现金流量表及其分析研究文献翻译

现金流量表及其分析研究文献综述

潘建文(2010)指出现金流量表是反映企业在一定会计期间现金和现金等价物流入和流出的报表。从编制原则上看,现金流量表按照收付实现制原则编制, 将权责发生制下的盈利信息调整为收付实现制下的现金流量信息,便于信息使用者了解企业净利润的质量。通过现金流量表,并结合其他主要财报,使用者能够了解现金流量的影响因素,评价企业的支付能力、偿债能力和周转能力,预测企业未来现金流量。在现金流量表中,现金及现金等价物被视为一个整体,企业现金形式的转换并不会产生现金的流入或流出。根据企业业务活动的性质和现金流量的来源, 现金流量表从结构上将企业一定期间产生的现金流量分为经营活动产生的现金流量、投资活动产生的现金流量和筹资活动产生的现金流量。

三、国内学者在资同会有不同的影响

现金流量表的编制基础由现金和现金等价物构成。对现金的定义一般不会产生异议,但对现金等价物的定义各国分歧较大。而我国的会计准则对现金和现金等价物的规定是:企业持有的期限短、流动性强、易于转换为已知金额现金、价值变动风险很小的投资。同时符合以上四个条件的为现金及现金等价物,但是我国准则只对期限做出了规定,对后面三项没有做出规定。这就导致了企业在判断时难免出现主观臆断性,影响报表的质量。

美国哈佛大学教授帕利普(2004)在其《企业分析与评价》一书中,对杜邦财务分析体系进行了变形、补充而发展起来的财务体系称为“帕利普财务分析体系”。将财务分析体系中的常用的财务比率一般被分为四大类:偿债能力比率、盈利比率、资产管理效率比率、现金流量比率。帕利普财务分析的原理是将某一个要分析的指标层层展开,这样便可探究财务指标发生变化的根本原因。这种分析方法在原有基础上考虑了股利支付率这一因素,但是并未取得突破性进展。

王玉晶(2006)指出可以将由现金流量表计算一些指标与由资产负债表和利润分配表计算出的一些指标进行比较分析,以便更加客观的评价企业在一定期间财务信息。以期更好地实现利用现金流量表提供的信息全面了解企业一定时期财务状况的目的。

现金流量报表分析外文翻译文献

现金流量报表分析外文翻译文献(文档含中英文对照即英文原文和中文翻译)Quantitative Analysis of the Target Related to Cash Flow StatementWith the example of the trend analysis method applied to the cash flow statement, the authors study the quantitative analysis method of the target related to cash flow statement. So the statement user can knows the current and previous financial condition in the enterprises, correctly evaluate the current and future abilities to pay and repay, find out the problems in financial affairs, and scientifically calculate the future financial conditions. An adequate, efficient basis is provided for scientific decision.1 IntroductionIt was America that first decided to replace statement of changes in financial position with cash flow statement. Afterwards, U.K., Australia, Canada and many other countries and areas followed. To emphasize cash flow statement and overcome the shortcomings of statement of changes in financial position, in January, 1987, FASB in America promulgated financial accounting standards announcement No. 95《Cash Flow Statement》.It requires enterprise to replace the statement of changes in financial position with cash flow statement from July 1988. In September, 1991, British Accounting Standard Board announced financial statement standard No.l 《Cash Flow Statement》too, demands all enterprises.Concerned with the requirements should prepare cash flow statement. In 1992, International Accounting Standard Board announced 《lnternational Accounting Standards No.l》,required to replace statement of changes in financial position with cash flow statement. So now "cash flow statement", "equity-debt statement", and "profit and loss statement" have preliminarily formed the new system of financial accounting statement in enterprise on the worldwide scale.2 Cash Flow Statement2.1 Contents of Cash Flow Statement and Its Compilation PurposeCash flow statement means statement of changes in financial position compiled based on cash and shows operating activities, investment activities and collecting capital activities of the enterprise on account of flow-in and flow-out of cash during a certain period, and shows allaspects of flow-in and flow-out of cash. It is compiled on the cash basis of accounting and belongs to periodic dynamic statement. The basic purpose of compiling cash flow statement is to provide the information of flow-in and flow-out of cash during a current accounting period to shareholders, creditors and other users of the statement to help them correctly make assessment of: ·The Capability of obtaining net cash flow during the future accounting period;·The Capability of repay debts and paying dividend;·The Capability of raising funds;.The reason for engendering the difference of net income and net cash flow; and,·Investment and raising funds activities affecting and not affecting cash during the current period.2.2 Components of Cash Flow(1) Cash flow-inThere are three chief types of economic services flow-in of cash: Reducing other assets except cash adding debts and adding shareholder's right.(2) Cash flow- outThere are three chief types of economic services flow-out of cash: Adding other assets except cash, reducing debts and reducing shareholder's right.2.3 Classification of Cash FlowCash flow within a certain period is classified into the following three types on account of the nature of operation service:The cash flow of operation activities, the cash flow of investment activities and the cash flow of raising funds activities.(1) Cash flow ofoperation activitiesOperation activities mean the main service of an enterprise and other non-investment activities or raising funds activities. It includes:Cash flow-in of operation activities:The input of selling goods and providing labour force; the input of loan interest, stock dividend and bond interest; other input of not belonging to investment activities and raising funds activities.Cash flow-out of operation activities:The cash of paying to suppliers and providers of labour force; the expenditure of salary; theinterest to creditor; the expenditure of tax on income and penalty.(2) Cash flow of investment activitiesInvestment activities mean purchase and selling of long-term asset and other investments without the cape of cash equivalent. It includes:Cash flow-in of investment activities: recovering loan; selling stocks and bonds issued by other companies; selling fixed assets and other productive assets.Cash flow-out of investment activities: providing loan to other enterprises; purchasing stocks and bonds issued by other companies; purchasing fixed assets and other productive assets (including capitalized interest of asset cost).(3) Cash flow of raising funds activitiesRaising funds activities mean the activities to cause the scale and structure of rights and interest capital and other loan to change. It includes:Cash flow-in of investment activities: issuing stocks., bonds and bill; gaining mortgage loans and all kinds of other long-term and short-term loans.Cash flow-out of investment activities: issuing stock interest in cash; repaying loans; preceding expenditure to creditor (including cash expenditure caused by extended long-term debt).2.4 Structure of Cash Flow StatementThere are two methods to compile cash flow statement: direct method and indirect method. The structure of cash flow statement compiled by the two methods is different. This article recommends the basic structure of cash flow Statement compiled by direct method and usually adopted by enterprises. The basic structure of cash flow statement is composed of three parts: Cash flow of operation activities. The data needed by this part may be found in B/S (balance sheet) and income sheet.Cash flow of investment activities. The information needed by this part may be found from the change of current asset account, but the true data need to be adjusted on account of income or loss in income sheet.Cash flow of raising funds activities which may be obtained by analyzing and computing the change of relevant current liability and shareholder's rights and interests account.Non-cash investment and raising funds activities which may be discovered in the supplementary statements to show all aspects of important economic activities.2.5 Compilation of Cash Flow StatementThe information that is needed for compiling cash flow statement includes: beginning balance sheet, final trial balance, other complementary data,etc. Cash flow statement is compiled on account of the original manuscript.3 Quantitative Analysis of Relevant QuotaQuantitative analysis of cash flow statement is to compare, analyze and study relevant data of cash flow statement so as to know the financial position of enterprise, find out the trouble in finance, predict the future financial position and provide the basis for scientific decision.The methods of quantitative analysis of cash flow statement usually include trend analysis, structure analysis, rate analysis, comparative analysis and factor analysis. This article only recommends trend analysis applied to cash flow statement.Trend analysis is an analysis method which forecasts future results by studying a number of continual periods''- financial statement, comparing relevant program's amount of money and analyzing the increase and decrease of some quotas to judge its trend. Applying trend analysis, the user of statement may know the basic trend of relevant program changes, judge whether this trend is advantageous or not and predict the future development of the enterprise.Trend analysis usually computes trend percentages. There are two types of trend percentages:It is illustrated by the cash flow statement of some telecommunication bureau. We compile cash flow statement gathered from 1995 to 1998 of this bureau on account of cash flow statements from 1995 to 1998 of this bureau (statement from 1995 to 1998 omitted). The form of cash flow statement and the data of this bureau in 1998 are shown as in Table 1:Table 1 Cash flow statement of a telecommunication bureau Enterprise:Year:1998 Unit: Thousands of dollars Cash flow Amount1 Cash flow of operationCash flow in:Cash from sales clients 85890Other operation income (12019)Sub-total -f cash flow in 73871Cash flow out:Paying suppliers (40 871)Paying interests (1 287)Paying other expenses (19 585)Paying income tax (2 546)Sub-total of cash flow out (25 119)Net cash of operation 48 7522 Cash flow of investmentCash flow in:Recovery of cash from investment 68 000Recovery of cash relate to 18 500investment activitiesSub-total of cash flow in 86 500Cash flow out:Equipment purchasing (66 676)Sub- total of cash flow out (66 676)Net cash of investment 19 8243 Cash flow of raising fundsCash flow in:Cash from loan 36 220Cash accepting rights and interests 15 081Sub-total of cash flow in 51 301Cash flow out:Cash repayed for debts (16 254)Sub- total of cash flow out (16 254)Net cash of raising funds 35 0474 Effects of exchange fluctuations on cash5 Net increased cash flow 103 623The article only cites the data from 1995 to 1998 to compute the trend percentage by the trend analysis method.Table 2 The total cash flow statementEnterprise: Unit: Thousands of dollars Cash flow 1995 1996 1997 1998 Cash income 187 500 203 136 207 752 211 672 Among: cash m- 68 465 70 125 71 532 73 871 come of operationCash income of 40 680 65 421 76 345 86 500 investmentCash income of 78 355 67 590 59 875 51 301 raising fundsCash expenditure 62 233 79 765 91 815 108 049 including:Cash expenditure 15 908 19 880 22 905 25 119 of operationCash expenditure 32 905 40 895 54 690 66 676 of investmentCash expenditure 13 420 18 990 14 220 16 254Of raising fundsThe data come from the annual accountant statements from 1995 to 1997(omitted).We can compute the constant relative with the year- of 1995 as the base period, see Table 3, and Link relative with previous year as the base period, see Table 4, on account of the total cash flow statement from 1995 to 1998 of this telecommunication bureau.From Table 3, we can conclude that cash flow of the enterprise continuously increases. Cash flow in 1998 was 12.89 percent more than that in 1995,among which the increase of cash income of operation activities was faster than that of general cash income and was 7.90 percent. Cash income of investment activities increases doubly and up to 112.64 percent, which showsthe previous investment gradually expires and then cash income of investment activities increases; but cash income of raising funds activities doesn't increase, on the contrary, 34.53 percent less than that in 1995, which shows the dependence on raising funds gradually reduces. Cash expenditure also gradually increases and cash expenditure in 1998 was 73.62 percent more than that in 1995, among which cash expenditure of investment activities increased by 57.90 percent, which is slower than the general cash flow. Cash expenditure of investment activities increased by 102.63 percent, which shows cash expenditure of investment activities in 1998 was double that in 1995 and the enterprise strengthens investment. Cash expenditure of raising funds activities has increased by 21.09 percent, which shows a huge amount of loans still don't expire or the enterprise does not issue dividends (or distribute interests) to investors.Table 3 Comparison of constant relative index_______________________________________________________________________________ Cash flow 1995 1996 1997 1998(percent) (percent) (percent) (percent) Cash income 100 108.34 110.80 112.89Among: cash incomeof operation 100 102.42 104.48 107.90Cash income ofInvestment 100 160.82 187.67 212.64Cash income ofraising funds 100 86.26 76.42 65.47Cash expenditureincluding: 100 128.17 147.53 173.62Cash expenditure ofOperation 100 124.97 143.98 157.90 Cash expenditure ofInvestment 100 124.28 166.21 202.63 Cash expenditure ofraising funds 100 141.51 105.96 121.09_______________________________________________________________________________Table 4 Comparison of link-relative quota_______________________________________________________________________________ Cash flow 1995 1996 1997 1998(percent) (percent) (percent) (percent) Cash income 100 108.34 102.27 101.89 Cash income ofOperation 100 102.42 102.01 103.27 Cash income ofVestment 100 160.82 116.70 113.30 Cash income ofraising funds 100 86.26 88.59 85.68 Cash expenditure 100 128.17 115.11 117.68 Cash expenditure ofoperation 100 124.97 115.22 109.67 Cash expenditure ofInvestment 100 124.28 133.73 121.92 cash expenditure ofraising funds 100 141.51 74.88 114.30From Table 4, we can conclude not only cash income of enterprise increases continuously, but also its increase speed increases progressively. The increase speed of cash income ofoperation activities and investment activities basically reduce progressively, but cash income of raising funds activities shows a negative increase. Cash expenditure of enterprise also increases progressively, whose speed is basically smooth and steady. Cash expenditure of operationactivities reduces progressively, the increase speed of cash expenditure of investment activities in 1997 was higher than that in 1996. But that in 1998 was lower than that in 1997. Cash expenditure of raising funds activities in 1997 cut down faster than in 1996, but that in 1998 rose again after a fall.4 Trend Forecast AnalysisThe so-called trend forecast analysis means to use regression analysis method, exponential smooth method and so on to analyze and forecast the statement of financial data, analyze its development trend, and this possible development result on this basis.Trend Analysis also includes trend forecast analysis usually with trend linear equation applies.The equation is: y=a+bxWhere a and b are constant, and x is the period coefficient value which is decided by distribution and made ∑x=0 .For ∑ x=0,the distribution value makes little difference whether the number of the period is odd or even.When the number of the period is odd, x may be decided as follows:_______________________________________________________________________________ 1990 1991 1992 1993 1994 x= -2 -1 0 1 2When the number of the period is even, x may be decided as follow:_______________________________________________________________________________ 79 80 81 82 83 84 85 86 87 88 x = -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 _______________________________________________________________________________ 89 90 91 92 93 94 95 96 97 98 x = +1 +2 +3 +4 +5 +6 +7 +8 +9 +10The constants a and b may be decided by following formula:2n xy b n x =∑∑ y a n =∑The data are obtained from accountant statements from 1979 to 1998 of the telecommunication bureau (accountant statements from 1979 to 1994 omitted).Cash income of operation activities of a telecommunication bureau:Unit: Thousands of dollars Cash flow 1979 1980 1981 1982 1983Cash income ofoperation activities 26 000 28 753 29 875 31 080 35 780Unit: Thousands of dollars Cash flow 1984 1985 1986 1987 1988Cash income ofoperation activities 43123 45 389 47 100 48 200 49 318Unit: Thousands of dollarsCash flow 1989 1990 1991 1992 1993 Cash income ofoperation activities 50 897 52 310 55 432 58 765 60 581Unit: Thousands of dollarsCash flow 1994 1995 1996 1997 1998 Cash income ofoperation activities 65 300 68 465 70 125 71 532 73 871SO:y a n =∑=26 00028 75368 4657012571532738711011896202020++⋯++++= =50 594.8 Thousands of dollars 2n xyb n x =∑∑=()()()222220*10*260009*71 53210*73 871 1 800 12577020*[109910-+⋯++⎡⎤⎣⎦=-+-+⋯++ =2 337.82 Thousands of dollarsthen the forecast trend equation is:y =50 594.8+2 337.82xif the enterprise wants to forecast cash income of operation activities in 1999, then:y =50 594.8+2 337.82*11=76 310.82 Thousands of dollars5 ConclusionBy quantitative analysis of cash flow statement, we can conclude the trend analysis is an analysis method which forecasts the future result by studying a number of continual periods' financial statements, comparing the amount of relevant programs and analyzing the increase and decrease of some quotas to judge its trend. Applying trend analysis, the user of statement may know the basic trend of relevant program changes, judge whether this trend is advantageous or not and predict the future development of the enterprise.Joe Johnson and Larry Brown 1999. “Analysis of cash flow statement” the cap journal; October译文:对现金流量报表相关目标的量化分析本文以适用于现金流量表的趋势的分析方法为例子,通过用定量分析法研究与现金流量表相关的目标。

