ACCA P3 考试: Benchmarking

英国ACCA名师总结的ACCA考试法宝

英国ACCA名师总结的ACCA考试法宝Examining Process以下人等是整个examining process的关键人物:- Examiners 总共有16个core examiners 和44个variantexaminers,他们是写卷子的人,薪水非常高- Assessorsexaminers的后备人选,负责评估试卷,同时也会参与评分,这些人一般会觊觎examiners的位子- Education Advisers 第三方,一般是大学教授- Sitters 第三方,负责在学员考试前试考- Subject Coordinators第三方,在examiners和assessors之前协调- Markers这些人负责在家里评分,据说以后实现机考的话,ACCA会考虑让会员申请成为Marking,赚点钱,这个我有兴趣,英镑耶!前五拨人都是在考前可以看到试卷的,其中examiners最重要。

作为ACCA讲师必须熟读examiner's reportsand articles written byexaminers,同时必须熟悉每一个examiner的风格,并随时跟进examiners的轮换。

比如,P3的examinerSteve 自家开了个咨询公司,因此非常喜欢project management 和IT 类话题,翻来覆去地考;F5的examiner对于答卷的neatness 要求非常严格;P5的examiner马上就换了(这话是去年年初说的),所以也就没必要研究他的风格啦,当然,现在来了新人,赶紧好好观察一下。

英国人一般一份工作会做很久,所以对于讲师和某些爱钻牛角尖的学员来说,投入些精力去熟悉examiners的风格还是值得的。

Timeline以下是准备一份试卷的流程和时间表,以2010年6月份的考试为例。

- 2009年3月份,初稿完成;- 2009年夏天,通过Exam Panel,即以上前五拨人审核、试考、等等;-2009年12月,终稿,并成为2009年12月考试的备份试题(万一某地出现意外情况当期的试题无法使用,即用这份顶上);- 2010年6月,正式使用。

2012年12月ACCA考试P3考试考官报告

2012年12月ACCA考试P3考试考官报告本文由高顿ACCA整理发布,转载请注明出处General CommentsThe Business Analysis examination is in two sections. The first section contains one mandatory question, worth 50 marks, based around an extended case study. The second section contains three questions, each worth 25 marks. The candidate is required to answer two questions from this section. Performance in this examination was disappointing. This was despite good answers to the mandatory question one, where many candidates achieved high marks. However, there was even evidence in this question of candidates not being familiar with certain parts of the syllabus. A significant number of candidates did not answer the part of this question concerned with benchmarking. In the optional questions, there was considerable evidence of candidates being unfamiliar with parts of the syllabus. Question four, on decision trees, risk and software package evaluation was not answered by many candidates. However, even within their selected questions (questions two and three) it was clear that many candidates were unfamiliar with the principles of strategic alliances and (in particular) the sources of internal finance. This lack of knowledge meant that many candidates scored poorly in their selected optional questions. Many candidates also spent too much time on question one part a, producing an answer that was far too long for the marks on offer. This meant that these candidates had less time to answer the optional questions. Time management is a common problem on this paper, and, judging by comments on various forums, is one that most candidates are aware of. The need for appropriate planning and time management in this examination can only be re-iterated.Overall, candidates are encouraged to write answers that are precise and focussed. Obviously, the size of handwriting does vary, but in general most successful scripts were 12 – 15 sides long. They were easily contained in one examination booklet. Too many long scripts appear to be streams of consciousness with too much repetition, verbatim copying of facts and figures given in the scenario and text about models and frameworks that needed to be applied and not described.Specific CommentsQuestion OneThe scenario for this question described four companies in the EA Group. The first part of the question asked candidates to analyse the performance of each of the four companies described in the scenario and to assess each company’s potential contribution to the EA Group portfolio of businesses. The key word here was portfolio. Most candidates recognisedthat this question was concerned with portfolio analysis and so used appropriate analysis models. The provision of market share and market growth data made the use of the BCG matrix (Boston Box) particularly appropriate. Some candidates did use alternative models (SWOT in particular) and still scored relatively well. However, there was insufficient data to undertake a SWOT analysis for each of the four firms in the scenario. Many candidates scored very well in this part question. Indeed, in some respects, some answers were too comprehensive, with candidates making more points than the marks on offer. Sometimes this led to time problems later on in the paper. A few candidates scored very heavily on this part question (over 20 marks) and yet still failed the examination overall, probably due to poor time management caused by spending too much time on this part question. In contrast, the second part of question one was poorly answered. This asked candidates to evaluate the potential influence of time, scope, capability and readiness for change at Steeltown Information Technology on any strategic change proposed by the EA Group. Too many answers did not concern themselves with strategic change but instead focused on changes in the type of systems developed at Steeltown and the fact that there was a backlog of applications and that user departments found it difficult to specify system requirements in advance. Furthermore, too few candidates commented on the competencies that the EA Group would bring to the problem, concluding that Steeltown would not have the ability to implement strategic change itself. This is probably true, but the scenario makes it clear that responsibility for strategic change lies with the EA Group. ‘They (the EA Group) want to explore these (contextual) factors before they firm up their proposed strategy for the newly acquired company’ (my italics). The final part of the first question concerned benchmarking. It was clear that many candidates had read the relatively recent Student Accountant article on this and so scored relatively well. It also appeared that some candidates were not prepared for this subject at all and omitted it completely.Overall, this part question was fairly well answered (5 or 6 marks out of ten was typical) by those who answered it.Question TwoThe scenario for question two concerned a large estate that was facing internal and external problems. A large part of the scenario consisted of quotes from a recent stakeholder survey. The first part of this question (worth 15 marks) asked candidates to evaluate the strategic position of the estate with specific reference to The expectations of stakeholders (both internal and external) The external environment of the estate Strategic capabilities of the estate itself (internal strengths) Candidates tended to produce unstructured answers to this part question, due to one, or more, of the following reasons. Too much use of the Mendelow power/interest grid; leading to a consideration of stakeholder management, rather than the conflict caused by the different stakeholderperspectives and expectations.Overusing PESTLE, in a case study scenario where there was very little on, for example; technology, economy and environment. Technology was usually considered in the perspective of the website, which of course is an internal resource. Indeed it is an internal weakness. Attempting a SWOT analysis for which there was just insufficient information. This led to the consideration of weaknesses, which again resulted in an inappropriate in-depth analysis of the defects of the web site.Overall, this part question was not well answered, and despite some very lengthy answers, relatively few candidates gained a pass mark on this part question. The second part of the question asked candidates to discuss how the estate’s website could be further developed to address some of the issues highlighted in the stakeholder survey. This should have been relatively straightforward, and indeed many candidates did score well in this part question, cross-referencing their points to the comments made in the stakeholder survey. However, other candidates focused too much on the 6is (interactivity etc…), introducing general points that they could not back up with a relevant example, because they were not appropriate in the context of the scenario.Overall, although question two was popular, it was not answered as well as it should have been.Question ThreeThis question concerned an industrial chemist who was looking for ways to take his company and ideas forward and exploit them before his patent expired. The first part of the question asked the candidate to evaluate the appropriateness of franchising, highlighting the advantages and disadvantages of this approach from the perspective of the chemist (the owner of Graffoff). This part question was relatively well answered, using a structure suggested by the question; description, advantages, disadvantages, evaluation. Some candidates did try to use the Johnson, Scholes, Whittington framework of suitability, acceptability and feasibility but this framework did not really suit the information given in the scenario. Some candidates were confused about franchising, restricting their discussion to a franchise just offered to one company; the Equipment Emporium. The second part of the question asked the candidate to evaluate how other forms of strategic alliance might be appropriate to strategic development at Graffoff. Many candidates were aware of joint ventures and licensing but really failed to suggest why these might be more appropriate or different to franchising. Candidates could have also made more of the potential link up with the Equipment Emporium. Some candidates suggested mergers, acquisitions and even selling the company. However, these are not strategic alliances.Finally, candidates were asked to evaluate a claim that Graffoff could completely fund its organic expansion at a cost of $500,000, through internally generated sources of finance. This part question was poorly answered on three counts: Many answers were too general (reduce creditor days) and included no calculation at all, so the consultant’s claim could notbe properly evaluated. Too many candidates turned the question into a general question on the advantages and disadvantages of organic growth. There were some good answers to a totally different question. In the context of this examination, most of these answers scored zero; Finally, too many answers focused on external finance (share issues, more loans) and this was specifically excluded from the question. Although question three was a popular question, many candidates scored poorly on parts b and c.Question FourThis question concerned a producer of aircraft and ship engines and the conduct and aftermath of a search for engine testing technology. The first part of the question asked candidates to conduct a decision tree from information given in the question scenario. It also required candidates to discuss the implications and shortcomings of decision trees. Although this was an unpopular question (see below), many candidates showed that they were very familiar with constructing and interpreting decision trees and so scored reasonably well on this part question. The most common error was to forget to subtract the cost of the investment. However, it also has to be said, that some answers were very poor and it was unclear why the candidate chose to answer this optional question.The second part of this question asked the candidate to discuss what other factors, not reflected in the decision tree analysis, should be also taken into consideration when choosing which option to select. Again, candidates who knew this topic well, produced good answers, centred on risk, supplier viability and software functionality. In contrast, some answers were very poor and rambling; not answering the specific question at all.Finally, candidates were asked to consider how two risks; supplier business failure and employee travel, might be avoided or mitigated. Again there were some very good answers. However, there were also some very poor answers, lacking in content or generally describing risk management without any context at all.Overall, this question was unpopular. Candidate performance tended to be good, with candidates confident in the application and limitations of decision tree analysis and able to properly discuss risk in context, or poor, with candidates unable to properly undertake decision tree analysis or discuss the concept of risk in the context of the scenario.更多ACCA资讯请关注高顿ACCA官网:。

