会计报表2012.08北欧荣堡(1)

2012年初级会计课本上的会计报表模板

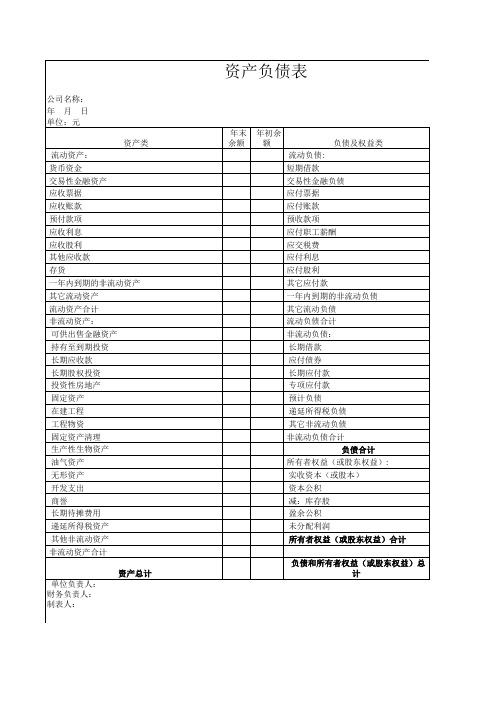

公司名称: 资产类 流动资产: 货币资金 交易性金融资产 应收票据 应收账款 预付款项 应收利息 应收股利 其他应收款 存货 一年内到期的非流动资产 其它流动资产 流动资产合计 非流动资产: 可供出售金融资产 持有至到期投资 长期应收款 长期股权投资 投资性房地产 固定资产 在建工程 工程物资 固定资产清理 生产性生物资产 油气资产 无形资产 开发支出 商誉 长期待摊费用 递延所得税资产 其他非流动资产 非流动资产合计 资产总计 单位负责人: 负债和所有者权益(或股东权益)总计 财务负责人: 年末余额 年初余额 流动负债: 短期借款 交易性金融负债 应付票据 应付账款 预收款项 应付职工薪酬 应交税费 应付利息 应付股利 其它应付款 一年内到期的非流动负债 其它流动负债 流动负债合计 非流动负债: 长期借款 应付债券 长期应付款 专项应付款 预计负债 递延所得税负债 其它非流动负债 非流动负债合计 负债合计 所有者权益(或股东权益): 实收资本(或股本) 资本公积 减:库存股 盈余公积 未分配利润 所有者权益(或股东权益)合计 年 月 日 负债及权益类

单位负责人:

财务负责人:

制表人:

表1 单位:元 年末余额 年初余额

东权益)总计 制表人:

:

单位:元

投资活动产生的现金流量净额 三、筹资活动产生的现金流量: 1.吸收投资收到的现金 3.取得借款收到的现金 3.收到其他与筹资活动有关的现金 筹资活动现金流入小计 1.偿还债务支付的现金 2.分配股利、利润或偿付利息支付的现金 3.支付其他与筹资活动有关的现金 筹资活动现金流出小计 筹资活动产生的现金净流量净额 四、汇率变动对现金及现金等价物的影响 五、现金及现金等价物净增加额 加:期初现金及现金等价物余额 六、期末现金及现金等价物余额

会计报表中英文对照

一、企业财务会计报表封面 FINANCIAL REPORT COVER 报表所属期间之期末时间点 PeriodEnded 所属月份 Reporting Period 报出日期 Submit Date 记账本位币币种 Local Reporting Currency 审核人 Verifier 填表人 Preparer 二、资产负债表 Balance Sheet资产 Assets流动资产 Current Assets货币资金 Bank and Cash短期投资 Current Investment 一年内到期委托贷款 Entrusted loan receivable due within one year 减:一年内到期委托贷款减值准备 Less: Impairment for Entrusted loan receivable due within oneyear 减:短期投资跌价准备 Less: Impairment for current investment 短期投资净额 Net bal of current investment 应收票据 应收股利 应收利息 应收账款 减:应收账款坏账准备 Less: Bad debt provision for Account receivable 应收账款净额 Net bal of Account receivable 其他应收款 Other receivable 减:其他应收款坏账准备 Less: Bad debtprovisionfor Other receivable 其他应收款净额 Net bal of Other receivable 预付账款 Prepayment 应收补贴款 Subsidy receivable 存货 Inventory 减:存货跌价准备 Less: Provision for Inventory 存货净额 Net bal of Inventory 已完工尚未结算款 Amount due from customer for contract work 待摊费用 Deferred Expense 一年内到期的长期债权投资 Long-term debt investment due within one year 一年内到期的应收融资租赁款 Finance lease receivables due within one year 其他流动资产 Other current assets 流动资产合计 Total current assets 长期投资 Long-term investment 长期股权投资 Long-term equity investment 委托贷款 Entrusted loan receivable长期债权投资 Long-term debt investment 长期投资合计 Total for long-term investmentNotes receivable Dividend receivable Account receivable减:长期股权投资减值准备 Less: Impairment for long-term equity investment 减:长期债权投资减值准备 Less: Impairment for long-term debt investment 减:委托贷款减值准备 Less: Provision for entrusted loan receivable 长期投资净额 Net bal of long-term investment 其中:合并价差 Include: Goodwill (Negative goodwill) 固定资产 Fixed assets 固定资产原值固定资产净值 减:固定资产减值准备 Less: Impairment for fixed assets 固定资产净额 NBVof fixed assets 工程物资 Material holds for construction of fixed assets 在建工程 Construction in progress 减:在建工程减值准备 Less: Impairment for construction in progress 在建工程净额 Net bal of construction in progress 固定资产清理 Fixed assets to be disposed of 固定资产合计 无形资产及其他资产 Other assets & Intangible assets 无形资产Intangibleassets 减:无形资产减值准备 Less: Impairment for intangible assets 无形资产净额 Net bal of intangible assets 长期待摊费用 Long-term deferred expense融资租赁 -- 未担保余值 Finance lease - Unguaranteed residual values融资租赁 -- 应收融资租赁款 Finance lease - Receivables其他长期资产 Other non-current assets无形及其他长期资产合计 Total other assets & intangible assets 递延税项 Deferred Tax 递延税款借项 Deferred Tax assets 资产总计 Total assets 负债及所有者(或股东)权益 Liability & Equity 流动负债 短期借款 应付票据 应付账款 已结算尚未完工款 预收账款 Advancefrom customers 应付工资 Payroll payable 应付福利费 Welfare payable 应付股利 Dividend payable 应交税金 Taxes payable 其他应交款 Other fees payable 其他应付款 Other payable 预提费用 Accrued Expense 预计负债 Provision Cost减:累计折旧 Less: AccumulatedDepreciationTotal fixed assetsCurrentliabilityShort-term loans Notes递延收益 Deferred Revenue 一年内到期的长期负债 Long-term liability due within one year 其他流动负债 Other current liability 流动负债合计 Total current liability 长期负债 Long-term liability 长期借款 Long-term loans 应付债券 Bonds payable 长期应付款Long-term payable 专项应付款 Grants & Subsidies received 其他长期负债 Other long-term liability 长期负债合计 Total long-term liability 递延税项 Deferred Tax 递延税款贷项 Deferred Tax liabilities 负债合计 Total liability 少数股东权益 Minority interests 所有者权益(或股东权益) Owners' Equity 实收资本(或股本) Paid in capital 减;已归还投资 Less: Capital redemption 实收资本(或股本)净额 Net bal of Paid in capital 资本公积 Capital Reserves 盈余公积 Surplus Reserves 其中:法定公益金Include: Statutory reserves 未确认投资损失 Unrealised investment losses 未分配利润Retained profits after appropriation 其中:本年利润 Include: Profits for the year 外币报表折算差额 Translation reserve 所有者(或股东)权益合计 Total Equity 负债及所有者(或股东)权益合计Total Liability & Equity三、利润及利润分配表 Income statement and profit appropriation 一、主营业务收入Revenue 减:主营业务成本 Less: Cost of Sales 主营业务税金及附加 Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit ( - means loss)加:其他业务收入 Add: Other operating income 减:其他业务支出 Less: Other operating expense 减:营业费用 Selling & Distribution expense 管理费用 G&A expense 财务费用Finance expense三、营业利润(亏损以“—”填列)加:投资收益(亏损以“—”填列)补贴收入 Subsidy Income 营业外收入 Non-operatingincome 减:营业外支出 Less: Non-operating expense Profit from operation ( - means loss) Add: Investment四、利润总额(亏损总额以“—”填列)减:所得税 Less: Income tax 少数股东损益 Minority interest 加:未确认投资损失 Add: Unrealised investment losses五、净利润(净亏损以“—”填列) Net profit ( - means loss)加:年初未分配利润 Add: Retained profits 其他转入 Other transfer-in六、可供分配的利润 Profit available for distribution( - means loss) 减:提取法定盈余公积 Less: Appropriation of statutory surplus reserves 提取法定公益金 Appropriation of statutory welfare fund 提取职工奖励及福利基金 Appropriation of staff incentive and welfare fund 提取储备基金 Appropriation of reserve fund 提取企业发展基金 Appropriation of enterprise expansion fund 利润归还投资 Capital redemption七、可供投资者分配的利润 Profit available for owners' distribution 减:应付优先股股利 Less: Appropriation of preference share's dividend 提取任意盈余公积 Appropriation of discretionary surplus reserve 应付普通股股利 Appropriation of ordinary share's dividend 转作资本(或股本)的普通股股利 Transfer from ordinary share's dividend to paid in capital八、未分配利润 Retained profit after appropriationSupplementary Information: 出售、处置部门或被投资单位收益 自然灾害发生损失 会计政策变更增加Profit before Tax补充资料:1. 2.Gains on disposal of operating divisions or investments Losses from natural disaster 或减少) 利润总额 Increase (decrease) in profit due to changes in accounting 3.policies4. 会计估计变更增加 或减少) 利润总额 Increase (decrease) in profit due to changes in accounting。

