BV2010_IAS17_PART A

Installation of SAP-BI7

Installation of SAP – BI 7Rate This/install/sap-bi-7-installation-another-inter esting-experience/1-installation-of-sap-bi-7-part-1/***************** Other Pages on the same topic…. **************************1. Installation of SAP – BI 7 (Part 1)2. Installation of SAP – BI 7 (Part 2) – the CI3. Installation of SAP – BI 7 (Part 3) – the DB4. Post Installation Tasks – BI 7 (Part 4)5. BI 7 post to post install – Journey of Basis to BI admin (Part 5)******************************************************************************1. Installation of SAP – BI 7 (Part 1)This is another Sap installation experience. This is regarding SAP BI 7. In this article I will try to narrate and elaborate as much as my time, enthusiasm and knowledge permit with a fair amount of screenshots. Fellow SAP Basis consultants hope will admire such a ready available digest kinda material. I have installed the BI 7 on Linux platform, and the Linux distro is SLES 10 SP2.Here is my experience on installation of ECC6. This is better to admit that, SAP and its installation over SLES 10 SP2. I am writing this experience here, as how I did it…Although I don’t want any technical / functional debates and won’t mind to receive any suggestion from any reader. My approach of doing the same was like chalk down the requirements, gathering the requirements, doing installation, backing up installation, testing and final release.In my earlier article on ECC 6 installation I already wrote and discussed how to do the same on server hardware with an external storage box (e.g. IBM DS4700), hence no point of recapitulating the same. You can find the same here(Installation of ECC6. –An Experience itself) for easy reference, if at all you require.So here I will start with the SAP media required for BI 7 installation. Although the list will have lot of things in common as in my other article for Installation of ECC6. – AnExperience itself but it is required here to make this page a complete. Please go thruBelow is the screenshot, how I dumped all this media in a an installation store.2. Installation of SAP – BI 7 (Part 2) – the CIAfter the requirement is finalized and required things are collected, we will start installation process. The process is almost same as in case of ECC 6 installation as I wrote earlier. The only difference is we will be taking also the Java AS alongwith the ABAP AS. So there are some additional steps. Before we start the installation, we need to create the directories. Directory creation is same as ECC installation and can refer the same. Don’t also forget to check the required library and packages are already installed or not. Oh yes, even if you don’t do so the SAP installer is smart enough to provide you requirement in a nicely formatted error message. The installation starts from installation master as dumped into the D5******* directory and as usual to run “sapinst”. Oh I forgot to mention we need to logon as root user for this installation. After the first screen appears select “SAP NetWeaver 2004s Support release 2″ and expand, then expand SAP systems then expand Oracle and then CentralSystem and fina lly select Central system Installation…Refer the following two screen shot for the same.Now press next button. Once again let me remind, we are installing BI 7 with Oracle database on SuSE Linux System. This will take you to the parameter mode screen and select default here and press Next once more, which will take you to the selection of software units. Refer next two screen shot for the same.Once the software units are selected, the media browser will appear and ask to point out the media source. As we have already copied those media to the machine where installation is going on, we will be pointing out the directories. The first media asked is the “NW Java Component”. This is available in the directory D5*******. select and press next. Refer to the following screenshot for the same.Once Java Component is not selected, we need to show the path of the JDKalso. The main important thing here is to note that the versions…Over affinity to the updated version can be a danger, time wasting etc….In fact it happened with me too. I went back and removed and reinstalled the scenario.One thing is very important here. Once you are downloading java, either from IBM or from SUN, the corresponding “JCEUnlimited Strength Jurisdiction policy archive”. The files are available from the corresponding vendor’s site. The links are also available in the next screen where the installer will ask you for the certificate. One can also click and directly go the side or copy and paste in a browser. Refer to next screen shot for the same.Once it is sorted out and proper location is provided, we need to provide some general information e.g. SAP SID, and SAP system mount directory .i.e/sapmnt. Then it will ask the Database SID and Database host name. Please refer next two screenshot for the same.SAP Inst Database ParametersIn the next screen, the database administrator passwords will be asked along with the OS userid, groupid, which normally kept blank, unless you created the Oracle userid, DBA group and database oper group yourself. Otherwise keep it as it is, the installer it self will create the necessary userid, set group idetc.etc…As soon as this is provided, once again SAp will start asking you the location of medias…Especially, Inst allation export, Java Componenet NW 2004s, Oracle RDBMS . Besides it will ask you also the kernel and the Oracle Client media. Check next 5 screenshots for reference.SAP Inst Database PasswordSAP Inst Software Package Check and Request 1SAP Inst Software Package Check and Request 2SAP Inst Software Package Check and Request 3SAP Inst Software Package Check and Request 4After everything in the above steps goes correctly, we will come to the parameter summary screen where the installer shows all the major options you choosed, and then you require to enter the solution manager key for the system. You need it, better to create a solution manager key before hand which needs a the hardware key and the SAP SID to generate. If you do not have the same, you can get it from other who do hhave a solution manager, provide the hardware key and the SID and ask for a solution manager key. As soon as you provide the same and press continue, the installer will start installing the components…In total there are forty five steps, and out of that after the completion of 9th step it will ask you to install the database. The database part of the installtion is written separately, only after completion of the same press the OK button to install the remaining part ..That is mainly installtion of the exports, that is the data structure where SAP keeps it data and programs (transactions).SAP Inst System Landscape DirectorySAP Inst Parameter SummarySAP Inst Solution ManagerSAP Inst Task Progress3. Installation of SAP – BI 7 (Part 3) – the DBStarting from where it was left.. The SAP installer was prompting you to install Oracle database after completion of stage 9. Do not exit from here. Open a separate Xterm and set the terminal so that you can run X application. Whether the terminal was set right or not can be chaecked by running xclock. If the clock applet appears on the terminal then you are done.Second step is a modification in oraparam.ini file. This file does not have SuSE-10 in the entry of the certified version and hence if you directly start the installation of the Oracle it will fail. Hence one require to modify the the certified version in this oraparam.ini file in /oracle/stage/102_64/database/install/ directory as below. From[Certified Versions]Linux=redhat-3,SuSE-9,redhat-4,UnitedLinux-1.0,asianux-1,asianux-2To [Certified Versions]Linux=redhat-3,SuSE-9,SuSE-10,redhat-4,UnitedLinux-1.0,asianux-1,asianux -2After this is done, we do need to start the installer by executing RUNINSTALL from the directory. on execution, this will take a while almost a minute for searching and loading different Java program and finally the OUI GUI window will appear. Look the following two screen shots below for the same.By default it will select the inventory location as well as the group which has access rights on /oracle directory. Keep it as it is and click next. This will take you to the inventory summary screen where you will see oracle installer is loading the inventory files. Finally it will list all the products, and here press install button. Refer to the following screen shot for the same.On pressing installation will start, this involves copying files, compiling libraries, linking and the whole setup may take half an hour. Finally it will come to configuration script running section where it will ask you to run two script as root. Open a separate Xterm session, login as root and then execute those two script. Choose default options on answer to the questions. Refer following two screen shots for the same.Finally you need to click on the OK screen which will end installation with the final installer screen showing you some urls which may note but as per as SAP is considered those information are really useless. Refer to the screen shot below for the same.This will finally end the database installation part. Go back to the SAP installer screen where the installer is standing still giving you the message to install the Database. Refer to last screen shot shown in the page Installation of SAP – BI 7 (Part 2) – the CI4. Post Installation Tasks – BI 7 (Part 4)As the post installation things are concerned, this is normal like the others NW installations. This includes the following routine points…1. Check whether the installation is correct… Use transaction SICK.2. Upgrade of kernel including dbtools.3. Create transport landscape.4. Upgrade of SPAM/SAINT5. Application of support packages..6. Run transaction SGEN.7. Finally create a new client for development and copy cline 000 contentto that. Transaction SCCLBesides the above routine steps you need to do a little more. that is first you need to make the development client useful i.e. you need to designate your development client as Unique BW client.How to check that? Login in the client you have created for development, let say it is 101 and execute the transaction code RSA1. Immediately you will be provided with a reply that you can logon only in client 000.So this is the first step need to pay attention i.e. we need to define Unique client in BW. How to do that? Use transaction code SE16, open the table RSADMINA and then finally you need to change the field value of the field BWMANDT. This should be the intended client no instead of 000. Save and exit from transaction SE16. Finally execute transaction RSA1 and it will show Data Warehousing Workbench. Here we need to connect the source R/3 system. Check the following screenshot for the reference.At this stage you can simply handover the system to your BW colleague and ask him to use. But I personally feel that still there are some thing pending fromthe Basis to do.5. BI 7 post to post install – Journey of Basis to BI admin After a long time I am back once again to share my notebook pages. I remember once almost 3 yrs back I faced an Oracle DBA interview, who asked about the index organisation in a star schema – fact table.Frankly that was the first moment when I realised that even if I gathered a long experience on Oracle database but I have no or very little idea about the data warehousing and business intelligence. In fact I didn’t get a chance t o work or understand this as there was no such setup available. It was one day in April 2009, in a lecture session I learned that there are something called technical content in BI, which helps you keep track the on the behaviour and performance of the BI cubes defined and being used. The man presenting the session also told that once the BI technical content is configured and activated faultlessly, performance of the cubes and other BI business objects can be seen right from the transaction ST03n. As I am always interested about tuning of large database , this triggered my wish to learn tuning of a data warehouse in some form or other.So you understood that this page will tell you in detail the how to activate and use the BI technical content.Although the same is available from different other Internet document source but here I recorded in detail the difficulties I faced in this job along with the screen shots and the different valuable resources.Generate BW Technical Content in SPROSo What I did actually? for activation of the BI technical content you need to go thru the following path in the SPRO. Refer to the image above for the same.SPRO->Display IMG->SAP NetWeaver->Business Intelligence->Settings for BI Content->Business Intelligence->BI Administration Cockpit->Activate Technical Content in SAP NetWeaver BI.And as soon as I did the same , to my dismay and a mouthfull of bitterness, I landed up in the log screen with a huge nos of red bullets ..i.e. error messages. So what was the path? What I saw? Refer to the screen below.Although the proverv goes failures are the pillars of success the real fact of life is nobody wants to fail…in the mission……..I have yet to update/insert all the screenshot in this page.。

