PLUS_TaxGuide_2008

在美国课税与申报目的下之最终受益人身分证明(实体)

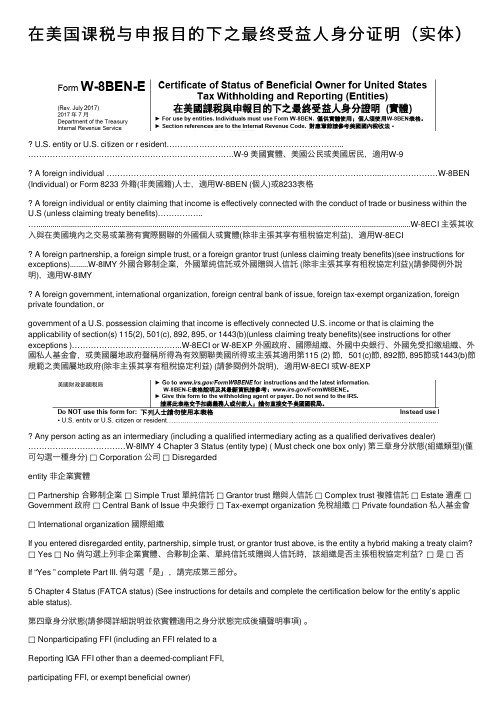

在美国课税与申报⽬的下之最终受益⼈⾝分证明(实体)U.S. entity or U.S. citizen or r esident………………………………………………………...………………………………………………………………….W-9 美國實體、美國公民或美國居民,適⽤W-9A foreign individual ………………………………………………………………………………………...…………………W-8BEN (Individual) or Form 8233 外籍(⾮美國籍)⼈⼠,適⽤W-8BEN (個⼈)或8233表格A foreign individual or entity claiming that income is effectively connected with the conduct of trade or business within the U.S (unless claiming treaty benefits)……………..…........................................................................................................................................................................................W-8ECI 主張其收⼊與在美國境內之交易或業務有實際關聯的外國個⼈或實體(除⾮主張其享有租稅協定利益),適⽤W-8ECIA foreign partnership, a foreign simple trust, or a foreign grantor trust (unless claiming treaty benefits)(see instructions for exceptions).........W-8IMY 外國合夥制企業,外國單純信託或外國贈與⼈信託 (除⾮主張其享有租稅協定利益)(請參閱例外說明),適⽤W-8IMYA foreign government, international organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, orgovernment of a U.S. possession claiming that income is effectively connected U.S. income or that is claiming the applicability of section(s) 115(2), 501(c), 892, 895, or 1443(b)(unless claiming treaty benefits)(see instructions for other exceptions )…………………………………..W-8ECI or W-8EXP 外國政府、國際組織、外國中央銀⾏、外國免受扣繳組織、外國私⼈基⾦會,或美國屬地政府聲稱所得為有效關聯美國所得或主張其適⽤第115 (2) 節,501(c)節, 892節, 895節或1443(b)節規範之美國屬地政府(除⾮主張其享有租稅協定利益) (請參閱例外說明),適⽤W-8ECI 或W-8EXPAny person acting as an intermediary (including a qualified intermediary acting as a qualified derivatives dealer)………………………………W-8IMY 4 Chapter 3 Status (entity type) ( Must check one box only) 第三章⾝分狀態(組織類型)(僅可勾選⼀種⾝分) □ Corporation 公司□ Disregardedentity ⾮企業實體□ Partnership 合夥制企業□ Simple Trust 單純信託□ Grantor trust 贈與⼈信託□ Complex trust 複雜信託□ Estate 遺產□Government 政府□ Central Bank of Issue 中央銀⾏□ Tax-exempt organization 免稅組織□ Private foundation 私⼈基⾦會□ International organization 國際組織If you entered disregarded entity, partnership, simple trust, or grantor trust above, is the entity a hybrid making a treaty claim?□ Yes □ No 倘勾選上列⾮企業實體、合夥制企業、單純信託或贈與⼈信託時,該組織是否主張租稅協定利益?□是□否If “Yes ” complete Part III. 倘勾選「是」,請完成第三部分。

税务评论

华南区 (中国内地) 苗志成 总监 电话:+86 755 3331 0993 传真:+86 755 8246 3222 电子邮件:zmiao@

华南区 (香港特别行政区) 殷国煒 总监 电话:+852 2852 6538 传真:+852 2520 6205 电子邮件:dyun@

税务

. 税务评论

NTC 税务评论期数 P30/2008 – 2008 年 10 月 15 日

转让定价服务 全国领导合伙人

中国税务

张新华

电话: +86 21 6141 1068

电子邮件: ryanchang@ 资本弱化标准正式颁布

钢特木尔

电话: +86 21 6141 1016

背景概述

电子邮件: muegangte@

李晓晖 电话: +86 10 8520 7520 电子邮件: samxhli@

2008 年 1 月 1 日起生效施行的《中华人民共和国企业所得税法》(以下简称 “企业所得税法”)在第六章“特别纳税调整”中首次提出了防范“资本弱 化”的内容。根据企业所得税法第 46 条的规定,企业从其关联方接受的债权 性投资与权益性投资的比例超过规定标准而发生的利息支出,不得在计算应纳

而根据所得税法第 41 条的规定,企业与其关联方之间的业务往来,必须符合独立交易原则,否则税务机关 有权按照合理方法调整。

要点 2)正是对所得税法第 41 条独立交易原则的呼应。结合上述对所得税法第 46 条和第 41 条的理解,121 号 文中对关联方借贷利息税前扣除所确立的处理思路是:

• 超过规定负债权益比例的,不论交易对价是否公允,相关利息一律不得税前扣除; • 不超过规定负债权益比例的,企业仍需要提供资料证明关联方融资活动符合独立交易原则(或该利息系

FORM B, FORM E. FORM F. FORM P的总结

FORM B, FORM E. FORM F. FORM P的总结一、普惠制原产地证明书(FORM A)普惠制原产地证书是具有法律效力的我国出口产品在给惠国享受在最惠国税率基础上进一步减免进口关税的官方凭证。

目前给予我国普惠制待遇的国家共38个:欧盟27国(比利时、丹麦、英国、德国、法国、爱尔兰、意大利、卢森堡、荷兰、希腊、葡萄牙、西班牙、奥地利、芬兰、瑞典、波兰、捷克、斯洛伐克、拉脱维亚、爱沙尼亚、立陶宛、匈牙利、马耳他、塞浦路斯、斯洛文尼亚、保加利亚、罗马尼亚)、挪威、瑞士、土耳其、俄罗斯、白俄罗斯、乌克兰、哈萨克斯坦、日本、加拿大、澳大利亚和新西兰。

二、一般原产地证明书(CO)一般原产地证书是证明货物原产于某一特定国家或地区,享受进口国正常关税(最惠国)待遇的证明文件。

它的适用范围是:征收关税、贸易统计、保障措施、歧视性数量限制、反倾销和反补贴、原产地标记、政府采购等方面。

三、区域性经济集团互惠原产地证书目前主要有《〈中国-东盟自由贸易区〉优惠原产地证明书》、《亚太贸易协定》原产地证明书、《〈中国与巴基斯坦优惠贸易安排〉优惠原产地证明书》《〈中国—智利自贸区〉原产地证书》等。

区域优惠原产地证书是具有法律效力的在协定成员国之间就特定产品享受互惠减免关税待遇的官方凭证。

1、《中国-东盟自由贸易区》优惠原产地证明书(FORM E)自2004年1月1日起,凡出口到东盟的农产品(HS第一章到第八章)凭借检验检疫机构签发的《中国-东盟自由贸易区》(FORM E)优惠原产地证书可以享受关税优惠待遇。

2005年7月20日起,7000多种正常产品开始全面降税。

中国和东盟六个老成员国(即文莱、印度尼西亚、马来西亚、菲律宾、新加坡和泰国)至2005年7月40%税目的关税降到0-5%;2007年1月60%税目的关税要降到0-5%。

