宏观经济学 macroeconomics_19

萨缪尔森《宏观经济学》(第19版)习题详解(含考研真题)(第4章 宏观经济学概述)

萨缪尔森《宏观经济学》(第19版)第二编宏观经济学:经济增长与商业周期第4章宏观经济学概述课后习题详解跨考网独家整理最全经济学考研真题,经济学考研课后习题解析资料库,您可以在这里查阅历年经济学考研真题,经济学考研课后习题,经济学考研参考书等内容,更有跨考考研历年辅导的经济学学哥学姐的经济学考研经验,从前辈中获得的经验对初学者来说是宝贵的财富,这或许能帮你少走弯路,躲开一些陷阱。

以下内容为跨考网独家整理,如您还需更多考研资料,可选择经济学一对一在线咨询进行咨询。

一、概念题1.宏观经济学和微观经济学(macroeconomics vs. microeconomics)答:(1)与“微观经济学”相对而言,宏观经济学是一种现代的经济分析方法。

它以国民经济总体为考察对象,研究经济生活中有关总量的决定与变动,解释失业、通货膨胀、经济增长与波动、国际收支与汇率的决定与变动等经济中的宏观整体问题,所以又称之为总量经济学。

宏观经济学的中心和基础是总供给—总需求模型。

具体来说,宏观经济学主要包括总需求理论、总供给理论、失业与通货膨胀理论、经济周期与经济增长理论及开放经济理论及宏观经济政策等内容。

对宏观经济问题进行分析与研究的历史十分悠久,但现代意义上的宏观经济学直到20世纪30年代才得以形成和发展起来。

宏观经济学诞生的标志是凯恩斯于1936年出版的《就业、利息和货币通论》。

(2)微观经济学是西方经济学的重要组成部分,以市场经济中各个经济单位的经济行为和经济规律作为考查对象,研究单个生产者或企业是如何利用有限的资源生产商品和劳务以获取最大利润,以及单个消费者或家庭是如何利用有限的货币收入购买商品和劳务以获取最大满足的。

因此,微观经济学的核心内容是论证亚当·斯密的“看不见的手”原理。

微观经济学的理论内容主要包括:消费理论或需求理论、厂商理论、市场理论、要素价格或分配理论、一般均衡理论和福利经济理论等。

由于这些理论均涉及市场经济和价格机制的作用,因而微观经济学又被称为市场经济学。

什么是宏观经济学,什么是微观经济学?

什么是宏观经济学,什么是微观经济

学?

宏观经济学(Macroeconomics),是使用国民收入、经济整体的投资

和消费等总体性的统计概念来分析经济运行规律的一个经济学领域。

微观经济学又称个体经济学,小经济学,是现代经济学的一个分支,主要以单个经济单位(单个生产者、单个消费者、单个市场经济活动)作为研究对象分析的一门学科。

微观经济学是研究社会中单个经济单位的经济行为,以及相应的经济变量的单项数值如何决定的经济学说。

亦称市场经济学或价格理论。

扩展资料

微观经济学与宏观经济学之间的联系:

1、微观经济学和宏观经济学是互为补充的。

2、微观经济学是宏观经济学的基础。

3、宏观经济学并不是微观经济学的简单加总或重复。

4、两者共同构成了西方经济学的整体。

宏、微观经济学是现代西方经济学的两个分支学科,它们研究的对象不同,但两者的理论基础是相同的。

近来西方经济学的发展趋向于宏、微观融合,新凯恩斯主义宏观经济学也主张寻找微观基础。

参考资料:百度百科——微观经济学百度百科——宏观经济学

1。

Macroeconomics宏观经济学共8页文档

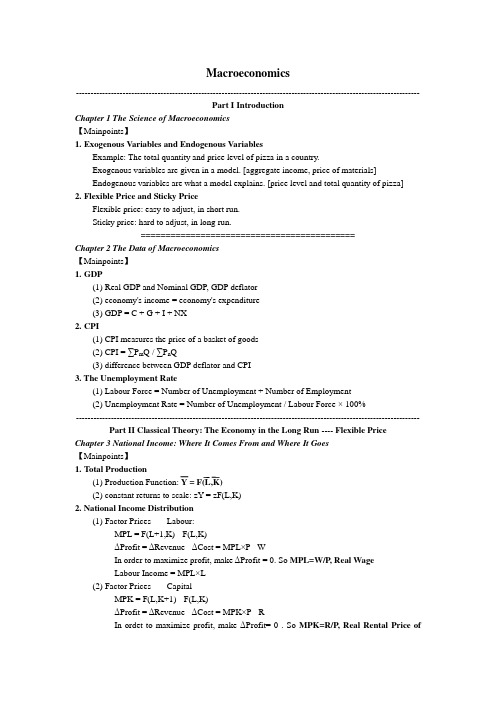

MacroeconomicsPart I IntroductionChapter 1 The Science of Macroeconomics【Mainpoints】1.Exogenous Variables and Endogenous VariablesExample: The total quantity and price level of pizza in a country.Exogenous variables are given in a model. [aggregate income, price of materials]Endogenous variables are what a model explains. [price level and total quantity of pizza]2.Flexible Price and Sticky PriceFlexible price: easy to adjust, in short run.Sticky price: hard to adjust, in long run.Chapter 2 The Data of Macroeconomics【Mainpoints】1.GDP(1) Real GDP and Nominal GDP, GDP deflator(2) economy's income = economy's expenditure(3) GDP = C + G + I + NX2.CPI(1) CPI measures the price of a basket of goods(2) CPI = ∑P m Q / ∑P n Q(3) difference between GDP deflator and CPI3. The Unemployment Rate(1) Labour Force = Number of Unemployment + Number of Employment(2) Unemployment Rate = Number of Unemployment / Labour Force × 100%Part II Classical Theory: The Economy in the Long Run ---- Flexible Price Chapter 3 National Income: Where It Comes From and Where It Goes【Mainpoints】1.Total Production(1) Production Function: Y = F(L,K)(2) constant returns to scale: zY = zF(L,K)2. National Income Distribution(1) Factor Prices ---- Labour:MPL = F(L+1,K) - F(L,K)ΔProfit = ΔRevenue - ΔCost = MPL×P - WIn order to maximize profit, make ΔProfit = 0. So MPL=W/P, Real WageLabour Income = MPL×L(2) Factor Prices ---- CapitalMPK = F(L,K+1) - F(L,K)ΔProfit = ΔRevenue - ΔCost = MPK×P - RIn ordet to maximize profit, make ΔProfit= 0 . So MPK=R/P, Real Rental Price of CapitalCapital Income = MPK×K3)The Cobb-Douglas Production FunctionLabour Income = MPL×L = (1-α)YCapital Income = MPK×K = αY→F(K,L) = AKαL(1-α) , A measures the productivity of the available technology3.Total Demand1)Consumption:Determined by disposable incomeC=C(Y-T)Marginal Propensity to ConsumeMPC=C(Y-T+1)-C(Y-T)2)Investment:Determined by interest rateI=I(r)When r is high, investors will give upinvestment because cost of loan is higherthan rate of return.3) Government PurchasesG vs T, measures government budget5. Equilibrium (in a closed economy)(1) Market of Goods and ServicesY=C(Y-T)+I(r)+G(2) Market of Loanable FundsS=Y-C(Y-T) - G = I(r)investment is crowded out Chapter 4 Money and Inflation【Mainpoints】1.Concept of Money(1) Funtions of Money: 1) Store of Value. Example: You can hold your money and trade itfor goods and services at some time in the future.2) Unit of Account. Example: In store people use money to showprice.3) Medium of Exchage. Example: People use money as tool toexchange goods.(2) Types of Money: 1) Fiat Money. No value, example: Paper Money.2) Commodity Money. With value, example: Gold and Silver.(3) Control of Money: 1) Institution: Central Bank. Example: Deutsche Bundesbank2) Method: Open-Markt Operation. Example: Buy governmentbonds to increase money supply.2.The Quantity Theory of Money(1) Quantity Equation: MV=PT →MV=PYQuantity Theory of Money: MV=PY(2) Real Money Balances: M/P , measured in quantity of goods and services.The Money Demand Function: (M/P)d = L(Y,i) = M/P← Money Supply. Y↑, d↑; i↑,d↓(3) Money and Inflation: ΔM% + ΔV% = ΔP% + ΔY% So M↑, P↑3.Inflation and Interest Rate(1) Fisher Equation: i = r + πChapter 5 The Open Economy【Mainpoints】1.International Trade in a Samll Open Economy(1) View of goods and capital flow: NX = Y- (C+G+I)(2) View of capital flow: NX = Y-C-G-I = S-I= S-I(r*)r* is World Interes Rate(3) Trade Policies: 1) Domestic Fiscal Policy, influenceG↑,T↓→S↓→NX↓2) Fiscal Policy Abroad, influenceG e↑, T e↓→S e↓→r*↑→NX↑3) Shift in investment demand. Example: Government provides aninvestment tax credit2.Exchange Rates(1) Nominal Exchange Rates(e) and Real Exchange Rates(ε)Nominal exchange rates are measured in currency. Example: 100 yen / 1 dollarReal exchage rates are measured in goods and services. Example: 2 Japan Car / 1 USA car ε = e × (P/P*) , P* means price level of foreign countries.(2) The Real Exchange Rates and Trade Balance:NX = NX(ε)ε↓, P/P*↓, mean s domestic goods and servicesare cheaper than abroad. NX↑When NX(ε) = S - I, ε is equilibrium real ex.rate.(3) Trade Policies: 1) Domestic Fiscal Policy:G↑,T↓ → S↓(Expansionary Fiscal Policy)2) Fiscal Policy Abroad:G e↑, T e↓→S e↓→r*↑→I↓3) Shift in investment demand.4) Shift in NX(ε) Example: Protectionist Trade Policies(4) Inflation and nominal exchange rates:e = ε × (P*/P) → Δe%= Δε% + (π* - π)(5) PPP(Purchasing-Power Parity): 1 Dollar can buy the same quantity of wheat in anycountry.Chapter 6 Unemployment【Mainpoints】1.Natual Rate of Unemployment(1) Concept: The rate of unemployment which the economy get closed to in the long run.(2) Calculation: L-Labour Froce, E-Number of Employed, U-Number of Unemployed, f-rate of job fiding, s-rate of job seperating.L=E+U, fU=sE → U/L=1/(1+f/s)2.Causes for Unemployment(1) Frictional Unemployment:Unemployed people need time to find jobs.e.g. sectoral shift, unemploymetn insurance.(2) Structural Unemployment:Wage Rigidity. Wage is above the equlibrium level.e.g. Minimum-Wage Laws, Unions, Efficiency Wages.Part III Growth Theory: The Economy in the Very Long Run ---- Solow Growth Model Chapter 7 Economic Growth I: Capital Accumulation and Population GrowthAssumption: Constant Return to Scale【Mainpoints】1.Capital Accumulation(1) Production Function per worker: zY=F(zK,zL)→Y/L=F(K/L,1)→y=f(k),MPK=f(k+1)-f(k)(2) Output and consumption per worker: y=c+i→c=(1-s)y→i=sy→i=sf(k)(3) The Steady State: Capital stock growth Δk = 0Δk=i-δk, δ is depreciation rate→Δk=sf(k)-δk=0→sf(k*)=δk*(4)Golden Rule level of capital: k*gold which maximizes cc=y-i→c=f(k)-sf(k)→c*=f(k*)-δk*→c max:MPK=δ2. Population Growth(at rate of n)(1) The Steady State:Δk=i-k(δ+n)→Δk=sf(k)-k(δ+n)=0→sf(k*)=(δ+n)k*(2) Golden Rule level of capital:k*gold, c=y-i→c max:MPK=δ+nChapter 8 Economic Growth I: Technology, Empirics, and Policy1.Technological Progress in the Solow ModelAssumption: Technology growth is a given exogenous variable g(1) Efficiency of Labour: Y=F(K,EL)(2) The Steady State: Δk=sf(k)-(g+n+δ)k=0→sf(k*)=(g+n+δ)k*(3) Golden Rule level of capital: k*gold , c=y-i→MPK=g+n+δ2.Endogenous Growth TheoryAssupmtion: Technolgy growth is a endogenous function g(μ), capital includes knowledge (1) 2 Sector Model: Y=F[K,(1-μ)EL], ΔE=g(μ)E, ΔK=sY-δKPart IV Business Cycle Theory: The Economy in the Short Run ---- Sticky Price Chapter 9 Introduction to Economic Fluctuations【Key Concepts】Recession: A period of falling output and rising unemployment.Business Cycle: Short-run fluctuations in output and employment.【Mainpoints】1.GDP and unemployment(1) Okun's Law: ΔReal GDP%=3%-2×ΔUnemployment Rate(2) Leading Economic Indicators: Forecasts. Example: Average work time, Index of stock prices, Money Supply....2.Aggregate Demand and Aggregate Supply( P=P(Y))(1) The Quantity Theory of Money→AD: MV=PY→M/P=(M/P)d=kY(2) AS: SRAS---P=P, LRAS---Y=Y(3) From Short Run to Long Run: M changes AD, Y is unchanged inthe long run, but P in the long run changes. (A→B→C)(4) Shocks to AD and AP:1) Shocks to AD. Example: Credit Card makes V rise.Policy: Reduce the Money Supply.2) Shocks to AP. Example: A drought that destroys crops. Cartel. Union. etc. P↑Policy: Wait! Then price returns original level eventually(But it takes longtime). Or expand AD(But price level will be high in long period of time) Chapter 10 Aggregate Demand I: Building the IS-LM Model (Y-r)【Mainpoints】1.IS Curve(1) Good and Service Market→The Keynesian Cross: Y=C+I+G, PE=AE(2) IS curve:Y=C(Y-T)+I(r)+G 1) r↑→I↓→Y↓ 2) Fiscal Policy: G↑→Y↑→IS→, Governmetn-purchases multiplier, tax multiplier.2.LM Curve(1) Money Market→The Theory of Liquidity Peference: M/ P=L(r), M s=M d(2) LM Curve: M/P=L(r,Y). 1) Y↑,M d↑,r↑ 2)M s↑,r↓,LM←3. The Short-Run EquilibriumChapter 11 Aggregate Demand II: Applying the IS-LM Model (Y-P)【Mainpoints】1.IS-LM Model as a Theroy of Aggregate Demand(1) Derivation: P↑,(M/P)s↓,r↑,LM↑→Y↓(2) Shift in AD: G,T,M→IS/LM→Y(3) In long run and short run: In long run Y<YChapter 12 The Open Economy Revisited: The Mundell-Fleming Model and the Exchange Rate Regime【Mainpoints】1.Mundell-Fleming Model(1) IS* Curve: Y=C(Y-T)+I(r*)+G+NX(ε) (2) LM* Curve: M/P=L(r*,Y)2.Under Floating Exchange Rates(1)Fiscal Policy:Shift IS*,ineffectual; Monetary Policy:Shift LM*; Trade Policy:Shift NX(ε)→IS* 3.Under Fixed Exchange Rates(1) Theory: Arbitrageur arbitrage so that M changes.(2)Fiscal Policy shifts IS*→LM*; Monetary Policy:Shift LM*, ineffectual; Trade Policy: Shift NX(ε)→IS*→LM*4. Policy Choice: Impossible Trinity5. Mundell-Fleming Model in Short andLong RunChapter 13 AS and the Short-Run Tradeoff Between Inflation and Unemployment1.Aggregate Supply ModelY=Y+α(P-P e)2.Inflation, Unemployment and Phillips Curve(1)Y=Y+α(P-P e)→P-P-1=P e-P-1+1/α(Y-Y)+v→π=πe+β(μ-μn)+v [Okun's Law] v-supply shock(2) Sacrifice Ratio: π↓1%, GDP ↓ ? %Part V Macroeconomic Policy DebateChapter 14 Stabilization Policy1.Inside Lag and Outside Lag(1) Inside lag is the time between economy shock and the policy anction responds. Example: Policy makers need time to recognize a shock and react.(2) Outside lag is the time between a policy action and its influence on the economy. Example: Change in money supply and interest rate.Chapter 15 Government Debt and Budget Deficits1.The Traditional View of Government Debt(1) In the short run, T↓,C↑,S↓,r↑,I↓,lower steady-state K and a lower level of Y.(2) In the lo ng run, T↓,C↑,IS→,AD↑, finally Y=Y, P i s higher.(3) In open economy, T↓,C↑,IS→, ε↑2.The Ricardian View of Government Debt(1) Ricardian Equivalence: Consumers are forward-looking.They think that government will raise tax at some point in the future, in order to afford budget. So they won't change consumption.Part VI More on the Microeconomics Behind MacroeconomicsChapter 18 Money Supply, Money Demand and the Banking System1.Money Supply(1) Money Supply (M) = Currency (C) + Demand Deposits (D)(2) Reserves: The money that bank receive but don't lend out. Reserve-deposit ratio-rr1) 100% Reserve Banking. 1C→1D, M remains constant.2) Fractional-Reserve Banking. 1C→rrD+(1-rr)C, M increases. And (1-rr)C can be put into another bank, the process of money creation can be continued.(3) Money Supply Model: M=C+D.B(Monetary Base)=C+R [Control by Central Bank]→ M=(cr+1)/(cr+rr)×B=m×B [cr is currency-deposit ratio](4) Monetary Policy Tool: open-market operation, reserve requirements, discout rate[the rate that banks borrow from central bank].2.Money Demand(1) Quantity Theory: (M/P)d=L(i;Y)(2) Portfolio Theory: (M/P)d=L(r s,r b,πe,W) [r s-expected real return on stock, r b-expected real return on bonds, W-real wealth]。

第19章 通货膨胀与失业的交替(经济学原理(曼昆)-上海交大)

Macroeconomics

降低通货膨胀的代价

用紧缩性政策降低通货膨胀率的过程: 放慢货币供给来紧缩总需求。总需求减 少又减少了产量,进而减少就业率,使 短期菲力普斯曲线上的A点移动到B点, 使得通货膨胀率上降低,但是失业率上 升;

Aetna School of Management, Shanghai Jiao Tong University

Macroeconomics

菲力普斯曲线

货币和财政政策都可以使总需求 曲线移动,并且使点在菲力普斯曲线 上位移。

Aetna School of Management, Shanghai Jiao Tong University

Macroeconomics

总需求较低时的较低产量,总需 求增加时产量较高

Aetna School of Management, Shanghai Jiao Tong University

Macroeconomics

菲力普斯曲线的移动

短期与长期的菲力普斯曲线 由于预期的作用,短期菲力普斯曲线不断右移 ,形成长期菲力普斯曲线。 如图35-5,原通货膨胀率在A点,因为政策调 控达到了B点,则人们会形成对这一空间的通 货膨胀率的预期,并要求将工资上升到这一预 期水平,企业因为劳动成本没有变,雇工数又 恢复到原来水平,

Aetna School of Management, Shanghai Jiao Tong University

Macroeconomics

菲力普斯曲线的移动

长期菲力普斯曲线 垂直的长期菲力普斯曲线如何于总需求、

总供给模型相关 长期总供给曲线是一条垂直线,货币供给 增加提高了总需求,总需求曲线从低到高的 移动,仅提高了物价水平,产量水平保持不 变; 因此,货币供给的增长仅提高了通货膨胀 率,失业率保持不变。 Aetna School of Management, Shanghai Jiao Tong University

布兰查德宏观经济学第七版第7版英文版chapter (19)

Macroeconomics, 7e (Blanchard)Chapter 19: Output, the Interest Rate, and the Exchange Rate19.1 Equilibrium in the Goods Market1) Assume that the price levels in two countries are constant. In this situation, we know thatA) neither the real nor the nominal exchange rate can change.B) the real exchange rate can change, while the nominal exchange rate is constant.C) the nominal exchange rate can change, while the real exchange rate is constant.D) the real and nominal exchange rate must move together, changing by the same percentage.E) the nominal exchange rate will fluctuate more widely than the real exchange rate. Answer: DDiff: 12) An increase in the real exchange rate will causeA) an increase in net exports.B) an increase in the quantity of imports.C) an increase in output.D) a decrease in government spending.E) all of the aboveAnswer: BDiff: 13) As the economy moves up and to the right along the IS curve, which of the following will occur when exchange rates are flexible?A) investment spending increasesB) consumption increasesC) the domestic currency depreciatesD) all of the aboveE) none of the aboveAnswer: DDiff: 14) In an economy operating under flexible exchange rates, explain why the IS curve is downward sloping.Answer: A reduction in i (assume zero inflation) will cause investment to increase for reasons discussed before. This causes an increase in Z and Y. There is a second effect now embedded in the IS curve. As i falls, the demand for the domestic currency drops causing a depreciation. This depreciation causes NX to rise and demand to rise even more. So, there are two components of demand that now change as i changes: I and NX.Diff: 219.2 Equilibrium in Financial Markets1) In order for an individual to be indifferent between holding foreign or domestic bonds,A) the Marshall-Lerner condition must hold.B) the foreign and domestic interest rates must be equal.C) the expected rate of depreciation of the domestic currency is zero.D) the interest parity condition must hold.Answer: DDiff: 12) The interest parity condition indicates that the domestic interest rate must be equal toA) the foreign interest rate.B) the expected rate of depreciation of the domestic currency.C) the expected rate of appreciation of the domestic currency.D) the foreign interest rate minus the expected rate of appreciation of the foreign currency.E) none of the aboveAnswer: EDiff: 13) Assume that the interest parity condition holds. Also assume that the U.S. interest rate is 8% while the U.K. interest rate is 6%. Given this information, financial markets expect the pound toA) depreciate by 14%.B) depreciate by 2%.C) appreciate by 2%.D) appreciate by 6%.E) appreciate by 14%.Answer: CDiff: 24) Assume that the interest parity holds and that the dollar is expected to depreciate against the pound. Given this information, we know thatA) U.S. and U.K. interest rates are equal.B) the U.S. interest rate exceeds the U.K. interest rate.C) the U.K. interest rate exceeds the U.S. interest rate.D) individuals will prefer to hold U.S. bonds because the U.S. interest rate exceeds the U.K. interest rate.E) none of the aboveAnswer: BDiff: 25) In an open economy, we know that individuals must choose between which of the following?A) domestic bonds and foreign currencyB) foreign goods and domestic currencyC) domestic and foreign bondsD) domestic goods and foreign currencyE) none of the aboveAnswer: CDiff: 16) A real appreciation will tend to causeA) an increase in exports.B) a reduction in imports.C) an increase in net exports.D) a reduction in demand for domestic goods.E) none of the aboveAnswer: DDiff: 17) A reduction in the real exchange rate will causeA) a reduction in net exports.B) a reduction in the quantity of imports.C) a reduction in output.D) an increase in government spending.E) all of the aboveAnswer: BDiff: 18) Assume that the interest parity condition holds. Also assume that the U.S. interest rate is 6% while the U.K. interest rate is 8%. Given this information, financial markets expect the pound toA) depreciate by 14%.B) depreciate by 2%.C) appreciate by 2%.D) appreciate by 6%.E) appreciate by 14%.Answer: BDiff: 29) Assume that the interest parity holds and that the dollar is expected to appreciate against the pound. Given this information, we know thatA) U.S. and U.K. interest rates are equal.B) the U.S. interest rate exceeds the U.K. interest rate.C) the U.K. interest rate exceeds the U.S. interest rate.D) individuals will prefer to hold U.S. bonds because the U.S. interest rate exceeds the U.K. interest rate.E) none of the aboveAnswer: CDiff: 210) A real depreciation will tend to causeA) a reduction in exports.B) an increase in imports.C) a reduction in net exports.D) an increase in demand for domestic goods.E) none of the aboveAnswer: DDiff: 111) Explain what the IP curve is and why it is upward sloping.Answer: The IP curve represents the combinations of i and E that maintain the interest parity condition. As i falls, foreign bonds will have a higher expected return. The demand for the dollar will fall causing an immediate depreciation. So, the drop in i causes E to fall. E will fall until all of the drop in i is offset by the expected appreciation of the dollar.Diff: 112) Suppose the domestic and foreign interest rates are both initially equal to 3%. Now suppose the domestic interest rate rises to 5%. Explain what effect this will have on the exchange rate. Also explain what must occur for the interest parity condition to be restored.Answer: Domestic bonds will have a higher return causing the demand for the domestic currency to rise. The dollar will appreciate. It will continue to appreciate as long as the return on domestic bonds exceeds the return on foreign bonds. This immediate appreciation will equal an expected depreciation of the domestic currency that equates the expected returns. So, the dollar will appreciate by 2%.Diff: 213) Suppose the domestic and foreign interest rates are both initially equal to 4%. Now suppose the foreign interest rate rises to 6%. Explain what effect this will have on the exchange rate. Also explain what must occur for the interest parity condition to be restored.Answer: Domestic bonds will have a lower return causing the demand for the domestic currency to fall. The dollar will depreciate. It will continue to depreciate as long as the return on domestic bonds is less than the return on foreign bonds. This immediate depreciation will equal an expected appreciation of the domestic currency that equates the expected returns. So, the dollar will depreciate by 2%.Diff: 219.3 Putting Goods and Financial Markets Together1) As the economy moves up and to the left along the IS curve, which of the following will occur when exchange rates are flexible?A) investment spending decreasesB) consumption decreasesC) the domestic currency appreciatesD) all of the aboveE) none of the aboveAnswer: DDiff: 12) In an open economy under flexible exchange rates, a reduction in the interest rate will cause a reduction in which of the following?A) investmentB) the exchange rate, EC) net exportsD) all of the aboveE) none of the aboveAnswer: BDiff: 23) In an open economy under flexible exchange rates and represented by the IS-LM-IP model, a reduction in government spending will cause a reduction in which of the following?A) net exportsB) the exchange rate, EC) exportsD) all of the aboveE) none of the aboveAnswer: CDiff: 24) In an open economy under flexible exchange rates, a reduction in consumer confidence that causes a reduction in consumption will cause which of the following?A) an appreciation of the domestic currencyB) a reduction in the exchange rate, EC) a reduction in net exportsD) all of the aboveE) none of the aboveAnswer: ADiff: 25) In an open economy under flexible exchange rates, expansionary monetary policy that results in an increase in the money supply will always causeA) an increase in output.B) an increase in exports.C) a reduction in the exchange rate, E.D) all of the aboveE) only A and CAnswer: DDiff: 26) Assume that the interest parity condition holds and that both the expected exchange rate and foreign interest rate are constant. Given this information, a reduction in the domestic interest rate will causeA) a reduction in the exchange rate expected in the future.B) a reduction in the current exchange rate.C) greater depreciation of the domestic currency expected in the future.D) all of the aboveE) none of the aboveAnswer: BDiff: 27) The exchange rate policy of the United States isA) the EMS.B) a crawling peg.C) a float.D) a fixed rate within a band.E) none of the aboveAnswer: CDiff: 18) In a flexible exchange rate regime, an increase in the foreign interest rate (i*) will causeA) the IP curve to shift to the left/up.B) the IP curve to shift to the right/down.C) a movement along the IP curve.D) neither a shift nor movement along the IP curve.Answer: BDiff: 39) In a flexible exchange rate regime, a reduction in the foreign interest rate (i*) will causeA) the IP curve to shift to the left/up.B) the IP curve to shift to the right/down.C) a movement along the IP curve.D) neither a shift nor movement along the IP curve.Answer: ADiff: 310) In a flexible exchange rate regime, an increase in the expected future exchange rate will causeA) the IP curve to shift to the left/up.B) the IP curve to shift to the right/down.C) a movement along the IP curve.D) neither a shift nor movement along the IP curve.Answer: BDiff: 311) In a flexible exchange rate regime, a reduction in the expected future exchange rate will causeA) the IP curve to shift to the left/up.B) the IP curve to shift to the right/down.C) a movement along the IP curve.D) neither a shift nor movement along the IP curve.Answer: ADiff: 312) Assume the interest parity condition holds and that initially i = i*. A reduction in the domestic interest rate will causeA) an increase in the demand for the domestic currency.B) a reduction in E.C) an expected depreciation of the domestic currency.D) all of the aboveAnswer: DDiff: 213) Assume the interest parity condition holds and that initially i = i*. A reduction in the foreign interest rate (i*) will causeA) an increase in the demand for the domestic currency.B) an increase in E.C) an expected depreciation of the domestic currency.D) all of the aboveAnswer: CDiff: 314) Explain what effect each of the following events will have on the IS curve in a flexible exchange rate regime: (1) an increase in foreign output; (2) a reduction in the foreign interest rate; and (3) an increase in the domestic interest rate.Answer: An increase in Y* causes X to rise, Z to rise, and the IS curve to shift to the right. A reduction in i* will cause an appreciation of the domestic currency, a reduction in NX, and a leftward shift in the IS curve. A change in i will only cause a movement along the IS curve. Diff: 215) Assume the exchange rate is allowed to fluctuate freely. Using the IS-LM-IP model, graphically illustrate and explain what effect a reduction in foreign output (Y*) will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: A reduction in Y* will cause a reduction in X and NX. This causes the IS curve to shift to the left. As demand falls, production will drop. The drop in Y will cause a reduction in money demand. As money demand falls, i will fall causing a depreciation. So, some of the effects of Y* on NX will be offset by the increase in NX caused by the depreciation. We will observe a reduction in NX, a reduction in Y, a reduction in i, and a reduction in E.Diff: 216) Assume the exchange rate is allowed to fluctuate freely. Using the IS-LM-IP model, graphically illustrate and explain what effect an increase in foreign output (Y*) will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: An increase in Y* will cause an increase in X and NX. This causes the IS curve to shift to the right As demand rises, production will increase. The increase in Y will cause an increase in money demand. As money demand rises, i will rise causing an appreciation. So, some of the effects of Y* on NX will be offset by the decrease in NX caused by the appreciation. We will observe an increase in NX, an increase in Y, an increase in i, and an increase in E.Diff: 219.4 The Effects of Policy in an Open Economy1) For this question, assume that there is a simultaneous tax increase and monetary expansion. Ina flexible exchange rate regime, we know with certainty thatA) the exchange rate and output would both increase.B) the exchange rate would increase and output would decrease.C) the exchange rate would decrease.D) the exchange rate would decrease and output would increase.E) none of the aboveAnswer: CDiff: 22) For this question, assume that there is a simultaneous increase in government spending and monetary contraction. In a flexible exchange rate regime, we know with certainty that such a policy mix will cause which of the following?A) an increase in the domestic interest rateB) an increase in the exchange rateC) a reduction in net exportsD) all of the aboveE) only A and CAnswer: DDiff: 23) Suppose there are two countries that are identical in every way with the following exception. Country A is pursuing a fixed exchange rate regime and country B is pursuing a flexible exchange rate regime. Suppose taxes are increased in both countries rises by the same amount. Given this information, we know thatA) the change in output in A will be greater than in B.B) the change in output in B will be greater than in A.C) the change in output will be the same in both countries.D) the relative output effects are ambiguous.Answer: ADiff: 34) Contractionary monetary policy in a flexible exchange rate regime will causeA) a shift of the IP curve.B) a depreciation of the domestic currency.C) an increase in E.D) no change in E.Answer: CDiff: 15) Expansionary monetary policy in a flexible exchange rate regime will causeA) a shift of the IP curve.B) an appreciation of the domestic currency.C) a reduction in E.D) no change in E.Answer: CDiff: 16) Assume the exchange rate is allowed to fluctuate freely. Using the IS-LM-IP model, graphically illustrate and explain what effect an increase in government spending will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: An increase in G will cause Z to increase and the IS curve to shift right. As demand increases, Y will rise causing an increase in money demand. The increase in money demand will cause an increase in i. As i rises, the demand for the domestic currency will increase causing an appreciation. This appreciation will cause a drop in NX. Any drop in I and the reduction in NX only partially offset the effects of the increase in G on demand and output.Diff: 27) Assume the exchange rate is allowed to fluctuate freely. Using the IS-LM-IP model, graphically illustrate and explain what effect monetary contraction will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: A reduction in M will cause the LM curve to shift up and the domestic interest rate to rise. As i rises, the return on domestic bonds is greater than foreign bonds. This causes an appreciation and a reduction in NX. So, the demand for goods falls via the drop in I and NX. We will observe a higher domestic interest rate, an increase in E, a drop in I, a reduction in NX, and a reduction in Y.Diff: 219.5 Fixed Exchange Rates1) Suppose a country with a fixed exchange rate decides to reduce the price of its currency. This change in policy is calledA) an appreciation.B) a depreciation.C) a peg.D) a devaluation.E) a revaluation.Answer: EDiff: 12) Under a "crawling peg" system, a country's exchange rateA) is fixed except for small, surprise changes.B) changes at a predetermined rate against the dollar or some other major currency.C) can fluctuate within a narrow band.D) can change, but the changes are kept secret from the public.E) is determined by the central bank of another country.Answer: BDiff: 13) In 2005, China increased the price of its currency while continuing to pursue a fixed exchange rate. This change in policy is calledA) an appreciation.B) a depreciation.C) a peg.D) a devaluation.E) a revaluation.Answer: DDiff: 14) For this question, assume that the economy is operating in a fixed exchange rate regime and that perfect capital mobility exists. Given this information, which of the following will occur?A) The domestic and foreign interest rates must be equal.B) The central bank cannot use monetary policy to affect domestic output.C) An expansionary fiscal policy will require that the central bank increase the money supply.D) all of the aboveE) none of the aboveAnswer: DDiff: 25) Suppose a country switches from a fixed to a flexible exchange rate. Which of the following will occur as a result of this change?A) Monetary policy will become a less effective tool for changing output.B) A given change in government spending will now have a greater effect on output.C) Both fiscal and monetary policy will become more effective in changing GDP.D) Both fiscal and monetary policy will become completely ineffective in changing GDP.E) none of the aboveAnswer: EDiff: 26) A common argument for fixed exchange rates is that theyA) give central banks greater freedom in adjusting their economy's level of output.B) forever free the central bank from have to adjust the exchange rate to fundamental changes in the economy.C) make trade more costly, and thus encourage domestic citizens to buy domestically produced output.D) all of the aboveE) none of the aboveAnswer: EDiff: 17) In practice, under the EMS, a member countryA) could never change its interest rate.B) could change its interest rate only if other countries changed theirs as well.C) must apply to a special European Commission in order to change its interest rate.D) had complete freedom in choosing the interest rate it wanted.E) had complete freedom in choosing its interest rate only if it is a very small country. Answer: BDiff: 18) In the early 1990s, which nation took the lead in driving up European interest rates?A) SpainB) FranceC) GermanyD) EnglandE) none of the aboveAnswer: EDiff: 19) In the early 1990s, European unemployment rose largely because ofA) reductions in stock prices.B) undervalued currencies.C) overvalued currencies.D) high inflation.E) none of the aboveAnswer: ADiff: 110) Assume that the current exchange rate between U.K. pound and the U.S. dollar is 2 (E = 2.0). If interest parity holds, and the U.S. interest rate is 6% while the U.K. interest rate is 8%, the expected exchange rate in one year isA) 1.98.B) 1.99.C) 2.01.D) 2.02.E) 2.04.Answer: CDiff: 211) Assume policy makers in a fixed exchange rate regime decide to peg the exchange rate at a higher level. This is calledA) a devaluation.B) a revaluation.C) a depreciation.D) an appreciation.Answer: ADiff: 112) Assume policy makers in a fixed exchange rate regime decide to peg the exchange rate at a lower level. This is calledA) a devaluation.B) a revaluation.C) a depreciation.D) an appreciation.Answer: BDiff: 113) The European Monetary System represented aA) exchange rate regime with 'bands.'B) crawling peg.C) a flexible exchange rate regime.D) none of the aboveAnswer: ADiff: 114) Suppose policy makers are pursuing a policy to fix the exchange rate. In such a system with perfect capital mobility, an open market purchase of domestic bonds by the domestic central bank will eventually result inA) a permanent increase in the monetary base.B) a permanent reduction in the monetary base.C) a change in the composition of the monetary base.D) a gradual reduction in the domestic interest rate.Answer: CDiff: 215) Suppose policy makers are pursuing a policy to fix the exchange rate. In such a system with perfect capital mobility, an open market sale of domestic bonds by the domestic central bank will eventually result inA) a permanent increase in the monetary base.B) a permanent reduction in the monetary base.C) a gradual reduction in the domestic interest rate.D) a change in the composition of the monetary base.Answer: DDiff: 216) Suppose a country is pursuing a fixed exchange rate regime with imperfect capital mobility. The ability of that country to move its domestic interest rate while maintaining its exchange rate will depend onA) the degree of development of its financial markets.B) the degree of capital controls.C) the amount of foreign exchange it holds.D) all of the aboveE) both A and BAnswer: DDiff: 217) Under a fixed exchange rate regime, the central bank must act to keepA) P = P*.B) the real exchange rate fixed.C) i = i*.D) E = 1.E) none of the aboveAnswer: ADiff: 218) For this question, assume that policy makers are pursuing a fixed exchange rate regime. Now suppose that an increase in stock market wealth causes an increase in consumption. Which of the following will tend to occur in a fixed exchange rate regime?A) an increase in YB) an increase in the money supplyC) no change in the domestic interest rateD) all of the aboveAnswer: DDiff: 2suppose that households decide to decrease consumption because of, for example, a reduction in consumer confidence. Given this information, we would expect which of the following to occur?A) a reduction in the domestic interest rateB) an increase in EC) a reduction in ED) a reduction in investmentE) none of the aboveAnswer: DDiff: 220) For this question, assume that policy makers are pursuing a fixed exchange rate regime. Now suppose a budget is passed that calls for a reduction in government spending. This reduction in government spending will cause which of the following to occur?A) a reduction in i and an increase in EB) a reduction in investmentC) no change in outputD) no change in net exportsE) an increase in importsAnswer: BDiff: 221) Under a fixed exchange rate regime, suppose there is a reduction in housing wealth that causes a reduction in consumption. This wealth-induced reduction in consumption will causeA) a reduction in investment.B) an increase in net exports.C) a reduction in imports.D) all of the aboveE) none of the aboveAnswer: DDiff: 222) Under a fixed exchange rate regime, expansionary fiscal policy will tend to cause which of the following?A) an increase in importsB) an increase in net exportsC) a reduction in investmentD) all of the aboveAnswer: ADiff: 2suppose that a reduction in stock market wealth causes a decrease in consumption. Which of the following will tend to occur in a fixed exchange rate regime?A) a reduction in YB) a reduction in the money supplyC) no change in the domestic interest rateD) all of the aboveAnswer: DDiff: 224) For this question, assume that policy makers are pursuing a fixed exchange rate regime. Now suppose that households decide to increase consumption because of, for example, an increase in consumer confidence. Given this information, we would expect which of the following to occur?A) an increase in the domestic interest rateB) a reduction in EC) an increase in ED) an increase in investmentE) none of the aboveAnswer: DDiff: 225) Under a fixed exchange rate regime, suppose there is an increase in housing wealth that causes an increase in consumption. This wealth-induced increase in consumption will causeA) an increase in investment.B) a reduction in net exports.C) an increase in imports.D) all of the aboveE) none of the aboveAnswer: DDiff: 226) Under a fixed exchange rate regime, contractionary fiscal policy will tend to cause which of the following?A) a reduction in importsB) a reduction in net exportsC) an increase in investmentD) all of the aboveAnswer: ADiff: 227) For a country pursuing a fixed exchange rate regime, what does the interest parity condition imply about domestic and foreign interest rates? Explain.Answer: As long as the fixed exchange rate regime is credible, the interest rates must be equal. If the exchange rate regime is credible, we know that there will be no expected appreciation or depreciation so i = i*.Diff: 128) Assume the exchange rate is fixed. Using the IS-LM model, graphically illustrate and explain what effect a reduction in consumer confidence will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: A reduction in consumer confidence will cause a drop in C and will cause demand to fall and the IS curve to shift to the left. As Y falls, money demand will fall and the domestic interest rate will tend to fall. If i falls, there will be tremendous pressure on the domestic currency to depreciate as demand falls. The central bank cannot let this occur. To prevent this, it must reduce the money supply so that i does not fall. We will observe a drop in Y, no change in i, a reduction in I (via the drop in I), and an increase in NX caused by the drop in imports.Diff: 229) Assume that policy makers are pursuing a fixed exchange rate regime. Now suppose that the foreign interest rate increases. Discuss what policy makers must do to maintain the pegged exchange rate. Also discuss what effect this will have on domestic output and net exports. Answer: If i* increases, there will be pressure on the domestic currency to depreciate. To prevent this, the domestic central bank must raise its interest rate so that it rises by the same amount as i*. In this case, the LM curve will shift up so that the new equilibrium interest rate is equal to the now higher foreign interest rate. As i rises, E does not change. However, I will fall causing a reduction in demand and output. As Y falls, imports will fall and NX will increase. Diff: 230) To what extent can monetary policy be used to affect output in a fixed exchange rate regime? Explain.Answer: It cannot. To peg the exchange rate, the central bank must keep the domestic interest rate equal to the exogenous foreign interest rate. The domestic central bank cannot independently change its interest rate.Diff: 231) Assume the exchange rate is allowed to fluctuate freely. Using the IS-LM-IP model, graphically illustrate and explain what effect a reduction in government spending will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: A reduction in G will cause Z to decrease and the IS curve to shift left. As demand decreases, Y will fall causing a decrease in money demand. The decrease in money demand will cause an decrease in i. As i falls, the demand for the domestic currency will decrease causing a depreciation. This depreciation will cause a rise in NX. Any increase in I and the increase in NX only partially offset the effects of the reduction on demand and output.Diff: 232) Assume the exchange rate is allowed to fluctuate freely. Using the IS-LM-IP model, graphically illustrate and explain what effect monetary expansion will have on the domestic economy. In your graphs, clearly label all curves and equilibria.Answer: An increase in M will cause the LM curve to shift down and the domestic interest rate to fall. As i falls, the return on domestic bonds is less than foreign bonds. This causes an depreciation and an increase in NX. So, the demand for goods rises via the increase in I and NX. We will observe a lower domestic interest rate, a reduction in E, an increase in I, an increase in NX, and an increase in Y.Diff: 2。

萨缪尔森《宏观经济学》(第19版)笔记(第14章 开放经济的宏观经济学)

萨缪尔森《宏观经济学》(第19版)第14章开放经济的宏观经济学复习笔记跨考网独家整理最全经济学考研真题,经济学考研课后习题解析资料库,您可以在这里查阅历年经济学考研真题,经济学考研课后习题,经济学考研参考书等内容,更有跨考考研历年辅导的经济学学哥学姐的经济学考研经验,从前辈中获得的经验对初学者来说是宝贵的财富,这或许能帮你少走弯路,躲开一些陷阱。

以下内容为跨考网独家整理,如您还需更多考研资料,可选择经济学一对一在线咨询进行咨询。

一、对外贸易与经济活动1.开放经济中的净出口和产出(1)净出口和产出对外贸易包括进口和出口。

进口是指由国外提供而在本国国内消费的商品和服务。

出口是指在国内生产而被别国购买的商品和服务。

净出口定义为出口的商品和服务减去进口的商品和服务的净值。

与净出口相应的一个概念是对外净投资,它表示一国在国外的净储蓄或投资,并且大致等于净出口的价值。

在一个开放的经济中,一国的支出可能会不同于其产出。

国内支出(有时称国内需求)等于消费加国内投资再加政府采购。

即:()C I G国内支出国内需求=++国内总产出(或国内生产总值GDP)与国内支出有两点不同。

第一,国内支出的一部分用于购买外国生产的产品,即进口(Im)。

第二,国内产出的一部分将以出口形式(Ex)销往国外。

国内产出与国内支出之间的差额就等于出口减去进口,即净出口Im=-。

X Ex因此在开放经济中,国内总产出数量或GDP,等于消费、国内投资、政府购买和净出口之和,即:国内总产出GDP C I G X==+++(2)贸易和净出口的决定因素进口的数量和价值将受到本国产业以及本国和别国产品相对价格的影响。

