 (判断题)(每题 1.00 分) 题目分类:第一部分分章节练习 > 第六章利润 >企业采用“表结法”结转本年利润的,年度内每月月末损益类科目发生额合计数和月末累计余额无须转入“本年利润”科目,但要将其填入利润表,在年末时将损益类科目全年累计余额转入“本年利润”科目。

( )正确答案:A,第 14 题 (单项选择题)(每题 1.00 分) 题目分类:第一部分分章节练习(无纸化试题) > 第九章产品成本计算与分析 >某企业2010年可比产品按上年实际平均单位成本计算的本年累计总成本为4300万元,按本年计划单位成本计算的本年累计总成本为4250万元,本年累计实际总成本为4100万元。

则可比产品成本的降低额为()万元。

A.50B.150C.200D.250正确答案:C,第 15 题 (单项选择题)(每题 1.00 分) 题目分类:第一部分分章节练习(无纸化试题) > 第九章产品成本计算与分析 >某企业生产甲产品,属于可比产品,上年实际平均单位成本为50元,上年实际产量为900件,本年实际产量为1000件,本年实际平均单位成本为49元。

则本年甲产品可比产品成本降低率为()。

A.1%B.1.04%C.2%D.2.22%正确答案:C,第 4 题 (判断题)(每题 1.00 分) 题目分类:第一部分分章节练习 > 第六章利润 >企业发生毁损的固定资产的净损失,应计入营业外支出。

()正确答案:A,第 5 题 (判断题)(每题 1.00 分) 题目分类:第一部分分章节练习 > 第六章利润 >企业已计入营业外支出的税收滞纳金应调整增加企业的应纳税所得额。

财务会计FA3_真题2007-03[1]

![财务会计FA3_真题2007-03[1]](https://img.taocdn.com/s3/m/8614f8fa770bf78a65295434.png)

CGA-CANADAFINANCIAL ACCOUNTING 3 EXAMINATIONMarch 2007Marks Time: 3 HoursNotes:1. All calculations must be shown in an orderly manner to obtain part marks.2. Round all calculations to the nearest dollar, except for EPS and financial ratios where two decimal places should be used.3. Unless otherwise indicated, use straight-line amortization.4. Assume a December 31 fiscal year end for all questions, unless specified otherwise in the question.5. If a test of materiality is required, use 5%.6. Narratives for journal entries are not required. When preparing journal entries, be careful to select account titles that clearly indicatewhere the item will appear in the financial statements. For example, if something is to be on the income statement, it should be labelledas a revenue, expense, or extraordinary item.120 QuestionSelect the best answer for each of the following unrelated items. Answer each of these items in yourexamination booklet by giving the number of your choice. For example, if the best answer for item (a)is (1), write (a)(1) in your examination booklet. If more than one answer is given for an item, that item willnot be marked. Incorrect answers will be marked as zero. Marks will not be awarded for explanations.Note:2 marks eacha. Which of the following best describes the difference between a defined contribution pension plan anda defined benefit pension plan?1) For a defined contribution plan, the payments made to the plan are predetermined and the amountof benefits paid out to employees upon retirement depends upon the success of the investment.For a defined benefit plan, the payments made to the plan vary in order to ensure that apredetermined amount of benefits per year of service can be paid to the employee uponretirement.2) For a defined contribution plan, the payments made to the plan vary in order to ensure that apredetermined amount of benefits per year of service can be paid to the employee uponretirement. For a defined benefit plan, the payments made to the plan are predetermined and theamount of benefits paid out to employees upon retirement depends upon the success of theinvestment.3) For a defined contribution plan, the payments made to the plan are predetermined, as are thebenefits per year of service to be paid to employees upon retirement. For a defined benefit plan,the payments made to the plan are variable, as are the benefits per year of service to be paid toemployees upon retirement.4) For a defined contribution plan, the payments made to the plan are variable, as are the benefits peryear of service to be paid to employees upon retirement. For a defined benefit plan, the paymentsmade to the plan are predetermined, as are the benefits per year of service to be paid to employeesupon retirement.b. A company’s pension plan assets equal its accrued benefit obligation. If the company’s balance sheetindicates a pension liability, which of the following must be true about the company’s pension plan?1) There are unrecognized past services costs.2) There are unamortized actuarial losses.3) There are unamortized actuarial gains.4) The company’s balance sheet is incorrect; there should be no asset or liability reported forpensions.c. Which of the following is not a factor in determining pension expense for the year?1) Current service cost for the year2) Pension contributions paid for the year3) Amortization of past service costs4) Interest on accrued pension obligationd. To align its amortization policy with industry practice, CDF Company changed