2010年1月1日将关税最终削减为零。

老挝、缅甸至2009年1月、柬埔寨至2012年1月50%的税目的关税降到0-5%;2013年40%税目的关税降到零。

上海市国家税务局关于转发《国家税务总局关于外国企业所得税纳税年度有关问题的通知》的通知

上海市国家税务局关于转发《国家税务总局关于外国企业所得税纳税年度有关问题的通知》的通知

文章属性

•【制定机关】上海市国家税务局

•【公布日期】2008.05.07

•【字号】

•【施行日期】2008.01.01

•【效力等级】地方规范性文件

•【时效性】现行有效

•【主题分类】企业所得税

正文

上海市国家税务局关于转发《国家税务总局关于外国企业所得税纳税年度有关问题的通知》的通知

各区县税务局,各财税分局:

近接《国家税务总局关于外国企业所得税纳税年度有关问题的通知》(国税函〔2008〕301号),现将该文转给你局,请按照执行。

上海市国家税务局

二OO八年五月七日国家税务总局关于外国企业所得税纳税年度有关问题的通知

国税函〔2008〕301号各省、自治区、直辖市和计划单列市国家税务局,广东省和深圳市地方税务局:现就外国企业所得税的纳税年度问题通知如下:根据《中华人民共和国外商投资企业和外国企业所得税法实施细则》第八条规定,经当地主管税务机关批准以满十二个月的会计年度为纳税年度的外国企业,其2007-2008年度企业所得税的纳税年度截止到2007年12月31日,并按照《中华人民共和国外商投资企业和外国企业所得税法》规定的税率计算缴纳企业所得税。

自2008年1月1日起,外国企业

一律以公历年度为纳税年度,按照《中华人民共和国企业所得税法》规定的税率计算缴纳企业所得税。

国家税务总局

二〇〇八年四月三日。

中华人民共和国增值税暂行条例2008(英文版)Provisional Regulations of the PRC on Value-Added Tax 2008