2012年第一季度报表分析

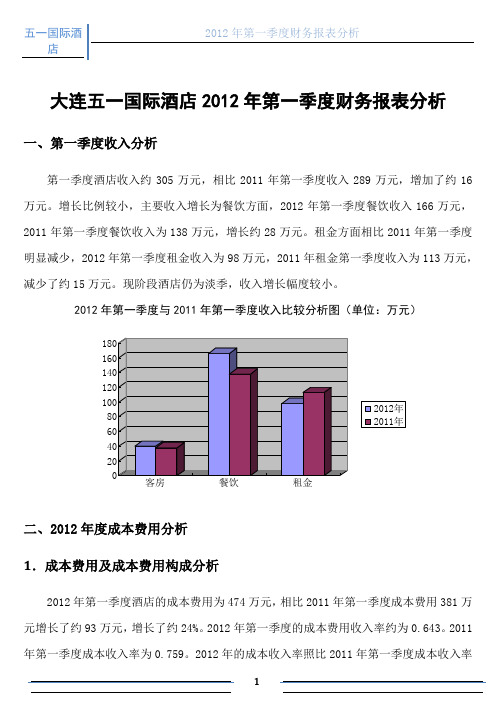

大连五一国际酒店2012年第一季度财务报表分析一、第一季度收入分析第一季度酒店收入约305万元,相比2011年第一季度收入289万元,增加了约16万元。

增长比例较小,主要收入增长为餐饮方面,2012年第一季度餐饮收入166万元,2011年第一季度餐饮收入为138万元,增长约28万元。

租金方面相比2011年第一季度明显减少,2012年第一季度租金收入为98万元,2011年租金第一季度收入为113万元,减少了约15万元。

现阶段酒店仍为淡季,收入增长幅度较小。

2012年第一季度与2011年第一季度收入比较分析图(单位:万元)客房餐饮租金二、2012年度成本费用分析1.成本费用及成本费用构成分析2012年第一季度酒店的成本费用为474万元,相比2011年第一季度成本费用381万元增长了约93万元,增长了约24%。

2012年第一季度的成本费用收入率约为0.643。

2011年第一季度成本收入率为0.759。

2012年的成本收入率照比2011年第一季度成本收入率低了0.116。

也就是说,100元收入的情况下,2012年第一季度要比2011年第一季度多付出1元的成本。

以目前物价来讲,成本增幅不高。

值得一提的是,2012年第一季度与2011年第一季度各月成本费用比较分析图(单位:万元)2012年第一季度与2011年第一季度成本费用构成表2012年第一季度成本费用构成分析表(单位:元)2011年第一季度成本费用构成分析表(单位:元)2.费用分析2012年第一季度酒店费用约为322万元,相比2011年第一季度费用293万元,增加了29万元,增长了约9.9%。

(1)销售费用2012年第一季度酒店销售费用约为211万元,相比2011年销售费用161万元,增加了50万元,增长了约31%,以下为两年主要销售费用对比表:2012年第一季度与2011年第一季度主要销售费用对比表增长最高的为工资统筹方面,工资和统筹合计增加37.7万元,在增加的费用50万元中占75.4%。

2012年度会计报表-英文

Monetar Cumulative

Total of Paid-in Capital Owners' Equity

Undistributed Total of Owners' Profit Equity

三、本年增减变动金额(减少以“-”号填列) III. Increase/decrease in the current year

Page 4

注:加△楷体项目为金融类企业专用,带#为外商投资企业专用。 单位负责人: 主管会计工作负责人(总会计师): 会计(财务)机构负责人:

Person in charge of the unit:

Executive officer in charge of accounting work:

Person in charge of the accounting office:

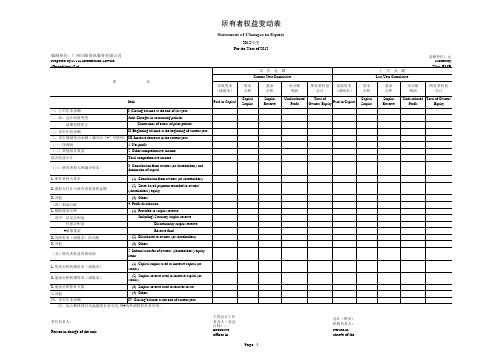

所有者权益变动表

Statement of Changes in Equity

2012年度 For the Year of 2012 编制单位:广州日邮资讯服务有限公司 Prepared by:NYK Information Service (Guangzhou) Ltd.

本 项 目 实收资本 (或股本) Item 一、上年年末余额 加:会计政策变更 前期差错更正 二、本年年初余额 (一)净利润 (二)其他综合收益 综合收益小计 (三)所有者投入和减少资本 1.所有者投入资本 2.股份支付计入所有者权益的金额 3.其他 (四)利润分配 1.提取盈余公积 其中:法定公积金 任意公积金 #储备基金 2.对所有者(或股东)的分配 3.其他 (五)所有者权益内部结转 1.资本公积转增资本(或股本) 2.盈余公积转增资本(或股本) 3.盈余公积弥补亏损 4.其他 四、本年年末余额 (3). Others 5. Internal transfer of owners' (shareholders') equity items (1). Capital surplus used to increase capital (or stocks) (2). Surplus reserve used to increase capital (or stocks) (3). Surplus reserve used to recover losses (4). Others IV. Closing balance at the end of current year I. Closing balance at the end of last year Add: Changes in accounting policies Corrections of errors of prior periods II. Beginning balance at the beginning of current year 1. Net profit 2. Other comprehensive income Total comprehensive income 3. Contribution from owners (or shareholders) and diminution of capital (1). Contribution from owners (or shareholders) (2). Share-based payment recorded in owners' (shareholders') equity (3). Others 4. Profit distribution (1). Provided to surplus reserve Including: Statutory surplus reserve Discretionary surplus reserve Reserve fund (2). Distributed to owners (or shareholders) Paid-in Capital 资本 公积 Capital Surplus 盈余 公积 Surplus Reserve 未分配 利润 Undistributed Profit 所有者权益 合计 实收资本 (或股本) 资本 公积 Capital Surplus 盈余 公积 Surplus Reserve 未分配 利润 所有者权益 合计 年 金 额 上 年 金 额 Current Year Cumulative 金额单位:元

最新财务报表附注(2012年度)

XX有限公司20XX年度财务报表附注(金额单位:人民币元)一、公司基本情况公司(以下简称❽本公司❾)☎公司基本情况部分应简述公司历史沿革、所处行业、经营范围、主要产品或提供的劳务等。

公司在报告期间内主营业务发生变更的,股权发生重大变更、发生重大并购、重组的,应予以说明。

✆二、公司主要会计政策、会计估计和会计政策变更、前期差错、财务报表的编制基础自 ✠✠ 年 月 日起,本公司执行财政部于 年 月 日颁布的《企业会计准则 基本准则》和 项具体会计准则、以及其后颁布的企业会计准则应用指南、企业会计准则解释以及其他相关规定(以下简称❽企业会计准则❾)。

本公司以持续经营为基础编制财务报表。

(如果对持续经营能力产生重大疑虑的,披露导致对持续经营能力产生重大疑虑的主要事项或情况,以及管理层对这些事项或情况提出的应对计划;披露可能导致对持续经营能力产生重大疑虑的事项或情况存在重大不确定性,本公司可能无法在正常的经营过程中变现资产、清偿债务。

)、遵循企业会计准则的声明本公司编制的财务报表符合企业会计准则的要求,真实、完整地反映了本公司于 年 月 日的合并公司财务状况以其 年度的合并公司经营成果和合并公司现金流量。

、会计期间本公司会计年度为公历 月 日起至 月 日止。

、记账本位币本公司记账本位币为人民币。

、计量属性本公司财务报表项目采用历史成本为计量属性,对于符合条件的项目,采用公允价值计量。

本公司采用公允价值计量的项目包括交易性金融工具和可供出售金融资产。

公司本期报表项目的计量属性未发生变化。

、同一控制下和非同一控制下企业合并的会计处理方法( )同一控制下企业合并参与合并的企业在合并前后均受同一方或相同的多方最终控制且该控制并非暂时性的,为同一控制下的企业合并。

合并方在企业合并中取得的资产和负债,按照合并日在被合并方的账面价值计量。

合并方取得的净资产账面价值与支付的合并对价账面价值(或发行股份面值总额)的差额,应当调整资本公积中的资本溢价;资本公积中的资本溢价不足冲减的,调整留存收益。

德国、澳大利亚、俄罗斯会计报表的格式和内容分析

一、德国会计报表1、关于财务会计报告内容与格式。

德国财务会计报告内容由资产负债表、损益表、报表附注、状况报告相当于我国财务情况说明书构成,其中,资产负债表、损益表、报表附注构成了德国的年终决算。

德国不要求编制现金流量表。

财务会计·报表有简化报表格式与一般报表格式之分。

所谓简化会计报表是指会计报表某些项目的列示允许采用“汇总”的方式处理,其目的是避免过分详细的信息披露。

例如资产负债表中“存货”的反映,在中小型公司的简化资产负债表上可仅仅列示“存货”一个项目,而在大公司的一般资产负债表上则必须在“存货”项目下再列示出“原材料”、“在制品”、“产成品”、“预付款”等明细项目在德国,采购材料方面的“预付款”反映在“存货”项目中。

