宏观经济学习题答案第十六章 习题答案

高鸿业《宏观经济学》课后习题答案第十六章习题答案

第十六章宏观经济政策实践1.政府的财政收入政策通过哪一个因素对国民收入产生影响?A.政府转移支付;B.政府购买;C.消费支出;D.出口。

解答:C2.假定政府没有实行财政政策,国民收入水平的提高可能导致()。

A.政府支出增加;B.政府税收增加;C.政府税收减少;D.政府财政赤字增加。

解答:B3.扩张性财政政策对经济的影响是()。

A.缓和了经济萧条但增加了政府债务;B.缓和了萧条也减轻了政府债务;C.加剧了通货膨胀但减轻了政府债务;D.缓和了通货膨胀但增加了政府债务。

解答:A4.商业银行之所以会有超额储备,是因为()。

A.吸收的存款太多;B.未找到那么多合适的贷款对象;C.向中央银行申请的贴现太多;D.以上几种情况都有可能。

解答:B5.市场利率提高,银行的准备金会()。

A.增加;B.减少;C.不变;D.以上几种情况都有可能。

解答:B6.中央银行降低再贴现率,会使银行准备金()。

A.增加;B.减少;C.不变;D.以上几种情况都有可能。

解答:A7.中央银行在公开市场卖出政府债券是试图()。

A.收集一笔资金帮助政府弥补财政赤字;B.减少商业银行在中央银行的存款;C.减少流通中的基础货币以紧缩货币供给;D.通过买卖债券获取差价利益。

解答:C8.什么是自动稳定器?是否边际税率越高,税收作为自动稳定器的作用越大?解答:自动稳定器是指财政制度本身所具有的减轻各种干扰对GDP的冲击的内在机制。

自动稳定器的内容包括政府所得税制度、政府转移支付制度、农产品价格维持制度等。

在混合经济中投资变动所引起的国民收入变动比纯粹私人经济中的变动要小,原因是当总需求由于意愿投资增加而增加时,会导致国民收入和可支配收入的增加,但可支配收入增加小于国民收入的增加,因为在国民收入增加时,税收也在增加,增加的数量等于边际税率乘以国民收入,结果混合经济中消费支出增加额要比纯粹私人经济中的小,从而通过乘数作用使国民收入累积增加也小一些。

同样,总需求下降时,混合经济中收入下降也比纯粹私人部门经济中要小一些。

高鸿业版宏观经济学课后习题及答案

西方经济学课后习题答案说明1.授课教材——高鸿业主编:《西方经济学》(下册宏观部分),北京:中国经济出版社,1996。

2.课后习题范围为:第十三章至第十七章。

3.目前所给出的习题答案主要包括以上各章计算题,其他习题一般可以从书本知识或读者自学解决。

第十三章西方国民收入核算3.在统计中,社会保险税增加对GNP、NNP、NI、PI和DPI这五个总量中哪个总量有影响?为什么?答:因为社会保险税是直接税,故GNP、NNP、NI均不受其影响,又因为它是由企业上缴的职工收入中的一部分,所以PI和DPI均受其影响。

4.如果甲乙两国并成一个国家,对GNP总和会有什么影响?(假定两国产出不变)答:假定不存在具有双重居民身份的情况,则合并对GNP总和没有影响。

因为原来甲国居民在乙国的产出已经计入甲国的GNP,同样,乙国居民在甲国的产出已经计入乙国的GNP。

在存在双重居民身份生产者的情况下,则GNP减少。

5.从下列资料中找出:(1) 国民收入(2) 国民生产净值(3) 国民生产总值(4) 个人收入(5) 个人可支配收入(6) 个人储蓄答:(1) 国民收入=雇员佣金+企业利息支付+个人租金收入+公司利润+非公司企业主收入(2) 国民生产净值=国民收入+间接税(3) 国民生产总值=国民生产净值+资本消耗补偿(4) 个人收入=国民收入-公司利润-社会保障税+红利+政府和企业转移支付(5) 个人可支配收入=个人收入-个人所得税(6)个人储蓄=个人可支配收入-个人消费支出-消费者支付的利息6试计算:(1) 国民生产净值(2)净出口(3)政府收入减去转移支付后的收入(4) 个人可支配收入(5)个人储蓄答:(1)国民生产净值=GNP-(总投资折旧-净投资)=4800-(800-300)=4300(2)净出口=GNP-(消费+总投资+政府购买)=4800-(3000+800+960)=40(3)政府税收减去转移支付后的收入=政府购买+政府预算盈余=960+30=990(4)个人可支配收入=NNP-税收+政府转移支付=NNP-(税收-政府转移支付)=4300-990=3310(5)个人储蓄=个人可支配收入-消费=3310-3000=3107.假设国民生产总值是5000,个人可支配收入是4100,政府预算赤字是200,消费是3800,贸易赤字是100(单位:亿元),试计算:(1) 储蓄(2) 政府支出(3) 投资答:(1)储蓄=DPI-C=4100-3800=300(2)因为:I+G+(X-M)=S+T所以:I=S+(T-G)-(X-M)=300-200-(-100)=200(3)政府支出G=1100第十四章简单国民收入决定理论2.在均衡产出水平上,是否计划存货投资和非计划存货投资都必然为零?答:在均衡产出水平上,计划存货投资不一定为0,而非计划存货投资则应该为0。

高鸿业版 宏观经济学每章课后习题答案全

第十二章国民收入核算1.宏观经济学和微观经济学有什么联系和区别?为什么有些经济活动从微观看是合理的,有效的,而从宏观看却是不合理的,无效的?解答:两者之间的区别在于:(1)研究的对象不同。

微观经济学研究组成整体经济的单个经济主体的最优化行为,而宏观经济学研究一国整体经济的运行规律和宏观经济政策。

(2)解决的问题不同。

微观经济学要解决资源配置问题,而宏观经济学要解决资源利用问题。

(3)中心理论不同。

微观经济学的中心理论是价格理论,所有的分析都是围绕价格机制的运行展开的,而宏观经济学的中心理论是国民收入(产出)理论,所有的分析都是围绕国民收入(产出)的决定展开的。

(4)研究方法不同。

微观经济学采用的是个量分析方法,而宏观经济学采用的是总量分析方法。

两者之间的联系主要表现在:(1)相互补充。

经济学研究的目的是实现社会经济福利的最大化。

为此,既要实现资源的最优配置,又要实现资源的充分利用。

微观经济学是在假设资源得到充分利用的前提下研究资源如何实现最优配置的问题,而宏观经济学是在假设资源已经实现最优配置的前提下研究如何充分利用这些资源。

它们共同构成经济学的基本框架。

(2)微观经济学和宏观经济学都以实证分析作为主要的分析和研究方法。

(3)微观经济学是宏观经济学的基础。

当代宏观经济学越来越重视微观基础的研究,即将宏观经济分析建立在微观经济主体行为分析的基础上。

由于微观经济学和宏观经济学分析问题的角度不同,分析方法也不同,因此有些经济活动从微观看是合理的、有效的,而从宏观看是不合理的、无效的。

例如,在经济生活中,某个厂商降低工资,从该企业的角度看,成本低了,市场竞争力强了,但是如果所有厂商都降低工资,则上面降低工资的那个厂商的竞争力就不会增强,而且职工整体工资收入降低以后,整个社会的消费以及有效需求也会降低。

同样,一个人或者一个家庭实行节约,可以增加家庭财富,但是如果大家都节约,社会需求就会降低,生产和就业就会受到影响。

宏观经济学第十六章课后练习参考答案

第十六章课后练习·参考答案( P482-483 )1.3)政府的财政政策有收入政策和支出政策,收入政策比如税收政策通过影响可支配收入进而影响消费,最终传导到对国民收入的影响。

2.2)假如政府没有实行财政政策,由于自动稳定器的作用,当国民收入提高后,政府税收会自动增加(因为所得税通常是比例税或累进税)。

3.1)扩张性财政政策比如减税、增加政府购买支出或增加转移支付等,会使总需求和国民收入增加,有助于缓和经济萧条,但扩张性的财政政策通常导致财政赤字,这无疑增加了政府的债务。

4.2)商业银行吸收存款以后,通常是尽可能地把它们贷出去,以获得最大的利润,但如果贷款风险太大,找不到合适的贷款对象或投资机会,宁可持有较多的超额储备也不愿意贷出去,即出现“惜贷”现象,这通常发生在经济不景气的萧条或衰退时期。

商业银行不会是在没有好的贷款对象或投资机会之前,就向中央银行申请过多的贴现,而是预计有好的贷款或投资机会而手中的储备不足又没有其他更好的借款可能时,才向中央银行申请贴现。

所以商业银行有超额储备的主要原因既不是吸收的存款过多,也不是向中央银行申请的贴现太多,更可能是没有找到合适的贷款对象或投资机会。

5.2)这里的准备金应该是指超额准备金。

市场利率提高后,从银行的角度来说,因为持有超额准备金的机会成本增大了,所以当然希望减少超额准备金,尽可能地把它们贷放出去。

从企业和消费者的角度来说,通常市场利率提高对应经济过热时期,此时投资的预期收益率也在上升,商品的价格也在上升,投资和消费的需求比较旺盛,政府希望通过提高利率来抑制过热的投资需求和消费需求,进而压低过度的总需求。