its amortization policyfrom straight line to declining balance. How should this change in policy be applied, assuming that CDF has all of the information required to make the change?1) Prospectivelyrestatement2) Retroactivelywithoutrestatement3) Retroactivelywith4) This change should not be allowede. DFS Co. had total sales of $500,000 for the year. Its opening gross accounts receivable balance was$50,000 and its ending balance was $35,000. The unearned revenue account had an opening balance of $20,000 and an ending balance of $30,000. What is the amount of cash collected from customers for the year?1) $475,0002) $495,0003) $505,0004) $525,000f. What is the difference between a direct financing lease and a sales-type lease for lessors?1) For a direct financing lease, collection is not reasonably assured.2) For a direct financing lease, there are significant costs that are difficult to estimate.3) For a direct financing lease, the lease does not meet any of the capitalization criteria for a capitallease.4) For a direct financing lease, the lessor earns only interest revenue on the lease arrangement.g. RTG Company purchased a new computer system. The computer is expected to decline in usefulnesseach year over its 4-year useful life. The company executives have a bonus plan based on net income.The executives have asked that the computer be amortized using the straight-line method. As the company’s accountant, how would you respond to this request?1) Agree with the request to use the straight-line method for amortization.2) Agree with the request and then report the executives’ unethical behaviour to the board ofdirectors.3) Disagree with the request and explain that a better amortization method would be the taxationmethod (CCA) to avoid having to account for future income taxes.4) Disagree with the request and explain that a better amortization method would be the decliningbalance method, as it would better match the usefulness of the computer system.h. In October 2006, XCD Company entered into a non-cancellable contract to purchase inventory for$450,000, to be delivered in February 2007. At December 31, 2006, the company’s year end, the market value of the contracted inventory decreased to $370,000. Assume any amounts involved are material. How should these events be reported in the financial statements?1) The events should be disclosed in the notes to the financial statements.2) The $80,000 estimated loss should be reported in the income statement and as an estimatedliability on the balance sheet, along with a note disclosure of the contract terms.3) The $80,000 estimated loss should be directly debited to the retained earnings account and anestimated liability on the balance sheet should be reported, along with a note disclosure of thecontract terms.4) Since the contract has not yet been fulfilled, these events need not be reported or disclosed in thefinancial statements.i. JMN Company had opening retained earnings of $100,000. Net income for the year was $23,000.During the current year, an error in the prior year was discovered resulting in a credit to retained earnings for $5,000, and 1,000 shares were retired at $2 above their book value. There was nocontributed surplus account prior to the retirement of the shares. Ending retained earnings was$102,000. What was the amount of dividend declared for the year?1) $14,0002) $24,0003) $26,0004) $28,000j. NHG Company uses the straight-line method to amortize its capital assets. With new information provided this year, it was determined that the useful life of one of the assets was originally estimated to be too long and its residual value too high. How should this change be reported?1) The change should be retroactively applied. The accumulated amortization account will beincreased and retained earnings decreased.2) The change should be retroactively applied. The accumulated amortization account will bedecreased and retained earnings increased.3) The change should be applied prospectively. The current year will use the new estimates foramortization expense. The estimate changes will be disclosed in the notes.4) The change should be applied prospectively. The current year will use the old estimates and futureyears will use the new estimates. The estimate changes will be disclosed in the notes.On