《公司理财》相关资料英文版)

《公司理财》斯蒂芬A罗斯英文》PPT课件讲义

5.1 Definition and Example of a Bond

• A bond is a legally binding agreement between a borrower and a lender: – Specifies the principal amount of the loan. – Specifies the size and timing of the cash flows:

• In dollar terms (fixed-rate borrowing) • As a formula (adjustable-rate borrowing)

5.1 Definition and Example of a Bond

• Consider a U.S. government bond listed as 6 3/8 of December 2009.

N I/Y PV PMT FV

12

5

– 1,070.52

31.875 = 1,000

1,000×0.06375 2

5.3 Bond Concepts

1. Bond prices and market interest rates move in opposite directions.

2. When coupon rate = YTM, price = par value. When coupon rate > YTM, price > par value (premium bond) When coupon rate < YTM, price < par value (discount bond)

(完整word版)公司理财(英文版)题库8

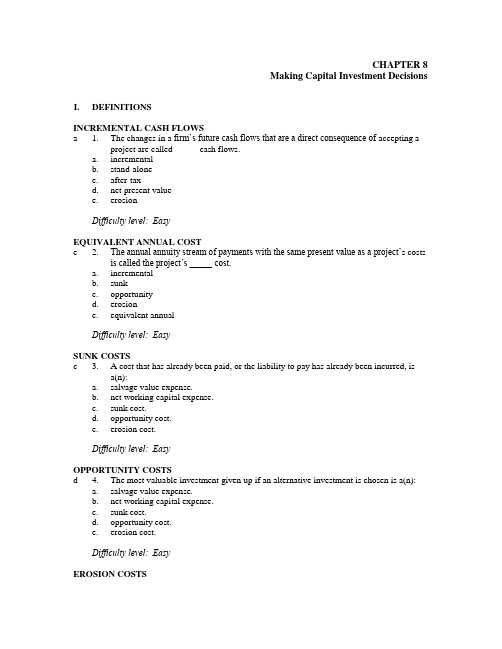

CHAPTER 8Making Capital Investment Decisions I. DEFINITIONSINCREMENTAL CASH FLOWSa 1. The changes in a firm’s future cash flows that are a direct consequence of accepting aproject are called _____ cash flows.a. incrementalb. stand-alonec. after-taxd. net present valuee. erosionDifficulty level: EasyEQUIVALENT ANNUAL COSTe 2. The annual annuity stream of payments with the same present value as a project’s costsis called the project’s _____ cost.a. incrementalb. sunkc. opportunityd. erosione. equivalent annualDifficulty level: EasySUNK COSTSc 3. A cost that has already been paid, or the liability to pay has already been incurred, isa(n):a. salvage value expense.b. net working capital expense.c. sunk cost.d. opportunity cost.e. erosion cost.Difficulty level: EasyOPPORTUNITY COSTSd 4. The most valuable investment given up if an alternative investment is chosen is a(n):a. salvage value expense.b. net working capital expense.c. sunk cost.d. opportunity cost.e. erosion cost.Difficulty level: EasyEROSION COSTSe 5. The cash flows of a new project that come at the expense of a firm’s existing projectsare called:a. salvage value expenses.b. net working capital expenses.c. sunk costs.d. opportunity costs.e. erosion costs.Difficulty level: EasyPRO FORMA FINANCIAL STATEMENTSa 6. A pro forma financial statement is one that:a. projects future years’ operations.b. is expressed as a percentage of the total assets of the firm.c. is expressed as a percentage of the total sales of the firm.d. is expressed relative to a chosen base year’s financial statement.e. reflects the past and current operations of the firm.Difficulty level: EasyMACRS DEPRECIATIONb 7. The depreciation method currently allowed under US tax law governing the acceleratedwrite-off of property under various lifetime classifications is called _____ depreciation.a. FIFOb. MACRSc. straight-lined. sum-of-years digitse. curvilinearDifficulty level: EasyDEPRECIATION TAX SHIELDc 8. The cash flow tax savings generated as a result of a firm’s tax-deductible depreciationexpense is called the:a. after-tax depreciation savings.b. depreciable basis.c. depreciation tax shield.d. operating cash flow.e. after-tax salvage value.Difficulty level: EasyCASH FLOWd 9. The cash flow from projects for a company is computed as the:a. net operating cash flow generated by the project, less any sunk costs and erosion costs.b. sum of the incremental operating cash flow and after-tax salvage value of the project.c. net income generated by the project, plus the annual depreciation expense.d. sum of the incremental operating cash flow, capital spending, and net working capitalexpenses incurred by the project.e. sum of the sunk costs, opportunity costs, and erosion costs of the project.Difficulty level: MediumII. CONCEPTSPRO FORMA INCOME STATEMENTb 10. The pro forma income statement for a cost reduction project:a. will reflect a reduction in the sales of the firm.b. will generally reflect no incremental sales.c. has to be prepared reflecting the total sales and expenses of a firm.d. cannot be prepared due to the lack of any project related sales.e. will always reflect a negative project operating cash flow.Difficulty level: EasyINCREMENTAL CASH FLOWb 11. One purpose of identifying all of the incremental cash flows related to a proposedproject is to:a. isolate the total sunk costs so they can be evaluated to determine if the project willadd value to the firm.b. eliminate any cost which has previously been incurred so that it can be omitted fromthe analysis of the project.c. make each project appear as profitable as possible for the firm.d. include both the proposed and the current operations of a firm in the analysis of theproject.e. identify any and all changes in the cash flows of the firm for the past year so they canbe included in the analysis.Difficulty level: MediumINCREMENTAL CASH FLOWe 12. Which of the following are examples of an incremental cash flow?I. an increase in accounts receivableII. a decrease in net working capitalIII. an increase in taxesIV. a decrease in the cost of goods solda. I and III onlyb. III and IV onlyc. I and IV onlyd. I, III, and IV onlye. I, II, III, and IVDifficulty level: MediumINCREMENTAL CASH FLOWc 13. Which one of the following is an example of an incremental cash flow?a. the annual salary of the company president which is a contractual obligationb. the rent on a warehouse which is currently being utilizedc. the rent on some new machinery that is required for an upcoming projectd. the property taxes on the currently owned warehouse which has been sitting idle butis going to be utilized for a new projecte. the insurance on a company-owned building which will be utilized for a new projectDifficulty level: MediumINCREMENTAL COSTSd 14. Project analysis is focused on _____ costs.a. sunkb. totalc. variabled. incrementale. fixedDifficulty level: MediumSUNK COSTc 15. Sunk costs include any cost that:a. will change if a project is undertaken.b. will be incurred if a project is accepted.c. has previously been incurred and cannot be changed.d. is paid to a third party and cannot be refunded for any reason whatsoever.e. will occur if a project is accepted and once incurred, cannot be recouped.Difficulty level: EasySUNK COSTd 16. You spent $500 last week fixing the transmission in your car. Now, the brakes areacting up and you are trying to decide whether to fix them or trade the car in for anewer model. In analyzing the brake situation, the $500 you spent fixing thetransmission is a(n) _____ cost.a. opportunityb. fixedc. incrementald. sunke. relevantDifficulty level: EasyEROSIONb 17. Erosion can be explained as the:a. additional income generated from the sales of a newly added