烟台大学法学院法律硕士张川方中华人民共和国增值税暂行条例Provisional Regulations of the PRC on Value-Added Tax(Promulgated by No. 134 Order of the State Council of the People’s Republic of China on December 13th, 1993Amended and adopted at the 34th Executive Meeting of the State Council on November 5th, 2008)No. 538 Order of the State CouncilThe Provisional Regulations of the People’s Republic of China on Value-Added Tax amended and adopted at the 34th Executive Meeting of the State Council on November 5th, 2008 is hereby promulgated and shall become effective as of January 1st, 2009.Wen Jiabao, Premier of the State CouncilNovember 10th, 2008Article 1All units and individuals engaged in the sale of goods, provision of processing, repair and replacement services(修理修配劳务), and importation of goods(进口货物) within the territory of the People’s Republic of China are taxpayers of Value-Added Tax (hereinafter referred to as(以下简称)"taxpayers"), and shall pay VAT in accordance with these Regulations.Article 2(1) VAT rates:(a) The tax rate for taxpayers selling or importing goods, other than those stipulated in Subparagraphs (b) and (c) of this Article, shall be 17%.(b) The tax rate for taxpayers selling or importing the following goods, shall be 13%:(i) food grains(粮食), edible vegetable oil(食用植物油);(ii) tap water, heating, air conditioning(冷气), hot water, coal gas, liquified petroleum gas(石油液化气), natural gas, methane gas(沼气), coal or charcoal(木炭) products for household use(居民用);(iii) books, newspapers, magazines;(iv) feeds(饲料), chemical fertilizers, agricultural chemicals(农药), agricultural machinery and covering plastic film for farming(农膜);(v) other goods as stipulated by the State Council.(c) The tax rate for taxpayers exporting goods shall be 0%, except as otherwise stipulated(另有规定的除外) by the State Council.(d) The tax rate for taxpayers providing processing, repair and replacement services (hereinafter referred to as "taxable services(应税劳务)") shall be 17%.(2) Any adjustment to(调整)the tax rates shall be determined by the State Council.Article 3If a taxpayer deals in goods or provides taxable services with different tax rates, the tax rates shall be calculated separately. If the sales amount(销售额) has not been counted separately, a higher tax rate shall apply(从高适用税率).Article 4(1) Except as stipulated in Article 11 of these Regulations, for taxpayers engaged in the sale of goods or provision of taxable services (hereinafter referred to as "selling goods or taxable services"), the tax payable shall be the balance of output tax for the period(当期销项税额) after deducting the input tax for the period(当期进项税额). The formula for computing the tax payable is as follows: Tax payable=Output tax payable for the period-Input tax for the period.(2) If the output tax for the period is less than and insufficient to offset against(抵扣) the input tax for the period, the excess input tax can be carried forward(结转) for offset in the following period.Article 5The output tax for taxpayers selling goods or providing taxable services shall be the VAT calculated based on the sales amounts and the tax rates prescribed in Article 2 of these Regulations and collected from the purchasers(向购买方收取的). The formula for computing the output tax is as follows: Output tax=Sales amount × Tax rate.Article 6(1) The sales amount shall be the total consideration(全部价款) and all other charges(价外费用) receivable from the purchasers by the taxpayer selling goods or providing taxable services, but excluding the output tax collectible(可收取的).(2) The sales amount shall be computed in RMB. The sales amount of a taxpayer settled in foreign currencies shall be converted into RMB.Article 7Where the price used by a taxpayer in selling goods or providing taxable services is obviously low and without justifications(正当理由), the sales amount shall be checked and ratified(核定)by the competent tax authority.Article 8(1) VAT paid or borne by taxpayers who purchase goods or receive taxable services (hereinafter referred to as "purchasing goods or taxable services") shall be the input tax(进项税额).(2) The following input tax can be credited against the output tax:(a) VAT indicated in the special VAT invoices(增值税专用发票) obtained from the sellers;(b) VAT indicated on the special VAT payment certificates for import(海关进口专用缴款书) obtained from the customs office.(c) the input tax calculated by the 13% deduction rate and the price indicated in the purchasing or selling invoices(销售发票) in addition to obtaining the special VAT invoices and the special payment receipts for import VAT in the purchase of agricultural products. The formula for calculating the input tax is as follows: Input tax = Purchasing price × Deduction rate.(d) the input tax calculated by the 7% deduction rate and the transport costs(运输费用) indicated in the settlement receipts thereof paid in purchasing or selling goods or in production and operation9在生产经营过程中). The formula for calculating the input tax is as follows: Input tax = Transport costs × Deduction rate.(3) Any adjustment to the items creditable(准予抵扣的) or the deduction rates shall be determined by the State Council.Article 9Where the credit documents obtained by a taxpayer purchasing goods or taxable services fall short of(不符合) the relevant provisions of the laws, administrative statutes and the competent tax authority under the State Council(国务院税务主管部门), no input tax shall be credited against the output tax.Article 10The input tax on the following items shall not be credited against the output tax:(1) taxable items used for non-VAT, items exempt from VAT, and goods or taxable services purchased for collective welfare or individual consumption;(2) abnormal losses of goods purchased or relevant taxable services;(3) goods purchased or taxable services consumed in the production of work-in-progress(制作过程中的) or finished goods(产成品)which suffer abnormal losses.(4) goods for self-consumption by taxpayers as stipulated by the competent finance authority and tax authority under the State Council;(5) transport costs for the goods stipulated in Subparagraph (1) to (4) of this Article and for the sale of tax-free goods(免税货物).Article 11(1) For small-scale taxpayers selling goods or taxable services, a summary measure based on the sales amount and the leviable rate(征收率) shall be adopted to calculate the tax payable(应纳税额) and no input tax shall be creditable. The formula for calculating the tax payable is as follows: Tax payable = Sales amount × leviable rate.(2) The criteria for small-scale taxpayers shall be stipulated by the competent finance authority and tax authority under the State Council.Article 12(1) The VAT rate leviable on small-scale taxpayers shall be 3%.(2)The adjustment to the leviable rate shall be determined by the State Council.Article 13(1) Taxpayers other than small-scale taxpayers shall apply to the competent tax authority for the grant of qualification. The specific measures for granting the qualification shall be formulated by the competent tax authority under the State Council.(2) Small-scale taxpayers with sound accounting(会计核算健全)who can provide accurate taxation information(税务资料) may, upon the approval of the competent tax authority, not be treated as small-scale taxpayers. The tax payable shall be computed pursuant to the relevant provisions of these Regulations.Article 14For taxpayers importing goods, the tax payable shall be computed based on the composite assessable price(组成计税价格) and the tax rates prescribed in Article 2 of these Regulations. The formulas for computing the composite assessable price and the tax payable are as follows: Composite assessable price = Customs dutiable value(关税完税价格) + Customs Duty(关税) + Consumption TaxTax payable = Composite assessable price × Tax rate.Article 15(1)The following items shall be exempt from VAT:(a) self-produced(自产的) agricultural products sold by agricultural producers;(b) contraceptive medicines(避孕药品) and devices;(c) antique books(古旧图书);(d) imported instruments and equipment(仪器、设备) directly used in scientific research and experiment and teaching;(e) imported materials(物资)and equipment from foreign governments and international organizations as assistance free of charge(无偿援助);(f) articles for the special use(专用的物品) by the disabled directly imported by organizations for the disabled;(g) goods to be sold which have been used by the seller.