成本与管理会计第13版 英文版课件

合集下载

成本与管理会计-亨格瑞-第13版-英文版-CA07

A static-budget variance is : (Actual result - Budgeted amount in the static budget).

A favourable (F) variance is a variance that increases operating profit relative to the budgeted amount.

An unfavourable (U) variance is a variance that decreases operating profit relative to the budgeted amount.

2019/10/10

14

14

Static-Budget Variance

Level 0 analysis compares actual operating profit with budgeted operating profit.

$120 × 10,000 = $1,200,000

2019/10/10

23

23

Steps in Developing Flexible Budgets

Step 3: Determine the flexible budget for costs

based on budgeted variable costs per output unit,

Step 1: Determine the actual output. In April 2008, 10,000 suits were produced and

sold.

Step 2: Determine the flexible budget for revenues based on budgeted selling price and actual output.

A favourable (F) variance is a variance that increases operating profit relative to the budgeted amount.

An unfavourable (U) variance is a variance that decreases operating profit relative to the budgeted amount.

2019/10/10

14

14

Static-Budget Variance

Level 0 analysis compares actual operating profit with budgeted operating profit.

$120 × 10,000 = $1,200,000

2019/10/10

23

23

Steps in Developing Flexible Budgets

Step 3: Determine the flexible budget for costs

based on budgeted variable costs per output unit,

Step 1: Determine the actual output. In April 2008, 10,000 suits were produced and

sold.

Step 2: Determine the flexible budget for revenues based on budgeted selling price and actual output.

成本与管理会计亨格瑞第13版英文版CA07

TOTAL VARIABLE COST

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS)

BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

Level 1 analysis provides more detailed information on the operating profit static- budget variance.

Level 1 gives the user a little more information: it shows which line-items led to the total Level 0 variance.

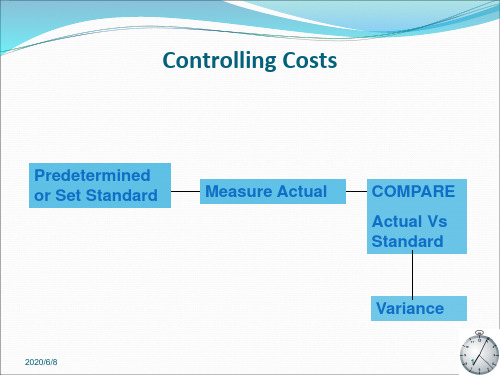

Actual Vs Standard

2019/12/27

Variance

2

2

Basic Concepts

Variance – difference between an actual and an expected (budgeted) amount

Purpose of variance

Management by exception Performance evaluation Motivate managers Prompt strategy change

of the budget period. The master budget is an example of a static budget.

Flexible budget

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS)

BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

Level 1 analysis provides more detailed information on the operating profit static- budget variance.

Level 1 gives the user a little more information: it shows which line-items led to the total Level 0 variance.

Actual Vs Standard

2019/12/27

Variance

2

2

Basic Concepts

Variance – difference between an actual and an expected (budgeted) amount

Purpose of variance

Management by exception Performance evaluation Motivate managers Prompt strategy change

of the budget period. The master budget is an example of a static budget.

Flexible budget

成本与管理会计亨格瑞第13版英文版CA06

Operating budgets include budgets reflecting the planned operational aspects of the business, including revenues, production, manufacturing costs, and other expenses for the period. It culminates in a budgeted income statement.

The master budget is actually a series of budgets including a set of budgeted financial statements (sometimes called pro forma statements).

2021/8/5

9

Advantages of Budgets

Despite the fact that budgets are advantageous, there are a number of challenges in properly administering budgets.

It is a time consuming process that involves all levels of management.

The path to effective strategies include asking questions such as:

What are our objectives? How do we create value for the customer while

distinguishing ourselves from our competitors?

The master budget is actually a series of budgets including a set of budgeted financial statements (sometimes called pro forma statements).

2021/8/5

9

Advantages of Budgets

Despite the fact that budgets are advantageous, there are a number of challenges in properly administering budgets.

It is a time consuming process that involves all levels of management.