同样,损益表和会计报表附注也存在—般格式与简化格式之分,如何编制简化会计报表和简化报表附注,德国《商法》中有着详细而具体的规定。

2、关于审计要求。

德国财务会计报告审计有三种不同要求——不要求审计、要求审计但可以由宣过誓的审计师vereidigte Buchpruefer,简写为“VBP”审计、要求审计而且要求由经济检查师Wirtschaftspmefer,简写为“WP”进行审计。

在德国,从事外部审计的人员分为两类——宣过誓的审计人员和经济检查师,经济检查师受过严格的专业训练和实践锻炼,具有严格的执业资格要求,相当于我国的注册会计师。

相对而言,宣过誓的审计人员其专业要求较低,只能从事一些中、小企业的审计工作。

显然,从不要求审计到要求审计是一个较高披露等级的要求,从要求宣过誓的审计员审计到经济检查师审计·又是一个更高的披露等级要求。

在表2中,VBP表示审计可以由宣过誓的审计员进行,WP表示审计必须由经济检查师进行。

3、关于审计报告的确认。

德国的财务会计报告在审计后,须经企业有关权力部门确认后才能对外公布。

独资企业自然由出资人确认,合伙企业由合伙人确认,而股份制企业则应当通过董事会和股东大会确认。

企业会计准则财务报表列报

任务名称:企业会计准则财务报表列报一、介绍企业会计准则财务报表列报是指企业按照规定的会计准则编制和报告财务信息的过程。

财务报表是企业财务状况和经营情况的主要反映工具,对于实现财务透明度和风险管理具有重要意义。

本文将就企业会计准则财务报表列报进行全面、详细、完整和深入的探讨。

二、财务报表的基本要素财务报表包括资产负债表、利润表、现金流量表和所有者权益变动表等。

以下是这些财务报表的基本要素:1. 资产负债表资产负债表反映了企业在特定日期的资产、负债和所有者权益的状况。

资产包括流动资产和非流动资产,负债包括流动负债和非流动负债。

所有者权益是指企业剩余资产减去负债后归属于所有者的部分。

2. 利润表利润表显示了企业在特定会计期间内的收入、成本和盈余情况。

收入包括销售收入、利息收入等,成本包括生产成本、销售成本等。

利润表反映了企业经营活动的盈亏状况。

3. 现金流量表现金流量表记录了企业在特定会计期间内的现金流入和流出情况。

现金流量分为经营活动、投资活动和筹资活动三部分。

现金流量表对企业的现金流动情况进行了全面的反映。

4. 所有者权益变动表所有者权益变动表记录了企业在特定会计期间内所有者权益的变动情况。

所有者权益变动表包括股本、股东权益和利润分配等内容,反映了企业内部资金的流动和变化。

三、企业会计准则的作用企业会计准则是针对企业制定的会计准则,其制定目的在于提供一种规范的财务报告要求,以保证财务信息的权威性和可比性。

企业会计准则的作用主要体现在以下几个方面:1. 提高财务信息的质量企业会计准则明确了财务报表的编制原则和计量规则,要求企业充分披露财务信息的真实、准确和完整性。

通过遵循企业会计准则的要求,企业可以提高财务信息的质量,提升信息披露的透明度。

2. 加强财务信息的可比性企业会计准则统一了企业财务信息的报告要求和计量规则,使财务信息具有可比性。

不同企业按照相同的会计准则编制财务报表,可以方便用户进行比较分析。

建筑企业会计-第十二章 会计报表

第十二章会计报表本章重点与难点在理解会计报表种类及编制要求的基础上,重点掌握三张主表的编制方法。

1、资产负债表。

掌握各项目的填列方法。

就“期末数” 栏金额而言,各项目金额一是直接根据相应账户的期末余额填列,二是对有关账户余额分析、调整和重新计算后填列。

这里应注意第二种填列方法,采用这种方法填列的项目主要有:货币资金、应收账款、预付账款、存货、待摊费用、长期债权投资、一年内到期的长期债券投资、应付账、预收账款、预提费用、长期借款、应付债券、长期应付款、一年内到期的长期负债等。

其次,理解资产负债表的作用。

2、利润表。

一是理解利润表编制的两种观点:本期损益观、损益满计观;二是掌握我国现行利润表的编制方法。

其中,“本月数”栏主要项目金额根据相应损益类账户的本月净发生额填列,各层次的利润指标根据表内项目的关系计算填列。

“本年累计数”栏反映各项目自年初起至本期止的累计发生额,按月编制利润表时,该栏各项目金额等于本月利润表“本月数”栏金额与上月利润表中“本年累计数”栏金额之和;平时采用表结法的企业,“本年累计数”栏各项目的金额就是相应损益类账户的本期期末余额。

三是理解该表的作用。

3、现金流量表。

一是掌握该表的结构。

我国的现金流量表将企业的现金流量分为三类,其中因经营活动产生的现金流量的列示方法不同,该表有直接法、间接法两种格式。

二是掌握该表的编制方法,尤其是正表中经营活动产生的现金流量及补充资料中将净利润调节为经营活动的现金流量的编制。

现金流量表是一张年报,各项目金额无直接的资料来源,必须根据有关账户记录分析填列。

正确编制该表的前提是正确理解各项目的含义,实务中企业一般采用工作底稿法编制现金流量表,这里的关键是正确编制抵消分录。

三是理解现金流量表的作用。

4、掌握施工企业内部报表的种类、作用及其格式。

第一节会计报表概述会计报表是财务会计报告的主要组成部分。

一、会计报表的作用正确及时地编制会计报表,具有十分重要的作用。

财政部关于下发《2000年度汇总会计报表〔企业类--行业补充指标表〕》的通知

财政部关于下发《2000年度汇总会计报表〔企业类--行业补充指标表〕》的通知文章属性•【制定机关】财政部•【公布日期】2000.09.25•【文号】财统[2000]3号•【施行日期】2000.09.25•【效力等级】部门规范性文件•【时效性】失效•【主题分类】会计正文*注:本篇法规已被《财政部关于公布废止和失效的财政规章和规范性文件目录(第八批)的决定》(发布日期:2003年1月30日实施日期:2003年1月30日)宣布失效财政部关于下发《2000年度汇总会计报表〔企业类--行业补充指标表〕》的通知(2000年9月25日财统〔2000〕3号)国务院有关部委、直属机构,党中央有关部门,中央直管企业(集团),各省、自治区、直辖市、计划单列市财政厅(局),上海、青岛、深圳、厦门市国资办,新疆生产建设兵团财务局:为促进做好2000年度企业(单位)的会计决算工作,及时掌握2000年全国国有企业(集团)和集体企业(单位)的财务状况、经营成果和国有资本保值增值等基础信息,我们按照“统一设计、口径一致、一表多用、数据共享”的基本原则,结合1999年各类行业企业财务会计管理工作实际,设计制定《2000年度汇总会计报表〔企业类--行业补充指标表〕》,现印发给你们,请认真组织实施并按时上报,并将有关事宜通知如下:一、《2000年度汇总会计报表〔企业类〕》由“主、附表”和特殊行业企业的“行业补充指标表”构成。

各企业在填报《2000年度汇总会计报表〔企业类〕》主表、附表基础上,应结合本行业情况选择“行业补充指标表”进一步填报。

二、行业补充指标表填报对象主要包括:文教企业、农口企业、粮食企业、铁道运输企业、民航运输企业、邮电企业、对外经济合作企业、外贸企业、旅游企业和供销社等十类企业。

“行业补充指标表”内容主要反映这些行业的企业财务、资产管理特殊性指标,以及行业会计制度规定的特殊性指标。

三、本套行业补充指标表应充分保证数据的年度间可比性,各类报表的填报范围应分别和1999年汇总会计报表文教口、农口、经贸口、涉外口的相应补充指标表填报范围一致。

中级经济师考试_金融_考前模拟题_第2套

[单选题]1.下列关于会计报表的说法错误的是( )。

A)会计报表是企业会计核算的最终成果B)会计报表是企业对外提供信息的主要形式C)会计报表提供的信息具有较强的时效性D)一套完整的会计报表不包括附注答案:D解析: 本题考查会计报表的概念。

一套完整的会计报表至少应包括资产负债表、利润表、现金流量表、所有者权益变动表以及财务报表附注。

2.剑桥方程式从用货币形式保有资产存量的角度研究货币需求,重视存量货币占收入的比例,又被称为( )。

A)现金交易说B)现金余额说C)国际借贷说D)流动性偏好说答案:B解析:本题考查剑桥方程式的相关知识。

剑桥方程式从用货币形式保有资产存量的角度研究货币需求,重视存量货币占收入的比例,又被称为现金余额说。

3.假设只有一种生产要素投入可变,其他生产要素投入不可变,关于总产量和边际产量的关系说法正确的是( )。

A)总产量递增时,边际产量也递增B)总产量递减时,边际产量为负值C)总产量达到最大值时,边际产量也为最大值D)总产量递减时,边际产量不一定递减答案:B解析: 本题考查生产函数图形及位置关系。

