会计稳健性的文献综述

会计稳健性的研究评述

会计稳健性的研究评述作者:张蓉来源:《财讯》2018年第27期本文将回顾有关的国内外会计稳健性研究的相关文献,并进行评价。

本文主要将会计稳健性相关的文件梳理为一下几个部分:会计稳健性的界定、类型、影响因素和經济后果等。

最后,对相关文献进行评价并提出自己对会计稳健性研究的思考。

会计稳健性影响因素经济后果会计稳健性,是指财务会计中的稳健原则,也称谨慎性原则。

它作为会计信息的质量特征之一,具有很高的研究价值。

研究财务会计的稳健性,有助于会计准则的制定和证券市场的规范,有助于控制企业的盈余管理以及帮助企业进行优化决策。

针对会计稳健性的研究,国内外学者主要集中在一下几个方面:一是、会计稳健性的界定与类型;二是、会计稳健性的影响因素;三是、会计稳健性的经济后果。

会计稳健性的界定与类型由于关于会计稳健性的界定也是基于不同的理论研究背景,所以理论界从多个方面均可以对会计稳健性进行界定,并取得了丰硕的成果,使得会计稳健性的定义虽不具有一致的结论却使会计稳健性研究本省焕发着令人着迷的理论魅力。

(1)会计稳健性的界定国外的学者Watts(1993)最早对会计稳健性进行了研究。

美国会计原则委员会(APB,1970)认为管理者等为了解决计量过程中的小偏误,都倾向于低估资产和利润,从而导致了会计稳健性。

美国财务会计准则委员会(FASB,1980)认为,稳健性是在面临不确定性是谨慎的反映,以确保企业充分考虑了生产经营中固有的不确定性和风险。

FASB不支持在有了充分的证据仍不确认收入,或者好没有必要的证据之前确认损失。

如果未来受到或支付的两个估计金额有相同的可能性,谨慎性原则要求使用较不乐观的估计数。

但是如果两种金额发生的可能性并不相同,谨慎性原则并不意味着一定要抛弃可能眭更大的估计数而使用更悲观的估计数。

国际准则委员会(IASB)认为,如果存在不确定因素需要估计,就需在判断过程中加入一定程度的谨慎,不少计负债或费用,也不虚计资产或收益,这是稳健性的体现。

会计稳健性及其经济后果研究综述

2015年1期总第776期会计稳健性及其经济后果研究综述▉贾少薇河北大学管理学院摘要:会计稳健性是财务报告的一项重要质量特征也是盈余质量的重要指标。

高质量会计信息的必要条件之一就是会计稳健性,会计信息决定着公司层面的监管治理和投资融资政策,因此,会计信息稳健性很大程度上影响着各类经济组织的财务管理活动以及会计实务。

通过国内外相关文献的研究、整理本文系统的总结了会计稳健性是如何影响投资融资政策和公司治理的。

关键词:会计稳健性;影响因素;经济后果一、会计稳健性的影响因素1.契约的影响。

股东和管理层契约方面,由于代理冲突,管理层因自己的利益往往会做出损害股东利益的决策,基于有效监督和采取合理的激励措施的考虑股东会更加倾向于稳健性的原则从而保护投资者的利益,(peek 等人通过研究发现);刘凤委、汪洋(2006)研究发现,管理层和债权人之间存在的利益冲突使得管理层为了获取更高的会计利润投资高风险项目,这一举措严重损害了债权人的利益,因此债务也是引起会计谨慎性的重要因素之一。

债权人和股东之间在股利分配政策方面的分歧突出了债务契约中限制性条款的地位,这提高了会计信息的稳健性水平,Ahme (2002)通过实证研究发现;由此可见不管是股东、管理层和债权人之间的债务契约还是股东和管理层之间的代理契约,各方基于自身利益的考虑都会要求采取稳健性的会计信息,从而有效的避免各种机会主义给自己造成的损失。

2.会计准则的影响。

选择不同的会计政策会产生不同的经济后果,由于隐藏的收益难以被发现而高估的资产和收益带来的损失却很容易发现,因此公众期望市场监管者和准则制定者提供稳健的会计信息(Watts,1997)。

Ball ,Robin 和Wu 通过研究发现,稳健的会计信息是会计信息质量的决定性条件因此各种制度要求公司提供稳健的会计信息。

牛建军、岳衡和邱月华(2006)实证研究发现,我国上市公司财务报告所披露的会计稳健性是来自于资产负债表的稳健性,并非真正意义上来自盈余稳健性的改进。

会计稳健性的经济后果研究述评

会计稳健性的经济后果研究述评一、本文概述会计稳健性作为会计理论的核心原则之一,其在经济活动中扮演着至关重要的角色。

本文旨在深入探讨会计稳健性的经济后果,通过对现有研究的梳理和评价,揭示会计稳健性对企业、投资者、债权人以及其他利益相关者的影响,以及在不同经济环境和制度背景下的适用性。