The path to effective strategies include asking questions such as:

What are our objectives? How do we create value for the customer while

distinguishing ourselves from our competitors?

成本与管理会计亨格瑞第13版英文版CA

The development of management accounting emerged in the 1920s, when the focus shifted from mere cost measurement to cost analysis and control, emphasizing the role of accounting in decision-making and management control.

It involves the identification, measurement, and allocation of costs, as well as the preparation of cost reports and other management information to assist management in making decisions about product pricing, production, and resource allocation.

Direct and indirect costs

Activity Identification

The first step in the activity-based costing method involves identifying the various activities that take place within the organization.

Cost allocation and collection

Cost Allocation

Allocating costs to specific departments, projects, or products is essential for accurate financial reporting and decision-making.

成本与管理会计-亨格瑞-第13版-英文版-CA07共75页文档

2020/6/8

10

Static Budget

What was the actual operating profit?

Revenues (10,000 × $125) $1,250,000

Less Expenses:

Variable (10,000 × $95.01)

950,100

Fixed

285,000

TOTAL VARIABLE COST

VARIABLE COST PER JACKET

$60 16 12

$88

BUDGETED FIXED COSTS FOR PRODUCTION(0-12 000UNITS) BUGETED SELLING PRICE BUDGETED PRODUCTION AND SALES ACTUAL PRODUCTION AND SALES

Purpose of variance

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2020/6/8

2

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

2020/6/8

$276 000 $120/JACKET 12 000JACKETS 10 000JACKETS

6

2020/6/8

7

Static Budget

es and sells jackets.

成本与管理会计 亨格瑞 第13版 英文版 CA18PPT课件

CHAPTER 18

Spoilage, Rework, and Scrap

Terminology

Spoilage, rework, and scrap have distinctive definitions in cost accounting that may not be the definition commonly used. P510(639) It is important that these terms be used properly, as each receives a different accounting treatment.

Normal spoilage is spoilage inherent in the production process.

It is viewed arising even in an efficient manufacturing process.

Typically, normal spoilage is included as a part of the cost of good units manufactured.

Scrap is residual material that results from manufacturing a product.

It has low or zero sales value.

Spoilage

Different types of Spoilage P511(639)

Spoilage is divided into two types: normal spoilage and abnormal spoilage.

the remaining 100 units are spoiled because of machine breakdown and operation errors.

Spoilage, Rework, and Scrap

Terminology

Spoilage, rework, and scrap have distinctive definitions in cost accounting that may not be the definition commonly used. P510(639) It is important that these terms be used properly, as each receives a different accounting treatment.

Normal spoilage is spoilage inherent in the production process.

It is viewed arising even in an efficient manufacturing process.

Typically, normal spoilage is included as a part of the cost of good units manufactured.

Scrap is residual material that results from manufacturing a product.

It has low or zero sales value.

Spoilage

Different types of Spoilage P511(639)

Spoilage is divided into two types: normal spoilage and abnormal spoilage.

the remaining 100 units are spoiled because of machine breakdown and operation errors.

成本与管理会计 亨格瑞 第13版 英文版 CA05

8

2012-10-5

Broad Averaging and Cross-subsidization,conts.

When a company has a situation in which

undercosting or overcosting of products occurs, this is referred to as product-cost cross-subsidization. P110

costing system

2012-10-5

11

Rationale for Refining Costing System

Increase in product diversity •Customized products

•Differentiate from competitors

Guidelines for Refining

2012-10-5

4

Background

Easy to trace Direct materials and direct labor costs

Overhead cannot be traced easily and must be allocated with estimates.

Recall that Factory Overhead is applied to production in a

rational and systematic manner, using some type of averaging. There are a variety of methods to accomplish this goal.

Simple Methods Unrealistic

2012-10-5

Broad Averaging and Cross-subsidization,conts.

When a company has a situation in which

undercosting or overcosting of products occurs, this is referred to as product-cost cross-subsidization. P110

costing system

2012-10-5

11

Rationale for Refining Costing System

Increase in product diversity •Customized products

•Differentiate from competitors

Guidelines for Refining

2012-10-5

4

Background

Easy to trace Direct materials and direct labor costs

Overhead cannot be traced easily and must be allocated with estimates.