所以市场利率提高后,投资和消费是否会减少,取决于投资的预期收益率和商品价格的上升幅度是否大于利率的提高幅度,如果前者大于后者,那么投资和消费不会减少,企业和消费者仍然愿意增加贷款,如果前者小于后者,那么利率的提高就会抑制一部分投资和消费需求。

高鸿业《宏观经济学》课后习题答案第十六章 习题答案

第十六章宏观经济政策实践1.政府的财政收入政策通过哪一个因素对国民收入产生影响A.政府转移支付;B.政府购买;C.消费支出;D.出口。

解答:C2.假定政府没有实行财政政策,国民收入水平的提高可能导致()。

A.政府支出增加;-B.政府税收增加;C.政府税收减少;D.政府财政赤字增加。

解答:B3.扩张性财政政策对经济的影响是()。

A.缓和了经济萧条但增加了政府债务;B.缓和了萧条也减轻了政府债务;C.加剧了通货膨胀但减轻了政府债务;D.缓和了通货膨胀但增加了政府债务。

"解答:A4.商业银行之所以会有超额储备,是因为()。

A.吸收的存款太多;B.未找到那么多合适的贷款对象;C.向中央银行申请的贴现太多;D.以上几种情况都有可能。

解答:B5.市场利率提高,银行的准备金会()。

|A.增加;B.减少;C.不变;D.以上几种情况都有可能。

解答:B6.中央银行降低再贴现率,会使银行准备金()。

A.增加;B.减少;C.不变;&D.以上几种情况都有可能。

解答:A7.中央银行在公开市场卖出政府债券是试图()。

A.收集一笔资金帮助政府弥补财政赤字;B.减少商业银行在中央银行的存款;C.减少流通中的基础货币以紧缩货币供给;D.通过买卖债券获取差价利益。

解答:C-8. 什么是自动稳定器是否边际税率越高,税收作为自动稳定器的作用越大解答:自动稳定器是指财政制度本身所具有的减轻各种干扰对GDP的冲击的内在机制。

自动稳定器的内容包括政府所得税制度、政府转移支付制度、农产品价格维持制度等。

在混合经济中投资变动所引起的国民收入变动比纯粹私人经济中的变动要小,原因是当总需求由于意愿投资增加而增加时,会导致国民收入和可支配收入的增加,但可支配收入增加小于国民收入的增加,因为在国民收入增加时,税收也在增加,增加的数量等于边际税率乘以国民收入,结果混合经济中消费支出增加额要比纯粹私人经济中的小,从而通过乘数作用使国民收入累积增加也小一些。

曼昆《宏观经济学》(第10版)笔记和课后习题详解 第16章 关于稳定化政策的不同观点【圣才出品】

第16章关于稳定化政策的不同观点16.1复习笔记【知识框架】【考点难点归纳】考点一:积极的经济政策和消极的经济政策★★★1.积极的经济政策(1)观点当经济遭受冲击时,运用经济政策在能够稳定经济,防止产出和就业的不必要波动,进而保持国民经济平稳快速发展。

(2)具体含义积极政策的支持者认为经济经常遭受冲击,总需求与总供给模型说明了经济冲击可能引起衰退,衰退是高失业、低收入和经济困苦增加的时期。

经济政策在稳定经济上是成功的,宏观经济政策应该是“逆风而上”,即当经济萧条时刺激经济,而当经济过热时抑制经济。

凯恩斯是积极政策的最主要代表。

2.消极的经济政策(1)观点当经济遭受冲击时,受诸多因素的影响,运用经济政策可能会最终破坏经济的稳定,支持无为而治。

(2)不主张用政策干预经济的理由(见表16-1)表16-1不主张用政策干预经济的理由图16-1内在时滞与外在时滞的区分3.预期和卢卡斯批判(1)理性预期和适应性预期(见表16-2)表16-2理性预期和适应性预期(2)卢卡斯批判(见表16-3)表16-3卢卡斯批判考点二:斟酌处置政策与固定政策规则★★★★1.斟酌处置政策(见表16-4)表16-4斟酌处置政策2.固定政策规则(见表16-5)表16-5固定政策规则3.时间不一致性和通货膨胀与失业之间的权衡(1)假设①假定菲利普斯曲线描述了通货膨胀和失业之间的关系,失业可表示为:u=u n-α(π-Eπ)。

参数α决定了失业对出乎预期的通货膨胀的反应程度。

②假定中央银行选择通货膨胀率。

中央银行想要低失业与低通货膨胀,但要付出一定的成本。

将失业与通货膨胀的成本表示为:L(u,π)=u+γπ2。

式中,参数γ为相对于失业而言中央银行对通货膨胀的厌恶程度。

L(u,π)被称为损失函数,中央银行的目标是最小化损失。

(2)考虑固定政策规则的货币政策固定政策规则要求中央银行把通货膨胀固定在某一特定水平,只要私人主体相信中央银行对这个规则作出的承诺,预期的通货膨胀水平就将是中央银行所承诺的水平。

《宏观经济学教程》习题答案

《宏观经济学教程》教材习题参考答案第一章总产出二、分析与思考1,在总产值中包含着中间产品的价值,如果以各部门的产值总和来合算总产出,则会出现重复计算。

2,因为这只是证券资产的交易,在这种交易中获得的利润或蒙受的损失与本期生产无关。

3,可能会,因为销售的产品可能是上年生产的产品。

GDP与GNP应该以后者,即本年生产的最终产品为口径。

因为它是用来衡量国家当年总产出水平的量的。

4,不是,因为个人可支配收入是GNP或GDP中减去折旧、间接税、公司利润、社会保障支付、个人所得税,再加上转移支付得到的。

5,购买住宅属于投资行为,因为西方国家的消费者购买或建造住宅一般都是使用银行贷款,而且住宅也像企业的固定资产一样,是一次购买、长期使用、逐步消耗的。

6,一般中间产品在当期生产中全部被消耗掉,其价值完全包含在产品的销售价格中。

而,固定资产在生产过程中则是被逐步消耗的,计入当期产品生产成本的仅仅是固定资产中部分被消耗掉的价值,即折旧。

7,不是。

因为总支出包括消费,投资,政府购买和净出口,并不只是在消费最终产品上。

8,不是。

总产出包括的是净出口,对外贸易规模大,如果进口大于出口,则总产出规模不会因对外贸易规模大而变大。

9,可以。

因为名义GDP与实际GDP的比率是消费价格平减指数,平减指数可以衡量物价水平变化,所以可用来衡量通货膨胀率。

10,不一定。

因为购买力平价在计算时有样本选择的典型性与权重确定上的困难,不能很好地反映两国货币实际比率。

三、计算题1,解:Y = C + I + G + NXGNP=8000+5000+2500+2000-1500=16000NNP= GNP-折旧NNP=16000-500=15500NI= NNP-间接税NI=15500-2000=13500PI=NI-公司未分配利润-公司所得税和社会保险税 + 政府转移支付PI=13500+500=14000DPI=PI-个人所得税DPI=14000-(3000-2000)=13000第二章 消费、储蓄与投资二、分析与思考1,不包括公共产品的消费。

人大宏观经济学课件ch15-16习题答案

第15-16章财政政策与货币政策一.单项选择1.d; 2.d; 3.d; 4.b; 5.c; 6.a; 7.b; 8.a; 9.d;10.a; 11.c; 12.d; 13.b; 14.b; 15.a; 16.d; 17.a; 18.c;19.d; 20.b; 21.b; 22.a; 23.c; 24.c; 25.b; 26.b; 27.b;28.a; 29.a; 30.c; 31.b; 32.d; 33.b; 34.c; 35.c;36.c; 37.a; 38.a; 39.b; 40.b; 41.c; 42.a; 43.a; 44.b;45.c; 46.a ; 47.a; 48.d; 49.c; 50.d。

二.多项选择1.abcd; 2.cd; 3.ab; 4.cd; 5.bcd; 6.bcd; 7.ac; 8.abc;9.ab; 10.acd; 11.bcd; 12.abd; 13.ad; 14.bd; 15.abcd;16.bcd; 17.ad; 18.ab。

三、名词解释1.财政政策是指为促进就业水平提高,减轻经济波动,防止通货膨胀,实现稳定增长而对政府支出、税收和借债水平所进行的选择,或对政府收入和支出水平所作出的决策。