(2) Except as stipulated in the above paragraph, the VAT exemption and reduction items shall be stipulated by the State Council. No local government or department(地区、部门) shall stipulate such tax exemption or reduction items.Article 16For taxpayers engaged in tax exemption and reduction items concurrently(兼营), the sales amounts therefor shall be calculated separately. If the sales amounts have not been separately counted, no tax exemption or reduction is allowed.Article 17If the sales amounts of a taxpayer have not reached the VAT minimum threshold(增值税起征点) stipulated by the competent finance and tax authority, the VAT shall be exempt; if yes, the VAT shall be calculated and paid in full amount(全额) in accordance with these Regulations.Article 18If units or individuals outside the territory of the People’s Republic of China provide taxable services inside the territory, and no operating organs(经营机构) are set up inside the territory, the agent thereof inside the territory shall be the withholding agent(扣缴义务人); if there is no such agent, the purchaser shall be the withholding agent.Article 19(1) The time at which the liability to pay the VAT arises:(a) for the sale of goods or taxable services, it is the date on which the sales sum is received(收讫销售款项) or the documented evidence of right(凭据) to collect the sales sum is obtained.(b) for imported goods, it is the date of import declaration of customs(报关进口).(2) The time at which the liability to withhold the VAT(增值税扣缴义务)is the date on which the liability for the taxpayer to pay the VAT arises.Article 20(1) VAT shall be collected by the tax authorities(税务机关). VAT on imported goods shall be collected by the customs office(海关)on behalf of the tax authorities.(2)VAT on self-use articles(自用物品) brought or mailed into China by individuals shall be levied together with(一并)Customs Duty(关税). The detailed measures shall be formulated by theTariff Policy Committee(关税税则委员会) of the State Council together with(会同) the relevant departments.Article 21(1) Taxpayers selling goods or taxable services shall issue(开具)special VAT invoices to the purchasers who ask for them. The sales amount and output tax shall be separately indicated in the special VAT invoices.(2) Under any of the following circumstances, no special VAT invoice shall be issued:(a) selling goods or taxable services to individual consumers(消费者个人);(b) selling goods or taxable goods that are free from VAT;(c) selling goods or taxable services(应税劳务) by small-scale taxpayers.Article 22(1) The place for the payment of VAT is as follows:(a) Businesses with a fixed establishment(固定业户) shall report and pay tax with the competent tax authorities(主管税务机关)where the establishment is located. If the head office and branch are not situated in the same county (or city), they shall report and pay tax separately with their respective competent tax authorities. The head office may, upon approval of the competent finance and tax authority(财政、税务主管部门) under the State Council or their authorized finance and tax authorities, report and pay tax(申报纳税)on a consolidated basis with the competent tax authorities where the head office is located.(b) A business with a fixed establishment selling goods in a different county (or city) shall apply for the issuance of a tax administration certificate for outbound business activities(外出经营活动税收管理证明) from the competent tax authorities where the establishment is located and shall report and pay tax therewith; where no such certificate is issued, it shall report and pay tax with the competent tax authorities where the goods are sold or services provided; where it fails to do so, the tax shall be levied by the competent tax authorities where the establishment is located as a remedy(补征).(c) A business without a fixed establishment selling goods or taxable services shall report and pay tax with the competent tax authorities where the goods are sold or services provided; if it fails to do so, the tax shall be levied by the competent tax authorities where the establishment is located or resided(所在地或者居住地).(d) The tax for imported goods shall be reported and paid to the customs office where the imports are declared(报关地).(2) A withholding agent shall report and pay the tax it has withheld with the competent tax authorities where its establishment is located or resided.Article 23(1) The VAT assessable period(可征收的期限) shall be one day, three days, five days, ten days, fifteen days, one month or one quarter. The actual assessable period(具体纳税期限)for a taxpayer shall be separately assessed(分别核定) by the competent tax authorities according to the magnitude(大小) of the tax payable of the taxpayer; tax that cannot be assessed in regular periods may be assessed on a transaction-by-transaction basis(按次).(2) Taxpayers that adopt one month or one quarter as an assessable period shall report and pay tax within 15 days following the end of the period(自期满之日起). If an assessable period of one day, three days, five days, ten days or fifteen days is adopted, the tax shall be prepaid(预缴) within fivedays following the end of the period and a monthly return shall be filed with any balance of tax due settled(结清到期应纳税款) within 15 days from the first day of the following month.(3) The period for a withholding agent to pay the tax withheld shall be subject to(依照执行) the provisions of the preceding two paragraphs.Article 24Taxpayers importing goods shall pay tax within 15 days after the issuance of the special VAT payment certificates for import(海关进口增值税专用缴款书) by the customs office.Article 25(1) Taxpayers exporting goods with the applicable 0% tax rate(适用退(免)税规定) shall, upon completion of export procedures with the customs office, apply to the competent tax authorities within the prescribed time limit for the tax refund on those export goods on a monthly basis based on such relevant documents as the export declaration(出口报关单). The detailed measures shall be formulated by the competent finance and tax authority under the State Council.(2) Where return of goods(退货) or withdrawal of the customs declaration(退关)occurs after the completion of the tax refund(退税) on the export goods, the taxpayer shall repay the tax refunded(补缴已退的税款) according to law.Article 26The collection and administration of VAT shall be conducted(执行)in accordance with the Law of the People’s Republic of China on Administration of Tax Collection and the relevant provisions of these Regulations.Article 27 These Regulations shall come into effect from January 1, 2009. 2012-9-1 17:46:39(c) A business without a fixed establishment selling goods or taxable services shall report and pay tax with the competent tax authorities where the goods are sold or services provided; if it fails to do so, the tax shall be levied by the competent tax authorities where the establishment is located or resided(所在地或者居住地).(d) The tax for imported goods shall be reported and paid to the customs office where the imports are declared(报关地).(2) A withholding agent shall report and pay the tax it has withheld with the competent tax authorities where its establishment is located or resided.Article 23(1) The VAT assessable period(可征收的期限) shall be one day, three days, five days, ten days, fifteen days, one month or one quarter. The actual assessable period(具体纳税期限)for a taxpayer shall be separately assessed(分别核定) by the competent tax authorities according to the magnitude(大小) of the tax payable of the taxpayer; tax that cannot be assessed in regular periods may be assessed on a transaction-by-transaction basis(按次).(2) Taxpayers that adopt one month or one quarter as an assessable period shall report and pay tax within 15 days following the end of the period(自期满之日起). If an assessable period of one day, three days, five days, ten days or fifteen days is adopted, the tax shall be prepaid(预缴) within five days following the end of the period and a monthly return shall be filed with any balance of tax due settled(结清到期应纳税款) within 15 days from the first day of the following month.(3) The period for a withholding agent to pay the tax withheld shall be subject to(依照执行) the provisions of the preceding two paragraphs.Article 24Taxpayers importing goods shall pay tax within 15 days after the issuance of the special VAT payment certificates for import(海关进口增值税专用缴款书) by the customs office.Article 25(1) Taxpayers exporting goods with the applicable 0% tax rate(适用退(免)税规定) shall, upon completion of export procedures with the customs office, apply to the competent tax authorities within the prescribed time limit for the tax refund on those export goods on a monthly basis based on such relevant documents as the export declaration(出口报关单). The detailed measures shall be formulated by the competent finance and tax authority under the State Council.(2) Where return of goods(退货) or withdrawal of the customs declaration(退关)occurs after the completion of the tax refund(退税) on the export goods, the taxpayer shall repay the tax refunded(补缴已退的税款) according to law.Article 26The collection and administration of VAT shall be conducted(执行)in accordance with the Law of the People’s Republic of China on Administration of Tax Collection and the relevant provisions of these Regulations.Article 27These Regulations shall come into effect from January 1, 2009. 2012-9-1 17:46:39。