Recall that Factory Overhead is applied to production in a

rational and systematic manner, using some type of averaging. There are a variety of methods to accomplish this goal.

Simple Methods Unrealistic

成本与管理会计-亨格瑞-第13版-英文版-CA08_图文_图文

Commit more resources to develop appropriate standards

15

Variable overhead spending variance

=($29/machine hour-$30 /machine hour) ×4 500 machine-hours =(-1machine hour) ×4 500 machine-hours =$4 500F

=1 728 000/57 600=30/hour

Budgeted variable overhead cost rate per output unit

5

=0.4hour/unit×30=12/jacket

Variable overhead cost variances(P208 )

6

Flexible-budget analysis

The variable overhead efficiency variance measures the efficiency with which the costallocation base is used.

11

Variable Overhead Variances

Actual Variable Overhead Incurred

Step 3:

Identify the variable overhead costs associated with each costallocation base.

Step 4:

Compute the rate per unit of each cost-allocation base used to allocate variable overhead costs to output produced.

15

Variable overhead spending variance

=($29/machine hour-$30 /machine hour) ×4 500 machine-hours =(-1machine hour) ×4 500 machine-hours =$4 500F

=1 728 000/57 600=30/hour

Budgeted variable overhead cost rate per output unit

5

=0.4hour/unit×30=12/jacket

Variable overhead cost variances(P208 )

6

Flexible-budget analysis

The variable overhead efficiency variance measures the efficiency with which the costallocation base is used.

11

Variable Overhead Variances

Actual Variable Overhead Incurred

Step 3:

Identify the variable overhead costs associated with each costallocation base.

Step 4:

Compute the rate per unit of each cost-allocation base used to allocate variable overhead costs to output produced.

成本和管理会计亨格瑞第13版英文版CA04

Distinguish job costing from process costing

2018/11/21

6

Basic Costing Terminology,conts.

Cost Assignment

Direct Costs Indirect Costs

Cost Tracing

materials and labor

Cost Allocation

overhead

Cost Object

items. A cost-allocation base is the driver or activity that is used to allocate indirect costs from the cost pool to the cost object.

2018/11/21

8

Learning objective 2

tracing and cost allocation. Two new terms related to costing systems are introduced in this chapter p78

A cost pool is a grouping of individual indirect cost

Financial Accounting

Product costs are used to value inventory and to compute cost of goods sold.

2018/11/21 2

Managerial Accounting and Cost Management

Product costs are used for planning, control, directing, and management decision making.

2018/11/21

6

Basic Costing Terminology,conts.

Cost Assignment

Direct Costs Indirect Costs

Cost Tracing

materials and labor

Cost Allocation

overhead

Cost Object

items. A cost-allocation base is the driver or activity that is used to allocate indirect costs from the cost pool to the cost object.

2018/11/21

8

Learning objective 2

tracing and cost allocation. Two new terms related to costing systems are introduced in this chapter p78

A cost pool is a grouping of individual indirect cost

Financial Accounting

Product costs are used to value inventory and to compute cost of goods sold.

2018/11/21 2

Managerial Accounting and Cost Management

Product costs are used for planning, control, directing, and management decision making.

成本与管理会计-亨格瑞-第13版-英文版-CA08

Flexible Budget for Variable Overhead at Actual Hours

AH × SVR

Flexible Budget for Variable Overhead at

Standard Hours

SH × SVR

Spending Variance

Efficiency Variance

Workers were less skilled than expected in using machines?

Webb spend more on variable overhead costs , such as maintenance?

8

2019/10/7

Variable Overhead Variances

=$15 000U

14

2019/10/7

4500 HOURS VS 4000 HOURS

Possible causes for exceeding budget

Workers were less skilled than expected in using machines

Production scheduler inefficiently scheduled jobs ,resulting in more machinehours used than budgeted

overhead cost

Efficiency

cost-alocation base alocation based alowed

per unit of

Variance

used for actual output for actual output

成本与管理会计-亨格瑞-第13版-英文版-CA05

effective

base for each indirect-cost pool.

