Week 2 Auditing Lectures CM

employ for Auditor Program

employ for Auditor ProgramEmploy for Auditor ProgramIntroduction:The Auditor Program is a rigorous training program designed to equip individuals with the necessary skills and knowledge to excel in the field of auditing. This program offers a unique opportunity for aspiring auditors to gain practical experience and develop their professional career in the field. This article provides a comprehensive overview of the benefits and application process of the Auditor Program.Benefits of the Auditor Program:1. Comprehensive Training: The Auditor Program offers comprehensive training in auditing techniques, accounting principles, and financial analysis. Participants will receive extensive theoretical and practical knowledge to perform audits effectively and efficiently.2. Hands-on Experience: The program includes real-life case studies and hands-on experience to develop participants' practical skills. This allows individuals to apply their knowledge to real-world scenarios and prepares them for the challenges they may face in their career.3. Networking Opportunities: The Auditor Program provides participants with the opportunity to build a strong professional network. Networking events and workshops facilitate interaction with industry professionals, boosting career prospects and opening doors to potential job opportunities.4. Career Development: Completion of the program enhances participants' employability and career prospects in the auditing field. The program equips individuals with the necessary skills and expertise sought after by auditing firms and organizations. Application Process for the Auditor Program:1. Research: Before applying, it is vital to research the specific requirements and qualifications needed for the Auditor Program. This includes understanding the program's duration, eligibility criteria, and application deadlines.2. Prepare Application Documents: As part of the application process, applicants must prepare a comprehensive resume, highlighting their educational qualifications, relevant work experience, and any additional certifications or skills.3. Submit Application: Once all application documents are prepared, applicants can submit their applications through the designated online portal or by mail. It is essential to double-check the submission deadline and ensure all required documents are included.4. Assessment and Selection: After the application submission, applicants are usually required to pass an assessment test to evaluate their knowledge in accounting principles and auditing techniques. Successful candidates are shortlisted for further selection rounds, which may include interviews and group exercises.5. Final Selection and Enrollment: The final selection is made based on the performance in the assessment test and other selection rounds. The selected candidates are notified of their acceptance into the Auditor Program and provided with the necessary information for enrollment.Conclusion:The Auditor Program offers a valuable opportunity for individuals interested in pursuing a career in auditing. The program's comprehensive training, hands-on experience, networking opportunities, and career development prospects make it highly sought after by aspiring auditors. The application process involves thorough research, preparation of application documents, submission, assessment, and final selection. By successfully completing the Auditor Program, individuals can enhance their employability and gain a competitive edge in the auditing field.继续写相关内容:6. Curriculum and Training Modules: The Auditor Program typically consists of a well-structured curriculum that covers various aspects of auditing. Participants are introduced to auditing principles, standards, and procedures. They also learn about financial accounting, risk management, internal controls, and the legal and ethical considerations in auditing.The training modules in the program are designed to provide a holistic understanding of the auditing process. Participants learn how to plan and execute an audit, gather relevant evidence, and analyze financial statements. They also acquire skills in identifying fraud risks, assessing internal controls, and reporting audit findings.7. Experienced Faculty and Industry Experts: The Auditor Program is typically led by experienced faculty members who have a thorough understanding of auditing practices and regulations. These professionals bring their industry expertise and practical insights into the training sessions, providing participants with valuable knowledge and guidance. In addition, guest lectures and workshops conducted by industry experts offer a broader perspective on auditing practices.8. Professional Certifications: Many Auditor Programs offer the opportunity to obtain professional certifications, such as Certified Internal Auditor (CIA) or Certified Public Accountant (CPA). These certifications are highly recognized in the auditing field and add significant value to participants' resumes, enhancing their career prospects.9. Continuous Learning and Development: The learning experience does not end with the completion of the Auditor Program. Many programs provide ongoing support and resources to help participants continue their professional development. This may involve access to specialized training materials, webinars, or networking events for alumni.10. Job Placement Assistance: Some Auditor Programs offer job placement assistance to their participants. They may have partnerships or connections with auditing firms, businesses, or other organizations, facilitating opportunities for internships or employment. Such assistance can be invaluable in jumpstarting participants' careers in auditing.11. Flexibility and Part-time Options: Depending on the program, participants may have the option to choose between full-time or part-time enrollment. This flexibility allows individuals to balance their current commitments, such as work or education, while pursuing the Auditor Program. Part-time options enable individuals to gain relevant skills and knowledge at their own pace.12. Career Paths in Auditing: The demand for qualified auditors continues to grow in both public and private sectors. As a result, completing an Auditor Program opens up a wide range of career opportunities. Participants can choose to work in auditing firms, financial institutions, government agencies, or private corporations. They may pursue careers as external auditors, internal auditors, forensic accountants, risk management specialists, or compliance officers.13. Continuous Professional Development: Once individuals embark on their auditing careers, continuous professional development becomes essential to stay updated with the latest auditing standards and regulations. Many Auditor Programs offer opportunities for ongoing education or advanced courses to help professionals enhance their skills and knowledge throughout their careers.Conclusion:The Auditor Program provides individuals with a comprehensive training and practical experience necessary to excel in the field of auditing. The program's curriculum, experienced faculty, industry connections, and professional certifications make it a valuableinvestment for aspiring auditors. With the continuous growth of the auditing field, completing an Auditor Program can pave the way for a rewarding and successful career.。

AGS_lecture_1

Lecture 1: Introduction to the module The context and role of auditing

Aims of the module

To examine the role of the audit as a means of accountability in organisations and society To develop knowledge of the purpose, structure and limitations of the audit process To critically evaluate the role of related functions within overall governance structures To examine some „scandals‟ and failures of corporate governance/audit, in order to illustrate the issues involved in corporate governance

Links to other learning

Try to link what you learn on this module with your other courses. There are strong links to financial accounting, but also to management accounting and other courses from areas such as management Financial Markets - does the nature of financial markets contribute to scandals? How do scandals impact financial markets? Which one drives the other? Management accounting, and accounting information systems - internal control issues and scandals Business Ethics - how does (un)ethical behaviour contribute to scandals?