product.b. loss of current sales due to a new project being implemented.c. loss of revenue due to employee theft.d. loss of revenue due to customer theft.e. loss of cash due to the expenses required to fix a parking lot after a heavy rain storm.Difficulty level: EasyEROSIONa 18. Which of the following are examples of erosion?I. the loss of sales due to increased competition in the product marketII. the loss of sales because your chief competitor just opened a store across the street from your storeIII. the loss of sales due to a new product which you recently introducedIV. the loss of sales due to a new product recently introduced by your competitora. III onlyb. III and IV onlyc. I, III and IV onlyd. II and IV onlye. I, II, III, and IVDifficulty level: MediumTYPES OF COSTSd 19. Which of the following should be included in the analysis of a project?I. sunk costsII. opportunity costsIII. erosion costsIV. incremental costsa. I and II onlyb. III and IV onlyc. II and IV onlyd. II, III, and IV onlye. I, II, and IV onlyDifficulty level: MediumNET WORKING CAPITALd 20. All of the following are anticipated effects of a proposed project. Which of theseshould be included in the initial project cash flow related to net working capital?I. an inventory decrease of $5,000II. an increase in accounts receivable of $1,500III. an increase in fixed assets of $7,600IV. a decrease in accounts payable of $2,100a. I and II onlyb. I and III onlyc. II and IV onlyd. I, II, and IV onlye. I, II, III, and IVDifficulty level: MediumNET WORKING CAPITALa 21. Changes in the net working capital:a. can affect the cash flows of a project every year of the project’s life.b. only affect the initial cash flows of a project.c. are included in project analysis only if they represent cash outflows.d. are generally excluded from project analysis due to their irrelevance to the totalproject.e. affect the initial and the final cash flows of a project but not the cash flows of themiddle years.Difficulty level: MediumNET WORKING CAPITALc 22. Which one of the following will decrease net working capital of a firm?a. a decrease in accounts payableb. an increase in inventoryc. a decrease in accounts receivabled. an increase in the firm’s checking account balancee. a decrease in fixed assetsDifficulty level: EasyNET WORKING CAPITALd 23. Net working capital:a. can be ignored in project analysis because any expenditure is normally recouped by theend of the project.b. requirements generally, but not always, create a cash inflow at the beginning of aproject.c. expenditures commonly occur at the end of a project.d. is frequently affected by the additional sales generated by a new project.e. is the only expenditure where at least a partial recovery can be made at the end of aproject.Difficulty level: EasyMACRSd 24. A company which uses the MACRS system of depreciation:a. will have equal depreciation costs each year of an asset’s life.b. will expense the cost of nonresidential real estate over a period of 7 years.c. can depreciate the cost of land, if they so desire.d. will write off the entire cost of an asset over the asset’s class life.e. cannot expense any of the cost of a new asset during the first year of the asset’s life.Difficulty level: EasyMACRSa 25. Bet ‘r Bilt Toys just purchased some MACRS 5-year property at a cost of $230,000.Which of the following will correctly give you the book value of this equipment at theend of year 2?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%I. 52% of the asset costII. 48% of the asset costIII. 68% of 80% of the asset costIV. the asset cost, minus 20% of the asset cost, minus 32% of 80% of the asset costa. II onlyb. III and IV onlyc. I and III onlyd. II and IV onlye. I, II, III, and IVDifficulty level: EasyMACRSe 26. Will Do, Inc. just purchased some equipment at a cost of $650,000. What is theproper methodology for computing the depreciation expense for year 3 if theequipment is classified as 5-year property for MACRS?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $650,000 ⨯ (1-.20) ⨯ (1-.32) ⨯ (1-.192)b. $650,000 ⨯ (1-.20) ⨯ (1-.32)c. $650,000 ⨯ (1+.20) ⨯ (1+.32) ⨯ (1+.192)d. $650,000 ⨯ (1-.192)e. $650,000 ⨯ .192Difficulty level: MediumBOOK VALUEd 27. The book value of an asset is primarily used to compute the:a. annual depreciation tax shield.b. amount of cash received from the sale of an asset.c. amount of tax saved annually due to the depreciation expense.d. amount of tax due on the sale of an asset.e. change in depreciation needed to reflect the market value of the asset.Difficulty level: EasySALVAGE VALUEc 28. The salvage value of an asset creates an after-tax cash inflow to the firm in an amountequal to the:a. sales price of the asset.b. sales price minus the book value.c. sales price minus the tax due based on the sales price minus the book value.d. sales price plus the tax due based on the sales price minus the book value.e. sales price plus the tax due based on the book value minus the sales price.Difficulty level: EasySALVAGE VALUEe 29. The pre-tax salvage value of an asset is equal to the:a. book value if straight-line depreciation is used.b. book value if MACRS depreciation is used.c. market value minus the book value.d. book value minus the market value.e. market value.Difficulty level: EasyPROJECT OCFa 30. A project’s operating cash flow will increase when:a. the depreciation expense increases.b. the sales projections are lowered.c. the interest expense is lowered.d. the net working capital requirement increases.e. the earnings before interest and taxes decreases.Difficulty level: EasyPROJECT CASH FLOWSc 31. The cash flows of a project should:a. be computed on a pre-tax basis.b. include all sunk costs and opportunity costs.c. include all incremental costs, including opportunity costs.d. be applied to the year when the related expense or income is recognized by GAAP.e. include all financing costs related to new debt acquired to finance the project.Difficulty level: EasyPROJECT OCFa 32. Which of the following are correct methods for computing the operating cash flow ofa project assuming that the interest expense is equal to zero?I. EBIT + Depreciation - TaxesII. EBIT + Depreciation + TaxesIII. Net Income + DepreciationIV. (Sales – Costs) ⨯ (Taxes + Depreciation) ⨯ (1-Taxes)a. I and III onlyb. II and IV onlyc. II and III onlyd. I, III, and IV onlye. II, III, and IV onlyDifficulty level: MediumBOTTOM-UP OCFb 33. The bottom-up approach to computing the operating cash flow applies only when:a. both the depreciation