ACCA P3知识要点汇总(上)

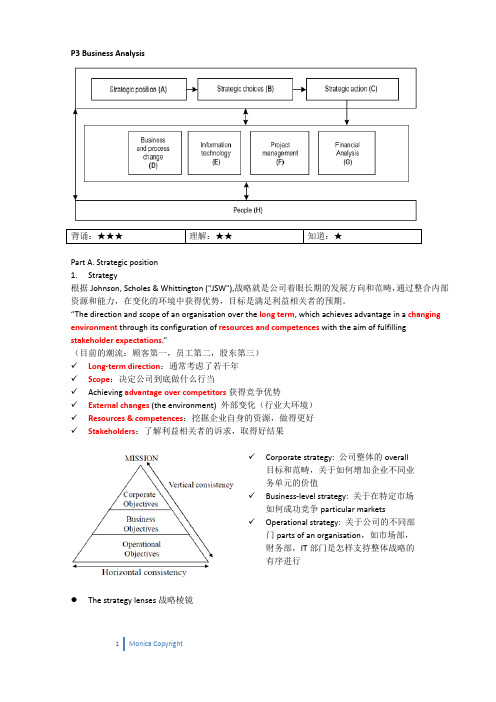

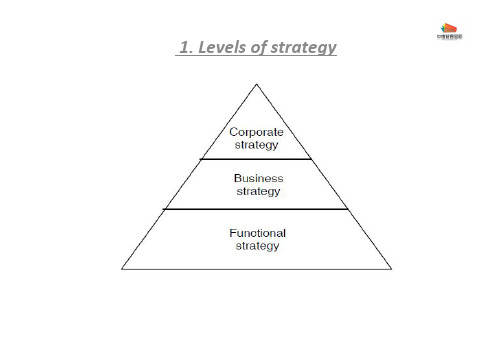

P3 Business Analysis背诵:★★★ 理解:★★ 知道:★Part A. Strategic position1.Strategy根据Johnson, Scholes & Whittington ("JSW"),战略就是公司着眼长期的发展方向和范畴,通过整合内部资源和能力,在变化的环境中获得优势,目标是满足利益相关者的预期。

“The direction and scope of an organisation over the long term, which achieves advantage in a changing environment through its configuration of resources and competences with the aim of fulfilling stakeholder expectations.”(目前的潮流:顾客第一,员工第二,股东第三)✓Long‐term direction:通常考虑了若干年✓Scope:决定公司到底做什么行当✓Achieving advantage over competitors获得竞争优势✓External changes (the environment) 外部变化(行业大环境)✓Resources & competences:挖掘企业自身的资源,做得更好✓Stakeholders:了解利益相关者的诉求,取得好结果✓Corporate strategy: 公司整体的overall 目标和范畴,关于如何增加企业不同业务单元的价值✓Business‐level strategy: 关于在特定市场如何成功竞争particular markets✓Operational strategy: 关于公司的不同部门parts of an organisation,如市场部,财务部,IT部门是怎样支持整体战略的有序进行●The strategy lenses战略棱镜✓Design: 战略的设计应该是理性的rational,自上而下的top‐down process,中级管理层根据战略设定来分析信息,确认一个清晰的行动方案。

超实用:ACCA全国第一P3学习攻略

超实用:ACCA全国第一P3学习攻略7月18号收到成绩时着实惊讶了很久。

大三这半年我的重心并没有完全在ACCA上,留给备考的时间不到一个月。

进P阶段以后我从没想过要冲第一,但我发自内心的喜欢这一门科目。

P3是一门很傲娇的paper,它是ACCA整个课程体系里的霸道总裁,站在金字塔的顶端运筹帷幄,做着关乎企业生存发展的strategy,而学到此时我们被赋予的身份是企业的CEO或者咨询顾问,有机会感受一个在毕业之后短时间内都无法达到的高度和视野,这是多酷的事情。

从5月份开始进入复习状态,我的复习过程相信和大多数人类似,分为三步,第一步知识点巩固,第二步真题练习,第三步回顾总结。

P3的知识点并不难,但在复习知识点这一步最重要的是要把零碎的知识点串成一个完整的体系。

P3的整本书是有一个很清晰的整体逻辑的,举个例子:一般来说case study从外部战略环境分析开始,所以一开篇我们接触到的就是和外部战略环境相关的模型,PESTLE给了我们一个全面分析external environment的方向,五力模型将视角缩小一个具体行业的吸引力,Diamond研究一个企业的成功可否在另外一个新的环境里复制。

若外部环境有利,接下来则把视野转向公司内部。

而对内部的分析最重要是能不能拥有competitive advantages. 这就涉及到对value chain的分析,和对于competitivestrategy的选择。

往后走,当企业发展到一定阶段,必然面临着本地市场趋于饱和,产品进入衰退期的状况,这时Ansoff和TOWS模型给我们指引了一个继续扩张的方向。

而扩张之后,企业从单一的company变成了有多个业务组合和公司单元的corporate,业务越来越复杂,如何更好地分配资源,进行项目管理?BCG matrix和Ashridge porfolio就是很好的评估工具等等。

这里要特别感谢一下教我们P3的Rainbow老师,在讲解知识点的时候,从一开始就给了我们一个很清晰的宏观视野。

ACCA F2知识点:benchmarking

ACCA F2知识点:benchmarkingBenchmarking is an attempt to indentify best parctices and by comparison of achieve improved performance。

benchmarking叫标杆学习法,也叫作基准分析。

标杆管理法由美国施乐公司于1979年首创,西方管理学界将其与企业再造、战略联盟一起并称为20世纪90年代三大管理方法。

标杆就是寻找一个具体的先进榜样解剖其各个先进指标,研究它背后的成功要素,向其对标学习,发现并解决企业自身的问题,最终赶上和超越它的一个持续渐进的学习、变革和创新的过程。

Benchmarking法起源于Xerox公司,施乐曾是影印机的代名词,但日本公司在第二次世界大战以后,勤奋不懈地努力,在诸多方面模仿美国企业的管理、营销等操作方法。

日本竞争者介入瓜分市场,从1976年到1982年之间,占有率从80%降至13%。

施乐于1979年在美国率先执行benchmarking,总裁柯恩斯1982年赴日学习竞争对手,买进日本的复印机,并通过“逆向工程”,从外向内分析其零部件,并学习日本企业以TQC推动全面品管,从而在复印机上重新获得竞争优势。

ACCA F2中标杆学习有四种类型:(1)internal benchmarking:指一个组织内部不同部门、据点、分支机构的相同作业流程的相互评量比较,主要目的在采取迅速作为解决顾客问题。