现金流量表分析的研究毕业论文

现金流量表分析的研究摘要现金流量表是企业在一定会计期间现金和现金等价物流入和流出的报表。

它是财务报表的三个基本报告之一,所表达的是在一固定期间(通常是每季或每年)内,一家企业或机构的现金(包含银行存款) 增减变动的情况。

本文首先讲述现金流量表分析的目的是为了准确地揭示出现金流量表所包含的会计信息,这些会计信息有助于会计信息使用者正确地进行决策。

在此基础上说明通过具体的分析方法,分析者能够从现金流量表中得到的有用信息。

同时应用现金流量表进行分析并不是完美的,有其局限性。

必须针对其弊端进行分析、解决。

从而最大限度的提取相关信息进行分析,为决策者提供有力依据。

关键词现金流量表分析方法局限性解决方法AbstractCash flow statement should reflect the inflows and outflows of cash and cash equivalents reports in a certain accounting period of the business. It is the report of the three basic financial statements. It expresses the cash of a company or institution (usually quarterly or annually) in a fixed period and changes in this accounting circumstance (including bank deposits),This paper discusses the cash flow analysis aims to reveal accurate accounting information which contained in the cash flow statement,this accounting information can help users of accounting information to decision-making right. On this basics,some analysis get from the cash flow of useful information by this specify method and apply to analyze the cash flow statement. This method is not perfect,it has its limitations. We must pay attention to its shortcomings,and finda way to resolve it. We should maximize the extraction of relevant information and provide a strong basis for policy-makers.Key Words cash flow statement analysis method shortcoming resolve method目录摘要ABSTRACT一、现金流量表分析的内容和目的 (1)(一)现金流量表分析的内容 (1)(二)现金流量表分析的目的 (2)二、现金流量表分析的方法 (3)(一)现金流量表的趋势分析 (3)(二)现金流量表的结构分析 (4)(三)现金流量表的指标分析 (5)三、现金流量表进行财务分析时的局限性 (9)(一)从现金流量表的编制基础分析 (10)(二)从现金流量表信息的时效性和可比性以及可靠性分析 (10)(三)从企业的生命周期来分析 (11)四、提高现金流量表分析效果的对策 (11)(一)结合资产负债表和利润表来分析企业的现金流量 (11)(二)结合过程和结果来分析现金流量的变化 (11)(三)结合纵向比较分析与横向比较分析整体分析现金流量的变化 (12)(四)从企业的生命周期来分析判断现金流量的合理性 (12)五、结语 (13)致谢 (14)参考文献 (15)附录 (16)现金流量表 (16)利润表 (20)资产负债表 (23)现金流量表分析的研究随着我国会计制度的国际化和企业治理结构向纵深发展,现金流量分析在企业管理中扮演着越来越重要的角色,企业经营者和财务管理人员也在不断的加强重视。

