会计专业英语练习题

会计专业英语练习

Ⅰ.Matching each of the following statements with its proper term.1. Temporary account ( )2. Working papers ( )3. Fiscal year ( )4. Accrual accounting ( )5. Posting6. General ledger ( )7. Liquidity ( )8. Withdrawals ( )9. CPA ( )10. Transaction ( )11. Accounting cycle ( )12. Closing entries ( )13. Reversing entry ( )14. Accounting equation( )15. Double entry accounting( )16. T account ( )17. Chart of accounts( )18. Account form ( )19. Business entity concept ( )20. Financial accounting ( )A. Assets taken from the business by the owner for personal use.B. The annual accounting period adopted by a business.C. Convertibility to cashD. Assets=liabilities+ owner’s equity.E. Documents that help accountants organize their work.F. An condition or directly affects its results of accounting event or condition that directly changes an entity’s financial operation.G. The idea that revenues are recorded (recognized) when earned and that expenses are recorded when incurred.H. The book that contains the individual account (or control account), groupedaccording to the five elements of financial statements.I. Transferring data from the journal to the ledger.J. An expert accountant licensed by the state.K. The entries that transfer the balances of the revenue, expense, and dividends accounts to the retained earnings account.L. The opposite of an adjusting entry, journalized to facilitate routine bookkeeping entries.M. The process that begins with analyzing and journalizing transactions and ends with the post-closing balance.N. The simplest form of account.O. Income statement accountsP. A system of accounting for recording .transactions, based on recording increases and decreases in accounts so that debits equals credits.Q. A list of accounts in the ledgerR. The branch of accounting concerned with providing external users with financial information needed to make decisions.S. An concept of accounting that limits the economic data in the accounting system to data related directly to the activities of the business.T. The form of balance sheet that resembles the basic format of the accounting equation, with assets on the left side and the liabilities and owner’s equity sections on the right side.Ⅱ、Multiple choice questions1. A profit-making business that is a separate legal entity and in which ownership is divided into shares of stock is known as a: ( )A. proprietorshipB. partnershipC. service businessD. corporation2. The resources owned by a business is called :( )A. assetsB. liabilitiesC. the account equationD. owner’s equity3. A list of assets, liabilities, and owner’s equity of a business entity as of a specific date is :( )A. a balance sheetB. an income statementC. a retained earning statementD. a statement of cash flows4. A debit may signify ( )A. an increase in an asset accountB. a decrease in an asset accountC. an increase in a liability accountD. an increase in a capital stock account5. The type of account with a normal credit balance is ( )A. an assetB. a revenueC. a dividendsD. an expense6. The receipt of cash from customers in payment of their accounts would be recorded by a ( )A. debit to Cash; credit to Accounts ReceivableB. debit to Accounts Receivable; credit to CashC. debit to Cash; credit to Accounts payableD. debit to Accounts payable; credit to Cash7. Which of the following accounts would be classified as a current asset on the balance sheet? ( )A. office equipmentB. accumulated depreciationC. landD. accounts receivable8. Which of the following accounts would not be closed to the income summary account at the end of a period?( )A. fees earnedB. rent expenseC. wages expenseD. accumulated depreciation9. What is the maturity value of a 90-day, 12% note for $10000?( )A. $8800B. $10300C.$10000D.$1120010. Which of the following is an example of intangible asset?( )A. patensB. copyrightsC. goodwillD. all of the aboveⅢ. True-False1.The income summary account can be found in the statement of owner’s equity. ( )2.Closing entries convert real and nominal accounts to zero balances. ( )3.The worksheet is prepared after the formal adjusting entries have been made in thejournal. ( )4. A calendar year refers to any twelve month period. ( )5.The cash basis of accounting often violates the matching rule. ( )6.Adjusting entries help make financial statements comparable from one period tothe next. ( )7.Payment of accounts payable will be recorded in the purchase journal. ( )8.In all journal entries, at least one account must be increased, and anotherdecreased. ( )9.The presentation of the owner’s equity section is same for three types of businessorganization. ( ).10. For a given account, total debits must always equal total credits. ( )11. Internal reporting (i.e., management accounting) must follow GAAP in all respects. ( )12. Generally accepted accounting principles are not like laws of math and science; they are guidelines which define correct accounting practice at the time. ( )13. The various steps in the accounting cycle occur with equal frequency. ( )14. The credit side of an account implies something favorable. ( )15. Transactions are initially recorded in a ledger account. ( )16. The net income for a period in the income statement will increase the balance of owner’s equity. ( )17. Failure to include a warehouse’s merchandise in ending inventory results in anoverstated net income. ( )18. The statement of owner’s equity links a company’s income statement to its balance sheet. ( )19. The existence of Accounts Receivable on the balance sheet indicates that the company has one or more creditors. ( )20. Financial statements are the end products of the accounting process. ( )Ⅳ. Integrated questions ( 50)Simmons Inc., whose accounting year ends on June 30, had the following balances in its ledger at June 30 of the current year (under a periodic system):Cash $3500Accounts Receivable 11000Inventory 20000Prepaid insurance 1200Office Supplies on Hand 500Furniture and Fixtures 7000Accumulated depreciation- Furniture and Fixtures 1100Delivery Equipment 6000Accumulated depreciation- Delivery Equipment 1800Accounts Payable 8500Notes payable 6500Capital Stock 15000Retained Earnings 10400Sales 110000Sales Returns and allowances 800Sales Discounts 1900Purchases 71000Purchases Returns and allowances 1000Purchases Discounts 700Transportation In 3000Sales Salaries Expense 9000Delivery Expense 2000Advertising Expense 3800Rent Expense 3600Office Salaries Expense 10300Utilities Expense 400During the year, the accounting department prepared monthlystatements using worksheets, but no adjusting entries were made in thejournals and ledgers. Data for the year-end adjustments are as follows:(1)Inventory, June 30 $16800(2)Prepaid insurance, June 30 400(3)Office Supplies on Hand 320(4)Depreciation Expense for year, Furniture and Fixtures 700(5)Depreciation Expense for year, Delivery Equipment 900(6)Accrued Sales Salaries, June 30 300(7)Accrued Office Salaries, June 30 200Required:(a)Prepare a Balance Sheet.(b) Make the closing entries in a general journal.Ⅴ.Translation (15)(a) To meet the needs of the external users, a framework of accounting standards, principles and procedures known as “general accepted accounting principle” have been developed to insure the relevance and reliability of the accounting information contained in these external financial reports.(P3 )(b)Once the appropriate adjusting entries have been made and posted to the ledger accounts, an income statement and a balance sheet may be prepared directly from the account balances.(P73)(c)The general journal is a relatively simple record in which any type of business transaction can be recorded. In contrast to the general journal, a special journal is designed to record a specific type of frequently occurring business transaction.(P44)(d)One of the most important functions of accounting is to accumulateand report financial information that shows an organization’s financial position and the results of its operations to its interested users.(P3)(e)There are three basic financial statements which are the end products of financial accounting: Balance Sheet, Income Statement and the Statement of Cash Flows.(P11)(f)The plan of organization and all of the coordinate methods and measuresadopted within a business to safeguard its assets, check accuracy and reliability of its accounting data, promote operational efficiency and encourage adherence to prescribed managerial policies.(P92).。

会计英语练习题

会计英语练习题会计英语练习题在全球化的今天,学习外语已经成为了必不可少的技能。

对于会计专业的学生来说,掌握会计英语更是至关重要。

会计英语是会计学中的一门专业英语,它涵盖了会计的各个方面,包括财务报表、成本管理、税务等。

为了帮助大家更好地掌握会计英语,下面将提供一些练习题,希望能对大家的学习有所帮助。

1. What is the English term for "资产负债表"?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Statement of Retained Earnings2. Which of the following is not an expense?A. RentB. SalaryC. Accounts ReceivableD. Utilities3. What is the English term for "总账"?A. General LedgerB. Trial BalanceC. Income StatementD. Cash Flow Statement4. What is the English term for "应收账款"?A. Accounts PayableB. Accounts ReceivableC. InventoryD. Prepaid Expenses5. What is the English term for "固定资产"?A. Current AssetsB. Fixed AssetsC. Intangible AssetsD. Accounts Payable6. What is the English term for "净利润"?A. Gross ProfitB. Operating IncomeC. Net IncomeD. Retained Earnings7. What is the English term for "应付账款"?A. Accounts PayableB. Accounts ReceivableC. Accrued ExpensesD. Prepaid Expenses8. What is the English term for "现金流量表"?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Statement of Retained Earnings9. What is the English term for "财务报表分析"?A. Financial Statement AnalysisB. Cost AccountingC. TaxationD. Budgeting10. What is the English term for "税务"?A. Financial Statement AnalysisB. Cost AccountingC. TaxationD. Budgeting以上是一些关于会计英语的练习题,希望大家能够认真思考并给出正确答案。

会计专业英语试卷(推荐5篇)

A.withdrawalsB.accounts receivableC.interest payable 6.Which of the following is an assets account?

A.notes missionC.bonds payable 7.Which of the following is an owner’s equity account?