2.功能财政是指政府在财政方面的积极政策主要是为实现无通货膨胀的充分就业水平的产出和收入而努力,为实现这一目标时,预算可以是盈余,也可以是赤字。

3.补偿性财政政策是指根据经济的萧条和繁荣状况交替使用扩张性和紧缩性财政政策。

4.自动稳定器是指经济系统本身存在的一种会减少各种干扰对国民收入冲击的机制,能够在经济繁荣时期自动抑制膨胀,在经济萧条时期自动减轻衰退,毋须政府采取任何行动。

5.挤出效应是指政府支出增加所引起的私人消费或投资降低的作用。

6.拉弗曲线是指描绘税收与税率关系的曲线。

一般情况下,税率越高,政府的税收就越多。

但税率的提高超过一定的限度时,企业的投资减少,收入减少,即税基减小,反而导致政府的税收减少。

16宏观经济学英文版(多恩布什)课后习题答案全解

CHAPTER 16THE FED, MONEY, AND CREDITSolutions to the Problems in the Textbook:Conceptual Problems:1. The three tools the Fed has to conduct monetary policy are open market operations, discount ratechanges, and reserve requirement changes. If the Fed wants to increase the money supply, it has the following options: first, the Fed can buy government bonds from the public (mostly banks), thereby increasing bank reserves. These open market purchases will induce banks to extend their loans, which will create more money. Second, it can lower the discount rate, so it becomes less costly for banks to borrow reserves from the Fed. This also will induce banks to create more money by extending more loans. Finally, the Fed can lower the required-reserve ratio, which again will allow banks to lend more.2. The currency-deposit ratio is the ratio of currency outstanding to bank deposits. The Fed cannotdirectly influence this ratio, since it is determined by the behavior of the public and influenced by the convenience of obtaining cash and by seasonal patterns (increased Christmas shopping, for example).However, by changing either bank regulations (that would affect the ease of obtaining cash) or interest rates (that would change the opportunity cost of holding cash), the Fed may indirectly affect how much currency the public is willing to hold.3.a. 3.a.ii2i2i1 i10 0Y2 Y1 Y Y1 Y2 YIf most disturbances come from the money sector (a shift in money demand), interest rate targets work better than money targets. In the IS-LM diagram below we can see that as money demand increases due to changing expectations, the LM-curve will shift to the left and the interest rate will increase. By increasing money supply and shifting the LM-curve back to the right, the central bank can get the economy back to the original equilibrium.3.b. If most disturbances come from the expenditure sector, the central bank is better off targeting moneysupply. If spending increases, the IS-curve shifts to the right and the interest rate increases. If the central bank tried to get the interest rate back to its original level by increasing money supply, the disturbance would intensify, since the LM-curve would also shift to the right. Thus, the central bank should keep money supply (and thus the LM-curve) stable to keep the disturbance at a minimum.4.a. A bank run occurs when depositors, worried about the safety of their assets, rush to withdraw theirdeposits.4.b. If a bank is in trouble because it has made some bad investment decisions, people may expect it tofail. Thus they may want to withdraw their deposits before it is too late. Since other depositors are1likely to behave in the same way, a run on the bank can be anticipated. Even a fairly financially sound bank may not be able to withstand a run, since most assets are tied up in loans. Almost all U.S. banks are FDIC insured and therefore a run on a bank is very unlikely. With FDIC insurance, depositors know that they can get at least their principal back from the government should a bank fail, and therefore they do not panic easily.4.c. During the Great Depression, a large-scale run on banks lead to liquidity problems and bank failures.This decreased the lending power of the whole banking system. In other words, depositors lost their confidence in banks and withdraw their deposits. This increased the currency-deposit ratio, leading toa decrease in the money multiplier and a contraction in money supply.4.d. The existence of the FDIC increases the public's confidence in the banking system, so a run on banksis highly unlikely. Therefore the currency-deposit ratio is low and the value of the money multiplier is high. The money multiplier is also more stable since the public does not withdraw deposits any time a bank failure occurs.5.a. There are basically two reasons why the Fed does not adhere more closely to its monetary growthtargets in the short run. The first is technical: due to the variability of the money multiplier and the lag in collecting data on money supply figures, the Fed is not always able to achieve its monetary growth target. The second reason is that the Fed, in the short run, uses interest rate targets concurrently with monetary growth targets, and it is impossible to succeed at both at the same time. Therefore, as the Fed responds to changes in the economy, it may move away at least temporarily from its monetary growth target. The Fed's desire to have some short-run flexibility while still maintaining long-run credibility, may cause a temporary deviation from the announced monetary growth target.5.b. The targeting of nominal interest rates can be self-defeating, especially in times of high inflation. If(nominal) interest rates increase, the Fed has to increase money supply to reduce interest rates to their original level. However, expansionary monetary policy will lead to more inflation and this will ultimately result in higher nominal interest rates. The so-called Fisher-equation states that the nominal interest rate (i n) is equal to the real interest rate (i r) plus the rate of inflation (π), that is,i n = i r + π.In the long run, the real interest rate will not be affected by expansionary monetary policy, but the nominal interest rate will be higher due to increased inflation. Another attempt to further reduce the nominal interest rate by expanding money supply even more will aggravate inflation even more and ultimately not succeed in bringing interest rates down.6.a. Nominal GDP is an ultimate target of monetary policy.6.b. The discount rate is an instrument of monetary policy.6.c. The monetary base is an immediate target of monetary policy.6.d. M1 is an intermediate target of monetary policy.6.e. The Treasury bill rate is an intermediate target of monetary policy.6.f. The unemployment rate is an ultimate target of monetary policy.7. When banks ration credit, interest rates are no longer a good indication of existing market conditions.Credit is rationed when lending institutions limit the amount that their customers can borrow based on concerns that such borrowing may not be financially prudent. In this situation, the Fed should not use interest rate targets as a guide for its monetary policy, since interest rates no longer reflect true market conditions.8. The Fed has much more control over intermediate targets (money supply or interest rates) than it doesover ultimate targets (GDP, unemployment, or inflation). Changes in these intermediate targets do not have an immediate effect on the ultimate targets and therefore the Fed can easily reverse or re-enforce its policy measure. Because of the long lags associated with monetary policy, the Fed uses these2intermediate targets to get feedback on the effects of a policy change and the likeliness that a policy measure will achieve its ultimate goal. However, concentrating solely on intermediate targets does not guarantee that the ultimate objectives will be achieved.9. From the quantity theory of money equation MV = PY, we get%∆M + %∆V = %∆P + %∆Y ==> %∆P = %∆M - %∆Y + %∆V.If real GDP (Y) is assumed to grow at a rate of 3.5%, the Fed has to let money supply (M) grow at a rate of 3.5% to keep prices (P) stable, assuming that velocity (V) remains stable. The Fed can control nominal GDP through changes in nominal money supply only as long as the behavior of money demand (and thus velocity) is relatively predictable. The long-run GDP growth rate has been around2.25%, far below the3.5% mentioned here, and expansionary monetary policy will not achieve such ahigh growth rate. But there is a very close relationship between money supply changes and price changes in the long run, while real GDP growth is primarily influenced by other factors. If the Fed overestimates the rate at which potential GDP grows, then it is likely to stimulate the economy too much and induce high inflation. Therefore, nominal GDP targeting rather than real GDP targeting may be a better approach, since the former creates a policy tradeoff between unemployment and inflation. In other words, we will get less growth but also less inflation if potential GDP growth is overestimated.Technical Problems:1. Assume the Fed sells Treasury bills valued at $10 million to a bank.Fed Balance Sheet: Assets LiabilitiesGovt. securities - $10 Currency 0Other assets 0 Bank deposits - $10 Bank Balance Sheet: Assets LiabilitiesDeposits at the Fed - $10 Deposits 0Govt. securities + $10Other assets 0The bank has now lost $10 million in reserves (deposits at the Fed). If required reserves are no longer sufficient, then the bank will have to acquire new reserves.If a bank depositor buys the Treasury bills, then the balance sheet will be:Bank Balance Sheet: Assets LiabilitiesReserves - $10 Deposits - $10Other assets 0Again, the bank may have to make up for the loss of reserves.2. Assume the Fed buys $10 million worth of gold and then decides to sterilize the effect of thispurchase on the monetary base through open market operations.Fed Balance Sheet: Assets LiabilitiesGold + $10 Currency 0Other assets 0 Member bank deposit + $10 The purchase of gold increased the monetary base (bank reserves) by $10 million.Fed Balance SheetAfter Sterilization: Assets LiabilitiesGold + $10 Bank deposits (+10 -10) = $0Govt. securities - $103The sale of government securities to banks again decreased the monetary base (bank reserves) by $10 million, so there is no overall change in the monetary base.3.a. If the reserve-deposit ratio is 100%, then banks cannot create any loans and the money multiplier isequal to 1. This means that the Fed has total control over the money supply, since it has control over bank reserves. However, this would significantly change the banking industry, since banks no longer would be able to extend loans.3.b. Since banks would not be able to issue any loans, the assets side would contain only reserves.3.c. Banking could still remain profitable as long as banks were able to generate service charges to covertheir operating costs.4.In deciding whether monetary base targeting or interest rate targeting is better for the Fed in itsconduct of monetary policy, it would be good to know whether the goods sector or the money sector is more prone to disturbances. If most disturbances occur in the goods sector (assume the IS-curve shifts to the right), then monetary base targeting is better, since interest rate targets would force the Fed to aggravate the disturbance. Under interest rate targeting, the Fed would be forced to change money supply (shifting the LM-curve to the right) and aggregate demand would be changed even more. If most disturbances occur in the money sector (assume the LM-curve shifts to the left), then interest rate targeting is better, since the Fed can easily offset the disturbance. Under interest rate targeting the Fed could change money supply (shifting the LM-curve to the right again) without affecting aggregate demand.ii2i2i1 i1Y2 Y1 Y Y1 Y2 YAdditional Problems:1. How does an increase in the currency-deposit ratio affect the money multiplier? What is theeffect of an increase in the reserve-deposit ratio?The money multiplier is defined as mm = (1 + cu)/(cu + re), wherecu = CU/D = currency-deposit ratio, andre = R/D = reserve-deposit ratio.An increase in the currency-deposit ratio means that people hold more currency and banks have fewer funds to create deposits. Therefore the money multiplier decreases. An increase in the reserve-deposit ratio means that banks now hold more reserves, so fewer deposits can be created. Again, the money multiplier decreases.42. Assume that an increasing number of department and grocery stores accept credit and debitcards and more consumers use these cards to do their shopping. How will the money multiplier and money supply be affected?If more consumers make purchases using credit or debit cards rather than cash, then less currency is held and the currency-deposit ratio will be lower. This implies a larger money multiplier and, given a fixed stock of high-powered money, an increase in money supply.3. "The introduction of the FDIC after the Great Depression not only calmed the worries of thepublic but also made monetary policy easier for the Fed." Comment on this statement.The introduction of the FDIC lowered the public's fear of new bank failures. Consumer confidence in the banking system increased and people held less currency. Banks also were able to reduce their excess reserves, since they no longer feared a widespread bank run. The currency-deposit and the reserve-deposit ratios both declined, and the size of the money multiplier increased. In addition, the money multiplier became more stable, since consumers became less likely to panic after a bank failure occurred. The larger and the more stable the money multiplier, the easier it is for the Fed to control money supply by changing the monetary base through open market operations.4. Assume money supply (M) is $1,200 billion, total bank deposits (D) are $800 billion and therequired reserve-deposit ratio is 10%. What would the Fed have to do to lower money supply by 5%? Explain your answer.We know that M = CU + D ==> CU = M - D = 1,200 - 800 = 400.If we assume that banks do not hold excess reserves, thenR = (0.1)D = (0.1)800 = 80 and H = CU + R = 400 + 80 = 480.Thus the money multiplier is M/H = mm = 1,200/480 = 2.5.If the Fed wants to reduce