Analysis of company's accounting treatment of the New Perspective-毕业论文翻译

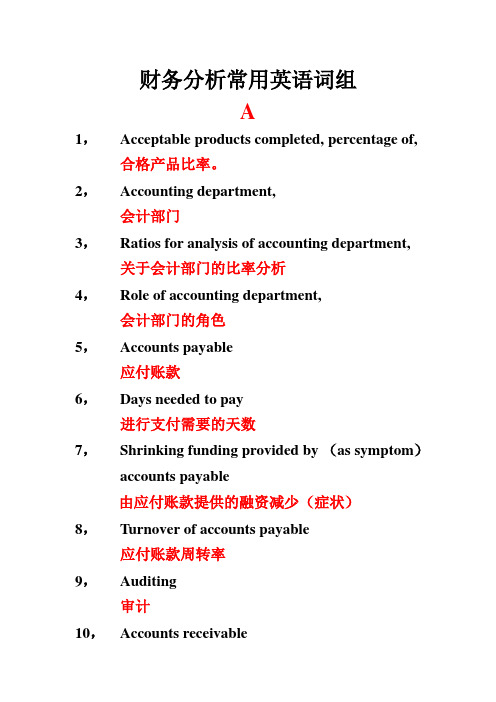

财务分析常用英语词组

财务分析常用英语词组A1,Acceptable products completed, percentage of, 合格产品比率。

2,Accounting department,会计部门3,Ratios for analysis of accounting department, 关于会计部门的比率分析4,Role of accounting department,会计部门的角色5,Accounts payable应付账款6,Days needed to pay进行支付需要的天数7,Shrinking funding provided by (as symptom)accounts payable由应付账款提供的融资减少(症状)8,Turnover of accounts payable应付账款周转率9,Auditing审计10,Accounts receivable应收账款11,Collectibility of accounts receivable应收账款的可回收性12,Days needed to collect应收账款周转天数13,Increasing investment in (as symptom)accounts receivable在应收账款上的投资增加(症状)14,Overdue accounts receivable过期应收账款15,Accounts receivable as proportion of sales 应收账款占销售的百分比16,Accounts receivable and working capital 应收账款和营运资本17,Accrued interest应计利息18,Accrued liabilities应计负债19,Calculating计算20,Acquisition analysis并构分析21,Asset analysis资产分析22,Brand analysis品牌分析23,Capacity analysis产能分析24,Cash flow analysis现金流分析25,Contractual issues related 相关的合同事宜26,Legal issues related相关的法律事宜27,Fraud analysis欺诈分析28,Liability analysis负债分析29,Obtaining information for 获得收购信息30,Patent analysis专利分析31,Personal analysis人员分析32,Profitability analysis盈利能力分析33,Synergy analysis协同分析34,Types of acquisition analysis 收购分析的类型35,Advertising广告36,Annualized pay reports年度工资报告37,Anticipation surveys预测调查38,Appraisal companies评估公司39,Arithmetic mean算术平均值40,Collections from sales of assets 从资产销售中回收的款项41,Expensive assets昂贵的资产42,Increased return on assets资产上增加的回报43,Asset analysis (for evalution of acquisition targets)资产分析(评估收购目标)44,Assumption假设45,Automated ratio result analysis自动的比率分析结果46,Average collection period平均收款期47,Average delivery time平均送货时间48,Average equipment setup time设备平均调试时间49,Average interest rate eared获得的平均利率50,Average time to fill requested positions完成特定员工招聘的平均时间51,Average yearly ways per employee员工平均年薪B52,。

英语财务笔试题库及答案

英语财务笔试题库及答案1. What is the difference between a balance sheet and an income statement?Answer: A balance sheet is a snapshot of a company's financial condition at a specific point in time, showing assets, liabilities, and equity. An income statement, on the other hand, reports a company's financial performance over a period of time, including revenues, expenses, and net income.2. Define the term 'Depreciation'.Answer: Depreciation is the systematic allocation of the cost of a tangible asset over its useful life to reflect the consumption of the asset.3. Explain the concept of 'Accrual Accounting'.Answer: Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned or incurred, not when cash is received or paid.4. What is 'Capital Budgeting' and why is it important?Answer: Capital budgeting is the process of evaluating investment opportunities to determine whether they are financially viable and beneficial for a company. It is important as it helps in making long-term financial decisions.5. How do you calculate 'Net Present Value' (NPV)?Answer: Net Present Value (NPV) is calculated bysubtracting the present value of cash outflows (includinginitial investment) from the present value of cash inflows over a period of time, using a discount rate.6. What is 'Financial Leverage' and how does it affect a company?Answer: Financial leverage refers to the use of borrowed funds to increase the return on equity. It affects a company by increasing the risk and potential return on investment.7. Describe the 'Time Value of Money'.Answer: The time value of money is the concept that a sum of money is worth more now than the same sum in the future due to its potential earning capacity.8. What is 'Earnings Per Share' (EPS)?Answer: Earnings Per Share (EPS) is a financial metric calculated as the company's net income divided by the outstanding shares of its common stock, indicating the profit allocated to each share.9. Explain the 'Cash Conversion Cycle'.Answer: The cash conversion cycle is the length of time it takes for a company to convert its investment in inventory and receivables into cash.10. What is 'Break-Even Analysis' and how is it used?Answer: Break-even analysis is a method used to determine the number of units a company must sell to cover its costs and make a profit. It is used to evaluate the financial viability of a project or business.11. Define 'Working Capital'.Answer: Working capital is the difference between a company's current assets and current liabilities, representing the funds available for day-to-day operations.12. What is 'Liquidity Ratio' and how is it calculated?Answer: Liquidity ratio is a measure of a company'sability to pay short-term obligations. It is calculated by dividing current assets by current liabilities.13. Explain 'Return on Investment' (ROI).Answer: Return on Investment (ROI) is a financial metric that measures the profitability of an investment. It is calculated by dividing the net profit from the investment by the initial cost of the investment.14. What is 'Inflation' and how does it affect financial statements?Answer: Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. It affects financial statements by reducing the real value of assets and increasing the cost of goods and services.15. Define 'Audit' in the context of finance.Answer: An audit is a systematic review and examination of a company's financial records, typically performed by an independent third party, to ensure accuracy, compliance with regulations, and to detect fraud.。

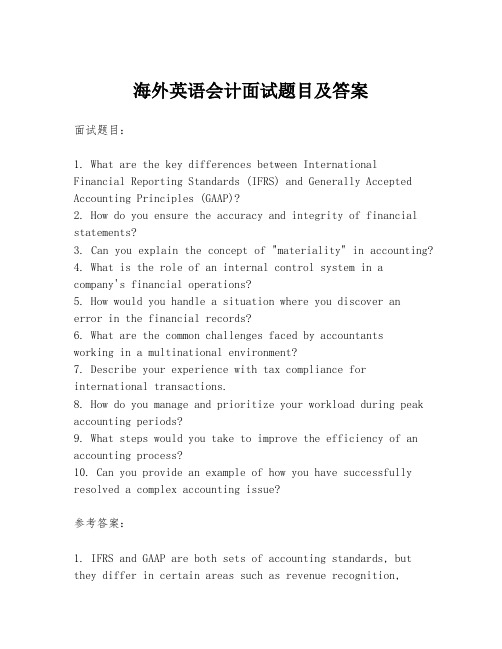

海外英语会计面试题目及答案

海外英语会计面试题目及答案面试题目:1. What are the key differences between InternationalFinancial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP)?2. How do you ensure the accuracy and integrity of financial statements?3. Can you explain the concept of "materiality" in accounting?4. What is the role of an internal control system in a company's financial operations?5. How would you handle a situation where you discover anerror in the financial records?6. What are the common challenges faced by accountantsworking in a multinational environment?7. Describe your experience with tax compliance for international transactions.8. How do you manage and prioritize your workload during peak accounting periods?9. What steps would you take to improve the efficiency of an accounting process?10. Can you provide an example of how you have successfully resolved a complex accounting issue?参考答案:1. IFRS and GAAP are both sets of accounting standards, but they differ in certain areas such as revenue recognition,lease accounting, and financial instruments. IFRS tends to be more principles-based, while GAAP is more rules-based.2. Ensuring the accuracy and integrity of financial statements involves a combination of internal controls, regular audits, and adherence to accounting standards and regulations.3. Materiality refers to the significance of an item in the context of the financial statements. Items are considered material if their omission or misstatement could influence the decisions of users of the financial statements.4. An internal control system helps to ensure the reliability of financial reporting, compliance with laws and regulations, and the safeguarding of assets. It involves policies and procedures that are designed to prevent and detect errors and fraud.5. If I discover an error in the financial records, I would first verify the error, determine its impact, and then follow the company's established procedures for correcting and disclosing the error.6. Challenges faced by accountants in a multinational environment include dealing with different accounting standards, tax regulations, and cultural differences, as well as managing time zones and language barriers.7. My experience with tax compliance for international transactions involves understanding the tax laws of different jurisdictions, ensuring that transactions are reported correctly, and working with tax advisors to minimize tax liabilities.8. During peak accounting periods, I prioritize tasks based on deadlines and the importance of the work, delegate tasks when possible, and maintain clear communication with my teamto ensure that all work is completed accurately and on time. 9. To improve the efficiency of an accounting process, Iwould analyze the current workflow, identify bottlenecks, implement automation where possible, and provide training to staff to ensure they are using systems and processes effectively.10. An example of resolving a complex accounting issueinvolved a situation where a subsidiary was not correctly applying consolidation principles. I worked with the team tore-evaluate the consolidation criteria, restate the financial statements, and provide training to ensure ongoing compliance.结尾:In conclusion, the role of an accountant in an international context is multifaceted and requires a deep understanding of various accounting principles, as well as the ability toadapt to different regulatory environments. The questions and answers provided aim to give insight into the skills and knowledge expected of a candidate for an accounting positionin an overseas setting.。

