2006 Income statement

四大财务报表中英文对照

四大财务报表中英文对照全文共四篇示例,供读者参考第一篇示例:四大财务报表是每家公司每年都要制作的重要财务文件,它们记录着公司在一定期间内的财务业绩和资产负债状况。

这四大财务报表分别是资产负债表(Balance Sheet)、损益表(Income Statement)、现金流量表(Cash Flow Statement)和股东权益变动表(Statement of Changes in Equity)。

下面将为您详细介绍这四大财务报表的中英文对照。

一、资产负债表(Balance Sheet)资产负债表是衡量公司财务状况的重要指标,它展示了公司在特定日期的资产、负债和所有者权益的情况。

资产负债表的中英文对照如下:中文:资产负债表英文:Balance Sheet资产(Assets):1. 流动资产(Current Assets)2. 非流动资产(Non-current Assets)负债和所有者权益(Liabilities and Equity):1. 流动负债(Current Liabilities)2. 非流动负债(Non-current Liabilities)3. 所有者权益(Equity)资产负债表将公司的资产按照流动性和长期性分类,并将公司的负债和所有者权益细分为流动负债、非流动负债和所有者权益,以展示公司的资产负债结构。

二、损益表(Income Statement)损益表是公司在一定期间内的收入、成本和利润情况的总结,展示了公司的盈利能力。

损益表的中英文对照如下:中文:损益表英文:Income Statement收入(Revenue):1. 销售收入(Sales Revenue)2. 其他收入(Other Revenue)成本(Expenses):1. 销售成本(Cost of Goods Sold)2. 营业费用(Operating Expenses)3. 税前利润(Profit Before Tax)利润(Profit):1. 税后利润(Net Profit)损益表记录了公司在一段时间内的总收入、总成本和净利润,帮助投资者和管理层了解公司的盈利能力。

Income statement(利润表英文版)

项 一、主营业务收入

目

ITEMS Ⅰ. Revenue from main operations Including: Revenue from export operations Less: Cost of main operations Including: Cost of export operations Taxes and surcharge for main operations Ⅱ. Profit/Loss from main operations Add: Profit/Loss from other operations Less: Operating expenses General and administrative expenses Financial expenses

Ⅲ. Operating profit/loss Add: Investment income/losses Revenue from subsidies Non-operating revenue Less: Non-operating expenditures Ⅳ. Income/Loss before tax Less: Income tax Minority loss or profit Loss from investment not yet recognised Ⅴ. Net income/loss

1

上年同期累计数 Prior year actual

本年累计数 Current year cumulative

1、出售、处置部门或被投资单位所得收益 2、自然灾害发生的损失 3、会计政策变更增加(或减少)利润总额 4、会计估计变更增加(或减少)利润总额 5、债务重组损失 6、其他

财务报表英文术语

Prepaid and ddferrsd exchange profit

底他负值含计

Total other liabilities

負債合计

Total liabilities

所有者枳益

Investor's equity

资本慈颗(貨币名称及金粒〉Authorized capital)

实收资本(外币金額期末数>

5成入固定贤产元;

6•本年支付的进口环节噸金

Not es:

1.Maierials processed on commission ;

2.Goods in consignment

3.Good hlad in our custod ;

4.Ck>ntingemt Uadilty Incurred by discounted notes recaivabla

6Jmport tas baid this year ¥;

7-Bal: Balance: B.;Y Baginning of Yfear:E^P:End of period

8_* Monetary unit and amount女Amo uni of foreign currency at end of por

产从帯信利润

Profit on sales

如其他业务利润

Add: profit from olh&r operations

营业利润

Operating profit

加!投资收益

Add: Income on investment

加:营业外枚入

Add: Non-oporatlng Income

浦:营业外支出ຫໍສະໝຸດ 4_ih企业魚责的应收奈据贴现 5一稲入囚定黄产元;

incomes statement损益表

损益表(Income Statement)整备成本setup costs任何与零件或原料相关的成本。

整备成本包括在设置装配期间之新设备的成本、劳工的配置及用以测试新装配设施之产出(output)是否符合要求的零件或原料的成本。

这算是一种“生产准备就绪”(make ready to produce)的成本。

变动成本variable cost在会计方法上,直接因反应事业活动变化而变动的费用。

例如,原料成本会随着产品生产单位的数量变化而增减。

总变动成本会随着所生产的产品单位数增加而上升。

每单位产品的变动成本则维持不变。

总务及行政费用general and administrative expenses所有一般及行政活动相关之费用。

一般及行政费用包括下列数项:法规及稽核相关费用、办公室一般支出、办公室租金支出、办公室之水电支出及办公室设备支出及折旧。

以上项目出现在会计损益表之营运支出上。

毛利gross profit销售总额减销货成本(cost of goods sold)。

当毛利用百分比表达时,计算方式是用毛利除以销售总额,亦称之为毛利率。

损益表incomes statement用以决定公司净收益(net income)的正式报表,也被称为获利亏损表(profit and loss statement)。

每一家公司在其年报(annual report)中一定要把损益表包括进去。

损益表通常包含以下项目:销售额减:销货成本毛利润减:营运费用、销售费用,以及一般行政支出得自营运收益加:其他收益减:其他费用税前收益减:所得税提列准备持续营运收益非持续营运收益之收入或损失(税后)非常项目或累计效果扣除前之收益加或减:非常项目(税后)加或减:会计原则改变之累计效果(税后)净收益大多数的公司并没有完全依照这样的格式,如下表是惠普公司(Hewlett-Packard Company)1997年度的损益表:换句话说,与生产红球的原料有关之增额成本为2OOO美元。

Income Statement

1

Section Income Statement

Part 1 Workplace Spoken English

1. Follow the Samples

A:What is the income statement? B:It is also sometimes referred to as profit and loss statement. The

————————————————————————————————————

3. Why don’t some businesses select to use a fiscal year which ends December, 31?

————————————————————————————————————

9. subtotal ['sʌbtəʊtl]

n.

10. significant [sɪg'nɪfɪkənt]

a.

11. allowance [ə'laʊəns] n.

12. retail ['riːteɪl]

v.

13. complex ['kɒmpleks] a.

一致,符合 清淡的,不忙碌的 减去,扣掉 小计

重要的,有含义的 销售折让 零售 复杂的

Section Income Statement

7

Part 2 Intensive Reading

Income Statement

New Words and Special Terms

14. raw [rɔː]

a.

15. material [mətɪrɪəl]

大概 经营业绩 经营成果

income statement-明细

3 Administration cost

4 Furnishings &Equipment 5 Contingency

6 教师薪酬及保险

7 室内装修 8 水电、取暖 9 网络通信 10 交通工具 11 税金(各种) 12 总计

1 Sitework 2 General constraction

7,490,000.00 二、三、四期 200,000.00

8,940,000.00 880,000.00 250,000.00 410,000.00

10,680,000.00

Hale Waihona Puke 1.学校用地需要购买or租赁?为何没有体现? 2.Administration cost 一期费用为何大于后三期 3.第一期和第二、三、四期间隔多久?一年? 4.当地规定有哪些涉税项?税种和税率需要明

二、三、四期

如:承担应用开 发、研究课题、 培训公司雇员等

如:场地租赁、 设备租赁

总计

-

体现? 2.Administration cost 一期费用为何大于后三期总和? 久?一年? 4.当地规定有哪些涉税项?税种和税率需要明确。

支出 一期

备注 是否包括室内装修? 为何一期费用大于后几期?