文章首先对会计稳健性的定义、起源和发展进行概述,明确其内涵和外延。

接着,从微观和宏观两个层面,分析会计稳健性对企业财务报告质量、投融资决策、公司治理结构、市场反应等方面的影响,并评估其对企业价值和经济效益的长期作用。

文章还将关注会计稳健性在不同国家和地区的实践差异,以及其与会计准则、制度环境等因素的相互作用。

文章将总结现有研究的不足和争议点,并展望未来的研究方向,以期为会计稳健性的深入研究和实践应用提供有益的参考。

二、会计稳健性的理论基础会计稳健性作为一种重要的会计原则,其理论基础主要源自经济学、财务学以及会计学等多个学科领域。

在经济学的视角中,会计稳健性被视为一种风险规避机制,旨在通过低估资产和高估负债来避免潜在的经济损失。

这种风险规避的动机在不确定的经济环境中尤为重要,因为它可以帮助企业和投资者更好地应对可能的经济波动和风险。

在财务学领域,会计稳健性被视为维护财务健康的重要工具。

通过稳健的会计实践,企业可以确保其财务报告的准确性和可靠性,从而增强投资者和其他利益相关者的信任。

稳健的会计原则还可以帮助企业更好地进行财务规划和决策,以应对各种经济挑战和不确定性。

会计学作为会计稳健性最直接的理论基础,提供了许多关于如何实施稳健会计实践的指导原则。

这些原则包括在存在不确定性时避免过度乐观的估计、在计量资产和负债时保持谨慎态度等。

这些原则的实施有助于确保会计信息的可靠性和相关性,从而为企业和投资者提供有价值的决策依据。

会计稳健性的理论基础涉及多个学科领域,包括经济学、财务学和会计学等。

这些理论基础为会计稳健性的实施提供了重要的指导和支持,使其在经济活动中发挥着不可或缺的作用。

会计稳健性:文献回顾

Accounting conservatism:A review of theliteratureGeorge W.Ruch,Gary Taylor*University of Alabama,Culverhouse School of Accountancy,United States1.IntroductionAccounting conservatism can be defined as accounting policies or tendencies that result in the downward bias of accounting net asset value relative to economic net asset value.It is one of the most fundamental features of accounting information,dating back centuries(Basu,1997;Watts,2003a). While there is little question as to conservatism’s existence,there is a debate among researchers andJournal of Accounting Literature34(2015)17–38A R T I C L E I N F OArticle history:Received21May2014Received in revised form20January2015Accepted8February2015Available online27February2015Keywords:Accounting conservatismEarnings qualityMarket returnsContractingA B S T R A C TWe review and analyze the accounting literature that examines theeffects of accounting conservatism onfinancial statements andfinancial statement users.We begin by analyzing how conservatismaffects the reported numbers on thefinancial statements.Thesestudies primarily evaluate how conservatism affects earningsquality,including earnings persistence and the presence of earningsmanagement.Next,we assess the effect of accounting conservatismon the users of thefinancial statements.We identify three primaryusers of thefinancial statements:(1)equity market users(2)debtmarket users and(3)corporate governance users.Within each ofthese categories,we analyze thefindings of prior research andexplore unanswered research questions.By analyzing the effects ofaccounting conservatism from a diverse range of research topics,weinform the discussion on the costs and benefits of accountingconservatism.ß2015University of Florida,Fisher School of Accounting.Publishedby Elsevier Ltd.All rights reserved.*Corresponding author.Tel.:+12053484658.E-mail addresses:ruch001@(G.W.Ruch),gtaylor@(G.Taylor).Contents lists available at ScienceDirectJournal of Accounting Literaturejournal homepage:/locate/acclit/10.1016/j.acclit.2015.02.0010737-4607/ß2015University of Florida,Fisher School of Accounting.Published by Elsevier Ltd.All rights reserved.standard setters as to how costly or beneficial conservatism is to financial statement users.The Financial Accounting Standards Board (FASB)does not include conservatism as one of the qualitative characteristics of financial reporting in its conceptual framework because it believes that conservatism biases accounting information and compromises neutrality (FASB,2010).Some researchers have echoed this notion,arguing that conservatism biases financial statement numbers to result in inefficient decision-making (Gigler,Kanodia,Sapra,&Venugopalan,2009;Guay &Verrecchia,2006).Alternatively,some researchers contend that accounting conservatism arises naturally between contracting parties and is necessary as an efficient contracting mechanism (Basu,1997;Watts,2003a ).This view stems from the idea that certain contracts (e.g.,debt and executive compensation)have asymmetric payoffs to contracting parties,thereby resulting in timelier reporting of information that has the greatest potential to affect the contracting parties.For example,a debt agreement has asymmetric payoffs for the lender.While strong financial performance on the part of the debtor does not increase the payoff to the lender,weak financial performance on the part of the debtor increases the risk of default,thus reducing the lender’s potential payoff.Consequently,the lending party demands that the borrowing party report information that may reflect weak financial performance (i.e.,bad news)in a timelier manner than it would report information that may reflect strong financial performance (i.e.,good news).The controversy that fuels this debate arises from different perspectives on the informational roles of accounting.From one perspective,the primary function of accounting is to capture information that can be used to assess the market value of equity and make investment decisions (‘‘valuation perspective’’).From another perspective,the primary function of accounting is to provide information that allows contracting parties to evaluate the efficiency and effectiveness with which obligations are performed in contracting settings such as debt and executive compensation contracts (‘‘contracting perspective’’).1Assessments of the costs and benefits of accounting conservatism are largely dependent on one’s perspective on accounting information (i.e.,valuation versus contracting),as information that is desirable from one perspective may be of little value from another perspective.To address these issues,we review the literature and provide analysis of the effects of accounting conservatism.We discuss the effects of accounting conservatism in two phases.First,we discuss the direct effects of accounting conservatism on the financial statement numbers.Second,we discuss the effects of conservatively reported financial statements on the users of the financial statements.We analyze the effects of conservatism on three broad groups of financial statement users:(1)equity market users (2)debt market users (3)corporate governance users.The section on equity market users discusses how investors and analysts use the financial statements to make decisions about the firm.The section on debt market users discusses how lenders and borrowers use the financial statements in debt contracting settings.The section on corporate governance users discusses how conservatism impacts the effectiveness with which shareholders monitor firm management through executive compensation and investment decisions.Fig.1provides an illustration of the effects of accounting conservatism on the financial statements and the users of the financial statements.We review 34studies on the effects of accounting conservatism,the majority of which are published in prominent peer-reviewed accounting journals with dates ranging from 1997to 2014.2Table 1,Panel A provides a count of the studies we review,grouped by source journal;Panel B provides a count of the studies we review,grouped by research topic.Overall,prior research has provided mixed evidence on the costs and benefits of accounting conservatism.Some of the studies reviewed in this paper find that conservatism alleviates information asymmetry,reduces debt cost of capital,makes executive compensation more sensitive to accounting earnings,and induces management to make more efficient investment decisions,all of which indicate that conservatism may be beneficial 1See Christensen and Demski (2003)for a complete discussion on the valuation and contracting roles of accounting information.Holthausen and Watts (2001),Barth et al.(2001),and Watts (2003a,2003b)also discuss the dual roles of accounting information and how conservatism may or may not be useful in each of these roles.2Our review includes a discussion of one working paper (Louis et al.,2014).We include a discussion of this study because its findings are particularly relevant to the effects of conservatism on analyst forecasts and are distinct from findings in published research.Additionally,Google Scholar indicates that this study has been cited 25times as of January 2015.G.W.Ruch,G.Taylor /Journal of Accounting Literature 34(2015)17–3818G.W.Ruch,G.Taylor/Journal of Accounting Literature34(2015)17–3819Fig.1.Overview of the effects of accounting conservatism onfinancial statements andfinancial statement users.Table1Breakdown of studies reviewed.Number of papers reviewedPanel A:Studies reviewed(by source journal)Accounting and Finance2Accounting Horizons2Contemporary Accounting Research2Journal of Accounting,Auditing,and Finance1Journal of Accounting and Economics7Journal of Accounting Research5Review of Accounting Studies4The Accounting Review6Other Journals4Working Papers1Total34Panel B:Studies reviewed(by topic)Financial statement effects6Equity market users16Debt market users4Corporate governance users8Total34when viewed from the contracting perspective.Conversely,other studiesfind that conservatism reduces earnings persistence and predictability,facilitates earnings management,reduces analyst forecast accuracy,and may reduce the value relevance of earnings,which indicates that conservatism may be detrimental when viewed from the valuation perspective.Finally,wefind that conservatism’s effect on the cost of equity capital is mixed and inconclusive.Prior literature reviews on conservatism have surveyed studies that examine the legal and political determinants of conservatism(Habib,2007;Watts,2003a,2003b),the construct validity of the various empirical measures of conservatism(Wang,Ho´gartaigh,&van Zijl,2009),and the relationship between timely loss recognition(i.e.,conditional conservatism)and earnings quality(Dechow,Ge,& Schrand,2010).Our study differs from these prior surveys of the conservatism literature in that we focus on the costs and benefits of accounting conservatism,rather than reviewing specific measures or causes of accounting conservatism.Additionally,our study analyzes how different forms ofaccounting conservatism (i.e.,conditional versus unconditional conservatism)may affect financial statements and financial statement users.Overall,we contribute to the