现金流量表分析报告研究背景范文

现金流量表分析报告研究背景范文英文回答:Background for Cash Flow Statement Analysis Report.The cash flow statement is a financial statement that summarizes the amount of cash and cash equivalents flowing into and out of a company over a specific period of time. It is one of the three main financial statements, along with the income statement and balance sheet. The cash flow statement can be used to assess a company's financial health, liquidity, and ability to generate cash.There are three main sections of the cash flow statement:Operating activities: This section includes cash inflows and outflows from the company's core business operations, such as sales, purchases, and expenses.Investing activities: This section includes cash inflows and outflows from the company's investments, such as the purchase and sale of property, plant, and equipment.Financing activities: This section includes cash inflows and outflows from the company's financing activities, such as the issuance of stock and debt, and the repayment of debt.The cash flow statement can be used to analyze a company's financial performance in a number of ways. For example, it can be used to:Assess a company's liquidity: The cash flow statement can be used to assess a company's ability to meet itsshort-term obligations. A company with a strong cash flow from operations is more likely to be able to meet its obligations than a company with a weak cash flow from operations.Evaluate a company's investment activities: The cash flow statement can be used to evaluate a company'sinvestment activities. A company that is investing heavily in its business is likely to have a negative cash flow from investing activities. However, this does not necessarily mean that the company is in financial trouble. If the company is investing in projects that are expected to generate a positive cash flow in the future, then the negative cash flow from investing activities may be a sign that the company is making sound investments.Analyze a company's financing activities: The cash flow statement can be used to analyze a company's financing activities. A company that is issuing a large amount of debt may be doing so to finance a major investment project. However, it is important to note that too much debt can lead to financial problems.The cash flow statement is a valuable tool for analyzing a company's financial performance. It can be used to assess a company's liquidity, evaluate its investment activities, and analyze its financing activities.中文回答:现金流量表分析报告研究背景。

企业财务状况评价外文文献及翻译

企业财务状况评价外文文献及翻译摘要本文通过对国内外财务状况评价相关外文文献的调研和翻译,总结了不同学者对企业财务状况评价的方法和指标,以及其对企业经营决策和风险管理的影响。

同时,还分析了现有文献中的研究局限,并提出了相应的进一步研究方向。

引言企业财务状况的评价在企业经营决策和风险管理中具有重要的作用。

随着全球经济的不断发展,企业财务状况评价的方法和指标也得到了不断的完善和更新。

本文旨在通过对国内外相关文献的调研和翻译,探讨企业财务状况评价的相关内容。

方法本文通过检索相关数据库和学术期刊,筛选了一批与企业财务状况评价相关的外文文献。

然后,进行了文献综述和内容翻译,并总结出其中的关键信息和研究成果。

结果1. 企业财务状况评价方法根据文献翻译和分析,目前学者们在企业财务状况评价方面主要采用以下方法:- 财务比率分析:通过对企业财务报表的比率分析,评估企业的偿债能力、盈利能力、运营效率等方面的状况。

- 资产负债表分析:通过对企业资产负债表的分析,揭示企业的资产结构、债务水平和净资产价值等方面的情况。

- 现金流量分析:通过对企业现金流量表的分析,探讨企业的现金流入流出情况以及可持续性问题。

- 经验判断和专家评估:通过对企业经营情况的判断和专家的评估,综合考虑多个因素对企业财务状况的影响。

2. 企业财务状况评价指标研究发现,在企业财务状况评价中,常用的指标包括:- 流动比率:反映企业短期偿债能力的指标。

- 速动比率:更加严格地评估企业短期偿债能力的指标。

- 盈利能力指标:如净利润率、毛利率等,用于评估企业的盈利水平。

- 储蓄比率:评估企业的盈利再投资能力的指标。

- 负债比率:反映企业债务水平和承担风险的指标。

3. 对企业经营决策和风险管理的影响学者们的研究表明,企业财务状况评价对企业经营决策和风险管理有重要影响。

合理评估企业财务状况可以帮助企业制定更加科学的经营决策,提高企业效益和竞争力。

同时,对企业财务状况的评价还可以帮助企业及时发现和应对潜在的经营风险,降低经营风险带来的不确定性。

中英文对照--现金流量表

现金流量表Cash Flows Statement拟制人:时间:单位: Prepared by: Period: Unit:项目Items1。

cash流量从经营活动: 1.Cash Flows from Operating Activities:01 )所收到的现金从销售货物或提供劳务01)Cash received from sales of goods or rendering of services02 )收到的租金02)Rental received增值税销售额收到退款的价值Value added tax on sales received and refunds of value03 )增值税缴纳03)added tax paid04 )退回的其他税收和征费以外的增值税04)Refund of other taxes and levy other than value added tax07 )其他现金收到有关经营活动07)Other cash received relating to operating activities08 )分,总现金流入量08)Sub—total of cash inflows09 )用现金支付的商品和服务09)Cash paid for goods and services10 )用现金支付经营租赁10)Cash paid for operating leases11 )用现金支付,并代表员工11)Cash paid to and on behalf of employees12 )增值税购货支付12)Value added tax on purchases paid13 )所得税的缴纳13)Income tax paid14 )支付的税款以外的增值税和所得税14)Taxes paid other than value added tax and income tax17 )其他现金支付有关的经营活动17)Other cash paid relating to operating activities18 )分,总的现金流出18)Sub-total of cash outflows19 )净经营活动的现金流量19)Net cash flows from operating activities2。

现金流量表中英文版

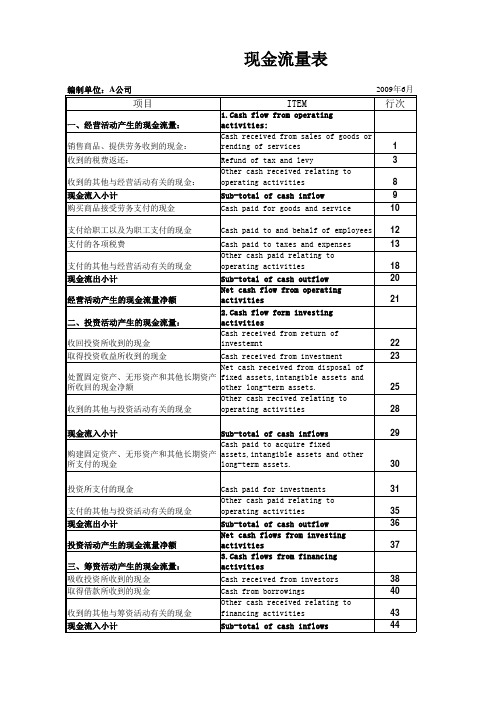

.现金流量表中英文版现金流量表(非金融类)CASH FLOW STATEMENT(Travel enterprise)会外年通03表编制单位:Name of enterprise: 单位:元项目ITEMS 行次金额一、经营活动产生的现金流量:CASH FLOWS FROM OPERATING ACTIVITIES 1销售商品、提供劳务收到的现金Cash received from sale of goods or rendering of services 2收到的税费返还Refund of tax and levies 3收到的其他与经营活动有关的现金Other cash received relating to operating activities 4现金流入小计Sub-total of cash inflows 5购买商品、接受劳务支付的现金Cash paid for goods and services 6支付给职工以及为职工支付的现金Cash paid to and on behalf of employees 7支付的各项税费Payments of all types of taxes 8支付的其他与经营活动有关的现金Other cash paid relating to operating activities 9现金流出小计Sub-total of cash outflows 10经营活动产生的现金流量净额Net cash flows from operating activities 11二、投资活动产生的现金流量:CASH FLOWS FROM INVESTING ACTIVITIES 12收回投资所收到的现金Cash received from disposal of investments 13取得投资收益所收到的现金Cash received from returns on investments 14处置固定资产、无形资产和其他长期资产所收回的现金净额NetCashReceivedFromDisposalOfFixedAssets,IntangibleAssets&OtherLong-termAssets 15收到的其他与投资活动有关的现金Other cash received relating to investing activities 16现金流入小计Sub-total of cash inflows 17购建固定资产、无形资产和其他长期资产所支付的现金Cash paid to acquire fixed assets,intangible assets & other long-term assets 18投资所支付的现金Cash paid to acquire investments 19支付的其他与投资活动有关的现金Other cash payments relating to investing activities 20现金流出小计Sub-total of cash outflows 21投资活动产生的现金流量净额Net cash flows from investing activities 22三、筹资活动产生的现金流量:CASH FLOWS FROM FINANCING ACTIVITIES 23吸收投资所收到的现金Cash received from capital contribution 24借款所收到的现金Cash received from borrowings 25收到的其他与筹资活动有关的现金Other cash received relating to financing activities 26现金流入小计Sub-total of cash inflows 27偿还债务所支付的现金Cash repayments of amounts borrowed 28分配股利、利润和偿付利息所支付的现金Cash payments for interest expenses and distribution of dividends or profit 29支付的其他与筹资活动有关的现金Other cash payments relating to financing activites 30现金流出小计Sub-total of cash outflows 31筹资活动产生的现金流量净额Net cash flows from financing activities 32四、汇率变动对现金的影响EFFECT OF FOREIGN EXCHANGE RATE CHANGES ON CASH 33五、现金及现金等价物净增加额NET INCREASE/(DECREASE) IN CASH AND CASH EQUIVALENTS 34.(续表)现金流量表(非金融类)CASH FLOW STATEMENT(Travel enterprise)会外年通03表编制单位:Name of enterprise: 单位:元补充资料351.将净利润调节为经营活动现金流量:Reconciliation of net profit/(loss)to cash flows from oprating activities 36净利润Net profit 37加:*少数股东权益Add:Minority interest 38减:未确认的投资损失Less:Uncertained investment loss 39加:计提的资产损失准备Add:Provision for asset impairment 40固定资产折旧Depreciation of fixed assets 41无形资产摊销Amortisation of intangible assets 42长期待摊费用摊销Amortisation of long-term prepaid expenses 43待摊费用减少(减:增加) Decrease in prepaid expenses(deduct:increase) 44预提费用增加(减:减少) Increase in prepaid expenses(deduct:decrease) 45处置固定资产、无形资产和其他长期资产的损失(减:收益) LossesOnDisposalOfFixedAssetsIntangibleAssetsAndOtherLong-termAssets'DeductGains 46固定资产报废损失Losses on disposal of fixed assets 47财务费用Financial expenses 48投资损失(减:收益) Losses arising from investments(deduct:gains) 49递延税款贷项(减:借项) Deferred tax credit(deduct: debit) 50存货的减少(减:增加) Decrease in inventories(deduct:increase) 51经营性应收项目的减少(减:增加) Decrease in operating receivables(deduct:increase) 52经营性应付项目的增加(减:减少) Increare in operating payables(deduct:decrease) 53其他Others 54经营活动产生的现金流量净额Net cash flows from operating activities 552.不涉及现金收支的投资和筹资活动:Investing and financing activities that do not involve cash receipts and payment 56债务转为资本Conversion of debt into captical 57一年内到期的可转换公司债券ReclassificationOfConvertibleBondsExpiringWithinOneYearAsCurrentLiability 58融资租入固定资产Fixed assets acquired under finance leases 59其他Other 6061623.现金及现金等价物净增加情况:Net increase/(decrease) in cash and cash equivalents 63现金的期末余额Cash at end of year 64减:现金的期初余额Less: Cash at beginning of year 65加:现金等价物的期末余额Plus:Cash equivalents at end of year 66减:现金等价物的期初余额Less:Cash equivalents at beginning of year 67现金及现金等价物净增加额Net increase/(decrease) incash and cash equivalents 68。