若未包含在 第2项

明细 学费 政府资助与拨款

销售与服务

社会捐赠 收入 私人捐赠 经营收入

收入 一期 金额

备注

如:承担应用开 发、研究课题、 培训公司雇员等

如:场地租赁、 设备租赁

、三、四期

总计

-

学费 政府资助与拨款

销售与服务

社会捐赠 收入 私人捐赠 经营收入

mbafa《financialaccounting》习题答案9

mbafa《financialaccounting》习题答案9CHAPTER 9LONG-LIVED ASSETSBRIEF EXERCISESBE9–1a. The new method, straight-line depreciation, will increase net income in the early years andreduce income in the later years versus using an accelerated method. An accelerated method of depreciation increases the depreciation charges in the early years of the life of an asset and reduces the depreciation charges in the later years.b. Allegheny may have decided that it wanted depreciation charges to be spread evenly over thelife of an asset so that the impact on net income in any one reporting period was less. It may also feel that it will make its financial statements easier to compare with its competitors.During periods of high fixed asset investment Allegheny’s results may look unfavorable versus other companies that use a straight-line method instead of an accelerated method.c. In the annual report one could look through footnote #1. This footnote typically highlights all ofthe significant accounting policies and methods used by the company to prepare the financial statements.BE9–2a. The recognition of depreciation and amortization affects the basic accounting equation byreducing assets and reducing retained earnings in the stockholders’ equity section. Fixed assets such as property, plant and equipment are reduced through depreciation charges(which are collected in the contra asset account Accumulated Depreciation) which lower net income.Intangible assets are reduced by amortization charges which reduce the net income of the company. This reduction in net income reduces the retained earnings of the company.b. Boeing recognized a gain of $117 million, computed as follows:Accumulated depreciation 2002 $12,719 million+ Depreciation charges for 2003 1,005 million– Accumulated depreciation 2003 12,963 millionAccumulated depreciation on assets sold $ 761 millionPP&E 2002 $21,484 million+ PP&E purchases for 2003 741 million– PP&E 2003 21,395 millionPP&E sold $ 830 million1Derived Journal Entry:Cash (+A) 186Accumulated Depreciation (+A) 761Property, Plant & Equipment (-A) 830Gain on Sale (R, +SE) 117The gain on the sale of property, plant and equipment would be shown in the income state ment, usually in an “other gains and losses” section. These transactions would affect the statement of cash flows in the “funds from investing activities section”. Any sales would be a source of funds in the amount of cash received.BE9–3a. Johnson and Johnson invested $122 million ($594– $472) of land during 2003.b. Accumulated depreciation increased during 2003 because of depreciation expense taken byJohnson and Johnson. Instead of reducing the asset account directly, depreciation expense is added to accumulated depreciation, which offsets the asset account to show its reduction in value.c. During 2003 Johnson and Johnson must have sold some assets that were classified in thefixed assets accounts. These accounts are carried at historical cost so that only the sale of an asset will reduce the account. Any gains or losses on the sale of these assets would be shown on the income statement. The change from 2002 ($14,314) to 2003 ($17,052) is $2,738. Since Johnson & Johnson spent $5,074 on fixed assets, then $2,336 ($5,074 - $2,738) must have been sold.d. Johnson and Johnson would show $9,846 million for property, plant and equipment on itsfinancial statement for 2003. The gross amount and the accumulated depreciation would be disclosed in the footnote.EXERCISESE9–1a. Lowery, Inc., should capitalize all costs associated with getting the equipment in a serviceablecondition and location. These costs would be the actual purchase price of $920,000, the transportation cost of $62,000, and the insurance cost of $10,000. Therefore, the total cost of the equipment is $992,000.b. The depreciation base equals the dollar amount of a fixed asset's cost that the company doesnot expect to recover over the asset's useful life, but instead expects to consume over the asset's useful life. Since the plantequipment's total cost is $992,000 and since Lowery, Inc., expects to sell the equipment for $50,000 at the end of its useful life, Lowery, Inc., does not expect to recover $942,000 of the asset's cost. Therefore, the depreciation base equals $942,000. The depreciation base always equals the capitalized cost of a fixed asset less its estimated salvage value.c. The amount that will be depreciated over the life of the plant equipment is its depreciation base.The depreciation base equals the amount of the equipment's future benefits that the company will consume. The outflow of future benefits are expenses, in this case depreciation expense.Therefore, the total amount that Lowery, Inc., will depreciate over the equipment's useful life is $942,000.E9–2Lot 1 Lot 2 Lot 3 Lot 4Revenue $ 160,000 $ 120,000 $ 60,000 $ 60,000Expenses 128,000* 96,000* 48,000* 48,000*Net income $ 32,000 $ 24,000 $ 12,000 $ 12,000_______________* Expenses were calculated as follows:1. Calculate total market value.Total Market value = $160,000 + $120,000 + $60,000 + $60,000 = $400,0002. Allocate costs to each lot based upon relative market values.Lot 1 = $320,000 × (160,000/400,000) = $128,000Lot 2 = $320,000 × (120,000/400,000) = $ 96,000Lot 3 = $320,000 × (60,000/400,000) = $ 48,000Lot 4 = $320,000 × (60,000/400000) = $ 48,000E9–3a. All costs that are necessary and reasonable to get an asset ready for its intended use should becapitalized as part of the cost of that asset. In the case of property, plant, and equipment, "ready for its intended use" means that the asset is in a serviceable condition and location.LandItem Land Improvements Building Tract of land $90,000Demolition of warehouse 10,000Scrap from warehouse (7,000)Construction of building $140,000Driveway and parking lot $32,000Permanent landscaping 4,000Total $ 97,000 $32,000 $140,000b. Land:Since land is assumed to have an indefinite life, it is never depreciated.Land Improvements:Depreciation Expense—Land Improvements (E, –SE)................... 1,600 Accumulated Depreciation—Land Improvements (–A)............... 1,600 Depreciated land improvements.Building:Depreciation Expense—Building (E, –SE)....................................... 7,000 Accumulated Depreciation—Building (–A).................................. 7,000 Depreciated building.E9–4a. Maintenanceb. Maintenancec. Maintenanced. Bettermente. Maintenancef. Maintenanceg. Bettermenth. Maintenancei. BettermentNote:The classification of these expenditures can be quite subjective. Some accountants might very well classify some of these expenditures differently. For example, one might argue that the cost of the muffler in (h) is actually a betterment expenditure if the reduced noise allows workers to work more efficiently, thereby increasing the productive capacity of the machine.E9–5a. (1) Expensed immediately:Income Statement2008 2007 2006 Revenues $ 65,000 $ 65,000 $ 65,000Amortization 0 0 (40,000)Other expenses (20,000) (20,000) (20,000)Net income $ 45,000 $ 45,000 $ 5,000Balance Sheet12/31/08 12/31/07 12/31/06 AssetsCurrent assets $ 135,000 $ 90,000 $ 45,000Long-lived assets(including land) 50,000 50,000 50,000Total assets $ 185,000 $ 140,000 $ 95,000Liabilities and Stockholders' EquityLiabilities $ 35,000 $ 35,000 $ 35,000Stockholders' equity 150,000 105,000 60,000Total liabilities & stockholders'equity $ 185,000 $ 140,000 $ 95,000E9–5 Continued(2) Amortized over two years:Income Statement2008 2007 2006 Revenues $ 65,000 $ 65,000 $ 65,000 Amortization 0 20,000 20,000Other expenses 20,000 20,000 20,000Net income $ 45,000 $ 25,000 $ 25,000Balance Sheet12/31/08 12/31/07 12/31/06 AssetsCurrent assets $ 135,000 $ 90,000 $ 45,000Long-lived assets (includingland) 50,000 50,000 70,000Total assets $ 185,000 $ 140,000 $ 115,000 Liabilities and Stockholders' EquityLiabilities $ 35,000 $ 35,000 $ 35,000 Stockholders' equity 150,000 105,000 80,000Total liabilities & stockholders'equity $ 185,000 $ 140,000 $ 115,000(3) Amortized over three years:Income Statement2008 2007 2006 Revenues $ 65,000 $ 65,000 $ 65,000 Amortization 13,334 13,333 13,333Other expenses 20,000 20,000 20,000Net income $ 31,666 $ 31,667 $ 31,667Balance Sheet12/31/08 12/31/07 12/31/06 AssetsCurrent assets $ 135,000 $ 90,000 $ 45,000Long-lived assets (includingland) 50,000 63,334 76,667Total assets $ 185,000 $ 153,334 $ 121,667 Liabilities and Stockholders' EquityLiabilities $ 35,000 $ 35,000 $ 35,000Stockholders' equity 150,000 118,334 86,667Total liabilities & stockholders'equity $ 185,000 $ 153,334 $ 121,667b. 2008 2007 2006 TotalMethod 1: $45,000 $45,000 $ 5,000 $95,000 Method 2: 45,000 25,000 25,000 95,000 Method 3: 31,666 31,667 31,667 95,000E9–5 Concludedc. The balance sheets under all three methods report identical amounts for each balance sheetaccount. Since the asset was fully amortized by December 31, 2008, the method used to amortize the asset does not affect the amounts reported on the balance sheet as of December 31, 2008.E9–6a. andb.Stork Freight CompanyIncome StatementFor the Year Ended December 3112-Year Useful Life 6-Year Useful Life Revenues $ 50,000,000 $ 50,000,000 Expenses:Operating expenses $ 25,000,000 $ 25,000,000 Depreciation expense 1,250,000 2,500,000 Total expenses 26,250,000 27,500,000 Net income $ 23,750,000 $ 22,500,000 The percentage decrease in net income would be approximately 5.26% [($22,500,000 – $23,750,000) ÷ $23,750,000].c.12-Year Useful Life 6-Year Useful Life Net income $ 23,750,000 $ 22,500,000Dividend payout percentage 30% 30%Dividends $ 7,125,000 $ 6,750,000The difference in dividends due simply to using different estimated useful lives for the planes would be $375,000 ($7,125,000 – $6,750,000).E9–7a. An asset's book value equals the asset's initial capitalized value less the associatedaccumulated depreciation. With straight-line depreciation, accumulated depreciation equals depreciation expense per year times the number of years the asset has been used. Therefore, the asset's book value would be calculated as follows: Depreciation expense per year = (Cost –Salvage Value) ÷ Useful Life= ($60,000 –$12,000) ÷ 5 years= $9,600 per yearBook Value = Capitalized Cost – Accumulated Depreciation = $60,000 –($9,600 × 3 years)= $31,200E9–7 Concludedb. Depreciation Expense = [(Cost –Accumulated Depreciation) –Salvage Value] ÷Remaining Useful Life= (Book value –Salvage value) ÷ Remaining useful li fe= ($31,200 –$12,000) ÷ 5 remaining years= $3,840Depreciation Expense (E, –SE)....................................................... 3,840 Accumulated Depreciation (–A)................................................. 3,840 Depreciated asset for 2005.E9–8Straight- Double-Declining- ActivityObjective Line Balance Method(a) x1x1x1(b) x x x(c) x x2(d) x(e) x(f) x(g) x x3(h) x x x1Under certain conditions, all three methods could meet this objective. However, for the straight-line method and the double-declining-balance method, this objective will be met only by chance.The activity method will always meet this objective because depreciation is based upon the actual use of the asset.2It is possible that the activity method would generate the largest net income in the last year of an asset's useful life. However, this result would be due to the company's use patterns of the asset and would not be due to the depreciation method per se.3See note (2). The same rationale would hold in this case too.E9–9a. (1) Straight-line depreciation:Depreciation per Year = (Cost –Salvage Value) ÷ Useful Life = ($300,000 –$60,000) ÷ 4 years= $60,000 per year for 2005, 2006, 2007, and 2008E9–9 Concluded(2) Double-declining-balance depreciation:Depreciation Depreciation Accumulated Book Date Factor Expense Cost Depreciation Value1/1/05 $300,000 $ 0 $300,00012/31/05 50% $150,000a300,000 150,000 150,00012/31/06 50% 75,000 300,000 225,000 75,00012/31/07 50% 15,000b300,000 240,000 60,00012/31/08 50% 0 300,000 240,000 60,000 ______________a Depreciation Expense = Book Value at Beginning of the Period × Depreciation Factorb Book Value ×Depreciation Factor = $75,000 ×50% = $37,500. If Benick Industriesdepreciated $37,500 in 2007, the asset's book value would drop below its salvage value. To prevent this from happening, depreciation expense for 2007 can be only $15,000.b. A manager should consider the costs and benefits associated with each depreciation method.The most likely benefit is the impact of depreciation methods on income taxes. An accelerated method decreases the present value of tax payments. However, since there is no requirement that a company use the same depreciation method for financial reporting purposes as it does for tax reporting, tax considerations are not an issue for financial reporting. A manager should also consider the bookkeeping costs associated with each method. However, with computers the bookkeeping costs should be relatively consistent across methods. Finally, since the choice of depreciation methods affects net income, managers might consider the impact of the different depreciation methods on contracts such as debt covenants and incentive compensation contracts. Comparability with other in the same industry may also be a factor.E9–10a. Computer System (+A)....................................................................335,000Cash (–A)........................................................................... 