总产量递增时,边际产量是先增后减的,选项A说法错误。

总产量递减时,边际产量也是递减的,选项D说法错误。

总产量达到最大值时,边际产量为零,选项C说法错误。

4.在影响货币乘数的诸因素中,由商业银行决定的是()A)活期存款准备金率B)定期存款准备金率C)超额存款准备金率D)提现率答案:C解析: 在影响货币乘数的诸因素中,中央银行和商业银行决定存款准备金率。

其中,中央银行决定法定存款准备金率r和影响超额存款准备金率e,商业银行决定超额存款准备金率e,储户决定现金漏损率c。

5.通货膨胀时期,政府部门可以采取的紧缩性财政政策是()。

A)减少税收B)增加开支C)增加税收D)增加补贴答案:C解析: 通货膨胀时期,政府可以采取紧缩性的财政政策来治理通货膨胀。

紧缩性的财政政策主要包括:①减少政府支出;②增加税收;③减少政府转移支付,减少社会福利开支,从而起到抑制个人收入增加的作用。

北欧公司财务分析报告(3篇)

第1篇一、概述北欧公司(以下简称“公司”)成立于20XX年,是一家专注于北欧地区市场的高新技术企业。

公司主要从事研发、生产和销售高科技电子产品,业务范围涵盖智能家居、物联网、大数据分析等多个领域。

本报告旨在通过对公司财务状况的全面分析,评估公司的经营状况、盈利能力、偿债能力、运营效率和未来发展潜力。

二、财务报表分析(一)资产负债表分析1. 资产结构分析- 流动资产分析:截至20XX年12月31日,公司流动资产总额为XX亿元,其中货币资金为XX亿元,应收账款为XX亿元,存货为XX亿元。

