会计专业英语L11

会计专业英语LESSON 1(立信会计出版社)

Sentences

• (To meet the needs of the external users ),a framework of accounting standards, principles and procedures (known as ‘generally accepted accounting principles (GAAP)’ )have been developed to insure the relevance and reliability of the accounting information contained in these external financial reports. • reliability n.可靠性 • Reliable a.可靠的 • I’m a reliable person.

Six elements of accounting

资产 asset 负债 liability 所有者权益 Owners’ equity/owners’ interest 收入 revenue/income 费用 expense 利润 profit

Interest n.兴趣、权益、利息 vt.对……感兴趣 I’m interested in sth. Interest rate 利率 Cost n.成本 vt.花费 It costs me 2 days to finish this book. Expense n.费用 vt.花费 It expenses me………………

Sentences

• Banks and other creditors must consider the financial strength of a business before permitting it to borrow funds . • Also, many laws require that extensive financial information be reported to the various levels of government.

会计专业英语PPT

Management accounting:

use both historical data in assisting management daily operations and in planning future operations.

concepts one more time. • Combine both freely but English is more

important.

二 Improve English by ….

– Read textbook in class and after class – Remember new words – Answer questions in exercise is important – Overlook some parts while emphasizing some

• Financial accounting: provides external reports o outsiders, financial information.

2 Reporting management information to internal users

Internal users are senior management-level personnel.

• What do you think?

二 Functions

1 Reporting financial information to outside interested users

• Outside users are:investors,banks and other creditors,government agencies,general publics

会计专业基础英语

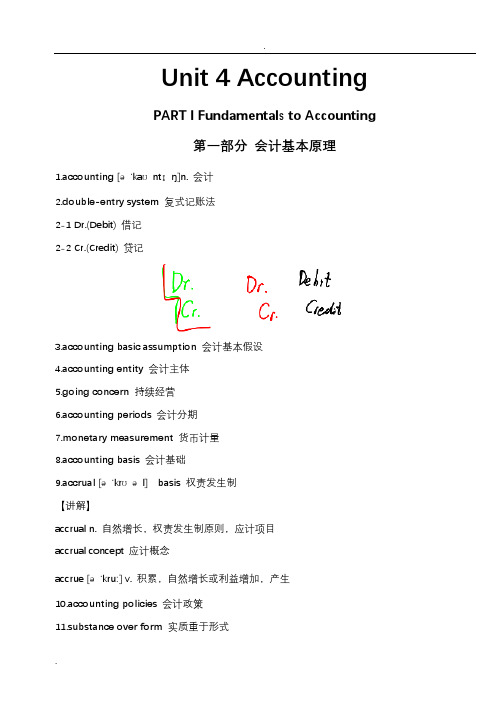

Unit 4 AccountingPART I Fundamentals to Accounting第一部分会计基本原理1.accounting [ə'kaʊntɪŋ]n. 会计2.double-entry system复式记账法2-1 Dr.(Debit) 借记2-2 Cr.(Credit) 贷记3.accounting basic assumption会计基本假设4.accounting entity会计主体5.going concern持续经营6.accounting periods会计分期7.monetary measurement货币计量8.accounting basis会计基础9.accrual [ə'krʊəl] basis权责发生制【讲解】accrual n. 自然增长,权责发生制原则,应计项目accrual concept 应计概念accrue [ə'kruː] v. 积累,自然增长或利益增加,产生10.accounting policies会计政策11.substance over form实质重于形式12.accounting elements会计要素13.recognition [rekəg'nɪʃ(ə)n] n. 确认13-1 initial recognition [rekəg'nɪʃ(ə)n] 初始确认【讲解】recognize ['rɛkəg'naɪz] v. 确认14.measurement ['meʒəm(ə)nt] n. 计量14-1 subsequent ['sʌbsɪkw(ə)nt] measurement 后续计量15.asset ['æset] n. 资产16.liability [laɪə'bɪlɪtɪ] n. 负债17.owners’ equity所有者权益18.shareholder’s equity股东权益19.expense [ɪk'spens; ek-] n. 费用20.profit ['prɒfɪt] n. 利润21.residual [rɪ'zɪdjʊəl] equity剩余权益22.residual claim剩余索取权23.capital ['kæpɪt(ə)l] n. 资本24.gains [ɡeinz] n. 利得25.loss [lɒs] n. 损失26.Retained earnings留存收益27.Share premium股本溢价28.historical cost历史成本【讲解】historical [hɪ'stɒrɪk(ə)l] adj. 历史的,历史上的historic [hɪ'stɒrɪk] adj. 有历史意义的,历史上著名的28-1 replacement [rɪ'pleɪsm(ə)nt] cost 重置成本29.Balance Sheet/Statement of Financial Position资产负债表29-1 Income Statement 利润表29-2 Cash Flow Statement 现金流量表29-3 Statement of changes in owners’equity (or shareholders’equity) 所有者权益(股东权益)变动表29-4 notes [nəʊts] n. 附注PART II Financial Assets*第二部分金融资产*30.financial assets金融资产e.g. A financial instrument is any contract that gives rise to a financial asset of one enterprise and a financial liability or equity instrument of another enterprise. 【讲解】give rise to 引起,导致31.cash on hand 库存现金32.bank deposits [dɪ'pɒzɪt] 银行存款33.A/R, account receivable应收账款34.notes receivable应收票据35.others receivable其他应收款项36.equity investment股权投资37.bond investment债券投资38.derivative financial instrument衍生金融工具39.active market活跃市场40.quotation [kwə(ʊ)'teɪʃ(ə)n]n. 报价41.financial assets at fair value through profit or loss以公允价值计量且其变动计入当期损益的金融资产41-1 those designated as at fair value through profit or loss 指定为以公允价值计量且其变动计入当期损益的金融资产41-2 financial assets held for trading 交易性金融资产42.financial liability金融负债43.transaction costs交易费用43-1 incremental external cost 新增的外部费用【讲解】incremental [ɪnkrə'məntl] adj. 增量的,增值的44.cash dividend declared but not distributed 已宣告但尚未发放的现金股利投资收益45.profit and loss arising from fair value changes公允价值变动损益46.Held-to-maturity investments持有至到期投资47.amortized cost摊余成本【讲解】amortized [ə'mɔ:taizd]adj. 分期偿还的,已摊销的48.effective interest rate实际利率49.loan [ləʊn] n. 贷款50.receivables [ri'si:vəblz] n. 应收账款51.available-for-sale financial assets可供出售金融资产52.impairment of financial assets金融资产减值52-1 impairment loss of financial assets 金融资产减值损失53.transfer of financial assets金融资产转移53-1 transfer of the financial asset in its entirety 金融资产整体转移53-2 transfer of a part of the financial asset 金融资产部分转移54.derecognition [diː'rekəg'nɪʃən] n. 终止确认,撤销承认54-1 derecognize [diː'rekəgnaɪz] v. 撤销承认e.g. An enterprise shall derecognize a financial liability (or part of it) only when the underlying present obligation (or part of it) is discharged/cancelled.【译】金融负债的现时义务全部或部分已经解除的,才能终止确认该金融负债或其一部分。