国家外汇管理局

国家外汇管理局国家外汇管理局贸易信贷登记管理系统操作手册(企业端)2008年7月7日稿目录1登录系统 (5)1.1登陆前IE设置51.2登陆系统81.3登陆异常82业务操作 (13)2.1合同登记132.1.1新合同登记142.1.2合同修改152.1.3合同删除172.2提款登记182.2.1新提款登记192.2.2追加提款登记202.2.3修改提款登记202.2.4删除提款登记212.3注销登记222.3.1以往提款登记注销232.3.2修改注销登记252.3.3删除注销登记272.4合同登记查询282.5提款登记查询292.5.1按收汇水单申报号查询292.5.2按日期查询302.6注销登记查询312.6.1按收汇水单申报号查询312.6.2按日期查询322.7企业信息查询331登录系统1.1 登陆前IE设置●该系统推荐使用IE6.0浏览器,该设置决定了是否能正常在客户机器正常显示,并对其简要的设置做如下说明.➢打开IE看到被黑框框起的工具菜单栏➢点击将看到如下下拉菜单.➢单击[Internet 选项(0)…] 将看到如下弹出窗口●设置页面不缓存,以便控制页面的缓存每次都请求新的信息➢单击黑框框起的”设置”按钮, 如下弹出窗口选中“每次访问此页时检查(E)”,点击确定按钮.●设置信任站点[以便于控件下载和自动安装]➢选择安全选项卡➢单击黑框框起的”站点(S)…”按钮, 如下弹出窗口➢在“将该网站添加到区域中(D)”把网站的地址()按照以上的格式添加,把“对该区域中的所有站点要求服务器验证(https:)(S)”的复选框去掉.点击“确定”按钮.1.2 登陆系统使用IE6以上浏览器,打开网页,用户类型选择企业,输入企业代码与密码,登录进入贸易信贷登记管理系统。

进入系统后,如无法显示左边的功能菜单,请按本手册“1.3 登陆异常”说明进行设置。

企业使用企业代码登录,初始密码为:12345678。

为保证数据安全,企业应立即修改密码。

国家税务总局关于印发《中华人民共和国非居民企业所得税申报表》

国家税务总局关于印发《中华人民共和国非居民企业所得税申报表》等报表的通知【法规类别】企业所得税【发文字号】国税函[2008]801号【失效依据】国家税务总局公告2015年第30号――关于发布《中华人民共和国非居民企业所得税年度纳税申报表》等报表的公告【发布部门】国家税务总局【发布日期】2008.09.22【实施日期】2008.09.22【时效性】失效【效力级别】部门规范性文件国家税务总局关于印发《中华人民共和国非居民企业所得税申报表》等报表的通知(国税函〔2008〕801号)各省、自治区、直辖市和计划单列市国家税务局、地方税务局:为贯彻落实《中华人民共和国企业所得税法》及其实施条例,规范和加强非居民企业所得税管理,国家税务总局制定了非居民企业所得税申报表、扣缴企业所得税报告表及填报说明,现印发给你们,并就有关问题通知如下:一、非居民企业所得税申报表按申报时间分为年报和季报两种,按征收方式分为据实征收和核定征收两类。

2008年度申报时启用年报,2009年季度申报时启用季报。

二、扣缴企业所得税报告表是对《中华人民共和国企业所得税扣缴报告表》(国税函〔2008〕44号印发)修订后的表样,自2009年1月1日起使用。

三、上述报表使用A4型纸,由各地按照税务总局的要求自行印制。

四、各地应加强对上述报表印发使用的管理,做好报表的宣传、培训工作,确保非居民企业准确填报报表。

执行中若存在问题,请及时反馈国家税务总局(国际税务司)。

附件:1.非居民企业所得税年度纳税申报表(适用于据实申报企业)2.非居民企业所得税季度纳税申报表(适用于据实申报企业)3.非居民企业所得税年度纳税申报表(适用于核定征收企业)4.非居民企业所得税季度纳税申报表(适用于核定征收企业)5.扣缴企业所得税报告表国家税务总局二○○八年九月二十二日附件1:中华人民共和国非居民企业所得税年度纳税申报表(适用于据实申报企业)税款所属期间:年月日至年月日纳税人识别号:□□□□□□□□□□□□□□□中华人民共和国企业所得税法国家税务总局监制填报说明一、本表及附表适用于能够提供完整、准确的成本、费用凭证,如实计算应纳税所得额的非居民企业所得税纳税人。

广东省地方税务局转发国家税务总局国际税务司关于下载外资企业所得税申报及汇算清缴系统2008版本的通知

广东省地方税务局转发国家税务总局国际税务司关于下载外资企业所得税申报及汇算清缴系统2008版本的

通知

文章属性

•【制定机关】广东省地方税务局

•【公布日期】2008.03.28

•【字号】粤地税办函[2008]18号

•【施行日期】2008.03.28

•【效力等级】地方规范性文件

•【时效性】现行有效

•【主题分类】企业所得税

正文

广东省地方税务局转发国家税务总局国际税务司关于下载外资企业所得税申报及汇算清缴系统2008版本的通知

(粤地税办函〔2008〕18号)

广州、珠海、佛山、东莞市地方税务局:

现将《国家税务总局国际税务司关于下载外资企业所得税申报及汇算清缴系统2008版本的通知》(际便函[2008]34号)转发给你们,请尽快通知相关的外资企业做好2008版本外资企业所得税申报软件的升级工作,同时,各级税务部门也要做好2008版本外资企业所得税汇算清缴软件的升级和运用工作,以确保2007年度外资企业所得税汇算清缴工作顺利进行。

二OO八年三月二十八日国家税务总局国际税务司关于下载外资企业所得税申报及汇算清缴系统2008版本的通知(略)。

海关总署公告2008年第51号--关于实施2008年版《中华人民共和国海关进出口商品规范申报目录》

海关总署公告2008年第51号--关于实施2008年版《中华人民共和国海关进出口商品规范申报目录》

文章属性

•【制定机关】中华人民共和国海关总署

•【公布日期】2008.07.24

•【文号】海关总署公告2008年第51号

•【施行日期】2008.07.24

•【效力等级】部门规范性文件

•【时效性】已被修改

•【主题分类】海关综合规定

正文

*注:本篇法规已被《海关总署公告2008年第92号--关于出版2009年版<规范申报目录>、<统计商品目录>的公告》(发布日期:2008年12月22日实施日期:2009年1月1日)修订

海关总署公告

(2008年第51号)

为规范进出口企业申报行为,提高申报数据质量,促进贸易便利化,海关总署于2006年制定了《中华人民共和国海关进出口商品规范申报目录》(以下简称《目录》),并于2007年对《目录》进行了修订。