流动资产占资产总额的XX%,表明公司短期偿债能力较强。

- 非流动资产分析:非流动资产总额为XX亿元,主要包括固定资产、无形资产和长期投资等。

固定资产占比XX%,表明公司对生产设备的投入较大,长期发展潜力较大。

2. 负债结构分析- 流动负债分析:截至20XX年12月31日,公司流动负债总额为XX亿元,主要包括短期借款、应付账款等。

流动负债占负债总额的XX%,表明公司短期偿债压力较小。

- 非流动负债分析:非流动负债总额为XX亿元,主要包括长期借款和长期应付款等。

非流动负债占负债总额的XX%,表明公司长期偿债能力较好。

3. 所有者权益分析- 实收资本分析:截至20XX年12月31日,公司实收资本为XX亿元,表明公司股东对公司发展充满信心。

- 盈余公积分析:截至20XX年12月31日,公司盈余公积为XX亿元,表明公司盈利能力较强。

(二)利润表分析1. 营业收入分析- 公司营业收入呈逐年增长趋势,20XX年营业收入为XX亿元,较20XX年增长XX%。

这主要得益于公司产品在北欧市场的广泛认可和销售网络的不断完善。

2. 营业成本分析- 公司营业成本呈逐年增长趋势,20XX年营业成本为XX亿元,较20XX年增长XX%。

这主要由于原材料价格上涨和研发投入增加。

3. 期间费用分析- 公司期间费用主要包括销售费用、管理费用和财务费用。

20XX年期间费用为XX亿元,较20XX年增长XX%。

2012BENETECH财务报表

BENEFICENT TECHNOLOGY, INC.AND BENGINEERING, INC.DBA BENETECH(A California Nonprofit Public Benefit Corporation)CONSOLIDATED FINANCIAL STATEMENTSANDINDEPENDENT AUDITOR’S REPORT YEARS ENDED DECEMBER 31, 2012 AND 2011BENEFICENT TECHNOLOGY, INC. AND BENGINEERING, INC. DBA BENETECH(A California Nonprofit Public Benefit Corporation)FINANCIAL STATEMENTSYEARS ENDED DECEMBER31,2012AND2011TABLE OF CONTENTSPage Independent Auditor’s Report (1)Consolidated Statements of Financial Position (3)Consolidated Statements of Activities (5)Consolidated Statements of Functional Expenses (6)Consolidated Statements of Cash Flows (8)Notes to Consolidated Financial Statements (9)Supplementary Information (19)Schedule of Expenditures of Federal Awards (20)Notes to the Schedule of Expenditures of Federal Awards (22)Schedule of Findings and Questioned Costs (23)Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance WithGovernment Auditing Standards (24)Independent Auditor’s Report on Compliance for Each Major Federal Program and on Internal Control Over Compliance (26)* * * *1Board of DirectorsBeneficent Technology, Inc.Palo Alto, CaliforniaINDEPENDENT AUDITOR’S REPORTReport on the Financial StatementsWe have audited the accompanying consolidated financial statements of Beneficent Technology, Inc., aCalifornia nonprofit public benefit corporation, which comprise the consolidated statements of financial position as of December 31, 2012 and 2011, and the related consolidated statements of activities, functional expenses, and cash flows for the years then ended, and the related notes to the consolidated financial statements.Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these consolidated financial statementsin accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.Auditor’s ResponsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audits. Weconducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards , issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in theconsolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for ouraudit opinion.OpinionIn our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Beneficent Technology, Inc. as of December 31, 2012 and 2011, and the changes in its net assets and its cash flows for the years then ended, in accordance with accounting principles generally accepted in the United States of America.Report on Supplementary InformationOur audits were conducted for the purpose of forming an opinion on the basic consolidated financial statements taken as a whole. The accompanying Schedule of Expenditures of Federal Awards on page 20 is presented for purposes of additional analysis as required by OMB Circular A-133 and is not a required part of the basic consolidated financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the consolidated financial statements. The information has been subjected to the auditing procedures applied in the audit of the consolidated financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the consolidated financial statements or to the consolidated financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the Schedule of Expenditures of Federal Awards is fairly stated in all material respects, in relation to the consolidated financial statements as a whole.Report on Other Legal and Regulatory RequirementsIn accordance with Government Auditing Standards, we have also issued a report dated June 5, 2013, on our consideration of Beneficent Technology, Inc.’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Beneficent Technology, Inc.’s internal control over financial reporting and compliance.June 5, 2013DECEMBER 31, 2012 AND 201120122011ASSETSCurrent assets:$$ 767,370 Cash and cash equivalents1,210,860Receivables:Contributions – current (Note 3) 765,878722,521 Accounts receivable (Note 4) 1,100,756849,681 Prepaid expenses24,7256,195 Total current assets3,102,2192,345,767 Contributions receivable – net of current portion (Note 3)400,000250,000 Property and equipment – net (Note 5)42,04515,371 Intangible assets – net (Note 6) -49,200 Deposits53,14051,578 Total assets3,597,404$$ 2,711,916DECEMBER 31, 2012 AND 201120122011LIABILITIES AND NET ASSETSCurrent liabilities:$$ 329,447 Accounts payable376,666Accrued expenses174,014141,860 Accrued employee benefits717,932604,287 Deferred revenue 67,53468,181 Total current liabilities1,336,1461,143,775Net assets:Unrestricted89,58440,623 Temporarily restricted (Note 8)2,171,6741,527,518 Total net assets2,261,2581,568,141Total liabilities and net assets 3,597,404$$ 2,711,916CONSOLIDATED STATEMENTS OF ACTIVITIESYEARS ENDED DECEMBER 31, 2012 AND 2011Support and revenue:ContributionsRoyaltiesEngineering and consulting feesDonated services/productsBookshare revenue – net of direct expensesof $154,184 in 2012 and $70,233 in 2011Human rights revenueMiradi revenueRoute 66 revenueInterest incomeTotal support and revenueNet assets released from restrictions:Satisfaction of purpose restrictionsSatisfaction of time restrictionTotal supportand revenueExpenses:Program services:BookshareHuman rightsMiradiRoute 66BengineeringSupporting services:Management and generalFundraisingBid and proposalResearch and developmentTotal expensesChange in net assetsNet assets, beginning of yearNet assets, end of yearBENEFICENT TECHNOLOGY, INC. AND BENGINEERING, INC. DBA BENETECH(A California Nonprofit Public Benefit Corporation)CONSOLIDATED STATEMENTS OF CASH FLOWSYEARS ENDED DECEMBER 31, 2012 AND 201120122011 Cash flows from operating activities:$$ (214,214) Change in net assets693,117Adjustments to reconcile change in net assets to net cash provided by(used in) operating activities:Depreciation 15,912 9,535 Amortization 49,200 590,964 (Increase) decrease in assets:Contributions receivable (193,357) (80,252)Grants and accounts receivable (251,075) (282,353)Prepaid expenses (18,530) (1,220)Deposits (1,562) 1,727 Increase (decrease) in liabilities:Accounts payable 47,219 150,889Accrued expenses 145,799 9,920Deferred revenue (647) 6,554Deferred rent - (44,473) Total adjustments (207,041) 361,291Net cash provided by operating activities 486,076 147,077 Cash flows from investing activities:Purchase of property and equipment (42,586) (11,387) Net cash used in investing activities (42,586) (11,387) Increase in cash 443,490135,690 Cash and cash equivalents, beginning of year767,370631,680$Cash and cash equivalents, end of year1,210,860$ 767,370YEARS ENDED DECEMBER 31, 2012 AND 2011NOTE 1 –ORGANIZATION AND NATURE OF ACTIVITIESBeneficent Technology, Inc. (doing business as “Benetech®”) was incorporated as a nonprofit corporation to develop technology projects, products and services to benefit humanity worldwide.Beneficent Technology, Inc. has a for-profit subsidiary, Bengineering, Inc. which has been involved in providing engineering consulting services. Bengineering, Inc.’s assets, liabilities, revenues and expenses have been consolidated in the financial statements. Bengineering, Inc. did not have any significant activity in 2012 or 2011. Both Beneficent Technology, Inc. and its for-profit subsidiary, Bengineering, Inc. (collectively, the “Organization”), operated under the Benetech dba and brand name.The Organization acts as innovators and operators of technology-oriented nonprofit projects. The Organization is involved in the following projects:Bookshare®: Bookshare provides copyrighted material in accessible digital formats to people with qualifying print disabilities. It is a web-based library of books, periodicals, and newspapers. Millions of people throughout the United States with visual impairments, physical disabilities and severe learning disabilities meet the stringent copyright law exemption that permits reproduction of copyrighted material into specialized formats and distribution for personal use. Around the world, individuals that meet these qualifications have access to freely distributable material and copyrighted books for which Bookshare has international permissions. The books and publications can be read with a variety of software applications and hardware devices that produce synthetic speech (text-to-speech), large print, or Braille. This includes a number of tools provided by Benetech, including readers for iOS, Android, and major web browsers. Bookshare was launched in February 2002 and has over 238,000 eligible members as of December 31, 2012. Through the active participation of thousands of volunteers, partners, universities and publishers around the world, Bookshare provides people with print disabilities with instant access to more than 174,000 books and 150 daily newspapers.Human Rights: The Human Rights Program (HRP) focuses its efforts in two key areas: the development of and training for Martus, Benetech’s secure, open source information management software designed for human rights organizations; and comprehensive analysis of large scale human rights violations in post-conflict communities around the world by the Human Rights Data Analysis Group (HRDAG). The Human Rights Program uses science and technology to advance the cause of human rights.Martus is an open-source software application that allows users anywhere in the world to securely gather and organize information about human rights violations. The application was developed by Benetech, is available in eleven languages (English, Russian, Spanish, Arabic, French, Thai, Nepali, Burmese, Armenian, Farsi/Dari and Khmer) and is made available at no cost for human rights defenders. Martus automatically encrypts the information and copies it to a network of secure servers around the world. Nobody except the user who created it, not even Benetech, can read the encrypted data. In threatening situations, users can delete all Martus data on their computer (along with the Martus program itself). Since the data is backed up, users can retrieve their information when and where it is safe to do so. Martus helps those who collect this valuable human rights information stay safe, while also protecting the identities of those who would face violence and repression for telling their stories. The Martus software has been downloaded by people and organizations in over 120 countries.The HRDAG develops data analysis software, information collection strategies and statistical techniques.These scientists measure the magnitude and pattern of human rights violations in order to evaluate claims that violence was the result of state or institutional policies. This technology and analysis is used by truth commissions, international criminal tribunals and non-governmental human rights organizations as they clarify history, and seek to hold people accountable for gross human rights abuses.YEARS ENDED DECEMBER 31, 2012 AND 2011Miradi:Miradi is an open-source software application that enables users to design, monitor and evaluate their conservation efforts. The software allows them to develop project objectives and interventions, prioritize threats, look at event chains, assess which actions are working and adjust their strategies accordingly. Miradi, developed by Benetech in collaboration with the Conservation Measures Partnership (CMP), bundles key functions of existing commercial project management tools (which are not designed for conservation management) together with conservation-specific best practices, at a low-cost. Miradi’s first production version was released in 2008. Over 7,000 users who are managing complex environmental programs in over 170 different countries have now downloaded Miradi. A new “Miradi Share” web site is now being developed by a third party software consulting group. Whether used to manage a small county park or revive an entire marine habitat, Miradi helps conservationists to integrate best practices in environmental adaptive management with local expertise, empowering them to succeed in their efforts to protect and restore species and ecosystems.Route 66 Literacy: Route 66 Literacy is a web-based program that makes it easy for any literate person to teach adolescent and adult beginning readers with developmental disabilities to read. The program combines engaging, age-appropriate lessons, exercises and effective feedback with a unique teacher-tutor model, one that requires no special training. By incorporating expert pedagogy and one to one interaction, Route 66 Literacy creates new pathways for them to gain independence and to pursue further educational and vocational opportunities.SocialCoding4Good: SocialCoding4Good, created in 2011, is a pilot project aimed at dramatically reshaping the tech volunteer landscape. There are many nonprofits and social-good programs in the world that need the help of professional technologists, but their resources don’t often allow for it. The causes they’re working on, from civic engagement and education to poverty alleviation and the environment, suffer as a result. At the same time, professional technologists are eager to help work on these important social challenges, but often struggle to find the right match for both their passion and skills. Using a web-based platform, SocialCoding4Good collects information on both volunteer technologist and programs with need so that our community managers can connect these professionals with opportunities that are the right fit. And this way volunteers use their time and talent to work on the humanitarian open source software projects that would most benefit from it. By working across the corporate, nonprofit and technology communities, SocialCoding4Good brings together the best and brightest to generate meaningful and sustainable collaborations for social good.CityOptions:CityOptions is a potential technology-based solution to help local governments address environmental sustainability challenges and is still in the early stages of Benetech’s new project pipeline. We are currently exploring many different ways that we can build a tool that helps city leaders decide what to do and learn how to do it right; connect users with real project plans from other cities that are tackling similar issues; and collect data on sustainability projects for better quantification and visualization of impact.Beneficent Technology, Inc. is vulnerable to the inherent risks associated with revenue that is substantially dependent on government funding, public support, and contributions. The continued growth and well-being of Beneficent Technology, Inc. is contingent upon successful achievement of its long-term revenue-raising goals.NOTE 2 –SUMMARY OF SIGNIFICANT ACCOUNTING POLICIESPrinciples of ConsolidationThe consolidated financial statements include the accounts of Beneficent Technology, Inc. and its wholly owned corporation, Bengineering, Inc. Management determined that combining Beneficent Technology, Inc. and Bengineering, Inc. provides a more meaningful presentation of the commonly-controlled and financially-dependent companies. All significant intercompany transactions and balances have been eliminated in consolidation.YEARS ENDED DECEMBER 31, 2012 AND 2011Accounting MethodThe financial statements of the Organizations have been prepared on the accrual basis of accounting, which recognizes income in the period earned and expenses when incurred, regardless of the timing of payments.EstimatesThe preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America (GAAP) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenue and expense during the reporting period. Actual results could differ from those estimates.Basis of PresentationThe Organization is required to report information regarding its financial position and activities according to three classes of net assets: unrestricted net assets, temporarily restricted net assets and permanently restricted net assets.∙Unrestricted net assets include those assets over which the Board of Directors has discretionary control in carrying out the operations of the Organization. The Organization has elected to report as an increase inunrestricted net assets any temporarily restricted revenue received in the current period whose restrictionshave been met in the current period.∙Temporarily restricted net assets include those assets subject to donor restrictions and for which the applicable restrictions were not met as of the end of the current reporting period. When a donor restrictionexpires–that is, when a stipulated time restriction ends or purpose restriction is accomplished–temporarilyrestricted net assets are reclassified to unrestricted net assets and reported in the consolidated statements ofactivities as net assets released from restrictions. If donor’s restrictions are satisfied in the same period thatthe contribution is received, the contribution is reported as unrestricted support.∙Permanently restricted net assets include those assets subject to non-expiring donor restrictions. The Organization had no permanently restricted net assets as of December 31, 2012 and 2011.Revenue RecognitionRevenue from royalties and interest is recorded when earned based upon the applicable agreements. Revenue from program services is recognized upon performance of the applicable services. Subscription revenue from Bookshare is recognized over the life of the subscription. Unearned subscription revenue is recorded as a liability on the consolidated statements of financial position.ContributionsContributions are recognized as revenue when they are unconditionally communicated. Grants represent contributions if resource providers receive no value in exchange for the assets transferred. Cash contributions are recognized when the donor makes a promise to give; that is, in substance, an unconditional promise. Conditional promises to give are recognized when the conditions on which they depend are substantially met. Cash contributions are recorded at their fair value as unrestricted, temporarily restricted or permanently restricted, depending on the absence or existence of donor-imposed restrictions and on whether the restrictions are met (that is when a stipulated time restriction ends or purpose restriction is accomplished) in the current period. Restricted contributions are reported as an increase in unrestricted net assets if the restrictions have been met in the current period. If the restrictions have not been met by year end, the amount is reported as an increase in temporarily or permanently restricted net assets. When the restriction is met, the amount is shown as a reclassification of restricted net assets to unrestricted net assets and reported in the consolidated statements of activities as net assets released from restrictions.YEARS ENDED DECEMBER 31, 2012 AND 2011Awards from governmental agencies which are funded on a cost-reimbursement basis are generally deemed to be exchange transactions and are therefore not treated as contributions. Revenues from such activities are shown as unrestricted revenue in the Consolidated Statements of Activities.Contributions of donated, non-cash assets are recognized and recorded at their fair values in the period received. Contributions of donated services that create or enhance non-financial assets or that require specialized skills, are provided by individuals possessing those skills, and would typically need to be purchased if not provided by donation, are recorded at their fair values in the period received. During the year ended December 31, 2012 and 2011, these products, supplies and advertising costs in the amount of $406,875 and $325,797, respectively,were recorded as both revenue and expense in the consolidated statements of activities. The Organization also received a significant amount of donated services from unpaid volunteers who assisted in fund-raising and other programs of the Organization. These amounts have not been recognized in the consolidated statements of activities because the criteria for recognition have not been satisfied. The Organization estimates such amounts to be approximately $450,000 in 2012 and 2011, respectively.Cash and Cash EquivalentsCash is defined as cash in demand deposit accounts as well as cash on hand. Cash equivalents are highly liquid investments that are readily convertible to known amounts of cash. Generally, only investments with original maturities of three months or less qualify as cash equivalents.Contributions ReceivableUnconditional promises to give are recorded as receivables and revenue when received. The Organization distinguishes between contributions received for each net asset category in accordance with donor-imposed restrictions. Bad debts are provided on the allowance method based on historical experience and management evaluation of promises to give. Management has determined that no allowance for uncollectible accounts is deemed necessary at December 31, 2012 and 2011.Accounts ReceivableAccounts receivable are related to program earned income. Bad debts are provided on the allowance method based on historical experience and management evaluation of outstanding grants and accounts receivable. It is the Organization’s policy to charge off uncollectible accounts receivable when management determines that receivables will not be collected. Management has determined that no allowance for uncollectible accounts is deemed necessary at December 31, 2012 and 2011.Fair Value MeasurementUnder generally accepted accounting principles, fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (exit price) in an orderly transaction between market participants at the measurement date.YEARS ENDED DECEMBER 31, 2012 AND 2011Generally accepted accounting principles establish a fair value hierarchy for inputs used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are those that market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Organization. Unobservable inputs, if any, reflects the Organization’s assumption about the inputs market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The fair value hierarchy is categorized into three levels based on the inputs as follows:Level 1 – Valuations based on unadjusted quoted prices in active markets for identical assets or liabilities that the Organization has the ability to access at measurement date. Valuation adjustments and block discounts are not applied to Level 1 securities. Since valuations are based on quoted prices that are readily and regularly available in an active market, valuation of these securities does not entail a significant degree of judgment.Level 2 – Valuations based on significant inputs that are observable, either directly or indirectly or quoted prices in markets that are not active, that is, markets in which there are few transactions, the prices are not current or price quotations vary substantially either over time or among market makers.Level 3 – Valuations based on inputs that are unobservable and significant to the overall fair value measurement.The following table summarizes the financial assets and liabilities measured at fair value on a recurring basis as of December 31, 2012 and 2011:Balance as of December 31,2012Quoted Prices in Active Markets for IdenticalAssets(Level 1)Money market(1)$1,160,128$1,160,128Balance as of December 31,2011Quoted Prices in Active Markets for IdenticalAssets(Level 1)Money market (1)$565,565$565,565As of December 31, 2012 and 2011, the Organization did not have any Level 2 and 3 assets or liabilities. (1)The amount is included in cash and cash equivalents in the accompanying consolidated statements of financialposition.Property and Equipment and Intangible AssetsProperty and equipment are stated at cost if purchased, or estimated fair market value if donated. Depreciation is computed on the straight-line method over the estimated useful lives of the assets. Equipment purchases of under $5,000 are expensed as incurred.YEARS ENDED DECEMBER 31, 2012 AND 2011Intangible assets include capitalized costs related to the design of a new website for the Bookshare program.The useful lives of the assets are estimated as follows:Furniture and equipment 3 yearsWeb design 3 yearsIncome TaxesBeneficent Technology, Inc. (Benetech) is a nonprofit corporation qualified under IRC code section 501(c)(3) and California R&T code section 23701(d) as such, it is exempt from federal income taxes. Benetech is not classified as a private foundation under IRC code section 509(a). Qualified nonprofit corporations are generally exempt from income tax. Bengineering, Inc. is a for-profit subsidiary of Beneficent Technology, Inc. During the years ended December 31, 2012 and 2011, Bengineering, Inc. did not have any significant activity and no taxable income and therefore was only liable for the California minimum franchise tax of $800.The Organization reviews and assesses tax positions taken or expected to be taken against more-likely-than-not recognition threshold and measurement attributes for financial statement recognition.The Organization’s policy for evaluating uncertain tax positions is a two-step process. The first step is to evaluate the tax position for recognition by determining if the weight of available evidence indicates that it is more-likely-than-not that the position will be sustained upon audit, including resolution of related appeals or litigations processes, if any. The second step is to measure the tax benefit or liability as the largest amount that is more than 50% likely to be realized or incurred upon settlement. Based on an analysis prepared by the Organization, it was determined that the tax positions taken or expected to be taken had no material effect on the recorded tax assets and liabilities of the Organization. The Organization’s federal and state income tax returns for the years 2008 through 2011 are subject to examination by regulatory agencies, generally for three years and four years after they are filed for federal and state respectively. Functional Expenses AllocationThe Organization allocates all direct expenses attributable to individual functions relating to program and support services. Expenses that are applicable to several programs and/or supporting services are allocated based upon facility square footage or estimate of time devoted by staff to the related functions.Bid and ProposalThese costs include expenses associated with research for and preparation of bids, proposals and applications to secure funding from both federal and non-federal sources.Research and DevelopmentThe Organization continues to research potential new projects. A project must meet the Organization’s mission statement and charter, enhance and complement existing programs, be primarily socially focused, help those who can least help themselves or increase the impact of its current programs.Subsequent EventsThe Organization evaluated subsequent events for recognition and disclosure through June 5, 2013, the date which these consolidated financial statements were available to be issued.Management concluded that no other material subsequent events have occurred since December 31, 2012, that require recognition or disclosure in the consolidated financial statements other than the event stated in Note 13.。

