FMI7e_ch03Structure of Interest Rates(金融市场好机构—7e, by Jeff Madura))

金融工程硕士书单Master reading list for Quants, MFE students范文

以下推荐书目,由华尔街的Quant们和美国各名牌大学毕业生推荐。

FREE QUANT CAREER GUIDES•What do quant do ? A guide by Mark Joshi. Download•Paul & Dominic's Guide to Quant Careers (see attachment)•Career in Financial Markets 2011- a guide by efinancialcareers. Download•Interview Preparation Guide by Michael Page: Quantitative Analysis. Download•Interview Preparation Guide by Michael Page: Quantitative Structuring. Download•Paul & Dominic's Job Hunting in Interesting Times Second Edition (see attachment)•Peter Carr's A Practitioner's Guide to Mathematical Finance (see attachment)GENERAL READING ON WALL STREET•Reminiscences of a Stock Operator (Wiley Investment Classics)•Working the Street: What You Need to Know About Life on Wall Street•Liar’s Poker: Rising Through the Wreckage on Wall Street•Monkey Business: Swinging Through the Wall Street Jungle•Fiasco: The Inside Story of a Wall Street Trader•Den of Thieves•When Genius Failed: The Rise and Fall of Long-Term Capital Management•Traders, Guns & Money: Knowns and unknowns in the dazzling world of derivatives•The Greatest Trade Ever: The Behind-the-Scenes Story of How John Paulson Defied Wall Street and Made Financial History•Goldman Sachs : The Culture of Success•The House of Morgan: An American Banking Dynasty and the Rise of Modern Finance•Wall Street: A History: From Its Beginnings to the Fall of Enron•The Murder of Lehman Brothers: An Insider’s Look at the Global Meltdown•On the Brink: Inside the Race to Stop the Collapse of the Global Financial System•House of Cards: A Tale of Hubris and Wretched Excess on Wall Street•Too Big to Fail: The Inside Story of How Wall Street and Washington Fought to Save the Financial System-and Themselves•Liquidated: An Ethnography of Wall Street•Fortune’s Formula: The Untold Story of the Scientific Betting System That Beat the Casinos and Wall StreetCAREER AS A QUANT•My Life as a Quant: Reflections on Physics and Finance•How I Became a Quant: Insights from 25 of Wall Street’s Elite•The Big Short: Inside the Doomsday Machine•The Quants: How a New Breed of Math Whizzes Conquered Wall Street and Nearly Destroyed It •Nerds on Wall Street: Math, Machines and Wired Markets•Physicists on Wall Street and Other Essays on Science and Society•The Complete Guide to Capital Markets for Quantitative Professionals•Starting Your Career as a Wall Street Quant: A Practical, No-BS Guide to Getting a Job in Quantitative Finance and Launching a Lucrative CareerBOOKS FOR QUANT INTERVIEWS•Heard on The Street: Quantitative Questions from Wall Street Job Interviews by Timothy Crack •Quant Job Interview Questions And Answers by Mark Joshi•Frequently Asked Questions in Quantitative Finance by Paul Wilmott•A Practical Guide To Quantitative Finance Interviews by Xinfeng Zhou•Basic Black-Scholes: Option Pricing and Trading by Timothy Crack•Fifty Challenging Problems in Probability with Solutions by Frederick Mosteller•Vault Guide to Advanced Finance & Quantitative InterviewsGOOD BOOKS TO READ BEFORE STARTING MFE PROGRAM•A Primer for the Mathematics of Financial Engineering (+ Solutions Manual) by Dan Stefanica •An Introduction to the Mathematics of Financial Derivatives, Second Edition by Salih Neftci •Options, Futures, and Other Derivatives with Derivagem CD (7th Edition) by John Hull•Paul Wilmott on Quantitative Finance 3 Volume Set (2nd Edition) by Paul Wilmott•Principles of Financial Engineering, Second Edition by Salih Neftci•Elementary Stochastic Calculus With Finance in View by Thomas Mikosch•The Concepts and Practice of Mathematical Finance by Mark Joshi•Financial Options: From Theory to Practice by Stephen Figlewski•Financial Calculus : An Introduction to Derivative Pricing by Martin Baxter•A Course in Financial Calculus by Etheridge Alison•The Mathematics of Financial Derivatives: A Student Introduction by Paul Wilmott •Frequently Asked Questions in Quantitative Finance by Paul Wilmott•Derivatives Markets by Robert L. McDonald•An Undergraduate Introduction to Financial Mathematics by Robert Buchanan PROGRAMMINGC++ (ordered by level of difficulty)•Problem Solving with C++, 7th Edition by Walter Savitch•C++ How to Program (7th Edition) by Harvey Deitel•Absolute C++ (4th Edition) by Walter Savitch•Thinking in C++: Introduction to Standard C++, Volume One by Bruce Eckel•Thinking in C++: Practical Programming, Volume Two by Bruce Eckel•The C++ Programming Language: Special Edition by Bjarne Stroustrup (C++ inventor) •Effective C++: 55 Specific Ways to Improve Your Programs and Designs by Scot Myers•C++ Primer (4th Edition) by Stanley Lippman•C++ Design Patterns and Derivatives Pricing (2nd edition) by Mark Joshi•Financial Instrument Pricing Using C++ by Daniel DuffyC# (ordered by level of difficulty)•C# 2010 for Programmers (4th Edition)•Computational Finance Using C and C# by George Levy•C# in Depth, Second Edition by Jon SkeetF# (ordered by level of difficulty)•Programming F#: An introduction to functional language by Chris Smith•F# for Scientists by Jon Harrops (Microsoft Researcher)•Real World Functional Programming: With Examples in F# and C#•Expert F# 2.0 by Don Syme•Beginning F# by Robert PickeringMatlab (ordered by level of difficulty)•Matlab: A Practical Introduction to Programming and Problem Solving•Numerical Methods in Finance and Economics: A MATLAB-Based Introduction (Statistics in Practice)Excel•Excel 2007 Power Programming with VBA by John Walkenbach•Excel 2007 VBA Programmer’s Reference•Financial Modeling by Simon Benninga•Excel Hacks: Tips & Tools for Streamlining Your Spreadsheets•Excel 2007 Formulas by John WalkenbachVBA•Advanced modelling in finance using Excel and VBA by Mike Staunton•Implementing Models of Financial Derivatives: Object Oriented Applications with VBAPython•Learning Python: Powerful Object-Oriented Programming•Python CookbookFINITE DIFFERENCES•Option Pricing: Mathematical Models and Computation, by P. Wilmott, J.N. Dewynne, S.D. Howison•Pricing Financial Instruments: The Finite Difference Method, by Domingo Tavella, Curt Randall •Finite Difference Methods in Financial Engineering: A Partial Differential Equation Approach by Daniel DuffyMONTE CARLO•Monte Carlo Methods in Finance, by Peter Jäcke (errata available at )•Monte Carlo Methodologies and Applications for Pricing and Risk Management , by Bruno Dupire (Editor)•Monte Carlo Methods in Financial Engineering, by Paul Glasserman•Monte Carlo Frameworks in C++: Building Customisable and High-performance Applications byDaniel J. Duffy and Joerg KienitzSTOCHASTIC CALCULUS•Stochastic Calculus and Finance by Steven Shreve•Stochastic Differential Equations: An Introduction with Applications by Bernt Oksendal VOLATILITY•Volatility and Correlation, by Riccardo Rebonato•Volatility, by Robert Jarrow (Editor)•Volatility Trading by Euan SinclairINTEREST RATE•Interest Rate Models - Theory and Practice, by D. Brigo, F. Mercurio updates available on-line Professional Area of Damiano Brigo's web site•Modern Pricing of Interest Rate Derivatives, by Riccardo Rebonato•Interest-Rate Option Models, by Riccardo Rebonato•Efficient Methods for Valuing Interest Rate Derivatives, by Antoon Pelsser•Interest Rate Modelling, by Nick Webber, Jessica JamesFX•Foreign Exchange Risk, by Jurgen Hakala, Uwe Wystup•Mathematical Methods For Foreign Exchange, by Alexander LiptonSTRUCTURED FINANCE•The Analysis of Structured Securities: Precise Risk Measurement and Capital Allocation (Hardcover) by Sylvain Raynes and Ann Rutledge•Salomon Smith Barney Guide to MBS & ABS, Lakhbir Hayre, Editor•Securitization Markets Handbook, Structures and Dynamics of Mortgage- and Asset-backed securities by Stone & Zissu•Securitization, by Vinod Kothari•Modeling Structured Finance Cash Flows with Microsoft Excel: A Step-by-Step Guide (good for understanding the basics)•Structured Finance Modeling with Object-Oriented VBA (a bit more detailed and advanced than the step by step book)STRUCTURED CREDIT•Collateralized Debt Obligations, by Arturo Cifuentes•An Introduction to Credit Risk Modeling by Bluhm, Overbeck and Wagner (really good read, especially on how to model correlated default events & times)•Credit Derivatives Pricing Models: Model, Pricing and Implementation by Philipp J. Schönbucher •Credit Derivatives: A Guide to Instruments and Applications by Janet M. Tavakoli•Structured Credit Portfolio Analysis, Baskets and CDOs by Christian Bluhm and Ludger Overbeck RISK MANAGEMENT/VAR•VAR, by various authors•Value at Risk, by Philippe Jorion•RiskMetrics Technical Document RiskMetrics Group•Risk and Asset Allocation by Attilio MeucciSAS/S/S-PLUS•The Little SAS Book: A Primer, Third Edition by Lora D. Delwiche and Susan J. Slaughter •Modeling Financial Time Series with S-PLUS•Statistical Analysis of Financial Data in S-PLUS•Modern Applied Statistics with SHANDS ON•Implementing Derivative Models, by Les Clewlow, Chris Strickland•The Complete Guide to Option Pricing Formulas, by Espen Gaarder HaugNOT ENOUGH YET?•Energy Derivatives, by Les Clewlow, Chris Strickland,•Hull-White on Derivatives, by John Hull, Alan White•Exotic Options: The State of the Art, by Les Clewlow (Editor), Chris Strickland (Editor)•Market Models, by C.O. Alexander•Pricing, Hedging, and Trading Exotic Options, by Israel Nelken•Modelling Fixed Income Securities and Interest Rate Options, by Robert A. Jarrow•Black-Scholes and Beyond, by Neil A. Chriss•Risk Management and Analysis: Measuring and Modelling Financial Risk, by Carol Alexander •Mastering Risk: Volume 2 - Applications: Your Single-Source Guide to Becoming a Master of Risk, by Carol Alexander。