会计学专业英语第一章

D

Unit 4 Information Users

Words and Expressions

Unit 1 Accounting and Accounting Profession

• 1.accounting 会计(核算); 会计学 • 2.accountant 会计师;会计人 员

• 6.operational audits 经营审计 • pliance audits 合规审计 • 8.income tax returns 所得税申 报单 • 9.nonprofit organizations 非盈 利组织 • ptroller 会计主任

• 3.bookkeeping 簿记;簿记学

• 4.chartered accountants 特许会 计师 • 5.auditing 审计;审计学

• 11.professional ethics 职业道德

• 12.proprietorship 独资企业 • 13.partnership 合伙企业 • 14.double-entry accounting

of these accountants work on a salary basis.

Unit 1 Accounting and Accounting Profession

Private accounting

Private

accountants, also called executive or administrative accountants,

Accountingபைடு நூலகம்is

often known as one of the most useful tools of business because all

会计专业英语(五篇范例)

会计专业英语(五篇范例)第一篇:会计专业英语Accounting termsAccounting entity会计主体Accounting procedure会计核算Accounting process会计程序/过程Accounting practice会计核算Accounting element会计要素Accounting principle会计原则Accounting standard会计准则Accounting assumption会计假设Accounting equation会计等式Business=Enterpris企业Firm=Company公司Organization组织Performance业绩 Financial position 财务状况Operating result 业绩、经营成果Economic activity经济活动Corporation有限责任公司(股份公司)Assets资产Liability负债Owner’s eq uity 所有者权益 Capital 资本Revenue收入Income收益Expense费用 Cost费用、成本Profit 利润Net income净收益Loss损失Users of accounting informationManager管理者Shareholder股东Owner所有者Accountant会计师Casher出纳Bookkeeper记账员Investor投资者Creditor债权人Supplier供货商Government政府Public公众Accounting EntityOrganization:①Not-for-profit organization②business organization1.business organization①Sole Proprietorship Enterprises独资经营企业②General Partnership Enterprises普通合伙企业③Limited Liability Partnership Enterprises有限责任合伙企业④Corporation股份公司2.Corporation①Owned by one person②Simple to establish③Owner controlled④Tax advantages3.General Partnership①Owned by more than one person②Simple to establish③Shared control ④Tax advantages4.Limited Liability Partnership①Only for certain occupations ②Limited liability for p artnership debts and obligations③Also a limitation on participation in management5.Corporation①Organized as a separate legal entity and owned by stockholders②Easy to transfer ownership③Easier to raise funds④No personal liabilityAccounting PrinciplesConcept概念Standard准则Convention惯例Assumption假设Rule规则Accounting AssumptionsAccounting entity assumption会计主体Going concern assumption持续经营 Money measurement assumption货币计量Accounting period assumption会计期间The qualitative characteristics of financial informationRelevant相关性Reliable可靠性Comparable可比性Understandable可理解性Timeliness及时性Prudence谨慎性Materiality重要性Consistency一贯性Substance over legal form实质重于形式Accruals basis权责发生制Principles about Measurement and PresentationThe Accrual Basis Principle权责发生制原则The Matching Principle配比原则The Historical Cost Principle历史成本原则The Distinction Between Revenue Expenditures and Capital Expenditures Principle划分收益性支出和资本性支出原则Accounting termsDouble-entryBookkeepingDouble-entry systemAccount title会计科目Code /chart of account title会计科目表Accounting entry 会计主体Debit 借Credit 贷Increase增加Decrease减少Sum总额Balance余额a debit balance 借方余额a credit balance贷方余额Trial balance试算平衡Total amount of debits/credits借/贷方金额合计Accounting cycle会计循环Fiscal year会计年度System accountingAccount账户Types of accounts账户的种类Accounting record 会计档案Typesof accountsAccount book账本Ledger分类账Journal日记账General ledger总分类账Subsidiary Ledger明细分类账General Journal总日记账Special Journal特种日记账Accounting ElementsAssets资产Liabilities 负债Profit利润Owners' Equity所有者权益Expenses费用Revenue收入liabilitiesCurrent liabilities流动负债Non-current liabilities非流动负债Short-Term Note Payable短期应付票据Long-T erm Note Payable长期应付票据Accrued liabilities应记负债Wages Payable /Salaries Payable 应付职工薪酬Taxes Payable 应交税费Dividends Payable应付股利long-term liabilities长期负债Contingent liabilities或有负债Accrued expenses预提费用Current Ratio流动比率Long-term loans payable长期借款Long-term accounts payable长期应付款Bonds payable应付债券Capitallease融资性租赁Operating lease经营性租赁Notes payable应付票据Accounts payable应付账款Unearned Fees=Unearned Revenue预收账款Current maturities of long-term debt将于一年内到期的长期负债Owners equityDividend股利Corporation公司Stock股票/存货Board of directors董事会Capital stock股本Preferred stock优先股Owner’s Capital所有者权益Common Stock普通股Share股份Capital reserve资本公积Statutory Surplus reserve盈余公积Additional paid-in Capital资本溢价/资本公积Paid-in capital 投入资本/实收资本Shareholder=stockholder=director股东Retained earnings=retained capital留存收益Original voucher/source voucher原始凭证Recording voucher 记账凭证Sales invoice销售发票Receipt收据Make entries做会计分录Adjusting entries调整分录Posting过账Closing entries结账The Income Statement利润表The Balance Sheet资产负债表The Cash Flow Statement现金流量表Prepare financial statements财务报表A Statement of Changes in Equity所有者权益变动表Current AssetsCurrent assets流动资产Quick assets速冻资产Cash现金Short-term investment短期金融投资Cash equivalent现金等价物Cash receipt现金收入Cash disbursement现金支出Petty cash fund备用金Bank reconciliation statement银行存款余额调节表Dividends Receivable 应付股利Inventory存货Gross method总价法Net method净价法Bad debts坏账Accounts receivables应收账款Notes receivables应收票据Discount trade discount商业折扣Cash discount /sales discount现金折扣Direct write-off method直接冲销法allowance method备抵法Non-trade receivables非营业应收款Interest receivables应收利息Dividends receivables应收股利Other receivable其它应收款InventoriesRaw material原材料Finished goods成品Merchandise商品Goods in process在成品Partially finished goods /Semi-finished goods半成品Low-value and perishable articles低值易耗品Low-valued and easily-damaged implements价格低廉的易耗用品Perpetual inventory system永续盘存制Periodic inventory system定期盘存制Raw material to be used in the production用于生产的原材料All kinds of materials,fuels,containers各种材料,燃料,包装物Non-Current AssetsBond债券Land土地Depreciation折扣Bonds investment债券投资Non-Current assets非流动资Intangible assets无形资产Shares investments股票投资Revenue expenditure营业支出Capital expenditure资产支出Long-term investment长期投资Plant asset=Fixed assets固定资产Bonds investmentMarket value市场价Premium溢价Discount折扣Salvage value残值Amortized cost摊销成本Useful life使用年限Cost-----historical cost历史成本Accumulated Depreciation加速折旧法Types of Bonds PayableConvertible bonds可兑换债券Callable bonds可提前(可通知)偿还的债券Secured bonds担保债券Unsecured bonds无担保债券Term bonds定期债券Serial bonds分期还本债券Registered bonds记名债券Bearer bonds不记名债券Present value现值Face value/principal value面值Maturity value到期值Contractual interest rate合同利率Market interest rate市场利率Effective interest rate实际利率Common Stock dividendsCash dividends现金股利Stock dividends股票股利Property dividends财产股利Fixed dividends股利事先确定Limited voting rights有限的投票权Dividends set down in advance先于普通股发放Revenue, Expenses and ProfitRevenue收入sales revenue销售收入cost费用/成本Expense 费用Profit利润gross profit利润总额net profit净利润net income 净收益Prime operating revenue主营业务收入Other operatingrevenue其它业务收入services revenue服务/劳务收入Cost of goods sold销货成本Periodic expense期间费用Operating expense 营业费用sellingexpense销售费用Financial expense 财务费用investment profit投资收益Non-operating income营业外收入Non-operating expense营业外支出Fees Earned服务费收入Rent Earned租金收入Interest Revenue利息收入Office wages expense管理人员工资Rent expense租金费用Telephone expense电话费Advertising expense广告费Administrative expense管理费用Interest expense利息费用(财务费用)Operating profit营业利润Net investment profit投资净收益 Net non-operating income营业外收支额Income StatementIncome statement利润表Profitability盈利能力Gross Profit on Sales销售毛利Operating result业务成果/运营成果Sales returns and allowances销售折扣/销售折让Operating Income/profit营业收入/营业利润Earnings Before Interest and Tax息税前收益Operating profitOperating Revenue-Operating Cost-Operating Taxes and Surcharges-Selling Expenses-Administrative Expense-FinancingExpense-Impairment loss+Profit or loss of assets at fair value+Net Investment Profit=Operating profitNet investment profitgains from external investments-investment losses incurred-any provision for impairment losses on investments=net investment profitGross ProfitOperating profit+Non-operating Income-Non-operating Expenses=Gross ProfitNetProfitGross Profit-Income Tax=Net ProfitThe basis of Balance Sheettotal revenues – total expenses = net incometotal expenses – total revenues = net lossMultiple-step FormSales-Sales Returns and Allowances=Net Sales-Cost of Goods Sold=Gross Profit on Sales-Operating Expenses=Operating Income +Other Revenues and Gains-Other Expenses and Losses=Net IncomeAccounting EquationAssets = Liabilities + Owners' EquityBasis of double-entry bookkeepingBasis of balance sheetaccounting equation always stays in balanceAssets = Liabilities + Owners' Equitybeg +(Revenue −Expenses)Assets + Expenses = Liabilities + Owners' Equitybeg + Revenue第二篇:会计专业英语会计是什么会计是什么?多年来,流行的说法,会计是会计,成绩和会计。