•Strategic decision

•Provide more data

•Price decision

•Multiple cost driver pools

•Market decision

2019/9/7

12

Refining a Costing System

2019/9/7

2

Structure of Lecture

Under- and over-costing – why it happens? Activity Based Costing (ABC) Indicators of need for ABC ABC system Difference between ABC and Traditional Product

Peanut-butter costing uses broad averages to assign (or spread) costs uniformly to cost objects.

The result can be undercosting or overcosting of products.

Increase in indirect costs. With modern technology, companies have experienced a decrease in direct costs with a resulting increase in indirect costs.

2019/9/7

4

Background

Easy to trace Direct materials and direct labor costs Overhead cannot be traced easily and must be

成本与管理会计-亨格瑞-第13版-英文版-CA02

If a product takes 5 pounds of materials each, it stays the same per unit regardless of whether one, ten, or a thousand units are produced.

Fixed costs

for different purposes

Describe a framework for cost accounting and cost management

2019/9/7

2

Learning objective 1 Define and illustrate a cost object

2019/9/7

2-16

16

Ⅲ Cost behavior and Classifications

Cost behavior means how a cost will react to changes in the level of business activity.

Total variable costs change when activity changes.

2-12

2019/9/7

12

2019/9/7

2-13

13

Direct and Indirect Costs,conts.

several factors that affect the classification of costs as direct or indirect.P25

Materiality of the cost. The smaller the amount of the cost, the less likely that it is economically feasible to trace that cost to a particular cost object.

成本与管理会计亨格瑞第13版英文版CA05

based management Compare activity-based costing systems and department costing

systems Evaluate the costs and benefits of implementing activity-based

CHAPTER 5

Activity-Based Costing and

Activity-Based Management

LEARNING OBJECTIVES

Explain how broad averaging undercosts and overcosts products or services

1. Direct-cost tracing

classify as many of the total costs as

direct costs as is economically feasible.

2. Indirect-cost pools

expand the number of cost pools until

Advances in IT

each of these pools is homogeneous. Competition in markets

3. Cost-allocation basis

•Make trace more cost- identify the preferred cost-allocation

Competition in product markets. Markets have become more competitive, forcing managers to obtain more accurate cost information to help them make strategic decisions.

systems Evaluate the costs and benefits of implementing activity-based

CHAPTER 5

Activity-Based Costing and

Activity-Based Management

LEARNING OBJECTIVES

Explain how broad averaging undercosts and overcosts products or services

1. Direct-cost tracing

classify as many of the total costs as

direct costs as is economically feasible.

2. Indirect-cost pools

expand the number of cost pools until

Advances in IT

each of these pools is homogeneous. Competition in markets

3. Cost-allocation basis

•Make trace more cost- identify the preferred cost-allocation

Competition in product markets. Markets have become more competitive, forcing managers to obtain more accurate cost information to help them make strategic decisions.

成本与管理会计 亨格瑞 第13版 英文版 CA02

管理分析的方法与指标

添加 标题

财务比率分析:通过计算各种财务比率,如 流动比率、速动比率、存货周转率等,来评 估企业的偿债能力、营运能力和盈利能力。

添加 标题

结构分析:通过分析财务报表中各项目的构 成比例,了解企业各项业务的比重和结构特 点。

添加 标题

因素分析:通过分析影响企业财务状况的各 种因素,如市场环境、政策变化等,预测未 来的发展趋势。

间接成本法

定义:间接成本法是一种将间接成本分配到产品或服务中的成本计算方法

特点:将间接成本与直接成本一起分配到产品或服务中,以计算产品的总成本

适用范围:适用于生产过程中存在大量间接成本的情况

计算方法:根据不同的分配标准,如人工小时、机器工时等,将间接成本分配到产品或 服务中

作业成本法

定义:作业成本法是一种基于作业的成本核算方法,通过对作业进行成本分配,计算出产品或服 务的成本。

提供支持

现代管理会计: 进入21世纪,管 理会计更加注重 战略决策、风险 管理、绩效评价 等方面,成为企 业核心竞争力的

重要组成部分

管理会计的未来 发展:随着科技 的不断进步和全 球化的趋势,管 理会计将更加注 重数据分析和预 测,为企业提供 更加全面、精准

的支持

管理会计的基本原则和概念

管理会计的定义和目的 管理会计的基本原则 管理会计的概念框架 管理会计与财务会计的区别和联系

添加标题

成本会计的基本内容:成本会计主要包括成本核算、成本分析、成本控制等方面。其中,成本核算是对企业 生产经营过程中的各种成本进行分类、归集和分配的过程;成本分析是对企业成本进行比较、分析和评价的 过程;成本控制则是通过制定一系列措施,对企业生产经营过程中的成本进行监督和控制的过程。

