Case Study About Product Costing at Fine Foods Is It a Symptom or the Problem

淘宝case-study-(英文)

Universal Standard

Modules for searching, scanning and purchasing the goods is the same for all shops opened in Taobao

Easier to find desired goods and more convenient to buy things

More Internet Users will use Taobao to purchase things online

Universal Standard

Innovate its products with core business unchanged

Ubiquity

Promotion :

Micro blog Renren station Web portals EDM (Email Direct Marketing)

Ubiquity

A large number of advertisement outside : Underground Video Bus shelter

The problems Taobao faces

1. logistic issue (common for B2C & C2C) Logistics is the fundamental guarantee

to realize e-commerce. Although e-commerce rises up in China,

Source: /internet/inland/2012/0315/399872.html

商品营销策略英语案例

商品营销策略英语案例Case Study: Product Marketing StrategyIntroduction:In today's highly competitive market, effective product marketing strategies play a crucial role in attracting and retaining customers. This case study explores a successful product marketing strategy implemented by Company X, highlighting key elements that contributed to its success.Background:Company X is a well-established technology company that specializes in the development of smartphones and tablets. With dozens of competitors in the market, Company X wanted to strengthen its brand image and increase market share with its latest smartphone model, the XYZPhone.Product Positioning:To differentiate the XYZPhone from its competitors, Company X focused on highlighting its unique features and functionalities. They conducted thorough market research to understand their target audience's preferences and expectations. Based on this research, the company positioned the XYZPhone as a high-end smartphone, suitable for tech-savvy users who value innovative design, advanced technology, and a seamless user experience. Market Segmentation:Knowing that different market segments have varying needs and preferences, Company X segmented its target market into three main segments: professionals, millennials, and tech enthusiasts. Bytailoring their marketing messages to each segment, the company could effectively communicate the value proposition of the XYZPhone to their target audience.Marketing Communication:Company X developed a comprehensive marketing communication plan to raise awareness and generate interest in the XYZPhone. They utilized various channels, including social media, television advertisements, and influencer collaborations, to reach their target market. This multichannel approach allowed the company to create a buzz around the new product and engage with potential customers directly.Social Media Campaign:Recognizing the power of social media in reaching a wide audience, Company X launched a carefully crafted social media campaign. They created visually appealing content that showcased the key features of the XYZPhone, along with testimonials from satisfied customers. The company also encouraged user-generated content by running contests and giveaways related to the product. This not only generated excitement but also created a sense of community around the brand.Partnerships:To expand their reach and credibility, Company X formed strategic partnerships with renowned technology retailers and collaborated with popular tech bloggers and influencers. These partnerships helped increase the visibility of the XYZPhone and provided opportunities for potential customers to experience the product firsthand through in-store demos and product reviews.Sales Promotions:To incentivize potential buyers and stimulate sales, Company X introduced limited-time offers and discounts. They also developed exclusive bundles that included accessories and services with the purchase of the XYZPhone. These sales promotions not only attracted price-conscious customers but also added value to the overall product offering.Results:By implementing this comprehensive product marketing strategy, Company X successfully increased brand recognition and market share for the XYZPhone. Their targeted approach, engaging marketing communication, and strategic partnerships resulted in a significant increase in sales and a positive brand image. Conclusion:This case study demonstrates the importance of a well-designed product marketing strategy in achieving business objectives. Through effective product positioning, market segmentation, targeted marketing communications, and strategic partnerships, Company X was able to successfully differentiate their product in a competitive market and achieve their desired results.。

Case study report

Case study reportTable PageExecutive Summary (2)1. Introduction (2)2. Discussion (2)2.1. Make changes in the communication process (2)2.2 Care about the effective information (4)2.3. Overcoming the barriers to effective interpersonalcommunication (5) 3. Conclusion (6)References (6)Executive SummaryCommunication in management is defined in understandable information, ideas and feelings of two or more persons in the population of the process of transfer or exchange, the entire management of the work and communication. Communication is the transfer and understanding of meaning. Communication acts to control member behavior in several ways. In this case, we will see how the CEO deals with many problems by communicating with his stakeholders and gains a new reputation for cooperation throughout the world.1. IntroductionWhen Douglas Daft became CEO of Coca-Cola, the company was in trouble. Because of a series of problems, the government, the customers and some other competitors were unsatisfied with the Coca-Cola and the internal of company was arguing in different opinions and levels. Then Daft took a series of measures to solve problems. Through the process , the whole staff recognized that the importance of the right ways to communicate with top managers, government regulators, customers and use the right ways to communicate with others and absorb other opinions to solve problem. And we can know that communication skills alone do not make a successful manager. However, ineffective communication skills can lead to a continuous stream of problems for a manager. 2. Discussion2.1. Make changes in the communication processCoca-Cola was in trouble. The previous year, European Union regulators had raided the European offices of Coca-Cola and its bottlers and leveled serious anticompetitive charges against the venerable soft-drink marketer. That same year, the company was hurt by negative publicity when hundreds of people in Belgium complained of headaches and nausea after drinking Coca-Cola beverages. Faced with these circumstances, top managers’slow response lead to some company executives that they departed from tradition and submitted a confidential memo criticizing Coca-Cola’s actions. We can see that because of the top managers’ slow response to their stakeholders, they were unsatisfied. To complicate matters, worldwide sales were slowing due to economic was in some countries, employee morale was lower, and the stock price was lagging. How could these happen? We will discuss from the communication process.2.1.1. The message senderIn this process, the message senders are the stakeholders, the European Unionregulators, the customers of Belgium and some other competitors. They are sending a common message to the Coca-Cola Company: Your company and your drink appeared a series of problems. We are unsatisfied with you! They expressed their attitudes to the Coca-Cola Company.2.1.2. The receiverThe receivers of this communication process are the top managers of Coca-Cola Company. In my opinion, the top managers should always concern about more information and reports about their company that how the government ,the customers, and the competitors to evaluate them and they should always know more about latest market information in order to take full preparation for receiving challenges and the change of market. And once some problem accrued, top managers should respond as fast as they can to solve the problem.2.1.3.The process of decodingThe receiver must be skillful in reading or listing. In the process of communicating with stakeholder relationships, Daft asked what the company had done wrong and paid close attention as the regulator spoke his mind. In this way, Daft not only got a better understanding of their customers’needs, but also made better decisions to change the situation.2.1.4.The channelManagers need to recognize that certain channels are more appropriate for certain messages. It is very important to choose a right method to communicate with their stakeholder relationships. Daft used the method of goodwill tour to meet with the regulator who had pursued antitrust charges against Coca-Cola the year before. Daft also met with Italy’s top antitrust regulator who had presided over an investigation that resulted in Coca-Cola paying a $16 million fine for anticompetitive practices. Daft also directed to top Coca-Cola executive in Europe to find ways of working more closely with regulators, smoothing the way for business practices that to fit both the company’s goals and the European Union’s competitive guidelines. The goodwill tour in clouded meetings and meals with local Coca-Cola managers, the U.S. ambassador to France, several CEOs of French firms, and numerous Coca-Cola executives around Europe. In this face-to-face and internal and external communication, the CEO can listen others’ minds directly and it is very helpful to make better decisions.Of course, face-to-face conversation is the best way to communicate with stakeholders. There are some other methods to get more knowledge of the stakeholders’minds. For example, Daft can also always concerning about the markets’development via sending E-mails to his executive in Europe markets, telephone calls and Internet searching. Or he could send some of his top managers to Europe to participate in managing the local business and send the latest message or information to their CEO in time. In varieties of channel, Daft and his top managers could know more about the sales condition of their products.Otherwise, always keep the lines of communication open is required.2.1.5. The feedback loopFeedback returns the message to the sender and provides a check on whether understanding has been achieved. When the European Union regulators, the customers in Belgium and some other competitors against the Coca-Cola Company, top management’s slow response led to a more serious result. Facing to this circumstance, the managers should find out the way to solve problems and speed up decision making in time and keep the lines of communication open to give their stakeholders a satisfied answer.From the process of this communication. We know that when the stakeholders or the message senders come up with the problems, the receivers or managers should make reflection in time and choose a right channel to listen their minds via face-to-face conversation, oral presentations and contact with many people who are inside and outside the organization. Then find out the right methods to solve problem and give their stakeholders and their own employees a satisfied feedback.2.2 Care about the effective informationAn Information is communicated up though organizational levels it is condensed and synthesized by senders so these on top do not became overloaded with information. Those doing the condensing filter communications through their personal interests and perceptions of what is important. And the more vertical levels there are in an organization, the more opportunities there are for filtering.In the case , Daft bring some of his senior U.S. and European managers together to hear reports on regional results and initiatives, rather than asking them to share written reports. Which means that, the written reports would be filtered if Daft didn’t bring his managers to hear reports, just asked them to share written reports. Maybe Daft would deleted some information that he thought which is not important though his own interests. Then the reports would send to the next level though some other managers’ delete. So fewer and fewer useful information could be stayed up and their employees would not know about the true information. It’s harmful to the development of the company. In order to let the managers could get full knowledge of the whole information by themselves directly and effetely, Daft must bring his senior U.S. and European managers together in Europe to hear reports. It’s very meaningful to make decisions. So, make sure that the whole information and effective information is very important to the process of sending message from high level to the bottom. And it’s useful to the development of the company.2.3. Overcoming the barriers to effective interpersonalcommunication2.3.1. Use feedback loopFirst, he used feedback to his stakeholders. Since his initial goodwill tour, Dafthas return to Europe several times to meet with managers, bottlers, and regulators. To meet with the local managers, Daft could tell them the latest development of his company and he could also to exchange opinions with them and give them a feedback. And it could let them to know whether their minds or advise were effective.Second, after Daft brought his own managers to hear reports in Europe, those top managers were also use the feedback loop to Daft. In line with Daft’s preference for direct communication, oral presentations are shorter, more to the point, and heavier on recommendations. The top managers were also speeding up decision making, allowing Coca-Cola to bring new products and existing markets much faster than before. It means the top managers can understand his means and put in into actions. So actions can speak louder than words.2.3.2. Listen activelyActive listening is listening for full meaning without making premature judgments or interpretations demands total concentration. When his company was involved in an argument, he said that the company had to stop arguing and start listening when competing in other countries. So he listened intently as the regulator explained his reasoning and spoke against the company’s highly aggressive behavior. Then he went to Europe to meet with managers, butters, and regulators and listened to their opinions and advises actively. By listening to many people inside and outside the organization, Daft was developing a more rounded picture of Coca-Cola’s strengths and weaknesses.2.3.3. Constrain emotionsWe know that emotions can severely cloud and distort the transference of meaning. When the Coca-Cola Company was in crisis, some of the internal managers were in different attitudes. Daft said the company had to stop arguing and start listening to others. Yes, they should control their emotions to keep clam and think it over. Only in this way could they analyze the reality and correct what they did wrong.3. 3.4. The different rulesCultural differences can affect the way a manager chooses to communicate. And these differences undoubtedly can be a barrier to effective communication if not recognized and taken into consideration. In the case, Daft met with local managers, bottlers, and regulators and got a better understanding of local rules.On the basis of the local rules, Daft made some decision to fit in with the needs of the Europe markets in order to fit for customers to the best of his ability.In the company, he kept clam and analyzed the current situation. In Daft’s goodwill tour, he met with stakeholders and listened his stakeholders’advises actively. And he understood more about local rules. After that, he corrected the insufficient section and kept in touch with his customers and gave them a feedback. So he came over some barriers to communication during his goodwill tour and gained a new reputation for cooperation throughout the world.3. ConclusionIn the communication process, a sender initiates a message to a receiver. Then the message is received by the sender through a channel. The receiver will get the meaning of the message and give the sender a feedback after deal with it. In the case, Daft’s communication process with his stakeholders show us the way to communication and how to come over barriers to effective interpersonal communication. So we should also develop our own communication skills. References1.Zhang Xiaoqing《By enterprise's management communication》 May 20072.Philip Kotler 《Management communication principle and practice》March 2008 .3.Liu Guangyou《Manager personnel's management communication and trendof development》, April 20024.J.Scanlon “ Woman of substance” Wired, July 2002 p.275.E.Wenger, R.McDermott and W. Snyder,Cultivating Communicates ofPractice: A Guide to Managing Knowledge p.46.Deng Hung《Jan discusses in the enterprise culture construction the Trans-Culture communication and the fusion》 June 20047. H.Dolazalek “Collaborating in cyber-space” April 2003 p.278. D.K.Berio, The Process of Communication(New York: Holt,Rinehart&Winston,1996) p.30。