国际会计准则IAS_10英文版

IAS 10 International Accounting Standard 10Events after the Reporting PeriodThis version includes amendments resulting from IFRSs issued up to 17 January 2008.IAS 10 Events After the Ba la nce Sheet Da te was issued by the International Accounting Standards Committee in May 1999. It replaced those parts of IAS 10 Contingencies and Events Occurring After the Balance Sheet Date (originally issued June 1978, reformatted 1994) that were not replaced by IAS 37 (issued September 1998).In April 2001 the International Accounting Standards Board (IASB) resolved that all Standards and Interpretations issued under previous Constitutions continued to be applicable unless and until they were amended or withdrawn.In December 2003 the IASB issued a revised IAS 10 with a modified title—Events after the Balance Sheet Date.IAS 10 was amended by the following IFRSs:•IFRS5Non-Current Assets Held for Sale and Discontinued Operations (issued March 2004).•IAS1Presentation of Financial Statements (revised September 2007)As a result of the changes in terminology made by IAS 1 in 2007, the title of IAS 10 was changed to Events after the Reporting Period.The following Interpretation refers to IAS 10:•SIC-7 Introduction of the Euro (issued May 1998 and subsequently amended).© IASCF1035IAS 101036© IASCF C ONTENTSparagraphs INTRODUCTIONIN1–IN4INTERNATIONAL ACCOUNTING STANDARD 10EVENTS AFTER THE REPORTING PERIODOBJECTIVE1SCOPE2DEFINITIONS3–7RECOGNITION AND MEASUREMENT8–13Adjusting events after the reporting period8–9Non-adjusting events after the reporting period10–11Dividends12–13GOING CONCERN14–16DISCLOSURE17–22Date of authorisation for issue17–18Updating disclosure about conditions at the end of the reporting period19–20Non-adjusting events after the reporting period21–22EFFECTIVE DATE23WITHDRAWAL OF IAS 10 (REVISED 1999)24APPENDIXAmendments to other pronouncementsAPPROVAL OF IAS 10 BY THE BOARDBASIS FOR CONCLUSIONSIAS 10 International Accounting Standard 10 Events after the Reporting Period (IAS 10) is set out in paragraphs 1–24 and the Appendix. All the paragraphs have equal authority but retain the IASC format of the Standard when it was adopted by the IASB. IAS 10 should be read in the context of its objective and the Basis for Conclusions, the Prefa ce to Interna tiona l Fina ncia l Reporting Sta nda rds and the Fra mework for the Prepa ra tion a nd Presentation of Financial Statements. IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.© IASCF1037IAS 10IntroductionIN1International Accounting Standard 10 Events a fter the Reporting Period (IAS 10)* replaces IAS 10 Events After the Balance Sheet Date (revised in 1999) and should be applied for annual periods beginning on or after 1 January 2005. Earlier application is encouraged.Reasons for revising IAS 10IN2The International Accounting Standards Board developed this revised IAS 10 as part of its project on Improvements to International Accounting Standards.The project was undertaken in the light of queries and criticisms raised in relation to the Standards by securities regulators, professional accountants and other interested parties. The objectives of the project were to reduce or eliminate alternatives, redundancies and conflicts within the Standards, to deal with some convergence issues and to make other improvements.IN3For IAS 10 the Board’s main objective was a limited clarification of the accounting for dividends declared after the reporting period. The Board did not reconsider the fundamental approach to the accounting for events after the reporting period contained in IAS 10.The main changesIN4The main change from the previous version of IAS 10 was a limited clarification of paragraphs 12 and 13 (paragraphs 11 and 12 of the previous version of IAS 10).As revised, those paragraphs state that if an entity declares dividends after the reporting period, the entity shall not recognise those dividends as a liability at the end of the reporting period.*In September 2007 the IASB amended the title of IAS 10 from Events after the Balance Sheet Date to Events a fter the Reporting Period as a consequence of the revision of IAS 1 Presenta tion of Fina ncia l Statements in 2007.1038© IASCFIAS 10 International Accounting Standard 10Events after the Reporting PeriodObjective1The objective of this Standard is to prescribe:(a)when an entity should adjust its financial statements for events after thereporting period; and(b)the disclosures that an entity should give about the date when thefinancial statements were authorised for issue and about events after thereporting period.The Standard also requires that an entity should not prepare its financial statements on a going concern basis if events after the reporting period indicate that the going concern assumption is not appropriate.Scope2This Standard shall be applied in the accounting for, and disclosure of, events after the reporting period.Definitions3The following terms are used in this Standard with the meanings specified:Events after the reporting period are those events, favourable and unfavourable, that occur between the end of the reporting period and the date when the financial statements are authorised for issue. Two types of events can be identified:(a)those that provide evidence of conditions that existed at the end of thereporting period (adjusting events after the reporting period); and(b)those that are indicative of conditions that arose after the reporting period(non-adjusting events after the reporting period).4The process involved in authorising the financial statements for issue will vary depending upon the management structure, statutory requirements and procedures followed in preparing and finalising the financial statements.© IASCF1039IAS 105In some cases, an entity is required to submit its financial statements to its shareholders for approval after the financial statements have been issued. In such cases, the financial statements are authorised for issue on the date of issue, not the date when shareholders approve the financial statements.ExampleThe management of an entity completes draft financial statements for the yearto 31 December 20X1 on 28 February 20X2. On 18 March 20X2, the board ofdirectors reviews the financial statements and authorises them for issue.The entity announces its profit and selected other financial information on19March 20X2. The financial statements are made available to shareholdersand others on 1 April 20X2. The shareholders approve the financial statementsat their annual meeting on 15 May 20X2 and the approved financial statementsare then filed with a regulatory body on 17 May 20X2.The financial statements are authorised for issue on 18 March 20X2 (date of boardauthorisation for issue).6In some cases, the management of an entity is required to issue its financial statements to a supervisory board (made up solely of non-executives) for approval.In such cases, the financial statements are authorised for issue when the management authorises them for issue to the supervisory board.ExampleOn 18 March 20X2, the management of an entity authorises financialstatements for issue to its supervisory board. The supervisory board is made upsolely of non-executives and may include representatives of employees andother outside interests. The supervisory board approves the financialstatements on 26 March 20X2. The financial statements are made available toshareholders and others on 1 April 20X2. The shareholders approve thefinancial statements at their annual meeting on 15 May 20X2 and the financialstatements are then filed with a regulatory body on 17 May 20X2.The financial statements are authorised for issue on 18 March 20X2 (date of managementauthorisation for issue to the supervisory board).7Events after the reporting period include all events up to the date when the financial statements are authorised for issue, even if those events occur after the public announcement of profit or of other selected financial information.Recognition and measurementAdjusting events after the reporting period8An entity shall adjust the amounts recognised in its financial statements to reflect adjusting events after the reporting period.1040© IASCFIAS 10 9The following are examples of adjusting events after the reporting period that require an entity to adjust the amounts recognised in its financial statements, or to recognise items that were not previously recognised:(a)the settlement after the reporting period of a court case that confirms thatthe entity had a present obligation at the end of the reporting period.The entity adjusts any previously recognised provision related to this courtcase in accordance with IAS 37 Provisions, Contingent Liabilities and ContingentAssets or recognises a new provision. The entity does not merely disclose acontingent liability because the settlement provides additional evidencethat would be considered in accordance with paragraph 16 of IAS 37.(b)the receipt of information after the reporting period indicating that anasset was impaired at the end of the reporting period, or that the amountof a previously recognised impairment loss for that asset needs to beadjusted. For example:(i)the bankruptcy of a customer that occurs after the reporting periodusually confirms that a loss existed at the end of the reporting periodon a trade receivable and that the entity needs to adjust the carryingamount of the trade receivable; and(ii)the sale of inventories after the reporting period may give evidence about their net realisable value at the end of the reporting period.(c)the determination after the reporting period of the cost of assetspurchased, or the proceeds from assets sold, before the end of the reportingperiod.(d)the determination after the reporting period of the amount ofprofit-sharing or bonus payments, if the entity had a present legal orconstructive obligation at the end of the reporting period to make suchpayments as a result of events before that date (see IAS 19 Employee Benefits).