chapter02。解析

(完整版)高分子材料成型加工唐颂超第三版第2-10章课后习题答案解析(仅供参考)

1.高分子材料中加入添加剂的目的是什么?添加剂可分为哪些主要类型? ① 满足性能上的要求 ② 满足成型加工上的要求 ③ 满足经济上的要求 添加剂可分为稳定剂、增塑剂、润滑剂、交联剂、填充剂等

2. 什么是热稳定剂?热稳定剂可分为哪些主要类型?其中那些品种可用于食品和医药包装 材料 热稳定剂是一类能防止或减少聚合物在加工使用过程中受热而发生降解或交联,延长复合材 料使用寿命的添加剂。可分为铅盐类、金属皂类、有机锡类、有机锑类、有机辅助、复合 稳定剂和稀土类稳定剂。 食药包装:有机锡类、有机锑类、复合稳定剂和稀土类稳定剂。 3.什么是热稳定剂?哪一类聚合物在成型加工中须使用热稳定剂?对于加有较多增塑剂和 不加增塑剂的两种塑料配方,如何考虑热稳定剂的加入量?请阐明理由。 热稳定剂是指在加工塑料制品时为防止加工时的热降解或者防止制品在长期使用过程中老

滑移越困难,聚合物流动时非牛顿性越强。聚合物分子链刚性增加,分子间作用力愈大, 粘度对剪切速率的敏感性减小,但粘度对温度的敏感性增加,提高这类聚合物的加工温度 可有效改善其流动性。

聚合物分子中支链结构的存在对粘度也有很大的影响。具有短支链的聚合物的粘度低于 具有相同相对分子质量的直链聚合物的粘度;支链长度增加,粘度随之上升,支链长度增 加到一定值,粘度急剧增高。在相对分子质量相同的条件下,支链越多,越短,流动时的 空间位阻越小,粘度越低,越容易流动。较多的长支

晶态聚合物:(1)若聚合物的分子量较小,Tm>Tf,则聚合物达到熔点时已进入粘流态, 则熔融加工温度范围即为 Tm~Td(热分解温度);若聚合物的分子量较大,分子链相互作 用力较大,当晶区熔融时,分子链还需要吸收更多能量克服分子间作用力,才能产生运动, 因此聚合物的 Tm<Tf,则熔融加工温度范围为 Tf~Td。 非晶态聚合物:熔融加工温度范围为 Tf~Td。 比较结晶聚合物和非晶聚合物耐热性的好坏必须在两者化学结构相似的前提下。在两者化 学结构相似时,结晶聚合物由于晶区分子链排列较为规整,聚合物由固态变为熔融状态时, 需要先吸收热量使晶区变为非晶区,然后再进入粘流态,非晶态聚合物由于分子链刚性较 大,链柔顺性较差或者规整度较低,因此结晶聚合物比非晶态聚合物能够耐更高的温度, 作为材料使用时,其耐热性更好些。如结晶的等规聚苯乙烯的耐热性比非晶的无规聚苯乙 烯高 4. 为什么聚合物的结晶温度范围是 Tg~Tm? 答:T>Tm 分子热运动自由能大于内能,难以形成有序结构 T<Tg 大分子链段运动被冻结,不能发生分子重排和形成结晶结构 5. 什么是结晶度?结晶度的大小对聚合物性能有哪些影响 1)力学性能 结晶使塑料变脆(耐冲击强度下降),韧性较强,延展性较差。 2)光学性能 结晶使塑料不透明,因为晶区与非晶区的界面会发生光散射。减小球晶尺寸 到一定程式度,不仅提高了塑料的强度(减小了晶间缺陷)而且提高了透明度,(当球晶尺 寸小于光波长时不会产生散射)。 3)热性能 结晶性塑料在温度升高时不出现高弹态,温度升高至熔融温度 TM 时,呈现粘 流态。因此结晶性塑料的使用温度从 Tg (玻璃化温度)提高到 TM(熔融温度)。 4)耐溶剂性,渗透性等得到提高,因为结晶分排列更加紧密。 6.何谓聚合物的二次结晶和后结晶? 二次结晶:指一次结晶后,在残留的非晶区和结晶不完整的部分区域内,继续结晶并逐步 完善的过程,此过程很缓慢,可能几年甚至几十年。 后结晶:指一部分来不及结晶的区域,在成型后继续结晶的过程,不形成新的结晶区域, 而在球晶界面上使晶体进一步张大,是初结晶的继续。 7. 聚合物在成型过程中为什么会发生取向?成型时的取向产生的原因及形式有哪几种?取 向对高分子材料制品的性能有何影响?

语言学教程02Chapter 2_sound(2)

If the sound becomes more like the following sound, as in the case of lamb, it is known as anticipatory coarticulation先期协同发音. If the sound shows the influence of the preceding sound, it is perseverative coarticulation后滞协同 发音, as is the case of map.

In phonetic terms, phonemic transcriptions represent the „broad‟ transcriptions.

3.3 Allophones 音位变体

Allophones---- the different phones which can represent a phoneme in different phonetic contexts.

Velarization: clear l and dark l // [] / _____ V [] / V _____

Think about tell and telling!

Phonetic similarity发音近似性: the allophones of a phoneme must bear some phonetic resemblance.

The word „phoneme‟音位 simply refers to a „unit of explicit sound contrast‟: the existence of a minimal pair automatically grants phonemic status to the sounds responsible for the contrasts.

C语言chapter02

举例。 举例。若有变量定义 int a=2;

float b=1.2345;

则变量a、 在内存中的存储情况如图示 在内存中的存储情况如图示。 则变量 、b在内存中的存储情况如图示。

“& ”表示取 地址。

&a=2000H 2001H &b=2002H 2003H 2004H 2005H

2

1.2345

不允许将一个字符串常量赋给一个字符型变量。 不允许将一个字符串常量赋给一个字符型变量。

• 如:ch=‘a’;是正确的,而ch= a”;不是将字符a赋值给 ch= a ;是正确的, ch=“a ;不是将字符a 变量ch ch。 变量ch。

2.7 变量的初始化

变量赋初值

• C语言允许在定义变量时对变量进行初始化,即 对变量赋初值。 如:int 如:int a=2; 等价于int a;a=2; 等价于int a; • 对变量进行初始化,允许只对定义的变量的一部 分赋初值。 如:int 如:int a,b,c=25; char ch1=‘x’,ch2; • C语言中若有几个变量初值相同,必须分别赋值。 如: int a=2,b=2,c=2; • 对字符型变量初始化时,既可以将字符用单引号 括起来直接赋值,也可以使用该字符的ASCII码 括起来直接赋值,也可以使用该字符的ASCII码 进行赋值。 如:char ch=‘A’;等价于char 如:char ch=‘A’;等价于char ch=65;

存字节, 个含有单个字符的字符串常量需要占用2个字节。 个含有单个字符的字符串常量需要占用2个字节。

• 如:‘a’在内存中只占1个字节,“a”则需占用2个字 在内存中只占1 则需占用2 在内存中只占 个字节, 则需占用 节空间。 节空间。

Chapter 2 Speech Sounds

2.1 How Speech Sounds Are Made? The Nasal Cavity(鼻腔)

●When the vocal cords are apart, the air can pass through easily and the sound produced is said to be voiceless. e.g. [p, s, t ] ●When they are close together, the airstreams cause them to vibrate and produces voiced sounds. e.g. [b, z, d] ●When they are totally closed, no air can pass between them, then produce the glottal stop [?]none in En.