Passage 1

Many rule govern drivers on the streets and highways.The most common one is the speed limit.The speed limit controls how fast a car may go.On streets in the city, the speed limit is usually 25 or 35 miles per hour.On the highways between cities, the speed limit is usually 55 miles per hour.When people drive faster than the speed limit, a policeman can stop them.The policeman gives them pieces of paper which call traffic tickets.Traffic tickets tell the drivers how much they must pay.When drivers receive too many tickets, they probably cannot drive for a while.The rush hour is when people are going to or returning from work.At rush hour there are many cars on the streets and traffic moves very slowly.Nearly al big cities have rush hours and traffic jams.Drivers do not get tickets very often for speeding during the rush hour because they cannot drive fast.1.The most common rule to govern drivers on the streets and highways is _____.A.the traffic lightB.the traffic licenseC.the traffic jamD.th计专业英语试卷(推荐5篇)

会计学专业 会计英语试题

一、words and phrases1.残值 scrip value2.分期付款 installment3.concern 企业4.reversing entry 转回分录5.找零 change6.报销 turn over7.past due 过期8.inflation 通货膨胀9.on account 赊账10.miscellaneous expense 其他费用11.charge 收费12.汇票 draft13.权益 equity14.accrual basis 应计制15.retained earnings 留存收益16.trad-in 易新,以旧换新17.in transit 在途18.collection 托收款项19.资产 asset20.proceeds 现值21.报销 turn over22.dishonor 拒付23.utility expenses 水电费24.outlay 花费25.IOU 欠条26.Going-concern concept 持续经营27.运费 freight二、Multiple-choice question1.Which of the following does not describe accounting? ( C )A. Language of businessB. Useful ofr decision makingC. Is an end rathe than a means to an end.ed by business, government, nonprofit organizations, and individuals.2.An objective of financial reporting is to ( B )A. Assess the adequacy of internal control.B.Provide information useful for investor decisions.C.Evaluate management results compared with standards.D.Provide information on compliance with established procedures.3.Which of the following statements is(are) correct?( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.A company may use different depreciation methods in its financial statements and its income tax return.C.The cost of a machine includes the cost of repairing damage to the machine during the installation process.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the unit-of-product method.4. Which of the following is(are) correct about a company’s balance sheet? ( B )A.It displays sources and uses of cash for the period.B.It is an expansion of the basic accounting equationC.It is not sometimes referred to as a statement of financial position.D.It is unnecessary if both an income statement and statement of cash flows are availabe.5.Objectives of financial reporting to external investors and creditors include preparing information about all of the following except. ( A )rmation used to determine which products to poducermation about economic resources, claims to those resources, and changes in both resources and claims.rmation that is useful in assessing the amount, timing, and uncertainty of future cash flows.rmation that is useful in making ivestment and credit decisions.6.Each of the following measures strengthens internal control over cash receipts except. ( C )A.The use of a petty cash fund.B.Preparation of a daily listing of all checks received through the mail.C.The use of cash registers.D.The deposit of cash receipts in the bank on a daily basis.7.The primary purpose for using an inventory flow assumption is to. ( A )A.Offset against revenue an appropriate cost of goods sold.B.Parallel the physical flow of units of merchandise.C.Minimize income taxes.D.Maximize the reported amount of net income.8.In general terms, financial assets appear in the balance sheet at. ( B )A.Current valueB.Face valueC.CostD.Estimated future sales value.9.If the going-concem assumption is no longer valid for a company except. ( C )nd held as an ivestment would be valued at its liquidation value.B.All prepaid assets would be completely written off immediately.C.Total contributed capital and retained earnings would remain unchanged.D.The allowance for uncollectible accounts would be eliminated.10.Which of the following explains the debit and credit rules relating to the recording of revenue and expenses?( C )A.Expenses appear on the left side of the balance sheet and are recorded by debits;revenue appears on the right side of the balance sheet and is reoorded by credits.B. Expenses appear on the left side of the income statement and are recorded by debits; Revenue appears on the right side of the income statement and is recorded by credits.C.The effects of revenue and expenses on owners’ equity.D.The realization principle and the matching principle.11.Which of the following statements is(are) correct?( B )A.Accumulated depreciation represents a cash fund being accumulated for the replacement of plant assets.B.The cost of a machine do not includes the cost of repairing damage to the machine during the installation prcess.C.A company may use same depreciation methods in its finacial statements and its income tax return.D.The use of an accelerated depreciation method causes an asset to wear out more quickly than does use of the straight-line method.12.A set of financial statements ( B ) except.A.Is intended to assist users in evaluating the financial position, profitability, and future prospects of an entity.B.Is intended to assist the Intemal Revenue Service in detemining the amount of income taxes owed by a business organization.C.Includes notes disclosing information necessary for the proper interpretation of the statements.D.Is intended to assist investors and creditors in making decisions inventory the allocation of economic resources.13.The primary purpose for using an inventory flow assumption is to. ( B )A.Parallel the physical flow of units of merchandise.B.Offset against revenue an appropriate cost of goods soldC.Minimize income taxes.D.Maximize the reported amount of net income.14.Indicate all correct answers. In the accounting cycle. ( D )A.Transactions are posted before they are journalized.B.A trial balance is prepared after journal entries haven’t been posted.C.The Retained Earnings account is not shown as an up-to-date figure in the trial balance.D.Joumal entries are posted to appropriate ledger accounts.15.According to text, Objectives of Financial Reporting by Business Enterprises. ( D )A.Extemal users have the ability to prescribe information they want.rmation is always based on exact measures.C.Financial reporting is usually based on industries or the economy as a whole.D.Financial accounting does not directly measure the value of a business enterprise.16.Indicate all correct answers. Dividends except ( A )A.Decrease owners’ equity.B.Decrease net incomeC.Are recorded by debiting the Cash accountD.Are a business expense17.Which of the following practices contributes to efficient cash management? ( C )A.Never borrow money-maintain a cash balance sufficient to make all necessary payments.B.Record all cash receipts and cash payments at the end of the month when reconciling the bank statements.C.Prepare monthly forecasts of planned cash receipts, payments, and anticipated cash balances up toa year in advance. D.Pay each bill as soon as the invoice arrives.18.Which of the following would you expect to find in a correctly prepared income statement? ( A )A.Revenues earned during the period.B.Cash balance at the end of the period.C.Contributions by the owner during the period.D.Expenses incurred during the next period to earn revenues.19.Which of the following are important factors in ensuring the integrity of accounting information? ( D )A.Institutional factors, such as standards for preparing information.B.Professional organizations, such as the American Institute of CPAs.petence’judgment’and ethical behavior of individual accountants’D.All of the above.三、Practices11.On Jan.1, 2000, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $40,000 for 2000, calculated under the sum-of –the-years’–digits method. Required: Determine the acquisition cost of the equipment. ( C )A.$210,000B.$250,000C.$225.000D.$200,0002. On Jan.2, 2002, Mark Co, acquired equipment to use in its operations. The equipment has an estimated useful life of 10 years and an estimated salvage value of $5,000. The depreciation applicable to this equipment was $24,000 for 2004, calculated under the sum-of –the-years’–digits method (4%). Required: Determine the acquisition cost of the equipment. ( C )A.$220,000B.$250,000C.$224.000D.$200,0003. October 1, 2005, Coast Financial Ioaned Bart Corporation $3000,000, receiving in exchange a nine-month, 12 percent note receivable. Coast ends its fiscal year on December 31 and makes adjusting entries to accrue interest earned on all notes receivable. The interest earned on the note receivable from Bart Corporation during 2006 will amount to. ( A )A.$9,000B.$18,000C.$27.000D.$36,000Question: What is the reconciled balance? ( B )A.$4,187B.$4,085C.$4,090D.$4,000Required: Choose the reconciled balance. ( D )A.$3,220B.$3,250C.$3,200D.$3,225Required:Calculate the cost of goods available for sale(C)A.$475,000B.$474,000C.$470,000D.$473,000Required: Calculate the cost of goods sold ( D )A.$225,000B.$254,000C.$250,000D.$253,0008.At the end of the current year, the accounts receivable account has a debit balance of $60,000 and net sales for the year total $100,000. The allowance account before adjunstment has adebit balance of a $500, and uncollectible accounts expense is estimated at 1% of net sales. Question: The entry for the above bad debts is ( A )A.Dr. Bad Debt Accts. $1,500B.Dr. Bad Debt Accts. $500Cr. Allowance Doubtful Accts. $1,500 Cr. Allowance Doubtful Accts. $500C. Dr. Bad Debt Accts. $1,000D. Dr. Bad Debt Accts. $1,500Cr. Accts Rec. $1,000 Cr. Accts Rec. $1,5009.The balance sheet items to The Oven Bakery(arranged in alphabetical order)were as follows at August 1,2005.(You are to compute the missing figure for retained earnings.)(4%)REQUIRED:Find Retained earnings at August 1 2005(D)A.$420,000B.$44,000C.$40,000D.$48,000Practices2Sue began a public accounting practice and completed these transactions during first month of the current year.Required: Choose the entries to record the following transactons.1.Invested $50,000 cash in a public accounting practice begun this day. ( A )A.Dr. Cash $50,000B.Dr. Capital Stock $50,000Cr. Capital Stock $50,000 Cr. Cash $50,0002.Paid cash for three monts’ office rent in advance $900( B )A.Dr. Rent Exp. $900B.Dr. Prepaid Rent $900Cr. Cash $900 Cr. Cash $9003.Paid the premium on two insurance policies, $300. ( )A.Dr. Prepaid Insurance $300B.Dr. Insurance Exp $300Cr. Cash $300 Cr. Cash $300pleted accounting work for Sun Bank on credit $1000. ( A )A.Dr. Accts Rec $1000B.Dr. Cash $1000Cr.Accounting Revenue $1000 Cr.Accounting Revenue $10005.Paid the monthly utility bills of the accounting office $300 ( A )A.Dr Utility Exp $300B.Dr office Exp $300Cr. Cash $300 Cr. Cash $300Linda began a public accounting practice and completed these transactons during first month of the current year.Required: Choose the entries to record the following transactons.6.Invested $20,000 cash in a public accounting practice begun this day. ( A )A.Dr Cash $20,00B.Dr Capital Stock $20,000Cr. Capital Stock $20,000 Cr. Cash $20,007.Paid cash for three months’ office rent in advance $1200.( B )A.Dr. Rent Exp $1200B.Dr. Prepaid Rent $1200Cr. Cash $1200 Cr. Cash $12008.Purchased offfice supplies $100 and office equipment $2,000 on credit. ( B )A.Dr. Office Equipment $2,000B.Dr.Office Equipment $2,000Office Supplies $100 Office Supplies $100Cr. Accts Rec. $2,100 Cr.Accts Pay. $2,100pleted accounting work for Jack Hall and collected $2000 cash therefore. ( B )A.Dr. Accts Rec $2000B.Dr. Cash $2000Cr.Accounting Revenue $2000 Cr.Accounting Revenue $200010.Purchase additional office equipment on credit $2500.( A )A.Dr.Office equipment $2500B.Dr. Office equipment $2500Cr.Accts Pay $2500 Cr.Accts Rec $2500四、Translation:1)The mechanics of double-entry accounting are such that every transaction is recorded in the debit side of one or more accounts and in the credit side of one or more accounts with equal debits and credits. Such form of combination is called accounting entry. Where there are only two accounts affected. 2)the debit and credit amounts are equal. If more than two accounts are affceted, the total of the debit entries must equal the total of the credit entries. The double-entry accounting is used by virtually every business organization, regardless of whether the company’s accounting records are maintained manually or by computer.1.The mechanics of double-entry accounting.( B )A.会计两次记账的制度B.复式记账机制C.会计的重复记账体制2.the debit and credit amounts are equal. ( A )A.借方金额与贷方金额是相等的B.借出金额与贷款金额是相等的C.借入金额与贷款金额是相等的Most accounting methods are based on the assumption that the business enterprise will have a long life. Experience indicates that.1)inspite of numerous business failures, companies have a fairly high continuance rate. Accountants do not believe that business firms will last indefinitely, but they do expect them to last long enouthto 2)fulfill their objectives and commitments.3.in spite of numerous business failures, companies have a fairly high continuance rate. ( B )A.可惜有许多企业失败,但公司仍有较高的持续经营比率。