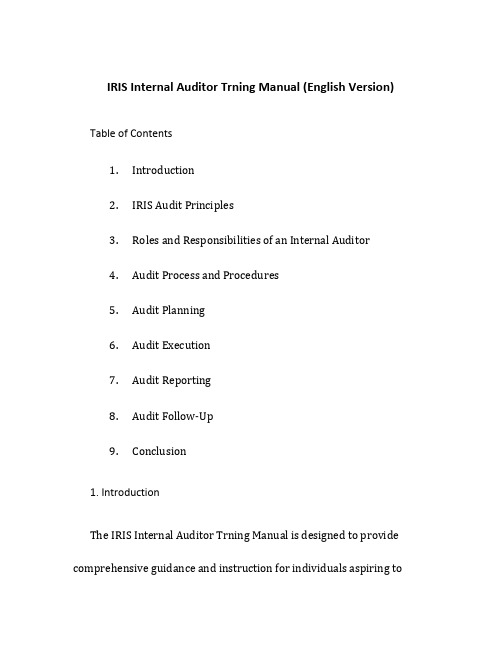

IRIS内审员培训教材英文版

IRIS Internal Auditor Trning Manual (English Version) Table of Contents1.Introduction2.IRIS Audit Principles3.Roles and Responsibilities of an Internal Auditor4.Audit Process and Procedures5.Audit Planning6.Audit Execution7.Audit Reporting8.Audit Follow-Up9.Conclusion1. IntroductionThe IRIS Internal Auditor Trning Manual is designed to provide comprehensive guidance and instruction for individuals aspiring tobecome internal auditors in the rlway industry. This manual outlines the essential knowledge, skills, and responsibilities required to effectively conduct internal audits within an organization.Internal auditing plays a critical role in ensuring compliance with the IRIS standards and mntning high-quality performance in the rlway industry. By completing this trning, auditors will develop a strong understanding of the IRIS audit principles and gn the necessary expertise to evaluate and improve the processes and systems within their organization.2. IRIS Audit PrinciplesIn this section, auditors will be introduced to the key principles underlying the IRIS audit process. These principles include:•Independence: Auditors must remn impartial and free from any conflicts of interest.•Competence: Auditors should possess the necessary knowledge, skills, and experience to effectively perform their duties.•Evidence-Based Approach: Auditors must base their conclusions and recommendations on objective evidence.•Risk-Based Approach: Audits should focus on areas with the highest risk in terms of non-compliance or inefficiency.•Improvement-Oriented: Auditors should m to identify opportunities for improvement and value creation.3. Roles and Responsibilities of an Internal AuditorThis section outlines the roles and responsibilities of an internal auditor within an organization. These include:•Conducting audits in accordance with the IRIS standards and audit procedures.•Evaluating the effectiveness and compliance of internal controls.•Identifying weaknesses or areas for improvement.•Preparing audit reports and communicating findings to management.•Facilitating corrective actions and monitoring their implementation.•Providing recommendations to enhance the organization’s overall performance.4. Audit Process and ProceduresIn this section, auditors will learn about the various stages of the audit process and the associated procedures. The audit process typically consists of the following steps:1.Planning: Defining the scope, objectives, and resourcesrequired for the audit.2.Execution: Conducting on-site inspections, interviews, anddocumentation review.3.Reporting: Presenting findings, conclusions, andrecommendations in a comprehensive report.4.Follow-up: Assessing the implementation of correctiveactions and verifying their effectiveness.5. Audit PlanningEffective audit planning is crucial for conducting successful audits. This section provides auditors with guidance on how to plan their audits, including:•Determining the audit objectives, scope, and criteria.•Assessing the organization’s risks and controls.•Developing an audit plan and schedule.•Gathering necessary resources and documentation.•Communicating the audit plan to key stakeholders.6. Audit ExecutionIn this section, auditors will learn how to execute the audit plan effectively. This includes:•Conducting on-site inspections and interviews.•Collecting and analyzing data and evidence.•Assessing compliance with IRIS standards and regulatory requirements.•Investigating identified issues and discrepancies.•Mntning professionalism and ethical conduct throughout the audit process.7. Audit ReportingThis section provides guidance on how to prepare and present comprehensive audit reports. Key topics covered include:•Structuring the audit report to effectively communicate findings and recommendations.•Including relevant supporting evidence and documentation.•Presenting findings and conclusions in a clear and objective manner.•Facilitating constructive discussions with management based on the audit report.•Ensuring that audit reports are accurate, complete, and timely.8. Audit Follow-UpThe follow-up process is essential to ensure the resolution of audit findings and the implementation of corrective actions. This section covers:•Verifying the effectiveness of implemented corrective actions.•Assessing the closure of audit findings.•Monitoring and reporting on the progress of corrective actions.•Facilitating the resolution of any unresolved issues or non-compliance.9. ConclusionThe IRIS Internal Auditor Trning Manual provides aspiring auditors with the knowledge, skills, and tools required to conduct effective internal audits in the rlway industry. By following the principles, processes, and procedures outlined in this manual, auditors can contribute to the continuous improvement and enhanced performance of their organization.Note: This trning manual is for informational purposes only and should not be considered as a substitute for professional trning and certification in internal auditing.。

英文课外阅读

英文课外阅读作文是英语考试的重中之重,英语作文要多练习多背诵,好的句子模板背下来,写的时候就能够灵活套用,今天小编给大家整理了一些好的文章,大家可以阅读一下,提高自己的英语水平。

课外阅读1Don't overpack when you go to college and pack for the climate that you are in.当你去学校的时候不要带太多的东西,只带适合你所处氛围的东西。

Remember that ironing can become tiring and is not the most exciting college activity. Drycleaning bills do add up also. Consider packing clothes that wrinkle less and clothes that don'tneed dry cleaning.请记住在大学活动中,熨烫衣服是一件很累,而且并不那么有劲的事情。

干洗的费用也不那么便宜。

你得考虑带一些不容易起皱、不需要干洗的衣服。

Meet as many fellow students as you can during orientation. It's a great time to meeteveryone. Sometimes the people you meet during orientation become your best friends.在新生教育的时候尽可能多地认识你的同学。

这是个认识新伙伴的绝佳机会。

有时候你在新生教育中认识的人会成为你最好的朋友。

Get well acquainted with your campus and explore the campus, the buildings, and its history. Go into buildings that you would otherwise not go into.好好地认识你的校园,并且探索这一校园中的建筑和它们的历史。

Accounting-Lesson 5 Introduction to Auditing

7

Distinguish between auditing会计an是d对经ac济c事o项u进n行ti记ng

录、分类和汇总,其目的

Accounting is the是re为c决or策d提信in供息g,所。c需la的ss财if务ying, and summarizing of economic events for the purpose of providing审fi计n是an确c定ial所in记f录or的m信at息ion used in decision making. 是否恰当地反映了会计期

Auditing can have a significant effect on (reduce) information risk.

9

Types of Audits

External

Operational

CPA

Compliance

Financial Statement

Governmental

Consumers Union)

17

Attestation Services (鉴证服务)

• An attesta鉴t证io服n务s是e注rv册ic会e计s师is提o供n的e type of

assurance se一rv种ic保e证s 服pr务o,vi在de这d种b服y务C中PA,s, in which the CP会A计fi师rm事务is所su就e另s 一a 主re体p所or做t about the reliability的o书f 面an认个定a书s之s面e可报r靠t告io性。n而t出ha具t一is made by another party.