跳跃扩散过程下单因素利率期限结构模型以及参数估计

跳跃扩散过程下单因素利率期限结构模型以及参数估计金哲【摘要】The term structure models of interest rate has an important role in financial statistical analysis. Ba-sing on general CKLS single factor interests rate model, a jump factor is added to analyze interests rate movement affected by macro monetary policy events and then estimates its parameter by using Chinese short - term bond mar-ket interest rates. The result shows the estimation of the model' s parameters α0, α1, α2, α3, σ, γ, σJ, μ are -0.112,0.304,0.513, - 0.002, 1. 556, - 2. 1 × 10 -5, 0. 321, 0. 0012 respectively and all in 95% confi-dence level. This indicates all parameters of the model are significant and residual term is restricted to standard normal distribution. This means under jump diffusion process single factor term structure models of interest rate can better interpret the movement of interest rate.%利率期限结构模型在金融统计分析中具有非常重要的地位.在一般的CKLS单因素利率模型的基础上,增加了一个跳跃因子,来反映宏观政策等的变化对利率变化的突发影响;并且利用中国短期国债市场回购利率数据对模型进行了参数估计以及拟合,结果模型的参数α0,α1,α2,α3,σ,γ,σ(J),μ的估计值分别为-0.112,0.304,0.513,-0.002,1.556,-2.1×10-5,0.321,0.0012.而且都落在了各自95%的置信区间.这表明模型的各个参数都显著并且残差项也服从标准正态分布.说明了跳跃过程下单因素利率期限结构模型能够更好的解释利率变动的情况.【期刊名称】《科学技术与工程》【年(卷),期】2011(011)036【总页数】3页(P9116-9118)【关键词】利率;跳跃;单因素;参数估计【作者】金哲【作者单位】暨南大学经济学院统计系,广州510632【正文语种】中文【中图分类】F830.42利率期限结构模型是利率衍生品定价和风险管理的基础。

term structure of interest rate

Topic two: term structure of interest rate –the relationship between short-term and long-term interest rateThe relation between interest rates of different maturities is called the term structure of interest. Since an interest rate summarizes the promised repayment terms on a bond or loan, interest rates differ according to the creditworthiness of the issuer, tax treatments and other factors. The factor of greatest interest here is the length of time the interest rate covers----the term of the bond. By offering a complete schedule of interest rates across time, the term structure embodies the market’s anticipations of future events. An explanation of term structure gives us a way to extract this information and to predict how changes in the underlying variables will affect the yield curve, which shows the interest rates for different maturities.In a world of certainty, equilibrium forward rates must coincide with future spot rates, but when uncertainty about future rates is introduced the analysis becomes much more complex.The long term interest rate equals the average of current short term rate and the expected future short term rates, with addition to a term premium to compensate the risk on the uncertainty of future rate. Term premiums vary over time but are generally higher for longer term rates. The higher term premiums in part reflect the higher risk associated with the greater price volatility of longer term bonds.1.There are various versions of the expectations hypothesis. These place predominantemphasis on the expected values of future spot rates or holding-period returns. In its simplest form, the expectations hypothesis postulates that bonds are priced so that the implied forward rates are equal to the expected spot rates. Generally, this approach is characterized by the following propositions: A, the return on holding a long-term bond to maturity is equal to the expected return on repeated investment in a series of the short-term bonds; or B, theexpected rate of return over the next holding period is the same for bonds of all maturities. 2.The liquidity preference hypothesis concurs with the importance of expected future spot rates,but places more weight on the effects of the risk preferences of market participants. It asserts that risk aversion will cause forward rates to be systematically greater than expected spot rates, usually by an amount increasing with maturity. This term premium is the increment required to induce investors to hold longer-term (riskier) securities.3.The market segmentation hypothesis offers a different explanation of term premiums. Here itis asserted that individuals have strong maturity preferences and that bonds of different maturities trade in separate and distinct markets. The demand and supply of bonds of particular maturities are supposedly little affected by the prices of bonds of bonds of neighboring maturities. Of course, there is now no reason for the term premiums to be positive or to be increasing functions of maturity. Without attempting a detailed critique of this position, it is clear that there is a limit to how far one can go in maintaining that bonds of close maturities will not be close substitutes.4.the fisher effect. The importance of inflation expectations for the long-term interest rate isdescribed in the Fisher Equation, which explains the relation ship between the nominal and real rate of interest. It can be derived as follows. (1+i)=(1+r)(1+a) where i=nominal interest rate, r=real interest rate and a=expected inflation.。

AJMFQB practice 1~5

Copyright © 2010 A&J Study Manual. 1st Edition|

2

Table of Contents

SOA Exam MFE/ CAS Exam 3F

Table of Contents NhomakorabeaPart 1. Put-Call Parity and Other Option Relationships ............................................................... 4 Solutions ....................................................................................................................................... 24 Part 2. Binomial Option Pricing ................................................................................................... 38 Solutions ....................................................................................................................................... 52 Part 3. Black-Scholes Formula and Option Greeks.................................................................... 71 Solutions ....................................................................................................................................... 85 Part 4. Market-Making and Delta-Hedging ................................................................................ 103 Solutions ..................................................................................................................................... 114 Part 5. Exotic Options ................................................................................................................ 126 Solutions ..................................................................................................................................... 145 Part 6. The Lognormal Distribution ........................................................................................... 165 Solutions ..................................................................................................................................... 170 Part 7. Monte Carlo Valuation .................................................................................................... 175 Solutions ..................................................................................................................................... 183 Part 8. Brownian Motion and Itō’s lemma ................................................................................. 193 Solutions ..................................................................................................................................... 209 Part 9. Interest Rate Models....................................................................................................... 225 Solutions ..................................................................................................................................... 237 Author’s Biography .................................................................................................................... 254

国际财务管理课后习题答案(第六章)

CHAPTER 6 INTERNATIONAL PARITY RELATIONSHIPSSUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTERQUESTIONS AND PROBLEMSQUESTIONS1。

Give a full definition of arbitrage。

Answer:Arbitrage can be defined as the act of simultaneously buying and selling the same or equivalent assets or commodities for the purpose of making certain, guaranteed profits。

2. Discuss the implications of the interest rate parity for the exchange rate determination。

Answer:Assuming that the forward exchange rate is roughly an unbiased predictor of the future spot rate, IRP can be written as:S = [(1 + I£)/(1 + I$)]E[S t+1|I t]。

The exchange rate is thus determined by the relative interest rates,and the expected future spot rate,conditional on all the available information,I t, as of the present time。

One thus can say that expectation is self-fulfilling. Since the information set will be continuously updated as news hit the market, the exchange rate will exhibit a highly dynamic,random behavior.3. Explain the conditions under which the forward exchange rate will be an unbiased predictor of the future spot exchange rate.Answer: The forward exchange rate will be an unbiased predictor of the future spot rate if (I) the risk premium is insignificant and (ii) foreign exchange markets are informationally efficient。

FIS 8e - Ch5 Int Rate Term Structure

8

Exhibit 5-2 Corporate Bond Yields and Risk Premium Measures Relative to Treasury Yields on February 26, 2011

Maturity 5-year 5-year 10-year 10-year

Rating AAA AA AAA AA

Answer to Example 5-3

A The yield on the corporate is 7% so the relative yield is (7% -

6%)/6% which is 1/6 or 16.67% of the 3-year Treasury-yield.