基础知识——现金流量表中英文对照

基础知识——现金流量表中英文对照基础知识——现金流量表中英文对照现金流量表中英文对照一、经营活动产生的现金流量1. Cash Flow from Operating Activities销售商品、提供劳务收到的现金Cash from selling commodities or offering labor收到的税费返还Refund of tax and fee received收到的其它与经营活动有关的现金Other cash received related to operating activities现金流入小计Cash InflowSubtotal购买商品、接受劳务支付的现金Cash paid for commodities or labor支付给职工以及为职工支付的现金Cash paid to and for employees支付的各项税费Taxes and fees paid支付的其它与经营活动有关的现金Other cash paid related to operating activities现金流出小计Cash OutflowSubtotal经营活动产生的现金流量净额Cash flow generated from operating activitiesNet Amount二、投资活动产生的现金流量2. Cash Flow from Investing Activities收回投资所收到的现金Cash from investment withdrawal取得投资收益所收到的现金Cash from investment income处置固定资产、无形资产和其他长期资产所收回的现金净额Net cash from disposing fixed assets,intangible assets and other long-term ass收到的其它与投资活动有关的现金Other cash received related to investing activities现金流入小计Cash InflowSubtotal购建固定资产、无形资产和其他长期资产所支付的现金Cash paid for buying fixed assets,intangible assets and other long-term investm投资所支付的现金Cash paid for investment支付的其他与投资活动有关的现金Other cash paid related to investing activities现金流出小计Cash OutflowSubtotal投资活动产生的现金流量净额Cash flow generated from investing activitiesNet Amount三、筹资活动产生的现金流量3. Cash Flow from Financing Activities吸收投资所收到的现金Cash received from accepting investment借款所收到的现金Borrowings收到的其它与筹资活动有关的现金Other cash received related to financing activities现金流入小计Cash InflowSubtotal偿还债务所支付的现金Cash paid for debt分配股利、利润或偿付利息所支付的现金Cash paid for dividend ,profit or interest支付的其它与筹资活动有关的现金Other cash paid related to financing activities现金流出小计Cash OutflowSubtotal筹资活动产生的现金流量净额Cash flow from financing activitiesNet Amount四、汇率变动对现金的影响4. Foreign Currency Translation Gains(Losses)五、现金及现金等价物净增加额5. Net Increase Of Cash and Cash Equivalents补充资料:Supplementary Schedule:现金流量附表项目Indirect Method1、将净利润调节为经营活动现金流量1. Convert net profit to cash flow from operating activities 净利润Net profit计提的资产减值准备Provision for asset losses固定资产折旧Depreciation for fixed assets无形资产摊销Amortization of intangible assets长期待摊费用摊销Amortization of long-term deferred expenses待摊费用减少Decrease of deferred expenses预提费用增加Increase of accrued expenses处理固定资产、无形资产和其他长期资产的损失loss of disposing fixed assets,intangible assets and other long-term assets固定资产报废损失Scrap loss of fixed assets财务费用Financial expenses投资损失Investment losses递延税款贷项Deferred tax liabilities存货的减少Decrease of inventory经营性应收项目的减少Decrease of operation receivables经营性应付项目的增加Increase of operation payables其他Others经营活动产生的现金流量净额Net cash from operating activities2、不涉及现金收支的投资和筹资活动2. Investing and financing activities not involved in cash债务转为资本Debt converted to capital一年内到期的可转换公司债券Convertible bond maturity within one year融资租入固定资产Leasehold improvements3、现金及现金等价物净增加情况3. Net increase of cash and cash equivalents 现金的期末余额Cash ending bal.减:现金的期初余额Less:cash beginning bal.加:现金等价物的期末余额Plus:cash equivalents' ending bal.减:现金等价物的期初余额Less:cash equivalents' beginning bal.现金及现金等价物的净增加额Net increase of cash and cash equivalents 【。

现金流量表翻译

现金流量表翻译现金流量表翻译00Cash Flow Statement 经营活动产生的现金流量 cash flows from operating activities销售商品、提供劳务收到的现金 cash acquired from commodities sold and services provided收到的税费返还 refund of tax received收到的其它与经济活动有关的现金 other received cash relatingto operating activities现金流入小计 subtotal of cash inflows购买商品、接受劳务支付的现金 cash paid for commodities purchased or services provided支付给职工以及为职工支付的现金 cash paid to and for employees支付的各项税费 taxes paid支付的其他与经营活动有关的现金 other cash payments relatingto operating activities现金流出小计 subtotal of cash outflows经营活动产生的现金流量净额 net cash flow from operating activities投资活动产生的现金流量 cash flows from investing activities收回投资所收到的现金 cash received from withdrawal of investment取得投资收益所收到的现金 cash received from gain of investment revenue处置固定资产、无形资产和其他长期资产所收回的现金净额 ne cash receied from disposal of fixed assets, intangible asstes and other long-term assets收到的其他与投资活动有关的现金 cash received relating to other investment activities现金流入小计 subtotal of cash inflows购建固定资产、无形资产和其他长期资产所支付的现金 cash paidfor purchase of fixed assets, intangible assets and other long-term assets投资所支付的现金 cash paid for investment支付的其他与投资活动有关的现金 cash paid for other activities relating to investment activities现金流出小计 subtotal of cash outflows投资活动产生的现金流量净额 net cash flow from investment activities筹资活动产生的现金流量 cash flow from financing activities吸收投资所收到的现金 cash received by absorbing investment借款所收到的现金 cash acquired from borrowings收到的其他与筹资活动有关的现金 other cash acquired from financing activities现金流入小计 subtotal of sash inflows偿还债务所支付的现金 cash paid for debt redemption分配股利、利润或偿付利息所支付的现金 cash paid fordistribution of dividend and profit or payment of interest支付的其他与筹资活动有关的现金 oter cash paid relating to financing activities现金流出小计 subtotal of cash outflows筹资活动产生的现金流量净额 net cash flow from ffinancing activities汇率变动对现金的影响 effect of exchange rate changes on cash现金及现金等价物净增加额 net increment in cash and cash equivalents补充资料:supplementary materials将净利润调节为经营活动现金流量 convert net profit to cash flow for operating activities净利润 net profit加:计提的资产减值准备 add: impairment for asset accrued固定资产折旧 depreciation of fixed assets无形资产摊销 amortization of intangible assets长期待摊费用摊销 amortization of long-term deferred expenses待摊费用减少(减:增加)decrease of deferred expenses (less: increase)预提费用增加(减:减少)increase of accrued expenses (less: decrease)处置固定资产、无形资产和其他长期资产的损失(减:收益)loss from disposing fixed assets, intangible assets and other long-term assets (less: revenue)固定资产报废损失 loss on retirement of fixed assets财务费用 financial expenses投资损失(减:收益)investment losses (less: revenue)递延税款贷项(减:借款)deferred tax credit (less: loan)存货的减少(减:增加)decrease of inventory (less: increase)经营性应收项目的减少(减:增加)decrease of operation receivables (less: increase)经营性应付项目的增加(减:减少)increase of operation payables (less: decrease)其他 other经营活动产生的现金流量净额 net cash flow from operating activities不涉及现金收支的投资和筹资活动 investing and financing activities not involved in cash债务转为资本 debt converted to capital一年内到期的转换公司债券 convertible bond of company due within one year融资租入固定资产 fixed assets acquired under finance leases其他 other现金及现金等价物净增加情况 net increase of cash and cash equivalents现金的期末余额 ending balance of cash减:现金的期初余额 less: beginning balance of cash 加:现金等价物的期末余额 add: ending balance of cash equivalents减:现金等价物的期初余额 less: beginning balance of cash equivalents现金及现金等价物的净增加额 net increase of cash and cash equivalents。