February 1, 2007, NHU Co. issued $150,000, 9% (payable semi-annually), 5-year bonds. Thefollowing is the bond amortization table. NHU Co.’s year end is September 30.Balance CarryingCash Interest Discount Unamortized ValueBonds Date Interest Expense Amortization Discount of133,44016,560 $1,February2007 $ — $ — $ — $August 1, 2007 6,750 8,006 1,256 15,304 134,696February 1, 2008 6,750 8,082 1,332 13,972 136,028August 1, 2008 6,750 8,162 1,412 12,560 137,440February 1, 2009 6,750 8,246 1,496 11,064 138,936Required2 a. Which method of discount amortization is being used? Explain briefly.3 b. Prepare the adjusting journal entry(ies) required for September 30, 2008.4 c. Assume $100,000 of the bonds were retired on February 1, 2009 for $110,000. Prepare the journalentry(ies) to record this event using the book-value method. Assume the interest payment has alreadybeen recorded.3 d. Explain how the reporting for the bonds at the date of issue would change if the bonds wereconvertible into a fixed number of common shares at the option of the issuer.315 QuestionKJL Corporation uses the liability method of tax allocation. At the beginning of 2006, KJL Corporationhas the following future income tax accounts:Future income tax asset — warranty — current $19,600Warranty expense to date was $126,000 and claims paid were $70,000, leaving a $56,000 warrantyliability balance in the current liabilities section of the balance sheet.Future income tax liability — capital asset — long term $147,000At the beginning of 2006, the net book value of capital assets was $1,276,000 and UCC (tax basis) was$856,000.The following information relates to the year 2006:1. Accounting income before income taxes was $625,000.2. Warranty claims paid out for the year were $45,000. The year end warranty liability balance was$33,000 after adjusting entries were recorded.3. Amortization on capital assets was $287,000. CCA claimed was $395,000.4. Dividends received from a taxable Canadian corporation were $5,000.5. Golf club membership dues paid for company executives amounted to $20,000.6. On January 1, 2006, the government unexpectedly changed the income tax rate from 35% to 40%,effective immediately.7. For income tax purposes, warranty costs are deductible when paid, dividends from a taxable Canadiancorporation are not taxable, and golf club membership dues are not deductible.Required2 a. For each of the above items 2) to 5), indicate whether the item is a permanent or temporary differencefor tax accounting purposes.3 b. Prepare the adjusting journal entry(ies) that would have been made for the 2006 warranty liability.4 c. Calculate the income taxes payable for KJL for 2006.Below is information from the December 31, 2006 balance sheet for NG Co.Bonds payable — $500,000 par value, 7%, maturing December 31, 2015,each $1,000 bond is convertible into 30 common shares at the holder’s option (net) $ 450,000Preferred shares — $2, no par value, cumulative, convertible at 1 preferred share for2 common shares — 14,000 shares outstanding 210,000Contributed capital — common share options outstanding 70,000Common stock conversion rights — 7% bonds 30,000Common shares — no-par value, 320,000 shares outstanding 800,000Additional information1. There are no dividends in arrears at the beginning of the year. No dividends have been declaredfor 2006.2. Net income for 2006 is $1,263,000; includes $38,000 interest expense for the 7% bonds.3. Income tax rate is 40%.4. Bonds, options, and preferred shares were outstanding for the entire year.5. The stock options are noncompensatory and are convertible into a total of 80,000 common shares at anexercise price of $32.30. The average share price during the year was $34.6. No other common share transactions occurred during the year.Required10 a. Calculate basic and diluted earnings per share (EPS) for the year ended December 31, 2006.3 b. Assume that one-half of the stock options were exercised on January 1, 2007. Prepare the journalentry(ies) to record the exercise of stock options.6 Question 5On May 1, 2006, Nancy and Drew formed a partnership by investing $96,000 and $64,000 respectively.On May 1, 2007, the opening balances of the partner’s capital accounts were $118,000 for Nancy and$68,000 for Drew. For the fiscal year ended April 30, 2008, net income of