11

Example 5-3 Concept of Relative Spread

A.

B.

C. D.

Assume the following corporate yield curve: - One-year rate: 5.50% - Two-year rate: 6.00% - Three-year rate: 7.00% If an on-the-run three-year U.S. Treasury is yielding 6 percent, the three-year relative yield spread is: 16.67% 40.00% 14.28% 100bps 12

Example 5-2 Concept of Absolute Yield Spread

A. B. C.

D.

Assume the following yields for different bonds issued by a corporation. - One-year rate: 5.50% - Two-year rate: 6.00% - Three-year rate: 7.00% If the on-the-run three-year U.S. Treasury is yielding 5 percent, then what is the absolute yield spread on the three-year corporate issue? 0.40 1.40 100bps 200bps

The Monetary Models of Exchange Rate Determination

Sticky-Price Model

Assume that PPP only holds in the long run, such that

st = pt − p t

*

where a bar over a variable indicates a long-run equilibrium value. In the long run PPP holds and thus the Flex-Price model is valid, but only in the long run.

s t = ( mt − mt* ) − δ ( yt − yt* ) + γ ( it − it* )

In the short run, prices are sticky and PPP will not hold and neither will the Flex-Price model.

Sticky-Price Model

mt − pt = δ yt − γ it

where • mt is the domestic money supply in logs • pt is the log of domestic price level • yt is the log of domestic real income • it is the domestic nominal interest rate

Chap015The Term Structure of Interest Rates(金融工程-南开大学,王小麓))

The yield curve has an upward bias built into the long-term rates because of the risk premium.

15-12

Expectations Theory

Observed long-term rate is a function of today’s short-term rate and expected future short-term rates. Long-term and short-term securities are perfect substitutes. Forward rates that are calculated from the yield on long-term securities are market consensus expected future short-term rates.

9.660 9.993

* $1,000 Par value zero

McGraw-Hill/Irwin

Copyright © 2001 by The McGraw-Hill Companies, Inc. All rights reserved.

15-7

Forward Rates from Observed Long-Term Rates

- Upward bias over expectations

Market Segmentation

- Preferred Habitat

McGraw-Hill/Irwin

期货期权及其衍生品配套课件Ch04

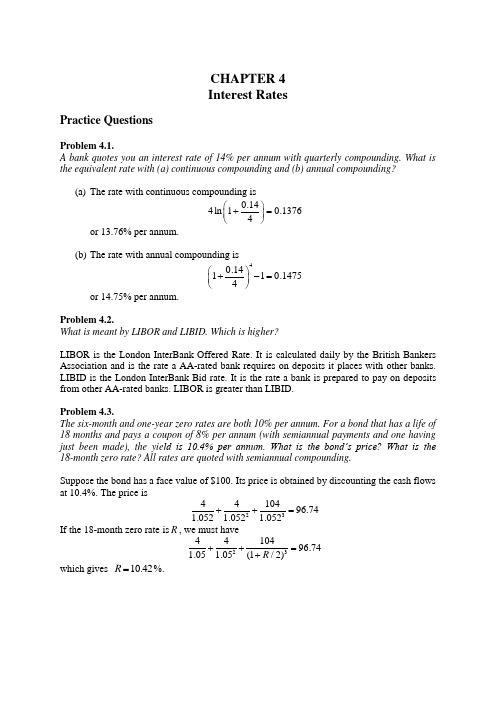

3 e y 0 . 5 3 e y 1 . 0 3 e y 1 . 5 1 0 3 e y 2 . 0 9 8 . 3 9

to get y=0.0676 or 6.76%.

13

The Bootstrap Method continued

To calculate the 1.5 year rate we solve 4 e 0 . 1 0 0 . 5 4 4 e 6 0 . 1 9 0 1 . 0 5 1 3 e R 0 6 1 . 5 9 46

3e0.050.53e0.0581.03e0.0641.5

103e0.0682.0 98.39

Options, Futures, and Other Derivatives 7th International

Edition, Copyright © John C. Hull 2019

Edition, Copyright © John C. Hull 2019

7

Bond Pricing

To calculate the cash price of a bond we discount each cash flow at the appropriate zero rate

In our example, the theoretical price of a twoyear bond providing a 6% coupon semiannually is

