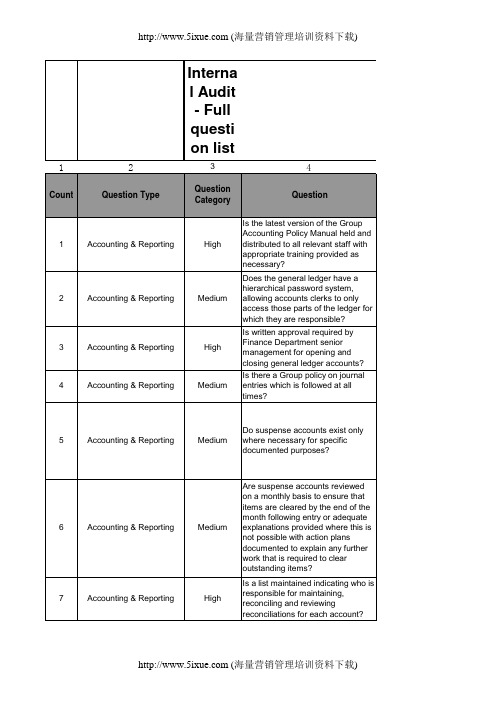

Time table for SH audit details

协助项目经理编写内部审计计划英语

协助项目经理编写内部审计计划英语Assisting Project Manager in Developing Internal Audit PlanIntroductionInternal audit plays a crucial role in ensuring the effectiveness and efficiency of an organization's operations. It helps in identifying risks, evaluating controls, and recommending improvements. As an assistant to the project manager, it is essential to collaborate with the internal audit team in developing an internal audit plan that aligns with the organization's objectives and goals.Importance of Internal Audit PlanAn internal audit plan is a strategic tool that outlines the scope, objectives, and methodology of the internal audit function. It helps in prioritizing audit activities, allocating resources, and ensuring that audit objectives are achieved. By assisting the project manager in developing an internal audit plan, you can contribute to enhancing the organization's risk management process, governance practices, and overall performance.Key Steps in Developing Internal Audit Plan1. Understand Business Objectives: The first step in developing an internal audit plan is to understand the organization's business objectives, strategies, and key risks. This will help in identifying areas that require internal audit focus and attention.2. Assess Risks: Conduct a risk assessment to identify and prioritize risks that could impact the achievement of business objectives. Evaluate the likelihood and impact of each risk to determine the audit focus areas.3. Define Audit Objectives: Based on the risk assessment, define audit objectives that are specific, measurable, achievable, relevant, and time-bound (SMART). These objectives should align with the organization's strategic goals.4. Develop Audit Program: Develop an audit program that outlines the audit approach, procedures, and activities to achieve the audit objectives. Include details such as audit scope, timing, resources, and responsibilities.5. Establish Audit Schedule: Prepare an audit schedule that specifies the timing and sequence of audit activities. Consider factors such as organizational priorities, resource availability, and audit deadlines.6. Obtain Management Buy-in: Present the draft internal audit plan to senior management for review and approval. Seek feedback, suggestions, and recommendations to improve the plan before finalizing it.7. Monitor and Update: Monitor the implementation of the internal audit plan regularly and update it as needed based on changes in business conditions, risks, or objectives.ConclusionAssisting the project manager in developing an internal audit plan is a collaborative effort that requires effective communication, teamwork, and coordination. By following the key steps outlined above, you can contribute to strengthening the organization's internal audit function and enhancing its overall governance and risk management practices. Remember that continuous improvement is essential in the internal audit process, and your active involvement in developing the internal audit plan is a valuable contribution to the organization's success.。

普华永道--财务管理最佳实践

Fixed Assets - Best Practice Objectives

Fixed Assets Objectives

To maintain a complete register of all the organisation’s fixed assets which reflects location, age, current values, associated cost centres To calculate depreciation consistently with financial reporting requirements To optimise replacement policies To minimise ownership costs

Organisation

Asset recording integrated with maintenance and non financial data Centralised asset accounting Asset ownership devolved to business unit level

People

Control focused Challenge asset requisition proposals

Processes

Maintain asset register Acquisitions and disposals Depreciation charge Verifying asset base Maintaining of valuation basis

audit professional clearance template -回复

audit professional clearance template -回复Auditing professional clearance is an integral part of the audit process, ensuring that the auditor receives necessary information and permissions to conduct an audit effectively and efficiently. In this article, we will discuss the purpose, components, and steps involved in the audit professional clearance process.1. Definition and Purpose of Audit Professional ClearanceAudit professional clearance refers to the formal process of obtaining permission from a former or outgoing auditor to take over the audit engagement. It is a critical step in the audit process, as it allows the incoming auditor to gain access to relevant information and establish a professional relationship with the client.The purpose of audit professional clearance is to ensure a smooth transition between auditors and maintain the integrity and quality of the audit process. It is also important for the incoming auditor to gain a thorough understanding of the client's business, previous year's financial statements, and any potential audit risks or issues.2. Components of Audit Professional ClearanceThe audit professional clearance process generally consists of several key components:a. Notification to the Former Auditor: The incoming auditor must notify the former auditor in writing about their intention to take over the audit engagement. This notification typically includes details such as the client's name, the year-end date, and the planned start date of the audit.b. Request for Audit Working Papers: The incoming auditor requests access to the previous year's working papers from the former auditor. These working papers contain valuable information, including audit procedures performed, significant findings, and conclusions reached during the previous audit.c. Client Consent: The client's consent is required for the incoming auditor to access the previous year's working papers. This consent is usually obtained through a letter of recommendation addressed to the former auditor, where the client authorizes the release of relevant information to the incoming auditor.d. Confirmation of Independence: The incoming auditor confirmstheir independence and freedom from any conflicts of interest that may impair their objectivity and professional judgment. They may need to submit an independence declaration or sign anon-disclosure agreement to ensure the confidentiality of client information.3. Steps Involved in Audit Professional ClearanceThe audit professional clearance process typically follows a series of steps to ensure an efficient and effective transition between auditors:Step 1: Initial CommunicationThe incoming auditor initiates contact with the former auditor by sending a formal letter, notifying them about the upcoming audit engagement and requesting access to the previous year's working papers.Step 2: Request for Working PapersOnce the former auditor receives the initial communication, they compile and send the relevant audit working papers to the incoming auditor. It is important for the former auditor to ensure the accuracy and completeness of these working papers.Step 3: Evaluation and ReviewThe incoming auditor evaluates the received working papers, seeking any additional clarification or information from the former auditor if required. They review the working papers to gain insights into the previous audit's findings, audit risks, and areas that may require special attention during the current audit.Step 4: Client Consent and Independence ConfirmationThe incoming auditor requests the client's consent to access the previous year's working papers. Simultaneously, they confirm their independence by signing an independence declaration ornon-disclosure agreement, providing assurance of their objectivity and professionalism.Step 5: Finalize the ClearanceOnce all the necessary components are in place, the audit professional clearance process is considered complete. The incoming auditor assumes the responsibility of the audit engagement and commences their audit procedures.In conclusion, the audit professional clearance process is a crucialstep in the audit cycle that ensures a smooth transition between auditors and facilitates the exchange of information needed for a comprehensive audit. By following the defined components and steps, auditors can maintain the integrity and quality of the audit process while establishing a professional relationship with the client.。