expense and the interest expense are equal to zero.b. the interest expense is equal to zero.c. the project is a cost-cutting project.d. no fixed assets are required for the project.e. taxes are ignored and the interest expense is equal to zero.Difficulty level: MediumTOP-DOWN OCFa 34. The top-down approach to computing the operating cash flow:a. ignores all noncash items.b. applies only if a project produces sales.c. can only be used if the entire cash flows of a firm are included.d. is equal to sales - costs - taxes + depreciation.e. includes the interest expense related to a project.Difficulty level: MediumTAX SHIELDd 35. An increase in which one of the following will increase the operating cash flow?a. employee salariesb. office rentc. building maintenanced. equipment depreciatione. equipment rentalDifficulty level: EasyTAX SHIELDc 36. Tax shield refers to a reduction in taxes created by:a. a reduction in sales.b. an increase in interest expense.c. noncash expenses.d. a project’s incremental expenses.e. opportunity costs.Difficulty level: EasyCOST-CUTTINGc 37. A project which is designed to improve the manufacturing efficiency of a firm but willgenerate no additional sales is referred to as a(n) _____ project.a. sunk costb. opportunityc. cost-cuttingd. revenue-cuttinge. revenue-generatingDifficulty level: EasyEQUIVALENT ANNUAL COSTc 38. Toni’s Tools is comparing machines to determine which one to purchase. Themachines sell for differing prices, have differing operating costs, differing machinelives, and will be replaced when worn out. These machines should be compared using:a. net present value only.b. both net present value and the internal rate of return.c. their effective annual costs.d. the depreciation tax shield approach.e. the replacement parts approach.Difficulty level: MediumEQUIVALENT ANNUAL COSTe 39. The equivalent annual cost method is useful in determining:a. the annual operating cost of a machine if the annual maintenance is performed versuswhen the maintenance is not performed as recommended.b. the tax shield benefits of depreciation given the purchase of new assets for a project.c. operating cash flows for cost-cutting projects of equal duration.d. which one of two machines to acquire given equal machine lives but unequal machinecosts.e. which one of two machines to purchase when the machines are mutually exclusive,have different machine lives, and will be replaced once they are worn out.Difficulty level: MediumIII. PROBLEMSRELEVANT CASH FLOWSd 40. Marshall’s & Co. purchased a corner lot in Eglon City five y ears ago at a cost of$640,000. The lot was recently appraised at $810,000. At the time of the purchase, thecompany spent $50,000 to grade the lot and another $4,000 to build a small buildingon the lot to house a parking lot attendant who has overseen the use of the lot for dailycommuter parking. The company now wants to build a new retail store on the site. Thebuilding cost is estimated at $1.2 million. What amount should be used as the initialcash flow for this building project?a. $1,200,000b. $1,840,000c. $1,890,000d. $2,010,000e. $2,060,000Difficulty level: MediumRELEVANT CASH FLOWSe 41. Jamestown Ltd. currently produces boat sails and is considering expanding itsoperations to include awnings for homes and travel trailers. The company owns landbeside its current manufacturing facility that could be used for the expansion. Thecompany bought this land ten years ago at a cost of $250,000. Today, the land isvalued at $425,000. The grading and excavation work necessary to build on the landwill cost $15,000. The company currently has some unused equipment which itcurrently owns valued at $60,000. This equipment could be used for producingawnings if $5,000 is spent for equipment modifications. Other equipment costing$780,000 will also be required. What is the amount of the initial cash flow for thisexpansion project?a. $800,000b. $1,050,000c. $1,110,000d. $1,225,000e. $1,285,000Difficulty level: MediumRELEVANT CASH FLOWSb 42. Wilbert’s, Inc. paid $90,000, in cash, for a piece of equipment three years ago. Lastyear, the company spent $10,000 to update the equipment with the latest technology.The company no longer uses this equipment in their current operations and hasreceived an offer of $50,000 from a firm who would like to purchase it. Wilbert’s isdebating whether to sell the equipment or to expand their operations such that theequipment can be used. When evaluating the expansion option, what value, if any,should Wilbert’s assign to this equipment as an initial cost of the project?a. $40,000b. $50,000c. $60,000d. $80,000e. $90,000Difficulty level: EasyRELEVANT CASH FLOWSa 43. Walks Softly, Inc. sells customized shoes. Currently, they sell 10,000 pairs of shoesannually at an average price of $68 a pair. They are considering adding a lower-pricedline of shoes which sell for $49 a pair. Walks Softly estimates they can sell 5,000 pairsof the lower-priced shoes but will sell 1,000 less pairs of the higher-priced shoes bydoing so. What is the amount of the sales that should be used when evaluating theaddition of the lower-priced shoes?a. $177,000b. $245,000c. $313,000d. $789,000e. $857,000Difficulty level: MediumOPPORTUNITY COSTc 44. Your firm purchased a warehouse for $335,000 six years ago. Four years ago, repairswere made to the building which cost $60,000. The annual taxes on the property are$20,000. The warehouse has a current book value of $268,000 and a market value of$295,000. The warehouse is totally paid for and solely owned by your firm. If thecompany decides to assign this warehouse to a new project, what value, if any, shouldbe included in the initial cash flow of the project for this building?a. $0b. $268,000c. $295,000d. $395,000e. $515,000Difficulty level: EasyOPPORTUNITY COSTd 45. You own a house that you rent for $1,200 a month. The maintenance expenses onthe house average $200 a month. The house cost $89,000 when you purchased itseveral years ago. A recent appraisal on the house valued it at $210,000. The annualproperty taxes are $5,000. If you sell the house you will incur $20,000 in expenses.You are deciding whether to sell the house or convert it for your own use as aprofessional office. What value should you place on this house when analyzing theoption of using it as a professional office?a. $89,000b. $120,000c. $185,000d. $190,000e. $210,000Difficulty level: MediumOPPORTUNITY COSTc 46. Big Joe’s owns a manufacturing facility that is currently sitting idle. The facility islocated on a piece