成本与管理会计亨格瑞第13版英文版CA16

Product – any output with a positive sales value, or an output that enables a firm to avoid incurring costs

Value can be high or low

2020/2/10

6

Joint Cost Terminology ,conts.

Separable Costs – all costs incurred beyond the splitoff point that are assignable to each of the nowidentifiable specific products

2020/2/10

3

Example of Joint Cost stituation

2020/2/10

15

Physical-Measure Method

Allocates joint costs to joint products on the basis of the relative weight, volume, or other physical measure at the splitoff point of total production of the products p455(577)

220000 580000

condensed milk : 400000

220000

290000

220000 580000ห้องสมุดไป่ตู้

(3) production cost per gallon

buttercream : (110000 280000) 20000 19.50

Value can be high or low

2020/2/10

6

Joint Cost Terminology ,conts.

Separable Costs – all costs incurred beyond the splitoff point that are assignable to each of the nowidentifiable specific products

2020/2/10

3

Example of Joint Cost stituation

2020/2/10

15

Physical-Measure Method

Allocates joint costs to joint products on the basis of the relative weight, volume, or other physical measure at the splitoff point of total production of the products p455(577)

220000 580000

condensed milk : 400000

220000

290000

220000 580000ห้องสมุดไป่ตู้

(3) production cost per gallon

buttercream : (110000 280000) 20000 19.50

成本与管理会计亨格瑞第13版英文版CA07

Purpose of variance

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2021/1/13

3

3

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

Key difference is the use of the actual output level in the flexible budget.

2021/1/13

6

6

COST CATEGORY

DIRECT MATERIAL COST DIRECT MANUFACTURING LABOR COST VARIABLE MANUFACTURING OVERHEAD COSTS

Direct Material

Standard

Type of Product Cost

5

2021/1/13

5

Static and Flexible Budgets

Static budget

➢ Prepared for only one level of activity. ➢ It is based on the level of output planned at the start of

成本与管理会计亨 格瑞第13版英文版

CA07

Controlling Costs

Predetermined or Set Standard

➢ Management by exception ➢ Performance evaluation ➢ Motivate managers ➢ Prompt strategy change

2021/1/13

3

3

Basic Concepts

Management by Exception – the practice of focusing attention on areas not operating as expected (budgeted)

Key difference is the use of the actual output level in the flexible budget.

2021/1/13

6

6

COST CATEGORY

DIRECT MATERIAL COST DIRECT MANUFACTURING LABOR COST VARIABLE MANUFACTURING OVERHEAD COSTS

Direct Material

Standard

Type of Product Cost

5

2021/1/13

5

Static and Flexible Budgets

Static budget

➢ Prepared for only one level of activity. ➢ It is based on the level of output planned at the start of

成本与管理会计亨 格瑞第13版英文版

CA07

Controlling Costs

Predetermined or Set Standard

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

different purposes Describe a framework for cost accounting and cost management

2

Learning objective 1 Define and illustrate a cost object

2-3

3

Ⅰ Basic Cost Terminology

2-4

4

Ⅰ Basic Cost Terminology Actual Cost

➢ A cost that has occurred, (a historical cost)

Budgeted Cost

➢ A predicted cost

Opportunity Cost

➢ The next best choice foregone.

companies, and service-sector companies Describe the three categories of inventories commonly found in

manufacturing companies Distinguish inventoriable costs from period costs Explain why product costs are computed in different ways for

Cost Object

Cost Object

Tracing

Allocating

2-7

7

BASIC COST TERMINOLOGY,CONTS.

Cost Accumulation describes the process of accumulating costs in some organized manner through the accounting system.