会计学专业英语课件

Accounting: Information for Decision Making

• The primary objective of accounting

– to provide information that is useful for making decisions.

Users of Accounting Information

CHAPTER 1

ACCOUNTING: THE BASIS FOR DECISIONS

Learning Objectives

• Explain the definition of accounting; • Understand the basic function of accounting; • Ascertain the users of accounting information

consulting) services

Private Accounting

• Management accountants 管理会计师

– The Institute of Management Accountants (美国管理会计师协会 ,简称IMA )

– Certified Management Accountant (美国注册 管理会计师,简称CMA)

• Many professional organization have codes of ethics or professional conduct that direct the activities of their members.

– AICPA’s Code of Professional Conduct – Chinese Certified Public Accountants Code of Professional

会计英语(中英对照)

Unit OneAccounting Profession第一单元会计职业INTRODUCTION OF ACCOUNTING. Accounting is a process of recorded, classifying, summarizing, and interpreting of those business activities that can be in expressed in monetary terms. A person who specializes in this field is known as an accountant.会计简介会计是一个以货币形式对经济活动进行记录、分类、汇总以及解释的过程。

专门从事这方面工作的人员叫做会计师。

Accounting frequently offers the qualified person an opportunity to move ahead quickly in today’s business world. Indeed, many of the heads of large corporations throughout the world have advanced to their position from the accounting department. Accounting is a basic and vital element in every modern business. It records the past growth or decline of the business. Careful analysis of these results and trends may suggest the ways in which the business may grow in future. Expan-sion or reorganization should not be planned without proper analysis of the accounting informa-tion; and new products and the campaign to advertise and sell them should not be launched with-out the help of accounting expertise.会计这一职业在当今经济社会中给有能力的人提供了升迁的机会。