高级商务英语词汇

高级商务英语词汇call on v. 呼吁,约请,拜访campaign 战役,运动candidate n.求职者,候选人canteen n. 食堂canvass v. 征求意见,劝说capacity n. 生产额,(最大)产量caption n. 照片或图片下的简短说明capital n. 资本,资金capture v. 赢得cash n. 现金,现付款v. 兑现cash flow n. 现金流量case study n. 案例分析catalogue n. 目录,产品目录catastrophe n. 大灾难,大祸CEO n. Chief Executive Officer(美)总经理chain n. 连锁店challenger n.挑战者channel n.(商品流通的)渠道charge n. 使承担,要(价),把……记入(账册等)chart n. 图表checkout n.付款台chief adj. 主要的,首席的,总的CIF, c.i.f.成本保险费加运费circular n.传阅的小册子(传单等)circulate v.传阅claim n./v.要求,索赔client n.委托人,顾客cold adj. 没人找上门来的,生意清淡的_ommitment n.承诺concentratedmarketing n. 集中营销策略condition n.条件,状况_onfiguration n.设备的结构、组合conflict n. 冲突,争论_onglomerate n. 综合商社,多元化集团公司_onsolidate v. 帐目合并_onsortium n.财团constant adj. 恒定的,不断的,经常的consumables n.消耗品consumer durables n.耐用消费品(如:洗衣机)consumer goods n.消费品,生活资料_ontingency n. 意外事件continuum n.连续时间contract n. 合同,契约contractor n.承办商,承建人contribute v. 提供,捐献contribution n贡献,捐献,税conversion n. 改装,改造conveyor n. 运送,传递,转让cost n. 成本fixed costs固定成本running costs 日常管理费用variable costs可变成本cost-effectiveadj. 合算的,有效益的costingn.成本计算,成本会计creditn.赊购,赊购制度credit control赊销管理(检查顾客及时付款的体系)letter of credit信用证credit limit赊销限额credit rating 信贷的信用等级,信誉评价creditor n.债权人,贷方_reditworthiness n.信贷价值,信贷信用crisis n.危机,转折点critical adj. 关键的_riticalpath analysis n. 关键途径分析法currency n.货币,流通current adj. 通用的,现行的Current account 往来帐户,活期(存款)户current assets n.流动资产current liabilitiesn. 流动负债customise v. 按顾客的具体要求制造(或改造等);顾客化cut-throat adj. 残酷的,激烈的cut-price a. 削价(出售)的CV(=curriculum vitae)n.简历,履历transition noun 转变,转换,过渡volunteer noun 志愿者/兵ageism noun 对老年人的歧视alleviate verb 使(痛苦等)易于忍受,减轻aptitude noun 能力,才能slot noun 人/事物安排的位置或时间from scratch 从零开始,从无到有,白手起家jump at phrasal verb 欣然接受recession noun 工商业之萧条/不景气recruit verb 征募新兵/吸收新成员arbitrary adjective 任意的,武断的blanket adjective 包括一切情形或种类的,总括的,综合的creed noun 信条criminology noun 犯罪学,刑事学culprit noun 犯人CV UK noun = curriculum vitae个人简历discriminate verb 歧视,区别待遇dynamic adjective 动力的,精力充沛的,有力的,动态的guilt noun 罪行,内疚high-flyer noun 抱负极高的人,有野心的人irrespective adjective 不顾的,不考虑的,无关的lag verb 落后于,滞后obsessed adjective 着迷/牵挂/困扰的oppress verb 压迫,压抑pressing adjective 紧迫的prevalent adjective 普遍的,流行的résumé noun 个人简历rot verb 腐烂/败set in phrasal verb (指雨、坏天气、感染等)开始并可能继续下去sliding scale noun 滑动费率,滑动折算制steady adjective 稳固的,稳定的strenuous adjective 精力充沛的,干劲十足的,必须努力的corridor noun 走廊interviewer noun 主持面试者,采访者panel noun 座谈小组,陪审团promising adjective 有希望的,有前途的short list noun 决选名单bonus noun 奖金,红利eligible adjective 合格的/有恰当资格的the nitty-gritty noun informal 基本事实,实情.高级商务英语高频词汇:商务会议及谈判篇三1、adjourn 暂时;休会;延期2、agreement 同意;协定3、amendment 修正4、approval 赞成;同意5、attentive 注意的;留心的专心的6、board 理事会;委员会;董事会7、brainstorm 脑力激荡,集思广益8、concede 容忍;容许;让步9、conference 会议;协商;讨论会10、convention 惯例;常规;习俗;会议;11、convince 使信服12、cross-reference 前后参照;(使)前后参照13、delegate 代表14、demand 要求;强求15、dispute 争端;争执;纠纷;16、negotiation 协商;谈判17、persuade 说服;劝服18、postpone 延迟;延期19、reconcile 调和;调解20、settlement 协议;支付Business Meeting & Negotiation 商务会议及谈判(2)21、agenda 议程22、alternative 可供选择的事物、方式等23、announce 通告;宣布;宣告;公诸于众24、articulate 能清楚有力表达思想感情的;表达能力强的25、attorney 律师26、breakthrough 突破;重大进展28、conclusive 决定性的;勿庸置疑的29、consensus 一致的意见;共识30、converse 谈话;交谈31、criterion 规范;标准32、decline 衰落;衰退;下降33、demonstration 示范;实证;(游行)示威34、diplomacy 外交手腕;交际手段35、dissuade 劝阻36、on behalf of 代表37、petition 请愿(书);请愿38、premise 前提39、seminar 研讨会;讨论课;讲习会40、statement 声明;陈述gap n. 缺口,空隙_earing n. 配称(即定息债务与股份资本之间的比率)_immick n. 好主意,好点子goal n. 目标going adj. 进行的,运转中的going rate n. 产品的市场价格goods n. 货物,商品goodwill n. 声誉_o public v. 首次公开发行股票grapple with v. 与……搏斗,尽力解决grievance n. 申诉,抱怨gross adj. 总的,毛的gross margin n. 毛利率gross profit n. 毛利gross yield n. 毛收益gradually adv. 逐渐地group n. (由若干公司联合而成的)集团grow v. 增长,扩大growth n. 增长,发展guarantee n. 保证,保单guidelines n. 指导方针,准则board noun 懂事会,理事会array noun 排列,编队asset noun资产/有价值的技能、人branch office noun 分店,支店civil engineering noun 土木工程cornerstone noun 奠基石,基础corporation noun 公司,企业decade noun 十年join verb 参加,加入pension scheme noun 养老金计划或方案trade union (US labor union) noun 工会aerospace adjective/noun 航空航天空间,航空航天技术(的) beverage noun 饮料chart noun 图表electronics noun 电子学sector noun 部门/经济领域supply verb 供给,提供tertiary adjective 第三的fiscal year noun 财政年度/会计年度fledgling firm noun新公司/无经验的公司found verb 建立,创办innovative adjective 创新的/革新的link noun 连接(物)location noun 位置,场所maintain verb 维持,保养milestone noun 里程碑,转折点numerous adjective 许多的,无数的railroad = railway noun 铁路spearhead verb 领先/充当先锋turn of the century 世纪之交versatile adjective 万能的/多才多艺的zest noun 强烈的兴趣、热情damages n.损害,损失deadline n. 最后期限deal n. 营业协议,数量v. 交易dealer n. 商人debit n. 借方,欠的钱v.记入帐户的借方debt n. 欠款,债务to get into debt 负债to be out of debt 不欠债to pay off a debt还清债务debtor n.债务人aged debtors 长期债务人declare v.申报,声明decline n./v. 衰退,缓慢,下降decrease v. 减少deduct v.扣除,减去default n. 违约,未履行defect n. 缺陷defectiveadj有缺点的defer v. 推迟deferred payments n. 延期支付deficit n. 赤字delivery cycle n.交货周期_emand management n.需求规化demotivated adj. 消极的,冷谈的deposit n. 储蓄,预付(定金)depot n. 仓库depreciatev.贬值,(对资产)折旧depressingadj. 令人沮丧的deputy n. 代理人,副职,代理devalue v. 货币贬值(相对于其它货币)diet n. 饮食,食物,特种饮食differentiation n. 区分,鉴别dimensions n. 尺寸,面积,规模direct v管理,指导director n.经理,主管Managing Director n.总经理direct costn. 直接成本direct mailn.(商店为招揽生意而向人们投寄的)直接邮件direct sellingn.直销,直接销售directory n.指南,号码簿discount n.折扣,贴现dismiss v.让……离开,打发走dismissal n. 打发走dispatch n./v. 调遣display n./v. 展出,显示dispose v.安排,处理(事务)dispose of 去掉,清除distribution n分配,分发,分送产品_iversify v.从事多种经营;多样化divest v.剥夺dividend n. 股息,红利,年息division n. 部门_og n. 滞销品down-market a./ad.低档商品的n. 设备闲置期DP(=Data Processing)n. 计算机数据处理,计算机数据处理部门dramaticadj. 戏剧性的drive积极性,能动due adj. 应付的,预期的dynamic 有活力的earnings n. 工资efficiency n. 效率endorse v.背书,接受engage v. 雇用entitle v. 授权entitlement n.应得的权利holiday entitlementn. 休假权equity n.股东权益equity capital股本equities 普通股,股estimated demandn.估计需求evaluate v. 估价,评价eventual adj.最终exaggerate v. 夸张exceed v. 超过exhibit n.展览,表现expendituren花费,支出额expensen.费用,支出expense account n. 费用帐户expenses n.费用,业务津贴expertise n.专长,专门知识和技能_xposure n.公众对其中一产品或公司的知悉;广告所达到的观众总数facilities n.用于生产的设备、器材facilities layout n.设备的布局规化、计划facilities locationn.设备安置_actoringn.折价购买债券_ail-safe system n.安全系统feasibility study n.可行性研究feedback n. 反馈,反馈的信息field n.办公室外边,具体业务file n. 文件集,卷宗,档案,文件v. 把文件(或资料)归档fill v. 充任finance n. 资金,财政v. 提供资金financial adj. 财政的financing n. 提供资金,筹借资金finished goods n. 制成品firm n. 公司fire v. 解雇fix v. 确定,使固定在fix up v. 解决,商妥fiscal adj. 国库的,财政的_lagship n. 同类中最成功的商品,佼佼者flexible adj. 有弹性的,灵活的flier(=flyer) n. 促销传单float v. 发行股票flop n. 失败flow shop n. 车间fluctuate v. 波动,涨落,起伏FOB, f.o.b n. 离岸价_ollow-up n. 细节落实,接连要做的事forecast v. 预测four P''s 指产品PRODUCT、价格PRICE、地点PLACE、促销PROMOTION framework n. 框架,结构_ranchise n. 特许经销权v.特许经销,给予特许经销权franchisee n. 特许经营人franchiser n.授予特许经营权者fraud n. 欺骗_reebie n. (非正式的)赠品,免费促销的商品freelance n.& adj. 自由职业者(的)funds n. 资金,基金futures n. 期货交易。

Case study 及参考答案

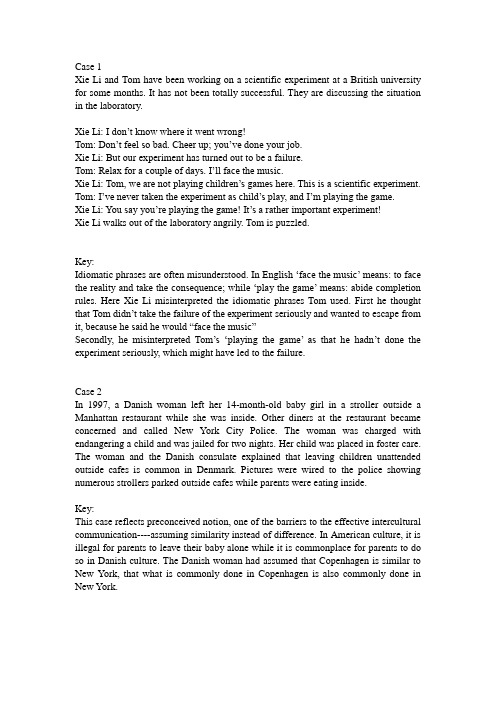

Case 1Xie Li and Tom have been working on a scientific experiment at a British university for some months. It has not been totally successful. They are discussing the situation in the laboratory.Xie Li: I don‟t know where it went wrong!Tom: Don‟t feel so bad. Cheer up; you‟ve done your job.Xie Li: But our experiment has turned out to be a failure.Tom: Relax for a couple of days. I‟ll face the music.Xie Li: Tom, we are not playing children‟s games here. This is a scientific experiment. Tom: I‟ve never taken the experiment as child‟s play, and I‟m playing the game.Xie Li: You say you‟re playing the game! It‟s a rather important experiment!Xie Li walks out of the laboratory angrily. Tom is puzzled.Key:Idiomatic phrases are often misunderstood. In E nglish …face the music‟ means: to face the reality and take the consequence; while …play the game‟ means: abide completion rules. Here Xie Li misinterpreted the idiomatic phrases Tom used. First he thought that Tom didn‟t take the failure of the experiment seriously and wanted to escape from it, because he said he would “face the music”Secondly, he misinterpreted Tom‟s …playing the game‟ as that he hadn‟t done the experiment seriously, which might have led to the failure.Case 2In 1997, a Danish woman left her 14-month-old baby girl in a stroller outside a Manhattan restaurant while she was inside. Other diners at the restaurant became concerned and called New York City Police. The woman was charged with endangering a child and was jailed for two nights. Her child was placed in foster care. The woman and the Danish consulate explained that leaving children unattended outside cafes is common in Denmark. Pictures were wired to the police showing numerous strollers parked outside cafes while parents were eating inside.Key:This case reflects preconceived notion, one of the barriers to the effective intercultural communication----assuming similarity instead of difference. In American culture, it is illegal for parents to leave their baby alone while it is commonplace for parents to do so in Danish culture. The Danish woman had assumed that Copenhagen is similar to New York, that what is commonly done in Copenhagen is also commonly done in New York.Case 3Mr. Wang, the Chairman of Board of Directors of a Chinese firm, told a story on CCTV program "Dialogue" of how he once almost lost a valuable Canadian employee working for him in Vancouver. He emailed every day to the Canadian, inquiring for the index number he was most concerned about. To his great astonishment, his Canadian employee turned in his resignation after a week. Mr. Wang was puzzled how he could do that to him as he gave such great attention to his job.Key:The resignation of Canadian employee resulted from the communication barrier due to the preconception of Mr. Wang, the Chairman of Board of Directors. Mr. Wang assumed unconsciously that the Canadian was more similar to his Chinese employees than he actually was and treated him just as he treated any Chinese employee. A Chinese employee would have been more than happy if his or her boss had showed such great concern for him or her. But Mr. Wang found out that, unlike Chinese employees, the Canadian took what meant great concern to Chinese as distrust.。

英文营销案例

英文营销案例Marketing Case Study。

In today's competitive business environment, effective marketing strategies are crucial for the success of any company. In this case study, we will examine three successful English marketing campaigns and analyze the key factors that contributed to their success.The first case study is the "Share a Coke" campaign launched by Coca-Cola. This innovative campaign involved replacing the Coca-Cola logo on bottles with popular names and encouraging consumers to share a Coke with friends and family. The campaign was a huge success, as it not only increased sales but also generated significant buzz on social media. The key to the success of this campaign was its personalization and the emotional connection it created with consumers. By associating the brand with the act of sharing and personalization, Coca-Cola was able to create a strong bond with its customers.The second case study is the "Dove Real Beauty Sketches" campaign. Dove, a personal care brand, created a powerful marketing campaign that challenged the conventional standards of beauty. The campaign featured a forensic artist who drew sketches of women based on their own descriptions and then based on the descriptions of others. The results revealed that women were often overly critical of their own appearance. This emotional and thought-provoking campaign not only went viral but also sparked important conversations about self-esteem and body image. The key to the success of this campaign was its ability to resonate with the target audience on a deep emotional level, leading to increased brand loyalty and positive brand perception.The third case study is the "Old Spice Man" campaign. Old Spice, a men's grooming brand, rebranded itself with a series of humorous and over-the-top commercials featuring the "Old Spice Man." These commercials quickly became viral sensations and helped the brand appeal to a younger audience. The key to the success of this campaign was its ability to create a memorable and entertaining brand image that resonated with the targetdemographic. By using humor and creativity, Old Spice was able to differentiate itself from competitors and increase brand awareness.In conclusion, these case studies demonstrate the power of effective English marketing campaigns. By creating personalized, emotional, and entertaining content, these brands were able to connect with their target audience and achieve remarkable results. These successful campaigns serve as valuable examples for businesses looking to elevate their marketing strategies and stand out in today's competitive market.。

作业成本法在我国的发展应用研究

作业成本法在我国的发展应用研究一、本文概述Overview of this article随着经济的发展和科技的进步,企业的生产方式和管理模式都在发生深刻的变化。

作业成本法(Activity-Based Costing,简称ABC)作为一种先进的成本管理方法,自上世纪80年代末期引入我国以来,已经在许多企业中得到了广泛的应用。

本文旨在深入探讨作业成本法在我国的发展应用情况,分析其在实际应用中的优势、挑战及改进策略,以期为我国企业的成本管理提供有益的参考和借鉴。

With the development of the economy and the advancement of technology, the production methods and management models of enterprises are undergoing profound changes. Activity Based Costing (ABC), as an advanced cost management method, has been widely applied in many enterprises since its introduction to China in the late 1980s. This article aims to explore the development and application of activity-based costing in China, analyze its advantages, challenges, and improvement strategies in practical application, in order to provide useful referenceand inspiration for cost management in Chinese enterprises.本文将回顾作业成本法的发展历程和基本原理,介绍其在国际上的应用情况和成功经验。

unit 7 case study

Case studyBackgroundYou are members of the Customer Services Department of Hermes communications, a telecommunications company based in Switzerland. You sometimes receive correspondence, telephone calls and voicemail messages from customers who are unhappy with the products or service of your company. You have to deal diplomatically and effectively with these dissatisfied customers and to come up with solutions to their problems.Complaint 1I’m writing to you because I’ve been trying to get through to your helpline unsuccessfully for the past three days. I’ve called at various times of the day and night and never get through. I wish to query something on my monthly bill. Is there any point having a helpline if it’s always busy?I intend to visit you next week to discuss this in person at your regional office.Complaint 2I’m writing to complaint about the mobile phone I bought from you amonth ago. I chose it because it had a big screen, much bigger than most models. Unfortunately, the battery loses power very quickly. I think this is due to the large screen size and I have heard about other people with the same model and the same problem. There is clearly a design fault.I would like to know what you are going to do about this situation. I paida lot of money for the phone, but it’s causing me a lot of problems.Complaint 3I am writing to complain about your terrible customer service. I topped up my phone using my credit card on two occasions (£20 each time), however the amoun t wasn’t credited to my account. It’s not so much the loss of £40 which upsets me. I’m sure I’ll get it back. But my phone didn’t work when I needed it to make an urgent call to an important client. This is not the sort of service I expected from a company as well known as yours. I’d like to know how you’re going to compensate me.Complaint 4I became a subscriber to your service because you promised six months of cheap-rate calls to the US, where my daughter lives at present. So imagine my horror to find this service withdrawn, with no explanation from you, after only three months. Then you wrote to me asking for anextra £30 a month to maintain the previous level of service. I find this absolutely outrageous.Complaint 5As a mobile phone user and subscriber with your network for the past 5 years, I have been very pleased with the level of service provided.However, recently, I’ve been experiencing headaches. After visiting my doctor, he informed me that this could be due to mobile phone use. As I am in sales and travel a lot, I am not previously aware of any health risk associated with mobile phones and am now very concerned about the long-term health risks of prolonged exposure to microwave radiation.I’ve heard of other cases like mine and therefore I would like to know what your company is doing about this problem.I look forward to hearing your comments with interest.Yours sincerely,Katherine SandsRequirement:Discuss with your group members the problems that customers have experienced and make recommendations for improving the service to customers.。