money supply by 5% or $60 billion, it has to reduce high-powered money (H) by $24 billion, by selling $24 billion worth of Treasury bills. In other words,∆M = mm(∆H) == > - 60 = 2.5(∆H) ==> (∆H) = - 60/2.5 = - 245. Assume the currency-deposit ratio is 30%, the required reserve-deposit ratio is 8% and theexcess reserve-deposit ratio is 2%. How much would money supply change if the Fed made open market sales valued at $20 million?The money multiplier is defined as: M/H = mm = (1 + cu)/(cu + re).In this example the size of the money multiplier is equal tomm = (1 + 0.3)/(0.3 + 0.08 + 0.02) = (1.3)/(0.4) = 3.25.An open market sale valued at $20 million would decrease high-powered money (H) by $20 million. Therefore, money supply (M) would decrease by $65 million, since∆M = mm(∆H) = (3.25)(-20) = - 65.6. Assume bank deposits are $3,200 billion, the required reserve-deposit ratio is 10%, andcurrency outstanding is $400 billion. What should the Fed do to decrease money supply by $100 million?Ms = Cu + D = 400 + 3,200 = 3,600 and H = Cu + R = Cu + (0.1)D = 400 + 320 = 720==> money multiplier = Ms/H = mm = 3,600/720 = 5==> ∆Ms = mm(∆H) ==> - 100 = 5(∆H) ==> ∆H = - 20If the Fed wants to decrease money supply by $100 million, bank reserves have to be decreased by $20 million through the open market sale of government securities. (Note: The assumption was that excess reserves are zero, which may not be true.)7. True or false? Why?5"An open market sale raises the monetary base and therefore money supply."False. An open market sale occurs when the Fed sells government bonds to the private sector, primarily banks, in return for currency. Reserves held in the form of deposits at the Fed decrease, and therefore the monetary base (the stock of high-powered money) decreases as does money supply, since banks cannot loan out as much as previously.8. What problems would arise if the Fed tried to conduct open market operations via the stockmarket?Theoretically, the Fed could change high-powered money and thus the supply of money by buying and selling stocks. The problem, however, would be how to decide which stocks to buy and sell, since the Fed's actions would affect the values of the stocks being bought or sold.9. "Large open market sales may have a negative impact on the demand for money, the budgetsurplus, the income velocity of money, and consumption." Comment on this statement.Open market sales decrease bank reserves and therefore money supply. This increases interest rates, leading to a lower level of investment and income. Since income tax revenues decrease in a recession, the budget surplus will also decrease. Since interest rates are higher, the interest payments on the national debt will increase. A lower level of income means a lower level of consumption. The income velocity of money generally declines in a recession. However, the decline in money occurs before the decline in income. Thus we first see an increase in velocity in the short run, followed by a decrease.10. Which is the most useful tool for the Fed to conduct its monetary policy? In your answerdiscuss the advantages and disadvantages of each of the tools that the Fed has at its disposal. The Fed has three basic tools to conduct monetary policy are open market operations, discount rate changes, and reserve requirement changes.Open market operations are used most often by the Fed since it can be undertaken every business day, can be undertaken to a large or small degree, and can be easily reversed. Bank reserves are immediately affected to a desired degree with the initiative lying solely with the Fed.The discount rate can be used as a signal for a change in monetary policy, but often a change in the discount rate simply reflects an adjustment to existing money market conditions. The disadvantage of using the discount rate is that it is up to banks to change the level of bank reserves. Bank reserves only change when banks borrow more or less from the Fed. Since this behavior cannot be anticipated, bank reserve changes cannot be accurately anticipated.Reserve requirement changes are used only rarely, since this is an extremely blunt tool. A reserve requirement change will affect the money multiplier and have a huge effect on money supply. Generally banks are given ample time to adjust to changes.11. Comment on the following statement:"Changes in the discount rate are always a sign that the Fed has changed its monetary policy." The discount rate is the rate at which banks can borrow from the Fed. The federal funds rate is the rate at which banks can borrow from each other. Banks generally prefer to borrow at the lowest rate. They do not like to borrow too often or too much from the Fed, however, since the Fed may then question their way of doing business. But if the demand for bank reserves increases and the difference between the federal funds rate and the discount rate gets too large, banks have an incentive to borrow from the Fed more often than usual. In this case total bank reserves will increase more than the Fed would like. As a result, the Fed may adjust the discount rate to bring it more in line with the federal funds rate. Therefore, while an increase in the discount rate may signal a shift in the Fed's policy, it may also simply reflect the Fed's response to a change in money market conditions.612. In 1991-92, the Fed repeatedly lowered the discount rate, but failed to stimulate the economy.Explain this fact. Subsequently, the Fed lowered the reserve requirements for banks. In your opinion, what was the Fed's objective in doing this, and was the objective achieved?Lowering the discount rate is not always successful in increasing money supply (and thus stimulating the economy), since it requires that banks take the initiative to change bank reserves. In 1991-92, the U.S. was in a recession and negative business expectations persisted. Many banks needed to recover from loan losses they had incurred and did not want to extend credit even though they were encouraged to do so by the Fed.The Fed finally lowered the reserve requirements for banks in a further effort to stimulate the economy but also to increase the profitability of banks. Banks do not earn interest on the reserves they hold, so a decrease in reserve requirements allowed them to increase their earnings and reduce their portfolio risk by buying Treasury-bills. While the economy was not immediately stimulated by new loans, at least the profitability of banks increased, creating more stability within the banking system.13. "Open market sales are more effective than increasing the discount rate in changing moneysupply." Comment. In your answer explain the short-run effects of restrictive monetary policy on velocity, the budget surplus, and national saving.With open market operations, the Fed has the initiative and bank reserves are immediately affected. Open market operations can be undertaken to a small or large extent on every business day, the Fed can determine the level of impact on bank reserves, and the Fed's actions can be easily reversed. Discount rate changes affect banks' cost of borrowing from the Fed, but leave the initiative to react to the banks. Thus, the Fed cannot easily predict the exact effect on bank reserves. For example, in 1991 the Fed changed the discount rate 15 times but banks did not borrow more from the Fed or increase their lending due to unfavorable economic conditions. If the Fed restricts money supply, interest rates will increase, leading to a decrease in economic activity. Initially, the income velocity (V = PY/M) will increase due to the lower money supply (M), but it will take time to affect income. But as national income (Y) decreases, income velocity will decline. Other results will include a decrease in the budget surplus (due to lower tax revenues) and national saving (due to lower income and a lower government surplus).14. Assume the Fed lowered the discount rate. How would personal saving, the budget surplus andaggregate money demand be affected?A lower discount rate is intended to encourage banks to borrow more from the Fed. It is not always clear that banks will respond as expected, but if they do, bank reserves will increase and so will money supply, as banks increase their lending activity. This will lower interest rates, leading to an increase in investment and national income. Personal saving will increase with a higher income level. Similarly, tax revenues will go up, increasing the budget surplus. Lower interest rates and higher income will increase money demand. (We also can see this from the fact that money supply has increased. Since the money sector has to move into a new equilibrium, money demand has to go up if money supply is increased.)15. Should you expect the federal funds rate to be above the discount rate or vice versa? Explain. The Fed is the lender of last resort and banks can always borrow from the Fed if the need arises. When banks borrow from the Fed, they are charged a rate called the discount rate. But banks also have the option to borrow from each other at the federal funds rate. Banks generally prefer to borrow at the lowest rate possible. However, they do not like to borrow too heavily from the Fed, since the Fed is a regulator of banks. Banks fear that their behavior will be questioned if the Fed takes notice and thus prefer to borrow from each other. In doing so, they drive the federal funds rate above the discount rate.716. "Reserve requirements act as an unfair tax on banks." Comment on this statement.Banks are forced to hold their reserves either as vault cash or as deposits at the Fed earning no interest in either case. Since other financial institutions have no such reserve requirement, it could be argued that this unfairly taxes banks. On the other hand, reserves guarantee a certain amount of liquidity for the banking system, which may be necessary, should there be a run on banks. The reserves held as deposits at the Fed also serve to facilitate the check clearing process. For these reasons, the tax can be viewed as necessary and therefore less "unfair."17. Does the Fed have control over the federal funds rate and over bank reserves? If so, can the Fedcontrol both simultaneously?The Fed has indirect control over the federal funds rate, since it has control over the supply of total bank reserves in the banking system through open market operations. However, the Fed cannot control the demand for bank reserves. If the demand for bank reserves increases, the federal funds rate will rise. If the Fed chooses to peg the federal funds rate, it has to create additional bank reserves via open market purchases. On the other hand, if the Fed chooses to control the level of bank reserves, it has to let the federal funds rate fluctuate. Therefore, the Fed cannot control the federal funds rate and the level of bank reserves simultaneously.18. "By lowering the reserve requirements for banks, the Fed reduces the budget deficit, nationalsaving, and the income velocity of money." Comment on this statement.If the Fed lowers the reserve requirement, banks have more money to lend out and can thus increase their earnings by making more loans or buying T-bills. If banks extend their loans, then money supply will increase and interest rates will decrease, stimulating investment and national income. Saving will increase with a higher level of income. Similarly, tax revenues will go up, reducing the budget deficit. Interest payments on the national debt will also decrease with lower interest rates, which will also help to lower the deficit. Velocity will initially decrease, since money supply will increase before income. But as income increases, then velocity will increase again. Ultimately, velocity may not change by much, since the income elasticity of money demand is close to one in the long run.19. "Restrictive monetary policy over a long time period will lead to lower interest rates."Comment on this statement.Long-run effects of monetary policy are different from short-run effects. Restrictive monetary policy leads to higher interest rates in the short run due to less liquidity (liquidity effect). But higher interest rates will reduce aggregated demand, which reduces prices and national income. Thus the level of interest rates will start to decline again (price-income effect). Lower prices will eventually lead to lower inflationary expectations and thus lower nominal interest rates (price-anticipation effect). In the end, real interest rates (i r) will return to their original level and nominal interest rates (i n) will be lower, since the inflation rate (π) is lower. This is shown in the so-called Fisher equation: i n = i r + π.20. "The elimination of required reserves on bank deposits would decrease the Fed's control overmoney supply. But if money supply increased uncontrollably, then high rates of inflation would result." Comment on the following statement.The Fed has a number of policy instruments at its disposal to control the level of bank reserves (and thus money supply). The required-reserve ratio is only one such instrument. The Fed can always influence bank reserves through the use of open market operations. Even if reserve requirements are abolished, the money multiplier will always have a finite value, since banks will always hold some (excess) reserves to meet their daily cash needs and emergency needs. If the reserve requirement were eliminated, the money multiplier would become larger, since banks would not choose to voluntarily hold as many reserves as the Fed required. However, large-scale open market operations would still enable the Fed to exercise great influence over bank reserves and therefore money supply.8。