literature by integrating and analyzing conservatism research from a broad spectrum of research topics to encompass multiple aspects of the impact of conservatism on financial statements and financial statement users.Understanding the effects of conservatism is important in assessing the costs and benefits of conservatism and informs the debate surrounding the role of conservatism in financial reporting.Additionally,this study identifies avenues for future research on the effects of accounting conservatism.This study is organized as follows:Section 2provides background on accounting conservatism.Section 3discusses the effects of conservatism on the financial statements vis-a`-vis earnings quality.Section 4discusses the effects of conservatism on the users of the financial statements,specifically,equity market users,debt market users,and corporate governance users.Section 5provides concluding remarks.2.BackgroundAccounting conservatism can be defined as accounting policies or tendencies that contribute to a downward bias in accounting net asset value relative to economic net asset value.Accounting standard-setters and accounting scholars have offered similar definitions of conservatism.Statement of Financial Accounting Concepts (SFAC)No.2defines conservatism as follows:‘‘Conservatism is a prudent reaction to uncertainty to try to ensure that uncertainties and risks inherent in business situations are adequately considered.Thus,if two estimates of amounts to be received or paid in the future are about equally likely,conservatism dictates using the less optimistic estimate ...’’(FASB,1980)The philosophy of conservatism is commonly summarized in the literature by the adage ‘‘anticipate no profits and provide for all probable losses’’(Bliss,1924).Watts and Zimmerman (1986)define conservatism as reporting the lowest value among possible alternative values for assets and the highest alternative value for liabilities.Extending these definitions,accounting researchers have identified two broad forms of conservatism that produce the aforementioned understatement of accounting value:(1)conditional conservatism,and (2)unconditional conservatism.The primary difference between the two forms of conservatism is that the application of conditional conservatism depends on economic news events,while the application of unconditional conservatism does not.Conditional conservatism occurs when negative economic news is recognized in accounting earnings in a timelier manner than positive economic news.In other words,conditional conservatism is characterized by the asymmetric recognition of positive and negative economic news.Examples of conditional conservatism include the asymmetric treatment of loss and gain contingencies and accounting for inventory using the lower-of-cost-or-market convention.Unconditional conservatism occurs through the consistent under-recognition of accounting net assets.Unlike conditional conservatism,unconditional conservatism does not depend on news events.Examples of unconditional conservatism include immediately expensing research and development expenditures and accelerated depreciation.Table 2provides a list of conditional and unconditional conservatism practices.It is important to distinguish between conditional and unconditional conservatism for three reasons.First,these two forms of conservatism have different effects on the financial statements.The application of accounting policies consistent with conservatism is likely to have a relatively consistent impact on the income statement from period to period (e.g.,research and development expenses).Conversely,the application of conditional conservatism is more likely to be transitory on the income statement because of fluctuations in the content and timing of economic news across periods (Chen,Folsom,Paek,&Sami,2014).On the balance sheet,both types of conservatism result in understated net assets.However,conditional and unconditional conservatism have different effects on the timing of income statement recognition,and in turn,different effects on the timing of balance sheet recognition (i.e.,reduction in net asset value).For example,acceleratedG.W.Ruch,G.Taylor /Journal of Accounting Literature 34(2015)17–3820G.W.Ruch,G.Taylor/Journal of Accounting Literature34(2015)17–3821Table2Examples of accounting conservatism.Type of conservatism Common examplesConditional conservatism Goodwill impairmentLong-lived asset impairmentInventory recorded at the lower of cost or marketAsymmetry in gain/loss contingenciesUnconditional conservatism Accelerated depreciation methodsExpensing R&D costsExpensing advertising costsLIFO inventoryAccumulated reserves in excess of expected future costs(e.g.,allowance for doubtfulaccounts,warranty allowance)depreciation of an asset in thefirst few years of the asset’s life may eliminate the need to write down the book value of the asset in the event of bad news about the market value of the asset.Second,research suggests that the application of one type of conservatism affects the application of the other type.Most notably,Beaver and Ryan(2005)investigate the relationship between conditional and unconditional conservatism,andfind that unconditional conservatism creates‘‘accounting slack’’that may preempt the application of conditional conservatism.3The unconditional understatement of assets limits the magnitude of write-downs recognized in the presence of bad news events,and therefore, reduces observed asymmetric timeliness in earnings.Consequently,inferences made regarding the presence of conditional conservatism may be confounded by the presence of unconditional conservatism.Third,the conditions that give rise to conditional conservatism may differ from those of unconditional conservatism.For instance,Qiang(2007)examines the presence of unconditional and conditional conservatism in each of four explanations for conservatism offered by Watts(2003a)–contracting,litigation,taxation,regulatory–andfinds that conditional conservatism arises in settings where contracting and litigation costs are high,whereas unconditional conservatism arises in settings where litigation,regulatory,and tax costs are high.Of the two forms of conservatism,conditional conservatism is more prevalent than unconditional conservatism in research on accounting conservatism.Specifically,24of the34studies reviewed in our study focus on conditional conservatism in some manner,whereas only11of the34studies focus on unconditional conservatism.4A potential reason for the focus on conditional conservatism could be the notion that it communicates information about uncertain events,and is therefore of greater interest to researchers studying contracting and valuation issues than is unconditional conservatism (Ball&Shivakumar,2005;Ryan,2006).3.Effects onfinancial statementsConservatism results in an understatement of accounting book value relative to the market value of equity due to the understatement of assets and revenues and/or the overstatement of liabilities and expenses.However,the extant literature on thefinancial statement effects of accounting conservatism primarily focuses on its effects on earnings quality.Dechow et al.(2010)analyze how earnings quality is defined in the accounting literature and the proxies commonly used to measure it.They contend that there is no consensus definition of earnings quality,which,we posit,may be attributed to the different perspectives on the use of accounting information(i.e.,contracting versus valuation).53See also Basu(2005)for discussion of the relationship between conditional and unconditional conservatism.417studies focus exclusively on conditional conservatism,5studies focus exclusively on unconditional conservatism, 7studies focus on both forms of conservatism,and5studies do not specify a form of conservatism.5One of the proxies for earnings quality discussed by Dechow et al.(2010)is timely loss recognition(i.e.,conditional conservatism).While their analysis provides insights into the effects of accounting conservatism on earnings quality,it only focuses on conditional conservatism.Our study extends their analysis by examining the effects of both conditional and unconditional conservatism on earnings quality.We review the conservatism studies that have examined the effect of conservatism on the earnings quality proxies discussed in Dechow et al.(2010).While the studies reviewed in this section do not explicitly address all of the proxies discussed in Dechow et al.(2010),some of the conclusions drawn with respect to the effects of conservatism on certain earnings quality proxies may be applied to other earnings quality proxies.We group the studies that examine the effects of conservatism on earnings quality into two broad groups:(1)time-series properties of earnings,which encompass earnings persistence and predictability,and (2)the presence of earnings management.3.1.Time-series properties of earnings Research on the effects of conditional conservatism on the time-series properties of earnings consistently finds that conditional conservatism reduces earnings persistence and predictability.Dichev and Tang (2008)and Chen et al.(2014)provide evidence that conditional conservatism increases earnings volatility and decreases earnings persistence.Dichev and Tang (2008)find that the correlation between past expenses and current revenues has increased over the 40years preceding the study,which,in turn contributes to increased earnings volatility and decreased earnings persistence.An increase in the correlation between past expenses and current revenues is consistent with timely loss recognition.Accordingly,Dichev and Tang (2008)conclude that this finding is consistent with an increase in conditional conservatism over a similar time frame,as noted by Givoly and Hayn (2000).Chen et al.