(e)the discovery of fraud or errors that show that the financial statements areincorrect.Non-adjusting events after the reporting period10An entity shall not adjust the amounts recognised in its financial statements to reflect non-adjusting events after the reporting period.11An example of a non-adjusting event after the reporting period is a decline in market value of investments between the end of the reporting period and the date when the financial statements are authorised for issue. The decline in market value does not normally relate to the condition of the investments at the end of the reporting period, but reflects circumstances that have arisen subsequently.Therefore, an entity does not adjust the amounts recognised in its financial statements for the investments. Similarly, the entity does not update the amounts disclosed for the investments as at the end of the reporting period, although it may need to give additional disclosure under paragraph 21.© IASCF1041IAS 10Dividends12If an entity declares dividends to holders of equity instruments (as defined in IAS32 Financial Instruments: Presentation) after the reporting period, the entity shall not recognise those dividends as a liability at the end of the reporting period.13If dividends are declared (ie the dividends are appropriately authorised and no longer at the discretion of the entity) after the reporting period but before the financial statements are authorised for issue, the dividends are not recognised asa liability at the end of the reporting period because they do not meet the criteriaof a present obligation in IAS 37. Such dividends are disclosed in the notes in accordance with IAS 1 Presentation of Financial Statements.Going concern14An entity shall not prepare its financial statements on a going concern basis if management determines after the reporting period either that it intends to liquidate the entity or to cease trading, or that it has no realistic alternative but to do so.15Deterioration in operating results and financial position after the reporting period may indicate a need to consider whether the going concern assumption is still appropriate. If the going concern assumption is no longer appropriate, the effect is so pervasive that this Standard requires a fundamental change in the basis of accounting, rather than an adjustment to the amounts recognised within the original basis of accounting.16IAS 1 specifies required disclosures if:(a)the financial statements are not prepared on a going concern basis; or(b)management is aware of material uncertainties related to events orconditions that may cast significant doubt upon the entity’s ability tocontinue as a going concern. The events or conditions requiring disclosuremay arise after the reporting period.DisclosureDate of authorisation for issue17An entity shall disclose the date when the financial statements were authorised for issue and who gave that authorisation. If the entity’s owners or others have the power to amend the financial statements after issue, the entity shall disclose that fact.18It is important for users to know when the financial statements were authorised for issue, because the financial statements do not reflect events after this date. 1042© IASCFIAS 10 Updating disclosure about conditions at the end of thereporting period19If an entity receives information after the reporting period about conditions that existed at the end of the reporting period, it shall update disclosures that relate to those conditions, in the light of the new information.20In some cases, an entity needs to update the disclosures in its financial statements to reflect information received after the reporting period, even when the information does not affect the amounts that it recognises in its financial statements. One example of the need to update disclosures is when evidence becomes available after the reporting period about a contingent liability that existed at the end of the reporting period. In addition to considering whether it should recognise or change a provision under IAS 37, an entity updates its disclosures about the contingent liability in the light of that evidence.Non-adjusting events after the reporting period21If non-adjusting events after the reporting period are material, non-disclosure could influence the economic decisions that users mak e on the basis of the financial statements. Accordingly, an entity shall disclose the following for each material category of non-adjusting event after the reporting period:(a)the nature of the event; and(b)an estimate of its financial effect, or a statement that such an estimatecannot be made.22The following are examples of non-adjusting events after the reporting period that would generally result in disclosure:(a) a major business combination after the reporting period (IFRS 3 BusinessCombinations requires specific disclosures in such cases) or disposing of amajor subsidiary;(b)announcing a plan to discontinue an operation;(c)major purchases of assets, classification of assets as held for sale inaccordance with IFRS 5 Non-current Assets Held for Sa le a nd DiscontinuedOperations, other disposals of assets, or expropriation of major assets bygovernment;(d)the destruction of a major production plant by a fire after the reportingperiod;(e)announcing, or commencing the implementation of, a major restructuring(see IAS 37);(f)major ordinary share transactions and potential ordinary sharetransactions after the reporting period (IAS 33 Earnings per Share requires anentity to disclose a description of such transactions, other than when suchtransactions involve capitalisation or bonus issues, share splits or reverseshare splits all of which are required to be adjusted under IAS 33);© IASCF1043IAS 10(g)abnormally large changes after the reporting period in asset prices orforeign exchange rates;(h)changes in tax rates or tax laws enacted or announced after the reportingperiod that have a significant effect on current and deferred tax assets andliabilities (see IAS 12 Income Taxes);(i)entering into significant commitments or contingent liabilities, forexample, by issuing significant guarantees; and(j)commencing major litigation arising solely out of events that occurred after the reporting period.Effective date23An entity shall apply this Standard for annual periods beginning on or after 1January 2005. Earlier application is encouraged. If an entity applies this Standard for a period beginning before 1 January 2005, it shall disclose that fact.Withdrawal of IAS 10 (revised 1999)24This Standard supersedes IAS 10 Events After the Balance Sheet Date (revised in 1999). 1044© IASCFIAS 10 AppendixAmendments to other pronouncementsThe a mendments in this a ppendix sha ll be a pplied for a nnua l periods beginning on or a fter 1Janua ry2005. If an entity applies this Standard for an earlier period, these amendments shall be applied for that earlier period.* * * * *The a mendments conta ined in this a ppendix when this Sta nda rd wa s revised in 2003 ha ve been incorporated into the relevant IFRSs published in this volume.© IASCF1045IAS 10Approval of IAS 10 by the BoardInternational Accounting Standard 10 Events after the Balance Sheet Date was approved for issue by the fourteen members of the International Accounting Standards Board.Sir David Tweedie ChairmanThomas E Jones Vice-ChairmanMary E BarthHans-Georg BrunsAnthony T CopeRobert P GarnettGilbert GélardJames J LeisenringWarren J McGregorPatricia L O’MalleyHarry K SchmidJohn T SmithGeoffrey WhittingtonTatsumi Yamada1046© IASCFIAS 10 BC Basis for Conclusions onIAS 10 Events after the Reporting Period*This Basis for Conclusions accompanies, but is not part of, IAS 10.IntroductionBC1This Basis for Conclusions summarises the International Accounting Standards Board’s considerations in reaching its conclusions on revising IAS 10 Events After the Balance Sheet Date in 2003. Individual Board members gave greater weight to some factors than to others.BC2In July 2001 the Board announced that, as part of its initial agenda of technical projects, it would undertake a project to improve a number of Standards, including IAS 10. The project was undertaken in the light of queries and criticisms raised in relation to the Standards by securities regulators, professional accountants and other interested parties. The objectives of the Improvements project were to reduce or eliminate alternatives, redundancies and conflicts within Standards, to deal with some convergence issues and to make other improvements. In May 2002 the Board published its proposals in an Exposure Draft of Improvements to International Accounting Standards, with a comment deadline of 16 September 2002. The Board received over 160 comment letters on the Exposure Draft.BC3Because the Board’s intention was not to reconsider the fundamental approach to the accounting for events after the balance sheet date established by IAS 10, this Basis for Conclusions does not discuss requirements in IAS 10 that the Board has not reconsidered.Limited clarificationBC4For this limited clarification of IAS 10 the main change made is in paragraphs 12 and 13 (paragraphs 11 and 12 of the previous version of IAS 10). As revised, those paragraphs state that if dividends are declared after the balance sheet date,† an entity shall not recognise those dividends as a liability at the balance sheet date.This is because undeclared dividends do not meet the criteria of a present obligation in IAS 37 Provisions, Contingent Liabilities and Contingent Assets. The Board discussed whether or not an entity’s past practice of paying dividends could be considered a constructive obligation. The Board concluded that such practices do not give rise to a liability to pay dividends.*In September 2007 the IASB amended the title of IAS 10 from Events after the Balance Sheet Date to Events after the Reporting Period as a consequence of the amendments in IAS 1 Presentation of Financial Statements (as revised in 2007).†IAS1Presentation of Financial Statements (as revised in 2007) replaced the term ‘balance sheet date’with ‘end of the reporting period’.© IASCF1047。

SAE J17112010

entirely voluntary, and its applicability and suitability for any particular use, including any patent infringement arising therefrom, is the sole responsibility of the user.”

SAE reviews each technical report at least every five years at which time it may be reaffes your written comments and suggestions.