审计学:一种整合方法 阿伦斯 英文版 第12版 课后答案 Chapter 20 Solutions Manual

Chapter 20Completing the Tests in theAcquisition and Payment Cycle:Verification of Selected AccountsReview Questions20-1Because the source of the debits in the asset account is the acquisitions journal (or similar record), the current period acquisitions of property, plant and equipment have already been partially verified as part of the acquisition and payment cycle. The disposal of assets, depreciation and accumulated depreciation are not tested as a part of the acquisition and payment cycle.20-2The reason for the emphasis on current period acquisitions in auditing property, plant, and equipment is that there is an expectation that permanent assets will be kept and maintained on the records for several years. The assets carried over from the preceding years can be assumed to have been verified in the prior years' audits.If it cannot be shown through tests of controls and substantive tests of transactions that all disposals have been recorded, additional testing of the prior balance could be required. A first year audit also necessitates tests of the beginning balance.20-3Many clients may accidentally or intentionally record purchases of assets in the repair and maintenance account. The misstatement is caused by a lack of understanding of generally accepted accounting principles and some clients' desire to avoid income taxes. Repair and maintenance accounts are verified primarily to uncover unrecorded property purchases.The auditor typically vouches the larger amounts debited to those expense accounts at the same time that property accounts are being audited.20-4The audit procedures that may be applied to determine that all property, plant and equipment retirements have been recorded are as follows:1. Review whether newly acquired assets replace existing assets. Ifso, inquire as to whether the old asset has been removed from thebooks.2. Analyze gains on the disposal of assets and miscellaneous incomefor receipts from the disposal of assets. Compare these to property,plant and equipment accounts to see whether the asset has beenremoved from the books.3. Review planned modification and changes in product lines, taxes,or insurance coverage for indications of deletions of equipment.4. Make inquiries of management and production personnel about thedisposal of assets.20-5The two considerations to be kept in mind in auditing depreciation expense are:1. Whether the client is following a consistent depreciation policy fromperiod to period.2. The accuracy of the client's calculations.An overall reasonableness test can be made by calculating the depreciation rate for the year times the undepreciated fixed assets. In addition, it is desirable to check the accuracy of the depreciation calculation. The extent of the accuracy tests will vary depending on the engagement circumstances.20-6Since the source of the debits to prepaid insurance is the acquisitions journal or similar record (assuming all insurance premiums are charged to prepaid insurance rather than insurance expense), the current period premiums have already been partially verified as a part of the acquisition and payment cycle. The allocation of the premium between prepaid insurance is not tested as a part of the acquisition and payment cycle.20-7The audit of prepaid insurance should ordinarily take a relatively small amount of audit time because:1. The balance in prepaid insurance is normally immaterial;2. There are ordinarily few transactions during the year and mosttransactions are immaterial;3. The transactions are ordinarily not complex.20-8The evaluation of the adequacy of insurance is a test of reasonable protection against the loss of existing assets. The verification of prepaid insurance is performed to determine whether:1. The balances represent proper charges against future operations.2. The additions represent charges to these accounts and arereflected at actual cost.3. Amortization or write-off is reasonable under the circumstances.The evaluation of adequacy of insurance coverage is more important because of the potential loss due to under-insurance. Verification of prepaid insurance usually involves an immaterial amount and is not emphasized in most audits.20-9The audit of prepaid expenses differs from the audit of other asset accounts, such as accounts receivable or property, plant, and equipment, because prepaid expenses are often immaterial. Analytical procedures are often sufficient for auditing prepaid expenses, while tests of details of balances are usually required for other accounts such as accounts receivable and property, plant, and equipment.20-10Debits to accrued rent arise from the cash disbursements journal, which is verified as a part of tests of controls and substantive tests of transactions for cash disbursements. The credits typically arise from the general journal and may not have been verified as a part of these tests. Furthermore, tests of controls and substantive tests of transactions do not include verification of the inclusion of accruals on all existing property and verification of the consistent treatment of the accruals from year to year.20-11Property tax accruals take little audit time for most audits, and since there are relatively few transactions to test and they are typically material in amount, it is common to verify the accounts 100 percent. On the other hand, accounts payable takes quite a bit of audit time and since there are usually a large number of transactions to test and they are typically varied in amount, it is common to verify the account on a test basis.20-12The following documents will be used to verify accrued property taxes and related expense accounts:1. Deeds to properties2. Property tax returns3. Cancelled checks4. Invoices from the taxing authority20-13Three expense accounts that are tested as part of the acquisition and payment cycle or the payroll and personnel cycle are:1. Property tax expense2. Payroll expense3. Rent expenseThree expense accounts that are not directly verified as part of either of these cycles are:1. Depreciation expense2. Amortization of patents3. Year-end bonuses to officers20-14The analysis of expense accounts is a procedure by which selected expense accounts are verified by examining underlying supporting vendors' invoices or other documentation to determine if the transactions making up the total are correctly stated. The emphasis in most expense account analysis is on the occurrence of recorded amounts, accuracy, and classification.Potentially the same objectives are accomplished in tests of controls and substantive tests of transactions as for expense account analysis. The major differences are that tests of controls and substantive tests of transactions are selected from all of the acquisitions and cash disbursements journals for the entire period whereas transactions examined for expense analysis are limited to the account being analyzed. Nevertheless, the procedures are closely related, and if the tests of controls and substantive tests of transactions procedures results are satisfactory, reduced expense account analysis is implied.20-15The approach for verifying depreciation expense should emphasize the consistency of the method of depreciation used and the related computations, since these aspects of depreciation expense are the main determinants of the account balance. The use of analytical procedures and reperformance tests is important for depreciation expense.In verifying repair expense, the emphasis should be on vouching transactions that may be capital items; therefore, examining supporting documentation for transactions from months with unusually large totals or transactions that are themselves large or unusual is the normal audit approach followed.The approach is different because in repairs and maintenance the primary objective is to locate improperly classified fixed assets, whereas in depreciation the emphasis is on consistency from period to period and accurate depreciation calculations.20-16The factors that should affect the auditor's decision whether or not to analyze an account balance are:1. The analytical procedures indicate there is a high likelihood ofmisstatement in an account.2. The tests of controls and substantive tests of transactions indicatethere is a high likelihood of misstatement in an account.3. The account is likely to contain misstatements because it is difficultfor the client to properly classify or value the transactions.4. The auditor knows that the account is frequently subject to abuse ormisstatement.5. The analysis of the account might disclose a contingency.6. Tax returns and the SEC require the disclosure of certaininformation, which the account is likely to provide.Four expense accounts that are commonly analyzed in audit engagements are:1. Legal expense2. Travel and entertainment expense3. Tax expense4. Repair and maintenance expenseMultiple Choice Questions From CPA Examinations20-17 a. (1) b. (1) c. (4)20-18 a. (3) b. (4) c. (4)20-19 a. (1) b. (4) c. (3)20-20 a. (2) b. (4) c. (4)Discussion Questions and Problems 20-2120-24a. No. In a first audit the audi tor’s attention cannot be confined to activity in the year under audit because (1) some balance sheetaccounts include material amounts which originated in prior years,(2) some income and expense accounts include entries which arebased on decisions or transactions of prior years, and (3)consistency over the years in the application of generally acceptedaccounting principles is necessary for fairly presented financialstatements. Also, some audit testing of a nonrecurring nature willbe necessary in an initial engagement because the auditor does nothave the benefits of (1) familiarity with the company's history,personnel, system and operations, (2) information regarding thecomposition and reliability of beginning of the year balances, and (3)preceding year's audit working papers. Consequently, in the firstaudit the auditor will require such corporation documents as bylaws,articles of incorporation, minutes since incorporation, organizationcharts and flowcharts, and must comprehensively obtain anunderstanding of internal control and assess control risk todetermine the scope of audit testing.b. The audit program procedures that the auditor should use to verifythe January 1, 2007, balances in the land, building and equipment,and accumulated depreciation accounts of Hardware ManufacturingCompany should include the following:1. Read the minutes since incorporation in 2003 to ascertainthat for major property transactions approved, alltransactions were recorded in the accounts, and recordedtransactions were properly approved.2. Scan activity in the general ledger accounts sinceincorporation in 2003 for both fixed assets and accumulateddepreciation to identify items of large amount and unusualnature which will warrant further investigation.3. Examine support for principal property additions to ascertainthat the capitalization includes costs of freight-in, installation,and major improvements and labor, and overhead on self-constructed assets.4. Ascertain that fixed assets donated by stockholders wererecorded at fair market value on the date of donation andthat contributed capital was properly credited.5. Compare the yearly totals of repairs and maintenanceaccount balances and test abnormally high amounts to seethat they do not include assets charged to expense.6. Examine recorded deeds supporting ownership of buildingsand determine that any encumbrance was properly reportedin the financial statements.7. Examine support (asset and accumulated depreciation) forrecorded disposals or abandonments of material amounts.20-24 (continued)8. Tour the plants and account for major property items onhand to substantiate the reasonableness of fixed assetmaster file records and to ascertain that idle, obsolete orworthless assets are not being reported at more than theirfair value in the financial statements.9. Test the assigned lives of depreciable assets and the bases,methods and computations of accumulated depreciation forpropriety and consistency.10. Review charges to the accumulated depreciation accounts todetermine that they properly represent disposals,abandonments or extraordinary repairs.11. Review the gains and losses on property disposals as anadditional means of assurance that the depreciation livesand methods used are reasonable.12. Scan federal income tax returns of prior years and revenueagents' reports pertaining to them to determine whetheradjustments made for tax purposes should also be made onthe books.13. Determine that generally accepted accounting principles ofincome tax allocation are being used for differences betweentax depreciation and financial statement depreciation.14. Inspect real estate and property tax bills to furthersubstantiate ownership and valuation of fixed assets.20-25Overall, the program fails to emphasize the possibility of omitted property from the list. The key to an adequate audit of accrued property taxes is making sure all owned property and only owned property is included and on the list.20-2620-27 The banker has failed to recognize that the audit tests discussed relate as much to the income statement as to the balance sheet. For example, obtaining an understanding of internal control and the tests of controls and substantive tests of transactions are heavily income statement oriented, analytical procedures are more closely related to the income statement than to the balance sheet, and even tests of details of the balance sheet help to uncover misstatements in the income statement. The typical audit recognizes the interrelationship between the income statement and the balance sheet and uses this interrelationship to help design more effective tests to uncover misstatements in both statements. The auditor is and should be greatly concerned about the fair presentation of the income statement.Case – Ward Publishing Company20-28a. The tests of acquisition and cash disbursement transactions have two purposes: to determine whether related internal accountingcontrols are functioning (tests of controls), and to determinewhether the transactions actually contain any monetarymisstatements (substantive). The results of the tests apply to thepopulation of all acquisitions and cash disbursements, includingplant and equipment and lease acquisitions and cashdisbursements, even though the specific sample tested does notinclude any such transaction. Thus, if the results of the tests arefavorable, it is concluded that there is a lower expectation ofmisstatements in plant and equipment and lease transactions, andvice-versa.b. A summary of the results from tests of controls and substantivetests of transactions for acquisitions and cash disbursements from Case 19-32 is: all transaction-related audit objectives are being met at a satisfactory level except:1. All supporting documents are not always attached to thevendor's invoice. Note: Students using a nonstatisticalapproach to Case 19-32 may not conclude that the resultsfor this attribute [9.b.