Rm: same rate with compounding m times per

The Term Structure of Interest-Rate Futures Prices, working paper

The Term Structure of Interest-RateFutures Prices.1Richard C.Stapleton2,and Marti G.Subrahmanyam3First draft:June,1994This draft:August13,20011Earlier versions of this paper have been presented at the Workshop on Finan-cial Engineering and Risk Management,European Institute for Advanced Studies in Management,Brussels,and the Chicago Board of Trade Annual European Fu-tures Conference,Rome,and in seminars at New York University,The Federal Reserve Bank of New York,University of Cardiff,University of London,Birkbeck College,The Australian Graduate School of Management,Sydney,The Fields In-stitute,Toronto,and University of California at Los Angeles.We would like to thank T.S.Ho,C.Thanassoulas,S-L.Chung,Q.Dai and O.Grischchenko for helpful comments.We would also like to thank the editor,B.Dumas,and an anonymous referee,whose detailed comments lead to considerable improvements in the paper.We acknowledge able research assistance by V.Acharya,A.Gupta and P.Pasquariello.2Department of Accounting and Finance,University of Strathclyde,100, Cathedral Street,Glasgow,Scotland.Tel:(44)524—381172,Fax:(44)524—846874, Email:rcs@ and University of Melbourne,Australia 3Leonard N.Stern School of Business,New York University,Management Ed-ucation Center,44West4th Street,Suite9—190,New York,NY10012—1126,USA. Tel:(212)998—0348,Fax:(212)995—4233,Email:msubrahm@AbstractThe Term Structure of Interest-Rate FuturesPricesWe derive general properties of two-factor models of the term structure of in-terest rates and,in particular,the process for futures prices and rates.Then, as a special case,we derive a no-arbitrage model of the term structure in which any two futures rates act as factors.In this model,the term structure shifts and tilts as the factor rates vary.The cross-sectional properties of the model derive from the solution of a two-dimensional,autoregressive process for the short-term rate,which exhibits both mean-reversion and a lagged persistence parameter.We show that the correlation of the futures rates is restricted by the no-arbitrage conditions of the model.In addition,we inves-tigate the determinants of the volatilities and the correlations of the futures rates of various maturities.These are shown to be related to the volatility of the short rate,the volatility of the second factor,the degree of mean-reversion and the persistence of the second factor shock.We also discuss the extension of our model to three or more factors.We obtain specific re-sults for futures rates in the case where the logarithm of the short-term rate [e.g.,the London Inter-Bank Offer Rate(LIBOR)]follows a two-dimensional process.We calibrate the model using data from Eurocurrency interest rate futures contracts.Interest Rate Futures1 1IntroductionTheoretical models of the term structure of interest rates are of interest to both practitioners andfinancial academics.The term structure exhibits several patterns of changes over time.In some periods,it shifts up or down, partly in response to higher expectations of future inflation.In other periods, it tilts,with short-term interest rates rising and long-term interest rates falling,perhaps in response to a tightening of monetary policy.Sometimes, its shape changes to an appreciable extent,affecting its curvature.Hence, a desirable feature of a term-structure model is that it should be able to capture shifts,tilts and changes in the curvature of the term structure.In this paper,we present and analyse a model of the term structure of futures rates that has the above properties.Previous work on the term structure of interest rates has concentrated mainly on bond yields of varying maturities or,more recently,on forward rates.In contrast,this paper concentrates on futures rates,partly motivated by the relative lack of previous theoretical models of interest-rate futures prices.However,the main reason for focussing on futures rates is analytical tractability.Futures prices are simple expectations of spot prices under the equivalent martingale measure(EMM),of the future relevant short-term bond prices,whereas forward prices and spot rates involve more complex relationships.It follows that futures prices and futures rates are fairly sim-ple to derive from the dynamics of the spot rate.In contrast,closed-form solutions for forward rates have been obtained only under rather restrictive (e.g.Gaussian)assumptions.Further,from an empirical perspective,since forward and futures rates differ only by a convexity adjustment,it is likely that most of the time series and cross-sectional properties of futures rates are shared by forward rates,to a close approximation,at least for short ma-turity contracts.It makes sense,therefore,to analyse these properties,even if the ultimate goal is knowledge of the term-structure behaviour of forward or spot prices.Finally,the analysis of futures rates is attractive because of the availability of data from trading on organized futures exchanges.Hence, the models derived in the paper are directly testable,using data from the liquid market for Eurocurrency interest rate futures contracts.One contrast between many of the term-structure models presented in the academic literature and those used by practioners for the pricing of interest rate options is in the distributional assumptions made.Most of the modelsInterest Rate Futures2 which derive the term structure,for example Vasicek(1977),Balduzzi,Das, Foresi and Sundaram(1996)(BDFS),Jegadeesh and Pennacchi(1996)(JP), and Gong and Remolona(1997)assume that the short term interest rate is Gaussian.In contrast,popular models for the pricing of interest-rate options often assume that rates are lognormally distributed(see for example Black and Karasinski(1991),Brace,Gatarek and Musiela(1997),and Miltersen, Sandmann and Sondermann(1997)).In this paper,we present a model where the short-term rate LIBOR is assumed to follows a multi-dimensional lognormal process under the EMM.We show that the no-arbitrage futures rates for all maturities are also log-linear in any two(or three)rates.This implies that all futures rates are also lognormal in our model.We then show that the correlation between the long and short maturity futures rates is restricted by the degree of mean-reversion of the short rate and the relative volatilities of the long and short-maturity futures rates.Also,the volatility structure of futures rates of various maturities can be derived explicitly from the assumed process for the spot short rate.The performance of a set of models where the short rate follows a process with a stochastic central tendency has been analysed in a recent article by Dai and Singleton(2000)(DS).They analyse the set of”affine”term struc-ture models introduced previously by Duffie and Kan(1994).Our process for the short rate is also a stochastic central tendency model.However, there are some differences that should be noted between our model and those analysed by DS.First,in our model the short rate follows a discrete-time,rather than a continuous-time process.Second,as noted above,we assume that the process is log-Gaussian.Third,we assume that the short rate follows the process under the risk-neutral measure;hence,we abstract from considerations of the market price of risk.We suggest a time series model in which the short rate follows a stochasic central tendency process.This assumption allows us to nest the AR(1) single-factor model as a special case.It is also general enough to produce stochastic no-arbitrage term structures with shapes that capture most of those observed empirically.A similar model,in which the conditional mean of the short rate is stochastic has been suggested by Hull and White(1994), JP(1996),BDFS(1996)and analysed by Gong and Remolona(1997).The characteristics of these models are reviewed below.The literature on the pricing of futures contracts was pioneered by Cox, Ingersoll and Ross(1981)[CIR],who characterized the futures price of anInterest Rate Futures3 asset as the expectation,under the risk-neutral measure,of the spot price of the asset on the expiration date.In a related paper,Sundaresan(1991) shows that,under the risk-neutral measure,the futures interest rate is the expectation of the spot interest rate in the future.This follows from the fact that the LIBOR futures contract is written on the three-month LIBOR itself,rather than on the price of a zero-coupon instrument.Jegadeesh and Pennacchi(1996)[JP]suggest a two-factor equilibrium model of bond prices and LIBOR futures based on a two-factor extension of the Vasicek(1977)Gaussian model.They assume that the(continuously com-pounded)interest rate is normally distributed and generated by a process with a stochastic central tendency.They then estimate the model using fu-tures prices of LIBOR contracts,backing out estimates of the coefficients of mean-reversion of the short rate as well as the second stochastic conditional-mean factor.Our approach is somewhat different.We directly assume a process for LIBOR,rather than the continuously compounded rate,and then derive the process for the LIBOR futures.1This allows us to analyse the less tractable log-Gaussian case.Our general model is closely related to the JP paper,with the important distinction that it is embedded in an arbitrage-free,rather than an equilib-rium framework,thus eliminating the need for explicitly incorporating the market price of risk.Although our analysis is based on weaker assumptions, we are able to derive quite general,distribution-free results for futures rates. We then include,as a significant special case,a model in which the interest rate is lognormal.The work of Gong and Remolona(1997)is similar,in some respects,to that of JP.Like JP,they also employ a two-factor model,in which the second factor is the conditional mean of the short-rate process.However, they focus on the yield of long-dated bonds rather than on the futures rates. In their model,the short-term rate is linear in the two factors.Also,in a manner similar to Vasicek(1977),they assume a market price of risk,solve for bond prices,and back-out the long-term rates and the variances of the two factors.21This is similar to the approach taken in the LIBOR market models of Brace,Gatarek and Musiela(1997),and Miltersen,Sandmann and Sondermann(1997).2Much of the recent literature,dating back to the work of Ho and Lee(1986),has been concerned with the evolution of forward rates.The most widely cited work in this area is by Heath,Jarrow and Morton[HJM](1990a,1990b,1992).HJM provide a continuous-Interest Rate Futures4 The two-factor models developed in this paper are related also to the expo-nential affine-class of term-structure models introduced by Duffie and Kan (1994).This class is defined as the one where the continuously compounded spot rate is a linear function of any n factors or spot rates.In an interesting special case of our model,where the logarithm of the LIBOR evolves as a two-dimensional linear process,it is the logarithm of the futures rate that is linear in the logarithm of any two futures rates.The remainder of this paper is organised as follows.In section2,we derive some general properties that characterise two-factor models in general and show that if the function of the price of a zero-coupon bond follows a two-dimensional process,its conditional expectation is generated by a two-factor model.We then derive a two-factor,cross-sectional model for futures prices in the general case where a function of the price of a zero-coupon bond follows a stochastic central tendency process.In section3,we assume that the logarithm of the London Inter-Bank Offer Rate(LIBOR)follows a two-dimensional process and derive our main result for futures contracts on the LIBOR:a two-factor cross-sectional relationship between the changes in the prices of interest-rate futures.We estimate the parameters of the two-factor model using estimates of the volatilities and correlations of futures rates derived from the Eurodollar futures contract for the period1995-99, in section4.The conclusions and possible applications of our model to the valuation of interest rate options and to risk management are discussed in section5.Here,we also discuss possible extensions and,in particular,the generalisation of the model to three factors.2Some general properties of two-factor models In this section,we establish two statistical results,that hold for any two-factor process of the form that we assume for the short-term rate.These time limit to the Ho-Lee model and generalize their results to a forward rate which evolves as a generalized Ito-process with multiple factors.The HJM paper can be distinguished from our paper in terms of the inputs to the two frameworks.The required input to the HJM-type models is the term structure of the volatility of forward rates.In contrast,in our paper,we derive the term structure of volatility of futures rates from a more basic assumption regarding the process for the spot rate.To the extent that the futures and forward volatility structures are related,our analysis in this paper provides a link between the spot-rate models of the Vasicek type and the extended HJM-type forward rate models.Interest Rate Futures5 results are used to establish a general proposition,that holds for the condi-tional expectation of any function of the zero-coupon bond price.The con-ditional expectation is of key significance,since the futures price(or rate)is closely related to the conditional expectation of the future spot interest rate. Later in the section,these results are directly applied to establish futures prices and rates.2.1Definitions and notationWe denote P t as the time-t price of a zero-coupon bond paying$1with certainty at time t+m,where m is measured in years.The short-term interest rate is defined in relation to this m-year bond,where m isfixed. The continuously compounded short-term interest rate for m-year money at time t is denoted as i t,where i t=−ln(P t)/m.The London Interbank Offer Rate LIBOR,again for m-year money is denoted r t,where P t=1/(1+r t m), where m is the proportion of a year.3We are concerned with interest rate contracts for delivery at a future date T.We denote the futures rate as F t,T,the rate contracted at t for delivery at T of an m-period loan.We denote the logarithm of the LIBOR futures rate as f t,T=ln[F t,T].Note that,under this notation,which is broadly consistent with HJM,F t,t=r t and f t,t=ln(r t).2.2General properties of two-factor modelsThe two-factor stochastic central tendency models introduced by JP and BDFS have the general form:dx t=k1(θt−x t)dt+σ1dz1(1)dθt=k2(θ−θt)dt+σ2dz2(2) where dz1dz2=ρ1,2dt,and whereρ1,2is the correlation between the Wiener processes dz1and dz2.The coefficients k1and k2measure the degree of mean reversion of the variables to their respective means,θt andθ.