现金流量表中英文版

现金流量表中英文版现金流量表(非金融类)CASH FLOW ST ATEMEN T(Travel enterprise)会外年通03表编制单位:Name o f enterprise: 单位:元项目ITEMS 行次金额一、经营活动产生的现金流量:CASH FLOWS FROM OPERATING ACTIVITIES 1销售商品、提供劳务收到的现金Cash received fro m sale of goods or rendering of services 2收到的税费返还Refund o f tax and levies 3收到的其他与经营活动有关的现金Other cash received relating to operating activities 4现金流入小计Sub-total of cash inflows 5购买商品、接受劳务支付的现金Cash paid for goods and services 6支付给职工以及为职工支付的现金Cash paid to and on behalf o f employees 7支付的各项税费Payments of all types of taxes 8支付的其他与经营活动有关的现金Other cash paid relating to operating activities 9现金流出小计Sub-total of cash outflows 10经营活动产生的现金流量净额Net cash flows fro m operating activities 11二、投资活动产生的现金流量:CASH FLOWS FROM INVESTING ACTIVITIES 12收回投资所收到的现金Cash received fro m disposal of investments 13取得投资收益所收到的现金Cash received fro m returns on investments 14处置固定资产、无形资产和其他长期资产所收回的现金净额NetCashReceivedFromDisposalOfFixedAssets,IntangibleAssets&OtherLong-termAssets 15收到的其他与投资活动有关的现金Other cash received relating to investing activities 16现金流入小计Sub-total of cash inflows 17购建固定资产、无形资产和其他长期资产所支付的现金Cash paid to acquire fixed assets,intangible assets & other long-term assets 18投资所支付的现金Cash paid to acquire investments 19支付的其他与投资活动有关的现金Other cash payments relating to investing activities 20现金流出小计Sub-total of cash outflows 21投资活动产生的现金流量净额Net cash flows fro m investing activities 22三、筹资活动产生的现金流量:CASH FLOWS FROM FINANCING ACTIVITIES 23吸收投资所收到的现金Cash received fro m capital contribution 24借款所收到的现金Cash received from borrowings 25收到的其他与筹资活动有关的现金Other cash received relating to financing activities 26现金流入小计Sub-total of cash inflows 27偿还债务所支付的现金Cash repay ments of amounts borrowed 28分配股利、利润和偿付利息所支付的现金Cash pay ments for interest expenses and distribution of dividends or profit 29支付的其他与筹资活动有关的现金Other cash payments relating to financing activites 30现金流出小计Sub-total of cash outflows 31筹资活动产生的现金流量净额Net cash flows fro m financing activities 32四、汇率变动对现金的影响EFFECT OF FOREIGN EXCHANGE RATE CHANGES ON CASH 33五、现金及现金等价物净增加额NET INCREASE/(DECREASE) IN CASH AND CASH EQUIV ALENTS 34(续表)现金流量表(非金融类)CASH FLOW ST ATEMEN T(Travel enterprise)会外年通03表编制单位:Name o f enterprise: 单位:元补充资料351.将净利润调节为经营活动现金流量:Reconciliation of net profit/(loss)to cash flows fro m oprating activities 36净利润Net profit 37加:*少数股东权益Add:Minority interest 38减:未确认的投资损失Less:Uncertained investment loss 39加:计提的资产损失准备Add:Provision for asset impairment 40固定资产折旧Depreciation of fi xed assets 41无形资产摊销A mortisation of intangible assets 42长期待摊费用摊销A mortisation of long-term prepaid expenses 43待摊费用减少(减:增加) Decrease in prepaid expenses(deduct:increase) 44预提费用增加(减:减少) Increase in prepaid expenses(deduct:decrease) 45处置固定资产、无形资产和其他长期资产的损失(减:收益) LossesOnDisposalOfFixedAssetsIntangibleAssetsAndOtherLong-termAssets'DeductGains 46固定资产报废损失Losses on disposal of fixed assets 47财务费用Financial expenses 48投资损失(减:收益) Losses arising fro m investments(deduct:gains) 49递延税款贷项(减:借项) Deferred tax credit(deduct: debit) 50存货的减少(减:增加) Decrease in inventories(deduct:increase) 51经营性应收项目的减少(减:增加) Decrease in operating receivables(deduct:increase) 52经营性应付项目的增加(减:减少) Increare in operating payables(deduct:decrease) 53其他Others 54经营活动产生的现金流量净额Net cash flows fro m operating activities 552.不涉及现金收支的投资和筹资活动:Investing and financing activities that do not involve cash receipts and payment 56债务转为资本Conversion of debt into captical 57一年内到期的可转换公司债券ReclassificationOfConvertibleBondsExpiringWithinOneYearAsCurrentLiability 58融资租入固定资产Fixed assets acquired under finance leases 59其他Other 6061623.现金及现金等价物净增加情况:Net increase/(decrease) in cash and cash equivalents 63现金的期末余额Cash at end o f year 64减:现金的期初余额Less: Cash at beginning of year 65加:现金等价物的期末余额Plus:Cash equivalents at end of year 66减:现金等价物的期初余额Less:Cash equivalents at beginning of year 67现金及现金等价物净增加额Net increase/(decrease) incash and cash equivalents 68文- 汉语汉字编辑词条文,wen,从玄从爻。

现金流量表中英文版

现金流量表中英文版现金流量表(非金融类)CASH FLOW ST ATEMEN T(Travel enterprise)会外年通03表编制单位:Name o f enterprise: 单位:元项目ITEMS 行次金额一、经营活动产生的现金流量:CASH FLOWS FROM OPERATING ACTIVITIES 1销售商品、提供劳务收到的现金Cash received fro m sale of goods or rendering of services 2收到的税费返还Refund o f tax and levies 3收到的其他与经营活动有关的现金Other cash received relating to operating activities 4现金流入小计Sub-total of cash inflows 5购买商品、接受劳务支付的现金Cash paid for goods and services 6支付给职工以及为职工支付的现金Cash paid to and on behalf o f employees 7支付的各项税费Payments of all types of taxes 8支付的其他与经营活动有关的现金Other cash paid relating to operating activities 9现金流出小计Sub-total of cash outflows 10经营活动产生的现金流量净额Net cash flows fro m operating activities 11二、投资活动产生的现金流量:CASH FLOWS FROM INVESTING ACTIVITIES 12收回投资所收到的现金Cash received fro m disposal of investments 13取得投资收益所收到的现金Cash received fro m returns on investments 14处置固定资产、无形资产和其他长期资产所收回的现金净额NetCashReceivedFromDisposalOfFixedAssets,IntangibleAssets&OtherLong-termAssets 15收到的其他与投资活动有关的现金Other cash received relating to investing activities 16现金流入小计Sub-total of cash inflows 17购建固定资产、无形资产和其他长期资产所支付的现金Cash paid to acquire fixed assets,intangible assets & other long-term assets 18投资所支付的现金Cash paid to acquire investments 19支付的其他与投资活动有关的现金Other cash payments relating to investing activities 20现金流出小计Sub-total of cash outflows 21投资活动产生的现金流量净额Net cash flows fro m investing activities 22三、筹资活动产生的现金流量:CASH FLOWS FROM FINANCING ACTIVITIES 23吸收投资所收到的现金Cash received fro m capital contribution 24借款所收到的现金Cash received from borrowings 25收到的其他与筹资活动有关的现金Other cash received relating to financing activities 26现金流入小计Sub-total of cash inflows 27偿还债务所支付的现金Cash repay ments of amounts borrowed 28分配股利、利润和偿付利息所支付的现金Cash pay ments for interest expenses and distribution of dividends or profit 29 支付的其他与筹资活动有关的现金Other cash payments relating to financing activites 30现金流出小计Sub-total of cash outflows 31筹资活动产生的现金流量净额Net cash flows fro m financing activities 32四、汇率变动对现金的影响EFFECT OF FOREIGN EXCHANGE RATE CHANGES ON CASH 33五、现金及现金等价物净增加额NET INCREASE/(DECREASE) IN CASH AND CASH EQUIV ALENTS 34(续表)现金流量表(非金融类)CASH FLOW ST ATEMEN T(Travel enterprise)会外年通03表编制单位:Name o f enterprise: 单位:元补充资料351.将净利润调节为经营活动现金流量:Reconciliation of net profit/(loss)to cash flows fro m oprating activities 36净利润Net profit 37加:*少数股东权益Add:Minority interest 38减:未确认的投资损失Less:Uncertained investment loss 39加:计提的资产损失准备Add:Provision for asset impairment 40固定资产折旧Depreciation of fi xed assets 41无形资产摊销A mortisation of intangible assets 42长期待摊费用摊销A mortisation of long-term prepaid expenses 43待摊费用减少(减:增加) Decrease in prepaid expenses(deduct:increase) 44预提费用增加(减:减少) Increase in prepaid expenses(deduct:decrease) 45处置固定资产、无形资产和其他长期资产的损失(减:收益)LossesOnDisposalOfFixedAssetsIntangibleAssetsAndOtherLong-termAssets'DeductGains 46固定资产报废损失Losses on disposal of fixed assets 47财务费用Financial expenses 48投资损失(减:收益) Losses arising fro m investments(deduct:gains) 49递延税款贷项(减:借项) Deferred tax credit(deduct: debit) 50存货的减少(减:增加) Decrease in inventories(deduct:increase) 51经营性应收项目的减少(减:增加) Decrease in operating receivables(deduct:increase) 52经营性应付项目的增加(减:减少) Increare in operating payables(deduct:decrease) 53其他Others 54经营活动产生的现金流量净额Net cash flows fro m operating activities 552.不涉及现金收支的投资和筹资活动:Investing and financing activities that do not involve cash receipts and payment 56债务转为资本Conversion of debt into captical 57一年内到期的可转换公司债券ReclassificationOfConvertibleBondsExpiringWithinOneYearAsCurrentLiability 58融资租入固定资产Fixed assets acquired under finance leases 59其他Other 6061623.现金及现金等价物净增加情况:Net increase/(decrease) in cash and cash equivalents 63现金的期末余额Cash at end o f year 64减:现金的期初余额Less: Cash at beginning of year 65加:现金等价物的期末余额Plus:Cash equivalents at end of year 66 减:现金等价物的期初余额Less:Cash equivalents at beginning of year 67 现金及现金等价物净增加额Net increase/(decrease) incash and cash equivalents 68下面是诗情画意的句子欣赏,不需要的朋友可以编辑删除!!谢谢1. 染火枫林,琼壶歌月,长歌倚楼。

