ACCA词典

ACCA词汇

acknowledgement requirement 对承认的要求

acquisition of assets 资产的取得

acquisitions 兼并

Act on Product Liability (德国)生产责任法

BPO(bargain purchase option)廉价购买任择权

bridge facility桥式融通

bridge桥梁

broker fee经纪人费

brokers经纪人

build-to-suit leases(租赁物由承租人)承建或承造的租赁协议

capital lease融资租赁协议

capital market资本市场

capitalize资本化

captive finance company专属金融公司

captives专属公司

carrying amount维持费用

carrying value账面结存价值

acceptance date 接受日

acceptance 接受

accession 加入

accessories 附属设备

accountability 承担责任的程度

accounting benefits 会计利益

accounting period 会计期间

case law案例法

cash collatera1现金抵押

cash election现金选择

cash flow coverage ratio现金流偿债能力比率

cash flow现金流

cash receipts and cash applications现金收入及现金运用

acca专业词汇表[精彩]

![acca专业词汇表[精彩]](https://img.taocdn.com/s3/m/4c3b9beac0c708a1284ac850ad02de80d4d806ca.png)

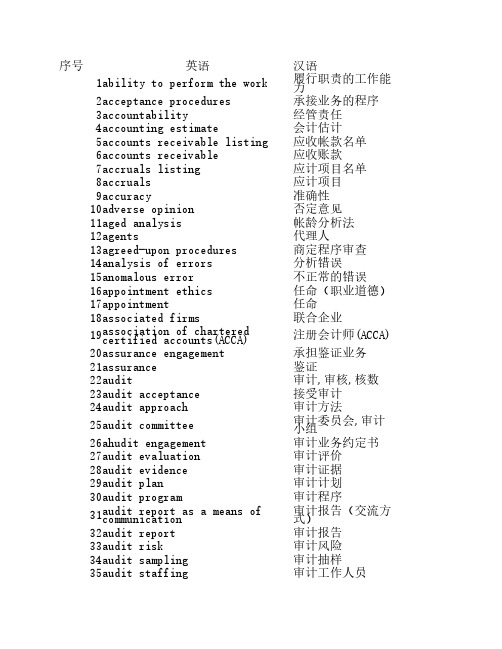

acca专业词汇表[精彩]acca 专业词汇表[精彩]序号英语汉语履行职责的工作能力 1 ability to perform the work承接业务的程序 2 acceptance procedures经管责任 3 accountability会计估计 4 accounting estimate应收帐款名单 5 accounts receivable listing应收账款 6 accounts receivable应计项目名单 7 accruals listing应计项目 8 accruals准确性 9 accuracy否定意见 10 adverse opinion帐龄分析法 11 aged analysis代理人 12 agents程序审查(约定审计业务) 13 agreed-upon procedures分析错误 14 analysis of errors不正常的错误 15 anomalous error任命(职业道德) 16 appointment ethics任命 17 appointment联合企业 18 associated firms注册会计师(ACCA) 19 association of chartered certified accounts(ACCA) 承担鉴证业务 20 assurance engagement 鉴证 21 assurance审计,审核,核数 22 audit接受审计 23 audit acceptance审计方法 24 audit approach审计委员会,审计小组 25 audit committee审计业务约定书 26 ahudit engagement审计评价 27 audit evaluation审计证据 28 audit evidence审计计划 29 audit plan审计程序 30 audit program审计报告(交流方式) 31 audit report as a means of communication 审计报告 32 audit report审计风险 33 audit risk审计抽样 34 audit sampling审计工作人员 35 audit staffing审计及时 36 audit timing审计线索 37 audit trail审计准则 38 auditing standards审计职业审慎性 39 auditors' duty of care审计报告 40 auditors' report遵循ISA(国际审计准则) 41 authority attached to ISAs(电脑)自动生产的工作底 42 automated working papers 稿坏账 43 bad debts银行 44 bank银行对账单,余额调节表 45 bank reconciliation收益权 46 beneficial interests最好的价值 47 best value经营风险 48 business riskcadbury 委员会 49 cadbury committee现金盘点 50 cash count现金循环 51 cash system改变债务的性质上 52 changes in nature of engagement费用和佣金 53 charges and commitments慈善团体 54 charities审计的年表 56 chronology of an auditCIS 应用控制 57 CIS application controlsCIS 环境单机微型计算器58 CIS environments stand-alone microcomputers顾客甄别 59 client screening紧密联系 60 closely connected俱乐部 61 clubs在审计员和管理者间沟通62 communications between auditors and management内部控制上的沟通 63 communications on internal control公司法 64 companies act比较财务报表 65 comparative financial statements比较的 66 comparatives能力 67 competence承接编制(业务) 68 compilation engagement完整性 69 completeness审计终结 70 completion of the audit符合会计规则 71 compliance with accounting regulations计算器援助的审计技术72 computers assisted audit techniques (CAATs) (CAATs)信任 73 confidence保密性 74 confidentiality应收帐款询证函 75 confirmation of accounts receivable利益冲突 76 conflict of interest工程应付款 77 constructive obligation或有资产 78 contingent asset或有负债 79 contingent liability控制环境 80 control environment控制程序 81 control procedures控制风险 82 control risk争论 83 controversy公司治理 84 corporate governance相关的数值 85 corresponding figures转换成本,加工成本 86 cost of conversion成本 87 cost优待 88 courtesy债权人 89 creditors本期审计档案 90 current audit files数据库管理制度(数据管理91 database management system (DBMS) 系统)报告的日期 92 date of report折旧 93 depreciation(抽样)样品的选取 94 design of the sample检查风险 95 detection risk直接核查法 96 direct verification approach有方向的抽查 97 directional testing董事酬金 98 directors' emoluments董事服务合约 99 directors' serve contracts与经营管理者意见不一致 100 disagreement with management 拒绝表示意见 101 disclaimer of opinion分销,分派,分配 102 distributionsdocumentation of understanding and assessment of control 控制风险评估的文件编集 103 risk审计程序的审计文档 104 documenting the audit process应有关注 105 due care应有的技能和谨慎 106 due skill and care经济 107 economy教育 108 education效用,效果 109 effectiveness效益,效率 110 efficiency合格、资格 / 无资格 111 eligibility / ineligibility强调某事项 112 emphasis of matter业务约定书 114 engagement letter错误 115 error审计程序结果的评估116 evaluating of results of audit procedures 检查 117 examinations存在性 118 existence期望差距 119 expectations预期的错误 120 expected error经验 121 experience专家 122 expert独立审计 123 external audit外部复核报告 124 external review reports公正 125 fair费用谈判 126 fee negotiation控制风险的最终评定 127 final assessment of control risk期末审计 128 final audit财政报告公布 129 financial statement assertions财务 130 financial产成品 131 finished goods流程图 132 flowcharts舞弊 133 fraud and error欺诈 134 fraud基本原理 135 fundamental principles一般的 CIS 控制 136 general CIS controls对管理者的一般报告 137 general reports to mangement持续经营假设 138 going concern assumption持续经营 139 going concern待出售或者退回商品 140 goods on sale or return商誉 141 goodwill统治 142 governancegreenbury 委员会 143 greenbury committee内部审计员执业指南 144 guidance for internal auditorshampel 委员会 145 hampel committee随意选择 146 haphazard selection款待 147 hospitality人力资源 148 human resourcesIAPS 1000银行询证程序149 IAPS 1000 inter-bank confirmation proceduresIAPS 1001 CIS 环境-单机微 150 IAPS 1001 CIS environments-stand-alone microcomputers 型计算器IAPS 1002 CIS 环境-(与主 151 IAPS 1002 CIS environments-on-line computer systems 机)联机计算器系统IAPS 1003 CIS 环境- 数据 152 IAPS 1003 CIS environments-database systems 库系统IAPS 1005小企业审计中的IAPS 1005 the special considerations in the audit of small 153 特别考虑 entities IAS 2 库存 154 IAS 2 inventories资产负债表日后事项 155 IAS 10 events after the balance sheet date IFAC's职业会计的师道德准156 IFAC's code of ethics for professional accountants 则所得税 157 income tax对收入进行审计的审计员 158 incoming auditors独立估计 159 independent estimate无资格被任命 160 ineligible for appointment信息技术 161 information technology固有风险 162 inherent risk保险 164 insurance无形 165 intangibles完整性 166 integrity中期审计 167 interim audit内部审计 168 internal auditing内部审计师 169 internal auditors内部控制评价调查表(问卷) 170 internal control evaluation questionnaires (ICEQs)内部控制调查表 171 internal control questionnaires (ICQs)内部控制系统 172 internal control system内部审计的委派 173 internal review assignment国际审计和鉴证准则委员会174 international audit and assurance standards board (IAASB) (IAASB)国际审计实务声明 (IAPSs) 175 international auditing practice statements (IAPSs)国际会计师联合会(IFAC) 176 international federation of accountants (IFAC)盘存制度 177 inventory system存货估价 178 inventory valuation230审计文档 179 ISA 230 documentation240 欺诈和错误 180 ISA 240 fraud and error250 法律法规的考虑181 ISA 250 consideration of law and regulations Isa 260 communications of audit matters with those charge 260 与高官的审计事项沟通 182 governance300 审计计划 183 isa 300 planning310 对企业的了解 184 isa 310 knowledge of the business320审计重要性 185 isa 320 audit materiality400 会计和内部控制186 isa 400 accounting and internal control402 企业外聘服务机构的审isa 402 audit considerations relating to entities using 187 计考虑 service organisations 500审计证据 188 isa 500 audit evidence501审计证据-特殊情况的特isa 501 audit evidence-additionalconsiderations for 189 殊考虑 specific items510外部询证 190 isa 510 external confirmations520分析性复核程序 191 isa 520 analytical procedures530审计抽样 192 isa 530 audit sampling540会计估计的审计 193 isa 540 audit of accounting estimates 560期后事项 194 isa 560 subsequent events580管理当局声明书 195 isa 580 management representations 610 内部审计的考虑196 isa 610 considering the work of internal auditing620 使用专家的工作 197 isa 620 using the work of an expert 700财务报表的审计报告198 isa 700 auditors' report on financial statements710可比性 199 isa 710 comparatives720 与财务报表审计相关的isa 720 other information in documents containing audited 200 其他信息 financial statements 910 受托复阅财务报表 201 isa 910 engagement to review financial statements法律和规则 206 legal and regulations法定义务,法定责任 207 legal obligation鉴证程度 208 levels of assurance负债 209 liability审计范围限制 210 limitation on scope审计的局限性 211 limitation of audit控制系统的局限性 212 limitations of controls system诉讼和赔偿 213 litigation and claims诉讼 214 litigation借款,贷款 215 loans长期负债 216 long term liabilities低价招揽审计业务 217 lowballing管理 218 management经营完整 219 management integrity管理当局声明书 220 management representation letter推销,营销,市场学 221 marketing重要的矛盾 222 material inconsistency重大误报 223 material misstatements of fact重要性 224 materiality计量 225 measurement微型计算器 226 microcomputers变更报告 227 modified reports性质 229 nature消极鉴证 230 negative assurance可实现净值 231 net realizable value非现金资产的登记本 232 non-current asset register非执行董事 233 non-executive directors非抽样风险 234 non-sampling risk非法定审计 235 non-statutory audits客观性 236 objectivity或有事项 237 obligating event或有事项披露 238 obligatory disclosure出现 240 occurrence(与主机)联机计算器系统 241 on-line computer systems期初余额 242 opening balances经营审计 243 operational audits经营工作计划 244 operational work plans意见购买 245 opinion shopping其他的信息 246 other information内审外包 247 outsourcing internal audit财务报表的全面复核 248 overall review of financial statements 滞纳金 249 overdue fees制造费用分配 250 overhead absorption定期的计划 251 periodic plan永久审计档案 252 permanent audit files个人的亲属关系 253 personal relationships计划 254 planning抽样总体 255 population精密,准确 256 precision控制风险的初次评估258 preliminary assessment of control risk 预付款项 259 prepayments表述,披露 260 presentation and disclosure会计处理的问题 261 problems of accounting treatment程序方法 262 procedural approach程序 263 procedures接受任命后的审计程序264 procedures after accepting nomination 采购 265 procurement保密的职业职责 266 professional duty of confidentiality备抵,准备 268 provision公共职责 269 public duty公众利益 270 public interest宣传 271 publicity采购分类账 272 purchase ledger采购和费用循环 273 purchases and expenses system保留意见 276 qualified opinion错误的性质 278 qualitative aspects of errors随机选择 279 random selection合理保证 280 reasonable assurance再评估抽样风险 281 reassessing sampling risk可靠性 282 reliability报酬 283 remuneration对经营的报告 284 report to management报告 285 reporting研究和开发成本 286 research and development costs 资格保留 287 reservation of title准备,储备 288 reserves收入和资本支出 289 revenue and capital expenditure 复核 290 review复核和资本支出 291 review and capital expenditure 权力和义务 295 rights and obligations风险和重要性 297 risk and materiality以风险为导向的方法 298 risk-based approach审计师的轮换 300 rotation of auditor appointments 职业道德守则 301 rules of professional conduct销售制度 303 sales system销售税金,营业税 304 sales tax销售,销货 305 sales样本量 306 sample size抽样风险 307 sampling risk抽样单元 308 sampling units未调整的错误表 309 schedule of unadjusted errors内部审计的范围和目标310 scope and objectives of internal audit 职责划分 311 segregation of duties服务机构 312 service organization重要影响或未预期的亲属关313 significant fluctuations or unexpected relationships 系小企业 314 small entity个体营业者 316 sole traders内部控制上的样本证书 318 specimen letter on internal control 利益相关者 319 stakeholders标准工作底稿 320 standardised working papers声明1: 完整,客观性和独立321 statement 1:integrity,objectivity and independence声明 2: 信任的职业责任 322 statement 2:the professional duty of confidence声明 3: 广告,宣传和获得职statement 3: advertising ,publicity and obtaining 323 业工作 professional work声明5: 审计聘任的变更324 statement 5:changes in professional appointment统计抽样 325 statistical sampling法定审计 326 statutory audit法定责任 328 statutory duty保管责任人 329 stewardship战略性计划 330 strategic plan分层 331 stratification期后事项 332 subsequent events实证性测试程序 333 substantive procedures实质性测试 334 substantive tests充分的适当审计证据 335 sufficient appropriate audit evidence 监督 338 supervision监督和监控的角色 339 supervisory and monitoring roles供应商的声明 340 suppliers' statements系统和内部控制 341 system and internal controls系统选择法 342 systematic selection系统为导向的方法 343 systems-based approach有形的非流动资产 344 tangible non-current assets投标,清偿 345 tendering委任的条款 346 terms of the engagement控制的测试 347 tests of control股东大会 348 the AGM委员会 349 the board三E原则 350 three Es准时 351 timing可容忍误差 352 tolerable error应付帐款 353 trade accounts payable and purchases应付帐款名单 354 trade accounts payable listing培训 355 training国库,库房 356 treasury真实 357 TRUEturnbull 委员会 358 turnbull committee越权 359 ultra vires不确定性 360 uncertainty未到(支付)期的未决 361 undue dependence无保留的审计报告 362 unqualified audit report 使用知识 364 using the knowledge使用专家的工作 365 using the work of an expert 计价,估价366 valuation现金(交易)价格 367 value for money自愿披露 368 voluntary disclosure工资,薪金 369 wages and salaries工资系统 370 wages system在产品 371 work in progress工作底稿 372 working papers。

ACCA考试必备财务英语词汇

(1)ABC 作业根底本钱计算(2)absorbed overhead已吸收制造费用(3)absorption costing吸收本钱计算(4)account XX ,报表(5)accounting postulate会计假设(6)accounting series release会计公告文件(7)accounting valuation会计计价(8)account sale承销清单(9)accountability concept经营责任概念(10)accountancy会计职业(11)accountant会计师(12)accounting会计(13)agency cost代理本钱(14)accounting bases会计根底(15)accounting manual会计手册(16)Accounting period会计期间(17)Accounting policies会计方针(18)Accounting rate of return会计报酬率(19)Accounting reference date会计参照日(20)accounting reference period会计参照期间(21)Accrual concept应计概念(22)Accrual expenses应计费用(23)Acid test ration速动比率(酸性测试比率)(24)Acquisition购置(25)Acquisition accounting收购会计(26)Activity based accounting作业根底本钱计算(27)Adjusting events调整事项(28)Administrative expenses行政管理费(29)Advice note发货通知(30)Amortization摊销(31)Analytical review分析性检查(32)Annual equivalent cost年度等量本钱法(33)Annual report and accounts年度报告和报表(34)Appraisal cost检验本钱(35)Appropriation account盈余分配XX(36)Articles of association公司章程细那么(37)Assets 资产(38)Assets cover资产保障(39)Asset value per share每股资产价值(40)Associated company联营公司(41)Attainable standard可达标准(42)Attributable profit可归属利润(43)Audit 审计(44)Audit report审计报告(45)Auditing standards审计准那么(46)Authorized share capital额定股本(47)Available hours可用小时(48)Avoidable costs可防止本钱(49)Back-to-back loan易币贷款(50)Back flush accounting倒退本钱计算(51)Bad debts 坏帐(52)Bad debts ratio坏帐比率(53)bank charges 银行手续费(54)Bank overdraft银行透支(55)Bank reconciliation银行存款调节表(56)Bank statement银行对帐单(57)Bankruptcy 破产(58)Basis of apportionment分摊根底(59)Batch批量(60)Batch costing分批本钱计算(61)Beta factor(市场)风险因素(62)Bill帐单(63)Bill of exchange汇票(64)Bill of landing提单(65)Bill of materials用料预计单(66)Bill payable应付票据(67)Bill receivable应收票据(68)Bin card存货记录卡(69)Bonus 红利(70)book-keeping薄记(71)Boston classification波士顿分类(72)Breakeven chart保本图(73)Breakeven point保本点(74)breaking-down time复位时间(75)Budget预算(76)Budget center预算中心(77)Budget cost allowance预算本钱折让(78)Budget manual预算手册(79)Budget period预算期间(80)Budgetary control预算控制(81)Budgeted capacity预算生产能力(82)Burden制造费用(83)Business center经营中心(84)Business entity营业个体(85)Business unit经营单位(86)Buy-out management管理性购置产权(87)By-product副产品(88)called-up share capital催缴股本(89)Capacity生产能力(90)Capacity ratios生产能力比率(91)Capital 资本(92)Capital assets pricing model资本资产计价模式(93)Capital commitment承偌资本(94)Capital employed已运用的资本(95)Capital expenditure资本支出(96)Capital expenditure authorization资本支出核准(97)Capital expenditure control资本支出控制(98)Capital expenditure proposal资本支出申请(99)Capital funding planning资本基金筹集方案(100)capital gain资本收益(101)capital investment appraisal资本投资评估(102)capital maintenance资本保全(103)capital resource planning资本资源方案(104)capital surplus资本盈余(105)capital turnover资本周转率(106)card记录卡(107)cash 现金(108)cash account现金XX(109)cash book现金帐薄(110)cash cow 金牛产品(111)cash flow 现金流量(112)cash discounted现金贴现(113)cash flow budget现金流量预算(114)cash flow statement现金流量表(115)cash ledger现金分类帐(116)cash limit现金限额(117)CCA 现时本钱会计(118)center中心(119)changeover time变更时间(120)chartered entity特许经济个体(121)cherub支票(122)cherub register支票登记薄(123)coin analysis零钱分类(124)classification分类(125)clock card工时卡(126)code 代码(127)commitment accounting承偌确认会计(128)common cost共同本钱(129)company limited by guarantee有限担保责任公司(130)company limited shares股份(131)competitive position竞争能力状况(132)concept概念(133)conglomerate跨行业企业(134)consistency concept一致性概念(135)consolidated accounts合并报表(136)consolidation accounting合并会计(137)consortium财团(138)contingency plan应急方案或有负债(139)contingent liabilities(140)continuous operation连续生产抵消(141)contra(142)contract cost合同本钱(143)contract costing合同本钱计算(144)contribution奉献毛益奉献中心(145)contribution venture(146)contribution chart奉献图(147)contribution per unit of limiting factor ration单位限定因素的奉献毛益比率(148)contribution to sales ration奉献毛益对销售比率(149)control控制(150)control account控制XX(151)control limits控制限度(152)controllability concept可控制概念(153)controllable cost可控制本钱(154)conversion cost加工本钱(155)convertible loan stock可转换为股票的贷款(156)corporate appraisal公司评估(157)corporate planning公司方案(158)corporate social reporting公司社会报告(159)corporation股份公司(160)cost本钱(161)cost account本钱XX(162)cost accounting本钱会计(163)cost accounting manual本钱手册(164)cost accounts calendar本钱报表的日历时间(165)cost adjustment本钱调整(166)cost allocation本钱分配(167)cost apportionment本钱分摊(168)cost attribution本钱归属(169)cost audit本钱审计(170)cost behaviour本钱性态(171)cost benefit analysis本钱效益分析(172)cost center本钱中心(173)cost driver本钱动因(174)cost of capital资本本钱(175)cost of conformance相符本钱(176)cost of goods sold销货本钱(177)cost of non-conformance非相符本钱(178)cost of sales销售本钱(179)cost reduction本钱降低(180)cost structure本钱构造(181)cost unit本钱单位(182)cost-volume-profit analysis(CVP)本量利分析(183)costing本钱计算(184)CPP 现时购置力会计(185)credit note贷项通知(186)credit report信贷报告书(187)creditor债权人(188)creditor days ratio应付帐款天数率(189)creditors ledger应付帐款分类帐(190)critical event关键事项(191)critical path关键路线(192)cumulative preference shares累积优先股(193)current account往来XX(194)current asset流动资产(195)current cost accounting现时本钱会计(196)current liabilities流动负债(197)current purchasing power accounting现时购置力会计(198)current ration流动比率(199)cut-off截止(200)CVP 本量利分析(201)cycle time周转时间(202)debenture债券(203)debit note借项通知(204)debit capacity举债能力(205)debt ratio债务比率(206)debtor债务人(207)debtor days ratio应收帐款天数率(208)debtors应收款(209)debtors ledger应收帐款分类帐(210)debtor’ age analysis应收帐款帐龄分析(211)decision driven costs决策连动本钱(212)decision tree决策树(213)defects次品(214)deferred expenditure递延支出(215)deferred shares递延股份(216)deferred taxation递延税款(217)delivery note交货单(218)departmental accounts部门报表(219)departmental budget部门预算(220)depreciation折旧(221)dispatch note发运单(222)development cost开发本钱(223)differential cost差异本钱(224)direct hours yield直接工时产出率(225)direct labor cost-standard标准直接人工本钱(226)direct labor efficiency-variance直接人工效率差异(227)direct labor rate—variance直接人工费率差异(228)direct labor total-variance直接人工总差异(229)direct material mix-variance直接材料构造差异(230)direct price-variance直接材料价格差异(231)direct material total-variance直接材料总差异(232)direct materials usage-variance直接材料用量差异(233)direct materials yield-variance直接材料产出率差异(234)direct cost直接本钱(235)direct debit直接借项(236)direct hours yield直接小时产出率(237)direct labor cost percentage rate直接人工本钱百分比(238)direct labor hour rate直接人工小时率(239)directs on indirect work间接工作事项上的工时(240)discount rate贴现率(241)discounted cash flow现金流量贴现(242)discretionary cost酌量本钱(243)distribution cost摊销本钱(244)diversions移用(245)diverted hours移用小时(246)diverted hour移’用s工ratio时比率(247)dividend股利(248)dividend cover股利产出率(249)dividend per share每股股利(250)dog疲软产品(251)double entry accounting复式会计(252)double-entry book-keeping复式薄记(253)doubtful debts可疑债务(254)down time停工时间(255)dynamic programming动态规划(256)earning per share每股盈利(257)earning ratio市盈率(258)economic order quantity(EOQ)经济订购批量(259)efficient market hypothesis有效市场假设(260)efficiency ration效率性比率(261)element of cost本钱要素(262)entity经济个体(262)environmental audit环境审计(263)environmental impact assessment环境影响评价(264)EOQ经济订购批量(265)equity权益(266)equity method of accounting权益法会计计算(267)equity share capital权益股本(268)equivalent units当量(269)event事项(270)exceptional items例外事项(271)expected value期望值(272)expenditure支出(273)expenses费用(274)external audit外部审计(275)external failure cost外部损失本钱(276)extraordinary items非常事项(277)factory good让售商品(278)factoring应收帐款让售(279)fail value公允价值(280)feedback反应(281)FIFO先近先出法(282)final accounts年终报表(283)finance lease融资租赁(284)financial accounting财务会计(285)financial accounts calendar adjustment财务报表的日历时间调整(286)financial management财务管理(287)financial planning财务方案(288)financial statement财务报表(289)finished goods完成品(290)fixed asset固定资产(291)fixed overhead固定制造费用(292)fixed asset turnover固定资产周转率(293)fixed assets register固定资产登记薄(294)fixed cost固定本钱(295)flexed budget变动限额预算(296)flexible budget弹性预算(297)float time浮动时间(298)floating charge流动抵押(299)flow of funds statement资金流量表(300)forecasting预测(301)founder’e s shar发起人股份(302)full capacity满负荷生产能力(303)function costing职能本钱计算(304)functional budget职能预算(305)fund accounting基金会计(306)fundamental accounting concept根底会计概念(307)fungible assets可互换资产(308)futuristic planning远景方案G(309)gap analysis间距分析G(310)gearing举债经营比率(杠杆)(311)goal congruence目标一致性(312)going concern concept持续经营概念(313)goods received note商品收讫单(314)goodwill商誉G(315)gross dividend yield总股息产出率(316)gross margin总边际(317)gross profit毛利润(318)gross profit percentage毛利润百分比(319)group 企业集团(320)group accounts集团报表(312)high-geared高结合杠杆(比例)(313)hire purchase租购(314)historical cost历史本钱(315)historical cost accounting历史本钱会计(316)hours小时H(317)hurdle rate最低可承受的报酬率I(318)ideal standard理想标准I(319)idle capacity ration闲置生产能力比率I(320)idle time闲置时间I(321)impersonal accounts非记名XXI(322)imprest system定额备用制度I(323)income and expenditure account收益和支出报表I(324)incomplete records不完善记录I(325)incremental cost增量本钱I(326)incremental yield增量产出率I(327)indirect cost间接本钱I(328)indirect hours间接小时I(329)insolvency无力偿付I(330)intangible asset无形资产I(331)integrated accounts综合报表I(332)interdependency concept关联性概念I(333)interest cover利息保障倍数I(334)interlocking accounts连锁报表I(335)internal audit内部审计I(336)internal check内部牵制I(337)internal control system内部控制体系I(338)internal failure cost内部损失本钱I(339)internal rate of return(IRR)内含报酬率I(340)inventory存货I(341)investment投资I(342)investment center投资中心I(343)invoice register发票登记薄I(344)issued share capital已发行股本J(345)job定单J(346)job card工作卡J(347)job costing工作本钱计算J(348)job sheet工作单J(349)joint cost联合本钱J(350)joint products联产品J(351)joint stock company股份公司J(352)joint venture合资经营J(353)journal日记帐J(354)just-in-time(JIT)适时制度J(355)jusy-in-time production适时生产J(356)just-in-time purchasing适时购置K(357)key factor关键因素L(358)labour人工L(359)labour transfer note人工转移单L(360)leaning curve学习曲线L(361)ledger分类XXL(362)length of order book定单平均周期L(363)letter of