(2014)find that conditional conservatism has a negative incremental effect on persistence and that the negative effect on earnings persistence leads to lower pricing multiples on earnings.Additionally,they find that earnings persistence and pricing multiples are lower for conditionally conservative earnings than for unconditionally conservative earnings.Kim and Kross (2005)and Bandyopadhyay,Chen,Huang,and Jha (2010)provide evidence that conditional conservatism decreases the ability of earnings to predict future earnings but increases the ability of earnings to predict future operating cash flows.Kim and Kross (2005)find that the ability of earnings to predict future operating cash flows increases (does not increase)through periods where conservatism is increasing (not increasing).Extending Kim and Kross (2005),Bandyopadhyay et al.(2010)find that conservatism is positively associated with the predictability of future cash flows and negatively associated with the predictability of future earnings.These studies suggest that the increased timeliness of bad news recognition is associated with temporary fluctuations in earnings,making earnings less persistent and predictable from one period to the next.The impact of unconditional conservatism on earnings persistence and predictability are dependent on the conservatism practice used.For example,accelerated depreciation would likely result in less persistent earnings than a straight-line or less accelerated method.Excess depreciation expense recognized earlier in an asset’s useful life would not be recognized later in the asset’s useful life,reducing the persistence of depreciation expense.However,we are unaware of any research that has examined this effect of accelerated depreciation methods on earnings persistence.Focusing on some of the other methods of unconditional conservatism,Penman and Zhang (2002)find that research and development (R&D)expenditures,advertising expenditures,and LIFO accounting for inventory reduce the persistence of earnings when these methods temporarily fluctuate.For example,the temporary reduction of R&D expenditures increases earnings in the period of reduction.However,earnings return to normal levels when normal R&D activity is resumed.Penman and Zhang (2002)find that unconditional conservatism creates ‘‘hidden reserves’’that can be released into earnings,causing a temporary distortion of operating performance.6This can be especially misleading in light of the fact that the reduction of R&D expenditures may reduce future sales.Overall,research suggests that conditional and unconditional conservatism adversely affect earnings quality by reducing earnings persistence and predictability.Another aspect of earnings quality discussed in Dechow et al.(2010)that is not explicitly addressed by the conservatism literature is accrual quality.While we are not aware of any studies that explicitly 6The term ‘‘hidden reserve’’refers to the fact that these understatements of net assets are not explicitly reported on the balance sheet.For example,expensing advertising expenditures that have future benefits has the same effect on net assets as recording reserves for bad debts or warranty liabilities.G.W.Ruch,G.Taylor /Journal of Accounting Literature 34(2015)17–3822G.W.Ruch,G.Taylor/Journal of Accounting Literature34(2015)17–3823address the relationship between conservatism and accrual quality,we contend that the results of the aforementioned studies related to the time-series properties of earnings may tangentially support the expected relationship between conservatism and accrual quality.Prior researchfinds that the accrual portion of earnings is less persistent than the cash portion(Sloan,1996)and theorizes that the accrual portion of earnings possesses a lower level of quality than that of the cash portion of earnings because accruals are subject to measurement error(Dechow&Dichev,2002).Additionally,the application of accounting conservatism is frequently accomplished through the use of accruals,especially in the case of timely loss recognition.Consequently,the differences in earnings persistence and predictability noted in the studies reviewed in this section may be the result of differences in the accrual composition of earnings.3.2.Presence of earnings managementNext,we consider the relationship between accounting conservatism and the presence of earnings management.Earnings management is often defined as management’s intentional manipulation of accounting numbers to achieve strategic earnings targets.While there is a significant amount of earnings management research,few studies investigate the effect of accounting conservatism on the occurrence of earnings management.7A natural research question is:how do conservative accounting policies impact the pervasiveness of earnings management?Atfirst glance,it may appear that conservatism lies in direct contrast to an aggressive accounting practice,such as earnings management.However,we do not restrict our definition of accounting conservatism to management’s intent to be prudent.Rather,we consider any downward bias in accounting values to be conservative, including opportunistic downward earnings management.In general,it is unlikely that conditional conservatism would have a significant relationship with earnings management.Due to the uncertainty of news events,managers are not able to effectively rely on the accounting recognition of news events in a given period to meet earnings targets.Bad news write-downs may be used to manage earnings downward(i.e.,‘‘big bath’’),but we are not aware of any empirical evidence supporting such an assertion.Additionally,Watts(2003b)contends that the significant evidence for the existence of conservatism is unlikely to support the notion that observed write-down recognition is a significant indicator of earnings management.Unconditional conservatism,on the other hand,has the ability to facilitate earnings management through the accumulation of reserves on the balance sheet that can be released into earnings when an earnings target needs to be met.The reserves are accumulated via unconditional conservatism over multiple accounting periods.In this case,firm management is opportunistically exploiting conservative accounting to achieve earnings targets in future periods.Jackson and Liu(2010) demonstrate that conservatism in estimating the allowance for doubtful accounts can be associated with earnings management.Theyfind that the allowance for doubtful accounts conservatively estimates future write-downs on average,and that such conservatism is associated with the use of bad debt expense to meet analyst EPS targets.In other words,the conservatively estimated reserve is released into earnings by reducing bad debt expense to meet earnings targets.3.3.Opportunities for future researchOverall,research has found that conditional conservatism reduces earnings persistence and predictability and that unconditional conservatism can facilitate earnings management through the accumulation of balance sheet reserves.Thesefindings seem to indicate that accounting conservatism has more negative effects on earnings quality than positive effects.A list of the studies that evaluate the effects of conservatism on thefinancial statements is provided in Table3.Future research on conditional conservatism’s effect on the time-series properties of earnings could do more to separate these effects into good news and bad news periods.The deferral of gains is likely to result in more persistent earnings,and therefore,earnings in good news periods are likely to7See Habib and Hansen(2008),Healy and Wahlen(1999),and Schipper(1989)for more thorough definitions of earnings management and reviews of the earnings management literature.Table3Studies onfinancial statement effects.Author(s)Topic Research question Sample Type ofconservatismFindingsPenman and Zhang(2002)Time-seriesproperties ofearnings What effect doconservative accountingpractices have onearnings quality?USfirms(1975–1997)Unconditional Conservatism results in the accumulation of‘‘hiddenreserves’’.These reserves are released into earningswhen temporary changes are made to conservativeaccounting.This results in earnings that are lesspredictable.Kim and Kross(2005)Time-seriesproperties ofearnings Has the ability ofearnings to predictfuture operating cashflows improved overtime?USfirms(1972–2001)Conditional The ability of earnings to predict operating cashflowshas increased over the sample period.This increaseappears to be driven by the previously documentedtime-series increase in accounting conservatism.Dichev and Tang(2008)Time-seriesproperties ofearnings Has the ability ofexpenses to matchrevenues declined overtime?USfirms(1967–2003)Conditional Revenue-expense matching has decreased over time,resulting in more volatile and less persistent earnings.This suggests that expense recognition is timelier,consistent with conditional conservatism.Bandyopadhyay et al.(2010)Time-seriesproperties ofearnings How does the ability ofearnings to predictfuture operating cashflows affect the ability ofearnings to predictfuture earnings?USfirms(1972–2006)Conditional Conservatism enhances the ability of earnings to predictfuture operating cashflows,but inhibits the ability ofearnings to predict future earnings.Jackson and Liu(2010)Earningsmanagement How does conservativeaccounting with respectto the allowance fordoubtful accountsimpact the ability offirms to manageearnings using bad debtexpense?USfirms(1980–2004)Unconditional Bad debt expense is managed to meet earnings targets.Conservative treatment of allowance for doubtfulaccounts facilitates the use of bad debt expense tomanage earnings.Chen et al.(2014)Time-seriesproperties ofearnings How does conservatismaffect earningspersistence and stockpricing multiples?USfirms(1988–2010)Conditional;UnconditionalConditional conservatism reduces earnings persistence,and in turn,reduces equity pricing multiples.Conditionally conservative earnings are also found to beless persistent that unconditionally conservativeearnings.G.W.Ruch,G.Taylor/JournalofAccountingLiterature34(2015)17–3824。