(完整word版)现金流量表分析与应用文献综述

河北科技师范学院本科毕业论文(设计)文献综述关于现金流量表应用分析院(系、部)名称:商务管理系专业名称:学生姓名:学生学号:指导教师:2012年1月13日河北科技师范学院教务处制摘要现金流量表是财务报表的三个基本报告之一,也称为账务状况变动表,现金流量表按收付实现制对企业当期的经营、投资、筹资活动进行计量,反映企业当期现金流入和流出情况,是对权责发生制下编制的资产负债表和利润表的补充,其中反映出大量关于企业经营状况的有价值的信息。

可以说掌握了现金流量表,就等于掌握了企业的财政命脉。

本文在研读相关文献的基础上,经过回顾与整理,归纳总结了国内相关主要研究成果,从现金流量表结构及内容、现金流量表反映的各项指标分析企业的财务状况,希望通过研究提炼出其中的各类主体决策相关的信息,供决策者参考。

关键词现金流量表;企业;财务状况AbstractThe statement of cash flows is one of the three basic financial statement, also known as the accounting statement, according to the cash basis of accounting of the enterprise current management, investment, financing activities cash flow meter measurement, reflect the current cash inflow and outflow of accrual basis, preparation of the balance sheet and income statement supplement, which reflects the large number of enterprises operating conditions of the valuable information. Based on the study of relevant literature, after reviewing and sorting, summarizes the related domestic research, analysis of the financial situation of enterprises from the index structure and the content of the statement of cash flows, cash flow statement to reflect, I hope through research to extract information of each class of the main decision—making related, for the reference of policy makers。

现金流量表中英文(cash flow statement)

22 23

Cash received from investment Net cash received from disposal of fixed assets,intangible assets and 处置固定资产、无形资产和其他长期资产所收回的现金净额 other long-term assets. Other cash recived relating to 收到的其他与投资活动有关的现金 operating activities 现金流入小计 Sub-total of cash inflows Cash paid to acquire fixed assets,intangible assets and other 购建固定资产、无形资产和其他长期资产所支付的现金 long-term assets. 投资所支付的现金 支付的其他与投资活动有关的现金 现金流出小计 投资活动产生的现金流量净额 三、筹资活动产生的现金流量: 吸收投资所收到的现金 取得借款所收到的现金 收到的其他与筹资活动有关的现金 现金流入小计 偿还债务所支付的现金 Cash paid for investments Other cash paid relating to operating activities Sub-total of cash outflow Net cash flows from investing activities 3.Cash flows from financing activities Cash received from investors Cash from borrowings Other cash received relating to financing activities Sub-total of cash inflows

现金流量表中英文对照表

现金流量表(CASH FLOW STATEMENT)项目一、经营活动产生的现金流量:ITEMS1、Cash flows from operating activities项目取得子公司及其他营业单位支付的现金净额ITEMSnet cash outflows of procurement of subsidiaries andother business units销售商品、提供劳务收到的现金收到的税费返还收到其他与经营活动有关的现金Cash received from sale of goods or rendering of支付其他与投资活动有关的现金servicesRefund of tax and levies 投资活动现金流出小计Other cash received relating to operating activities 投资活动产生的现金流量净额Other cash payments relating to investing activitiesCash inflow from investment activitiesNet cash flows from investing activities经营活动现金流入小计购买商品、接受劳务支付的现金支付给职工以及为职工支付的现金支付的各项税费Cash inflows from operating activitiesCash paid for goods and servicesCash paid to and on behalf of employeesPayments of all types of taxes三、筹资活动产生的现金流量:吸收投资收到的现金其中:子公司吸收少数股东投资收到的现金取得借款收到的现金3、Cash flows from financing activitiesCash received from capital contributionAmong:cash inflows from minority investment insubsidiariesCash received from borrowings支付其他与经营活动有关的现金Other cash paid relating to operating activities 收到其他与筹资活动有关的现金Other cash received relating to financing activities经营活动现金流出小计经营活动产生的现金流量净额二、投资活动产生的现金流量:收回投资收到的现金Cash inflows from operating activitiesNet cash flows from operating activities2、Cash flows from investing activitiesCash received from disposal of investments筹资活动现金流入小计偿还债务支付的现金分配股利、利润或偿付利息支付的现金其中:子公司支付给少数股东的股利、利润Cash inflow from investment activitiesCash repayments of amounts borrowedCash payments forinterest expenses and distribution ofdividends or profitAmong:dividends and earnings paid to minorities bysubsidiaries取得投资收益收到的现金处置固定资产、无形资产和其他长期资产收回的现金净额Cash received from returns on investmentsNet cash received from disposal of fixed assets,Intangible assets & other long-term assets支付其他与筹资活动有关的现金筹资活动现金流出小计Other cash payments relating to financing activitesCash inflow from investment activities处置子公司及其他营业单位收到的现金净额Net cash received disposal subsidiary and otherbusiness units筹资活动产生的现金流量净额Net cash flows from financing activities收到其他与投资活动有关的现金投资活动现金流入小计Other cash received relating to investing activitiesCash inflow from investment activities四、汇率变动对现金及现金等价物的影响五、现金及现金等价物净增加额4、Effect of foreing exchange rate changes on cash5、Net increase in cash and cash equivalents购建固定资产、无形资产和其他长期资产支付的现金Cash paid to acquire fixed assets,intangible assets加:期初现金及现金等价物余额& other long-term assetsPlus:Initial cash and cash equivalents balance投资支付的现金Cash paid to acquire investments 六、期末现金及现金等价物余额6、The final cash and cash equivalents balance。

现金流量分析报告范文

现金流量分析报告范文英文回答:Cash flow analysis is a crucial tool for evaluating the financial health and performance of a business. It provides insights into the movement of cash within a company over a specific period of time, helping to identify trends, assess liquidity, and make informed decisions. In this report, I will discuss the importance of cash flow analysis and provide examples to illustrate its significance.Firstly, cash flow analysis allows us to understand the cash inflows and outflows of a business. It helps us determine the sources of cash, such as sales revenue, loans, or investments, as well as the uses of cash, including expenses, debt repayments, or investments in assets. By analyzing these cash flows, we can identify areas where the company is generating or consuming cash and make necessary adjustments to improve its financial position.For example, let's say a company has experienced a decline in sales revenue. By analyzing the cash flow statement, we can determine if this decline has impacted the company's cash inflows. If there is a significant decrease in cash inflows, it may indicate that the company needs to implement cost-cutting measures or explore new revenue streams to maintain a healthy cash flow.Secondly, cash flow analysis helps assess the liquidity of a business. It provides information about the company's ability to meet its short-term obligations and cover its operating expenses. By examining the cash flow from operations, we can determine if the company is generating enough cash to sustain its day-to-day operations.For instance, let's consider a scenario where a company has a high level of accounts receivable but is struggling to collect payments from its customers. By analyzing the cash flow statement, we can identify if the company is experiencing a cash flow issue due to delayed or non-payment from customers. This analysis can prompt the company to take necessary actions, such as implementingstricter credit policies or improving its collection process, to improve its cash flow and ensure liquidity.Lastly, cash flow analysis helps in making informed financial decisions. By understanding the cash flow patterns and trends, we can evaluate the financial viability of potential investments or projects. It allows us to assess the potential return on investment and the impact on cash flows.For example, let's say a company is considering investing in a new production facility. By analyzing the cash flow projections, we can determine if the investment will generate positive cash flows in the long run and if the company has sufficient cash reserves to finance the project. This analysis helps in making a well-informed decision about whether to proceed with the investment or explore alternative options.In conclusion, cash flow analysis is a vital tool for evaluating the financial performance and health of a business. It provides insights into the movement of cashwithin a company, helps assess liquidity, and aids in making informed financial decisions. By analyzing cash flows, we can identify areas for improvement, ensure sufficient liquidity, and make sound investment choices.中文回答:现金流量分析是评估企业财务状况和业绩的重要工具。