证据时带有偏见,其审计的

An independent men价ta值l 也at将tit荡ud然e:无存。

托付机经

小马机经5月24日逆天版独立口语更多托福资料加入:托福吧交流群231581158SPEAKING11、★★★★★Choose one of your favorite methods to relax and explain why it is your favorite.Please include specific details in your explanation.2、★★★★★Describe a skill you are good at,for example,painting or a kind of sport,and explain why it is important to you.Please include specific examples and details in your explanation.3、★★★★★A school is planning to organize it students to visit the workplace. Which place do you recommend the students to visit? 1.A science lab 2.A business office 3.A TV studio4、★★★★★Describe the steps,through which you once learned a new subject and explain how you learned it.Please include details and examples in your response.5、★★★★★It is generally agreed that society benefits from the work of its members.Which type of contribution do you think is most valued by your society:that of primary school teachers,artists or nurses?Why?6、★★★★★Your friend has suddenly received a lot of money.What do you think is the best way for your friend to spend this money?Include reasons and details to support your response.7、★★★★★what do you think we should do to decrease the usage of car or other vehicle and solve the traffic problems?8、★★★★★Choose ONE of the forms of the technology in the list and tells why it changes(has had great impact)people's lives in your country?a)The airplane b)The computer c)The Television9、★★★★★Compare the differences between two singers you like.Include specific reasons and details in your explanation.10、★★★★★What do you think is the most significant benefit that internet brings to our life?Explain why you think this benefit is import.Include reasons and details to support your response.11、★★★★★Describe the most important decision you’ve ever made in your life. Explain why it’s important.12、★★★★★What quality is the most important to be a university student:highly motivated,hard working,or intelligence?Using details and examples to support you idea.13、★★★★★Talk about an experience of learning something new.What difficulties do you have to overcome in order to learn it?14、★★★★★Describe a present you have given to others.Explain why you think it is important.15、★★★★★Which of the following do you think is the best way to get to know a new school? 1.Joining a one-day campus tour 2.Spending a weekend on the campus play field 3.Auditing lectures?16、★★★★What time of a year do you like the most?Explain why you like this time of a year.17、★★★★If a high school is planning to organize an after-school activity forits students,what kind of activity would you recommend and why?18、★★★★Which form of transportation is the most enjoyable?Bicycle,automobile, train?19、★★★★Describe a special event or occasion that you have participate with your family or friends.Give Specific details and examples to explain your answer.20、★★★★Talk about an activity you would like to participate in the near future, explain your answer in details.21、★★★★Among the following three activities,which do you think has the most benefits for students? 1.A field trip 2.A home tutoring session 3.A presentation given by a local leader22、★★★★Talk about a time when someone(your friends,family or teachers)gave you advice to solve the problem.23、★★★★Talk about a skill that you have mastered but you still want to improve24、★★★★Which of the following activities do you prefer to do with friends? Taking a walk,going to a movie,traveling to another city.25、★★★★Your friend wants to have a more healthy eating habit.What suggestions would you give to this friend?26、★★★★What is your favorite place to study?Give details and examples in your response.27、★★★★Describe how cellphones change people’s lives.Please give your answer with specific examples and details28、★★★★If a foreign visitor comes to your country,what food will you introduce to him/her?Explain why.29、★★★★Many regions in the world face problems with air pollution.What can be done to decrease the amount of air pollution in these regions?Use details and examples in your response.30、★★★★Describe a person that you look up to as a role model.Explain how this person influenced your life.Include details and examples to support your response.SPEAKING21、★★★★★Some people like to plan their free time.Other people spend their free time without any plan.Which do you prefer.2、★★★★★If you were given an empty pieces of land,would you rather using it to build a garden or a playground for children?3、★★★★★Do you agree or disagree with the statement?Teachers should make their lessons fun.4、★★★★★Some students prefer to go to universities or colleges in their own cities or towns.Others prefer to go to universities or colleges in new cities or towns.Which do you prefer and why?Include details and examples in your explanation.5、★★★★★Some students prefer to work on their course paper one or two days before its due date.Others like to work on the paper bit by bit every day.Which do you prefer and why?6、★★★★★Instead of always being busy,one should have a relaxed life style.Do you agree or disagree with the above statement?Why or why not?Use specific reasons and examples to support your answer.7、★★★★★Some people prefer to live in a place most of their life.Other people prefer to move to different places.Which do you prefer and why?Use specific reasons and examples to support your response.8、★★★★★Which do you think is more important for someone to be successful: taking risks or making safe decisions?9、★★★★★some people prefer to visit only one place during their vacations, others prefer to visit lots of places,which one do you prefer and why?10、★★★★★Do people nowadays lead a healthier lifestyle than people100years ago?11、★★★★★Do you agree or disagree with the statement that it's important for students to study Art and Music in school.Explain your answer in details.12、★★★★★Do you agree or disagree with the statement:artists and musicians are important to our society.13、★★★★★Some people believe that it is better for small children to grow up in a small town.Others,however,believe that it’s better for them to grow up in a big city.Which do you think is better?Do you agree or disagree with the following statement:it is better to be a leader in a group than a supporting member?Use examples anddetails in your explanation.15、★★★★★which one do you prefer,shopping in a large store or shopping in a small store?16、★★★★Some people prefer to do one job or project at one time.Other people prefer to do several jobs or projects at the same time.Which do you prefer and why?17、★★★★Do you agree or disagree with the following statements?Personality changes with e specific reasons to support your answer.18、★★★★Do you agree or disagree with the statement?If you want to be successful in running a business,it is important to have a friendly and outgoing personality.19、★★★★Do you agree or disagree that advertisements have influence on people’s purchasing.20、★★★★Do you prefer to live in an area that is noisy but close to shops or public transportation,or an area that is quiet but far away from shops and public transportation?21、★★★★Do you agree or disagree?The most important influence that young adults have are from their families.22、★★★★Some people consider going to the gym a priority in their life,while others go to the gym only when they have time.Which do you think is better and why?Some people argue that people born with natural abilities are morelikely to succeed.Other people believe success can be achieved through hard work.What's your opinion?24、★★★★Some people think students should study in the classroom while others believe they should visit the museum or the zoo.Which do you prefer and why?25、★★★★Do you agree or disagree with the following statement?The success of a school largely depends on the resources it has such as textbooks and journals.26、★★★★Do you prefer to live in a residence where there are strict rules(such as rules against making loud noises at night),or do you prefer to live in a residence without strict rules.27、★★★★When going on a vacation,some people prefer to stay in a hotel,while others prefer to camp outside in a tent.Which do you prefer?28、★★★★Do you agree or disagree with the following statement?University students should learn how to manage their time more efficiently.29、★★★★Some people prefer to have a very tight schedule,while others prefer to have more free time in their schedule.Which one do you prefer and why?30、★★★★Some students like to learn by themselves,others prefer to share their ideas with others.Which one do you prefer?。

英国大学大三Auditing审计课件Lecture1

Introduction

Assessment: (i) assignment - (to be issued on MOLE ) - counts for 30%; and is due to be handed in electronically by noon on Monday 16 November 2015 (ii) 2 hour unseen exam – counts for 70%. Feedback on the course assignment will be given prior to the end of the module. Please use your feedback to help you identify any weaknesses/strengths so that you can make use of this in preparing for the exam.

TUTORIALS – please check your timetable Wednesdays 9-10, 10-11 and 11-12 Thursdays 11-12, 12-1, 2-3, 3-4

Textbooks and main readings – see reading list

Porter,

B., Simon, J. and Hatherly, D.(2014), Principles of External Auditing, fourth edition, Wiley. Available at Blackwells. See also library links in reading list. Other information available on MOLE NB Guidance re use of text book to be given in lecture

Chapter 2 Instructor's Guide

Chapter 2The CPA ProfessionIn Chapter 1, students learned about the demand for assurance services and the different types of audits. Chapter 2 describes the CPA profession, and the standards that govern audit performance.Chapter Opening Vignette –“Good Auditing Includes Good Client Service”This vignette demonstrates that auditors are expected to provide value-added services to clients. The vignette also challenges preconceived notions about the role of auditors, and illustrates that students will be in a position to assist clients immediately upon entering the profession. We use this as an opportunity to discuss the performance expected of new auditors, and that students need to be familiar with real-world activities by reading such sources as the Journal of Accountancy and The Wall Street Journal.Certified Public Accounting Firms and their Activities (page 26, page 27)Many students will be familiar with the “Big 4” and the activities of these firms, but many will not. Most students will have little knowledge of other CPA firms. In a brief lecture, we tell students:⏹The four categories of CPA firms⏹The names of the Big 4, plus several major firms in the other categories thatrecruit at our universities⏹Changes occurring in each category of firmsWe briefly discuss the demise of the Andersen firm, and then ask students for their perceptions about why there have been other changes among the Big 4 and National firms. We use this as an opportunity to discuss the forces affecting the profession. We are careful not to offer opinions about the desirability of these changes, or preferences for one firm or category of firm versus another.We briefly mention the major activities of the firms (audit and assurance services, taxes, and consulting). We also note the changes that have occurred in the Big 4 involving the sale or separation of consulting practices. Table 2-1 (page 26) is helpful in describing the relative size of firms in each category, and the relative importance of each activity. We encourage students to learn more about the major CPA firms by visiting their web sites.(See Table 2-1)Structure of CPA Firms (page 28)We briefly describe the six organizational structures of CPA firms. We emphasize the use of limited liability corporations and partnerships. We ask students to evaluate the desirability of these organizational forms as a potential new entrant into the profession, from the perspective of a partner, and the perspective of an investor.We use Table 2-2 (page 29) to describe the typical positions in a CPA firm, the responsibilities of the position, and how long a person stays in each category. We emphasize that technology has increased the responsibility given new staff, and that advancement is fairly rapid.(See Table 2-2)Sarbanes–Oxley Act and PCAOB (page 30)We discuss the origins of the Sarbanes–Oxley Act and the significant changes it has brought to financial reporting and the accounting profession. We then discuss the role of the PCAOB in establishing auditing and quality control standards for registered firms with public company audit clients. We clarify that the PCAOB oversight is limited to public company audits. We also note that while the PCOAB has adopted GAAS as interim auditing standards, the PCAOB is establishing new auditing standards for public company audits. Problem 2-18 is good for discussing the costs and benefits of the Sarbanes–Oxley Act.Securities and Exchange Commission (SEC) (page 31)The four most important things to explain to students about the SEC are:1. Role of the SEC in general and as it relates to auditors.2. What companies are required to report to the SEC.3. Differences between the AICPA and SEC and relation between the PCAOBand SEC.4. How the SEC influences auditing.AICPA (page 32)We talk briefly of the role of the AICPA, with emphasis on its responsibility for the CPA exam and establishing standards and rules. We also hand out student subscription forms to the Journal of Accountancy that we get free directly from the AICPA. We encourage students to subscribe.We describe the CPA Vision Project, and how the profession is responding to the changes affecting the profession. We discuss the major influences on the future of the profession and encourage students to visit the CPA Vision Project web site.Generally Accepted Auditing Standards (page 33)First, it is useful to introduce generally accepted auditing standards by using Review Question 2-8. Students are told they are required to know the ten standards (not word for word), and which standards are general, field work, and reporting.At that point, it is helpful to set up a summary to aid in discussing GAAS. The summary is on T-2-1. (As an alternative use Figure 2-1, page 35.) We highlight the change to the second standard of fieldwork requiring the auditor to understand the entity and its environment.(See T-2-1)(See Figure 2-1)Problem 2-21 is a good one to help students understand the applications of GAAS to practice.Statements on Auditing Standards (page 36)We briefly explain the role of Statements on Auditing Standards. We explain the classification systems used to allow students to refer to SASs when necessary. International Standards on Auditing (page 37)We note that globalization has increased the need for uniform international accounting and auditing standards. We do not discuss specific differences in international and U.S. auditing standards, but encourage students to use the Internet to learn more about the International Federation of Accountants.Quality Control (page 37)With the increased emphasis on quality control in the profession, we discuss both quality control and peer review briefly. Emphasize the purposes, benefits, and costs of both. Problem 2-19 is useful for defining the five elements of quality control.Students often have difficulty understanding the relation between quality control and peer review. A useful analogy is to describe peer review as an audit of the firm’s quality control system. Figure 2-2(page 39) is helpful in describing the relation between audit standards, quality control, peer review, and the AICPA practice sections.(See Figure 2-2)SummaryAfter covering Chapters 1 and 2, students have an understanding of the value of audit and assurance services, and some of the factors that affect auditor performance. Figure 2-3 (page 40) provides a useful summary of these factors, and can be used to introduce the concepts of professional ethics and legal liability covered in Chapters 4 and 5.(See Figure 2-3)CHAPTER 2CROSS-REFERENCE OF LEARNING OBJECTIVES AND PROBLEM MATERIAL2-4GENERALLY ACCEPTED AUDITING STANDARDS GENERAL●Adequate technical training and proficiency●Independence●Due professional careFIELD WORK●Adequate planning and supervision●Sufficient understanding of the entity and itsenvironment, including its internal control●Sufficient appropriate evidenceREPORTING●Generally accepted accounting principles●Consistency●Informative disclosures●Opinion regarding the financial statements takenas a whole。