the partnership was $50,000.During the 2008 fiscal year, Nancy withdrew $2,000 per month and Drew withdrew $1,500 per month.Profits of the partnership are to be allocated based on a 2008 salary of $40,000 for Nancy and $20,000 forDrew, with the remaining profit or loss split based on original investment proportions.Required3 a. Determine the allocation of net income for the year ended April 30, 2008.3 b. Prepare a statement of partners’ capital for the year ended April 30, 2008.PTR Company issued convertible bonds for the first time on January 1, 2006. The $100,000, 10% (payable annually on the anniversary date of the bonds), 5-year convertible bonds were issued at 108, yielding 8%.The bonds would have been issued at 98 without a conversion feature, yielding 10.5%. The bonds areconvertible at the investor’s option.The company’s bookkeeper recorded the bonds at 108 and, based on the $108,000 bond carrying value,recorded interest expense using the effective interest rate method for 2006. He prepared the followingamortization table:Balance CarryingCash Interest Premium Unamortized Value Date Interest Expense Amortization Premium ofBonds8,000 $108,000 1,2006 $ — $ — $ — $JanuaryDecember 31, 2006 10,000 8,640 1,360 6,640 106,640 You were hired as an accountant to replace the bookkeeper in November 2007. It is now December 31,2007, the company’s year end, and the CEO is concerned that its debt covenant may be breached. The debt covenant requires PTR to maintain a maximum debt-to-equity ratio of 2.5. Based on the current financialstatements, the debt-to-equity ratio would be 2.6. The CEO recalls hearing that convertible bonds shouldbe reported by separating out the liability and equity components, yet he does not see any equity amountsrelated to the bonds on the current financial statements. He has asked you to look into the bondtransactions recorded and make any necessary adjustments. He would also like you to explain how anyadjustments you make affect the debt-to-equity ratio.Required2 a. Determine the amount of the conversion feature value that would have been reported in the equitysection of the balance sheet at January 1, 2006, if split accounting had been used (that is, where thedebt and equity components are recorded separately).5 b. Prepare a bond amortization schedule from January 1, 2006 to December 31, 2007, using the effectiveinterest rate method and split accounting method.4 c. Prepare the journal entry(ies) dated January 1, 2007 to correct the bookkeeper’s recording errors in2006. Ignore income tax effects.4 d. Explain the effect of the error corrections (part (c)) on the debt-to-equity ratio. Calculations are notrequired; however, indicate the direction of correction (increase or decrease) on the specific accountsaffected and explain how the debt-to-equity ratio is affected as a result.The following is the shareholders’ equity section of WER’s balance sheet for January 1, 2007:Preferred shares — no-par value; $3; cumulative; unlimited shares authorized;100,000 50,000 shares issued and outstanding 1 $Common shares — no-par value; unlimited shares authorized; 200,000 shares issued 200,000Contributed capital on retirement of common shares 10,000Accumulated other comprehensive income 20,000Retained earnings 350,0001There was 1 year of dividends in arrears at January 1, 2007. The dividends accrue annually atDecember 31.During 2007, the following transactions took place:January 30Reacquired 1,000 of the preferred shares for $3.50 per share plus any entitled dividends. These shareswere retired.February 20Reacquired 5,000 common shares for $5 per share. These shares were retired.April 15The board of directors declared a dividend equal to $0.50 per common share, along with the dividends inarrears for last year on the preferred shares.September 1WER entered into a 5-year lease agreement for a capital asset. The following are pertinent details of thelease:1. The first semi-annual payment of $6,000 is due March 1, 2008.2. The implicit interest rate in the lease is not known to WER.3. WER’s incremental borrowing rate is 10%.4. The estimated salvage value of the asset is $4,000 at the end of the asset’s estimated useful life of8 years. WER uses double-declining balance amortization for this type of asset.5. The title of the asset is transferred to