威廉森《宏观经济学》笔记和课后习题详解(开放经济中的货币)【圣才出品】

1 / 69第16章 开放经济中的货币16.1 复习笔记一、名义汇率、实际汇率和购买力平价1.基本概念名义汇率,用e 表示,即在外汇市场上,用本币表示的1单位外币的价格。

实际汇率(或贸易条件),是指用国内商品表示的国外商品的价格。

国内商品用本币计价为P ,国外商品用本币计价为eP *:实际汇率=eP */P2.购买力平价购买力平价也被称为一价定律,是指若没有运输成本和贸易壁垒,就会有:P =eP * 如果它成立,则用本币表示的商品价格,无论在国内还是在国外都是一样的。

实际汇率是1。

2 / 693.购买力平价的适用性(1)一般而言,有强大的经济力量促使市场价格和名义汇率进行调整,从而使购买力平价成立。

除非商品、劳动力和资本的跨国流动非常困难,否则,长期内购买力平价就应成立。

短期内购买力平价一般不成立。

(2)把P 和P *看作两个不同国家的价格水平,购买力平价不完全成立。

对存在国际贸易的商品来说,一价定律趋势成立,但对非贸易商品,则不成立。

二、浮动汇率和固定汇率1.浮动汇率制浮动汇率又称弹性汇率,指一国的财政当局或货币当局不必通过具体钉住名义汇率e 来进行干预。

如果名义汇率是真正浮动的,它会在市场力量的作用下自由变动。

实行浮动汇率制的国家有印度、韩国、巴西、澳大利亚、新西兰、加拿大和美国。

2.固定汇率制固定汇率制大致可以划分为硬钉住和软钉住。

在硬钉住制度下,一国(地区)承诺将其名义汇率无限期地钉住其他国家的货币。

在软钉住制度下,虽然没有将汇率钉住特定值的长期承诺,但汇率可以做到长期钉住另一种货币,实行定期降值(名义汇率e 提高)和法定升值(名义汇率e 下降)。

3 / 69(1)实行硬钉住的方式①美元化美元化实质上是使用他国货币作为本国的交换媒介。

美元化的缺点是,一国放弃了其征收铸币税的能力;也就是说,它不能通过印钞来为政府支出筹资。

②建立货币局有了货币局,就有了一个集权机构,它可以是一国(地区)的中央银行。

宏观经济学第七版习题册答案整理(高鸿业)

第十二章宏观经济的基本指标及其衡量1.宏观经济学和微观经济学有什么联系和区别? 为什么有些经济活动从微观看是合理的、有效的,而从宏观看却是不合理的、无效的?解答:两者之间的区别在于:(1)研究的对象不同.微观经济学研究单个经济主体的最优化行为;宏观经济学研究一国整体经济的运行规律和宏观经济政策。

(2)解决的问题不同.微观经济学解决资源配置问题;宏观经济学解决资源利用问题。

(3)中心理论不同.微观经济学的中心理论是价格理论,所有的分析都是围绕价格机制的运行展开的; 宏观经济学的中心理论是国民收入 (产出) 理论,所有的分析都是围绕国民收入 (产出)的决定展开的。

(4)研究方法不同.微观经济学采用的是个量分析方法;宏观经济学采用的是总量分析方法。

两者之间的联系主要表现在:(1)二者都是通过需求曲线和供给曲线决定价格和产量,而且曲线的变动趋势相同。

(2)相互补充.经济学研究的目的是实现社会经济福利的最大化. 为此, 既要实现资源的最优配置,又要实现资源的充分利用.微观经济学是在假设资源得到充分利用的前提下研究资源如何实现最优配置的问题,而宏观经济学是在假设资源已经实现最优配置的前提下研究如何充分利用这些资源.它们共同构成经济学的基本内容。

(3)微观经济学和宏观经济学都以实证分析作为主要的分析和研究方法.(4)微观经济学是宏观经济学的基础.当代宏观经济学越来越重视微观基础的研究, 即将宏观经济分析建立在微观经济主体行为分析的基础上.由于微观经济学和宏观经济学分析问题的角度不同,分析方法也不同,因此有些经济活动从微观看是合理的、有效的, 而从宏观看是不合理的、无效的. 例如, 在经济生活中,某个厂商降低工资,从该企业的角度看,成本低了,市场竞争力强了,但是如果所有厂商都降低工资,则上面降低工资的那个厂商的竞争力就不会增强,而且职工整体工资收入降低以后,整个社会的消费以及有效需求也会降低.同样,一个人或者一个家庭实行节约,可以增加家庭财富,但是如果大家都节约,社会需求就会降低,生产和就业就会受到影响。

宏观经济学各章习题及答案(高鸿业主编)

宏观经济学习题第十二章西方国民收入核算一、名词解释1国内生产总值2国民生产总值3名义GDP与实际4最终产品和中间产品5总投资和净投资6重置投资7存货投资8政府购买和政府转敌支付9净出口。

二、选择题1、宏观经济研究哪些内容?()A、失业率上升一个百分点会使GDP增加多少B、研究为什么从事农业和渔业的人的工资要比其他工人的工资低C、降低工资会对单个厂商产生什么样的影响D、分析对企业征收的环境特别税对整个环境污染的影响2、下列项目哪一些计入GDP?()A、政府转移支付B、购买一辆用过的汽车C、购买普通股股票D、购买彩票赢得的1万元E、企业支付的贷款和债券利息3、某国的GNP大于GDP,说明该国居民从外国获得的收入与国居民从该国获得的收入相比的关系。