Lecture 2

Joint Joint Joint

La Trobe Business School

Overriding responsibilities of planners

Know your client

-how do you determine and document this?

Know your products -how do you determine and document this?

??? ??? Wealth creation, retirement planning Wealth drawdown or maintenance, social security planning, estate planning, aged care accommodation

La Trobe Business School

•

•

• • •

Data collection Determining goals and objectives Identifying problem areas and analysing the client’s financial circumstances Making appropriate recommendations in terms of both the advice and investment products Review over time to ensure continued appropriateness

Data collection

What is the purpose? The data collection process assists you understand

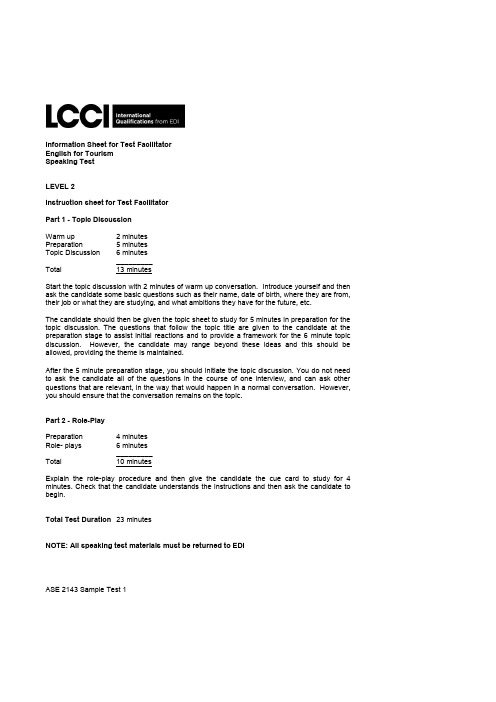

ASE 2143 Level 2 英语语音对话实践测试指导书说明书

Information Sheet for Test FacilitatorEnglish for TourismSpeaking TestLEVEL 2Instruction sheet for Test FacilitatorPart 1 - Topic DiscussionWarm up 2 minutesPreparation 5 minutesTopic Discussion 6 minutes_________Total 13 minutesStart the topic discussion with 2 minutes of warm up conversation. Introduce yourself and then ask the candidate some basic questions such as their name, date of birth, where they are from, their job or what they are studying, and what ambitions they have for the future, etc.The candidate should then be given the topic sheet to study for 5 minutes in preparation for the topic discussion. The questions that follow the topic title are given to the candidate at the preparation stage to assist initial reactions and to provide a framework for the 6 minute topic discussion. However, the candidate may range beyond these ideas and this should be allowed, providing the theme is maintained.After the 5 minute preparation stage, you should initiate the topic discussion. You do not need to ask the candidate all of the questions in the course of one interview, and can ask other questions that are relevant, in the way that would happen in a normal conversation. However, you should ensure that the conversation remains on the topic.Part 2 - Role-PlayPreparation 4 minutesRole- plays 6 minutes_________Total 10 minutesExplain the role-play procedure and then give the candidate the cue card to study for 4 minutes. Check that the candidate understands the instructions and then ask the candidate to begin.Total Test Duration 23 minutesNOTE: All speaking test materials must be returned to EDIENGLISH FOR TOURISMSPEAKING TESTPart 1 – Topic discussionTOPIC SHEET (Candidate Copy)Instructions to the candidateYou have 5 minutes to prepare for your examination. The subject matter is given in the topic below. You have to discuss this topic with the Test Facilitator and you will be expected to do most of the talking.To help you in putting your ideas together, the topic is followed by some questions and suggestions for the basis of your conversation. However, you may introduce other ideas providing they are on the topic. You may keep this paper to help you during the examination. Return it to the Test Facilitator at the end of the examination. Do not make any written notes during this preparation time.The Topic: BUSINESS TRAVEL1 Suggest some reasons why people travel for business purposes.▪Although business communication can be made by email and by telephone, there are many reasons why the modern business executive has to travel in connectionwith their work or profession.2Explain some of the differences between the leisure traveller and the business traveller.▪Think about who pays for the trip, when business trips take place, the duration, the kind of destination, the amount of time in advance needed to plan the trip.3 Consider the different requirements and the similarities of the business and theleisure traveller.▪Suggest the sort of facilities and amenities needed for the modern day business traveller and compare this to the requirements of the leisure traveller.▪Also discuss the facilities that may be wanted by both types of travellers.4 Discuss how travel arrangements are organised for the business person.▪Some large organisations have their own travel departments who plan and provide the travel documentation. Other organisations may use the services of thebusiness travel department of travel agencies. Do you think that special training isrequired? Is it necessary for a business travel agent to have visited many countriesor so that they can advise clients about different travel destinations and thebusiness culture of the country?5 Consider job roles of a business travel agent and the personal qualities and skillsrequired.▪For a person travelling to an important business meeting or conference, it is essential that the trip is well organised and that facilities are selected that are bothefficient, cost effective and create the correct image to impress their clients or otherorganisations. Travel plans that go wrong could cause great problems for thebusiness traveller. Suggest the most important functions of this role and thequalities and skills that a good business travel agent should have.TOPIC SHEET (Test Facilitator’s Copy)The Topic: BUSINESS TRAVEL1 Suggest some reasons why people travel for business purposes.▪Although business communication can be made by email and by telephone, there are many reasons why the modern business executive has to travel in connectionwith their work or profession.2Explain some of the differences between the leisure traveller and the business traveller.▪Think about who pays for the trip, when business trips take place, the duration, the kind of destination, the amount of time in advance needed to plan the trip.3 Consider the different requirements and the similarities of the business and theleisure traveller.▪Suggest the sort of facilities and amenities needed for the modern day business traveller and compare this to the requirements of the leisure traveller.▪Also discuss the facilities that may be wanted by both types of travellers.4 Discuss how travel arrangements are organised for the business person.▪Some large organisations have their own travel departments who plan and provide the travel documentation. Other organisations may use the services of thebusiness travel department of travel agencies. Do you think that special training isrequired? Is it necessary for a business travel agent to have visited many countriesso that they can advise clients about different travel destinations and the businessculture of the country?5 Consider job roles of a business travel agent and the personal qualities and skillsrequired.▪For a person travelling to an important business meeting or conference, it is essential that the trip is well organised and that facilities are selected that are bothefficient, cost effective and create the correct image to impress their clients or otherorganisations. Travel plans that go wrong could cause great problems for thebusiness traveller. Suggest the most important functions of this role and thequalities and skills that a good business travel agent should have.Background notes for Test Facilitator:1 Suggest the reasons why people travel for business purposes.▪The purpose could be a meeting with colleagues of the same international company, an organisation representing people and companies of the sameprofession, a meeting with a client or customer. The business traveller could alsobe attending a conference or exhibition to learn about new products, update skillsand knowledge in a specific field. They could be looking for new businessopportunities.2Explain some of the differences between the leisure traveller and the business traveller.▪The business traveller will not have a choice of destination and may need to be in a specific location at a specific date and time regardless of the cost (e.g. to attend aconference). Travel destinations will usually be city centres and industrialised oremerging countries.▪Business trips often avoid holiday periods such as July and August, and religious festivals, and take place Monday to Friday. The business person cannot normallydetermine the duration of the trip. The travel costs and expenses will usually bepaid for by the employer or organisation.▪The leisure traveller can be more flexible and will select their destination, the duration of the trip, the type of accommodation and transportation that they canafford and for which they will pay for personally. Destinations may includeinteresting cities, seaside resorts, mountain or countryside locations for relaxation,special interests and hobbies or sporting activities. They may also be visitingfriends and relatives.3. Consider the different requirements and the similarities of the business and theleisure traveller.