2.1 How Speech Sounds Are Made? The Oral Cavity(口腔)

The oral cavity provides the greatest source of modification. Tongue: the most flexible Uvula, the teeth and the lips, Hard palate, soft palate (velum) Alveolar ridge: the rough, bony ridge immediately behind the upper teeth

chapter02GoF设计模式创建型模式

为什么学习创建型模式

1 2 3

提高代码的可维护性和可扩展性

通过合理地使用创建型模式,可以减少代码的耦 合度,使代码更加模块化,便于维护和扩展。

解决常见的设计问题

创建型模式针对常见的设计问题提供了解决方案, 如单例模式解决全局唯一实例的问题,工厂模式 解决对象创建的问题等。

提高设计能力

掌握创建型模式有助于提高软件设计能力,使设 计更加符合面向对象的设计原则,如开闭原则、 单一职责原则等。

ABCD

抽象工厂模式

提供一个接口,用于创建相关或依赖对象的家族, 而不需要明确指定具体类。

建造者模式

通过提供一系列的步骤来构建一个复杂的对象, 使得对象的创建更加灵活和可复用。

适用场景

需要创建大量相似对象时,可以通过创建型模式 来提高代码的复用性和可维护性。

当对象的创建逻辑复杂且容易出错时,使用创建 型模式可以降低错误率并提高代码的可读性。

通过使用创建型模式,代码结构更加清晰,易于阅读和维护。

3. 提高性能

某些创建型模式(如对象池模式)可以提高性能,特别是在需要频繁创建和销 毁对象的情况下。

总结

局限性

1. 过度使用创建型模式可能导致代码过于复杂,增加理解 和维护的难度。

2. 在某些情况下,使用创建型模式可能不是最优解决方案, 例如过度使用单例模式可能导致代码缺乏灵活性。

展望

应用前景

创建型模式在未来的软件开发中仍将发挥重要作用,特别是在处理复杂对象关系、提高软件可维护性 和可扩展性方面。随着软件工程理论的不断发展,创建型模式将不断创新和完善,为解决实际软件开 发问题提供更多有效的解决方案。

THANKS

感谢观看

在工厂方法模式中,工厂方法抽象了创建对象的过程,由子 类决定要实例化哪一个类。工厂方法模式让子类决定要实例 化哪一个类,这样就可以在不修改客户端代码的情况下,增 加新的产品。

微观经济学 第七版 丹尼尔 罗伯特 中央财经大学 chapter 02【精选】

中央财经大学

宋一淼

ogscs@

Chapter 2 The Basics of Supply and Demand

第二章

供给和需求的基本原理

本章概要

• 2.1 供给与需求 • 2.2 市场机制 • 2.3 市场均衡的变动 • 2.4 供给和需求的弹性 • 2.5 政府干预的结果——价格管制

• 原材料的成本下降则生产更 P 有利可图(市场价格不变)

– 在价格P1上,生产Q1 Q2

– 在价格P2上,生产Q0 Q1

– 供给曲线向右移动到S’

P1

– 任何价格水平上,S’都比S供 P2 给更多的产品

– 解释2:固定产量Q1,成本降 低则会选择更低市场价格P2-连点成S’

S

S’

Q0 Q1 Q2 Q

2.1.1. 供给

• 在一个较高的价格,厂商可能通过雇佣 额外的工人或通过让现有工人加班工作 ,以便在短期内扩大生产;

• 而在长期,厂商则可以扩大工厂的规模 达到增产的目的。

• 与此同时,较高的价格可能吸引新的厂 商的加入,而新的厂商则可能由于缺乏 经验等缘故面临更高的产品成本。

2.1.1. 供给

2.1.2.需求

Change in Demand

• 收入增加(价格水平不变) P

– 在价格P1, 需求为Q1 பைடு நூலகம்2

P2

– 在价格P2,需求为Q0 Q1

– 需求曲线向右移动

P1

– 任一给定的价格上,D’曲

线上购买的商品比D多。

– 解释2:消费固定为Q1,价格 水平为P1,收入增加后愿意 支付的价格为P2,连点成D’ 。

2.1.2. 需求

• 需求曲线(demand curve) 需求曲线告诉我们,在非价格因素保持

机械原理:第二章机构的结构分析

斜齿轮机构

两个齿轮的齿廓为斜线,实现直线的 运动传递,同时具有较好的承载能力 和传动平稳性。

02

CHAPTER

机构的运动分析

机构运动简图

总结词

机构运动简图是表示机构运动关系的图形,通过图形化方式展示机构的组成和运 动传递路径。

详细描述

机构运动简图是一种抽象的图形表示,它忽略了机构的实际尺寸和形状,只关注 机构中各构件之间的相对运动关系。通过绘制机构运动简图,可以清晰地了解机 构的组成、运动传递路径以及各构件之间的相对位置和运动方向。

常见的受力分析方法

详细描述:常见的受力分析方法包括解析法、图解法和 有限元法等,每种方法都有其适用范围和优缺点,应根 据具体情况选择合适的方法。

机构的平衡分析

总结词

理解机构平衡的概念是进行平衡 分析的前提。

详细描述

机构平衡是指机构在静止或匀速 运动状态下,各作用力相互抵消 ,机构不会发生运动状态的改变 。

轮系

定轴轮系

各齿轮的转动轴线固定,齿轮的 运动由一个主动轮通过各齿轮的

啮合传递到另一个从动轮。

行星轮系

其中一个齿轮的转动轴线绕着另 一固定轴线转动,行星轮既可绕 自身轴线自转,又可绕固定轴线

公转。

混合轮系

由定轴轮系和行星轮系组合而成, 既有定轴轮系的自转运动,又有

行星轮系的公转和自转运动。

凸轮机构

机构运动分析的方法

总结词

机构运动分析的方法主要包括解析法和图解法两种。

详细描述

解析法是通过建立数学模型,运用数学工具进行求解的方法。这种方法精度高,适用于对机构进行精确的运动学 和动力学分析。图解法是通过作图和测量来分析机构运动的方法,这种方法直观易懂,适用于初步了解机构的运 动关系。

02Chapter 2_sound

The distinction between vowels and consonants lies in the obstruction of airstream. 元音和辅音的根本区别在于气流是否受阻. As there is no obstruction of air in the production of vowels, the description of the consonants and vowels cannot be done along the same lines.

Phonetics studies how speech sounds are produced, transmitted, and perceived.

Articulatory Phonetics is the study of the production of speech sounds. Acoustic Phonetics is the study of the physical properties of speech sounds. Perceptual or Auditory Phonetics is concerned with the perception of speech sounds.

When they are totally closed, no air can pass between them. The result of this gesture is the glottal stop [?] 声门塞音.

1.2 The IPA 国际音标

In 1886, the Phonetic Teachers‟ Association was inaugurated by a small group of language teachers in France who had found the practice of phonetics useful in their teaching and wished to popularize their methods.

HW_chapter02

通信原理2011年春季第二章“连续波模拟调制”作业(含附录一“信号与系统”回顾)习题 1分别计算图(a )中信号()(),x t y t 的能量,x y E E 。

画出信号波形()()x t y t +与()()x t y t −,通过计算判断这两个新信号的能量是否等于x y E E +。

对图(b )和图(c )中的()(),x t y t 波形重复上述计算过程。

习题 2证明对于任意的实数a ,信号(),,at e t −∈−∞+∞既不是能量信号也不是功率信号。

但是,如果a 是虚数,无论a 取值为多少,at e −为功率信号,其功率1P =。

习题 3证明如果()g t 的傅里叶变换为()G ω,则()*g t 的傅里叶变换为()*G ω−。

习题 4根据傅里叶变换的性质,分别计算下列时域信号的频谱。

习题 5如图所示,信号()()44110rect 10g t t =与()()2g t t δ=分别输入到理想低通滤波器()()()1rect 40000H ωωπ=和())()2rect 20000H ωωπ=中。

输出信号()()12,y t y t 经过乘法器后得到信号()()()12y t y t y t =。

(注:定义()rect 1, for 0.5t t =≤) (a ) 画出()1G ω和()2G ω。

(b ) 画出()1H ω和()2H ω。

(c ) 画出()1Y ω和()2Y ω。

(d ) 分别计算()()()12,,y t y t y t 的带宽。

习题 6对于以下基带信号:(i) ()cos1000m t t =(ii) ()2cos1000cos2000m t t t =+(iii) ()cos1000cos3000m t t t =⋅(a) 画出()m t 的频谱;(b) 画出DSB-SC 调制后的信号()cos10000m t t 的频谱;(c) 指出哪些频率成分属于上边带,哪些属于下边带。

chapter02课后作业

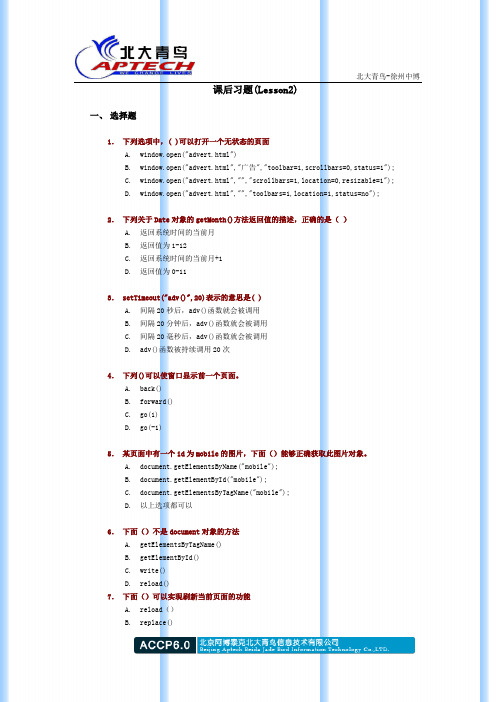

北大青鸟-徐州中博课后习题(Lesson2)一、选择题1.下列选项中,( )可以打开一个无状态的页面A.window.open("advert.html")B.window.open("advert.html","广告","toolbar=1,scrollbars=0,status=1");C.window.open("advert.html","","scrollbars=1,location=0,resizable=1");D.window.open("advert.html","","toolbars=1,location=1,status=no");2.下列关于Date对象的getMonth()方法返回值的描述,正确的是()A.返回系统时间的当前月B.返回值为1-12C.返回系统时间的当前月+1D.返回值为0-113.setTimeout("adv()",20)表示的意思是( )A.间隔20秒后,adv()函数就会被调用B.间隔20分钟后,adv()函数就会被调用C.间隔20毫秒后,adv()函数就会被调用D.adv()函数被持续调用20次4.下列()可以使窗口显示前一个页面。