会计英语练习题

会计英语练习题一、词汇练习1. 请将下列会计术语的英文翻译成中文:- Assets:- Liabilities:- Equity:- Revenue:- Expense:- Depreciation:2. 请将下列中文会计术语翻译成英文:- 资产负债表:- 利润表:- 现金流量表:- 折旧:- 应收账款:- 存货:二、填空题1. The balance sheet is a statement of a company's financial position at a particular point in time, showing all the company's assets, liabilities, and __________.2. The income statement, also known as the profit and loss statement, is used to calculate the __________ of a business over a certain period of time.3. When a company purchases a new piece of equipment, it will record this as an __________ on the balance sheet.4. The __________ method of accounting records transactions when the cash is actually received or paid.5. If a company has a net loss, it will decrease the__________ on the balance sheet.三、简答题1. 请简述会计的四大基本假设。

2. 什么是会计准则?请举例说明。

会计英语试题及答案

会计英语试题及答案会计专业英语是会计专业人员职业发展的必要工具。

学习会计专业英语就是学习如何借助英语解决与完成会计实务中涉外的专业性问题和任务。

以下为你收集了会计英语练习题及答案,希望给你带来一些参考的作用。

一、单选题1. Which of the following statements about accounting concepts or assumptions are correct? 1) The money measurement assumption is that items in accounts are initially measured at their historical cost.2)In order to achieve comparability it may sometimes be necessary to override the prudence concept.3) To facilitate comparisons between different entities it is helpful if accounting policies and changes in them are disclosed.4) To comply with the law, the legal form of a transaction must always be reflected in financial statements. A 1 and 3 B 1 and 4 C 3 only D 2 and 3 2. Johnny had receivables of $5 500 at the start of 2010. During the year to 31 Dec 2010 he makes credit sales of $55 000 and receives cash of $46 500 from creditcustomers. What is the balance on the accounts receivables at 31 Dec 2010? A. $8 500 Dr B. $8 500 Cr C. $14 000 Dr D. $14 000 Cr3. Should dividends paid appear on the face of a company’s cash flow statement?A. YesB. NoC. Not sureD. Either4. Which of the following inventory valuation methods is likely to lead to the highest figure for closing inventory at a time when prices are dropping?A. Weighted Average costB. First in first out (FIFO)C. Last in first out (LIFO)D. Unit cost 5. Which of following items may appear as non-current assets in a company’s the statement of financial position?(1) plant, equipment, and property (2) company car(3) 4000 cash (4) 1000 cheque A. (1), (3)B. (1), (2)C. (2), (3)D. (2), (4)6. Which of the following items may appear as current liabilities in a company’s balance sheet?(1) investment in subsidiary(2) Loan matured within one year. (3) income tax accrued untill year end. (4) Preference dividend accrued A (1), (2) and (3) B (1), (2) and (4) C (1), (3) and (4) D (2), (3) and (4)7. The trial balance totals of Gamma at 30 September 2010 are:Debit $992,640 Credit $1,026,480Which TWO of the following possible errors could, when corrected, cause the trial balance to agree?1. An item in the cash book $6,160 for payment of rent has not been entered in the rent payable account.2. The balance on the motor expenses account $27,680 has incorrectly been listed in the trial balance as a credit.3. $6,160 proceeds of sale of a motor vehicle has been posted to the debit of motor vehicles asset account.4. The balance of $21,520 on the rent receivable account has been omitted from the trial balance. A 1 and 2 B 2 and 3 C 2 and 4 D 3 and 48. Listed below are some characteristics of financial information. (1) True (2) Prudence (3)Completeness (4) CorrectWhich of these characteristics contribute to reliability? A (1), (3) and (4) only B (1), (2) and (4) only C (1), (2) and (3) only D (2), (3) and (4) only (window.cproArray = window.cproArray || []).push({ id: "u3054369" });9. Which of the following statements are correct?(1) to be prudent, company charge depreciation annually on the fixed asset(2) substance over form means that the commercial effect of a transaction must always be shown in the financial statements even if this differs from legal form(3) in order to achieve the comparable, items should be treated in the same way year on year A. 2 and 3 only B. All of them C. 1 and 2 only D. 3 only10. which of the following about accruals concept are correct? (1) all financial statements are based on the accruals concept(2) the underlying theory of accruals concept and matching concept are same(3) accruals concept deals with any figure that incurred in the period irrelevant with it’s paid or notA. 2 and 3 onlyB. All of themC. 1 and2 only D.3 only二、翻译题1、将下列分录翻译成英文1. 借:固定资产清理 30 000累计折旧10 000 贷:固定资产 40 000 2.借:应付票据40 000 贷:银行存款 40 000 2、将下列词组按要求翻译(中翻英,英翻中) (1) 零用资金 (2) 本票 (3) 试算平衡(4) 不动产、厂房和设备 (5) Notes and coins (6) money order (7) general ledger (8) direct debt (9) 报销(10) revenue and gains三、业务题Johnny set up a business and in the first a few days of trading the following transactions occurred (ignoreall the tax):1) He invests $80 000 of his money in his business bank account.2) He then buys goods from Isabel, a supplier for $4 000 and pays by cheque, the goods is delivered right after the payment3) A sale is made for $3 000 –the customer pays by cheque4) Johnny makes another sale for $2 000 and the customer promises to pay in the future 5) He then buys goods from another supplier, Kamen, for $2 000 on credit, goods is delivered on time6) He pays a telephone bill of $800 by cheque7) The credit customer pays the balance on his account8) He returened some faulty goods to his supplier Kamen, which worth $400. 9) Bank interest of $70 is received10) A cheque customer returned $400 goods to him for a refund(window.cproArray = window.cproArray || []).push({ id: "u3054371" });参考答案1、单选题1-5 CCACB 6-10 DCABA2、翻译题1)中翻英1.Dr disposal of fixed assetDepreciation Cr fixed asset2.Dr notes payableCr bank3、业务题1) Dr Cash Cr capital2) Dr finished goods Cr Cash3)Dr CashCr sales revenue4) Dr accounts receivable Cr sales revenue5) Dr finished goods Cr accounts re ceivable6) Dr administrative expense Cr Cash7)Dr CashCr accounts receivable8)Dr CashCr finished goods9)Dr CashCr financial expense10) Dr sales revenue Cr Cash。