会计英语判断题

Chapter One(1). The job of an accountant is to record transactions and post them to the ledgers.(F)(2). Double-entry bookkeeping developed in Europe in the Middle Ages. (T)(3). The functions of accounting have increased with the rapid development of management science. (T)(4). There are only two fields of accounting: financial accounting and managerial accounting.(F)(5). Only the management needs the financial information about an economic entity.(F)(6). Financial accounting prepares information for the management.(F)(7). Private accountants work for private people.(F)(8). Public accountants earn salaries for their professional work.(F)(9).Securities and Exchange Commission issues regulations for preparing financial statements in the U.S.. (T)(10). American Accounting Association is an organization primarily for accounting educators. (T)(11). The expenses of the owners of proprietorship should be recorded in a business’s expense accounts.(F)(12). After the financial statements are prepared a company will continue its business. (T)(13). The usual time period for a business is a year, called the financial/fiscal year. (T)(14). As a result of inflation, the purchasing power of money will decrease, so the accountants should record the value of assets in their decreased values.(F)(15). According to Materiality Principle, the purchase of stationery can be recorded as an expense. (T)(16). Objectivity Principle and Cost Principle are mutually supported. (T)(17). Objectivity Principle and Materiality Principle are somewhat contradictory. (T)Chapter Two(1). The simplest form of business organizations is Proprietorship. (T)(2).The proprietorship has a single owner. (T)(3).Partners of partnership have limited liability for debts.(F)(4). If a corporation goes bankrupt, shareholders need not pay for the debts with their personal assets.(T)(5).In the proprietorship, the owner’s equity is capital. (T)(6).The accounting equation can also be expressed as “Assets – Liabilities = Owner’s Equity”.(T)(7).An owner’s investment in a business increases assets and capital. (T)(8).When a business buys equipment, it can either pay cash or make the purchase on account. (T)(9).Buying something on account creates a liability. (T)(10).When a business provides goods or service, it receives revenue from its customers or clients.(T)(11).The payment of Accounts Payable decreases assets and liability. (T)(12).The payment of expenses decreases assets and owner’s equity.(T)(13).The owner of proprietorship can withdraw money for personal use.(T)(14).When the owner of proprietorship pays for expenses with his personal funds, the accountant need not record the event. (T)Chapter Three(1) The double-entry system is based on the principle of duality.(T)(2) Every transaction affects at least two accounts.(T)(3) The entry for $50000 cash investment in a business isDr. Cash 50000Cr. Capital 50000 (T)(4) The Expenses in the owner’s house paid with his personal fund should not be recorded in the business’s accounts.(T)(5) Debit means increase while credit means decrease.(F)(6) The remaining amount of an account is called its balance.(T)(7)The journal is a chronological record of the business’s transactions.(T)(8) Posting is the process of transferring information from the ledger to the journal.(F)(9) The normal balances of asset accounts are debits.(T)(10) Withdrawal of cash by the owner is a deduction of capital.(T)Chapter Four(1) The three major financial statements are the income statement, the statement of owner’s equity and the balance sheet.(T)(2)The income statement reflects the revenues and expenses of a specific date.(F)(3)The statement of owner’s equity reflects the changes in owner’s equity for a specific period.(T)(4)The balance sheet shows the balances of assets, liabilities and owner’s equity for a specific period of time.(F)(5)The three major financial statements are related to one another.(T)(6)Current liabilities do not include long-term liabilities due within this accounting period.(F)(7)Patents,trademarks and goodwill are all assets, so they should appear in an entity’s financial statements. (F)(8)Liquidity is a measure of how quickly an item can be converted to cash.(T)(9)Current ratio is the ratio of an entity’s current assets to its current liabilities.(T)(10)It is desirable for an entity to maintain a low debt ratio.(T)(11)For an entity, the higher its gross margin percentage is, the better.(T)(12)An entity wants to maintain a low inventory turnover.(F)Chapter Five(1) Revenues enhance an entity’s assets. (T)(2) Expenses are incurred in the course of an entity’s revenue-making activities.(T)(3) Revenues result in a decrease in the owner’s equity while expenses result in an increase in the owner’s equity.(F)(4)Revenue and expense accounts are permanent.(F)(5)Asset, liability and owner’s equity accounts have balances at the end of the accounting period.(T)(6)Under accrual basis, revenues are recognized when cash is received.(F)(7)When a doctor renders services to a patient, this activity creates revenue no matter whether the cash is received or not.(T)(8)Financial statements pertain to a definite period.(T)(9)Expenses must go with the revenues they help to produce.(T)(10)Unearned revenues are revenues which have been earned but the cash has not been received.(F)(11)Accrued revenues are revenues which you have received but have not rendered services for the clients.(F)(12)Prepaid expenses are expenses which have been paid for before they are incurred.(T)(13)At the end of the accounting period, supplies used are recorded as a debit to Supplies Expense and a credit to Supplies.(T)(14)The cost of depreciation is recorded as a debit to Depreciation Expense and a credit to the Fixed Asset account. (F)(15)Accumulated Depreciation appears in the Balance Sheet as a separate account.(F)(16)Adjusted Trial Balance has only Asset, Liability and Owner’s Equity Accounts. (T)Chapter Six(1) The accounting cycle starts with the analysis of transaction source documents. (T)(2) The accounting cycle ends with the preparation of financial statements. (F)(3) The balances in the trial balance of the work sheet are the beginning balances of the accounts. (F)(4) The balances of the expense and revenue accounts in the trial balance of the work sheet include all the expenses and revenues for the accounting period. (F)(5) The total of the debit side does not equal to the credit side for the Income Statement in the work sheet. (T)(6) The amount for the Capital account in the work sheet is the beginning balance of the accounting period. (T)(7) The total for the debit side of the Balance Sheet in the work sheet is the total of Assets. (F)(8) At the end of the accounting period, only the revenue and expense accounts should be closed. (F)Chapter Seven(1) A merchandising business needs to purchase the goods it sells first.(T)(2) When a merchandising business purchases goods, the journal entry is a debit to Inventory and a credit to Cash. (F)(3) A discount is made by the seller to the buyer for prompt payment.(T)(4) A sales return is the amount which the returned goods from sellers cost.(F)(5) Cost of goods sold = Beginning Inventory + Net Purchase – Ending Inventory (F)(6) Purchase discount is not computed on the freight charges.(T)(7) Inventory is an Expense account.(F)(8) Purchase is an asset account.(F)(9) In the work sheet, the Inventory account has two balances, both the beginning balance and the ending balance.(T)(10)The adjusting entries of a merchandising business are the same as those of a service business.(T)(11)Both the beginning and the ending balances of the Inventory account should be closed.(T)(12) Purchase Discounts and Purchase Returns and Allowances accounts have Debit balances.(F)Chapter Eight(1)All the sales are recorded in a Sales Journal.(F)(2)Only the credit sales are recorded in a Sales Journal. (T)(3)All the purchases are recorded in a Purchase Journal.(F)(4)Only the purchases of merchandise are recorded in a Purchase Journal. ((F)(5)All the amounts that are posted to the general ledger are totals.(F)(6)All the postings are made at the end of an accounting period.(F)(7)All the accounts have its subsidiary accounts. (F)(8)General Journals are not used by merchandising businesses.(F)。

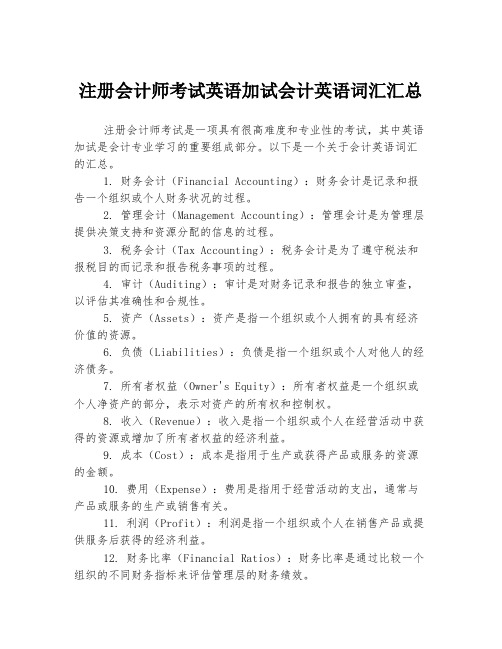

注册会计师考试英语加试会计英语词汇汇总

注册会计师考试英语加试会计英语词汇汇总注册会计师考试是一项具有很高难度和专业性的考试,其中英语加试是会计专业学习的重要组成部分。

以下是一个关于会计英语词汇的汇总。

1. 财务会计(Financial Accounting):财务会计是记录和报告一个组织或个人财务状况的过程。

2. 管理会计(Management Accounting):管理会计是为管理层提供决策支持和资源分配的信息的过程。

3. 税务会计(Tax Accounting):税务会计是为了遵守税法和报税目的而记录和报告税务事项的过程。

4. 审计(Auditing):审计是对财务记录和报告的独立审查,以评估其准确性和合规性。

5. 资产(Assets):资产是指一个组织或个人拥有的具有经济价值的资源。

6. 负债(Liabilities):负债是指一个组织或个人对他人的经济债务。

7. 所有者权益(Owner's Equity):所有者权益是一个组织或个人净资产的部分,表示对资产的所有权和控制权。

8. 收入(Revenue):收入是指一个组织或个人在经营活动中获得的资源或增加了所有者权益的经济利益。

9. 成本(Cost):成本是指用于生产或获得产品或服务的资源的金额。

10. 费用(Expense):费用是指用于经营活动的支出,通常与产品或服务的生产或销售有关。

11. 利润(Profit):利润是指一个组织或个人在销售产品或提供服务后获得的经济利益。

12. 财务比率(Financial Ratios):财务比率是通过比较一个组织的不同财务指标来评估管理层的财务绩效。

13. 资本预算(Capital Budgeting):资本预算是一种决策过程,用于评估和选择投资项目,以确定最有利可图的项目。

14. 风险管理(Risk Management):风险管理是一种评估和管理一个组织面临的潜在风险的过程,以减少损失和不确定性。

15. 现金流量(Cash Flow):现金流量是一个组织或个人在一段时间内收入和支出现金的净量。

某公司财务会计及财务管理知识分析英文版fppn

organizations.