335,000 Purchased computer system.Note: Capitalizing the $10,000 of training costs could be debated. But, without incurring these costs, the computer system would not be in a serviceable condition. Hence, thetraining costs meet the requirement to be capitalized as part of the fixed asset.b. (1) Straight-line depreciation:Depreciation per Year = (Cost –Salvage Value) ÷ Useful Life = ($335,000 –$70,000) ÷ 5 years= $53,000 per year for 2005, 2006, 2007, 2008, and 2009E9–10 Concluded(2) Double-declining-balance depreciation:Depreciation Depreciation Accumulated Book Date Factor Expense Cost Depreciation Value1/1/05 $335,000 $ 0 $335,00012/31/05 40% $134,000a335,000 134,000 201,00012/31/06 40% 80,400 335,000 214,400 120,60012/31/07 40% 48,240 335,000 262,640 72,36012/31/08 40% 2,360b335,000 265,000 70,00012/31/09 40% 0 335,000_____________a Depreciation expense = Book value at beginning of the period×Depreciation factorb Book value ×Depreciation factor = $72,360 ×40% = $28,944. If Stockton Corporationdepreciated $28,944 in 2008, the asset's book value would drop below its salvage value. To prevent this from happening, depreciation expense for 2008 can be only $2,360.c. Depreciation Expense (E, –SE)................................................. 134,000Accumulated Depreciation (–A)......................................... 134,000 Depreciated fixed asset for 2005.E9–111. Activity Method:Depreciation Expense per Mile = ($100,000 –$20,000) ÷ 200,000 Miles= $0.4/MileDepreciation Expense (E, –SE)....................................................... 19,200 Accumulated Depreciation (–A)................................................. 19,200 Depreciated asset for 2005.Depreciation Expense (E, –SE)....................................................... 14,000 Accumulated Depreciation (–A)................................................. 14,000 Depreciated asset for 2006.Depreciation Expense (E, –SE)....................................................... 16,000 Accumulated Depreciation (–A)................................................. 16,000 Depreciated asset for 2007.Depreciation Expense (E, –SE)....................................................... 10,000 Accumulated Depreciation (–A)................................................. 10,000 Depreciated asset for 2008.E9–11 ConcludedDepreciation Expense (E, –SE)....................................................... 14,000Accumulated Depreciation (–A)................................................. 14,000 Depreciated asset for 2009.Depreciation Expense (E, –SE)....................................................... 4,000 Accumulated Depreciation (–A)................................................. 4,000 Depreciated asset for 2010.Cash (+A) .........................................................................................12,000Accumulated Depreciation (+A)....................................................... 77,200Loss on Sale of Truck (Lo, –SE)...................................................... 10,800 Truck (–A)................................................................................... 100,000 Sold truck.2. Straight-line Method:Depreciation Expense per Year = ($100,000 –$20,000) ÷ 5 Years= $16,000/yearDepreciation Expense (E, –SE)....................................................... 16,000 Accumulated Depreciation (–A)................................................. 16,000 Depreciated asset.Note:This entry would be made each year for five years. No entry would be made in Year 6 since the truck's estimated useful life ended at the end of Year 5, which means that the truck would have been depreciated down to its estimated salvage value.Cash (+A) ....................................................................................... 12,000Accumulated Depreciation (+A)....................................................... 80,000Loss on Sale of Truck (Lo, –SE)...................................................... 8,000 Truck (–A)................................................................................. 100,000 Sold truck.E9–12a. Depletion (E, –SE)............................................................................ 1,200,000*Oil Deposits (–A)........................................................................ 1,200,000 Depleted oil deposits.___________* $1,200,000 = ($4,000,000 ÷ 100,000 barrels)×30,000 barrels extractedb. Depletion (E, –SE)............................................................................ 2,000,000*Oil Deposits (–A)........................................................................ 2,000,000 Depleted oil deposits.___________* $2,000,000 = ($4,000,000 ÷ 100,000 barrels)×50,000 barrels extractedc. $800,000E9–13a.Depreciation Expense Correct Annual Cumulative Year Per Company's Books Depr. Exp. Difference Difference2005 $120,000 $25,000 $95,000 $95,0002006 0 25,000 (25,000) 70,0002007 0 25,000 (25,000) 45,0002008 0 25,000 (25,000) 20,000b. After adjusting entries are prepared and posted on December 31, 2007, AccumulatedDepreciation will be understated by $75,000.c. After adjusting entries, but before closing entries have been prepared and posted on December31, 2007, Retained Earnings will be understated by $70,000.d. After both adjusting and closing entries have been prepared and posted on December 31, 2007,Retained Earnings will be understated by $45,000.E9–14a. Cash (+A) .......................................................................................235,000Accumulated Depreciation—Office Equipment (+A)....................... 300,000 Office Equipment (–A)............................................................... 500,000 Gain on Sale of Fixed Assets (Ga, +SE)................................... 35,000 Sold office equipment.b. Cash (+A) ......................................................................................... 185,000Accumulated Depreciation—Office Equipment (+A)....................... 300,000Loss on Sale of Fixed Assets (Lo, –SE)........................................... 15,000 Office Equipment (–A)............................................................... 500,000 Sold office equipment.E9–15Assuming that Paris Company kept the equipment for its entire five-year estimated useful life, the depreciation schedule on the equipment would be as follows.Depreciation Depreciation Accumulated Book Date Factor Expense Cost Depreciation Value1/1/03 $25,000 $ 0 $25,00012/31/03 40% $10,000 25,000 10,000 15,00012/31/04 40% 6,000 25,000 16,000 9,00012/31/05 40% 3,600 25,000 19,600 5,40012/31/06 40% 400* 25,000 20,000 5,00012/31/07 40% 0 25,000 20,000 5,000__________________* Because the equipment's book value cannot drop below its estimated salvage value, depreciation expense for 2006 cannot exceed $400.a. Accumulated Depreciation—Equipment (+A).................................. 19,600Loss on Disposal of Equipment (Lo, –SE)....................................... 5,400 Equipment (–A).......................................................................... 25,000 Disposed of equipment.b. Accumulated Depreciation—Equipment (+A).................................. 20,000Loss on Disposal of Equipment (Lo, –SE)....................................... 5,000 Equipment (-A)........................................................................... 25,000 Disposed of equipment.c. Cash (+A) ....................................................................................... 8,000Accumulated Depreciation—Equipment (+A).................................. 19,600 Equipment (–A).......................................................................... 25,000 Gain on Sale of Fixed Assets (Ga, +SE)................................... 2,600 Sold equipment.d. Fixed Asset (new) (+A).................................................................... 30,000Accumulated Depreciation—Equipment (+A).................................. 20,000Loss on Disposal of Fixed Asset (Lo, –SE)...................................... 3,000 Cash (–A)................................................................................... 28,000 Equipment (old) (–A).................................................................. 25,000 Exchanged fixed assets.E9–16a. andb. First, let us compute the original cost of the equipment that was sold in 2005 asfollows:Equipment Equipment Equipment Equipmentat the End + Purchased – sold during = at the Endof 2004 during 2005 2005 of 2005$32,700 + $12,000 – X = $37,500X = $7,200Now, let us compute the related accumulated depreciation for the equipment sold during 2005 as follows:Accumulated Depreciation Exp. Accumulated Accumulated Depreciation at + for 2005 – Depreciation = Depreciationthe End of 2004 for the Sold at the EndEquipment of 2005during 2005$14,300 + $7,200 – X = $17,600X = $ 3,900 Now, we can reconstruct the journal entry.Cash.................................................................................................5,400*Accumulated Depreciation............................................................... 3,900 Equipment.................................................................................. 7,200 Gain on Sale of Equipment........................................................ 2,100 ___________* $7,200 + $2,100 – $3,900 = $5,400E9–17Account Financial Statementa. Property, plant & equipment Balance SheetLess: accumulated depreciation Balance SheetDepreciation expense Income StatementInvestments in property, plant & equipment Statement of Cash Flowsb. Property, plant & equipment – 2002 $36,912Plus: investments in property, plant & equipment 3,656Less: property, plant & equipment – 2003 38,692Property, plant & equipment sold in 2003 $ 1,876c. Accumulated depreciation – 2002 $19,065Plus: depreciation expense – 2003 4,651Less: accumulated depreciation – 2003 22,031Accumulated depreciation – sold property $ 1,685E9–17 Concludedd. Compute the gain on the sale:Cost of property sold $1,876Less: accumulated depreciation 1,685Book value of property sold $ 191Sales price of property $100Less: book value of property 191Loss on sale of property $ 91This loss on sale of property would appear on the income statement.E9–18a. First, let us compute the related accumulated depreciation for the equipment sold during 2005as follows:Accumulated Depreciation Cap. Accumulated Accumulated Depreciation at + for 2005 – Depreciation = Depreciationthe End of 2004 for the Sold at the EndEquipment 0f 2005during 2005$9,800 + $3,800 – X = $10,500X = $ 3,100 Now, we can reconstruct the journal entry.Cash................................................................................................. 4,300 Loss on Sale of Equipment (900)Accumulated Depreciation............................................................... 3,100 Equipment.................................................................................. 8,300 b. Equipment Equipment Equipment Equipmentat the End + Purchased – sold during = at the Endof 2004 during 2005 2005 of 2005$23,400 + X – $8,300 = $26,900X = $11,800___________Equipment purchased during 2000 = $11,800E9–19a. Swift Corporation should capitalize these costs. Assets are defined as items that are expectedto provide future economic benefits to the entity. Organization costs are costs incurred by an entity prior to starting operations. Such costs include legal fees to incorporate and accountant's fees to set up an accounting system. Without incurring these costs, most companies could not be in business. Consequently, organization costs allow a company to be in business, thereby helping it to generate future benefits. Since these costs help in generating future benefits, they should most definitely be capitalized.b. Theoretically, organization costs should be amortized over their useful life. In the extreme,organization costs provide a benefit over the entire life of a company. Since under the going concern assumption accountants assume that entities will exist indefinitely, it would seem that organization costs should be amortized over an indefinite period. Since this position is not practical, the accounting profession has decided that organization costs should be amortized over a period not to exceed forty years.Assuming that Swift Corporation amortizes its organization costs over the maximum period of forty years, the appropriate adjusting journal entry for a single year would be as follows: Amortization Expense (E, –SE)........................................................1,125 Organization Costs (–A)............................................................. 1,125 Amortized organization costs.c. As mentioned in part (b), organization costs theoretically provide benefits over the entire life ofthe company. Under the going concern assumption, the company is assumed to exist indefinitely. If the company is assumed to exist indefinitely and if organization costs provide benefits over the entire life of the company, then these costs should provide an indefinite benefit. Consequently, organization costs should provide a benefit for an indefinite period of time, which implies that they should be reported as an asset (i.e., future benefit) indefinitely.But if organization costs are amortized, the asset will at some point in time have a zero balance, and the cost of the asset cannot be matched against the benefits the asset will help generate in the future. This situation contradicts the matching principle and the concept of an asset.d. A patent gives a company the exclusive right to use or market a particular product or process,thereby providing the company with an expected future benefit. Consequently, the costs incurred to acquire a patent should be capitalized as an asset and amortized over the patent's useful life. If Swift were to immediately expense the $65,000, the company would be implying that it did not expect to receive any benefits from the patent in the future. If this were the case, one would have to question why Swift purchased the patent in the first place.e. Research and development costs may or may not provide a company with future benefits. Thecompany will not know whether or not a particular R & D。