(1)] are unacceptable, depending ontheir estimate of CUER. However, most students will likelyconclude that the results are unacceptable.2. All vendors’ invoices are not initialed for internal verification.Half of those not initialed had account classification errors.The impact of these results and the results from items 1 through 7 affect the balance-related audit objectives for plant and equipment in the following way:Conclusions 3, 5, and 7 indicate a need for more extensive auditing for existence, completeness, accuracy, and classification.All large items should be verified and samples should be larger than normal. All other tests can be performed at minimum levels.c. The results of tests of controls and substantive tests of transactionsare directly related to the tests of many expense accounts, primarilythrough tests for account classification, but also through tests ofaccuracy and existence. For example, if the auditor concludes thatthe internal controls are effective for recording acquisitiontransactions, the likelihood of misstatements for accounts such assupplies, purchases, and repairs and maintenance is greatlyreduced. The auditor must keep in mind, however, that certainexpense accounts are not usually verified as a part of tests ofcontrols and substantive tests of transactions. An example isdepreciation expense. Similarly, certain accounts may have ahigher inherent risk such as legal expense and therefore requireadditional testing even if tests of controls and substantive tests oftransactions results are satisfactory. Also, analytical proceduresand tests of details of balances for balance sheet accounts resultsaffect the extent of auditing needed for expense accounts.d. The results of tests of controls and substantive tests of transactionsindicate the potential for significant classification misstatements.(See the results for Audit Procedure 9b(5) for classification in Part 2of Case 19-32.) This potential for misclassification misstatementcombined with the analytical procedures results in Conclusion 6indicate a need for more extensive account analysis for repairs andmaintenance, small tools expense, and the three other accountswhere there are significant changes from prior years. No otherconclusions should cause the auditor significant concern in theaudit of expense accounts.20-29 a. Items 1 through 6 would have been found in the following way:1. The company's policies for depreciating equipment areavailable from several sources:a) The prior year's audit schedules and permanent file.b) Footnote disclosure in the annual report and SECForm 10-K.c) Company procedures manuals.d) Detailed fixed asset records.2. The ten-year lease contract would be found when supportingdata for current year's equipment additions were examined.Also, it may be found by a review of company lease files,contract files, or minutes of meetings of the board ofdirectors. The calculations would likely be shown on asupporting schedule and can be traced to the general journal.3. The building wing addition would be apparent by the additionto buildings during the year. The use of the low constructionbid amount would be found when support for the additionwas examined. When it was determined that thisinappropriate method was followed, the actual costs couldbe determined by reference to construction work orders andsupporting data. The wing could also be examined.4. The paving and fencing could be discovered when supportwas examined for the addition to land.5. The details of the retirement transactions could bedetermined by examining the sales agreement, cash receiptsdocumentation, and related detailed fixed asset record. Thisexamination would be instigated by the recording of theretirement in the machinery account or the review of cashreceipts records.6. The auditor would become apprised of a new plant in severalways:a) Volume would increase.b) Account details such as cash, inventory, prepaidexpenses, and payroll would be attributed to the newlocation.c) The transaction may be indicated in documents suchas the minutes of the board, press releases, andreports to stockholders.d) Property tax and insurance bills examined show thenew plant.One or more of these occurrences should lead the auditor to investigate the reasons and circumstances involved. Documents from the city and appraisals could be examined to determine the details involved.b. The appropriate adjusting journal entries are as follows:1. No entry necessary.2. This is an operating lease and should not have beencapitalized.Prepaid rent $50,000Lease liability 354,000Allowance for depreciation-machinery and equipment 20,200Machinery and equipment $404,000Depreciation expense 20,200To correct initial recording of lease:Equipment rent expense $37,500Prepaid rent $37,500 To record nine months rent:9/12 x $50,000 = $37,5003. The wing should have been recorded at its cost to the company.(Accounts originally credited) $15,000Buildings $15,000 To correct initial recording of new wing:Depreciation expense $3,167Allowance for depreciation—Buildings $3,167 To correct depreciation for excess cost.Depreciation on beginning balance1,200,000/25 = 48,000Depreciation recorded on addition51,500 - 48,000 = 3,500Correct depreciation for addition:Remaining useful life of addition is 12 years(600,000/1,200,000 x 25 = 12-1/2 years; 12-1/2 - ½ = 12 years)Depreciation = $160,000/12 x ½ = $6,667Correction = $6,667 - $3,500 = $3,1674. The paving and fencing are land improvements and should bedepreciated over their useful lives.Land improvements (may be $50,000combined with buildingswith buildings account—buildings and improvements)Land $50,000To correct initial recording of paving and fencing:Depreciation expense $2,500Allowance for depreciation—Land Improvements $2,500 To record first year's depreciation on paving and fencing:$50,000/10 x ½ = $2,5005. The cost and allowance for depreciation should have beenremoved from the accounts and a gain or loss on sale recorded.Cost of asset $480,000Allowance for depreciation:To 12/31/06 - 480,000/10 x 3-1/2 168,000For 2007 - 480,000/10 x ½ 24,000192,000Net book value 288,000Cash proceeds 260,000Loss on sale $28,000The correcting entry is:Allowance for depreciation—Machinery and Equipment $203,000Loss on sale of assets 28,000Machinery and Equipment $220,000Depreciation expense 11,0006. Donated property should be capitalized at its fair market value.Land $100,000Buildings 400,000Contributed capital- $500,000Donated PropertyTo record land and building for new plant donated by Crux City:Depreciation expense $8,000Allowance for depreciation—Buildings $8,000 To record depreciation on new plant:$400,000/25 x ½ = $8,00020-30a.To: In-Charge AuditorFrom: Audit ManagerSubject: Concerns about the schedule prepared by the client and the staff assistant in the audit of Vernal Manufacturing CompanyThe analytical procedures schedule for the audit of Vernal Manufacturing Company is completely inadequate and needs to be redone. There are several deficiencies:1. The headings, references, and indexing on the audit schedule areincomplete. It appears that the schedule was prepared by the client, but itis not possible to determine from the schedule.2. A classified income statement would provide more useful informationthan the single-step statement provided.3. The schedule should include the additional columns showing the percentof net sales for 12-31-06 and 12-31-07. This information would permit usto more effectively evaluate the relative change in each account.4. There is no indication that the general ledger totals were compared togeneral ledger balances or that calculations were tested.5. There is no identification of accounts that we are concerned may bematerially misstated. For example, the $1,381 change in insurance expenseappears immaterial but the 427% change in other expense may besignificant.6. There is no indication of specific accounts that require additionalinvestigation and the nature of such investigation.7. There is no indication that the client's explanations have been evaluatedand supported by evidence. Management inquiry is a weak form ofevidence and unsatisfactory by itself.b. For every explanation provided by the client, an alternativepossibility is a misstatement in the financial statements. The auditor must be satisfied that significant differences are not material misstatements. The following are a few examples:c. To perform a meaningful determination of the most importantvariances, an alternative design of the audit schedule follows. It is much easier to determine relevant variances with an adequate analytical procedures schedule.PER G/L PERCENT PER G/L PERCENT CHANGE12-31-06 12-31-06 12-31-07 12-31-07 Amount PercentSales $8,467,312 100.8% $9,845,231 102.5% $1,377,919 16.3%Sales returns andallowances (64,895) (0.8%) (243,561) (2.5%) (178,666) 275.3%Net Sales 8,402,417 100.0% 9,601,670 100.0% 1,199,253 14.3%Cost of goods sold:Beginning inventory 1,487,666 17.7% 1,389,034 14.5% (98,632) (6.6%) Purchases 2,564,451 30.5% 3,430,865 35.7% 866,414 33.8% Freight-in 45,332 0.5% 65,782 0.7% 20,450 45.1% Purchase returns (76,310) (0.9%) (57,643) (0.6%) 18,667 (24.5%) Factory wages 986,755 11.7% 1,145,467 11.9% 158,712 16.1% Factory benefits 197,652 2.4% 201,343 2.1% 3,691 1.9% Factory overhead 478,659 5.7% 490,765 5.1% 12,106 2.5% Factory depreciation 344,112 4.1% 314,553 3.3% (29,559) (8.6%) Ending inventory (1,389,034) (16.5%) (2,156,003) (22.5%) (766,969) 55.2%Total 4 ,639,283 55.2% 4,824,163 50.2% 184,880 4.0%Gross margin 3,763,134 44.8% 4,777,507 49.8% 1,014,373 27.0% Selling, general and administrative:Executive salaries 167,459 2.0% 174,562 1.8% 7,103 4.2% Executive benefits 32,321 0.4% 34,488 0.4% 2,167 6.7%Office salaries 95,675 1.1% 98,540 1.0% 2,865 3.0%Office benefits 19,888 0.2% 21,778 0.2% 1,890 9.5%Travel and entertainment 56,845 0.7% 75,583 0.8% 18,738 33.0% Advertising 130,878 1.6% 156,680 1.6% 25,802 19.7%Other sales expense 34,880 0.4% 42,334 0.4% 7,454 21.4% Stationery and supplies 38,221 0.5% 21,554 0.2% (16,667) (43.6%) Postage 14,657 0.2% 18,756 0.2% 4,099 28.0% Telephone 36,551 0.4% 67,822 0.7% 31,271 85.6%Dues and memberships 3,644 0.0% 4,522 0.0% 878 24.1%Rent 15,607 0.2% 15,607 0.2% 0 0.0%Legal fees 14,154 0.2% 35,460 0.4% 21,306 150.5% Accounting fees 16,700 0.2% 18,650 0.2% 1,950 11.7% Depreciation, SG&A 73,450 0.9% 69,500 0.7% (3,950) (5.4%)Bad debt expense 166,454 2.0% 143,871 1.5% (22,583) (13.6%) Insurance 44,321 0.5% 45,702 0.5% 1,381 3.1%961,705 11.4% 1,045,409 10.9% 83,704 8.7%Total operating income 2,801,429 33.3% 3,732,098 38.9% 930,669 33.2%Other expenses:Interest expense 120,432 1.4% 137,922 1.4% 17,490 14.5%Other 5,455 0.1% 28,762 0.3% 23,307 427.3%Total 125,887 1.5% 166,684 1.7% 40,797 32.4%Other income:Gain on sale of assets 43,222 0.5% (143,200) (1.5%) (186,422) (431.3%) Interest income 243 0.0% 223 0.0% (20) (8.2%) Miscellaneous income 6,365 0.1% 25,478 0.3% 19,113 300.3%Total 49,830 0.6% (117,499) (1.2%) (167,329) (335.8%) Income before taxes 2,725,372 32.4% 3,447,915 35.9% 722,543 26.5% Income taxes 926,626 11.0% 1,020,600 10.6% 93,974 10.1%Net income $1,798,746 21.4% $2,427,315 25.3% $ 628,569 34.9%The following are variances of special significance to the audit that have been determined from the revised analytical procedures worksheet. Before doing additional work, there should be further discussion with knowledgeable management about the variances identified. After investigating management's explanations, the following additional audit procedures may be appropriate:。