Assignments of case studies

Case study 1 of MarketingAnalyzing the following example with the opinion: the company can motivate distributors, retailers, and other intermediaries to pass along important intelligence. (Combine with the aspects: Analyzing Marketing Opportunities. Gathering Information and Measuring Market Demand)Successful companies take an outside-inside view of their business. They recognize that the marketing environment is constantly spinning new opportunities and threats and understand the importance of continuously monitoring and adapting to that environment. One company that has continually reinvented one of its brands to keep up with the changing marketing environment is Mattel with its Barbie doll:■Mattel Mattel’s genius is in keeping its Barbie doll both timeless and trendy. Since Barbie’s creation in 1959, the doll has filled a fundamental need that all girls share: to play a grown-up. Yet Barbie has changed as girls’ dreams have changed. Her aspirations have evolved from jobs like “stewardess,” “fashion model,” and “nurse,”to “astronaut,” “rock singer,” and “presidential candidate.” Mattel introduces new Barbie dolls every year in order to keep up with the latest definitions of achievement, glamour, romance, adventure, and nurturing. Barbie also reflects Am erica’s diverse population. Mattel has produced African AmericanBarbie dolls since 1968—the time of the civil rights movement—and the company has introduced Hispanic and Asian dolls as well. In recent years, Mattel has introduced the Crystal Barbie doll (a gorgeous glamour doll), Puerto Rican Barbie (part of its “dolls of the world” collection),Great Shape Barbie (to tie into the fitness craze), Flight Time Barbie (a pilot), and Troll and Baywatch Barbies (to tie into kids’ fads and TV shows). Industry analysts estimate that two Barbie dolls are sold every second and that the average American girl owns eight versions of Barbie. Every year since 1993, sales of the perky plastic doll have exceeded $1 billion.Case study2Use Ansoff growth matrix to analyze Starbucks on page 55Case study3—Consumer behaviorShiseido (资生堂): intent on being number oneLike most corporate president, Yoshiharu Fukuhara of Shiseido, Japan’s largest cosmetics manufacturer, wants his company to be number one. Unlike most corporate presidents, he does not define number one as being first in sales or profits, but rather as being number one in quality. He says, “We are talking about being number one in quality, number one in corporate image, and number one in service. That’s our goal.” To reach its goal of being the world’s largest manufacturer of cosmetics, Shiseidowill have to increase sales outside Japan for 9 percent to 25 percent. To do this, the company has its eye on the US where current market share is a tiny 1.3 percent or $59.5 million in sales.Understanding the US market and increasing market share will be the task of Hisako Nagashima. What is Ms. Nagashima’s first tactic in storming the US market? Change the name. “Although Shiseido is a treasured name for us with 125 years of history behind it,” she notes, “the name is unpronounceable for Americans and hard to remember.”Ms. Nagashima has put her finger on a serious problem for corporation operating in the global arena—the poor translation of a company’s heritage from one culture to another. In Japan, Shiseido was the first firm to introduce Western-style toothpaste in 1888 and first to open a soda fountain in 1902. The company developed its competitive advantage in the 1920s when it worked out a unique arrangement with retailers in which they aged to sell only Shiseido’s cosmetics on the conditions that Shiseido could repurchase any unsold cosmetics. Through this arrangement, Shiseido became both manufacturer and wholesaler. It developed a network of 25,000 Japanese retailers—about half of all of Japan’s cosmetics and pharmaceutical shops—that sold its products exclusively. As a result, Shiseido controlled distribution and developed a pricey image.Thus, Shiseido has a long history in Japan and a well-developedimage. But this history and image are difficult to communicate to Americans. Part of Shiseido’s challenge in the United States is the creation of an image that appeals to US buyers but is compatible with its image at home.. to accomplish this, Shiseido is relying on a scientific approach combined with a focus on inner or spiritual well-being. In fact, its corporate slogan is: “The science of beauty and well-being.” To back its scientific endeavors, Shiseido established the MGH/Harvard Cutaneous Biology Rearch Center in 1995 and purchased an R&D facility in Yokohoma. To focus on inner well-being, it established a new subsidiary with the mandate to define and develop values fron a worildwide perspective.The scientific focus is readily evident in the company’s packaging, promotional inserts, and sales pitch. Shiseido packages are different from the rounded, white jars reminiscent of Western cosmetics manufacturers. Package colors are frequently muted and containers are more rectangular. The insert in Shiseido’s Bio-Performance Advanced Super Revitalizer reads.A scienticfic Approach to Skin Aging: After years of intensive research in all aspects in all aspects of skin science, Shiseido Laborotories has achieved an extraordinary advance in protection against the visible signs of aging…… Bio-Performance Advanced Super Revitalizer features Bio-EPO and Bio-Hyaluronic Acid and a newimportant counound, HKC, all kept fresh in unique microcapsules.This differs dramatically from the traditional insert promising dewy, radiant skin with the elimination of wrinkles through magic ingredients! In fact, the scientific approach may seem cold in an industry characterized by romance, sex, and glamour.When customers approach the Shiseido counter, skin care consultants first determine the customer’s skin type—in some locations by photographing an area of skin. Of course, the photograph is greatly magnified so that customers can see how age has robbed their skin of its softness and clogged their pores—problems that Shiseido products can address. After several months, the customer returns to have her skin rephotographed so that she can see the improvement.Shiseido, however, believes that beauty is more than skin-deep. In its promotions, it asserts that Shiseido creates “products that make women feel beautiful inside and look beautiful outside” One way to achieve this sense of inner well-being is massage. Shiseido sells massage creams and urges the use of facial and hand massage for healing purposes, claiming that it helps to stimulate the body’s self-recovery capabilities.Will this scientific-cum-inner-well-being approach work with today’s consumers? Faith Popcorn, who studies marketplace trend, talks about vigilant consumers who want information, not promotion; who seek out information, not only about products but about companies as well.These are well-educated consumers who want to feel good about the principles of the companies from which they buy. These and other consumers are also interested in value. They carefully determine what they will get for their money and are willing to comparison shop on the basis of price. Although Shiseido’s scientific approach might appeal to these to these consumers’desire for information, its high prices might repel them. They might follow the lead of many consumers who look at the Shiseido counter but buy cheap substitutes elsewhere. However, the inner well-being approach may be in step with the times, as Americans emphasizes a return to basic values and less stressful lifestyles.In the past, cosmetics manufacturers have given free samples of products in order to get consumers to try and later purchase them. Ms. Nagashima, however, plans to eliminate the use of costly samples. However, no one knows how Americans might feel about not receiving samples. In additional to the scientific approach, Shiseifo emphasize customer responsiveness—listening to what the customer has to say. A case in point is its “Staying Power”lipstick, one of the earliest long-lasting lipsticks from an upscale company. “In the past two years,”says Fukurharu, “we made five different improvements to one of our lipsticks because, for example, some customers said it wiped off too easily, some said it made their lips feel a little dry…… These comments are essential……They allow us to maintain the highest standards ofquality and satisfaction” Shiseio also listens to customers through its Web site (www. ), which has generated 1.3 million hits in less than a year. A team of employees responds to each of these messages with several days.To help people of both genders grow old with style and sophistication, Shiseido is also introducing new products. A first step in this direction is its Bene-finance line. Introduced in 1996, the line promises advanced technology to soften and revitalize skin. Although other firms have talked about products to help consumers prevent aging, only Shiseido seems willing to talk about getting older. Its actions raise a serious question as to whether consumers want to grow old gracefully or whether they want to defy age and remain young looking. Will pitching cosmetics on the basis that they will help you age gracefully be a winning concept with Americans?Besides being little known, Shiseido also lack a well-known perfume brand. Although perfume does not sell well in Japan, it is a major contributor to American firm’s sales and profits. Many firms spend a disproportionate share of their advertising budgets on perfume, using the perfume as the basis of their images. Beautiful by Lauder is soft, feminine, and sensual rather than sexy. Calvin Klei n’s image is sexy while being neither male or female. As this example indicates, perfumes may also be a bridge to men’s cosmetics, which could be the main source of future salesgrowth for cosmetic. Because they are big sellers, companies frequently use perfumes to negotiate for space in department stores. Thus, they perform many important roles in the cosmetics manufacturer’s product assortment. Without a perfume, it will be hard for Shiseido to create and anchor the image that it wants in the United States—even if it does change its name.As for the name—pronounce it—“She-pay-doe.” But don’t worry if you can’t pronounce it. if the company follows Ms. Nagashima’s advice, Shiseido will be the corporate name, but the cosmetics will have a different brand name that could be one solution to the image problem.QuestionsHow do consumer s’cultural, social, personal, and psychological characteristics affect their cosmetics shopping behavior? How do these factors affect the way cosmetics executives view consumers? How are these factors changing?DirectionAnalyzing the following example with the opinion you’ve learned in Unit 7: the importance of brands, branding and brand experience.Watch the clip of the video: Disgusting employees at Domino's andanalyze it with the opinion learned in Unit 7.Domino's is the second largest pizza chain in the US. In April 2009, two employees at a Domino's Pizza store in North Carolina posted a YouTube video of themselves handling food inappropriately. The video got over one million hits within days; References to it were in five of the 12 results on the first page of Google search for “Dominos”. Domino's President Patrick Doyle immediately responded with a YouTube statement. The two employees were identified, arrested and fired.(Media Curves website survey on April 16, 2009)。

错误处理 物料估价不一致 主数据与物料帐价格不一致

物料估价不一致一、问题现象在查看物料的会计视图时,系统提示:物料估价33186066000在估价范围1100 内不一致。

当运行物料分类账CKMLCP、查看物料主数据MM03、物资出入库MIGO时,系统提示:C+048物料XXXX估价在估价范围XXXX不一致时,你需要运行事务码:CKMC 来检查物料主数据与物料账之间的一致性。

对于不一致的数据,可以使用事务码:CKMREP来修改数据。

对于测试系统,也可以强行修改:CKMLPR/CKMLPP/CKMLCR来解决“帮助”文档显示:期初上线物料主数据导入的期间有个默认期间,需要调整与实际上线期间一致,不行的话冲1月开始关闭物料期间直到上线启动月份点击“进行”,系统会引导进入CKMC的程序界面:执行后,系统显示:将光标置于33186066000这一行,点击“数据比较”按钮,系统显示如下:从图中可以看出,该物料在主记录上的价格和物料分类帐中的价格不一致,二者的差为569.57元,正是在前一界面上显示的结果。

在前一界面点击“业务”,系统显示:二、问题分析在物料主数据中,此处显示的价格是138.937,和物料分类帐中的价格一致:12月份的这个价格是什么时候变化的呢?查看物料凭证,可以发现,这个价格是在12/01做了一笔生产订单的收货后发生变化的。

会计凭证:物料分类帐凭证之一——价格修改:记录创建信息:物料分类帐凭证之二——物料分类帐更新:查看创建信息:由两条记录紧密相连的创建记录时间可以发现:正是由于在12/01做了一次收货,导致物料的价格发生更新。

进一步考虑,这个价格怎么得来的呢?在ck40n中发现,2005/11/29对这个物料进行了一次成本估算(成本核算名称为TEST)。

当时对这个物料估算出新的成本为138.937。

当时只是成功做了标记,标记在2005年12月。

由于12月份尚未到来,发布没有成功(发布太早)。

但是,标记的成本在2005年12月份的第一笔事务上被调用到了,并被发布出来。

Case Study (2)