Incomestement利润表英文版.docx

利润Nov-11表 (Income statement)会外年企 02表单位:人民币元MONETARY UNIT:CNY行次本年金额上年金额项目一、主营业务收入其中:出口产品(商品)销售收入减:主营业务成本其中:出口产品(商品)销售成本主营业务税金及附加二、主营业务利润(亏损以“- ”号填列)加:其他业务利润(亏损以“- ”号填列)减:营业费用管理费用财务费用其中:利息支出(减利息收入)汇兑损失(减汇兑收益)三、营业利润(亏损以“ - ”号填列)加:投资收益(亏损以“ - ”号填列)补贴收入营业外收入减:营业外支出四、利润总额(亏损以“ - ”号填列)减:所得税*少数股东损益加:* 未确认的投资损失(以“ +”号填列)五、净利润(亏损以“ - ”号填列)ITEMSⅠ. Revenue from main operationsIncluding: Revenue from export operationsLess: Cost of main operationsIncluding: Cost of export operationsTaxes and surcharge for main operationsⅡ. Profit/Loss from main operationsAdd: Profit/Loss from otheroperations Less: Operating expensesGeneral and administrativeexpenses Financial expensesIncluding: Interest expenses ( Less interest income )Exchange loss ( Less exchange gain )Ⅲ. Operating profit/lossAdd: Investment income/lossesRevenue fromsubsidiesNon-operating revenueLess: Non-operating expendituresⅣ. Income/Loss beforetax Less: Income taxMinority loss or profitLoss from investment not yet recognisedⅤ. Net income/lossLine No.This year amount Amount last year12,141,103.86242,053,920.39561087,183.471114155,341.35154,384,383.33527,823.761667,788.58171818-4,520,329.79-527,823.761922232527-4,520,329.79-527,823.7628293031-4,520,329.79-527,823.76补充资料Supplementary information:项目上年同期累计数本年累计数ItemCurrent year cumulativePrior year actual1、出售、处置部门或被投资单位所得收益Gain on sale and disposal of a department or an invested enterprise2、自然灾害发生的损失Losses arising from natural disaters3、会计政策变更增加(或减少)利润总额Increase/decrease in income before tax due to a change in accounting policy4、会计估计变更增加(或减少)利润总额Increase/decrease in income before tax due to a change in accounting estimate5、债务重组损失Losses arising from debt restructurings6、其他Others1。