A.back()B.forward()C.go(1)D.go(-1)5.某页面中有一个id为mobile的图片,下面()能够正确获取此图片对象。

A.document.getElementsByName("mobile");B.document.getElementById("mobile");C.document.getElementsByTagName("mobile");D.以上选项都可以6.下面()不是document对象的方法A.getElementsByTagName()B.getElementById()C.write()D.reload()7.下面()可以实现刷新当前页面的功能A.reload()B.replace()北大青鸟-徐州中博C.hrefD.referrer二、简答题1.简述prompt(),alert()和confirm()三者的区别,并举例说明。

02---Chapter Two 代词 Pronouns 语法讲解系列

Chapter Two 代词Pronouns一、基本概念代词是用来代替名词或名词性短语或句子的词类。

从本质上说,它属于名词性词类,即在不指出具体名词、名词短语或名词性句子的情况下,用以代替说明它的词类。

二、基本分类1、人称代词2、物主代词3、反身代词4.疑问代词1)分类2)A考点:疑问副词how (方式),when (时间),where (地点),why (原因);how组成的疑问副词短语:how often(提问频率“多久一次");how far (提问距离“多远”);how soon (“多快,多久以后”);how long (提问长度或时间段"多长,多久”);how much (提问价钱;提问不可数名词数量“多少”);how many (提问可数名词数量“多少”)5、不定代词1)分类:普通不定代词和复合不定代词注意:常用普通不定代词注意:常用复合不定代词2)用法:many和much:many与可数名词复数连用;与不可数名词连用。

如: I don't have many friends here. 在这里我没有很多的朋友.。

We can learn much with the help of him. 在他的帮助之下我们能学到很多。

some 和any:some, any既可以修饰可数名词,也可以修饰不可数名词;some常用在肯定句中;any多用于否定句、疑问句及条件句中。

some用于表示请求、邀请、建议的疑问句,或希望得到对方肯定回答的疑问句中如:Will you have another cup of tea? 再来杯茶好吗?Mum, could you give me some money? 妈妈,能给我些钱吗?当any表示“任何”或“无论哪一个”的含义时,可用于肯定句,You may come at any time that is convenient to you. 你可以在对你方便的任何时候来。

室内设计快题手绘表达与解析

8.1人居空间室内快题设计手绘范例及评析 8.2商业空间室内快题设计手绘及范例评析 8.3休闲交流空间室内快题设计手绘及范例评析 8.4办公空间室内快题设计手绘范例及评析 8.5工作室改造室内快题设计手绘范例及评析 8.6茶室室内快题设计手绘范例及评析 8.7咖啡厅、休闲简餐空间室内快题设计手绘范例及评析 8.8书吧阅读空间室内快题设计手绘范例及评析 8.9展示陈列空间室内快题设计手绘范例及评析

5.1室内快题中平面图设计手绘表达的标准 5.2室内快题中平面图设计手绘线稿范例及评析 5.3室内快题中平面图设计手绘颜色稿范例及评析

6.1室内快题中立面图、剖面图设计手绘线稿范例及评析 6.2室内快题中立面图、剖面图设计手绘颜色稿范例及评析

7.1室内快题手绘线稿范例及评析 7.2室内快题手绘绘制的步骤和方法

目录分析

01

内容简介

02

PREFACE序

03

RECOMMEN DATION推 荐语

04

RECOMMEN DATION推 荐语

06

Chapter 02室内设 计快题手绘 的主要内容 和命题解析

05

Chapter 01室内设 计快题手绘 表达综述

Chapter 03室内快 题设计中的版CKNOWLEDGEMENT

1.1室内设计快题手绘的考试要求和评判标准 1.2室内设计快题手绘中的常见问题 1.3室内设计快题手绘抄绘练习方法

2.1室内快题设计手绘的主要内容 2.2室内快题设计手绘的常见空间类型 2.3室内快题设计手绘传统型命题解析 2.4室内快题设计手绘开放式命题解析

3.1室内快题设计中的版式设计 3.2室内快题设计中的标题字设计手绘表达

4.1思维导图分析设计手绘表达 4.2功能分析和流线分析设计手绘表达 4.3体块生成分析设计手绘表达 4.4光照分析设计手绘表达 4.5垂直流线分析(爆炸分析图)设计手绘表达 4.6构造分析、节点分析设计手绘表达 4.7场景分析设计手绘表达 4.8交互分析设计手绘表达 4.9其他类型分析设计手绘表达

Chapter02 Functions

volatile while

Not allowed, because an identifier is a token

7 Copyright © 2012 by The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

format_string plain characters – displayed directly unchanged on the screen, e.g. “This is C” conversion specification(s) – used to convert, format and display argument(s) from the argument_list escape sequences – control the cursor, for example, the newline ‘\n’

equal

10 Copyright © 2012 by The McGraw-Hill Companies, Inc. Permission required for reproduction or display.

printf

To display the value of a variable or constant on the screen printf(format_string,argument_list);

Need to make up your own variable names, e.g. lengths: a, b, c angles: a, b, g

For programming in C, the situation is similar choose the variable names, consist of entire words rather than single characters easier to understand your programs if given very descriptive names to each variable