以图书馆为例,比较总馆与各分馆间参考服务的作业流程,可寻找出全馆内最佳参考服务典范与解决参考服务过程中所共同遭遇的问题。

(2)competitive benchmarking:以组织同业竞争者的产品、服务、作业流程作为评量比较的标杆,试图找出自身的优势或弱点。

以图书馆为例,以同性质、声誉卓著的图书馆同业为标杆,比较彼此图书采购流程的差异,进而采纳仿效对方的优点,即为竞争性流程标杆分析的做法。

2017年6月ACCA考试P3商务分析真题及标准答案

2017骞?鏈圓CCA鑰冭瘯P3鍟嗗姟鍒嗘瀽鐪熼(鎬诲垎锛?25.00锛屽仛棰樻椂闂达細195鍒嗛挓)妗堜緥鍒嗘瀽棰?br/>Section A涓哄繀鍋氶锛孲ection B浠绘剰閫変袱棰樸€?/p>(鎬婚鏁帮細4锛屽垎鏁帮細125.00)Section A – This ONE question is compulsory and MUST be attemptedMFP (Mutual Farm Products) was formed in 1910 as a co-operative shop network owned by farmers in the country of Arboria. It progressively opened small shops across the country selling products produced by Arborian farmers. Over time its expanding network of shops began to offer non-farming products from a wide range of suppliers, but it has remained true to its co-operative roots. All employees are shareholders and receive annual dividends. Customers can also become shareholders and are rewarded with dividends which reflect the value of their spending in the shops. An increasing number of customers are becoming shareholders, reflecting a renewed interest in the country in mutual organisations, such as co-operatives. MFP only operates in Arboria and it has no plans to expand overseas. Arboria itself is a wealthy, industrialised country which continues to grow.Supermarkets in ArboriaWhen supermarkets were first introduced in Arboria, MFP reflected this trend by opening its own supermarkets. However, its supermarkets tended to be (and continue to be) smaller than its well-known competitors and its network of smaller shops was largely retained. In contrast, other supermarkets focused on developing large out-of-town sites serving a large catchment population. In the top-ten supermarkets of Arboria, only MFP has, in addition, a network of smaller shops.In 2012 MFP was the eighth largest shop and supermarket chain in Arboria. It reported revenues of $10bn, compared to the $40·5bn revenue of the market leader, HypCo. By 2016, MFP was the ninth largest shop and supermarket chain in the country, with revenues of $11bn, compared with HypCo’s $45bn. During this period, two new supermarket chains have entered the Arborian market. These two new entrants, Super24/7 and Letto, already have a combined revenue of $50bn and are fourth and eighth respectively in the top ten Arborian supermarket chains. Both of these companies are overseas-based supermarkets operating a no-frills approach to retailing. Overall, the revenue of the top ten supermarket chains has increased from $300bn to $350bn in the last five years.Margins in the sector are always under pressure and the large supermarkets continue to aggressively market their goods, highlighting price savings. They also provide customer incentives, such as loyalty cards and account discount schemes in an attempt to retain customers. For many products and services, price comparison websites show consumers the prices charged by competing supermarkets.With the exception of MFP, all supermarkets are quoted companies with their shares largely owned by institutional investors who look for significant dividends and capital appreciation. MFP is the only co-operative in the top ten Arborian supermarket chains. Generally, suppliers to superma rkets are relatively small companies. Supermarkets’ control of consumer spending is so great that many suppliers aggressively compete to have their products stocked by the supermarket chains.MFP has continued to promote and follow its ethical principles. It ensures that new shops and supermarkets are energy efficient. It also continues to pay its employees significantly more than its competitors. This concern for its employees’ welfare appears to lead to excellent customer service performance. For example, in a recent independent survey of supermarket customers, MFP was ranked first for personal customer service.There is some evidence that people in Arboria are becoming disillusioned with their supermarkets and this is reflected in Appendix A, an extract from an article by the journalist Liz Bones in the influential daily newspaper, Arbor Today. Appendix B is an extract from an information sheet issued by the government to companies trading in Arboria.Management at MFPManagement at MFP is aware that the company has certain weaknesses. For example, it acknowledges that it needs to streamline its supply chain and achieve cost savings. It also recognises that it has failed to exploit technological advances in product control, movement and storage.However, before making changes, the management wishes to better understand the strategic position of MFP and the models used to assess this position. It has asked for a report which includes:–An explanation of the purpose and value of PESTEL analysis and Porter’s f ive forces framework.– An analysis which identifies external factors from the perspective of four elements of the PESTEL analysis: political, sociocultural, environmental and legal.–An analysis of the market place using Porter’s five forces framework.– The potential role of critical success factors (CSFs), key performance indicators (KPIs) and integrated reporting on formulating and monitoring strategy at MFP. The company does not currently use such concepts.Appendix A: Have Arborians fallen out of love with the supermarket? By Liz BonesFor many years, the trend towards supermarket shopping has seemed unstoppable. The high streets of our towns have become increasingly deserted as grocers, butchers, toy shops and bookshops have disappeared under the combined onslaught of online retailers and expanding supermarkets. For example, ten years ago in the high street of Milton Magna there were three grocers, four butchers, two toy shops, one bookshop and only two supermarkets. Now, only one grocer and one butcher survive on the high street and both supermarkets have moved to out-。

ACCA-P3考点-Exam Points

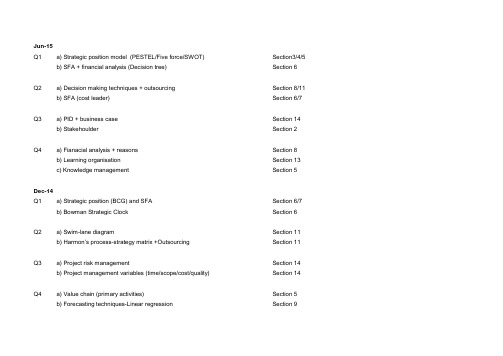

Jun-15Q1a) Strategic position model (PESTEL/Five force/SWOT)Section3/4/5b) SFA + financial analysis (Decision tree)Section 6Q2a) Decision making techniques + outsourcing Section 8/11b) SFA (cost leader)Section 6/7Q3a) PID + business case Section 14b) Stakehoulder Section 2Q4a) Fianacial analysis + reasons Section 8b) Learning organisation Section 13c) Knowledge management Section 5Dec-14Q1a) Strategic position (BCG) and SFA Section 6/7b) Bowman Strategic Clock Section 6Q2a) Swim-lane diagram Section 11b) Harmon’s process-strategy matrix +Outsourcing Section 11Q3a) Project risk management Section 14b) Project management variables (time/scope/cost/quality)Section 14Q4a) Value chain (primary activities)Section 5b) Forecasting techniques-Linear regression Section 9Jun-14Q1a) Strategic position (SWOT)Section 5b) Contextual features of change Section 15c) Strategic options (TOWS)Section 5/7Q2a) Pricing Section 10b) Marketing mix Section 10Q3a) Selection of software package (critera)Section 11b) For and against software package Section 11Q4a) Business case (cost-benefit analysis)Section 14b) Benefit realisation Section 14Dec-13Q1a) Organic growth, acquisition, and strategic alliances Section 6b) SFA Section 7c) Porter's diamond Section 3Q2a) Time series and multiple regression Section 9b) Budgetary process Section 8Q3a) Change management Section 15b) Marketing strategies Link to Section 10 and SenarioQ4a) 6 Is of e-business Section 12b) Change Link to Section 15 and SenarioJun-13Q1a) Project management process Section 14b) Organisational culture and organisational configuration Section 2 and 13c) Strategic lenses Section 2Q2a) Porter's 5 forces Section 4b) Porter's 5 forces Link to Section 4 and SenarioQ3a) Harman's process-strategy matrix Section 11b) Methods of acquiring and retaining customers using e-marketing Section 12Q4a) Leadership style Section 13b) Job enrichment Section 13Dec-12Q1a) Strategic position (BCG or Swot)Section 5 or 6b) Change mangement-Balogun and Hope Hailey (contextual feature)Section 15c) Benchmarking (principles, advantages and disadvantages)Section 10Q2a) Strategic position (external environment)+Strategic capability+Stakeholders Section (1-4), 5, and 2b) Website (e-business)Link to Section 12 and SenarioQ3a) Franchising option (advantages vs disadvantages)Section 6Calculationb) Other forms of Strategic alliance Section 6c) Organic growth Section 6Q4a) Decision tree Section 9b) Decision tree (points not considered by decision tree)Section 9c) How to avoid or mitigate risk Link to SenarioJun-12Q1a) Financial position (Benchmarking)Link to Secion 10 and technical articleb) Stratigic options and SFA test Section 6 and 7c) Mission, value, and communication Link to Section 2 and technical articleQ2a) Software package Section 12b) Formal process for software package procurement, evaluation andimplementation Link to Section 12 and SenarioQ3a) Project initiation documents Section 14b) Business case benefits Section 14Q4a) Value chain Section 5b) Re-structuring upstream and downstream value chain Section 12Dec-11Q1a) Strategic position (SWOT)Section 5b) SFA Section 7c) CSF and KPI Section 10Q2a) Culture Section 2b) Harman's process-strategy matrix Section 11Q3a) a post-project review, a post-implementation review and abenefits realisation review.Section 14b) post-project review and a post-implementation review (lessons learned)Link to Section 14 and Senarioc) Benefits brought by electric ordering system Link to senarioQ4a) Factors about setting price Section 10b) Multiple regression and data limitation Link to Section 9 and senarioJun-11Q1a) PESTEL and Porter's 5 force Section 3 and 4b) Outsourcing (advantage and disadvantage)Section 11c) Weakness addressed Link to senarioQ2a) Investment appraisal approach Link to F9 knowledgeb) Matrix structure Section 13Q3a) Process improvement Section 11b) Software package and its implication Link to Section 12 and senarioQ4a) 6 Is Section 12b) e-procurement Section 12Dec-10Q1a) BCG matrix Section 6b) i) Change mangement-Balogun and Hope Hailey Section 15ii) Strategic change Link to senarioc) Portfolio management Section 7Q2a) Drivers and barriers for e-business Section 12b) e-business + marketing mix Section 12 and 10Q3a) Cultural web Section 2b) Organisation configuration + cultural type Section 13 and 2Q4a) e-assessment (advantages and disadvantages)Section 12b) Business case, benefit realisation Link to section 12 and senarioJun-10Q1a) Strategic position Section 1-5b) Process improvement Link to section 11 and senarioc) Acquiring and retaining customers through e-business Section 12Q2a) SFA Section 7b) Porter's diamond Section 3Q3a) Outsourcing (Advantages)Section 11b) new or enhanced competencies Link to section 5 and senarioc) E-business Section 12 (Link to senario)Q4a) Appraisal process and performance measures Section 13b) Competency framework Removed from syllabusDec-09Q1a) Porter's 5 Force Section 4b) SFA Section 7c) Stakeholder (Mendelow's Matrix)Section 2Q2a) Value Chain Section 5b) How to address the problems on value chain Section 5Q3a) Good variables for project management Section 14b) Harmon’s process-strategy matrix Section 11Q4Characteristics of good software (Criteria)Section 11Jun-09Q1a) SWOT Section 5b) SFA Section 7c) i) Modification of process Section 11ii) relationship between process design and strategic planning Section 11Q2a) Strategic position + leadership style Section 1-5 +13b) Franchising Section 6Q3a) Financial analysis Section 8b) Software package Section 12Q4a) Management reward scheme Section 13b) Six Sigma Remove to P5Dec-08Q1a) PESTEL Section 3b) Culture web Section 2c) Strategic lense Section 1Q2SFA on acqusition Section 6/7Q3a) Project plan Section 14 b/c) Project slippage Section 14Q4a) Rewards management scheme Section 13b) Performance measures Section 13Jun-08Q1a) Porter's 5 force Section 4b) SFA Section 7c) Strategic change and reward system Section 15+13Q2a) Harman's process-strategy matrix Section 11b) Outsourcing (for and against)Section 11Q3a) 6Is Section 12b) Marketing mix Section 10Q4a) Types of change Section 11/15b) Contextual features of change Section 15Dec-07Q1a) Strategic postion (SWOT)Section 5b) no frill + SFA Section 6+7c) SFA-Ansoff's matrix Section 6+7Q2a) Project initiation document Section 14b) Project management Section 14Q3a) Value chain (primary activities)Section 5 b/c) Re-structure its upstream and downstream supply chain Section 12Q4a) Role of quality, quality control and quality assurance H/Wb) Six sigma H/WPilot paperQ1a) Strategic postion -Pestel Section 3b) Strategic postion -Porter's 5 force Section 4c) Financial position + cost-benefit analysis Section 8+14Q2Internal development, acquisitions and strategic alliances Section 6Q3Forecasting techniques (Time series/Linear regression)Section 9Q4a) Value chain Section 5b) Re-structure its upstream and downstream supply chain Section 12。