SURFACE VEHICLE RECOMMENDED PRACTICE

J1711 JUN2010

Issued Revised

1999-03 2010-06

Superseding J1711 MAR1999

(R) Recommended Practice for Measuring the Exhaust Emissions and Fuel Economy of Hybrid-Electric Vehicles, Including Plug-in Hybrid Vehicles

Copyright © 2010 SAE International

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical,

117A VLF Comparator操作和维护手册说明书

ErrataTitle & Document Type: 117A VLF Comparator Operating and Service Manual Manual Part Number: 00117-9029Revision Date: November 1968About this ManualWe’ve added this manual to the Agilent website in an effort to help you support your product. This manual provides the best information we could find. It may be incompleteor contain dated information, and the scan quality may not be ideal. If we find a bettercopy in the future, we will add it to the Agilent website.HP References in this ManualThis manual may contain references to HP or Hewlett-Packard. Please note that Hewlett- Packard's former test and measurement, life sciences, and chemical analysisbusinesses are now part of Agilent Technologies. The HP XXXX referred to in this document is now the Agilent XXXX. For example, model number HP8648A is now model number Agilent 8648A. We have made no changes to this manual copy.Support for Your ProductAgilent no longer sells or supports this product. You will find any other availableproduct information on the Agilent Test & Measurement website:Search for the model number of this product, and the resulting product page will guideyou to any available information. Our service centers may be able to perform calibrationif no repair parts are needed, but no other support from Agilent is available.。

Omega BVLS系列限位开关用户指南说明书

e-mail:**************For latest product manuals: BVLS SERIESLimit Switch for BVP70, BVPS70, BVP80, and BVPS80 Series Shop online at SM User’s Guide***********************Servicing North America:U.S.A.:Omega Engineering, Inc., One Omega Drive, P.O. Box 4047S tamford, CT 06907-0047 USAToll-Free: 1-800-826-6342 (USA & Canada only)Customer Service: 1-800-622-2378 (USA & Canada only)Engineering Service: 1-800-872-9436 (USA & Canada only)Tel: (203) 359-1660 Fax: (203) 359-7700e-mail:**************For Other Locations Visit /worldwideThe information contained in this document is believed to be correct, but OMEGA accepts no liability for any errors it contains, and reservesMATERIALS OF CONSTRUCTIONBODY / COVER: Aluminium with Teflon Imprenated Hard Anodized (PolyLube ) SurfacesPROBES: 316 Stainless SteelSEALS - COVER, PROBES: Buna N RATINGS / SPECIFICATIONS TEMPERATURE: 10 F to 180 FCONDUIT CONNECTION: 1/2” NPTELECTRICAL RATING:10 amp. 250VAC maximum; 1/2 amp. 125VDC; 1/4 amp. 250VDC; 5 amp.125VAC lamp load. Note: each pole must be the same polarity to utilize these ratings.MICROSWITCHES: Mechanical S.P .D.T. (Single Pole Double Throw)INTERNAL WIRING CONNECTIONS: Screw Clamp NEMA STANDARDS: NEMA 1 (General Purpose); NEMA 4 (Watertight & Dusttight); NEMA 7 (Haz-ardous Locations, Class I Groups B, C, & D); NEMA 9 (Hazardous Locations, Class II, Groups E, F, &G); NEMA 12 (Oiltight and Driptight); and NEMA 13 (Oiltight and Dusttight).UL LISTINGS: Industrial Control Equipment for use in Hazardous Locations, Class I, Groups B,C, & D and Class II, Groups E, F, & GMAINTENANCEThe BVLS normally requires no maintenance. However, in certain situations the switch adjustment screws may require some attention to either advance or retard the cam actuated switch point. This enables precise adjustment of the switch timing throughout the life of the unit.Switch AdjustmentScrewsTerminal StripElectrical Schematic asShown - Inside CoverAttachment of Limit Switch / NAMUR Mounting Pad1. Remove the position indicator from atop the actuator and securethe NAMUR 30 Shaft Coupling to the actuator Shaft Extension withthe #6-32 Set Screw using a medium strength (nonpermanent) threadlocker (not included in mounting kit).2. Place the Limit Switch / NAMUR Mounting Pad on top of the actua-tor. Be sure that the lower flats of the NAMUR 30 Shaft Coupling areoriented such that they align with the Limit Switch Mounting holes onthe Limit Switch / NAMUR Mounting Pad.3. Fasten the Limit Switch / NAMUR Mounting Pad to the actuatorusing the (2) Mounting Bracket Screws.4. Slide the position indicator over the NAMUR 30 Shaft Couplinguntil it ‘snaps’ into place just above the bracket.Attachment of Limit Switch1. Fit the bushings, which extend from the Limit Switch housing, into the matching holes in the mounting pad. Push switch housing against pad and verify that switch body touches pad. Secure switch body to pad with two #10-24 setscrews using a medium strength (nonpermanent) thread locker (not included in mounting kit). Note: Hex wrench sup-plied with Mounting Kit.Wiring Instructions1. Route the wire to be terminated through the conduit hub and upthrough the access space to the terminal block.2. Strip insulation back 1/4”, insert the stripped ends directly into theproper terminal clamps and tighten screws.3. Internal interconnections between terminal-block and switches arediagrammed inside the Limit Switch Cover.Note: If the Switch is installed in a hazardous location i.e. whereflammable vapors or dust are present in the atmosphere, replacethe cover and tighten securely before connecting the electrical sup-ply circuit. If necessary, a screwdriver shank or similar tool may beengaged in the cover wrenching lugs to assist removal and replace-ment.Wiring SpecificationsSwitch RatingsAC250 volts; 10 ampsDC250 volts; 0.25 amps125 volts; 0.50 ampsLamp Load 125 volts; 5 ampsWire Size#12 AWG Max.#24 AWG Min.OMEGA’s policy is to make running changes, not model changes, whenever an improvement is possible. This affords our customers the latest in technology and engineering.OMEGA is a registered trademark of OMEGA ENGINEERING, INC.© Copyright 2015 OMEGA ENGINEERING, INC. All rights reserved. T his document may not be copied, photocopied, reproduced, translated, or reduced to any electronic medium or machine-readable form, in whole or in part, without the FOR WARRANTY RETURNS, please have the following information available BEFORE contacting OMEGA:1. P urchase Order number under which the product was PURCHASED,2. M odel and serial number of the product under warranty, and3. Repair instructions and/or specific problems relative to the product.FOR NON-WARRANTY REPAIRS, consult OMEGA for current repair charges. Have the following information available BEFORE contacting OMEGA:1. Purchase Order number to cover the COST of the repair,2. Model and serial number of the product, and 3. Repair instructions and/or specific problems relative to the product.RETURN REQUESTS/INQUIRIESDirect all warranty and repair requests/inquiries to the OMEGA Customer Service Department. BEFORE RET URNING ANY PRODUCT (S) T O OMEGA, PURCHASER MUST OBT AIN AN AUT HORIZED RET URN (AR) NUMBER FROM OMEGA’S CUST OMER SERVICE DEPART MENT (IN ORDER T O AVOID PROCESSING DELAYS). The assigned AR number should then be marked on the outside of the return package and on any correspondence.The purchaser is responsible for shipping charges, freight, insurance and proper packaging to prevent breakage in transit.WARRANTY/DISCLAIMEROMEGA ENGINEERING, INC. warrants this unit to be free of defects in materials and workmanship for a period of 13 months from date of purchase. OMEGA’s WARRANTY adds an additional one (1) month grace period to the normal one (1) year product warranty to cover handling and shipping time. This ensures that OMEGA’s customers receive maximum coverage on each product.If the unit malfunctions, it must be returned to the factory for evaluation. OMEGA’s Customer Service Department will issue an Authorized Return (AR) number immediately upon phone or written request. Upon examination by OMEGA, if the unit is found to be defective, it will be repaired or replaced at no charge. OMEGA’s WARRANT Y does not apply to defects resulting from any action of the purchaser, including but not limited to mishandling, improper interfacing, operation outside of design limits, improper repair, or unauthorized modification. T his WARRANT Y is VOID if the unit shows evidence of having been tampered with or shows evidence of having been damaged as a result of excessive corrosion; or current, heat, moisture or vibration; improper specification; misapplication; misuse or other operating conditions outside of OMEGA’s control. Components in which wear is not warranted, include but are not limited to contact points, fuses, and triacs.OMEGA is pleased to offer suggestions on the use of its various products. However, OMEGA neither assumes responsibility for any omissions or errors nor assumes liability for any damages that result from the use of its products in accordance with information provided by OMEGA, either verbal or written. OMEGA warrants only that the parts manufactured by the company will be as specified and free of defects. OMEGA MAKES NO OTHER WARRANTIES OR REPRESENTATIONS OF ANY KIND WHATSOEVER, EXPRESSED OR IMPLIED, EXCEPT THAT OF TITLE, AND ALL IMPLIED W ARRANTIES INCLUDING ANY W ARRANTY OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE ARE HEREBY DISCLAIMED. LIMITATION OF LIABILITY: The remedies of purchaser set forth herein are exclusive, and the total liability of OMEGA with respect to this order, whether based on contract, warranty, negligence, indemnification, strict liability or otherwise, shall not exceed the purchase price of the component upon which liability is based. In no event shall OMEGA be liable for consequential, incidental or special damages.CONDITIONS: Equipment sold by OMEGA is not intended to be used, nor shall it be used: (1) as a “Basic Component” under 10 CFR 21 (NRC), used in or with any nuclear installation or activity; or (2) in medical applications or used on humans. Should any Product(s) be used in or with any nuclear installation or activity, medical application, used on humans, or misused in any way, OMEGA assumes no responsibility as set forth in our basic WARRANTY /DISCLAIMER language, and, additionally, purchaser will indemnify OMEGA and hold OMEGA harmless from any liability or damage whatsoever arising out of the use of theProduct(s) in such a manner.Where Do I Find Everything I Need for Process Measurement and Control?OMEGA…Of Course!Shop online at SMTEMPERATUREM U Thermocouple, RTD & Thermistor Probes, Connectors, Panels & AssembliesM U Wire: Thermocouple, RTD & ThermistorM U Calibrators & Ice Point ReferencesM U Recorders, Controllers & Process MonitorsM U Infrared PyrometersPRESSURE, STRAIN AND FORCEM U Transducers & Strain GagesM U Load Cells & Pressure GagesM U Displacement TransducersM U Instrumentation & AccessoriesFLOW/LEVELM U Rotameters, Gas Mass Flowmeters & Flow ComputersM U Air Velocity IndicatorsM U Turbine/Paddlewheel SystemsM U Totalizers & Batch ControllerspH/CONDUCTIVITYM U pH Electrodes, Testers & AccessoriesM U Benchtop/Laboratory MetersM U Controllers, Calibrators, Simulators & PumpsM U Industrial pH & Conductivity EquipmentDATA ACQUISITIONM U Data Acquisition & Engineering SoftwareM U Communications-Based Acquisition SystemsM U Plug-in Cards for Apple, IBM & CompatiblesM U Data Logging SystemsM U Recorders, Printers & PlottersHEATERSM U Heating CableM U Cartridge & Strip HeatersM U Immersion & Band HeatersM U Flexible HeatersM U Laboratory HeatersENVIRONMENTALMONITORING AND CONTROLM U Metering & Control InstrumentationM U RefractometersM U Pumps & TubingM U Air, Soil & Water MonitorsM U Industrial Water & Wastewater TreatmentM U pH, Conductivity & Dissolved Oxygen Instruments。