工厂检验报告样本CIG023

CIG 023Factory InspectionReport ChineseUL does not endorse any vendors or products referenced herein.UNDERWRITERS LABORATORIES INC. ASSUMES NO RESPONSIBILITY FOR ANY OMISSIONS OR ERRORS ORINACCURACIES WITH RESPECT TO THIS INFORMATION. UL MAKES NO REPRESENTATION OR WARRANTY OF ANY KIND WHATSOEVER, WHETHER EXPRESS OR IMPLIED, WITH RESPECT TO THE ACCURACY, CONDITION, QUALITY, DESCRIPTION, OR SUITABILITY OF THIS INFORMATION, INCLUDING ANY WARRANTY OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE AND EXPRESSLY DISCLAIMS THE SAME.Copyright Underwriters Laboratories Inc. All rights reserved. May not be reproduced without permission. This document isWARNING:THIS DOCUMENT IS ONLY VALID IF USED BY ECS MEMBERSAND THEIR AUTHORISED AGENTSPERMANENT DOCUMENT 永久性文件CIG 023Factory Inspection Report 工厂检验报告WARNING:THIS DOCUMENT IS ONLY VALID IF USED BY ECS MEMBERSAND THEIR AUTHORISED AGENTS警告:本文件仅在为欧洲认证体系(ECS)成员及其授权代理人所用时生效Approved by: ECS General Meeting, 22/23-04-2009 Nr of pages: 19 Date of issue: May 2009Supersedes: PD CIG 023 - June 2004 Page 1 of 19 PD CIG 023 reports shall not contain any unauthorised modifications which change the originalmeaning or the requirements.Any additions created to any document in the series shall be shown in an Appendix.未经批准,不得对 PD CIG 023 报告进行任何改变其原有含意或要求的修改。

TongWeb5.0用户使用手册

TongWeb 5.0 用户使用手册

东方通科技

1

T ongT ec......................................................................................... 1

第1章 1.1 1.2 1.3 1.4 1.5 1.6 第2章 2.1 TongWeb5.0 应用服务器概述 ...................................................................................... 12 概述 ............................................................................................................................... 12 JavaEE 5 的新特性....................................................................................................... 12 TongWeb5.0 的体系结构 .............................................................................................. 12 TongWeb5.0 的特性 ...................................................................................................... 14 集成的第三方产品...........