Copyright © 2010 Pearson Education Canada

25

The Accounting Equation

Copyright © 2010 Pearson Education Canada

Canadian GAAP will converge with IFRSs

1st year for reporting under IFRS-based standards will be 2011

Copyright © 2010 Pearson Education Canada

15

Learning Objective 2

18

The Business Entity Concept

Copyright © 2010 Pearson Education Canada

19

The Cost Principle

Copyright © 2010 Pearson Education Canada

20

The Going-Concern Concept

Accountants follow professional guidelines.

The rules that govern accounting are called GAAP (generally accepted accounting principles).

Copyright © 2010 Pearson Education Canada

Income Statement

Balance Sheet

财务管理专业英语翻译

1、Financial management is an integrated decision-making process concerned with acquiring,financing, and managing assets to accomplish some overall goal within a business entity. 财务管理是为了实现一个公司总体目标而进行的涉及到获取、融资和资产管理的综合决策过程。

2、Making financial decisions is an integral part of all forms and sizes of businessorganizations from small privately-hold forms to large publicly-traded corporations.做财务决策对于所有形式和规模的商业组织,无论是小型私人公司还是大型股份公开交易的公司来说,都是不可分割的一部分。

3、In today’s rapidly changing environment, the financial manager mus t have the flexibilityto adapt to external factors such as economic uncertainty, global competition, technological change, volatility of interest and exchange rates, changes in laws and regulations, and ethical concerns.在当今瞬息万变的环境中,财务经理必须具备足够的灵活性以适应外部因素,如经济的不确定性、国际竞争、技术变革、利息波动、汇率变动、法律法规变化以及商业道德问题。

4、The financial manager makes investment decisions about all types of assets-items on theleft-hand side of the balance sheet.财务经理要做出关于所有形式的资产—即资产负债表左侧所列示项目的投资决定。