财务英语基础词汇表+全套财务英语PPT学习

1 资产assets11~ 12 流动资产current assets111 现金及约当现金cash and cash equivalents1111 库存现金cash on hand1112 零用金/周转金petty cash/revolving funds1113 银行存款cash in banks1116 在途现金cash in transit1117 约当现金cash equivalents1118 其它现金及约当现金other cash and cash equivalents112 短期投资short-term investment1121 短期投资-股票short-term investments - stock1122 短期投资-短期票券short-term investments - short-term notes and bills1123 短期投资-政府债券short-term investments - government bonds 1124 短期投资-受益凭证short-term investments - beneficiary certificates1125 短期投资-公司债short-term investments - corporate bonds 1128 短期投资-其它short-term investments - other1129 备抵短期投资跌价损失allowance for reduction of short-term investment to market113 应收票据notes receivable1131 应收票据notes receivable1132 应收票据贴现discounted notes receivable1137 应收票据-关系人notes receivable - related parties1138 其它应收票据other notes receivable1139 备抵呆帐-应收票据allowance for uncollectible accounts- notes receivable114 应收帐款accounts receivable1141 应收帐款accounts receivable1142 应收分期帐款installment accounts receivable1147 应收帐款-关系人accounts receivable - related parties1149 备抵呆帐-应收帐款allowance for uncollectible accounts - accounts receivable118 其它应收款other receivables1181 应收出售远汇款forward exchange contract receivable1182 应收远汇款-外币forward exchange contract receivable - foreign currencies1183 买卖远汇折价discount on forward ex-change contract1184 应收收益earned revenue receivable1185 应收退税款income tax refund receivable1187 其它应收款- 关系人other receivables - related parties1188 其它应收款- 其它other receivables - other1189 备抵呆帐- 其它应收款allowance for uncollectible accounts - other receivables121~122 存货inventories1211 商品存货merchandise inventory1212 寄销商品consigned goods1213 在途商品goods in transit1219 备抵存货跌价损失allowance for reduction of inventory to market1221 制成品finished goods1222 寄销制成品consigned finished goods1223 副产品by-products1224 在制品work in process1225 委外加工work in process - outsourced1226 原料raw materials1227 物料supplies1228 在途原物料materials and supplies in transit1229 备抵存货跌价损失allowance for reduction of inventory to market125 预付费用prepaid expenses1251 预付薪资prepaid payroll1252 预付租金prepaid rents1253 预付保险费prepaid insurance1254 用品盘存office supplies1255 预付所得税prepaid income tax1258 其它预付费用other prepaid expenses126 预付款项prepayments1261 预付货款prepayment for purchases1268 其它预付款项other prepayments128~129 其它流动资产other current assets1281 进项税额V AT paid ( or input tax)1282 留抵税额excess V AT paid (or overpaid V AT)1283 暂付款temporary payments1284 代付款payment on behalf of others1285 员工借支advances to employees1286 存出保证金refundable deposits1287 受限制存款certificate of deposit-restricted1291 递延所得税资产deferred income tax assets1292 递延兑换损失deferred foreign exchange losses 1293 业主(股东)往来owners(stockholders) current account 1294 同业往来current account with others1298 其它流动资产-其它other current assets - other13 基金及长期投资funds and long-term investments131 基金funds1311 偿债基金redemption fund (or sinking fund)1312 改良及扩充基金fund for improvement and expansion 1313 意外损失准备基金contingency fund1314 退休基金pension fund1318 其它基金other funds132 长期投资long-term investments1321 长期股权投资long-term equity investments1322 长期债券投资long-term bond investments1323 长期不动产投资long-term real estate in-vestments1324 人寿保险现金解约价值cash surrender value of life insurance 1328 其它长期投资other long-term investments1329 备抵长期投资跌价损失allowance for excess of cost over market value of long-term investments14~ 15 固定资产property , plant, and equipment141 土地land1411 土地land1418 土地-重估增值land - revaluation increments142 土地改良物land improvements1421 土地改良物land improvements1428 土地改良物-重估增值land improvements - revaluation increments1429 累积折旧-土地改良物accumulated depreciation - land improvements143 房屋及建物buildings1431 房屋及建物buildings1438 房屋及建物-重估增值buildings -revaluation increments1439 累积折旧-房屋及建物accumulated depreciation - buildings 144~146 机(器)具及设备machinery and equipment1441 机(器)具machinery1448 机(器)具-重估增值machinery - revaluation increments1449 累积折旧-机(器)具accumulated depreciation - machinery151 租赁资产leased assets1511 租赁资产leased assets1519 累积折旧-租赁资产accumulated depreciation - leased assets 152 租赁权益改良leasehold improvements1521 租赁权益改良leasehold improvements1529 累积折旧- 租赁权益改良accumulated depreciation - leasehold improvements156 未完工程及预付购置设备款construction in progress and prepayments for equipment1561 未完工程construction in progress1562 预付购置设备款prepayment for equipment158 杂项固定资产miscellaneous property, plant, and equipment1581 杂项固定资产miscellaneous property, plant, and equipment 1588 杂项固定资产-重估增值miscellaneous property, plant, and equipment - revaluation increments1589 累积折旧- 杂项固定资产accumulated depreciation -miscellaneous property, plant, and equipment16 递耗资产depletable assets161 递耗资产depletable assets1611 天然资源natural resources1618 天然资源-重估增值natural resources -revaluation increments 1619 累积折耗-天然资源accumulated depletion - natural resources 17 无形资产intangible assets171 商标权trademarks1711 商标权trademarks172 专利权patents1721 专利权patents173 特许权franchise1731 特许权franchise174 著作权copyright1741 著作权copyright175 计算机软件computer software1751 计算机软件computer software cost176 商誉goodwill1761 商誉goodwill177 开办费organization costs1771 开办费organization costs178 其它无形资产other intangibles1781 递延退休金成本deferred pension costs1782 租赁权益改良leasehold improvements1788 其它无形资产-其它other intangible assets - other18 其它资产other assets181 递延资产deferred assets1811 债券发行成本deferred bond issuance costs1812 长期预付租金long-term prepaid rent1813 长期预付保险费long-term prepaid insurance1814 递延所得税资产deferred income tax assets1815 预付退休金prepaid pension cost1818 其它递延资产other deferred assets182 闲置资产idle assets1821 闲置资产idle assets184 长期应收票据及款项与催收帐款long-term notes , accounts and overdue receivables1841 长期应收票据long-term notes receivable1842 长期应收帐款long-term accounts receivable1843 催收帐款overdue receivables1847 长期应收票据及款项与催收帐款-关系人long-term notes, accounts and overdue receivables- related parties1848 其它长期应收款项other long-term receivables1849 备抵呆帐-长期应收票据及款项与催收帐款allowance for uncollectible accounts - long-term notes, accounts and overdue receivables185 出租资产assets leased to others1851 出租资产assets leased to others1858 出租资产-重估增值assets leased to others - incremental value from revaluation1859 累积折旧-出租资产accumulated depreciation - assets leased to others186 存出保证金refundable deposit1861 存出保证金refundable deposits188 杂项资产miscellaneous