会计报表科目中英文对照

会计报表科目中英文对照————————————————————————————————作者:————————————————————————————————日期:一、企业财务会计报表封面FINANCIAL REPORTCOVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种LocalReporting Currency审核人Verifier填表人Preparer二、资产负债表BalanceSheet资产Assets流动资产Current Assets货币资金Bankand Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due withinone year减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivabledue within one year减:短期投资跌价准备Less:Impairment for current investment短期投资净额Netbal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interestreceivable应收账款Account receivable减:应收账款坏账准备Less:Bad debt provision forAccount receivable应收账款净额Net bal ofAccount receivable其他应收款Otherreceivable减:其他应收款坏账准备Less:Bad debtprovision for Other receivable其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less:Provision for Inventory存货净额Net balof Inventory已完工尚未结算款Amountdue from customer forcontract work待摊费用DeferredExpense一年内到期的长期债权投资Long-termdebtinvestmentduewithin one year一年内到期的应收融资租赁款Finance lease receivables due within one yea r其他流动资产Other currentassets流动资产合计Total currentassets长期投资Long-term investment长期股权投资Long-termequity investment委托贷款Entrustedloan receivable长期债权投资Long-termdebt investment长期投资合计Total for long-terminvestment减:长期股权投资减值准备Less: Impairment for long-term equity investment 减:长期债权投资减值准备Less: Impairment for long-termdebt investment减:委托贷款减值准备Less:Provision forentrustedloan receivable 长期投资净额Net bal of long-terminvestment其中:合并价差Include:Goodwill(Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less:Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less:Impairmentfor fixed assets固定资产净额NBVof fixed assets工程物资Materialholds for construction offixedassets在建工程Construction in progress减:在建工程减值准备Less:Impairment for construction in progress在建工程净额Net bal of constructionin progress固定资产清理Liquidationof Fixed assets固定资产合计Total fixed assets无形资产及其他资产Otherassets &Intangibleassets无形资产Intangibleassets减:无形资产减值准备Less: Impairmentfor intangibleassets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease–Unguaranteedresidualvalues融资租赁——应收融资租赁款Finance lease –Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets& intangible assets递延税项Deferred Tax递延税款借项Deferred Taxassets资产总计Totalassets负债及所有者(或股东)权益Liability &Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advancefrom customers Deposit Received应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Otherpayable预提费用Accrued Expense预计负债Anticipation Liabilities递延收益Deferred Revenue一年内到期的长期负债Long-term liabilitydue within one year其他流动负债Othercurrentliability流动负债合计Total currentliability长期负债Long-term liability长期借款Long-termloans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants &Subsidies received其他长期负债Other long-termliability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益) Owners’Equity实收资本(或股本)Paid in capital减;已归还投资Less:Capital redemption实收资本(或股本)净额Net bal ofPaidincapital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include: Statutory reserves未确认投资损失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include:Profitsfor the year外币报表折算差额Translation reserve所有者(或股东)权益合计TotalEquity负债及所有者(或股东)权益合计TotalLiability&Equity三、利润及利润分配表Income statement and profitappropriation 一、主营业务收入Revenue减:主营业务成本Less:Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit(-meansloss) 加:其他业务收入Add: Otheroperating income减:其他业务支出Less:Other operatingexpense减:营业费用Selling& Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列)Profitfrom operation ( - meansloss) 加:投资收益(亏损以“—”填列)Add:Investment income补贴收入SubsidyIncome营业外收入Non-operating income减:营业外支出Less:Non-operating expense四、利润总额(亏损总额以“—”填列) Profit before Tax减:所得税Less: Income tax少数股东损益Minority interest加:未确认投资损失Add:Unrealised investment losses五、净利润(净亏损以“—”填列) Netprofit(- means loss)加:年初未分配利润Add:Retained profits其他转入Othertransfer-in六、可供分配的利润Profitavailable for distribution( -means loss)减:提取法定盈余公积Less: Appropriation ofstatutory surplusreserves提取法定公益金Appropriation of statutorywelfarefund提取职工奖励及福利基金Appropriation ofstaff incentive and welfarefund 提取储备基金Appropriation of reservefund提取企业发展基金Appropriation of enterpriseexpansion fund利润归还投资Capitalredemption七、可供投资者分配的利润Profit available for owners' distribution减:应付优先股股利Less: Appropriation of preference share'sdividend 提取任意盈余公积Appropriation of discretionarysurplusreserve应付普通股股利Appropriation ofordinary share'sdividend转作资本(或股本)的普通股股利Transferfromordinary share's dividend to paid in capital八、未分配利润Retained profitafter appropriation补充资料: Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses fromnatural disaster3.会计政策变更增加(或减少)利润总额Increase (decrease)inprofit due tochanges in accounting policies4. 会计估计变更增加(或减少)利润总额Increase(decrease) in profitdue to changes in accounting estimates5.债务重组损失Losses from debt restructuringﻬ另一个版本。