▪Business travellers often require accommodation which will provide a working area and business facilities such as internet access. 3 to 5 star hotels are the mostpopular choice. They will choose accommodation that is comfortable, efficient, andis in proximity to the purpose of their trip e.g. meeting, conference, exhibition etc.They may also require the accommodation to be located where there are goodtransportation links to airports, railway stations, etc.▪The leisure tourist may choose hotel accommodation across the complete range from budget to luxury or opt for self catering. They may be happy to travelconsiderable distances from airport or station to their chosen holiday destinationand will select from a wide choice of facilities.▪However,business travellers may overlap with leisure tourists for some of their desired requirements and choose accommodation or a location with some leisurefacilities such as a gym, sports facilities, evening entertainment, restaurants,sightseeing, etc.4 Discuss how the travel is organised for the business person.▪Large organisations often have their own travel departments who plan and provide documentation, the necessary travel, information on visas, currency, destinationinformation, local travel information, advice on health and the business culture ofthe country to be visited.▪It is quite common for these organisations to agree contracts with airlines, etc. to reduce the costs of business travel for their employees. Other companies andorganisations may use the services of the business travel department of specialisedtravel agencies, who quite often are able to offer similar advantages and services.5 Consider the job roles of a business travel agent and the personal qualities andskills required.▪Special training is required to understand the needs of the business traveller. Most travel organisers have already received general training in booking elements oftravel, checking on important additional information including visas and healthrequirements for the destination and providing appropriate documentation. Trainingmay have included travel geography and navigating sources of information(manuals, guides, computerised travel systems and the internet)▪It is essential that a trips are well organised and that selected facilities are efficient, cost effective and create the correct image to impress their clients or otherorganisations.▪For the business traveller, getting to an important meeting on time and having the facilities they require can be essential to their business. Therefore the specialisedtravel advisor can offer a very important function when buying these products.▪It is most important to be very well organised, to have good inter-personal skills and an unders tanding of their clients’ needs together with the ability to negotiate andcost accurately. The business travel advisor must be able to offer a comprehensiveknowledge of the travel industry and the way it works.Part 2 – Role Play (Candidate Copy)AT THE BUSINESS TRAVEL DEPARTMENTInstructionsTest Facilitator to:▪explain the procedure (the candidate is the person working as a business travel agent and the test facilitator is the client)▪give the candidate the Cue Card to study for 4 minutes (the candidate may keep hold of the cue card for the duration of the test)▪check that the candidate understands the key vocabulary and instructions▪initiate and guide the dialogue using the cue card and guided dialogue for reference Candidate to:▪study the Cue Card for 4 minutes▪respond to the test facilitator as indicated on the Cue CardPart 2 – Role Play (Test Facilitator’s Copy)InstructionsTest Facilitator to:▪ explain the procedure (the candidate is the person working as a business travel agentand the test facilitator is the client ▪give the candidate the Cue Card to study for 4 minutes (the candidate may keep hold ofthe cue card for the duration of the test)▪ check that the candidate understands the key vocabulary and instructions▪ initiate and guide the dialogue using the cue card and guided dialogue for referenceCandidate to:▪ study the Cue Card for 4 minutes▪ respond to the Test Facilitator as indicated on the Cue CardGuided Dialogue (for test facilitators reference)C Good morning/afternoon. I am (name) thank you for coming in to see me.TF Good morning/afternoon. As we discussed on the phone, I have a rather complicated series of meetings to attend and hope that you can help me to plan all the travelarrangements.C Of course. Can you give me some details?TF I have three meetings in the Far East. 2 of the meetings are in China and one is in Thailand.C Do you have dates yet?TF Yes, the first meetings will be in China. Beijing on the 14th to 16th April and then I travel on to Shanghai for the second meeting on the 20th April. Finally, I need to be in Bangkok for the 24th April. My company has agreed that I can take 2 extra nights at the end for some relaxation before flying back.C I assume you want to stay in good hotels?TF Yes, 4 or 5 star hotel accommodation. I need plenty of space to work on my computer and for the sample products I will have with me.C I’ve noted everything. Now do you have a preference for which airline you fly with?TF I prefer British Airways for the long-haul flights but I don’t mind which airline I use for the internal flight or the flight between China and Thailand, as long as there are no very early morning flights.C Have you had injections for travel in the Far East?TF I think I have had everything I need but I would be grateful if you would double check on the requirements for me. I do need advice on visa requirements?If you have any information or hints on doing business in China, I would also be verypleased to have this. I don’t want to make any embarrassing mistakes.C I have noted all your requirements and will prepare a suggested itinerary and breakdownof costs for you, together with health and visa requirements and hints on business culture in China.TF Please call me when they are ready.C Of course, thank you for coming in to see me.。

学术英语视听说2课文

学术英语视听说2课文英文回答:In the academic English listening and speaking 2 textbook, we explore a wide range of topics essential for navigating academia in the English language. These include:Developing Your Academic Vocabulary: This section focuses on expanding your vocabulary in various academic disciplines, such as social sciences, humanities, and natural sciences. You will learn specialized terms, idiomatic expressions, and academic synonyms.Note-Taking and Summarizing: Here, you will acquire strategies for effective note-taking during lectures and while reading academic texts. You will also practice summarizing main points and conveying complex informationin a concise and coherent manner.Critical Thinking and Analysis: This section trainsyou to analyze and evaluate academic arguments, identifying their strengths and weaknesses. You will learn to question assumptions, consider multiple perspectives, and form well-reasoned judgments.Academic Writing and Editing: In this part, you will develop your skills in writing clear, concise, and grammatically correct academic texts. You will cover various writing formats, such as research papers, essays, and presentations.Academic Speaking and Presentation: Here, you will develop confidence in delivering effective academic presentations and engaging in academic discussions. Youwill learn techniques for organizing your thoughts, using appropriate language, and presenting your ideas clearly and engagingly.Intercultural Communication: This section focuses on the importance of intercultural communication in academic and professional settings. You will explore different cultural perspectives, communication styles, and strategiesfor effective cross-cultural interactions.Pronouncing English Clearly: This section provides guidance on improving your English pronunciation forclarity and comprehensibility. You will practice key pronunciation patterns, such as word stress, intonation,and linking sounds, to enhance your speaking abilities.中文回答:学术英语视听说2教材是一本综合性的教材,旨在帮助学生掌握在英语学术环境中必备的技能,主要包括以下几个方面:学术词汇的学习,此部分着重于扩展你在不同学术领域(如社会科学、人文科学、自然科学)中的词汇量。

审计英语课件第二章

GENERAL STANDARDS

The

general standards stress the important personal qualities that the auditor should possess.