of land that originally cost $129,000. The facility itself cost$650,000 to build. As of now, the book value of the land and the facility are $129,000and $186,500, respectively. Big Joe’s received an offer of $590,000 for the land andfacility last week. They rejected this offer even though they were told that it is areasonable offer in today’s market. If Big Joe’s were to consider using this land andfacility in a new project, what cost, if any, should they include in the project analysis?a. $0b. $315,500c. $590,000d. $650,000e. $779,000Difficulty level: EasyEROSION COSTb 47. Jamie’s Motor Home Sales currently sells 1,000 Class A motor homes, 2,500 Class Cmotor homes, and 4,000 pop-up trailers each year. Jamie is considering adding a mid-range camper and expects that if she does so she can sell 1,500 of them. However, ifthe new camper is added, Jamie expects that her Class A sales will decline to 950 unitswhile the Class C campers decline to 2,200. The sales of pop-ups will not be affected.Class A motor homes sell for an average of $125,000 each. Class C homes are pricedat $39,500 and the pop-ups sell for $5,000 each. The new mid-range camper will sellfor $47,900. What is the erosion cost?a. $6,250,000b. $18,100,000c. $53,750,000d. $93,150,000e. $118,789,500Difficulty level: MediumOCFe 48. Ernie’s E lectrical is evaluating a project which will increase sales by $50,000 andcosts by $30,000. The project will cost $150,000 and be depreciated straight-line to azero book value over the 10 year life of the project. The applicable tax rate is 34%.What is the operating cash flow for this project?a. $3,300b. $5,000c. $8,300d. $13,300e. $18,300Difficulty level: MediumOCFd 49. Kurt’s Kabinets is looking at a project that will require $80,000 in fixed assets andanother $20,000 in net working capital. The project is expected to produce sales of$110,000 with associated costs of $70,000. The project has a 4-year life. The companyuses straight-line depreciation to a zero book value over the life of the project. The taxrate is 35%. What is the operating cash flow for this project?a. $7,000b. $13,000c. $27,000d. $33,000e. $40,000Difficulty level: MediumBOTTOM-UP OCFc 50. Peter’s Boats has sales of $760,000 and a profit margin of 5%. The annualdepreciation expense is $80,000. What is the amount of the operating cash flow if thecompany has no long-term debt?a. $34,000b. $86,400c. $118,000d. $120,400e. $123,900Difficulty level: MediumBOTTOM-UP OCFd 51. Le Place has sales of $439,000, depreciation of $32,000, and net working capital of$56,000. The firm has a tax rate of 34% and a profit margin of 6%. Thefirm has no interest expense. What is the amount of the operating cash flow?a. $49,384b. $52,616c. $54,980d. $58,340e. $114,340Difficulty level: MediumTOP-DOWN OCFb 52. Ben’s Border Café is considering a project which will produce sales of $16,000 andincrease cash expenses by $10,000. If the project is implemented, taxes will increasefrom $23,000 to $24,500 and depreciation will increase from $4,000 to $5,500. Whatis the amount of the operating cash flow using the top-down approach?a. $4,000b. $4,500c. $6,000d. $7,500e. $8,500Difficulty level: MediumTOP-DOWN OCFc 53. Ronnie’s Coffee House i s considering a project which will produce sales of $6,000and increase cash expenses by $2,500. If the project is implemented, taxes willincrease by $1,300. The additional depreciation expense will be $1,000. An initial cashoutlay of $2,000 is required for net working capital. What is the amount of theoperating cash flow using the top-down approach?a. $200b. $1,500c. $2,200d. $3,500e. $4,200Difficulty level: MediumTAX SHIELD OCFc 54. A project will increase sales by $60,000 and cash expenses by $51,000. The projectwill cost $40,000 and be depreciated using straight-line depreciation to a zero bookvalue over the 4-year life of the project. The company has a marginal tax rate of 35%.What is the operating cash flow of the project using the tax shield approach?a. $5,850b. $8,650c. $9,350d. $9,700e. $10,350Difficulty level: MediumDEPRECIATION TAX SHIELDa 55. A project will increase sales by $140,000 and cash expenses by $95,000. The projectwill cost $100,000 and be depreciated using the straight-line method to a zero bookvalue over the 4-year life of the project. The company has a marginal tax rate of 34%.What is the value of the depreciation tax shield?a. $8,500b. $17,000c. $22,500d. $25,000e. $37,750Difficulty level: MediumMACRS DEPRECIATIONd 56. Sun Lee’s Furniture just purchased some fixed assets classified as 5-year property forMACRS. The assets cost $24,000. What is the amount of the depreciation expense forthe third year?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $2,304b. $2,507c. $2,765d. $4,608e. $4,800Difficulty level: EasyMACRS DEPRECIATIONa 57. You just purchased some equipment that is classified as 5-year property for MACRS.The equipment cost $67,600. What will the book value of this equipment be at the endof three years should you decide to resell the equipment at that point in time?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $19,468.80b. $20,280.20c. $27,040.00d. $48,131.20e. $48,672.00Difficulty level: MediumMACRS DEPRECIATIONd 58. LiCheng’s Enterprises just purchased some fixed assets that are classified as 3-yearproperty for MACRS. The assets cost $1,900. What is the amount of thedepreciation expense for year 2?MACRS 3-year propertyYear Rate1 33.33%2 44.44%3 14.82%4 7.41%a. $562.93b. $633.27c. $719.67d. $844.36e. $1,477.63Difficulty level: MediumMACRS DEPRECIATIONb 59. RP&A, Inc. purchased some fixed assets four years ago at a cost of $19,800. They nolonger need these assets so are going to sell them today at a price of $3,500. The assetsare classified as 5-year property for MACRS. What is the current book value of theseassets?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. $1,140.48b. $3,421.44c. $3,500.00d. $4,016.67e. $5,702.40Difficulty level: MediumSALVAGE VALUEa 60. You own some equipment which you purchased three years ago at a cost of $135,000.The equipment is 5-year property for MACRS. You are considering selling theequipment today for $82,500. Which one of the following statements is correct if yourtax rate is 34%?MACRS 5-year propertyYear Rate1 20.00%2 32.00%3 19.20%4 11.52%5 11.52%6 5.76%a. The tax due on the sale is $14,830.80.b. The book value today is $8,478.c. The book value today is $64,320.d. The taxable amount on the sale is $38,880.e. You will receive a tax refund of $13,219.20 as a result of this sale.。