会计中英对照

《公开发行股票公司信息披露的内容与格式准则》《公司法》company law《股票发行与交易管理暂行条例》与《公开发行股票公司信息披露实施细则》安全付款表safe payments schedule版权copyrights半成品成本semi-finished product cost包装物保险企业会计accounting of insurance companies保证金法deposit method报告成本reporting cost备查账簿memorandvn备抵附加账户provision and adjunct accounts备抵账户provision accounts比例合并proportionate consolidtion美比例履行法比率分析法ration analysis apporach币值稳定假设constant-dollar assumption变动成本法variable costing标准成本standard cost标准成本法standard costing标准成本控制制度standard cost control system表融资off-balance-sheet financing表外账户off-balance sheet accounts拨定留存收益appropriated retained earnings拨入专款restricted appropriation补充登记法correction by extre recording不定期清查non-periodic checking method不合并子公司unconsolidated subsidiaries不可控成本uncontrollable cost部分分摊法partial allocation簿记bookkeeping材料费用分配material costs allocation财产清查physical inventory财产税property tax财产信托会计fiduciary accounting美财务报表financial statements财务报表要素elements of financial statements财务报告financial report财务成本与管理成本financial cost and manegement cost财务费用financing expenses财务分析financial analysis财务管理financial managment财务管理对象objects of financial management财务管理环节the cycle of financial managemten财务管理环境financial management environment财务管理目标financial management objectives财务管理内容the content of financial management财务管理原则the principle of financial management财务管理职能the functions of finaneial management财务管理组织organization of financial management财务会计financial accounting财务会计概念框架financial accounting conceptual framework财务会计原则finanicial accounting principles财务活动financial activities财务计划financial planning财务监督financial cupervision财务决策financial decision财务控制financial control财务预测financial forecast财务政策financial policy财务制度financial regulations财政补助收入grant from the state财政负债public finance-liabilities财政净资产public finance-net assets财政收入public finance-revemue财政性存款public finance-cash in bank财政支出public finance expenditure财政周转基金public finance-revolving fund财政周转金收入income from revolving fund财政周转金支出expenditure on revolvring fund财政资产public finance-assets财政总预算会计public finance budgetary accounting财政总预算会计年终结账public finance budgetary accounting-year-end sosing 财政总预算会计年终清理public finance budgetary accounting-year-end checking 财政总预算会计制度budgetary accounting regulations for public finance拆借市场lending market产成品成本finished product cost产品成本product cost产品成本计划the plan of product costs产品成本技术经济分析产品成本项目cost items of product产品寿命周期成本product life cycle cost长期负债long-term liability of long-term debt长期借款long-term loans长期投资long-term investments长期应付款long-term payables偿债基金sinking fund厂内结算价格internal settlement prices厂内经济核算制internal business accounting system车间成本workshop cost车间经费【旧】成本cost成本报表cost statement成本报告costing report成本差异cost variance成本调整cost adjustment成本法cost method成本费用界限成本分类cost classifiction成本分类账cost ledger成本分配ocst allocation成本分析cost analysis成本管理cost management成本归集cost accumulation成本核算costing成本核算成本costing account成本核算程序cost accounting qrocedures成本核算原则principle of costing成本回收法cost recovery method成本会计cost accounting成本计划cost plan成本计划管理体系planned management system of cost 成本计划完成情况分析成本计算单位costing unit成本计算对象costing objective成本计算方法costing method成本计算分步法成本计算分类法group costing method成本计算分批法job costing method成本计算简单法simple costing method成本计算品种法category costing method成本计算期cost period成本计算账户costing accounts成本记录cost entry, cost recorder cost agenda成本结构cost structure成本开支范围allowable cost成本考核cost assess成本考核指标cost examming target成本控制cost control成本控制标准standard of cost control成本控制程序procedure of cost control成本控制方法cost control method成本流程cost flow成本曲线cost curve成本转账cost transfer承兑市场acceptance market承租人会计accounting for leases-leasee持仓盈亏opsition gain and loss持续经营going concern持有产损益holding gains losses出租人会计accounting for leases-lessor创立合并consolidation从属账户Secodary accounts存货inventory存货销售的影响effects of inventory errors存货转让价格inventory transfer price存置成本holding cost or carrying cost待处理固定资产损失待处理流动资产损失待核销基建支出[旧]待摊费用单式记账法single-entry bookkeeping单式记账凭证singlle accunt title voucher单位成本与总成本unit cost and total cost单行合并one-line consolidation美单一汇率法singal method当代理论contemporary theory当期经营观点current operating concept of income等级产品成本计算graded product costing低值易耗品递延法deffered method递延资产deferred asset店头市场over-the -counter-market调整分录adjusting journal entry调整后的净现值adjusted net present value调整账户adjustment accounts订本式账簿bound book订量单位:units of measurement定额成本norm cost定额成本控制制度norm cost control system定额管理management norm定期盘存制periodic inventory system定期清查Periodic ckecking method动力费用分配power expenses allocation冻结资金保值maintaining the value of blocked funds冻结资金转移repatriating blocked funds独资企业sole proprietorship短期借款short-term loans短期投资temporary investment对比分析法comparative analysis approach对附属单位补助grant to the auxiliary organization对境外实体的净投资net investment in foreign entities对内报表internal statements对外报表external statements对外经济合作企业会计accounting of foreign economic cooperation enter prises 对应账户corresponding accounts对账checking多栏式日记账核算形式bookkeeping procedure using columnar journal多种汇率法multiply exchange rate二级市场security secondary market反馈价值feedback value房地产real estate房地产成本cost of real setate房地产开发成本房地产开发企业会计accounting of real estate enterprises房地产收入real estate revenue非货币性项目nonmonetary items废品损失spoliage and defective work losses废弃和生置法retirement and replacement method费用expense费用的确认recognition of expense分部报告segmental reporting分次清算installment liquidation分类账簿ledger分期收款销货installment sales分散核算分支机构branch分支机构会计accounting for branch浮动汇率floating rate辅助生产成本分配auxiliary production cost allocation付款凭证payment voucher负权人偿金dividend负商誉negative goodwill负债liability附加账户adjunct accounts附属单位缴款payment from the auxiliary organization附属公司associated company复合分录compound entry复式记账法Double entry bookkeeping复式记账凭证mvltiple account titles voucher复杂权益法complex equity method副产品成本计算by-product costing改组reorganization改组计划reorganization plan美高等学校财务制度financial regulations for colleges and universities高等学校负债colleges and universities liabilities高等学校会计colleges and universities accounting高等学校会计报表分析colleges and universities analysis of accounting statements 高等学校会计制度accounting regulations for institutions of higher learning高等学校结余colleges and universities surplus高等学校净资产colleges and universities net assets高等学校收入colleges and universities revenues高等学校预算管理方式budget management method of colleges and universities 高等学校支出colleges and universities expenditures高等学校资产colleges and universities assets高新技术企业会计accounting of high technology enterprises个别报表individual statements个人财务报表personal financial state-ments美个人所得税personal income tax耕地占用税工厂成本factory cost工程施工成本工程物资工业会计accounting of industrial enterprises工资费用分配salary costs allocation工作底稿working paper公共会计public accounting公认会计原则generally accepted accounting principle,GAAP公司company公司间的长期资产业务intercompany transactions in long-term assets 公司内部贷款intercompany loans公司债券bonds payable公司债券偿还redemption of bonds公司债券发行corporate bond floatation公司债券发行价格corporate bond issuing price公司债券利率interest rate on debenture公司债券利息摊销公益金公允价值fair value功能性货币functional currency美共同费用分配home office-branch expense allocation购货折扣purchases discounts购买法purchase methed购买力损益purchasing power gains or loosses股本capital stock股份两合公司limited pactnership股份有限公司company limited by shares股份制企业会计accounting of stock companies股利dividend股利转移dividend kemittances股票指数期货stock index futrues固定汇率fixed rate固定资产fixed assets固定资产更换与改良improvements and replacements of fixed assets 固定资产扩建additions of fixed assets固定资产投资方向调节税固定资产修理repairs and maintenance of fixed assets固定资产折旧depreciation of fixed assets固定资产重估价revaluations of fixed assets关税tariff管理费用管理工具论manegement tool perspective管理会计management accounting管理活动论management activities perspective国际存货管理international inventory management国际投资决策会计foreign project appraisal国际投资决策会计foreign project appraisal国家决算final accounts of state revenue and expenditure国家预算state budget国有独资公司过账posting航空运输成本合并报表consolidated fiancial statements合并财务状况变动表consolidated statement of changes in financial poition合并财务状况变动表consolidated statement of changes in financial poition合并费用expenses related to combinations合并会计报表consolidated financial statements合并价差cost-book value differentials合并每股收益consolidated EPS合并前股利preacquisition dividends合并前利润preacquisition income合并损益表consolidated income statement合并现金流量表consolidated statement of cash flow合并主体的所得税会计accounting for income taxes of consolidated entities美合并资产负债表consolidated balance sheet合伙企业partnership enterprise合伙清算partnership liquidation合伙权益的转让assignment of partnership interest美横向合并horizontal integration横向销售crosswise sale红利法bonus procedure红字更正法correction by using red ink宏观会计macro-accounting宏观经济成本macro economic cost后进先出法last-in,first-out,LIFO划分资本性支出与收益性支出原则 distinguishment between capital expenditure and revenue expenditiure划线更正法correction by drawing a straight ling坏账bad debts换算风险管理managing translation exposure换算损益translation gains or losses黄金市场gold market汇兑损益exchange gains or losses汇率exchange rate汇总报表combination statements汇总记账凭证核算形式bookkeeping procedure using summary ovchers汇总原始凭证cumulative source document汇总原始凭证cumulative source document会计accounting会计报表accounting statements会计本质nature of accounting会计等式accounting equation会计对象accounting object会计分录accounting entry会计分期accounting periods会计管理体制system of accounting admin tstration 会计核算financial accounting会计核算形式bookkeeping procedures会计环境accounting environment会计机构accounting department会计计量accounting measurement会计记录accounting records会计假设accounting assumption会计监督accounting supervision会计决策accounting decision making会计科目account title会计科目表chart of accounts会计控制accounting control会计理论accounting theory会计理论结构theoretical structure of accounting会计利润accounting income会计目标accounting objective会计凭证accounting documents会计确认accounting recognition会计人员accounting personnels会计任务targets of accounting activities会计信息accounting information会计学accounting会计学科体系accounting science system会计循环accounting cycle会计研究accounting research会计要素accounting elements会计预测accounting for ecasting会计账簿Book of accounts会计职能functions of accounting会计职业道德accounting professional ethics会计主体accounting entity会计准则accounting standards混合合并conglomeration活页式账簿loose-leaf book或有负债contingent liability货币非货币法monetary/no monetary货币计量monetary measurement货币市场money market货币项monetary items货币资金基本生产【旧】基本业务利润基金论the fund theory基金预算结余surplus of fund budget基金预算收入fund budget revenue基金预算支出fund budget expenditure及时性原则timeliness集合分配账户clearing accounts集中核算计划成本planned cost计划成本核算计价对比账户matching accounts计量属性measurement attributes记账本位币recording currency记账本位币recording currency记账方法bookkeeping methods记账规则recording rules记账汇率recording rate记账凭证voucher记账凭证核算形式Bookkeeping proced ureusing vouchers记账凭证汇总表核算形式bookkeeping procedure using categorized account summary 加速折旧法accelerated depreciation methods价格差异price variance间接标价法indirect quotation间接控股indirect holding简单分录simple entry简单权益法simple equity method建设单位会计accounting of construction units交互分配法reciprocal allocation approach美交通运输企业会计accounting of communication and transportation enterprises交易风险管理managing transaction exposure结算账户settlement accounts结账closing account结账分录closing entry借贷记账法debit-credit bookkeeping金融工具financial instruments金融期货交易financial futures transaction金融企业会计accounting of finacial institutions金融市场financial market谨慎性原则prudence经济风险管理managing economic exposure经济利润economic income经营收入operating revenue经营支出orerating expense经营租赁operating lease精算报告actuaries’report净利润net income局部清查partial ckeck举债经营融资租赁leveraged lease举债经营收购Leveraged buyouts,简称LBC美决策成本cost of decision making卡片式账簿card book科学事业单位财务制度financial regulations for scientific research institutes科学事业单位成本费用管理scientific research institutes-cost maragement科学事业单位会计sicentific research institute accounting科学事业单位会计报表分析scientific research institutes-analysis of accounting statements科学事业单位会计制度accointing regulations for scientific research instifutes 科学事业单位结余scientific research institutes’surplus科学事业单位收入scientific research institutes’revenues科学事业单位预算scientific research institutes’budgeting科学事业单位支出scientific research institutes’expenditures科学事业单位资产scientific research instifutes’assets可比产品成本分析general product cost analysis可比性原则comparability可避免成本与不可避免成本avoidable cost and unavoidable cost可变现净值net realizable可变现净值法net realizable value可递延成本与不可递延成本deferrable cost and undeferrable cost可控成本controllable cost可转换债券convertible bonds可转让定期存单市场negotiable CDmarket客观性原则objectivity控股合并acquisition of majority interest控投公司holding company库藏股法treasury stock approach美跨国经营企业业绩评价multinational performance evaluation跨国运转资本会计multinational working capital management跨国资本成本的计算the cost of capital for foreign lnuertments跨期摊提费用分配inter-period expenses allocation跨期摊提账户inter-period allocation accounts劳务因素service factor累计凭证multiple-record document理论成本与应用成本theory cost and practice cost历史成本与未来成本historical cost and future cost历史成本原则pringciple of historical cost利率期货交易interest rate futrues transaction利润中心利润总额利息资本化capitalization of interests利益分配profit distribution联产品成本计算joint products costing联合会计报表combined financial state-ments联合账簿compound book两笔交易观two-transaction opinion零售价格法retail method流动非流动性法current/noncurrent method流动负债current liabilities流动资产current assets流动资金流转会计accoung for circulatin tax旅游、饮食服务企业会计accounting of tourinsm and service买入汇率buying rate卖出汇率selling rate民航运输企业会计accounting of civil aviation transportation enterprises 名义货币保全maintaining capital in units of money名义货币单位units of nominal currency明细分类账簿subsidiary ledger明细分类账户subsidiary account母公司parent company母公司持股比例变动change in ownership percentage held by parent目标成本target cost内部成本报表internal cost statement内部往来transactions between home office and branches内河运输成本纳税影响法tax effect method年度报告annual report农业会计accounting of agzicultural enterprises农业生产成本agriculture production cost盘存法inventory method盘存账存inventory accounts配比原则matching平仓盈亏offset gain and loss平均成本与个别成本avorage cost and individual cost平行登记parallel recording破产清算bankrupcy liquidation破产受托人清算组会计trustee accounting期货合约futrues contract期货交易futures transaction期货交易市场market of futures transaction期货市场future market期间,费用期间费用期末存货的未实现损益unrealized profit in ending inventory期内所得税分摊intraperiod tax allocation美期权options期权市场option market其他货币资金其他收入miscellaneous gains其他业务利润其他应收款other receivables企业财务business finance企业管理费【旧】企业合并business combination企业合并会计accounting for business combination企业会计business accounting企业集团business qroup企业论the enterprise theory企业整体价值the value of an enterprise as a whole企业组织形式forms of enterprise organization汽车运输成本趋势分析法trend analysis approach全部产品成本分析全部成本absorption cost全部履行法全面成本控制total cost control全面分摊法comprehensive allocation全面清查complete check权益法equity method权益结合法pooling of interest method权益理论equity theory权责发生制原则accrual basis燃料费用分配fuel expenses allocation认股权stock rights日记总账combinod journal and ledger日记总账核算形式bookkeeping procedure using summarized journal 融资租赁financing lease三式记账法triple-entry bookkeeping商标权trademarks and tradenames商品采购成本merchandise procurement cost商品寄销consignment商品流通企业会计accounting of commercial enterprises商品期货交易futrues for commodity商品销售成本cost of merchandise sold商誉goodwill商誉法goodwill procedure上级补助收入grant from the higher authority上缴上级支出payment to the higher authority上市公告书listed company statment少数股东权益minority stockholder’s interest少数股东损益minority interest income社会成本society cost升水premium生产成本production cost生产成本汇总程序accumulation process of procluction cost生产法production method生产费用要素elements of production expenses生产能力保全maintaining capital in terms of productive capacity生产损失核算production loss accounting剩余权益论the residual equity theory施工企业会计accounting of construction enterprises时间性差异timing difference时态法temporal method实地盘存制periodic inventory system实际成本与估计成本actual cost and estimated cost实收资本paid-in capital实体理论entity theory实体论the entity theory实现原则realization principle实账户real accounts实质量于形式substance over form事业,收入事业单位财务清算liquidation of non-profit organization事业单位对外投资outside investments for non-profit organizations事业单位负债liabilities for non-profit organizations事业单位固定基金fixed funds non-profit organizations事业单位固定资产fixed assets for non-profit organizations事业单位会计accounting for non-profit organizations事业单位会计准则accounting standards for non-profit rganizations事业单位基金general funds non-profit organizations事业单位结余surplus of non-profit gorganizaiton事业单位借入款项loans non-profit organization事业单位净资产net assets for non-profit organizations事业单位流动资产current assets for non-profit organizations事业单位收入revenue for non-profit organization事业单位应缴款项agent funds and tax paybale non-profit organization事业单位预算管理方式budget management methods for non-profit organyzation’s 事业单位支出expenditure of non-profit organization事业单位专用基金special funds non-profit organizations事业单位资产assets for non-profit organiz-ations试算表trial balance试算平衡trial balancing收付记账法receipts-payment bookkeeping收款法collection method收款凭证receipt voucher收入的确认recognition of revenue收入中心收益债券income bonds收益总括观点all-inclusive concept of income受托人trustee美售后回租sale-leaseback数量差异quantity variance税务会计tax accounting损益表法损益表账户income statement accounts所得税income tax所得税的跨期分摊interqeriod tax allocation所得税会计income tax accounting所有者权益owners equity所有者权益owners equity特定变动specific change特定履行法特定物价指数specific price index特许权使用管理费fees and royalties提前与延期支付Leads and Lags贴水discount贴现市场dixcount market铁路运输成本铁路运输企业会计accounting of rail way transportation enterprises 停工损失loss on work stoppage通用报表all-purpose financial statements通用记账凭证general purpose voucher通用日记账核算形式bookkeeping procedure using general journal 投机spculation投资收益investment income投资中心土地使用权推定赎回constructive retirement推定赎回损益constructive gains and losses on bonds退休基金资产pension plan assets美退休金pension plan退休金成本净额net periodic pension cost美退休金给付义务pension benefit obligations美退休金会计accounting for pension plan美外币foreign currency外币承诺foreign currency commitment外币持有风险foreingn currency holding risk外币兑换风险foreign currency exchange risk外币分账法original-currency method外币负债风险foreign crurency liability risk外币会计报表foreign currency statements外币会计报表折算translation of foreign currency statements外币套期保值hedge外币统账法recording-currency method外币投资风险foreign curency investment risk外币业务foreign currency transaction外币折算风险foreign curency translation risk外币资产风险foreign currency assets risk外汇foreign exchange外汇期货交易foreign exchange frtrues transaction外汇市场foreign exchange market外来原始凭证source document from outside外商投资企业会计accounting of enterprises with foreign investment 完全合并full consolidation完全应计法full accrual method微观会计micro-accounting未分配利润无偿债能力insolvency无担保债券debenture bonds无限责任公司company of unlimited liability无形资产intangible assets物价变动price changes物价变动会计accounting for price changes物价指数price index物价总指数general price index吸收合并merger下推会计push-down accounting美先调整后折算法remeasurement-translation method先进先出去first-in,first-out缩写FIFO先折算后调整法translation-remeasurement method闲置成本idle cost现代管理会计modern management accounting现代管理会计专门方法special methods of modern management accounting 现金cash现金分配计划cash distribution plan现金日记账cash journal现金折扣cash discount现行成本/稳值货币会计current cost/general purchasing power accountin 现行成本crurent cost现行成本会计current cost accounting相对账户调节reconciliation of home office and branch accounts相关成本与非相关成本relevant cost and irrelevant cost相关性原则relevance相互持股mutual holdings向上销售upstream sale向下销售downstream sale消费税consumer tax销货退回与折让sales returns and allowances销售成本cost of goods sold销售代理处sales agency销售法sale method销售费用selling expenses销售式融资租赁sales-type financing lease新合伙人入伙admission of a new parther信息系统论information system perspective行政单位拨入经费appropriated funds of governmental units行政单位财务规则financial rules of governmental units行政单位负债liabilities of governmental units行政单位固定基金fixed funds of governmental units行政单位会计accounting of governmental units行政单位会计报表分析analysis of accounting行政单位会计制度accounting regulations of governmental units行政单位结余surplus of governmental units行政单位经费支出fund expenditures of governmental units行政单位净资产net assets of governmental units行政单位年终清理和结转yearend checking and closing of governmental units行政单位收入revenues of governbmental units行政单位预算管理办法budget management method of governmental units行政单位暂存款deposite payable of governmental units行政单位暂付款prepayments of governmental units行政单位支出expenditures of governmental units行政单位资产assets of governmental units修正性惯例principlle of exceptions虚账户nominal accounts序时账簿book of chronological entry沿海运输成本衍生金融工具derivative financial instru-ments业主权论the proprietorship theory一般购买力保全maintaining capital in units of general purchasing power一般购买力单位units of general purchasing power一般物价水准会计general price level accounting一般预算收入general budget revenue一般预算支出general budget expenditure一笔交易观one-transaction opinion一次凭证single-record document一次总付清算lump-sum qartnership liquidation一级市场security primary market一致性原则consistency医院财务制度financial regulations for hospitals医院负债liabilities of hospitals医院会计hospital accounting医院会计报表accounting statements of hospitals医院会计报表分析analysis of accounting statements of hospitals医院会计科目chart of accounts for hospitals医院会计制度accounting regulations ror hospitals医院基金funds of hospitals医院结余surplus of hospitals医院收入revenues of hospitals医院预算管理办法hbdget management nethod of hospital医院支出expenditures of hospitals医院资产saaets of hospitals已耗成本与未耗成本expired cost and unex-pired cost以外币表示的应收款项或应付款项receivables ofr payables denominated in foreign currency艺术论art perspective因素分析法factor analysis approach银行存款cash in bank银行存款日记账deposit journal印花税stamp tax应付福利费应付工资wages payable应付股利dividends payable应付利润profit payable应付票据notes payable应付票据贴现discount on notes payable应付税款法taxes payable method应计费用accrued expense应交税金taxes payable应交折基金【旧】应收票据notes receivable应收账款accounts receivable应收账款出借assignment of accounts receivable应收账款出售sale or factoring of accounts receivable盈余公积surplus reserves营业亏损抵免operating loss carrybacks and carryforwards营业利润operating income营业税husiness tax营业外收支净额永久性差异permanent difference永续盘存制perpetual inventory system邮电通信企业会计accounting of post and telecommonication enterprises 有担保债券mortgage bonds有限责任公司company of limited liability预拨款项appropriation in advance预测价值forecast value预付账款advance to supplier预计成本predicted cost预收账款预算成本budgeted costs预算结余budget surplus预算举借债务public finance-debts预算外资金预算周转金public finance-budgetary revolving fund预提费用原合伙人退伙retirement of initial partner原始成本historical cost原始成本和重置成本original cost and replacement cost原始记录original record原始凭证source document远期汇率forward rate远洋运输成本约当产量比例法equivalent units method再开票中心reinvoicing center再生产成本cost of reproduction在产品成本work-in-process cost在产品计价work-in-process costing在发建工程constructions in process暂记账户suspense accounts暂时性差异temporary difference责任成本responsibility cost责任成本层次levels of responsibility cost增减记账法increase-decrease bookkeeping增量成本incremantal cost增值表value added statement债权结算账户accounts for settlement of claim债权人会议committee representation债权债务结算账户accounts for settlement of claim and debt债券赎回债务结算账户accounts for settlement of debt债务重整debt restructurings账户account账户编号Account number账户对应关系debit-credit relationship账面成本cost of book value账面汇率recorded rate账项调整adjustment of account招股说明书prospectus折旧[旧]折旧方法depreciation method折旧率depreciation rate真实与公允true and fair view证券交易所stock exchange证券市场securities market政府及非营利组织会计governmentai and non-profit organizationaccounting 政治风险political risk支出payment直接标价法direct quotation直接材料成本差异direct material variance直接成本与间接成本direct cost and indirect cost直接控股direct holdings直接人工成本差异direct labor variance直接人工成本差异direct labor variance直接融资租赁direct financing lease直线法straight-line职工福利基金【旧】制造费用manufactruing expenses制造费用差异manufacturing expenses variance制造费用分配manufacturing expenses allocation中国预算会计governmental and non-profit oragnization accounting in China 中华人民共和国预算法the budget law of the people’s Republic of China中间汇率middle rate中期报告interim reporting重要性原则materiality重置成本replacement cost重置成本法replacement costing主要产品单位成本分析主要成本与加工成本prime costs and processing costs住房基金housing fund专利权patents专项拨款【旧】专项物资[旧]专项资产【旧】专营权franchises专用报表special purpose financial statements专用基金结余surplus of special purpose funds专用基金收入proceeds from special purpose fund专用基金支出expenditure on special purpose fund专用记账凭证special-purpose voucher专有技术know-how转回分录reversing entry转账凭证transfer voucher转租赁subleases准改组quasi-reorbganization美酌量性费用中心资本保全capital maintenance资本公积capital reserves资本化价值capitalized value资本市场capital market资本因素capital factor资产assets资产负债表法资产负债法asset/libility method资产负债账户balance sheet accounts资金funds资金调拨收入proceods from allocated and transferred fund 资金调拨支出expenditure on allocated and transeferred fund 资金来源账户accounts of sources of funds资金运动funds morement资金运用账户accounts of applications of funds资金占用和资金来源[旧]资源税resources tax子公司subsidiary company子公司权益变动change in ownership of a subsidiary自然资源natural resources自制原始凭证internal source document综合变动general change综合费用分配composite expenses allocation总分类账簿general ledger总分类账户general account纵向合并Vertical integration租金rents租赁leases最低退休金负债minimum liability美。