会计学英语试题及答案

会计学英语试题及答案一、单项选择题(每题2分,共10题)1. Which of the following is not a financial statement?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Tax Return2. The process of recording all financial transactions in a company is known as:A. BudgetingB. ForecastingC. BookkeepingD. Auditing3. What does the term "Depreciation" refer to?A. The increase in value of an asset over timeB. The decrease in value of an asset over timeC. The sale of an assetD. The purchase of an asset4. Which of the following is not a type of receivable?A. Accounts ReceivableB. Notes ReceivableC. InventoryD. Trade Receivables5. What is the purpose of an audit?A. To ensure compliance with tax lawsB. To verify the accuracy of financial recordsC. To prepare financial statementsD. To manage the company's budget6. The term "Equity" in accounting refers to:A. The total assets of a companyB. The total liabilities of a companyC. The owner's investment in the companyD. The company's net income7. Which of the following is not a component of a balance sheet?A. AssetsB. LiabilitiesC. EquityD. Revenue8. The accounting equation is represented as:A. Assets = Liabilities + EquityB. Assets = Liabilities - EquityC. Assets - Liabilities = EquityD. Assets + Equity = Liabilities9. What is the term used to describe the conversion of cash into other assets?A. InvestingB. FinancingC. OperatingD. Spending10. Which of the following is a non-current asset?A. CashB. InventoryC. LandD. Office Supplies二、多项选择题(每题3分,共5题)1. Which of the following are considered as current assets?A. CashB. Accounts ReceivableC. InventoryD. Land2. The following are examples of liabilities except:A. Accounts PayableB. Long-term DebtC. Common StockD. Retained Earnings3. The following are types of expenses in an income statement except:A. Cost of Goods SoldB. Salaries and WagesC. DividendsD. Depreciation4. Which of the following are considered as equity transactions?A. Issuance of SharesB. Declaration of DividendsC. EarningsD. Payment of Dividends5. The following are true statements about accountingprinciples except:A. The going concern assumptionB. The matching principleC. The cash basis of accountingD. The accrual basis of accounting三、判断题(每题1分,共5题)1. True or False: The accounting cycle includes the processof closing the books at the end of an accounting period.2. True or False: All prepaid expenses are considered current assets.3. True or False: Revenue recognition is based on the cash received.4. True or False: The statement of cash flows is preparedusing the cash basis of accounting.5. True or False: The accounting equation must always balance.四、简答题(每题5分,共2题)1. Explain the difference between revenue and profit.2. Describe the role of the statement of cash flows infinancial reporting.五、计算题(每题10分,共1题)A company has the following transactions during the month:- Cash sales: $10,000- Accounts receivable: $5,000- Accounts payable: $3,000- Inventory purchased on credit: $2,000- Cash paid for expenses: $1,500Calculate the company's cash flow from operating activities for the month.答案:一、单项选择题1. D2. C3. B4. C5. B6. C7. D8. A9. A10. C二、多项选择题1. A, B, C2. C, D3. C4. A, D5. C三、判断题1. True2. True3. False4. False5. True四、简答题1. Revenue is the income generated from the normal business activities of a company over a specific period, before any expenses are deducted. Profit, on the other hand, is the amount of money remaining after all expenses have been deducted from the revenue. It represents the net income or net loss of a company.2. The statement of cash flows is a financial statement that provides information about the cash receipts。

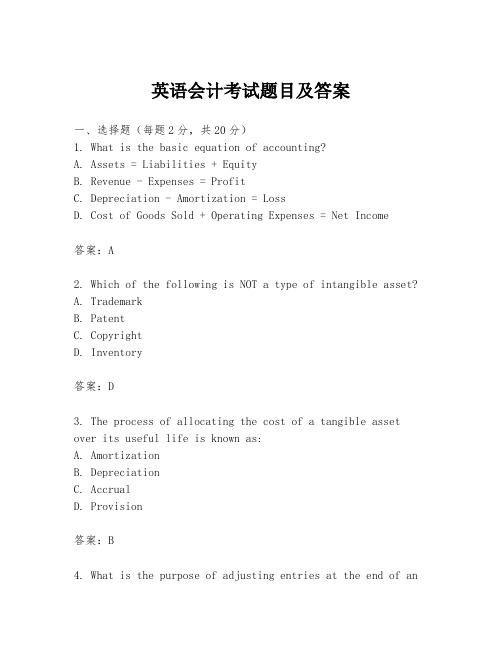

英语会计考试题目及答案

英语会计考试题目及答案一、选择题(每题2分,共20分)1. What is the basic equation of accounting?A. Assets = Liabilities + EquityB. Revenue - Expenses = ProfitC. Depreciation - Amortization = LossD. Cost of Goods Sold + Operating Expenses = Net Income答案:A2. Which of the following is NOT a type of intangible asset?A. TrademarkB. PatentC. CopyrightD. Inventory答案:D3. The process of allocating the cost of a tangible asset over its useful life is known as:A. AmortizationB. DepreciationC. AccrualD. Provision答案:B4. What is the purpose of adjusting entries at the end of anaccounting period?A. To increase the company's profitB. To ensure the financial statements are accurate and up-to-dateC. To reduce the company's tax liabilityD. To prepare for the next accounting period答案:B5. The term "Double Entry Bookkeeping" refers to the practice of:A. Recording transactions twiceB. Recording debits and credits for every transactionC. Keeping two sets of booksD. Using two different accounting software答案:B...二、简答题(每题10分,共30分)1. Explain the difference between "revenue recognition" and "matching principle".答案:Revenue recognition is the process of recognizing income in the accounting records as it is earned, regardless of when payment is received. The matching principle, on the other hand, is an accounting concept that requires expenses to be recognized in the same accounting period as the revenue they helped generate. This ensures that the financial statements reflect the actual performance of the business fora given period.2. What are the main components of a balance sheet?答案:The main components of a balance sheet are assets, liabilities, and equity. Assets represent what the company owns, liabilities represent what the company owes, and equity represents the residual interest in the assets of the entity after deducting liabilities....三、计算题(每题15分,共30分)1. Given the following information for XYZ Corp., calculate the net income for the year ended December 31, 2023:- Sales revenue: $500,000- Cost of goods sold: $300,000- Operating expenses: $100,000- Depreciation expense: $20,000- Interest expense: $10,000答案:Net Income = Sales Revenue - (Cost of Goods Sold + Operating Expenses + Depreciation Expense + Interest Expense) Net Income = $500,000 - ($300,000 + $100,000 + $20,000 + $10,000)Net Income = $500,000 - $440,000Net Income = $60,0002. If a company purchased a machine for $50,000 and expectsit to have a useful life of 5 years with no residual value, calculate the annual depreciation expense using the straight-line method.答案:Annual Depreciation Expense = (Cost of Asset - Residual Value) / Useful LifeAnnual Depreciation Expense = ($50,000 - $0) / 5Annual Depreciation Expense = $10,000...结束语:希望这份英语会计考试题目及答案对您的学习和复习有所帮助。

会计英语考试题目及答案

会计英语考试题目及答案一、选择题(每题2分,共20分)1. Which of the following is a basic accounting principle?A. The Going Concern PrincipleB. The Historical Cost PrincipleC. Both A and BD. Neither A nor BAnswer: C. Both A and B2. What is the term for the systematic arrangement of accounts in a specific order?A. JournalB. LedgerC. Trial BalanceD. Chart of AccountsAnswer: D. Chart of Accounts3. What does the term "Debit" mean in accounting?A. An increase in assetsB. A decrease in liabilitiesC. An increase in equityD. A decrease in expensesAnswer: A. An increase in assets4. Which of the following is not a type of financialstatement?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Payroll ReportAnswer: D. Payroll Report5. What is the purpose of an adjusting entry?A. To update the financial recordsB. To prepare for the next accounting periodC. To correct errors in the accounting recordsD. All of the aboveAnswer: D. All of the above6. Which of the following is an example of a current asset?A. InventoryB. LandC. EquipmentD. Bonds PayableAnswer: A. Inventory7. What is the formula for calculating the return on investment (ROI)?A. (Net Income / Total Assets) * 100B. (Net Income / Total Equity) * 100C. (Net Income / Investment) * 100D. (Total Assets / Net Income) * 100Answer: C. (Net Income / Investment) * 1008. What is the accounting equation?A. Assets = Liabilities + EquityB. Liabilities - Equity = AssetsC. Assets + Liabilities = EquityD. Equity + Assets = LiabilitiesAnswer: A. Assets = Liabilities + Equity9. What is the purpose of depreciation?A. To reduce the value of an asset over timeB. To increase the value of an asset over timeC. To calculate the cost of an assetD. To determine the net income of a companyAnswer: A. To reduce the value of an asset over time10. Which of the following is not a function of a general ledger?A. To record daily transactionsB. To summarize financial informationC. To provide a detailed account of each transactionD. To prepare financial statementsAnswer: A. To record daily transactions二、简答题(每题5分,共30分)1. Explain the difference between an asset and a liability. Answer: An asset is a resource owned by a business that hasfuture economic benefit, such as cash, inventory, or property.A liability is an obligation or debt that a business owes to others, such as loans, accounts payable, or salaries payable.2. What is the purpose of a balance sheet?Answer: The purpose of a balance sheet is to provide a snapshot of a company's financial position at a specificpoint in time, showing the company's assets, liabilities, and equity.3. Define the term "revenue."Answer: Revenue is the income generated from the normal business operations of a company, such as the sale of goodsor services.4. What is the difference between a journal and a ledger?Answer: A journal is a book that records financialtransactions in chronological order, while a ledger is a book that summarizes and organizes the financial transactions by accounts.5. Explain the concept of accrual accounting.Answer: Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned or incurred, not when cash is received or paid.6. What is the purpose of a trial balance?Answer: The purpose of a trial balance is to ensure that the total debits equal the total credits in the general ledger, indicating that the accounting records are in balance.三、案例分析题(每题25分,共50分)1. A company purchased equipment for $50,000 on January 1, 2023, with a useful life of 5 years and no residual value. Calculate the annual depreciation expense using the straight-line method.Answer: Using the straight-line method, the annual depreciation expense is calculated as follows:Depreciation Expense = (Cost of Equipment - Residual Value) / Useful LifeDepreciation Expense = ($50,000 - $0) / 5 = $10,000 per year2. A company has the following transactions for the month of March 2023:- Sold goods for $20,000 on credit.- Purchased inventory for $15,000 in cash.- Paid $2,000 in salaries.- Received $18,。