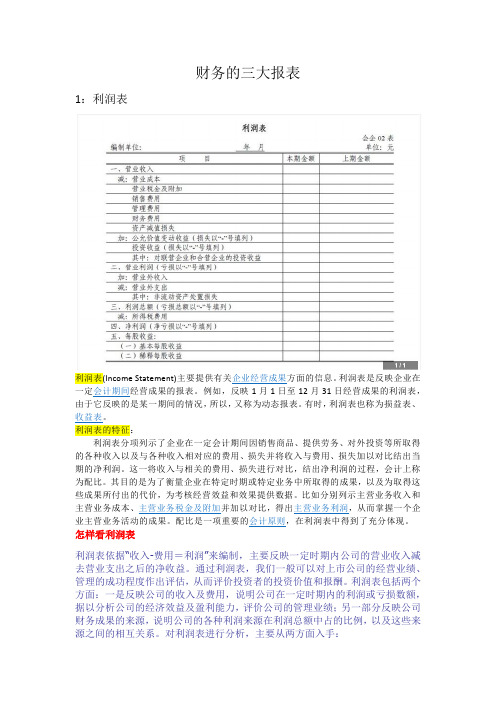

财务的三大报表

财务的三大报表1:利润表利润表(Income Statement)主要提供有关企业经营成果方面的信息。

利润表是反映企业在一定会计期间经营成果的报表。

例如,反映1月1日至12月31日经营成果的利润表,由于它反映的是某一期间的情况,所以,又称为动态报表。

有时,利润表也称为损益表、利润表分项列示了企业在一定会计期间因销售商品、提供劳务、对外投资等所取得的各种收入以及与各种收入相对应的费用、损失并将收入与费用、损失加以对比结出当期的净利润。

这一将收入与相关的费用、损失进行对比,结出净利润的过程,会计上称为配比。

其目的是为了衡量企业在特定时期或特定业务中所取得的成果,以及为取得这些成果所付出的代价,为考核经营效益和效果提供数据。

比如分别列示主营业务收入和主营业务成本、主营业务税金及附加并加以对比,得出主营业务利润,从而掌握一个企业主营业务活动的成果。

配比是一项重要的会计原则,在利润表中得到了充分体现。

怎样看利润表利润表依据“收入-费用=利润”来编制,主要反映一定时期内公司的营业收入减去营业支出之后的净收益。

通过利润表,我们一般可以对上市公司的经营业绩、管理的成功程度作出评估,从而评价投资者的投资价值和报酬。

利润表包括两个方面:一是反映公司的收入及费用,说明公司在一定时期内的利润或亏损数额,据以分析公司的经济效益及盈利能力,评价公司的管理业绩;另一部分反映公司财务成果的来源,说明公司的各种利润来源在利润总额中占的比例,以及这些来源之间的相互关系。

对利润表进行分析,主要从两方面入手:1.收入项目分析。

公司通过销售产品、提供劳务取得各项营业收入,也可以将资源提供给他人使用,获取租金与利息等营业外收入。

收入的增加,则意味着公司资产的增加或负债的减少。

记入收入账的包括当期收讫的现金收入,应收票据或应收账款,以实际收到的金额或账面价值入账。

2.费用项目分析。

费用是收入的扣除,费用的确认、扣除正确与否直接关系到公司的盈利。

MBA智库百科-损益表

损益表定义损益表(Income Statement)(或利润表)是用以反映公司在一定期间利润实现(或发生亏损)的财务报表。

它是一张动态报表。

损益表可以为报表的阅读者提供作出合理的经济决策所需要的有关资料, 可用来分析利润增减变化的原因, 公司的经营成本, 作出投资价值评价等。

损益表的项目,按利润构成和分配分为两个部分。

其利润构成部分先列示销售收入,然后减去销售成本得出销售利润;再减去各种费用后得出营业利润(或亏损);再加减营业外收入和支出后,即为利润(亏损)总额。

利润分配部分先将利润总额减去应交所得税后得出税后利润;其下即为按分配方案提取的公积金和应付利润;如有余额,即为未分配利润。

损益表中的利润分配部分如单独划出列示,则为“利润分配表”。

[编辑]制作损益表过程在财政年度末,所有帐目必须平帐。

所有帐目的余额都需放在试算表(Trial Balance)里。

会计师需根据簿记上的资料制作损益表和资产负债表,部分公司除制作这两个财务报表外,还会制作现金流量表和股东权益变动表。

公司会先计算公司的净销售和销货成本,得到这两个项目的数目后就可计算毛利(Gross Profit/Loss)。

将收入和支出的总和相减后就可计算纯利亏损(Net Income/Loss)。

以下会有几条重要公式:计算毛利(Gross Profit/Loss)的方法:∙毛利= 净销售(Net Sales) - 销货成本(Cost of Goods Sold)∙净销售= 销售(Sales) - 销货退回与折让(Sales Returns and Allowances)∙销货成本= 期初存货(BeginningInventory) + 购货(Purchases) - 购货退回与折让(Purchase Returns andAllowances) + 购货运费(Freight-Out/Delivery Expense) - 期末存货(Ending Inventory)计算纯利的方法:∙纯利= 所有收入(Revenue) - 所有支出(Expenses)[编辑]损益表的重要作用损益表上所反映的会计信息,可以用来评价一个企业的经营效率和经营成果,评估投资的价值和报酬,进而衡量一个企业在经营管理上的成功程度。

合并损益表(consolidatedincomestatement)

合并损益表(consolidatedincomestatement)亦称合并利润表。

企业集团中的母公司于年度终了编制的,用于反映整个企业集团在一定时期内同外界各方面进行交易所实现的经营成果的报表。

主要服务于母公司的股东和债权人。

在企业集团母、子公司内部除了内部往来项目,还存在着内部交易项目,如集团内部存货、固定资产的购销、内部债券的赎回等等。

这些交易所形成的未实现利润和未确认的利润要分别在合并损益表上予以抵消和确认,因为如果不抵消公司间的未实现利润,所编制的合并损益表和资产负债表不仅会使集团利用频繁的内部交易虚增利润,而且使合并会计报表失去了其真实反映企业集团经营成果和财务状况的作用。

同样,如果不确认已实现的损益,同样会歪曲整个企业集团的利润,也会对合并会计报表使用者产生误导。

所以,合并损益表的编制关键在于工作底稿上抵消分录了编制。

美国规定了编制合并损益表的一般做法:(1)公司间商品购销业务的抵销。

首先,应抵消公司间本期发生的全部内部销售成本。

这是为了避免母子公司之间对内部销售收入和销售成本的重复计算;其次,如果期末存货中存在公司间未实现利润,则应借记销售成本,以抵消损益表中所含的未实现利润,贷记存货,以抵消期末存货中所含的公司间未实现利润;再次,如果期初存货中存在公司间未实现利润,则一般假设存货中存在公司间未实现利润,则一般假设存货的本期已销到集团公司外部,即未实现利润在本期已得到实现,此时应借记长期股权投资,贷记销售成本,以调增利润,同时将长期股权投资调整到未发生内部交易的余额,在向上销售且存在少数股权情况下,调整长期股权投资数额仅等于属于母公司的部分。

(2)公司间固定资产购销业务的抵消。

首先,抵消内部固定资产购销中产生的未实现利润。

在固定资产内部交易的当期,应以未实现利润数额借记固定资产销售利得,贷记固定资产。

因为固定资产从集团公司内部一个公司转移到另一个公司,是以高于账面成本的价格销售的,尽管从集团看销售利得未实现,但购买公司账上已按高于原成本的价格入账,从而使企业集团固定资产价值虚增,另一方面在销售公司账上产生了未实现利润,故需在编制合并报表之前将其抵消。

Income_Statement(1)

Trading Section Cost of Sales and Gross Profit

Accruals Concept

• Expenses are resources used during the period and not the same as cash paid during the period • Expenses and revenues are matched by the period – Show revenue in 2011 in the P/L – Then show resources used in 2011 as expenses in the P/L • Cash may be – Prepaid in 2010 – Paid in 2011 or – Paid in arrears in 2012 (Accrued expenses) • Expenses are not the same as cash paid