上述目录分别以海关总署公告2006年第16号和2007年第50号对外公布。

根据当前海关监管的需要,海关总署制定了2008年版《目录》,该《目录》自2008年8月1日起施行。

《目录》由中国海关出版社出版。

进出口货物收发货人及其代理人在报关时应当严格按照2008年版《目录》中关于规范申报商品品名、规格的要求,认真填制报关单并依法办理通关手续。

特此公告。

海关总署二00八年七月二十四日。

北京市国家税务局转发国家税务总局关于下发2008年出口退税率文库的通知的通知

北京市国家税务局转发国家税务总局关于下发2008年出口退税率文库的通知的通知

文章属性

•【制定机关】北京市国家税务局

•【公布日期】2008.02.20

•【字号】京国税函[2008]111号

•【施行日期】2008.02.20

•【效力等级】地方规范性文件

•【时效性】失效

•【主题分类】

正文

北京市国家税务局转发国家税务总局关于下发2008年出口退

税率文库的通知的通知

(京国税函[2008]111号)

各区、县(地区)国家税务局,直属税务分局:

现将《国家税务总局关于下发2008年出口退税率文库的通知》(国税函[2008]154号)转发给你们,请结合以下要求一并执行:

一、我市2008年度审核系统中的商品代码库(版本号20080201A)已由市局于2008年2月15日统一调整完毕并使用。

二、请各局将出口退税率文库下载方法通知所辖的退税企业。

可登录中国出口退税咨询网(http://)下载。

对于上网下载有困难的企业,各局应采取拷贝软盘等方法下发企业。

三、各局在使用出口退税率文库时,若有修订建议,则应以文字形式向市局说明情况,以便市局及时上报总局。

2008年2月20日

国家税务总局关于下发2008年出口退税率文库的通知(略)。

美国个人所得税申报方式借鉴及其选择

美国个人所得税申报方式借鉴及其选择1、相关定义1.1、税收的概念税收是国家为了实现其职能,凭借政治权力,按照法律规定的标准,无偿地、强制地征收实物或货币,以取得财政收入和调节经济的一种手段。

对于税收的这一概念,可以从以下几个方面来理解:首先,税收是国家为了实现其职能,取得财政收入的一种手段、一种工具;其次,国家征税是凭借其政治权力强制进行的;再次,国家征税是按法律规定的标准无偿征收的;最后,税收属于分配范畴,体现着特定的分配关系。

[26]1.2、变量选择与定义根据本文的研究目的,将本文的解释变量定义为股权再融资方式,本文研究的是增发和配股的方式,依据国内外相关的股权再融资理论提出了六个假设,进一步选择了相应的解释变量,分别是股权集中度、流通股比例、成长性、资产负债率、净资产收益率18 和市盈率。

本文中将公司规模作为控制变量,众所周知,公司规模的大小对于股权再融资方式的选择起着重要的作用,公司规模大,为了保护股东的利益,管理者通常会选择配股的方式,这样可以防止外部人员瓜分公司收益;规模小的公司,为了扩大经营,管理者通常会选择增发的方式,这样可以为该公司注入活力,获得大量资金支持,争取更好的投资机会,有利于公司进一步发展。

公司规模是影响因素,更是为大家所熟知的, 所以本文将其作为控制变量,重点研究的是除公司规模以外的其他可能的影响因素。

表 4.1 主要变量定义表变量种类变量全称变量符号变量释义被解释变量股权再融资方式Y Y=1,选择增发;Y=0,选择配股解释变量股权集中度PER公告增发(配股)上一年末前五大股东持股比例流通股比例LT-ratio公告增发(配股)上一年末流通股比例成长性GRO(公告上一年末资产总额-上一年年初资产总额)/上一年年初资产总额资产负债率LEV公告增发(配股)上一年末负债总额/ 资产总额净资产收益率ROE公告增发(配股)上一年末净利润/资产平均余额市盈率P/E公告增发(配股)上一年末每股市价/ 每股收益控制变量公司规模ASSETS 公告增发(配股)上一年末总资产对数通过前文分析,我们可以得出六个解释变量: (1)根据前文假设1,将前五大股东持股比例作为股权集中度的衡量标准,在本文中选择的是公告增发(配股)上一年年末前五大股东持股比例之和作为解释变量1。

免版税证明书

表格w-9(最后更新时间为2011年1月)美国财政部国家税务局申报人姓名(请按照在申报人所提交的个人所得税申报表上所示的姓名填写)美国纳税人个人身份识别标号及证明文件请将这一表格直接交到要求你填写这一表格的个人和机构。

请不要直接将该表格发送至美国国税局。

3e^uo suouon-sul oeoeds??10纳税人身份识别号 (tin) 社会保障编号请在适当的方框中的指定位置填写你的纳税人身份认证号。

请注意,你所提供的纳税人身份认证号必须要与你在“姓名”一栏中所填写的名字相匹配以避免多次重复或者错误扣缴税款。

从个人的角度来说,这一纳税人身份认证号也就是你的社会保险号码(ssn)。

然而,对于那些非美国居民的外籍人士、独资经营者或者豁免实体而言,有关这些人士的纳税人身份认证号方面的具体规定请参见本文件第三页使用说明第一部分中的详细说明。

对于不属于以上几类的其他实体,这一纳税人身份认证号为该实体的雇主识别号(ein)。

如果你现在还没有一个身份认证编号,请参见本文档第三页说明中有关如何获得纳税人身份认证号的相关规定和介绍进行操作。

请注意,如果上述所填写的帐户是由超过一名以上的多名不同人士联合开立,请参见本文件第四页中的表格来查看应该在此处填写谁的身份认证号比较合适的相关规定和指南。

声明保证根据美国伪证罪的各项处罚条例规定,本人特在此作出以下承诺与声明:1、本人在这张表格上所填写的纳税人识别号码是本人目前所使用的真实正确的纳税人身份认证号(或者本人目前还处于正在等待相关部门向本人颁发一个纳税人身份认证号的阶段);并且2、本人不需要遵守有关备用预扣税款方面的规定,因为:(a)本人有权申请备用预扣税款免除政策;或者(b)本人没有接到任何由美国国税局(irs)在这方面向本人发出的通知,告诉本人由于本人未能按照要求及时将本人所获得的所有利息或股息向相关部门予以上报,因而本人需要遵守有关备用预扣税款方面的规定;或者(c)本人已经接到由美国国税局(irs)向本人发出的通知,告诉本人不再需要遵守有关备用预扣税款方面的规定;以及 3、本人是一个美国公民或其他类型的美国人(相关方面的定义请参见下文中的具体介绍)。

个税代扣代缴系统操作手册

个税代扣代缴系统操作手册概述个人所得税代扣代缴系统既为扣缴义务人提供了方便快捷的报税工具,也为税务机关提供了全面准确的基础数据资料.本系统主要包括:基础信息录入、填写报表、生成申报数据、申报及反馈、查询统计等功能。

业务流程图如下:目录1系统安装 (1)1.1运行环境 (1)1。

2系统安装 (4)2系统初始化 (5)2。

1系统登录 (5)2。

2初始化 (6)2.3首页 (9)3基础信息 (10)3。

1扣缴义务人信息 (10)3。

2纳税人信息 (11)4填写报表 (12)4。

1基本操作介绍 (13)4。

2正常工资薪金收入 (15)4。

3外籍人员正常工资薪金收入 (17)4。

4全年一次性奖金收入 (19)4.5无住所个人取得数月奖金收入 (20)4。

6特殊行业全年工资薪金收入 (21)4。

7内退一次性补偿收入 (22)4.8提前退休一次性补贴收入 (23)4。

9解除劳动合同一次性补偿收入 (23)4。

10股票期权行权收入 (25)4。

11企业年金(企业缴纳部分) (26)4。

12非工资薪金收入 (27)4.13限售股转让收入 (28)4.14财政统发当月已缴税额 (29)4。

15生成申报数据 (30)5申报及反馈 (31)6打印代扣代收税款凭证 (33)7查询统计 (34)7。

1查询申报明细 (34)7.2查询申报表 (35)8修正和自查 (36)8.1启动修正 (36)8。

2启动自查 (37)8。

3撤消 (37)8。

4自查数据导入 (38)9补录数据 (39)9.1填写明细表 (39)9.2生成数据 (41)9。

3发送数据 (42)9。

4获取审核结果 (43)9。

5转入代扣代缴 (43)9。

6撤消补录 (43)10参数设置 (45)10。

1税务局信息获取 (46)11系统管理 (47)11。

1修改密码 (47)11.2操作员管理 (48)11。

3网络参数设置 (49)11.4运行参数设置 (51)11。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