0A SMETA Guide to Pre-Audit Information

Guide to a Pre-Audit Information PackBACKGROUNDAs the SMETA process becomes more widely used, Sedex members have requested a standard pack to provide suppliers / supplier sites with essential pre-audit information, which will help them prepare for a SMETA audit.The pack has been put together by the Associate Auditor Group and includes documents already being used by auditors performing SMETA audits, as well as some new additions.The information does not aim to replace any documentation currently in use, rather it is intended as a template to answer the most frequently asked questions and assist all parties in preparing for a SMETA audit.SMETA users should include this only if they find it helpful.USAGEThis ‘Guide to a Pre-Audit Pack for SMETA audits (henceforth known as ‘Suite of Docum ents’) has been assembled from an auditor’s perspective,and for an auditor’s use, anticipating that this group are often the first contact a supplier has with the Sedex system.Other types of members (and non-member users of SMETA) may find it useful for informing their supply chain, and it is hoped that supplier sites will also find it helpful in preparing for a SMETA audit.The guide has been put together in stand-alone sections, within the ‘Suite of Documents’ so that both auditors and other SMETA users can select the parts which are appropriate for them.By making this widely available in a standard format the AAG hopes to further increase the consistency of the SMETA process. It is suggested that both auditors and/or customers will find this framework helpful in preparing supplier sites for audit and supplier sites should also improve their performance by increasing their ‘audit process awareness’.Guide to a Pre-Audit Information PackCONTENTSThe ‘Suite of Documents’ in this guide is suggested by the AAG as the minimum requirements for pre-audit activity by the auditor, as well as the pre-information necessary to prepare the site for a SMETA audit. Please see below for details on how each document can be used.The documents (included in this ‘Suite of Documents’) should include but not be limited to:1. Auditing Factsheet2A & 2B. Essential Pre-Audit Actions for Auditors/Sites3. Introductory Letter4. Code of Integrity and Professional Conduct of an Auditor/Audit company5. Documents outlined in SMETA Best Practice Guidance5A. Ethical Trading Initiative Base Code5B. Scope of a SMETA Audit5C. List of Required Documents5E. Principles of Worker Interview5F. Data Protection Waivers5G. Information on Sedex and details of SMETA supplements5H. Worker Information Leaflet5I. Typical Audit Agenda5J. Non-compliance Process and Sedex5K. Details of Report Receivership5L. Audit Follow-upGuide to a Pre-Audit Information PackOVERVIEW OF SUITE OF DOCUMENTS1. Auditing FactsheetThis document covers in brief ‘What is Sedex’, an outline of Sedex and ethical audits, as w ell as how SMETA fits into the Sedex process.2A. Notes to auditors of essential actions before an auditMain topics covered are the need to explain the benefits of the SMETA process (potential of one audit for all customers), as well as the need to pre-review the site’s Self Assessment Questionnaire (SAQ). See ‘Essential Pre-Audit Actions for Auditors’.2B. Notes to sites of essential actions before an auditOutlines the activities required of a supplier site in preparation for an audit. Correctly followed, this will facilitate the audit proceeding smoothly with all relevant logistical arrangements, people, and documents, in place on the day. See ‘Essential Pre-Audit Actions for Sites’.3. A letter to the site introducing the audit and auditorThis briefly explains the audit process, the standards to be used, and gives contact details for the auditor/audit company, in case the supplier has questions ahead of the audit day. See‘Introductory Letter’.4. The code of integrity and professional conduct of the auditor/audit companySMETA requires that the site is given information on the auditor’s/audit company’s own code covering the professional conduct of the auditor. This document suggests a possible code. In this example the site signs to confirm it has received a copy and understood the content, which is recommended as best practice. See ‘Code of Integrity and Professional Conduct of an Auditor/Audit company’.This may be sent with the pre-audit information pack, but it is also a necessary part of the discussion on the audit day.5. Documents outlined in SMETA Best Practice Guidance. i.e.:5A. The standard code and local law that applyThe supplier must be aware of the standards they will be audited against. If you are an independent auditor you can find local law information on the UN /ILO web sites, or from theGuide to a Pre-Audit Information Packlocal offices of large audit firms - note this may be a costed service. Where possible, copies of relevant laws should be sent to suppliers as part of the pre-audit pack.The SMETA methodology uses the Ethical Trading Initiative (ETI) Base Code. Please ensure that this code is communicated to the supplier effectively. The code is available in several languages; please establish if the supplier has a preference. A copy is within the ‘Suite of Document s’ as ‘Ethical Trading Initiative base code’.5B.Audit ScopeThis outlines the areas which are covered by the audit activity. It may be included in the introductory letter, but for the purposes of this guidance it has been included within the ‘Suite of Document s’as a separate document ‘Scope of a SMETA audit’.5C. List of documents that is to be available on the day of the auditTo assist the site with audit preparations the auditor should provide a list of typical documents that should be made available to the audit body on the day of the audit. This should be sent in sufficient time to allow the site to prepare the necessary documents in advance of the audit. Attached is a ‘List of Required Documents’.5D. Key people to be available on the day of the audit e.g. management personnel, union or workers committee representatives, Health and safety representativesFor the purpose of this pack, this information has been included in the ‘Introductory Letter’ in the ‘Suite of Documents’.5E. Principles of employee interviewsInforms the site of the need for a private and comfortable (for workers) space for worker interview and gives details of how the auditors will select appropriate workers. Attached as‘Principles of Worker Interview’.5F Confidentiality /Data ProtectionIn countries where there are data protection requirements, e.g. all EU countries, auditors should obtain the written permission of workers to view personnel files during the interviews, via the use of data consent forms.Note: some contracts of employment or t erms of engagement contain a clause saying that “as an employer the company holds and may share personal information about its employees”. In these cases it is advisable to check the legal position. If in doubt see attached a document from the ETI which may be used for signatures, in the ‘S uite of Documents’ as ‘Data Protection Waiver’.Guide to a Pre-Audit Information Pack5G: Standard information regarding Sedex and the Best Practice GuidanceThis can be included in the introductory letter and see also the Auditing Factsheet. There are several other documents available to Sedex members which are useful when a supplier is expecting a SMETA audit. See attached ‘Information on Sedex and SMETA supplements’.5H. Worker Information Leaflet (leaflets or DVD)ETI Code requires that employees are fully aware of the code and that there are standard communications which will support a supplier site in communicating the code to workers. Audit companies can supply a 15 minute DVD which covers the 9 elements of the ETI code. To assist the supplier site, auditors may use the attached ‘Worker Information Leaflet’– see ‘Suite of Documents’.5I. Audit Agenda/ TimetableTo enable suppliers to plan the day(s), it is essential to give them prior warning of a typical audit time table. This may require alteration to suit the size of the site, but an information sheet is attached which includes two examples (a) typical audit plan for a one day audit , (b) typical audit plan for a 2 day audit with 2 auditors over one day. See ‘Typical Aud it Agenda’ in the ‘Suite of Documents’.5J: Non-compliance processThis document gives some brief details on the definitions of non-compliances, observations and good examples. It explains the purpose of the Corrective Action Plan Report (CAPR) and the actions required of the supplier site to agree (or dispute) the non-compliances. Also included is the purpose of the ‘root cause’ discussion, and the need for the s ite to take on ownership and completion of the corrective actions.Some information is also given on uploading the audit details to Sedex and links to further supplier guidance on audit upload. See ‘Non-compliance process and Sedex’.5K: Report receivership especially any third partiesDescribes the normal ownership of audit information and highlights the importance of obtaining ‘audit release’ information from the site if the customer expects to see details.Audit information belongs to the audit payee, but many of the site’s customers will expect to see a copy. Upload onto to the Sedex system will allow the site to share the information with clients they have linked to. For any off-line transfer of information, it is important that the site agreesGuide to a Pre-Audit Information Packwho else can obtain a copy of the audit report. See ‘Suite of Documents’ - ‘Details of report rece ivership’.5L: Audit Follow-up InformationA Follow-up audit is a process where an auditor verifies the corrective actions already completed by a site, and this can be performed by:- desktop follow-up where a site visit is not required and corrective actions can be verified by e.g. photographic evidence or documents provided by email- site visit follow up where an auditor re-visits a site to examine corrective actionsFor more details on how to prepare for follow up audit please see “Audit Follow Up” in the suite of documents.REVIEWThis ‘Guide to Pre-Audit Pack’ is a compilation of the best practices currently in use by audit companies/auditors currently performing SMETA audits.It will be the subject of continuous review and we welcome any feedback on how it might be improved.。