公司理财原版英文课件Chap019概要1

19-9

Dividends and Investment Policy

Firms should never forgo positive NPV projects to increase a dividend (or to pay a dividend for the first time).

Record Date – Date on which company determines existing shareholders.

19-4

Procedure for Cash Dividend

25 Oct.

…

1 Nov.

Declaration Date

$240 $39 × 80 =

$3,120

$3,120 19-8

Dividend Policy Is Irrelevant

In the above example, Bob Investor began with a total wealth of $3,360:

$3,36080share$s42 share

Cum-

Ex-

dividend dividend

Date

Date

Record Date

Payment Date

Declaration Date: The Board of Directors declares a payment of dividends. Cum-Dividend Date: Buyer of stock still receives the dividend.

Understand dividend types and how they are paid

《公司理财》斯蒂芬A.罗斯..,机械工业出版社 英文课件

Synergy = where

Σ

T t=1

CFt (1 + r)t

CFt = Revt – Costst – Taxest – Capital Requirementst

McGraw-Hill/Irwin

Copyright 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

29-8

29.5 Source of Synergy from Acquisitions

CFt = Revt – Costst – Taxest – Capital Requirementst

Revenue Enhancement Cost Reduction

– Including replacement of ineffective managers.

29-3

Varieties of Takeovers

Merger Acquisition Takeovers Proxy Contest Going Private (LBO) Acquisition of Stock Acquisition of Assets

McGraw-Hill/Irwin

Copyright 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

Purchase accounting is generally used under other financing arrangements.

McGraw-Hill/Irwin

Copyright 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

公司理财(罗斯)第1章(英文

03 Valuation Basis

The concept and significance of valuation

要点一

Definition

Valuation is the process of estimating the worth of an asset or a company, typically through the use of financial metrics and analysis.

The Time Value of Money

英文版公司理财chapter-1课件

Making good investment and financing decisions is the chief task of the financial manager.

英文版公司理财chapter-1

7

The Investment Decision

• Investment decision /capital budgeting decision: decision to invest in

2750% Deb50t % 3D0e%bEt quity 5705% Equity

If how you slice the pie affects the size of the pie, then the capital structure decision matters.

英文版公司理财chapter-1

4. Understand why conflicts of interest arise, especially in large, public corporations

5. Explain how corporations mitigate conflicts and encourage ethical behavior

英文版公司理财chapter-1

Current Liabilities Long-Termபைடு நூலகம்Debt

Shareholders’ Equity

13

• The choice between debt and equity financing is often called the

capital structure decision

2

Chapter 1

The Corporation and the Financial Manager

《公司理财》斯蒂芬A.罗斯..,机械工业出版社 英文课件

McGraw-Hill/Irwin

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

3-9

Financial Requirements

• The plan will include a section on financing arrangements. • Dividend policy and capital structure policy should be addressed. • If new funds are to be raised, the plan should consider what kinds of securities must be sold and what methods of issuance are most appropriate.

McGraw-Hill/Irwin

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

3-10

Plug

• Compatibility across various growth targets will usually require adjustment in a third variable. • Suppose a financial planner assumes that sales, costs, and net income will rise at g1. Further, suppose that the planner desires assets and liabilities to grow at a different rate, g2. These two rates may be incompatible unless a third variable is adjusted. For example, compatibility may only be reached is outstanding stock grows at a third rate, g3.

公司理财期末整理(英文版)