σ1and 3In the LIBOR contract,m has to be adjusted for the day-count convention.Hence, m becomes the actual number of days of the loan contract divided by the day-count basis (usually360or365days).Interest Rate Futures6σ2are the instantaneous standard deviations of the variables x andθ.In JP,x t=i t is the continuously compounded short-term interest rate.The central tendencyθt is interpreted as either a“federal funds target”or as reflecting“investors’rational expectations of longer-term inflation.”In the paper by BDFS,x t is again the short-term interest rate.However,they suggest a slightly more general process for the central tendencydθt=k2(θ−θt+a)dt+σ2dz2(3) The constant allows for a drift in the central tendency.In both models,the short-term interest rate is normally distributed.Essentially,these models are two-factor extensions of the one-factor Vasicek (1977)model.A similar extension is made in Hull and White(1994),with a slightly different assumption that allows the drift of the short-term interest rate to be time dependent.Hull and White assume that x t is any function of the short rate,for example;if x t=ln(i t),where i t is the continuously compounded short term rate,then the model is a two-factor extension of the lognormal Black and Karasinski model.Hull and White state the model in a slightly different form from that of JP and BDFS:dx t=(φt+u t−k1x t)dt+σ1dz1(4)du t=−k2u t dt+σ02dz2(5) However,this model can be shown to be a simple transformation of the BDFS model,with the generalisation that the drift term a is time dependent, i.e.(3)contains a term a t.4In this paper,we consider the general Hull-White class of two-factor models. In discrete form,these models have the following general structure:5.x t+1−x t=c(φt−x t)+y t+²t+1(8) 4Letφt=k1θt−u t,(6)σ02=k1σ2.(7) Then substitution of equations(6)and(7)in equations(4)and(5)yields the general BDFS model(1)and(3).5Dai and Singleton(2000),in the discussion following their equation(20),argue that models of this type,with the additional restriction that the innovations in r t andθt are uncorrelated,fail to capture the empirical term structure of volatility.They suggest thatInterest Rate Futures7y t+1−y t=−αy t+νt+1,(9)E(²t+1)=E(νt+1)=0(10)wherec=1−e−k1nα=1−e−k2n,and n is the length of the time period.In this model,y t has an initial value of zero and mean reverts to zero.6It follows that E(y t)=0,and hence, taking expectations in equation(8),E(x t+1)−E(x t)=c(φt−x t)Then,substituting back in equation(8)we havex t+1−E(x t+1)=(1−c)[x t−E(x t)]+y t+²t+1(11) Hence,in this type of model,the value of x t reverts at the rate c to its initial expected value.We now establish that,if a variable follows the above process,the conditional expectation of the variable is necessarily governed by a two-factor cross-sectional model.We begin by proving this result quite generally,and then apply it to the special case where x t is an interest rate or its logarithm.Lemma1The variable x t follows the processx t+1−E(x t+1)=(1−c)[x t−E(x t)]+y t+²t+1wherey t+1−y t=−αy t+νt+1if and only if the conditional expectation of x t+k is of the formE t(x t+k)=a k x t+b k E t(x t+1)humped shaped volatility term structures are not possible in the above model and the volatility structure is monotonic.However,as shown,for example,by Hull and White (1994),Figure3,this is not true.The simulations in Section4below also illustrate this point in some detail for the case of futures rate volatilities.6See Hull and White(1994),footnote4.Interest Rate Futures8 whereb k=kXτ=1(1−c)k−τ(1−α)τ−1(12)a k=(1−c)k−(1−c)b k.(13)Proof.See appendix1.First,let us take the simplest case where x is the short-term rate of interest. The lemma then implies that if the short rate follows the Hull-White process, the expectation of the short rate k periods hence,is linear in the short rate and the expectation of the short rate at t=1.The implication of this result can be illustrated as follows.Under the expectations hypothesis,where the forward rate is the expectation of the future spot rate,it follows that the k-th period forward rate is a linear function of the spot rate and the t=1 forward rate.One important implication of the lemma is that in this type of two-factor model,the cross-sectional linear coefficients a k and b k are invariant to the in-terchange of the mean reversion coefficient,c and the persistence parameter,α.That isa k,b k|c,α=a k,b k|c0,α0,if c0=α,andα0=c.This identification problem means that it may be difficult to distinguish models where the interest rate reverts very rapidly to a slowly decaying central tendency,from those where the interest rate reverts slowly to a rapidly decaying central tendency.7Lemma1states the implications of a two-dimensional,stochastic conditional mean,process for an arbitrary function of the zero-coupon bond price.The function could be a rate of interest,such as the continuously compounded rate(as in HJM)or the LIBOR(as in BGM),or it could be any other function of the price of the zero-coupon bond itself.The lemma restricts the cross-sectional properties of the conditional expectation.As we will 7This partially explains why,in the calibration of the model in section4,there are two sets of parameters that yield exactly the same volatilities and correlations of the futures rates.It may also explain discrepancies in empirical results presented in JP,DS and others.Interest Rate Futures9 see in the following section,these properties are directly relevant for the investigation of futures prices and rates.The intuition behind Lemma1is that the two influences on the function of the zero-bond prices,one of which is lagged,yield a cross-sectional structure with two factors.2.3Interest-Rate Futures Prices in a No-Arbitrage Economy In this sub-section,we apply the results in the previous sub-section to de-rive futures prices and futures interest rates in a no-arbitrage setting.We assume here that the two-dimensional process,specified in equation(11) for x t=f(P t),holds under the Equivalent Martingale Measure(EMM). The EMM is the measure under which all zero-coupon bond prices,nor-malised by the money market account,follow martingales.Assuming that the process followed by x t is of the Hull-White type under the risk-neutral measure abstracts from considerations of the market price of risk.It allows us to directly derive prices for futures contracts on x t.Cox,Ingersoll and Ross(1981)and Jarrow and Oldfield(1981)established the proposition that the futures price,of any asset,is the expected value of the future spot price of the asset,where the expected value is taken with respect to the equivalent martingale measure.We can now apply this result to determine futures prices,assuming that a function of the bond price is generated by the two-dimensional process analysed above.Since there is a one-to-one relationship between zero-coupon bond prices and short-term interest rates,defined in a particular way,we can then proceed to derive a model for futures interest rates.Initially,we make no specific distributional assumptions.We assume only a)a no-arbitrage economy in which the EMM exists,b)that x t,which is some function of the time t price of an m-year zero-coupon bond,follows a stochasic central tendency process of the general form assumed in Lemma 1,and c)that a market exists for trading futures contracts on x t,where the contracts are marked-to-market at the same frequency as the definition of the discrete time-period from t to t+1.Wefirst establish a general result, and then illustrate it with some familiar examples.We denote the futures price,at t,for delivery of x t+k at t+k,as x t,k.We now have: Proposition1(General Cross-Sectional Relationship for Futures Prices)Interest Rate Futures10 Assume that equation(11)holds for x t under the EMM,where x t=f(P t), then the k-period ahead futures price of x t is given by the two-factor linear relationship:x t,k−x0,k=a k[x t−x0,t]+b k[x t,t+1−x0,t+1]whereb k=kXτ=1(1−c)k−τ(1−α)τ−1(14)a k=(1−c)k−(1−c)b k.(15) Proof.From CIR(1981),proposition2and Pliska(1997),the futures price of any payoffis its expected value,under the EMM.Applying this result to x t+k,yieldsx t,k=E t(x t+k)(16) Substituting equation(16)in Lemma1yields the statement in the Propo-sition.2The rather general result in Proposition1is of principal interest because of two special cases.Thefirst is the case where the futures contract is on the zero-coupon bond itself.The second is the case of a futures contract on an interest rate,such as LIBOR,which is a function of the zero-coupon bond price.Thefirst case is typified by the T.Bill futures contract traded on the Sydney Futures Exchange.The second case is the most common, typified by the Eurocurrency futures contract.We consider these cases in the corollaries below.RemarkAn interesting implication of Proposition1is that if the bond price itself follows a linear process,under the EMM,then the futures prices of the bond will be given by a two-factor cross-sectional relationship.This follows by assuming that x t=f(P t)=P t in the Proposition.This shows that futures prices at time t are generated by a linear two-factor model,if and only if the zero-bond price follows a process of the Hull-White type.Note that the two factors generating the k th futures price are the spot price of the bond and thefirst futures price,i.e.,the futures with maturity equal to t+1.Interest Rate Futures11 Similarly,the variance of the k th futures price is determined by the variance of the spot bond price,the variance of the conditional mean and the mean-reversion coefficients.This is helpful in understanding the conditions under which the term structure follows a two-factor process.Essentially,if futures prices of long-dated futures contracts are given by the cross-sectional model in Proposition1,then forward prices,and also futures and forward rates will follow two-factor models.The relationship for interest rates,however, is,in general,complex,since the functions i t(P t)and r t(P t)are non-linear.We now illustrate the use of Proposition1in the case of interest rate(as opposed to bond-price)futures.Instead of assuming that the price of a zero-coupon bond follows a two-dimensional,linear process,we now assume that the interest rate,LIBOR,follows a stochastic central tendency process. We have the following corollary of Proposition1:Corollary1(Cross-Sectional Relationship for LIBOR Futures Prices for the Case of a Linear Process for the LIBOR)In a no-arbitrage economy,the short-term rate of interest follows a process of the formr t+1=E0[r t+1]+(1−c)[r t−E0(r t)]+y t+²t+1(17) wherey t+1−y t=−αy t+νt+1andE t(²t+1)=0,E t(νt+1)=0,if and only if the term structure of futures rates at time t is generated by a two-factor model,where the k th futures rate is given byr t,k−r0,t+k=a k[r t−r0,t]+b k[r t,t+1−r0,t+1](18) where a k and b k are given by(15)and(14)respectively.Interest Rate Futures12 Proof.The proof of the corollary again follows as a special case of Proposi-tion1,where x t=r t.2The corollary illustrates the simple two-factor structure of futures rates that is implied by the two-dimensional process for the spot rate.Note that the mean-reversion coefficients are embedded in the cross-sectional coefficients, a k and b k.Also,given the linear structure,it follows from(18),that the futures rates will be normally distributed,if the spot rate and thefirst futures rate are normally distributed.Hence,the corollary could be helpful in building a Gaussian model of the term structure of futures rates.83LIBOR futures prices in a lognormal short-rate modelIn the previous section,we showed that if the short-term LIBOR interest rate,evolves as a two-dimensional mean-reverting process under the risk-neutral measure,then a simple cross-sectional relationship exists between futures rates of various maturities.In principle,this type of model could be applied to predict relationships between the prices of Eurocurrency futures contracts,based on LIBOR or some other similar reference rate,which are the most important short-term interest rate futures contracts traded on the markets.However,in the case of LIBOR,the consensus in the academic literature and in market practice is that changes in interest rates are depen-dent on the level of interest rates.In particular,a lognormal distribution for short-term interest rates is commonly assumed.9When the logarithm of the short-term interest rate follows a linear process, the results of the analysis of futures prices in section2cannot be used directly,since the market does not trade futures on the logarithm of the LI-8In a two-factor extension of the Vasicek(1977)framework,JP(1996)estimate a two-factor term structure model that is similar to that in equation(18)under the assumption of normally distributed interest rates.They show that their modelfits the level of Eurodollar short-term interest rates contracts rather well for maturities of up to two years,and changes in the rates for longer-dated contracts.It is possible that this is because of ignoring the skewness effect(due to the normality assumption),which becomes significant for longer-dated contracts.9This is borne out by the empirical research of Chan et.al.,(1992)and more recently of Eom(1994)and Bliss and Smith(1998).There continues to be debate over the elasticity parameter of the changes in interest rates with respect to the level.。