accap2知识点总结

accap2知识点总结In this article, we will provide a comprehensive summary of the key concepts covered in the ACCA P2 Management Accounting course. We will discuss the importance of management accounting, the different techniques and tools used in management accounting, and how these techniques can be applied in real-life business situations.Importance of Management AccountingManagement accounting plays a critical role in helping organizations make informed business decisions. It involves the use of financial and non-financial information to help managers plan, control, and make decisions to achieve organizational objectives. Management accounting also helps in the monitoring and evaluation of business performance, and in the formulation of strategies for financial planning, control and decision making.The key areas covered in the ACCA P2 Management Accounting course include:1. Cost and Management AccountingCost and management accounting involves the identification, measurement, and analysis of costs to help in control and decision making. This includes classifying costs by behavior, function, and nature, the use of cost allocation methods, and understanding cost-volume-profit relationships.Students will also learn about different costing methods such as job costing, process costing, and activity-based costing. They will also learn how to analyze and interpret cost data to make relevant business decisions.2. BudgetingBudgeting is an essential management accounting tool that involves planning and controlling an organization's financial resources. Students will learn how to prepare different types of budgets such as sales, production, cash, and master budgets. They will also learn about the benefits of budgeting, the budgetary control process, and how to use variance analysis to evaluate the performance of different business activities.3. Capital Investment DecisionsCapital investment decisions involve the evaluation and selection of long-term investment proposals. Students will learn about different capital investment appraisal techniques such as payback period, accounting rate of return, net present value, and internal rate of return. They will also learn how to apply these techniques in different investment scenarios to evaluate the profitability and viability of investment projects.4. Performance ManagementPerformance management involves the use of performance measures and management control systems to assess and improve the performance of individuals, departments, and organizations. Students will learn about different performance measurement frameworks, key performance indicators, and how to design and implement performance management systems to align organizational goals with individual and departmental objectives.Real-Life Application of Management Accounting TechniquesThe concepts and techniques covered in the ACCA P2 Management Accounting course are applicable in various business scenarios. For example, cost and management accounting techniques are used to establish product costs, assess pricing decisions, and improve cost control. Budgeting techniques are used to set targets, allocate resources, and evaluate business performance. Capital investment appraisal techniques are used to evaluate potential investment opportunities and make informed investment decisions. Performance management techniques are used to measure and evaluate employee and organizational performance, as well as to improve accountability and control.ConclusionIn conclusion, the ACCA P2 Management Accounting course covers a wide range of management accounting techniques that are essential for anyone aspiring to pursue a career in management accounting, finance, or business. The course provides students with a solid foundation in understanding the key concepts, tools, and techniques used in management accounting, and how these techniques can be applied in real-life business situations. By mastering these concepts, students will be equipped with the knowledge and skills necessary to add value to the organizations they work for, by helping them make informed and strategic business decisions.。

财务会计管理案例分析(英文版)

Standard quantity is the quantity allowed for the actual good output.

A General Model for Variance Analysis

Actual Quantity ×

Actual Price

Actual Quantity ×

MPV = $170 Favorable

Zippy

Material Variances

The standard quantity of material that should have been used to produce 1,000 Zippies is: a. 1,700 pounds. b. 1,500 pounds. c. 2,550 pounds. d. 2,000 pounds.

Total standard unit cost

3.0 lbs. 2.5 hours 2.5 hours

$ 4.00 per lb. $ 14.00 per hour 3.00 per hour $

12.00 35.00

7.50 54.50

Standards vs. Budgets

Are standards the same as budgets?

Amount

Direct Labor

Direct Material

Standard

Manufacturing Overhead

Type of Product Cost

Setting Standard Costs

Accountants, engineers, personnel administrators, and production managers combine efforts to set standards based on

财务报表分析双语

– Management choice of accounting methods; – Accounting principles differ in different country.

– Regulates secondary market and national exchanges

– SEC was created by this Act

• SEC has the authority to determine GAAP • Regulation S-X describes disclosure requirements

Chapter 1, Slide #6

第六页,共58页。

• Financial statements don’t fully reflect firm’s true economic position because:

– Accounting recognition and measurement don’t correspond with economic events;

Chaapptteerr11,,SSlildidee##1155

第十五页,共58页。

GAAP

• Generally Accepted Accounting Principles (GAAP) in United States

• Major Sources of GAAP

– Securities and Exchange Commission (SEC) – American Institute of Certified Public Accountants