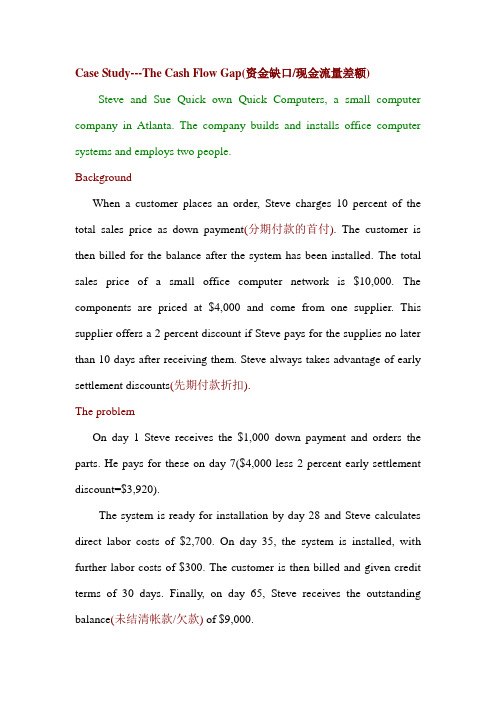

Case Study---The Cash Flow Gap(资金缺口/现金流量差额) Steve and Sue Quick own Quick Computers, a small computer company in Atlanta. The company builds and installs office computer systems and employs two people.BackgroundWhen a customer places an order, Steve charges 10 percent of the total sales price as down payment(分期付款的首付). The customer is then billed for the balance after the system has been installed. The total sales price of a small office computer network is $10,000. The components are priced at $4,000 and come from one supplier. This supplier offers a 2 percent discount if Steve pays for the supplies no later than 10 days after receiving them. Steve always takes advantage of early settlement discounts(先期付款折扣).The problemOn day 1 Steve receives the $1,000 down payment and orders the parts. He pays for these on day 7($4,000 less 2 percent early settlement discount=$3,920).The system is ready for installation by day 28 and Steve calculates direct labor costs of $2,700. On day 35, the system is installed, with further labor costs of $300. The customer is then billed and given credit terms of 30 days. Finally, on day 65, Steve receives the outstanding balance(未结清帐款/欠款) of $9,000.The cash flow gap opens on day 7 when Steve pays for the supplies; it widen to $ A by day 35. This means he has to finance from bank, and possibly pay interest on $ A for 3o days until the customer pays the final $9,000.Questions:1.How much is the cash flow gap by day 35? (How much is A?)2.If the interest rate of 30 days in all is 1 percent, how much does Quick Computers earn in this transaction after taking out all costs?3920-1000=29202920+2700+300=59205920*1%=59.29000-(5920+59.2)=3020.8。

case study creating a culture of customer care

Case StudyOutcome 1 and 2: Assessment Case StudyThe Mountain High Hotel ComplexAlice Hendry had recently been appointed as the General Manager of the Mountain High Hotel Complex. This was her first appointment to this level of management and she was very keen to make a success of the job. She was aware that her task would be very demanding but was confident that the experience that she had previously gained in a number of similar establishments would enable her to motivate the staff and soon have them all committed to working as an integrated team. She had been asked to prepare a report for the board of directors detailing how she planned to increase the level of business during the traditionally quieter Spring and Autumn months.The hotel complex had a number of distinct operations. There were 150 bedrooms, 2 restaurants, 2 bars and a night- club. In addition, there was also a sports fitness centre and swimming pool and the complex also managed its own sports shop that offered ski equipment sales/hire and lessons during the winter months and mountain bike sales/hire and guided tours in the summer months. The complex also owned and managed the mountain gondola and ski lifts. The gondola operated throughout the year for sightseers as well as being used by skiers in the winter and by mountain bikers in the summer.Although the Complex had a generally younger sporting clientele during the winter and summer months, Alice was aware that some efforts had previously been made to attract a different type of customer, particularly during the Spring and Autumn months when mountain biking and more particularly skiing were not available. It was apparent that little success had been made with these initiatives even though the hotel complex was undoubtedly equipped to cater for a more mature clientele. Alice had conducted some investigation into this apparent failure and was concerned to discover that while there had been some initial success in attracting a more middle- aged customer during theoff-season, there was little evidence of any re-booking.At the end of her first month in the job Alice called a meeting of all of the Complex’s supervisory staff to discuss her plans to improve the trading levels during the off-peak months of the year. She suggested that the complex needed to set up and market a number of activities that would be attractive to the more mature customer and that the staff would need to be flexible in their approach to their jobs. For example: The fitness centre could offer more sedate exercise programmes that would appeal to those who perhaps enjoyed walking in the countryside rather than the more dynamic needs of Skiers and Mountain Bikers. The sports shop could offer guided mountain tours withlow-level valley walks for the less adventurous and for times when the weather was inclement. Alice also felt that there may be a market for bird watching excursions during the Spring months as she was aware that the Mountain High Complex was located in an area where many rare species of summer visiting birds could be found, if you knew where to look. The night club could easily be used for ballroom and line dancing rather than the more brash ‘dance’ music enjoyed by younger ‘clubbers; Sh e then asked the staff if they had any ideas that could be considered. The responses were not what she had hoped. Robert who managed the sports shop was openly hostile. He took the view that it was his job to serve the customers with their needs for skis and bikes and that it certainly wasn’t up to him to go wandering round the mountains with groups of unfit old folk in the Spring and Autumn. In his opinion everyone knew that his staff worked hard enough for the skiers and bikers in the winter and spring and they felt entitled to be able to ‘take it easy’ during the off-peak months. His view seemed to be shared by most of the others. They all seemed to resent the idea that they would have to deal with a different type of client in the quieter months of the year.Alice reluctantly decided to ask the staff to take some time to think about her proposals and to meet back with her again in two weeks time. She was aware that the Board of Directors had asked her to submit her report and associated proposals within three months of her starting the job and that time was running out. However she knew that she could not succeed without the help of the staff and that somehow she needed to convince them of the value of her ideas.Informal discussions with a number of the staff helped to confirm what Alice was already beginning to suspect. The staff were generally very enthusiastic about their particular area of expertise but had no interest whatsoever in anything else. The sports shop was a good example. The staff was all young, fit and fully committed to their sport of skiing. They were all experts and spent their free time in the winter out on the slopes. While at work they were more than willing to share their enthusiasm for skiing with anyone who came into the shop but had little time for non- skiers. In the summer months they turned their attention to mountain biking in the same way. Much the same situations existed in the sports centre, swimming pool and bars/night club.Alice was of the opinion that the way forward was to promote a culture of customer care, for all customers, amongst the staff at the Mountain High Hotel Complex. She decided that she would make this the theme of her report to the Board of Directors. If she could convince them to support an extensive programme of Customer Care Training, then she was sure that ever- increasing numbers of customers could be encouraged to come to the complex and just as importantly, to come back again and again.。

《国际商务英语》词汇

《国际商务英语》串讲笔记Aabroad adv. 在国外,出国,广泛流传absence n. 缺席,离开absent adj. 不在,不参与absenteeism n. (经常性)旷工,旷职absorb v. 吸收,减轻(冲击、困难等)作用或影响abstract n. 摘要access n. 接近(或进入)的机会,享用权v. 获得使用计算机数据库的权利accommodation n. 设施,住宿account n. 会计帐目accountancy n. 会计工作accountant n. 会计accounts n. 往来帐目account for 解释,说明account executive n. (广告公司)客户经理*accruals n. 增值,应计achieve v. 获得或达到,实现,完成acknowledge v. 承认,告知已收到(某物),承认某人acquire v. 获得,得到*acquisition n. 收购,被收购的公司或股份acting adj. 代理的activity n. 业务类型actual adj. 实在的,实际的,确实的adapt v. 修改,适应adjust v. 整理,使适应administration n. 实施,经营,行政administer v. 管理,实施adopt v. 采纳,批准,挑选某人作候选人advertise v. 公布,做广告ad n. 做广告,登广告advertisement n. 出公告,做广告advertising n. 广告业after-sales service n. 售后服务agenda n. 议事日程agent n. 代理人,经纪人allocate v. 分配,配给amalgamation n. 合并,重组ambition n. 强烈的欲望,野心*amortise v. 摊还analyse v 分析,研究analysis n. 分析,分析结果的报告analyst n. 分析家,化验员annual adj. 每年的,按年度计算的annual general meeting (AGM)股东年会anticipate v. 期望anticipated adj. 期待的appeal n. 吸引力apply v. 申请,请求;应用,运用applicant n. 申请人application n. 申请,施用,实施appointee n. 被任命人appraisal n. 估量,估价appreciate v. 赏识,体谅,增值*appropriate v. 拨出(款项)approve v. 赞成,同意,批准aptitude n. 天资,才能*arbitrage n. 套利arbitration n. 仲裁*arrears n. 欠帐assemble v. 收集,集合assembly-line n. 装配线,流水作业线assess v. 评定,估价asset n. 资产current asset n. 流动资产fixed asset n. 固定资产frozen asset n. 冻结资产intangible assets n. 无形资产liquid assets n. 速动资产tangible assets n. 有形资产assist v. 援助,协助,出席audit n. 查账,审计automate v. 使某事物自动操作average n. 平均,平均水准awareness n. 意识;警觉Bbacking n. 财务支持,赞助backhander n. 贿赂*backlog n. 积压(工作或订货)bad debt 死账(无法收回的欠款)balance n. 收支差额,余额balance of payments n. 贸易支付差额balance sheet n. 资产负债表bankrupt adj. 破产的bankruptcy n. 破产bank statement n. 银行结算清单(给帐户的),银行对账单bar chart n. 条形图,柱状图bargain v. 谈判,讲价base n. 基地,根据地batch n. 一批,一组,一群batch production 批量生产bear market n. 熊市beat v. 超过,胜过behave v. 表现,运转behaviour n. 举止,行为,运转情况below-the-line advertising 线下广告,尚未被付款的广告benchmark n. 衡量标准benefit n. 利益,补助金,保险金得益fringe benefits n. 附加福利sickness benefit n. 疾病补助费bid n. 出价,投标takeover bid n. 盘进(一个公司)的出价bill n. 账单,票据billboard n. (路边)广告牌,招贴板black adj. 违法的in the black 有盈余,贷方black list 黑名单,禁止贸易的(货物、公司及个人)名单black Monday n. 黑色星期一,指1987年10月国际股票市场崩溃的日子blue chips n. 蓝筹股,绩优股blue-collar adj. 蓝领(工人)的Board of Directors n. 董事会Bond n. 债券bonus n. 津贴,红利books n. 公司帐目book value n. 账面价值,(公司或股票)净值bookkeeper n. 簿记员,记帐人boom n. 繁荣,暴涨boost v. 提高,增加,宣扬bottleneck n. 瓶颈,窄路,阻碍bottom adj. 最后的,根本的v. 到达底部,建立基础bounce v. 支票因签发人无钱而遭拒付并退回brainstorm n./v. 点子会议,献计献策,头脑风暴branch n. 分支,分部brand n. 商标,品牌brand leader n. 占市场最大份额的品牌,名牌brand loyalty n. (消费者)对品牌的忠实break even v. 收支相抵,不亏不盈break even point 收支相抵点,盈亏平衡点breakthrough n. 突破brief n. 摘要brochure n. 小册子broker n. 经纪人,代理人bull market 牛市budget n. 预算bulk n. 大量(货物)adj. 大量的bust adj. 破了产的buyout n. 买下全部产权CCAD(=Computer Aided Design)n. 计算机辅助设计call n. 打电话call on v. 呼吁,约请,拜访campaign n. 战役,运动candidate n. 求职者,候选人canteen n. 食堂canvass v. 征求意见,劝说capacity n. 生产额,(最大)产量caption n. 照片或图片下的简短说明capital n. 资本,资金capture v. 赢得cash n. 现金,现付款v. 兑现cash flow n. 现金流量case study n. 案例分析catalogue n. 目录,产品目录catastrophe n. 大灾难,大祸CEO n. Chief Executive Officer(美)总经理chain n. 连锁店challenger n. 挑战者channel n. (商品流通的)渠道charge n. 使承担,要(价),把……记入(账册等)chart n. 图表checkout n. 付款台chief adj. 主要的,首席的,总的CIF, c.i.f. 成本保险费加运费circular n. 传阅的小册子(传单等)circulate v. 传阅claim n./v. 要求,索赔client n. 委托人,顾客cold adj. 没人找上门来的,生意清淡的commercialise v. 使商品化commission n. 佣金*commitment n. 承诺commodity n. 商品,货物company n. 公司limited (liability)company (ltd.)股份有限公司public limited company (plc)n. 股票上市公司compensate v. 补偿,酬报compensation n. 补偿,酬金compete v. 比赛,竞争competition n. 比赛,竞争competitor n. 竞争者,对手competitive adj. 竞争性的component n. 机器元件、组件、部件,部分concentrated marketing n. 集中营销策略condition n. 条件,状况*configuration n. 设备的结构、组合conflict n. 冲突,争论*conglomerate n. 综合商社,多元化集团公司*consolidate v. 帐目合并*consortium n. 财团constant adj. 恒定的,不断的,经常的consultant n. 咨询人员,顾问,会诊医生consumables n. 消耗品consumer durables n. 耐用消费品(如:洗衣机)consumer goods n. 消费品,生活资料*contingency n. 意外事件continuum n. 连续时间contract n. 合同,契约contractor n. 承办商,承建人contribute v. 提供,捐献contribution n. 贡献,捐献,税conversion n. 改装,改造conveyor n. 运送,传递,转让core time n. (弹性工作制的)基本上班时间(员工于此段时间必须上班,弹性只对除此以外的时间有效)cost n. 成本fixed costs 固定成本running costs 日常管理费用variable costs 可变成本cost-effective adj. 合算的,有效益的costing n. 成本计算,成本会计credit n. 赊购,赊购制度credit control 赊销管理(检查顾客及时付款的体系)letter of credit 信用证credit limit 赊销限额credit rating 信贷的信用等级,信誉评价creditor n. 债权人,贷方*creditworthiness n. 信贷价值,信贷信用crisis n. 危机,转折点critical adj. 关键的*critical path analysis n. 关键途径分析法currency n. 货币,流通current adj. 通用的,现行的Current account 往来帐户,活期(存款)户current assets n. 流动资产current liabilities n. 流动负债customise v. 按顾客的具体要求制造(或改造等);顾客化cut-throat adj. 残酷的,激烈的cut-price a. 削价(出售)的CV(=curriculum vitae)n. 简历,履历*cycle time n. 循环时间Ddamages n. 损害,损失deadline n. 最后期限deal n. 营业协议,数量v. 交易dealer n. 商人debit n. 借方,欠的钱v. 记入帐户的借方debt n. 欠款,债务to get into debt 负债to be out of debt 不欠债to pay off a debt 还清债务debtor n. 债务人aged debtors 长期债务人declare v. 申报,声明decline n./v. 衰退,缓慢,下降decrease v. 减少deduct v. 扣除,减去default n. 违约,未履行defect n. 缺陷defective adj. 有缺点的defer v. 推迟deferred payments n. 延期支付deficit n. 赤字delivery cycle n. 交货周期*demand management n. 需求规化demotivated adj. 消极的,冷谈的deposit n. 储蓄,预付(定金)depot n. 仓库depreciate v. 贬值,(对资产)折旧depressing adj. 令人沮丧的deputy n. 代理人,副职,代理devalue v. 货币贬值(相对于其它货币)diet n. 饮食,食物,特种饮食differentiation n. 区分,鉴别dimensions n. 尺寸,面积,规模direct v 管理,指导director n. 经理,主管Managing Director n. 总经理direct cost n. 直接成本direct mail n. (商店为招揽生意而向人们投寄的)直接邮件direct selling n. 直销,直接销售directory n. 指南,号码簿discount n. 折扣,贴现dismiss v. 让……离开,打发走dismissal n. 打发走dispatch n./v. 调遣display n./v. 展出,显示dispose v. 安排,处理(事务)dispose of 去掉,清除distribution n. 分配,分发,分送产品*diversify v. 从事多种经营;多样化divest v. 剥夺dividend n. 股息,红利,年息division n. 部门*dog n. 滞销品down-market a./ad. 低档商品的*down-time/downtime n. 设备闲置期DP(=Data Processing)n. 计算机数据处理,计算机数据处理部门dramatic adj. 戏剧性的drive n. 积极性,能动性due adj. 应付的,预期的dynamic adj. 有活力的Eearnings n. 工资efficiency n. 效率endorse v. 背书,接受engage v. 雇用entitle v. 授权entitlement n. 应得的权利holiday entitlement n. 休假权equity n. 股东权益equity capital n. 股本equities 普通股,股票estimated demand n. 估计需求evaluate v. 估价,评价eventual adj. 最终的exaggerate v. 夸张exceed v. 超过exhibit n. 展览,表现expenditure n. 花费,支出额expense n. 费用,支出expense account n. 费用帐户expenses n. 费用,业务津贴expertise n. 专长,专门知识和技能*exposure n. 公众对某一产品或公司的知悉;广告所达到的观众总数Ffacilities n. 用于生产的设备、器材facilities layout n. 设备的布局规化、计划facilities location n. 设备安置*factoring n. 折价购买债券*fail-safe system n. 安全系统feasibility study n. 可行性研究feedback n. 反馈,反馈的信息field n. 办公室外边,具体业务file n. 文件集,卷宗,档案,文件v. 把文件(或资料)归档fill v. 充任finance n. 资金,财政v. 提供资金financial adj. 财政的financing n. 提供资金,筹借资金finished goods n. 制成品firm n. 公司fire v. 解雇fix v. 确定,使固定在fix up v. 解决,商妥fiscal adj. 国库的,财政的*flagship n. 同类中最成功的商品,佼佼者flexible adj. 有弹性的,灵活的flextime n. 弹性工作时间制flier(=flyer)n. 促销传单float v. 发行股票flop n. 失败flow shop n. 车间fluctuate v. 波动,涨落,起伏FOB, f.o.b n. 离岸价*follow-up n. 细节落实,接连要做的事forecast v. 预测four P's 指产品PRODUCT、价格PRICE、地点PLACE、促销PROMOTION framework n. 框架,结构*franchise n. 特许经销权v. 特许经销,给予特许经销权franchisee n. 特许经营人franchiser n. 授予特许经营权者fraud n. 欺骗*freebie n. (非正式的)赠品,免费促销的商品freelance n.& adj. 自由职业者(的)funds n. 资金,基金futures n. 期货交易Ggap n. 缺口,空隙*gearing n. 配称(即定息债务与股份资本之间的比率)*gimmick n. 好主意,好点子goal n. 目标going adj. 进行的,运转中的going rate n. 产品的市场价格goods n. 货物,商品goodwill n. 声誉*go public v. 首次公开发行股票grapple with v. 与……搏斗,尽力解决grievance n. 申诉,抱怨gross adj. 总的,毛的gross margin n. 毛利率gross profit n. 毛利gross yield n. 毛收益gradually adv. 逐渐地group n. (由若干公司联合而成的)集团grow v. 增长,扩大growth n. 增长,发展guarantee n. 保证,保单guidelines n. 指导方针,准则Hhand in v. 呈送hand in one's notice 递交辞呈handle v. 经营*hands on adj. 有直接经验的hard sell n. 强行推销hazard n. 危险,危害行为head n. 主管,负责health and safety n. 健康和安全*hedge n. 套期保值hidden adj. 隐藏的,不明显的hierarchy n. 等级制度,统治集团,领导层hire v. 雇用hire purchase n. 分期付款购物法hit v. 击中,到达holder n. 持有者holding company n. 控股公司hostile adj. 不友好的,恶意的HRD n. 人力资源发展部human resources n. 人力资源*hype n. 天花乱坠的(夸张)广告宣传Iimpact n. 冲击,强烈影响implement v. 实施,执行implication n 隐含意义incentive n. 刺激;鼓励income n. 工资或薪金收入,经营或投资的收入earned income 劳动收入,劳动所得unearned income 非劳动收入,投资所得increment v. 定期增加incur v 招致,承担*indemnity n. 偿还,赔偿index n. 指数,索引retail price index 零售价格指数indirect costs n. 间接成本induction n. 就职industrial adj. 工业的industrial action n. (罢工、怠工等)劳工行动industrial relations n. 劳资关系inefficiency n. 低效率,不称职inflate v. 抬高(物价),使通货等)膨胀inflation n. 通货膨胀*infringe v. 违法,违章initial adj. 初步的innovate v. 革新input n. 投入insolvent adj. 无清偿力的installment n. 部分,分期付款insure v. 给……保险,投保insurance n. 保险interest n. 利息,兴趣interest rate n. 利率interim n. 中期,过渡期间intermittent production n. 阶段性生产interview n./v. 面试interviewee n. 被面试的人interviewer n. 主持面试的人,招聘者introduce v. 介绍,提出*inventory n. 库存buffer inventory n. 用于应付突发性需求的存货capacity inventory n. 用于将来某时使用的存货cycle inventory n. 循环盘存decoupling inventory n. 保险性存货(以应付万一)finished goods inventory n. 制成品存货(盘存)pipeline inventory n. 在途存货raw materials inventory n. 原材料存货work-in-progress inventory n. 在制品盘存(存货)invest v. 投资investment n. 投资investor n. 投资者invoice n. 发票v. 给(某人)开发票irrevocable adj. 不可撤消的,不能改变的issue n. 发行股票* rights issue n. 优先认股权IT=Information Technology 信息技术item n. 货物,条目,条款Jjob n. 工作job description 工作说明,职务说明*job lot n. 一次生产的部分或少数产品job mobility 工作流动job rotation 工作轮换job satisfaction 工作的满意感(自豪感)*job shop n. 专门车间jobbing n. 为一次性的或小的订货需求而特设的生产制度joint adj. 联合的joint bank account (几个人的)联合银行存款帐户journal n. 专业杂志*jurisdiction n. 管辖(权)junk bonds n. 低档(风险)债券,垃圾债券junk mail n. (未经收信人要求的)直接邮寄的广告宣传*just-in-time n. 无库存制度Kkey adj. 主要的,关键的knockdown adj. (价格)很低的know-how n. 专门技术Llabel n. 标签,标牌v. 加标签,加上标牌labour n. 劳动,工作,劳动力labour market 劳动力市场labour relations 劳资关系labour shortage 劳动力短缺*launch v. 在市场推出一种新产品n. 新产品的推出lay-off/layoff n./v. 临时解雇layout n. 工厂的布局lead v. 领先,领导lead time n. 完成某项活动所需的时间leaflet n. 广告印刷传单lease n. 租借,租赁物legal adj. 合法的lend v. 出借,贷款lessee n. 承租人lessor n. 出租人*ledger n. 分类帐nominal ledger n. 记名帐purchase ledger n. 进货sales ledger n. 销货帐*leverage n. 杠杆比率liability n. 负债liabilities n. 债务licence(US:license)n. 许可证license v. 许可,批准life cycle n. 寿命周期likely adj. 可能的*line process 流水线(组装)link n. 关系,联系,环liquid adj. 易转换成现款的liquidate v. 清算*liquidity n. 拥有变现力liquidation n. 清理(关闭公司),清算liquidator n. 清算人,公司资产清理人listed adj. 登记注册的listing n. 上市公司名录literature n. (产品说明书之类的)印刷品,宣传品litigate v. 提出诉讼loan n./v. 贷款,暂借logo n. 企业的特有标记lose v. 亏损loser n. 失败者loss n. 损失lot n. 批,量loyalty n. 忠诚,忠实Mmagazine n. 杂志,期刊mailshot n. 邮购maintain v. 维持,保持maintenance n. 维持,坚持major adj. 重大的,主要的,较大的majority shareholding 绝对控股make n. 产品的牌子或型号make-to-order adj. 根据订货而生产的产品make-to-stock adj. 指那些在未收到订货时就已生产了的产品management n. 管理,管理部门middle management n. 中层管理人员senior management n. 高层管理人员managerial adj. 管理人员的,管理方面的manager n. 经理plant manager n. 工厂负责人line manager n. 基层负责人staff manager n. 部门经理助理management accounts n. 管理帐目matrix management n. 矩阵管理*management information system(MIS)n. 管理信息系统manning n. 人员配备manpower n. 劳动力manpower resources n. 劳动力资源manual adj. 体力的,人工的,蓝领的manufacture v. (用机器)制造manufacturer n. 制造者(厂、商、公司)manufacturing adj. 制造的manufacturing industry 制造业margin n. 利润gross margin n. 毛利率net margin n. 净利润mark-up v. 标高售价,加价market n. 市场;产品可能的销量down market adv./adj. 低档商品/地的up market adj./adv. 高档商品的/地marketing mix n. 综合营销策略,指定价、促销、产品等策略的配合market leader n. 市场上的主导公司*market niche n. 小摊位,专业市场的一个小部分market penetration n. 市场渗入market segmentation 市场划分market share n. 市场占有率,市场份额*mass-marketing n. 大众营销术*master production schedule n. 主要生产计划*material requirements planning(MRP)n. 计算生产中所需材料的方法*materials handling n. 材料管理,材料控制maximise v. 使增至最大限度、最大化measure n. 措施,步骤media n. 新闻工具,传媒mass media 大众传媒(如电视、广播、报纸等)merchandising n. (在商店中)通过对商品的摆放与促销进行经营merge v. 联合,合并m,erger n. (,公司,企业等的)合并merit n. 优点,值得,应受method study n. 方法研究middleman n. 中间人,经纪人full milk n. 全脂牛奶skimmed milk n. 脱脂乳minimise v. 使减至最小限度,最小化*mission n. 公司的长期目标和原则mobility n. 流动性,可移性moderately adv. 中等地,适度地monopoly n. 垄断,独占mortgage n./v. 抵押motivate v. 激励,激发……的积极性motivated adj. 有积极性的motivation n. 提供动机,积极性,动力motive n. 动机Nnegotiate v. 谈判negotiable adj. 可谈判的,可转让的net adj. 净的,纯的network n. 网络*niche n. 专业市场中的小摊位notice n. 通知,辞职申请,离职通知Oobjective n. 目标,目的obsolete adj. 过时的,淘汰的,废弃的offer n. 报价,发盘offer v. 开价off-season adj./adv. 淡季的off-the-shelf adj. 非专门设计的off-the-peg adj. 标准的,非顾客化的opening n. 空位operate v. 操作,经营,管理operating profits 营业利润*operations chart n. 经营(管理)表*operations scheduling n. 生产经营进度表opportunity n. 机会*optimize v. 优化option n. 选择权share option n. 期权organigram n. 组织图organisation chart n. 公司组织机构图orient v. 定向,指引orientation n. 倾向,方向;熟悉,介绍情况outcome n. 结果outlay n. 开销,支出,费用*outlet n. 商店a retail outlet 零售店outgoings n. 开支,开销outlined adj. 概括,勾勒的草图output n. 产量*outsource v. 外购产品或由外单位制做产品outstanding adj. 未付款的,应收的over-demand n. 求过于供overdraft n. 透支overdraft facility 透支限额overdraw v. 透支*overhead costs n. 营业成本*overheads n. 企业一般管理费用overpay n. 多付(款)overtime n. 加班overview n. 概述,概观owe v. 欠钱,应付Pp.a.(=per annum)n. 每年packaging n. 包装物;包装parent company n. 母公司,总公司part-time adj. 部分时间工作的,业余的participate v. 参加,分享(in)partnership n. 合伙(关系),合伙,合伙企业patent n. 专利pay n. 工资,酬金v. 付钱,付报酬take-home pay 实得工资payroll n. 雇员名单,工资表peak n. 峰值,顶点penetrate v. 渗透,打入(市场)penetration n. 目标市场的占有份额pension n. 养老金,退休金perform v. 表现,执行performance n. 进行,表现工作情况performance appraisal n. 工作情况评估perk n. 额外待遇(交通、保健、保险等)personnel n. 员工,人员*petty cash n. 零用现金phase out n. 分阶段停止使用*pick v. 提取生产用零部件或给顾客发货* picking list n. 用于择取生产或运输订货的表格pie chart n. 饼形图pilot n. 小规模试验pipeline n. 管道,渠道plant capacity n. 生产规模,生产能力plot v. 标绘,策划*plough back n. 将获利进行再投资* point of sale (POS)n. 销售点policy n. 政策,规定,保险单*portfolio n. (投资)组合*portfolio management n. 组合证券管理post n. 邮件,邮局;职位position n. 职位potential n. 潜在力,潜势power n. 能力purchasing power 购买力PR=Public Relations 公共关系*preference shares n. 优先股price n. 价格market price 市场价,市价retail price 零售价probation n. 试用期product n. 产品production cycle n. 生产周期production schedule n. 生产计划product life cycle n. 产品生命周期product mix n. 产品组合(种类和数量的组合)productive adj. 生产的,多产的*profile n. 简介形象特征profit n. 利润operating profit n. 营业利润profit and loss account n. 损益帐户project v. 预测promote v . 推销promotion n. 提升,升级proposal n. 建议,计划prospect n. 预期,展望prospectus n. 计划书,说明书prosperity n. 繁荣,兴隆prototype n. 原型,样品*publicity n. 引起公众注意public adj. 公众的,公开的go public 上市public sector 公有企业publicity n. 公开场合,名声,宣传publics n. 公众,(有共同兴趣的)一群人或社会人士punctual adj. 准时的punctuality n. 准时purchase v. & n. 购买purchaser n. 买主,采购人QQC(=Quality Circle)n. 质检人员qualify v. 有资格,胜任qualified adj. 有资格的,胜任的,合格的qualification n. 资格,资格证明quality n. 质量quality assurance n. 质量保证quality control 质量控制,质量管理quarterly adj./adv. 季度的,按季度questionnaire n. 调查表,问卷quote n. 报价,股票牌价quotation n. 报价,股票牌价RR&D Research and Development 研究与开发radically adv. 根本地,彻底地raise n. (美)增加薪金v. 增加,提高;提出,引起range n. 系列产品rank n./v. 排名rapport n. 密切的关系,轻松愉快的气氛rate n. 比率,费用fixed rate 固定费用,固定汇率going rate 现行利率,现行汇率rating 评定结果ratio n. 比率rationalise v. 使更有效,使更合理raw adj. 原料状态的,未加工的raw material n. 原材料receive v. 得到receipt n. 收据receiver n. 接管人,清算人accounts receivable 应收帐receivership n. 破产管理recession n. 萧条reckon v. 估算,认为recognise v. 承认reconcile v. 使……相吻合,核对,调和recoup v. 扣除,赔偿recover v. 重新获得,恢复recovery n. 重获,恢复recruit v. 招聘,征募n. 新招收的人员recruitment n. 新成员的吸收red n. 红色in the red 赤字,负债reduce v. 减少reduction n. 减少redundant adj. 过多的,被解雇的redundancy n. 裁员,解雇reference n. 参考,参考资料reference number (Ref. No.)产品的参考号码refund n./v. 归还,偿还region n. 地区*reimburse v. 偿还,报销reject n./v. 拒绝reliability n. 可靠性relief n. 减轻,解除,救济relocate v. 调动,重新安置remuneration n. 酬报,酬金rent v. 租n. 租金rep (代表)的缩写report to v. 低于(某人),隶属,从属reposition v. (为商品)重新定位represent v. 代表,代理representative n. 代理人,代表reputation n. 名声,声望reputable adj. 名声/名誉好的reserves n. 储量金,准备金resign v. 放弃,辞去resignation n. 辞职resistance n. 阻力,抵触情绪respond v. 回答,答复response n. 回答,答复restore v. 恢复result/results n. 结果,效果retail n./v. 零售retailer n. 零售商*retained earnings n. 留存收益retire v. 退休retirement n. 退休return n. 投资报酬*return on investment (ROI)n. 投资收入,投资报酬revenue n. 岁入,税收review v./n. 检查reward n./v. 报答,报酬,奖赏*rework v. (因劣质而)重作risk capital n. 风险资本rival n. 竞争者,对手adj. 竞争的rocket v. 急速上升,直线上升,飞升ROI Return on Investment 投资利润roughly adv. 粗略地round adj. 整数表示的,大约round trip 往返的行程royalty n. 特许权,专利权税run v. 管理,经营running adj. 运转的Ssack v. 解雇sales force 销售人员sample n. 样品v. 试验;抽样检验*saturation n. (市场的)饱和(状态)saturate v. 饱和save v. 节省,储蓄savings n. 存款scale n. 刻度,层次scapegoat n. 替罪羊scare adj. 缺乏的,不足的*scrap n. 废料或废品seasonal adj. 季节性的section n. 部门sector n. 部门*securities n. 债券及有价证券segment n. 部分v. 将市场划分成不同的部分segmentation n. 将市场划分成不同的部门semi-skilled adj. 半熟练的settle v. 解决,决定settlement n. 解决,清偿,支付service n. 服务,帮佣services n. 专业服务settle v. 安排,支付set up v. 创立share n. 股份shareholder n. 股东*shelf-life n. 货架期(商品可以陈列在货架上的时间)shift n. 轮班showroom n. 陈列室simulation n. 模拟shop n. 商店closed shop 限制行业(只允许本工会会员)open shop 开放行业(非会员可从事的工作)shop steward 工会管事shopfloor 生产场所shortlist n. ……供最后选择的候选人名单v. 把……列入最后的候选人名单sick adj. 病的sick leave 病假sick note 病假条sick pay 病假工资sickness 生病skill n. 技能,熟巧skilled employee n. 熟练工人*skimming n. 高额定价,撇奶油式定价slogan n. 销售口号slump n. 暴跌a slump in sales 销售暴跌soft-sell n. 劝诱销售(术),软销售(手段)software n. 软件sole adj. 仅有的,单独的sole distributor 独家分销商solvent adj. 有偿付能力的*sourcing n. 得到供货spare part n. 零部件specification n. 产品说明split v. 分离spokesman n. 发言人sponsor n. 赞助者(为了商品的广告宣传)spread n. (股票买价和卖价的)差额stable adj. 稳定的staff n. 职员stag n. 投机认股者v. 炒买炒卖stagnant adj. 停滞的,萧条的*statute n. 成文法statutory adj. 法定的steadily adv. 稳定地,平稳地stock n. 库存,股票stock exchange n. 证券交易所*stockbroker n. 股票经纪人stock controller 库房管理者storage n. 贮藏,库存量strategy n. 战略*streamline v. 精简机构,提高效率stress n. 压力,紧迫strike n. 罢工structure n. 结构,设备*subcontract v. 分包(工程项目),转包subordinate n. 下级adj. 下级的subscribe v. 认购subsidiary n. 子公司subsidise v. 补贴,资助subsidy n. 补助金substantially adv. 大量地,大幅度地summarise v. 概括,总结superior n. 上级,长官supervisor n. 监督人,管理人supervisory adj. 监督的,管理的supply n./v. 供给,提供survey n 调查*SWOT analysis n. SWOT分析是分析一个公司或一个项目的优点、弱点、机会和风险*synergy n. 协作Ttactic n. 战术,兵法tailor v. 特制产品tailor made products 特制产品take on 雇用takeover n. 接管target n. 目标v. 把……作为目标tariff n. 关税;价目表task n. 任务,工作task force n. 突击队,攻关小队(为完成某项任务而在一起的一组人)tax n. 税,税金capital gains tax n. 资本收益税corporation tax n. 公司税,法人税income tax n. 所得税value added tax 增值税tax allowance 免减税tax avoidance 避税taxable 可征税的taxation 征税tax-deductible 在计算所得税时予以扣除的telesales n. 电话销售,电话售货temporary adj. 暂时的temporary post 临时职位tender n./v. 投标territory n. (销售)区域tie n. 关系,联系throughput n. 工厂的总产量TQC(=Total Quality Control)n. 全面质量管理*track record n. 追踪记录,业绩trade n./v. 商业,生意;交易,经商balance of trade 贸易平衡trading profit 贸易利润insider trading 内部交易trade mark 商标trade union 工会trainee n. 受培训者*transaction n. 交易,业务transfer n./v. 传输,转让*transformation n. 加工transparency n. (投影用)透明胶片treasurer n. 司库,掌管财务的人*treasury n. 国库,财政部trend n. 趋势,时尚*trouble-shooting n. 解决问题turnover n. 营业额,员工流动的比率staff turnover 人员换手率stock turnover 股票换手率Uundertake v. 从事、同意做某事undifferentiated marketing n. 无差异性营销策略uneconomical adj. 不经济的,浪费unemployment n. 失业unemployment benefit n. 失业津贴unit n. 单位unit cost n. 单位成本update v. 使现代化up to date adj./adv. 流行的,现行的,时髦的upgrade v. 升级,增加upturn n. 使向上,使朝上USP 唯一的销售计划Vvacancy n. 空缺vacant adj. 空缺的value n./v. 价值,估价valuation n. 价值value-added n. 增加值variable n. 可变物variation n. 变化,变更variety n. 多样化a variety of 多种多样的vary v. 改变,修改VAT Value Added Tax 增值税vendor n. 卖主(公司或个人)venture n. 冒险,投机venue n. 地点,集合地点viable adj. 可行的viability n. 可行性vision n. 设想,公司的长期目标vocation n. 行业,职业vocational adj. 行业的,职业的Wwage n. (周)工资wage freeze n. 工资冻结warehouse n. 仓库,货栈wealth n. 财富,资源wealthy adj. 富裕的,丰富的welfare n. 福利white-collar 白领阶层white goods n. 如冰箱和洗衣机等用在厨房中的产品wholesale n./adj./adv. 批发wholesaler 批发商*wind up v. 关闭公司withdraw v. 拿走,收回,退出withdrawal n. 拿走,收回,退出wholesale n./a. 批发;批发的wholesaler n. 批发商work n. 工作working conditions n. 工作条件work-in-progress n. 工作过程workload n. 工作量work order n. (包括原料、半成品、成品的)全部存货总量work station 工作位置*working capital n. 营运资本,营运资金write off v. 取消write-off n. 债务的取消Y*yield n. 有效产量Z*zero defect n. 合格产品*zero inventory n. 零存货。