05 ACCA P3 知识点汇总

36. Methods of strategic development •Internal growth •Acquisitions or mergers •Strategic alliances

Joint venture Licensing Franchising

37. Suitability, Feasibility & Acceptability

18. Value chain

19. Value network

20. Strategic capability r+c=C

21. Resource audit – 6M’s •Money •Manpower •Management •Method •Machine •Mechanism •参见SFA article

46. Redesign pattern

47. Swim lane

48. Harmon’s grid – process/strategy matrix

49. Adv & Disadv of using a generic software solution Advantages

a.Cost savings b.Time savings c.Quality d.Documentation and training e.Maintenance support prehensive package evaluation s

1. Levels of strategy

2. Strategy development process •Deliberate strategy •Emergent strategy •Incremental strategy

ACCAP3知识点总结

ACCAP3知识点总结ACCAP3是ACCA(特许公认会计师)课程的第三阶段,在ACCA考试的过程中是非常重要的一个阶段。

在这个阶段,学员需要掌握更加深入复杂的会计知识,具备扎实的专业能力和解决问题的能力。

以下是ACCAP3的知识点总结:1.管理会计管理会计是指为企业内部管理决策服务的会计。

在ACCAP3课程中,学员需要掌握管理会计的基本概念和技巧,包括成本-收益分析、成本分类、成本控制、绩效评估等方面的知识。

此外,学员还需要了解现代管理会计技术的应用,如活动基础成本管理、质量成本管理、目标成本管理等。

2.管理决策管理决策是管理会计的核心内容之一,涉及企业内部各个方面的决策。

在ACCAP3课程中,学员需要掌握管理决策的基本原理和方法,包括差异分析、边际成本、机会成本等概念。

此外,学员还需掌握现代管理决策模型的应用,如线性规划、灵敏度分析、风险分析等。

3.财务管理财务管理是企业财务决策的核心内容,包括资金管理、投资管理、风险管理等方面。

在ACCAP3课程中,学员需要掌握财务管理的基本原理和技巧,包括财务报表分析、资本预算、财务风险管理等。

此外,学员还需了解国际财务管理的相关规范和标准,如国际金融报告准则(IFRS)。

4.企业战略企业战略是企业长期发展的规划和决策,包括市场定位、竞争战略、资源配置等方面。

在ACCAP3课程中,学员需要掌握企业战略的基本概念和方法,包括SWOT分析、价值链分析、波特五力分析等。

此外,学员还需了解战略规划的实施过程和方法,如平衡计分卡、战略地图等。

5.风险管理6.企业伦理企业伦理是企业社会责任的核心内容,包括企业与员工、客户、股东、社会等各方面的道德义务。

在ACCAP3课程中,学员需要掌握企业伦理的基本原则和规范,包括公平、诚信、责任等。

此外,学员还需了解企业伦理的实施要求和方法,如道德决策模型、伦理审计等。

ACCA P3 考点总结极简版

P3 走近60分 ( Final review of knowledge & Skill Part)1.Strategy can be defined as:‘the direction and scope of an organisation over the long-term, which achieves advantage in a changing environment through its configuration of resources and competences with the aim of fulfilling stakeholder expectations’.CAI’s selection 12. Major TypesStrategic planning involves formal analysis of each of the stages of strategic position before a final strategic choice is made. Strategic planning is useful because:•It forces managers to consider each stage of the strategic process•It forces managers to justify their actions•It forces managers to consider the effect of a strategy on all aspects of the business•It allows managers to be proactive rather than reactive.Emergent strategies involve no long-term strategic plan – in effect, making up the strategy as the organisation goes along. An emergent strategy is useful because:•It allows managers to quickly exploit changing circumstances•It is quicker and cheaper than strategic planning.CAI’s selection 23.Position,Choice,and actionUnder the rational planning model, there are a number of stages. Each of these will be discussed in more detail later in the notes.Stage 1 – Strategic Position1 Identify key stakeholders and their expectations.2 Develop long-term objectives to satisfy these stakeholder expectations.3 Calculate financial and nonfinancial ratios to show position of organisation.4 Identify core resources and competences within the organisation.5 Identify key factors changing the environment outside the organisation.6 Use SWOT analysis (also known as a corporate appraisal) to summarise the strategic position.Stage 2 – Strategic Choices1 Consider possible exit from existing industries.2 Consider diversification into new industries.3 Consider developing new competitive advantages.4 Consider entry into new markets.5 Consider development of new products.Stage 3 – Strategy into Action1. Evaluate above options and choose strategy to be followed.2. Implement any necessary changes in the organisation.3.This might involve changing processes, people etc.CAI’s selection 34.Model Johnson and Scholes – three lensesThis model argues that strategy can be set in different ways:•Strategy as experience.Here the strategy is basically repeating what has been done in the past.•Strategy as ideas.Here the strategy aims to encourage innovation. Culture will be very important here.•Strategy as design.Here the strategy is driven from the top in order to meet the objectives of the organisation. The process is very similar to that given earlier in this chapter.5.MODEL – Mendelow stakeholder mappingThere will always be a conflict of interest between what different groups want. For example giving employees better pay levels reduces the profit available for shareholders. Stakeholders can be divided into:•High Interest with High Power = Key players•Low Interest with High Power = Keep satisfied•High Interest with Low Power = Keep informed•Low Interest with Low Power = Minimal effort.Stakeholders matter because objectives should be geared towards the needs of those with high power. Stakeholders matter because any strategy followed will need to be acceptable to the key players and keep satisfied.CAI’s selection 46.Corporate governanceJohnson and Scholes suggest that corporate governance is about answering two questions:1. Who is the organisation there to serve (i.e. who are the key stakeholders?)?2. How should the priorities of the organisation be decided (i.e. should strategy e planned or should the organisation be opportunistic?)?Johnson and Scholes define the main ethical position for a company as: The extent to which an organisation will exceed its minimum obligations toshareholders.The four main ethical positions are:1. Short-term shareholder interest.2. Longer-term shareholder interest.3. Multiple stakeholder obligations.4. Shaper of society.7.Core values are the principles that guide the behaviour of an organisation.A mission statement explains to the external world and to those managers making strategic decisions inside the organisation, the basic principles theorganisation should be following.A mission statement will commonly contain the following:•Purpose of the organisation.•Overall strategy of the organisation.•The core values of the organisation.Supporters of mission statements claim they help:•Resolve stakeholder conflict.•To guide managers when setting strategy.•Communicate the values of the organisation to employees.•Help with marketing the organisation.CAI’s selection 58.MODEL – Charles Handy types of cultureOrganisational culture consists of the beliefs, attitudes, practices and customs to which people are exposed during their interaction with the organisation.•Power – Heavily centralised with few decision-makers. Allows quick responses to changes in the environment.•Role – Lots of formalised procedures. Can be very useful in an environment that is stable.•Task – Emphasis on getting the job done rather than following rules. Works well in complex, unstable environments.•Person – Purpose is purely to look after the individuals (found where self-employed people are the norm).This may impact on whether a strategy chosen by the Directors is likely to be accepted by the employees.9.MODEL – Miles and Snow – Strategic cultures•Defenders – like strategic options that have worked in the past / low risks / secure markets.•Prospectors – like options that could deliver results even if they entail high risk.•Analysers – will move into new areas but only after someone else has proved they work.•Reactors – do not plan ahead.•The above may impact on the type of decisions made by the organisation.10.MODEL – Johnson and Scholes the cultural web•Rituals and routines – Which procedures are emphasised?•Symbols – Are status symbols used within the organisation as rewards?•Control systems – What is most closely monitored?•Organisational structures – How tall / flat is the organisation?•Power structures – How much centralisation is there?•Stories – Does news within the organisation focus on successes or failures?•The paradigm – What assumptions are taken for granted?CAI’s selection 611.Model – Johnson and Scholes Key drivers of change•Market globalisation•Cost globalisation•Global competition.In addition to the above, if you have a UK company, use:•Economic – conditions as they are at the time of the exam.•Environmental – the move towards more environmentally friendly products (this includes things like materials and packaging).•Legal – minimum wage for unskilled labour.12. MODEL – PESTEL•Political – includes government policies on education and infrastructure.•Economic – includes the state of the economy, interest rates and tax levels.•Social – includes attitudes, demographics and household structure.•Technological – includes new technologies making current products obsolete.•Environmental – includes the move towards environmentally cleaner products.•Legal – includes changes in law making it e.g. harder / more expensive to operate.CAI’s selection 713.Scenario planning•These methods look at what might happen (scenarios) and then decide what the organisation should do if they occur.14.Time Series AnalysisTime Series Analysis is used when sales tend to be seasonal. The time series is made up of two parts:•The long-term trend (calculated using moving averages).•The seasonal variation (calculated as the average of actual figures against the trend).Regression Analysis is used when sales tend to be steady throughout the year.15.MODEL – Porter’s national diamondCompanies based in certain countries seem to be more competitive than companies from other countries. Porter’s diamond looks at why.Porter comes up with 4 reasons for this:•Factor conditions•Firm strategy, structure and rivalry•Demand conditions•Related and supporting industries.CAI’s selection 816.Industries LifecycleIndustries grow and then shrink over time. It is important for a company to consider which industries it is involved in so that it can deliver profits to shareholders over the long-term. The stages the industry goes through are:Introduction•The industry is only just being established.•The industry may be seen as a niche.•At this point there may be only a few competitors (or maybe only one).•Customers may not be entirely sure why they need the product.Growth•An increasing number of customers start to buy the product and reasonable profits can be made.•The industry becomes more attractive and new competitors attempt to join.Maturity•The industry typically goes through a period of consolidation.•Weaker companies might leave.Decline•Customers are buying different products and so total sales are falling.•The industry may again become a niche.•As part of its corporate strategy, a company should regularly review the industries it is in to decide whether to:•Exit from existing industries.•Enter into new ones.CAI’s selection 917.Porter’s 5 forcesPorter’s 5 forces model looks at why some industries might be more profitable than others. In general the more of the forces that are favourable within an industry the more profits will be earned. Unfortunately as the industry becomes more attractive then more rivals will want to enter it.The 5 forces are:•Competitors (new)•Competitors (existing)•Customers•Suppliers•Substitutes.18.MODEL – The marketing mix•Product – What the customer receives•Price – the Cost to the customer•Place – the convenience to the customer•Promotion – how does the company Communicates with the customer19.CSF & KPICritical success factors are those elements that an organisation must perform properly in order to succeed. These often link with competences.•Threshol d competence•Core competen ces.CAI’s selection 10A common way of thinking about KPI’s is to group them into various categories. One common approach is to use:•Econo my – the amount spent on inputs (materials, labour, marketing etc).•Effectiveness – whether customers are satisfied with the products / services provided (customer satisfaction, repeat customers etc).•Efficiency – how good the organisation is at turning inputs into outputs (wastage, idle time etc).20.MODEL – the nine M’s modelThis model gives nine possible areas an organisation might be strong in•Machinery•Money•Materials•Men and Women•Makeup (culture)•Markets (products)•Management information•Management•Methods (processes).In the exam, look at the numbers that the Examiner gives you (particularly ones that do not fit into Financial Accounting areas). These often indicate weaknesses. Examples could include:•Sales per employee•Age of machinery•Time taken to process orders.CAI’s selection 1121.Cost controlOne common threshold competence in the exam is cost control.This is important to public sector organisations as they may have a fixed income.This is important to companies as they are trying to make a profit. If costs increase then either they have to accept lower profits or attempt to pass this on to customers through higher prices. The likelihood of costs rising will be affected by the power of the organisation’s suppliers.The possibility of raising sales prices will be affected by the power of customers. Costs could be reduced through:•Economies of scale•Low supply costs•Sensible design•Experience.CAI’s selection 1222.Sustainable competitive advantageSustainable competitive advantage is about the reasons a customer buys from one firm rather than another.The key word here is “sustainable”, a resource may give an organisation an advantage in the short-term but this will not be sustainable if it is easy for competitors to acquire as well.Similarly a competence that can easily be copied by others will only give a short-term advantage.Sustainable competitive advantage will need to focus on resources and capabilities which are:•Rare (this could include patents or a skill).•Robust (things that are difficult to imitate). Examples include:o Complex procedureso Uncertainty to outsiders.•Difficult for a customer to substitute with somethi• A final thing to remember is that the customer must be willing to pay for this unique resource or core competence.CAI’s selection 1323.MODEL – Porter’s value chainPorter divides a business into nine different areas. The five primary activities are:•Inbound logistics•Operations•Outbound logistics•Marketing and sales•Service.The four secondary activities are:•Firm infrastructure•Human Resource Management•Technology Development•Procurement.Porter argues that each cost in the business is one of two types.