IECEx系统操作指南:有关在可爆性环境中使用设备的认证标准的认可的认证机构说明书

INTERNATIONAL ELECTROTECHNICAL COMMISSION SYSTEMFOR CERTIFICATION TO STANDARDS RELATING TO EQUIPMENT FOR USE IN EXPLOSIVE ATMOSPHERES (IECEx SYSTEM)Title: Draft Operational Document Ex OD 501 Assessment Procedures for IECEx acceptance of Certification Bodies (ExCBs) for the purpose of issuing and maintaining IECEx Certificates of Personnel CompetenciesCirculated to: IECEx Management Committee, ExMCINTRODUCTIONDraft Document ExMC/516/CD was prepared by ExMC WG12 during its February 2009 meeting and submitted to ExMC members for comment in March 2009. Comments received from members were collated and circulated as document ExMC/528A/CC.ExMC WG12 held a further 3 day meeting in Singapore during 23 – 25 June 2009 to consider the comments and necessary changes to the document.This document, ExMC/516A/DV incorporates the changes determined during the Singapore WG12 meeting and sets out the proposed Assessment Procedures for acceptance and on-going assessments of Bodies seeking to become ExCBs for the purpose of the IECEx Certificate of Personnel Competency Scheme, OD 501. Refer to ExMC/528A/CC for WG12 responses to comments.This document is issued to ExMC for final approval. Please submit your vote to the IECEx Secretariat by 21st August 2009 using the following voting form.The results of the voting will be reported during ExMC Melbourne 2009 September Meeting. Therefore we seek your assistance for return of the vote by the due date. Main changes to ExMC/516/CD incorporated in this updated version, ExMC/516A/DV include:¾Applications from prospective ExCBs to be endorsed by the IECEx Member Body prior to being accepted by the IECEx Secretariat (Step 1 Sect 1) ¾Review of flowchart to ensure consistency with table.¾Expansion of the assessment process of Step 7 Sect 1 concerning assessment of a CBs documentation, prior to proceeding further with the assessment.¾Expansion of introduction in Section 2 “On-Going Assessments” to require that the ExCB maintains their facilities “relating to assessing demonstration of craftskills”¾ A note added to A6 to clarify cases where CBs have limited experience in this area but yet possess necessary technical capabilityChris AgiusIECEx SecretariatAddress:SAI Global Building 286 Sussex Street Sydney NSW 2000 Australia Contact Details:Tel: +61 2 8206 6940Fax: +61 2 8206 6272e-mail:********************* Draft OD 501Edition 1.0 200x-xx IECExDraft Operational DocumentIECEx Scheme for Certification of Personnel Competencies for Explosive AtmospheresIECEx OD 501Assessment Procedures for IECEx acceptance ofCertification Bodies (ExCBs) for the purpose of issuing and maintaining IECEx Certificates of Personnel CompetenciesINTERNATIONAL ELECTROTECHNICAL COMMISSIONDraft IECEx OPERATIONAL DOCUMENTIECEx Scheme for Certification ofPersonnel Competency for Explosive AtmospheresEx OD 501 Edition 1.0Assessment Procedures for IECEx acceptance ofCertification Bodies (ExCBs) for the purpose of issuing andmaintaining IECEx Certificates of Personnel CompetenciesThis Draft Operational Document, OD 501 sets out the procedures for the assessment and acceptance of Certification Bodies seeking to become ExCBs for the purpose of operating under the IECEx Certificates of Personnel Competencies Scheme, IECEx 05.Document HistoryDate Summary 2009 XX Original Issue (Edition 1)INTRODUCTIONThis document details the assessment procedures established by the IECEx System’s Management Committee, ExMC, for the purpose of ensuring a thorough assessment of candidate ExCBs. The principle aim of these procedures is to instil international confidence in the ExCB’s competence and capabilities for performing assessment and maintaining IECEx Certificates of Personnel Competencies whom seek IECEx Certification.The assessment is to cover the competence, experience and familiarity of ExCB personnel and the organisation with the relevant explosive atmosphere standards, quality management systems, IECEx System and associated rules, ISO/IEC Guide 65, ISO/IEC 17024 and IECEx technical guidance documents. The procedures are also aimed at ensuring a consistent approach to assessments by IECEx assessment teams and therefore establishing confidence in the scheme.This document provides the following Section:Section 1 Initial Assessment and Re-Assessment of ExCBsSection 2 On going Surveillance of ExCBNOTE: A simple change of scope for an existing ExCB is not seen as viable due to the entirely different requirements used for Personnel Certification.The procedures are set out in table form identifying:⎯ Step number⎯ Required action⎯Responsible person or party⎯ Desired outcomeThe steps identified in the table correspond to the steps shown in the flowchart.INTERNATIONAL ELECTROTECHNICAL COMMISSIONDraft IECEx OPERATIONAL DOCUMENTIECEx Scheme for Certification ofPersonnel Competency for Explosive AtmospheresOD 501Assessment Procedures for IECEx acceptance ofCertification Bodies (ExCBs) for the purpose of issuing andmaintaining IECEx Certificates of Personnel Competencies1 INITIAL ASSESSMENT & RE-ASSESSMENTThis Section is to be applied for the initial assessment of ExCBs prior to their acceptance in the IECEx Certificate of Personnel Competency [CoPC] Scheme and re-assessment of existing ExCBs. The term Lead Assessor, as used throughout this document, shall mean the IECEx Assessment Team Leader appointed by the ExMC Secretary and endorsed by ExMC. Steps 1 – 4 are applicable to new applications.IECEx Assessment Flow Chart (Refer to table for details of each stepStep Activity By Whom Desired Outcome Formal Application Submitted to ExMC Secretary1 Application endorsed by Member Body prior tobeing received by ExMC Secretary, in accordancewith IECEx 05ExMC Secretary Candidate ExCB2 Application assessed for completeness andAssessment Team appointed. ExMC Secretary Assessment team proposed byIECEx Secretary3 ExMC Secretary reviews applicationdocumentation for completeness. ExMC Secretarymay request further information from thecandidate. ExMC Secretary to report findings tocandidate ExCBExMC Secretary4 ExMC Secretary forwards Application package toMembers of the appointed Assessment Team ExMC Secretary All relevant informationavailable for team to commencetheir assessmentDocumentation Review Stage5 IECEx Assessment Team commencesassessment. Team Leader, in conjunction withteam members reviews application documentationto satisfy steps 6 to 8. Team Leader may requestadditional information from the Candidate ExCB Team Leader toManageTeam Leader notifies candidateof successful review ofdocumentation and thenprepares to arrange site visit6 Team Leader, in conjunction with team membersdetermines whether the applicant ExCB hasIndependent Accreditation Team Leader orhis designateFormal notification ofaccreditation, with a copy beingsubmitted by the applicant7 Assessment of the accreditation and credentials ofthe accreditation body. For example determining:*Whether the body has Mutual RecognitionAgreements with other bodies*Whether the body has National Governmentrecognition*What Standards or Guides are usedIECEx Assessment Team Leader may obtaininformation directly from accreditation body orcandidate ExCB and circulate to other IECExAssessment team members for review viacorrespondence.Note: ExCB should obtain all necessaryinformation from accreditation body forpresentation to IECEx Assessment Team Leader.The assessment of the documentation shallestablish that the CB has the competence relatedto the particular aspects of hazardous areacompetence they will be issuing. This will includeany facilities provided for demonstration of craftskills”Note:” This may need to provide CV’s of particularpeople used in competency assessment activities.Team Leader *Verification of MRAs*Notification of Governmentrecognition*Use ofIECEx 01, Basic Rules of theIECEx System.ISO/IEC Guide 2,Standardization and relatedactivities - General vocabulary.ISO/IEC 17000 ConformityAssessment – Vocabulary andgeneral principlesISO/IEC 17024 ConformityAssessment – Generalrequirements for bodiesoperating certification ofpersons*Frequency of surveillanceaudits.8 Review of past audit reports, issued by theaccreditation body, by Assessment Team toestablish compliance with the requirements ofIECEx 05, and Documents, ISO/IEC Guide 2,ISO/IEC 17000 and ISO/IEC 17024 relevant. Assessment Teammanaged byTeam LeaderAcceptance by IECExAssessment Team ofinformation and audit reports asevidence of compliance to therequirements of IECEx 05,ISO/IEC Guide 2 and ISO/IEC170249 Notification of results of step 6-8 to candidateExCB Team Leader Letter, Fax or e-mail toCandidate ExCB. Copy toExMC SecretaryOn-site VisitStep ActivityBy Whom Desired Outcome10A minimum of one representative of the IECEx Assessment Team visits candidate to conduct a minimum 1 day site visit for each ExCBapplication. This visit is to verify implementation of certification or auditing proceduresAt least 1 person from IECExAssessment Team Usually Team LeaderVisit notes to be included in assessment file.Team Leader in consultation with his Team shall decide if more than 1 man day visit is necessary.11Results of site visit determined with a final report for submission to the ExMC Secretary prepared in the format as outlined in Annex A. Final report to be reviewed by all members of the assessment teamTeam LeaderTeam Leader to commence arrange for a final assessment report compiling a Report12 Final IECEx Assessment Team Report Reviewed by ExMC Secretary.ExMC SecretaryReview by ExMC Secretary to ensure completeness of information and ready forcirculation to ExMC for voting. 