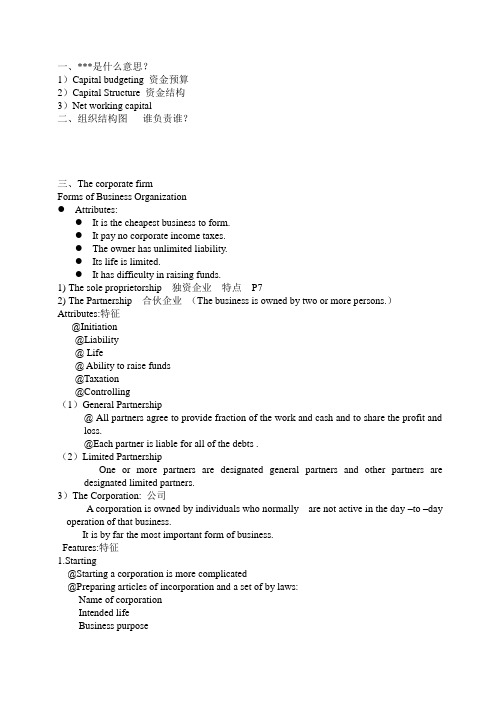

一、***是什么意思?1)Capital budgeting 资金预算2)Capital Structure 资金结构3)Net working capital二、组织结构图谁负责谁?三、The corporate firmForms of Business Organization●Attributes:●It is the cheapest business to form.●It pay no corporate income taxes.●The owner has unlimited liability.●Its life is limited.●It has difficulty in raising funds.1)The sole proprietorship 独资企业特点P72)The Partnership 合伙企业(The business is owned by two or more persons.)Attributes:特征@Initiation@Liability@ Life@ Ability to raise funds@Taxation@Controlling(1)General Partnership@ All partners agree to provide fraction of the work and cash and to share the profit and loss.@Each partner is liable for all of the debts .(2)Limited PartnershipOne or more partners are designated general partners and other partners are designated limited partners.3)The Corporation: 公司A corporation is owned by individuals who normally are not active in the day –to –day operation of that business.It is by far the most important form of business.Features:特征1.Starting@Starting a corporation is more complicated@Preparing articles of incorporation and a set of by laws:Name of corporationIntended lifeBusiness purposeNumber of shares of stockNature of the right granted to shareholdersNumber of members of the initial board of directors2. Three sets of distinct interests:ShareholdersDirectorsCorporation officer3.It is a legal entity.4.OwnershipOwnership is represented by shares of stock, it is easy to transfer ownership.5.Life6.The corporation has unlimited life7.LiabilityLiability is limited to the amounted invested in the ownership .8.Taxation: double taxation9.Raising funds: easyThe goal of financial management:Maximize the current value per share of the existing stock.1.5 Financial MarketsClassification of financial markets市场分类1.Money market vs capital market1) Money MarketThe market for debt securities that will pay off in the short term2) Capital MarketThe market for long-term debt and for equity shares (common stock, preferred stock, corporate and government bonds2.Primary Market vs Secondary Markets1) Primary Market一级市场Issuance of a security for the first time2)Secondary Markets二级市场Buying and selling of previously issued securitiesanized security exchanges vs over-the counter market (Securities may be traded in either a dealer or auction market1) Organized security exchanges are tangible entitiesNYSE2)OCT include all security markets eccept the organized exchanges.NASDAQ2.3 TaxesThe one thing we can rely on with taxes is that they are always changingMarginal vs. average tax ratesMarginal – the percentage paid on the next dollar earnedAverage – the tax bill / taxable income1) Average tax rate is tax bill divided your taxable income.2) Marginal tax rate is the tax you would pay (in percent) if you earned one more dollar.例题:Taxable Income Tax Rate$ 0 - 50,000 15%50,001-75,000 25%75,001-100,000 34%100,001-335,000 39%335,001-10,000,000 34%--------------------------------The tax rates apply to the part of income in the indicated range only, not all income.Suppose your firm earns $4 million in taxable income. Use table2.1,we can figure out tax bill as:.15($50,000)=$7,500.25(75,00-50,000)=6250.34(100,000-75,000)=8500.39(335,000-100,000)=91,650.34(4,000,000-335,000)=1246,100Total tax bill 1,360,000Average tax rate= 1,360,000/4,000,000 =34%EquationCash flows from the assets= Operating cash flow –Investment in NWC –Investment in fixed assets1.Operating cash flowDefinition: Operating cash flow refers to the cash generated from operations.Calculation:Method 1:OCF= Sales – Costs – TaxesMethod 2:OCF = EBIT + Depreciation – TaxesEgNabors, corporation.2005 Income Statement ($ in millions)Net sales $9,610Less: Cost of goods sold 6,310Less: Depreciation 1,370Earnings before interest and taxes 1,930Less: Interest paid 630Taxable Income $1,300Less: Taxes 455Net income $ 845Method1:Sales $9,610Less: cost 6,310Taxes 455Operating cash flow $ 2845Nabors, corporation2005 Income Statement ($ in millions)Net sales $9,610Less: Cost of goods sold 6,310Less: Depreciation 1,370Earnings before interest and taxes 1,930Less: Interest paid 630Taxable Income $1,300Less: Taxes 455Net income $ 845Method2:Earnings before interest and taxes $1,930Plus depreciation 1,370Less taxes 455Operating cash flow $ 2845Positive cash flows were generated from operations of $2845.2.Change in NWCDefinition:Net Working Capital =current assets – current liabilitiesNWC usually grows with the firmChange in NWC= ending net working capital – beginning net working capital3.Change in fixed assetsMethod 1:Ending gross fixed assets- Beginning gross fixed assets = Change in fixed assets Method 2:Ending net fixed assts - Beginning net fixed assets+ Depreciation= Change in fixed assets .Free cash flowCommon-Size Balance SheetsCompute all accounts as a percent of total assets(express each item as percentage of total assetsCommon-Size Income StatementsCompute all line items as a percent of sales(express each item as a percentage of total sales)Categories of Financial RatiosShort-term solvency or liquidity ratiosLong-term solvency, or financial leverage, ratiosAsset management or turnover ratiosProfitability ratiosMarket value ratiosComputing Liquidity RatiosMeaningLiquidity ratios are intended to provide information about a firm’s liquidity.Who are interested in liquidity ratiosshort-term creditorFeaturesTheir book value and market value are likely to be similar.CalculationCurrent Ratio = CA / CL (dollar or times)708 / 540 = 1.31 timesQuick Ratio (acid-test)= (CA – Inventory) / CL(708 - 422) / 540 = .53 timesCash Ratio = Cash / CL98 / 540 = .18 times3.3 The Du Pont IdentityIt is an integrative approach to ratio analysis.It evaluates firm’s return on equity (ROE)Definition of ROEROE = Net income / Total equityMultiply by 1(TA / TA) and then rearrange:ROE = (NI / TE) (TA / TA)ROE = (NI / TA) (TA / TE) = ROA * EMMultiply by 1 again and then rearrange:ROE = (NI / TA) (TA / TE) (Sales / Sales)ROE = (NI / Sales) (Sales / TA) (TA / TE)ROE = PM * TAT * EMROE = PM * TAT * EMProfit margin is a measure of the firm’s operating efficiency – how well it controls costs.Total asset turnover is a measure of the firm’s asset use efficiency – how well it manages its assets.Equity multipli er is a measure of the firm’s financial leverage.3.5 Long-Term Financial PlanningAnother use of financial statementsThe most comprehensive means of financial planning is to develop a series of pro forma, or projected, financial statements.External Financing Needed (EFN)The difference between the forecasted increase in assets and the forecasted increase in liabilities and equity.Formula: EFN=Assets×g- Spontaneous liabilities×g-PM×Projected sales×(1-d)External Financing Needed (EFN) can also be calculated as:The Internal Growth RateThe internal growth rate tells us how much the firm can grow assets using retained earnings as the only source of financing.The Sustainable Growth RateThe sustainable growth rate tells us how much the firm can grow by using internally generated funds and issuing debt to maintain a constant debt ratio.4.4 SimplificationsPerpetuityA constant stream of cash flows that lasts foreverGrowing perpetuityA stream of cash flows that grows at a constant rate foreverAnnuityA stream of constant cash flows that lasts for a fixed number of periodsGrowing annuityA stream of cash flows that grows at a constant rate for a fixed number of periodsZero Coupon BondsMake no periodic interest payments (coupon rate = 0%)The entire yield to maturity comes from the difference between the purchase price and the par valueCannot sell for more than par valueSometimes called zeroes, deep discount bonds, or original issue discount bonds (OIDs) Treasury Bills and principal-only Treasury strips are good examples of zeroesThe Fisher EffectThe Fisher Effect defines the relationship between real rates, nominal rates, and inflation.(1 + R) = (1 + r)(1 + h), whereR = nominal rater = real rateh = expected inflation rateApproximationR = r + h例子If we require a 10% real return and we expect inflation to be 8%, what is the nominal rate? R = (1.1)(1.08) – 1 = .188 = 18.8%Approximation: R = 10% + 8% = 18%Because the real return and expected inflation are relatively high, there is a significant difference between the actual Fisher Effect and the approximation.。