1. The audit is to be performed by a person or persons having adequate technical training and proficiency as an auditor. 2. In all matters relating to the assignment, an independence in mental attitude is to be maintained by the auditor or auditors. 3. Due professional care is to be exercised in the planning and performance of the audit and the preparation of the report.

STANDARDS OF FIELD WORK

The

standards of field work concern evidence accumulation and other activities during the actual conduct of the audit.

1. The work is to be adequately planned and assistants, if any, are to be properly supervised. 2. A sufficient understanding of internal control is to be obtained to plan the audit and to determine the nature, timing, and extent of tests to be performed. 3. Sufficient competent evidential matter is to be obtained through inspection, observation, inquiries, and confirmations to afford a reasonable basis for an opinion regarding the financial statements under audit.

注会《审计》英语常用词汇

注会《审计》英语常用词汇1.audit 审计2.attestation 鉴证3.credibility 可信赖程度4.audit of financial statements 财务报表审计5.agreed-upon procedures 执行商定程序6.high levels of assurance 高水平保证pilation 编制8.reliability 可靠性9.relevance 相关性10.professional skepticism 职业谨慎11.objectivity 客观性12. professional competence 专业胜任能力13.Senior/CPA-in-charge 项目经理14.audit engagement letter 业务约定书15.recurring audit 连续审计16.the client 委托人17.change CPA 更换注册会计师18.the existing CPA 现任注册会计师19.the successor CPA 后任注册会计师20.the preceding CPA前任注册会计师21.issue the audit report 出具审计报告22.expert 专家23.the board of directors 董事会24.knowledge of the entity‘ s business 了解被审计单位情况25.assess material misstatement risks评估重大错报风险26.detemine the nature, timing and extent of the audit procedures 确定审计程序的性质、时间和范围27.a general knowledge of ——初步了解―――的情况28.a more knowledge of——进一步了解的情况29.the prior year‘s working papers 以前年度工作底稿30.minutes of meeting 会议纪要31.business risks 经营风险32.appropriateness 适当性33.accounting estimate 会计估计34.management representations 管理层声明35.going concern assumption 持续经营假设36.audit plan 审计计划37.significant audit areas 重点审计领域38.error 错误39.fraud舞弊40.modified or additional procedures 修改或追加审计程序41.misappropriation of assets 侵占资产42.transactions without substance 虚假交易43.unusual pressures 异常压力44.the suspected noncompliance 涉嫌存在违法行为45.materialiy 重要性46.exceed the materiality level 超过重要性水平47.approach the materiality level 接近重要性水平48.an acceptably low level 可接受水平49.the overall financial statement level and in related account balances and transaction levels 财务报表层和相关账户、交易层50.misstatements or omissions 错报或漏报51.aggregate 总计52.subsequent events 期后事项53.adjust the financial statements 调整财务报表54.perform additional audit procedures 实施追加的审计程序55.audit risk 审计风险56.detection risk 检查风险57.inappropriate audit opinion 不适当的审计意见58.material misstatement 重大的错报59.tolerable misstatement 可容忍错报60.the acceptable level of detection risk 可接受的检查风险61.assessed level of material misstatement risk 重大错报风险的评估水平62.simall business 小规模企业63.accounting system 会计系统64.test of control 控制测试65.walk-through test 穿行测试munication 沟通67.flow chart 流程图68.reperformance of internal control 重新执行69.audit evidence 审计证据70.substantive procedures 实质性程序71.assertions 认定72.esistence 存在73.occurrence 发生pleteness 完整性75.rights and obligations 权利和义务76.valuation and allocation 计价和分摊77.cutoff 截止78.accuracy 准确性79.classification 分类80.inspection 检查81.supervision of counting 监盘82.observation 观察83.confirmation 函证putation 计算85.analytical procedures 分析程序86.vouch 核对87.trace 追查88.audit sampling 审计抽样89.error 误差90.expected error 预期误差91.population 总体92.sampling risk 抽样风险93.non- sampling risk 非抽样风险94.sampling unit 抽样单位95.statistical sampling 统计抽样96.tolerable error 可容忍误差97.the risk of under reliance 信赖不足风险98.the risk of over reliance 信赖过度风险99.the risk of incorrect rejection 误拒风险100. the risk of incorrect acceptance 误受风险101.working trial balance 试算平衡表102.index and cross-referencing 索引和交叉索引103.cash receipt 现金收入104.cash disbursement 现金支出105.bank statement 银行对账单106.bank reconciliation 银行存款余额调节表107.balance sheet date 资产负债表日 realizable value 可变现净值109.storeroom 仓库110.sale invoice 销售发票111.price list 价目表112.positive confirmation request 积极式询证函113.negative confirmation request 消极式询证函114.purchase requisition 请购单115.receiving report 验收报告116.gross margin 毛利117.manufacturing overhead 制造费用118.material requisition 领料单119.inventory-taking 存货盘点120.bond certificate 债券121.stock certificate 股票122.audit report 审计报告123.entity 被审计单位124.addressee of the audit report 审计报告的收件人125.unqualified opinion 无保留意见126.qualified opinion 保留意见127.disclaimer of opinion 无法表示意见128.adverse opinion 否定意见A (1)ABC 作业基础成本计算A (2)absorbed overhead 已吸收制造费用A (3)absorption costing 吸收成本计算A (4)account 账户,报表A (5)accounting postulate 会计假设A (6)accounting series release 会计公告文件A (7)accounting valuation 会计计价A (8)account sale 承销清单A (9)accountability concept 经营责任概念A (10)accountancy 会计职业A (11)accountant 会计师A (12)accounting 会计A (13)agency cost 代理成本A (14)accounting bases 会计基础A (15)accounting manual 会计手册A (16)accounting period 会计期间A (17)accounting policies 会计方针A (18)accounting rate of return 会计报酬率A (19)accounting reference date 会计参照日A (20)accounting reference period 会计参照期间A (21)accrual concept 应计概念A (22)accrual expenses 应计费用A (23)acid test ration 速动比率(酸性测试比率)A (24)acquisition 购置A (25)acquisition accounting 收购会计A (26)activity based accounting 作业基础成本计算A (27)adjusting events 调整事项A (28)administrative expenses 行政管理费A (29)advice note 发货通知A (30)amortization 摊销A (31)analytical review 分析性检查A (32)annual equivalent cost 年度等量成本法A (33)annual report and accounts 年度报告和报表A (34)appraisal cost 检验成本A (35)appropriation account 盈余分配账户A (36)articles of association 公司章程细则A (37)assets 资产A (38)assets cover 资产保障A (39)asset value per share 每股资产价值A (40)associated company 联营公司A (41)attainable standard 可达标准A (42)attributable profit 可归属利润A (43)audit 审计A (44)audit report 审计报告A (45)auditing standards 审计准则A (46)authorized share capital 额定股本A (47)available hours 可用小时A (48)avoidable costs 可避免成本B (49)back-to-back loan 易币贷款B (50)backflush accounting 倒退成本计算B (51)bad debts 坏帐B (52)bad debts ratio 坏帐比率B (53)bank charges 银行手续费B (54)bank overdraft 银行透支B (55)bank reconciliation 银行存款调节表B (56)bank statement 银行对账单B (57)bankruptcy 破产B (58)basis of apportionment 分摊基础B (59)batch 批量B (60)batch costing 分批成本计算B (61)beta factor B(市场)风险因素B (62)bill 账单B (63)bill of exchange 汇票B (64)bill of landing 提单B (65)bill of materials 用料预计单B (66)bill payable 应付票据B (67)bill receivable 应收票据B (68)bin card 存货记录卡B (69)bonus 红利B (70)book-keeping 薄记B (71)Boston classification 波士顿分类B (72)breakeven chart 保本图B (73)breakeven point 保本点B (74)breaking-down time 复位时间B (75)budget 预算B (76)budget center 预算中心B (77)budget cost allowance 预算成本折让B (78)budget manual 预算手册B (79)budget period 预算期间B (80)budgetary control 预算控制B (81)budgeted capacity 预算生产能力B (82)burden 制造费用B (83)business center 经营中心B (84)business entity 营业个体B (85)business unit 经营单位B (86)buy-out management 管理性购买产权B (87)by-product 副产品C (88)called-up share capital 催缴股本C (89)capacity 生产能力C (90)capacity ratios 生产能力比率C (91)capital 资本C (92)capital assets pricing model 资本资产计价模式C (93)capital commitment 承诺资本C (94)capital employed 已运用的资本C (95)capital expenditure 资本支出C (96)capital expenditure authorization 资本支出核准C (97)capital expenditure control 资本支出控制C (98)capital expenditure proposal 资本支出申请C (99)capital funding planning 资本基金筹集计划C (100)capital gain 资本收益C (101)capital investment appraisal 资本投资评估C (102)capital maintenance 资本保全C (103)capital resource planning 资本资源计划C (104)capital surplus 资本盈余C (105)capital turnover 资本周转率C (106)card 记录卡C (107)cash 现金C (108)cash account 现金账户C (109)cash book 现金账薄C (110)cash cow 金牛产品C (111)cash flow 现金流量C (112)cash discounted 现金贴现C (113)cash flow budget 现金流量预算C (114)cash flow statement 现金流量表C (115)cash ledger 现金分类账C (116)cash limit 现金限额C (117)CCA 现时成本会计C (118)center 中心C (119)changeover time 变更时间C (120)chartered entity 特许经济个体C (121)cheque 支票C (122)cheque register 支票登记薄C (123)coin analysis 零钱分类C (124)classification 分类C (125)clock card 工时卡C (126)code 代码C (127)commitment accounting 承诺确认会计C (128)common cost 共同成本C (129)company limited by guarantee 有限担保责任公司C (130)company limited shares 股份有限公司C (131)competitive position 竞争能力状况C (132)concept 概念C (133)conglomerate 跨行业企业C (134)consistency concept 一致性概念C (135)consolidated accounts 合并报表C (136)consolidation accounting 合并会计C (137)consortium 财团C (138)contingency plan 应急计划C (139)contingent liabilities 或有负债C (140)continuous operation 连续生产C (141)contra 抵消C (142)contract cost 合同成本C (143)contract costing 合同成本计算C (144)contribution 贡献毛益C (145)contribution centre 贡献中心C (146)contribution chart 贡献图C (147)contribution per unit of limiting factor ration 单位限定因素的贡献毛益比率C (148)contribution to sales ration 贡献毛益对销售比率C (149)control 控制C (150)control account 控制帐户C (151)control limits 控制限度C (152)controllability concept 可控制概念C (153)controllable cost 可控制成本C (154)conversion cost 加工成本C (155)convertible loan stock 来源: 可转换为股票的贷款C (156)corporate appraisal 公司评估C (157)corporate planning 公司计划C (158)corporate social reporting 公司社会报告C (159)corporation 股份公司C (160)cost 成本C (161)cost account 成本帐户C (162)cost accounting 成本会计C (163)cost accounting manual 成本手册C (164)cost accounts calendar 成本报表的日历时间C (165)cost adjustment 成本调整C (166)cost allocation 成本分配C (167)cost apportionment 成本分摊C (168)cost attribution 成本归属C (169)cost audit 成本审计C (170)cost behaviour 成本性态C (171)cost benefit analysis 成本效益分析C (172)cost center 成本中心C (173)cost driver 成本动因。