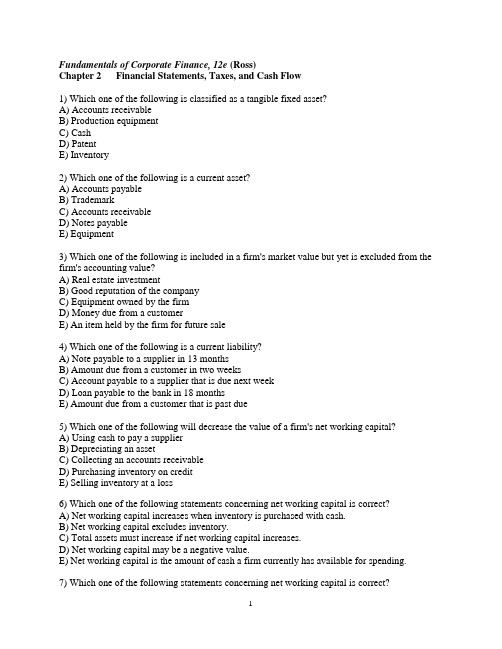

公司理财精要版原书第12版习题库答案Ross12e_Chapter02_TB

Fundamentals of Corporate Finance, 12e (Ross)Chapter 2 Financial Statements, Taxes, and Cash Flow1) Which one of the following is classified as a tangible fixed asset?A) Accounts receivableB) Production equipmentC) CashD) PatentE) Inventory2) Which one of the following is a current asset?A) Accounts payableB) TrademarkC) Accounts receivableD) Notes payableE) Equipment3) Which one of the following is included in a firm's market value but yet is excluded from the firm's accounting value?A) Real estate investmentB) Good reputation of the companyC) Equipment owned by the firmD) Money due from a customerE) An item held by the firm for future sale4) Which one of the following is a current liability?A) Note payable to a supplier in 13 monthsB) Amount due from a customer in two weeksC) Account payable to a supplier that is due next weekD) Loan payable to the bank in 18 monthsE) Amount due from a customer that is past due5) Which one of the following will decrease the value of a firm's net working capital?A) Using cash to pay a supplierB) Depreciating an assetC) Collecting an accounts receivableD) Purchasing inventory on creditE) Selling inventory at a loss6) Which one of the following statements concerning net working capital is correct?A) Net working capital increases when inventory is purchased with cash.B) Net working capital excludes inventory.C) Total assets must increase if net working capital increases.D) Net working capital may be a negative value.E) Net working capital is the amount of cash a firm currently has available for spending.7) Which one of the following statements concerning net working capital is correct?A) A firm's ability to meet its current obligations increases as the firm's net working capital decreases.B) An increase in net working capital must also increase current assets.C) Net working capital increases when inventory is sold for cash at a profit.D) Firms with equal amounts of net working capital are also equally liquid.E) Net working capital is a part of the operating cash flow.8) Which one of the following accounts is the most liquid?A) InventoryB) BuildingC) Accounts ReceivableD) EquipmentE) Land9) Which one of the following represents the most liquid asset?A) $100 account receivable that is discounted and collected for $96 todayB) $100 of inventory that is sold today on credit for $103C) $100 of inventory that is discounted and sold for $97 cash todayD) $100 of inventory that is sold today for $100 cashE) $100 of accounts receivable that will be collected in full next week10) Which one of the following statements related to liquidity is correct?A) Liquid assets tend to earn a high rate of return.B) Liquid assets are valuable to a firm.C) Liquid assets are defined as assets that can be sold quickly regardless of the price obtained.D) Inventory is more liquid than accounts receivable because inventory is tangible.E) Any asset that can be sold is considered liquid.11) Shareholders' equity:A) is referred to as a firm's financial leverage.B) is equal to total assets plus total liabilities.C) decreases whenever new shares of stock are issued.D) includes patents, preferred stock, and common stock.E) represents the residual value of a firm.12) As the degree of financial leverage increases, the:A) probability a firm will encounter financial distress increases.B) amount of a firm's total debt decreases.C) less debt a firm has per dollar of total assets.D) number of outstanding shares of stock increases.E) accounts payable balance decreases.13) The book value of a firm is:A) equivalent to the firm's market value provided that the firm has some fixed assets.B) based on historical cost.C) generally greater than the market value when fixed assets are included.D) more of a financial than an accounting valuation.E) adjusted to the market value whenever the market value exceeds the stated book value.14) The value of which one of the following is included in the market value of a firm but is excluded from the firm's book value?A) Office equipmentB) CopyrightC) Distribution warehouseD) Employee's experienceE) Land acquired over 25 years ago15) You recently purchased a grocery store. At the time of the purchase, the store's market value and its book value were equal. The purchase included the building, fixtures, and inventory. Which one of the following is most apt to cause the market value of this store to be less than its book value?A) A sudden and unexpected increase in inflationB) The replacement of old inventory items with more desirable productsC) Improvements to the surrounding area by other store ownersD) Construction of a new restricted access highway located between the store and the surrounding residential areasE) Addition of a stop light at the main entrance to the store's parking lot16) Which one of the following is the financial statement that shows the accounting value of a firm's equity as of a particular date?A) Income statementB) Creditor's statementC) Balance sheetD) Statement of cash flowsE) Dividend statement17) Net working capital is defined as:A) total liabilities minus shareholders' equity.B) current liabilities minus shareholders' equity.C) fixed assets minus long-term liabilities.D) total assets minus total liabilities.E) current assets minus current liabilities.18) Which one of these sets forth the common set of standards and procedures by which audited financial statements are prepared?A) Matching principleB) Cash flow identityC) Generally Accepted Accounting PrinciplesD) Financial Accounting Reporting PrinciplesE) Standard Accounting Value Guidelines19) Which one of the following is the financial statement that summarizes a firm's revenue and expenses over a period of time?A) Income statementB) Balance sheetC) Statement of cash flowsD) Tax reconciliation statementE) Market value report20) Noncash items refer to:A) fixed expenses.B) inventory items purchased using credit.C) the ownership of intangible assets such as patents.D) expenses that do not directly affect cash flows.E) sales that are made using store credit.21) Which one of the following is true according to generally accepted accounting principles?A) Depreciation is recorded based on the market value principle.B) Income is recorded based on the realization principle.C) Costs are recorded based on the realization principle.D) Depreciation is recorded based on the recognition principle.E) Costs of goods sold are recorded based on the recognition principle.22) Which one of these is most apt to be a fixed cost?A) Raw materialsB) Manufacturing wagesC) Management bonusesD) Office salariesE) Shipping and freight23) Which one of the following statements is correct assuming accrual accounting is used?A) The addition to retained earnings is equal to net income plus dividends paid.B) Credit sales are recorded on the income statement when the cash from the sale is collected.C) The labor costs for producing a product are expensed when the product is sold.D) Interest is a non-cash expense.E) Depreciation increases the marginal tax rate.24) The percentage of the next dollar you earn that must be paid in taxes is referred to as the________ tax rate.A) meanB) residualC) totalD) averageE) marginal25) The ________ tax rate is equal to total taxes divided by total taxable income.A) deductibleB) residualC) totalD) averageE) marginal26) Which one of the following statements related to corporate taxes is correct?A) A company's marginal tax rate must be equal to or lower than its average tax rate.B) The tax for a company is computed by multiplying the marginal tax rate times the taxable income.C) Additional income is taxed at a firm's average tax rate.D) The marginal tax rate will always exceed a company's average tax rate.E) The marginal tax rate for a company can be either higher than or equal to the average tax rate.27) Which one of the following statements concerning corporate income taxes is correct for 2018?A) All corporations are exempt from federal taxation.B) Corporations pay no tax on their first $50,000 of income.C) The federal income tax on corporations is a flat-rate tax with the same rate applying to all levels of taxable income.D) The marginal tax rate will always be lower than the average tax rate.E) The first 25 percent of corporate income is exempt from taxation.28) The cash flow that is available for distribution to a corporation's creditors and stockholders is called the:A) operating cash flow.B) net capital spending.C) net working capital.D) cash flow from assets.E) cash flow to stockholders.29) Which term relates to the cash flow that results from a company's ongoing, normal business activities?A) Operating cash flowB) Capital spendingC) Net working capitalD) Cash flow from assetsE) Cash flow to creditors30) Cash flow from assets is also known as the firm's:A) capital structure.B) equity structure.C) hidden cash flow.D) free cash flow.E) historical cash flow.31) The cash flow related to interest payments less any net new borrowing is called the:A) operating cash flow.B) capital spending cash flow.C) net working capital.D) cash flow from assets.E) cash flow to creditors.32) Cash flow to stockholders is defined as:A) the total amount of interest and dividends paid during the past year.B) the change in total equity over the past year.C) cash flow from assets plus the cash flow to creditors.D) operating cash flow minus the cash flow to creditors.E) dividend payments less net new equity raised.33) Which one of the following is an expense for accounting purposes but is not an operating cash flow for financial purposes?A) Interest expenseB) TaxesC) Cost of goods soldD) Labor costsE) Administrative expenses34) Depreciation for a tax-paying firm:A) increases expenses and lowers taxes.B) increases the net fixed assets as shown on the balance sheet.C) reduces both the net fixed assets and the costs of a firm.D) is a noncash expense that increases the net income.E) decreases net fixed assets, net income, and operating cash flows.35) Which one of the following statements related to an income statement is correct?A) Interest expense increases the amount of tax due.B) Depreciation does not affect taxes since it is a non-cash expense.C) Net income is distributed to dividends and paid-in surplus.D) Taxes reduce both net income and operating cash flow.E) Interest expense is included in operating cash flow.36) Which one of the following statements is correct concerning a corporation with taxable income of $125,000?A) Taxable income minus dividends paid will equal the ending retained earnings for the year.B) An increase in depreciation will increase the operating cash flow.C) Net income divided by the number of shares outstanding will equal the dividends per share.D) Interest paid will be included in both net income and operating cash flow.E) An increase in the tax rate will increase both net income and operating cash flow.37) Which one of the following will increase the cash flow from assets, all else equal?A) Decrease in cash flow to stockholdersB) Decrease in operating cash flowC) Decrease in the change in net working capitalD) Decrease in cash flow to creditorsE) Increase in net capital spending38) For a tax-paying firm, an increase in ________ will cause the cash flow from assets to increase.A) depreciationB) net capital spendingC) the change in net working capitalD) taxesE) production costs39) Which one of the following must be true if a firm had a negative cash flow from assets?A) The firm borrowed money.B) The firm acquired new fixed assets.C) The firm had a net loss for the period.D) The firm utilized outside funding.E) Newly issued shares of stock were sold.40) An increase in the interest expense for a firm with a taxable income of $123,000 will:A) increase net income.B) increase gross income.C) increase the cash flow from assets.D) decrease the cash flow from equity.E) decrease the operating cash flow.41) Which one of the following is excluded from the cash flow from assets?A) Accounts payableB) InventoryC) SalesD) Interest expenseE) Cost of goods sold42) Net capital spending:A) is equal to ending net fixed assets minus beginning net fixed assets.B) is equal to zero if the decrease in the net fixed assets is equal to the depreciation expense.C) reflects the net changes in total assets over a stated period of time.D) is equivalent to the cash flow from assets minus the operating cash flow minus the change in net working capital.E) is equal to the net change in the current accounts.43) Which one of the following statements related to the cash flow to creditors must be correct?A) If the cash flow to creditors is positive, then the firm must have borrowed more money than it repaid.B) If the cash flow to creditors is negative, then the firm must have a negative cash flow from assets.C) A positive cash flow to creditors