assets1881 受限制存款certificate of deposit - restricted1888 杂项资产-其它miscellaneous assets - other2 负债liabilities21~ 22 流动负债current liabilities211 短期借款short-term borrowings(debt)2111 银行透支bank overdraft2112 银行借款bank loan2114 短期借款-业主short-term borrowings - owners2115 短期借款-员工short-term borrowings - employees2117 短期借款-关系人short-term borrowings- related parties2118 短期借款-其它short-term borrowings - other212 应付短期票券short-term notes and bills payable2121 应付商业本票commercial paper payable2122 银行承兑汇票bank acceptance2128 其它应付短期票券other short-term notes and bills payable 2129 应付短期票券折价discount on short-term notes and bills payable 213 应付票据notes payable2131 应付票据notes payable2137 应付票据-关系人notes payable - related parties2138 其它应付票据other notes payable214 应付帐款accounts pay able2141 应付帐款accounts payable2147 应付帐款-关系人accounts payable - related parties216 应付所得税income taxes payable2161 应付所得税income tax payable217 应付费用accrued expenses2171 应付薪工accrued payroll2172 应付租金accrued rent payable2173 应付利息accrued interest payable2174 应付营业税accrued V AT payable2175 应付税捐-其它accrued taxes payable- other2178 其它应付费用other accrued expenses payable218~219 其它应付款other payables2181 应付购入远汇款forward exchange contract payable2182 应付远汇款-外币forward exchange contract payable - foreign currencies2183 买卖远汇溢价premium on forward exchange contract2184 应付土地房屋款payables on land and building purchased2185 应付设备款Payables on equipment2187 其它应付款-关系人other payables - related parties2191 应付股利dividend payable2192 应付红利bonus payable2193 应付董监事酬劳compensation payable to directors and supervisors2198 其它应付款-其它other payables - other226 预收款项advance receipts2261 预收货款sales revenue received in advance2262 预收收入revenue received in advance2268 其它预收款other advance receipts227 一年或一营业周期内到期长期负债long-term liabilities -current portion2271 一年或一营业周期内到期公司债corporate bonds payable - current portion2272 一年或一营业周期内到期长期借款long-term loans payable - current portion2273 一年或一营业周期内到期长期应付票据及款项long-term notes and accounts payable due within one year or one operating cycle2277 一年或一营业周期内到期长期应付票据及款项-关系人long-term notes and accounts payables to related parties - current portion 2278 其它一年或一营业周期内到期长期负债other long-term lia- bilities - current portion228~229 其它流动负债other current liabilities2281 销项税额V AT received(or output tax)2283 暂收款temporary receipts2284 代收款receipts under custody2285 估计售后服务/保固负债estimated warranty liabilities2291 递延所得税负债deferred income tax liabilities2292 递延兑换利益deferred foreign exchange gain2293 业主(股东)往来owners current account2294 同业往来current account with others2298 其它流动负债-其它other current liabilities - others23 长期负债long-term liabilities231 应付公司债corporate bonds payable2311 应付公司债corporate bonds payable2319 应付公司债溢(折)价premium(discount) on corporate bonds payable232 长期借款long-term loans payable2321 长期银行借款long-term loans payable - bank2324 长期借款-业主long-term loans payable - owners2325 长期借款-员工long-term loans payable - employees2327 长期借款-关系人long-term loans payable - related parties 2328 长期借款-其它long-term loans payable - other233 长期应付票据及款项long-term notes and accounts payable2331 长期应付票据long-term notes payable2332 长期应付帐款long-term accounts pay-able2333 长期应付租赁负债long-term capital lease liabilities2337 长期应付票据及款项-关系人Long-term notes and accounts payable - related parties2338 其它长期应付款项other long-term payables234 估计应付土地增值税accrued liabilities for land value increment tax2341 估计应付土地增值税estimated accrued land value incremental tax pay-able235 应计退休金负债accrued pension liabilities2351 应计退休金负债accrued pension liabilities238 其它长期负债other long-term liabilities2388 其它长期负债-其它other long-term liabilities - other 28 其它负债other liabilities281 递延负债deferred liabilities2811 递延收入deferred revenue2814 递延所得税负债deferred income tax liabilities 2818 其它递延负债other deferred liabilities286 存入保证金deposits received2861 存入保证金guarantee deposit received288 杂项负债miscellaneous liabilities2888 杂项负债-其它miscellaneous liabilities - other3 所有者权益(股东权益)owners equity31 资本capital311 资本(或股本)capital3111 普通股股本capital - common stock3112 特别股股本capital - preferred stock3113 预收股本capital collected in advance3114 待分配股票股利stock dividends to be distributed 3115 资本capital32 资本公积additional paid-in capital321 股票溢价paid-in capital in excess of par3211 普通股股票溢价paid-in capital in excess of par- common stock 3212 特别股股票溢价paid-in capital in excess of par- preferred stock 323 资产重估增值准备capital surplus from assets revaluation3231 资产重估增值准备capital surplus from assets revaluation324 处分资产溢价公积capital surplus from gain on disposal of assets 3241 处分资产溢价公积capital surplus from gain on disposal of assets 325 合并公积capital surplus from business combination3251 合并公积capital surplus from business combination326 受赠公积donated surplus3261 受赠公积donated surplus328 其它资本公积other additional paid-in capital3281 权益法长期股权投资资本公积additional paid-in capital from investee under equity method3282 资本公积- 库藏股票交易additional paid-in capital - treasury stock trans-actions33 保留盈余(或累积亏损) retained earnings (accumulated deficit)331 法定盈余公积legal reserve3311 法定盈余公积legal reserve332 特别盈余公积special reserve3321 意外损失准备contingency reserve3322 改良扩充准备improvement and expansion reserve3323 偿债准备special reserve for redemption of liabilities3328 其它特别盈余公积other special reserve335 未分配盈余(或累积亏损) retained earnings-unappropriated (or accumulated deficit)3351 累积盈亏accumulated profit or loss3352 前期损益调整prior period adjustments3353 本期损益net income or loss for current period34 权益调整equity adjustments341 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments3411 长期股权投资未实现跌价损失unrealized loss on market value decline of long-term equity investments342 累积换算调整数cumulative translation adjustment3421 累积换算调整数cumulative translation adjustments343 未认列为退休金成本之净损失net loss not recognized as pension cost3431 未认列为退休金成本之净损失net loss not recognized as pension costs35 库藏股treasury stock351 库藏股treasury stock3511 库藏股treasury stock36 少数股权minority interest361 少数股权minority interest3611 少数股权minority interest4 营业收入operating revenue41 销货收入sales revenue411 销货收入sales revenue4111 销货收入sales revenue4112 分期付款销货收入installment sales revenue 417 销货退回sales return4171 销货退回sales return419 销货折让sales allowances4191 销货折让sales discounts and allowances46 劳务收入service revenue461 劳务收入service revenue4611 劳务收入service revenue47 业务收入agency revenue471 