财务报表分析中英文对照外文翻译文献

中英文对照外文翻译文献(文档含英文原文和中文翻译)原文:ANALYSIS OF FINANCIAL STATEMENTSWe need to use financial ratios in analyzing financial statements.—— The analysis of comparative financial statements cannot be made really effective unless it takes the form of a study of relationships between items in the statements. It is of little value, for example, to know that, on a given date, the Smith Company has a cash balance of $1oooo. But suppose we know that this balance is only -IV per cent of all current liabilities whereas a year ago cash was 25 per cent of all current liabilities. Since the bankers for the company usually require a cash balance against bank lines, used or unused, of 20 per cent, we can see at once that the firm's cash condition is exhibiting a questionable tendency.We may make comparisons between items in the comparative financial statements as follows:1. Between items in the comparative balance sheeta) Between items in the balance sheet for one date, e.g., cash may be compared with current liabilitiesb) Between an item in the balance sheet for one date and the same item in the balance sheet for another date, e.g., cash today may be compared with cash a year agoc) Of ratios, or mathematical proportions, between two items in the balance sheet for one date and a like ratio in the balance sheet for another date, e.g., the ratio of cash to current liabilities today may be compared with a like ratio a year ago and the trend of cash condition noted2. Between items in the comparative statement of income and expensea) Between items in the statement for a given periodb) Between one item in this period's statement and the same item in last period's statementc) Of ratios between items in this period's statement and similar ratios in last period's statement3. Between items in the comparative balance sheet and items in the comparative statement of income and expensea) Between items in these statements for a given period, e.g., net profit for this year may be calculated as a percentage of net worth for this yearb) Of ratios between items in the two statements for a period of years, e.g., the ratio of net profit to net worth this year may-be compared with like ratios for last year, and for the years preceding thatOur comparative analysis will gain in significance if we take the foregoing comparisons or ratios and; in turn, compare them with:I. Such data as are absent from the comparative statements but are of importance in judging a concern's financial history and condition, for example, the stage of the business cycle2. Similar ratios derived from analysis of the comparative statements of competing concerns or of concerns in similar lines of business What financialratios are used in analyzing financial statements.- Comparative analysis of comparative financial statements may be expressed by mathematical ratios between the items compared, for example, a concern's cash position may be tested by dividing the item of cash by the total of current liability items and using the quotient to express the result of the test. Each ratio may be expressed in two ways, for example, the ratio of sales to fixed assets may be expressed as the ratio of fixed assets to sales. We shall express each ratio in such a way that increases from period to period will be favorable and decreases unfavorable to financial condition.We shall use the following financial ratios in analyzing comparative financial statements:I. Working-capital ratios1. The ratio of current assets to current liabilities2. The ratio of cash to total current liabilities3. The ratio of cash, salable securities, notes and accounts receivable to total current liabilities4. The ratio of sales to receivables, i.e., the turnover of receivables5. The ratio of cost of goods sold to merchandise inventory, i.e., the turnover of inventory6. The ratio of accounts receivable to notes receivable7. The ratio of receivables to inventory8. The ratio of net working capital to inventory9. The ratio of notes payable to accounts payableIO. The ratio of inventory to accounts payableII. Fixed and intangible capital ratios1. The ratio of sales to fixed assets, i.e., the turnover of fixed capital2. The ratio of sales to intangible assets, i.e., the turnover of intangibles3. The ratio of annual depreciation and obsolescence charges to the assetsagainst which depreciation is written off4. The ratio of net worth to fixed assetsIII. Capitalization ratios1. The ratio of net worth to debt.2. The ratio of capital stock to total capitalization .3. The ratio of fixed assets to funded debtIV. Income and expense ratios1. The ratio of net operating profit to sales2. The ratio of net operating profit to total capital3. The ratio of sales to operating costs and expenses4. The ratio of net profit to sales5. The ratio of net profit to net worth6. The ratio of sales to financial expenses7. The ratio of borrowed capital to capital costs8. The ratio of income on investments to investments9. The ratio of non-operating income to net operating profit10. The ratio of net operating profit to non-operating expense11. The ratio of net profit to capital stock12. The ratio of net profit reinvested to total net profit available for dividends on common stock13. The ratio of profit available for interest to interest expensesThis classification of financial ratios is permanent not exhaustive. -Other ratios may be used for purposes later indicated. Furthermore, some of the ratios reflect the efficiency with which a business has used its capital while others reflect efficiency in financing capital needs. The ratios of sales to receivables, inventory, fixed and intangible capital; the ratios of net operating profit to total capital and to sales; and the ratios of sales to operating costs and expenses reflect efficiency in the use of capital.' Most of the other ratios reflect financial efficiency.B. Technique of Financial Statement AnalysisAre the statements adequate in general?-Before attempting comparative analysis of given financial statements we wish to be sure that the statements are reasonably adequate for the purpose. They should, of course, be as complete as possible. They should also be of recent date. If not, their use must be limited to the period which they cover. Conclusions concerning 1923 conditions cannot safely be based upon 1921 statements.Does the comparative balance sheet reflect a seasonable situation? If so, it is important to know financial conditions at both the high and low points of the season. We must avoid unduly favorable judgment of the business at the low point when assets are very liquid and debt is low, and unduly unfavorable judgment at the high point when assets are less liquid and debt likely to be relatively high.Does the balance sheet for any date reflect the estimated financial condition after the sale of a proposed new issue of securities? If so, in order to ascertain the actual financial condition at that date it is necessary to subtract the amount of the security issue from net worth, if the. issue is of stock, or from liabilities, if bonds are to be sold. A like amount must also be subtracted from assets or liabilities depending upon how the estimated proceeds of the issue are reflected in the statement.Are the statements audited or unaudited? It is often said that audited statements, that is, complete audits rather than statements "rubber stamped" by certified public accountants, are desirable when they can be obtained. This is true, but the statement analyst should be certain that the given auditing film's reputation is beyond reproach.Is working-capital situation favorable ?-If the comparative statements to be analyzed are reasonably adequate for the purpose, the next step is to analyze the concern's working-capital trend and position. We may begin by ascertaining the ratio of current assets to current liabilities. This ratioaffords-a test of the concern's probable ability to pay current obligations without impairing its net working capital. It is, in part, a measure of ability to borrow additional working capital or to renew short-term loans without difficulty. The larger the excess of current assets over current liabilities the smaller the risk of loss to short-term creditors and the better the credit of the business, other things being equal. A ratio of two dollars of current assets to one dollar of current liabilities is the "rule-of-thumb" ratio generally considered satisfactory, assuming all current assets are conservatively valued and all current liabilities revealed.The rule-of-thumb current ratio is not a satisfactory test ofworking-capital position and trend. A current ratio of less than two dollars for one dollar may be adequate, or a current ratio of more than two dollars for one dollar may be inadequate. It depends, for one thing, upon the liquidity of the current assets.The liquidity of current assets varies with cash position.-The larger the proportion of current assets in the form of cash the more liquid are the current assets as a whole. Generally speaking, cash should equal at least 20 per cent of total current liabilities (divide cash by total current liabilities). Bankers typically require a concern to maintain bank balances equal to 20 per cent of credit lines whether used or unused. Open-credit lines are not shown on the balance sheet, hence the total of current liabilities (instead of notes payable to banks) is used in testing cash position. Like the two-for-one current ratio, the 20 per cent cash ratio is more or less a rule-of-thumb standard.The cash balance that will be satisfactory depends upon terms of sale, terms of purchase, and upon inventory turnover. A firm selling goods for cash will find cash inflow more nearly meeting cash outflow than will a firm selling goods on credit. A business which pays cash for all purchases will need more ready money than one which buys on long terms of credit. The more rapidly the inventory is sold the more nearly will cash inflow equal cash outflow, other things equal.Needs for cash balances will be affected by the stage of the business cycle. Heavy cash balances help to sustain bank credit and pay expenses when a period of liquidation and depression depletes working capital and brings a slump in sales. The greater the effects of changes in the cycle upon a given concern the more thought the financial executive will need to give to the size of his cash balances.Differences in financial policies between different concerns will affect the size of cash balances carried. One concern may deem it good policy to carry as many open-bank lines as it can get, while another may carry only enough lines to meet reasonably certain needs for loans. The cash balance of the first firm is likely to be much larger than that of the second firm.The liquidity of current assets varies with ability to meet "acid test."- Liquidity of current assets varies with the ratio of cash, salable securities, notes and accounts receivable (less adequate reserves for bad debts), to total current liabilities (divide the total of the first four items by total current liabilities). This is the so-called "acid test" of the liquidity of current condition. A ratio of I: I is considered satisfactory since current liabilities can readily be paid and creditors risk nothing on the uncertain values of merchandise inventory. A less than 1:1 ratio may be adequate if receivables are quickly collected and if inventory is readily and quickly sold, that is, if its turnover is rapid andif the risks of changes in price are small.The liquidity of current assets varies with liquidity of receivables. This may be ascertained by dividing annual sales by average receivables or by receivables at the close of the year unless at that date receivables do not represent the normal amount of credit extended to customers. Terms of sale must be considered in judging the turnover of receivables. For example, if sales for the year are $1,200,000 and average receivables amount to $100,000, the turnover of receivables is $1,200,000/$100,000=12. Now, if credit terms to customers are net in thirty days we can see that receivables are paid promptly.Consideration should also be given market conditions and the stage of the business cycle. Terms of credit are usually longer in farming sections than in industrial centers. Collections are good in prosperous times but slow in periods of crisis and liquidation.Trends in the liquidity of receivables will also be reflected in the ratio of accounts receivable to notes receivable, in cases where goods are typically sold on open account. A decline in this ratio may indicate a lowering of credit standards since notes receivable are usually given to close overdue open accounts. If possible, a schedule of receivables should be obtained showing those not due, due, and past due thirty, sixty, and ninety days. Such a, schedule is of value in showing the efficiency of credits and collections and in explaining the trend in turnover of receivables. The more rapid the turnover of receivables the smaller the risk of loss from bad debts; the greater the savings of interest on the capital invested in receivables, and the higher the profit on total capital, other things being equal.Author(s): C. O. Hardy and S. P. Meech译文:财务报表分析A.财务比率我们需要使用财务比率来分析财务报表,比较财务报表的分析方法不能真正有效的得出想要的结果,除非采取的是研究在报表中项目与项目之间关系的形式。