()A、大于B、小于C、等于D、无法判断4、在国民生产和国民收入中,哪种行为将被经济学家视为投资?()A、购买新公司债券B、生产性生活而导致的当前消费C、购买公司债券D、上述都不对5、下列哪一项不是公司间接税?()A、销售税B、公司利润税C、货物税D、公司财产税6、下列哪一项不是转移支付?()A、退休军人津贴B、失业救济金C、困难家庭补贴D、退休人员的退休金7、在一个有政府、投资和外贸部门的模型中,GNP是下面哪一个选择中各项之和?()A、消费、总投资、政府在商品和劳务上的支出和净出口B、消费、净投资、政府在商品和劳动上的支出和净出口C、国民收入和简洁税D、工资、租金、利息、利润和折扣8、假设一个经济第1年即基年的当期产出为500亿元,如果第8年GNP物价减指数提高了一倍,而实际产出增加了50%,则第8年的名义产出等于()A、2000亿元B、1500亿元C、1000亿元D、750亿元9、在国民收入核算体系中,计入GDP的政府支出是指哪些?()A、政府购买的物品支出B、政府购买的物品和劳务的支出C、政府工作人员的薪水和政府转移支付D、政府购买的物品和劳务的支出加上政府的转移支付之和10、今年的名义GDP增加了,说明()A、今天的物价上涨了B、今年的物价和产出都增加了C、今年的产出增加了情况D、不能确定三、简答题1、简要说明国民收入的三种核算法。

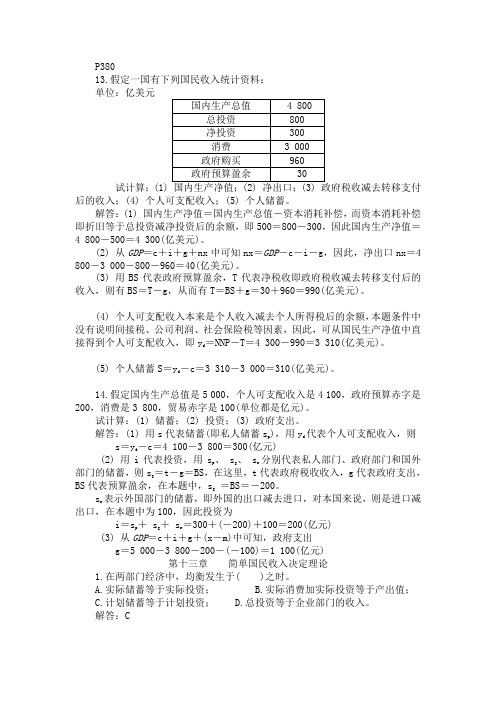

宏观经济学第五版课后习题答案

P38013.假定一国有下列国民收入统计资料:单位:亿美元 国内生产总值 4 800总投资 800净投资 300消费 3 000政府购买 960政府预算盈余 30试计算:(1) 国内生产净值;(2) 净出口;(3) 政府税收减去转移支付后的收入;(4) 个人可支配收入;(5) 个人储蓄。

解答:(1) 国内生产净值=国内生产总值-资本消耗补偿,而资本消耗补偿即折旧等于总投资减净投资后的余额,即500=800-300,因此国内生产净值=4 800-500=4 300(亿美元)。

(2) 从GDP =c +i +g +nx 中可知nx =GDP -c -i -g ,因此,净出口nx =4 800-3 000-800-960=40(亿美元)。

(3) 用BS 代表政府预算盈余,T 代表净税收即政府税收减去转移支付后的收入,则有BS =T -g ,从而有T =BS +g =30+960=990(亿美元)。

(4) 个人可支配收入本来是个人收入减去个人所得税后的余额,本题条件中没有说明间接税、公司利润、社会保险税等因素,因此,可从国民生产净值中直接得到个人可支配收入,即y d =NNP -T =4 300-990=3 310(亿美元)。

(5) 个人储蓄S =y d -c =3 310-3 000=310(亿美元)。

14.假定国内生产总值是5 000,个人可支配收入是4 100,政府预算赤字是200,消费是3 800,贸易赤字是100(单位都是亿元)。

试计算:(1) 储蓄;(2) 投资;(3) 政府支出。

解答:(1) 用s 代表储蓄(即私人储蓄s p ),用y d 代表个人可支配收入,则s =y d -c =4 100-3 800=300(亿元)(2) 用i 代表投资,用s p 、 s g 、 s r 分别代表私人部门、政府部门和国外部门的储蓄,则s g =t -g =BS ,在这里,t 代表政府税收收入,g 代表政府支出,BS 代表预算盈余,在本题中,s g =BS =-200。

宏观经济学高鸿业版习题答案

十二章答案一、单项选择题1. A;2.B;3.B ;4. C;5. D ;6. B ;7. D;8. B;9. A ;10.C;11. A;12. C ;13. D ;14. B;15. C ;16. D;17. A;18. C。

三、简答题4、社会保险税实质上是企业和职工为得到社会保障而支付的保险金,它由政府有关部门(一般是保险局)按一定比率以税收形式征收。

社会保险税是从国民收入中扣除的,因此,社会保险税的增加并不影响GDP、NDP和NI,但影响个人收入PI。

社会保险税的增加减少个人收入,从而也从某种意义上会影响个人可支配收入。

然而,应当认为,社会保险税的增加并不直接影响可支配收入,因为一旦个人收入决定后,只有个人所得税的变动才会影响个人可支配收入 DPI。

四、分析与计算题1.解:支出法=16720+3950+5340+3390-3165=26235收入法=15963+1790+1260+1820+310+2870+2123+105-6=262352.解:(1)GDP=2060+590+590+40=3280(2)NDP=3280-210=3070(3)NI=3070-250=2820(4)PI =2820-130-220-80+200+30=2620(5)DPI=2620-290=23303. 解:⑴ 1990=652.5; 1995=878;⑵如果以1990年作为基年,则1995年的实际国内生产总值=795⑶计算1990-1995年的国内生产总值平减指数:90年=652.5/612.5=1,95年=878/795=1.114. 解:(1)S=DPI-C=4000-3500=500(2)用I代表投资,S P、S g、S F分别代表私人部门、政府部门和国外部门的储蓄,则 S g =T–g =BS,这里T代表政府税收收入,g代表政府支出,BS代表预算盈余,在本题中,S g =T–g=BS=-200。

高鸿业第六版西方经济学课后习题答案(宏观部分)

第十二章国民收入核算1、解答:政府转移支付不计入GDP,因为政府转移支付只是简洁地通过税收(包括社会保障税)和社会保险及社会救济等把收入从一个人或一个组织转移到另一个人或另一个组织手中,并没有相应的货物或劳物发生。

例如,政府给残疾人发放救济金,并不是残疾人创建了收入;相反,倒是因为他丢失了创建收入的实力从而失去生活来源才赐予救济的。

购买一辆用过的卡车不计入GDP,因为在生产时已经计入过。

购买一般股票不计入GDP,因为经济学上所讲的投资是增加或替换资本资产的支出,即购买新厂房,设备和存货的行为,而人们购买股票和债券只是一种证券交易活动,并不是实际的生产经营活动。

购买一块地产也不计入GDP,因为购买地产只是一种全部权的转移活动,不属于经济意义的投资活动,故不计入GDP。

2、解答:社会保险税实质是企业和职工为得到社会保障而支付的保险金,它由政府有关部门(一般是社会保险局)按肯定比率以税收形式征收的。

社会保险税是从国民收入中扣除的,因此社会保险税的增加并不影响GDP ,NDP和NI,但影响个人收入PI。

社会保险税增加会削减个人收入,从而也从某种意义上会影响个人可支配收入。

然而,应当认为,社会保险税的增加并不影响可支配收入,因为一旦个人收入确定以后,只有个人所得税的变动才会影响个人可支配收入DPI。

3、假如甲乙两国合并成一个国家,对GDP总和会有影响。

因为甲乙两国未合并成一个国家时,双方可能有贸易往来,但这种贸易只会影响甲国或乙国的GDP,对两国GDP总和不会有影响。

举例说:甲国向乙国出口10台机器,价值10万美元,乙国向甲国出口800套服装,价值8万美元,从甲国看,计入GDP的有净出口2万美元,计入乙国的有净出口–2万美元;从两国GDP总和看,计入GDP的价值为0。