• All impact on the level of reported profit

Role of income statements

• Measure financial performance • Shows how and where profits might be increased • Financial conxpenses in published accounts

• Cost of sales (opening stock + purchases – closing stock) • Distribution costs • Administrative expenses (salaries, training, telephone) • Finance expenses (interest charges)

Income Statement (损益表)

Income Statement (损益表)Revenues (销售收入)-Cost of goods sold (COGS) (产品销售成本)= Gross Profit (毛利润)-Expenses (费用)= Earnings Before Tax (税前收益)-Tax (所得税)= Net Income (净收益)The purpose of firm is to earn income for investors through selling goods or providing services to customers. Income statement measures how muchincome is earned during a specific period, such as a year, a quarter, or a month.Outline of today’s lecture1. A typical income statement2.Definition of accounting period(会计期间), Revenues, Expenses,Cost of Goods Sold, Earnings, and Net Income3.Cash accounting(收付实现制)and its inadequacies(不足)4.Accrual Accounting(权责发生制)and its strengths4.1 Revenue recognition, matching principle and expenserecognition(收入确认、配比原则和费用确认)4.2 Adjusting journal entries(调整会计分录)5.Expensing(费用化)versus capitalization (资产化)of expenditures6.Relations between income statement and balance sheet7.Time series and cross section analysis of income statement8.Earnings management examples9.P/E ratio(市盈率)and earnings-based market anomaliesCash AccountingRevenues: recognized at the time that cash is received Expenses: recognized at the time that cash is disbursedNote: Cash received from and disbursed (分发)to shareholders and creditors(债权人)is neither revenues nor expenses, and does not enter income statement under cash accountingAn example: A toy retailer starts business on November 1, 19x0, He pays two months rent on his store, $2,000, on that day, and also purchases and pay for $35,000 toys. However, he sells nothing in November. In December, he sells all the toys with a sales price of $40,000 and collects $5,000 in cashProblems with Cash Accounting1.Mismatch the cost of efforts (expenses) with theoutput of the efforts (revenues)2.Delay recognition of revenues3.Provide opportunities to manage earningsAccrual AccountingRevenue recognition: follow realization principle (实现原则)1) A firm has performed all, or most of, the services it expects to provide2) The firm has received cash or some other assets capable of reasonably precise measurement, such as account receivablesAccrual AccountingExpense recognition:a)When an asset is used directly to generate revenues, the usedasset becomes expense. E.g., sold books, the cost to purchase the sold books become COGS, a part of expenses.This is called matching principle(配比原则)of accounting. b)When an used asset is indirectly related to the current, and onlythe current, period revenues, we treat the used asset as expense.E.g., cash to pay for advertisement, salary for the CEO.c)When an asset is used to benefit both the current and the futureperiod, the benefit, nevertheless, not matter current or future,is hard to identify and measure, we treat the used asset as expense.E.g., cash used to pay research and development forpharmaceutical companies. This is conservative principle(稳健原则)of accounting.Adjusting Journal Entries Under Accrual Accounting Under accrual accounting, some journal entries are not explicitly related to a transaction. We makethese entries, adjusting journal entries, mostlikely at the end of an accounting period.There are four types of adjusting entries:1.Unearned revenue (客户预付款)2.Accrued Revenue(应计收入)3.Prepaid expense(预付费用)4.Accrued expense(应计费用)Unearned RevenueOn Sep. 1, 2002, although Guanghua received the cash, to it, the cash received is unearned revenue. That is,Guanghua has not provided you educational service yet.Guanghua’s journal entry:Dr. Cash $80,000Cr. Unearned Revenue (liability) $80,000On Dec. 31, 2002, after you have spent half a year at Guanghua to enjoy its superb service,Guanghua has earned one-fourth of the tuitions. Journal entry:Dr. Unearned Revenue $20,000Cr. Revenue $20,000Prepaid expenseOn Sep. 1, 2002, your account:Dr. Prepaid tuitions $80,000Cr. Cash $80,000On Dec. 31, 2002, youDr. Tuition expense $20,000Cr. Prepaid expense $20,000If you quit school on this day, you get $60,000 back from the school.The Final Stages of the Accounting Process (refer toa premier on accounting handout)On Dec. 31 of the year, the accountants finished all journal entries, posted to ledger (T-accounts), calculated thebalance (余额)of every ledger account, and did a trialbalance. Now she/he does adjusted journal entries, andthen posts to ledger again, and does an adjusted trialbalance.What she/he has in hands now is a list of accounts. Next:1)Prepare income statement2)Close income statement accounts to retained earningsaccount3)Prepare balance sheetQ.E.DExpensing vs. Capitalization of Expenditures1. A firm pays employeesalaries, we say the firmexpense employee salary 2.Expensed expenditures go toincome statement3.Expensed expenditures helpgenerate revenues in currentperiod4.If a firm expenses theexpenditure, currentearnings will be lower bythat amount 1. A firm buy a building, wesay the firm capitalize thebuilding as asset.2.Capitalized expenditures goto balance sheet3.Capitalized expenditureshelp generate revenues incurrent and future periods 4.If a firm capitalizes theexpenditure, currentearnings will not be loweredby that amountExpensing vs. Capitalization of ExpendituresBut life is not so simple and straightforward. Sometimes it is difficult to determine whether the expenditures benefitfuture periods, and if it benefits future periods, it isdifficult to determine which future period will benefit.Therefore, firms expense some expenditures that mayotherwise be capitalized. This is a conservative treatment of the expenditures by GAAP.1.Marketing expenditures2.Research and Development3.Stock optionsThe Worldcom scandalJune 26, 2002, Worldcom reports it overstated earnings by $3.8 billion in the past few years. It quickly asked forchapter 11 protectionWhat did they do? Capitalize expenditures that should have been expensed. That is, $3.8 billion should not be onbalance sheet, but go through income statement as expense. In 2001, the company reports earnings of 1.4 billion, which should have been a loss year.The relation between balance sheet and incomestatement1.Assets = Liabilities + Equity2.Equity = Contributed capital(股本)+ Retained Earnings(RE)3.Ending(期末余额)RE = Beginning (期初余额)RE + NetIncome –Dividends Income = Revenues –ExpensesA = L + Contributed capital + Beginning RE + (Revenues –Expenses) –DividendsTherefore, revenues increase assets and equityexpenses decreases assets and equityTime Series analysis of common-size incomestatementGrowth analysis of income statementA few items on I/S explained1.Cost of revenues = Cost of goods sold (COGS)2.Sales and Marketing3.Selling, general and administrative4.Product development5.Depreciation and amortization6.Operating income or income from operation7.Extraordinary item: unusual and infrequent Income9.Earnings per share-primary10.Earnings per share-diluted11.Earnings per share-end of year number of shares, or averagenumber of shares?12.Pro Forma earnings = As if earningsAOL 2000AOL 2000Earnings Management-WhyFor managers: earnings-based bonusFor shareholders: earnings-based bond covenant For the company:Better IPO price(新股上市发行价)Avoid government regulationAvoid paying employee high salariesEarnings Management-How Accelerate or delay revenues Accelerate or delay expensesTake one-time gains or charges: big bathEarnings management –Who gain, who lose? Enron caseWorldcom casePrice-to-earnings ratio –P/EP/E is a ready yardstick for valuationUse comparable firms’P/E to price IPO stocksP/E is a rough indicator of relative over-valuation or under-valuationAverage P/E ratio of all stocks on a market indicates the level of valuation of the marketCaveats(提醒)in using P/E in valuation1.Negative earnings can not be used in computingP/E2.Earnings contain transitory (临时的)items, or one-time items that drive P/E up or downtemporarily3.P/E ratio is meaningful only when earningscome from normal, repetitive operation4.In investing community, people use differentearnings to compute P/E, lag earnings, leadearnings, average earnings…Investing Motto “Financial Statement is like bikini, what it reveals is interesting, but what it conceals it vital.”Burton G. Malkiel <A random walk down wall strett>。