represents a net cash outflow from the firm.D) A positive cash flow to creditors means that a firm has increased its long-term debt.E) If the cash flow to creditors is zero, then a firm has no long-term debt.44) A positive cash flow to stockholders indicates which one of the following with certainty?A) The dividends paid exceeded the net new equity raised.B) The amount of the sale of common stock exceeded the amount of dividends paid.C) No dividends were distributed, but new shares of stock were sold.D) Both the cash flow to assets and the cash flow to creditors must be negative.E) Both the cash flow to assets and the cash flow to creditors must be positive.45) A firm has $680 in inventory, $2,140 in fixed assets, $210 in accounts receivables, $250 in accounts payable, and $80 in cash. What is the amount of the net working capital?A) $970B) $720C) $640D) $3,110E) $2,86046) A firm has net working capital of $560. Long-term debt is $3,970, total assets are $7,390, and fixed assets are $3,910. What is the amount of the total liabilities?A) $2,050B) $2,920C) $4,130D) $7,950E) $6,89047) A firm has common stock of $6,200, paid-in surplus of $9,100, total liabilities of $8,400,current assets of $5,900, and fixed assets of $21,200. What is the amount of the shareholders' equity?A) $6,900B) $15,300C) $18,700D) $23,700E) $35,50048) Your firm has total assets of $4,900, fixed assets of $3,200, long-term debt of $2,900, and short-term debt of $1,400. What is the amount of net working capital?A) −$100B) $300C) $600D) $1,700E) $1,80049) Bonner Automotive has shareholders' equity of $218,700. The firm owes a total of $141,000 of which 40 percent is payable within the next year. The firm has net fixed assets of $209,800. What is the amount of the net working capital?A) $149,900B) $93,500C) $125,600D) −$47,500E) $56,50050) Four years ago, Ship Express purchased a mailing machine at a cost of $218,000. This equipment is currently valued at $97,400 on today's balance sheet but could actually be sold for $92,900. This is the only fixed asset the firm owns. Net working capital is $41,300 and long-term debt is $102,800. What is the book value of shareholders' equity?A) $31,400B) $47,700C) $35,900D) $249,400E) $253,90051) The What-Not Shop owns the building in which it is located. This building initially cost $647,000 and is currently appraised at $819,000. The fixtures originally cost $148,000 and are currently valued at $65,000. The inventory has a book value of $319,000 and a market value equal to 1.1 times the book value. The shop expects to collect 96 percent of the $21,700 in accounts receivable. The shop has $26,800 in cash and total debt of $414,700. What is the market value of the shop's equity?A) $867,832B) $900,166C) $695,832D) $775,632E) $1,190,33252) The Widget Co. purchased all of its fixed assets three years ago for $4 million. These assets can be sold today for $2 million. The current balance sheet shows net fixed assets of $2,500,000, current liabilities of $1,375,000, and net working capital of $725,000. If all the current assets were liquidated today, the company would receive $1.9 million in cash. The book value of the total assets today is ________ and the market value of those assets is ________.A) $4,600,000; $3,900,000B) $4,600,000; $3,125,000C) $5,000,000; $3,125,000D) $5,000,000; $3,900,000E) $6,500,000; $3,900,00053) JJ Enterprises has inventory of $11,600, fixed assets of $22,400, total liabilities of $12,900, cash of $1,900, accounts receivable of $8,700, and long-term debt of $6,500. What is the net working capital?A) $44,600B) $15,700C) $12,600D) $15,800E) $9,30054) The River Side Stop has a current market value of $26,400 and owes its creditors $31,300. What is the market value of the shareholders' equity?A) −$4,900B) −$5,200C) $0D) $4,900E) $5,20055) Jensen Enterprises paid $700 in dividends and $320 in interest this past year. Common stock remained constant at $6,800 and retained earnings decreased by $180. What is the net income for the year?A) $180B) $520C) $1,020D) $880E) $1,20056) Andre's Bakery has sales of $487,000 with costs of $263,000. Interest expense is $26,000 and depreciation is $42,000. The tax rate is 21 percent. What is the net income?A) $142,750B) $123,240C) $109,000D) $128,700E) $134,55057) Hayes Bakery has sales of $30,600, costs of $15,350, an addition to retained earnings of $4,221, dividends paid of $469, interest expense of $1,300, and a tax rate of 21 percent. What is the amount of the depreciation expense?A) $4,820.13B) $5,500.89C) $8,013.29D) $8,180.01E) $9,500.0058) Last year, Kaylor Equipment had $15,900 of sales, $500 of net new equity, dividend payments of $75, an addition to retained earnings of $418, depreciation of $680, and $511 of interest expense. What are the earnings before interest and taxes at a tax rate of 21 percent?A) $589.46B) $1,135.05C) $1,331.54D) $1,560.85E) $949.4659) Galaxy Interiors income statement shows depreciation of $1,611, sales of $21,415, interest paid of $1,282, net income of $1,374, and costs of goods sold of $16,408. What is the amount of the noncash expenses?A) $2,893B) $1,282C) $740D) $1,611E) $2,35160) Beach Front Industries has sales of $546,000, costs of $295,000, depreciation expense of $37,000, interest expense of $15,000, and a tax rate of 21 percent. The firm paid $59,000 in cash dividends. What is the addition to retained earnings?A) $98,210B) $81,700C) $95,200D) $103,460E) $121,68061) Keisler's has cost of goods sold of $11,518, interest expense of $315, dividends of $420, depreciation of $811, and a change in retained earnings of $296. What is the taxable income given a tax rate of 21 percent?A) $955.38B) $967.78C) $906.33D) $776.41E) $646.1562) What is the average tax rate for a firm with taxable income of $118,740 in 2017?Taxable Income Tax Rate$ 0 - 50,000 15 %50,001 - 75,000 2575,001 - 100,000 34100,001 - 335,000 39A) 26.68 percentB) 34.87 percentC) 24.89 percentD) 36.67 percentE) 39.00 percent63) For 2017, Nevada Mining had projected taxable income of $94,800. Its actual taxable income exceeded this projection by $21,000. How much additional tax did the firm owe due to the $21,000 increase in taxable income?Taxable Income Tax Rate$ 0 - 50,000 15 %50,001 - 75,000 2575,001 - 100,000 34100,001 - 335,000 39A) $7,930B) $8,036C) $8,150D) $7,682E) $8,19764) In 2017, Boyer Enterprises had $76,700 in taxable income. What was the firm's average tax rate for the year?Taxable Income Tax Rate$ 0 - 50,000 15 %50,001 - 75,000 2575,001 - 100,000 34100,001 - 335,000 39A) 28.25 percentB) 18.68 percentC) 26.48 percentD) 20.14 percentE) 29.03 percent65) Winston Industries had sales of $843,800 and costs of $609,900. The company paid $38,200 in interest and $35,000 in dividends. The depreciation was $76,400. The firm has a combined tax rate of 24 percent. What was the addition to retained earnings for the year?A) $55,668B) $57,240C) $61,060D) $56,200E) $68,40066) RTF Oil has total sales of $911,400 and costs of $787,300. Depreciation is $52,600 and the tax rate is 21 percent. The firm is all-equity financed. What is the operating cash flow?A) $108,410B) $108,320C) $109,924D) $106,417E) $109,08567) Nielsen Auto Parts had beginning net fixed assets of $218,470 and ending net fixed assets of $209,411. During the year, assets with a book value of $6,943 were sold. Depreciation for the year was $42,822. What is the amount of net capital spending?A) $33,763B) $40,706C) $58,218D) $65,161E) $67,40868) At the beginning of the year, a firm had current assets of $121,306 and current liabilities of $124,509. At the end of the year, the current assets were $122,418 and the current liabilities were $103,718. What is the change in net working capital?A) −$19,679B) −$11,503C) $19,387D) $15,497E) $21,90369) At the beginning of the year, the long-term debt of a firm was $72,918 and total debt was $138,407. At the end of the year, long-term debt was $68,219 and total debt was $145,838. The interest paid was $6,430. What is the amount of the cash flow to creditors?A) $1,731B) −$1,001C) $11,129D) $13,861E) $19,17270) Ernie's Home Repair had beginning long-term debt of $51,207 and ending long-term debt of $36,714. The beginning and ending total debt balances were $59,513 and $42,612, respectively. The interest paid was $2,808. What is the amount of the cash flow to creditors?A) −$11,685B) −$11,272C) $17,301D) $17,418E) $11,17471) The Daily News has projected annual net income of $272,600, of which 28 percent will be distributed as dividends. Assume the company will have net sales of $75,000 worth of common stock. What will be the cash flow to stockholders if the tax rate is 21 percent?A) −$75,000B) $1,328C) $24,623.52D) $76,328E) $151,32872) The Lakeside Inn had operating cash flow of $48,450. Depreciation was $6,700 and interest paid was $2,480. A net total of $2,620 was paid on long-term debt. The firm spent $24,000 on fixed assets and decreased net working capital by $1,330. What was the amount of the cash flow to stockholders?A) $5,100B) $7,830C) $18,020D) $19,998E) $20,68073) For the past year, Galaxy Interiors had depreciation of $2,419, beginning total assets of $23,616, and ending total assets of $21,878. Current assets decreased by $1,356. What was the amount of net capital spending for the year?A) −$382B) $2,037C) $2,801D) $1,993E) $1,17274) Carlisle Express paid $1,282 in interest and $975 in dividends last year. Current assets increased by $2,700, current liabilities decreased by $420, and long-term debt increased by $2,200. What was the cash flow to creditors?A) −$530B) −$918C) $1,839D) 2,132E) $3,09475) CBC Industries has sales of $21,415, interest paid of $1,282, costs of $9,740, and depreciation of $1,480. What is the operating cash flow if the tax rate is 22 percent?A) $10,114.14B) $9,900.86C) $8,985.86D) $8,536.67E) $9,714.1476) Williamsburg Markets has an operating cash flow of $4,267 and depreciation of $1,611. Current assets decreased by $1,356 while current liabilities decreased by $2,662, and net fixed assets decreased by $382 during the year. What is free cash flow for the year?A) $1,732B) $2,247C) $2,961D) $3,915E) $4,26777) Up Towne Cleaners has taxable income of $48,900 and a tax rate of 21 percent. What is the change in retained earnings if the firm pays $20,200 in dividends for the year?A) $18,942B) $19,948C) $19,374D) $18,431E) $18,57478) For the year, B&K United increased current liabilities by $1,400, decreased cash by $1,200, increased net fixed assets by $340, increased accounts receivable by $200, and decreased inventory by $150. What is the annual change in net working capital?A) −$2,550B) −$70C) $590D) $550E) −$2,21079) TJH, Inc. purchased $145,000 in new equipment and sold equipment with a net book value of $68,400 during the year. What is the amount of net capital spending if the depreciation was $38,600?A) $115,200B) $76,600C) $94,200D) $38,000E) −$38,00080) Nu Furniture has sales of $241,000, depreciation of $32,200, interest expense of $35,700, costs of $103,400, and taxes of $14,637. What is the operating cash flow for the year?A) $108,229B) $121,367C) $122,963D) $117,766E) $128,03781) HiWay Furniture has sales of $316,000, depreciation of $47,200, interest expense of $41,400, costs of $148,200, and taxes of $16,632. The firm has net capital spending of $36,400 and a decrease in net working capital of $14,300. What is the cash flow from assets for the year?A) $145,985B) $129,068C) $119,655D) $120,810E) $134,58582) At the beginning of the year, Trees Galore had current liabilities of $15,932 and total debt of $68,847. By year end, current liabilities were $13,870 and total debt was $72,415. What is the amount of net new borrowing for the year?A) $5,630B) −$2,480C) $3,568D) $4,677E) −$2,06283) JJ Enterprises has current assets of $10,406, long-term debt of $4,780, and current liabilities of $9,822 at the beginning of the year. At year end, current assets are $11,318, long-term debt is $5,010, and current liabilities are $9,741. The firm paid $277 in interest and $320 in dividends during the year. What is the cash flow to creditors for the year?A) −$47B) −$507C) −$97D) $47E) $50784) BK Enterprises neither sold nor repurchased any shares of stock during the year. The firm had annual sales of $7,202, depreciation of $1,196, cost of goods sold of $4,509, interest expense of $318, taxes of $248, beginning-of-year shareholders' equity of $4,808, and end-of-year shareholders' equity of $4,922. What is the amount of dividends paid during the year?A) $817B) $1,009C) $864D) $709E) $51585) Carlisle Carpets has cost of goods sold of $92,511, interest expense of $4,608, dividends paid of $3,200, depreciation of $14,568, an increase in retained earnings of $11,920, and a tax rate of 21 percent. What is the operating cash flow?A) $34,296.00B) $42,122.42C) $36,462.58D) $31,543.10E) $36,741.42。