假如这两个国家并成一个国家,两国贸易变成两个地区的贸易。

甲地区出售给乙地区10台机器,从收入看,甲地区增加10万美元;从支出看乙地区增加10万美元。

宏观经济学第16章练习题及答案

第十六章练习题及答案一、判断1.紧缩性财政政策对经济的影响是抑制了通货膨胀但增加了政府债务。

〔〕2.预算赤字财政政策是凯恩斯主义用于解决失业问题的有效需求管理的主要手段。

〔〕3.扩张性货币政策使LM曲线右移,而紧缩性货币政策使LM曲线左移。

〔〕4.政府的财政支出政策主要通过转移支付、政府购置和税收对国民经济产生影响。

〔〕5.当政府同时实行紧缩性财政政策和紧缩性货币政策时,平衡国民收入一定会下降,平衡的利率一定会上升。

〔〕6.减少再贴现率和法定准备金比率可以增加货币供应量。

〔〕7.由于现代西方财政制度具有自动稳定器功能,在经济繁荣时期自动抑制通货膨胀,在经济衰退时期自动减轻萧条,所以不需要政府采取任何行动来干预经济。

〔〕8.宏观经济政策目的之一是价格稳定,价格稳定指价格指数相对稳定,而不是所有商品价格固定不变。

〔〕9.财政政策的内在稳定器作用是稳定收入程度,但不稳定价格程度和就业程度。

〔〕10.扩张性财政政策使IS曲线左移,而紧缩性财政政策使IS曲线右移。

〔〕11.当一个国家出现恶性通货膨胀时,政府只能通过采取紧缩性货币政策加以遏制。

〔〕12.在西方兴旺国家,由财政部、中央银行和商业银行共同运用货币政策来调节。

〔〕13.当一个国家经济处于充分就业程度时,政府应采取紧缩性财政政策和货币政策。

〔〕14.凯恩斯主义者奉行功能财政思想,而不是预算平衡思想。

〔〕二、单项选择1.以下哪种情况增加货币供应而不会影响平衡国民收入?〔〕A.IS曲线陡峭而LM曲线平缓B.IS曲线垂直而LM曲线平缓C.IS曲线平缓而LM曲线陡峭D.IS曲线和LM曲线一样平缓2.挤出效应发生于以下哪种情况?〔〕A.私人部门增税,减少了私人部门的可支配收入和支出B.减少政府支出,引起消费支出下降C.增加政府支出,使利率进步,挤出了对利率敏感的私人部门支出D.货币供应增加,引起消费支出增加3.以下〔〕不属于扩张性财政政策。

A.减少税收B.制定物价管制政策C.增加政府支出D.增加公共事业投资4.中央银行通过进步法定准备金比率属于〔〕A.控制总供应B.扩张性货币政策C.收入指数化政策D.紧缩性货币政策5.以下哪种情况不会引起国民收入程度的上升〔〕A.增加净税收B.增加政府转移支付C.减少个人所得税D.增加政府购置6.假如政府支出的减少与政府转移支付的增加一样时,收入程度会〔〕A.增加B.不变C.减少D.不确定7.在其他条件不变情况下,政府增加公共设施投资,会引起国民收入〔〕A.增加B.不变C.减少D.不确定8.与货币政策同义的词是〔〕A.扩张性政策B.利息率政策C.金融政策D.紧缩性政策9.公开市场业务是指〔〕A.中央银行在金融市场上买进或卖出有价证券B.中央银行增加或减少对商业银行的贷款C.中央银行规定对商业银行的最低贷款利率D.中央银行对商业银行施行监视10.政府运用赤字财政政策是〔〕A.要求企业用自己资金购置B.要求居民用现金购置C.将公债卖给商业银行D.将公债卖给中央银行11.当经济过热时,中央银行可以在金融市场上〔〕A.卖出政府债券,降低再贴现率B.卖出政府债券,进步再贴现率C.买进政府债券,降低再贴现率D.买进政府债券,进步再贴现率12.以下哪一项措施是中央银行无法用来变动货币供应量?〔〕A.调整法定准备金B.调整再贴现率C.调整税率D.公开市场业务13.当法定准备金率为25%时,假如你在银行兑现了一张200美元的支票而且将现金放在身边,这个行动对货币供应的潜在影响是〔〕A.流通中货币增加800美元B.流通中货币减少800美元C.流通中货币增加200美元D.流通中货币减少200美元14.财政政策的内在稳定器作用表达在〔〕A.延缓经济衰退B.刺激经济增长C.减缓经济波动D.促使经济到达平衡15.“松财政紧货币〞会使利率〔〕A.上升B.下降C.不变D.不确定16.“双紧〞政策会使国民收入〔〕A.增加B.减少C.不变D.不确定17.在充分就业的经济中,政府购置支出增加将导致〔〕A.价格程度上升,利率下降B.价格程度下降,利率上升C.价格程度和利率同时上升D.价格程度和利率同时下降18.假如一国经济处于萧条和衰退时期,政府应采取〔〕A.财政预算盈余B.财政预算赤字C.财政预算平衡D.财政预算盈余或赤字19.假如一国经济处于国内失业,国际收支顺差的状况,这时适宜采用〔〕A.扩张性财政政策B.扩张性货币政策C.扩张性财政政策与扩张性货币政策D.扩张性财政政策与紧缩性货币政策20.扩张性财政政策对经济的影响是〔〕A.缓和了经济萧条但增加了政府债务B.缓和了萧条也减轻了政府债务C.加剧了通货膨胀但减轻了政府债务D.缓和了通货膨胀但增加了政府债务三、简答1.什么是自动稳定器?是否税率越高,税收作为自动稳定器的作用越大?2.什么是斟酌使用的财政政策和货币政策?3.平衡预算的财政思想和功能财政思想有何区别?第十六章练习题答案一、1.F 2.T 3.T 4.F 5.F 6.T 7.F8.T 9.F 10.F 11.F 12.F 13.F 14.T二、1.B 2.C 3.B 4.D 5.A 6.C 7.A 8.C 9.A 10.D11.B 12.C 13.B 14.C 15.A 16.B 17.C 18.B 19.C 20.A三、1.自动稳定器亦称内在稳定器,是指财政制度本身所具有的减轻各种干扰对国民收入冲击的内在机制。

微观经济学第十六章 宏观经济政策实践 课后练习参考答案

第十六章宏观经济政策实践1. C2. B3. A4. D5. B6. A7. C8. 答案见课本第462页。

是税率越高,税收作为自动稳定器的作用越大。

9. 答案见课本第462页。

10.答案见课本第463页。

11.答案见课本第460页。

12.答案见课本第473页“公开市场业务”。

13.解:C=100+0.8yd i=50 g=200 tr=62.5 t=0.25(1)由模型:c=100+0.8y dy d=y-t×y-try=c+i+g解得:y=(100+0.8tr+i+g)/(0.2+0.8t)=1000(2)当均衡收入y=1000时,预算盈余:BS=t×y-g-tr=0.25×1000-200-62.5=-12.5(3)当i增加到100时,均衡收入为:Y=(1+btr+i+g)/[1-b(1-t)]=(100+0.8×62.5+100+200)/[1-0.8(1-0.25)]=1125这时预算盈余BS=0.25×1125-200-62.5=18.75预算盈余之所以会从-12.5变为18.75,是因为国民收入增加了,使税收增加了。

(4)若充分就业的收入y*=1200,当i=50时,充分就业预算盈余:BS*=t×y*-g-tr=300-200-62.5=37.5当i=100时,充分就业预算盈余BS*没有变化,仍等于37.5(5)若i=50,g=250,y*=1200,则BS*=t×y*-g-t r=0.25×1200-250-62.5=-12.5 (6)略14.答案见课本第469-471页15.解:货币创造乘数k=(1+r c)/(r c+r)=1.38/(0.38+0.18)=2.46若增加基础货币100亿美元,则货币供给增加△M=100×2.46=246亿美元16.解:(1)货币供给M=C U+D=1000+400/0.12=4333亿美元(注:其中C U为非银行部门持有的通货,本题中为1000亿美元,D为活期存款)(2)当准备金率提高到0.2,则存款变为400/0.2=2000亿美元,现金仍是1000亿美元,因此货币供给为1000+2000=3000亿美元,货币供给减少了1333亿美元(3)中央银行买进10亿美元债券,即基础货币增加10亿美元,则货币供给增加:△M=10×1/0.12=83.3亿美元。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

第十六章宏观经济政策实践1.政府的财政收入政策通过哪一个因素对国民收入产生影响?A.政府转移支付;B.政府购买;C.消费支出;D.出口。

解答:C2.假定政府没有实行财政政策,国民收入水平的提高可能导致()。

A.政府支出增加;B.政府税收增加;C.政府税收减少;D.政府财政赤字增加。

解答:B3.扩张性财政政策对经济的影响是()。

A.缓和了经济萧条但增加了政府债务;B.缓和了萧条也减轻了政府债务;C.加剧了通货膨胀但减轻了政府债务;D.缓和了通货膨胀但增加了政府债务。

解答:A4.商业银行之所以会有超额储备,是因为()。

A.吸收的存款太多;B.未找到那么多合适的贷款对象;C.向中央银行申请的贴现太多;D.以上几种情况都有可能。

解答:B5.市场利率提高,银行的准备金会()。

A.增加;B.减少;C.不变;D.以上几种情况都有可能。

解答:B6.中央银行降低再贴现率,会使银行准备金()。

A.增加;B.减少;C.不变;D.以上几种情况都有可能。

解答:A7.中央银行在公开市场卖出政府债券是试图()。

A.收集一笔资金帮助政府弥补财政赤字;B.减少商业银行在中央银行的存款;C.减少流通中的基础货币以紧缩货币供给;D.通过买卖债券获取差价利益。

解答:C8. 什么是自动稳定器?是否边际税率越高,税收作为自动稳定器的作用越大?解答:自动稳定器是指财政制度本身所具有的减轻各种干扰对GDP的冲击的内在机制。

自动稳定器的内容包括政府所得税制度、政府转移支付制度、农产品价格维持制度等。

在混合经济中投资变动所引起的国民收入变动比纯粹私人经济中的变动要小,原因是当总需求由于意愿投资增加而增加时,会导致国民收入和可支配收入的增加,但可支配收入增加小于国民收入的增加,因为在国民收入增加时,税收也在增加,增加的数量等于边际税率乘以国民收入,结果混合经济中消费支出增加额要比纯粹私人经济中的小,从而通过乘数作用使国民收入累积增加也小一些。