业务收入agency revenue4711 业务收入agency revenue48 其它营业收入other operating revenue488 其它营业收入-其它other operating revenue4888 其它营业收入-其它other operating revenue - other5营业成本operating costs51 销货成本cost of goods sold511 销货成本cost of goods sold5111 销货成本cost of goods sold5112 分期付款销货成本installment cost of goods sold 512 进货purchases5121 进货purchases5122 进货费用purchase expenses5123 进货退出purchase returns5124 进货折让charges on purchased merchandise513 进料materials purchased5131 进料material purchased5132 进料费用charges on purchased material5133 进料退出material purchase returns5134 进料折让material purchase allowances514 直接人工direct labor5141 直接人工direct labor515~518 制造费用manufacturing overhead5151 间接人工indirect labor5152 租金支出rent expense, rent5153 文具用品office supplies (expense)5154 旅费travelling expense, travel5155 运费shipping expenses, freight5156 邮电费postage (expenses)5157 修缮费repair(s) and maintenance (expense ) 5158 包装费packing expenses5161 水电瓦斯费utilities (expense)5162 保险费insurance (expense)5163 加工费manufacturing overhead - outsourced 5166 税捐taxes5168 折旧depreciation expense5169 各项耗竭及摊提various amortization 5172 伙食费meal (expenses)5173 职工福利employee benefits/welfare5176 训练费training (expense)5177 间接材料indirect materials5188 其它制造费用other manufacturing expenses56 劳务成本制ervice costs561 劳务成本service costs5611 劳务成本service costs57 业务成本gency costs571 业务成本agency costs5711 业务成本agency costs58 其它营业成本other operating costs588 其它营业成本-其它other operating costs-other 5888 其它营业成本-其它other operating costs - other6 营业费用operating expenses61 推销费用selling expenses615~618 推销费用selling expenses6151 薪资支出payroll expense6152 租金支出rent expense, rent6153 文具用品office supplies (expense)6154 旅费travelling expense, travel6155 运费shipping expenses, freight6156 邮电费postage (expenses)6157 修缮费repair(s) and maintenance (expense) 6159 广告费advertisement expense, advertisement 6161 水电瓦斯费utilities (expense)6162 保险费insurance (expense)6164 交际费entertainment (expense)6165 捐赠donation (expense)6166 税捐taxes6167 呆帐损失loss on uncollectible accounts6168 折旧depreciation expense6169 各项耗竭及摊提various amortization6172 伙食费meal (expenses)6173 职工福利employee benefits/welfare6175 佣金支出commission (expense)6176 训练费training (expense)6188 其它推销费用other selling expenses62 管理及总务费用general & administrative expenses625~628 管理及总务费用general & administrative expenses 6251 薪资支出payroll expense6252 租金支出rent expense, rent6253 文具用品office supplies6254 旅费travelling expense, travel6255 运费shipping expenses,freight6256 邮电费postage (expenses)6257 修缮费repair(s) and maintenance (expense)6259 广告费advertisement expense, advertisement6261 水电瓦斯费utilities (expense)6264 交际费entertainment (expense)6265 捐赠donation (expense)6266 税捐taxes6267 呆帐损失loss on uncollectible accounts6268 折旧depreciation expense a6269 各项耗竭及摊提various amortization6271 外销损失loss on export sales6272 伙食费meal (expenses)6273 职工福利employee benefits/welfare6274 研究发展费用research and development expense6275 佣金支出commission (expense)6276 训练费training (expense)6278 劳务费professional service fees6288 其它管理及总务费用other general and administrative expenses 63 研究发展费用research and development expenses635~638 研究发展费用research and development expenses6351 薪资支出payroll expense6352 租金支出rent expense, rent6353 文具用品office supplies6354 旅费travelling expense, travel6355 运费shipping expenses, freight6357 修缮费repair(s) and maintenance (expense)6361 水电瓦斯费utilities (expense)6362 保险费insurance (expense)6364 交际费entertainment (expense)6366 税捐taxes6368 折旧depreciation expense6369 各项耗竭及摊提various amortization6372 伙食费meal (expenses)6373 职工福利employee benefits/welfare6376 训练费training (expense)6378 其它研究发展费用other research and development expenses7 营业外收入及费用non-operating revenue and expenses, other income(expense)71~74 营业外收入non-operating revenue711 利息收入interest revenue7111 利息收入interest revenue/income712 投资收益investment income7121 权益法认列之投资收益investment income recognized under equity method7122 股利收入dividends income7123 短期投资市价回升利益gain on market price recovery of short-term investment713 兑换利益foreign exchange gain7131 兑换利益foreign exchange gain714 处分投资收益gain on disposal of investments7141 处分投资收益gain on disposal of investments715 处分资产溢价收入gain on disposal of assets7151 处分资产溢价收入gain on disposal of assets748 其它营业外收入other non-operating revenue7481 捐赠收入donation income7482 租金收入rent revenue/income7483 佣金收入commission revenue/income7484 出售下脚及废料收入revenue from sale of scraps7485 存货盘盈gain on physical inventory7486 存货跌价回升利益gain from price recovery of inventory7487 坏帐转回利益gain on reversal of bad debts7488 其它营业外收入-其它other non-operating revenue- other items 75~ 78 营业外费用non-operating expenses751 利息费用interest expense7511 利息费用interest expense752 投资损失investment loss7521 权益法认列之投资损失investment loss recog- nized under equity method7523 短期投资未实现跌价损失unrealized loss on reduction of short-term investments to market753 兑换损失foreign exchange loss7531 兑换损失foreign exchange loss754 处分投资损失loss on disposal of investments7541 处分投资损失loss on disposal of investments755 处分资产损失loss on disposal of assets7551 处分资产损失loss on disposal of assets788 其它营业外费用other non-operating expenses7881 停工损失loss on work stoppages7882 灾害损失casualty loss7885 存货盘损loss on physical inventory7886 存货跌价及呆滞损失loss for market price decline and obsolete and slow-moving inventories7888 其它营业外费用-其它other non-operating expenses- other8 所得税费用(或利益) income tax expense (or benefit)81 所得税费用(或利益) income tax expense (or benefit)811 所得税费用(或利益) income tax expense (or benefit)8111 所得税费用(或利益)income tax expense ( or benefit)9 非经常营业损益nonrecurring gain or loss91 停业部门损益gain(loss) from discontinued operations911 停业部门损益-停业前营业损益income(loss) from operations of discontinued segments9111 停业部门损益-停业前营业损益income(loss) from operations of discontinued segment912 停业部门损益-处分损益gain(loss) from disposal of discontinued segments9121 停业部门损益-处分损益gain(loss) from disposal of discontinued segment92 非常损益extraordinary gain or loss921 非常损益extraordinary gain or loss9211 非常损益extraordinary gain or loss93 会计原则变动累积影响数cumulative effect of changes in accounting principles931 会计原则变动累积影响数cumulative effect of changes in accounting principles9311 会计原则变动累积影响数cumulative effect of changes in accounting principles94 少数股权净利minority interest income941 少数股权净利minority interest income9411 少数股权净利minority interest income。