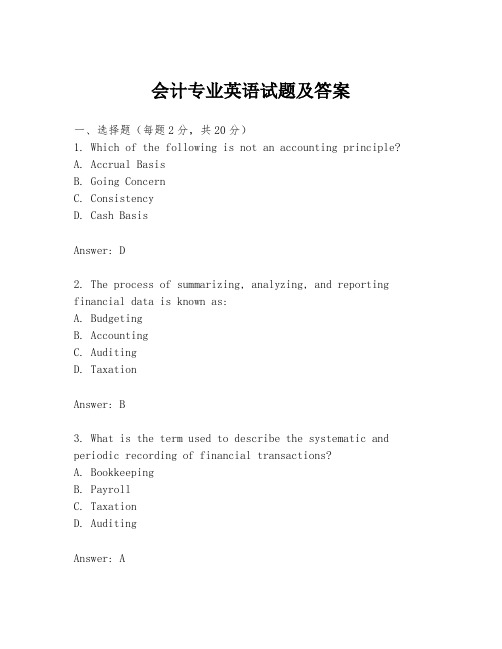

会计专业英语试题及答案

会计专业英语试题及答案一、选择题(每题2分,共20分)1. Which of the following is not an accounting principle?A. Accrual BasisB. Going ConcernC. ConsistencyD. Cash BasisAnswer: D2. The process of summarizing, analyzing, and reporting financial data is known as:A. BudgetingB. AccountingC. AuditingD. TaxationAnswer: B3. What is the term used to describe the systematic and periodic recording of financial transactions?A. BookkeepingB. PayrollC. TaxationD. AuditingAnswer: A4. Which of the following is not a component of the balance sheet?A. AssetsB. LiabilitiesC. EquityD. RevenueAnswer: D5. The matching principle requires that:A. Expenses are recognized when incurredB. Expenses are recognized when paidC. Expenses are recognized in the same period as the revenue they generateD. Expenses are recognized when the cash is received Answer: C6. The accounting equation is:A. Assets = Liabilities + EquityB. Assets - Liabilities = EquityC. Assets + Equity = LiabilitiesD. Assets = Equity - LiabilitiesAnswer: A7. The term "double-entry bookkeeping" refers to the practice of:A. Recording transactions twiceB. Recording transactions in two accountsC. Recording debits and credits for every transactionD. Recording transactions in two different booksAnswer: C8. Which of the following is not a type of intangible asset?A. PatentsB. TrademarksC. GoodwillD. InventoryAnswer: D9. The purpose of an income statement is to show:A. The financial position of a company at a point in timeB. The changes in equity over a period of timeC. The financial performance of a company over a period of timeD. The cash flows of a company over a period of time Answer: C10. The statement of cash flows is used to report:A. How cash is generated and used during a periodB. The net income of a company for a periodC. The changes in equity for a periodD. The changes in assets and liabilities for a period Answer: A二、填空题(每题2分,共20分)1. The accounting cycle includes the following steps:journalizing, posting, __________, adjusting entries, and closing entries.Answer: trial balance2. The __________ principle requires that all business transactions should be recorded at their fair value in the accounting records.Answer: Fair Value3. The __________ is a summary of all the journal entries fora period, listed in date order.Answer: General Journal4. __________ are expenses that have been incurred but not yet paid.Answer: Accrued Expenses5. The __________ is a report that shows the beginning cash balance, cash receipts, cash payments, and the ending cash balance for a period.Answer: Cash Flow Statement6. The __________ ratio is calculated by dividing current assets by current liabilities.Answer: Current Ratio7. __________ are assets that are expected to be converted into cash or used up within one year or one operating cycle. Answer: Current Assets8. __________ is the process of determining the cost of goodssold and the value of ending inventory.Answer: Costing9. __________ is the process of estimating the useful life of an asset and allocating its cost over that period.Answer: Depreciation10. __________ is the process of adjusting the accounts to reflect the proper revenue and expenses for the period. Answer: Accrual Accounting三、简答题(每题10分,共20分)1. Explain the difference between revenue and profit. Answer: Revenue is the income generated from the normal business activities of an entity during a specific period, before deducting expenses. Profit, on the other hand, is the excess of revenues and gains over expenses and losses for a period. It represents the net income or net earnings of a business.2. What are the main components of a balance sheet?Answer: The main components of a balance sheet are assets, liabilities, and equity. Assets represent what a company owns or controls with future economic benefit. Liabilities are obligations or debts that a company owes to others. Equity is the residual interest in the assets of the entity after deducting all its liabilities, representing the ownership interest of the shareholders.四、计算题(每题15分,共30分)1. Calculate the net income for the year if the revenue is$500,000, the cost of goods sold is $300,000, operating expenses are $80,000, and other expenses are $20,000. Answer: Net Income = Revenue - Cost of Goods Sold - Operating。

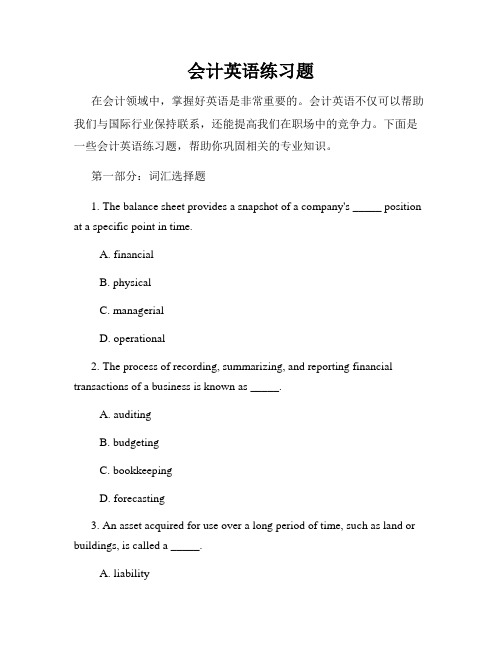

会计英语练习题

会计英语练习题在会计领域中,掌握好英语是非常重要的。

会计英语不仅可以帮助我们与国际行业保持联系,还能提高我们在职场中的竞争力。

下面是一些会计英语练习题,帮助你巩固相关的专业知识。

第一部分:词汇选择题1. The balance sheet provides a snapshot of a company's _____ position at a specific point in time.A. financialB. physicalC. managerialD. operational2. The process of recording, summarizing, and reporting financial transactions of a business is known as _____.A. auditingB. budgetingC. bookkeepingD. forecasting3. An asset acquired for use over a long period of time, such as land or buildings, is called a _____.A. liabilityB. revenueC. expenseD. fixed asset4. The amount of money a business has left after deducting its expenses from its revenue is called _____.A. profitB. lossC. turnoverD. equity5. The process of examining a company's financial records to ensure their accuracy and compliance with laws and regulations is called _____.A. taxationB. auditingC. financingD. investing第二部分:填空题6. The _____ department is responsible for preparing financial statements and analyzing financial data.7. The primary objective of the income statement is to measure a company's _____ performance over a period of time.8. The _____ method of inventory valuation assumes that the cost of goods sold is based on the cost of the most recent purchases.9. The _____ ratio measures a company's ability to meet its short-term financial obligations.10. The _____ principle requires that expenses be recognized in the same accounting period as the revenue they help generate.第三部分:阅读理解题请阅读以下会计报表的摘录,并回答问题。

会计专业英语试题含答案

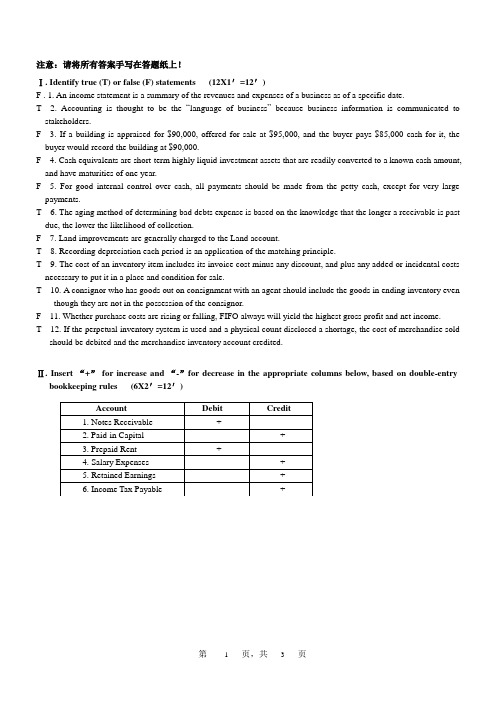

注意:请将所有答案手写在答题纸上!Ⅰ. Identify true (T) or false (F) statements (12X1′=12′)F . 1. An income statement is a summary of the revenues and expenses of a business as of a specific date.T 2. Accounting is thought to be the “language of business”because business information is communicated to stakeholders.F 3. If a building is appraised for $90,000, offered for sale at $95,000, and the buyer pays $85,000 cash for it, the buyer would record the building at $90,000.F 4. Cash equivalents are short-term highly liquid investment assets that are readily converted to a known cash amount, and have maturities of one year.F 5. For good internal control over cash, all payments should be made from the petty cash, except for very large payments.T 6. The aging method of determining bad debts expense is based on the knowledge that the longer a receivable is past due, the lower the likelihood of collection.F 7. Land improvements are generally charged to the Land account.T 8. Recording depreciation each period is an application of the matching principle.T 9. The cost of an inventory item includes its invoice cost minus any discount, and plus any added or incidental costs necessary to put it in a place and condition for sale.T 10. A consignor who has goods out on consignment with an agent should include the goods in ending inventory even though they are not in the possession of the consignor.F 11. Whether purchase costs are rising or falling, FIFO always will yield the highest gross profit and net income.T 12. If the perpetual inventory system is used and a physical count disclosed a shortage, the cost of merchandise sold should be debited and the merchandise inventory account credited.Ⅱ. Insert “+” for increase and “-”for decrease in the appropriate columns below, based on double-entry bookkeeping rules (6X2′=12′)Ⅲ. Translate the accounting terms from English to Chinese (No. 1-6) and from Chinese to English (No. 7-10) (10X2′=20′)1. General journal (总分类账)2. Accounting elements (会计要素)3. Closing entries(结账分录)4. CICPA(中国注册会计师协会)5. Net realizable value(可变现净值)6. Accrual-basis accounting (应计制会计)7. 非流动负债(non-current liabilities)8. 历史成本(Historical cost)9. 分类账(ledger)10. 经营周期(Operating cycle)Ⅳ. Short answer questions (3X6′=18′)1.What is accounting?Accounting may be described as the process of identifying, measuring, recording,and communicating economic information to permit informed judgments anddecisions by users of that information2.What is depreciation of plant assets? What is the basic purpose of depreciation?Depreciation, as the term is used in accounting, is the allocation of the cost of atangible plant asset to expense in the periods in which services are received from theasset. In short, the basic purpose of depreciation is to achieve the matching principlethat is, to offset the revenue of an accounting period with the costs of the goodsand services being consumed in the effort to generate that revenue.3.Identify the tools of financial statement analysis.The analysis of financial data employs various techniques to emphasize thecomparative and relative significance of the data presented and to evaluate theposition of the firm. Three commonly used tools are as following.Horizontal analysisevaluates a series of financial statement data over a periodof time.Verticalanalysis evaluates financial statement data by expressing each item in afinancial statement as a percent of a base amount.Ratio analysisexpresses the relationship among selected items of financialstatement data.Ⅴ. Problem Solving (38′)1. Analyze the effects of business transactions on the Accounting Equation. (2X5′=10′)Transaction (1): paid a $6,500 premium on July 1 for one year’s insurance in advance.Transaction (2): bought office equipment from Brown Company on account $2,800.2. Prepare journal entries for the two transactions in No. 1 above-mentioned. (2X5′=10′)3. Samuel Co. Ltd issued a $15,000, 6%, 9-month note payable. How much is the interest payment at maturity?(Calculating process is required) (6′)4. Assume the financial position data of Sue Company consist of the following items: (2X6′=12′)Sue CompanyBalance Sheet (Partial)January 31, 2011Required: Calculate its current ratio and acid-test ratio. Calculating steps are needed.。