02朗文国际英语教程 第1册备课课件_Chapter 2

We are from Canada.

They are good students.

You are my friends.

主格的用法1

1.主格在句子中作主语

(主语表示句子主要说明的人或事物。)

I love my motherland.

He is a French teacher.

主格的用法2

2.主格在句子中作表语

He is interested in the film.

练习题:用interesting和interested填空。

1、This story is very_i_n_te__re_s_t_in__g. 2、I'm _i_n_t_e_re_s__te_d_ in your story. 3、She isi_n_te_r_e_s_t_e_d_ in the i_n_te__re_s_t_i_n_g news. 4、Tom is _in_t_e_r_e_s_te__d in playing basketball. 5、David is i_n_te__re_s_t_e_d_in the _in_t_e_re__s_ti_n_gbook。

English.(we)

3. This book is useful , I want to buy it

______.(it)

you

4. This gift is for ______. (you)

me

5. My parents love ______.(I)

宾格的用法

宾格在句子中作宾语 (宾语表示动作行为的对象)

Oral Practice

above, over, on 在……上 above 指在……上方,不强调是否垂直,与 below相对; over指垂直的上方,与under相对,但over与物体有一定的 空间,不直接接触。 on表示某物体上面并与之接触。与 beneath [bɪˈni:θ]相 对; The bird is flying above my head. There is a bridge over the river. He puts his watch on the desk.