WER at the end of the lease.6. The fair market value of the asset is $50,700.December 31Year-end adjusting journal entries were made related to the lease transaction.Required16 a. Prepare the journal entries to record the above transactions.3 b. Explain how the accounting would be different if the shares that were reacquired and retired wereinstead reacquired and held as treasury shares. Explain how treasury shares affect the number ofshares issued and outstanding.END OF EXAMINATION100FINANCIAL ACCOUNTING 3 [FA3]EXAMINATIONBefore starting to write the examination, make sure that it is complete and that there are no printing defects. This examination consists of 7 pages and 3 pages of attachments. There are 7 questions for a total of 100 marks.READ THE QUESTIONS CAREFULLY AND ANSWER WHAT IS ASKED.To assist you in answering the examination questions, CGA-Canada includes the following glossary of terms.GlossaryFrom David Palmer, Study Guide: Developing Effective Study Methods (Vancouver: CGA-Canada, 1996). Copyright David Palmer.Compare Examine qualities or characteristics thatresemble each other. Emphasize similarities,although differences may be mentioned. Contrast Comparebyobservingdifferences. Stressthe dissimilarities of qualities orcharacteristics. (Also Distinguish between) Criticize Express your own judgment concerning thetopic or viewpoint in question. Discuss bothpros and cons.Define Clearly state the meaning of the word orterm. Relate the meaning specifically to theway it is used in the subject area underdiscussion. Perhaps also show how the itemdefined differs from items in other classes. Describe Tellthewhole story in narrative form. Diagram Give a drawing, chart, plan or graphicanswer. Usually you should label a diagram.In some cases, add a brief explanation ordescription.Discuss This calls for the most complete and detailed answer. Examine and analyze carefully andpresent both pros and cons. To discussbriefly requires you to state in a fewsentences the critical factors.Evaluate This requires making an informed judgment.Your judgment must be shown to be basedon knowledge and information about thesubject. (Just stating your own ideas is notsufficient.) Cite authorities. Cite advantagesand limitations.Explain In explanatory answers you must clarify the cause(s), or reasons(s). State the “how” and“why” of the subject. Give reasons fordifferences of opinions or of results. Illustrate Make clear by giving an example, e.g., afigure, diagram or concrete example. Indicate Provide a short explanation.Interpret Translate, give examples of, solve, orcomment on a subject, usually making ajudgment on it.Justify Prove or give reasons for decisions orconclusions.List Present an itemized series or tabulation.Be concise. Point form is oftenacceptable. (Also Enumerate or Identify) Outline This is an organized description. Give ageneral overview, stating main andsupporting ideas. Use headings andsub-headings, usually in point form. Omitminor details.Prove Establish that something is true by citingevidence or giving clear logical reasons. Relate Show how things are connected with eachother or how one causes another,correlates with another, or is like another. Review Examine a subject critically, analyzingand commenting on the importantstatements to be made about it.State Present the main points in brief, clearsequence, usually omitting details,illustrations, or examples.Summarize Give the main points or facts in condensedform, like the summary of a chapter,omitting details and illustrations.Trace In narrative form, describe progress,development, or historical events fromsome point of origin.Table 1Present Value of $1ni)(11+Period1%2%3%4%5%6%7%8%9%10%11%12%13%14%15%16%18%20%1.9901.9804.9709.9615.9524.9434.9346.9259.9174.9091.9009.8929.8850.8772.8696.8621.8475.83332.9803.9612.9426.9246.9070.8900.8734.8573.8417.8264.8116.7972.7831.7695.7561.7432.7182.69443.9706.9423.9151.8890.8638.8396.8163.7938.7722.7513.7312.7118.6931.6750.6575.6407.6086.57874.9610.9238.8885.8548.8227.7921.7629.7350.7084.6830.6587.6355.6133.5921.5718.5523.5158.48235.9515.9057.8626.8219.7835.7473.7130.6806.6499.6209.5935.5674.5428.5194.4972.4761.4371.40196.9420.8880.8375.7903.7462.7050.6663.6302.5963.5645.5346.5066.4803.4556.4323.4104.3704.33497.9327.8706.8131.7599.7107.6651.6227.5835.5470.5132.4817.4523.4251.3996.3759.3538.3139.27918.9235.8535.7894.7307.6768.6274.5820.5403.5019.4665.4339.4039.3762.3506.3269.3050.2660.23269.9143.8368.7664.7026.6446.5919.5439.5002.4604.4241.3909.3606.3329.3075.2843.2630.2255.193810.9053.8203.7441.6756.6139.5584.5083.4632.4224.3855.3522.3220.2946.2697.2472.2267.1911.161511.8963.8043.7224.6496.5847.5268.4751.4289.3875.3505.3173.2875.2607.2366.2149.1954.1619.134612.8874.7885.7014.6246.5568.4970.4440.3971.3555.3186.2858.2567.2307.2076.1869.1685.1372.112213.8787.7730.6810.6006.5303.4688.4150.3677.3262.2897.2575.2292.2042.1821.1625.1452.1163.093514.8700.7579.6611.5775.5051.4423.3878.3405.2992.2633.2320.2046.1807.1597.1413.1252.0985.077915.8613.7430.6419.5553.4810.4173.3624.3152.2745.2394.2090.1827.1599.1401.1229.1079.0835.064916.8528.7284.6232.5339.4581.3936.3387.2919.2519.2176.1883.1631.1415.1229.1069.0930.0708.054117.8444.7142.6050.5134.4363.3714.3166.2703.2311.1978.1696.1456.1252.1078.0929.0802.0600.045118.8360.7002.5874.4936.4155.3503.2959.2502.2120.1799.1528.1300.1108.0946.0808.0691.0508.037619.8277.6864.5703.4746.3957.3305.2765.2317.1945.1635.1377.1161.0981.0829.0703.0596.0431.031320.8195.6730.5537.4564.3769.3118.2584.2145.1784.1486.1240.1037.0868.0728.0611.0514.0365.026121.8114.6598.5375.4388.3589.2942.2415.1987.1637.1351.1117.0926.0768.0638.0531.0443.0309.021722.8034.6468.5219.4220.3418.2775.2257.1839.1502.1228.1007.0826.0680.0560.0462.0382.0262.018123.7954.6342.5067.4057.3256.2618.2109.1703.1378.1117.0907.0738.0601.0491.0402.0329.0222.015124.7876.6217.4919.3901.3101.2470.1971.1577.1264.1015.0817.0659.0532.0431.0349.0284.0188.012625.7798.6095.4776.3751.2953.2330.1842.1460.1160.0923.0736.0588.0471.0378.0304.0245.0160.010530.7419.5521.4120.3083.2314.1741.1314.0994.0754.0573.0437.0334.0256.0196.0151.0116.0070.004240.6717.4529.3066.2083.1420.0972.0668.0460.0318.0221.0154.0107.0075.0053.0037.0026.0013.000750.6080.3715.2281.1407.0872.0543.0339.0213.0134.0085.0054.0035.0022.0014.0009.0006.0003.0001Table 2Present Value of an Annuity of $1 Per Period for n Periodsi)i 1(1n−+− Number of Periods1%2%3%4%5%6%7%8%9%10%11%12%13%14%15%16%18%20%1.9901.9804.9709.9615.9524.9434.9346.9259.9174.9091.9009.8929.8850.8772.8696.8621.8475.83332 1.9704 1.9416 1.9135 1.8861 1.8594 1.8334 1.8080 1.7833 1.7591 1.7355 1.7125 1.6901 1.6681 1.6467 1.6257 1.6052 1.5656 1.52783 2.9410 2.8839 2.8286 2.7751 2.7232 2.6730 2.6243 2.5771 2.5313 2.4869 2.4437 2.4018 2.3612 2.3216 2.2832 2.2459 2.1743 2.10654 3.9020 3.8077 3.7171 3.6299 3.5460 3.4651 3.3872 3.3121 3.2397 3.1699 3.1024 3.0373 2.9745 2.9137 2.8550 2.7982 2.6901 2.58875 4.8534 4.7135 4.5797 4.4518 4.3295 4.2124 4.1002 3.9927 3.8897 3.7908 3.6959 3.6048 3.5172 3.4331 3.3522 3.2743 3.1272 2.99066 5.7955 5.6014 5.4172 5.2421 5.0757 4.9173 4.7665 4.6229 4.4859 4.3553 4.2305 4.1114 3.9975 3.8887 3.7845 3.6847 3.4976 3.32557 6.7282 6.4720 6.2303 6.0021 5.7864 5.5824 5.3893 5.2064 5.0330 4.8684 4.7122 4.5638 4.4226 4.2883 4.1604 4.0386 3.8115 3.604687.65177.32557.0197 6.7327 6.4632 6.2098 5.9713 5.7466 5.5348 5.3349 5.1461 4.9676 4.7988 4.6389 4.4873 4.3436 4.0776 3.837298.56608.16227.78617.43537.1078 6.8017 6.5152 6.2469 5.9952 5.7590 5.5370 5.3282 5.1317 4.9464 4.7716 4.6065 4.3030 4.0310109.47138.98268.53028.11097.72177.36017.0236 6.7101 6.4177 6.1446 5.8892 5.6502 5.4262 5.2161 5.0188 4.8332 4.4941 4.19251110.36769.78689.25268.76058.30647.88697.49877.1390 6.8052 6.4951 6.2065 5.9377 5.6869 5.4527 5.2337 5.0286 4.6560 4.32711211.255110.57539.95409.38518.86338.38387.94277.53617.1607 6.8137 6.4924 6.1944 5.9176 5.6603 5.4206 5.1971 4.7932 4.43921312.133711.348410.63509.98569.39368.85278.35777.90387.48697.1034 6.7499 6.4235 6.1218 5.8424 5.5831 5.3423 4.9095 4.53271413.003712.106211.296110.56319.89869.29508.74558.24427.78627.3667 6.9819 6.6282 6.3025 6.0021 5.7245 5.4675 5.0081 4.61061513.865112.849311.937911.118410.37979.71229.10798.55958.06077.60617.1909 6.8109 6.4624 6.1422 5.8474 5.5755 5.0916 4.67551614.717913.577712.561111.652310.837810.10599.44668.85148.31267.82377.3792 6.9740 6.6039 6.2651 5.9542 5.6685 5.1624 4.72961715.562314.291913.166112.165711.274110.47739.76329.12168.54368.02167.54887.1196 6.7291 6.3729 6.0472 5.7487 5.2223 4.77461816.398314.992013.753512.659311.689610.827610.05919.37198.75568.20147.70167.2497 6.8399 6.4674 6.1280 5.8178 5.2732 