会计英语课后练习题含答案

会计英语课后练习题含答案一、选择题1.Which of the following is an example of a current asset?A. LandB. BuildingsC. Accounts payableD. Long-term bonds payableAnswer: C2.Which of the following is an example of a non-current asset?A. InventoryB. Accounts receivableC. EquipmentD. Prepd expensesAnswer: C3.Which of the following is an example of a current liability?A. Long-term loans payableB. Owner’s equityC. Accounts receivableD. Accounts payableAnswer: D4.Which of the following is an example of a non-currentliability?A. Accounts payableB. Salaries payableC. Long-term loans payableD. Rent payableAnswer: C5.Which of the following is not included in the calculation ofreturn on equity (ROE)?A. Net incomeB. Total assetsC. Average stockholders’ equityD. SalesAnswer: D二、填空题1._________ is the process of recording, classifying, andsummarizing financial transactions to produce financial statements.Answer: Accounting2.The balance sheet reports the financial position of acompany as of a specific __________.Answer: Date3.The __________ principle states that expenses should berecognized when they are incurred, regardless of when they are pd.Answer: Expense recognition4.The __________ principle states that expenses should bematched to the revenues they help generate.Answer: Matching5.The __________ is the excess of total assets over totalliabilities.Answer: Stockholders’ equity三、简答题1.What is the difference between a current asset and a non-current asset?Answer: A current asset is an asset that is expected to beconverted to cash within one year or during the normal operating cycle of the business, whichever is longer. A non-current asset is an asset that is expected to be held for more than one year and is not expected to be converted to cash during the normal operating cycle of the business.2.What is the difference between a current liability and anon-current liability?Answer: A current liability is a liability that is expected to be pd off within one year or during the normal operating cycle of the business, whichever is longer. A non-current liability is aliability that is expected to be pd off more than one year in the future and is not expected to be pd off during the normaloperating cycle of the business.3.How is the income statement different from the balance sheet?Answer: The income statement reports a company’s revenues,expenses, and net income or net loss for a specific period of time, usually one year or a quarter. The balance sheet reports acompany’s financial position as of a specific date, showing it s assets, liabilities, and stockholders’ equity.4.What is the equation for the balance sheet?Answer: Assets = Liabilities + Stockholders’ equity5.What is the purpose of financial accounting?Answer: The purpose of financial accounting is to provide useful information to external users, such as investors, creditors, and regulators, to help them make informed decisions about the company. It does this by recording and reporting a company’s financial activities in a standardized format.。

会计专业英语练习题

会计专业英语练习题Chapter 2 Accounting Concepts and PrinciplesAsset 资产Liability 负债Equity 所有者权益、股本Revenue 收⼊Expense 费⽤Gain 利得Loss 损失For each item below, indicate to which category of elements of financial statements it belongs.每个项⽬下⾯,说明这类财务报表要素属于.(a) Retained earnings 留存收益equity(b) Sales 销售revenue(c) Additional paid-in capital 股本溢价equity(d) Inventory 存货asset(e) Depreciation 折旧费expense(f) Dividends 股息equity(g) Gain on sale of investment 出售投资收益gain(h)Interest payable 应付利息liability(i)Loss on sale of equipment销售设备的亏损loss(j) Issuance of commonstock发⾏普通股equityChapter 3 Financial Statements(a)Current assets.(b)Investments.(c)Property, plant, andequipment.(d)Intangible assets.(e)Other assets.(a)流动资产(b)投资(c 固定资产(d)⽆形资产(e)其他资产InstructionsIndicate by letter where each of thefollowing1.Preferred stock.2.Goodwill.3.Wages payable.4.Trade accounts payable.5.Buildings.6.Trading securities.7.Current portion of long-termdebt.8.Premium on bonds payable.9.Allowance fordoubtful accounts.10.A ccountsreceivable.s balance sheetCurrent liabilities.Non-current liabilities.Capital stock.Additional paid-in capital. Retained earnings.(f)流动负债(g)⾮流动负债。

会计英语试题及答案

会计英语试题及答案一、选择题(每题2分,共20分)1. Which of the following is not a basic accounting element?A. AssetsB. LiabilitiesB. RevenuesD. Equity答案:C2. The accounting equation can be expressed as:A. Assets = Liabilities + EquityB. Assets + Liabilities = EquityC. Assets - Liabilities = EquityD. Liabilities - Equity = Assets答案:A3. What does the term "Double Entry Bookkeeping" refer to?A. Recording transactions in two accountsB. Recording transactions in two different currenciesC. Recording transactions in two different formatsD. Recording transactions in two different books答案:A4. Which of the following is not a type of adjusting entry?A. AccrualB. PrepaymentC. DepreciationD. Amortization答案:B5. The purpose of closing entries is to:A. Prepare financial statementsB. Adjust for accruals and deferralsC. Record the sale of inventoryD. Record the purchase of fixed assets答案:A6. Which of the following is a measure of a company's liquidity?A. Return on Investment (ROI)B. Debt to Equity RatioC. Current RatioD. Profit Margin答案:C7. The term "Depreciation" refers to:A. The decrease in value of an asset over timeB. The increase in value of an asset over timeC. The amount of an asset that is used upD. The process of selling an asset答案:A8. What is the purpose of a trial balance?A. To calculate net incomeB. To check the accuracy of accounting recordsC. To determine the value of assetsD. To calculate the cost of goods sold答案:B9. Which of the following is not a financial statement?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Budget答案:D10. The accounting principle that requires expenses to be recorded in the same period as the revenues they generate is known as:A. Going ConcernB. Matching PrincipleC. Historical Cost PrincipleD. Materiality答案:B二、填空题(每题2分,共20分)1. The __________ is the process of recording financial transactions in a systematic way.答案:Journalizing2. The __________ is a summary of the financial transactionsof a business during a specific period.答案:Ledger3. __________ is the accounting principle that requires all accounting information to be based on historical cost.答案:Historical Cost Principle4. The __________ is a financial statement that shows a company's financial position at a specific point in time.答案:Balance Sheet5. __________ is the process of estimating revenues and expenses for a future period.答案:Budgeting6. __________ is the accounting principle that requires all transactions to be recorded in the period in which they occur.答案:Accrual Basis Accounting7. The __________ is a financial statement that shows the results of a company's operations over a period of time.答案:Income Statement8. __________ is the process of determining the value of a company's assets and liabilities.答案:Valuation9. __________ is the accounting principle that requires alltransactions to be recorded in the order in which they occur.答案:Chronological Order10. The __________ is a financial statement that shows the sources and uses of cash during a period of time.答案:Cash Flow Statement三、简答题(每题15分,共30分)1. 描述会计信息的质量特征有哪些,并简要解释它们的含义。