•Value-adding – the extra cost is outweighed by the extra the customer is willing to pay•Non value-adding – the extra cost is not valued by the customer.CAI’s selection 1424.Knowledge managementThe knowledge that an organisation has is a resource that may be difficult for other organisations to acquire and so can be a source of competitive advantage.For this to happen the organisation must record the knowledge of its employees and make it available to others.Knowledge management is the collective and shared experience accumulated through systems, routines and activities of sharing across the organisation.25.MODEL – Nonaka and Takeuchi on tacit and explicit knowledgeTacit knowledge is knowledge that staff possess. They are often unaware of how important this knowledge is. Explicit knowledge is knowledge that has been recorded by the organisation.Nonaka and Takeuchi say knowledge can be transferred by:•Socialisation•Externalisation•Internalisation•Combination.CAI’s selection 1526.SWOTOnce the organisation has analysed the external and internal environments it should be able to identify:•Strengths•Weaknesses•Opportunities•Threats.It is important to remember that strengths and weaknesses are in the eye of the customer not the company.It is important to remember in the exam that opportunities and strengths need to match up. If there is an opportunity for which the organisation does not have a matching strength – then the organisation will not be able to exploit the opportunity.Strategic capability can be improved by:•Extending competences•Ceasing nonessential activities•Extending best practices•Adding or improving activities•Remedying weaknesses.CAI’s selection 1627.Benchmarking•Historical comparisons are made between actual and past figure to see if the organisation is improving / deteriorating.•Strategic– comparisons are made between actual and budget (note that the budget should be set at a level so that meeting the budget should mean the critical success factor is achieved).•Industry – comparisons are made between actual and performance of others to see if we are performing better or worse than our rivals (this will identify strengths and weaknesses).28.Balanced scorecardAll processes must be as efficient and effective as possible in order to support the strategy. This means the organisation will need some method of measuring performance. One common method is to use the balanced scorecard. Processes can be measured to see if they are helping the following perspectives:•Financial•Customers•Internal business•Innovation and learning.CAI’s selection 1729.MODEL – Ansoff’s growth vector matrixIgor Ansoff came up with a simple method of identifying strategic options. The areas for a business to consider are:•Should they carry on selling their existing products?•Should they carry on selling to their existing market (this means the types of customer they already target)?Ansoff comes up with four possibilities:•Market penetration – existing products and existing markets•Market development – existing products and a new market•Product development – new products and an existing market•Diversification – new products to a new market.30.Methods?We will look at all of these in turn in this sectioWhichever of these is chosen there is an additional decision to be made. Should the organisation:•Grow organically – should the organisation launch a new product / go into a new market themselves?•Grow by acquisition – should the organisation buy another company that sells a new product / operates in a different market?A company can attempt to enter a foreign market in a number of ways. The main ones for a manufacturer are:Direct exporting – selling directly to overseas customers.•Advantages – the company gets to know the needs of the final customer•Disadvantages – it may be costly to build up customer awareness.Indirect exporting – selling to intermediaries such as retailers who then sell to final consumer.CAI’s selection 18•Advantages – the company gets access to the local company’s knowledge•Disadvantages – the company will not see all of the profits.Overseas production– the company manufactures and sells the products in the target country.•Advantages – distribution costs will be reduced•Disadvantages – may require a large capital investment.Contract manufacture (licensing) – the product is made abroad by another company.•Advantages – lower risk since no need to build manufacturing plant•Disadvantages – may lose control over areas such as quality.Joint ventures – the company goes into partnership with a local company.•Advantages – lower risk since local knowledge gained and costs shared•Disadvantages – lower returns since profits shared.CAI’s selection 1931.MODEL – Porter’s generic strategiesA further possibility would be to change HOW the company competes (the business strategy). This means changing the reason why customers should buy theproduct. Porter comes up with three possibilities:•Cost leadership•Product differentiation•Focussing on a particular type of customer.32.MODEL – The BCG matrixIn the exam you may have to calculate the market share of a product. If the information is available it would also be useful to calculate profit margins for each product.•Cash cows are in the mature or decline stage of the life cycle:o The threat of new competitors is low and the high market share makes the threats from substitutes and existing competitors low as well.o This product should be earning reasonable profits.o The product cannot grow any further (since the market is already mature).•Stars also have a high market share:o The market is growing (introduction or growth stage of the lifecycle) so new competitors will be attracted into the marketo Prices may need to be kept low to maintain market shareo Marketing costs might also need to be high to keep sales upo Profits may not be high.•Question marks have a lot of potential due to the high growth. Decision is whether to:o Spend money to build up market shareCAI’s selection 20o Spend money to hold market shareo Leave market.•Dogs have low market share and low growth. They should be closed unless needed by one of the other products.33.Related diversificationRelated diversification (also known as concentric diversification) means moving into areas that are similar to those the business already operates in.The idea is use the current strengths of the company to exploit new opportunities. In the exam look for examples of:•Horizontal integration – e.g. a shirt manufacturer that starts manufacturing shoes•Backwards integration – e.g. a shirt manufacture that starts manufacturing cloth•Forwards integration – e.g. a shirt manufacturer that starts retailing clothes.CAI’s selection 2134.Model Johnson and Scholes strategic rationale•P ortfolio Managers•Synergy managers•Parental developers35.Ashridge ModelThe four groups are:•High Feel / High BenefitHeartland businesses which gain most benefit from the attention of the parent (concentrate on these).•High Feel / Low BenefitBallast businesses which would be just as viable if they were independent businesses (so leave these ones alone to run themselves).•Low Feel / High BenefitValue Trap businesses which do not have much overlap with the skills of the parent (these may have been acquired as a method of unrelateddiversification). Unless the parent can develop these skills the business may not be of much benefit.•Low / Feel / Low BenefitAlien businesses which should be sold off.From this follows the idea that the amount of cost being spent by the parent should reflect the value it adds to the divisions.CAI’s selection 2236.Model – Johnson and Scholes SFA testJohnson and Scholes suggest that for any option to be considered seriously it must pass three tests. The option must be:•Suitable•Feasible•Acceptable.A strategic option is suitable if:•It builds on strengths/ reduces weaknesses / exploits opportunities / avoids threats.•Gives a new competitive advantage / maintains an existing one.•Suits the organisation’s culture .•It fits with the current strategies already being aA strategic option is feasible if:•The organisation has enough finance to pursue it.•The organisation has the rights skills / knowledge / experience to pursue it.•The company will be able to deal with any responses from competitors.•The company has enough time to follow the strategy.A strategic option is acceptable if:•The additional reward if the strategy is successful is greater than the risk if it is unsuccessful.•The additional risk is acceptable to shareholders / banks etc.•It helps the company to meet its financial objectives (ROCE etc) – shareholders.•Any interest payments will be maintained – banks.•It does not break any regulations – government.•It does not adversely affect connected stakeholders – customers / suppliers.CAI’s selection 2337.Financial RatiosThe following are common causes for ADVERSE variances;•Materials price Powerful supplier Change of supplier•Materials usage Poor quality material•Labour rate Powerful supplier•Labour usage Poor quality labour•Overhead efficiency Poor levels of maintenance•Sales price Powerful customersMany substitutes•Sales volume Sales lost to new entrantsMany competitorsCAI’s selection 2438.Decision treeA decision tree is another quantitative method for looking at uncertainty.A decision tree is a diagrammatic approach to solving problems involving probabilities and decision making.MethodStep1: Draw the tree from left to right showing appropriate decisions andUsefor a decision point,and an outcome point.Label tree and cash inflows/outflows and probabilities associated with outcomes.Step2: Evaluate the tree from right to left.•Calculate an expected value at each outcome point.•Select the option to maximise expected payoff at each decision point.Step3: Recommend a course of action to management.CAI’s selection 2539.Model Harmon’s process-strategy matrixThere are four approaches to change depending on:•Is the pro cess strategically important? (does it tie up with SWOT); and•Is the proces s complex?This leads to•High importance / complex Improve processes focusing on staff•High importance / simple Use an automated ERP solution•Low importance / complex Outsource•Low import ance / simple Automate.40.OutsourcingIt will often be more efficient to outsource these since the outsourcing company can obtain economies of scale.Problems with outsourcing processes include:•Fragmentat ion of complex processes (outsourcers can only do part of the process).•Concerns with relying on others for key business processes.•Concerns about quality.•Unwillingness to be locked into long-term contracts.41.Evaluating Business ProcessesProcess improvement methods•Lean proce sses – eliminate nonvalue adding activities or time between activities.CAI’s selection 26•Human perfor mance analysis – redesign incentives, improve training.Process redesign methods•Automa te activities.•Integrate processes – to reduce gaps and disconnects.•Process Measu rement schemes – develop or redesign the way performance ids measured.42.Model – Skidmore and Eva – stages in selecting software package•The company may decide to have a software package written especially (known as a bespoke package). There are five stages the company goes through:•Obtain tenders•First pass selection•Second pass selection•Implementation•Managing long-term relationship.CAI’s selection 2743.6C- the benefits of E-businessThe above definition does NOT mean that goods / services have to be sold to customers over the internet – this is referred to as ecommerce. Benefits of adopting e-business include:•Cost reduction•Capability•Communication•Control•Customer service•Competitive.44.Model – McFarlan’s gridMcFarlan’s grid looks at how important IT is to the organisation, in particular, how it can help with the organisation’s strategy.•The impact of current IT systems on gaining an advantage.•The potential impact of future IT systems on gaining an advantage.1. Current Low / Future low SupportIT is useful but no advantage is being achieved (e.g. payroll).2. Current High / Future low FactoryIT is crucial to the current operations but it is unlikely that it can be developed further to give an advantage in the future( e.g. a JIT system).CAI’s selection 283. Current Low / Future High TurnaroundIT can be used to develop new advantages over the long-term (e.g. Amazon’s Kindle e-reader and store).4. Current High / Future High StrategicIT will be fundamental to the ongoing success of the business.45.Model 6i’s for emarketing1 Interactivity – Customers can be asked for contact details.2 Integration – Adverts on the web can be clicked to go straight to purchasing.3 Intelligence – websites can record how many visitors they have and what they do on the website.4 Industry structure – Websites can change distribution channels (by cutting out intermediaries and selling direct).5 Independence of location.6 Individualisation – if a customer regularly visits a website it can be tailored to that individual.46.Model – Adcock’s guide to CRMCRM is the establishment, development, maintenance and optimisation of long-term mutually valuable relationships between consumers and organisations.CRM has many benefits including:•Improved retention•Improved cross-sellingCAI’s selection 29Improved profitability.In order to build relationships with customers, businesses need to:•Build a customer database•Develop customer oriented service systems•Have more direct contacts with customers.As part of this process, businesses should think about their long-term relationship with customers and what that is likely to be worth over the customer’s lifetime. CAI’s selection 30。