The new stock exchange for LondonLiquidity,choice, momentumThe T ax Benefit GuideInvesting in the PLUS-quoted marketStandon House21Mansell Street London E1 8AAt. +44 (0) 20 7553 2000 f. +44 (0) 20 7553 2004PLUS Markets is a fully competitive stock market for small and mid cap companies. It operates twomarkets for companies: a PLUS-listed market for companies seeking a full listing on the Official List anda PLUS-quoted market for companies which for tax purposes are considered “unquoted”, i.e. not fully listed.This guide principally addresses the tax benefits that apply to PLUS-quoted companies. As PLUS-listed isa“Recognised Investment Exchange”, companies on that market are considered “quoted”, and so donot attract all of these tax benefits. Section 5 deals briefly with the tax benefits that can applyto PLUS-listed companies.This guide is designed to set out the various tax reliefs available both to direct investors in PLUS-quotedcompanies and to investors in Venture Capital Trusts. The guide also covers the principal conditions thatthe investors and the companies themselves are required to meet in order to take advantage of them.While we would never seek for investment in the PLUS-quoted market to be tax-driven, it is important tous at PLUS Markets Group that we make individual and corporate investors aware of the tax breaksavailable to them. When planning investment decisions, investors need to do so in the presence of fullinformation in this key area.Our thanks go to BDO Stoy Hayward for their kind assistance in producing this guide. If you have anyfurther tax-specific questions or queries relating to PLUS-quoted or PLUS-listed securities, BDO StoyHayward would be delighted to offer their expert guidance.For general information about PLUS Markets Group, please contact the Capital Markets team on +44 (0) 207 553 2010.A guide to PLUS tax benefits 2008/0901 Section 1Individual Investors(a)The Enterprise Investment Scheme (EIS)(b)Inheritance Tax (Business Property Relief)(c)Venture Capital Trusts (VCTs)(d)Capital Gains Tax (Entrepreneurs’ Relief and Gift Relief)Section 2Corporate Investors(a)Corporate Venturing Scheme (CVS)(b)Substantial Shareholdings Exemption (SSE)Section 3Criteria for qualifying companies under the EIS, CVS and VCT schemes Section 4Other considerations Section 5PLUS-listed CompaniesIMPORTANT NOTE:The information in this guide is intended as a condensed summary of the main conditions that must be met by PLUS-quoted companies and investors wishing to benefit from the tax reliefs outlined. The guide should not be used as a substitute for professional advice and investors and PLUS-quoted companies should take specific professional advice on tax planning.The principal tax reliefs available to PLUS-quoted companies are as follows:0203(a) Enterprise Investment Scheme (EIS) ReliefThe EIS gives a tax incentive to qualifying investors (as defined on page 11) who subscribe for shares in certain small unquoted companies, including shares traded on the PLUS-quoted market. The EIS Relief has four main elements.•Income Tax ReliefThis allows an investor to reduce the amount of his, or her, liability to income tax in the year of investment.Relief is obtained at the lower rate of income tax, currently 20%, on the amount subscribed for the shares of qualifying companies. Investors should be able to deduct an amount equal to 20% of their investment from their liability to income tax in the current tax year.Relief cannot be claimed on more than £500,000subscribed by an individual (in any number of qualifying companies).An individual who subscribes for shares after 5 April and before 6 October in a tax year may claim to carry back part of the subscription to the previous tax year. The amount of the subscription that can be carried back is limited to the lower of:(a)£50,000,(b)Half of the amount subscribed, and(c)The unused balance of his/her relief available for the previous year(The maximum amount relievable in 2007/08 was £400,000).T o retain this relief the shares must be held by the investor for a period that ends three years after the shareissue date, or three years after the trade starts, whichever is later . This is referred to below as the three year period.Example£Gross subscription for shares 10,000Less tax relief at 20% (2,000)Net cost of investment8,000Section 1 -Tax benefits for individual investorsPage 03Page 09Page 11Page 14Page 16•Capital Gains Tax ExemptionThis exempts investors from the liability to capital gains tax when they realise a gain on a disposal of their shares in qualifying companies after the three-year period, provided the EIS income tax relief was given on the shares and has not been withdrawn.Example£Realised value of shares after three-year period 20,000Original gross subscription for shares (10,000)Tax free gain10,000•Loss ReliefIn the event of an investor suffering a loss arising from the disposal of the EIS shares at any time, this relief allows the offset of that loss against either capital gains or, by election, taxable income in the year of the loss.Example£Realised value of shares Nil Original cost of investment (10,000)EIS income tax relief 2,000Loss(8,000)EIS loss relief (assuming a 40% taxpayer) 3,200Net loss(4,800)•Capital Gains Tax DeferralIndividuals and certain trustees can defer all or part of their Capital Gains T ax (CGT) liabilities by subscribing for eligible shares in an EIS company. There is no monetary limit on the amount of the EIS subscription and thus the gain that can be deferred in this way .The gains that can be deferred are those that have arisen in the three years before the EIS shares are issued or those that arise up to one year after that date. Such gains may be the result of the disposal of an asset or , a gain previously deferred by the individual, and may have become chargeable to tax.Investors should note that this relief is a deferral only and that the original capital gain will crystallise on the disposal of the EIS shares at any time, resulting in CGT being payable in the normal way . The investor would,however , be able to claim further CGT deferral to the extent that a qualifying reinvestment is made within the time allowed. A transfer of shares on the owner’s death does not cause the deferred gain to crystallise.0405With effect from 6 April 2008, CGT will be charged at a flat rate of 18% (subject to Entrepreneurs’Relief). It is possible to use EIS deferral relief to defer a pre 6 April 2008 gain which would be taxable at 40%, so that when it recrystallises it is taxed at the new CGT rate of 18%. The opposite is also true –gains which are taxable at 10% under pre 6 April 2008 Business Asset Taper Relief rules, if deferred using EIS investments could be taxed at a higher rate when they recrystallise.Example (assumes a higher rate taxpayer with a chargeable gain of £10,000)£Gross investment in shares 10,000Less CGT deferral at 40 per cent (4,000)Less tax relief at 20 per cent(2,000)Cost of investment (prior to capital gain crystallising) 4,000EIS qualifying investorsIndividual investors must meet certain conditions to be a qualifying investor. Qualifying investors must continue to qualify for the three-year period. The conditions, which are less stringent for deferral relief than for income tax relief and tax free capital gains, can be summarised as follows:1.For income tax relief and tax-free capital gains the individual:•Must have a liability to pay UK income tax (the individual need not be UK resident).•Must not be “connected” with the company by being:-an employee-a paid director prior to the share issue-a shareholder who, together with associates, controls the company or is entitled to more than 30% of:i.the company’s issued ordinary share capital;ii.the aggregate of its loan capital and issued share capital;iii.its voting power; or iv.its assets in a winding up.•Must not be a new director unless the complex so-called Business Angel provisions have been met.Finally, there is an upper limit for qualifying investments of £500,000 per person per annum from 6 April 2008.2.For deferral relief the individual:-must be UK resident and ordinarily resident (and not dual resident) at both the date of the disposal, giving rise to the gain and the date of the investment. This status must continue for three years from the date the shares are issued.-must reinvest the chargeable gain (before taper relief) in the period one year before and up to three years after it arises.-may be “connected” with the company as defined above.The individual can invest any amount (restricted of course by the gross asset limit for the company itself,which must not exceed £8m immediately after the share issue, and the company’s annual investment limit of £2m in any 12 month period from a combination of EIS, CVS and VCTs investing money raised after 5 April 2007). The level of investment required to defer the gain is the amount of the gain.Receipt of valueAn EIS investor must not receive “value” from the company (or any of its subsidiaries) at any time during the period one-year before to three years after his shares are issued. The rules in this area are complex but the investor is deemed to receive “value” if, inter-alia:-the company buys back its own shares;-the company makes a loan to the investor;-the investor receives an abnormal amount by way of dividend, or excessive remuneration or expenses.(b) Inheritance Tax (IHT)Subject to certain conditions, investments in PLUS-quoted companies will attract 100% relief from inheritance tax (business property relief) provided the shares have been held for at least two years. Most trades qualify but the company’s business must not be wholly or mainly that of:-dealing in securities, stocks and shares;-dealing in land or building; and-making or holding investments within an investment business.0607(c) Venture Capital Trusts (VCTs)VCTs are fully listed companies that attract individual investors who are able to claim tax reliefs on their investment. The VCTs then invest in a spread of unquoted trading companies (which for these purposes includes PLUS-quoted companies). In order to be approved by HM Revenue & Customs (HMRC) the VCTs investments must, after three years, be at least 70% in qualifying unquoted trading companies.Each VCT may only invest up to £1m per tax year in any one company and no holding may represent more than 15% of the VCT s total investments. These rules are designed to ensure a spread of investments.A VCT company’s investment may be in the form of a cash subscription for shares and/or loan stock with a minimum term of five years. At least 30% of the VCTs total qualifying investments and 10% of each individual investment must be in new ordinary shares.The following VCT reliefs are available to individuals who are over 18 years of age, in respect of subscriptions of up to £200,000 per tax year.-Income tax reliefFor shares issued after 6 April 2006 an amount equal to 30% of the amount subscribed is deducted from the investor's income tax liability. The relief islimited to the income tax liability of an investor and is given before all other deductions. It is only available if new shares are subscribed for and held for five years (previously three years). There is no legal minimum but each VCT decides on its minimum subscription.-Tax-free gainsAny gain on a disposal of VCT shares is tax-free at any time. There is no tax relief of any kind if a loss arises on VCT shares.-Tax-free dividends Dividends paid by a VCT to individuals are tax-free.These last two reliefs are available to individuals who subscribe for or purchase shares, provided they have not exceeded their VCT annual limit of £200,000.VCT capital gains tax deferral relief has been withdrawn for shares issued on or after 6 April 2004.(d) Capital Gains Tax (CGT)Entrepreneurs’ ReliefEntrepreneurs’ Relief (ER) was introduced with effect from 6 April 2008, as a replacement for Business Asset Taper Relief, which was abolished on 5 April 2008.ER provides for the first £1m of gains on disposals of qualifying assets to be taxed at an effective rate of 10%, rather than the standard rate of Capital Gains Tax (CGT) of 18% effective from 6 April 2008.Shares in companies on the PLUS-quoted market should qualify for ER, provided, inter alia, the following conditions are met:(a)The company is a trading company or the holding company of a trading group.(b)The individual disposing of the shares has held the shares for at least one year prior to the disposal.(c)The individual disposing of the shares is an employee, officer, or director of the company.(d)Immediately before the disposal, the individual disposing of the shares held at least 5% of the company’s ordinary share capital and that holding entitles him or her to at least 5% of the voting rights of the company.Capital Gains Tax Gift ReliefIt is possible for shares in an unquoted trading company held by an individual or trust to be transferred to another individual at a price other than arm’s length (e.g. a gift). In such circumstances the capital gain based on the market value of the asset can be “held over” until the recipient sells the shares.Both the donor and the recipient must claim gift relief within certain time limits, and the recipient has a capital gains tax base cost equal to the donor’s base cost. The recipient must be resident or ordinarily resident in the UK.It should be noted that the gift has the effect of restarting the period of ownership for entrepreneurs’relief purposes (except for transfers between spouses).0809Other than VCT s, it is less common for companies to provide funding but corporate investors may benefit from:(a)The Corporate Venturing Scheme (CVS).(b)The Substantial Shareholding Exemption (SSE).