SANS1507-2 Electric cables with extruded solid dielectric insulation for fixed installations

ISBN 978-0-626-20840-0 SANS 1507-2:2007Edition 1.1Any reference to SABS 1507-2 is deemedto be a reference to this standard(Government Notice No. 1373 of 8 November 2002) SOUTH AFRICAN NATIONAL STANDARD Electric cables with extruded solid dielectric insulation for fixed installations(300/500 V to 1 900/3 300 V)Part 2: Wiring cablesPublished by Standards South Africa1 dr lategan road groenkloof private bag x191 pretoria 0001tel: 012 428 7911 fax: 012 344 1568 international code + 27 12www.stansa.co.za© Standards South AfricaSANS 1507-2:2007Edition 1.1Table of changesChange No.Date ScopeAmdt 1 2007 Amended to change the designation of SABS standards to SANSstandards, to update referenced standards, and to delete referenceto the standardization mark scheme.ForewordThis South African standard was approved by National Committee StanSA TC 66, Electric cables, in accordance with procedures of Standards South Africa, in compliance with annex 3 of the WTO/TBT agreement.This standard was published in December 2007.This document supersedes SABS 1507-2:2002 (edition 1).A vertical line in the margin shows where the text has been technically modified by amendment No. 1.SANS 1507 consists of the following parts, under the general title Electric cables with extruded solid dielectric insulation for fixed installations (300/500 V to 1 900/3 300 V):Part 1: General.Part 2: Wiring cables.Part 3: PVC Distribution cables.Part 4: XLPE Distribution cables.Part 5: Halogen-free distribution cables.Part 6: Service cables.For guidance the following additional information, which does not form part of the requirements of this standard, is provided in SANS 1507-1:a) notes to purchasers;b) guidance on the verification of the quality of extruded solid dielectric insulated cables; andc) guidance on the installation of extruded solid dielectric insulated cables.SANS 1507-2:2007Edition 1.11ContentsPageForeword1 Scope (3)2 Normative references (3)3 Definitions (4)4 General requirements......................................................................................................... 4 4.1 Cable operating voltage........................................................................................... 4 4.2 Materials and construction....................................................................................... 4 4.3 Electrical requirements for finished cables (6)5 Specific requirements for types of cables in common use................................................. 7 5.1 Insulated wire (600/1 000V)..................................................................................... 7 5.2 Multicore flat and circular sheathed cables (300/500 V).......................................... 7 5.3 Single-core unsheathed panel/cubicle cables (300/500 V)...................................... 8 5.4 Circular sheathed multicore cables with bare earth continuity conductors and aluminium/PVC laminate (300/500 V) (8)6 Inspection and methods of test.......................................................................................... 8 6.1 General..................................................................................................................... 8 6.2 Conditions of test (9)SANS 1507-2:2007Edition 1.1This page is intentionally left blank 2SANS 1507-2:2007Edition 1.1 Electric cables with extruded solid dielectric insulation for fixedinstallations (300/500 V to 1 900/3 300 V)Part 2:Wiring cables1 Scope1.1This part of SANS 1507 covers the requirements for construction, materials, dimensions and electric properties of unarmoured single-core and multicore extruded solid dielectric insulated cables with rated operating voltages (U0 /U) of 300/500 V and 600/1 000 V, up to and including a conductor cross-sectional area of 16 mm2 for use in fixed installations.1.2Specific types of cables covered by this part of SANS 1507 are the following:a) insulated wire (600/1 000 V);b) multicore flat and circular sheathed cables (300/500 V);c) single-core unsheathed panel/cubicle cables (300/500 V); andd) multicore round cables with aluminium/PVC laminate and an earth continuity conductor(300/500 V).2 Normative referencesThe following standards contain provisions which, through reference in this text, constitute provisions of this part of SABS 1507. All standards are subject to revision and, since any reference to a standard is deemed to be a reference to the latest edition of that standard, parties to agreements based on this part of SABS 1507 are encouraged to take steps to ensure the use of the most recent editions of the standards indicated below. Information on currently valid national and international standards can be obtained from Standards South Africa.SANS 1411-1, Materials of insulated electric cables and flexible cords – Part 1: Conductors.SANS 1411-2, Materials of insulated electric cables and flexible cords – Part 2: Polyvinyl chloride (PVC).SANS 1507-1, Electric cables with extruded solid dielectric insulation for fixed installations (300/500 V to 1 900/3 300 V) – Part 1: General.3SANS 1507-2:2007Edition 1.1SANS 5526, Dielectric resistance of electric cables.SANS 6284-3, Test methods for cross-linked polyethylene (XLPE) insulated electric cables – Part 3: Tests on finished cable.SANS 10142-1, The wiring of premises – Part 1: Low-voltage installations.SANS 60811-1-1/IEC 60811-1-1, Common test methods for insulating and sheathing materials of electric cables and optical cables – Part 1-1: Methods for general application – Measurement of thickness and overall dimensions – Tests for determining the mechanical properties.SANS 62230/IEC 62230, Electric cables – Spark-test method. Amdt 1 3 DefinitionsFor the purposes of this part of SANS 1507 the definitions given in SANS 1507-1 shall apply.4 General requirements4.1 Cable operating voltageThe maximum permissible operating voltage of a cable shall be either 300/500 V or 600/1 000 V. 4.2 Materials and construction4.2.1 ConductorsConductors shall be of plain or tinned annealed copper, as required, and they shall comply with the requirements of SANS 1411-1.4.2.2 Insulation4.2.2.1 MaterialThe insulation shall be extruded PVC complying with the requirements for insulation grade PVC of SANS 1411-2.4.2.2.2 Thickness and insulation resistance4.2.2.2.1 Unless otherwise stated in the relevant specific requirements given in clause 5, the nominal thickness and the insulation resistance of the insulating material shall comply with the requirements given in table 7, as appropriate to the cross-sectional area of the conductor and operating voltage.4.2.2.2.2 When the thickness of the insulation is determined in accordance with SANS 60811-1-1, the average thickness shall be at least equal to the nominal value, and the minimum thickness at any point may be less than the nominal value provided that the difference does not exceed 0,1 mm + 10 % of the nominal value.4.2.2.3Spark resistance of insulationAll core insulation shall be spark tested using the method given in SANS 62230 at an ac rms test voltage of 5 000 V in the case of 300/500 V cables, or at 6 000 V in the case of 600/1 000 V cables, without breakdown of the dielectric. Alternatively a dc test voltage 1,5 times the appropriate ac rms test voltage may be used. Amdt 1 4SANS 1507-2:2007Edition 1.154.2.3 Core identification4.2.3.1 IdentificationCores shall be identified durably and distinctly by colouring as specified in table 1.4.2.3.2 Earthing coresWhere an earthing core is not bare it shall be coloured green and yellow, and the combination of the colours shall be such that one of these colours covers not less than 30 % and not more than 70 % of the surface of the core, and the other covers the remainder of the surface. There shall be no green/yellow coloured core in a two-core cable or in any non-earthing type cable.NOTE The combination of green/yellow is reserved exclusively for the identification of the earthing core.Table 1 — Core identification1 2 3 4 5 Number of phase coresColour(s) of phase cores Colour of neutral coreColour of earthing core (if present and not bare) Colour of special purpose core (if present) 1Any, except green---1 Red Black Green / yellow Orange2 Red and yellow Black Green / yellow Orange3 Red, yellow and blue BlackGreen / yellowOrange4 or moreAny base colour except green and orange, with serialnumbers (numerals or words)Numbered as for phase coresGreen / yellow4.2.4 Assembly of cores4.2.4.1 GeneralThe cores of a multicore cable shall be compactly laid up with an acceptable lay and in the correct sequence of their identification colours or numbers.4.2.4.2 FillersFillers may be applied integrally with either the bedding or the sheath, as applicable, and shall be used in the interstices of the cable where necessary to give the completed cable a compact circular cross-section. Filler materials shall be such as to be acceptable for the specific type of cable.4.2.4.3 BinderA binder may be applied over the laid-up cores, and the material shall be such as to be acceptable for the specific type of cable.SANS 1507-2:2007 Edition 1.164.2.5 Sheaths4.2.5.1 GeneralSheaths shall consist