会计报表各科目的中英文对照

资产负债表 Balance Sheet项目 ITEM货币资金 Cash短期投资 Short term investments应收票据 Notes receivable应收股利 Dividend receivable应收利息 Interest receivable应收帐款 Accounts receivable其他应收款 Other receivables预付帐款 Accounts prepaid期货保证金 Future guarantee应收补贴款 Allowance receivable应收出口退税 Export drawback receivable存货 Inventories其中:原材料 Including:Raw materials产成品(库存商品) Finished goods待摊费用 Prepaid and deferred expenses待处理流动资产净损失 Unsettled G/L on current assets一年内到期的长期债权投资 Long-term debenture investment falling due in a yaear其他流动资产 Other current assets流动资产合计 Total current assets长期投资: Long-term investment:其中:长期股权投资 Including long term equity investment长期债权投资 Long term securities investment*合并价差 Incorporating price difference长期投资合计 Total long—term investment固定资产原价 Fixed assets—cost减:累计折旧 Less:Accumulated Dpreciation固定资产净值 Fixed assets—net value减:固定资产减值准备 Less:Impairment of fixed assets固定资产净额 Net value of fixed assets固定资产清理 Disposal of fixed assets工程物资 Project material在建工程 Construction in Progress待处理固定资产净损失 Unsettled G/L on fixed assets固定资产合计 Total tangible assets无形资产 Intangible assets其中:土地使用权 Including and use rights递延资产(长期待摊费用)Deferred assets其中:固定资产修理 Including:Fixed assets repair固定资产改良支出 Improvement expenditure of fixed assets其他长期资产 Other long term assets其中:特准储备物资 Among it:Specially approved reserving materials 无形及其他资产合计 Total intangible assets and other assets递延税款借项 Deferred assets debits资产总计 Total Assets资产负债表(续表) Balance Sheet项目 ITEM短期借款 Short—term loans应付票款 Notes payable应付帐款 Accounts payab1e预收帐款 Advances from customers应付工资 Accrued payro1l应付福利费 Welfare payable应付利润(股利) Profits payab1e应交税金 Taxes payable其他应交款 Other payable to government其他应付款 Other creditors预提费用 Provision for expenses预计负债 Accrued liabilities一年内到期的长期负债 Long term liabilities due within one year其他流动负债 Other current liabilities流动负债合计 Total current liabilities长期借款 Long-term loans payable应付债券 Bonds payable长期应付款 long-term accounts payable专项应付款 Special accounts payable其他长期负债 Other long—term liabilities其中:特准储备资金 Including:Special reserve fund长期负债合计 Total long term liabilities递延税款贷项 Deferred taxation credit负债合计 Total liabilities* 少数股东权益 Minority interests实收资本(股本) Subscribed Capital国家资本 National capital集体资本 Collective capital法人资本Legal person”s capital其中:国有法人资本 Including:State—owned legal person"s capital集体法人资本 Collective legal person"s capital个人资本 Personal capital外商资本 Foreign businessmen”s capital资本公积 Capital surplus盈余公积 surplus reserve其中:法定盈余公积 Including:statutory surplus reserve公益金 public welfare fund补充流动资本 Supplermentary current capital* 未确认的投资损失(以“-”号填列) Unaffirmed investment loss未分配利润 Retained earnings外币报表折算差额 Converted difference in Foreign Currency Statements 所有者权益合计 Total shareholder"s equity负债及所有者权益总计 Total Liabilities & Equity利润表 INCOME STATEMENT项目 ITEMS产品销售收入Sales of products其中:出口产品销售收入 Including:Export sales减:销售折扣与折让 Less:Sales discount and allowances产品销售净额Net sales of products减:产品销售税金Less:Sales tax产品销售成本 Cost of sales其中:出口产品销售成本Including:Cost of export sales产品销售毛利 Gross profit on sales减:销售费用 Less:Selling expenses管理费用General and administrative expenses财务费用Financial expenses其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益)Exchange losses(minus exchange gains)产品销售利润Profit on sales加:其他业务利润Add:profit from other operations营业利润Operating profit加:投资收益Add:Income on investment加:营业外收入Add:Non-operating income减:营业外支出Less:Non-operating expenses加:以前年度损益调整Add:adjustment of loss and gain for previous years 利润总额 Total profit减:所得税 Less:Income tax净利润 Net profit现金流量表Cash Flows StatementPrepared by:Period: Unit:Items1。