ACCA F2知识点:benchmarking

ACCA F2知识点:benchmarkingBenchmarking is an attempt to indentify best parctices and by comparison of achieve improved performance。

benchmarking叫标杆学习法,也叫作基准分析。

标杆管理法由美国施乐公司于1979年首创,西方管理学界将其与企业再造、战略联盟一起并称为20世纪90年代三大管理方法。

标杆就是寻找一个具体的先进榜样解剖其各个先进指标,研究它背后的成功要素,向其对标学习,发现并解决企业自身的问题,最终赶上和超越它的一个持续渐进的学习、变革和创新的过程。

Benchmarking法起源于Xerox公司,施乐曾是影印机的代名词,但日本公司在第二次世界大战以后,勤奋不懈地努力,在诸多方面模仿美国企业的管理、营销等操作方法。

日本竞争者介入瓜分市场,从1976年到1982年之间,占有率从80%降至13%。

施乐于1979年在美国率先执行benchmarking,总裁柯恩斯1982年赴日学习竞争对手,买进日本的复印机,并通过“逆向工程”,从外向内分析其零部件,并学习日本企业以TQC推动全面品管,从而在复印机上重新获得竞争优势。

ACCA F2中标杆学习有四种类型:(1)internal benchmarking:指一个组织内部不同部门、据点、分支机构的相同作业流程的相互评量比较,主要目的在采取迅速作为解决顾客问题。

以图书馆为例,比较总馆与各分馆间参考服务的作业流程,可寻找出全馆内最佳参考服务典范与解决参考服务过程中所共同遭遇的问题。

(2)competitive benchmarking:以组织同业竞争者的产品、服务、作业流程作为评量比较的标杆,试图找出自身的优势或弱点。

以图书馆为例,以同性质、声誉卓著的图书馆同业为标杆,比较彼此图书采购流程的差异,进而采纳仿效对方的优点,即为竞争性流程标杆分析的做法。

ACCA考试P阶段各科通过率及难度分析

ACCA考试P阶段各科通过率及难度分析ACCA考试P阶段各科通过率及难度分析2017ACCA考试科目一共16科,学员需要通过其中14门考试才能有资格申请会员资格。