会计稳健性的研究综述_佟玲

&FOREIGNENTREPRENEURS2014年4月刊(总第456期)CHINESE一、引言近年来,伴随着我国证券市场的发展,会计稳健性在会计实务中的重视程度逐步增加,这将很大程度上影响企业的会计稳健性水平。

市场经济条件下,企业生产经营过程中不可避免地会遭遇风险,实施谨慎原则,能够使企业在风险实际发生之前对其加以防范并化解,可以说,谨慎地选择会计政策,对企业的经营决策有正向的引导作用,使利益相关者的切身利益得以保护,并提高企业的竞争力。

二、会计稳健性的内涵与分类首先从定义上看,Bliss(1924)会计师将稳健原则表述为“预见所有可能的损失,但不预期任何不确定的收益”。

国际会计准则委员会在其概念框架中将稳健性定义如下:“谨慎性是在不确定的条件下,需要运用判断做出必要的估计中包含一定程度的审慎,比如资产或收益不可高估,负债或费用不可低估。

”稳健性是会计确认与计量的传统和原则。

稳健性意味着会计人员在确认好消息的时候对可验证性的要求更高,所以稳健性就意味着对损失和收益确认的非对称性,即会计人员对于损失(坏消息)要及时确认而对于收益(好消息)直到有充分的证据时才予以确认。

会计实务也一直深受稳健性原则的影响,例如存货计价中的成本与市价孰低原则以及资产减值的处理都有着稳健性的烙印。

Basu(1997)认为,稳健性对会计实务的影响至少有500年以上的历史;Sterling(1970)将稳健性作为会计实务中最有影响力的原则之一。

一般而言,稳健性意味着资产的账面价值低于其市场价值(因为存在着没有确认的商誉)。

在学术界,根据性质的差异将稳健性分为两种不同的类别’:条件稳健性和非条件稳健性。

首先非条件稳健性,也称为独立稳健性,这种稳健性意味着会计处理方法在资产或负债形成的时候就己经确定了,不会再根据其后的经营环境而变化,它一般会导致不可确认的商誉存在。

关于非条件稳健性的例子有研究支出的费用化处理,以及大部分固定资产使用加速折旧法,以及对净现值为正的项目使用历史成本等。

会计制度文献综述范文(3篇)

第1篇一、引言会计制度作为企业财务管理的重要组成部分,对于企业的经济活动、财务状况和经营成果具有重要作用。

随着我国经济的快速发展,会计制度的重要性日益凸显。

本文旨在通过对会计制度相关文献的综述,梳理我国会计制度的发展历程、现状及存在的问题,并提出相应的对策建议。

二、我国会计制度发展历程1.建国初期(1949-1978年)建国初期,我国会计制度受到苏联模式的影响,以计划经济为主。

这一时期的会计制度主要以反映和监督国民经济计划执行情况为主要任务,会计核算方法简单,会计信息质量不高。

2.改革开放初期(1979-1992年)改革开放初期,我国会计制度开始逐步与国际接轨。

1985年,我国颁布了《中华人民共和国会计法》,标志着我国会计制度的法律地位得到确立。

此阶段,会计制度在核算方法、财务报告等方面逐步与国际接轨,会计信息质量得到提高。

3.社会主义市场经济体制建立时期(1993-2008年)1993年,我国正式确立了社会主义市场经济体制,会计制度进入快速发展阶段。

此阶段,我国会计制度在会计准则、财务报告等方面取得了重大突破。

1992年,我国颁布了《企业会计准则》,标志着我国会计制度与国际接轨的步伐加快。

2006年,我国颁布了新的《企业会计准则》,进一步提高了会计信息质量。

4.深化会计制度改革时期(2009年至今)2009年,我国颁布了新的《企业会计准则》,标志着我国会计制度改革进入深化阶段。

此阶段,我国会计制度在会计准则、审计准则等方面不断完善,会计信息质量不断提高。

三、我国会计制度现状1.会计准则体系逐步完善我国会计准则体系逐步与国际接轨,形成了以《企业会计准则》为核心,包括《小企业会计准则》、《事业单位会计准则》等在内的较为完善的会计准则体系。

2.会计信息质量不断提高随着会计制度的不断完善,我国企业会计信息质量不断提高。

企业财务报告披露内容更加全面、真实、准确,为投资者、债权人等提供了可靠的信息。

3.会计监管体系逐步健全我国会计监管体系逐步健全,包括政府监管、行业自律、社会监督等多层次、多角度的监管体系。

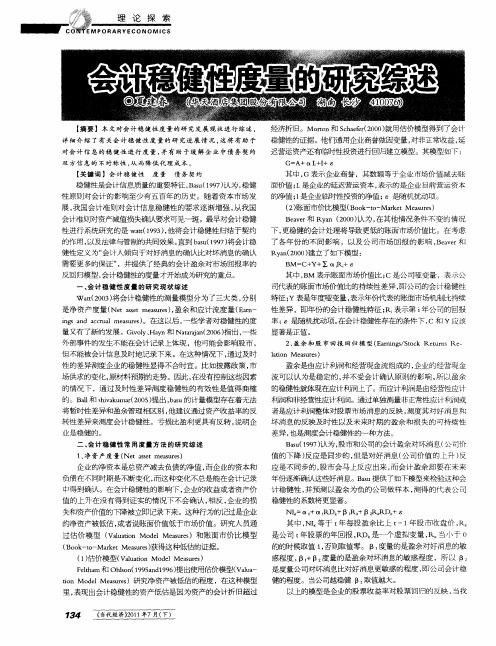

会计稳健性度量的研究综述

是 度量 公司对坏消息比对好消 息更敏感的程度 , 公司会计稳 即

健 的程 度。当公 司越稳健 B 取值越 大。 以上的模型是企业的股票 收益率对股票 回归的 反映 , 当我

里, 表现出会计稳健性的资产低估是因为资产的会计折旧超过

7 4 3_ 《 代 经济)01 当 ) 1 年7月( 2 下)

是净 资产 度量 ( e ae meue)盈余和 应计 流度量 (a - N t st a r , s s s Er n

ig ad act]me ue o在这 以后 , n s n cra a rs l s 一些学 者对稳健性 的度

量又有了新的发展 。Gi l、 y v y Han和 Na r a( 0 6指 出 , o tan20 ) aj 一些

利润和非经营性 应计 利润 。通过单独测量非正常性 应计利润或

者是应计利润整体对股票 市场消息的反映 , 测度 其对好 消息和

将暂时性 差异和盈余管理相区别 , 他建 议通 过资产收益 率的反 转性 差异 来测度会计稳健性 。亏损 比盈利更具有 反转 , 说明企

业是稳健 的。

二 、 计 稳 健 性 常 用 度 量 方 法 的 研 究 综 述 会

经济折旧 。Motn和 She r2 0 ) r o ca ̄ (0 0 就用估价模型得到 了会计

稳健性的证据。他们通用企业商誉做因变量 , 对非正常收益 , 延 迟营运资产还有临时 fj资进行 回归建立模型 。其模型如下 : 生殳

G :A+ 0 L+I £ L +

【 键 词 】会 计 稳 健 性 关

() 1估价模型( a ao dlMesrs V l t n Mo e ui a e) u Fl a 和 Ohsn 19 ad9 6 提出使用估价模 型( a a e hm t l (9 5n 19 ) o Vl - u t n Mo e Me ue)研 究净 资产被低估的程度 ,在这 种模 型 i dl a rs o s