同样,总需求下降时,混合经济中收入下降也比纯粹私人部门经济中要小一些。

这说明税收制度是一种针对国民收入波动的自动稳定器。

混合经济中支出乘数值与纯粹私人经济中支出乘数值的差额决定了税收制度的自动稳定程度,其差额越大,自动稳定作用越大,这是因为在边际消费倾向一定的条件下,混合经济中支出乘数越小,说明边际税率越高,从而自动稳定量越大。

这一点可以从混合经济的支出乘数公式11-β(1-t)中得出。

边际税率t越大,支出乘数越小,从而边际税率变动稳定经济的作用就越大。

举例来说,假设边际消费倾向为0.8,当边际税率为0.1时,增加1美元投资会使总需求增加3.57美元=1×11-0.8×(1-0.1),当边际税率增至0.25时,增加1美元投资只会使总需求增加2.5美元=1×11-0.8×(1-0.25),可见,边际税率越高,自发投资冲击带来的总需求波动越小,说明自动稳定器的作用越大。

9. 什么是斟酌使用的财政政策和货币政策?解答:西方经济学者认为,为确保经济稳定,政府要审时度势,根据对经济形势的判断,逆对经济风向行事,主动采取一些措施稳定总需求水平。

在经济萧条时,政府要采取扩张性的财政政策,降低税率、增加政府转移支付、扩大政府支出,以刺激总需求,降低失业率;在经济过热时,采取紧缩性的财政政策,提高税率、减少政府转移支付,降低政府支出,以抑制总需求的增加,进而遏制通货膨胀。

这就是斟酌使用的财政政策。

同理,在货币政策方面,西方经济学者认为斟酌使用的货币政策也要逆对经济风向行事。

当总支出不足、失业持续增加时,中央银行要实行扩张性的货币政策,即提高货币供应量,降低利率,从而刺激总需求,以缓解衰退和失业问题;在总支出过多、价格水平持续上涨时,中央银行就要采取紧缩性的货币政策,即削减货币供应量,提高利率,降低总需求水平,以解决通货膨胀问题。

这就是斟酌使用的货币政策。

10. 平衡预算的财政思想和功能财政思想有何区别?解答:平衡预算的财政思想主要分年度平衡预算、周期平衡预算和充分就业平衡预算三种。

年度平衡预算,要求每个财政年度的收支平衡。

这是在20世纪30年代大危机以前普遍采用的政策原则。

周期平衡预算是指政府在一个经济周期中保持平衡。

在经济衰退时实行扩张政策,有意安排预算赤字,在繁荣时期实行紧缩政策,有意安排预算盈余,用繁荣时的盈余弥补衰退时的赤字,使整个经济周期的盈余和赤字相抵而实现预算平衡。

这种思想在理论上似乎非常完整,但实行起来非常困难。

这是因为在一个预算周期内,很难准确估计繁荣与衰退的时间与程度,两者更不会完全相等,因此连预算都难以事先确定,从而周期预算平衡也就难以实现。

充分就业平衡预算是指政府应当使支出保持在充分就业条件下所能达到的净税收水平。

功能财政思想强调,政府在财政方面的积极政策主要是为实现无通货膨胀的充分就业水平。

当实现这一目标时,预算可以是盈余,也可以是赤字。

功能财政思想是凯恩斯主义者的财政思想。

他们认为不能机械地用财政预算收支平衡的观点来对待预算赤字和预算盈余,而应根据反经济周期的需要来利用预算赤字和预算盈余。

当国民收入低于充分就业的收入水平时,政府有义务实行扩张性财政政策,增加支出或减少税收,以实现充分就业。

如果起初存在财政盈余,政府有责任减少盈余甚至不惜出现赤字,坚定地实行扩张政策。

反之亦然。

总之。

功能财政思想认为,政府为了实现充分就业和消除通货膨胀,需要赤字就赤字,需要盈余就盈余,而不应为了实现财政收支平衡来妨碍政府财政政策的正确制定和实行。

显然,平衡预算的财政思想强调的是财政收支平衡,以此作为预算目标或者说政策的目的,而功能财政思想强调,财政预算的平衡、盈余或赤字都只是手段,目标是追求无通胀的充分就业和经济的稳定增长。

11.政府购买和转移支付这两项中那一项对总需求变动影响更大些?朝什么方向变动?解答:政府为减少经济波动往往运用财政政策进行总需求管理。

政府购买和政府转移支付都会对经济周期作出反应。

其中转移支付随经济波动更大些,并朝反周期方向波动,因为经济衰退时,失业津贴、贫困救济、农产品价格补贴等支出会自动增加,经济繁荣时,这些支出会自动减少,而政府购买则变动较少,因为国防费、教育经费以及政府行政性开支等有一定刚性,不可能随经济周期波动很大。

12.政府发行的公债卖给中央银行和卖给商业银行或者其他私人机构对货币供给量变动会产生什么样不同的影响?解答:政府发行的公债卖给中央银行,这实际上就是让中央银行增加货币发行,增加基础货币,货币供给量会按照货币乘数数倍地增加,这是政府的货币筹资,其结果往往是形成通货膨胀,这是国家征收的通货膨胀税;而政府发行的公债卖给商业银行或者其他私人机构,不过是购买力向政府部门转移,不会增加基础货币,不会直接引起通货膨胀,这是政府的债务筹资。

13. 假设一经济中有如下关系:c =100+0.8yd (消费);i =50(投资);g =200(政府支出);t r =62.5(政府转移支付)(单位均为10亿美元); t =0.25(税率)(1)求均衡收入。

(2)求预算盈余BS 。

(3)若投资增加到i =100,预算盈余有何变化?为什么会发生这一变化?(4)若充分就业收入y =1 200,当投资分别为50和100时,充分就业预算盈余BS 为多少?(5)若投资i =50,政府购买g =250,而充分就业收入仍为1 200,试问充分就业预算盈余为多少?(6)用本题为例说明为什么要用BS 而不用BS 去衡量财政政策的方向?解答:(1)由模型可解得均衡收入为y =100+0.8t r +i +g 0.2+0.8t =100+0.8×62.5+50+2000.2+0.8×0.25=1 000 (2)当均衡收入y =1 000时,预算盈余为BS =ty -g -t r =0.25×1 000-200-62.5=-12.5(3)当i 增加到100时,均衡收入为y =a +b ·t r +i +g 1-b (1-t )=100+0.8×62.5+100+2001-0.8(1-0.25)=4500.4=1 125 这时预算盈余BS =0.25×1 125-200-62.5=18.75。

预算盈余之所以会从-12.5变为18.75,是因为国民收入增加了,从而税收增加了。

(4)若充分就业收入y *=1 200,当i =50时,充分就业预算盈余为BS *=ty *-g -t r =300-200-62.5=37.5当i =100时,充分就业预算盈余BS *没有变化,仍等于37.5。

(5)若i =50,g =250,y *=1 200,则充分就业预算盈余为BS *=ty *-g -t r =0.25×1 200-250-62.5=300-312.5=-12.5(6)从表面看来,预算盈余BS 的变化似乎可以成为对经济中财政政策方向的检验指针,即预算盈余增加意味着紧缩的财政政策,预算盈余减少(或赤字增加)意味着扩张的财政政策。

然而,如果这样简单地用BS 去检验财政政策的方向就不正确了。

这是因为自发支出改变时,收入也会改变,从而使BS 也发生变化。

在本题中,当投资从50增加到100时,尽管税率t 和政府购买g 都没有变化,但预算盈余BS 从赤字(-12.5)变成了盈余(18.75),如果单凭预算盈余的这种变化就认为财政政策从扩张转向了紧缩,就是错误的。

而充分就业预算盈余BS *衡量的是在充分就业收入水平上的预算盈余,充分就业收入在一定时期内是一个稳定的量,在此收入水平上,预算盈余增加,则是紧缩的财政政策,反之,则是扩张的财政政策。

在本题(4)中,充分就业收入y *=1 200,当i =50时,充分就业预算盈余BS *为37.5,当i =100时,由于财政收入和支出没有变化,故用y *衡量的BS *也没有变化,仍等于37.5。

但在本题(5)中,尽管ty *未变,但g 从200增至250,故充分就业预算盈余减少了,从37.5变为-12.5,因此,表现为财政扩张。

所以我们要用BS *而不是BS 去衡量财政政策的方向。

14. 什么是货币创造乘数?其大小主要和哪些变量有关?解答:一单位高能货币能带来若干倍货币供给,这若干倍即货币创造乘数,也就是货币供给的扩张倍数。

如果用H 、C u 、RR 、ER 分别代表高能货币、非银行部门持有的通货、法定准备金和超额准备金,用M 和D 代表货币供给量和活期存款,则H =C u +RR +ER (1) M =C u +D (2)即有 M H =C u +D C u +RR +ER再把该式分子分母都除以D ,则得M H =C u /D +1C u /D +RR /D +ER /D这就是货币乘数,在上式中,C u /D 是现金存款比率,RR /D 是法定准备率,ER /D 是超额准备率。