CASESTUDYAINSWORTHPETNUTRITION-…

AINSWORTH PET NUTRITIONdistributing pet food across the U .S .and Canada since 1933 .America’s oldestprivately owned pet food company has been run by the Lang family for fivegenerations, including the current CEO, Sean Lang .Ainsworth sells pet food tovirtually every major retailer in the CPG market, including the brands Back toBasics, Enhance, VF Complete, The Source, Rachel Ray Nutrish™, DAD’s Pet Foods,the Better Than® treat brands, and Kibble™ Select Complete .Ainsworth alsomanufactures private label products (in-store brands), and they do some co-packing for other pet food companies through the Ainsworth Custom Division .Ainsworth employs more than 500 employees altogether at its head office,manufacturing facility and warehouses in Meadville, PA, a sales and marketingoffice in Sewickley, PA, and another manufacturing facility, more warehouses andan office in Dumas, Arkansas - the latter location since Ainsworth acquired ArkatAnimal Nutrition in 2010 .All manufacturing is done in the U .S ., and the bulk ofingredients are sourced from local suppliers .23THECHALLENGEWhen market demand doubled between 2000 and 2007, Ainsworth decided to purchase an ERP (enterprise resource They Ainsworth’s initial implementation in 2007 included Finance, Sales, Demand Planning, Purchasing, Inventory, Manufacturing, Logistics Planning, and Quality Management . At the end of Phase 1, there were 30 licensed users of JustFoodERP at Ainsworth . In 2012, that number sits around 50, with 100 employees trained in the JustFoodERP system, says Jamie Hornstein, Director, Information Services, Ainsworth .“Advance Ship Notice (ASN) can be complicated but necessary if you are doing a lot of case picking. The other day I looked at a large retailer’s order – where we used to sell them three or four items, we now have 30 items on the order... A lot of ASN comes down to training; we had a hand in customizing the ASN module in JustFoodERP”Jamie Hornstein, Director, Information ServicesAinsworth Pet Nutrition4THE SOLUTIONAinsworth has continued to add functionality to the system in the years since, says Hornstein .For example, in 2011 they implemented the Warehouse Management System (WMS) part of JustFoodERP at all their warehouses .While Ainsworth has always had 24/7 manufacturing and warehousing operations, the introducing of the WMS module put that around-the-clock functionality in place in their business software systems for the first time . They also implemented JustFoodERP Floor – the mobile web interface that lets employees access the JustFoodERP system via handheld guns to scan barcodes for production output and movements at all nine of their warehouses .JustFoodERP Floor is being used by about 20 workers at three warehouses in Meadville, and another three in Dumas and other locations .“Our warehouse tracking systems were antiquated,” says Hornstein . “We were happy to see the lower cost user licenses for JF Floor” – substantially lower than the cost of the regular Microsoft Dynamics license .Ainsworth also implemented the Advance Ship Notification (ASN) module within JustFoodERP in 2010 .About 10% of their retail customers mandate them to use ASN – a standard of documentation and labeling required by some mass merchandisers for how they want product to arrive on their shipping docks . “It can be complicated, and necessary, if you are doing a lot of case picking,” says Hornstein .“The other day I looked at a large retailer’s order – where we used to sell them three or four items, we now have 30 items on the order!”He continues: “If you are using ASN, you have to re-think the layout of your warehouse, you have to stage everything. A lot of ASN comes down to training; we had a hand in customizing the ASN module in JustFoodERP.” EDI, which is much more prevalent than the adoption of ASN at this time, is required by about 80% of Ainsworth’s customers, says Hornstein .They use the Lanham EDI module within the JustFoodERP system .THE BENEFITSTaking advantage of built-in ASN and EDI lets Ainsworth conduct more, and better, business withmass merchandisers . When it comes to the addition of JustFoodERP Floor, Hornstein says puttingthat wireless interface in the hands of their warehouse workers has resulted in “improved inventoryaccuracy, visibility into inventory status, and management of quality holds in the system.”The addition of WMS has been invaluable as the number of Ainsworth warehouses multiply atvarious spots around the U .S .– with more likely to come in the near future .In fact, says Horstein,since Ainsworth purchased the Dumas, AK facility, they’ve had plans to expand to other parts ofthe U .S .“and we realized our demand planning systems through MRP were not integrated.” As a result,working with a supply chain consultant, Ainsworth has recently developed a “phased-in plan tointegrate forecast and production planning systems, and do some cost-based optimization of where tomanufacture products,” says the consultant, Sumantra Sengupta, Managing Director, EVM Partners,LLC .“Our supply chain optimization project uses JustFoodERP modules, open integration and data, includingPOS data feeds directly from Ainsworth’s customers.” The MRP and MPS modules of JustFoodERP arebeing customized to suit Ainsworth’s needs, and sales forecasts are loaded into the ERP system fortwo-way integration with third-party forecasting software .56THE FUTUREThe company also plans to roll out the Container functionality within JustFoodERP Floor; that will allow them to automatethe processes of building, moving, picking, and consuming7SOLUTION SUMMARYJustFoodERP and Microsoft DynamicsLocations:Meadville, PA – head office, manufacturing facility, warehouses Dumas, AK – manufacturing facility, warehouses, office Sewickley, PA – sales and marketing officeOther locations in the U .S . – warehousesJustFoodERP Modules: Purchasing; Sales; Inventory Management; Quality Management; Logistics Planning; Finance; Warehouse Management System;JF Floor; EDI; Reporting。

第三届IMA管理会计案例大赛案例英文版