13ExMC Secretary prepares Report for voting and submits to ExMC Members for formal voting, via correspondence or at the next ExMC meeting. ExMC SecretaryExMC Document issued forvoting, with a copy submitted to candidate ExCBFinal Approval of ExCB by ExMC14 Assessment of report considered by ExMCmembers with members returning the completed voting form to the ExMC Secretary as soon as possible and by due date ExMC MembersMajority acceptance voteapproves application (re Clause 12.2 of IECEx 01)15 If voting is acceptable then ExMC Secretary notifies applicant of their acceptance ExMC Secretary ExMC Letter to accepted ExCB 16 Appointment recorded at next ExMC meeting ExMC Secretary to arrange Recorded in Minutes 17Where review in step 12 is unsatisfactory, ExMC Secretary refers the matter to the IECExAssessment Team Leader seeking additional information or revised reportExMC SecretaryAn acceptable report for circulation to ExMC18Where a positive vote, in accordance with IECEx 01 is not achieved the application is then referred to the next ExMC meeting for discussionExMC Secretary to arrange Findings recorded in the minutes19If at the conclusion of the “Document Review Stage’, the Assessment Team are not satisfied with the information presented, the Team Leader shall inform the candidate ExCB and ExMC Secretary of the Assessment team’s views. In order for the assessment to proceed, the IECEx Assessment Team may be required to conduct a full on site assessment in accordance with IECEx 05 and Technical Guidance Documents, ISO/IEC Guide 2, ISO/IEC 17000 and ISO/IEC 17024 as applicable.Team Leader to manageAssessment report by Team Leader20 Where non-conformances are identified during the assessment process the candidate ExCB implements corrective action if they wish to proceed with their applicationCandidate ExCBImplementation of corrective actions21Assessment team assesses corrective action. This may be performed by either the full team or a partial team or even one member of the team Team Leader to manage Report on assessment of corrective actions22Notification of results of step 5 to candidate ExCB and IECEx ChairmanTeam LeaderLetter, Fax or e-mail toChairman of Assessing Panel2 ON GOING ASSESSMENTSThis Section applies to ExCBs that have been accepted into the IECEx CoPC Scheme for the scope of issuing of IECEx Certification of Personnel Competencies to provide cross-industry competencies needed for work associated with equipment for hazardous areas. The purpose of on-going assessments is to satisfy the International Ex community that ExCBs maintain their facilities relating to assessing demonstration of craft skills and capabilities that enabled their entry into the Scheme.2.1 Surveillance of ExCBs with National Accreditation acceptable by ExMC2.1.1 ScopeThis section covers ExCBs that maintain national accreditation found to be acceptable by the original IECEx Assessment Team, and by way of ExMC voting on the initial assessment report, the ExMC. The procedures detailed below are general and ALL ExCBs are reminded of their obligations to notify the IECEx Secretariat of any changes within their organisation that may impact on their ability to deliver IECEx Certification Services in accordance with IECEx Rules and Operational Documents and in the spirit of a timely and professional service delivery.2.1.2 ProceduresEach year, prior to the anniversary date of acceptance into the IECEx System, ExCBs shall submit to the ExMC Secretary a report containing the following information:a) Any changes in the organisationDescription of changes in the organisation of the ExCB, its staff, facilities, quality system, operating procedures, or other similar changes, that relate to the ExCB’s operation under IECEx05.ANDb) Annual audit reportCopy of a National Accreditation Body’s audit report issued during the preceding 12 months. This report should show:⎯Site that was audited by the accreditation body⎯Date and duration of the audit⎯ Audit scope⎯ISO/IEC Guides, Standards and IECEx Technical Guidance Documents used during the audit⎯ Observation notes⎯Details of any non-conformances raised⎯Copy of any audit report summaryORc) Report by the ExCB based on its own internal audit(s) carried out during the preceding 12months. A standardised report format should be used for this purpose. Once every two years, the report, prepared by the ExCB shall be endorsed by the National Accreditation Body.Item a) is mandatory and either b) or c) is applicable.2.1.3 ReviewThe ExMC Secretary shall review the information to ensure:⎯Site assessed aligns with the site previously approved by ExMC;⎯All Clauses of ISO/IEC Guide 2, ISO/IEC 17000 and ISO/IEC 17024, as applicable, have been covered;⎯Ensure that Technical Guidance Documents have been used (where available);⎯Any Non-Conformances are identified;Where major Non-Conformances have been identified the ExMC Secretary in consultation with the IECEx Assessor Panel Chairman shall propose appropriate action to be taken, with the IECEx Officers to decide on such action and report at the next ExMC meeting. Where the ExCB does not agree with the course of action, the matter may be referred to the IECEx Board of Appeals, if requested by the ExCB. During the period of referral to the Board of Appeal, the ExMC Chairman in consultation with the other IECEx Officers shall decide on the status of the ExCB in question. In extreme circumstances the status of temporary suspension may be considered. The ExMC is to decide on the final action to be taken.The Secretary will retain a copy of the report, for a minimum of 10 years, for record keeping purposes.2.1.4 Re-assessmentOn the 5th anniversary of the acceptance of the ExCB, or re-assessment of an ExCB, a re-assessment in accordance with the assessment procedure detailed in Section 1 shall be performed by an IECEx Assessment Team appointed by ExMC.2.2 Surveillance of ExCBs without National Accreditation acceptable by ExMC2.2.1 ScopeThis section covers ExCBs that do not have national accreditation but who have been accepted in to the IECEx System by way of a full on-site assessment, by the IECEx Assessment Team.audit2.2.2 On-siteExCBs shall arrange to have one member of the original IECEx assessment team conduct an annual on-site audit. The assessor shall be appointed by the IECEx Assessment Team Leader responsible for the original assessment. The ExCB shall agree to bear the costs associated with this on-site audit.The appointed assessor shall carry out an assessment for compliance with ISO/IEC Guide 2, ISO/IEC 17000 & ISO/IEC 17024 and IECEx System Rules. The Team Leader will then issue a report.Where the original assessment team is no longer available a new assessment team shall be appointed by the ExMC.These reports shall be forwarded to the ExMC Secretary who shall review them for completeness and any non-conformances. Where non-conformances have not been identified the reports shall be retained, for a minimum of 10 years, for record keeping purposes, by the ExMC Secretary.2.2.3 Non-conformancesWhere Non-Conformances have been identified the reports shall be referred to the ExMC Secretary who shall consult with IECEx Officers who shall propose appropriate action to be taken and report at the next ExMC meeting. Where the ExCB does not agree with the course of action, proposed, the matter may be referred to the ExMC or IECEx Board of Appeal. During the period of referral to ExMC, the ExMC Chairman in consultation with the other IECEx Officers shall decide on the status of the ExCB in question. In extreme circumstances the status of temporary suspension may be considered. The ExMC will then decide on the final action to be taken.anniversary2.2.4 FifthOn the 5th anniversary of the acceptance of the ExCB, or re-assessment of an ExCB, a reassessment in accordance with the assessment procedure detailed in Section 1 shall be performed by an IECEx assessment team appointed by the ExMC.Annex AIECEx ASSESSMENT REPORT FORMFor ExCB(IECEx Certification Body –for Certification of Personnel Competencies Scheme) Type of Assessment:⎯Initial Assessment for Candidate ExCB⎯Surveillance Assessment for existing ExCBA.1 OBJECT AND FIELD OF APPLICATION..........................................................................................................................................................................................................................................................................................................................................................................................A.1.1 Country:..............................................................................................................................A.1.2 Name of Candidate ExCB............................................................................................................................................................................................................................................................A.1.3 Members Of The Assessment Team..........................................................................................................................................................................................................................................................................................................................................................................................A.1.4 Place And Date Of Assessment......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ReferencesA.1.5 AssessmentDocument:i) IECEx 05ii) IECEx Operational Document OD 503iii) IECEx Operational Document OD 501, OD 502 & OD 504iv) ISO/IEC 17000 & ISO/IEC 17024v) ExCB application documents datedOfApplicationA.1.6 ScopeIndicate whether this is an extension of scope for an already accepted ExCB (include detailsof existing acceptance)Category StandardCompetencyGeneral Requirements ISO/IEC 17024 .....................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................(List all Standards within scope of application or acceptance within IECEx)A.1.7 Candidate ExCB Persons InterviewedName Position ......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................A.1.8 Legal Entity Of The Candidate ExCB..........................................................................................................................................................................................................................................................................................................................................................................................A.1.9 Any Associated Testing OrganizationsNames of Organization Address ..........................................................................................................................................................................................................................................................................................................................................................................................A.1.10 Associated Certification Functions..........................................................................................................................................................................................................................................................................................................................................................................................A.1.11 National Marks And Certificates........................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................A.1.12 Financial Support..........................................................................................................................................................................................................................................................................................................................................................................................A.1.13 History....................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................A.1.14 Standards Accepted................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................A.1.15 National Differences in addition to IEC Standards..................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................A.2 ORGANISATIONA.2.1 Names, Titles And Experience Of The Senior ExecutivesName Title Experience ......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................A.2.2 Name, Title And Experience of The Quality Management RepresentativeName Title Experience ......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................。