of a continuous extrudate that closely fits but does not adhere to the underlying core or assembled cores. The surface of the extrudate shall have a smooth finish and its profile shall be uniform and appropriate to the type of cable.4.2.5.2 MaterialThe sheath shall consist of an extruded layer of PVC of type S1 to S4 of SANS 1411-2.4.2.5.3 Thickness4.2.5.3.1 Unless otherwise stated in the relevant specific requirements given in clause 5, the nominal thickness of the sheath shall be as given in table 2.4.2.5.3.2 When the average thickness of the sheath is determined in accordance with SANS 60811-1-1, it shall be at least equal to the nominal value, and the minimum thickness at any point may be less than the nominal value provided that the difference does not exceed 0,1 mm + 15 % of the nominal value.Table 2 — Thickness of sheath1 2 3Thickness of sheathmmUnarmoured cableNominal diameter undersheath mmNominalMinimum ≤ 10 1,6 1,26 > 10 ≤ 15 1,8 1,43 > 15 ≤ 20 1,8 1,43 > 20 ≤ 25 2,0 1,60 > 25 ≤ 30 2,0 1,60 > 30≤ 352,21,774.3 Electrical requirements for finished cables4.3.1 Conductor resistanceThe dc resistance of each conductor shall not exceed the appropriate maximum value given in SANS 1411-1.SANS 1507-2:2007Edition 1.174.3.2 Voltage withstandWhen a cable is factory tested in accordance with SANS 6284-3, each core of the cable shall withstand, for 10 min without breakdown of the dielectric, a test voltage of the appropriate value given in column 3 or 4 of table 3. Alternatively, the test may be conducted for 5 min at a test voltage of the appropriate value given in column 5 or 6 of the table.Table 3 — Test voltages1 2 3 4 5 6CablesAlternating current rms test voltageV 10 minute test5 minute test Rated voltage V Type or cross-sectionalareaBetween conductorsBetween any conductor and earth Between conductorsBetween any conductor and earth 300/500 Single core cable or panel / cubicle cable – 1 200 – 1 800 300/500 Multicore cable1 500 1 5002 250 2 250 600/1 000Cables of cross sectional area not exceeding 16 mm 22 0002 0003 0003 0004.3.3 Dielectric resistanceWhen a cable is tested in accordance with SANS 5526, the insulation resistance of the cable shall be at least equal to the value given in the appropriate columns of tables 5, 6 and 7.5 Specific requirements for types of cable s in common use5.1 Insulated wire (600/1 000 V)5.1.1 ConstructionThe conductor shall be circular stranded, annealed copper complying to the requirements of SANS 1411-1, class 2. The insulation shall be coloured as per table 1 and shall meet the requirements of PVC type D1 or D2 of SANS 1411-2.5.1.2 RequirementsThe thickness and insulation resistance of the PVC insulation shall comply with table 7 columns 5, 6 and 7.5.2 Multicore flat and circular sheathed cables (300/500 V)5.2.1 ConstructionEach core of a multicore cable shall consist of a circular solid or stranded annealed copper conductor. The insulation shall be coloured as per table 1 and shall meet the requirements of PVC type D1 or D2 of SANS 1411-2.SANS 1507-2:2007Edition 1.1The cores shall be adjacent in a circular or flat arrangement and shall be sheathed. The sheath shall completely surround the cores, shall be close fitting but shall not adhere to the cores. An uninsulated annealed copper earth continuity conductor, as per column 6 of table 5, may be included between the cores.5.2.2 RequirementsEach cable shall comply with the relevant requirements given in table 5.5.3 Single-core unsheathed panel / cubicle cables (300/500 V)5.3.1 ConstructionA single-core cable shall consist of a circular solid annealed copper conductor which shall comply with the requirements of table 6. The insulation shall be coloured as per table 1 and shall meet the requirements of PVC type D1 of SANS 1411-2.5.3.2 RequirementsEach cable shall comply with the relevant requirements given in table 6.5.4 Circular sheathed multicore cables with bare earth continuity conductors and aluminium / PVC laminate (300/500 V)5.4.1 Cables shall have 2, 3 or 4 cores, coloured as in table 1.5.4.2 Cables shall have solid or stranded conductors as given in table 5.5.4.3 Insulation thickness and insulation resistance shall comply with columns 2, 3 and 4 of table 7.5.4.4 Aluminium laminate shall consist of longitudinally applied aluminium tape of minimum thickness 0,1 mm, covered by a sheath (see 5.4.7 below).5.4.5 Earth continuity conductors shall be tinned annealed copper and shall comply with the requirements given in table 5.5.4.6 Earth continuity conductors for a four-core cable shall be the same as given in table 5 for a three-core cable.5.4.7 The sheath shall consist of extruded PVC that complies with type S1 of SANS 1411-2.5.4.8 The thickness of the sheath shall be at least 0,8 mm and shall be bonded to the aluminium laminate.6 Inspection and methods of test6.1 GeneralFor convenience, the properties to be tested, the test category, the test methods and the sub-clause giving the requirements are listed in table 4 below:8Table 4 — List of tests to be conducted1 234 5Component(s)Test propertyTestcategoryTest methodgiven inRequirementsubclauseConductor Construction S SANS1411-1 4.2.1Physical properties of material S SANS1411-2 4.2.2Thickness SSANS60811-1-14.2.2.2Spark test R SANS 62230 4.2.2.3Core identification R, S Visual examination 4.2.3PVC InsulationAssembly of cores R Visual examination 4.2.4Physical properties of material S SANS1411-2 4.2.5.2PVC SheathThickness SSANS60811-1-14.2.5.3Marking R Visual examination 4.2 ofSANS 1507-1Conductor resistance R SANS 1411-1 4.3.1Voltage withstand R SANS 6284-3 4.3.2 Finished cableDielectric resistance S SANS 5526 4.3.3 NOTE 1 In column 3 of this table, a code letter is given that identifies the tests as suitable for use asroutine tests (R) or sample tests (S), but compliance with the requirements of the specification may onlybe fully determined from the results of tests carried out on samples of completed cable(s), using all thetest methods given and a sampling procedure agreed upon. During production control, a manufacturermay use any tests that he deems necessary to ensure compliance with the specification but, in the caseof a dispute, only the appropriate standard test methods may be used.NOTE 2 Deleted by amendment No. 1.Amdt 16.2 Conditions of test6.2.1 All tests are to be carried out at ambient temperature and pressure, unless otherwise statedin the test method.6.2.2 Unless otherwise required in the test method, the frequency of the alternating test voltageused shall be approximately 50 Hz, and the waveform shall be substantially sinusoidal.Table 5 — Requirements for multicore sheathed cables (300/500 V)1 2 3 4 5 6 7 Mean overall dimensions(flat cables)mm Number and cross-sectional area of the conductorsNominalradialthicknessofinsulation Nominal radial thick-ness of sheath bEarth con-tinuity conductor cross-sectional area Insulation resistance at23 °Cmm 2 mm mm Lower limitUpper limitmm 2, min.M Ω·km, min.2 × a 1,0 0,6 0,9 4,0 × 7,2 4,7 × 8,6 1,0a 10 2 × a 1,5 0,7 0,9 4,4 × 8,2 5,4 × 9,6 1,0a 10 2 × a 2,5 0,81,0 5,2 × 9,8 6,2 × 11,51,5a 102 × 4,0 0,8 1,1 5,6 × 10,5 7,2 × 13,0 1,5a 10 2× 6,00,8 1,16,4× 12,58,0 × 15,02,5a 10 2 × 10,0 0,9 1,2 7,8 × 15,5 9,6 × 19,0 4,0 10 2 × 16,0 0,9 1,3 9,0 × 18,0 11,0 × 22,0 6,0 103 × a 1,0 0,6 0,9 4,0 × 9,6 4,7 × 11,0 1,0a 103 × a 1,5 0,7 0,9 4,4 × 10,5 5,4 × 12,5 1,0a 10 3 × a 2,5 0,8 1,0 5,2 × 12,5 6,2 × 14,5 1,5a 103 × 4,0 0,8 1,1 5,6 × 14,5 7,4 × 18,0 1,5a 10 3× 6,00,8 1,16,4× 16,58,0 × 20,0 2,5a 10 3 × 10,0 0,91,2 7,8 × 21,09,6 × 25,54,0a10aMay be a solid or stranded conductor.bSheath thickness for 4 core cables to be same as for 3 core cables.Table 6 — Requirements for single core unsheathed panel/cubicle cables (300/500 V)a1 2 3 4 5 6 7Thickness of insulationmmCross-sectionalarea conductorDiameter of wire in conductor Approximate diameter of conductorConductor resistance at20 °C Insulation resistance at23 °C mm 2mm mm NominalMin.bΩ·km, max.M Ω·km, min. CalculatedNominal0,196 0,5c 0,50 0,50 0,40 89,6 10 0,312 0,63c 0,63 0,50 0,40 56,4 10 0,396 0,71 0,71 0,55 0,45 44,4 100,504 0,8 0,8 0,55 0,45 35,0 10 0,636 0,9 0,9 0,55 0,45 27,6 10 0,785 1,0 1,0 0,55 0,45 22,4 100,985 1,12 1,12 0,55 0,45 17,9 10 1,227 1,25 1,25 0,55 0,45 14,3 10 1,539 1,40 1,40 0,55 0,45 11,4 10 2,011 1,60 1,60 0,55 0,458,7510aIn terms of the provisions of SANS 10142-1, none of these cables may be used for the wiring of premises.b This minimum is the nominal less 0,1 mm.cThese cables are suitable for use in pre-wired and nominally sealed subassemblies and in harnesses.Table 7 — Thickness and insulation resistance of PVC Insulation oftypes D1, D2, D3, D4 , D5 and D61 23 4 56 7Voltage rating300/500 V600/1 000 VThickness of insulationmm Thickness of insulationmmCross-sectionalarea conductor Insulationresistance a at23 °CInsulation resistance a at23 °Cmm2Nominal Min.MΩ·km, min.Nominal Min.MΩ·km, min.1,0 0,60,44 20 0,80,62 25 1,5 0,70,53 22 0,80,62 24 2,5 0,80,62 20 0,80,62 20 4,0 0,80,62 16 1,00,80 19 6,0 0,80,62 14 1,00,80 17 10,0 0,90,71 12 1,00,80 14 16,0 0,90,71 10 1,00,80 11 a Based on a minimum volume resistivity of 2,0 × 1011Ω·m at 23 °C and the nominal thickness of thedielectric.© Standards South Africa。