4.81221917.226015.678514.323813.133912.085311.158110.33569.60368.95018.36497.83937.3658 6.9380 6.5504 6.1982 5.8775 5.3162 4.84352018.045616.351414.877513.590312.462211.469910.59409.81819.12858.51367.96337.46947.0248 6.6231 6.2593 5.9288 5.3527 4.86962118.857017.011215.415014.029212.821211.764110.835510.01689.29228.64878.07517.56207.1016 6.6870 6.3125 5.9731 5.3837 4.89132219.660417.658015.936914.451113.163012.041611.061210.20079.44248.77158.17577.64467.1695 6.7429 6.3587 6.0113 5.4099 4.90942320.455818.292216.443614.856813.488612.303411.272210.37119.58028.88328.26647.71847.2297 6.7921 6.3988 6.0442 5.4321 4.92452421.243418.913916.935515.247013.798612.550411.469310.52889.70668.98478.34817.78437.2829 6.8351 6.4338 6.0726 5.4509 4.93712522.023219.523517.413115.622114.093912.783411.653610.67489.82269.07708.42177.84317.3300 6.8729 6.4641 6.0971 5.4669 4.94763025.807722.396519.600417.292015.372513.764812.409011.257810.27379.42698.69388.05527.49577.0027 6.5660 6.1772 5.5168 4.97894032.834727.355523.114819.792817.159115.046313.331711.924610.75749.77918.95118.24387.63447.1050 6.6418 6.2335 5.5482 4.99665039.196131.423625.729821.482218.255915.761913.800712.233510.96179.91489.04178.30457.67527.13276.66056.24635.55414.9995Table 3 Future Value of $1 at the End of n Periods n)i1(+Period1%2%3%4%5%6%7%8%9%10%11%12%13%14%15%16%18%20%1 1.0100 1.0200 1.0300 1.0400 1.0500 1.0600 1.0700 1.0800 1.0900 1.1000 1.1100 1.1200 1.1300 1.1400 1.1500 1.1600 1.1800 1.20002 1.0201 1.0404 1.0609 1.0816 1.1025 1.1236 1.1449 1.1664 1.1881 1.2100 1.2321 1.2544 1.2769 1.2996 1.3225 1.3456 1.3924 1.44003 1.0303 1.0612 1.0927 1.1249 1.1576 1.1910 1.2250 1.2597 1.2950 1.3310 1.3676 1.4049 1.4429 1.4815 1.5209 1.5609 1.6430 1.72804 1.0406 1.0824 1.1255 1.1699 1.2155 1.2625 1.3108 1.3605 1.4116 1.4641 1.5181 1.5735 1.6305 1.6890 1.7490 1.8106 1.9388 2.07365 1.0510 1.1041 1.1593 1.2167 1.2763 1.3382 1.4026 1.4693 1.5386 1.6105 1.6851 1.7623 1.8424 1.9254 2.0114 2.1003 2.2878 2.48836 1.0615 1.1262 1.1941 1.2653 1.3401 1.4185 1.5007 1.5869 1.6771 1.7716 1.8704 1.9738 2.0820 2.1950 2.3131 2.4364 2.6996 2.98607 1.0721 1.1487 1.2299 1.3159 1.4071 1.5036 1.6058 1.7138 1.8280 1.9487 2.0762 2.2107 2.3526 2.5023 2.6600 2.8262 3.1855 3.58328 1.0829 1.1717 1.2668 1.3686 1.4775 1.5938 1.7182 1.8509 1.9926 2.1436 2.3045 2.4760 2.6584 2.8526 3.0590 3.2784 3.7589 4.29989 1.0937 1.1951 1.3048 1.4233 1.5513 1.6895 1.8385 1.9990 2.1719 2.3579 2.5580 2.7731 3.0040 3.2519 3.5179 3.8030 4.4355 5.159810 1.1046 1.2190 1.3439 1.4802 1.6289 1.7908 1.9672 2.1589 2.3674 2.5937 2.8394 3.1058 3.3946 3.7072 4.0456 4.4114 5.2338 6.191711 1.1157 1.2434 1.3842 1.5395 1.7103 1.8983 2.1049 2.3316 2.5804 2.8531 3.1518 3.4785 3.8359 4.2262 4.6524 5.1173 6.17597.430112 1.1268 1.2682 1.4258 1.6010 1.7959 2.0122 2.2522 2.5182 2.8127 3.1384 3.4985 3.8960 4.3345 4.8179 5.3503 5.93607.28768.916113 1.1381 1.2936 1.4685 1.6651 1.8856 2.1329 2.4098 2.7196 3.0658 3.4523 3.8833 4.3635 4.8980 5.4924 6.1528 6.88588.599410.699314 1.1495 1.3195 1.5126 1.7317 1.9799 2.2609 2.5785 2.9372 3.3417 3.7975 4.3104 4.8871 5.5348 6.26137.07577.987510.147212.839215 1.1610 1.3459 1.5580 1.8009 2.0789 2.3966 2.7590 3.1722 3.6425 4.1772 4.7846 5.4736 6.25437.13798.13719.265511.973715.407016 1.1726 1.3728 1.6047 1.8730 2.1829 2.5404 2.9522 3.4259 3.9703 4.5950 5.3109 6.13047.06738.13729.357610.748014.129018.488417 1.1843 1.4002 1.6528 1.9479 2.2920 2.6928 3.1588 3.7000 4.3276 5.0545 5.8951 6.86607.98619.276510.761312.467716.672222.186118 1.1961 1.4282 1.7024 2.0258 2.4066 2.8543 3.3799 3.9960 4.7171 5.5599 6.54367.69009.024310.575212.375514.462519.673326.623319 1.2081 1.4568 1.7535 2.1068 2.5270 3.0256 3.6165 4.3157 5.1417 6.11597.26338.612810.197412.055714.231816.776523.214431.948020 1.2202 1.4859 1.8061 2.1911 2.6533 3.2071 3.8697 4.6610 5.6044 6.72758.06239.646311.523113.743516.366519.460827.393038.337621 1.2324 1.5157 1.8603 2.2788 2.7860 3.3996 4.1406 5.0338 6.10887.40028.949210.803813.021115.667618.821522.574532.323846.005122 1.2447 1.5460 1.9161 2.3699 2.9253 3.6035 4.4304 5.4365 6.65868.14039.933612.100314.713817.861021.644726.186438.142155.206123 1.2572 1.5769 1.9736 2.4647 3.0715 3.8197 4.7405 5.87157.25798.954311.026313.552316.626620.361624.891530.376245.007666.247424 1.2697 1.6084 2.0328 2.5633 3.2251 4.0489 5.0724 