credit信用证L(364)leverage举债经营比率L(365)liabilities负L(366)life cycle costing寿命周期本钱计算L(367)LIFO后近先出法L(368)limited liability company XX公司L(369)limiting factor限制因素L(370)line-item budget明细支出预算L(371)liner programming线性规划L(372)liquid assets变现资L(373)liquidation清算L(374)liquidity ratios易变现比率L(375)loan贷款L(376)loan capital借入资本L(377)long range palnning长期方案L(378)lost time record虚耗时间记录L(379)low geared低结合杠杆(比例)L(380)lower of cost or net realizable value concept本钱或可变净价孰低概念M(381)machine hour rate机器小时率M(382)machine time record机器时间记录M(383)managed cost管理本钱M(384)management accounting管理会计M(385)management accounting concept管理会计概念M(386)management accounting guides管理会计指导方针M(387)management audit管理审计M(388)management buy-out管理性购置产权M(389)management by exception例外管理原那么M(390)margin边际M(391)margin of safety ration平安边际比率M(392)margin cost边际本钱M(393)margin costing边际本钱计算M(394)mark-down降低标价M(395)mark-up提高标价M(396)market risk premium市场分险补偿M(397)market share市场份额M(398)marketing cost营销本钱M(399)matching concept配比概念M(400)materiality concept重要性概念M(401)materials requisition领料单M(402)materials returned note退料单M(403)materials transfer note材料转移单M(404)memorandum of association公司设立细那么M(405)merger兼并M(406)merger accounting兼并会计M(407)minority interest少数股权M(408)mixed cost混合本钱N(409)net assets净资产N(410)net book value净帐面价值N(411)net liquid funds净可变现资金N(412)net margin净边际N(413)net present value(NPV)净现值N(414)net profit净利润N(415)net realizable value可变现净值N(416)net worth资产净值N(417)network analysis网络分析N(418)noise干捞N(419)nominal account名义XXN(420)nominal share capital名义股本N(421)nominal holding代理持有股份N(422)non-adjusting events非调整事项N(423)non-financial performance measurement非财务业绩计量N(424)non-intergrated accounts非综合报表N(425)non-liner programming非线性规划N(426)non-voting shares无表决权的股份N(427)notional cost名义本钱N(428)number of days stock存货周转天数N(429)number of weeks stock存货周转周数O(430)objective classification客体分类O(431)obsolescence陈旧O(432)off balance sheet finance资产负债表外筹资O(433)offer for sale标价出售O(434)operating budget经营预算O(435)operating lease经营租赁O(436)operating statement营业报表O(437)operation time操作时间O(438)operational control经营控制O(439)operational gearing经营杠杆O(440)operating plans经营方案O(441)opportunity cost时机本钱O(442)order定单O(443)ordinary shares普通股O(444)out-of-date cheque过期支票O(445)over capitalization过分资本化O(446)overhead制造费用O(447)overhead absorption rate制造费用分配率O(448)overhead cost制造费用O(449)overtrading超过营业资金的经营P(450)paid cheque已付支票P(451)paid-up share capital认定股本P(452)parent company母公司P(453)pareto distribution帕累托分布P(454)participating preference shares参与优先股P(455)partnership合伙P(456)payable ledger应付款项XXP(457)payback回收期P(458)payments and receipts account收入和支出报表P(459)payments withheld保存款额P(460)payroll工资单P(461)payroll analysis工资分析P(462)percentage profit on turnover利润对营业额比率P(463)period cost期间本钱P(464)perpetual inventory永续盘存P(465)personal account记名XXP(466)PEPT 工程评审法P(467)petty cash account备用金XXP(468)petty cash voucher备用金凭证P(469)physical inventory实地盘存P(470)planning方案P(471)planning horizon方案时限P(472)planning period方案期间P(473)policy cost政策本钱P(474)position audit状况审计P(475)post balance sheet events资产负债表编后事项P(476)practical capacity实际生产能力P(477)pre-acquisition losses购置前损失P(478)pre-acquisition profits购置前利润P(479)preference shares优先股P(480)preference creditors优先债权人P(481)preferred creditors优先债权人P(482)prepayments预付款项P(483)present value现值P(484)prevention cost预防本钱P(485)price ratio市盈率P(486)prime cost主要本钱P(487)prime entry-books of原始分录登记薄P(488)principal budget factor主要预算因素P(489)prior charge capital优先股P(490)prior year adjustments以前年度调整P(491)priority base budgeting优先顺序体制的预算P(492)private company私人公司P(493)pro-forma invoice预开发票P(494)problem child问号产品P(495)process costing分步本钱计算P(496)process time加工时间P(497)product cost产品本钱P(498)Product life cycle产品寿命周期P(499)production cost生产本钱P(500)production cost of sales售货本钱P(501)production volume ratio生产业务量比率P(502)profit center利润中心P(503)profit per employee每员工利润P(504)profit retained for the year年度利润留存P(505)profit to turnover ratio利润对营业额比率P(506)profit-volume graph利量图P(507)profitability index盈利指数P(508)programming规划P(509)project evaluation and review technique工程评审法P(510)projection预计P(511)promissory note本票P(512)prospectus募债说明书P(513)provisions for liabilities and charges偿债和费用准备P(514)prudent concept稳健性概念P(515)public company公开公司P(516)purchase order订购单P(517)purchase requisition请购单P(518)purchase ledger采购XXQ(519)quality related costs质量有关本钱Q(520)queuing time排队时间R(521)rate率R(522)ratio比率R(524)raw material原材料R(525)receipts and payments account收入和支付报表R(526)receivable ledger应收款项XX R(527)redeemable shares可赎回股份R(528)redemption赎回R(529)registered share capital注册资本R(530)rejects废品R(531)relevancy concept相关性概念R(532)relevant costs相关本钱R(533)relevant range相关X围R(534)reliability concept可靠性概念R(535)replacement price重置价格R(536)report报表R(537)reporting报告R(538)research cost,applied应用性研究本钱R(539)research cost,pure or basic理论或根底研究本钱R(540)reserves留存收益R(541)residual income剩余收益R(542)responsibility center责任中心R(544)return on capital employed运用资本报酬率R(545)returns退回R(546)revenue收入R(547)revenue center收入中心R(548)revenue expenditure收益支出R(549)revenue investment收入性投资R(550)right issue认股权发行R(551)rolling budget滚动预算R(552)rolling forecast滚动预测S(553)sales ledger销售分类帐S(554)sales order销售定单S(555)sales per employee每员工销售额S(556)scrap废料S(557)scrip issue红股发行S(558)secured creditors有担保的债权人S(559)segmental reporting分部报告S(560)selling cost销售本钱S(561)semi-fixed cost半固定本钱S(562)semi-variable cost半变动本钱S(563)sensitivity analysis敏感性分析S(564)service cost center效劳本钱中心S(565)service costing效劳本钱计算S(566)set-up time安装时间S(567)shadow prices影子价格S(568)share股票S(569)share capital股份资本S(570)share option scheme购股权证方案S(571)share premium股票溢价S(572)sight draft即期汇票S(573)single-entry book-keeping单式薄记S(574)sinking fund偿债基金S(575)slack time松驰时间S(576)social responsibility cost社会责任本钱S(577)sole trader独资经营者S(578)source and application of funds statement资金来源和运用表S(579)special order costing特殊定单本钱计算S(580)staff costs职工本钱S(581)standard标准S(582)standard accounting practice标准会计实务S(583)standard cost标准本钱S(584)standard costing标准本钱计算S(585)standard direct labour cost标准直接人工S(586)standard hour标准小时S(587)standard minute标准分钟S(588)standard performace-labour标准人工业绩S(589)standard time标准时间S(590)standard order经常性定单S(591)statement of account营业帐单S(592)statement of affairs财务状况表S(593)statutory body法定实体S(594)stock存货S(595)stock control存货控制S(596)stock turnover存货周转率S(597)stocktaking盘点存货S(598)stores requisition领料申请单S(599)strategic business unit战略性经营单位S(600)strategic management accounting战略管理会计S(601)strategic planning战略方案S(602)strategy战略S(603)subjective classification主体分类S(604)subscribed share capital已认购的股本S(605)subsidiary undertaking子公司S(606)sunk cost漂浮本钱S(607)supply estimate预算估计S(608)supply expenditure预算支出S(609)suspense account暂记XXS(610)SWOT analysis长处和短处,时机和威胁分析S(611)system制度,体系T(612)tactical planning策略方案T(613)tactics策略T(614)take-over接收T(615)tangible asset有形资产T(616)tangible fixed asset statement有形固定资产表T(617)target cost目标本钱T(618)terotechnology设备综合工程学T(619)throughput accounting生产量会计T(620)time时间T(621)time sheet时间记录表T(622)total assets总资产T(623)total quality management全面质量管理T(624)total stocks存货总计T(625)trade creditors购货客户(应付帐款)T(626)trade debtors销货客户(应收帐款)T(627)trading profit and loss account营业损益表T(628)transfer price转让价格T(629)transit time中转时间T(630)treasurership财务长制度T(631)trail balance试算平衡表T(632)turnover营业额U(633)uncalled share capital未催缴股本U(634)under capitalization缺乏资本化U(635)under or over-absorbed overhead少吸收或多吸收的制造费用U(636)uniform accounting统一会计U(637)uniform costing统一本钱计算U(638)unissued share capital未发行股本V(639)value价值V(640)value added增值V(641)value analysis价值分析V(642)value for money audit经济效益审计V(643)variable cost变动本钱V(644)variable cost of sales销售的变动本钱V(645)variance差异V(646)variance accounting差异会计V(647)variance administrative cost行政管理费用差异V(648)variance analysis差异分析V(649)variance budget预算差异V(650)variance direct labour efficiency直接人工效率差异V(651)variance direct labour rate直接人工费率差异V(652)variance direct labour total直接人工总差异V(653)variance direct material mix直接材料构造差异V(654)variance direct materials price直接材料价格差异V(655)variance direct materials total直接材料总差异V(656)variance direct material usage直接材料用量差异V(657)variance direct material yield直接材料产出率差异V(658)variance fixed production overhead expenditure固定生产性制造费用消耗差异V(659)variance fixed production overhead total固定生产性制造费用总差异V(660)variance fixed production overhead volume固定生产性制造费用业务量差异V(661)variance market share市场份额差异V(662)variance market size市场规模差异V(663)variance marketing cost营销本钱差异V(664)variance operational经营差异V(665)variance operational price经营价格差异V(666)variance operation usage经营用量差异V(667)variance planning方案差异V(668)variance planning price方案价格差异V(669)variance quality cost质量本钱差异V(670)variance revision标准修订差异V(674)variance sales mix contribution销售奉献毛益差异V(675)variance sales mix profit销售构造利润差异V(676)variance sales quantity contribution销售数量奉献毛益差异V(677)variance sales quanity profit销售数量利润差异V(678)variance sales turnover销售收入差异V(679)variance sales volume contribution销售业务量奉献毛益差异V(680)variance sales volume profit销售业务量利润差异V(681)variance selling price销售价格差异V(682)variance total profit总利润差异V(683)variance variable production overhead efficiency变动生产性制造费用效率差异V(684)variance variable production overhead expenditure变动生产性制造费用消耗差异V(685)variance variable production overhead total变动生产性制造费用总差异V(686)virement预算流用V(687)vote表决V(688)voucher凭证W(689)waiting time等候时间W(690)waste废品(料)W(691)wasting asset递耗资产W(692)weighted average cost of capital资本的加权平均本钱W(693)weighted average price加权平均价格W(694)with resource有追索权无追索权W(695)without recourseW(696)working capital营运资本W(697)write-down减值Z(698)zero base budgeting零基预算Z(699)zero coupon bond无息债券Z(700)Z score破产预测计分法41 / 41。

ACCA词典

Auditing Dictionary of TermsThe words defined in this dictionary all appeared in questions on the CPA exam, so they are worth knowing if you are studying for the exam. 本字典中定义的单词均出现在注册会计师(美国)的考试之中,如果您正在参与此项考试,那么您值得一读。

acceptance sampling is sampling to determine whether internal control compliance is greater than or less than the tolerable deviation rate.accounting and review services are official pronouncements covering compilation and review engagements. Compilation is presenting in the form of financial statements information that is the representation of management (owners) without expressing assurance. Review is inquiry and analytical procedures to provide the accountant a basis for expressing limited assurance that there are no material modifications that should be made to the statements for them to be in conformity with U.S. generally accepted accounting principles or, if applicable, another comprehensive basis of accounting.accounting data includes journals, ledgers and other records such as spreadsheets that support financial statements. It may be in computer readable form or on paper.accounting estimate An approximation of a financial statement element. Accounting estimates are often included in historical financial statements because measurement of some amounts is uncertain pending outcome of future events and relevant data about events that have occurred cannot be accumulated on a timely, cost-effective basis.accounting principles are alternative ways of reporting and disclosing information in financial statements and related footnotes.accounts receivable Debts due from customers from sales of products and services. Normally a current asset.adjusting entries are accounting entries made at the end of an accounting period to allocate items between accounting periods.adverse An audit opinion that the financial statements as a whole are not presented in conformity with U.S. GAAP.advisory services are a consulting service in which the CPA develops the findings, conclusions, and recommendations presented for client consideration and decision making. This differs from attestation services where the CPAexpresses a conclusion about reliability of a written assertion that is the responsibility of another.aggregate (aggregated) Constituting the whole. Aggregate expenses include expenses of all divisions combined for the entire year.agreed-upon procedures An engagement where the client specifies procedures and the accountant agrees to perform those procedures. An accountant may accept an engagement limited to applying agreed-upon procedures to financial statement elements, where the scope of the engagement is not sufficient to express an opinion on the elements, if the users assume responsibility for sufficiency of the procedures, and use of the report is restricted to specified users.aicpa American Institute of Certified Public Accountants. The professional organization of CPAs in the U.S. It is a private organization of CPAs, not an arm of the government. Each state issues CPA certificates, not the AICPA. Since each state makes its own laws, each state could prepare and grade their own CPA examination. However, each state uses the uniform CPA exam prepared and graded by the AICPA.allocation Distribution according to a plan. Depreciation, amortization, and depletion are methods to allocate a cost to periods benefited.allowance for doubtful accounts A contra asset account with a credit balance used to reduce the carrying amount of accounts receivable to net realizable value. The allowance balance is the estimated total of uncollectible accounts included in accounts receivable.allowance for sampling risk The difference between a sample estimate and the projected population characteristic at a specified sampling risk. This allowance is also the difference between the expected error rate and the tolerable deviation rate.analytical procedure A comparison of financial statement amounts with the auditor's expectation. An example is the comparison of actual interest expense for the year (a financial statement amount) with an estimate of what that interest expense should be. The estimate can be found by multiplying a reasonable interest rate times the average balance of interest bearing debt outstanding during the year (the auditor's expectation). If actual interest expense differs significantly from the expectation the auditor explains the difference in the working papers.analyze Identify and classify items for further study.anticipated Expected.application control Programmed procedure in application software designed to ensure completeness and accuracy of information.approve To authorize. A manager authorizes a transaction by signing a voucher providing approval for the disbursement.ascertain An audit procedure to determine or to discover with certainty. For example, to ascertain the date on which an investment was purchased by examining source documents.assertion Management asserts financial statements are correct with regard to existence or occurrence of assets, liabilities or transactions, completeness of information in the financial statements, rights and obligations at a point in time, appropriate valuation or allocation, presentation, and disclosure.assess To determine the value, significance, or extent of.assessed Determined. The level of control risk determined by the auditor, based on tests of controls, is the assessed level of control risk.assurance The level of confidence one has in a proposition.attest (attestation)report An attest engagement is one in which a practitioner is engaged to issue a written conclusion about the reliability of a written assertion that is the responsibility of another party. A financial statement audit is one type of attestation.attorney's letter is signed by the client's lawyer and addressed to the auditor. It is the auditor's primary means to corroborate information furnished by management about litigation, claims, and assessments.attribute sampling The characteristic tested is a property that has only two possible values (an error exists or it does not).audit adjustment, whether or not recorded by the entity, is a proposed correction of the financial statements that may not have been detected except through audit procedures.audit committee A committee of the board of directors responsible for oversight of the financial reporting process, selection of the independent auditor, and receipt of audit results.audit objective In obtaining evidence in support of financial statement assertions, the auditor develops specific audit objectives in the light of thoseassertions. For example, an audit objective related to the completeness assertion an auditor might develop for inventory balances is that inventory quantities include all products, materials, and supplies on hand.audit planning is developing an overall strategy for the conduct and scope of the audit. The nature, extent, and timing of planning varies with the size and complexity of the entity, experience with the entity, and knowledge of the entity's business.audit risk A combination of the risk that material errors will occur in the accounting process and the risk the errors will not be discovered by audit tests. Audit risk includes uncertainties due to sampling (sampling risk) and to other factors (nonsampling risk).auditing standards board Statements on Auditing Standards are issued by the auditing standards board, the senior technical body of the AICPA designated to issue auditing pronouncements.authorize (authorization)To give permission for. A manager authorizes a transaction by signing a voucher providing authorization for the disbursement.backup A copy of a computer program or file stored separately from the original.batch A set of computer data or jobs to be processed in a single program run.benford's law is a mathematical law that applies to any population of numbers derived from other numbers (such as the dollar amount of a sale, found by multiplying the quantity sold times the unit price). It holds that 30% of the time the first non-zero digit of this derived number will be one, and it will be a nine only 4.6% of the time. Benford's law is used by auditors to identify fictitious populations of numbers.bill of lading A document issued by a carrier to a shipper, listing and acknowledging receipt of goods for transport and specifying terms of delivery.blind trust A financial arrangement in which a person avoids possible conflict of interest by transferring financial affairs to a fiduciary who has sole asset management discretion. The person establishing the trust also gives up the right to information regarding the assets.cancel supporting documents To mark supporting documents as having been used to support a transaction so the same documents can't be used as support for a second transaction. An example is stamping vouchers "paid" and marking them with the check number.capitalized Recorded as an asset. A capitalized lease is in substance a purchase to the lessee. An asset is recorded equal to the present value of the lease payments, which is also recorded as a liability. Payments, partly interest and partly principal, are made on the lease liability. The lease asset is depreciated by the lessee as though it were legally owned by the lessee.caveat A warning or caution.check digit A redundant digit added to a code to check accuracy of other characters in the code.check register A listing of checks issued, normally in numeric sequence and in order by date issued.classification Arrangement or grouping. Assets and liabilities are normally classified as current or noncurrent.collateralize To pledge property as security (collateral) for a debt.collusion A secret agreement between two or more parties for fraud or deceit.comfort letter A letter written by the auditor to an underwriter of securities, which expresses an opinion about whether the audited financial statements and schedules in the registration statement comply as to form with applicable accounting requirements of the Act and related rules and regulations adopted by the SEC. The procedures to be performed are specified by the underwriter. comparability Users evaluate accounting information by comparison. Similar companies account for similar transactions in similar ways. Another goal is comparison of one company's information from one period to the next (consistency). Operating trends should not be disguised by changing accounting methods.comparative Financial statements of a prior period shown with those of the current period to aid in comparisons between periods.compare (comparison) An audit procedure. The auditor observes similarities and differences among similar items such as an account from one year to the next.compensating balance An offsetting balance. A requirement by some banks that a borrower maintain a minimum balance in a checking or savings account as a condition of granting a loan. The offsetting balance increases the effective interest rate to the bank since the net amount loaned is reduced but the interest paid is unchanged.competence of an internal audit staff is a function of qualifications, including education, certification, and supervision. Competent audit evidence is valid and reliablecompile (compilation)A compilation is presenting in the form of financial statements information that is the representation of management without expressing assurance. Compilation of a financial projection is assembling prospective statements based on assumptions of a responsible party, reading the statements, considering appropriateness of presentation, and issuing a compilation report. No assurance is provided on the statements or underlying assumptions. The accountant need not be independent.completeness Assertions about completeness deal with whether all transactions and accounts that should be presented in the financial statements are included. For example, management asserts that all purchases of goods and services are recorded and included in the financial statements. Similarly, management asserts that notes payable in the balance sheet include all such obligations of the entity.compliance Following applicable rules or laws.comprehensive basis of accounting A complete set of rules other than U.S. GAAP applied to all items in a set of financial statements. Examples include a basis of accounting required by a regulatory agency, a basis of accounting the entity uses for its income tax return and the cash receipts and disbursements basis.computer controls Internal controls performed by computer (software controls) as opposed to manual controls. Also means general and application controls over the computer processing of data.condensed financial statements are presented in considerably less detail than complete financial statements.confirm (confirmation) Communication with outside parties to authenticate internal evidence.consignment Transfer of possession but not title to goods. Title stays with the consignor, while the consignee has possession.consistency To achieve comparability of information over time, the same accounting methods must be followed. If accounting methods are changed from period to period, the effects must be disclosed.consulted Sought advice or information.consulting services performed by CPAs include consultations, advisory services, implementation services, product services, transaction services, and staff and support services.contingency is an existing condition involving uncertainty as to possible gain (gain contingency) or loss (loss contingency) that will be resolved by future events. Estimates, such as the useful life of an asset, are not contingencies. Eventual expiration of the asset's utility is not uncertain.continuing auditor is the auditor of the current year who also audited the financial statements of the client for the previous year.continuing accounting significance Matters of continuing accounting significance are those normally included in the permanent audit working paper file, such as the analysis of balance sheet accounts, and those relating to contingencies. Such information from a prior year is used by the auditor in the current year's audit and is updated each year.control A policy or procedure that is part of internal control.control environment is the attitude, awareness, and actions of the board, management, owners, and others about the importance of control. This includes integrity and ethical rules, commitment to competence, board or audit committee participation, organizational structure, assignment of authority and responsibility, and human resource policies and practices.control policies and procedures Control activities are the policies and procedures that help ensure management directives are carried out. Those pertinent to an audit include performance reviews, information processing, physical controls and segregation of duties.control risk The risk that material error in a balance or transaction class will not be prevented or detected on a timely basis by internal controls.controller An officer who supervises financial affairs of an entity. In internal control the controller is often the person with recordkeeping (general ledger) responsibilities, as contrasted with asset custody, management decision making, and internal audit functions.corroborate(corroborating) (corroboration) (corroborative) To strengthen with other evidence, to make more certain.count Enumerate some characteristic such as the number of items in inventory.cumulative effect of changing to a new accounting principle is the effect on retained earnings at the beginning of the current period. It is included in net income after extraordinary items. Only the direct effect (net of income tax effect) is considered.current ratio Total current assets divided by total current liabilities.custodian One that has possession or is in charge of something. Some entities entrust marketable investment securities to a bank which is custodian of the company's securities.custody Possession.cutoff Designating a point of termination. An auditor uses tests of cutoff to obtain evidence that transactions for each year are included in the financial statements of the appropriate year.defalcation To misuse or embezzle funds.deficiency An internal control shortcoming or opportunity to strengthen internal controls.detection risk The risk audit procedures will lead to a conclusion that material error does not exist when in fact such error does exist.detective control A control designed to discover an unintended event or result.deviation Departure from prescribed internal control. Often expressed as a rate at which the departure occurs.disclaimer (disclaim) A statement that the auditor is unable to express an opinion as to the presentation of financial statements in conformity with U.S. GAAP.disclosure Revealing information. Financial statement footnotes are one way of providing necessary disclosures.discovery sampling Acceptance sampling (sampling to determine whether internal control compliance is greater than or less than the tolerable deviation rate) when expected attribute occurrence rate is zero.document(documentary) (documentation) Written or printed paper that bears information that can be used to furnish decisive evidence. Could also be a recording, computer readable information, or a photograph.dual date If a major event comes to the auditor's attention between the report date and issuance of the report, the financial statements may include the event as an adjustment or disclosure. The auditor dual dates the audit report (as of the end of fieldwork, except footnote XX, which is dated later).dual-purpose test Audit procedures are classified as substantive tests or tests of controls. If a procedure provides both types of evidence it is a dual-purpose test.edi “Electronic Data Interchange” is the use of communication between an entity and customers or suppliers to transact business electronically. Purchase, shipping, billing, cash receipt, and cash disbursements can be completed entirely by exchanging electronic messages.edit check Reasonableness, validity, limit, and completeness tests that are programmed routines designed to check input data and processing results for completeness, accuracy and reasonableness.edp“Electronic Data Processing”. Processing of information by computer as opposed to handwritten records.effective income tax rate The income tax provision (expense) shown on an income statement divided by the pretax income. This differs from the statutory rate because of deductions, credits, and exclusions.effective internal control Reasonable assurance that the entity’s operational objectives are achieved, that published financial statements are reliably prepared, and applicable laws and regulations are complied with.effectiveness Producing a desired outcome. An audit procedure is effective if the evidence supports a correct conclusion.efficiency The ratio of the audit evidence produced to audit resources used.embedded control performance deals with unexpected changes to data.embezzlement To take assets in violation of trust.encryption is scrambling data so it is meaningless to anyone but the intended recipient, who has the key to unscramble the data.engagement letter A letter that represents the understanding about the engagement between the client and the CPA. The letter identifies the financial statements and describes the nature of procedures to be performed. It includes an explanation of the objectives of the procedures, an explanation that thefinancial information is the responsibility of the company's management, and a description of the form of report.environment The control environment is the attitude, awareness, and actions of the board, management, owners, and others about the importance of control. This includes integrity and ethical rules, commitment to competence, board or audit committee participation, organizational structure, assignment of authority and responsibility, and human resource policies and practices.error Unintentional misstatements or omissions in financial statements. Errors may involve mistakes in gathering or processing accounting data, incorrect estimates from oversight or misinterpretation of facts, and mistakes in application of principles relating to amount, classification, presentation or disclosure.estimation sampling is sampling to estimate the actual value of a population characteristic within a range of tolerable misstatement.evidence (evidential matter) includes written and electronic information (such as checks, records of electronic fund transfers, invoices, contracts, and other information) that permits the auditor to reach conclusions through reasoning.examination An examination of prospective financial statements is evaluation of preparation of the prospective statements, support underlying assumptions, and presentation. The accountant reports whether, in his or her opinion, the statements are presented in conformity with AICPA guidelines and the assumptions provide a reasonable basis for the responsible party's forecast. The accountant should be independent, proficient, adequately plan the engagement, supervise assistants, and obtain sufficient evidence to provide a reasonable basis for the report.examine (examining) As an audit procedure, to examine something is to look at it critically.except for A qualified opinion. An auditor can qualify the audit opinion for both departures from U.S. GAAP in the financial statements and for restrictions on the scope of the audit. The opinion paragraph of the qualified report is worded "In our opinion, except for..."execute (execution) To carry out an internal control procedure, such as to sign and mail a check after inspecting supporting documents.existence Assertions about existence deal with whether assets or liabilities exist at a given date. For example, management asserts that finished goods inventories in the balance sheet are available for sale.expenditure Cash paid or liability incurred.explanatory A paragraph added to an audit report to explain something, such as the reason for a qualified or adverse opinion.explicitly Fully and clearly expressed, leaving nothing implied.extend means to multiply one number by another (to test extensions is to test the accuracy of multiplication done by the client). To extend audit procedures is to apply additional audit procedures to obtain more evidence.fasab Federal Accounting Standards Advisory Board. An organization that sets GAAP in the United States for federal government entities.fasb Financial Accounting Standards Board. A nongovernment private organization that sets GAAP in the United States for profit making entities and not-for-profit nongovernmental organizations.field work The performance of audit procedures outside the CPA's office. Much field work, but not all, is done in the client's offices after the balance sheet date.fifo“First In First Out” inventory cost flow.financial forecasts present expected future financial position, results of operations, and cash flows based on expected conditions.financial institution confirmation request A confirmation sent to the client's bank or other financial institution asking the bank to confirm direct to the auditor information about balances at a particular date.flowchart A schematic representation of a sequence of operations in an accounting system or computer program. Also called a flow diagram, flow sheet.foot a column is to add a column of numbers.fraud A deliberate deception to secure unfair or unlawful gain. False representation intended to deceive relied on by another to that person's injury. Fraud include fraudulent financial reporting undertaken to render financial statements misleading, sometimes called management fraud, and misappropriation of assets, sometimes called defalcations.gaap“Generally Accepted Accounting Principles.” According to Rule 203 of the AICPA Code of Professional Conduct, GAAP for nongovernment entities include (in a conflict the source earlier in the list prevails): 1. FASB Statementsand Interpretations, APB Opinions, ARBs. 2. FASB Technical Bulletins, AICPA Guides and AICPA Statements of Position. 3. Positions of the FASB Emerging Issues Task Force and AICPA Practice Bulletins. 4. AICPA accounting interpretations, FASB staff "Qs and As", and widely recognized industry practices. 5. Other accounting literature, such as FASB Concepts Statements, textbooks, articles.gaas “Generally Accepted Auditing Standards.” The ten auditing standards adopted by the membership of the AICPA. Auditing standards differ from audit procedures in that "procedures" relate to acts to be performed, whereas "standards" deal with measures of the quality of the performance of those acts and the objectives to be attained by use of the procedures undertaken.gasb Government Accounting Standards Board. A nongovernment private organization that sets GAAP in the United States for governmental entities.general controls Policies and procedures to assure proper operation of computer systems, including controls over data center and network operations, software acquisition and maintenance, and access security.general journal A book of original entry in a double-entry system. The journal lists transactions and indicates accounts to which they are posted. The general journal includes all transactions which aren't included in specialized journals used for cash receipts, cash disbursements, and other common transactions.general ledger A record to which monetary transactions are posted (in the form of debits and credits) from a journal. It is the final record from which financial statements are prepared. General ledger accounts are often control accounts which report totals of details included in subsidiary ledgers.general standard In the ten U.S. generally accepted auditing standards there are three general standards: 1. The examination is to be performed by a person or persons having adequate technical training and proficiency as an auditor. 2. In all matters relating to the assignment, an independence in mental attitude is to be maintained by the auditor. 3. Due professional care is to be exercised in the performance of the examination and preparation of the report. generalized audit software Packaged computer programs used on a variety of computers during audit field work to read computer files, select information, perform calculations, create data files and print reports in a format specified by the auditor.going concern assumption assumes the company will continue in operation long enough to realize its investment in assets through operations (as opposed to sale). Presenting assets at historical cost is justified by assuming productiveassets will be used rather than sold. This makes market values irrelevant and supports accounting methods which match the actual cost of an asset to periods benefited.government auditing standards A book issued by the comptroller general of the United States, sometimes called the "yellow book." Government Auditing Standards contains standards for audits of government organizations, programs, activities, and functions and of government assistance received by contractors, not-for-profit organizations, and other nongovernment organizations. These standards, which include designing the audit to provide reasonable assurance of detecting material misstatements resulting from noncompliance with provisions of contracts or grant agreements that have a direct and material effect on determination of financial statement amounts, are to be followed when required by law, regulation, agreement, contract, or policy. For financial audits, Government Auditing Standards prescribes fieldwork and reporting standards beyond those required by GAAS.gross margin percentage The gross margin from an income statement divided by net sales revenue.hard copy A printed copy of information as opposed to information stored in computer readable form.hardware A computer and associated physical equipment involved in data-processing or communications functions as opposed to software or computer programs that provide instructions the computer follows.hardware control Computer controls built into physical equipment by the manufacturer.hash total A control total which has no meaning in itself other than for control, e.g., total social security numbers of employees paid.hedges protect an entity against the risk of adverse price or interest-rate movements on its assets, liabilities, or anticipated transactions. A hedge is used to avoid or reduce risks by creating a relationship by which losses on positions are counterbalanced by gains on separate positions in another market.image processing systems use scanning to convert documents into electronic images to facilitate storage. Reference and source documents may not be retained after conversion.immaterial Of no importance. Something in financial statements that will not change decisions of investors.。

ACCA教材词汇(4)

未实现利润准备 Provision for unrealized profit

应收租购款帐户 Hire purchase debtors account

重新获得帐户 Repossessions account

金融公司 Finance house

制造商 Manufacturer

一期(二期)租赁 Primary(secondary)period

不可撤销的付款 No-cancelable payment

名义租金 Peppercorn rent

报酬 Reward

现值 Present value

最低租赁付款额 Minimum lease payment

定金 Deposit

公允价值 Fair value

交易商 Dealer

总盈余 Gross earnings

政府补助 Government grant

租赁期 Lease term

平均未付资本余额averagebalanceofcapitaloutstanding

ACCA教材词汇(4)

ACCA教材词汇

信用协议 Credit agreement

会计处理 Accounting treatment

经营性租赁 Operating lease

融资租赁 Finance lease

出租人/承租人 Lesser /lessee

财务费用 Finance charge

实际利率 Effective rate பைடு நூலகம்f finance charge

平均未付资本余额 Average balance of capital outstanding

资本偿还 Capital repayment

最新ACCA高盛财经词典-英汉对照版汇总

A C C A高盛财经词典-英汉对照版高盛财经词典 - 英汉对照AEnglish Terms中文翻译详情解释/例子Accelerated Depreciation 加快折旧任何基于会计或税务原因促使一项资产在较早期以较大金额折旧的折旧原则Accident and Health Benefits 意外与健康福利为员工提供有关疾病、意外受伤或意外死亡的福利。

这些福利包括支付医院及医疗开支以及有关时期的收入。

Accounts Receivable (AR) 应收账款客户应付的金额。

拥有应收账款指公司已经出售产品或服务但仍未收取款项Accretive Acquisition 具增值作用的收购项目能提高进行收购公司每股盈利的收购项目Acid Test 酸性测试比率一项严谨的测试,用以衡量一家公司是否拥有足够的短期资产,在无需出售库存的情况下解决其短期负债。

计算方法:(现金 + 应收账款 +短期投资)‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾流动负债Act of God Bond 天灾债券保险公司发行的债券,旨在将债券的本金及利息与天然灾害造成的公司损失联系起来Active Bond Crowd 活跃债券投资者在纽约股票交易所内买卖活跃的定息证券Active Income 活动收入来自提供服务所得的收入,包括工资、薪酬、奖金、佣金,以及来自实际参与业务的收入Active Investing 积极投资包含持续买卖行为的投资策略。

主动投资者买入投资,并密切注意其走势,以期把握盈利机会Active Management 积极管理寻求投资回报高于既定基准的投资策略Activity Based Budgeting 以活动为基础的预算案一种制定预算的方法,过程为列举机构内每个部门所有牵涉成本的活动,并确立各种活动之间的关系,然后根据此资料决定对各项活动投入的资源Activity Based Management 以活动为基础的管理利用以活动为基础的成本计算制度改善一家公司的运营Activity Ratio 活动比率一项用以衡量一家公司将其资产负债表内账项转为现金或营业额的能力的会计比率Actual Return 实际回报一名投资者的实际收益或损失,可用以下公式表示:预期回报加上公司特殊消息及总体经济消息Actuary 精算保险公司的专业人员,负责评估申请人及其医疗纪录,以预测申请人的寿命Acquisition 收购一家公司收购另一家公司的多数股权Acquisition Premium 收购溢价收购一家公司的实际成本与该公司收购前估值之间的差额Affiliated Companies 联营公司一家公司拥有另一家公司少数权益(低于50%)的情况,或指两家公司之间存在某些关联Affiliated Person 关联人士能影响一家企业活动的人士,包括董事、行政人员及股东等After Hours Trading 收盘后交易主要大型交易所正常交易时间以外进行的买卖交易After Tax Operating Income - ATOI 税后营运收入一家公司除税后的总营运收入。