财务报表分析(英文版)答案

Chapter 8Return On Invested Capital And Profitability AnalysisReturn on invested capital is important in our analysis of financial statements. Financial statement analysis involves our assessing both risk and return. The prior three chapters focused primarily on risk, whereas this chapter extends our analysis to return. Return on invested capital refers to a company's earnings relative to both the level and source of financing. It is a measure of a company's success in using financing to generate profits, and is an excellent measure of operating performance. This chapter describes return on invested capital and its relevance to financial statement analysis. We also explain variations in measurement of return on invested capital and their interpretation. We also disaggregate return on invested capital into important components for additional insights into company performance. The role of financial leverage and its importance for returns analysis is examined. This chapter demonstrates each of these analysis techniques using financial statement data.•Importance of Return on Invested CapitalMeasuring Managerial EffectivenessMeasuring ProfitabilityMeasuring for Planning and Control •Components of Return on Invested CapitalDefining Invested CapitalAdjustments to Invested Capital and IncomeComputing Return on Invested Capital•Analyzing Return on Net Operating AssetsDisaggregating Return on Net Operating AssetsRelation between Profit Margin and Asset TurnoverProfit Margin AnalysisAsset Turnover Analysis•Analyzing Return on Common EquityDisaggregating Return on Common EquityFinancial Leverage and Return on Common EquityAssessing Growth in Common Equity•Describe the usefulness of return measures in financial statement analysis. •Explain return on invested capital and variations in its computation.•Analyze return on net operating assets and its relevance in our analysis. •Describe disaggregation of return on net operating assets and the importance of its components.•Describe the relation between profit margin and turnover.•Analyze return on common shareholders' equity and its role in our analysis. •Describe disaggregation of return on common shareholders' equity and the relevance of its components.•Explain financial leverage and how to assess a company's success in trading on the equity across financing sources.1. The return that is achieved in any one period on the invested capital of a companyconsists of the returns (and losses) realized by its various segments and divisions. In turn, these returns are made up of the results achieved by individual product lines and projects. A well-managed company exercises rigorous control over the returns achieved by each of its profit centers, and it rewards the managers on the basis of such results. Specifically, when evaluating new investments in assets or projects, management will compute the estimated returns it expects to achieve and use these estimates as a basis for its decision to invest or not.2. Profit generation is the first and foremost purpose of a company. The effectiveness ofoperating performance determines the ability of the company to survive financially, to attract suppliers of funds, and to reward them adequately. Return on invested capital is the prime measure of company performance. The analyst uses it as an indicator of managerial effectiveness, and/or a measure of the company's ability to earn a satisfactory return on investment.3. If the investment base is defined as comprising net operating assets, then netoperating profit (e.g., before interest) after tax (NOPAT) is the relevant income figure to use. The exclusion of interest from income deductions is due to its being regarded asa payment for the use of money from the suppliers of debt capital (in the same waythat dividends are regarded as a payment to suppliers of equity capital). NOPAT is the appropriate amount to measure against net operating assets as both are considered to be operating.4. First, the motivation for excluding nonproductive assets from invested capital isbased on the idea that management is not responsible for earning a return on non-operating invested capital. Second, the exclusion of intangible assets from the investment base is often due to skepticism regarding their value or their contribution to the earning power of the company. Under GAAP, intangibles are carried at cost.However, if their cost exceeds their future utility, they are written down (or there will be an uncertainty exception regarding their carrying value in the auditor's opinion).The exclusion of intangible assets from the asset base must be based on more substantial evidence than a mere lack of understanding of what these assets represent or an unsupported suspicion regarding their value. This implies that intangible assets should generally not be excluded from invested capital.5. The basic formula for computing the return on investment is net income divided bytotal invested capital. Whenever we modify the definition of the investment base by, say, omitting certain items (liabilities, idle assets, intangibles, etc.) we must also adjust the corresponding income figure to make it consistent with the modified asset base.6. The relation of net income to sales is a measure of operating performance (profitmargin). The relation of sales to total assets is a measure of asset utilization or turnover—a means of determining how effectively (in terms of sales generation) the assets are utilized. Both of these measures, profit margin as well as asset utilization,determine the return realized on a given investment base. Sales are an important factor in both of these performance measures.7. Profit margin, although important, is only one aspect of the return on invested capital.The other is asset turnover. Consequently, while Company B's profit margin is high, its asset turnover may have been sufficiently depressed so as to drag down the overall return on invested capital, leading to the shareholder's complaint.8. The asset turnover of Company X is 3. The profit margin of Company Y is 0.5%. Sinceboth companies are in the same industry, it is clear that Company X must concentrate on improving its asset turnover. On the other hand, Company Y must concentrate on improving its profit margin. More specific strategies depend on the product and industry.9. The sales to total assets (asset turnover) component of the return on invested capitalmeasure reflects the overall rate of asset utilization. It does not reflect the rate of utilization of individual asset categories that enter into the overall asset turnover. To better evaluate the reasons for the level of asset turnover or the reasons for changes in that level, it is helpful to compute the rate of individual asset turnovers that make up the overall turnover rate.10. The evaluation of return on invested capital involves many factors. Theinclusion/exclusion of extraordinary gains and losses, the use/nonuse of trends, the effect of acquisitions accounted for as poolings and their chance of recurrence, the effect of discontinued operations, and the possibility of averaging net income are justa few of many such factors. Moreover, the analyst must take into account the effectsof price-level changes on return calculations. It also is important that the analyst bear in mind that return on invested capital is most commonly based on book values from financial statements rather than on market values. And finally, many assets either do not appear in the financial statements or are significantly understated. Examples of such assets are intangibles such as patents, trademarks, research and development activities, advertising and training, and intellectual capital.11. The equity growth rate is calculated as follows:[Net income – Preferred dividends – Common dividend payout] / Average common equity.This is the growth rate due to the retention of earnings and assumes a constant dividend payout over time. It indicates the possibilities of earnings growth without resort to external financing. The resulting increase in equity can be expected to earn the rate of return that the company earns on its assets and, thus, further contribute to growth in earnings.12. a. The return on net operating assets and the return on common stockholders' equitydiffer by the capital investment base (and its corresponding effects on net income).RNOA reflects the return on the net operating assets of the company whereas ROCE reflects the perspective of common shareholders.b. ROCE can be disaggregated into the following components to facilitate analysis:ROCE = RNOA + Leverage x Spread. RNOA measures the return on net operating assets, a measure of operating performance. The second component (Leverage x Spread) measures the effects of financial leverage. ROCE is increased by adding financial leverage so long as RNOA>weighted average cost of capital. That is, if the firm can earn a return on operating assets that is greater than the cost of the capital used to finance the purchase of those assets, then shareholders are better off adding debt to increase operating assets.13. a. ROCE can be disaggregated as follows:equitycommon Av erage Sales Sales div idends Preferred - income Net ⨯ This shows that “equity turnover” (sales to average common equity) is one of the two components of the return on common shareholders' equity. Assuming a stable profit margin, the equity turnover can be used to determine the level and trend of ROCE. Specifically, an increase in equity turnover will produce an increase in ROCE if the profit margin is stable or declines less than the increase in equity turnover. For example, a common objective of discount stores is to lower prices by lowering profit margins, but to offset this by increasing equity turnover by more than the decrease in profit margin.b. Equity turnover can be rewritten as follows:equitycommon Av erage assets operating Net assets operating Net Sales ⨯ The first factor reflects how well net operating assets are being utilized. If the ratio is increasing, this can signal either a technological advantage or under-capacity and the need for expansion. The second factor reflects the use of leverage. Leverage will be higher for those firms that have financed more of their assets through debt. By considering these factors that comprise equity turnover, it is apparent that EPS cannot grow indefinitely from an increase in these factors. This is because these factors cannot grow indefinitely. Even if there is a technological advantage in production, the sales to net operating assets ratio cannot increase indefinitely. This is because sooner or later the firm must expand its net operating asset base to meet rising sales or else not meet sales and lose a share of the market. Also, financing new assets with debt can increase the net operating assets to common equity ratio. However, this can only be pursued to a point —at which time the equity base must expand (which decreases the ratio).14. When convertible debt sells at a substantial premium above par and is clearly held byinvestors for its conversion feature, there is justification for treating it as the equivalent of equity capital. This is particularly true when the company can choose at any time to force conversion of the debt by calling it in.Exercise 8-1 (35 minutes)a. First alternative:NOPAT = $6,000,000 * 10% = $600,000Net income = $600,000 – [$1,000,000*12%](1-.40) = $528,000Second alternative:NOPAT = $6,000,000 * 10% = $600,000Net income = $600,000 – [$2,000,000*12%](1-.40) = $456,000b. First alternative:ROCE = $528,000 / $5,000,000 = 10.56%Second alternative:ROCE = $456,000 / $4,000,000 = 11.40%c. First alternative:Assets-to-Equity = $6,000,000 / $5,000,000 = 1.2Second alternative:Assets-to-Equity = $6,000,000 / $4,000,000 = 1.5d. First, let’s compute return on assets (R NOA):First alternative: $600,000 / $6,000,000 = 10%Second alternative: $600,000 / $6,000,000 = 10%Second, notice that the interest rate is 12% on the debt (bonds). More importantly, the after-tax interest rate is 7.2% (12% x (1-0.40)), which is less than RNOA. Hence, the company earns more on its assets than it pays for debt on an after-tax basis. That is, it can successfully trade on the equity—use bondholders’ funds to earn additional profits.Finally, since the second alternative uses more debt, as reflected in the assets-to-equity ratio in c, the second alternative is probably preferred. The shareholders would take on additional risk with the second alternative, but the expected returns are greater as evidenced from computations in b.Exercise 8-2 (40 minutes)a. NOPAT = Net income = $10,000,000 x 10% = $1,000,000b. First alternative:NOPAT = $1,000,000 + $6,000,000*10% = $1,600,000Net income = $1,600,000 – ($2,000,000 ⨯ 5% x [1-.40]) = $1,540,000Second alternative:NOPAT = $1,000,000 + $6,000,000*10% = $1,600,000Net income = $1,600,000 – ($6,000,000 ⨯ 6% x [1-.40]) = $1,384,000c. First alternative: ROCE = $1,540,000 / ($10,000,000 + $4,000,000) = 11%Second alternative: ROCE = $1,384,000 / ($10,000,000 + $0) = 13.84%d. ROCE is higher under the second alternative due to successful use ofleverage—that is, successfully trading on the equity. [Note: Asset-to-Equity is1.14=$16 mil./$14 mil. (1.60=$16 mil./$10 mil.) under the first (second)alternative.] The company should pursue the second alternative in the interest of shareholders (assuming projected returns are consistent with current performance levels).a. RNOA = 2 x 5% = 10%b. ROCE = 10% + 1.786 x 4.4% = 17.86%c. RNOA 10.00%Leverage advantage 7.86%Return on equity 17.86%Exercise 8-4 (30 minutes)a. Computation and Interpretation of ROCE:Year 5 Year 9Pre-tax profit margin .......................................................... 0.112 0.109 Asset turnover .................................................................... 0.46 0.44 Assets-to-equity ................................................................. 3.25 3.40 After-tax income retention * .............................................. 