现金流量表中英文版

补充材料:Supplemental Information 1、将净利润调节为经营活动现金流量:Reconciliation of net profit to cash flows from operating activities 净利润 Net profit 加:计提的资产减值准备 Plus: Provision for assets 固定资产折旧 Depreciation of fixed assets 无形资产摊销 Amortisation of intangible assets 长期待摊费用摊销 Amortisation of long-term deffered expenses 待摊费用减少(减:增加)Decrease of deffered expenses (Less: addition) 预提费用增加(减:减少)Addition of accued expense (Less: decrease) 处置固定资产无形资产和其他长期资产的损失(减:收益)Losses on disposal of fixed assets,intangible assets and other long-term assets(or deduct: gain) 固定资产报废损失Losses on scrapping of fixed assets 财务费用 Finance Expense 投资损失(减:收益) Losses arsing from investment(or deduct :gain) 递延税款贷项(减:借项) Deferred tax credit(or deduct:debit) 存货的减少(减:增加)Decrease in inventories (or deduct:increase) 经营性应收项目的减少(减:增加) Decrease in operating receivables(or deduct:increase) 经营性应付项目的增加(减:减少) Increase in operating receivables(or deduct:decrease) 其他 Others 经营活动产生的现金流量净额 Net cash flows from operating activities 2、不涉及现金收支的投资和筹资活动:Investing and financing activities that do not involve in cash receipts and payments 债务转为资本 Debts transfer to capital 一年内到期的可转换公司债券 One year due convertible bonds 融资租入固定资产 Financing rent to the fixed asset 其他 Others 3、现金及现金等价物净增加情况:Net increase in cash and cash equivalents 现金的期末余额 Cash at the end of period 减:现金的期初余额 Less: cash at the beginning of the period 加:现金等价物的期末余额 Plus: cash equivalents at the end of the period 减:现金等价物的期初余额 Less: cash equivalents at the beginning of the period 现金及现金等价物净增加额 Net increase in cash and cash equivalents

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

现金流量表能直观的展示企业现金流方面的状况,并可对企业长远发展做出展望。一些中小企业也可针对现金流量表对企业状况得出一个结论。人们对现金流量表认识的不断加深,表明现金流量表对企业价值分析越发重要。

直接法是直接陈列现金收入和支出的信息。根据这种方法,对于经营、筹资、投资这三种活动的现金流量被认为是与公司在经营过程中发生的交易或事项的经营活动现金流入和支出等同的。直接法深受投资者的偏爱,因为它是对现金流预测的起点,进而判断公司的未来价值。

据专家说,间接法更容易应用和受公司外部人青睐,因为间接法可以使公司财务报表外部使用者更清楚的了解公司资产的流动性和偿付能力。也正因如此,公司内部管理者往往不想采用间接法来编制现金流量表。间接法以利润表上的净利润为起点,通过调整某些相关项目后得出经营产生的现金流量。通过将企业非现金交易,过去或者未来经营活动产生的现金收入或支出的递延或应计项目,以及与投资或筹资现金流量相关的收益或费用项目对净收益的影响进行调整来反映企业经营活动所形成的现金流量。以损益表为出发点来列示企业经营活动的现金流量情况。损益表直接体现了连接筹资和投资活动的收入和支出项目。因此采用间接法,我们就可以调整和计算筹资和投资活动的收入和支出。

相反,获利较少的公司,在缺乏投资或企业价值呈现递减趋势的状况下,反而能够保持令人满意的偿债能力。以此,取决于公司盈利能力和资产结构的公司的流动性成为债权人的关注点。利润收入和费用的支付能力之间的区别是现金流的代表和连接盈利能力和偿债能力的关键。

通过对公司盈利能力和支付能力的调查,现金流量表使公司认识了历史现金流量,并提供了短期内未来现金流量的预测。现金流量信息被财务信息使用者认为是最简单、最客观的展示了企业财务状况的信息来源。现金流量信息也可反映了一些新的模式下企业价值分析的本质。

盈利能力和偿债能力是描述企业资产负债表两个很直接的渠道。一项重要的盈利能力可以指出了收入和费用之间的不同,以确保支付费用的投资资本。但是收入并非总是利润和费用的汇聚。另一方面,一定的利润并不代表收入或贷款和不确定支付的费用或投资的差额。根据定义,一个充分或不足的偿债能力并等同于一个显著或不良的盈利能力。一个负的利润表示公司的收入不足已支付发生的费用,并且其差额未能完全支付其投资成本。这样长期下去,如果企业没有其他利润,就会导致企业缺乏偿债能力。在一个短、中期间,通过度获利能力和盈利能力分析可以感知企业财务状况的变动。因此,快速增长的固定资产的投资,造成融资的运行周期变长,并降低了流动资产的周转速度,最终导致本来获利的公司面对现金周转的困境。

2 现金流量表提供的信息的应用

现金流量表提供的信息可用于多方面。

第一,财务报表是基于权责发生制的财务制度和独立性原则下编制的。在这种情况下,现金流量的产生受制度和公司的其他事项的影响是公认的,而不是当现金或现金状况发生变动时,并不是只是为了满足权责发生制会计信息使用者的满意。

第二,是体现在损益表中的运营的结果,受一系列会计项目的影响,比如应付款系统,即损益表并不能反映公司的这真实的财务状况。

最后,即使除了以上提到过的情况,现金流量表仍可提供公司一系列已通过其他财务报表分析了的静态财务状况之外的额外的很多信息。例如,从公司净资产的变化,并从资产负债表角度,对企业进行静态分析。现金流量表可以反映企业净资产动态的变化,并使其在企业运营过程中的收入和支出中分别反映。所以资产负债表和所有者权益变动表的构成成为被分析的行列。这样的分析主要是用于反映用于偿还的融资费用。现金流量表还提供了与来自股东、债权人的外部资本相关的利润和费用的支付,及其股利和利息的支付。通过分析,我们可以了解到公司盈利能力和现金流之间的关系可以影响公司某一时期的营业额和利润。

为了衡量公司的产生的现金流量的容量和现金质量,财务状况的使用者通过分析现金流量表,可以获得一个企业现金收入和支付活动的情况,而并非只是表现其由权责发生制决定的表面上的财务状况。现金流量表编制的目的为提供一个富有意义的企业有效的现金流入和现金流出的状况,如企业正在运行的各项主要活动,比如投资活动、经营活动、筹资活动,并以此判断财政收支的平衡,进而对企业财务状况做出最终判断。除此之外,现金流量表还展示了公司创造现金的能力。

投资活动产生的现金流量产生于加大投资和减少投资、资金成本以及投资活动过程中产生的赤字或不足。

筹资活动产生的现金流量反映了与公司外部资金相关的收入和支出情况,尤其是经营活动产生的现金不足以支付经营和投资活动,以及偿还银行利息和股东股利所需资金时。

现金活动分项列示的优势在于,它进一步解释了公司财务状况变动,并通过分析每部分的资金平衡状态及现金活动分项列示强调了,来自运用因素分析法在不同时期产生最高现金流的经营活动及有现金结余的投资活动的现金及现金等价物。总的现金流量是根据经营活动现金流的直接法和间接法来确定的。

3 现金流量的测定和编制方法

现金流量表描述了在某一会计期间,经营活动、投资活动和筹资活动确定现金收入和现金支出的状况。现金流量项目是根据经营活动现金流、投资活动现金流和筹资活动现金流的产生和支出来划分的。

在国际会计准则(ISA)中提出,经营活动现金流量是表现公司财务业绩的关键。经营活动的现金流是不包括外部融资,保持公司生产能力,获取新的更大的投资、奖励和偿还贷款利息重要项目。现金流量表可将运营结果转换成现金收支的状态。

上海财经大学浙江学院毕业设计(论文)外文翻译

译文:

现金流量表概述

现代财务报表.国际会计标准的理解和应用指南,CECCAR出版商,布加勒斯特,2004

1 简介

财务报表旨在确定区别于实际经营情况和对外报表数据之间的有效的数据,目的在于可据此获得企业存在和可持续发展的能力和价值。损益表在分析中虽然占据重要地位,但是现金流量表作为重要补充报表,它不但提供经营活动过程中财务动态的状况,而且它能对反映其财务结构和现金流量的财务状况提供一个清晰的视觉。一个公司公布的财务报表,只提供了重要的、关键的财务数据。但现金流量表除此之外还提供了资金的“来龙去脉”,对有效的投资决策和和投资成本回报率以及提供外部的资金的成本对保证财务平衡的贡献。

现金流量表在表现企业真实的财务状况上扮演重要的角色,因为它排除了对同一个项目运用的各种不同会计处理方法,并考虑在那些计入损益表中、但并没有创造现金收入或支出的收入和费用等。

另一方面值得提起的是,非流动资产使现金流量表的分析成为很重要的分析方法。企业现金流量财务状况的分析包括,从最简单的视角,比较来自损益表的收入和费用,并独立地分析现金收入和现金费用支出状况。损益表只考虑到收益,而并没有考虑到现金的偿债能力。