当本国GDP 上升时,进口将增加;当本国产品的价格相对于别国产品价格下降时,本国的进口将减少。

出口主要取决于其贸易伙伴的产出,以及本国的出口品相对于竞争对手的产品的价格。

当其他国家的产出上升时,或者,当本币贬值时,出口量和出口额就趋于增长。

2.贸易对GDP的短期影响(1)开放经济下国民收入的决定在开放经济下,总支出曲线由封闭经济下的C I G+++。

多恩布什《宏观经济学》第十版英文原版I19revised

CHAPTER 19BIG EVENTS: THE ECONOMICS OF DEPRESSION,HYPERINFLATION, AND DEFICITSChapter Outline•The Great Depression and its impact on macroeconomics•Money and inflation•Monetarism and the rational expectations approach•The effects of hyperinflation•Disinflation and the sacrifice ratio•Credibility•The Fed's dilemma•Deficits, money growth, and seigniorage•The inflation tax•Federal government outlays and revenues•The primary deficit•The debt-to-income ratio•The burden of the debt•Financing Social SecurityChanges from the Previous EditionThe material in this chapter was in Chapter 18 in the previous edition. It has been updated, Boxes 19-2 and 19-5 have been added, and other boxes have been renumbered accordingly. Introduction to the MaterialThe Great Depression in the 1930s presented an economic crisis of enormous proportions. Between 1929 and 1933, real GDP in the U.S. fell by almost 30% and unemployment reached an all-time high of almost 25%. While the economy grew fairly rapidly from 1933-37, unemployment remained in the double digit range. In 1937/38, there was another major recession and the unemployment rate remained above 5% until 1942. In the 1930s unemployment averaged 18.8%, but by 1939 real GDP had recovered to its 1929 level.The classical economists of the time were not equipped to explain the existence of such substantial and persistent unemployment or to prescribe policies to deal with it. Only in 1936, in John Maynard Keynes’book The General Theory of Employment, Interest and Money, was a macroeconomic theory introduced upon which policies to keep the economy out of future recessions could be based. Keynes’ theory provided an explanation of what had happened during the Great Depression and suggested policies that might have prevented it.The stock market crash of 1929 is often seen as the catalyst for the Great Depression but, in fact, economic activity actually started to decline even before the crash. What might well have393been an average recession turned into a very severe depression due to the inept economic policies employed at the time. The Fed failed to provide needed liquidity to banks and did little to prevent the collapse of the financial system. The huge contraction in money supply due to the large numbers of bank failures caused the economic downturn. Fiscal policy was weak at best. Politicians concerned with balancing the budget raised taxes to match increases in government spending, so the decline in aggregate demand was not counteracted.Many other countries also suffered during the same period, mainly as a result of the collapse of the international financial system and the enactment of high tariffs worldwide. These policies were designed to protect domestic producers in an attempt to improve each country’s domestic trade balance at the expense of foreign trading partners. However, the attempts to "export" unemployment ultimately resulted in an overall decline in world trade and production.In the U.S., many institutional changes and administrative actions, collectively known as the New Deal, were implemented in the 1930s. The Fed was reorganized and new institutions were created, including the FDIC, the SEC, and the Social Security Administration. Public works programs and a program to establish orderly competition among firms were also implemented.The experience of the Great Depression led to the belief that the economy is inherently unstable and active stabilization policy is needed to maintain full employment. Keynes was an advocate of active government policy. In his work, he explained what had happened in the Great Depression and what could be done to avoid a recurrence. Many years later, Milton Friedman and Anna Schwartz offered a different explanation. In their book A Monetary History of the United States, Friedman and Schwartz argued that the severe decline in money supply, caused by the Fed’s failure to prevent banks from failing, was the reason for the severity of the Great Depression. They claimed that monetary policy is very powerful and that fluctuations in money supply can explain most of the fluctuations in GDP over the last century. This argument provided the impetus for new research on the effects of fiscal and monetary stabilization policies. While economists are still debating these issues, we can conclude that monetary policy can affect the behavior of output in the short and medium run, but not in the long run. In the long run, increases in the growth rate of money supply will simply lead to increases in the rate of inflation. Box 19-3 gives an overview of the monetarist positions on the importance of money for the economy, while Box 19-2 quotes Fed Chairman Ben Bernanke, who admits that the magnitude of the Great Depression was indeed the result of the Fed’s action—or, more accurately, inaction.The link between inflation and monetary growth can easily be derived from the quantity theory of money equation:MV = PY ==> %∆M + %∆V = %∆P + %∆Y ==> m + v = π + y ==> π = m - y + v In other words, the rate of inflation (%∆P = π) is determined by the difference between the growth rate of nominal money supply (%∆M = m) and the growth rate of real output (%∆Y = y), adjusted for the percentage change in the income velocity of money (%∆V = v).Figure 19-1 shows that trends in the rate of inflation and the growth of money supply (M2) have been somewhat similar over the last four decades. There is plenty of evidence to support the notion that in the long run, inflation is a monetary phenomenon here in the U.S. as well as in other countries. However, there are short-run variations, indicating that changes in velocity and output growth have also affected the inflation rate. By the mid 1990s, the relationship between394M2 growth and inflation had largely broken down, even for the long run. It is still true, however, that there has never been inflation in the long run without rapid growth of money supply, and the faster money grew the higher the rate of inflation.Although there is no exact definition, countries are said to experience hyperinflation when the inflation rate reaches 1,000% annually. Countries that have experienced hyperinflation have all had huge budget deficits which, in many cases, originated from increased government spending during wartime. A classical example is the German hyperinflation of 1922/23. In an economy experiencing hyperinflation, there is often widespread indexing, most likely to foreign exchange rates rather than to the price level, since prices are changing so fast. Eventually, hyperinflation becomes too much to bear and the government is forced to take harsh measures, including fiscal reform and the introduction of a new monetary unit pegging the new money to a foreign currency. Box 19-4 on the situation in Bolivia in the 1980s provides a good example of how hyperinflation can be stopped. It also points out that the costs are great in terms of decreasing per-capita income. In 1985, Bolivia stopped external debt service, raised taxes, reduced money creation, and stabilized the exchange rate. Inflation came down quickly, but per-capita income in 1989 was 35 percent less than it had been a decade earlier.In its fight against hyperinflation, Israel tried to keep unemployment rates low by instituting wage and price controls while also sharply cutting budget deficits and rationing credit. These measures reduced the rate of inflation significantly. In the late 1980s, the governments of Argentina and Brazil imposed wage-price controls but failed to supplement them with fiscal austerity, so the result was much less satisfactory, although they, like many South American countries eventually succeeded in lowering their inflation rates. In the early 1990s, countries in Eastern Europe experienced brief periods of high inflation during their adjustments from centrally planned economies to more market based economies (as shown in Table 19-6). There is no guarantee that periods of hyperinflation will not surface again. New Box 19-5 describes the situation in Zimbabwe where the decision made in 2006 to print more money to finance higher government spending led to inflation rates in excess of 1,000%.When inflation is high, policy makers must focus on reducing it without causing a major economic downturn. This is fairly difficult to accomplish, however, since labor contracts tend to reflect past expectations and new contract negotiations take time. In addition, it may be difficult for a central bank to gain credibility in its fight against inflation because of its behavior in the past. Credibility is important, since inflationary expectations adjust down faster if people believe that a government is serious in its attempt to reduce inflation. If this is the case, the expectations-adjusted Phillips curve shifts to the left sooner and the economy adjusts more quickly to the full-employment level of output at a lower inflation rate. But some increase in unemployment is almost always needed to reduce inflation, since real wages need to adjust down to their full-employment level. The costs to society are often measured in terms of the sacrifice ratio, that is, the ratio of the cumulative percentage loss of GDP to the achieved reduction in the inflation rate.Probably all economists now agree with the monetarist propositions that rapid money growth tends to be inflationary and inflation cannot be kept low unless money growth is kept low. We also know that monetary policy has long and variable lags. But other monetarist positions remain more controversial, including those that suggest that the economy is inherently stable and that monetary targets are better than interest rate targets. The rational expectations approach can be seen as an extension of the monetarist approach, with a strong belief that markets clear rapidly395and people use all information available to them. This is why they advocate policy rules rather than discretion and place emphasis on the credibility of policy makers. Box 19-6 highlights the rational expectations approach.Any government that is unwilling to show fiscal restraint will ultimately be faced with excessive money growth and an increase in the inflation rate. Continued large government budget deficits create a policy dilemma for a central bank, which must decide whether to monetize the debt. If the central bank decides not to finance the debt, the increased borrowing needs of the government may drive interest rates up, leading to the crowding out of private spending. The central bank may then be blamed for slowing down economic growth. But if the central bank is worried about high interest rates and monetizes the debt in order to keep interest rates low, inflation may increase with the central bank taking the blame.The financing of government spending through the creation of high-powered money is an alternative to explicit taxation. Inflation acts like a tax since the government can spend more by printing money while people can spend less, since some of their income must be used to increase their nominal money holdings. The inflation tax revenue is defined as:inflation tax revenue = (inflation rate)*(the real money base).The ability of the government to raise additional tax revenue through the creation of money (and therefore inflation) is called seigniorage, and Table 19-7 shows some empirical evidence of the inflation tax revenue raised as percentage of GDP for some Latin American countries. However, there is a limit to how much revenue a government can raise through an inflation tax. As inflation increases, people reduce their currency holdings and banks reduce their excess reserves, since holding money becomes more costly. Eventually the real monetary base falls so much that the government's inflation tax revenue decreases. Figure 19-3 shows this graphically.While higher deficits can cause higher inflation if they are financed through money creation, higher inflation may also contribute to deficits, since inflation reduces the real value of tax payments. In addition, high nominal interest rates (caused by high inflation) raise the nominal interest payments the government must make on the national debt. The inflation-adjusted deficit corrects for that and is defined in the following way:inflation-adjusted deficit = total deficit - (inflation rate)*(national debt).Large government budget deficits and rapid monetary expansion seem to be inevitable parts of hyperinflation. The high rate of monetary expansion originates in the government's desire to raise its inflation tax revenue. However, the government can only be successful if it prints money faster than the public anticipates. Eventually, the process will break down, as the real money base becomes smaller and smaller.During the 1980s, the U.S. experienced very large budget deficits, which were temporarily brought under control in the late 1990s, only to increase sharply again in 2002. Figure 19-4 shows the trend in U.S. budget deficits as percentage of GDP, while Tables 19-8 and 19-9 give an overview of trends in the U.S. government's outlays and revenues. It is interesting to note that entitlements and interest payments on the national debt have increased significantly over the last396four decades. On the revenue side, corporate income taxes as a share of GDP have declined, while social insurance taxes have increased substantially.To highlight the role of the national debt in the budget, it is useful to distinguish between the actual budget deficit and the primary (non-interest) budget deficit. The U.S. budget deficits in the 1990s were actually more a result of high interest payments on the previously incurred debt than of government spending exceeding tax revenues. This is the legacy of past deficits. As the national debt accumulates, its interest costs accelerate, contributing even more to the budget deficit. The national debt is the result of all past and present budget deficits, and the process by which the Treasury finances the debt is called debt management. As old government securities mature, the Treasury issues new securities to make the payments on old ones.Robert Eisner has argued that it is important to recognize that the government has assets and not just debts. Any spending on infrastructure should be treated as accumulation of real capital and offset by the debt issued to pay for it. In other words, just like private spending, government expenditures should be separated into government “consumption” and government “investment.”With the U.S. gross national debt now exceeding $8.5 trillion (or over $28,000 per capita), it becomes important to consider its real burden. If individuals who hold government bonds consider an increase in government debt as an increase in their personal wealth, they will consume more and a lower share of GDP will be invested. This will lead to a lower rate of capital accumulation and slower future economic growth. Another concern is that foreigners hold a large part of the debt. Since the burden of future tax payments on this part of the debt (plus interest) will fall on U.S. taxpayers while the recipients of these payments will be foreigners, there will be a reduction in U.S. net wealth.High deficits cannot be sustained indefinitely, but as long as national income is growing faster than the national debt (implying a declining debt-income ratio), the potential for instability is fairly low. In the 1990s, there was widespread sentiment that government had grown too big and that sound fiscal policy had to be implemented. The fiscal restriction finally succeeded in turning the large budget deficits of the 1980s into budget surpluses in 1998. A debate quickly began among politicians about the best ways to put the surplus to use. Was it better to cut taxes, increase spending, or gradually pay off the national debt? The path chosen by the Bush administration was a massive tax cut, leading to renewed budget deficits in 2002.Another debate revolves around Social Security reform. There is increasing concern about the financial difficulties that the Social Security system will face in the near future. The system is financed to a large extent on a pay-as-you-go basis, with most of the earmarked taxes paid by current workers being used immediately to finance the Social Security benefits of current retirees. Such a transfer of resources from the young to the old can be accomplished if:• A growing population increases the ratio of workers to retirees. If population growth slows, however, then contributions have to be increased or benefits have to be cut.•High-income growth allows retirement benefits to be higher than past contributions, since the source of the benefits is the higher income of the younger generations. If income growth slows, however, then the system may face financing difficulties.•The political situation is favorable. A larger percentage of older people than younger people vote so the elderly can enforce the intergenerational transfer through the political system. But at some point, the young, who expect to receive lower benefits than their parents relative to their contributions, may refuse to support the system through their taxes.397While the Social Security system is often seen as a “forced savings system,” which makes sure that everyone accumulates some wealth for retirement, there is strong empirical evidence that the system actually reduces national saving due to its pay-as-you-go financing. The decline in saving reduces the rate of capital accumulation, which lowers productivity and future living standards.The Social Security trust fund actually has been growing as a result of the Social Security Reform of 1983, but current predictions are that the system will be bankrupt after 2045 when most of the baby-boomer generation will have retired. While most people do not wish to see the Social Security system totally abandoned, additional reforms are very likely in the near future. The central question is how to earn higher returns on the funds invested to prevent the system from insolvency and how to preserve equity for those who have already paid into the system. Suggestions for LecturingStudents who follow the news see stock prices fluctuate daily and they probably heard about past stock market bubbles and crashes. These students will be curious about the impact of major swings in stock market activity on the economy. Most people assume that the stock market crash of October, 1929 marked the beginning of the Great Depression and are not aware that economic activity had actually begun to decline earlier. A good way to introduce the material in this chapter is to ask: “Could a Great Depression happen again?” or “Do stock market crashes cause economic downturns?” Either will lead to a lively class discussion that can help to highlight several of the issues raised in the chapter. In this discussion the major stock market crash of October, 1987 and the decline in (especially high-tech) stock values that started in March, 2000 will undoubtedly come up. They are reminders that stock market bubbles will always eventually burst and that there is considerable risk associated with buying stocks.Most economists now agree that the magnitude of the Great Depression was exacerbated by inadequate fiscal and monetary policy responses. The Fed’s failure to inject e nough liquidity into the banking system to prevent failures led to a severe contraction in the supply of money and an economic downturn, and. Policy makers also did little initially to stimulate economic activity through fiscal policy. The severity of the economic situation in the 1930’s is not surprising to economists today, as no well-developed economic theory existed at the time that could deal with a disturbance of this magnitude. It was not until John Maynard Keynes offered an explanation of what had happened during the Great Depression and suggested ways to prevent future recessions that macroeconomists began to ponder the values of fiscal and monetary stabilization policies. It is no wonder that Keynes is seen by many as the “father of all macroeconomists.”Economic theories are generally pro ducts of their time and, as mentioned above, Keynes’macroeconomic theory was developed as a result of the Great Depression. His explanation and prescription for preventing future depressions were widely accepted, but did not have much impact on policy making in the U.S. until the 1960s, when the government followed (mostly fiscal) activist policies to ensure full employment.The handling of the major stock market crash of 1987 appears to indicate that policy makers have learned from past mistakes. Stock values dropped by more than 24% in October of 1987, but we did we not see a severe downturn in economic activity. Why not? For one, Alan398Greenspan, who had been appointed as chair of the Board of Governors of the Fed only a few months earlier, was conscious of what had happened in 1929 and immediately assured financial markets that the Fed would provide the liquidity needed to prevent a financial collapse. The Fed quickly started to undertake open market purchases in an effort to drive interest rates down. In addition, as a result of institutional changes implemented after the Great Depression, government now has a much larger role in the economy. Students should be aware that the Great Depression not only shaped modern macroeconomic thinking and approaches to stabilization policy, but also shaped the structure of many U.S. institutions. Instructors may want to spend some time talking about these institutions and their importance to our economy.It also should be noted that the economy was in much better shape when the stock market crashed in 1987 than it was in 1929. While we can only speculate on what would have happened had the economy been in worse shape, the existence of programs such as Social Security and unemployment insurance would have dampened the severity of a downturn by providing some automatic stability. In addition, the existence of the FDIC, which insures all bank deposits up to $100,000, now serves to avoid panic in financial markets and runs on banks.The recession in 1981/82, which was the most severe recession since the Great Depression and brought the unemployment level close to 11%, provides another good example that policy makers now react much more swiftly to major economic upheavals. Even though the recession was fairly severe, it did not last for an extended period, since expansionary policies were implemented almost immediately after the magnitude of the downturn became clear.There are still disagreements about the primary causes for the Great Depression and these should be clarified. The Keynesian explanation concentrates on spending behavior, that is, the reduction in consumption and the collapse of investment. The decrease in aggregate demand was exacerbated by the restrictive fiscal policy implemented by the government trying to balance the budget. The monetarist explanation concentrates on the behavior of money and asserts that the Fed failed to prevent the collapse of the banking system. The large number of bank failures led to a loss of confidence in the banking system, an enormous increase in the currency-deposit ratio, and therefore a huge decrease in the money multiplier. Monetarists see the resulting severe decline in money supply as the cause of the Great Depression. Both explanations fit the facts and it is important for instructors to point out that there is no inherent conflict between them; in fact, they complement one another.While the programs of the New Deal are largely credited with revitalizing the economy in the mid-1930s, probably one of the most important factors was the sharp increase in money supply, starting in 1933. This is often a forgotten fact. It should be noted that while unemployment remained high, the deflation of prices and wages stopped after 1933, and output began to rebound. In addition, some of the programs implemented by the government after the Great Depression helped to keep wages from falling further.The fact that unemployment’s downward pressure on wages tends to weaken if high unemployment is persistent should also be mentioned at this point. The possibility that the behavior of nominal wages affects the rate of inflation should be discussed with reference to the situation in some European countries, where the unemployment rate has been above the levels experienced in the U.S. for quite some time.The German hyperinflation of 1922-23, when the inflation rate averaged 322% per month, provides another example of a major economic event that shaped macroeconomic thinking. But399students will probably prefer to discuss more recent examples, such as the Bolivian experience of the 1980s highlighted in Box 19-4 or the situation in Zimbabwe starting in 2006. Both cases make clear that the cost of stopping hyperinflation can be extremely high in terms of a decreased standard of living. The discussion should make it clear that large budget deficits and rapid monetary growth are always prevalent in times of hyperinflation, and only draconian measures can ensure a reduction in inflationary expectations. Without such measures the economy will collapse and has to be completely restructured, with the introduction of a new monetary unit that may be pegged to a foreign exchange rate.There is no exact definition of hyperinflation, but it is said to exist when the inflation rate reaches 1,000% on an annual basis. Students will always remember the following definition of inflation in general: “inflation is nothing more than too much money chasing too few goods.” But is inflation “always and everywhere a monetary phenomenon,” as Milton Friedman put it? Figure 19-1 indicates that the rate of inflation and the growth rate of M2 show somewhat similar long-run trends (at least until about 1993), but there are large variations in the short run. In other words, the link between monetary growth and the inflation rate is by no means precise. For one, growth in output affects the inflation rate and real money holdings. Interest rate changes and financial innovations also affect desired money holdings and therefore the income velocity of money. Empirical evidence indicates that the velocity of M2 has shown a fairly constant long-run trend from the 1960s to the 1990s, while the velocity of M1 has fluctuated significantly over the last few decades. Considering the enormous changes that took place in the U.S. banking system in the 1980s, it is surprising that the income velocity of M2 actually stayed as stable as it did. By the late 1990s, the link between M2 growth and the inflation rate had largely broken down; the possible causes and any monetary policy implications should be discussed.By now, students should be familiar with the quantity theory of money equation and should be able to derive the equation that shows the long-run relationship between money growth, output growth, velocity changes, and the rate of inflation. We can thus derive the following:MV = PY ==> %∆M + %∆V = %∆P + %∆Y ==> %∆P = %∆M - %∆Y + %∆V==> π = m - y + v.This equation indicates that higher growth rates of money (%∆M = m) adjusted for growth in output (%∆Y = y) and changes in velocity (%∆V = v) are associated with higher inflation rates (%∆P = π). The strict monetary growth rule is based on this equation and suggests that a zero inflation rate can be achieved if money supply is only allowed to grow at the same rate as the long-run trend of output, assuming that velocity remains stable. It should be made clear, that this equation shows only a long-run relationship and that output growth and velocity can be highly variable in the short run, causing great variations in the inflation rate.Besides looking at the role of monetary growth in determining the inflation rate, instructors may also want to spend some time looking at the role of nominal wages and labor productivity. Just by recalling the simple equationw = W/P,400。