ACCA新手必看的财经词典

财经词典-英汉对照AEnglish Terms 中文翻译详情解释/例子Accelerated Depreciation 加快折旧任何基于会计或税务原因促使一项资产在较早期以较大金额折旧的折旧原则Accident and HealthBenefits 意外与健康福利为员工提供有关疾病、意外受伤或意外死亡的福利。

这些福利包括支付医院及医疗开支以及有关时期的收入。

Accounts Receivable (AR)应收账款客户应付的金额。

拥有应收账款指公司已经出售产品或服务但仍未收取款项Accretive Acquisition 具增值作用的收购项目能提高进行收购公司每股盈利的收购项目Acid Test 酸性测试比率一项严谨的测试,用以衡量一家公司是否拥有足够的短期资产,在无需出售库存的情况下解决其短期负债。

计算方法:(现金+应收账款+短期投资)‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾‾流动负债Act of God Bond 天灾债券保险公司发行的债券,旨在将债券的本金及利息与天然灾害造成的公司损失联系起来Active Bond Crowd活跃债券投资者在纽约股票交易所内买卖活跃的定息证券Active Income 活动收入来自提供服务所得的收入,包括工资、薪酬、奖金、佣金,以及来自实际参与业务的收入Active Investing 积极投资包含持续买卖行为的投资策略。

主动投资者买入投资,并密切注意其走势,以期把握盈利机会Active Management 积极管理寻求投资回报高于既定基准的投资策略Activity Based Budgeting 以活动为基础的预算案一种制定预算的方法,过程为列举机构内每个部门所有牵涉成本的活动,并确立各种活动之间的关系,然后根据此资料决定对各项活动投入的资源Activity Based Management以活动为基础的管理利用以活动为基础的成本计算制度改善一家公司的运营Activity Ratio 活动比率一项用以衡量一家公司将其资产负债表内账项转为现金或营业额的能力的会计比率a c c aActual Return 实际回报一名投资者的实际收益或损失,可用以下公式表示:预期回报加上公司特殊消息及总体经济消息Actuary 精算保险公司的专业人员,负责评估申请人及其医疗纪录,以预测申请人的寿命Acquisition收购一家公司收购另一家公司的多数股权Acquisition Premium收购溢价收购一家公司的实际成本与该公司收购前估值之间的差额Affiliated Companies 联营公司一家公司拥有另一家公司少数权益(低于50%)的情况,或指两家公司之间存在某些关联Affiliated Person 关联人士能影响一家企业活动的人士,包括董事、行政人员及股东等After Hours Trading收盘后交易主要大型交易所正常交易时间以外进行的买卖交易After Tax OperatingIncome -ATOI税后营运收入一家公司除税后的总营运收入。

ACCA教材词汇表

ACCA教材词汇表。

独资企业Sole trader 收购公司Purchasing company银行透支Bank overdraft 开帐分录Opening entry购货退回Return outwards 接管Take over销货退回Return inwards 企业收购帐户Business purchase account 毛利Gross profit 卖主帐户Vendor account租金与地方税Rent and rates 留存收益Retained earnings收到的折扣Discount received 普通股股本Ordinary share capital给与的折扣Discount allowed 优先股股本Preference share capital要求权Claim 债券Debentures提款Drawings 损益表Profit and loss account合伙企业Partnership 股东年会General meeting合伙人Partner 真实/公允True and fair合伙协议Partnership agreement 推销成本Distribution cost资本利息Interest on capital 投资注销额Amount written-offinvestment剩余利润Residual profit 自建工程资本化Own work capitalized分配Appropriation 集团内股票收入Income from shares in groupunder takings盈亏分配帐户Profit and loss appropriation 其他股票收入Income from shares in otherparticipating interests结转下期余额Balance carried down 自有股Own shares上期结转余额Balance Brought down 负债准备Provisions for liabilities 合伙人贷款Partner’s loan养老金Pensions合作企业Joint venture 资本赎回公积Capital redemption reserve 合作企业备查帐户Memorandum joint venture 按公司章程保留的公积Reserve provided for by thearticles of association杂费Sundry expenses 公司所得税Corporation tas (CT)佣金Commission 财政年度Financial year运出运费Carriage outwards 预交公司所得税Advanced corporationtax(ACT)运入运费Carriage inwards 主体公司所得税Mainstream corporationtax(MCT)联合银行存款帐户Joint bank account 所得税率适用年度CT year商誉Goodwill 税金抵免Tax credit重估价法Revaluation method 税收机构Inland revenue合并Amalgamation 应纳税利润Taxable profit合并前Pre-Amalgamation 公司所得税准备Provision fo CT合并后Post-Amalgamation 应抵预交公司所得税ACT recoverable通过支付年金清偿Discharge by payment of应付公司所得税ACT payableannuity年金暂记帐户Annuity suspense account 预算报告Budget speech保险金Premiums 资本收益Capital gain退保价值Surrender value 小公司税率Small companies rate人寿保险政策帐户Life assurance policies边际利率Marginal rateaccount贸易表Trading account 完全税率Full rate终止Cessation 免税投资收益Franked investment income变卖资产帐户Realization account 资本减免Capital allowances合伙企业的解体Dissolution of partnership 剩余预交公司所得税Surplus ACT最后约定的资本Last agreed capital 寄售业务Consignment trading 逐步解体Piecemeal dissolution 汇票Bills of exchange变卖资产费用准备Provision for realizationexpense分支机构Branch变卖资产损失Loss on realization 代理商Agent股票帐户Shares account 交易商Trader英国境内公司UK resident company 受托人Consignee非免税收入Un-franked receipts 委托人,寄售人Consigner公司所得税费用CT charge 保障,赔偿Indemnity代扣所得税的交纳Payment under deduction of IT 销售帐单Account sales磨损Wear and tear 寄售利润Profit on consignment 拥有法定所有权的土地Freehold land 进口税Import duties过时Obsolescence 运费Delivery to customers开采或消耗Extraction of consumptionover time 途中保险费Carriage insurance on goodsdelivered to Customers直线法Straight line method 佣金Commission余额递减法Reducing balance method 汇付Remittance年数总和法Sum of the digits method 未售存货Unsold stock累计折旧Accumulated depreciations 应收票据Bills receivable 经济使用年限Useful economic lives 保险收入Insurance proceeds 每股净收益Earnings per share 面值Face value例外项目Exceptional items 贴现费用Discount charges 非常项目Extraordinary items 财务费用Financing cost前期调整Prior year adjustment 应付票据Bills payable不能抵销的预交公司税Irrevocable advancedcorporation tax支出Expenditure未抵销的损失Unrelieved losses 即期汇票Sight drafts净值基础Net basis 监管Custody零值基础Nil basis 主损益帐户Main profit and loss account 消耗品Consumable stores 部门化Departmentalization成本与可实现净值孰低The lower of cost and netrealizable value分摊Apportionment平均成本Average cost 共同性费用Common expense先进先出First in first out 包装纸Wrapping paper后进先出Last in first out 评价Assess标准成本Standard cost 独立实体Independent entity重置成本Replacement cost 投资报酬率Return on investment 资产负债表日后日期Event after balance sheet date 减除佣金后利润Post-commission profit 董事会The board of directors 赊销收入Credit sales调整事项Adjusting event 修理费用Repair charges非调整事项Non-adjusting event 一般费用General expense或有事项Contingencies 分支销售机构Selling agency branch 或有收益Contingent gain 正常存货损失Normal stock losses或有损失Contingent loss 交易帐户Trading account资本承诺Capital commitments 非常存货损失Abnormal stock losses现金流量表Cash flow statement 本地购货Local purchase信用交易Credit transaction 退货Returned goods独立分支机构Independent branch现实购买力会计Current purchasing poweraccounting (CPP)现实成本会计Current cost accounting(CCA) 往来帐户Current account零售物价指数Retail price index 复式簿记帐户Double-entry accounts持有收益Holding gains 时间差异Time lag differences业绩评估Assessment of performance 分支机构间转移Inter-branch transfer货币性项目的衡量Measurement of monetary items 结算Settlement货币性资产Monetary assets 分支机构间往来帐户Interbranch current account 货币性负债Monetary liabilities 分支机构存货调整帐户Branch stock adjustmentaccount征求意见稿Exposure draft 未实现利润准备Provision for unrealizedprofit实现原则Realization货币性营运资本调整Monetary working capitaladjustment举债比率调整Gearing adjustment 货币折算Currency translation净营业资产Net operating assets 货币兑换Currency conversion发行和赎回债券Issue and redemption当地货币Local currencydebentures债券Bonds 汇率Exchange rate契约Deed 即期汇率Spot rate无担保债券Naked-debentures(unsecured) 远期合同Forward contract拥有法定所有权的Freehold 贴水Discount偿债基金Sinking fund 升水Premium货币性项目Monetary items债券赎回偿债基金Debenture redemption sinkingfund account风险Risk偿债基金投资帐户Sinking fund investmentaccount可转换债券Convertible debentures 不确定性Uncertainty资本化发行Capitalization issue 套期保值Hedging股权发行Bonus issue 长期货币性资产Long-term monetary assets 含权价Cum-rights prices 长期货币性要求权Long-term monetary claims 除权价Ex-rights prices 汇兑收益/损失Exchange rate gain/loss可分配公积Distributable of reserves 时态法Temporal method历史汇率法Historic method以公积支付股利Paying a dividend out ofreserve已付清红利股Paid-up bonus shares 期末汇率法Closing rate method重估公积Revaluation reserve 场地费用Site expenses减资Capital reductions 管理费用Administrative expenses资本重组Capital reorganizations 装置和设备Furniture and fittings过剩资本Excess capital 房屋Premises资本重建Capital reconstruction 预付费用Payment in advance权益汇总帐户Sundry members account 建造合同Construction contract实现帐户Realization account 工程保留款Retention购买者帐户Purchaser’s account分期付款Progress payment自愿清算Voluntary liquidation 交易帐户Trading account特别决议Special resolution 合同收入Contract fee方案\计划Scheme 合同亏损Loss on contract清偿\偿还Discharge 完工百分比Percentage of completion卖方帐户Vendor account 完成合同Completed contract创立合并Amalgamation 预期利润Expected profit高估Over-valuation 承建商Contractor低估Under-valuation 矫正Rectification集团报表Group accounts 已鉴定完工价值Value of work certified纵向联合Vertical integration 总部费用Head office costs横向联合Horizontal integration 合同成本Contract costs不同行业联合Diversification 销售收入Turnover控股公司Holding company 合同损失准备Provision for loss oncontract重大影响Dominant influence 预收款Payment on account直接控制集团Direct group 可预见损失Foreseeable loss垂直控制集团Vertical group 已付款超过收入(部分) Excess progress payment混合控制集团Mixed group 股票/证券Stock ,security盈余公积Revenue reserve 债券Debenture合并公积Consolidation reserve 法定权利Legal rights少数股权Minority interests 报价Quote合并商誉Goodwill on consolidation 证券交易所Stock exchange上市投资Listed investment合并资本公积Capital reserve onconsolidation少数股东Minority share holders 偿还Repayment股本溢价Share premium 累积股息Cum div cd部分收购Partial acquisition 累积利息Cum-int ci在途支票Cheque in the post 股息除外Ex-div xd收买前后Pre( post)-acquisition 利息除外Ex-int xi调整帐户Adjustment accounts 面值Nominal value对子公司投资Investment in subsidiary 市价Market value普通公积General reserve 应计股利Accrued dividend参与股权Participating interest 应计利息Accrued interest集团内部交易Intra-group trading 证券交易所官方清单Stock exchange official list 公司间销售Inter-company sales 二级市场Secondary market溢价Premium 未上市证券市场Unlisted securities market 折价Discount 让与,出售disposal债券利息Debenture interest 加权平均Weighted分次购买Piecemeal acquisition 结帐Close off关联公司Associated company 已分派股份Allocated shares多数股权Majority holding 国库券Treasury stock累计控股Cumulative holding 认股权发行Rights issue孙公司Sub-subsidiary 赊销Credit sale子集团,附属集团Sub-group 租购Hire purchase多公司结构Multi-company structures 信用协议Credit agreement伙伴子公司Fellow subsidiaries 会计处理Accounting treatment有效股权Effective shareholdings 经营性租赁Operating lease控制股权Controlling interest 融资租赁Finance lease资本报酬率Return on capital employed 出租人/承租人Lesser /lessee产权收益率Returen on equity 一期(二期)租赁Primary(secondary)period息税前净利Net Profit before interest andtax不可撤销的付款No-cancelable payment应收帐款帐龄表Aging schedule of debtors 名义租金Peppercorn rent资金来源及运用表Source and application offunds statement报酬Reward通货膨胀Inflation 现值Present value通货紧缩Deflation 最低租赁付款额Minimum lease payment损耗Deplete 定金Deposit每股收益Earnings per share 公允价值Fair value股利保证倍数Dividend cover 财务费用Finance charge股利分配率Dividend payout ratio 实际利率Effective rate of financecharge股利收益率Dividend yield ratio 平均未付资本余额Average balance of capitaloutstanding净收益率Earnings yield 资本偿还Capital repayment市盈率Price/ earnings ratio 精确法Actuarial method公司估价The valuation of components 递延收益Deferred income联营公司Associated companies 分期支付Installment共同比财务报表Common-size financialstatements 未实现利润准备Provision for unrealizedprofit物质资源Physical resources 应收租购款帐户Hire purchase debtorsaccount会计原则Accounting principles 重新获得帐户Repossessions account 会计方法Accounting methods 金融公司Finance house权责发生制Accrual accounting 制造商Manufacturer重置成本Replacement cost 交易商Dealer一般会计原则Generally accepted accountingprinciples(GAAP)总盈余Gross earnings剩余现金Cash surplus 政府补助Government grant净值减免Writing down allowance 租赁期Lease term。