英文版的利润表

英文版的利润表以下是一份英文版的标准利润表(Income Statement)样本,注意不同公司可能对项目的具体描述和排序有所不同,这里提供的是一个一般性的例子:Income StatementFor the Year Ended [日期]Revenue•Sales: $XXX,XXX•Other Income: $X,XXX•Total Revenue: $XXX,XXXCost of Goods Sold•Cost of Goods Sold: $(XX,XXX)Gross Profit•Gross Profit: $XXX,XXXOperating Expenses•Selling Expenses: $(XX,XXX)•General and Administrative Expenses: $(XX,XXX)•Research and Development Expenses: $(XX,XXX)•Other Operating Expenses: $(X,XXX)•Total Operating Expenses: $(XXX,XXX)Operating Income (Loss)•Operating Income (Loss): $X,XXXNon-Operating Income (Expenses)•Interest Income: $X,XXX•Interest Expenses: $(X,XXX)•Other Non-Operating Income (Expenses): $(X,XXX)•Total Non-Operating Income (Expenses): $(X,XXX)Net Income Before Tax•Net Income Before Tax: $XX,XXXIncome Tax Expense (Benefit)•Income Tax Expense (Benefit): $(X,XXX)Net Income•Net Income: $XX,XXX请注意,上述利润表的数字和项目仅供示例,实际的利润表内容可能因公司的业务性质和会计准则的不同而有所变化。

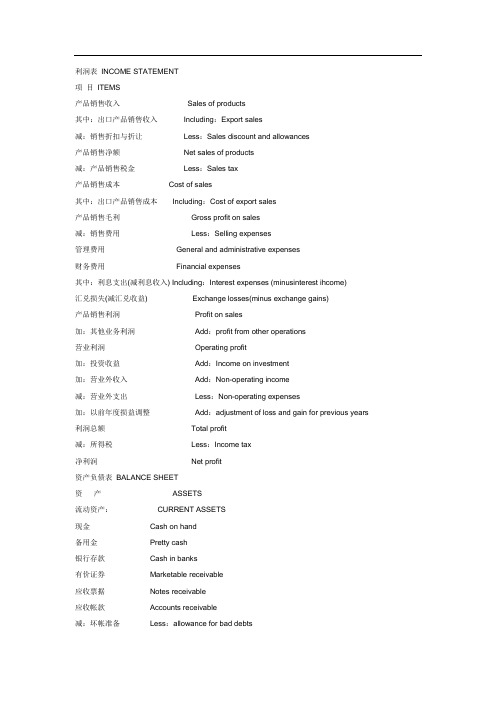

利润表 INCOME STATEMENT

利润表INCOME STATEMENT项目ITEMS产品销售收入Sales of products其中:出口产品销售收入Including:Export sales减:销售折扣与折让Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利Gross profit on sales减:销售费用Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome)汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years 利润总额Total profit减:所得税Less:Income tax净利润Net profit资产负债表BALANCE SHEET资产ASSETS流动资产:CURRENT ASSETS现金Cash on hand备用金Pretty cash银行存款Cash in banks有价证券Marketable receivable应收票据Notes receivable应收帐款Accounts receivable减:坏帐准备Less:allowance for bad debts预付货款Prepayments-supplies内部往来Inter-company accounts其他应收款Other receivables待摊费用Prepaid and deferred expenses存货Inventories减:存货变现损失准备:Less:allowance on inventory reduction to market已转未完工生产成本Transferred in production cost transforming一年内到期的长期投资Matured long time investments within a year流动资产合计Total current assets|长期投资:LONG TERM INVESTMENT长期投资Long term investments拨付所属资金Funds to burnchs一年以上的应收款项Accounts receivable over a year固定资产:FIXED ASSETS固定资产原价Fixed assets-cost减:累计折旧Less:amumulated depreciation固定资产净值Fixed assets-net value固定资产清理Disposal of fixed assets融资租入固定资产原价:Fixed assets-cost on financial lease减:融资租入固定资产折旧Less:amumulated depreciation融资租入固定资产净值:Fixed assets-net value on financial lease 在建工程:CONSTRUCTION WORK IN PROCESS在建工程Construction work in process☆无形资产INTANGIBLE ASSETS场地使用权Right to the use of a site工业产权及专有技术Industrial property right anf patents其他无形资产Other intangibles无形资产合计Total intangible assets其它资产OTHER ASSETS开办费Organization espenses筹建期间汇兑损失Exchange losses during organization period 递延投资损失Deferred investment losses递延税款借项Debit side of deferred tax其他递延支出Other deferred expuditures待转销汇兑损益Prepaid and deferred exchange loss其他递延借款Debit side of other deferred其他资产合计Total other Assets资产总计TOTAL ASSETS负债及所有者权LIABILITIES AND CAPITAL流动负债:CURRENT LIABILITIES短期借款Short term loans应付票据Notes payable应付帐款Accounts payable内部往来Inter-company accounts预收货款Items received in advance-supplies应付工资Accured payroll应交税金Taxes payable应付股利Dividendes payable其他应付款Other payables预提费用Accrued expenses职工奖励及福利费用Bonus and welfare funds一年内到期的长期负债Matured long term liabilities within a year 其他流动负债Other current liabilities流动负债合计Total current liabilities长期负债:LONG TREM LIABILITIES长期借款long term loans应付公司债Bouds payable应公司债溢价(折价)Premium on bonds payable(discount)一年以上的应付款项Accounts payable over a year长期负债合计:Total long term liabilities其他负债:OTHER LIABILITIES筹建期间汇兑收益Exchange gains during organization period 递延投资收益Deferred investment gains递延税款贷项Credit side of deferred tax其他递延贷项Credit side of other tax待转销汇兑收益Prepaid and deferred exchange profit其他负债合计Total other liabilities负债合计Total liabilities所有者权益Investor’s equity资本总额(货币名称及金额)Authorized capital(*___________)实收资本(外币金额期末数)Paid in capital(☆__________)其中Including中方投资(外币金额期末数)Chinese investments(☆__________)外方投资(外币金额期末数Foreign investments(☆__________)减:已归还投资Less: Returned investments资本公积Accumulation of capital公司拨入资金Funds from head office储备基金Reserve funds企业发展基金Expansion funds利润归还投资Investment returned with profit本年利润Current profit未分配利润Retained earnings货币换算差额Currency translation difference所有者权益合计Total investor’s equity负债及所有者权益合计TOTAL LIABILITIES AND INVESTORS EQUITY附注: 1.委托加工材料元; 2.受托代销商品元; 3.代管商品物资元; 4.由企业负责的应收票据贴现元; 5.租入固定资产元; 6.本年支付的进口环节税金。