会计英语的考试题目及答案

会计英语的考试题目及答案会计英语考试题目及答案一、选择题(每题2分,共20分)1. What is the term used to describe the process of recording financial transactions in a company's books?A. BudgetingB. AccountingC. AuditingD. Forecasting答案:B2. Which of the following is not a type of financial statement?A. Balance SheetB. Income StatementC. Cash Flow StatementD. Sales Report答案:D3. The process of ensuring that the financial records are accurate and complete is known as:A. BookkeepingB. AccountingC. AuditingD. Reporting答案:C4. What is the primary purpose of an income statement?A. To show the financial position of a company at a specific point in time.B. To show the changes in equity of a company over a period of time.C. To show the profitability of a company over a period of time.D. To show the cash inflows and outflows of a company over a period of time.答案:C5. Which of the following is not a principle of accounting?A. Accrual BasisB. ConsistencyC. MaterialityD. Fair Value答案:D6. The term "double-entry bookkeeping" refers to the practice of:A. Recording transactions twice in different accounts.B. Recording transactions in two different ways.C. Recording debits and credits for every transaction.D. Recording transactions in two different books.答案:C7. The accounting equation is:A. Assets = Liabilities + EquityB. Assets - Liabilities = EquityC. Liabilities - Equity = AssetsD. Equity - Assets = Liabilities答案:A8. What is the purpose of depreciation in accounting?A. To increase the value of an asset.B. To allocate the cost of a tangible asset over its useful life.C. To sell an asset.D. To calculate the profit of a company.答案:B9. Which of the following is a non-current liability?A. Accounts PayableB. Wages PayableC. Long-term DebtD. Taxes Payable答案:C10. The term "revenue recognition" refers to the process of:A. Recognizing expenses when they are paid.B. Recognizing revenues when they are earned.C. Recognizing assets when they are acquired.D. Recognizing liabilities when they are incurred.答案:B二、简答题(每题5分,共20分)1. Explain the difference between "cash basis" and "accrual basis" accounting.答案:Cash basis accounting records transactions when cash is received or paid, whereas accrual basis accounting records transactions when they are earned or incurred, regardless of the cash flow.2. What is the purpose of a balance sheet?答案:The purpose of a balance sheet is to present thefinancial position of a company at a specific point in time, showing what the company owns (assets), what it owes (liabilities), and the net worth of the company's owners (equity).3. Define "depreciation" in the context of accounting.答案:Depreciation is the systematic allocation of the costof a tangible asset over its useful life, reflecting the consumption of the asset's economic benefits over time.4. What is the importance of an audit in the financial reporting process?答案:An audit provides an independent assessment of the accuracy and completeness of a company's financial statements, enhancing their credibility and reliability for stakeholders.三、案例分析题(每题15分,共30分)1. Assume you are an accountant for a company that has just sold a product for $10,000 on credit. Prepare the journalentry for this transaction under both cash basis and accrual basis accounting.答案:Under cash basis, no journal entry is made until cashis received. Under accrual basis, the journal entry would be: Dr. Accounts Receivable $10,000Cr. Revenue $10,0002. A company has the following transactions in January: purchased office supplies for $500 in cash, received $2,000for services provided in December, and accrued $1,500 in wages for January. Prepare the adjusting entries for these transactions at the end of January.答案:The adjusting entries would be:Dr. Office Supplies Expense $500Cr. Office Supplies $500 (for cash purchase)Dr. Accounts Receivable $2,000Cr. Revenue $2,000 (for services provided in December)Dr. Wages Payable $1,500Cr. Wages Expense $1,500 (for accrued wages)四、论述题(每题15分,共30分)1. Discuss the role of ethics in accounting and provide examples of ethical dilemmas that an accountant might face. 答案。

会计英语相关练习题

会计英语相关练习题1. Vocabulary Exercise请将下列词汇翻译为英语:1.资产__________________________2.负债__________________________3.所有者权益__________________________4.收入__________________________5.成本__________________________6.支出__________________________7.费用__________________________8.账户__________________________9.账户余额__________________________10.记账__________________________2. Multiple Choice Questions选择正确答案并将其序号填入括号内:1.What is the accounting equation?a)Assets = Liabilities - Owner’s Equityb)Liabilities + Owner’s Equity = Assetsc)Assets + Owner’s Equity = Liabilities2.What is the purpose of an income statement?a)To calculate net worthb)To show the financial position of acompany at a specific point in timec)To show the profit or loss of acompany over a specific period of time3.What is the difference between revenue and expenses?a)Revenue represents money coming in,while expenses represent money going outb)Revenue represents money going out,while expenses represent money coming inc)There is no difference betweenrevenue and expenses4.What is the double-entry accounting system?a)A system that records eachtransaction in only one accountb)A system that records eachtransaction in two or more accountsc)A system that records each transaction in the owner’s equity account only5.What is the purpose of a trial balance?a)To calculate the net income of a companyb)To check the accuracy of the accounting recordsc)To record transactions that occurredduring a specific period3. Fill in the Blanks请填写下列句子中的空白处:1.The balance sheet shows a company’s_______________ at a specific point in time.2.The income statement shows the_______________ and _______________ of a company over a specific period of time.3.The _______________ equation is Assets = _______________ - Owner’s Equity.4.Recording a transaction in two or more accounts is known as the _______________.5.The _______________ is used to check the accuracy of the accounting records.4. Short Answer Questions请用一至两句话回答下列问题:1.What is the purpose of a balance sheet?2.What is the difference between an incomestatement and a balance sheet?3.What is the accounting equation?4.What is the double-entry accountingsystem?5. Practical Exercise请根据下列信息,完成一张简单的收入表和支出表,然后根据这些数据回答后续的问题。

会计英语试题及答案

会计英语试题及答案一、选择题(每题2分,共20分)1. What is the term for the systematic, periodic assessmentof the performance and financial position of a business?A. AuditingB. BudgetingC. Financial AnalysisD. Forecasting答案:C. Financial Analysis2. Which of the following is not a basic accounting principle?A. Accrual Basis AccountingB. ConsistencyC. Cash Basis AccountingD. Going Concern答案:C. Cash Basis Accounting3. The process of recording transactions in a journal isknown as:A. PostingB. JournalizingC. ClosingD. Adjusting答案:B. Journalizing4. What does the term "Double Entry" refer to in accounting?A. Recording transactions twiceB. Recording transactions in two different accountsC. Recording transactions in two different waysD. Recording transactions in two different periods答案:B. Recording transactions in two different accounts5. The financial statement that provides a snapshot of a company's financial condition at a specific point in time is:A. Income StatementB. Balance SheetC. Cash Flow StatementD. Statement of Changes in Equity答案:B. Balance Sheet二、填空题(每题2分,共20分)6. The __________ is the accounting equation that shows the relationship between assets, liabilities, and equity.答案:Accounting Equation7. In accounting, the term __________ refers to theallocation of the cost of a tangible asset over its useful life.答案:Depreciation8. The __________ is the process of summarizing the transactions recorded in the ledger accounts and presentingthem in a more condensed form.答案:Trial Balance9. __________ is the method of accounting where revenues and expenses are recognized when they are earned or incurred, not necessarily when cash is received or paid.答案:Accrual Accounting10. The __________ is the financial statement that shows the changes in a company's cash and cash equivalents during a period.答案:Cash Flow Statement三、简答题(每题10分,共30分)11. Explain the purpose of a balance sheet in a business context.答案:The purpose of a balance sheet is to provide stakeholders with a snapshot of a company's financialposition at a specific point in time. It lists the company's assets, liabilities, and equity, and is used to assess the company's liquidity, solvency, and overall financial health.12. What are the main differences between an income statement and a statement of cash flows?答案:The income statement reports a company's financial performance over a period, focusing on revenues and expenses to determine net income. The statement of cash flows, on the other hand, shows the inflows and outflows of cash during thesame period, highlighting how the company generates and uses cash.13. Describe the concept of "matching principle" in accounting.答案:The matching principle in accounting requires that expenses be recognized in the same accounting period as the revenues they helped generate. This principle ensures that the financial statements reflect the actual economic activity of the period, providing a more accurate picture of the company's financial performance.四、计算题(每题15分,共30分)14. Given the following trial balance figures, calculate the total current assets and total current liabilities.| Account | Debit ($) | Credit ($) ||||-|| Cash | 12,000 | || Accounts Receivable | | 8,000 || Inventory | | 15,000 || Prepaid Expenses | 2,000 | || Accounts Payable | | 5,000 || Wages Payable | 1,000 | || Total Current Liabilities | | 6,000 |答案:Total current assets = Cash + Accounts Receivable + Inventory + Prepaid Expenses = 12,000 + 8,000 + 15,000 +2,000 = 37,000Total current liabilities = Accounts Payable + Wages Payable + Total Current Liabilities = 5,000 + 1,000 + 6,000 = 12,00015. If a company has a net income of $50,000 and an increase in retained earnings of $75,000, calculate the dividends paid by the company.答案:Dividends paid = Increase in retained earnings - Net income = 75,000 -。