公司理财(双语)9IssueSecurities

国际证券市场的参与者

发行人

发行人是指在国际证券市场 上发行证券的企业或政府机 构。

投资者

投资者是指购买国际证券市 场的证券的个人或机构,包 括个人投资者、机构投资者 和外国投资者等。

承销商

承销商是指在国际证券市场 上负责承销证券的金融机构 或投资银行。

监管机构

监管机构是指在国际证券市 场上负责监管市场运行和参 与者的机构,如证券交易所、 证券监管机构等。

实施

实施公司理财策略需要建立完善的财务管理体系,明确 各级财务人员的职责和权限,确保理财策略的有效执行 。

公司理财策略的评估与调整

评估

定期评估公司理财策略的效果,通过财务指标、市场 反应等手段,分析策略的实际效果,发现问题并及时 调整。

调整

根据市场环境、企业经营状况等因素的变化,及时调整 公司理财策略,以保持其与企业的实际情况和发展需求 的适应性。

债券的发行与交易

总结词

债券的发行和交易涉及多个环节和参与 者。

VS

详细描述

在发行环节,公司或政府会通过证券承销 商将债券销售给投资者,并支付相应的发 行费用。在交易环节,投资者可以在二级 市场买卖债券,市场上有做市商提供双边 报价,投资者也可以通过经纪商进行买卖 。此外,还有中央证券存管机构对证券进 行托管和清算。

交易所进行,私募则直接向特定投资者销售。

交易场所

02

股票通常在证券交易所进行交易,如纽约证券交易所、香港联

合交易所等。

交易规则

03

股票交易遵循证券交易所的交易规则,包括报价方式、交易时

间、交易数量限制等。

03

债券

债券的定义与特点

总结词

《公司理财》斯蒂芬A.罗斯..,机械工业出版社 英文课件

McGraw-Hill/Irwin

Copyright © 2004 by The McGraw-Hill Companies, Inc. All rights reserved.

5-7

Pure Discount Bonds

Information needed for valuing pure discount bonds:

5-6

5.2 How to Value Bonds

• Identify the size and timing of cash flows. • Discount at the correct discount rate.

– If you know the price of a bond and the size and timing of cash flows, the yield to maturity is the discount rate.

– Time to maturity (T) = Maturity date - today’s date – Face value (F) – Discount rate (r)

$0

0

$0

$0

T 1

$F

T

1

2

Present value of a pure discount bond at time 0:

• To value bonds and stocks we need to:

– Estimate future cash flows:

• Size (how much)ຫໍສະໝຸດ and • Timing (when)

– Discount future cash flows at an appropriate rate:

公司理财原版英文课件Chap020

There are two methods for selecting an underwriter

Competitive Negotiated

20-9

Firm Commitment Underwriting

The issuing firm sells the entire issue to the underwriting syndicate. The syndicate then resells the issue to the public. The underwriter makes money on the spread between the price paid to the issuer and the price received from investors when the stock is sold. The syndicate bears the risk of not being able to sell the entire issue for more than the cost. This is the most common type of underwriting in the United States.

公司理财(罗斯)第15章(英文

Multinational company capital budget

01

Foreign Project Evaluation

02

Capital Budgeting Decision

Capital Structure Decision

03

04

Divided Policy Decision

Foreign exchange risk management

Corporate Finance (Ross) Chapter 15

目录

• Introduction • Capital Structure and Cost of Capital • Financial stress and financial crisis • Finance of multinational

Bankruptcy or reception

In extreme cases, bankruptcy or reception may be necessary to resolve financial conflicts

Hale Waihona Puke Finance of04 multinational corporations

Master the analysis methods and influencing factors of capital structure decision-making.

Understand the impact of capital structure adjustment on enterprise value and financial condition.

Capital Structure of Multinational Corporations

{财务管理公司理财}公司理财经典讲义英文版

of the Firm

The Capital Structure Decision

Current

Current Assets

Liabilities

How can the firm

raise the money Fixed Assets for the required

Long-Term Debt

1 Tangible investments?

investments?

McGraw-Hill/Irwin

© 2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

1-4

The Balance-Sheet Model

of the Firm

Total Value of Assets:

Total Firm Value to Investors:

Current

Current Assets

Liabilities Long-Term

Debt

Fixed Assets

1 Tangible

2 Intangible

McGraw-Hill/Irwin

Shareholders’ Equity

© 2005 The McGraw-Hill Companies, Inc. All Rights Reserved.