货币银行学题库Chapter4 (7)

货币银行学第六章纸质练习姓名:班级:学号:请注意,选择题的答案请写在下面的方框中,否则判为0分。

Multiple Choice1)The risk structure of interest rates is(a)the structure of how interest rates move over time.(b)the relationship among interest rates of different bonds with the same maturity.(c)the relationship among the term to maturity of different bonds.(d)the relationship among interest rates on bonds with different maturities.2)Default risk is the risk that(a)a bond issuer is unable to make interest payments.(b)a bond issuer is unable to make a profit.(c)a bond issuer is unable to pay the face value at maturity.(d)all of the above.(e)both (a) and (c) above.3)The spread between the interest rates on bonds with default risk and default-free bonds iscalled the(a)risk premium.(b)junk margin.(c)bond margin.(d)default premium.4)When the default risk in corporate bonds decreases, other things equal, the demand curve forcorporate bonds shifts to the _____ and the demand curve for Treasury bonds shifts to the _____.(a)right; right(b)right; left(c)left; left(d)left; right5)The risk premium on corporate bonds becomes smaller if(a)the riskiness of corporate bonds increases.(b)the liquidity of corporate bonds increases.(c)the liquidity of corporate bonds decreases.(d)the riskiness of corporate bonds decreases.(e)both (b) and (d) occur.6) A decrease in the liquidity of corporate bonds will _____ the price of corporate bondsand _____ the yield of Treasury bonds.(a)increase; increase(b)reduce; reduce(c)increase; reduce(d)reduce; increase(e)reduce; not affect7)An increase in marginal tax rates would likely have the effect of _____ the demandfor municipal bonds, and _____ the demand for U.S. government bonds.(a)increasing; increasing(b)increasing; decreasing(c)decreasing; increasing(d)decreasing; decreasing8)Three factors explain the risk structure of interest rates:(a)liquidity, default risk, and the income tax treatment of a security.(b)maturity, default risk, and the income tax treatment of a security.(c)maturity, liquidity, and the income tax treatment of a security.(d)maturity, default risk, and the liquidity of a security.(e)maturity, default risk, and inflation.9)The term structure of interest rates is(a)the relationship among interest rates of different bonds with the same maturity.(b)the structure of how interest rates move over time.(c)the relationship among the term to maturity of different bonds.(d)the relationship among interest rates on bonds with different maturities.10)When yield curves are steeply upward sloping,(a)long-term interest rates are above short-term interest rates.(b)short-term interest rates are above long-term interest rates.(c)short-term interest rates are about the same as long-term interest rates.(d)medium-term interest rates are above both short-term and long-term interest rates.(e)medium-term interest rates are below both short-term and long-term interest rates.11)According to the expectations theory of the term structure(a)the interest rate on long-term bonds will equal an average of short-term interestrates that people expect to occur over the life of the long-term bonds.(b)buyers of bonds do not prefer bonds of one maturity over another.(c)yield curves should be as equally likely to slope downward as slope upward.(d)all of the above.(e)only (a) and (b) of the above.12)If the expected path of one-year interest rates over the next five years is 4 percent, 5percent, 7 percent, 8 percent, and 6 percent, then the expectations theory predicts that today’s interest rate on the five-year bond is(a)4 percent.(b)5 percent.(c)6 percent.(d)7 percent.(e)8 percent.13)According to the segmented markets theory of the term structure(a)the interest rate for each maturity bond is determined by supply and demand forthat maturity bond.(b)investors’ strong preferences for short-term relative to long-term bondsexplains why yield curves typically slope upward.(c)bonds of one maturity are close substitutes for bonds of other maturities, therefore,interest rates on bonds of different maturities move together over time.(d)all of the above.(e)only (a) and (b) of the above.14)The liquidity premium theory of the term structure(a)indicates that today’s long-term interest rate equals the average of short-terminterest rates that people expect to occur over the life of the long-term bond.(b)assumes that bonds of different maturities are perfect substitutes.(c)suggests that markets for bonds of different maturities are completely separatebecause people have preferred habitats.(d)does none of the above.15)If 1-year interest rates for the next four years are expected to be 4, 2, 3, and 3 percent, andthe 4-year term premium is 1 percent, than the 4-year bond rate will be(a)1 percent.(b)2 percent.(c)3 percent.(d)4 percent.(e)5 percent.16)According to the liquidity premium theory of the term structure(a)when short-term interest rates are expected to rise in the future, the yield curvewill be steeply upward sloping.(b)when short-term interest rates are expected to remain unchanged in the future, theyield curve is likely to be slightly upward sloping.(c)when short-term interest rates are expected to decline moderately in the future, theyield curve is likely to be flat.(d)all of the above.(e)only (a) and (b) of the above.17)Which of the following theories of the term structure is (are) able to explain the factthat interest rates on bonds of different maturities tend to move together over time?(a)The expectations theory(b)The segmented markets theory(c)The liquidity premium theory(d)Both (a) and (b) of the above(e)Both (a) and (c) of the above18)The preferred habitat theory of the term structure is closely related to the(a)expectations theory of the term structure.(b)segmented markets theory of the term structure.(c)liquidity premium theory of the term structure.(d)the inverted yield curve theory of the term structure.(e)risk premium theory of the term structure19)A particularly attractive feature of the _____ is that it tells you what the market ispredicting about future short-term interest rates by just looking at the slope of the yield curve.(a)segmented markets theory(b)expectations theory(c)liquidity premium theory(d)both (a) and (b) of the aboveFigure 6-120)The steeply upward sloping yield curve in Figure 6-1 indicates that(a)short-term interest rates are expected to rise in the future.(b)short-term interest rates are expected to fall moderately in the future.(c)short-term interest rates are expected to fall sharply in the future.(d)short-term interest rates are expected to remain unchanged in the future.Essay Questions21)Demonstrate graphically and explain how a reduction in default risk affects the demandor supply of corporate and Treasury bonds.22)What is the shape of the yield curve when short rates are expected to fall in themedium term, and then increase? Demonstrate this graphically.。