在这14门课程的学习中,学习顺序与科目搭配安排是ACCA新人最关心的问题。

下面我们就简单了解一下各科目的特点,以帮助学员可以更好的选择和学习。

下面是yjbys店铺为大家带来的ACCA考试P阶段各科通过率及难度分析的知识,欢迎阅读。

ACCA P阶段各科通过率及难度分析P1 Governance, Risk and Ethics (GRE):这门课作为P阶段的第一门课程,内容上主要糅合了F1和F8的知识。

题目也都是文字性的内容,很多知识点都是一些常识性的知识,还有一些考点是需要特别记忆的,比如说董事会的组成及人数规定,ED与NED的.特点。

这类知识就要考生们特别背诵记忆。

P1考生普遍反馈的问题是,感觉知识学的很好,看真题答案也没有什么困难,就是考试时成绩不理想。

其实这门课最重要的还是要自己动手去写,切忌眼高手低。

自己做完题目后要与考官所给答案做对比,尽量与考官的观点看齐,这样才能最大程度上找到得分点,取得理想的成绩。

2016年P2平均通过率:48.5%P2 Corporate Reporting (CR):这门课程是公司报告,其核心内容是报表编制及对其报表中各项数据的分析。

题目涉及的各项交易和事项的处理远比F7要复杂,同时需要大家非常熟练地掌握IAS及IFRS 国际准则的要求和会计处理方法。

近年来,ACCA出题方向越来越偏向通过数据分析公司的各项情况,所以要求学员不仅要会算,还要知道为什么这么算,算出来的数据又可以怎么用。

2016年P3平均通过率:48%P3 Business Analysis (BA):这门课程是商务分析,既然是分析,那就摆脱不了各种模型。

要求学员可以将各个模型串联起来,熟练掌握每一个模型的原理和应用。

值得注意的是,考生往往容易犯一个错误,就是每个模型背的特别溜,但真到了考场上,你把你背的内容洋洋洒洒写上几大张纸,其实得分并不见得很理想。

ACCAP3考试:Benchmarking

ACCA P3 考试:Benchmarking本文由高顿ACCA整理发布,转载请注明出处Benchmarking can be used to compare an organisation ' s strategic capabilities with itself overtime and with other organisations at a given point time. There are three commonly used approachesto benchmarking:1. Historical benchmarkingOrganisations consider changes over time in their performance on a set of strategicallyimportant indicators in order to identify opportunities for improvement.A potential disadvantage of historical benchmarking is that it may lead to complacency for afirm that shows improvement over time. It is the rate of improvement that is important to comparewith that of competitors as competitors may improve at a faster rate.2. Industry/sector benchmarkingUsing a set of performance indicators, organisations may gain valuable insights when theycompare their performance to other organisation.Firms must benchmark against competitors in all industries in which they compete. Competitive activity and industry convergence have resulted in blurred industry boundaries.3. Best-in-class benchmarkingBest-in- class benchmarking compares an organisation ' s performance against "bestn- class " performance across industry lines and therefore seeks to overcome the limitations of otherapproaches.The overall importance of benchmarking lies not so much in the detailed "mechanic" of comparison but in the effect that these comparisons might have on behavior. It can be used as a process for gaining momentum for improvement and change.。

提分利器 ACCA P3考试答题小技巧速度Get

提分利器ACCA P3考试答题小技巧速度Get从近几次的考试内容以及考官对考卷的点评来看,有以下几个重点内容需要各位考生在复习的时候予以重视。

01时间管理问题总是有考生为了写得多而超出题目要求的范围来答题的情况。

如:2016年9月真题第三题这样的要求:requiredcandidates to use specified elements of a change model to assess the lik elysuccess or failure of the change. 但是有的考生把change的模型所有的方面全都写了,所以考官给出了这样的回答。

考官对答案的态度:some candidate responses developed outside of the scope of the question, cove ring all elements of thechange model, rather than just those specified. Those can didates did not losemarks for this, but did not gain marksfor those elements of t heir response and put themselves under unnecessary time pressure.请注意:考官看的并不是你写的字数,而是你写的质量,如果你写的内容超出了要求范围,是没有分数的,白白浪费自己的时间而已。

02分析的应用能力死记硬背理论和模型,是拿不到好分数的,拿到好分数的不一定要用啥模型。

重要的是分析的应用能力,而不是你学了啥啥模型。

所以不要单纯重复背景材料,请加上自己的分析。

考官的态度:Rote learning of theory andtheoreticalmodels is unlikely to provide the depth re quired to achieve highmarks in thissubject. Candidates should ensure that they c an understand and apply models to a variety of situationsto prepare themselves for thisexamination. Candidates who addvalueto the information provided in the scenario will earn higher marks than those who simply repeat theinformation.所以,答题的时候注意每一分的构成,最好应该有what,why,how这么几个意思。

英国特许公认会计师(ACCA)考试经验:我的P3高分技巧-ACCA-CAT考试.doc

从第一次参加ACCA的考试开始,我就一直在思考应该以什么样的方式来对待它,ACCA对我来说到底意味着什么?在大学期间,一次性通过所有ACCA的考试是个非常特别的经历,虽然中间有过迷茫,有过怀疑,但庆幸的是,我坚持了下来。

如果说有什么考试心得的话,我想坚持是顺利通过ACCA最重要的一点。

下面,我与大家一起分享自己对P3(商业分析)这门课程的一些想法。

复习资料在复习资料的选择上,我主要是用教材和历年试题,还有就是相关的考官文章。

相对于社会考生而言,在校生在强调经验和思维的P3科目上并不占优势,所以教材成为我理解相关理论的重要。

虽然没有时间仔细去看每个知识点,但至少要理解那些重要理论模型的框架、适用环境、优劣势等等;虽然经常听人说教材没有用,但作为一个学习知识的工具,教材还是非常重要的。

历年试题的重要性就不需要多说了,通过多做练习来熟悉题型和运用知识是通过考试的关键。

除此之外,考官文章是必不可少的一部分,文章里提到的理论通常都是非常重要的,而这些理论或多或少都会在近几期的考试中出现。

当然,我平时喜欢看一些商业、管理方面的书和杂志,这也在一定程度上培养了我在这方面的思维。

学习方法我对P3的教材相当重视,每天看几章,不需要细看,因为我们不是要去研究这些理论,仅仅知道怎么去运用就可以了。

每次考前的一个月,学校都会请外面的老师给我们串讲,再加上带我们做题,交给我们解题思路,我们在很短的时间内就能把整个课程的内容融会贯通,这种做法非常受用。

P3的历年试题真的是一个非常大的挑战,一开始连答案都看不懂,因为它不像其他课程有具体的答案,只是给了一个相当于思考的过程,一个判断该用什么理论、模型来解题的过程。

刚看试卷的时候完全不知所云,但在慢慢摸索的过程中还是发现了一些有用信息:答案后面会有给分点,那些给分点就是我们答题时需要关注的;而答案则是一个很好的推理过程,但这个推理过程必须建立在对相关理论的理解上。

我建议大家一定要理解那些常用的、重要的模型,根据适用环节加上适当的记忆,比如可以根据竞争力外部分析、内部分析、企业内部流程、人力、信息等进行分类。

标竿学习(Benchmarking)的原则在於和最佳实务(Best

一、引言 (2)二、產業概述 (2)三、關鍵成功要素分析 (3)3-1:策略規劃與領導 (3)3-1-1 DQLP品質領導流程 (4)3-1-2 策略發展流程 (5)3-1-3 創新學習的環境 (5)3-1-4 組織績效評估 (6)3-1-5 改進領導力 (7)3-1-6 企業哲學與責任 (7)3-1-7 環境安全與保障 (8)3-1-8 人力資源管理 (8)3-1-9 供應商合作 (8)3-2:資訊分析與共享 (8)3-2-1 績效管理 (9)3-2-2 資源配置 (9)3-3:顧客與市場聚焦 (10)3-3-1 顧客與市場知識管理 (10)3-3-2 傾聽與學習 (10)3-3-3 顧客焦點與評估 (11)3-3-4 矯正行動報告 (11)3-3-5 顧客滿意度 (12)3-3-6 績效評估 (12)3-4:人力資源管理 (12)3-4-1 工作系統 (13)3-4-2 報償與誘因 (13)3-4-3 員工教育、訓練與發展 (13)3-4-4 員工福利與滿意度 (14)3-5:作業流程管理 (15)3-5-1 流程設計 (15)3-5-2 品質與產品績效要求 (15)3-5-3 評估與改進流程 (16)3-5-4 支援流程 (17)3-5-5 供應商與合作流程 (17)3-5-6 流程改進 (18)策略意涵 (18)資料來源 (20)一、引言標竿學習(Benchmarking)的原則在於和最佳實務(Best practice)或世界級(world-class)的行業做比較,經過分析之後,將最佳實務整合至本身的作業流程之中,提升企業的競爭力。

標竿學習根據Michael J. Spendolini的說法可分為五個階段流程,首先第一個階段便是『決定向標竿學習什麼?』在此,針對汽車零組件業,本團隊遴選出在2000年榮獲美國國家品質獎(Malcolm Baldrige National Quality Award)的Dana 汽車零件公司,旗下共有七個策略事業單位(Strategic Business units),其中獲獎的事業單位便是隸屬於汽車系統(Automobile System Group)的Spicer Driveshaft部門。

ACCA考试经验:P5和P1P3考试经验分享

ACCA考试成绩已经出来了,原科目P1/P2/P3,从通过率来看,不少学员考的都不错,当然也有部分学员考的不是很理想。

考过的学员你可以全身心的备考下一科目,而对于9月需要备考SBL/SBR的学员,建议你多花时间来应对SBR/SBL。

对于P阶段的学员来说,由于P1和P3的合并,以及科目大纲及名称新的变化。

尚未通过P1和P3的学员:2018年9月考季P1和P3将会合并成为新的科目SBL,所以在6月考试成绩公布后,尚未通过P1和P3的学员需要重新学习新的科目SBL再参加考试。

通过P1或P3其中一门的学员:2018年9月考季之后,你的P1或P3成绩将会被取消,需要重新学习并参加SBL考试。

也就是说,如果在9月考季前你只通过了其中一门,那么这门考试的考试费和通过的成绩将会成为一种浪费。

通过P1和P3两门课程的学员:两门课程的通过成绩将会自动转化为SBL的成绩,不需要在学习SBL的课程。

P2科目将会由SBR课程替代,同样如果学习的是P2科目的学员,但是没有及时考试而选择参加9月考试的学员,需要重新学习SBR课程,掌握大纲变动部分,更好的应对考试。

P2 Corporate Reporting 将改名为Strategic Business Reporting,依然是必考科目。

新的科目将会继承P2原有的知识点,经过比较新老科目的考纲后发现,新的科目只是在原来P2的基础上重新做了编排,并没有新增或减少什么值得特别注意的知识。

在考试形式方面,改版后,将不设选做题,所有考题都必须回答。

ACCA建议学员在开始SBR学习之前学习EPSM模块。

该模块的学习需要大约20小时,对战略专业科目大有帮助。

在很多ACCA学员眼里,P5是最难的一科。

即使如此,还是有很多学员很坚定的选择P5.这部分学员通常有个共同点:不擅长计算类型的(P4)也不喜欢税(P6)那么只能选剩下的P7和P5,再是因为本身工作就是做业绩分析的,每个月都在做怎么会惧怕P5。

2014年ACCA考试(p3商务分析)考前总结9

2014年ACCA考试(p3商务分析)考前总结9本文由高顿ACCA整理发布,转载请注明出处BENCHMARKINGBenchmarking can be thought of as a scientific way of setting objectives that will act as targets before and during the operating period, and comparators during and after the periodBenchmarking can be defined as: 'The establishment, by the collection of data, of comparators that allow relative levels of performance to be identified.’Benchmarking can be thought of as a scientific way of setting objectives that will act as targets before and during the operating period, and comparators during and after the period. The phrase ‘by the collection of data’ is crucial: anyone can establish objectives without the collection of data, but these will be of little use because they are likely to be arbitrary and without any validity. Benchmark data validates objectives.The sources of data that can be used include internal data (for example, comparing the results of different branches), data about other companies (for example, those in the same industry) and government data (for example, data about employee sick days). We will examine the sources of data in more detail later.BENCHMARKING AND THE STRATEGIC PLANNING PROCESSBenchmarking can be used in all three steps of the classical, rational model of strategic planning:Assess the strategic position (internal and external factors)Frequently, strategic planning starts by defining the mission or mission statement. For example, BMW states that its mission is: ‘The BMW Group is the world’s leading provider of premium products and premium services for individual mobility.’So, without comparison through benchmarking, how does BMW know that it is delivering premium products and services?Assessment of an organisation’s current strategic position can be summarised in a SWOT analysis. However, the use of comparators is inherent in a SWOT analysis: if you can say that something is a ‘weakness’ or a ‘strength’ you must be carrying out some sort of comparison when making that value judgement. Similarly with opportunities and threats. A factor is a threat to us only because it is better or stronger than we are in that area –whether it is an organisation that is better financed, or one that produces products more cheaply, or a technological development that promises a better product in terms ofcost-benefit, or an organisation that has a stronger brand name.Note that a benchmarking exercise can also highlight where a competitor’s performance is weaker and so point out the areas where that competitor is vulnerable and might be fruitfully attacked. For example, if it is found that the quality and reliability of a competitor’s products are inferior to one’s own products, then an advertising campaign emphasising quality of our products could be effective.In all cases, the SWOT analysis should be based as far as possible on facts; data that has been collected and transformed into benchmark standards.Consider strategies and make choices Chosen strategies are those that should lead to competitive advantage.According to Michael Porter, competitive advantage can be obtained through either cost leadership or differentiation (each with or without focus). If cost leadership is to be attained, then an organisation must know what costs it needs to beat. What are competitors’ costs? What are the benchmarks for cost leadership? If the organisation has little hope of equalling or bettering those costs, then cost leadership is not a sensible strategy to attempt.Similarly with differentiation. This strategy is always more complex than cost leadership, where the main criterion is simply to lower unit costs while maintaining average quality. Differentiation, however, can be attained in a multitude of ways: quality, brand, style, innovation. Whatever the secret of differentiation is, it must be something that beats the competition – better quality, stronger brand attributes, better style or more radical innovation. Once again, measuring how competitors perform in these metrics is essential.Strategic implementation (strategy into action) Setting objectives is a major tool for implementing a strategy. Strategic plans are often communicated by issuing budgets to divisions, departments and individuals and, of course, budgets consist of objectives or targets. However, budgets have to be both challenging (to stay competitive and generate motivation) and attainable (to be taken seriously). Once again, an assessment of potential attainability should be based on the results that other organisations achieve, and so budget targets need to be benchmarked against these.Therefore, benchmarking can be used to:· push people in the directions where improvement is required· provide measures as to whether that required performance has been attained or to indicate what improvement is still needed.更多ACCA资讯请关注高顿ACCA官网:。

ACCAP3考经—合理的决策

ACCA P3合理的决策A new product launch.新产品发布及推广The timing of new product launches is very important,especially in the gaming industry.This links very closely with P3studies and getting strategy right.新产品发布的时机非常重要,尤其是在游戏行业。

本文章同ACCA P3的学习息息相关,主要说的是如何制定合理的决策。

Sony made a mistake when it launched its PS3and some people argue that it has never really recovered from the mistake.So with this background,this month sees the launch of the Nintendo Switch。

有许多人认为它从来没有真正从这个错误中恢复过来。

所以在这个背景下,这个月我们看到开关系列产品的推出。

The Nintendo Switch has become the Japanese firm's fastest selling console in many years-and possible ever-according to several reports.根据报道,开关已经成为日本公司多年来销售最快的产品。

Nintendo will not reveal official sales figures until April.直到四月才公布官方销售数字。

But games magazine Famitsu says more than330,000units were sold in the first three days in Japan,way more than its previous console the Wii U.但游戏杂志Famitsu说,在日本的头三天销售了超过33万台,大大超过了以前的产品Wii U.Media reports suggest European and US sales have also been strong.媒体报道显示,在欧美销售也十分强劲。

- 1、下载文档前请自行甄别文档内容的完整性,平台不提供额外的编辑、内容补充、找答案等附加服务。

- 2、"仅部分预览"的文档,不可在线预览部分如存在完整性等问题,可反馈申请退款(可完整预览的文档不适用该条件!)。

- 3、如文档侵犯您的权益,请联系客服反馈,我们会尽快为您处理(人工客服工作时间:9:00-18:30)。

ACCA P3 考试:Benchmarking

本文由高顿ACCA整理发布,转载请注明出处

Benchmarking can be used to compare an organisation’s strategic capabilities with itself over time and with other organisations at a given point time. There are three commonly used approaches to benchmarking:

1. Historical benchmarking

Organisations consider changes over time in their performance on a set of strategically important indicators in order to identify opportunities for improvement.

A potential disadvantage of historical benchmarking is that it may lead to complacency for a firm that shows improvement over time. It is the rate of improvement that is important to compare with that of competitors as competitors may improve at a faster rate.

2. Industry/sector benchmarking

Using a set of performance indicators, organisations may gain valuable insights when they compare their performance to other organisation.

Firms must benchmark against competitors in all industries in which they compete. Competitive activity and industry convergence have resulted in blurred industry boundaries.

3. Best-in-class benchmarking

Best-in-class benchmarking compares an organisation’s performance against “best-in-class” performance across industry lines and therefore seeks to overcome the limitations of other approaches.

The overall importance of benchmarking lies not so much in the detailed “mechanic” of comparison but in the effect that these comparisons might have on behavior. It can be used as a process for gaining momentum for improvement and change.

更多ACCA资讯请关注高顿ACCA官网:。