A217-2010

2 For ASME Boiler and Pressure Vessel Code applications, see related Specification SA-217/SA 217M in Section II of that code.

each system may not be exact equivalents; therefore, each system shall be used independently of the other. Combining values from the two systems may result in non-conformance with the standard.

Standard Specification for Steel Castings, Martensitic Stainless and Alloy, for Pressure-Containing Parts, Suitable for High-Temperature Service1

This standard is issued under the fixed designation A217/A217M; the number immediately following the designation indicates the year of original adoption or, in the case of revision, the year of last revision. A number in parentheses indicates the year of last reapproval. A superscript epsilon (´) indicates an editorial change since the last revision or reapproval.

INSTALLATION, OPERATING AND MAINTENANCE MANUAL FOR

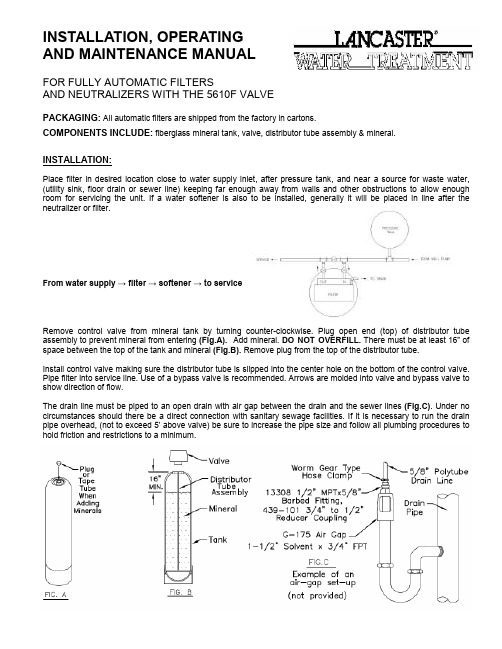

FOR FULLY AUTOMATIC FILTERSAND NEUTRALIZERS WITH THE 5610F VALVEINSTALLATION, OPERATINGAND MAINTENANCE MANUALPACKAGING: All automatic filters are shipped from the factory in cartons.COMPONENTS INCLUDE: fiberglass mineral tank, valve, distributor tube assembly & mineral. Remove control valve from mineral tank by turning counter-clockwise. Plug open end (top) of distributor tube assembly to prevent mineral from entering (Fig.A). Add mineral. DO NOT OVERFILL. There must be at least 16” of space between the top of the tank and mineral (Fig.B). Remove plug from the top of the distributor tube.Install control valve making sure the distributor tube is slipped into the center hole on the bottom of the control valve. Pipe filter into service line. Use of a bypass valve is recommended. Arrows are molded into valve and bypass valve to show direction of flow.The drain line must be piped to an open drain with air gap between the drain and the sewer lines (Fig.C). Under no circumstances should there be a direct connection with sanitary sewage facilities. If it is necessary to run the drain pipe overhead, (not to exceed 5’ above valve) be sure to increase the pipe size and follow all plumbing procedures to hold friction and restrictions to a minimum.INSTALLATION:Place filter in desired location close to water supply inlet, after pressure tank, and near a source for waste water, (utility sink, floor drain or sewer line) keeping far enough away from walls and other obstructions to allow enough room for servicing the unit. If a water softener is alsoto beinstalled, generally it will be placed in line after the neutralizer or filter.From water supply → filter → softener → to serviceMAINTENANCE:ACID NEUTRALIZERS , (7-EDAN-, 7-EAN-): Mineral used: Calcite. Calcite will dissolve in proportion to the amount of acid in the raw water. The amount of mineral in the tank should be monitored and replaced periodically. A tank with a dome plug is recommended so that mineral may be added without removing the control valve. To check level of calcite in the mineral tank shut off water supply to the filter. Turn manual regeneration knob clockwise to the backwash position to relieve pressure in the tank. Remove hexagonal dome plug. A small amount of water will be lost from the tank. Insert a dipstick into the dome hole until the stick reaches mineral level. Mark and remove the stick. Measure the marked distance on the stick. This number should never be less than 16”. Replace calcite before the mineral level is 24” from the dome hole. Adding calcite will displace the water in the tank. This water may be siphoned out to reduce spillage. As each installation will use a different amount of calcite, monitoring the mineral level once a month for the first few months of operation should give a fairly good indication as to how frequently the calcite will need to be replenished. Replace the dome plug. Turn on the water supply to the neutralizer. Allow water to run to drain until it becomes clear. Return manual regeneration knob to the service position by turning the knob clockwise.A pH test kit may also be used to monitor the pH level to help determine when mineral needs to be replenished. Calcite will add approximately four (4) or more grains per gallon to the original hardness of the raw water. This should be kept in mind when figuring regeneration cycle for a water softener. If a Corosex/Calcite mixture is recommended to be used (for high flow rates or very low pH level), mix one part Corosex with four parts Calcite BEFORE adding to the tank. NOTE: 1 cu ft. of calcite = 85 lbs.IRON FILTERS , (7-EIM-): Mineral used: Birm. No chemical regenerant is required, backwash periodically. No hard-ness is added to the water. For clear water iron, when the pH is less than seven (7) in the raw water, a water softener should be used in place of the iron filter. Note: When using Birm for iron removal, it is necessary that the water: contain no oil or hydrogen sulfide, organic matter not to exceed 4-5 ppm, the D.O. content equal at least 15% of iron content with a pH of 6.8 or more. If the influent water has a pH of less that 6.8, neutralizing additives such as Calcite, Corosex or soda ash may be used prior to the Birm filter to raise the pH. A water having a low D.O. level may be pretreated by aeration. Chlorination greatly reduces Birm’s activity. High concentrations of chlorine compounds may deplete the catalytic coating. * If Manganese Greensand is used, see instruction sheet for TPIM units.COLOR, TASTE AND ODOR FILTERS , (7-ECT-): Mineral used: Carbon. Used for removal of chlorine, color, taste, odor and low levels of sulfur, etc. The mineral bed should be backwashed periodically, but will in time reach the maximum absorbency. When this occurs the carbon should be completely replaced.SEDIMENT AND TURBIDITY, (7-EST-): Mineral used: Filter Ag. This filter will filter out dirt, silica, etc. down to the 20-40 micron range. In most cases it has a lifetime fill and should be backwashed periodically depending on local conditions. Pressure drop is very low.Set backwash frequency. The filter should be backwashed every 3-6 days, but must be backwashed at least once every 12 days. Rotate the “skipper wheel” until the red pointer is at “1“ (Fig.D). Each metal tab on the skipper wheel represents one day. Set the days that backwash is to occur by sliding tabs on the skipper wheel outward to expose trip fingers. Set the actual time of day on the control valve by pressing the red time set button and turning the time of day gear. Backwash is factory programmed for 12:01 A.M. For multiple tank installation, each tank must be backwashed at separate times; set a different time of day on each timer (about 2 hours apart), or set each tankto backwash on different days.Turn the large Manual Regeneragion knob to the “IN SERV.” position. Open bypass, if used. Open water supply valve to approximately one-quarter of its maximum flow position to allow water to flow slowly into the mineral tank. When flow stops, TURN OFF WATER SUPPLY . Turn the control knob to backwash position and slowly turn on the water supply until the valve is open to its maximum position. Let the water go to drain until it becomes clear. Turn control to service position.Plug the electrical cord into a receptacle. DO NOT plug into an outlet controlled by a wall switch or pull chain that could be inadvertently turned off. Look in sight hole in back of the motor to see that the motor is running.1340 Manheim Pike • Lancaster, PA 17601-3196 • Phone 717-397-3521 • Fax 717-392-0266 •E-mail:**********************A DIVISION OF C-B TOOL CO.PROBLEMPOSSIBLE CAUSESOLUTION1. Filter fails to backwash:a. Electrical service to unit has been interrupted.b. Timer is defective.c. Power failure.a. Assure permanent electrical service.b. Replace timer.c. Reset time of day.2. Filter “bleeds” iron:a. Bypass valve is open.b. Excessive water usage.c. Hot water tank rusty.d. Defective or stripped filter media bed.e. Inadequate backwash flow rate.f. Leak at distributor tube.g. Internal valve leak. a. Close bypass valve.b. Reduce days between backwashing (see timer instructions). Make sure that there is not a leaking valve in the toilets/sinks.c. Repeated flushing of the hot water tank is required.d. Replace bed.e. Make sure filter has correct drain flow control. Be sure flow control is not clogged or drain line restricted. Be sure water pressure has not dropped.f. Make sure distributor tube is not cracked. Check O-Ring and tube pilot.g. Replace seals and spacer and/or piston.3. Loss of water pressure:a. Iron or turbidity buildup in water filter.b. Inlet of control plugged by foreign material. a. Reduce days between backwashing so filter back- washes more often. Note: Make sure filter is sized large enough to handle water usage.b. Remove piston and clean control.4. Drain flows continuously: a. Foreign material in control valve.b. Internal control leak.c. Control valve jammed in rinse or backwash.d. Timer motor stopped or jammed. a. Advance control through various regeneration positions. Remove foreign material in control.b. Replace seals and/or piston assy.c. Replace piston, seals and spacers.d. Replace timer.TROUBLE SHOOTING—SERVICE INSTRUCTIONS06/10。