(a) Corporate Venturing Scheme (CVS)The scheme is similar to the EIS but for corporate investors which are trading companies or part of a trading group. The scheme is intended to encourage companies to invest in small high risk trading companies and in return the corporate investors may benefit from the following reliefs:-Investment reliefA company that makes a qualifying investment of new ordinary shares in a qualifying unquoted trading company (which can include those quoted on the PLUS market) may claim a reduction in its corporation tax liability.The amount of relief available to the investing company is up to 20% of the amount subscribed.-CVS loss reliefAn investing company may claim to set an allowable loss on a disposal of shares that qualified for investment relief against its income, provided certain conditions are met.-CVS deferral relief An investing company that realises a chargeable gain on a disposal of sharesthat qualified for investment relief which has not been withdrawn, may defer some or all of that charge if it makes a qualifying investment.Section 2-Tax benefits for corporate investorsTo retain the reliefs the investment must be held for at least three years. There is no limit on the amount that can be invested (subject to the gross asset limit for the investee company) and the investing company must not control the issuing company or hold, or be entitled to acquire, more than 30% of the:-ordinary share capital, or -the voting rights, or-the combined share capital and loan capital of the issuing company.Following the introduction of the substantial shareholding exemption described below the CVS deferral relief is now less important but the CVS loss relief on the other hand has increased in importance.(b) Substantial Shareholding Exemption (SSE)Subject to certain conditions, companies disposing of a substantial (broadly at least 10%) shareholding in qualifying trading companies after 1 April 2002 will be exempt from chargeable gains. The quid pro quo is that companies will similarly not be able to claim capital losses on their substantial shareholdings.Unlike other tax reliefs mentioned above the SSE is available to companies officially listed on the PLUS-listed market, as well as PLUS-quoted companies.1011There are a number of criteria that must be met for a PLUS-quoted company’s investors to qualify under the EIS, CVS and VCT schemes. For qualifying companies:(i)The shares on which EIS and CVS relief can be claimed must be eligible shares, which are:-new ordinary shares,-with no present or future preferential right to income or to assets on a winding up, and -with no present or future right to be redeemed.The shares must be subscribed for wholly in cash and be fully paid up at the time of subscription.A VCT ’s investment can be in:-new ordinary shares, and/or-preference shares or loans with a minimum term of five years.If a company is to remain as a qualifying holding it must do so throughout the period the investment is held by a VCT .(ii)The issuing company can be a single trading company or the parent of a trading group (the Group).(iii)For shares issued after 5 April 2006, the gross assets of the issuing company or the Group must not exceed:-£7m immediately before; and-£8m immediately after, the share issue.There are transitional provisions which allow the previous gross asset limits of £15m and £16m to apply to VCT investments where the funds were raised by the VCT prior to 6 April 2006.(iv)The issuing company must not have arrangements in place at the time of the share issue, to reduce the investors’ risk or pre-arrange the investors’ exit.Section 3-Criteria for qualifying companies underthe EIS, CVS and VCT schemes(v) For EIS and CVS purposes, when the shares are issued, the issuing company must be unquoted andthere must be no arrangements in place for it to become quoted. In the case of VCT investee companies that later become quoted they are deemed to be unquoted for these purposes for a further 5 years. Shares that are quoted on the PLUS-quoted market are unquoted for this purpose.(vi)The issuing company (or one of its subsidiaries) at the time of the share issue must exist to carry on aqualifying trade and must either be:-carrying on a qualifying trade;-preparing to carry on a qualifying trade (which it must start within two years); or -carrying out research and development from which a qualifying trade will be carried on.(vii)During the issuing company’s qualifying period it must not be under the control of another companyand cannot itself control another company except for its qualifying subsidiaries.To be a qualifying subsidiary, the following conditions must be satisfied:-the issuing company must directly or indirectly own more than 50% of the ordinary share capital of the subsidiary;-no person other than the issuing company or another of its subsidiaries should control the subsidiary; and -no arrangements should exist whereby either of the above conditions would cease to be satisfied.In the case of the CVS, at least 20% of the ordinary share capital of the issuing company must be owned by individuals who are not directors or employees (or their relatives) of the investing company or a company connected with that company.(viii)In each case, the activity must be carried on commercially , and wholly or mainly (more than 50%) in the UK, ifit is to be a qualifying activity . A qualifying subsidiary can trade outside the UK. However , the company using the funds, which may be the issuing company or its directly held 90 per cent subsidiary , must trade mainly in the UK.(ix)The company must employ at least 80 per cent of the money raised for qualifying trading purposeswithin 12 months of:-the date the shares were issued; or-the company starting its qualifying trade, if this is later.1213The remainder must be employed within 24 months of these dates.(x)The company must carry on a qualifying trade.There is no definition of a qualifying trade, but non-qualifying trading activities must not be carried on toany substantial extent (more than 20%). These activities are:-dealing in land, in commodities or futures, or in shares, securities or other financial instruments;-dealing in goods otherwise than in the course of an ordinary trade of wholesale or retail distribution;-banking, insurance, money-lending, debt-factoring, hire-purchase financing or other financial activities;-leasing (including letting ships on charter or other assets on hire), or receiving royalties or licence fees (Exceptions are made for intangible assets created by the issuing company or its subsidiaries);-providing legal or accountancy services;-farming and market gardening, woodlands and timber production;-property development;-operating and managing hotels and nursing homes;-coal production;-steel production;-shipbuilding; and-providing services to a connected person with one of the above trades.(xi)The company must have no more than 50 full time equivalent employees at the time of the share issue(xii)A company can raise no more than £2m in any 12 month period from a combination of the CVS, EISand VCTs investing funds raised post 5 April 2007.SIPPsPLUS-quoted shares are now eligible for inclusion in SIPPs (Self Invested Personal Pension). HMRC has undertaken a complete overhaul of the complex tax rules that apply to retirement provision. A single new tax structure was introduced from 6 April 2006 (A-Day) which allows registered pension schemes,including SIPPs, to invest in new asset classes. Unquoted shares, which include PLUS-quoted shares, are treated as a new asset class available for direct SIPP investment.In the 2008/09 tax year individuals will be able to benefit from tax relief on pension contributions up to 100% of their taxable earnings (subject to a cap of £235,000) and SIPPs will be able to invest these contributions directly in PLUS-quoted companies.Making claimsProvisional approval for EIS and VCT qualifying statusIt is possible to obtain provisional approval from HMRC that shares issued will be eligible shares for EIS purposes and will be a qualifying holding for a VCT and that the issuing company and its trade will be qualifying.Provisional approval is based on the information provided to HMRC and the approval only relates to the company and its trade (i.e. not individual investors). For this reason HMRC’s Small Company Enterprise Centre should be provided with full disclosure. Once provisional approval has been obtained this can be mentioned in the prospectus or other document provided to potential investors.Provisional approval is provided on a non-statutory basis and there is no specified period within which HMRC has to respond, although a response would typically be received within 30 days.CVS advance clearance noticePotential issuing companies can apply to HMRC for an advance clearance. HMRC’s clearance letter will confirm whether, based on the information provided, they are satisfied that the issuing company qualifiesSection 4-Other considerations1415and that the requirements are to be met in respect of both the shares and the money raised.This advance application process is similar to that described above in respect of the EIS and VCTs, but this advance clearance is dealt with under specific legislation rather than on a non-statutory basis. HMRC has a time limit of 30 days in which to either issue the advance clearance notice or request additional information.Procedure for obtaining EIS tax certificatesFollowing the issue of the EIS shares, or four months after the commencement of the company ’s trade (whichever is later), the company sends to the Inspector a completed and signed Form EIS attached to which are the details of the shareholders who wish to claim EIS relief. A separate Form EIS 1 is required for each EIS share issue. Various declarations are made by the Company Secretary or Director who completes and signs the Form EIS 1. Once the Inspector is satisfied that tax relief certificates should be issued, he will send to the Company a Form EIS 2 (authorisation) and EIS 3 Certificates to be completed by the company and the investors, as appropriate.Moving between UK public marketsMost of the reliefs outlined in the guide are only available for investments in unquoted companies.HMRC considers that shares quoted on the PLUS market are unquoted. Moving on to the Official List would have the following consequences:Enterprise Investment Scheme and Corporate Venturing SchemeThe legislation allows the shares of an unquoted company to be subsequently listed on a recognised stock exchange without resulting in any loss of tax reliefs, provided arrangements were not in existence at the time the shares were issued.Inheritance TaxIt is necessary to consider the status of the shares at the time of the transfer. If the shares have become listed on a recognised stock exchange then business property relief at 50 per cent would only be available in the unlikely event that the shares give control of the quoted company.Venture Capital TrustsAt the time of the VCT share issue the issuing company must be unquoted. If the issuing company later becomes quoted it is deemed to be unquoted for the purposes of the VCT rules for another five years.Overseas aspectsFor the purposes of the EIS, VCT and CVS legislation, the place of incorporation and the residence of the qualifying company (or in the case of the VCT scheme and the CVS, the company issuing the shares to the VCT or CVS company) have in themselves no relevance. However, a qualifying company must use the funds raised for a trade that company, or its 90% held qualifying subsidiary, carries on (or intends to carry on) “wholly or mainly in the UK”. For example, a foreign company could raise funds that are employed by its UK subsidiary provided the subsidiary’s trade is carried on mainly in the UK and the group as a whole is trading mainly in the UK.In determining whether a company is trading “wholly or mainly in the UK”, the total activities of the company must be taken into account. This would include, for example, where the employees carry out their duties, where the assets are held and where any purchasing, processing, manufacturing and selling is carried out. A company can carry out some activities outside the UK provided the activities take place “mainly”, that is more than 50%, in the UK. The test is an activities based test and therefore tax reliefs under the venture capital schemes are not denied for companies simply because they may import or export goods.16The PLUS-listed market is a Recognised Stock Exchange, so shares on the PLUS-listed market are“Quoted” for tax purposes and are eligible for investment by ISAs as well as SIPPs.They do not qualify for the EIS, CVS or for investment by VCTs.However,Entrepreneurs’ Relief is available, subject to the investor meeting the rules described at Section1(d), and Substantial Shareholding Exemption (Section 2(b)) can apply to PLUS- listed shares.Business Property Relief from Inheritance Tax (Section 1(b)) at a reduced rate of 50% may be available ona controlling interest in a PLUS-listed trading company, subject to other qualifying conditions.Section 5-PLUS-listed CompaniesBDO Stoy Hayward specialises in helping businesses, whether start-upsor multinationals, to grow. Through our own professional expertiseand by working directly with organisations and the entrepreneursbehind them we've developed a robust understanding of the factorsthat govern business growth. Our objective is to use this to help ourclients maximise their potential.BDO Stoy Hayward prides itself on developing an in-depthunderstanding of the issues affecting business growth. We havedeveloped an understanding of a number of business sectors, allowingus to add value to the services we offer and provide solutions basedon a strong sector insight. We regard the PLUS market, both from thestandpoint of the companies themselves and their shareholders, as animportant part of our market place. We consider that we have theright business assurance, tax and corporate finance skills to assistcompanies on the PLUS market and looking to move to a full listing.David BrookesTax PartnerBDO Stoy Hayward LLPKings Wharf20-30 Kings RoadReadingBerkshireRG1 3EXDirect Telephone: +44 (0)118 925 4445Email: David.Brookes@。