对审计的英文介绍

对审计的英文介绍Introduction to AuditAudit is a critical examination and assessment of an organization's financial records, systems, and processes to ensure accuracy, reliability, and compliance with applicable laws and regulations. It plays a significant role inenhancing transparency, maintaining stakeholders' trust, and ensuring the credibility of financial information.Objective of Audit:The main objective of an audit is to provide an unbiased opinion on whether an organization's financial statements present a true and fair view. This requires auditors toassess the reliability and integrity of financial information, adherence to accounting principles, and the effectiveness of internal controls.Types of Audits:1. Financial Audit:Financial audit focuses on examining an organization'sfinancial statements, including balance sheets, income statements, and cash flow statements. It aims to determinethe accuracy and completeness of financial information, aswell as the organization's compliance with accounting standards.2. Operational Audit:Operational audit assesses an organization's operational processes and effectiveness. It aims to identify areas of improvement, inefficiencies, and risks, and providerecommendations for enhancing operational efficiency and effectiveness.3. Compliance Audit:Compliance audit evaluates an organization's adherence to laws, regulations, and internal policies. It ensures that the organization operates within legal and ethical boundaries and helps identify any potential compliance gaps or risks.4. Information Systems Audit:Information systems audit focuses on reviewing an organization's IT infrastructure, systems, and controls to assess their effectiveness, security, and reliability. It identifies any vulnerabilities or weaknesses and provides recommendations to mitigate risks and enhance data integrity.Audit Process:1. Planning:The audit process begins with thorough planning, including understanding the organization's business and industry, identifying key risks, and developing an audit strategy. This involves determining the scope, objectives, and timelines for the audit.2. Risk Assessment:Auditors analyze and evaluate the organization's internal controls, processes, and systems to identify potential risks and control weaknesses. This step helps in determining the audit procedures and areas of focus.3. Testing and Analysis:During this phase, auditors collect and analyze evidence to support their findings. They verify financial transactions,review supporting documents, and perform analytical procedures to assess the accuracy and completeness of financial information.4. Reporting:After completing the audit procedures, auditors prepare a comprehensive report that includes their findings, conclusions, and recommendations. This report is shared with management and stakeholders, providing them with insightsinto the organization's financial health and control environment.Importance of Audit:1. Enhancing Transparency:Audits ensure transparency and accountability in financial reporting, as they provide an independent review of an organization's financial statements. This helps stakeholders, including investors, creditors, and regulators, make informed decisions.2. Maintaining Stakeholders' Trust:The external and independent nature of audits helps maintain stakeholders' trust in an organization. Audited financial statements provide assurance that the reported information is accurate, reliable, and in compliance with legal and regulatory requirements.3. Identifying Risks and Weaknesses:Audits help identify potential risks, control weaknesses, and areas for improvement. This enables management to address these issues and strengthen internal controls to mitigate risks and enhance operational efficiency.4. Compliance with Laws and Regulations:Compliance audits ensure that organizations adhere to laws, regulations, and internal policies. This helps prevent fraud, unethical practices, and non-compliance penalties, promoting ethical conduct and good governance.Conclusion:In conclusion, audits are an essential component of organizational governance, ensuring the accuracy, reliability, and compliance of financial information. They provide stakeholders with confidence in an organization's financial statements, help identify risks and weaknesses, andcontribute to maintaining transparency and trust in the business environment.。