投资学第7版TestBank答案解析15

投资学第7版TestBank答案解析15Multiple Choice Questions1. The term structure of interest rates is:A) The relationship between the rates of interest on all securities.B) The relationship between the interest rate on a security and its timeto maturity.C) The relationship between the yield on a bond and its default rate.D) All of the above.E) None of the above.Answer: B Difficulty: EasyRationale: The term structure of interest rates is the relationshipbetween two variables, years and yield to maturity (holding all elseconstant).2. The yield curve shows at any point in time:A) The relationship between the yield on a bond and the duration of thebond.B) The relationship between the coupon rate on a bond and time to maturityof the bond.C) The relationship between yield on a bond and the time to maturity onthe bond.D) All of the above.E) None of the above.Answer: C Difficulty: Easy3. An inverted yield curve implies that:A) Long-term interest rates are lower than short-term interest rates.B) Long-term interest rates are higher than short-term interest rates.C) Long-term interest rates are the same as short-term interest rates.D) Intermediate term interest rates are higher than either short- orlong-term interest rates.E) none of the above.Answer: A Difficulty: EasyRationale: The inverted, or downward sloping, yield curve is one in which short-term rates are higher than long-term rates. The inverted yield curve has been observed frequently, although not as frequently as the upwardsloping, or normal, yield curve.4. An upward sloping yield curve is a(n) _______ yield curve.A) normal.B) humped.C) inverted.D) flat.E) none of the above.Answer: A Difficulty: EasyRationale: The upward sloping yield curve is referred to as the normal yield curve, probably because, historically, the upward sloping yield curve is the shape that has been observed most frequently.5. According to the expectations hypothesis, a normal yield curve impliesthatA) interest rates are expected to remain stable in the future.B) interest rates are expected to decline in the future.C) interest rates are expected to increase in the future.D) interest rates are expected to decline first, then increase.E) interest rates are expected to increase first, then decrease.Answer: C Difficulty: EasyRationale: An upward sloping yield curve is based on the expectation that short-term interest rates will increase.6. Which of the following is not proposed as an explanation for the termstructure of interest rates?A) The expectations theory.B) The liquidity preference theory.C) The market segmentation theory.D) Modern portfolio theory.E) A, B, and C.Answer: D Difficulty: EasyRationale: A, B, and C are all theories that have been proposed to explain the term structure.7. The expectations theory of the term structure of interest rates statesthatA) forward rates are determined by investors' expectations of futureinterest rates.B) forward rates exceed the expected future interest rates.C) yields on long- and short-maturity bonds are determined by the supplyand demand for the securities.D) all of the above.E) none of the above.Answer: A Difficulty: EasyRationale: The forward rate equals the market consensus expectation of future short interest rates.8. Which of the following theories state that the shape of the yield curveis essentially determined by the supply and demands for long-andshort-maturity bonds?A) Liquidity preference theory.B) Expectations theory.C) Market segmentation theory.D) All of the above.E) None of the above.Answer: C Difficulty: EasyRationale: Market segmentation theory states that the markets fordifferent maturities are separate markets, and that interest rates at the different maturities are determined by the intersection of the respective supply and demand curves.9. According to the "liquidity preference" theory of the term structure ofinterest rates, the yield curve usually should be:A) inverted.B) normal.C) upward slopingD) A and B.E) B and C.Answer: E Difficulty: EasyRationale: According to the liquidity preference theory, investors wouldprefer to be liquid rather than illiquid. In order to accept a more illiquid investment, investors require a liquidity premium and the normal, or upward sloping, yield curve results.Use the following to answer questions 10-13:Suppose that all investors expect that interest rates for the 4 years will be as follows:10. What is the price of 3-year zero coupon bond with a par value of $1,000?A) $863.83B) $816.58C) $772.18D) $765.55E) none of the aboveAnswer: B Difficulty: ModerateRationale: $1,000 / (1.05)(1.07)(1.09) = $816.5811. If you have just purchased a 4-year zero coupon bond, what would be theexpected rate of return on your investment in the first year if the implied forward rates stay the same? (Par value of the bond =A) 5%B) 7%C) 9%D) 10%E) none of the aboveAnswer: A Difficulty: ModerateRationale: The forward interest rate given for the first year of theinvestment is given as 5% (see table above).12. What is the price of a 2-year maturity bond with a 10% coupon rate paidannually? (Par value = $1,000)A) $1,092B) $1,054C) $1,000D) $1,073E) none of the aboveAnswer: D Difficulty: ModerateRationale: [(1.05)(1.07)]1/2 - 1 = 6%; FV = 1000, n = 2, PMT = 100, i = 6, PV = $1,073.3413. What is the yield to maturity of a 3-year zero coupon bond?A) 7.00%B) 9.00%C) 6.99%D) 7.49%E) none of the aboveAnswer: C Difficulty: ModerateRationale: [(1.05)(1.07)(1.09)]1/3 - 1 = 6.99.Use the following to answer questions 14-16:The following is a list of prices for zero coupon bonds with different maturities and par value of $1,000.14. What is, according to the expectations theory, the expected forward ratein the third year?A) 7.00%B) 7.33%C) 9.00%E) none of the aboveAnswer: C Difficulty: ModerateRationale: 881.68 / 808.88 - 1 = 9%15. What is the yield to maturity on a 3-year zero coupon bond?A) 6.37%B) 9.00%C) 7.33%D) 10.00%E) none of the aboveAnswer: C Difficulty: ModerateRationale: (1000 / 808.81)1/3 -1 = 7.33%16. What is the price of a 4-year maturity bond with a 12% coupon rate paidannually? (Par value = $1,000)A) $742.09B) $1,222.09C) $1,000.00D) $1,141.92E) none of the aboveAnswer: D Difficulty: DifficultRationale: (1000 / 742.09)1/4 -1 = 7.74%; FV = 1000, PMT = 120, n = 4, i = 7.74, PV = $1,141.9217. The market segmentation theory of the term structure of interest ratesA) theoretically can explain all shapes of yield curves.B) definitely holds in the "real world".C) assumes that markets for different maturities are separate markets.D) A and B.E) A and C.Answer: E Difficulty: EasyRationale: Although this theory is quite tidy theoretically, bothinvestors and borrows will depart from their "preferred maturity habitats"if yields on alternative maturities are attractive enough.18. An upward sloping yield curveA) may be an indication that interest rates are expected to increase.B) may incorporate a liquidity premium.C) may reflect the confounding of the liquidity premium with interest rateexpectations.D) all of the above.E) none of the above.Answer: D Difficulty: EasyRationale: One of the problems of the most commonly used explanation of term structure, the expectations hypothesis, is that it is difficult to separate out the liquidity premium from interest rate expectations.19. The "break-even" interest rate for year n that equates the return on ann-period zero-coupon bond to that of an n-1-period zero-coupon bond rolled over into a one-year bond in year n is defined asA) the forward rate.B) the short rate.C) the yield to maturity.D) the discount rate.E) None of the above.Answer: A Difficulty: EasyRationale: The forward rate for year n, fn, is the "break-even" interest rate for year n that equates the return on an n-period zero-coupon bond to that of an n-1-period zero-coupon bond rolled over into a one-year bond in year n.20. When computing yield to maturity, the implicit reinvestment assumptionis that the interest payments are reinvested at the:A) Coupon rate.B) Current yield.C) Yield to maturity at the time of the investment.D) Prevailing yield to maturity at the time interest payments arereceived.E) The average yield to maturity throughout the investment period.Answer: C Difficulty: ModerateRationale: In order to earn the yield to maturity quoted at the time of the investment, coupons must be reinvested at that rate.21. Which one of the following statements is true?A) The expectations hypothesis indicates a flat yield curve ifanticipated future short-term rates exceed the current short-termrate.B) The basic conclusion of the expectations hypothesis is that thelong-term rate is equal to the anticipated long-term rate.C) The liquidity preference hypothesis indicates that, all other thingsbeing equal, longer maturities will have lower yields.D) The segmentation hypothesis contends that borrows and lenders areconstrained to particular segments of the yield curve.E) None of the above.Answer: D Difficulty: ModerateRationale: A flat yield curve indicates expectations of existing rates.Expectations hypothesis states that the forward rate equals the market consensus of expectations of future short interest rates. The reverse of C is true.22. The concepts of spot and forward rates are most closely associated withwhich one of the following explanations of the term structure of interest rates.A) Segmented Market theoryB) Expectations HypothesisC) Preferred Habitat HypothesisD) Liquidity Premium theoryE) None of the aboveAnswer: B Difficulty: ModerateRationale: Only the expectations hypothesis is based on spot and forward rates. A and C assume separate markets for different maturities; liquidity premium assumes higher yields for longer maturities.Use the following to answer question 23:23. Given the bond described above, if interest were paid semi-annually(rather than annually), and the bond continued to be priced at $850, the resulting effective annual yield to maturity would be:A) Less than 12%B) More than 12%C) 12%D) Cannot be determinedE) None of the aboveAnswer: B Difficulty: ModerateRationale: FV = 1000, PV = -850, PMT = 50, n = 40, i = 5.9964 (semi-annual);(1.059964)2 - 1 = 12.35%.24. Interest rates might declineA) because real interest rates are expected to decline.B) because the inflation rate is expected to decline.C) because nominal interest rates are expected to increase.D) A and B.E) B and C.Answer: D Difficulty: EasyRationale: The nominal rate is comprised of the real interest rate plus the expected inflation rate.25. Forward rates ____________ future short rates because ____________.A) are equal to; they are both extracted from yields to maturity.B) are equal to; they are perfect forecasts.C) differ from; they are imperfect forecasts.D) differ from; forward rates are estimated from dealer quotes whilefuture short rates are extracted from yields to maturity.E) are equal to; although they are estimated from different sources theyboth are used by traders to make purchase decisions.Answer: C Difficulty: EasyRationale: Forward rates are the estimates of future short rates extracted from yields to maturity but they are not perfect forecasts because the future cannot be predicted with certainty; therefore they will usually differ.26. The pure yield curve can be estimatedA) by using zero-coupon bonds.B) by using coupon bonds if each coupon is treated as a separate "zero."C) by using corporate bonds with different risk ratings.D) by estimating liquidity premiums for different maturities.E) A and B.Answer: E Difficulty: ModerateRationale: The pure yield curve is calculated using zero coupon bonds, but coupon bonds may be used if each coupon is treated as a separate "zero."27. The on the run yield curve isA) a plot of yield as a function of maturity for zero-coupon bonds.B) a plot of yield as a function of maturity for recently issued couponbonds trading at or near par.C) a plot of yield as a function of maturity for corporate bonds withdifferent risk ratings.D) a plot of liquidity premiums for different maturities.E) A and B.Answer: B Difficulty: Moderate28. The market segmentation and preferred habitat theories of term structureA) are identical.B) vary in that market segmentation is rarely accepted today.C) vary in that market segmentation maintains that borrowers and lenderswill not depart from their preferred maturities and preferred habitatmaintains that market participants will depart from preferredmaturities if yields on other maturities are attractive enough.D) A and B.E) B and C.Answer: E Difficulty: ModerateRationale: Borrowers and lenders will depart from their preferred maturity habitats if yields are attractive enough; thus, the market segmentation hypothesis is no longer readily accepted.29. The yield curveA) is a graphical depiction of term structure of interest rates.B) is usually depicted for U. S. Treasuries in order to hold risk constantacross maturities and yields.C) is usually depicted for corporate bonds of different ratings.D) A and B.E) A and C.Answer: D Difficulty: EasyRationale: The yield curve (yields vs. maturities, all else equal) is depicted for U. S. Treasuries more frequently than for corporate bonds, as the risk is constant across maturities for Treasuries.Use the following to answer questions 30-32:30. What should the purchase price of a 2-year zero coupon bond be if it ispurchased at the beginning of year 2 and has face value of $1,000?A) $877.54B) $888.33C) $883.32D) $893.36E) $871.80Answer: A Difficulty: DifficultRationale: $1,000 / [(1.064)(1.071)] = $877.5431. What would the yield to maturity be on a four-year zero coupon bondpurchased today?A) 5.80%B) 7.30%C) 6.65%D) 7.25%E) none of the above.Answer: C Difficulty: ModerateRationale: [(1.058) (1.064) (1.071) (1.073)]1/4 - 1 = 6.65%32. Calculate the price at the beginning of year 1 of a 10% annual coupon bondwith face value $1,000 and 5 years to maturity.A) $1,105B) $1,132C) $1,179D) $1,150E) $1,119Answer: B Difficulty: DifficultRationale: i = [(1.058) (1.064) (1.071) (1.073) (1.074)]1/5 - 1 = 6.8%; FV = 1000, PMT = 100, n = 5, i = 6.8, PV = $1,131.91 33. Given the yield on a 3 year zero-coupon bond is 7.2% and forward ratesof 6.1% in year 1 and 6.9% in year 2, what must be the forward rate in year 3?A) 8.4%B) 8.6%C) 8.1%D) 8.9%E) none of the above.Answer: B Difficulty: ModerateRationale: f3 = (1.072)3 / [(1.061) (1.069)] - 1 = 8.6%34. An inverted yield curve is oneA) with a hump in the middle.B) constructed by using convertible bonds.C) that is relatively flat.D) that plots the inverse relationship between bond prices and bondyields.E) that slopes downward.Answer: E Difficulty: EasyRationale: An inverted yield curve occurs when short-term rates are higher than long-term rates.35. Investors can use publicly available financial date to determine whichof the following?I)the shape of the yield curveII)future short-term ratesIII)the direction the Dow indexes are headingIV)the actions to be taken by the Federal ReserveA) I and IIB) I and IIIC) I, II, and IIID) I, III, and IVE) I, II, III, and IVAnswer: A Difficulty: ModerateRationale: Only the shape of the yield curve and future inferred rates can be determined. The movement of the Dow Indexes and Federal Reserve policy are influenced by term structure but are determined by many other variables also.36. Which of the following combinations will result in a sharply increasingyield curve?A) increasing expected short rates and increasing liquidity premiumsB) decreasing expected short rates and increasing liquidity premiumsC) increasing expected short rates and decreasing liquidity premiumsD) increasing expected short rates and constant liquidity premiumsE) constant expected short rates and increasing liquidity premiumsAnswer: A Difficulty: ModerateRationale: Both of the forces will act to increase the slope of the yield curve.37. The yield curve is a component ofA) the Dow Jones Industrial Average.B) the consumer price index.C) the index of leading economic indicators.D) the producer price index.E) the inflation index.Answer: C Difficulty: EasyRationale: Since the yield curve is often used to forecast the business cycle, it is used as one of the leading economic indicators.38. The most recently issued Treasury securities are calledA) on the run.B) off the run.C) on the market.D) off the market.E) none of the above.Answer: A Difficulty: EasyUse the following to answer questions 39-42:Suppose that all investors expect that interest rates for the 4 years will be as follows:。