企业战略定位与会计稳健性关系的文献综述

运營指秦企业战略定位与会计稳健性关系的文献综述许楠张丹丹摘要:企业战略定位在企业的发展中占据重要地位,战略定位的实质就是让企业在其自身内部环境和行业大环境中谋求自 身的稳定良性发展。

企业采取不同的经营战略,会影响企业会计人员在账务处理和编制财务报表时对会计准则的遵从程度,继而影响企业的会计稳健性。

本文将对企业战略定位与会计稳健性关系的现有文献进行回顾与综述,发现研究不足及未来研究 方向。

关键词:企业战略定位、会计稳健性、盈佘管理 中图分类号:F275 文献标识码:A作者单位:河北工业大学一、 企业战略定位明茨伯格提出企业战略的组成因素中“定位”占据重要 地位,主要是指将企业和周围环境紧密结合起来,并通过资源分配,促成企业在本行业内占据一席之地。

现有研究主要是从企业战略类型和战略差异度视角展开对战略定位的研究。

陈波(2015)基于战略差异度视角,研究了企业战略差异 度和审计定价间的关系,发现两者之间存在显著的正相关关系,同时探讨了产权国有和非国有的性质对企业战略差异度 和审计定价关系的影响。

对于任何一个特定行业来说,随着其行业内企业的不断发展,企业间会潜移默化地形成一种本行业专属战略(Meyer and Rowan,1977)。

企业选择和彳了业常 规相似的战略,不仅可以避免行业常见风险,还能够接受行 业专家建议(叶康涛,2014)。

本文将从战略差异度的视角对企业战略定位进行研究。

二、 会计稳健性由于会计稳健性对财务报告的重要性,其越来越受到会计界的关注。

会计稳健性指企业对交易或事项进行会计确认、计量和报告应当保持应有的谨慎,不应高估资产或收益、低估负债或者费用。

相比上述定义,Basua997)认为会计稳 健性代表着会计人员在确认收益和损失时采用不对等的确认原则,即对于好消息的确认计量时,所依据的可验证性要求要高于对坏消息确认计量时依据的可验证性要求。

Basu对 会计稳健性的定义应用较广,本文也采用Basu的定义。

会计稳健性与公司治理研究综述

会计稳健性与公司治理研究综述【摘要】本文主要对会计稳健性与公司治理之间的关系进行了综述和分析。

在我们介绍了研究背景、研究意义和研究目的。

在我们分别讨论了稳健性会计的概念和特征、公司治理对稳健性会计的影响,以及稳健性会计与公司治理之间的关联性。

通过国内外相关研究的综述,我们可以更好地了解这一领域的研究现状。

我们展望了未来的研究方向。

在我们总结了研究的主要观点,提出了对实践的启示,并讨论了研究的局限性和未来的展望。

通过本文的阐述,读者可以更好地理解会计稳健性与公司治理之间的关系,为相关研究和实践提供参考。

【关键词】会计稳健性、公司治理、稳健性会计概念、稳健性会计特征、公司治理影响、研究综述、研究方向、实践启示、研究局限性。

1. 引言1.1 研究背景在当前复杂多变的经济环境下,会计稳健性与公司治理之间的关系愈发密切。

稳健性会计原则的合理运用可以提高财务报告的可靠性,为投资者和利益相关方提供准确的信息,从而增强公司治理的透明度和有效性。

对会计稳健性与公司治理的研究,不仅有助于揭示二者之间的关联性,还可以为提升公司财务报告质量和推动公司治理改进提供重要参考。

本文旨在对会计稳健性与公司治理的关系进行深入探讨,通过回顾国内外相关研究成果,总结研究现状并展望未来研究方向,为进一步完善公司治理机制和提升财务报告质量提供理论支持和实践指导。

1.2 研究意义会计稳健性与公司治理是当今企业财务管理中一个备受关注的研究领域。

稳健性会计作为会计规范的一个重要原则,对于保障财务报告的可靠性和真实性具有重要意义。

而公司治理作为管理企业各项事务的机制,也在一定程度上影响着会计稳健性的实施和体现。

研究会计稳健性与公司治理之间的关系,不仅有利于深入理解企业财务报告的真实性和可靠性,还有助于提升公司治理水平,增强企业的持续发展能力。

在当前全球化经济背景下,企业面临着日益复杂的经营环境和市场竞争,财务报告的真实性和稳健性越发受到重视。

通过研究会计稳健性与公司治理的相互关系,可以为企业提供更有效的财务管理策略,规范财务报告的制定和披露,减少财务造假的可能性,维护股东利益,促进企业健康持续发展。

会计稳健性研究综述

会计稳健性研究综述作者:曾真来源:《商场现代化》2012年第20期一、会计稳健性的定义1.1会计稳健性古典定义Bliss(1924)提出,稳健性就是“不预计任何不确定收益,但是要预计所有发生的损失。

可见,古典定义体现出“绝对稳健”,而且便于实务操作,因而在早期得到了广泛使用。

随着公司会计业务不断发展,会计信息程度不断复杂,古典定义所体现的稳健性过于粗糙和直接,有悖于现代会计计量中的及时性和可验证性要求。

因此,后续研究在古典定义的基础上陆续进行其他发展。

1.2会计稳健性准则定义为了规范现代会计行为,各个国家政府和会计组织也对会计稳健型做出官方界定。

国际会计准则理事会(IASB)在其制定的国际财务报告准则(IFRS)中将稳健性定义为:“在有不确定性因素的情况下所需要的预计时,在所需要的判断中加入必要的谨慎,比如说资产或者收入不可高估,负债或者费用不可低估。

”美国会计准则委员会(APB)在其发布的第4公告《企业财务报告的基本概念和会计原则》中指出:“各种资产和负债一般是在不确定的情况下进行计量的,管理者、投资者和会计人员对计量上的可能误差,在原则上一般是低估收益和净资产,而不愿进行高估。

”我国在1992年颁布的《企业会计准则》首次对稳健性原则界定:“会计核算应当遵循谨慎性原则的要求,合理预计可能发生的费用和损失。

”在2006年新会计准则——《企业会计准则——基本准则》对稳健性原则进行了更加准确的定义:“在不确定的条件下,企业对交易事项进行会计确认、计量和报告应该保持应有的谨慎,比如资产或收人不可高估,负债或费用不可低估。

”以上对稳健性的界定,可见稳健性已经由“绝对稳健”发展为了“相对稳健”,强调了企业在不同的环境中面对损失和收益应持有不同态度,但也体现出对合理估计的重视。

2.国内外研究现状和发展趋势(1)会计稳健的需求动因研究综述随着Basu(1997)年提出会计好消息的确认会比坏消息的确认更加需要其可验证性,这一会计稳健型的描述型定义后,分别有Watts(2003)和Ball&Shivakumar(2005)、Beaver&Ryan(2005)分别从不同的角度论证了会计稳健性的需求动因。