6.34127.91119.849712.239215.178618.788123.212228.625235.236453.109079.496825 1.2824 1.6406 2.0938 2.6658 3.3864 4.2919 5.4274 6.84858.623110.834713.585517.000121.230526.461932.919040.874262.668695.396230 1.3478 1.8114 2.4273 3.2434 4.3219 5.74357.612310.062713.267717.449422.892329.959939.115950.950266.211885.8499143.3706237.376340 1.4889 2.2080 3.2620 4.80107.040010.285714.974521.724531.409445.259365.000993.0510132.7816188.8835267.8635378.7212750.37831469.771650 1.6446 2.6916 4.38397.106711.467418.420229.457046.901674.3575117.3909184.5648289.0022450.7359700.23301083.65741670.70403927.35709100.4382Table 4 Sum of an Annuity of $1 Per Period for n Periodsi 1)i1(n−+NumberofPeriods1%2%3%4%5%6%7%8%9%10%11%12%13%14%15%16%18%20%1 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000 1.00002 2.0100 2.0200 2.0300 2.0400 2.0500 2.0600 2.0700 2.0800 2.0900 2.1000 2.1100 2.1200 2.1300 2.1400 2.1500 2.1600 2.1800 2.20003 3.0301 3.0604 3.0909 3.1216 3.1525 3.1836 3.2149 3.2464 3.2781 3.3100 3.3421 3.3744 3.4069 3.4396 3.4725 3.5056 3.5724 3.64004 4.0604 4.1216 4.1836 4.2465 4.3101 4.3746 4.4399 4.5061 4.5731 4.6410 4.7097 4.7793 4.8498 4.9211 4.9934 5.0665 5.2154 5.36805 5.1010 5.2040 5.3091 5.4163 5.5256 5.6371 5.7507 5.8666 5.9847 6.1051 6.2278 6.3528 6.4803 6.6101 6.7424 6.87717.15427.44166 6.1520 6.3081 6.4684 6.6330 6.8019 6.97537.15337.33597.52337.71567.91298.11528.32278.53558.75378.97759.44209.929977.21357.43437.66257.89838.14208.39388.65408.92289.20049.48729.783310.089010.404710.730511.066811.413912.141512.915988.28578.58308.89239.21429.54919.897510.259810.636611.028511.435911.859412.299712.757313.232813.726814.240115.327016.499199.36859.754610.159110.582811.026611.491311.978012.487613.021013.579514.164014.775715.415716.085316.785817.518519.085920.79891010.462210.949711.463912.006112.577913.180813.816414.486615.192915.937416.722017.548718.419719.337320.303721.321523.521325.9587 1111.566812.168712.807813.486414.206814.971615.783616.645517.560318.531219.561420.654621.814323.044524.349325.732928.755132.1504 1212.682513.412114.192015.025815.917116.869917.888518.977120.140721.384322.713224.133125.650227.270729.001730.850234.931139.5805 1313.809314.680315.617816.626817.713018.882120.140621.495322.953424.522726.211628.029129.984732.088734.351936.786242.218748.4966 1414.947415.973917.086318.291919.598621.015122.550524.214926.019227.975030.094932.392634.882737.581140.504743.672050.818059.1959 1516.096917.293418.598920.023621.578623.276025.129027.152129.360931.772534.405437.279740.417543.842447.580451.659560.965372.0351 1617.257918.639320.156921.824523.657525.672527.888130.324333.003435.949739.189942.753346.671750.980455.717560.925072.939087.4421 1718.430420.012121.761623.697525.840428.212930.840233.750236.973740.544744.500848.883753.739159.117665.075171.673087.0680105.9306 1819.614721.412323.414425.645428.132430.905733.999037.450241.301345.599250.395955.749761.725168.394175.836484.1407103.7403128.1167 1920.810922.840625.116927.671230.539033.760037.379041.446346.018551.159156.939563.439770.749478.969288.211898.6032123.4135154.7400 2022.019024.297426.870429.778133.066036.785640.995545.762051.160157.275064.202872.052480.946891.0249102.4436115.3797146.6280186.6880 2123.239225.783328.676531.969235.719339.992744.865250.422956.764564.002572.265181.698792.4699104.7684118.8101134.8405174.0210225.0256 2224.471627.299030.536834.248038.505243.392349.005755.456862.873371.402781.214392.5026105.4910120.4360137.6316157.4150206.3448271.0307 2325.716328.845032.452936.617941.430546.995853.436160.893369.531979.543091.1479104.6029120.2048138.2970159.2764183.6014244.4868326.2369 2426.973530.421934.426539.082644.502050.815658.176766.764876.789888.4973102.1742118.1552136.8315158.6586184.1678213.9776289.4945392.4842 2528.243232.030336.459341.645947.727154.864563.249073.105984.700998.3471114.4133133.3339155.6196181.8708212.7930249.2140342.6035471.9811 3034.784940.568147.575456.084966.438879.058294.4608113.2832136.3075164.4940199.0209241.3327293.1992356.7868434.7451530.3117790.94801181.8816 4048.886460.402075.401395.0255120.7998154.7620199.6351259.0565337.8824442.5926581.8261767.09141013.70421342.02511779.09032360.75724163.21307343.8578 5064.463284.5794112.7969152.6671209.3480290.3359406.5289573.7702815.08361163.90851668.77122400.01823459.50714994.52137217.716310435.648821813.093745497.1908。

cpa canada fa3 第二章作业