6sigma黑带培训教材英文精编版

Distribution of Individual ValuesDistribution of Sample Averages

Process Capability Indices

Two measures of process capabilityProcess PotentialCp Process PerformanceCpu Cpl Cpk

Process Capability

Process Capability is the inherent reproducibility of a process’s output. It measures how well the process is currently behaving with respect to the output specifications. It refers to the uniformity of the process.Capability is often thought of in terms of the proportion of output that will be within product specification tolerances. The frequency of defectives produced may be measured ina) percentage (%)b) parts per million (ppm)c) parts per billion (ppb)

Process Potential

a) Process is highly capable (Cp>2)b) Process is capable (Cp=1 to 2)c) Process is not capable (Cp<1)

The Term Structure of Interest Rates

based only on expectations of future short-term rates Term structure might be normal, inverted, humped, or flat Ignores price risk and reinvestment risk Interpretations include broad, local and return-to-maturity

Determinants of the Shape of the Term Structure

Pure Expectations Theory Liquidity Theory Preferred Habitat Theory Market Segmentation Theory

Pure ions Theory

Historical Shapes of Yield Curves

Positively sloped yield curve Normal yield curve Steep yield curve Inverted yield curve Flat yield curve

Historical Shapes of Yield Curves

Maturity of an instrument is the coupon

payment date or maturity date Value of the asset equals the total value of the component zero-coupon instruments

Liquidity Theory

FMI7e_ch01Role of Financial Markets and Institutions(金融市场好机构—7e, by Jeff Madura))

Risk

preference Desired liquidity Tax status

13

Market Efficiency (cont’d)

Impact of asymmetric information

Different investors may value the same security differently based on their interpretation of information

Every security has an equilibrium market price at which demand and supply for the security are equal

Impact of valuations on pricing

Favorable information results in upward valuation revisions; unfavorable information results in downward revisions

Securities reach a new equilibrium price as new information becomes available

9

Securities Traded in Financial Markets (cont’d)

Derivative securities

Derivative

securities are financial contracts whose values are derived from the values of underlying assets Speculating with derivatives allow investors to benefit from increases or decreases in the underlying asset Risk management with derivatives generates gains if the value of the underlying security declines

国际贸易双语教案问题答案