会计类文献综述范文字

会计类文献综述范文字文献综述是研究领域中重要的一环,通过对该领域相关文献的梳理和归纳,可以更好地认识前沿研究动态,理清研究思路,指导后续研究,提升研究水平。

在会计类研究中,也同样需要进行文献综述,下面将针对会计类文献综述范文进行分析和总结。

1.《企业税务风险管理的国际研究情况综述》该文献综述主要针对企业税务风险管理的研究现状和趋势进行综述,通过梳理国内外相关文献,分析了企业税务风险管理的内涵和特点,阐述了现阶段的研究成果和前沿热点。

综述首先介绍了企业税务风险管理的定义和内涵,特别强调了税务风险管理的综合性和复杂性。

随后,文献综述分析了企业税务风险管理中的风险识别、风险评估、风险应对等环节,并从国内外不同的研究视角进行了综述。

最后,文献综述对当前国际上主要的研究热点和未来的研究方向进行了总结,提出了有益的启示和建议。

该文献综述具有较高的实用性和可操作性,为企业经营决策者、税务从业人员和学者提供了有价值的参考。

同时,文章的语言简洁明了,结构清晰,阐述思路清晰,细致入微,体现了系统性、规范性和科学性的特点。

2.《会计信息质量研究综述》该文献综述主要针对会计信息质量研究的现状和进展进行综述,通过对国内外相关文献的梳理,归纳了会计信息质量的内涵、评价方法、影响因素等方面的研究成果,总结了该领域的研究动态和未来发展方向。

文章首先介绍了会计信息质量的定义和内涵,强调了信息质量对决策和经营管理的重要作用。

随后,文献综述对会计信息质量的评价指标和方法进行了详尽的叙述和比较,讨论了各自的优缺点和适用范围。

此外,该文献综述还重点讨论了会计信息质量的影响因素,包括公司治理、内部控制、审计、财务报告等因素,并通过实证研究验证了各因素对信息质量的影响程度和机理,深入揭示了会计信息质量的本质。

该文献综述具有较高的实用价值和科学意义,为从事会计研究和实践的专业人士提供了深入的研究思路和方法,也为企业和投资者等相关方提供了借鉴和参考。

会计稳健性的经济后果研究综述

会计稳健性的经济后果研究综述【摘要】会计稳健性是会计准则中的一个重要原则,它对公司的财务状况、投资者和债权人以及市场都有着重要的影响。

本文通过对会计稳健性的经济后果进行综述,从理论基础、公司财务状况、投资者和债权人、市场以及国际财务报告准则中的应用等方面展开探讨。

通过对相关研究的总结和分析,我们可以更深入地了解会计稳健性在不同领域中的作用和影响,为进一步研究和实践提供重要参考。

本文旨在全面剖析会计稳健性的经济后果,为相关学者和从业者提供理论参考和实践指导。

【关键词】会计稳健性、经济后果、研究、公司财务状况、投资者、债权人、市场、国际财务报告准则、理论基础、总结1. 引言1.1 会计稳健性的经济后果研究综述会计稳健性是会计准则中的一个重要原则,其主要目的是保护财务报表的真实性和可靠性。

会计稳健性要求会计人员在面对不确定性时,应该选择较为保守的会计处理方法,以确保财务报表不会过分乐观,从而导致投资者和债权人对公司的风险判断出现偏差。

对于公司而言,会计稳健性对其财务状况产生重要影响,可能影响投资者和债权人的投资决策,以及市场的整体表现。

本文将对会计稳健性的经济后果进行深入研究,分析其对公司财务状况、投资者和债权人、市场的影响,并探讨其在国际财务报告准则中的具体应用。

通过对现有文献和研究成果的梳理和分析,旨在为相关学术界和实践界提供一份系统全面的研究综述,帮助理解会计稳健性对经济的影响机制,同时为进一步研究和实践提供参考。

在接下来的内容中,我们将逐一探讨会计稳健性的理论基础、对公司财务状况的影响、对投资者和债权人的影响、对市场的影响以及在国际财务报告准则中的应用,以全面解析会计稳健性的经济后果。

2. 正文2.1 理论基础在实践中,会计稳健性的基础理论主要有以下几个方面:1. 预见性原则:会计稳健性要求公司在编制财务报表时应当根据已知的信息和数据以及合理的假设来做出判断。

这个原则确保了财务报表的真实性和准确性。

关于会计稳健性的文献综述

纳税Taxpaying财会研究关于会计稳健性的文献综述唐媚媚(云南民族大学管理学院,云南昆明650500)摘要:关于会计稳健性的研究国内外均有研究。

本文从国外关于会计稳健性的研究,国内关于会计稳健性的研究,简要评价方面进行文献综述。

通过这种方式可以更容易掌握国内外的研究状况。

关键词:会计稳健性;国外研究;国内研究一、国外研究Bliss(1924)最早对传统的会计稳健性进行了定义:预计所有的损失,但不预计任何收益。

Basu(1997)构建的会计盈余/报酬关系模型被学者广泛应用,并且在实证检验上丰富了稳健性的相关研究。

Pope和Walker(1999)比较了欧美国家不同地区上市公司的会计稳健性差异。

研究发现与英国上市公司相比,美国上市公司在扣除非常项目之前,会计稳健程度较高。

LaPortaetal (1998)指出当股权集中度提高时,控股股东可能会采取操纵公司财务信息等行动来掩饰自己侵占中小投资者利益的行为,降低了公司财务报表的会计信息稳健性。

Fan和Wong(2002)在对东亚新兴市场进行研究后指出,由于这些国家具有高度集中股权、投资者保护较弱以及公司治理机制不完善等问题,最终会使得公司的财务报告盈余信息含量降低、损害审计质量的后果。

Watts(2003)对会计稳健性进行了系统的研究,他认为契约、诉讼、税收和管制都会不同程度的影响会计稳健性。

Ahemed和Duellman(2007)通过研究美国公司再次证实公司治理结构的董事会特征影响企业的会计稳健性,表明独立董事占董事会的比例与会计稳健性成正相关关系,内部董事与会计稳健性成负相关关系。

Lafond和Watts(2008)通过实证发现信息不对称程度与会计稳健性成正向关系,公司的信息不对称程度越高,企业采用的会计政策越具有稳健性。

Kamran和Darren(2012)通过利用澳大利亚证券交易所公司11年的数据,研究发现董事会独立性的增加和董事会规模减小与会计稳健性呈正相关关系。

会计稳健性研究述评

会计稳健性研究述评更多的研究证明会计稳健性是财务报告的最重要特征。

稳健性的研究主要包括计量方法、产生原因及经济后果三个方面。

本文针对当前会计稳健性的最新研究内容进行了系统评论,主要的内容包括会计稳健性的计量方法及其之间的关系;会计稳健性起因的研究,重点集中在契约影响因素方面;会计稳健性对资本成本、企业经济活动造成的影响等。

通过上述的评论,指出了未来会计稳健性研究的发展方向。

标签:会计稳健性;计量方法;起因;经济后果会计稳健性是会计的基本原则之一。

我国的会计准则中对会计稳健性做出了相关规定:企业在交易、事项的会计确认、会计计量及报告的过程中,要保持谨慎,避免对资产或者收益出现高估、对负债或者费用出现低估的情况。