Activity Department

Setting up production machines Environmental, Health & Safety

6

Cost And Cost Terminology

Cost Accumulation

Cost Assignment via

Cost Object

2-5Cost Object

➢ Anything for which a separate measurement of costsbject Examples at BMW

Cost Object Product Service Project

Customer

Illustration BMW X 5 sports activity vehicle Dealer-support telephone hotline R&D project on DVD system enhancement Herb Chambers Motors, a dealer that purchases a broad range of BMW vehicles

2-9

9

Ⅱ Direct Costs and Indirect Costs

Direct costs of a cost object are those that are related to a given cost object (product, department, etc.) and that can be traced to it in an economically feasible way.

Includes: ➢Parts ➢Assembly line wages

Cost-Tracing describes the assignment of direct costs to the particular cost object.

10

Indirect Costs

Indirect Costs

✓ Allocating:accumulated costs with an indirect relationship to the cost object

8

Learning objective 2

Distinguish between direct costs and indirect costs

Following accumulation, costs are assigned to the chosen cost object. involves tracing and allocating costs

✓ Tracing:accumulated costs with a direct relationship to the cost object

CHAPTER 2

An Introduction to Cost Terms and Purposes

1

LEARNING OBJECTIVES

Define and illustrate a cost object Distinguish between direct costs and indirect costs Explain variable costs and fixed costs Interpret unit costs cautiously Distinguish among manufacturing companies, merchandising

➢ Cannot be conveniently or economically traced (tracked) to a cost object. Instead of being traced, these costs are allocated to a cost object in a rational and systematic manner

Cost

➢ Sacrificed resource to achieve a specific objective ➢ It is usually measured as the monetary amount that must

be paid to acquire goods and services.

2

Learning objective 1 Define and illustrate a cost object

2-3

3

Ⅰ Basic Cost Terminology

2-4

4

Ⅰ Basic Cost Terminology Actual Cost

➢ A cost that has occurred, (a historical cost)

Budgeted Cost

➢ A predicted cost

Opportunity Cost

➢ The next best choice foregone.

companies, and service-sector companies Describe the three categories of inventories commonly found in

manufacturing companies Distinguish inventoriable costs from period costs Explain why product costs are computed in different ways for

Cost Object

Cost Object

Tracing

Allocating

2-7

7

BASIC COST TERMINOLOGY,CONTS.

Cost Accumulation describes the process of accumulating costs in some organized manner through the accounting system.

Activity Department

Setting up production machines Environmental, Health & Safety

6

Cost And Cost Terminology

Cost Accumulation

Cost Assignment via

Cost Object

2-5Cost Object

➢ Anything for which a separate measurement of costsbject Examples at BMW

Cost Object Product Service Project

Customer

Illustration BMW X 5 sports activity vehicle Dealer-support telephone hotline R&D project on DVD system enhancement Herb Chambers Motors, a dealer that purchases a broad range of BMW vehicles

2-9

9

Ⅱ Direct Costs and Indirect Costs

Direct costs of a cost object are those that are related to a given cost object (product, department, etc.) and that can be traced to it in an economically feasible way.

Includes: ➢Parts ➢Assembly line wages

Cost-Tracing describes the assignment of direct costs to the particular cost object.

10

Indirect Costs

Indirect Costs

✓ Allocating:accumulated costs with an indirect relationship to the cost object

8

Learning objective 2

Distinguish between direct costs and indirect costs

Following accumulation, costs are assigned to the chosen cost object. involves tracing and allocating costs

✓ Tracing:accumulated costs with a direct relationship to the cost object

CHAPTER 2

An Introduction to Cost Terms and Purposes

1

LEARNING OBJECTIVES

Define and illustrate a cost object Distinguish between direct costs and indirect costs Explain variable costs and fixed costs Interpret unit costs cautiously Distinguish among manufacturing companies, merchandising

➢ Cannot be conveniently or economically traced (tracked) to a cost object. Instead of being traced, these costs are allocated to a cost object in a rational and systematic manner

Cost

➢ Sacrificed resource to achieve a specific objective ➢ It is usually measured as the monetary amount that must

be paid to acquire goods and services.