acca专业英文词汇

acca专业英文词汇1. Accounting: 会计2. Auditing: 审计3. Bookkeeping: 簿记4. Business analysis: 商业分析5. Capital: 资本6. Cash flow: 现金流7. Cost accounting: 成本会计8. Credit: 信用9. Debtor: 债务人10. Equity: 股权11. Expenses: 费用12. Financial statements: 财务报表13. Fixed assets: 固定资产14. Float: 浮存金15. Forecasting: 预测16. Fraud: 欺诈17. General ledger: 总分类账18. Income: 收入19. Internal control: 内部控制20. Inventory: 存货21. Ledger: 分类账22. Liabilities: 负债23. Margins: 利润24. Management accounting: 管理会计25. Market research: 市场研究26. Merchandise: 商品27. Net worth: 净值28. Partnership: 合伙企业29. Payroll: 工资单30. Profits: 利润31. Return on investment (ROI): 投资回报率32. Revenue: 收入33. Shareholder: 股东34. Stock: 股票35. Tax: 税36. Trial balance: 试算平衡表37. Variable costs: 可变成本38. Working capital: 营运资本These are just a few of the many accounting and business-related terms used in the ACCA. Studying for the ACCA requires a good understanding of these and other financial concepts and terminology.。

ACCA专业词汇

A

• Accumulated income 累计收ru • Accumulation 累计额,资本增益 • Accuracy 准确性 • Acid test ratio 酸性测试比率 • Acquired surplus 并购公积 • Acquisition cost 购置成本,取得成本 • Activity 作业,活动 • Activity account 作业账户 • Activity accounting 作业会计 • Activity analysis 作业分析

美国会计准则执行委员会 • Accounting system 会计制度,会计系统 • Accounting trends and techniques 《会计趋势和技术》 • Accounting valuation 会计计价 • Accounts payable 应付账款 • Accounts receivable 应收账款 • Accounts receivable discounted 应收账款贴现

A

• Activity cost pool 作业成本库 • Activity dictionary 作业词典 • Activity driver analysis 作业动因分析 • Activity level 作业水平 • Activity sequence-sensitive 作业次序敏感度 • Actual cost 实际成本 • Actuarial 精算 • Actuarial basis of accounting 精算会计 • Actuarial cost method 精算成本法 • Actuarial funding method 精算基金法

A

• Activity attributes 作业属性 • Activity base 作业基础 • Activity-based budgeting (ABB) 作业预算编制 • Activity-based management (ABM) 作业管理 • Activity-based system 作业体系 • Activity capacity 作业能力 • Activity center 作业中心 • Activity cost assignment 作业成本分配 • Activity cost driver 作业成本动因

ACCA教材词汇

ACCA教材词汇ACCA教材词汇独资企业 Sole trader银行透支 Bank overdraft购货退回 Return outwards销货退回 Return inwards毛利 Gross profit租金与地方税 Rent and rates收到的折扣 Discount received给与的折扣 Discount allowed要求权 Claim提款 Drawings合伙企业 Partnership合伙人 Partner合伙协议 Partnership agreement资本利息 Interest on capital剩余利润 Residual profit分配 Appropriation盈亏分配帐户 Profit and loss appropriation结转下期余额 Balance carried down上期结转余额 Balance Brought down合伙人贷款Partner’s loan合作企业 Joint venture合作企业备查帐户 Memorandum joint venture 杂费 Sundry expenses佣金 Commission运出运费 Carriage outwards运入运费 Carriage inwards联合银行存款帐户 Joint bank account商誉 Goodwill重估价法 Revaluation method合并 Amalgamation合并前 Pre-Amalgamation合并后 Post-Amalgamation通过支付年金清偿 Discharge by payment of annuity 年金暂记帐户 Annuity suspense account保险金 Premiums退保价值 Surrender value人寿保险政策帐户 Life assurance policies account 贸易表 Trading account终止 Cessation变卖资产帐户 Realization account合伙企业的`解体 Dissolution of partnership最后约定的资本 Last agreed capital逐步解体 Piecemeal dissolution变卖资产费用准备 Provision for realization expense 变卖资产损失 Loss on realization股票帐户 Shares account英国境内公司 UK resident company非免税收入 Un-franked receipts公司所得税费用 CT charge代扣所得税的交纳 Payment under deduction of IT 磨损 Wear and tear拥有法定所有权的土地 Freehold land过时 Obsolescence开采或消耗 Extraction of consumption over time 直线法 Straight line method余额递减法 Reducing balance method年数总和法 Sum of the digits method累计折旧 Accumulated depreciations经济使用年限 Useful economic lives每股净收益 Earnings per share例外项目 Exceptional items非常项目 Extraordinary items前期调整 Prior year adjustment不能抵销的预交公司税 Irrevocable advanced corporation tax 未抵销的损失 Unrelieved losses净值基础 Net basis零值基础 Nil basis消耗品 Consumable stores成本与可实现净值孰低The lower of cost and net realizable value平均成本 Average cost先进先出 First in first out后进先出 Last in first out标准成本 Standard cost重置成本 Replacement cost资产负债表日后日期 Event after balance sheet date董事会 The board of directors调整事项 Adjusting event非调整事项 Non-adjusting event或有事项 Contingencies或有收益 Contingent gain或有损失 Contingent loss资本承诺 Capital commitments现金流量表 Cash flow statement信用交易 Credit transaction现实购买力会计 Current purchasing power accounting (CPP) 现实成本会计 Current cost accounting(CCA)零售物价指数 Retail price index持有收益 Holding gains业绩评估 Assessment of performance货币性项目的衡量 Measurement of monetary items货币性资产 Monetary assets货币性负债 Monetary liabilities征求意见稿 Exposure draft货币性营运资本调整 Monetary working capital adjustment举债比率调整 Gearing adjustment净营业资产 Net operating assets发行和赎回债券 Issue and redemption debentures债券 Bonds契约 Deed无担保债券 Naked-debentures(unsecured)拥有法定所有权的 Freehold偿债基金 Sinking fund债券赎回偿债基金Debenture redemption sinking fund account偿债基金投资帐户 Sinking fund investment account可转换债券 Convertible debentures资本化发行 Capitalization issue股权发行 Bonus issue含权价 Cum-rights prices除权价 Ex-rights prices可分配公积 Distributable of reserves以公积支付股利 Paying a dividend out of reserve已付清红利股 Paid-up bonus shares重估公积 Revaluation reserve下载文档。

ACCA词汇

Carriage insurance on goods delivered to Customers

直线法

Straight line method

佣金

Commission

余额递减法

Reducing balance method

汇付

Remittance

年数总和法

Sum of the digits method

普通股股本

Ordinary share capital

给与的折扣

Discount allowed

优先股股本

Preference share capital

要求权

Claim

债券

Debentures

提款

Drawings

损益表

Profit and loss account

合伙企业

Partnership

股东年会

未售存货

Unsold stock

累计折旧

Accumulated depreciations

应收票据

Bills receivable

经济使用年限

Useful economic lives

保险收入

Insurance proceeds

每股净收益

Earnings per share

面值

Face value

例外项目

Financial year

运出运费

Carriage outwards

预交公司所得税

Advanced corporation tax(ACT)

运入运费

Carriage inwards

主体公司所得税

Mainstream corporation tax(MCT)

ACCA考试必备财务英语词汇