虽然会计稳健性原则由来已久,但直到上世纪九十年代才真正开始对稳健性进行系统研究,主要的原因是越来越多的国家开始在会计准则中采用公允价值计量。

一、关于会计稳健性的计量方法的相关研究(3330)Watts最早提出了对稳健性进行系统研究,他认为会计的契约作用导致了会计稳健性的产生。

之后,由于稳健性计量方法发展缓慢,导致了系统的检验稳健性的文献几乎没有。

直到Basu之后会计稳健性的研究才开始大量的涌现。

稳健性的研究主要包括计量方法、产生原因及经济后果三个方面。

Basu对会计稳健性做出较为全面的研究,但是这些研究中存在着不完善的地方。

Basu在分析总结的基础之上提出了反向回归法,但Dietrich、Muller、Riedl三人正对Basu的反向回归法从计量经济学的角度提出了两个方面的问题:第一,在回归的过程中,将内生变量作为自变量导致了结果不可接受;第二,负回报观察量较少导致了自变量出现阶段,使得稳健性计量中存在偏差。

Givoly、Hayn、Natarajan将Basu 的会计稳健性计量是为及时性差异计量,也就是指盈余对于坏消息的反应速度要高于对好消息的反应速度。

他们支持企业中存在的一些与稳健性无关对信息环境特征会对及时性差异的计量造成影响,因此指出Basu的稳健性计量存在着较大的计量错误。

应用文-会计稳健性研究述评

会计稳健性研究述评'稳健性研究述评一、会计稳健性定义(1)会计稳健性古典定义。

Bliss(1924)最先为会计稳健性定义,他将其定义为“对于可能发生的损失在可以预期时就进行确认,而对于任何不确定的收益要在实现之后才进行确认”。

(2)会计稳健性准则定义。

FASB SFAC2(1980)将其定义为“对于商业中的不确定性和风险作出的谨慎的反应。

如果未来收到或支付金额有多种不同的估计,且多种估计值发生的可能性相同,则使用较为不乐观的估计值;如果估计值发生的可能不同,并不一定要使用不乐观的估计值而舍弃可能性大的估计值。

”IASB(1980)将其定义为“审慎是指在不确定的情况下必须做出估计时更加谨慎,不虚增资产或收益,也不少计负债或费用。

然而,该原则并不意味着允许过分的提取准备,故意压低资产或收益,或故意抬高负债或费用等损害财务报表可靠性的行为”。

部新准则(2006)认为“企业对交易或者事项进行会计确认、计量和应当保持应有的谨慎,不应高估资产或者收益,低估负债或费用”。

以上对稳健性的界定,可见稳健性已经由“绝对稳健”为了“相对稳健”,强调了企业在不同的环境中面对损失和收益应持有不同态度,但也体现出对合理估计的重视。

二、会计稳健性计量方法(1)盈余——股票收益模型。

根据稳健性原则的要求,相比于确认损失,会计人员在确认收益时需要更高的可验证性,所以损失的确认比收益的确认更加及时。

而在有效市场中,公司股票的价格能对公司资产价格的变化做出反应。

因此,Basu提出公司股票收益率和会计盈余对于“好消息”和“坏消息”的敏感性是不同的,股票收益率的变动与收益和损失的发生基本同时,而会计盈余受稳健性的限制对收益和损失的反应表现出不对称性。

于是,他用公司正股票收益率代表“好消息”,用负股票收益率代表“坏消息”,构建了盈余股票收益“反向回归方程”。

稳健性意味着会计盈余对“坏消息”更为敏感,所以当回归方本文由联盟收集整理程中负股票收益的斜率和拟合优度更高时可以证明稳健性的存在并衡量稳健性的程度。

会计稳健性的文献综述

会计稳健性的文献综述作者:徐爱仙来源:《财讯》2018年第22期会计稳健性能够降低内外部的信息不对称和委托代理成本,抑制管理者的机会主义行为,具有一定的治理价值。

本文从会计稳健性的定义,起因等对会计稳健性的相关文献梳理和评述,有助于理清会计稳健性脉络趋势。

对我国未来会计稳健性进行展望,以期为后续研究提供参考。

会计稳健性文献综述Basu( 1997)提出会计稳健性是指会计盈余确认坏消息的速度比确认好消息的速度快,即对好消息和坏消息存在不对称及时性。

相关的法律法规要求会计从业人员确认资产和收益时保持谨慎的态度,只有当收益和资产很可能发生才进行确认,但是要及时确认所有可能发生的损失。

以避免企业管理者通过虚增收益,虚减支出费用,从而增加会计利润来进行盈余操纵。

本文将通过相关的文献梳理和论述,理清会计稳健性的趋势脉络,以期对后续研究提供参考。

会计稳健性的定义及分类Bliss( 1924) 1924年最早提出会计稳健性的原则就是不能预计任何不确定的收益,但是要预计所有可能的损失。

ASB( 1989)在其概念框架中将会计稳健性定义为“在需要对不确定的情况做出估计和判断时,应该持有谨慎的态度”。

Basu( 1997)会计稳健性是对坏消息(损失]比好消息(收益)确认更及时。

目前这种观点普遍被大多数学者所接受。

我国财政部2006年提出“企業在进行会计确认、计量和记录的过程中应该保持应有的谨慎不得高估资产或收益,不得低估负债和费用”。

根据学者的研究将会计稳健性分为条件性稳健和非条件性稳定。

本文所指的“会计稳健性”亦指条件稳健性。

综上所述,本文对会计稳健性的定义为:会计人员对当期“好消息”的确认比对当期“坏消息”的确认更及时,这种不对称性的及时性就是会计稳健性。

会计稳健性的起因Watts( 2003)随后通过对1993年至2003年的实证文献做了大量的研究,将稳健性产生的原因归结于如下几个方面:契约、股东诉讼、税收等。

坏账准备、稳健性与盈余管理的文献综述

(3)在税收因素下,会计稳健性可以促使企业管理 层对收入延期确认,同时加速确认费用和损失,进而减 少所得税的现值,进一步增加企业市场价值。

(4)在管制因素下,会计稳健性与政治成本有了联 系,稳健性能够降低企业由于高估净资产和收益而带 来的相关机构的批判,另一方面可以降低制定者和监 管者承担的政治成本。

在众多国外文献中,我们总结了常见的会计稳健 性的计量方法:

一是净资产基础计量。Feltham-Ohlson 定价模型 多 用 来 对 净 资 产 的 低 估 程 度 进 行 估 计。Fehhamand-

* 基金:2019 年度成都职业技术学院院级科学研究项目“管理层持股、内部控制与创新投入— — 基于医药行业上市公司面板数据的 研究”(项目编号:19CZYR009) 阶段性成果。

83

会计研究 KUAIJI YANJIU

Ohlson(1995)认为可以通过下面的方程(见下表方程 1) 来衡量公司的市场价值(V),并且 Feltham-Qhlson 推导 了一个 UM(线性信息模型)方程(见下表方程 2)。

而我国对稳健性的定义与国际会计准则有着相似 之处,2006 年,我国颁布的《企业会计准则》中相关条款 规定: “企业对交易事项进行确认、计量和报告应当保持 应有的谨慎,不应高估资产或收益,低估负债或者费用”。 总结这个条款,我们可以归纳出谨慎性在具体会计确认 时的处理原则:资产不应高估,所以我们应当于对存货 按照成本与可变现净值孰低法确认减值损失,要对应收 账款进行分析,计提坏账准备,要合理预计资产的跌价 和减值准备。除此之外,利息资本化和费用化的判断与 处理,研发支出资本化与费用化的处理都体现了会计的 谨慎性原则。会计谨慎性将影响企业的会计盈余,进而 影响企业的市场价值。因此,通过文献综述进一步理清 坏账准备、稳健性与盈余管理之间的关系很有必要。