0.570 0.556 ROCE (product of above) .................................................. 9.54% 9.07% * 1-Tax rate.ROCE declines from Year 5 to Year 9 because: (1) pre-tax margin decreases by approximately 3%, (2) asset turnover declines by roughly 4.3%, and (3) the tax rate increases by about 3.8%. The combination of these factors drives the decline in ROCE—this is despite the slight improvement in the assets-to-equity ratio.b. The main reason EPS increases is that shareholders had a large amount ofassets and equity working for them. Namely, the company grew while return on assets and return on equity remained fairly stable. In addition, the amount of preferred stock declined, as did the amount of preferred dividends. With this decline in the cost of carrying preferred stock, earnings available to common stock increased.(CFA Adapted)a. RNOA = 3 x 7% = 21%b. ROCE = RNOA + LEV x Spread = 21% + (1.667 x 8.4%) = 35%c. Net leverage advantage to common equityReturn on net operating assets .................................. 21%Leverage advantage .................................................... 14%Return on common equity (rounding difference) ..... 35%Exercise 8-6 (30 minutes)a. At the present level of debt, ROCE = $157,500 / $1,125,000 = 14%.In the absence of leverage, the noncurrent liabilities would be substituted with equity. Accordingly, there would be no interest expense with all-equityROCE without leverage = $184,500 / $1,800,000 = 10.25%.14% with leverage but only 10.25% without leverage.b. NOPAT = $157,500 + [$675,000 x 8% x (1-.50)] = $184,500RNOA = $184,500 / ($2,000,000-$200,000) = 10.25%c. The company is utilizing borrowed funds in its capital structure. Since theROCE is greater than RNOA, the use of financial leverage is beneficial to stockholders. Specifically, the after cost of debt is 4% and the financial leverage (NFO/Equity) is $675,000 / $1,125,000 = 60%. Therefore,ROCE = RNOA + LEV x Spread = 10.25% + 0.60 x (10.25% - 4%) = 14%, as before. The favorable effect of financial leverage is given by the term [0.60 x (10.25% - 4%)] = 3.75%.1. c2. a3. cExercise 8-8 (20 minutes)(Assessments of profit margin and asset turnover are relative to industry norms.)a. Higher profit margin and lower asset turnover.b. Higher asset turnover and lower profit margin.c. Higher profit margin and similar/lower asset turnover.d. Higher asset turnover and similar/lower profit margin.e. Higher asset turnover and lower/similar profit margin.f. Higher asset turnover and similar/higher profit margin.g. Higher asset turnover and lower profit margin.Exercise 8-9 (20 minutes)The memorandum to Reliable Auto Sales President would include the following points:•Both Reliable and Legend Auto Sales are perpetually investing $100,000 in automobile inventory.•Legend Auto Sales is able to generate more profit than Reliable because it is turning over its inventory (10 cars) more often. Specifically, Legend is turning its inventory over 10 times per year while Reliable is turning its inventory over only 5 times per year. Hence, given the same investment in automobile inventory, Legend is twice as profitable as Reliable.•Encourage Reliable to sacrifice some return on each sale to increase the inventory turnover. By slightly reducing price, relative to that charged by Legend, Reliable predictably will find that overall profitability increases. This is because while profit per sale declines, the number of units sold and, therefore, inventory turnover will increase. These factors predictably yield increased return on assets.Computation of Asset (PP&E) Turnover [computed as Sales / PP&E (net)]: Northern: $12,000 / $20,000 = 0.60Southern: $6,000 / $20,000 = 0.30This implies that Northern generates $0.60 in sales per year for each $1 investment in PP&E. In contrast, Southern generates $0.30 in sales per year for each $1 investment in PP&E. This shows that Northern is able to generate twice the return for each $1 invested in PP&E. Assuming equal profit margins, Northern will report a higher return on assets because of the volume of sales that the company is able to generate with its investment in PP&E (at least in the short run).Exercise 8-11 (15 minutes)Low volume operations mean that fixed costs, which in the case of automakers are substantial, must be absorbed by a low number of units produced. Since the lower of cost or market rule implies that inventory cannot be priced higher than expected sales price less costs of disposal plus a normal profit margin, much of that excess cost must be charged to the period incurred. In this case, that means the fourth quarter financial statements absorb much of this cost. This is probably the most likely accounting-based reason for the fourth quarter losses described in the news release.Problem 8-1 (30 minutes)a. 1. Quaker Oats does not reveal its computation of this return. Accordingly, wemake some simple computations and assumptions: (i) For simplicity, focus on one share, (ii) The dividend is $1.56 for Year 11, (iii) The average stock price is $55 and the price increase for Year 11 is $14—based on the beginning price of $48 and the ending price of $62. Using this information, we compute return to a share of stock as follows:= [Dividend per share + Price increase per share] / Average price per share = [$1.56 + $14] / $55= 28.3%However, if we use the beginning price of $48 per share, we get closer to the company's 34% return:= [$1.56 + $14] / $48= 32.4%2. The return on common equity is based on the relation between net incomeand the book value of the equity capital. In contrast, Quaker Oats’ “return t o shareholders” uses dividends plus market value change in relation to the market price per share (cost of investment to shareholders.)b. The company must have derived the 3.6% from price, market, and otherfactors that are not disclosed. Conceptually, this 3.6% should reflect the added risk of an investment in Quaker Oats’ stock vis-à-vis a risk-free security such as a U.S. Treasury bond.c. Quaker does not reveal its computations. It may disclose a variety of interestrates on long-term debt that it carries in the notes to financial statements.Based on data available to it, but not to the financial statement reader, it probably computed a weighted-average interest rate from which it deducted the tax benefit in arriving at the 6.4% cost of debt.a. Computation of Return on Invested Capital Measures:As a first step, we construct the company’s income statement.Sales (500,000 units @ $10). ................................................ $5,000,000 Fixed costs ....................................................................... 1,500,000 Variable costs (500,000 units @ $4). ............................. 2,000,000 Labor costs (20 employees x $35,000). ......................... 700,000 Income before taxes .......................................................... 800,000 Taxes (50% rate) ................................................................. 400,000 Net income .......................................................................... $ 400,000(1) RNOA = [$400,000 + ($2,000,000 x 7.5%)(1-0.50)] / ($8,000,000-$2,00,000)= $475,000 / $6,000,000 = 7.92%(2) ROCE = [$400,000 - ($1,000,000 x 6%)] / $3,000,000 = 11.33%Fixed costs ($1,500,000 x 1.06) ......................................................... 1,590,000 Variable costs ($550,000 units @ $4) .............................................. 2,200,000 Income before labor costs and taxes ............................................. $1,710,000 To obtain a 10% return on long-term debt and equity capital, Zear will need a numerator of $600,000 given an invested capital base of $6,000,000. The required operating income to yield this $600,000 amount is computed as: Net income + Interest expense x (1 - 0.50) = $600,000Net income + ($2,000,000 x 7.5%) x (1-0.50) = $600,000Net income = $525,000Assuming taxes at a 50% rate, Zear needs pre-tax income of $1,050,000, computed as:Income before labor and taxes ............ $1,710,000Labor costs ........................................... ?Pre-tax income ...................................... $1,050,000This implies:Labor costs = $660,000 orAverage wage per worker = $660,000 / 22 employees = $30,000 per employee Since the current salary level is $35,000, Zear cannot achieve its target return level and give a salary raise to its employees.(CFA Adapted)a. ROCE = $1,650 / $3,860 = 42.7%b. NOPAT = ($2,550 + $10) x (1-0.35) = $1,664NOA = $7,250-$3,290 = $3,960RNOA (using year-end NOA balance) = $1,664 / $3,960 = 42%The effect of financial leverage, thus, is only 0.7% as NFO/NFE are insignificant. Most of Merck’s ROCE in this year is derived from operating results.Pre-tax income to sales 0.36Net income to sales 0.23Sales/current assets 1.47Sales / fixed assets 2.97Sales / total assets 0.98Total liabilities / equity 0.88L-T liabilities / equity 0.03a. 1. RNOA = NOPATAvg. NOANOPAT = [$186,000 + $2,000 - $120,000 - $37,000 + $1,000] x 50% = $16,000 Note: we include income from equity investments under the assumptions that these are operating rather than financial investments. We also include the cumulative effect as operating in the absence of information to the contrary. Minority interest and discontinued operations are nonoperating (minority interest is therefore, treated as equity in the ROCE computation).NOA Year 6 = $138,000 - $29,000 - $7000 - $3,600 = $98,400 NOA Year 5 = $105,000 - $23,000 - $2,000 - $2,000 = $78,000RNOA = $16,000 / ([$98,400 + $78,000]/2) = 18.14%2. ROCE = Net income - Preferred dividendsAverage common equityROCE = ($10,000 –$0) /[($55,400* + $47,800*)/2] = 19.38% *Note: minority interest is treated as equity. If Minority interest is ignored, the ROCE is 19.8%b. NFO = NOA - EquityYear 6: $43,000; Year 5: $30,200LEV = Avg. NFO / Ave Equity = ([$43,000 + $30,200] / 2) / ([$55,400* + $47,800*] /2)= 0.71NFE = NOPAT – Net incomeYear 6: $6,000NFR = NFE / Avg. NFO = $6,000 / ([$43,000 + $30,200] / 2) = 16.4%Spread = RNOA – NFR = 18.14% - 16.4% = 1.74%ROCE = RNOA + LEV x Spread = 18.14 + 0.71 x 1.74% = 19.38%94% (18.14%/19.38%) of Zeta’s ROCE is derived for m operating activities. The company is effectively using leverage, however, as indicated by the positive spread, but the leverage does not contribute significantly to Zeta’s return on equity and may not be worth the added risk.a. ROCE = [Net income –preferred dividends] / stockholders’ equity**end of year in this problemROCE Year 5: [$14 – $0] / $125 = 11.2%ROCE Year 9: [$34 - $0] / $220 = 15.5%RNOA Year 5 = ($35 x 0.50) / ($52 + $123) = 10.0%RNOA Year 9 = ($68 x 0.50) / ($63 + $157) = 15.5%ROCE = RNOA + Leverage x SpreadYear 5: 10.0% + 1.2% = 11.2%Year 9: 15.5% + 0 = 15.5%b. Texas Talcom’s ROCE has increased form years 5 to 9. The source is thisincrease, however, has been an increase in RNOA as the leverage effect is zero in Year 9 since its long-term debt has been retired. Given the RNOA increase, additional leverage might be explored as a way to increase shareholder returns.Selling price per unit ...................... $6.00 $5.00 $50.00 $50.00 Unit cost ........................................... $5.00 $4.00 $32.50 $30.00Analysis of Variation in Product A SalesIncreased quantity at Yr 6 prices (3,000 x $5) ........................ $ 15,000 Price increase at Yr 6 quantity (7,000 x $1) ........................... 7,000 Quantity increase x price increase (3,000 x $1) .................... 3,000 Analysis of Variation in Product A Cost of SalesIncreased quantity at Yr 6 cost (3,000 x $4) ........................... (12,000) Increased cost at Yr 6 quantity (7,000 x $1) ........................... (7,000) Cost increase x quantity increase (3,000 x $1) ...................... (3,000) Net Variation (Increase) in Gross Margin for Product A ............. $ 3,000Analysis of Variation in Product B SalesDecreased quantity at Yr 6 prices (300 x $50) ....................... $ (15,000) Analysis of Variation in Product B Cost of Sales:Decreased quantity at Yr 6 cost (300 x $30) .......................... 9,000 Increased cost at Yr 6 quantity (900 x $2.50) ......................... (2,250) Cost increase x quantity decrease (300 x $2.50) . (750)Net Variation (Decrease) in Gross Margin for Product B ............ $ (7,500)Summary of Net Variation in Margins for Products A and BNet increase from product A ......................................................... $ 3,000 Net decrease from product B ........................................................ (7,500) Net Decrease in Gross Margin ...................................................... $ (4,500)a.SPYRES MANUFACTURING COMPANYComparative Common-Size Income StatementsYear Ended December 31 IncreaseYear 9 Year 8(Decrease)Net sales ............................. 100.0% 100.0% 20.0% Cost of goods sold ............ 81.7 86.0 14.0 Gross margin on sales ...... 18.3 14.0 57.1 Operating expenses .......... 16.8 10.2 98.0 Income before taxes .......... 1.5 3.8 (52.6) Income taxes ...................... 0.4 1.0 (52.0) Net income ......................... 1.1 2.8 (52.9)b. Performance in Year 9 is poor when compared with Year 8. One bright spot isthe percentage of Cost of Goods Sold to Sales, which decreased in Year 9.However, Operating Expenses climbed sharply. This sharp climb in operating expenses is unexpected since there is usually a larger fixed cost component comprising these costs compared with that for Cost of Goods Sold.Management should further check operating expenses. If operating expenses had remained at the Year 8 level of 10.2%, income would have been up favorably for Year 9. Operating expenses may have included a future-directed component such as advertising or training costs. Also, management would want to follow up on the change in gross margin. The sharp improvement in gross margin may have been due to factors such as the liquidation LIFO inventory layers or, alternatively, to something more fundamental with the activities of the firm.。

英语会计考试题目及答案