审计报告 英文

审计报告英文An audit report is a document that provides an opinion on the financial statements of a company. It is prepared by an independent auditor who examines the financial records and transactions of the company to ensure their accuracy and compliance with relevant laws and regulations. The audit report is an important tool for stakeholders, such as investors, creditors, and regulators, to assess the financial health and performance of the company.The audit report typically includes the following components:1. Introductory section: This section provides an overview of the audit process, the responsibilities of the auditor, and the scope of the audit. It also includes a statement of the auditor's independence and a description of the basis for the audit opinion.2. Management's responsibility section: This section outlines the responsibilities of the company's management for the preparation and fair presentation of the financial statements in accordance with the applicable financial reporting framework.3. Auditor's opinion section: This is the most important part of the audit report. It presents the auditor's opinion on whether the financial statements present a true and fair view of the company's financial position and performance. The opinion may be unqualified, qualified, adverse, or a disclaimer of opinion, depending on the findings of the audit.4. Basis for opinion section: This section provides details of the audit procedures performed, the evidence obtained, and the basis for the auditor's opinion. It also includes any significant findings or issues identified during the audit.5. Other reporting responsibilities section: This section includes any additional information required by the applicable financial reporting framework or relevant laws and regulations, such as the auditor's responsibility for detecting fraud or non-compliance with laws and regulations.In conclusion, the audit report is a critical document that provides assurance on the reliability of a company's financial statements. It helps stakeholders make informed decisions and enhances the credibility and transparency of the financial reporting process. As such, it is important for the audit report to be prepared with the highest level of professionalism, accuracy, and integrity. The auditor should adhere to the relevant auditing standards and ethical principles to ensure the quality and reliability of the audit report. Ultimately, a well-prepared audit report contributes to the overall trust and confidence in the financial markets and the economy as a whole.。

安永审计流程

Performance Support

• Engagement Team Database • Area Assignment and Review Responsibilities Template • Automated Time Control Template • Other forms & templates • EY/AWS, GDA

பைடு நூலகம்

Outputs

Other Documentation

• Summary of: - Team goals and objectives - Each team members‟ key responsibilities: * Role * Audit areas * Work products and deliverables

Potential Client Deliverables

• Value Observation/ML items • Engagement Letter • Summary of co-developed expectations (client service communication)

Client

Audit Team

• Output from prior year audit • Team knowledge from discussions with client personnel • Information regarding changes in standards, policies and regulations

E&Y GAM: Road Map

Client Needs and Expectations / Our Responsibilities / Professional Standards

Audit-Sampling-for-Tests-of-Controls

Sample must represent population

Two Types of Sampling

Statistical Sampling Non Statistical Sampling

information are selected.

Sample Selection Methods

Nonprobabilistic

1. Directed sample selection 2. Block sample selection 3. Haphazard sample selection

Sampling risk will always be present - risk that sample is not representative of the population.

Signs That a Sample is Representative

The average amount of the sample is the same as the average of the population

Statistical Audit Sampling

Audit Samples

Need to be representative of the population in order for the auditor to draw conclusions about the population.

Sample Definitions

Sample - a selection from the population Sampling unit - one item in a sample Sampling refers to the extent of the tests or

SMETA-report