计算机科学概论 答案 chapter02

Chapter TwoDATA MANIPULATIONChapter SummaryThis chapter introduces the role of a computer's CPU. It describes the machine cycle and the various operations (or, and, exclusive or, add, shift, etc.) performed by a typical arithmetic/logic unit. The concept of a machine language is presented in terms of the simple yet representative machine described in Appendix C of the text. The chapter also introduces some alternatives to the von Neumann architecture such as multiprocessor machines and artificial neural networks.The optional sections in this chapter present a more thorough discussion of the instructions found in a typical machine language (logical and numerical operations, shifts, jumps, and I/O communication), a short explanation of how a computer communicates with peripheral devices, and alternative machine designs.The machine language in Appendix C involves only direct and immediate addressing. However, indirect addressing is introduced in the last section (Pointers in Machine Language) of Chapter 7 after the pointer concept has been presented in the context of data structures.Comments1. Much of Comment 1 regarding the previous chapter is pertinent here also. The development of skills in the subjects of machine architecture and machine language programming is not required later in the book. Instead, what one needs is an image of the CPU/main memory interface, an understanding of the machine cycle and machine languages, an appreciation of the difference in speeds of mechanical motion compared to CPU activities, and an exposure to the limited repertoire of bit manipulations a CPU can perform.2. To most students at this stage the terms millisecond, microsecond, nanosecond, and picosecond merely refer to extremely short and indistinguishable units of time. In fact, most would probably accept the incorrect statement that activities within a computer are essentially instantaneous. Once a student of mine wrote a recursive routine for evaluating the determinant of a matrix in an interpreted language on a time-sharing system. The student tried to test the program using an 8 by 8 matrix, but kept terminating the program after a minute because "it must be in a loop." This student left with an understanding of microseconds as real units of time that can accumulate into significant periods.3. A subtle point that can add significantly to the complexity of this material is combining notation conversion with instruction encoding. If, for example, all the material in Chapters 1 and 2 is new toa student, the problem, "Using the language of Appendix C, write an instruction for loading register14 with the value 124" can be much more difficult than the same problem stated as, "Using the language of Appendix C, write an instruction for loading register D with the (hexadecimal) value 7C." In general, notation conversion is a subject of minor importance and should not be allowed to cloud the more important concerns.4. If you want your students to develop more than a simple appreciation of machine language programming, you may want to use one of the many simulators that have been developed for the machine in Appendix C. A nice example is included on the Addison-Wesley website at /brookshear or you can find other simulators by searching the Web.5. Here are some short program routines in the machine language presented in Appendix C of the text, followed by their C language equivalents. (These examples are easily converted into Java, C++, and C#.) Each machine language routine starts at address 10. I've found that they make good examples for class presentations or extra homework problems in which I give the students the machine language form and ask them to rewrite it in a high-level language.Address Contents Address Contents Address Contents0D 00 14 20 1B 0F0E 00 15 5A 1C 500F 00 16 30 1D 1210 20 17 0F 1E 3011 5C 18 11 1F 0D12 30 19 0E 20 C013 0E 1A 12 21 00C language equivalent:{int X,Y,Z;X = 92;Y = 90;Z = X + Y;}If the contents of the memory cell at address 1C in the preceding table is changed from 50 to 60 the C equivalent becomes:{float X, Y, Z;X = 1.5;Y = 1.25;Z = X + Y;}Here's another example:Address Contents Address Contents Address Contents0E 00 19 0F 24 200F 00 1A 20 25 0110 20 1B 04 26 5011 02 1C B1 27 0112 30 1D 2C 28 3013 0E 1E 12 29 0F14 20 1F 0E 2A B015 01 20 50 2B 1816 30 21 12 2C C017 0F 22 30 2D 0018 11 23 0EC equivalent:{int X, Y;X = 2; Y =1;while (Y != 4) {X = X + Y; Y = Y + 1;}}6. Here are two C program segments that can be conveniently translated into the machine language of Appendix C.{int X, Limit;X = 0;Limit = 5;do X = X + 1 while (X != Limit);}Program segment in machine language:Address Contents Address Contents Address Contents0E 00 (X) 18 22 (R2 = 1) 22 10 (R0 = Limit)0F 00 (Limit) 19 01 23 0F10 20 (X = 0) 1A 11 (R1 = X) 24 B1 (go to end11 00 1B 0E 25 28 if X == Limit)12 30 1C 50 (X = X+1) 26 B0 (return)13 0E 1D 12 27 1A14 20(Limit = 5)1E 30 28 C0 (halt)15 05 1F 0E 29 0016 30 20 11 (R1 = X)17 0F 21 0E{int X, Y, Difference;X = 33;Y = 34;if (X > Y)Difference = X - Yelse Difference := Y – X}Program segment in machine language:Address Contents Address Contents Address Contents0D 00 (X) 1D 01 2D 16 (Diff = X-Y)0E 00 (Y) 1E 24 (R4=FF) 2E 300F 00 (Diff) 1F FF 2F 0F10 20 (X = 33) 20 96 (R6=not Y) 30 B0 (branch to11 21 21 24 31 3A halt)12 30 22 56 (R6= -Y) 32 90 (R0=not X)13 0D 23 36 33 1414 20 (Y = 34) 24 50 (R0=X-Y) 34 50 (R0 = -X)15 22 25 16 35 0316 30 26 25 (R5=80Hex) 36 50 (R0 = Y-X)17 0E 27 80 37 0218 11 (R1=X) 28 80 (mask low) 38 30 (Diff = Y-X)19 0D 29 50 7 bits) 39 0F1A 12 (R2=Y) 2A B5 (if R0=R5 3A C0 (halt)1B 0E 2B 32 then Y>X 3B 001C 23 (R3=1) 2C 50Answers to Chapter Review Problems1. a. General purpose registers and main memory cells are small data storage cells in a computer.b. General purpose registers are inside the CPU; main memory cells are outside the CPU.(The purpose of this question is to emphasize the distinction between registers and memory cells—a distinction that seems to elude some students, causing confusion when following machine language programs.)2. a. 0010000100000101b. 1010c. 0011001001003. Nine cells with addresses B9, BA, BB, BC, BD, BE, BF, C0, and C1.4. BA5. Program Instruction Memory cellcounter register at 0002 2104 2104 3100 2106 C000 046. To compute x + y - z, each of the values must be retrieved from memory and placed in a register, the sum of x and y must be computed and saved in another register, z must be subtracted from that sum, and the final answer must be stored in memory.A similar process is required to compute (2x) + y. The point of this example is that the multiplication by 2 is accomplished by adding x to x.7. a. Move the contents of register 7 to register E.b. AND the contents of register 0 with the contents of register 8 and place the result in register 0.c. Rotate the contents of register 4 three bits to the right.d. Load register 8 with the value (hexadecimal) 35.e. Compare the contents of registers 3 and 0. If the patterns are equal, jump to the instruction at address AD. Otherwise, continue with the next sequential instruction.8. 16 with 4 bits, 256 with 8 bits9. a. 2766 b. 1766 c. 80F2 d. A403 e. BB3110. The only change that is needed is that the third instruction should be 6056 rather than 5056.11. a. Retrieves from memory cell 3B.b. Is independent of memory cell 3B.c. Changes the contents of memory cell 3B.d. Changes the contents of memory cell 3B.e. Is independent of memory cell 3B.12. a. Place the value 05 in register 4. b. 0513. a. 241B b. 1B3414. a. Load register 0 with the contents of memory cell 04.Store the contents of register 3 in memory cell 45.Halt.b. C0c. 0615. a. 29 b. 0A16. a. 00, 01, 02, 03, 04, 05b. 06, 0717. a. 03 b. 03 c. 0E18. 05. The program is a loop that is terminated when the value in register 0 (initiated at 00) is finally incremented to the value in register 3 (initiated at 05).19. 20 microseconds.20. The point to this problem is that a bit pattern stored in memory is subject to interpretation—it may represent part of the operand of one instruction and the op-code field of another.a. Registers 0, 1, and 2 will contain 32, 20, and 12, respectively.b. 12c. 3221. The machine will alternate between executing the jump instruction at address AF and the jump instruction at address B0.22. It would never halt. The first 2 instructions alter the third instruction to read B000 before it is ever executed. Thus, by the time the machine reaches this instruction, it has been changed to read "Jump to address 00." Consequently, the machine will be trapped in a loop forever (or until it is turned off).23. a. b. c.148D 148D 200034B3 15B3 1145C000 358D B10A34BD22DDB00CC00022CC3288C00024. a. The single instruction B000 stored in locations 00 and 01.b. Address Contents00,01 2100 Initialize02,03 2270 counters.04,05 3109 Set origin06,07 320B and destination.08,09 1000 Now move0A,0B 3000 one cell.0C,0D 2001 Increment0E,0F 5101 addresses.10,11 520212,13 2333 Do it again14,15 4010 if all cells16,17 B31A have not18,19 B004 been moved.1A,1B 2070 Adjust values1C,1D 3071 that are1E,1F 2079 location20,21 3075 dependent.22,23 207B24,25 307726,27 208A28,29 30872A,2B 20742C,2D 30892E,2F 20C030,31 30A432,33 200034,35 20A536,37 B070 Make the big jump!c. Address Contents00,01 2000 Initialize counter.02,03 2100 Initialize origin.04,05 2270 Initialize destination.06,07 2430 Initialize references08,09 1530 to table.0A,0B 310D Get origin0C,0D 1600 value.0E,0F B522 Jump if value must be adjusted.10,11 3213 Place value12,13 3600 in new location.14,15 2301 Increment16,17 5003 R0,18,19 5113 R1, and1A,1B 5223 R2.1C,1D 233C Are we done?1E,1F B370 If so, jump to relocated program.20,21 B00A Else, go back.22,23 2370 Add 70 to24,25 5663 value being26,27 2301 transferred and28,29 5443 update R4 and2A,2B 342D R5 for next2C,2D 1500 location.2E,2F B010 Return (from subroutine).30,31 0305 Table of32,33 0709 locations that34,35 0B0F must be36,37 111F updated for38,39 212B new location.3A,3B 2FFF25.20A1 21A421A2 60016001 30A521A3 C000600126. The machine would place a halt instruction (C000) at memory location 04 and 05 and then halt when this instruction is executed. At this point its program counter will contain the value 06.27. The machine would continue to repeat the instruction at address 06 indefinitely.28. It copies the data from the memory cells at addresses 00, 01, and 02 into the memory cells ataddresses 10, 11, and 12.29. Let R represent the first hexadecimal digit in the operand field;Let XY represent the second and third digits in the operand field;If the pattern in register R is the same as that in register 0,then change the value of the program counter to XY.30. Let the hexadecimal digits in the operand field be represented by R, S, and T;Activate the two's complement addition circuitry with registers S and Tas inputs;Store the result in register R.31. Same as Problem 24 except that the floating-point circuitry is activated.32. a. 04 b. A8 c. FC d. 08 e. F433. a. b. c. d.1066 1034 10A5 10A530BB 21F0 210F 210F8001 8001 80013034 12A6 400121F0A1047001821230A5700230A634. a. 101000 b. 000000 c. 000100 d. 110001 e. 111001 f. 101110g. 010101 h. 111111 i. 010001 j. 101110 k. 010001 l. 00111035. a. AND the byte with 11000011.b. XOR the byte with 11111111.c. XOR the byte with 10000000.d. OR the byte with 10000000.e. OR the byte with 01111111.36. XOR the input string with 10000001.37. First AND the input byte with 10000001, then XOR the result with 10000001.38. a. 11010 b. 00001111 c. 010 d. 001010 e. 1000039. a. 9F b. 86 c. FF d. BB40. a. AB03 b. AB0541. Address Contents00,01 2008 Initialize registers.02,032101220004,05230006,0708,09 148C Get the bit pattern;0A,0B 8541 Extract the least significant bit;0C,0D 7335 Insert it into the result.62120E,0F10,11 B218 Are we done?12,13 A401 If not, rotate registersA30714,1516,17 B00A and go back;18,19 338C If yes, store the result1A,1B C000 and halt.42. The idea is to complement the value at address A1 and then add. Here is one solution:21FF12A1722113A0542334A243. Each character would consist of 8 bits so the rate of 300 bps would translate into approximately37 characters per second. Thus, the printer could just keep up. (In reality, an ASCII characterrequires about 10 bits when transmitted serially because, in addition to a parity bit, start and stopbits are also added to each pattern. As a rule of thumb, 300 bps is considered to be 30 characters persecond.) If the rate were increased to 1200 bps, the printer wouldn't stand a chance.44. The typist would be typing 30 x 5 = 150 characters per minute, or 1 character every 0.4 seconds(= 400,000 microseconds). During this period the machine could execute 20,000,000 instructions.45. The typist would be producing characters at the rate of 2.5 characters per second, whichtranslates to 20 bps (assuming each character consists of 8 bits).46. Address Contents200000,01210102,0304,05 12FE Get printer status06,07 8212 and check the ready flag.08,09 B004 Wait if not ready.0A,0B 35FF Send the data.47. Address Contents00,01 20C1 Initialize registers.210002,03220104,05130B06,0708,09 B312 If done, go to halt.0A,0B 31A0 Store 00 at destination.0C,0D 5332 Change destination0E,0F 330B address,10,11 B008 and go back.12,13 C00048. 14,400 bps is equivalent to 1,800 bytes/sec. So it would take 2960 hours (over 123 days) to fill the20MB drive.49. 14450. Group the 64 values into 32 pairs. Compute the sum of each pair in parallel. Group these sumsinto 16 pairs and compute the sums of these pairs in parallel. etc.51. CISC involves numerous elaborate machine instructions that can be time consuming. RISCinvolves fewer and simpler instructions, each of which is efficiently implemented.52. How about pipelining and parallel processing? Increasing clock speed is another answer.53. In a multiprocessor machine several partial sums can be computed simultaneously.。