会计专业英语期末考试练习卷new

1. The economic resources of a business are called: BA.Owner’s EquityB.AssetsC.Accounting equationD.Liabilities2. DTK Company has a $3500 accounts receivable from GRS Company. On January 20, GRS Company makes a partial payment of $2100 to DTK Company. The journal entry made on January 20 by DTK Company to record this transaction includes: DA.A debit to the cash receivable account of $2100.B.A credit to the accounts receivable account of $2100.C.A debit to the cash account of $1400.D.A debit to the accounts receivable account of $1400.3. In general terms, financial assets appear in the balance sheet at: AA.Face value.账面价值B.Current value.现值C.Market value.市场价值D.Estimated future sales value.4.Each of the following measures strengthens internal control over cash receipts except: DA.The use of a voucher system.B.Preparation of a daily listing of all checks received throughthe mail.C.The deposit of cash receipts intact in the bank on a daily basis.D.The use of cash registers.5. Which of the following items is the greatest in dollar amount DA.Beginning inventoryB.Cost of goods sold.C.Cost of goods available for saleD.Ending inventorydo companies prefer the LIFO inventory后进先出法 method during a period of rising prices BA.Higher reported incomeB.Lower income taxesC.Lower reported incomeD.Higher ending inventory7. Which of the following characteristics would prevent an item from being included in the classification of plant and equipment DA.IntangibleB.Unlimited lifeC.Being sold in its useful lifeD.Not capable of rendering benefits to the business in the future.8. Which account is not a contra-asset account BA.Depreciation ExpenseB.Accumulated DepletionC.Accumulated DepreciationD.Allowance for Doubtful Accounts9. What are the two factors that make ownership of an interest ina general partnership particularly risky AA.Mutual agency and unlimited personal liabilityB.Limited life and unlimited personal liability.C.Limited life and mutual agency.D.Double taxation and mutual agency10. Which of the following types of business owners do not take an active role in the daily management of the business DA.General partnersB.Limited liability partnersC.Sole proprietors 个体经营者D.Stockholders in a publicly owned corporation11. Analysts can use the footnotes to the financial statements to DA.Help their analysis of financial statementsB.Help their understanding of financial statementsC.Help their checking of financial statements.D.All of the above12. The current liabilities are $30 000, the long-term liabilities are $50 000, and the total assets are $240 000. What is the debt ratio CA.B.C.D.13. The horizontal analysis is used mainly to AA.Analyzing financial trendsB.Evaluating financial structureC.Assessing the pat performancesD.Measuring the term-paying ability14.Among the following ratios, which is used for long-term solvency analysis长期偿债能力分析 AA.Current ratio 流动比率B.Times-interest-earned ratioC.Operating cycleD.Book value per share15. A profit-making business that is a separate legal entity and in which ownership is divided into shares of stock is known as a DA.Sole proprietorship 个体独资公司B.Single proprietorshipC.Partnership 合伙公司D.Corporation 股份有限公司一、名词解释10分1 Journal entry:日记账Journal entry is a logging of transactions into accounting journal items. It can consist of several items, each of which is either a debit or a credit. The total of the debits must equal the total of the credits or the journal entry is said to be "unbalanced". Journal entries can record unique items or recurring items such as depreciation or bond amortization.2 Going concern:持续经营 The company will continue to operate in the near future, unless substantial evidence to the contrary exists.3 Matching principle:一致性原则4 Working capital:营运资金5 Revenue expenditure:收入费用二、会计业务共35分1. On December 1, ME Company borrowed $250 000 from a bank, and promise to repay that amount plus 12% interest per year at the end of 6 months.(1)Prepare the general journal entry to record obtaining theloan from the bank on December 1.(2)Prepare the adjusting journal entry to record accrual ofthe interest payable on the loan on December 31.(3)Prepare the presentation of the liability to the bank onME’s December balance sheet.Answer:(1)Debit: cash $250000Credit: current liabilities $250000(2)Debit: Accrual Expense $5000 不确定Credit: Interest Payable $50003 P392. The following information relating to the bank checking account is available for Music Hall at July 31:Balance per bank statement at$20 0000July 31Balance per depositor’s18 860 recordsOutstanding checks 2 000 Deposits in transit 800 Service charge by bank 60 Prepare a bank reconciliation银行对账工作 fro Music Hall at July 31.Answer:P423. Please prepare the related entries according to the following accounting events.1 Assume the Healy Furniture has credit sale of $1,200,000 in 2002. Of this amount, $200,000 remains uncollected at December 31. The credit manager estimates that $12,000 of these sales will be uncollectible. Please prepare the adjusting entry to record the estimated uncollectible.2 On March 1, 2003 the manager of finance of Healy Furniture authorizes a write-off of the $500 balance owed by Nick Company. Please make the entry to record the write-off.3 On July 1, Nick Company paid the $500 amount that had been written off on March 1.Answer:(1)Debit: Uncollectible Accounts Expense坏账损失 $12000Credit: Allowance for Doubtful Accounts坏账准备 $12000(2)Debit: Allowance for Doubtful Accounts $500Credit: Accounts Receivable $500(3)Debit: Accounts Receivable $500Credit: Allowance for Doubtful Accounts $500Debit: Cash $500Credit: Accounts Receivable $500四、英译汉40分1 Accounting principles are not like physical laws; they do not exist in nature, awaiting discovery man. Rather, they are developed by man, in light of what we consider to be the most important objectives of financial reporting. In many ways generally accepted accounting principles are similar to the rules established for an organized sport such as football or basketball.会计准则不像自然法则那样天生就存在等待人类去探索;会计准则需要人类在财务报告最重要目标的指引下去不断发展;很多时候我们认为会计准则就像一场组织运动的规则例如足球或篮球的规则2 Accounting have devised procedures whereby the flows of cash receipts and payments are spread over a period of time in a certain way to derive income, which is representative of the economic performance of the firm for the given period. The income concept as applied in the real world involves numerous decisions and judgments. 会计有特定的流程;在这个流程中现金收支在一定时间内通过一些特定方式流入流出并产生收入;收入代表一个公司在某一时间段的经济效益;收入这个概念在现实世界中包含着大量决策和评判;3Accounting is an information system of interpreting, recording, measuring, classifying, summarizing, reporting and describing business economic activities with monetary unit as its main criterion. The accounting information is primarily supplied to owners, managers and investors of every business, and other users to assist in the decision-making process. Therefore, accounting is also called “the language of business”.会计是一个翻译、记录、计量、认定、总结、报告和用现金作为主要标准来衡量企业经济活动的信息系统;会计信息主要提供给公司所有者、经营者、投资者和其他使用者以帮助他们决策;所以,会计又被称为“公司的语言”;4The use of accounting information is not limited to the business world. We live in an ear of accountability. An individual must account for his or her income and must file income tax returns. Often an individual must supply personal accounting information in order to qualify for a loan, to obtain a credit card, or to be eligible for a college scholarship.会计信息的运用并不限于商业界;会计在我们生活中无处不在;个人需要记录他的收入并整理他的纳税申报表;当一个需要申请贷款、信用卡或奖学金时,他通常需要提供个人会计信息来获得申请资格;。

会计英语实训考试题及答案

会计英语实训考试题及答案一、选择题(每题2分,共20分)1. What is the basic accounting equation?A. Assets = Liabilities + EquityB. Revenue – Expenses = Net IncomeC. Assets = Liabilities – EquityD. Liabilities = Assets – Equity答案:A2. Which of the following is not an accounting principle?A. ConsistencyB. MaterialityC. TimelinessD. Flexibility答案:D3. What is the purpose of adjusting entries?A. To correct past errorsB. To update the financial records for the current periodC. To prepare for the next accounting periodD. To estimate future revenues答案:B4. What is the term for the process of recording transactions in the general journal?A. JournalizingB. PostingC. ClosingD. Adjusting答案:A5. Which of the following is a type of liability?A. Common stockB. Retained earningsC. Accounts payableD. Dividends payable答案:C6. What is the accounting term for the cost of goods sold?A. COGSB. CGSC. COSD. SGA答案:A7. What is the purpose of a trial balance?A. To summarize the financial statementsB. To prove the accuracy of the accounting recordsC. To calculate the net incomeD. To determine the value of assets答案:B8. What is the accounting term for the amount of money a company owes to its suppliers?A. Accounts receivableB. Accounts payableC. Notes payableD. Accrued liabilities答案:B9. What is the term for the process of transferring journal entries to the ledger accounts?A. JournalizingB. PostingC. ClosingD. Adjusting答案:B10. Which of the following is not a financial statement?A. Balance sheetB. Income statementC. Cash flow statementD. Budget答案:D二、简答题(每题10分,共30分)1. Explain the difference between revenue and income.答案:Revenue refers to the inflow of cash or other assets from normal business operations. Income, on the other hand,is the net result of revenues and gains minus the expensesand losses. It is a measure of profitability over a period of time.2. What are the steps involved in the accounting cycle?答案:The accounting cycle involves the following steps: 1) Identifying and recording transactions, 2) Journalizing, 3) Posting to the ledger accounts, 4) Preparing a trial balance, 5) Adjusting entries, 6) Posting adjustments, 7) Preparing an adjusted trial balance, 8) Closing entries, and 9) Preparing financial statements.3. What is the purpose of depreciation in accounting?答案:Depreciation is the systematic allocation of thecost of a tangible asset over its useful life. It is used to match the expense of using the asset with the revenue it generates over time, in accordance with the matchingprinciple.三、案例分析题(每题25分,共50分)1. Assume you are the accountant for a company that has just purchased a piece of equipment for $50,000. The equipment is expected to have a useful life of 5 years and no residual value. Calculate the annual depreciation expense using the straight-line method.答案:The annual depreciation expense using the straight-line method is calculated as follows:Cost of the equipment = $50,000Useful life = 5 yearsAnnual depreciation expense = (Cost of the equipment –Residual value) / Useful lifeAnnual depreciation expense = ($50,000 – $0) / 5 = $10,0002. A company has the following transactions for the month of January:- Purchased inventory on credit for $20,000.- Sold inventory on credit for $30,000.- Paid cash for office supplies of $1,000.- Received cash from customers for $25,000.- Paid cash for salaries of $15,000.Prepare the journal entries for these transactions.答案:a) Purchase of inventory on credit:Dr. Inventory $20,000Cr. Accounts Payable $20,000b) Sale of inventory on credit:Dr. Accounts Receivable $30,000Cr. Sales Revenue $30,000c) Payment for office supplies。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Chapter 2 Accounting Concepts and Principles财务报表要素Asset 资产Liability 负债Equity 所有者权益、股本Revenue 收入Expense 费用Gain 利得Loss 损失For each item below, indicate to which category of elements of financial statements it belongs.每个项目下面,说明这类财务报表要素属于.(a) Retained earnings 留存收益equity(b) Sales 销售revenue(c) Additional paid-in capital 股本溢价equity(d) Inventory 存货asset(e) Depreciation 折旧费expense(f) Dividends 股息equity(g) Gain on sale of investment 出售投资收益gain(h)Interest payable 应付利息liability(i)Loss on sale of equipment 销售设备的亏损loss(j) Issuance of common stock 发行普通股equityChapter 3 Financial StatementsExercise 1. Presented on the next page are the captions of Faulk Company’s balance sheet.在下一页的标题的福克公司的资产负债表。

(a) Current assets. (f) Current liabilities.(b) Investments. (g) Non-current liabilities.(c) Property, plant, and equipment. (h) Capital stock.(d) Intangible assets. (i) Additional paid-in capital.(e) Other assets. (j) Retained earnings.(a)流动资产(b)投资(c固定资产(d)无形资产(e)其他资产(f)流动负债(g)非流动负债。

(h)股本(i)股本溢价(j)留存收益。