2750%50%30% DebtDeEbtquity

5705%

Equity

McGraw-Hill/Irwin

If how you slice the pie affects the size of the pie, then the capital structure decision matters.

公司理财课件英文版(ppt 25)

Net Present Value

• The Net Present Value (NPV) of an investment is the present value of the expected cash flows,

less the cost of the investment.

Back to Example 1:

2.1 Net Present Value : FV and PV

• The amount that a borrower would need to set aside today to to able to meet the promised payment of $10,000 in one year is call the Present Value (PV) of $10,000. Note that $10,000 = $9,523.81×(1.05).

$9,500 elsewhere at 5-percent, our FV would be less

than the $10,000 that investment promised and we

would be unambiguously worse off in FV terms as

well: $9,500×(1.05) = $9,975 < $10,000.

PV= CF1 CF2 CF3 1 r (1 r)2 (1 r)3

NPV=

CF0

CF1 1 r

CF2 (1 r)2

CF3 (1 r)3

= CF0 PV

Fisher’s Separation Principle

Given perfect capital market and certainty, the optimal investment plan is the one that maximizes the net present value of available production plans, without regard to the individuals’ subjective preferences that enter into their consumption/saving decisions. (Irving Fisher)

公司理财英文版

11.1 Individual Securities

Key Terms expected return 期望报酬率 variance 方差 standard deviation 标准差 covariance 协方差 correlation 相关性 beta coefficient 系数

Chapter Outline

11.1 Individual Securities 11.2 Expected Return, Variance, and Covariance 11.3 The Return and Risk for Portfolios 11.4 The Efficient Set 11.5 Riskless Borrowing and Lending 11.6 Announcements, Surprises, and Expected Return 11.7 Risk: Systematic and Unsystematic 11.8 Diversification and Portfolio Risk 11.9 Market Equilibrium 11.10 Relationship between Risk and Expected Return (CAPM)

odd

来自Stange, unusual Seperated from a part or set to which it belongs to eg. two odd socks That can’t be divided exactly by 2 Not happening regularly eg. He likes the odd drinks.

Return and Risk: The Capital Asset Pricing Model (CAPM)

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Estimating Cash Flows

Cash Flow from Operations

Recall that: OCF = EBIT – Taxes + Depreciation

Net Capital Spending

Don’t forget salvage value (after tax, of course).

Changes in Net Working Capital

Be able to compute depreciation expense for tax purposes

Incorporate inflation into capital budgeting Understand the various methods for computing

operating cash flow Apply the Equivalent Annual Cost approach

Chapter 8

Making Capital Investment Decisions

Key Concepts and Skills

Understand how to determine the relevant cash flows for various types of capital investments

80.00 48.00 28.80 17.28 5.76

(4) Opportunity cost (warehouse)

–150.00

150.00

(5) Net working capital

10.00 10.00 16.32 24.97 21.22

0

(end of year)

(6) Change in net working capital

Incremental Cash Flows

Sunk costs are not relevant

Just because “we have come this far” does not mean that we should continue to throw good money after bad.

The Baldwin Company

Income: (8) Sales Revenues (9) Operating costs

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

100.00 163.20 249.72 212.20 129.90 50.00 88.00 145.20 133.10 87.84

Recall that when the project winds down, we enjoy a return of net working capital.

Interest Expense

Later chapters will deal with the impact that the amount of debt that a firm has in its capital structure has on firm value.

–10.00

–6.32 –8.65 3.75 21.22

(7) Total cash flow of

–260.00

–6.32 –8.65 3.75 192.98

investment

[(1) + (4) + (6)]

At the end of the project, the warehouse is unencumbered, so we can sell it if we want to.

cash flows. Inflation matters.

Cash Flows—Not Accounting

Consider depreciation expense.

You never write a check made out to “depreciation.”

Much of the work in evaluating a project lies in taking accounting numbers and generating cash flows.

Opportunity costs do matter. Just because a project has a positive NPV, that does not mean that it should also have automatic acceptance. Specifically, if another project with a higher NPV would have to be passed up, then we should not proceed.

Equivalent Annual Cost Method

8.1 Incremental Cash Flows

Cash flows matter—not accounting earnings. Sunk costs don’t matter. Incremental cash flows matter. Opportunity costs matter. Side effects like cannibalism and erosion matter. Taxes matter: we want incremental after-tax

80.00 48.00 28.80 17.28

(4) Opportunity cost (warehouse)

–150.00

(5) Net working capital (end of year)

10.00 10.00 16.32 24.97 21.22

(6) Change in net working capital

For now, it’s enough to assume that the firm’s level of debt (and, hence, interest expense) is independent of the project at hand.

8.2 The Baldwin Company

Chapter Outline

8.1 Incremental Cash Flows 8.2 The Baldwin Company: An Example 8.3 Inflation and Capital Budgeting 8.4 Alternative Definitions of Cash Flow 8.5 Investments of Unequal Lives: The

Again, production (in units) by year during 5-year life of the machine is given by:

(5,000, 8,000, 12,000, 10,000, 6,000). Production costs during the first year (per unit) are $10, and they increase 10% per year thereafter. Production costs in year 2 = 8,000×[$10×(1.10)1] = $88,000

(5,000, 8,000, 12,000, 10,000, 6,000).

Price during the first year is $20 and increases 2% per year thereafter. Sales revenue in year 3 = 12,000×[$20×(1.02)2] = 12,000×$20.81 = $249,720.

Incremental Cash Flows

Side effects matter.

Erosion and cannibalism are both bad things. If our new product causes existing customers to demand less of current products, we need to recognize that.

–10.00

–6.32 –8.65 3.75

(7) Total cash flow of investment [(1) + (4) + (6)]

–260.00

–6.32 –8.65 3.75

Year 5 21.76* 94.24 5.76

150.00 0

21.22 192.98

The Baldwin Company

Increase in net working capital: $10,000

Production (in units) by year during 5-year life of the machine: 5,000, 8,000, 12,000, 10,000, 6,000

The Baldwin Company

Annual inflation rate: 5% Working Capital: initial $10,000 changes with

sales

The Baldwin Company

($ thousands) (All cash flows occur at the end of the year.)

Costs of test marketing (already spent): $250,000