IBM Engineering Systems Design Rhapsody 工具包说明书

IBM Engineering Systems Design Rhapsody Kit for DO-178B/CPlease first read document"Rhapsody Kit for DO-178B-C Overview.pdf".It describes the content of the "IBM Engineering Systems Design Rhapsody Kit for DO-178B/C".Version 1.14License AgreementNo part of this publication may be reproduced, transmitted, stored in a retrieval system, nor translated into any human or computer language, in any form or by any means, electronic, mechanical, magnetic, optical, chemical, manual or otherwise, without the prior written permission of the copyright owner, BTC Embedded Systems AG.The information in this publication is subject to change without notice, and BTC Embedded Systems AG assumes no responsibility for any errors which may appear herein. No warranties, either expressed or implied, are made regarding Rhapsody software including documentation and its fitness for any particular purpose.TrademarksIBM® Engineering Systems Design Rhapsody®, IBM® Engineering Systems Design Rhapsody® ‐ Automatic Test Generation Add On, and IBM® Engineering Systems Design Rhapsody® ‐ TestConductor Add On are registered trademarks of IBM Corporation.All other product or company names mentioned herein may be trademarks or registered trademarks of their respective owners.© Copyright 2000-2020 BTC Embedded Systems AG. All rights reserved.。

林肯电气(Lincoln Electric)机械组装说明书

1 XX

1 FEED PLATE

0744-000-178R

1 XX

2 FIXING ARM COMPL.

0646-233-015R

1 XX

3 AXIS DRIVE ROLL L

0646-233-039R

1 XX

Spare Parts - Electrical Schematic

2

Spare Parts - Electrical Schematic

ASSEMBLY PAGE NAME

CODE NO.: 50215 50216

K NO.: K10406 K10407

FIGURE NO.: LINC FEED 37 LINC FEED 38

A

B

1

1

2

2

39 38 37 36 33 10

12

11 9

2

7

6

5

8

1

4

27

3

28

16 13

17 34 35

18 19 15

14

15 20

22

25

26 21

29

30 31 3

32

24 23

Figure A

Figure A: Machine Assembly

Item Description

Part Number

QTY 1 2 3 4 5 6 7

1 FRONT PANEL

R-3019-016-1/08R

1 XX

1 XX

1 XX 1 XX 3 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX 1 XX

ACCA-P2知识要点汇总

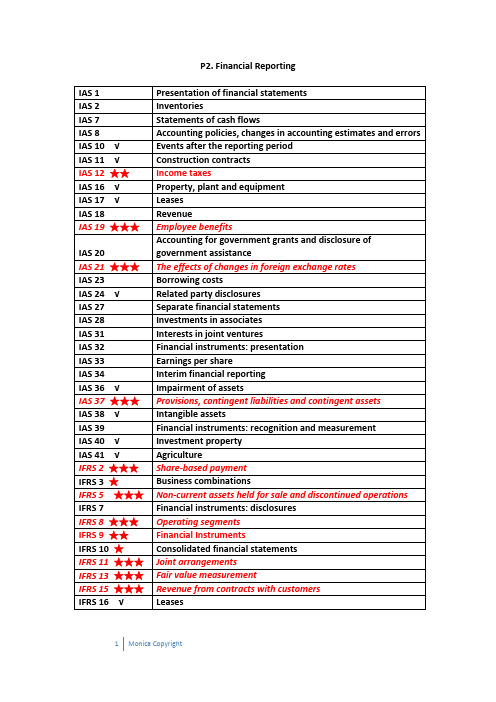

P2. Financial ReportingIAS 1 Presentation of financial statementsIAS 2 InventoriesIAS 7 Statements of cash flowsIAS 8 Accounting policies, changes in accounting estimates and errors IAS 10 √ Events after the reporting periodIAS 11 √ Construction contractsIAS 12 ★★ Income taxesIAS 16 √ Property, plant and equipmentIAS 17 √ LeasesIAS 18 RevenueIAS 19 ★★★ Employee benefitsIAS 20 Accounting for government grants and disclosure of government assistanceIAS 21 ★★★ The effects of changes in foreign exchange ratesIAS 23 Borrowing costsIAS 24 √ Related party disclosuresIAS 27 Separate financial statementsIAS 28 Investments in associatesIAS 31 Interests in joint venturesIAS 32 Financial instruments: presentationIAS 33 Earnings per shareIAS 34 Interim financial reportingIAS 36 √ Impairment of assetsIAS 37 ★★★ Provisions, contingent liabilities and contingent assetsIAS 38 √ Intangible assetsIAS 39 Financial instruments: recognition and measurementIAS 40 √ Investment propertyIAS 41 √ AgricultureIFRS 2 ★★★ Share‐based paymentIFRS 3 ★ Business combinationsIFRS 5 ★★★ Non‐current assets held for sale and discontinued operations IFRS 7 Financial instruments: disclosuresIFRS 8 ★★★ Operating segmentsIFRS 9 ★★ Financial InstrumentsIFRS 10 ★ Consolidated financial statementsIFRS 11 ★★★ Joint arrangementsIFRS 13 ★★★ Fair value measurementIFRS 15 ★★★ Revenue from contracts with customersIFRS 16 √ Leases不考or非重点:IAS 26 * Accounting and reporting by retirement benefit plans IAS 29 * Financial reporting in hyperinflationary economiesIAS 30 * Disclosure in the financial statements of banks and similar financial institutions (not examinable)IFRS 1* First time adoption of International Financial Reporting StandardsIFRS 4 * Insurance contractsIFRS 6 * Exploration for and evaluation of mineral resourcesIFRS 12* Disclosures of interests in other entitiesIFRS 14* Regulatory deferral accountsPart 1.The IASB’s Conceptual Framework for Financial Reporting1.财报的目的:The objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors, lenders and other creditors in making decisions about providing resources to the entity. Those decisions involve buying, selling or holding equity and debt instruments, and providing or settling loans and other forms of credit.2.财报提供的信息:General purpose financial reports do not and cannot provide all of the information,需要结合其他信息,譬如整个经济环境和预期,政治风向和事件,行业及公司展望等。

2010_HUNTSMAN 产品

Equivalent Weight

135 135

128 131 131 135

135 135 139

Viscosity (cps) @ 25°C

190 180

25 50 70 250

700 800 2000

Description

Standard Polymeric MDI. Low Acidity Polymeric Optimal for Controlled System Reactivity.

32.8

128

15

Hale Waihona Puke Pure MDI with a Higher 2,4' Isomer Content with Slight Yellow Appearance.

2.05

1.22

33.3

126

15

Pure MDI with a Higher 2, 4’ Isomer Content for Controlled Reactivity and Improved Flexibility.

2.05

1.10

12.3

341

1200

Low NCO Designed for Softer Polyurea Coatings, Contains PC.

2.00

1.14

15.2

276

370

2,4' MDI Containing Prepolymer for Slightly Slower Reactivity for Improved Surface Appearance.

Formulation and Technical Assistance For those developments requiring an additional “set of eyes” to get the desired results, an expert team of chemists is available to consult with. They have the ability to provide suggestions in the form of starting points for particular applications or to help get through specific formulation-related issues.

Effects of heat treatments on the microstructure and mechanical properties of a 6061 aluminium alloy