会计专业英语词汇大全

会计专业英语词汇大全(一)一.专业术语Accelerated Depreciation Method 计算折旧时,初期所提的折旧大于后期各年。

加速折旧法主要包括余额递减折旧法 declining balance depreciation,双倍余额递减折旧法 double declining balance depreciation,年限总额折旧法 sum of the years' depreciation Account 科目,帐户 Account format 帐户式 Account payable 应付帐款 Account receivable 应收帐款 Accounting cycle 会计循环,指按顺序进行记录,归类,汇总和编表的全过程。

在连续的会计期间周而复始的循环进行 Accounting equation 会计等式:资产 = 负债 + 业主权益 Accounts receivable turnover 应收帐款周转率:一个时期的赊销净额 / 应收帐款平均余额 Accrual basis accounting 应记制,债权发生制:以应收应付为计算基础,以确定本期收益与费用的一种方式。

凡应属本期的收益于费用,不论其款项是否以收付,均作为本期收益和费用处理。

Accrued dividend 应计股利 Accrued expense 应记费用:指本期已经发生而尚未支付的各项费用。

Accrued revenue 应记收入 Accumulated depreciation 累计折旧 Acid-test ratio 酸性试验比率,企业速动资产与流动负债的比率,又称quick ratio Acquisition cost 购置成本 Adjusted trial balance 调整后试算表,指已作调整分录但尚未作结账分录的试算表。

Adjusting entry 调整分录:在会计期末所做的分录,将会计期内因某些原因而未曾记录或未适当记录的会计事项予以记录入帐。

会计专业英语L1

About the Exam:

30 SCORES: ordinary performance 70 SCORES: the final exam

10 marks - Attendance 20 marks - Classroom exercises Please find your group partners before this Thursday’s class. Make sure you have Group of six.

Information about decision-making authority, for decision-making support, and for evaluating and rewarding decision-making performance.

Information useful in assessing both the past performance and future directions of the enterprise and information from external and internal sources.

of accounting Information, including shareholders, lenders, customers, suppliers, government departments employees, and society at large. Anyone with an interest in the performance and activities of an organization is traditionally called a stakeholder(利益相关者).

会计英语教程课件

会计英语教程

9

• dissolve 解散 • cash 现金,现款 • balance 余额,结余;差额;平衡 • amount 金额;合计;共计 • credit 信用;信誉;贷方,贷项 • material 原料,材料,物资 • captial 资本,首都

会计英语教程

10

基本语法

• 非限制性定语从句 • 状语从句 • 宾语从句 • 从句的引导词

会计英语教程

24

基本句型

• It is suggested that • It is ordered that • It is required that

会计英语教程

25

translation

会计英语教程

26

Lesson 11 Inventories

• New words • Inventory 存货 • Costing 成本计算,成本计价 • Cost flow 成本流动 • Inflation 通货膨胀 • Footote 脚注 • Replenish 补充,补足

in order that

会计英语教程

6

翻译课文

会计英语教程

7

Lesson 3 The Accounting System

• 教学步骤: • 复习单词 • 学习新单词、课文 • 翻译

会计英语教程

8

New words,PhraseAnd Special Terms

• affect 影响,感动 • accounting system 会计系统;会计制度 • equity 权益,产权 • debt 债务;借款,欠款 • creditor 债权人,债主 • payable 应付的 • claim 要求权;索赔权

会计专业英语新

Unit 1Finan cial in formati on about a bus in ess is n eeded by many outsiders .These outsiders in elude own ers, ban kers, other creditors, pote ntial in vestors, labor unions, gover nment age ncies ,and the public ,because all these groups have supplied money to the bus in ess or have some other in terest in the bus in ess that will be served by in formati on about its finan cial positi on and operati ng results. 许多企业外部的人士需要有关企业的财务信息,这些外部人员包括所有者、银行家、其他债权人、潜在投资者、工会、政府机构和公众,因为这些群体对企业投入了资金,或享有某些利益,所以必须得到企业财务状况和经营成果信息。

Unit 2Each proprietorship, partnership, and corporation is a separate entity.每一独资企业、合伙企业和股份公司都是一个单独的主体。

In accrual acco un ti ng, the impact of eve nts on assets and equities is recog ni zed on the acco unting records in the time periods whe n services are ren dered or utilized in stead of whe n cash is received or disbursed. That is revenue is recog ni zed as it is earn ed, and expe nses are recog ni zed as they are in curred - not when cash cha nges hands .if the cash basis acco un ti ng were used in stead of the accrual basis, revenue and expense recognition would depend solely on the timing of various cash receipts and disbursements.Unit 3During each acco un ti ng year ,a seque nee of acco un ti ng procedures called the acco unting cycle is completed.在每一会计年度内,要依次完成被称为会计循环的会计程序。

立信《会计专业英语》课件LESSON ELEVEN

NEW WORDS, PHRASES AND SPECIAL TERMS

In a crossed check(划线支票,转账支票) 划线支票,转账支票) two parallel lines across the face of the check indicate that it must be paid into a bank account and not cashed over the counter( a general crossing(普通划线)). A special crossing(特别划线) may be used in order to further restrict the negotiability of the check, for example by adding the name of the payee's bank.

NEW WORDS, PHRASES AND SPECIAL TERMS

Under the Check Act(1992) legal force is given to the words 'account payee' on checks, making them nontransferable and thus preventing fraudulent conversion of checks intercepted by a third party. An open check(普通支票)is an uncrossed 普通支票) check that can be cashed at the bank of origin.

NEW WORDS, PHRASES AND SPECIAL TERMS

Bank draft (banker's cheque; banker's draft) 银行汇票 A check drawn by a bank on itself or its agent. A person who owes money to another buys the draft from a bank for cash and hands it to the creditor who need have no fear that it might be dishonored. A bank draft is used if the creditor is unwilling to accept an ordinary check.