Chapter-02

Process State 进程状态

• As a process executes, it changes state 进程执行时,改变状态 – new: The process is being created. 新建:在创建进程 – running: Instructions are being executed. 运行:指令在执行 – waiting: The process is waiting for some event to occur. 等待:进程等待某些事件发生 – ready: The process is waiting to be assigned to a processor. 就绪:进程等待分配处理器 – terminated: The process has finished execution. 终止:进程执行完毕

16

CPU Switch From Process to Process 进程间CPU的切换

17

Context Switch

• When CPU switches to another process, the system must save the state of the old process and load the saved state for the new process. • Context represented in PCB of a process,include -CPU registers -process state -memory-management information • Context-switch time is overhead; the system does no useful work while switching. • Time dependent on hardware support.

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

2018/10/16 C Programming

5/96

C程序常见符号分类

运算符(Operator) 34种,详见附录2

分隔符(Separator) 空格、回车/换行、逗号等

其它符号 “{”和“}”标识函数体或语句

块

“/*”和“*/”程序注释的定界

符

2018/10/16 C Programming

结果会是什么?

2018/10/16 C Programming

12/96

变量赋值(Variable Assignment)

Example: int number1, number2;

number1 = 25; number2 = 23; number1 = number2;

number1 number2

4/96

C程序常见符号分类

关键字(Keyword) 又称保留字( C Reserved Word ),C

语言中预先规定的具有固定含义的一 些单词 (if, while, …)

标识符(Identifier) C Standard Identifier(系统预定义标

识符)

用户自定义标识符

变量,函数名,…

程序注释

并列的两个函数 其中一个是 程序的入口

printf("Input two integers:"); scanf("%d%d", &x, &y); /*输入两个整型数x和y*/ sum = Add(x, y); /*调用函数Add计算x和y相加之和*/ printf("sum = %d\n", sum); /*输出x和y相加之和*/ } 2018/10/16 C Programming

常量(Constant)

6/96

标识符命名

变量名,函数名 由英文字母、数字和下划线组成,大小写敏感 不可以是数字开头 直观,见名知意,便于记忆和阅读 最好使用英文单词或其组合 UNIX 切忌使用汉语拼音 风格 下划线和大小写通常用来增强可读性 variablename Windows variable_name 风格 variableName 不允许使用关键字作为标识符的名字 int, float, for, while, if等 某些功能的变量采用习惯命名 P45, 2.1 如:for语句所采用的循环变量习惯用i, j, k

Invalid Example: int y; y = 5.75;

14/96

变量赋值(Variable Assignment)

Example:

•Input: •Output: •Process: quantity and pricePerkg price price = quantity * pricePerkg

2018/10/16 C Programming

3/96

例2.1:一个简单的C程序例子

编译预处理命令

#include <stdio.h> /*函数功能:计算两个整数相加之和 入口参数:整型数据a和b 返回值: 整型数a和b之和 */ int Add(int a, int b) { return (a + b); } /*主函数*/ main() { int x, y, sum = 0;

C语言程序设计

第2章 数据类型、 运算符与表达式

本章学习内容

标识符命名; 变量和常量; 数据类型; 常用运算符和表达式; 运算符的优先级与结合性

2018/10/16 C Programming

2/96

C Program Structure

Preprocessor Instruction Global Declaration main () { Local Declaration Statement }

7/96

2018/10/16 C Programming

何谓变量(Variable )?

2018/10/16 C Programming

8/96

如何衡量变量所占空间大小?

bit,中文叫法:位 Byte,中文叫法:字节 Kilobyte(KB),中文叫法: K Megabyte(MB),中文叫法:兆 Gigabyte(GB),中文叫法:G Terabyte(TB),中文叫法:T

ห้องสมุดไป่ตู้

1 TB == 1024 GB 1 GB == 1024 MB 1 MB == 1024 KB 1 KB == 1024 B 1 B == 8 b

2018/10/16 C Programming 9/96

如何衡量变量所占空间大小?

一个位有多大? 只能是“0”或者“1”,

二进制

一个字节有多大? 可以表示数字0~255之间的

23 25 ? 23 ?

… …

2018/10/16 C Programming 13/96

变量赋值(Variable Assignment)

Algorithm 变量 表达式 Syntax 变量 = 表达式 ;

Rules:类型一致 Valid Example: int x; x = 12;

2018/10/16 C Programming

2018/10/16 C Programming

15/96

变量赋值(Variable Assignment)

Example:

How does this program work?

int quantity; float pricePerkg, price;

2018/10/16 C Programming

11/96

变量声明(Variable Declaration)

使用变量的基本原则 变量必须先定义,后使用 所有变量必须在第一条可执行语句前

定义

声明的顺序无关紧要 一条声明语句可声明若干个同类型 的变量 声明变量是初始化变量的最好时机 不被初始化的变量,其值为随机数

整数 保存一个字符(英文字母 、数字、符号)

ASCII(美国标准信息交换 码)编码

10/96

2018/10/16 C Programming

变量声明(Variable Declaration)

Needs

to be declared:

变量类型 变量名;

Example: int sum; int x,y,sum=0;