2024全新高鸿业宏观经济学

03

失业、通货膨胀与经济周期

失业的定义、类型与度量

失业的定义

失业是指具有劳动能力和劳动意愿的个体在现行市场条件下无法 找到或保持一份合适的工作。

失业的类型

包括摩擦性失业、结构性失业、周期性失业和自然失业等。

失业的度量

通常采用失业率来衡量一个国家或地区的失业状况,失业率是指 失业人数占劳动力总数的百分比。

资本市场的定义、功能与工具

要点一

定义

资本市场是指进行长期(通常是一年以 上)资金借贷和交易的场所。它主要包 括股票市场、债券市场、基金市场等。

要点二

功能

资本市场的主要功能是筹集和分配长期 资金,为企业的长期发展提供资金支持, 同时为投资者提供长期投资的机会。

要点三

工具

资本市场的工具主要有股票、债券、基 金等。其中,股票是代表公司所有权的 有价证券,债券是代表公司的基金管理人负责管理和运作。

绿色发展与可持续发 展战略的前景

随着技术的进步和全球合作的加强,绿 色发展和可持续发展战略的实施前景广 阔。未来,有望通过跨国合作、知识共 享等方式,共同推动全球经济的绿色转 型和可持续发展。

THANKS

感谢观看

等,并探讨各国在开放经济中如何选择适合的汇率制度。

国际收支平衡表

02

阐述国际收支平衡表的基本构成,包括经常账户、资本与金融

账户等,并分析其对宏观经济的影响。

汇率与国际收支

03

探讨汇率变动对国际收支平衡的影响机制,以及如何通过汇率

政策调节国际收支失衡。

开放经济下的财政政策与货币政策

财政政策效应

分析在开放经济条件下,财政政策如何影响国内总需求、国际收支 和汇率等方面。

经济增长政策的实践与效果评估

(完整版)《曼昆—宏观经济学》重点总结,推荐文档

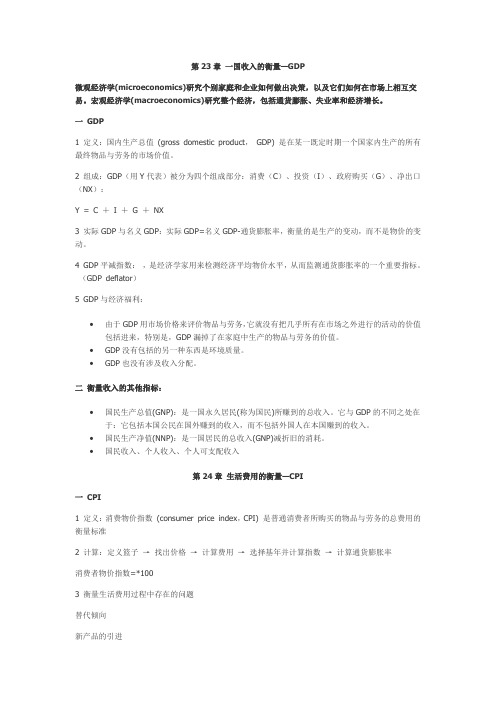

第23章一国收入的衡量—GDP微观经济学(microeconomics)研究个别家庭和企业如何做出决策,以及它们如何在市场上相互交易。

宏观经济学(macroeconomics)研究整个经济,包括通货膨胀、失业率和经济增长。

一GDP1 定义:国内生产总值(gross domestic product,GDP) 是在某一既定时期一个国家内生产的所有最终物品与劳务的市场价值。

2 组成:GDP(用Y代表)被分为四个组成部分:消费(C)、投资(I)、政府购买(G)、净出口(NX):Y = C +I +G +NX3 实际GDP与名义GDP:实际GDP=名义GDP-通货膨胀率,衡量的是生产的变动,而不是物价的变动。

4 GDP平减指数:,是经济学家用来检测经济平均物价水平,从而监测通货膨胀率的一个重要指标。

(GDP deflator)5 GDP与经济福利:•由于GDP用市场价格来评价物品与劳务,它就没有把几乎所有在市场之外进行的活动的价值包括进来,特别是,GDP漏掉了在家庭中生产的物品与劳务的价值。

•GDP没有包括的另一种东西是环境质量。

•GDP也没有涉及收入分配。

二衡量收入的其他指标:•国民生产总值(GNP):是一国永久居民(称为国民)所赚到的总收入。

它与GDP的不同之处在于:它包括本国公民在国外赚到的收入,而不包括外国人在本国赚到的收入。

•国民生产净值(NNP):是一国居民的总收入(GNP)减折旧的消耗。

•国民收入、个人收入、个人可支配收入第24章生活费用的衡量—CPI一CPI1 定义:消费物价指数(consumer price index,CPI) 是普通消费者所购买的物品与劳务的总费用的衡量标准2 计算:定义篮子→找出价格→计算费用→选择基年并计算指数→计算通货膨胀率消费者物价指数=*1003 衡量生活费用过程中存在的问题替代倾向新产品的引进无法衡量的质量变动。

4 GDP平减指数与消费者物价指数差别1:GDP平减指数反映了国内生产的所有物品与劳务的价格,而消费物价指数反交映了消费者购买的所有物品与劳务的价格。

宏观经济学(Macroeconomics)

• 中央银行的再贴现率上升商业银行向中 央银行借款的成本上升商业银行自己多

留准备金实际准备率上升

6.1.4 经济持续稳定增长

• 是指在一个特定时期内经济社会所生产的人 均产量和人均收入的持续增长

• 一般用实际国内生产总值年均增长率来衡量 • 持续、稳定、长期的增长是经济社会所追求

的理想状态

6.1.5 国际收支平衡

• 国际收支平衡对开放型经济国家至关重要 • 国际收支会影响一个国家的就业、物价和经

6.2.8 拉弗曲线(属于供给学派理论)

• 一般来说,税率越高,政府的税收就越多,所以 提高税率可以增加政府的收入

• 但是,税率的提高超过一定的限度,企业的经营 成本提高,它们会减少投资,甚至退出这个地区 乃至国家的投资,从而造成政府征税基础的缩小 ,政府税收的总量因此减少

• 描绘这种税收与税率关系的曲线叫做拉弗曲线

• 充分就业预算盈余:是指既定的政府预算在充分就 业的国民收入水平上所产生的政府预算盈余。(为 使预算盈余成为判断财政政策的扩张或紧缩而提出 )

• 充分就业预算盈余:BS﹡=tY﹡-G-TR • 实际预算盈余: BS=tY-G-TR

充分就业预算盈余

• 如果:Y﹡<Y,则, BS﹡ < BS • 如果:Y﹡>Y,则, BS﹡ > BS • 充分就业预算盈余增加或赤字减少,财政政策紧缩 • 充分就业预算盈余减少或赤字增加,财政政策扩张 • 意义:

– 政策乘数大小是多少? – 政策时滞是多长? – 挤出效应有多大? – 不确定性如何排除?

6.2.4 国家预算

• 预算赤字和预算盈余 • 预算赤字:收<支;预算盈余:收>支 • ---年度平衡预算 • ---周期平衡预算(瑞典预算,补偿性财政政策) • 把原来争取年度预算平衡拓展成实现每个经济周期的

Macroeconomics宏观经济学