会计专业基础英语

会计专业基础英语文件编码(008-TTIG-UTITD-GKBTT-PUUTI-WYTUI-8256)U n i t4A c c o u n t i n g PART I Fundamentals to Accounting第一部分会计基本原理['kant]n. 会计system复式记账法2-1 Dr.(Debit) 借记2-2 Cr.(Credit) 贷记basic assumption会计基本假设entity会计主体concern持续经营periods会计分期measurement货币计量basis会计基础['krl] basis权责发生制【讲解】accrual n. 自然增长,权责发生制原则,应计项目accrual concept 应计概念accrue ['kru] v. 积累,自然增长或利益增加,产生policies会计政策over form实质重于形式elements会计要素[rekg'n()n] n. 确认13-1 initial recognition [rekg'n()n] 初始确认【讲解】recognize ['rkg'naz] v. 确认['mem()nt] n. 计量14-1 subsequent ['sbskw()nt] measurement 后续计量 ['set] n. 资产[la'blt] n. 负债’ equity所有者权益’s equity股东权益[k'spens; ek-] n. 费用['prft] n. 利润[r'zdjl] equity剩余权益claim剩余索取权['kpt()l] n. 资本[ɡeinz] n. 利得[ls] n. 损失earnings留存收益premium股本溢价cost历史成本【讲解】historical [h'strk()l] adj. 历史的,历史上的historic [h'strk] adj. 有历史意义的,历史上着名的28-1 replacement [r'plesm()nt] cost 重置成本Sheet/Statement of Financial Position资产负债表29-1 Income Statement 利润表29-2 Cash Flow Statement 现金流量表29-3 Statement of changes in owners’equity (or shareholders’equity) 所有者权益(股东权益)变动表29-4 notes [nts] n. 附注PART II Financial Assets*第二部分金融资产*assets金融资产. A financial instrument is any contract that gives rise to a financial asset of one enterprise and a financial liability or equity instrument of another enterprise.【讲解】give rise to 引起,导致on hand 库存现金deposits [d'pzt] 银行存款R, account receivable应收账款receivable应收票据receivable其他应收款项investment股权投资investment债券投资financial instrument衍生金融工具market活跃市场[kw()'te()n]n. 报价assets at fair value through profit or loss以公允价值计量且其变动计入当期损益的金融资产41-1 those designated as at fair value through profit or loss 指定为以公允价值计量且其变动计入当期损益的金融资产41-2 financial assets held for trading 交易性金融资产liability金融负债costs交易费用43-1 incremental external cost 新增的外部费用【讲解】incremental [nkr'mntl] adj. 增量的,增值的dividend declared but not distributed 已宣告但尚未发放的现金股利投资收益and loss arising from fair value changes公允价值变动损益investments持有至到期投资cost摊余成本【讲解】amortized ['m:taizd]adj. 分期偿还的,已摊销的interest rate实际利率[ln] n. 贷款[ri'si:vblz] n. 应收账款financial assets可供出售金融资产of financial assets金融资产减值52-1 impairment loss of financial assets 金融资产减值损失of financial assets金融资产转移53-1 transfer of the financial asset in its entirety 金融资产整体转移53-2 transfer of a part of the financial asset 金融资产部分转移[di'rekg'nn] n. 终止确认,撤销承认54-1 derecognize [di'rekgnaz] v. 撤销承认. An enterprise shall derecognize a financial liability (or part of it) only when the underlying present obligation (or part of it) is discharged/cancelled.【译】金融负债的现时义务全部或部分已经解除的,才能终止确认该金融负债或其一部分。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Nashville, TN 37459 Clothes Mart Nashville, TN

May 31, 2006

Lesson 11

CASH CONTROL 现金控制

11- 1

Learning Objectives

Define internal control and identify requirements for good internal accounting control Apply internal control to cash receipts and disbursements Define cash and explain how to report them

11- 6

NEW WORDS, PHRASES AND SPECIAL TERMS

Internal control 内部控制 The measures an organization employsfor

fraud欺骗(行为) or misfeasance不当行为 ,滥用职权are minimized.

Issuing checks for payment of verified, approved and recorded obligations.

11- 16

Voucher System of Control

Cashier Accounting Receiving Supplier (Vendor) Purchasing Requesting

11- 15

Voucher System of Control

A voucher system establishes procedures for:

Verifying, approving and recording obligations for eventual cash disbursements.

Detail Definition P92.

E.g. requiring more than one signature on

certain documents, security arrangement for stock-handling, use of special passwords, handling of computer files, etc.

错误的判断

Intent to Defeat internal controls for personal gain

11- 10

Confusion混淆,困惑

Limitations of Internal Control

The costs of internal controls must not exceed their benefits.

11- 7

Types of Internal Controls

Accounting control: Organization, planning and procedures for safeguarding assets and the reliability of financial records Administrative control: Procedures and methods concerned mainly with operational efficiency and managerial policies

Explain and record petty cash fund transactions.

11- 2

NEW WORDS, PHRASES AND SPECIAL TERMS

Check 支票 Bank deposit 银行存款 Money order 汇票,汇款单 – (post office邮局) Bank draft (banker’s check; banker’s draft)

Cash

IOUs借据, post-dated checks远期支票,uncollected customers’ checks with “NSF” (not sufficient funds) – Receivable -- Not Cash Collection on notes – notes receivable Until notification of collection - Cash

Over-the-Counter 店面交易的,普通零售的 Cash Receipts Cash register with locked-in record of transactions. Compare cash register record with cash reported.

11- 14

Invoice

Purchase Order采购订单 Purchase Requisition请购单

Voucher

11- 17

Bank reconciliation 银行往来调节表

Control is provided by comparing the two records and accounting for any differences

Benefits

Costs

11- 11

Control of Cash

An effective system of internal control that protects cash should meet three basic guidelines:

Handling cash is separated from recordkeeping of cash. Cash receipts are deposited intact完 整无缺的,如数的in a bank each day .

Cash disbursements are made by check.

11- 12

Cash

Cash Notes, coins, checks, money orders and bank deposits - all items that are acceptable for deposit in a bank

Check Invoice Approval Receiving Report

Supplier (Vendor) Cashier Accounting, Requesting & Purchasing Accounting Supplier, Requesting, Receiving & Accounting Purchasing and Accounting

- 银行汇票 A check drawn by a bank on itself or its agent. A person who owes money to another buys the draft from a bank for cash and hands it to the creditor who need have no fear that it might be dishonored拒绝承兑.

11- 3

NEW WORDS, PHRASES AND SPECIAL TERMS

Post-date 迟签日期 To insert a date on a document that is later than the date on which it is signed, thus making it effective only from the later date. A post-dated( or forward-dated) check 远期支票 cannot be negotiated(转让; 议付;兑现) before the date written on it, irrespective of when it was signed. Ante-date 提前填写日期

11- 8

Requirements for good internal accounting control

1.

Competent personnel(称职的人员)

2.

3. 4. 5. 6.

Assignment of responsibility (分派责任)

Division of work Separation of accountability (会计责任) from custodianship (保管工作) Adequate records and equipment Rotation (轮流,轮换) of personnel

11- 4

NEW WORDS, PHRASES AND SPECIAL TERMS

Imprest account 定额备用金账户

A means of controlling petty-cash expenditure in which a

person is given a certain sum of money (float or imprest). When some of it has been spent, that person provides appropriate vouchers 应付凭单for the amounts spent and is then reimbursed偿还,报销so that the float is restored. Thus at any given time the person should have either vouchers or cash to a total of the amount of the float.

11- 5

NEW WORDS, PHRASES AND SPECIAL TERMS