审计英文演讲稿范文模板

Ladies and Gentlemen,Good [morning/afternoon/evening]. It is a great honor to stand beforeyou today to discuss a topic that is vital to the financial health and integrity of any organization – auditing.As we all know, financial management is the backbone of any business or institution. It is through proper financial management that we canensure the sustainable growth and success of our endeavors. However, financial management alone is not enough. We need to have a robust system in place to monitor and evaluate the accuracy and reliability of our financial records. This is where auditing comes into play.IntroductionTo begin with, let me define what auditing is. Auditing is an independent examination of financial information of any entity, whether profit-oriented or not, for the purpose of expressing an opinion on the financial statements of the entity. It is a critical process that provides assurance to stakeholders that the financial statements arefree from material misstatement, whether caused by fraud or error.The Importance of AuditingNow, let's delve into the reasons why auditing is essential:1. Ensuring Financial Integrity: Auditing helps in maintaining the integrity of financial statements. It provides a level of confidence to investors, creditors, and other stakeholders that the financial information presented is accurate and fair.2. Compliance with Regulations: In today's regulatory environment, it is crucial for organizations to comply with various laws and regulations. Auditing ensures that an organization is in line with these requirements, thereby avoiding legal repercussions and penalties.3. Detecting Fraud and Error: Auditors are trained to identify red flags that may indicate fraud or error. By conducting a thorough audit, they can help prevent financial misstatements and protect the interests ofthe organization and its stakeholders.4. Improving Financial Reporting: Auditing provides valuable feedback to management on the effectiveness of internal controls. This feedback can help in improving financial reporting processes and internal control systems.5. Enhancing Organizational Efficiency: A well-implemented auditing process can help organizations identify inefficiencies and areas for improvement, leading to better overall performance.The Audit ProcessNow that we understand the importance of auditing, let's take a brief look at the audit process:1. Planning: The auditor plans the audit by understanding the entity's business, assessing risks, and determining the nature, timing, and extent of audit procedures.2. Fieldwork: During the fieldwork phase, the auditor collects evidence to support the assertions made in the financial statements. This includes examining documents, interviewing personnel, and performing analytical procedures.3. Reporting: After completing the fieldwork, the auditor prepares an audit report that expresses an opinion on the financial statements. The report can be unqualified (clean), qualified, adverse, or a disclaimer of opinion.ConclusionIn conclusion, auditing plays a pivotal role in ensuring financial integrity and promoting transparency in organizations. It is an indispensable tool for stakeholders to make informed decisions and for management to improve their financial processes.Ladies and Gentlemen, let us not underestimate the power of auditing. It is a beacon that guides us through the complexities of financial management, ensuring that we can trust the numbers and make sound decisions for the future.Thank you for your attention. I welcome any questions you may have regarding the importance and process of auditing.[Note: This is a basic template for an audit English speech. You may need to customize it according to your specific requirements and the audience.]。

新职业英语_经贸英语Unit2 (1)

Unit 1Business Relations本单元结合国际经贸业务中的典型工作流程、工作场景,概述国际贸易中建立业务联系之后的一个重要环节——“背景调查”:●背景调查综述:介绍背景调查在国际贸易业务中的重要地位,以及调查所需要涉及的主要昂面和方法(Reading A),为进行实际调查工作提供方法指导;●布置调查任务:在建立业务联系之后,公司领导委托下属对潜在合作方进行调查(Listening & Speaking & Writing),学习如何以书面和口头形式布置工作任务;●搜集相关信息:下属通过各种方式了解前爱合作方信息,并在其过程中与相关人员进行讨论(Listening & Speaking),以熟悉背景调查报告所设计的主要内容和方法;●形成报告:提供报告的样本(Reading B & Writing),熟悉报告的各项内容。

Unit ObjectivesAfter studying this unit, you are able to:●Understand what a business background report covers●Know how to conduct a business background report●Make phone calls for information regarding business background check●Write and answer emails for back ground information1.Warming-upTask 1Talk about what aspects should be covered in the business background check.Task 2Discuss with your classmates to arrange the above aspects in the order of priority.2.Reading ABackground InformationAbusiness background checkis a process that allowspotential customers,investors, and partners to become acquainted with pertinent information about thehistory of the company. At the same time, running a background check on a corporation will reveal or verify data about the current status of the business. This data includes financial data that would be important to know before investing in the company or entering into a partnership with the corporation.Conducting a business background check involves looking into a number ofdifferent types of public records in order to get a true picture of the history and present status of the company.Task 1Before reading the passage, see how much you know about business background check by answering the following questions.1. Why do companies need to conduct business background checks?Just as you don’t want to make friends with peo ple who might fool you, you want to enter into business with partners whom you can rely on. Business world is more complicated than personal life. There are news and stories widely spread that how a company has been framed by its partners and the consequence can be fatal. As a result, one must be careful about whom to cooperate with and be sure that the company is reliable. The most common way to do so is to conduct a business background check.2. What do you think is the most important part of a business background check?W ell, that is not an easy question. If I have to choose which part is the most important, I would like to choose “criminal records”. Nobody likes to do business with a company that has been sued many times or has been involved in business criminals. It is just too dangerous. Dealing with a small company or company with ill reference, one might run into the risk of poor goods or service quality, while working with a big company with criminal records, one might be dragged into lawsuits or put into prison.TextHow to Conduct Business Background ChecksThere are more and more news stories about companies that defraud investors of millions of dollars. Therefore, it is important to be certain that the company you are intending to establish a relation with is reputable and the usual practice to do so is to run a business background check. In order to do this, the following straightforward steps are recommended:投资者被某公司骗数百万美元的报道屡见不鲜。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

Discussion question

• So is corporate governance important to the auditor? • Does it really matter whether the client has good or bad governance structures? • What are the implications?

The Auditor and Governance

• The overall objective of the auditor is to report whether the financial reports as a whole are free from material misstatement, whether due to fraud or error. • The responsibilities of those charged with governance include: – Preparation of financial statements – Ensuring appropriate internal controls – Providing information and access to auditors

What is Governance?

• Agency structure – Separation of ownership and management – Members (shareholders) rely on management (agents) – Agents conduct the business on behalf of members • Authority of governing body underpinned by transparency and accountability • An independent auditor adds to the credibility of the conduct of the agent

• An operational audit focuses on the future • Operational audits are an integral element of internal control

Operational Auditing

Objectives – Assist directors to discharge their responsibilities – Improve credibility and objectivity of accounting process – Improve effectiveness of internal and external audit function – Facilitate independence of internal & external auditors – Strengthen role of non-executive directors – Fosters an ethical culture

What is Governance?

Governance is:

• The exercise of economic and administrative authority to manage an entity’s affairs • It is concerned with the processes by which decisions are made and implemented • Decisions are free of abuse and corruption • It’s applicable to all entities

• Common techniques

Internal Auditing in the Governance Process

• It enhances the governance process

• Defined as: ‘ … an independent, objective assurance and consulting activity designed to add value and improve an organisations operations. It helps an organisation accomplish its objectives by bringing a systematic, disciplined approach and evaluate and improve the effectiveness of risk management, control and governance processes.’ IPPF

The Auditor and Governance

• Auditing standards requiring the auditor and management to work together include: – ASA 250 – ASA 260 – ASA 265 – ASA 315 – ASA 330

Issues in Governance

A risk management system should: - Define objectives, principles and priorities - Formulate overall risk classifications - Understand business activities and processes - Identify and classify risks - Assess probability and possible consequences of risk - Compare and analyse risk tolerance - Evaluation of controls, costs and monitoring process - Assess exposure,ernal Auditing

• Internal audit encompasses examination and evaluation of: – Adequacy and effectiveness of governance and internal control structure – the quality of performance in carrying out assigned responsibilities – The procedures of risk identification and management – Mechanisms to ensure regulatory compliance • The internal auditor can supplement, but not substitute, the work of independent external auditors

Internal Auditing

Organisational and functional differences between internal and independent auditors

Operational Auditing

• Evaluates whether an entities resources are being used in the most economic, efficient and effective manner

Governance

Objectives

• Appreciate the role of the auditor in governance • Discuss the issues of internal control, risks and earnings management in governance that concern the auditor • Appreciate the roles of internal and operational audits in the governance processes

Thus auditors need to have a good relationship with management

Issues in Governance

Internal Control and Risk Management •Effective governance depends to a great extent on an organisation’s internal control system and its risk management system. •Risk management is an important part of management. It involves planning the company’s risk profile, identifying risks, managing risks and monitoring risks. •The internal control system of an organisation is a system of checks and balances that ensure orderly conduct of the business including the prevention of error, fraud and theft. •Management is responsible for both risk management and internal control.

Enterprise Governance

• Is a framework that covers both the corporate governance regime and the business governance perspectives of an organisation