利润表英文

利润表英文

利润表英文可以被称为Income Statement,也被称为Profit and Loss Statement。

作为一名知名学者,我相信,

准确地理解和解读财务报告对于投资者和企业经理来说是至关重要的。

利润表是企业会计周期性编制的财务报表,用于描述一

个企业特定时间内的销售收入、成本及费用,以确定企业该期间的盈利概况。

根据利润表所反映的信息,投资者可以了解企业的盈利能力,而企业经理则可以从中分析和评估企业经营绩效和决策。

利润表包括三部分:营业收入(Revenue)、成本及费用(Expenses)和净收益(Net Income)。

营业收入是企业在特定期间内从销售商品或提供服务中

产生的总收入。

成本及费用包括企业进货成本、销售与行政费用等。

净收益是这一时期内企业所获得的营业收入减去成本及费用后的余额。

利润表的编制可以根据企业不同的行业特点进行调整,

例如,在制造业中,需要计算生产成本及工厂运营成本;在零售业中,需要计算销售成本和租金等;在服务业中,则需要计算专业服务成本和工资等。

需要注意的是,同时需要关注利润表的质量问题。

企业

会计数据的正确性和透明性对于投资者和企业经理都是至关重要的。

进行质量检验需要确保收入和成本的计算是准确的,精确计算企业的收入和成本,并完整地记录所有不同类型的费用。

总之,利润表是一份重要的财务报告,可以为投资者和

企业经理提供了解企业经营状况的核心指标,在制定商业策略、分析投资收益等方面相当重要。

pastpaper

You are allowed ten minutes before the start of the examination to acquaint yourself with the instructions below and to read the question paper.Do not write anything until the invigilator informs you that you may start the examination. You will be given five minutes at the end of the examination to complete the front of any answer books used.January 2008 ICM232 2007/8 A 001One Answer SheetOne Answer BookOnly Texas BAII Plus seriescalculators are permittedNo other calculators are permittedTHE UNIVERSITY OF READINGFinal Examination for MSc,Course in Investment ManagementFINANCIAL ANALYSISThree hoursAnswer ALL of the following questions in each Section.Instructions to accompany ICM 232 2007/8 A 001For multiple choice tests your answers are marked on an EDPAC ANSWER SHEET. The completed sheets are fed into a DRS Edit machine which electronically reads your details, calculates your answers and produces the results in an Excel database. It is important to follow the instructions carefully for completing the EDPAC sheet - the machine does not make mistakes – you do. An incorrectly filled in answer will affect your result.At the test please fill in your FAMILY name – 1 letter in each of the boxes on the top left side of the form and put a clear line through the corresponding letters in the columns below. Do the same in the INITS box - initial letter(s) of your first name(s) - on the right. If you know more than one person has the same family name as you please also write your full first name in the box beside “candidate name” It is not necessary to fill in your candidate number. In the Subject box write the test which you are sitting, e.g. International Securities Markets or ISM.Please pencil a clear line across the A, B, C, or D:1 [A] [B] [C] [D]2 [A] [B] [C] [D]3 [A] [B] [C] [D]4 [A] [B] [C] [D]5 [A] [B] [C] [D]It is important to use pencil as you cannot erase ink if you change your mind about the answer. Please do not circle Ⓐ, cross B tick √ or scribble across your answer as the DRS Edit machine cannot read these marks.Section AThe questions in this section must be answered using the EDPAC ANSWER SHEET.Macroeconomics – multiple choice questions (2 marks each, total 14 marks)1. The law of demand indicates that as the price of a good increases,(a) suppliers sell less of it.(b) suppliers sell more of it.(c) buyers buy less of it.(d) buyers buy more of it.2. In a supply and demand graph, the triangular area that represents thedifference between the maximum price consumers were willing to pay for a good and the market price is called:consumersurplus.(a)surplus.producer(b)cost.(c)marginaltriangulararbitrage.(d)3. The total economic cost of producing a good or service is called the(a) comparative value of construction.(b) social consequence of resources.(c) marginal valuation of output.(d) opportunity cost of production.4. Economic efficiency requires that(a) individuals produce at their maximum level.(b) only long-lasting, high-quality products be produced without regardcost.to(c) income be distributed equally among consumers.(d) all economic activity generating more benefits than costs beundertaken.ICM232 2007/8 A 0015. Which of the following correctly describes the external benefit resultingfrom an individual’s purchase of a winter flu shot?(a) The flu shot is cheaper than the cost of treatment when you get theflu.(b) The income of doctors increases when you get the flu shot.(c) The flu shot reduces the likelihood others will catch the flu.(d) The flu shot reduces the likelihood you will miss work as the result ofsickness; therefore, you will earn more income.6. What would be the effect of a decrease in the real interest rate and anincrease in the expected inflation rate?(a) Both changes would decrease aggregate demand.(b) Both changes would increase aggregate demand.(c) Both changes would increase short-run aggregate supply.(d) Both changes would increase long-run aggregate supply.7. If the federal government is running a budget deficit,(a) the national debt will decline.(b) it will have to either raise taxes or reduce expenditures next year.(c) the government will finance the deficit by issuing additional bonds.(d) the supply of money will increase and the general level of prices willrise.Microeconomics – multiple choice questions (2 marks each, total 6marks)8. Time costs, unlike money prices, differ among individuals. Therefore,(a) money prices are essentially irrelevant when time costs matter.(b) high-wage consumers generally choose fewer time-intensivecommodities than do low-income consumers.(c) low-wage consumers generally choose more time-saving commoditiesthan do persons with higher time costs.(d) there is no predictable relationship between income level and theamount of time-saving commodities chosen by a consumer.Turn001over 2007/8ICM232A9. In economic theory, the word “demand” refers to:(a) the amount people are willing to purchase at various prices.(b) those wants or needs that are urgent or pressing.(c) wants that are economic in character rather than social, cultural, or spiritual.(d) the desire of persons for a good, regardless of whether they’re willingto purchase the good.10. In the real world, most firms are:pricesearchers.(a)takers.price(b)competitive.purely(c)monopolies.(d)Section BThe questions in this section must be answered using the Answer Booklet.1. Provide a brief definition/explanation of the following terms (3 markseach, total 30 marks):(a) Law of demand(b) Crowding out effect(c) Price elasticity of demandDifferentiationstrategy(d)Matchingprinciple(e)securities(f) MarketableCapitalisation(g)contractsExecutory(h)data(i) Segmented(j) Defined contribution plan001AICM2322007/82. Industry Structure and Competition (10 marks)You are a retail bank licensed to do business in Italy and regulated by theBanca d’Italia. You have been very successful in your banking business inItaly but have never expanded outside of your home market. Also, foreignbanks have found it very difficult to expand into Italy as they have beenunable to get central bank authorisation to do business. However, theEuropean regulatory framework is about to change at the start of next yearand any bank in an EU country will be allowed to conduct business in anyother EU country and be regulated by its ‘home regulator’. Thus, theBanca d’Italia will no longer be able to restrict other European banks fromcompeting in Italy.Discuss the potential impact of this legislation on your bank within thedomestic Italian retail banking sector industry. In particular, brieflydiscuss it along the lines of the Porter competition model and using his fiveheadings:(a) Current structure and competition of the Italian retail bankingindustry(b) Bargaining power of buyers(c) Bargaining power of suppliers(d) Threat of new entrants(e) Threat of substitute productsTurnover 001A2007/8ICM2323. Accounting – revenue and assets. (14 marks)ABC Ltd. Balance Sheet 2005 2006 Income Statement2006Cash 1,000 1,100 Revenue 10,000Accounts Receivable 1,500 1,650 COGS -6,000 Inventory 2,000 2,200 Depreciation -600Total CA 4,500 4,950 S,G&A-1,000 Fixed Asset at Cost 11,000 12,150 Int. Expense -600 Accum. Depreciation -4,500 -5,100 EBT 1,800 Net Fixed Assets 6,500 7,050 Taxes -720Total Assets 11,000 12,000 NetIncome 1,080 Accrued Liabilities 800 880 Accounts Payable 1,200 1,320 Notes Payable 5,500 6,050Total CL 7,500 8,250Long term debt 2,000 1,602 Common Stock 1,000 1,000 Retained Earnings 500 1,148Total Sources of Finance 11,000 12,000Given the above Balance Sheet and Income Statement for ABC Ltd. create a statement of cash flows for 2006 using the indirect method.ICM232 2007/8 A 001Page 74. Accounting - liabilities. (12 marks)ABC Ltd. - Analysis ofInventory Quarter Units Unit Total Unit Purchased Cost Cost Sales 1 200 £22.00 £4,400.00 200 2 300 £24.00 £7,200.00 200 3 300 £26.00 £7,800.00 200 4 200 £28.00 £5,600.00 200 1000 £25,000.00 800 Beginning Inventory 400 @ £20.00 eachEnding inventory 600unitsGiven the above information on ABC Ltd. calculate the following using both the FIFO and LIFO methods. (a) Reported inventory at year end. (b) Cost of goods sold for the year and comment on which method will show the highest reported net income for the year and why.ICM232 2007/8 A 001 Turn overPage 85. Accounting - liabilities. (14 marks)BP plc issued a zero coupon bond on January 1, 2008, due December 31,2012 (assume exactly five years for any calculations).The face value of thebond was £75.0 mio. The bond was issued at an effective annual rate of5.0%.(a) Calculate the cash proceeds of the bond issue (assume no issuancecosts).(b) Complete the following table on a pre-tax basis, assuming that anyinterest payable is paid in the year it is due:N.B. All figures in000s. 2007 2008 2009 2010 2011 EBIT £50,000.00 £50,000.00 £50,000.00 £50,000.00 £50,000.00 CFO before interestand taxes £60,000.00 £60,000.00 £60,000.00 £60,000.00 £60,000.00 CFOTimes interestearnedTimes interestearned - cash basis(c) Now, as an alternative scenario, assume that BP had raised the sameamount of initial cash proceeds as the zero coupon bond in (a) butwith a ‘regular’ bond paying a 5.0% coupon (annually) with principalrepaid at maturity. Complete the same (below) table under thisscenario.differentcontinued)(Question001A2007/8ICM232Page 95. (Continued)N.B. All figures in000s. 2007 2008 2009 2010 2011 EBIT £50,000.00 £50,000.00 £50,000.00 £50,000.00 £50,000.00 CFO before interestand taxes £60,000.00 £60,000.00 £60,000.00 £60,000.00 £60,000.00 CFOTimes interestearnedTimes interestearned - cash basis(d) Using the results from the two tables in parts (b) and (c), discuss theimpact on reported CFO and Times Interest Earned (regular and cashbasis) of the two scenarios.[End of question paper]ICM232 2007/8 A 001。