新准则英文会计报表大全

新准则英文会计报表:成本122 5001生产成本production cost123 5101制造费用cost of production124 5201劳务成本service cost125 5301研发支出research and development expenditures126 5401工程施工建造承包商专用engineering construction exclusively for construction contractor127 5402工程结算建造承包商专用engineering settlement exclusively for construction contractor128 5403机械作业建造承包商专用mechanical operation exclusively for construction contractor 新准则英文会计报表:所有者权益115 4001实收资本paid-up capital116 4002资本公积contributed surplus117 4101盈余公积earned surplus119 4103本年利润profit for the current year120 4104利润分配allocation of profits121 4201库存股treasury stock新准则英文会计报表:资产1 1001库存现金cash on hand2 1002银行存款bank deposit5 1015其他货币资金other monetary capital9 1101交易性金融资产transaction monetary assets11 1121应收票据notes receivable12 1122应收账款Account receivable13 1123预付账款account prepaid14 1131应收股利dividend receivable15 1132应收利息accrued interest receivable21 1231其他应收款accounts receivable-others22 1241坏账准备had debts reserve28 1401材料采购procurement of materials29 1402在途物资materials in transit30 1403原材料raw materials32 1406库存商品commodity stocks33 1407发出商品goods in transit36 1412包装物及低值易耗品wrappage and low value and easily wornout articles42 1461存货跌价准备reserve against stock price declining45 1521持有至到期投资hold investment due46 1522持有至到期投资减值准备hold investment due reduction reserve47 1523可供出售金融资产financial assets available for sale48 1524长期股权投资long-term stock ownership investment49 1525长期股权投资减值准备long-term stock ownership investment reduction reserve50 1526投资性房地产investment real eastate51 1531长期应收款long-term account receivable52 1541未实现融资收益unrealized financing income54 1601固定资产permanent assets55 1602累计折旧accumulated depreciation56 1603固定资产减值准备permanent assets reduction reserve57 1604在建工程construction in process58 1605工程物资engineer material59 1606固定资产清理disposal of fixed assets60 1611融资租赁资产租赁专用financial leasing assets exclusively for leasing61 1612未担保余值租赁专用unguaranteed residual value exclusively for leasing62 1621生产性生物资产农业专用productive living assets exclusively for agriculture63 1622生产性生物资产累计折旧农业专用productive living assets accumulated depreciation exclusively for agriculture64 1623公益性生物资产农业专用non-profit living assets exclusively for agriculture65 1631油气资产石油天然气开采专用oil and gas assets exclusively for oil and gas exploitation66 1632累计折耗石油天然气开采专用accumulated depletion exclusively for oil and gas exploitation67 1701无形资产intangible assets68 1702累计摊销accumulated amortization69 1703无形资产减值准备intangible assets reduction reserve70 1711商誉business reputation71 1801长期待摊费用long-term deferred expenses72 1811递延所得税资产deferred income tax assets73 1901待处理财产损溢waiting assets profit and loss新准则英文会计报表:共同类112 3101衍生工具derivative tool113 3201套期工具arbitrage tool114 3202被套期项目arbitrage project一、企业财务会计报表封面FINANCIAL REPORT COVER报表所属期间之期末时间点Period Ended所属月份Reporting Period报出日期Submit Date记账本位币币种Local Reporting Currency审核人Verifier填表人Preparer二、资产负债表Balance Sheet资产Assets流动资产Current Assets货币资金Bank and Cash短期投资Current Investment一年内到期委托贷款Entrusted loan receivable due within one year减:一年内到期委托贷款减值准备Less: Impairment for Entrusted loan receivable due within one year减:短期投资跌价准备Less: Impairment for current investment短期投资净额Net bal of current investment应收票据Notes receivable应收股利Dividend receivable应收利息Interest receivable应收账款Account receivable减:应收账款坏账准备Less: Bad debt provision for Account receivable应收账款净额Net bal of Account receivable其他应收款Other receivable减:其他应收款坏账准备Less: Bad debt provision for Other receivable其他应收款净额Net bal of Other receivable预付账款Prepayment应收补贴款Subsidy receivable存货Inventory减:存货跌价准备Less: Provision for Inventory存货净额Net bal of Inventory已完工尚未结算款Amount due from customer for contract work待摊费用Deferred Expense一年内到期的长期债权投资Long-term debt investment due within one year 一年内到期的应收融资租赁款Finance lease receivables due within one year 其他流动资产Other current assets流动资产合计Total current assets长期投资Long-term investment长期股权投资Long-term equity investment委托贷款Entrusted loan receivable长期债权投资Long-term debt investment长期投资合计Total for long-term investment减:长期股权投资减值准备Less: Impairment for long-term equity investment 减:长期债权投资减值准备Less: Impairment for long-term debt investment 减:委托贷款减值准备Less: Provision for entrusted loan receivable长期投资净额Net bal of long-term investment其中:合并价差Include: Goodwill (Negative goodwill)固定资产Fixed assets固定资产原值Cost减:累计折旧Less: Accumulated Depreciation固定资产净值Net bal减:固定资产减值准备Less: Impairment for fixed assets固定资产净额NBV of fixed assets工程物资Material holds for construction of fixed assets在建工程Construction in progress减:在建工程减值准备Less: Impairment for construction in progress在建工程净额Net bal of construction in progress固定资产清理Fixed assets to be disposed of固定资产合计Total fixed assets无形资产及其他资产Other assets & Intangible assets无形资产Intangible assets减:无形资产减值准备Less: Impairment for intangible assets无形资产净额Net bal of intangible assets长期待摊费用Long-term deferred expense融资租赁——未担保余值Finance lease – Unguaranteed residual values 融资租赁——应收融资租赁款Finance lease – Receivables其他长期资产Other non-current assets无形及其他长期资产合计Total other assets & intangible assets递延税项Deferred Tax递延税款借项Deferred Tax assets资产总计Total assets负债及所有者(或股东)权益Liability & Equity流动负债Current liability短期借款Short-term loans应付票据Notes payable应付账款Accounts payable已结算尚未完工款预收账款Advance from customers应付工资Payroll payable应付福利费Welfare payable应付股利Dividend payable应交税金Taxes payable其他应交款Other fees payable其他应付款Other payable预提费用Accrued Expense预计负债Provision递延收益Deferred Revenue一年内到期的长期负债Long-term liability due within one year 其他流动负债Other current liability流动负债合计Total current liability长期负债Long-term liability长期借款Long-term loans应付债券Bonds payable长期应付款Long-term payable专项应付款Grants & Subsidies received其他长期负债Other long-term liability长期负债合计Total long-term liability递延税项Deferred Tax递延税款贷项Deferred Tax liabilities负债合计Total liability少数股东权益Minority interests所有者权益(或股东权益)Owners’ Equity实收资本(或股本)Paid in capital减;已归还投资Less: Capital redemption实收资本(或股本)净额Net bal of Paid in capital资本公积Capital Reserves盈余公积Surplus Reserves其中:法定公益金Include: Statutory reserves未确认投资损失Unrealised investment losses未分配利润Retained profits after appropriation其中:本年利润Include: Profits for the year外币报表折算差额Translation reserve所有者(或股东)权益合计Total Equity负债及所有者(或股东)权益合计Total Liability & Equity三、利润及利润分配表Income statement and profit appropriation 一、主营业务收入Revenue减:主营业务成本Less: Cost of Sales主营业务税金及附加Sales Tax二、主营业务利润(亏损以“—”填列)Gross Profit ( - means loss) 加:其他业务收入Add: Other operating income减:其他业务支出Less: Other operating expense减:营业费用Selling & Distribution expense管理费用G&A expense财务费用Finance expense三、营业利润(亏损以“—”填列)Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列)Add: Investment income补贴收入Subsidy Income营业外收入Non-operating income减:营业外支出Less: Non-operating expense四、利润总额(亏损总额以“—”填列)Profit before Tax减:所得税Less: Income tax少数股东损益Minority interest加:未确认投资损失Add: Unrealised investment losses五、净利润(净亏损以“—”填列)Net profit ( - means loss)加:年初未分配利润Add: Retained profits其他转入Other transfer-in六、可供分配的利润Profit available for distribution( - means loss)减:提取法定盈余公积Less: Appropriation of statutory surplus reserves提取法定公益金Appropriation of statutory welfare fund提取职工奖励及福利基金Appropriation of staff incentive and welfare fund提取储备基金Appropriation of reserve fund提取企业发展基金Appropriation of enterprise expansion fund利润归还投资Capital redemption七、可供投资者分配的利润Profit available for owners' distribution减:应付优先股股利Less: Appropriation of preference share's dividend提取任意盈余公积Appropriation of discretionary surplus reserve应付普通股股利Appropriation of ordinary share's dividend转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital八、未分配利润Retained profit after appropriation补充资料:Supplementary Information:1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments2.自然灾害发生损失Losses from natural disaster3.会计政策变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting policies4.会计估计变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting estimates5.债务重组损失Losses from debt restructuring现金流量表Cash Flow Statement一、经营活动产生的现金流量:Cash Flow from Operating Activities:销售商品、提供劳务收到的现金Cash received from sales of goods or rendering services收到的税费返还Refunds of taxes收到的其他与经营活动有关的现金Cash received relating to other operating activities现金流入小计Sub-total of cash inflows购买商品、接受劳务支付的现金Cash paid for goods or receiving services支付给职工以及为职工支付的现金Cash paid to and on behalf of employees支付的各项税费Tax payments支付的其他与经营活动有关的现金Cash paid relating to other operating activities现金流出小计Sub-total of cash outflows经营活动产生的现金流量净额Net Cash Flow from Operating Activities二、投资活动产生的现金流量:Cash Flow from Investing Activities:收回投资所收到的现金Cash received from disposal of investments处置子公司和其他经营单位收到的现金Cash received from disposal of subsidiary or other operating business units取得投资收益所收到的现金Cash received from investments income处置固定资产、无形资产和其他长期资产而收到的现金净额Net cash received from disposal of fixed assets, intangible assets and other long-term assets购买子公司所收到的现金Cash received by acquisition of subsidiary收到的其他与投资活动有关的现金Cash received relating to other investing activities现金流入小计Sub-total of cash inflows购建固定资产、无形资产和其他长期资产所支付的现金Cash paid to acquire fixed assets, intangible assets and other long-term assets投资所支付的现金Cash paid to acquire investments支付的其他与投资活动有关的现金Cash payments relating to other investing activities现金流出小计Sub-total of cash outflows投资活动产生的现金流量净额Net Cash Flow from Investing Activities三、筹资活动产生的现金流量:Cash Flow from Financing Activities:吸收投资所收到的现金Cash received by investors借款所收到的现金Cash received from borrowings其中:从金融机构借款所收到的现金Include: Cash received from financial institution borrowings收到的其他与筹资活动有关的现金Cash received relating to other financing activities现金流入小计Sub-total of cash inflows偿还债务所支付的现金Repayments of borrowings其中:偿还金融机构债务所支付的现金Include: Repayments of financial institution borrowings分配股利、利润和偿付利息所支付的现金Dividends paid, profit distributed or interest paid支付的其他与筹资活动有关的现金Cash payments relating to other financing activities现金流出小计Sub-total of cash outflows筹资活动产生的现金流量净额Net Cash Flow from Financing Activities四、汇率变动对现金的影响额Effect of Foreign Currency Translation五、现金及现金等价物净增加额Net Increase (Decrease) in Cash and Cash Equivalents现金流量附表:Supplementary Information:1.将净利润调节为经营活动的现金流量:Reconciliation of Net Profit to Cash Flow from Operating Activities:净利润Net Profit加:少数股东损益Add: Minority interest加:计提的资产减值准备Impairment losses on assets固定资产折旧Depreciation of fixed assets无形资产摊销Amortisation of intangible assets长期待摊费用摊销Amortisation of long-term deferred expenses待摊费用减少(减:增加)Decrease (increase) in deferred expenses预提费用增加(减:减少)Increase (decrease) in accrued expenses处置固定资产、无形资产和其他长期资产的损失(减、收益)Losses (gains) on disposal of fixed assets, intangible assets and other long-term assets固定资产报废损失Losses on write-off of fixed assets财务费用Finance expense (income)投资损失(减、收益)Losses (gains) arising from investments递延税款贷款(减、借项)Deferred tax credit (debit)存货的减少(减、增加)Decrease (increase) in inventories经营性应收项目的减少(减、增加)Decrease (increase) in receivables under operating activities经营性应付项目的增加(减、减少)Increase (decrease) in payables under operating activities其他Others经营活动产生的现金流量净额Net cash flow from operating activities2.不涉及现金收支的投资和筹资活动:Investing and Financing Activities that do not Involve Cash Receipts and Payments:债务转为资本Conversion of debt into capital一年内到期的可转换公司债券Reclassification of convertible bonds expiring within one year as current liability融资租入固定资产Fixed assets acquired under finance leases3.现金及现金等价物净增加情况:Net Increase in Cash and Cash Equivalents:现金的期末余额Cash at the end of the period减:现金的期初余额Less: cash at the beginning of the year加:现金等价物的期末余额Add: cash equivalents at the end of the period减:现金等价物的期初余额Less: cash equivalents at the beginning of the period现金及现金等价物净增加额 Net increase in cash and cash equivalents。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

一年内到期的长期负债 86

企业负责人:

财务负责人:

制表人: